Global Electrolytic Manganese Dioxide Market Size and Share Analysis 2026-2033

Global Electrolytic Manganese Dioxide Market Size & Forecast

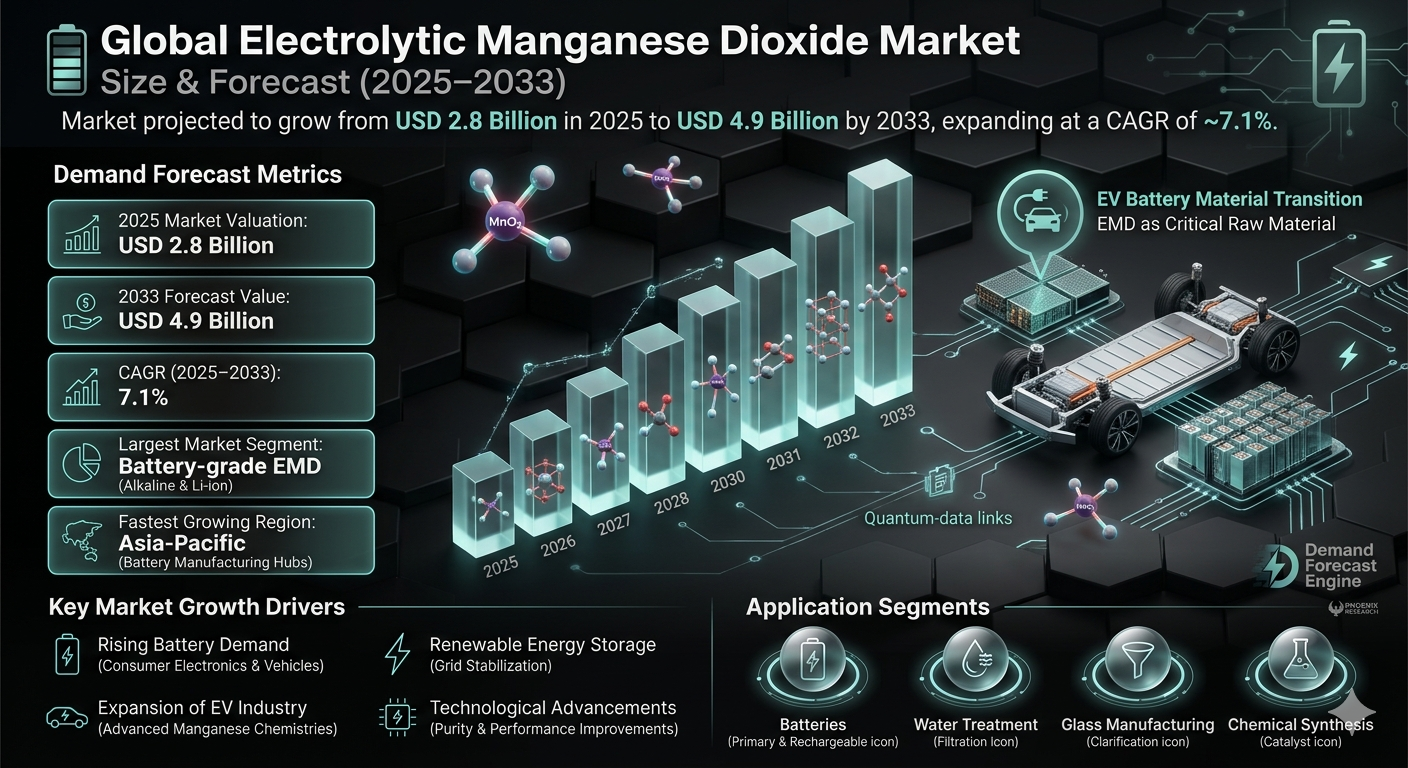

The global electrolytic manganese dioxide (EMD) market is projected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 2.8 billion in 2025 and is expected to reach nearly USD 4.9 billion by 2033, expanding at a CAGR of around 7.1%. The market growth is driven by rising demand for batteries, increasing adoption of electric vehicles (EVs), expanding renewable energy storage infrastructure, and growing industrial applications of manganese compounds. Electrolytic manganese dioxide is a highly purified form of manganese dioxide produced through an electrolytic process. It is widely used as a cathode material in alkaline batteries, lithium-ion batteries, zinc-carbon batteries, and other energy storage applications due to its excellent electrochemical properties and high purity levels. The market is experiencing significant momentum due to increasing global battery production, rapid electrification trends, and technological advancements in energy storage systems. Additionally, the transition toward sustainable energy solutions and rising investments in EV battery manufacturing are further accelerating demand for high-quality electrolytic manganese dioxide worldwide.

Global Electrolytic Manganese Dioxide Market Overview

The electrolytic manganese dioxide market forms an essential segment of the global battery materials and specialty chemicals industry. EMD serves as a critical raw material for battery manufacturers producing consumer electronics batteries, automotive batteries, and industrial energy storage systems. The market includes high-density EMD, chemical manganese dioxide (CMD), battery-grade EMD, and specialty-grade manganese dioxide products. Technological advancements in cathode material engineering, battery chemistry optimization, and sustainable manganese extraction technologies are reshaping the competitive landscape. Growing demand for rechargeable batteries, portable electronics, and large-scale energy storage systems is creating strong opportunities for EMD manufacturers globally. Major market participants include Tosoh Corporation, Mesa Minerals Limited, Prince International Corporation, Xiangtan Electrochemical Scientific Ltd., Tronox Holdings plc, Cegasa International, CITIC Dameng Holdings Ltd., and ERACHEM Comilog.Key Drivers of Global Electrolytic Manganese Dioxide Market Growth

Rising Demand for Batteries

Electrolytic manganese dioxide is widely used in alkaline and lithium-ion batteries due to its high energy density and electrochemical stability. Increasing battery demand from consumer electronics, automotive, and industrial sectors is significantly driving market growth.Expansion of Electric Vehicle Industry

