Global Craft Soda Market Report Analysis, Size and Forecast 2026-2033

Global Craft Soda Market Forecast Snapshot: 2026–2033

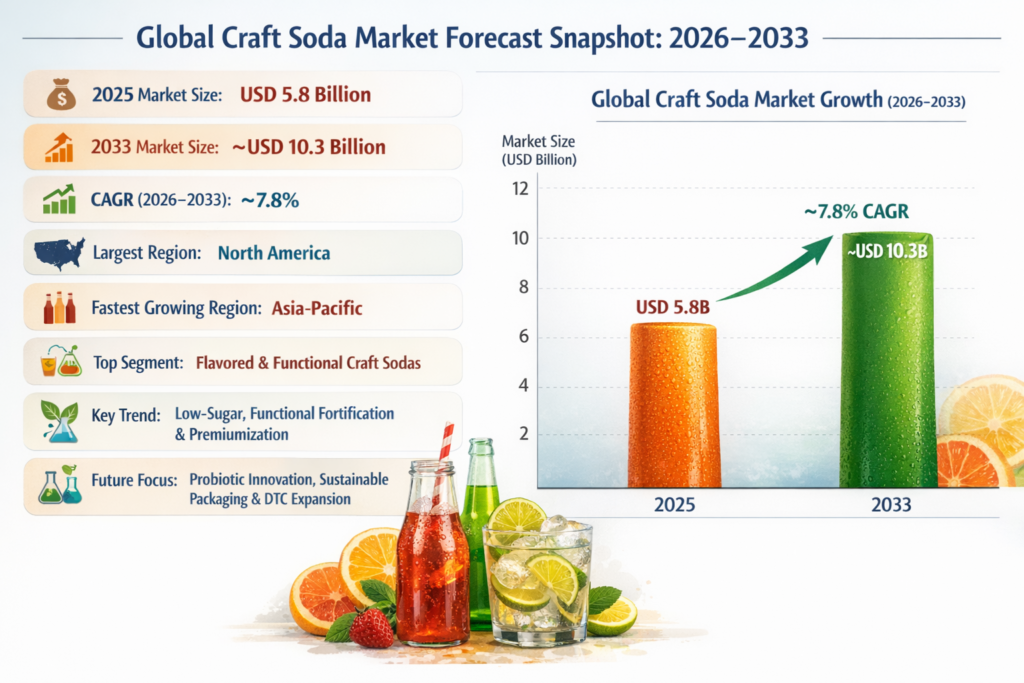

| Metric | Value |

|---|---|

| 2025 Market Size | USD 5.8 Billion |

| 2033 Market Size | ~USD 10.3 Billion |

| CAGR (2026–2033) | ~7.8% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Flavored & Functional Craft Sodas |

| Key Trend | Low-Sugar, Functional Fortification & Premiumization |

| Future Focus | Probiotic Innovation, Sustainable Packaging & DTC Expansion |

Global Craft Soda Market Overview

The Global Craft Soda Market is experiencing rapid transformation, driven by rising consumer demand for healthier, flavorful, and ethically produced beverages, coupled with innovation, premiumization, and sustainability trends. Craft soda formats—including flavored, functional, low-sugar, and fortified variants—are evolving into innovation-led, digitally enabled beverage ecosystems that cater to health-conscious and taste-driven consumers.

According to Pheonix Research, the Global Craft Soda Market is valued at USD 5.8 billion in 2025 and is projected to reach approximately USD 10.3 billion by 2033, registering a CAGR of ~7.8% (2026–2033). This revenue forecast reflects consistent growth fueled by premiumization, functional fortification, DTC and e-commerce expansion, and sustainable packaging adoption across both mature and emerging markets.

North America holds the largest market share, supported by high consumer awareness of probiotics and functional beverages, established craft soda brands, and widespread online and retail availability. Asia-Pacific is emerging as the fastest-growing region, driven by urbanization, rising disposable income, and increasing preference for natural, low-sugar, and functional beverages among younger consumers.

The Post-2025 outlook for the Craft Soda Market highlights continued innovation in flavor and functional ingredients, adoption of AI-driven consumer analytics, expansion of DTC subscription models, and sustainability initiatives, enabling brands to enhance market penetration, optimize operations, and respond effectively to evolving consumer preferences.

