Global Data Center Construction Market Size and Share Analysis 2026-2033

Global Data Center Construction Market Forecast Snapshot (2026–2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 245.8 Billion |

| Market Size (2033) | USD 468.3 Billion |

| CAGR (2026–2033) | 8.4% |

| Largest Infrastructure Segment | Electrical Infrastructure |

| Fastest Growing Data Center Type | Hyperscale Data Centers |

| Leading End-Use Industry | IT & Telecommunications |

| Key Growth Driver | Expansion of Cloud Computing & AI Workloads |

| Major Technology Trend | AI-Optimized, Sustainable & Modular Data Centers |

| Emerging Opportunity | Edge Data Centers and 5G Infrastructure Deployment |

| Top Investment Area | Hyperscale and Colocation Facility Development |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Sustainability Focus | Renewable Energy Integration & Advanced Cooling Systems |

| Key Challenge | High Capital Expenditure and Energy Consumption |

| Strategic Outlook | Strong Long-Term Growth Driven by Digital Infrastructure Expansion, AI Adoption, and Cloud Service Demand |

Global Data Center Construction Market Size & Forecast

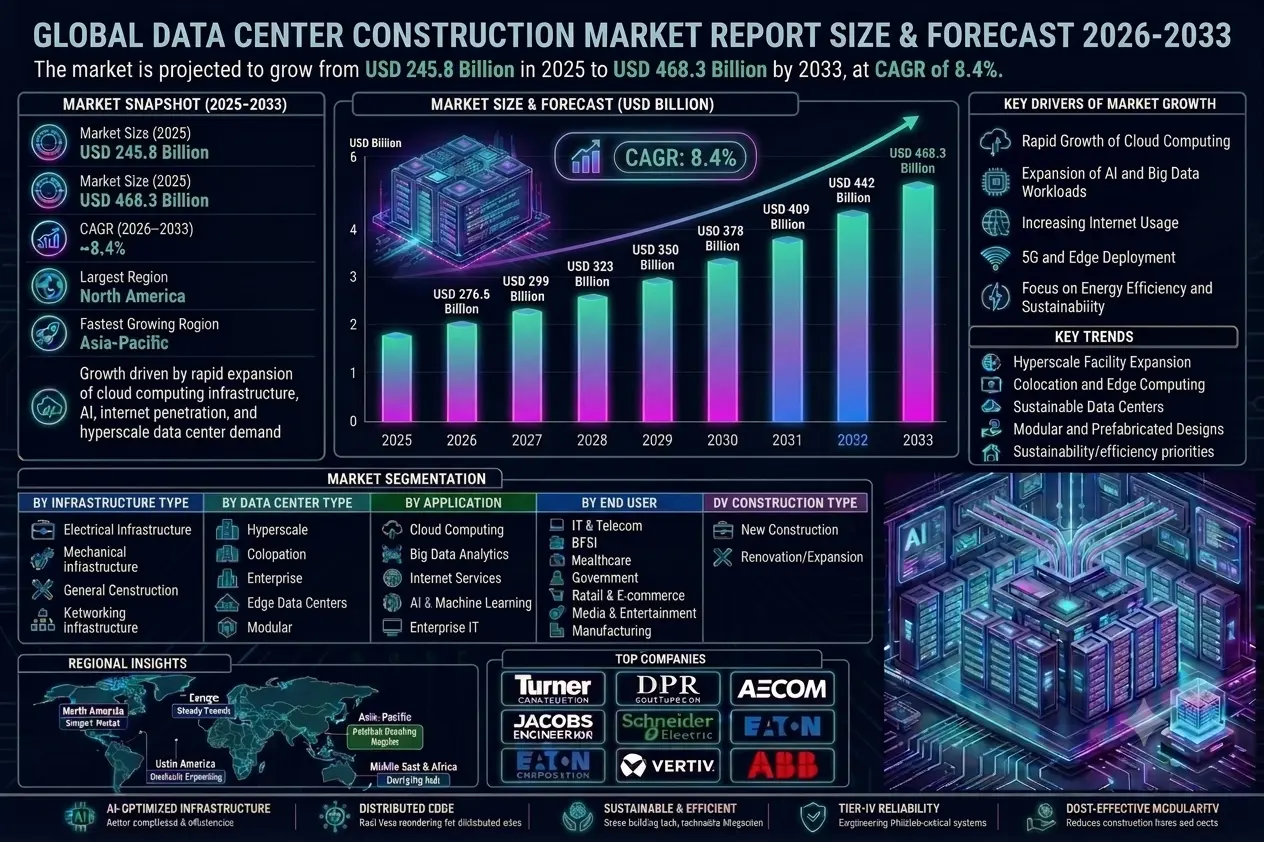

The global data center construction market is projected to witness significant growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 245.8 billion in 2025 and is expected to reach nearly USD 468.3 billion by 2033, expanding at a CAGR of around 8.4%. This growth is driven by rapid expansion of cloud computing infrastructure, rising adoption of artificial intelligence (AI), increasing internet penetration, and growing demand for hyperscale data centers worldwide. Data center construction involves the planning, engineering, development, and deployment of facilities designed to house computing systems, servers, storage infrastructure, networking equipment, and power management systems. These facilities are essential for supporting digital transformation, enterprise IT operations, cloud services, and high-performance computing environments. The market is experiencing accelerated investments from hyperscale cloud providers, colocation companies, telecommunications operators, and governments seeking to strengthen digital infrastructure and support growing data traffic volumes. Expansion of 5G networks, IoT ecosystems, edge computing, and AI-driven workloads is further increasing demand for advanced data center facilities. In addition, sustainability and energy efficiency have become major priorities in modern data center construction projects, driving adoption of green building technologies, renewable energy integration, advanced cooling systems, and modular infrastructure designs.Global Data Center Construction Market Overview

The data center construction market represents a critical segment of the global digital infrastructure industry. It includes construction services, engineering solutions, electrical systems, cooling technologies, physical security infrastructure, and networking deployment required to establish modern data center facilities. Data centers serve as the backbone of the digital economy by supporting cloud computing platforms, enterprise applications, e-commerce, streaming services, financial transactions, AI processing, and telecommunications operations. The market includes hyperscale data centers, enterprise data centers, colocation facilities, edge data centers, and modular data center solutions. Hyperscale facilities dominate large-scale investments due to increasing demand from global cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. Key industry participants include Turner Construction, DPR Construction, AECOM, Jacobs Engineering, Schneider Electric, Vertiv, Eaton Corporation, ABB Ltd., and various infrastructure engineering and facility management companies.Key Drivers of Global Data Center Construction Market Growth

Rapid Growth of Cloud Computing

Increasing adoption of cloud-based services by enterprises and consumers is driving strong demand for hyperscale and colocation data center facilities globally.Expansion of AI and Big Data Workloads

Artificial intelligence, machine learning, and big data analytics require advanced computing infrastructure and high-capacity data processing environments.Increasing Internet and Digital Service Usage

Growth in digital streaming, e-commerce, social media, gaming, and online services is significantly increasing global data traffic volumes.Deployment of 5G and Edge Computing Infrastructure

5G network expansion and edge computing adoption are driving construction of distributed data center facilities closer to end users to reduce latency.Focus on Energy Efficiency and Sustainability

Data center operators are increasingly investing in green construction practices, renewable energy integration, and advanced cooling systems to reduce environmental impact.Global Data Center Construction Market Segmentation

By Infrastructure Type

The market is segmented into electrical infrastructure, mechanical infrastructure, general construction, and networking infrastructure. Electrical infrastructure accounts for a major share due to high demand for uninterrupted power systems and backup energy solutions.By Data Center Type

