Global Critical Communication Market Size and Share Analysis 2026-2033

Global Critical Communication Market Size & Forecast

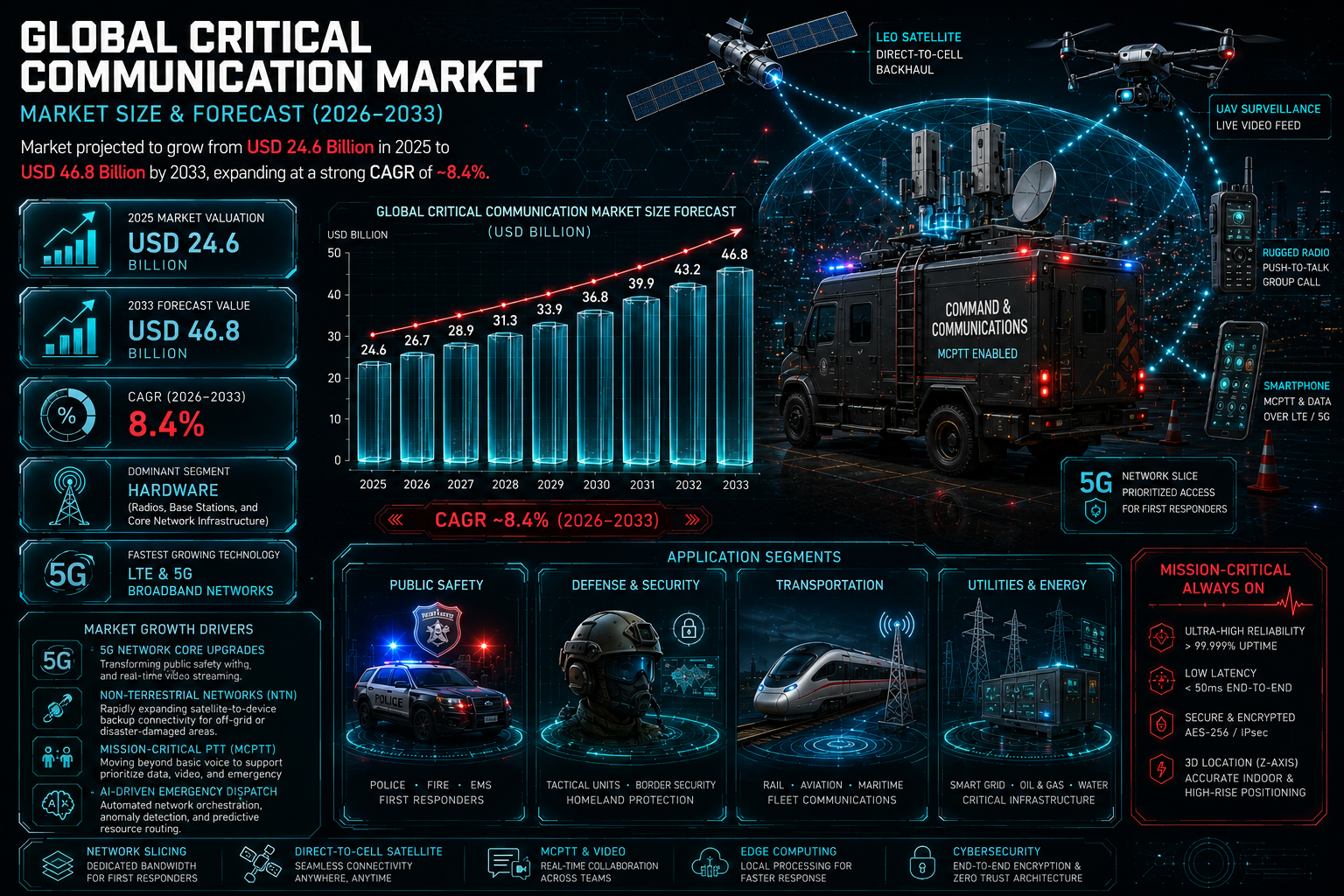

The global critical communication market is projected to witness substantial growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 24.6 billion in 2025 and is expected to reach nearly USD 46.8 billion by 2033, expanding at a CAGR of around 8.4%. The market growth is driven by rising public safety concerns, increasing investments in emergency response infrastructure, expanding deployment of mission-critical communication networks, and rapid adoption of broadband-based communication technologies across defense, transportation, utilities, and industrial sectors. Critical communication systems are specialized communication solutions designed to provide secure, reliable, real-time, and uninterrupted connectivity during emergency situations, disaster response operations, military missions, industrial accidents, and public safety incidents. The market is experiencing significant transformation through integration of LTE and 5G technologies, AI-powered dispatch systems, IoT-enabled emergency response platforms, satellite communication systems, and cloud-based command-and-control infrastructure. Additionally, increasing natural disasters, cybersecurity threats, urbanization, and modernization of public safety communication systems are accelerating global demand for advanced critical communication solutions.

Global Critical Communication Market Overview

The critical communication market forms a vital segment of the global telecommunications, public safety, and defense technology industries. These communication systems are essential for police forces, fire departments, emergency medical services, military operations, transportation authorities, energy utilities, mining companies, and industrial facilities. The market includes land mobile radio (LMR) systems, mission-critical push-to-talk (MCPTT) solutions, emergency dispatch systems, satellite communication systems, broadband public safety networks, and integrated command-and-control platforms. Modern critical communication solutions emphasize network resilience, ultra-low latency, secure encryption, interoperability, and real-time situational awareness capabilities. Technological advancements such as AI-based analytics, edge computing, software-defined radio, and integrated video communication are reshaping industry capabilities. Major market participants include Motorola Solutions Inc., Airbus SE, Nokia Corporation, Ericsson AB, Hytera Communications Corporation, Leonardo S.p.A., L3Harris Technologies, Huawei Technologies Co., Ltd., JVCKENWOOD Corporation, and AT&T Inc.Key Drivers of Global Critical Communication Market Growth

Increasing Public Safety and Emergency Response Requirements

Governments and emergency agencies are investing heavily in advanced communication systems to improve disaster response, law enforcement coordination, and emergency management capabilities. Reliable communication infrastructure is critical for ensuring operational efficiency during crises and large-scale emergencies.Expansion of LTE and 5G-Based Mission-Critical Networks

The deployment of broadband LTE and 5G networks is significantly enhancing mission-critical communication capabilities. High-speed data transmission, video streaming, and real-time situational awareness are improving field operations and decision-making.Growing Demand from Defense and Homeland Security Sectors