The rapid growth of electric vehicles is increasing demand for advanced battery materials, including high-purity manganese compounds. Battery manufacturers are increasingly adopting manganese-based chemistries to improve battery performance and cost efficiency.Growth of Renewable Energy Storage Systems

Large-scale renewable energy projects require efficient battery storage systems for grid stabilization and energy management. EMD-based batteries are increasingly used in stationary energy storage applications.Increasing Consumption of Consumer Electronics

Growing global demand for smartphones, laptops, wearable devices, and portable electronics is supporting battery production growth. This directly contributes to rising consumption of electrolytic manganese dioxide.Technological Advancements in Battery Chemistry

Continuous innovation in battery materials and cathode technologies is improving manganese utilization in advanced batteries. Manufacturers are focusing on higher purity levels and improved electrochemical performance.Global Electrolytic Manganese Dioxide Market Segmentation

By Type

The market is segmented into battery-grade EMD, chemical-grade EMD, and specialty-grade EMD. Battery-grade EMD dominates the market due to widespread use in alkaline and lithium-ion batteries.By Application

Applications include alkaline batteries, lithium-ion batteries, zinc-carbon batteries, water treatment, glass manufacturing, and chemical synthesis. Battery applications account for the largest market share globally.By End User

End users include battery manufacturers, electronics companies, automotive manufacturers, chemical industries, and industrial energy storage providers. Battery manufacturers remain the dominant end-user segment.By Purity Level

The market includes standard purity EMD and high-purity EMD. High-purity EMD is witnessing strong growth due to increasing adoption in advanced lithium-ion batteries.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global electrolytic manganese dioxide market due to strong battery manufacturing infrastructure, rapid EV adoption, and large-scale electronics production. China, Japan, South Korea, and India are major regional contributors. China remains the leading producer and consumer of EMD globally.North America

North America is witnessing strong growth due to increasing EV production, battery gigafactory investments, and renewable energy storage projects. The United States leads regional demand supported by battery supply chain localization initiatives.Europe

Europe is experiencing increasing demand driven by aggressive EV adoption targets, battery manufacturing expansion, and sustainability regulations. Germany, France, and the Nordic countries are major contributors.Latin America

Latin America is gradually expanding due to increasing industrialization and growing battery demand. Brazil and Mexico represent key emerging markets.Middle East & Africa

The region is witnessing moderate growth supported by mining activities, industrial applications, and increasing energy infrastructure investments.Competitive Landscape

The global electrolytic manganese dioxide market is moderately consolidated, with major players competing on purity levels, production efficiency, and battery-grade quality standards. Key companies include Tosoh Corporation, Prince International Corporation, Mesa Minerals Limited, Xiangtan Electrochemical Scientific Ltd., Tronox Holdings plc, Cegasa International, CITIC Dameng Holdings Ltd., and ERACHEM Comilog. Companies are increasingly investing in advanced refining technologies, sustainable manganese extraction, and battery material innovation. Strategic partnerships with battery manufacturers and EV companies are becoming increasingly important for long-term supply agreements.Strategic Outlook

The strategic outlook for the global electrolytic manganese dioxide market remains highly positive due to rising global battery demand and accelerating electrification trends. Future growth opportunities include next-generation lithium-ion battery chemistries, grid-scale energy storage systems, and sustainable battery recycling technologies. Increasing investments in battery supply chain localization and critical mineral processing are expected to strengthen market development. Manufacturers investing in high-purity EMD production, environmentally sustainable processes, and long-term battery industry partnerships are likely to gain strong competitive advantages.Final Market Perspective

The global electrolytic manganese dioxide market is becoming increasingly important within the evolving battery materials and energy storage ecosystem. Growing demand for electric vehicles, renewable energy systems, and portable electronics will continue driving market expansion throughout the forecast period. Organizations that successfully combine high-purity production capabilities, sustainable sourcing, and advanced battery material innovation will remain strongly positioned in the evolving electrolytic manganese dioxide market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Electrolytic Manganese Dioxide Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Key Growth Highlights

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Market Insights

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Electrolytic Manganese Dioxide (EMD)

- 2.2 Scope of the Study

- 2.3 Market Evolution & Industry Background

- 2.4 Value Chain Analysis

- 2.5 Raw Material Supply & Processing Overview

- 2.6 Regulatory Framework & Sustainability Trends

- 2.7 Technological Advancements in EMD Production

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Methodology

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Demand for Batteries

- 4.1.2 Expansion of Electric Vehicle Industry

- 4.1.3 Growth of Renewable Energy Storage Systems

- 4.1.4 Increasing Consumption of Consumer Electronics

- 4.1.5 Technological Advancements in Battery Chemistry

- 4.2 Restraints

- 4.2.1 Volatility in Manganese Raw Material Prices

- 4.2.2 High Energy Consumption in EMD Production

- 4.2.3 Environmental & Mining Regulations

- 4.2.4 Competition from Alternative Battery Materials

- 4.3 Opportunities

- 4.3.1 Expansion of Lithium-Ion Battery Manufacturing

- 4.3.2 Increasing Investments in Battery Gigafactories

- 4.3.3 Sustainable & Recycled Battery Material Development

- 4.3.4 Emerging Grid-Scale Energy Storage Applications

- 4.4 Challenges

- 4.4.1 Supply Chain Disruptions

- 4.4.2 Maintaining High Purity Standards

- 4.4.3 Carbon Emission Reduction Pressures

- 4.4.4 Global Trade & Export Restrictions

- 4.1 Drivers

- 5. Global Electrolytic Manganese Dioxide Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Revenue Forecast Analysis