The market includes hyperscale data centers, colocation data centers, enterprise data centers, edge data centers, and modular data centers. Hyperscale data centers dominate due to increasing investments from global cloud service providers.By Tier Standard

The market is segmented into Tier I, Tier II, Tier III, and Tier IV data centers. Tier III and Tier IV facilities are witnessing higher demand due to increased requirements for reliability and redundancy.By End User

End users include IT & telecom, BFSI, healthcare, government, retail & e-commerce, media & entertainment, and manufacturing industries.By Construction Type

The market includes new construction and renovation/expansion projects. New hyperscale facility development represents a significant growth segment globally.Regional Market Dynamics

North America dominates the global data center construction market due to strong cloud infrastructure investments, presence of hyperscale providers, and advanced digital ecosystems in the United States and Canada. Asia-Pacific is the fastest-growing region driven by rapid digitalization, expanding internet penetration, and increasing cloud adoption in China, India, Japan, Singapore, and Southeast Asia. Europe is witnessing substantial growth supported by increasing demand for sustainable data centers, strict data protection regulations, and expansion of enterprise digital infrastructure. Middle East is emerging as a strategic data center hub due to smart city projects, digital transformation initiatives, and increasing investments in cloud services. Latin America is gradually expanding with rising investments in telecommunications infrastructure and growing adoption of cloud-based enterprise services.Competitive Landscape

The global data center construction market is highly competitive and capital-intensive, involving construction firms, infrastructure engineering companies, electrical equipment providers, and specialized data center solution vendors. Key players include Turner Construction, DPR Construction, AECOM, Jacobs Engineering Group, Schneider Electric, Vertiv Holdings, Eaton Corporation, ABB Ltd., Cisco Systems, and Huawei Technologies. Companies are increasingly focusing on modular construction techniques, AI-powered infrastructure management, energy-efficient cooling technologies, and renewable energy integration to strengthen competitiveness. Strategic partnerships between cloud providers, infrastructure developers, and energy companies are becoming increasingly common as operators seek scalable and sustainable expansion models.Strategic Outlook

The strategic outlook for the data center construction market remains highly positive due to accelerating digital transformation and rising global dependence on cloud-based services and digital infrastructure. Future growth opportunities include AI-optimized data centers, liquid cooling systems, renewable-powered facilities, modular edge data centers, and carbon-neutral infrastructure development. Governments and private enterprises are expected to continue increasing investments in digital infrastructure to support smart cities, AI ecosystems, and national data sovereignty initiatives.Final Market Perspective

The global data center construction market is becoming increasingly vital to the modern digital economy. Rapid growth in cloud computing, AI applications, IoT ecosystems, and digital communication networks is driving unprecedented demand for scalable and energy-efficient data center infrastructure. As organizations continue prioritizing digital transformation and data-driven operations, investments in advanced data center construction will remain strong worldwide. Companies that combine engineering expertise, sustainability initiatives, and high-performance infrastructure capabilities will remain strongly positioned in the evolving global data center construction market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Data Center Construction Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Data Center Construction

- 2.2 Scope of the Study

- 2.3 Evolution of Digital Infrastructure

- 2.4 Data Center Construction Value Chain

- 2.5 Infrastructure Components & System Architecture

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Construction Innovation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rapid Growth of Cloud Computing

- 4.1.2 Expansion of AI & Big Data Workloads

- 4.1.3 Increasing Internet & Digital Service Usage

- 4.1.4 Deployment of 5G & Edge Computing Infrastructure

- 4.1.5 Focus on Energy Efficiency & Sustainability

- 4.2 Restraints

- 4.2.1 High Initial Capital Investment

- 4.2.2 Rising Energy Consumption Costs

- 4.2.3 Complex Regulatory & Compliance Requirements

- 4.2.4 Land & Power Availability Constraints

- 4.3 Opportunities

- 4.3.1 Growth of Hyperscale Data Centers

- 4.3.2 Renewable Energy Powered Facilities

- 4.3.3 Expansion of Modular & Edge Data Centers

- 4.3.4 AI-Driven Infrastructure Optimization

- 4.4 Challenges

- 4.4.1 Supply Chain Disruptions

- 4.4.2 Cooling & Thermal Management Complexity

- 4.4.3 Skilled Workforce Shortages

- 4.4.4 Cybersecurity & Physical Security Risks

- 4.1 Drivers

- 5. Global Data Center Construction Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Infrastructure Investment Trends

- 5.6 Construction Capacity & Deployment Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Infrastructure Type

- 6.1.1 Electrical Infrastructure

- 6.1.1.1 Power Distribution Systems

- 6.1.1.1.1 Backup Power Solutions

- 6.1.1.1.1.1 UPS & Generator Systems

- 6.1.1.1.1 Backup Power Solutions

- 6.1.1.1 Power Distribution Systems

- 6.1.2 Mechanical Infrastructure

- 6.1.2.1 Cooling & HVAC Systems

- 6.1.2.1.1 Advanced Thermal Management

- 6.1.2.1.1.1 Liquid Cooling Applications

- 6.1.2.1.1 Advanced Thermal Management

- 6.1.2.1 Cooling & HVAC Systems

- 6.1.3 General Construction

- 6.1.3.1 Facility Development & Engineering

- 6.1.3.1.1 Sustainable Building Design

- 6.1.3.1.1.1 Green Data Center Infrastructure

- 6.1.3.1.1 Sustainable Building Design

- 6.1.3.1 Facility Development & Engineering

- 6.1.4 Networking Infrastructure

- 6.1.4.1 High-Speed Connectivity Systems

- 6.1.4.2 Fiber & Interconnection Infrastructure

- 6.1.5 Others

- 6.1.1 Electrical Infrastructure

- 6.2 By Data Center Type

- 6.2.1 Hyperscale Data Centers

- 6.2.2 Colocation Data Centers

- 6.2.3 Enterprise Data Centers

- 6.2.4 Edge Data Centers

- 6.2.5 Modular Data Centers

- 6.3 By Tier Standard

- 6.3.1 Tier I

- 6.3.2 Tier II

- 6.3.3 Tier III

- 6.3.4 Tier IV

- 6.4 By End User

- 6.4.1 IT & Telecommunications

- 6.4.2 BFSI

- 6.4.3 Healthcare

- 6.4.4 Government & Defense

- 6.4.5 Retail & E-commerce

- 6.4.6 Media & Entertainment

- 6.4.7 Manufacturing

- 6.5 By Construction Type

- 6.5.1 New Construction

- 6.5.2 Renovation & Expansion

- 6.1 By Infrastructure Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Infrastructure Capability Benchmarking

- 8.3 Strategic Partnerships & Joint Ventures

- 8.4 Sustainable Construction Initiatives

- 8.5 Technology & Innovation Analysis

- 9. Company Profiles

- 9.1 Turner Construction

- 9.2 DPR Construction

- 9.3 AECOM

- 9.4 Jacobs Engineering Group

- 9.5 Schneider Electric

- 9.6 Vertiv Holdings

- 9.7 Eaton Corporation

- 9.8 ABB Ltd.

- 9.9 Cisco Systems

- 9.10 Huawei Technologies

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Digital Infrastructure Capacity Analyzer

- 10.3 Energy Efficiency & Cooling Optimization Tracker

- 10.4 Data Center Expansion Monitoring System

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Hyperscale Infrastructure

- 11.2 Adoption of Renewable-Powered Data Centers

- 11.3 Investment in Edge & Modular Facilities

- 11.4 AI-Optimized Infrastructure Management

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Data Center Construction Market Competitive Intensity & Market Structure Overview

The Global Data Center Construction Market is highly competitive, capital-intensive, and infrastructure-driven, characterized by the participation of global construction giants, engineering and design firms, electrical infrastructure providers, and specialized data center solution vendors. Competition spans across hyperscale, colocation, enterprise, and edge data center developments, with strong emphasis on speed of deployment, energy efficiency, scalability, and uptime reliability.