Military forces and homeland security agencies increasingly require secure, encrypted, and interoperable communication systems for mission-critical operations. Advanced tactical communication solutions are becoming central to modern defense strategies.Rising Industrial Safety and Operational Monitoring Needs

Industries such as oil & gas, mining, transportation, utilities, and manufacturing are adopting critical communication systems to enhance worker safety and operational coordination. Industrial digitalization is increasing demand for integrated communication and monitoring platforms.Increasing Natural Disasters and Climate-Related Emergencies

The growing frequency of floods, wildfires, earthquakes, and extreme weather events is driving investments in resilient emergency communication infrastructure. Governments worldwide are prioritizing disaster preparedness and rapid response capabilities.Global Critical Communication Market Segmentation

By Component

The market is segmented into hardware, software, and services. Hardware components such as radios, base stations, and network infrastructure account for a major market share.By Technology

The market includes land mobile radio (LMR), LTE, 5G, satellite communication, and hybrid communication systems. LTE and 5G-based critical communication systems are witnessing the fastest growth due to increasing broadband adoption.By Application

Applications include public safety, transportation, defense, utilities, mining, oil & gas, industrial manufacturing, and healthcare emergency services. Public safety and defense remain the dominant application segments globally.By End User

End users include government agencies, military organizations, emergency responders, industrial enterprises, transportation authorities, and utility providers. Government and public safety organizations account for the largest market demand.Regional Market Dynamics

North America

North America holds the largest share of the critical communication market due to advanced emergency response infrastructure, high public safety investments, and widespread deployment of broadband communication systems. The United States leads regional growth supported by FirstNet deployment and defense modernization programs.Europe

Europe represents a significant market driven by strong public safety regulations, transportation infrastructure modernization, and cross-border emergency communication initiatives. Countries such as Germany, the United Kingdom, France, and Italy are major regional contributors.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid urbanization, expanding smart city initiatives, and increasing investments in public safety infrastructure. China, India, Japan, South Korea, and Australia are key regional markets.Middle East & Africa

The Middle East & Africa region is witnessing strong growth due to increasing homeland security investments, oil & gas sector requirements, and smart infrastructure development. GCC countries are major adopters of advanced mission-critical communication systems.Latin America

Latin America is gradually expanding due to increasing public safety modernization initiatives and investments in emergency communication infrastructure. Brazil and Mexico represent leading regional markets.Competitive Landscape

The global critical communication market is highly competitive and technology-driven, with major players focusing on secure communication systems, broadband integration, and AI-enabled command solutions. Key companies include Motorola Solutions Inc., Airbus SE, Nokia Corporation, Ericsson AB, Hytera Communications Corporation, Leonardo S.p.A., L3Harris Technologies, Huawei Technologies Co., Ltd., JVCKENWOOD Corporation, and AT&T Inc. Companies are increasingly investing in mission-critical LTE, private 5G networks, AI-powered analytics, cloud-based dispatch platforms, and integrated communication ecosystems. Strategic collaborations with governments, defense agencies, telecom operators, and industrial enterprises are shaping the competitive landscape.Strategic Outlook

The strategic outlook for the global critical communication market remains highly positive due to increasing demand for secure, resilient, and real-time communication infrastructure. Future growth opportunities include AI-driven emergency response systems, autonomous communication networks, satellite-integrated public safety platforms, and next-generation 5G mission-critical services. Integration of IoT sensors, drones, edge computing, and advanced cybersecurity frameworks will further transform the market landscape. Organizations investing in interoperable communication ecosystems, low-latency broadband infrastructure, and cloud-native mission-critical platforms are expected to strengthen their competitive positioning.Final Market Perspective

The global critical communication market is becoming increasingly essential for ensuring public safety, defense readiness, industrial security, and disaster response efficiency worldwide. Growing investments in emergency communication infrastructure, smart cities, and mission-critical broadband technologies will continue driving market expansion throughout the forecast period. Companies that successfully combine advanced communication technologies, secure network capabilities, and integrated operational intelligence solutions will remain strongly positioned in the evolving global critical communication market.Table of Contents

Table of Contents

1. Executive Summary

- 1.1 Global Critical Communication Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Key Market Drivers & Opportunities

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Leadership & Growth Trends

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

2. Introduction & Market Overview

- 2.1 Definition of Critical Communication Systems

- 2.2 Scope of the Global Critical Communication Market

- 2.3 Market Size & Forecast (2026???2033)

- 2.4 Evolution of Mission-Critical Communication Technologies

- 2.5 Role of Critical Communication in Public Safety & Defense

- 2.6 Regulatory & Spectrum Management Landscape

- 2.7 Technology & Innovation Trends in Critical Communication

3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Data Collection & Validation Framework

- 3.4 Market Estimation Methodology

- 3.5 Forecast Assumptions (2026???2033)

- 3.6 Data Triangulation & Analytical Modeling

4. Market Dynamics

4.1 Market Drivers

- 4.1.1 Increasing Public Safety & Emergency Response Requirements

- 4.1.2 Expansion of LTE & 5G-Based Mission-Critical Networks

- 4.1.3 Growing Demand from Defense & Homeland Security Sectors

- 4.1.4 Rising Industrial Safety & Operational Monitoring Needs

- 4.1.5 Increasing Natural Disasters & Climate-Related Emergencies

4.2 Market Restraints

- 4.2.1 High Infrastructure Deployment Costs

- 4.2.2 Interoperability Challenges Across Legacy Systems

- 4.2.3 Cybersecurity Risks in Mission-Critical Networks

- 4.2.4 Regulatory & Spectrum Allocation Constraints

4.3 Market Opportunities

- 4.3.1 AI-Driven Emergency Response Platforms

- 4.3.2 Growth of Private LTE & 5G Networks

- 4.3.3 Satellite-Integrated Public Safety Communication Systems

- 4.3.4 Expansion of Smart City Communication Infrastructure

4.4 Market Challenges

- 4.4.1 Managing Network Reliability During Disasters

- 4.4.2 Integration Complexity Across Communication Platforms

- 4.4.3 Rising Demand for Ultra-Low Latency Connectivity

- 4.4.4 Data Privacy & Secure Encryption Requirements

5. Global Critical Communication Market Analysis (USD Billion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Technology Adoption Analysis