- 5.4 Demand-Supply Analysis

- 5.5 Battery Industry Consumption Trends

- 5.6 Pricing Trend Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Type

- 6.1.1 Battery-Grade EMD

- 6.1.1.1 High-Purity Battery Materials

- 6.1.1.1.1 Lithium-Ion Battery Applications

- 6.1.1.1.1.1 EV Battery Systems

- 6.1.1.1.1 Lithium-Ion Battery Applications

- 6.1.1.1 High-Purity Battery Materials

- 6.1.2 Chemical-Grade EMD

- 6.1.2.1 Industrial Chemical Applications

- 6.1.3 Specialty-Grade EMD

- 6.1.3.1 Advanced Electrochemical Applications

- 6.1.1 Battery-Grade EMD

- 6.2 By Application

- 6.2.1 Alkaline Batteries

- 6.2.2 Lithium-Ion Batteries

- 6.2.3 Zinc-Carbon Batteries

- 6.2.4 Water Treatment

- 6.2.5 Glass Manufacturing

- 6.2.6 Chemical Synthesis

- 6.3 By End User

- 6.3.1 Battery Manufacturers

- 6.3.2 Electronics Companies

- 6.3.3 Automotive Manufacturers

- 6.3.4 Chemical Industries

- 6.3.5 Industrial Energy Storage Providers

- 6.4 By Purity Level

- 6.4.1 Standard Purity EMD

- 6.4.2 High-Purity EMD

- 6.1 By Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Production Capacity Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Sustainability & ESG Initiatives

- 8.5 Technology & Product Innovation Analysis

- 9. Company Profiles

- 9.1 Tosoh Corporation

- 9.2 Prince International Corporation

- 9.3 Mesa Minerals Limited

- 9.4 Xiangtan Electrochemical Scientific Ltd.

- 9.5 Tronox Holdings plc

- 9.6 Cegasa International

- 9.7 CITIC Dameng Holdings Ltd.

- 9.8 ERACHEM Comilog

- 9.9 Manganese Metal Company

- 9.10 Vibrantz Technologies

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Battery Materials Supply Chain Analyzer

- 10.3 EV Battery Demand Monitoring System

- 10.4 Sustainable Mining & Processing Tracker

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of EV Battery Manufacturing

- 11.2 Growth in Renewable Energy Storage Systems

- 11.3 Investment in High-Purity EMD Production

- 11.4 Sustainable Battery Recycling Opportunities

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Electrolytic Manganese Dioxide Market Competitive Intensity & Market Structure Overview

The global electrolytic manganese dioxide (EMD) market is moderately consolidated and highly quality-sensitive, with competition primarily centered around product purity, battery-grade performance, production scalability, raw material access, and long-term supply agreements with battery manufacturers. Market participants are increasingly focusing on advanced refining technologies and sustainable production methods to strengthen their competitive positioning.

The market structure includes multinational specialty chemical companies, manganese processing firms, battery material suppliers, and regional EMD manufacturers serving consumer electronics, automotive, and industrial energy storage industries. Growing demand for lithium-ion batteries and alkaline batteries is intensifying competition among suppliers globally.

Rapid electrification trends, renewable energy expansion, and increasing investments in battery gigafactories are reshaping the competitive environment, particularly for manufacturers capable of producing high-purity EMD suitable for advanced battery chemistries.

Global Electrolytic Manganese Dioxide Market Competitive Intensity & Market Structure Current Scenario

Leading Electrolytic Manganese Dioxide & Battery Material Companies

Tosoh Corporation: Major producer of high-purity electrolytic manganese dioxide used in advanced battery applications with strong technological expertise in specialty chemicals.

Prince International Corporation: Important supplier of manganese-based materials and specialty compounds serving global battery and industrial markets.

Mesa Minerals Limited: Focused on manganese processing and battery-grade EMD production for energy storage and industrial applications.

Xiangtan Electrochemical Scientific Ltd.: Leading Chinese EMD manufacturer with strong production capabilities supporting large-scale battery manufacturing demand.

Tronox Holdings plc: Active participant in specialty chemical and mineral processing markets with involvement in manganese dioxide supply chains.

Cegasa International: Established battery technology company involved in manganese dioxide-based energy storage applications and battery manufacturing.

CITIC Dameng Holdings Ltd.: Major integrated manganese producer with extensive mining and manganese processing operations supporting EMD production.

ERACHEM Comilog: Key global supplier of manganese-based specialty materials focused on battery and industrial-grade manganese products.

Key Competitive Intensity & Market Structure Drivers

The rapid expansion of electric vehicle production and lithium-ion battery manufacturing is significantly increasing competition among EMD suppliers to secure long-term contracts with battery manufacturers.

High-purity EMD production capability is becoming a major competitive differentiator as advanced battery chemistries require enhanced electrochemical performance and material consistency.

Growing demand for renewable energy storage systems is accelerating investments in battery-grade manganese materials and integrated supply chain development.

Asia-Pacific, particularly China, continues to dominate global production and consumption, intensifying regional competition among large-scale manganese processing companies.

Sustainability and environmentally responsible extraction processes are becoming increasingly important as battery manufacturers prioritize ethical sourcing and lower-carbon supply chains.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly investing in advanced purification technologies, process optimization, and production efficiency improvements to enhance battery-grade EMD quality.

Strategic partnerships and long-term supply agreements with EV battery manufacturers are becoming critical for ensuring stable demand and strengthening market positioning.

Vertical integration strategies involving manganese mining, refining, and battery material production are gaining importance to improve supply chain security and cost control.

Companies are also focusing on regional production expansion, particularly in North America and Europe, to support battery supply chain localization initiatives and reduce dependency on imports.

Research and development activities related to next-generation manganese-based cathode materials and recyclable battery technologies are expected to further influence competitive dynamics.

Global Electrolytic Manganese Dioxide Market Competitive Intensity & Market Structure Forward Outlook

The global electrolytic manganese dioxide market is expected to become increasingly strategic within the broader battery materials ecosystem as electrification and renewable energy adoption accelerate worldwide.

Future competition will likely focus on high-purity EMD production, sustainable extraction technologies, localized battery supply chains, and compatibility with advanced lithium-ion battery chemistries.

Battery recycling and circular economy initiatives are expected to create new opportunities for manganese recovery and secondary raw material integration within EMD production processes.