Competitive intensity in the market is increasing significantly due to the rapid expansion of cloud computing, AI workloads, and digital services. Players are competing not only on construction capability but also on integrated delivery models that include design, build, power systems, cooling technologies, and long-term facility optimization services.

The market structure is moderately consolidated at the top, with major global engineering and construction firms working alongside specialized data center infrastructure providers. However, it remains fragmented across regional contractors and niche service providers involved in electrical systems, cooling solutions, and modular construction projects.

Global Data Center Construction Market Competitive Intensity & Market Structure Current Scenario

Leading Construction & Infrastructure Service Providers

Turner Construction: One of the leading global data center builders, specializing in hyperscale and mission-critical facilities with strong expertise in large-scale infrastructure delivery.

DPR Construction: Major player focused on complex data center construction projects, known for high-speed execution and advanced project delivery models.

AECOM: Global infrastructure and engineering leader providing end-to-end design, planning, and construction management services for large data center projects.

Jacobs Engineering Group: Strong presence in mission-critical infrastructure design, sustainability-focused engineering, and large-scale digital infrastructure projects.

Schneider Electric: Key provider of electrical infrastructure, power management systems, and integrated energy efficiency solutions for data centers.

Vertiv Holdings: Specialized in critical digital infrastructure including cooling systems, UPS solutions, and thermal management technologies.

Eaton Corporation: Major supplier of power distribution, backup systems, and energy management solutions for data center facilities.

ABB Ltd.: Strong competitor in electrical infrastructure, smart grid integration, and energy-efficient data center power systems.

Cisco Systems: Key technology provider for networking infrastructure, data center connectivity, and digital architecture solutions.

Huawei Technologies: Significant global player offering integrated data center infrastructure, networking solutions, and modular facility technologies.

Key Competitive Intensity & Market Structure Signals in Global Data Center Construction Market

A major competitive signal in the market is the shift toward integrated data center delivery models, where companies provide end-to-end solutions combining construction, electrical systems, cooling infrastructure, and digital monitoring platforms. This integrated approach is becoming essential for hyperscale operators seeking faster deployment and operational efficiency.

Another key trend is the increasing demand for speed-to-market execution. Hyperscale cloud providers and colocation operators are aggressively expanding capacity, pushing construction firms to adopt modular construction techniques, prefabricated components, and standardized designs to reduce build time.

Sustainability has become a critical competitive factor. Companies are competing on carbon-neutral construction practices, renewable energy integration, liquid cooling systems, and advanced energy optimization technologies to meet global ESG targets and regulatory requirements.

The rise of AI and high-density computing is reshaping infrastructure requirements, increasing competition in advanced cooling technologies, high-capacity power systems, and next-generation facility design optimized for high-performance workloads.

Supply chain resilience and access to critical electrical and mechanical components are also becoming competitive differentiators, as global demand for data center infrastructure continues to outpace supply in many regions.

Strategic Implications of Competitive Intensity & Market Structure in Global Data Center Construction Market

Market participants are increasingly adopting vertically integrated strategies that combine construction expertise with electrical engineering, cooling technology provision, and digital infrastructure management to offer unified solutions for hyperscale clients.

Strategic alliances between construction companies, cloud service providers, and energy suppliers are becoming more common to ensure reliable power access, renewable energy sourcing, and scalable infrastructure deployment.

Technology-driven differentiation is gaining importance, with companies investing in AI-based facility management systems, predictive maintenance tools, and digital twin technologies to optimize construction planning and operational efficiency.

Regional expansion strategies are intensifying, particularly in Asia-Pacific and the Middle East, where rapid digitalization and government-led infrastructure initiatives are driving strong demand for new data center capacity.

Cost efficiency, sustainability compliance, and scalability remain central to competitive positioning as operators seek to balance rapid expansion with long-term operational stability and environmental responsibility.

Global Data Center Construction Market Competitive Intensity & Market Structure Forward Outlook

The Global Data Center Construction Market is expected to become increasingly specialized and technology-intensive, with strong emphasis on modular construction, AI-optimized facility design, and sustainable infrastructure development.

Future competition will be shaped by the ability to deliver ultra-efficient, high-density, and renewable-powered data centers capable of supporting next-generation AI, cloud computing, and edge workloads.

The adoption of liquid cooling systems, prefabricated modular data center units, and carbon-neutral construction methodologies will significantly reshape competitive dynamics across global markets.

Market consolidation is expected to increase as large infrastructure and engineering firms acquire niche specialists in electrical systems, cooling technologies, and digital infrastructure management to strengthen end-to-end capabilities.

Overall, the market will remain highly competitive and rapidly evolving, with success increasingly dependent on integrated engineering capabilities, sustainability performance, construction speed, and technological innovation. Companies that combine large-scale execution strength with advanced digital infrastructure expertise will maintain strong leadership positions in the Global Data Center Construction Market through 2033.

Value Chain

Global Data Center Construction Market Value Chain & Supply Chain Evolution Overview

The Global Data Center Construction Market value chain is undergoing rapid transformation as digital infrastructure becomes increasingly critical to global economic activity, enterprise operations, cloud computing ecosystems, artificial intelligence workloads, and connected communication networks. Data center construction has evolved from conventional IT facility development into a highly specialized and technologically advanced infrastructure ecosystem that integrates power systems, cooling technologies, networking infrastructure, cybersecurity architecture, renewable energy integration, modular engineering, and intelligent facility management platforms. This transformation is being driven by accelerating demand for cloud services, rapid expansion of hyperscale computing environments, rising internet penetration, deployment of 5G infrastructure, and increasing enterprise dependence on real-time data processing and AI-driven applications.

The market value chain encompasses a highly interconnected network of stakeholders including land developers, engineering and construction firms, electrical equipment manufacturers, cooling system providers, networking infrastructure vendors, semiconductor companies, renewable energy developers, cloud service providers, and facility management organizations. Major companies such as Turner Construction, DPR Construction, AECOM, Jacobs Engineering Group, Schneider Electric, Vertiv Holdings, Eaton Corporation, ABB Ltd., Cisco Systems, and Huawei Technologies are actively investing in modular construction techniques, intelligent energy management systems, advanced cooling technologies, and AI-powered operational infrastructure to support next-generation data center requirements.

Upstream supply chain operations increasingly rely on advanced electrical infrastructure components, backup power systems, switchgear equipment, transformers, precision cooling systems, fiber-optic networking hardware, server racks, building automation technologies, and high-performance construction materials capable of supporting large-scale digital infrastructure environments. At the same time, renewable energy integration and sustainability-focused engineering solutions are becoming central components within the value chain as governments and enterprises prioritize carbon reduction targets and energy-efficient infrastructure deployment across global markets.

The operational structure of the market is also evolving as hyperscale cloud providers, colocation operators, telecommunications companies, and governments aggressively expand digital infrastructure investments to support exponential growth in cloud computing, edge computing, streaming services, AI processing, financial transactions, and IoT ecosystems. Modern data center projects increasingly require sophisticated infrastructure planning, scalable modular architectures, advanced thermal management systems, intelligent monitoring platforms, and resilient backup power capabilities to ensure operational continuity across mission-critical environments.