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Growth Highlights

1.3 Largest & Fastest Growing Regions

1.4 Dominant & Emerging Segments

1.5 Strategic Opportunity Areas

2. Global Craft Soda Market Overview

2.1 Definition & Product Scope

2.2 Evolution of Craft Soda Industry

2.3 Value Chain Analysis

2.4 Business Models (Artisanal, DTC, E-Commerce, Private Label)

2.5 Pricing Analysis

2.6 Regulatory Landscape

3. Market Forecast Snapshot (2026–2033)

3.1 2025 Market Size: USD 5.8 Billion

3.2 2033 Market Size: ~USD 10.3 Billion

3.3 CAGR (2026–2033): ~7.8%

3.4 Largest Region: North America

3.5 Fastest Growing Region: Asia-Pacific

3.6 Top Segment: Flavored & Functional Craft Sodas

3.7 Key Trend: Low-Sugar, Functional Fortification & Premiumization

3.8 Future Focus: Probiotic Innovation, Sustainable Packaging & DTC Expansion

4. Market Dynamics

4.1 Key Growth Drivers

4.2 Market Restraints

4.3 Emerging Opportunities

4.4 Industry Challenges

4.5 Impact of Macroeconomic Factors

5. Market Segmentation by Product Type (USD Billion), 2026–2033

5.1 Natural / Organic Craft Soda

5.1.1 Sugar-Free / Low-Sugar Natural Sodas

5.1.1.1 Stevia-Sweetened Sodas

5.1.1.2 Monk Fruit-Sweetened Sodas

5.1.1.3 Erythritol / Other Low-Calorie Sweeteners

5.1.2 Organic Fruit-Based Sodas

5.1.2.1 Citrus Organic Sodas (Lemon, Lime, Orange)

5.1.2.2 Berry Organic Sodas (Strawberry, Blueberry, Raspberry)

5.1.2.3 Tropical Organic Sodas (Mango, Pineapple, Passion Fruit)

5.1.3 Organic Botanical & Herbal Sodas

5.1.3.1 Herbal Infusions (Mint, Ginger, Lemongrass)

5.1.3.2 Floral Infusions (Hibiscus, Lavender, Rose)

5.1.3.3 Spiced / Exotic Botanical Blends

5.2 Conventional Craft Soda

5.2.1 Classic Cola Variants

5.2.1.1 Original Cola

5.2.1.2 Spiced / Flavored Cola

5.2.1.3 Regional Cola Blends

5.2.2 Traditional Root Beer & Ginger Ale

5.2.2.1 Root Beer Classic

5.2.2.2 Premium / Small-Batch Root Beer

5.2.2.3 Ginger Ale Variants (Spiced, Premium)

5.2.3 Standard Citrus & Fruit Blends

5.2.3.1 Lemon-Lime Sodas

5.2.3.2 Orange-Based Blends

5.2.3.3 Mixed Fruit Sodas

5.3 Functional & Botanical Infused Craft Soda

5.3.1 Vitamin & Mineral Fortified Sodas

5.3.1.1 Vitamin C Enriched Sodas

5.3.1.2 Multivitamin Craft Sodas

5.3.1.3 Mineral-Enriched Sodas

5.3.2 Adaptogen-Infused Sodas

5.3.2.1 Ashwagandha-Based Sodas

5.3.2.2 Ginseng-Infused Sodas

5.3.2.3 Herbal Adaptogen Blends

5.3.3 Herbal & Botanical Infusions

5.3.3.1 Hibiscus Craft Sodas

5.3.3.2 Lavender-Infused Sodas

5.3.3.3 Mint & Herbal Blends

6. Market Segmentation by Flavor (USD Billion), 2026–2033

6.1 Fruit-Based

6.1.1 Citrus (Lemon, Lime, Orange)

6.1.1.1 Lemon Craft Soda

6.1.1.2 Lime Craft Soda

6.1.1.3 Orange Craft Soda

6.1.2 Berry (Strawberry, Blueberry, Raspberry)

6.1.2.1 Strawberry

6.1.2.2 Blueberry

6.1.2.3 Raspberry

6.1.3 Tropical (Mango, Pineapple, Passion Fruit)

6.1.3.1 Mango

6.1.3.2 Pineapple

6.1.3.3 Passion Fruit

6.2 Spice & Herb-Based

6.2.1 Ginger Variants

6.2.1.1 Classic Ginger Ale

6.2.1.2 Spiced Ginger

6.2.1.3 Premium Small-Batch Ginger

6.2.2 Mint Infused

6.2.2.1 Mint-Citrus Blend

6.2.2.2 Herbal Mint Blend

6.2.2.3 Seasonal Mint Varieties

6.2.3 Cinnamon & Spice Blends

6.2.3.1 Cinnamon Citrus Sodas

6.2.3.2 Spiced Fruit Blends

6.2.3.3 Limited-Edition Seasonal Blends

6.3 Floral & Botanical

6.3.1 Hibiscus

6.3.2 Lavender

6.3.3 Rose & Other Floral Blends

6.4 Cola & Traditional Blends

6.4.1 Classic Cola

6.4.2 Blended Cola with Citrus / Spice

6.4.3 Root Beer & Traditional Craft Soda Mixes

7. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

7.1 Supermarkets & Hypermarkets

7.1.1 Premium Craft Soda Shelves

7.1.1.1 Organic / Natural Craft Sodas

7.1.1.2 Functional & Botanical Sodas

7.1.2 Limited-Edition Packs