Asia-Pacific is expected to remain the dominant manufacturing hub, while North America and Europe are likely to witness rapid investment growth due to battery localization and EV infrastructure expansion.

Overall, companies that successfully combine scalable production capacity, high-purity processing expertise, sustainable sourcing practices, and strategic battery industry partnerships will remain strongly positioned in the evolving global electrolytic manganese dioxide market.

Value Chain

Global Electrolytic Manganese Dioxide Market Value Chain & Supply Chain Evolution Overview

The global electrolytic manganese dioxide (EMD) market value chain is evolving rapidly as rising battery demand, electric vehicle (EV) adoption, renewable energy storage expansion, and advanced battery material innovation reshape the global energy storage ecosystem. Electrolytic manganese dioxide has emerged as a critical battery-grade material widely used in alkaline batteries, lithium-ion batteries, zinc-carbon batteries, and industrial energy storage systems due to its superior electrochemical performance, high purity levels, and cost-effective cathode properties.

The market value chain encompasses manganese ore mining, manganese refining, electrolytic processing, purification technologies, cathode material manufacturing, battery integration, and downstream energy storage applications. EMD manufacturers are increasingly focusing on high-purity production technologies, energy-efficient refining systems, environmentally sustainable extraction processes, and advanced battery-grade material development to meet the rapidly expanding demand from EV manufacturers, battery producers, and renewable energy storage providers.

The global EMD ecosystem involves mining companies, manganese refiners, electrolytic processing facilities, battery material suppliers, cathode manufacturers, battery cell producers, automotive OEMs, energy storage system providers, and recycling companies. Major companies including Tosoh Corporation, Mesa Minerals Limited, Prince International Corporation, Xiangtan Electrochemical Scientific Ltd., Tronox Holdings plc, CITIC Dameng Holdings Ltd., ERACHEM Comilog, and Cegasa International are actively investing in capacity expansion, sustainable processing technologies, and long-term supply agreements with battery manufacturers.

Upstream supply chain activities depend heavily on manganese ore availability, mining infrastructure, chemical refining systems, electrolytic processing technologies, energy-intensive production facilities, industrial automation systems, and environmental compliance infrastructure. Midstream operations focus on purification, quality control, battery-grade processing, and logistics optimization to ensure consistent material performance for battery applications. Downstream demand is increasingly driven by EV battery gigafactories, consumer electronics manufacturing, grid-scale energy storage systems, and industrial battery applications.

Operational strategies across the EMD value chain increasingly prioritize supply security, purity optimization, production scalability, energy efficiency, sustainable sourcing, and battery chemistry compatibility. However, the industry continues to face challenges associated with raw material price volatility, environmental regulations, energy-intensive production processes, geopolitical supply chain risks, mining sustainability concerns, and increasing competition within the global battery materials market.

Global Electrolytic Manganese Dioxide Market Value Chain & Supply Chain Evolution Current Scenario

The current electrolytic manganese dioxide market is being strongly influenced by rapid battery manufacturing expansion, accelerating EV adoption, increasing renewable energy investments, and global efforts to localize critical mineral supply chains. Battery manufacturers are increasingly seeking high-purity EMD materials capable of supporting advanced lithium-ion battery chemistries, high-performance alkaline batteries, and next-generation energy storage systems.

Asia-Pacific currently dominates the global EMD supply chain due to its extensive battery manufacturing infrastructure, integrated manganese processing capabilities, and large-scale electronics production ecosystem. China remains the leading producer and consumer of electrolytic manganese dioxide globally, supported by significant investments in EV battery production and critical mineral processing capacity.

North America and Europe are increasingly strengthening domestic battery material supply chains through government-backed critical mineral initiatives, battery gigafactory investments, and strategic partnerships between mining companies, battery manufacturers, and automotive OEMs. These regions are actively working to reduce dependence on imported battery materials while improving long-term supply chain resilience.

Manufacturers are investing heavily in advanced refining technologies, process automation systems, sustainable manganese extraction methods, and environmentally compliant production infrastructure. Simultaneously, battery companies are prioritizing long-term procurement agreements with EMD suppliers to ensure raw material security amid rising battery production volumes and increasing global competition for critical battery materials.

Growing demand for high-purity manganese materials, improved cathode performance, battery recycling technologies, and low-carbon battery production processes is accelerating innovation across the EMD value chain. Companies are also focusing on circular economy initiatives and battery material recovery systems to improve sustainability and reduce long-term raw material dependency.

Key Value Chain & Supply Chain Evolution Signals in Global Electrolytic Manganese Dioxide Market

One of the most significant transformation signals in the EMD market is the accelerating global shift toward electric mobility and renewable energy storage systems. The rapid expansion of EV production and battery gigafactory investments is substantially increasing demand for battery-grade manganese materials used in advanced cathode chemistries and energy storage applications.

Another important market signal is the increasing adoption of manganese-rich lithium-ion battery chemistries that improve battery safety, energy density, and cost efficiency. Battery manufacturers are actively exploring advanced manganese-based cathode technologies as an alternative to more expensive battery materials, creating long-term growth opportunities for high-purity EMD producers.

The localization of battery supply chains is also reshaping market dynamics. Governments across North America, Europe, and Asia-Pacific are prioritizing domestic battery material production, critical mineral security, and regional processing infrastructure to strengthen energy independence and reduce geopolitical supply chain vulnerabilities.

Another major trend is the growing emphasis on environmentally sustainable manganese processing technologies. Manufacturers are increasingly investing in low-emission refining systems, renewable energy-powered production facilities, wastewater treatment technologies, and sustainable mining practices to comply with stricter environmental regulations and ESG expectations.