Despite strong growth momentum, the market continues to face several supply chain and operational challenges including rising construction costs, energy availability constraints, semiconductor shortages, land acquisition complexity, regulatory compliance requirements, sustainability mandates, grid infrastructure limitations, and increasing pressure to reduce environmental impact while maintaining high-performance operational reliability. As a result, companies across the ecosystem are increasingly prioritizing supply chain diversification, localized infrastructure sourcing, renewable energy partnerships, and digital project management systems to improve long-term resilience and operational efficiency.

Global Data Center Construction Market Value Chain & Supply Chain Evolution Current Scenario

The current global data center construction ecosystem is being shaped by unprecedented investments in hyperscale cloud infrastructure, rapid expansion of AI-driven computing environments, increasing enterprise digital transformation initiatives, and growing deployment of edge computing facilities designed to reduce latency and improve real-time data processing capabilities. Cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud continue to aggressively expand hyperscale data center capacity worldwide in response to accelerating demand for cloud-based applications, AI workloads, enterprise SaaS platforms, and digital collaboration systems.

Construction companies and infrastructure engineering firms across North America, Europe, Asia-Pacific, and the Middle East are increasingly focusing on large-scale data center projects that incorporate advanced energy-efficient systems, modular construction methodologies, intelligent building automation technologies, and renewable-powered operational frameworks. The adoption of prefabricated modular infrastructure designs is growing rapidly as operators seek faster deployment timelines, improved scalability, reduced construction complexity, and enhanced operational flexibility across geographically distributed digital infrastructure environments.

The rapid deployment of 5G telecommunications infrastructure and expansion of edge computing ecosystems are also driving increased demand for distributed data center facilities located closer to end users and enterprise networks. Edge data centers are becoming increasingly important for supporting low-latency applications including autonomous systems, industrial IoT, real-time analytics, gaming platforms, smart city technologies, and AI-enabled industrial automation systems that require localized processing capabilities.

Sustainability has emerged as a major operational priority across the industry, with data center operators investing heavily in renewable energy procurement, advanced cooling systems, liquid cooling technologies, waste heat recovery systems, intelligent energy optimization platforms, and low-carbon building materials. Governments and enterprise customers are increasingly demanding environmentally sustainable infrastructure solutions capable of reducing power consumption, improving energy utilization effectiveness (PUE), and supporting long-term decarbonization objectives across digital infrastructure operations.

Key Value Chain & Supply Chain Evolution Signals in Global Data Center Construction Market

Several transformative trends are significantly reshaping the global data center construction value chain and influencing long-term competitive dynamics across the digital infrastructure ecosystem. One of the most important signals is the accelerating global expansion of hyperscale cloud infrastructure driven by increasing enterprise cloud adoption, AI application growth, digital transformation initiatives, and rising demand for scalable computing resources. Hyperscale operators are continuously investing in larger, more energy-efficient, and highly automated facilities capable of supporting exponential growth in data processing and storage requirements.

Another major evolution signal is the increasing adoption of modular and prefabricated construction methodologies designed to reduce deployment timelines, improve scalability, optimize project costs, and enhance operational flexibility. Modular infrastructure systems enable faster commissioning and more efficient expansion strategies, particularly in regions experiencing rapid growth in cloud services, telecommunications infrastructure, and enterprise digitalization.

The rapid rise of artificial intelligence and machine learning workloads is also reshaping infrastructure design priorities by significantly increasing demand for high-density computing environments, advanced thermal management systems, and AI-optimized power distribution architectures. Data center operators are increasingly deploying liquid cooling systems, immersion cooling technologies, and intelligent energy management platforms to support growing computational intensity while minimizing energy consumption and operational costs.

Another important market signal is the increasing convergence between renewable energy systems, smart grid technologies, and digital infrastructure operations. Data center operators are forming strategic partnerships with renewable energy providers and utility companies to secure sustainable energy supplies, improve grid stability, and reduce long-term operational carbon footprints. Simultaneously, governments worldwide are implementing stricter sustainability regulations and energy efficiency standards that are accelerating adoption of green building technologies and carbon-neutral infrastructure development strategies.

The expansion of edge computing infrastructure is also becoming a defining transformation trend as industries increasingly require decentralized processing capabilities capable of supporting low-latency applications and real-time analytics. This shift is driving construction of smaller, geographically distributed edge facilities integrated with telecommunications networks, industrial IoT systems, and urban smart infrastructure environments.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Data Center Construction Market

Leading industry participants including Turner Construction, DPR Construction, AECOM, Jacobs Engineering Group, Schneider Electric, Vertiv Holdings, Eaton Corporation, ABB Ltd., Cisco Systems, and Huawei Technologies are actively strengthening market positioning through investments in modular infrastructure engineering, renewable energy integration, AI-powered facility management systems, advanced cooling technologies, and intelligent electrical infrastructure solutions. Competitive differentiation increasingly depends on the ability to deliver scalable, sustainable, energy-efficient, and highly resilient data center infrastructure capable of supporting rapidly evolving digital ecosystem requirements.

Companies capable of integrating advanced cooling systems, renewable energy frameworks, intelligent monitoring technologies, and modular deployment capabilities into unified digital infrastructure solutions are expected to capture premium growth opportunities across hyperscale cloud computing, edge computing, telecommunications infrastructure, AI processing environments, and enterprise digital transformation projects. Operators are also prioritizing flexible infrastructure architectures capable of supporting future technological upgrades, increasing computational density, and changing regulatory requirements over long operational lifecycles.

Strategic partnerships between cloud service providers, construction companies, energy utilities, semiconductor manufacturers, networking vendors, and infrastructure engineering firms are becoming increasingly important for improving project scalability, securing energy availability, strengthening supply chain resilience, and accelerating deployment timelines across large-scale infrastructure projects. In parallel, increasing geopolitical uncertainty and supply chain disruptions are encouraging operators to regionalize supply networks, diversify sourcing strategies, and strengthen domestic manufacturing capabilities for critical infrastructure components.

Sustainability and environmental compliance are becoming central strategic priorities across the value chain as enterprise customers, regulators, and investors increasingly evaluate infrastructure providers based on carbon reduction initiatives, renewable energy utilization, energy efficiency performance, and environmental sustainability commitments. Data center operators that successfully align infrastructure expansion with sustainability goals are expected to strengthen long-term market competitiveness and investor confidence.

Global Data Center Construction Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the global data center construction value chain is expected to become increasingly intelligent, modular, energy-efficient, AI-optimized, and deeply integrated with renewable energy ecosystems as global digital infrastructure demand continues accelerating. Future data center facilities will increasingly incorporate AI-driven infrastructure management systems, autonomous cooling optimization technologies, predictive maintenance platforms, and intelligent power distribution architectures capable of improving operational efficiency and reducing total energy consumption across large-scale computing environments.

The adoption of liquid cooling systems, immersion cooling technologies, and advanced thermal management platforms is expected to expand significantly as AI processing environments and high-performance computing workloads continue increasing server density and thermal complexity. Operators will increasingly prioritize advanced cooling architectures capable of supporting next-generation AI infrastructure while maintaining energy efficiency and operational reliability.

Renewable-powered and carbon-neutral data center developments are expected to become mainstream across the industry as governments strengthen environmental regulations and enterprise customers prioritize sustainable digital infrastructure partnerships. Solar energy integration, battery storage systems, smart grid connectivity, hydrogen backup power technologies, and advanced energy optimization platforms are anticipated to play increasingly important roles within future data center ecosystems.

Edge computing infrastructure is also expected to experience substantial long-term growth as telecommunications providers, industrial operators, smart city developers, and enterprise networks increasingly deploy localized computing facilities to support real-time analytics, autonomous systems, industrial automation, and latency-sensitive applications. This evolution will likely accelerate demand for compact modular edge facilities integrated with AI-enabled monitoring systems and distributed energy management technologies.