7.1.2.1 Seasonal Collections

7.1.2.2 Holiday / Festive Packs

7.1.3 Promotional Bundles

7.1.3.1 Multi-Pack Combos

7.1.3.2 Retailer Exclusive Bundles

7.2 Convenience Stores

7.2.1 Single-Serve Bottles

7.2.2 Ready-to-Drink Multipacks

7.2.3 Seasonal or Regional Variants

7.3 Online Retail / E-Commerce

7.3.1 Third-Party Marketplaces

7.3.2 Brand-Owned Online Stores

7.3.3 Subscription Boxes / Curated Collections

7.4 Cafés & Specialty Beverage Stores

7.4.1 Barista-Style Craft Soda Mixes

7.4.2 Specialty Bottled Beverages

7.4.3 Seasonal & Experimental Flavors

8. Market Segmentation by End User (USD Billion), 2026–2033

8.1 Household Consumption

8.1.1 Daily Refreshment & Family Packs

8.1.2 Health-Conscious Home Consumption

8.1.3 Limited-Edition / Seasonal Packs

8.2 HoReCa (Hotels, Restaurants, Cafés)

8.2.1 Fine Dining Beverage Menus

8.2.2 Café & Specialty Drink Pairings

8.2.3 Event & Banquet Services

8.3 Specialty Retailers

8.3.1 Gourmet Stores

8.3.2 Organic / Health-Focused Retailers

8.3.3 Curated Beverage Shops

9. Market Segmentation by Region (USD Billion), 2026–2033

9.1 North America

9.2 Europe

9.3 Asia-Pacific

9.4 Latin America

9.5 Middle East & Africa

10. Regional Insights

10.1 North America – Market Leadership

10.2 Europe – Premiumization & Specialty Adoption

10.3 Asia-Pacific – Rapid Urbanization & Young Consumer Base

10.4 Latin America – Gradual Adoption & Urban Growth

10.5 Middle East & Africa – Urban & Premium Segment Expansion

11. Competitive Landscape

11.1 Market Share Analysis

11.2 Competitive Positioning Matrix

11.3 Mergers & Acquisitions

11.4 Product Launch & Innovation Trends

12. Company Profiles

12.1 Reed’s Inc.

12.2 Boylan Bottling Co.

12.3 Fentimans Ltd.

12.4 Virgil’s Soda Company

12.5 Brooklyn Bottling Co.

12.6 Q Drinks

12.7 Maine Root Soda

12.8 Polar Beverages

12.9 Sanpellegrino

12.10 SodaStream (Artisan & Botanical Lines)

13. Strategic Intelligence & AI-Driven Insights

13.1 Pheonix Demand Forecast Engine

13.2 Sentiment Analyzer Tool

13.3 Innovation Tracker

13.4 Porter’s Five Forces Analysis

13.5 Investment & Expansion Strategy Outlook

14. Why the Global Craft Soda Market Remains Critical

14.1 Health & Wellness Alignment

14.2 Sustainable Sourcing & Eco-Packaging

14.3 AI-Enabled Consumer Insights

14.4 Premiumization & Innovation Growth

14.5 Artisanal & Local Entrepreneurship

15. Appendix

16. About Us

17. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Craft Soda Market

Executive Framing

The Global Craft Soda Market is characterized by high competitive intensity and a fragmented market structure, where artisanal producers, regional brands, and select multinational beverage companies compete across premium, functional, and low-sugar segments. Unlike traditional carbonated soft drinks, craft soda emphasizes authenticity, natural ingredients, and innovative flavor profiles, making differentiation a key competitive lever. As consumer demand shifts toward clean-label, health-oriented, and ethically produced beverages, companies are increasingly focusing on premiumization, sustainability, and direct-to-consumer engagement strategies to strengthen market positioning.

Current Market Reality

The craft soda market is highly fragmented, with numerous small and mid-sized producers operating alongside a few established beverage brands such as Reed’s Inc., Boylan Bottling Co., and Fentimans Ltd. While global players like Sanpellegrino bring scale and distribution strength, the majority of market growth is driven by niche brands offering unique, small-batch, and functional beverages.