- 5.5 Public Safety Infrastructure Investment Trends

- 5.6 Communication Network Modernization Analysis

6. Market Segmentation (USD Billion), 2026???2033

6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

6.2 By Technology

- 6.2.1 Land Mobile Radio (LMR)

- 6.2.2 LTE

- 6.2.3 5G

- 6.2.4 Satellite Communication

- 6.2.5 Hybrid Communication Systems

6.3 By Application

- 6.3.1 Public Safety

- 6.3.2 Transportation

- 6.3.3 Defense

- 6.3.4 Utilities

- 6.3.5 Mining

- 6.3.6 Oil & Gas

- 6.3.7 Industrial Manufacturing

- 6.3.8 Healthcare Emergency Services

6.4 By End User

- 6.4.1 Government Agencies

- 6.4.2 Military Organizations

- 6.4.3 Emergency Responders

- 6.4.4 Industrial Enterprises

- 6.4.5 Transportation Authorities

- 6.4.6 Utility Providers

7. Market Segmentation by Region

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Middle East & Africa

- 7.5 Latin America

8. Regional Market Insights

- 8.1 North America Market Analysis

- 8.2 Europe Market Analysis

- 8.3 Asia-Pacific Market Analysis

- 8.4 Middle East & Africa Market Analysis

- 8.5 Latin America Market Analysis

9. Competitive Landscape

- 9.1 Market Share Analysis

- 9.2 Product Portfolio Benchmarking

- 9.3 LTE & 5G Mission-Critical Strategy Analysis

- 9.4 AI & Cloud Communication Integration Trends

- 9.5 Strategic Partnerships & Government Contracts

- 9.6 Competitive Positioning Analysis

10. Company Profiles

- 10.1 Motorola Solutions Inc.

- 10.2 Airbus SE

- 10.3 Nokia Corporation

- 10.4 Ericsson AB

- 10.5 Hytera Communications Corporation

- 10.6 Leonardo S.p.A.

- 10.7 L3Harris Technologies

- 10.8 Huawei Technologies Co., Ltd.

- 10.9 JVCKENWOOD Corporation

- 10.10 AT&T Inc.

11. Strategic Intelligence & AI Insights

- 11.1 AI-Powered Emergency Dispatch Systems

- 11.2 IoT & Edge Computing Integration Trends

- 11.3 Smart City Communication Infrastructure Outlook

- 11.4 Cybersecurity & Encrypted Communication Analysis

- 11.5 Porter???s Five Forces Analysis

12. Future Outlook & Strategic Recommendations

- 12.1 Future of Mission-Critical LTE & 5G Networks

- 12.2 Growth of AI-Enabled Public Safety Platforms

- 12.3 Expansion of Cloud-Native Communication Ecosystems

- 12.4 Integrated Disaster Response Strategies

- 12.5 Long-Term Market Outlook (2033+)

13. Appendix

14. About Pheonix Research

15. Disclaimer

Competitive Landscape

Global Critical Communication Market Competitive Intensity & Market Structure Overview

The global critical communication market is highly competitive, technology-driven, and moderately consolidated, with strong participation from telecommunications companies, defense contractors, public safety communication providers, and network infrastructure vendors. Competition is primarily centered around network reliability, secure communication capabilities, interoperability, low-latency performance, broadband integration, and mission-critical operational resilience.

The market structure is characterized by long-term government contracts, high regulatory compliance requirements, and strong dependence on advanced communication infrastructure. Large multinational companies dominate major public safety and defense projects, while specialized technology providers contribute to software platforms, encryption technologies, and integrated communication solutions.

Increasing convergence between telecommunications, public safety infrastructure, defense modernization, and industrial digitalization is intensifying competition across LTE, 5G, satellite communication, and hybrid mission-critical network ecosystems.

Global Critical Communication Market Competitive Intensity & Market Structure Current Scenario

Leading Critical Communication & Public Safety Technology Companies

Motorola Solutions Inc.: One of the global leaders in mission-critical communication systems, public safety networks, emergency dispatch platforms, and integrated command-and-control technologies.

Airbus SE: Major provider of secure communication solutions, public safety radio systems, and mission-critical network infrastructure for government and defense applications.

Nokia Corporation: Strong participant in private LTE, mission-critical broadband, industrial communication networks, and next-generation 5G infrastructure.

Ericsson AB: Leading telecommunications company actively expanding mission-critical LTE and 5G communication capabilities for emergency response and industrial sectors.

Hytera Communications Corporation: Key provider of professional mobile radio (PMR), land mobile radio (LMR), and integrated mission-critical communication systems.

Leonardo S.p.A.: Important defense and aerospace company offering secure tactical communication systems and integrated public safety technologies.

L3Harris Technologies: Major defense communication provider specializing in tactical radios, encrypted communication systems, and military network solutions.

Huawei Technologies Co., Ltd.: Active participant in broadband mission-critical communication infrastructure and smart city communication platforms.

JVCKENWOOD Corporation: Established provider of professional radio communication systems and public safety communication equipment.

AT&T Inc.: Significant telecom operator involved in mission-critical broadband services and public safety communication network deployment.

Key Competitive Intensity & Market Structure Drivers

The rapid transition from traditional land mobile radio systems toward LTE and 5G-based mission-critical communication platforms is significantly intensifying technological competition across the market.

Increasing public safety modernization programs and government investments in emergency communication infrastructure remain major competitive drivers globally.

Secure encryption, interoperability between agencies, and ultra-low latency communication capabilities are becoming critical differentiators for solution providers.

Industrial digitalization across oil & gas, mining, utilities, transportation, and manufacturing sectors is increasing demand for integrated critical communication ecosystems.

Artificial intelligence, IoT integration, cloud-native communication platforms, and real-time situational analytics are emerging as major competitive focus areas for technology vendors.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly investing in private 5G networks, mission-critical push-to-talk (MCPTT) platforms, and cloud-based dispatch systems to strengthen long-term market positioning.

Strategic partnerships between telecom operators, defense contractors, public safety agencies, and industrial enterprises are becoming increasingly important for integrated communication ecosystem development.

Interoperability across communication platforms and multi-agency coordination capabilities are becoming essential for securing large-scale government contracts and emergency response projects.

Cybersecurity and secure network architecture investments are growing rapidly due to rising concerns regarding cyberattacks, critical infrastructure protection, and national security risks.

Companies are also focusing on satellite-integrated communication systems and edge computing technologies to improve network resilience during disasters and remote-area operations.