Cybersecurity and digital resilience will become increasingly important across data center construction ecosystems as critical infrastructure operators prioritize secure facility architecture, intelligent threat monitoring systems, encrypted operational networks, and resilient backup infrastructure capable of protecting mission-critical digital operations against cyber threats and operational disruptions. Advanced physical security technologies and AI-powered infrastructure monitoring systems are expected to become standard components within next-generation data center environments.

Ultimately, the future data center construction market value chain will evolve from conventional facility engineering into highly integrated intelligent infrastructure ecosystems combining AI-driven operational management, renewable energy optimization, modular deployment capabilities, advanced cooling technologies, cybersecurity architecture, and autonomous digital infrastructure management systems designed to support the rapidly expanding global digital economy.

Market-Specific Value Chain

- Land Acquisition & Infrastructure Planning: Site selection, land development, zoning approvals, environmental assessments, utility connectivity planning, renewable energy feasibility studies, and infrastructure engineering consultation services.

- Electrical, Mechanical & Cooling Infrastructure Supply: UPS systems, switchgear, transformers, backup generators, cooling systems, liquid cooling technologies, HVAC infrastructure, power distribution systems, and energy management technologies.

- Construction & Modular Facility Development: Civil engineering, modular construction systems, prefabricated infrastructure deployment, structural development, smart building technologies, and facility commissioning services.

- Networking, Computing & Digital Infrastructure Integration: Fiber-optic connectivity, server deployment, networking systems, storage infrastructure, cloud integration technologies, cybersecurity systems, and AI computing hardware deployment.

- Operations, Monitoring & Energy Optimization: AI-powered infrastructure management, predictive maintenance systems, intelligent cooling optimization, remote monitoring platforms, digital twin technologies, and operational analytics solutions.

- Long-Term Sustainability & Infrastructure Lifecycle Management: Renewable energy integration, carbon reduction strategies, smart grid connectivity, infrastructure modernization, facility expansion, environmental compliance, and lifecycle operational optimization.

Company-to-Stage Mapping

- Land Acquisition & Infrastructure Planning: AECOM, Jacobs Engineering Group, CBRE Data Center Solutions, Cushman & Wakefield, infrastructure consulting firms.

- Electrical, Mechanical & Cooling Infrastructure Supply: Schneider Electric, Vertiv Holdings, Eaton Corporation, ABB Ltd., Johnson Controls, Stulz, Trane Technologies.

- Construction & Modular Facility Development: Turner Construction, DPR Construction, Skanska, Fluor Corporation, modular infrastructure engineering firms.

- Networking, Computing & Digital Infrastructure Integration: Cisco Systems, Huawei Technologies, Dell Technologies, HPE, Lenovo, cloud infrastructure hardware providers.

- Operations, Monitoring & Energy Optimization: Schneider Electric EcoStruxure, Siemens Smart Infrastructure, Vertiv management platforms, AI infrastructure analytics providers.

- Long-Term Sustainability & Infrastructure Lifecycle Management: Renewable energy developers, smart grid technology companies, ESG infrastructure consultants, facility management providers, energy optimization firms.

Investment Activity

Global Data Center Construction Market Investment & Funding Dynamics Overview

Investment and funding activity in the Global Data Center Construction Market is witnessing rapid acceleration due to rising global demand for cloud computing infrastructure, artificial intelligence workloads, digital transformation initiatives, and expanding internet connectivity worldwide. Between 2026 and 2033, capital allocation is expected to increase significantly toward hyperscale data centers, edge computing facilities, modular infrastructure systems, renewable-powered campuses, and AI-optimized computing environments.

The market is highly capital-intensive, requiring substantial investments in land acquisition, electrical infrastructure, cooling systems, backup power solutions, networking architecture, cybersecurity infrastructure, and advanced facility engineering. Major hyperscale cloud providers including Amazon Web Services (AWS), Microsoft Azure, Google Cloud, Meta, and Oracle are continuously increasing investments in large-scale data center expansion projects to support rapidly growing global data traffic and AI processing requirements.

Construction firms, infrastructure engineering companies, private equity investors, sovereign wealth funds, real estate investment trusts (REITs), and telecommunications providers are also playing a critical role in funding new data center developments. Companies such as Turner Construction, DPR Construction, AECOM, Schneider Electric, Vertiv, ABB Ltd., Eaton Corporation, and Jacobs Engineering are investing heavily in next-generation energy-efficient infrastructure and modular deployment technologies.

Global Data Center Construction Market Investment & Funding Dynamics Current Scenario

The current investment environment is strongly supported by exponential growth in cloud services, AI model training workloads, enterprise digitalization, 5G network deployment, and increasing enterprise reliance on high-performance computing infrastructure. Investors are prioritizing scalable, energy-efficient, and geographically diversified data center assets capable of supporting future digital demand.

- North America: Leads global investment activity due to the presence of major hyperscale cloud providers, strong AI infrastructure expansion, advanced digital ecosystems, and large-scale colocation projects across the United States and Canada.

- Asia-Pacific: Emerging as the fastest-growing investment region supported by rapid internet penetration, increasing cloud adoption, smart city initiatives, and strong government-backed digital infrastructure programs in China, India, Japan, Singapore, and Southeast Asia.

- Europe: Attracting substantial investments focused on sustainable and carbon-neutral data centers, regulatory-compliant digital infrastructure, and renewable energy integration.

- Middle East: Witnessing increasing funding activity driven by smart city development, digital economy diversification strategies, and expansion of regional cloud infrastructure hubs.

- Latin America: Experiencing moderate investment growth supported by rising cloud adoption, telecommunications infrastructure upgrades, and expanding enterprise digital services.

Key Investment & Funding Dynamics Signals in Global Data Center Construction Market

- Rapid expansion of hyperscale cloud infrastructure is driving large-scale investments in Tier III and Tier IV data center facilities globally.

- AI and machine learning workloads are accelerating funding into high-density computing infrastructure and advanced cooling technologies.

- Growing edge computing adoption is supporting investments in modular and distributed data center construction projects closer to end users.

- Renewable energy integration and carbon-neutral construction initiatives are increasingly influencing capital allocation decisions across the industry.

- Private equity firms, infrastructure funds, and REITs are increasing investments in colocation and hyperscale data center assets due to strong long-term revenue potential.

Strategic Implications of Investment & Funding Dynamics in Global Data Center Construction Market

- The market strongly favors companies with expertise in large-scale infrastructure engineering, energy management, and sustainable facility design.

- Energy efficiency and operational sustainability are becoming major competitive differentiators as operators seek to reduce power consumption and carbon emissions.

- Strategic partnerships between cloud providers, utility companies, renewable energy developers, and infrastructure contractors are increasing to accelerate scalable expansion.

- AI-driven infrastructure management, predictive maintenance systems, and digital twin technologies are attracting growing investment interest.

- Geographic diversification strategies are becoming critical as enterprises prioritize low-latency infrastructure, regulatory compliance, and regional data sovereignty.

Global Data Center Construction Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Data Center Construction Market is expected to remain one of the most attractive infrastructure investment sectors due to sustained digital transformation, rising AI computing demand, and rapid expansion of cloud ecosystems worldwide.

Future capital allocation will increasingly prioritize renewable-powered hyperscale campuses, liquid cooling technologies, AI-optimized infrastructure, modular edge facilities, and smart energy management systems capable of improving operational efficiency and scalability.

- North America: Will continue dominating investments through expansion of AI-focused hyperscale infrastructure and advanced cloud ecosystems.