North America dominates the market due to strong craft beverage culture and high consumer awareness, while Asia-Pacific is emerging as a high-growth region driven by urbanization and demand for premium, natural beverages. E-commerce and DTC channels are playing a crucial role in enabling smaller brands to expand reach and build direct consumer relationships, intensifying competition across digital platforms.

Key Signals and Evidence

Several signals highlight the evolving competitive dynamics in the craft soda market:

- Rising demand for low-sugar, organic, and functional craft sodas with botanical and probiotic ingredients.

- Strong innovation in unique flavor combinations such as hibiscus-ginger, cucumber-mint, and citrus-herbal blends.

- Growth of direct-to-consumer (DTC) channels, subscription models, and online retail platforms.

- Increasing focus on sustainable packaging, including glass bottles, recyclable cans, and biodegradable materials.

- Expansion of craft soda presence in cafés, specialty stores, and premium hospitality segments.

Strategic Implications

Market participants must adopt agile and innovation-driven strategies to remain competitive:

- Product Differentiation: Developing functional, botanical, and low-sugar variants to cater to health-conscious consumers.

- Brand Positioning: Emphasizing authenticity, craftsmanship, and clean-label ingredients to build consumer trust.

- Distribution Expansion: Leveraging e-commerce, DTC channels, and specialty retail to increase market reach.

- Sustainability Focus: Investing in eco-friendly packaging and ethical sourcing practices.

- Innovation & Analytics: Utilizing AI-driven consumer insights and demand forecasting to optimize product development and marketing strategies.

Forward Outlook

By 2033, the Global Craft Soda Market is expected to reach approximately USD 10.3 billion, growing at a CAGR of ~7.8%. Growth will be driven by increasing consumer preference for healthier alternatives to traditional sodas, rising demand for premium and functional beverages, and continued innovation in flavors and formulations.

The market will evolve through a dual-structure model, where premium, small-batch, and functional craft sodas cater to niche, high-margin segments, while scalable flavored variants expand across retail and online channels. Companies that successfully integrate sustainability, digital engagement, and product innovation will be best positioned to capture long-term growth in this competitive and rapidly evolving market.

Value Chain

Global Craft Soda Market: Value Chain & Market Dynamics

Executive Framing

The Global Craft Soda Market operates within an innovation-driven and consumer-centric value chain, shaped by evolving preferences for healthier, flavorful, and ethically produced beverages. Unlike traditional carbonated drinks, craft sodas emphasize natural ingredients, small-batch production, and premium positioning, creating a differentiated and flexible operational ecosystem.

The value chain follows a hybrid structure, where established beverage companies leverage large-scale manufacturing and distribution, while emerging craft brands focus on niche formulations, local sourcing, and direct-to-consumer (DTC) engagement. This dual ecosystem supports both scalability and innovation.

However, variability in natural ingredient sourcing, clean-label compliance, and sustainability expectations introduces operational challenges, particularly for smaller players aiming to maintain consistency and cost efficiency.

Current Market Reality

The craft soda value chain reflects moderate complexity, balancing artisanal production with expanding global distribution. Leading players and regional brands operate across diverse sourcing and manufacturing models, ranging from in-house small-batch production to contract manufacturing partnerships.