Global Critical Communication Market Competitive Intensity & Market Structure Forward Outlook

The global critical communication market is expected to remain highly innovation-driven as governments, defense agencies, and industrial sectors increasingly prioritize resilient and real-time communication infrastructure.

Future competition is likely to intensify around AI-powered emergency response systems, autonomous communication networks, integrated drone communication platforms, and advanced mission-critical 5G applications.

The deployment of smart cities, connected transportation systems, and industrial IoT infrastructure is expected to create substantial opportunities for advanced communication solution providers.

North America and Europe are expected to maintain strong technological leadership, while Asia-Pacific continues witnessing rapid infrastructure expansion and public safety modernization investments.

Overall, organizations that successfully combine secure communication technologies, broadband interoperability, AI-enabled analytics, and scalable mission-critical infrastructure will remain strongly positioned in the evolving global critical communication market.

Value Chain

Global Critical Communication Market Value Chain & Supply Chain Evolution Overview

The global critical communication market value chain is evolving into a highly resilient, software-defined, and interoperability-focused ecosystem driven by increasing public safety requirements, defense modernization programs, industrial digitalization, and rapid deployment of mission-critical broadband networks. The industry is transitioning from traditional narrowband radio communication systems toward integrated LTE, 5G, satellite-enabled, and AI-powered communication infrastructures.

The value chain begins with upstream component sourcing and network infrastructure manufacturing, including semiconductors, antennas, radio frequency modules, fiber-optic systems, servers, cybersecurity hardware, routers, sensors, and communication chips. Suppliers of mission-critical electronic components and telecom infrastructure equipment play a vital role in ensuring system reliability, low latency, and secure connectivity.

The communication equipment and platform development stage forms the technological core of the market. Companies develop land mobile radio (LMR) systems, mission-critical push-to-talk (MCPTT) platforms, LTE and 5G communication modules, emergency dispatch systems, encrypted communication software, and satellite communication technologies. Advanced software integration, cloud-native architecture, and AI-driven analytics are significantly reshaping solution capabilities.

The system integration and deployment layer includes telecom operators, defense contractors, network integrators, public safety communication providers, and industrial automation companies responsible for implementing mission-critical communication ecosystems across transportation, utilities, defense, mining, healthcare, and emergency response sectors.

Post-deployment operations involve network monitoring, cybersecurity management, software upgrades, predictive maintenance, cloud hosting, and operational support services. Managed communication services and real-time analytics platforms are becoming increasingly important for maintaining continuous network performance and emergency readiness.

The distribution and commercialization layer is largely driven by government procurement agencies, telecom partnerships, industrial infrastructure projects, and public-private collaborations. Large-scale infrastructure modernization programs and smart city initiatives are strongly influencing global supply chain development.

Cybersecurity, interoperability, and network resilience are becoming foundational pillars across the value chain. Organizations are increasingly investing in encrypted communication systems, redundant network architectures, and AI-powered threat detection solutions to ensure uninterrupted mission-critical connectivity.

Global Critical Communication Market Value Chain & Supply Chain Evolution Current Scenario

The current critical communication supply chain is characterized by increasing convergence between telecommunications infrastructure, cloud computing, public safety systems, and defense communication technologies. The industry remains highly technology-intensive with strong involvement from telecom vendors, defense contractors, software providers, and infrastructure integrators.

North America dominates the market due to advanced public safety infrastructure, widespread deployment of broadband emergency communication systems, and strong investments in defense modernization. The United States leads the market through initiatives such as FirstNet and advanced mission-critical LTE deployment.

Europe maintains a strong market position through transportation modernization programs, cross-border emergency communication systems, and public safety interoperability initiatives supported by NATO and regional government agencies.

Asia-Pacific is emerging as the fastest-growing region due to rapid urbanization, increasing smart city investments, rising industrial safety requirements, and large-scale deployment of public safety communication infrastructure. China, India, Japan, South Korea, and Australia are investing heavily in next-generation mission-critical communication technologies.

The market is rapidly shifting toward broadband-based communication ecosystems integrating LTE, 5G, satellite communication, IoT sensors, drones, and cloud-native command-and-control platforms. This transition is enabling higher data throughput, real-time video communication, and advanced situational awareness capabilities.

However, the industry continues to face challenges related to interoperability limitations, cybersecurity threats, spectrum allocation complexities, infrastructure modernization costs, and supply chain vulnerabilities associated with telecom equipment and semiconductor dependencies.

Key Value Chain & Supply Chain Evolution Signals in Global Critical Communication Market

One of the most significant transformation signals is the rapid migration from traditional narrowband radio systems to broadband LTE and 5G mission-critical communication networks capable of supporting real-time data, video streaming, and AI-enabled operational analytics.

Another major signal is the growing integration of AI, edge computing, and cloud-native technologies into emergency response and command-and-control platforms, improving predictive decision-making and operational coordination.

The increasing deployment of private 5G networks across industrial facilities, transportation systems, utilities, and defense environments is reshaping enterprise communication infrastructure strategies.

Satellite communication integration is becoming increasingly important for remote operations, disaster response, military communication, and resilient connectivity in geographically challenging regions.

Cybersecurity is emerging as a strategic priority across the value chain as mission-critical networks become more interconnected and vulnerable to cyber threats. Organizations are investing heavily in encrypted communication systems, zero-trust architectures, and AI-powered cyber defense solutions.

Additionally, the integration of IoT devices, drones, wearable communication equipment, and smart sensors is expanding real-time situational awareness capabilities across emergency response and industrial safety applications.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Critical Communication Market

The evolving value chain presents significant strategic implications for telecom vendors, defense contractors, cloud service providers, government agencies, and industrial communication solution providers. Companies capable of delivering interoperable, secure, and scalable communication ecosystems are gaining strong competitive advantages.

Vertical integration across network infrastructure, software platforms, cybersecurity solutions, and managed communication services is becoming increasingly important for ensuring operational continuity and system reliability.

Investment in mission-critical LTE and private 5G infrastructure is emerging as a key growth strategy for telecom operators and technology providers seeking long-term public safety and industrial contracts.

Public-private partnerships and strategic collaborations between governments, telecom operators, and defense organizations are becoming central to communication infrastructure modernization initiatives worldwide.

Technological investment in AI-powered dispatch systems, edge computing, predictive analytics, and cloud-based command centers is improving emergency response efficiency and operational intelligence capabilities.