- Asia-Pacific: Will witness the fastest investment growth due to digital economy expansion, rising enterprise cloud adoption, and large-scale government digitalization initiatives.

- Europe: Will strengthen its position through sustainability-driven investments and increasing focus on green data center infrastructure.

Sustainability objectives and carbon reduction targets will increasingly reshape funding priorities, encouraging investments in renewable energy procurement, low-carbon construction materials, advanced cooling architectures, and circular infrastructure practices.

Overall, the market is expected to maintain strong long-term investment momentum due to its foundational role in supporting cloud computing, AI ecosystems, digital communications, and enterprise transformation. Companies that successfully combine engineering expertise, energy efficiency, scalability, and intelligent infrastructure management will remain strongly positioned to lead the Global Data Center Construction Market through 2033.

Technology & Innovation

Global Data Center Construction Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Data Center Construction Market is evolving rapidly as hyperscale cloud providers, colocation operators, telecommunications companies, and infrastructure developers increasingly invest in advanced, scalable, and energy-efficient digital infrastructure. Innovation across the market is centered around AI-optimized facility management, modular construction techniques, advanced cooling systems, renewable energy integration, intelligent power distribution, and automated infrastructure monitoring technologies designed to support next-generation digital ecosystems.

The rapid expansion of cloud computing, artificial intelligence, edge computing, and high-performance computing workloads is significantly transforming modern data center construction requirements. Operators are increasingly deploying high-density computing environments supported by advanced electrical infrastructure, intelligent cooling systems, and software-defined facility management platforms to ensure operational reliability and scalability.

Artificial intelligence and predictive analytics are becoming key innovation drivers within the data center construction ecosystem. AI-powered systems are being used for energy optimization, predictive maintenance, cooling management, workload balancing, and real-time infrastructure monitoring. These technologies help operators reduce operational costs, improve uptime efficiency, and optimize energy consumption across large-scale facilities.

Advanced cooling technologies are also reshaping the market as rising rack densities and AI workloads generate higher thermal demands. Liquid cooling systems, immersion cooling technologies, and AI-controlled airflow management solutions are increasingly replacing traditional air-cooling systems to improve thermal efficiency and reduce energy usage.

The market is also witnessing strong adoption of modular and prefabricated data center construction models. Modular infrastructure designs enable faster deployment, improved scalability, reduced construction timelines, and greater flexibility for expanding digital infrastructure capacity in response to growing data demands.

Sustainability innovation is becoming a major focus area across the industry. Data center operators are integrating renewable energy systems, smart grid technologies, battery energy storage, and carbon-neutral building practices to reduce environmental impact and comply with evolving energy efficiency regulations globally.

Global Data Center Construction Market Technology & Innovation Landscape Current Scenario

Currently, the global data center construction market is experiencing accelerated infrastructure modernization driven by hyperscale cloud expansion, AI-driven computing growth, and increasing enterprise digital transformation initiatives. Major cloud providers such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and Meta are heavily investing in large-scale hyperscale facilities equipped with advanced automation and energy-efficient technologies.

Hyperscale data centers represent the largest area of technological innovation in the market. These facilities are increasingly deploying AI-powered infrastructure management systems capable of optimizing power usage effectiveness (PUE), cooling efficiency, server utilization, and predictive maintenance operations in real time.

Modular data center construction is rapidly gaining traction due to its ability to reduce deployment time and improve operational scalability. Prefabricated power modules, cooling units, and containerized data center systems are enabling operators to quickly expand infrastructure capacity while minimizing construction complexity.

The rapid growth of AI workloads and high-density computing environments is significantly increasing demand for advanced cooling solutions. Liquid cooling systems, rear-door heat exchangers, and direct-to-chip cooling technologies are becoming increasingly common in next-generation AI-focused data centers.

Renewable energy integration is also expanding rapidly across the market. Data center operators are increasingly utilizing solar power, wind energy, battery storage systems, and energy-efficient power distribution technologies to reduce carbon emissions and improve long-term sustainability.

Edge data center construction is another emerging innovation area driven by 5G deployment, IoT ecosystems, and low-latency application requirements. Operators are building smaller distributed facilities closer to end users to improve data processing speed and support real-time digital services.

Key Technology & Innovation Trends in Global Data Center Construction Market

- AI-Powered Infrastructure Management: Intelligent systems optimizing cooling, power distribution, workload balancing, and predictive maintenance.

- Liquid & Immersion Cooling Technologies: Advanced thermal management systems improving cooling efficiency for high-density computing environments.

- Modular Data Center Construction: Prefabricated and scalable infrastructure enabling faster deployment and flexible expansion.

- Renewable Energy Integration: Solar, wind, and battery storage systems supporting sustainable and carbon-neutral data center operations.

- Edge Data Center Development: Distributed infrastructure supporting low-latency applications, 5G networks, and IoT ecosystems.

- Smart Power Distribution Systems: Digitally monitored electrical infrastructure improving energy efficiency and operational reliability.

- High-Density Rack Infrastructure: Advanced server architectures supporting AI, machine learning, and high-performance computing workloads.

- Digital Twin Technologies: Virtual simulation systems enabling infrastructure optimization and predictive operational analysis.

- Automated Facility Monitoring: IoT-enabled sensors and analytics platforms improving real-time infrastructure visibility.

- Carbon-Neutral Data Center Design: Sustainable building technologies reducing environmental impact and supporting energy efficiency goals.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping the data center construction market by improving scalability, operational efficiency, sustainability, and infrastructure reliability. Advanced digital infrastructure technologies are enabling operators to support rapidly growing cloud computing, AI processing, and real-time data analytics workloads more efficiently.

For infrastructure developers and data center operators, investment in AI-enabled facility management, modular infrastructure, and advanced cooling systems has become a major competitive differentiator. Companies leveraging intelligent infrastructure platforms are improving operational uptime, reducing energy consumption, and enhancing long-term cost efficiency.

The increasing integration of renewable energy technologies and energy-efficient infrastructure is also strengthening sustainability strategies across the market. Operators investing in green building technologies and low-carbon infrastructure are improving regulatory compliance while meeting rising enterprise sustainability requirements.

At the same time, edge computing expansion and low-latency application demands are driving strategic investments in distributed data center networks. This shift is creating new opportunities for modular infrastructure providers, telecommunications companies, and regional colocation operators.

However, high construction costs, energy availability challenges, land constraints, cybersecurity risks, and complex regulatory requirements remain significant barriers affecting market scalability. Companies must continue investing in resilient infrastructure design, advanced energy management systems, and secure operational frameworks to maintain competitiveness.

Global Data Center Construction Market Technology & Innovation Forward Outlook

Looking ahead, the global data center construction market is expected to evolve toward highly automated, AI-optimized, and carbon-neutral digital infrastructure ecosystems. Future facilities will increasingly utilize intelligent automation systems capable of autonomously managing cooling, power distribution, maintenance scheduling, and workload optimization in real time.

Artificial intelligence will play a larger role in predictive infrastructure analytics, automated facility operations, energy optimization, and cybersecurity management. AI-driven digital twins and simulation platforms will increasingly support efficient facility planning and operational optimization.

Liquid cooling and advanced thermal management systems are expected to become standard technologies for next-generation AI-focused hyperscale facilities due to increasing power density requirements and energy efficiency demands.

The continued expansion of edge computing, 5G infrastructure, and IoT ecosystems will significantly increase deployment of modular and distributed data center facilities worldwide. Operators will focus on scalable edge architectures capable of supporting real-time processing and localized digital services.

Renewable-powered data centers, hydrogen-based backup power systems, and advanced battery storage technologies are also expected to emerge as major innovation areas supporting sustainable digital infrastructure development.