The expansion of battery recycling and circular economy initiatives is also influencing the EMD value chain. Companies are exploring manganese recovery technologies and secondary raw material sourcing strategies to improve supply sustainability and reduce dependence on newly mined manganese resources.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Electrolytic Manganese Dioxide Market

Leading electrolytic manganese dioxide manufacturers are increasingly focusing on production capacity expansion, battery-grade purity enhancement, sustainable processing technologies, and strategic partnerships with battery manufacturers to strengthen market positioning. Competitive differentiation increasingly depends on product purity, supply reliability, cost efficiency, environmental compliance, and long-term battery industry integration.

Companies capable of producing high-purity EMD materials suitable for advanced lithium-ion battery applications are expected to capture significant growth opportunities as EV production accelerates globally. Investments in refining efficiency, automated production systems, and advanced quality control technologies are becoming critical for maintaining competitiveness in the evolving battery materials market.

Strategic collaborations between mining companies, cathode material suppliers, battery manufacturers, automotive OEMs, and energy storage providers are becoming increasingly important for ensuring supply security and long-term procurement stability. Vertical integration strategies are also expanding as companies seek greater control over raw material sourcing, refining, and downstream battery material production.

Environmental sustainability is emerging as a major competitive factor across the EMD value chain. Manufacturers adopting low-carbon production technologies, responsible mining practices, renewable energy integration, and battery recycling initiatives are expected to strengthen long-term market positioning as sustainability regulations become more stringent globally.

Geopolitical supply chain diversification is further encouraging investment in regional processing infrastructure and domestic battery material production. Companies with geographically diversified operations and localized supply networks are likely to gain strategic advantages in an increasingly competitive global battery ecosystem.

Global Electrolytic Manganese Dioxide Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the electrolytic manganese dioxide value chain is expected to become increasingly integrated, technologically advanced, sustainable, and strategically aligned with the global energy transition. Rising EV adoption, battery manufacturing expansion, renewable energy storage deployment, and electrification initiatives will continue driving strong long-term demand for high-purity manganese battery materials.

Advanced manganese processing technologies, AI-driven production optimization systems, automated quality monitoring platforms, and energy-efficient refining methods are expected to improve production efficiency and product consistency across the EMD industry. Manufacturers are likely to prioritize next-generation cathode material innovation and higher-purity EMD products designed for advanced battery chemistries.

Battery supply chain localization initiatives across North America, Europe, and Asia-Pacific will continue accelerating investment in domestic manganese refining infrastructure, battery material processing facilities, and regional battery ecosystems. Governments are expected to further strengthen critical mineral strategies to support energy security and industrial competitiveness.

Environmental sustainability will become increasingly central to the future EMD market. Companies are expected to invest heavily in carbon reduction technologies, renewable energy-powered processing systems, sustainable mining operations, closed-loop recycling infrastructure, and water-efficient refining technologies to align with evolving ESG standards and climate objectives.

Technological innovation in battery recycling, manganese recovery, and circular economy systems is expected to reshape raw material sourcing strategies over the long term. Recycled manganese materials may become an increasingly important secondary supply source for battery manufacturers and cathode producers.

Ultimately, the future electrolytic manganese dioxide value chain will evolve into a highly integrated global battery materials ecosystem focused on supply security, advanced material performance, sustainable processing, regional manufacturing resilience, and next-generation energy storage innovation.

Market-Specific Value Chain

- Manganese Mining & Raw Material Extraction: Manganese ore exploration, mining operations, ore processing, beneficiation technologies, raw material transportation, and mining infrastructure development.

- Refining & Electrolytic Processing: Manganese refining, electrolytic manganese dioxide production, purification technologies, chemical processing systems, energy-intensive refining operations, and industrial automation.

- Battery-Grade Material Manufacturing: High-purity EMD processing, cathode material preparation, material quality testing, particle engineering, specialty-grade manganese production, and performance optimization.

- Battery Manufacturing & Integration: Battery cell manufacturing, cathode integration, lithium-ion battery production, alkaline battery manufacturing, EV battery assembly, and industrial energy storage system development.

- Distribution & Industrial Applications: Global supply chain logistics, battery distribution networks, electronics manufacturing support, automotive battery supply, and renewable energy storage deployment.

- Recycling, Sustainability & Advanced Energy Ecosystems: Battery recycling technologies, manganese recovery systems, circular economy initiatives, ESG compliance management, sustainable sourcing strategies, and low-carbon battery ecosystems.

Company-to-Stage Mapping

- Manganese Mining & Raw Material Extraction: South32, ERAMET, Mesa Minerals Limited, OM Holdings Ltd., manganese mining operators.

- Refining & Electrolytic Processing: Tosoh Corporation, CITIC Dameng Holdings Ltd., Xiangtan Electrochemical Scientific Ltd., Tronox Holdings plc.

- Battery-Grade Material Manufacturing: Prince International Corporation, Cegasa International, specialty battery material suppliers, cathode material manufacturers.

- Battery Manufacturing & Integration: CATL, Panasonic, LG Energy Solution, Samsung SDI, BYD, EV battery manufacturers.

- Distribution & Industrial Applications: Consumer electronics companies, automotive OEMs, industrial battery suppliers, renewable energy storage integrators.

- Recycling, Sustainability & Advanced Energy Ecosystems: Battery recycling companies, sustainable mining firms, ESG-focused battery material suppliers, circular economy technology providers.

Investment Activity

Global Electrolytic Manganese Dioxide Market Investment & Funding Dynamics Overview

Investment activity in the global electrolytic manganese dioxide (EMD) market is accelerating due to rising battery demand, rapid electric vehicle (EV) adoption, expanding renewable energy storage infrastructure, and increasing focus on critical mineral supply chain localization. Between 2026 and 2033, funding is expected to increasingly target high-purity EMD production facilities, sustainable manganese refining technologies, advanced battery material innovation, and integrated cathode supply chain development.

The EMD market is evolving into a strategically important segment within the global battery materials and energy storage ecosystem. Governments, battery manufacturers, mining companies, and chemical producers are significantly increasing investments to secure long-term manganese supply and strengthen domestic battery manufacturing capabilities.