Long-term competitiveness in the critical communication market will depend on balancing network resilience, interoperability, cybersecurity, scalability, and cost-efficient infrastructure deployment strategies.

Global Critical Communication Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the critical communication value chain is expected to become increasingly software-defined, AI-enabled, and cloud-integrated. Mission-critical communication systems will evolve toward fully connected, data-centric operational ecosystems supporting autonomous decision-making and real-time collaboration.

5G standalone networks, satellite broadband integration, edge AI processing, and ultra-low latency communication systems will significantly enhance emergency response coordination, industrial safety operations, and defense communication capabilities.

AI-driven emergency response systems, predictive incident analytics, and autonomous communication management platforms are expected to improve disaster preparedness and operational efficiency across public safety organizations.

The integration of drones, robotic systems, wearable communication devices, and IoT-enabled sensors will further expand situational awareness and remote operational capabilities.

Cybersecurity frameworks will become increasingly advanced with implementation of quantum-resistant encryption, AI-powered threat intelligence, and zero-trust communication architectures across mission-critical networks.

Ultimately, the future critical communication value chain will evolve into a highly secure, interoperable, and intelligent communication ecosystem where resilience, real-time analytics, network autonomy, and integrated digital infrastructure define long-term market competitiveness.

Market-Specific Value Chain

- Component & Network Infrastructure Sourcing: Semiconductor manufacturers, antenna suppliers, RF module providers, fiber-optic infrastructure companies, telecom hardware manufacturers

- Communication System Development: LMR developers, LTE and 5G platform providers, emergency dispatch software companies, cybersecurity solution providers, satellite communication developers

- System Integration & Deployment: Telecom operators, defense contractors, public safety communication integrators, industrial network deployment companies

- Managed Services & Operational Support: Cloud service providers, AI analytics companies, cybersecurity monitoring firms, predictive maintenance service providers

- Distribution & Government Procurement: Public safety agencies, military procurement organizations, transportation authorities, utility companies, industrial enterprises

- End-Use Applications: Public safety, defense communication, emergency response, transportation systems, utilities, oil & gas operations, mining, industrial manufacturing, healthcare emergency services

Investment Activity

Global Critical Communication Market Investment & Funding Dynamics Overview

Investment and funding activity in the global critical communication market is accelerating rapidly due to increasing public safety modernization programs, rising geopolitical and cybersecurity threats, growing deployment of mission-critical broadband infrastructure, and expanding adoption of LTE and 5G-enabled emergency communication systems. Between 2026 and 2033, investments are expected to increasingly target resilient communication networks, AI-powered emergency response platforms, satellite-integrated communication systems, private 5G infrastructure, and cloud-native command-and-control technologies.

The critical communication industry is evolving into a strategically essential segment of the global telecommunications, defense, and public safety ecosystem. Governments, telecom operators, defense contractors, and industrial enterprises are significantly increasing investments in secure, low-latency, interoperable communication solutions capable of supporting emergency response operations, disaster management, industrial safety, and military coordination.

A major structural transformation influencing investment activity is the transition from legacy land mobile radio (LMR) systems toward broadband-based mission-critical communication platforms. Public safety agencies and industrial organizations are increasingly investing in next-generation communication systems that support real-time video transmission, AI-assisted analytics, geolocation tracking, and integrated situational awareness capabilities.

The market is also benefiting from rising investments in smart city infrastructure, industrial digitalization, autonomous emergency response systems, IoT-enabled operational monitoring, and advanced cybersecurity frameworks. Expansion of connected public safety ecosystems and cross-agency interoperability initiatives is creating substantial long-term funding opportunities globally.

Global Critical Communication Market Investment & Funding Dynamics Current Scenario

Current investment activity in the critical communication market is strongly supported by increasing government spending on emergency communication infrastructure, rapid deployment of private LTE and 5G networks, and growing demand for resilient communication systems across defense, transportation, utilities, mining, and industrial sectors. Companies are actively investing in AI-driven dispatch systems, edge computing capabilities, secure communication protocols, and cloud-based operational intelligence platforms to improve response efficiency and network reliability.

- North America: Dominates global investment activity due to extensive public safety modernization programs, strong defense expenditure, FirstNet network expansion, and advanced broadband communication infrastructure across the United States and Canada.

- Europe: Witnessing strong investment growth supported by cross-border emergency communication initiatives, transportation modernization programs, and increasing adoption of secure digital communication platforms.

- Asia-Pacific: Emerging as the fastest-growing investment region due to rapid urbanization, smart city development, increasing disaster management initiatives, and rising investments in public safety infrastructure across China, India, Japan, South Korea, and Australia.

- Middle East & Africa: Attracting growing investments driven by homeland security modernization, oil & gas communication requirements, critical infrastructure protection, and smart government initiatives.

Key Investment & Funding Dynamics Signals in Global Critical Communication Market

- Expansion of LTE and 5G-based mission-critical networks is driving investments into broadband communication infrastructure and ultra-low latency operational systems.

- Growing public safety modernization programs are increasing funding for AI-powered emergency dispatch platforms, integrated command centers, and advanced situational awareness technologies.

- Rising cybersecurity threats are encouraging investments into encrypted communication systems, secure network architectures, and cyber-resilient mission-critical platforms.

- Increasing natural disasters and climate-related emergencies are supporting investments in disaster recovery communication systems and resilient emergency response infrastructure.

- Industrial digitalization across utilities, mining, oil & gas, and transportation sectors is creating strong investment demand for integrated operational communication ecosystems.

- Satellite communication integration and hybrid communication architectures are emerging as important innovation areas attracting telecom and defense technology investments.

- Deployment of IoT-enabled sensors, drones, and autonomous emergency systems is accelerating investments in real-time data transmission and edge-based operational analytics.

Strategic Implications of Investment & Funding Dynamics in Global Critical Communication Market

- The investment landscape increasingly favors companies capable of combining secure communication infrastructure, broadband expertise, and AI-driven operational intelligence platforms.

- Technological innovation is becoming a major competitive differentiator, particularly in low-latency communication, interoperability, predictive analytics, and cloud-native mission-critical services.

- Strategic collaborations between telecom operators, defense contractors, public safety agencies, and cloud technology providers are becoming increasingly important for large-scale communication ecosystem deployment.

- Regional diversification strategies remain critical, with North America leading broadband public safety innovation, Europe emphasizing cross-border interoperability, and Asia-Pacific driving rapid smart city and emergency infrastructure expansion.