In conclusion, the Global Data Center Construction Market is undergoing a major technological transformation driven by AI integration, advanced cooling technologies, modular infrastructure, and sustainability-focused innovation. Companies that successfully combine engineering expertise, intelligent infrastructure management, and energy-efficient construction capabilities will lead the future evolution of the global data center construction industry.

Market Risk

Global Data Center Construction Market Risk Factors & Disruption Threats Overview

The global data center construction market is undergoing rapid expansion due to increasing demand for cloud computing, artificial intelligence workloads, hyperscale digital infrastructure, and enterprise data processing capabilities. Despite strong long-term growth potential, the market faces a highly complex risk environment driven by rising construction costs, energy supply constraints, geopolitical uncertainty, cybersecurity threats, regulatory pressures, and increasing sustainability expectations. As data centers become critical infrastructure supporting financial systems, government operations, telecommunications, AI ecosystems, and cloud platforms, operational disruptions or infrastructure failures can create widespread economic and technological consequences across global digital networks.

One of the primary risk factors in the data center construction market is power availability and energy infrastructure dependency. Modern hyperscale data centers require enormous amounts of electricity to support computing workloads, cooling systems, and backup power infrastructure. In several regions, energy grid limitations, power shortages, rising electricity costs, and delays in renewable energy integration are creating major constraints for new data center development. Increasing competition for reliable energy resources between industrial sectors, residential demand, and digital infrastructure operators is intensifying long-term energy security concerns within the industry.

Another major disruption threat involves rising construction costs and supply chain volatility across critical infrastructure components. Data center construction relies heavily on specialized equipment such as transformers, generators, semiconductors, cooling systems, electrical distribution units, fiber optic networking hardware, and advanced building materials. Global supply chain disruptions, raw material inflation, labor shortages, and transportation bottlenecks can significantly delay construction timelines and increase capital expenditure requirements. These risks are particularly severe for hyperscale facilities where project complexity and infrastructure scale are extremely high.

Geopolitical instability and regulatory fragmentation also represent substantial risks within the global data center construction ecosystem. Trade restrictions, cross-border technology controls, sanctions, and regional political tensions can disrupt access to critical technologies and international supply chains. In addition, governments are increasingly implementing stricter regulations related to data sovereignty, cybersecurity compliance, environmental impact, and local data storage requirements. Compliance with varying regulatory frameworks across regions increases operational complexity and may limit expansion opportunities for multinational infrastructure providers.

Cybersecurity and physical infrastructure security risks are becoming increasingly critical as data centers support essential digital services and AI-driven operations. Data centers are prime targets for cyberattacks, ransomware incidents, insider threats, and physical sabotage attempts. Any disruption to core infrastructure systems, cooling operations, or network connectivity can lead to large-scale service outages affecting enterprises, financial institutions, telecommunications providers, and government agencies. As facilities become more connected through AI-enabled monitoring and IoT-based infrastructure management systems, exposure to cyber vulnerabilities continues to increase.

Global Data Center Construction Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects unprecedented demand growth for hyperscale, colocation, and edge data center facilities due to expanding AI workloads, cloud computing adoption, and digital transformation initiatives worldwide. However, operators and construction firms are increasingly facing challenges related to energy capacity limitations, permitting delays, land availability constraints, and rising infrastructure development costs. In several major markets, utility providers are struggling to meet the electricity requirements of rapidly expanding data center clusters, creating delays in project approvals and operational deployment.

The accelerated growth of artificial intelligence and machine learning applications is significantly increasing power density requirements within modern data centers. AI workloads require advanced GPU infrastructure, high-performance computing clusters, and sophisticated cooling systems that consume substantially more electricity than traditional enterprise IT operations. This shift is increasing operational complexity and placing additional pressure on thermal management systems, power redundancy architecture, and sustainability targets.

Environmental and sustainability concerns are becoming central challenges in the current market landscape. Governments, regulators, and environmental organizations are scrutinizing the carbon footprint, water consumption, and land utilization of large-scale data center projects. Operators are under growing pressure to adopt renewable energy sourcing, energy-efficient cooling systems, low-carbon construction materials, and carbon-neutral operational strategies. Failure to meet sustainability expectations may lead to regulatory resistance, community opposition, and reputational damage.

Labor shortages and technical skill gaps are also affecting the pace of data center construction globally. The industry requires highly specialized expertise in electrical engineering, cooling infrastructure, fiber networking, cybersecurity systems, and AI-driven facility management. Shortages of skilled construction workers, engineers, and digital infrastructure specialists are increasing project timelines and operational costs, particularly in rapidly expanding regional markets.

Additionally, global macroeconomic uncertainty, inflationary pressures, and fluctuating interest rates are influencing investment decisions within the market. Since data center projects are highly capital-intensive, changes in financing conditions and construction cost escalation can impact project feasibility, return on investment expectations, and long-term expansion planning for infrastructure developers and cloud service providers.

Global Data Center Construction Market Key Risk Factors & Disruption Threat Signals

One of the most significant disruption signals in the market is the rapid rise of AI-optimized data centers and high-density computing infrastructure. AI applications require specialized facility designs capable of supporting extreme power loads, liquid cooling systems, and accelerated processing environments. While this creates strong growth opportunities, it also increases infrastructure complexity, cooling dependency, and energy consumption risk across future data center deployments.

Another major disruption trend involves the growing adoption of modular and edge data center architectures. Edge facilities are being deployed closer to end users to support low-latency applications such as autonomous systems, IoT networks, and 5G services. However, decentralized infrastructure models increase operational management complexity, cybersecurity exposure, and maintenance requirements across distributed facility networks.

The transition toward renewable-powered and carbon-neutral data center infrastructure is also reshaping competitive dynamics within the industry. Operators are increasingly investing in solar energy, wind power purchase agreements, battery storage systems, and advanced energy optimization technologies. While sustainability initiatives improve long-term operational resilience, they also require substantial capital investment and introduce dependency on renewable energy infrastructure availability.

Water scarcity and environmental resource limitations are emerging as additional long-term disruption threats. Advanced cooling systems used in hyperscale data centers often consume significant amounts of water, particularly in regions experiencing drought conditions or climate-related stress. Increasing environmental regulation and community opposition to high water usage may limit future construction opportunities in certain geographic regions.

In addition, rising regulatory focus on data sovereignty and localization requirements may disrupt global expansion strategies for cloud providers and colocation operators. Governments are increasingly requiring sensitive data to be stored within domestic borders, leading to fragmented infrastructure deployment models and increased compliance costs for multinational operators.

Global Data Center Construction Market Strategic Implications of Risk Factors

To address increasing energy-related risks, data center developers must prioritize long-term renewable energy partnerships, advanced power optimization technologies, and resilient backup energy infrastructure. Investment in battery storage systems, microgrids, and energy-efficient facility design will become essential for maintaining operational stability and regulatory compliance in power-constrained markets.

Companies operating within the market should also strengthen supply chain diversification strategies to reduce dependency on concentrated equipment sourcing regions and critical component suppliers. Building multi-regional procurement networks and maintaining strategic inventory reserves can improve resilience against semiconductor shortages, transportation disruptions, and geopolitical instability.

Cybersecurity resilience will become a strategic necessity as data centers increasingly support mission-critical digital infrastructure and AI-driven systems. Operators must implement advanced cybersecurity frameworks, zero-trust architectures, real-time monitoring systems, and AI-assisted threat detection capabilities to protect infrastructure integrity and ensure continuous service availability.