A major transformation influencing investment dynamics is the growing adoption of manganese-rich battery chemistries for EVs and grid-scale energy storage systems. Battery manufacturers are increasingly investing in advanced cathode materials that improve energy density, thermal stability, and cost efficiency while reducing dependency on more expensive battery metals.

The market is also benefiting from increasing investments in battery recycling technologies, sustainable mineral extraction processes, and low-carbon refining infrastructure. Growing geopolitical focus on critical mineral security and energy transition strategies is further accelerating capital inflows into the EMD value chain.

Current Investment & Funding Landscape

Current funding activity in the electrolytic manganese dioxide market is strongly supported by rapid expansion of EV battery gigafactories, increasing renewable energy storage deployment, and rising demand for advanced battery-grade manganese materials. Companies are actively investing in production capacity expansion, purification technologies, and strategic supply agreements with battery and automotive manufacturers.

- Asia-Pacific: Dominates global investment activity due to strong battery manufacturing ecosystems, large-scale EV production, and extensive manganese processing infrastructure across China, Japan, South Korea, and India.

- North America: Witnessing strong funding growth driven by battery supply chain localization initiatives, EV manufacturing expansion, and government support for critical mineral processing infrastructure.

- Europe: Attracting increasing investments due to aggressive EV adoption targets, battery manufacturing expansion, and sustainability-focused industrial policies.

- Latin America & Africa: Emerging as important investment regions due to manganese mining resources, industrial development initiatives, and growing participation in global battery material supply chains.

Key Investment & Funding Drivers

- Rapid expansion of electric vehicle production is increasing investments in battery-grade manganese supply chains.

- Growing deployment of renewable energy storage systems is supporting funding for large-scale battery material production infrastructure.

- Battery manufacturers are increasingly investing in manganese-rich cathode chemistries to improve cost efficiency and energy density.

- Government initiatives supporting critical mineral independence are accelerating investments in domestic manganese processing capabilities.

- Advancements in high-purity EMD refining technologies are attracting investments focused on improving electrochemical performance.

- Rising focus on sustainable mining and environmentally friendly refining processes is supporting green technology investments.

- Battery recycling and circular economy initiatives are creating additional investment opportunities in manganese recovery technologies.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of producing high-purity battery-grade EMD at large commercial scale.

- Vertical integration strategies between mining companies, refiners, and battery manufacturers are becoming increasingly important.

- Long-term supply agreements with EV manufacturers and battery producers are strengthening funding confidence across the industry.

- Technology leadership in refining efficiency, cathode optimization, and sustainable production is emerging as a major competitive differentiator.

- Regional diversification strategies are gaining importance as countries seek to reduce dependency on concentrated critical mineral supply chains.

- Companies investing in low-carbon processing technologies and renewable-energy-powered refining operations are expected to gain stronger market positioning.

- Strategic collaborations between chemical companies, mining firms, and battery developers are accelerating commercialization of advanced manganese battery materials.

Forward Investment Outlook

The global electrolytic manganese dioxide market is expected to maintain strong long-term investment momentum due to increasing global electrification, rapid battery manufacturing expansion, and rising demand for sustainable energy storage solutions.

Future funding activity is expected to prioritize high-purity EMD production facilities, next-generation lithium-ion battery materials, battery recycling technologies, and integrated critical mineral processing infrastructure.

- Asia-Pacific: Will remain the leading investment hub due to continued dominance in battery manufacturing and EV production capacity expansion.

- North America: Will strengthen its position through localized battery supply chain development and strategic mineral security initiatives.

- Europe: Will increasingly focus on sustainable battery ecosystems, green refining technologies, and low-carbon material sourcing.

Future innovation investments are also expected across AI-assisted mineral processing, advanced cathode chemistry optimization, carbon-neutral manganese refining, and closed-loop battery recycling systems.

The growing convergence of EV expansion, renewable energy adoption, and energy transition policies will continue reshaping the global investment landscape for electrolytic manganese dioxide.

Overall, the market is expected to remain highly attractive for long-term strategic investment as EMD becomes increasingly critical to global battery manufacturing and clean energy infrastructure development.

Technology & Innovation

Global Electrolytic Manganese Dioxide Market Technology & Innovation Landscape Overview

The global electrolytic manganese dioxide (EMD) market is undergoing significant technological transformation driven by advancements in battery chemistry, material purification technologies, sustainable mineral processing, and next-generation energy storage systems. Innovation across the market is focused on improving manganese purity, electrochemical performance, energy efficiency, and scalability of production processes to meet growing demand from electric vehicles, renewable energy storage, and consumer electronics industries.

Electrolytic manganese dioxide production technologies are evolving rapidly through improvements in electrolytic refining systems, automated process control, advanced leaching methods, and environmentally sustainable extraction techniques. These innovations are helping manufacturers produce high-purity battery-grade EMD with enhanced conductivity, stability, and energy density characteristics.

The market is also witnessing increased integration of AI-driven quality monitoring systems, digital process optimization platforms, and advanced cathode material engineering technologies aimed at improving battery efficiency and extending battery lifecycle performance.

Global Electrolytic Manganese Dioxide Market Technology & Innovation Current Scenario

Currently, the EMD industry is transitioning toward high-purity and energy-efficient manufacturing systems designed to support advanced lithium-ion battery chemistries and large-scale energy storage applications. Battery manufacturers are increasingly demanding ultra-high-purity manganese dioxide materials with tightly controlled particle size distribution and improved electrochemical consistency.

Advanced hydrometallurgical refining technologies are gaining traction as producers seek to improve extraction efficiency while minimizing environmental impact. Modern electrolytic processes are increasingly optimized to reduce energy consumption, wastewater generation, and chemical waste emissions.

Automation and digitalization are also becoming increasingly important across EMD production facilities. Smart monitoring systems equipped with real-time sensors and AI-based analytics are enabling better control of temperature, current density, pH levels, and impurity management during electrolytic processing.