- Companies investing in hybrid communication architectures integrating LTE, 5G, satellite, and legacy radio systems are expected to achieve stronger long-term competitive positioning.

- AI-assisted incident management, predictive emergency analytics, and real-time operational intelligence are emerging as major investment priorities across public safety and industrial sectors.

- Organizations with strong cybersecurity capabilities, scalable network infrastructure, and integrated communication ecosystems are expected to maintain stronger market leadership globally.

Global Critical Communication Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the global critical communication market is expected to attract strong long-term investment supported by increasing demand for resilient communication infrastructure, expansion of smart public safety systems, and rising adoption of mission-critical broadband technologies.

Future capital allocation will prioritize private 5G networks, AI-powered emergency response platforms, cloud-native communication ecosystems, autonomous operational coordination systems, satellite-integrated communication technologies, and advanced cybersecurity-driven mission-critical infrastructure.

- North America: Will remain the leading investment region due to continued public safety broadband deployment, advanced defense communication modernization, and strong technology innovation ecosystems.

- Asia-Pacific: Will continue strengthening its market position through rapid smart city expansion, emergency response modernization, and increasing government investments in secure communication infrastructure.

- Europe: Will increasingly focus on interoperable emergency communication systems, secure digital infrastructure, and integrated transportation communication networks.

Future funding activity is also expected to accelerate across drone-integrated emergency communication systems, AI-assisted operational command centers, edge-enabled situational awareness platforms, and next-generation disaster management technologies.

Public safety modernization, digital infrastructure resilience, and secure broadband communication technologies will remain central investment priorities across the critical communication industry. The growing convergence of AI, IoT, cloud computing, and mission-critical connectivity will continue reshaping competitive dynamics globally.

Overall, the market is expected to maintain strong long-term investment momentum due to its expanding role in public safety, industrial security, defense readiness, and emergency response operations. Companies that successfully combine advanced communication technologies, scalable network infrastructure, cybersecurity expertise, and integrated operational intelligence capabilities will remain strongly positioned to lead the global critical communication market through 2033.

Technology & Innovation

Global Critical Communication Market Technology & Innovation Landscape Overview

The global critical communication market is undergoing rapid technological transformation driven by the increasing need for secure, resilient, low-latency, and real-time communication systems across public safety, defense, transportation, utilities, and industrial sectors. Technological innovation is centered around broadband mission-critical communication networks, AI-powered situational awareness platforms, cloud-native communication infrastructure, and next-generation interoperability solutions.

Critical communication systems are evolving beyond traditional land mobile radio (LMR) networks toward integrated LTE, private 5G, satellite, and hybrid communication ecosystems capable of supporting voice, video, data, and IoT-enabled emergency response operations. The integration of advanced digital technologies is significantly improving operational coordination, disaster response efficiency, and field-level intelligence gathering.

The market is also witnessing increasing adoption of edge computing, AI-assisted dispatch systems, real-time geolocation services, software-defined radio (SDR), and secure encrypted communication frameworks to strengthen mission-critical operations in highly dynamic environments.

Global Critical Communication Market Technology & Innovation Current Scenario

Currently, the critical communication industry is transitioning from narrowband radio infrastructure toward broadband-enabled mission-critical communication systems capable of supporting high-speed multimedia transmission and integrated operational intelligence.

Mission-critical LTE (MC-LTE) and private 5G networks are becoming increasingly important for emergency responders, defense agencies, transportation operators, and industrial enterprises. These technologies enable ultra-low latency communication, high-bandwidth video streaming, and seamless interoperability across multiple operational units.

Artificial intelligence and advanced analytics are increasingly integrated into command-and-control platforms to improve emergency response decision-making, incident prediction, threat detection, and operational resource allocation.

Satellite communication technologies are also gaining momentum, particularly in remote locations, disaster recovery operations, military deployments, maritime applications, and areas with limited terrestrial network infrastructure.

Cybersecurity innovation has become a critical focus area as communication networks face rising cyber threats and data security challenges. Companies are investing heavily in encrypted communication protocols, zero-trust architectures, secure identity management systems, and AI-driven threat detection technologies.

Key Technology & Innovation Trends in Global Critical Communication Market

- Mission-Critical LTE and 5G: Deployment of broadband communication networks supporting ultra-low latency, real-time video, and data-intensive emergency operations.

- AI-Powered Dispatch Systems: Artificial intelligence integration for emergency response optimization, predictive analytics, and automated incident management.

- Private 5G Networks: Dedicated secure communication infrastructure for defense, industrial facilities, utilities, and transportation systems.

- Software-Defined Radio (SDR): Flexible communication platforms enabling multi-band, multi-network interoperability and scalable communication capabilities.

- Edge Computing Integration: Real-time data processing at the network edge improving response speed and operational intelligence.

- Satellite Communication Systems: Advanced satellite-based communication enabling connectivity in remote, disaster-hit, and military operational environments.

- IoT-Enabled Emergency Response: Integration of sensors, drones, connected devices, and smart monitoring systems into mission-critical communication platforms.

- Advanced Encryption Technologies: Secure communication frameworks protecting sensitive operational data from cyber threats and unauthorized access.

- Integrated Video Communication: Real-time body camera streaming, drone surveillance feeds, and video analytics improving situational awareness.

- Cloud-Based Command Platforms: Cloud-native communication infrastructure enabling scalable emergency coordination and centralized operational management.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally transforming the critical communication market from traditional radio-based systems into highly connected, intelligent, and data-driven communication ecosystems. Organizations adopting broadband communication infrastructure and AI-powered operational platforms are gaining significant advantages in emergency response efficiency, operational coordination, and situational awareness.

The shift toward LTE and private 5G communication systems is improving interoperability between emergency agencies, military units, transportation networks, and industrial operations. This convergence is enabling seamless voice, video, and data integration across mission-critical environments.

Cybersecurity is becoming a strategic differentiator within the market as communication systems increasingly handle sensitive operational and national security data. Vendors investing in advanced encryption technologies and secure communication frameworks are strengthening competitive positioning.

At the same time, the integration of IoT devices, drones, edge analytics, and cloud-based platforms is expanding the scope of mission-critical communication capabilities beyond traditional voice communications toward fully integrated operational intelligence ecosystems.

However, challenges related to infrastructure costs, interoperability standards, cybersecurity complexity, and spectrum availability continue to influence market deployment strategies globally.