Sustainability integration will also play a critical role in long-term competitiveness. Developers and operators must invest in green construction methods, liquid cooling systems, low-carbon materials, renewable-powered operations, and water-efficient cooling technologies to align with evolving environmental regulations and investor expectations.

Strategic collaboration between cloud providers, energy companies, telecommunications operators, and infrastructure engineering firms will become increasingly important for supporting scalable and resilient digital infrastructure ecosystems. Integrated partnerships can improve project execution efficiency, accelerate renewable energy deployment, and strengthen operational scalability in rapidly growing markets.

Global Data Center Construction Market Forward Risk Outlook

Looking ahead to 2026–2033, the global data center construction market is expected to experience continued expansion driven by AI adoption, cloud infrastructure growth, digital transformation, and increasing global data generation. However, long-term market stability will depend heavily on the industry’s ability to manage energy availability, infrastructure scalability, cybersecurity resilience, and environmental sustainability challenges.

The future market landscape will increasingly shift toward AI-ready, modular, renewable-powered, and highly automated data center ecosystems. Technologies such as liquid cooling, AI-powered infrastructure management, edge computing architectures, and carbon-neutral facility operations are expected to become central competitive differentiators across the industry.

Overall, while the global data center construction market presents substantial long-term growth opportunities, sustainable competitive success will depend on balancing infrastructure expansion with energy efficiency, regulatory compliance, cybersecurity protection, environmental responsibility, and operational resilience across increasingly interconnected global digital ecosystems.

Regulatory Landscape

Global Data Center Construction Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global data center construction market is evolving rapidly as governments, environmental agencies, energy regulators, and digital infrastructure authorities strengthen frameworks related to data sovereignty, energy efficiency, cybersecurity, environmental sustainability, and critical infrastructure development. Data centers are increasingly recognized as strategic national infrastructure assets due to their essential role in supporting cloud computing, AI workloads, telecommunications, enterprise digital operations, and government data systems.

Governments across major economies are implementing policies to accelerate digital infrastructure expansion while ensuring compliance with environmental and energy management objectives. Regulatory frameworks now address multiple aspects of data center construction, including land use approvals, power consumption limits, carbon emissions, water usage, electrical safety standards, renewable energy integration, and operational resilience requirements.

The rapid growth of hyperscale cloud infrastructure and AI-driven computing demand has also intensified regulatory focus on energy efficiency and sustainability. Authorities in North America, Europe, and Asia-Pacific are increasingly introducing strict energy performance standards, green building requirements, and carbon reduction mandates for newly constructed data center facilities. This is encouraging adoption of advanced cooling systems, modular construction techniques, renewable energy sourcing, and intelligent energy management systems.

In addition, rising concerns regarding cybersecurity, national data protection, and digital sovereignty are influencing where and how data centers are constructed. Governments are implementing data localization policies and cross-border data transfer regulations that require enterprises and cloud providers to establish regional data center infrastructure capable of meeting domestic compliance obligations.

Global Data Center Construction Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for data center construction is heavily influenced by sustainability initiatives, digital infrastructure modernization programs, and national cybersecurity strategies. Developed economies are maintaining highly structured compliance frameworks covering energy consumption, emissions reporting, and operational reliability standards for data center facilities.

In North America, government agencies and local authorities are focusing on energy-efficient infrastructure development, renewable power integration, and resilience planning for critical digital infrastructure. Data center projects are increasingly required to comply with energy efficiency certifications, environmental impact assessments, and backup power reliability regulations.

Europe maintains one of the strictest regulatory environments globally, driven by the European Green Deal, carbon neutrality targets, and GDPR-related data sovereignty requirements. Data center operators in the region must comply with strict sustainability regulations covering carbon emissions, cooling efficiency, water conservation, and renewable energy sourcing. Regulatory pressure is also increasing regarding transparent reporting of energy usage and environmental performance metrics.

Asia-Pacific is witnessing rapid policy development as countries such as China, India, Singapore, Japan, and South Korea expand digital infrastructure capacity while balancing energy consumption concerns. Governments are introducing data center zoning policies, renewable energy mandates, and national cloud infrastructure programs to support digital economy growth while maintaining grid stability and environmental compliance.

Middle Eastern countries are increasingly positioning themselves as regional cloud and digital infrastructure hubs through supportive regulatory frameworks, smart city initiatives, and strategic investments in hyperscale data center projects. Latin America is also strengthening digital infrastructure policies to encourage foreign investment and support growing enterprise cloud adoption.

Key Regulatory & Policy Environment Signals in Global Data Center Construction Market

- Energy Efficiency & Sustainability Regulations: Governments are enforcing stricter power usage effectiveness (PUE) standards, carbon reduction targets, and renewable energy integration requirements for data center facilities.

- Data Sovereignty & Localization Policies: Countries are implementing regulations requiring sensitive data to be stored and processed within national or regional boundaries.

- Environmental Impact & Green Building Standards: Data center projects are increasingly subject to environmental impact assessments, green building certifications, and water conservation requirements.

- Cybersecurity & Critical Infrastructure Compliance: Governments are strengthening regulations related to physical security, cyber resilience, operational continuity, and infrastructure protection.

- Renewable Energy & Grid Integration Policies: Regulatory frameworks are encouraging data centers to utilize renewable energy sources and participate in smart grid energy optimization systems.

- Construction Safety & Electrical Standards: Compliance with international electrical safety codes, fire protection systems, and industrial construction standards remains essential for facility approvals.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is significantly influencing how data centers are designed, constructed, and operated globally. Data center developers are increasingly prioritizing energy-efficient architecture, renewable energy procurement, advanced cooling technologies, and modular infrastructure strategies to align with tightening sustainability regulations and environmental expectations.

Compliance with data sovereignty and localization regulations is driving regional expansion of hyperscale and colocation facilities. Cloud providers and multinational enterprises are investing heavily in localized infrastructure to meet jurisdiction-specific data storage and processing requirements while maintaining operational flexibility.

Environmental regulations are also accelerating innovation in liquid cooling systems, waste heat recovery, low-carbon construction materials, and AI-based energy management systems. Operators that successfully optimize energy efficiency while reducing environmental impact are gaining competitive advantages in securing government approvals and long-term enterprise partnerships.

Cybersecurity and infrastructure resilience regulations are increasing investments in physical security systems, backup power infrastructure, disaster recovery capabilities, and operational monitoring technologies. These compliance requirements are becoming particularly important for government, financial services, healthcare, and telecommunications data center deployments.

Global Data Center Construction Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global data center construction market is expected to become increasingly sustainability-focused, digitally integrated, and security-oriented. Governments are likely to strengthen carbon neutrality mandates, renewable energy requirements, and energy consumption reporting obligations for large-scale data center operators.

AI-driven infrastructure optimization and smart energy management systems are expected to become central components of future regulatory frameworks as authorities seek to balance digital infrastructure expansion with climate and energy goals. This will encourage broader adoption of intelligent cooling systems, automated workload optimization, and dynamic energy management technologies.

Data sovereignty regulations are expected to expand further as governments prioritize national digital security and strategic control over sensitive information. This will continue driving regionalized data center construction and localized cloud infrastructure development across multiple geographies.

Water usage regulations may also become increasingly important, particularly in regions facing resource constraints. Future data center construction projects are expected to face stricter requirements related to cooling efficiency, water recycling systems, and sustainable resource utilization practices.

Overall, the regulatory and policy environment will play a critical role in shaping the future structure, scalability, and sustainability of the global data center construction market. Companies that successfully align with environmental regulations, energy efficiency standards, cybersecurity frameworks, and digital sovereignty requirements will be best positioned to maintain long-term competitiveness and infrastructure leadership in the evolving global digital economy.