In parallel, research institutions and battery companies are investing heavily in manganese-rich cathode technologies, including lithium manganese oxide (LMO) and nickel-manganese-cobalt (NMC) battery chemistries, to improve battery affordability, thermal stability, and energy density.

Sustainability-driven innovation is further accelerating development of low-carbon manganese refining technologies, battery recycling systems, and closed-loop material recovery processes.

Key Technology & Innovation Trends in Global Electrolytic Manganese Dioxide Market

- High-Purity EMD Production: Advanced refining and purification systems enabling ultra-high-purity battery-grade manganese dioxide manufacturing.

- AI-Driven Process Optimization: Machine learning systems improving electrolysis efficiency, impurity control, and production consistency.

- Advanced Hydrometallurgical Processing: Sustainable extraction technologies reducing waste generation and improving resource efficiency.

- Manganese-Rich Battery Chemistries: Increasing adoption of LMO and NMC cathode technologies in EV and energy storage batteries.

- Digital Quality Monitoring: Real-time analytics and automated inspection systems ensuring particle consistency and electrochemical performance.

- Battery Recycling Technologies: Recovery and reuse of manganese compounds from spent lithium-ion batteries and industrial waste streams.

- Low-Carbon Production Systems: Renewable energy integration and carbon reduction initiatives in EMD manufacturing facilities.

- Nanostructured Manganese Materials: Development of nano-engineered manganese dioxide materials with improved conductivity and battery performance.

- Automated Electrolytic Refining: Smart electrolytic systems improving operational efficiency and reducing human intervention.

- Sustainable Wastewater Treatment: Advanced water recycling and chemical recovery technologies supporting environmentally compliant production.

Strategic Implications of Technology & Innovation

Technological innovation is transforming the electrolytic manganese dioxide market from a traditional specialty chemicals industry into a strategically important component of the global battery materials ecosystem. Companies investing in high-purity production capabilities and advanced material engineering are gaining competitive advantages within rapidly expanding EV and renewable energy supply chains.

The increasing shift toward manganese-rich battery chemistries is strengthening long-term market demand while encouraging producers to enhance material consistency, scalability, and sustainability performance.

AI-enabled process optimization and digital manufacturing systems are significantly improving operational efficiency, reducing energy consumption, and minimizing production variability across EMD facilities. These technologies are becoming increasingly important as battery manufacturers demand tighter quality control standards.

At the same time, environmental sustainability is emerging as a major strategic priority. Producers adopting low-emission refining systems, wastewater recycling technologies, and circular economy models are strengthening their position within global battery supply chains increasingly influenced by ESG requirements.

However, challenges related to raw material price volatility, energy-intensive refining processes, and environmental compliance costs continue to influence long-term market competitiveness.

Global Electrolytic Manganese Dioxide Market Technology & Innovation Forward Outlook

Looking ahead, the global electrolytic manganese dioxide market is expected to become increasingly technology-intensive, sustainability-focused, and integrated with next-generation battery ecosystems. Future innovation will center on ultra-high-performance cathode materials, scalable green refining technologies, and AI-driven production automation.

The continued expansion of electric vehicle manufacturing and renewable energy storage infrastructure will accelerate research into advanced manganese battery chemistries with higher energy density, improved thermal stability, and lower production costs.

Battery recycling and circular material recovery technologies are expected to become increasingly important as governments and industries prioritize sustainable battery supply chains and critical mineral security.

Digital manufacturing ecosystems combining predictive analytics, automated quality control, and real-time process optimization will further improve operational efficiency and product consistency across EMD production facilities.

Overall, the technology and innovation landscape of the global electrolytic manganese dioxide market is evolving toward a highly specialized, environmentally sustainable, and strategically critical industry supporting the future of electrification, energy storage, and advanced battery technologies worldwide.

Market Risk

Global Electrolytic Manganese Dioxide Market Risk Factors & Disruption Threats Overview

The global electrolytic manganese dioxide (EMD) market is experiencing rapid expansion driven by growing battery demand, electric vehicle adoption, renewable energy storage deployment, and advancements in battery chemistry technologies. Despite favorable long-term growth prospects, the industry faces several critical risk factors including raw material supply volatility, environmental regulations, battery technology shifts, energy-intensive production processes, geopolitical disruptions, and increasing market competition.

One of the most significant disruption threats affecting the EMD market is the volatility in manganese ore supply and pricing. The production of electrolytic manganese dioxide depends heavily on stable access to high-grade manganese resources. Supply chain disruptions, mining restrictions, geopolitical instability, and export controls in major producing countries may create raw material shortages and cost fluctuations.

Environmental regulations and sustainability concerns also pose major challenges for EMD manufacturers. Traditional manganese extraction and electrolytic production processes are energy-intensive and may generate hazardous waste and carbon emissions. Governments worldwide are increasingly implementing stricter environmental compliance standards, emissions controls, and waste management regulations that could increase operational costs.

Rapid changes in battery chemistry technologies present another major market risk. While manganese-based battery chemistries remain widely used, the growing adoption of alternative cathode materials such as lithium iron phosphate (LFP), nickel-rich chemistries, and emerging solid-state battery technologies may alter long-term demand patterns for electrolytic manganese dioxide.

The market is also highly exposed to energy price volatility. EMD production requires substantial electricity consumption during the electrolytic refining process. Rising energy costs, grid instability, and power shortages may directly impact manufacturing profitability and production capacity.

Geopolitical tensions, trade restrictions, and supply chain localization initiatives are further reshaping the competitive landscape. Increasing resource nationalism and strategic control over critical battery minerals may disrupt global manganese supply chains and create regional market imbalances.

In addition, growing competition from low-cost regional producers, particularly in Asia-Pacific, may place pressure on pricing, profit margins, and long-term market consolidation.

Global Electrolytic Manganese Dioxide Market Risk Factors & Disruption Threats Current Scenario

The current EMD market environment is being strongly influenced by accelerating global battery manufacturing investments, EV production expansion, and renewable energy storage deployment. Demand for battery-grade manganese materials continues to rise, particularly across Asia-Pacific, North America, and Europe.