Global Critical Communication Market Technology & Innovation Forward Outlook

Looking ahead, the global critical communication market is expected to evolve toward highly autonomous, AI-driven, and fully interconnected communication ecosystems capable of supporting real-time decision-making across complex operational environments.

Future innovation will focus on autonomous emergency response coordination, AI-based predictive incident management, integrated drone communication systems, and advanced satellite-terrestrial hybrid communication networks.

Private 5G and future 6G technologies are expected to significantly enhance mission-critical communication performance through ultra-reliable low-latency connectivity, network slicing, and advanced edge intelligence capabilities.

The growing integration of digital twins, smart city infrastructure, biometric identification systems, and advanced operational analytics will further strengthen situational awareness and emergency response effectiveness.

Cloud-native mission-critical platforms and cross-agency interoperability frameworks will continue improving communication scalability, resilience, and operational flexibility across public safety and industrial sectors.

Overall, the technology and innovation landscape of the global critical communication market is evolving toward intelligent, secure, broadband-enabled, and highly resilient communication ecosystems that will play an increasingly vital role in public safety, defense operations, industrial security, and disaster response worldwide.

Market Risk

Global Critical Communication Market Risk Factors & Disruption Threats Overview

The global critical communication market is undergoing rapid transformation driven by rising public safety requirements, increasing adoption of LTE and 5G-based mission-critical networks, and growing investments in emergency response infrastructure. Despite strong long-term growth potential, the market faces several significant risks including cybersecurity threats, network infrastructure vulnerabilities, regulatory complexities, interoperability challenges, high deployment costs, and evolving technological disruption.

One of the most critical disruption threats affecting the market is the increasing frequency and sophistication of cyberattacks targeting communication infrastructure. Critical communication systems are widely used in defense, emergency response, utilities, transportation, and public safety operations, making them highly sensitive targets for cyber espionage, ransomware attacks, signal interception, and network disruption attempts.

The market also faces substantial risks associated with network reliability and infrastructure resilience. Mission-critical communication systems require uninterrupted connectivity during disasters, emergencies, and large-scale incidents. Power outages, infrastructure failures, natural disasters, satellite disruptions, and telecom network congestion may compromise operational effectiveness and emergency response coordination.

Rapid technological evolution presents another major challenge for industry participants. The transition from legacy land mobile radio (LMR) systems to LTE and 5G-based communication platforms requires significant infrastructure upgrades, interoperability management, and long-term investment planning. Organizations unable to modernize quickly may face operational limitations and reduced competitiveness.

Interoperability challenges across communication platforms, agencies, and jurisdictions also remain a major concern. Public safety organizations, military agencies, industrial operators, and emergency responders often use different communication standards and technologies, creating integration difficulties during coordinated operations.

Regulatory compliance and spectrum allocation complexities further increase market uncertainty. Governments tightly regulate mission-critical communication frequencies, encryption standards, and public safety network operations. Delays in spectrum allocation, changing telecom regulations, and international compliance requirements may impact deployment timelines and operational scalability.

Additionally, high implementation and maintenance costs may restrict adoption among smaller municipalities, emerging economies, and budget-constrained organizations. Advanced mission-critical communication systems require substantial investments in infrastructure, cybersecurity, maintenance, training, and ongoing software upgrades.

Global Critical Communication Market Risk Factors & Disruption Threats Current Scenario

The current critical communication market environment reflects increasing global demand for resilient, secure, and broadband-enabled communication systems across public safety, defense, transportation, industrial, and emergency response sectors.

Governments worldwide are accelerating modernization of emergency communication infrastructure through deployment of private LTE networks, mission-critical push-to-talk (MCPTT) platforms, AI-powered command centers, and integrated public safety ecosystems.

The rapid deployment of 5G technologies is creating new opportunities for ultra-low-latency communication, real-time video streaming, drone coordination, and IoT-enabled emergency response systems. However, this transition is also increasing technological complexity and cybersecurity exposure.

Rising geopolitical tensions, natural disasters, urban security challenges, and industrial safety concerns are significantly increasing demand for interoperable and highly resilient communication systems. At the same time, communication providers face mounting pressure to ensure secure data transmission, operational continuity, and compliance with evolving cybersecurity regulations.

The market is also witnessing increasing convergence between telecom operators, cloud service providers, satellite communication companies, and public safety agencies, reshaping the competitive landscape and accelerating ecosystem integration.

Global Critical Communication Market Key Risk Factors & Disruption Threat Signals

- Cybersecurity Threats: Increasing risks of cyberattacks, ransomware, signal interception, and network breaches targeting mission-critical infrastructure.

- Network Reliability Risks: Potential service disruption caused by power failures, telecom outages, natural disasters, and infrastructure damage.

- Technological Transition Challenges: Migration from legacy LMR systems to LTE and 5G platforms requiring complex infrastructure upgrades.

- Interoperability Issues: Difficulties integrating communication systems across agencies, regions, and technology standards.

- Regulatory & Spectrum Allocation Constraints: Government regulations and spectrum licensing complexities impacting deployment timelines.

- High Capital & Maintenance Costs: Significant investments required for infrastructure modernization and cybersecurity upgrades.

- Supply Chain Disruptions: Dependence on semiconductors, telecom equipment, network hardware, and satellite communication components.

- Geopolitical & National Security Risks: Trade restrictions, sanctions, and political tensions affecting communication technology supply chains.

- Data Privacy & Compliance Pressure: Increasing requirements related to secure communication, encryption, and sensitive data management.

- Rapid Technology Obsolescence: Continuous advancements in AI, edge computing, cloud communication, and 5G networks shortening technology lifecycles.

Strategic Implications of Risk Factors

Critical communication providers must prioritize advanced cybersecurity frameworks, encrypted communication protocols, AI-driven threat detection, and resilient network architectures to mitigate operational and national security risks.

Organizations should accelerate investment in interoperable LTE and 5G communication ecosystems capable of integrating public safety agencies, industrial operations, satellite systems, and IoT-enabled emergency response infrastructure.

Strategic partnerships between telecom operators, governments, defense organizations, and cloud service providers will become increasingly important for supporting scalable and resilient mission-critical communication networks.

Companies are also expected to diversify component sourcing strategies and strengthen semiconductor supply chain resilience to reduce exposure to geopolitical and logistics disruptions.

Continuous investment in AI-powered dispatch systems, edge computing, real-time analytics, and autonomous communication technologies will remain essential for maintaining competitive positioning within the rapidly evolving market landscape.