Upstream activities involve sourcing natural sweeteners, fruit extracts, botanical infusions, and functional ingredients such as vitamins and adaptogens. The shift toward organic and low-sugar formulations has increased reliance on specialized suppliers.

Midstream processes include formulation, carbonation, bottling, and packaging, often emphasizing glass bottles, recyclable cans, and sustainable materials. Innovation cycles are relatively fast, driven by seasonal flavors and limited-edition releases.

Downstream, the market utilizes a hybrid distribution network including supermarkets, specialty stores, cafés, and rapidly growing e-commerce and subscription channels. DTC models are particularly important for brand differentiation and consumer engagement.

Despite growth, challenges such as higher production costs, shelf-life limitations, and competition from both large beverage companies and adjacent functional drink categories persist.

Key Signals and Evidence

Several indicators highlight the evolving craft soda value chain:

- Market growth from USD 5.8 billion (2025) to ~USD 10.3 billion (2033) at a CAGR of ~7.8%, reflecting strong demand for premium and functional beverages.

- Rising preference for low-sugar, organic, and clean-label formulations, reshaping ingredient sourcing and product development.

- Expansion of functional and botanical-infused sodas, enabling premium pricing and differentiation.

- Growth of e-commerce and DTC subscription models, reducing reliance on traditional retail channels.

- Increasing demand in Asia-Pacific, driving localized production and flavor innovation.

Supplier power remains moderate due to dependence on natural and specialty ingredients, while buyer power is high given the wide availability of alternatives and strong brand competition.

Strategic Implications

The craft soda market requires companies to balance innovation, cost efficiency, and brand differentiation. Large beverage companies benefit from scale and distribution, while smaller brands compete through unique flavors, clean-label positioning, and storytelling.

Technology adoption is becoming critical, with AI-driven consumer insights, demand forecasting, and product innovation enabling faster response to changing preferences. Additionally, sustainable packaging and ethical sourcing are essential for maintaining brand credibility.

DTC and subscription-based models provide higher margins and direct consumer relationships, allowing brands to build loyalty and gather valuable consumption data.

Forward Outlook

The craft soda value chain is expected to evolve with continued emphasis on health, sustainability, and digital transformation:

- Expansion of functional and probiotic-infused craft sodas

- Growth in DTC channels and personalized subscription models

- Increased focus on sustainable packaging and eco-friendly production

- Rising investment in AI-driven product development and consumer analytics

Companies that can deliver innovative flavors, clean-label products, and strong omnichannel presence will be best positioned for long-term growth.

In conclusion, the Global Craft Soda Market is transforming into a premium, health-focused, and innovation-led beverage ecosystem, where value chain agility and consumer alignment are key to competitive success.

Investment Activity

Investment & Funding Dynamics – Global Craft Soda Market

Executive Framing

Current Market Reality

The Global Craft Soda Market, valued at USD 5.8 billion in 2025 and projected to reach ~USD 10.3 billion by 2033 (CAGR ~7.8%), is witnessing rising investment activity. North America leads the market, while Asia-Pacific is the fastest-growing region attracting new capital inflows. Investments are primarily directed toward low-sugar formulations, functional beverages, sustainable packaging, and e-commerce expansion. Major players and emerging brands are leveraging funding to scale production, expand retail presence, and strengthen DTC subscription models. Strategic partnerships and selective acquisitions are helping companies enhance product portfolios and market reach.

Key Signals and Evidence

- Shift Toward Healthier Alternatives: Increasing demand for low-sugar, natural, and clean-label beverages is driving investment inflows.

- Flavor & Functional Innovation: Botanical, herbal, and adaptogen-infused sodas are attracting premium positioning and funding.

- DTC & E-Commerce Growth: Subscription models and online retail channels are enabling scalable revenue streams.

- Sustainability Initiatives: Investments in eco-friendly packaging, recyclable materials, and ethical sourcing are increasing.

- Youth-Driven Demand: Millennials and Gen Z consumers are driving demand for artisanal, innovative, and socially responsible brands.

- M&A Activity: Beverage companies are acquiring niche craft soda brands to expand functional beverage portfolios.

- AI & Data Analytics: AI-driven consumer insights and demand forecasting are shaping product development and marketing strategies.

Strategic Implications

Companies focusing on premiumization, health-oriented formulations, and sustainable practices are better positioned to attract investment and scale globally. Investors are prioritizing brands with strong differentiation, digital capabilities, and scalable production models. Strategic collaborations and acquisitions enable faster expansion into new markets and enhance innovation capabilities, particularly in functional and botanical soda segments.

Forward Outlook

Between 2026 and 2033, the Global Craft Soda Market is expected to experience sustained investment growth. Capital will increasingly flow toward functional beverage innovation, low-sugar formulations, sustainable packaging, and DTC ecosystem expansion. M&A activity is expected to remain active, particularly targeting emerging craft brands with strong consumer engagement. Investors focusing on AI-driven analytics, personalized beverage experiences, and global distribution strategies will capture long-term growth opportunities.

Technology & Innovation

Global Craft Soda Market: Technology & Innovation

Executive Framing

In the global craft soda market, technology and innovation are playing a pivotal role in transforming traditional carbonated beverages into premium, functional, and health-oriented offerings. As consumers increasingly demand low-sugar, clean-label, and naturally flavored beverages, manufacturers are leveraging advanced formulation techniques, AI-driven consumer insights, and sustainable production methods. Innovation spans across natural sweeteners, botanical infusions, probiotic fortification, and eco-friendly packaging, enabling brands to differentiate in a competitive and rapidly evolving beverage landscape.

Current Market Reality

The current craft soda market is characterized by rapid innovation in flavor development, functional ingredients, and production processes. Companies are adopting alternative sweeteners such as stevia and monk fruit to reduce sugar content while maintaining taste profiles. Functional sodas enriched with vitamins, adaptogens, and botanicals are gaining traction among health-conscious consumers. Additionally, digital platforms, e-commerce channels, and direct-to-consumer (DTC) models are enhancing brand reach and customer engagement. Sustainability initiatives, including recyclable packaging and small-batch production, are becoming core differentiators across leading brands.

Key Signals and Evidence

- Low-Sugar & Natural Formulation: Adoption of plant-based sweeteners and clean-label ingredients supports health-driven consumption trends.

- Functional & Probiotic Innovation: Integration of vitamins, adaptogens, and gut-health ingredients enhances product value and premium positioning.

- Flavor Experimentation: Unique botanical, herbal, and exotic fruit blends drive differentiation and consumer curiosity.

- Digital & DTC Expansion: E-commerce platforms and subscription models enable personalized experiences and recurring revenue streams.

- Sustainable Packaging: Increased use of recyclable materials, glass bottles, and eco-friendly production processes aligns with environmental expectations.

Strategic Implications

For craft soda producers, innovation enables premiumization, brand differentiation, and improved consumer loyalty. Functional and low-sugar products command higher margins while addressing health-conscious demand. Digital and DTC channels allow brands to build direct relationships with consumers and optimize marketing strategies through data analytics. Sustainability-focused innovations further strengthen brand equity and regulatory compliance. Companies that balance taste innovation, health benefits, and environmental responsibility are better positioned to capture market share.

Forward Outlook

The global craft soda market is expected to witness continued innovation driven by health trends, sustainability goals, and digital transformation. Future developments will focus on probiotic-infused sodas, advanced natural sweetener formulations, biodegradable packaging, and AI-powered product personalization. Expansion of DTC ecosystems and global e-commerce platforms will further accelerate market reach. Brands that successfully integrate functional benefits, sustainable practices, and digital engagement will achieve long-term competitive advantage in the post-2026 beverage landscape.

Market Risk

Risk Factors and Disruption Threats in the Global Craft Soda Market

Executive Framing

The Global Craft Soda Market is an emerging, innovation-driven beverage segment fueled by premiumization, functional fortification, and clean-label trends. With a projected CAGR of ~7.8% from 2026–2033, the market offers strong growth potential but also faces structural risks related to pricing sensitivity, competitive intensity, and evolving regulatory scrutiny on sugar content and health claims.

Current Market Reality

North America leads the market, while Asia-Pacific is the fastest-growing region. However, the industry faces challenges including higher pricing compared to conventional carbonated beverages, limited mass-market penetration, and dependence on niche consumer segments. Supply chain pressures related to natural ingredients, sustainable packaging, and small-batch production further impact cost structures and scalability.