Global Critical Communication Market Forward Risk Outlook

Looking ahead to 2026???2033, the critical communication market is expected to remain highly innovation-driven as governments and enterprises increasingly prioritize resilient communication infrastructure, disaster preparedness, and secure operational coordination.

Future market dynamics will be shaped by AI-integrated emergency response systems, autonomous network management, satellite-enabled public safety platforms, drone-assisted communication networks, and private 5G mission-critical ecosystems.

However, cybersecurity threats, infrastructure vulnerabilities, spectrum management challenges, and rapid technological disruption are expected to remain major operational and strategic concerns for market participants.

The increasing integration of cloud-native communication platforms, IoT sensors, edge computing, and real-time situational awareness technologies will further increase complexity while creating new growth opportunities.

Overall, while the global critical communication market offers strong long-term growth potential driven by public safety modernization and industrial digitalization, long-term competitiveness will depend on cybersecurity resilience, interoperability capabilities, infrastructure reliability, and continuous technological innovation.

Regulatory Landscape

Global Critical Communication Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global critical communication market is heavily influenced by public safety mandates, national security requirements, telecommunications regulations, cybersecurity frameworks, and emergency response modernization initiatives. Critical communication systems are considered essential infrastructure in many countries due to their role in supporting emergency services, military operations, disaster response, transportation safety, and industrial security.

Governments and regulatory authorities worldwide are increasingly prioritizing resilient, interoperable, and secure communication networks capable of operating during crises, natural disasters, cyberattacks, and large-scale emergencies. Regulatory frameworks are evolving to support next-generation broadband technologies including LTE, private 5G, satellite communications, and mission-critical push-to-talk (MCPTT) systems.

The market is also being shaped by growing policy emphasis on cybersecurity resilience, spectrum allocation efficiency, cross-agency interoperability, and modernization of legacy land mobile radio (LMR) infrastructure. In parallel, smart city development programs and critical infrastructure protection policies are accelerating investments in advanced communication ecosystems.

Global Critical Communication Market Regulatory & Policy Environment Current Scenario

The current regulatory environment for critical communication systems is characterized by a combination of telecom regulations, emergency response mandates, defense communication standards, and national cybersecurity policies. Governments worldwide are implementing stricter requirements for communication reliability, network redundancy, and secure data transmission for mission-critical operations.

In the United States, critical communication infrastructure is regulated through agencies including the Federal Communications Commission (FCC), Department of Homeland Security (DHS), and National Institute of Standards and Technology (NIST). Programs such as FirstNet are driving nationwide deployment of broadband public safety communication networks with enhanced interoperability and emergency response capabilities.

In Europe, regulatory frameworks are guided by the European Electronic Communications Code (EECC), cybersecurity directives, and public safety communication modernization programs. European governments are increasingly supporting mission-critical broadband systems and cross-border emergency communication interoperability across EU member states.

Asia-Pacific countries are rapidly strengthening regulatory support for critical communication infrastructure due to increasing urbanization, disaster preparedness initiatives, and smart city expansion. China, Japan, South Korea, India, and Australia are investing heavily in next-generation emergency communication systems, private LTE networks, and public safety spectrum allocation.

Middle Eastern countries are focusing on homeland security modernization, critical infrastructure protection, and secure communication systems for defense and energy sectors. Latin America and Africa are gradually expanding regulatory frameworks to improve emergency response coordination, public safety modernization, and disaster management communication networks.

Key Regulatory & Policy Environment Signals in Global Critical Communication Market

- Public Safety Communication Regulations: Governments are mandating reliable emergency communication systems for police, fire, healthcare, and disaster response agencies.

- Spectrum Allocation Policies: Regulatory authorities are allocating dedicated frequency bands for mission-critical LTE, 5G, and emergency communication services.

- Cybersecurity and Data Protection Standards: Critical communication systems are increasingly subject to strict cybersecurity compliance, encryption requirements, and secure network architecture standards.

- Interoperability Mandates: Governments are promoting interoperability between communication systems to improve coordination among emergency response agencies and defense organizations.

- Critical Infrastructure Protection Policies: Energy, transportation, utilities, and industrial sectors are required to implement resilient communication systems to support operational continuity and security.

- Disaster Preparedness and Resilience Programs: National disaster management policies are accelerating investments in redundant and highly available communication infrastructure.

- 5G and Broadband Modernization Initiatives: Governments are supporting migration from legacy radio systems toward broadband-based mission-critical communication platforms.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is significantly influencing investment priorities and technology adoption across the critical communication market. Organizations are increasingly investing in secure, standards-compliant, and interoperable communication systems to align with government mandates and public safety requirements.

The shift toward broadband mission-critical communication is encouraging telecom operators, defense contractors, and technology providers to accelerate deployment of LTE and private 5G networks optimized for emergency response and industrial safety applications.

Cybersecurity regulations are also driving substantial investments in encrypted communication systems, AI-powered threat monitoring, and resilient network architectures capable of operating under cyberattack or infrastructure failure scenarios.

Regulatory support for smart cities, transportation modernization, and industrial digitalization is creating additional demand for integrated communication ecosystems capable of supporting real-time operational intelligence and emergency coordination.

Defense modernization programs and cross-border security cooperation initiatives are further strengthening long-term market opportunities for advanced critical communication technologies.

Global Critical Communication Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global critical communication market is expected to become increasingly focused on broadband connectivity, cybersecurity resilience, AI-enabled emergency response systems, and integrated public safety communication infrastructure.

Governments are likely to expand dedicated public safety spectrum allocation policies and accelerate nationwide deployment of mission-critical 5G networks to support real-time video communication, drone operations, IoT integration, and advanced situational awareness capabilities.

Cybersecurity and data sovereignty regulations are expected to become more stringent, particularly for defense, public safety, and critical infrastructure communication systems. This will increase demand for secure cloud-native communication platforms and zero-trust network architectures.

International cooperation on disaster response, border security, and emergency communication interoperability is expected to strengthen harmonization of technical standards and operational frameworks across regions.

The growing adoption of AI, edge computing, satellite communications, and autonomous emergency response technologies will further reshape regulatory frameworks governing mission-critical communication systems.

Overall, the regulatory and policy environment will remain a major driver of innovation and infrastructure investment within the critical communication market, with organizations that prioritize secure, interoperable, and compliance-ready communication ecosystems expected to maintain strong long-term competitive positioning.