Key Signals and Evidence

Key indicators include increasing demand for low-sugar, organic, and functional beverages, expansion of DTC and e-commerce channels, and rapid flavor innovation. At the same time, competition from functional drinks such as kombucha, flavored water, energy drinks, and traditional soft drinks is intensifying. Regulatory focus on labeling, sugar reduction, and functional claims is also shaping product development strategies.

Strategic Implications

Brands must focus on cost optimization, scalable production, and wider distribution to move beyond premium niches. Investment in sustainable packaging, natural ingredient sourcing, and AI-driven consumer analytics can help mitigate risks. Expanding into emerging markets and strengthening omnichannel presence across retail, cafés, and online platforms will be critical for long-term growth.

Forward Outlook

The Global Craft Soda Market is expected to grow steadily, supported by health-conscious consumption trends and product innovation. However, long-term success will depend on managing competitive substitution, maintaining pricing balance, and adapting to regulatory and consumer preference shifts.

Regulatory Landscape

Regulatory & Policy Landscape: Global Craft Soda Market

Executive Framing

The Global Craft Soda Market operates under evolving food and beverage regulations that emphasize ingredient safety, nutritional transparency, and health-related claims. As craft sodas increasingly position themselves as healthier, low-sugar, and functional alternatives to traditional carbonated drinks, regulatory scrutiny around labeling, sweeteners, and functional ingredients is intensifying.

Key regulatory authorities such as the U.S. Food and Drug Administration (FDA), European Food Safety Authority (EFSA), Food Safety and Standards Authority of India (FSSAI), and other global agencies govern product formulation, ingredient approvals, labeling standards, and marketing practices. These frameworks ensure consumer safety while influencing innovation and product positioning strategies.

With the inclusion of botanical extracts, adaptogens, vitamins, and natural sweeteners, craft soda products increasingly overlap with functional beverages, leading to stricter compliance requirements and greater regulatory oversight.

Current Market Reality

In North America, regulatory bodies enforce strict labeling requirements for sugar content, calorie disclosure, and ingredient transparency. Functional claims related to health benefits must be substantiated, particularly for products containing probiotics, adaptogens, or fortified nutrients.

Europe maintains stringent standards on clean-label products, organic certification, and artificial additives. EFSA closely monitors health claims and functional ingredient usage, requiring scientific validation for any marketed benefits.

Asia-Pacific markets, including India, China, and Japan, are tightening regulations around low-sugar labeling, artificial sweeteners, and imported beverage standards. Authorities such as FSSAI emphasize clear labeling, permissible additive limits, and consumer safety compliance.

Globally, sugar reduction initiatives, beverage taxation policies, and sustainability regulations related to packaging are reshaping product development and distribution strategies.

Key Signals and Evidence

- Mandatory nutritional labeling for sugar, calories, and ingredient composition.

- Increasing restrictions on added sugars and artificial sweeteners.

- Regulatory scrutiny of functional claims (probiotics, adaptogens, vitamins).

- Rising demand for organic, non-GMO, and clean-label certifications.

- Implementation of sugar taxes and public health policies in multiple regions.

- Expansion of sustainability regulations for recyclable and eco-friendly packaging.

Strategic Implications

Regulatory compliance is becoming a key differentiator in the craft soda market. Brands that prioritize transparent labeling, low-sugar formulations, and clean-label ingredients are better positioned to gain consumer trust and regulatory approval. Functional and fortified products require additional validation, increasing the importance of R&D investment and regulatory expertise.

Emerging brands must navigate complex regional regulations, particularly when expanding internationally. Established players benefit from scale and compliance capabilities, enabling faster market entry and broader distribution.

Sustainability-focused regulations are also influencing packaging decisions, encouraging the adoption of recyclable materials, reduced plastic usage, and environmentally responsible production processes.

Forward Outlook

Regulatory frameworks are expected to tighten further, particularly around sugar content, health claims, and functional ingredient validation. Governments will continue to promote healthier beverage consumption through taxation policies and labeling requirements, accelerating the shift toward low-sugar and natural formulations.

Sustainability will become a central regulatory focus, with stricter mandates on packaging waste reduction, carbon footprint disclosure, and eco-friendly materials. E-commerce channels will also face increased scrutiny regarding product labeling and claims transparency.

Companies that proactively align with evolving regulatory standards, invest in compliant innovation, and adopt sustainable practices will be best positioned to capture growth opportunities in the global craft soda market.