Battery manufacturers are increasingly prioritizing secure and localized supply chains for critical raw materials, including manganese compounds. Governments in several countries are promoting domestic battery material production to reduce dependency on foreign supply sources.

At the same time, the industry is witnessing growing pressure to improve sustainability across mining, refining, and battery material manufacturing operations. Companies are increasingly investing in cleaner extraction technologies, recycling initiatives, and renewable energy integration within production facilities.

The market is also facing rising competition from alternative battery chemistries that may reduce reliance on traditional manganese dioxide applications in certain segments. Continuous innovation in lithium-ion battery design is rapidly reshaping cathode material demand structures.

Additionally, manufacturers are experiencing rising operational costs associated with electricity consumption, environmental compliance, logistics disruptions, and advanced purification technologies required for high-purity battery-grade EMD production.

Global Electrolytic Manganese Dioxide Market Key Risk Factors & Disruption Threat Signals

- Raw Material Supply Volatility: Dependence on stable manganese ore availability and exposure to mining disruptions and export restrictions.

- Environmental Compliance Risks: Increasing regulations related to emissions, waste disposal, and sustainable mining operations.

- Battery Chemistry Shifts: Growing adoption of alternative cathode technologies potentially reducing long-term EMD demand.

- Energy Cost Inflation: High electricity consumption during electrolytic processing vulnerable to rising energy prices.

- Geopolitical & Trade Risks: Global trade tensions and resource nationalism impacting critical mineral supply chains.

- Technological Obsolescence: Rapid advancements in next-generation battery technologies creating competitive pressure.

- Supply Chain Disruptions: Logistics bottlenecks and transportation instability affecting global battery material distribution.

- Competitive Pricing Pressure: Rising competition from low-cost regional producers affecting profit margins.

- Sustainability & ESG Pressure: Increasing investor and regulatory focus on environmentally responsible production practices.

- Capital Investment Challenges: High infrastructure and purification technology costs required for battery-grade EMD production expansion.

Strategic Implications of Risk Factors

EMD manufacturers must prioritize supply chain diversification, sustainable mining partnerships, and regional production expansion strategies to reduce exposure to geopolitical and raw material risks.

Companies are increasingly expected to invest in energy-efficient electrolytic refining systems, renewable energy integration, and advanced purification technologies to improve operational efficiency and environmental compliance.

Strategic collaboration with battery manufacturers, EV companies, and energy storage providers will become increasingly important for securing long-term supply agreements and market stability.

Manufacturers should also accelerate investment in battery recycling technologies and circular economy initiatives to strengthen resource sustainability and reduce dependence on newly mined manganese.

Continuous R&D investment in high-purity manganese materials and next-generation battery compatibility will be essential for maintaining long-term competitiveness within evolving energy storage ecosystems.

Global Electrolytic Manganese Dioxide Market Forward Risk Outlook

Looking ahead to 2026???2033, the electrolytic manganese dioxide market is expected to remain strategically important within the global battery materials supply chain. However, market dynamics will increasingly depend on battery chemistry evolution, critical mineral supply stability, sustainability regulations, and geopolitical developments.

Future industry transformation will likely be shaped by growth in electric vehicles, renewable energy storage systems, and localized battery manufacturing ecosystems. These trends are expected to create substantial opportunities for high-purity EMD suppliers capable of meeting evolving quality and sustainability requirements.

At the same time, ongoing technological innovation in battery chemistries may alter manganese demand patterns across different applications. Companies unable to adapt to changing battery technology requirements may face long-term competitive risks.

Environmental sustainability, carbon reduction initiatives, and responsible mineral sourcing practices are expected to become increasingly important competitive differentiators within the industry.

Overall, while the global electrolytic manganese dioxide market offers strong long-term growth potential, future competitiveness will depend on technological adaptability, sustainable production capabilities, resilient supply chain management, and strategic alignment with the evolving global battery ecosystem.

Regulatory Landscape

Global Electrolytic Manganese Dioxide Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global electrolytic manganese dioxide (EMD) market is strongly influenced by battery material regulations, mining and mineral processing standards, environmental compliance requirements, and clean energy transition policies. As EMD is a critical component in battery manufacturing, especially for alkaline and lithium-ion batteries, the market is increasingly affected by regulations surrounding electric vehicles (EVs), energy storage systems, and critical mineral supply chains.

Governments worldwide are implementing stricter environmental standards for mining operations, chemical processing facilities, wastewater management, and industrial emissions associated with manganese extraction and EMD production. Regulatory agencies are also focusing on sustainable sourcing, worker safety, hazardous material handling, and battery recycling frameworks.

At the same time, the accelerating global transition toward electrification and renewable energy is creating strong policy support for battery material localization, critical mineral security, and domestic battery manufacturing ecosystems. These trends are significantly influencing investment flows and production strategies across the EMD industry.

Global Electrolytic Manganese Dioxide Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for electrolytic manganese dioxide is characterized by a combination of industrial chemical regulations, environmental protection laws, mining governance policies, and battery supply chain initiatives. EMD production facilities are subject to strict operational standards related to emissions control, hazardous waste management, and energy-intensive chemical processing.

In the United States, EMD production and manganese-related chemical operations are regulated under Environmental Protection Agency (EPA) standards, Occupational Safety and Health Administration (OSHA) regulations, and hazardous material transportation guidelines established by the Department of Transportation (DOT). Battery supply chain localization initiatives under clean energy and EV programs are also strengthening policy support for domestic battery material production.

In Europe, EMD manufacturers must comply with REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations, the EU Battery Regulation, industrial emissions standards, and circular economy directives. European governments are actively supporting battery recycling, sustainable mineral sourcing, and low-carbon battery manufacturing ecosystems.

Asia-Pacific dominates global EMD production and consumption, particularly China, which regulates the industry through industrial emissions laws, mining regulations, energy efficiency standards, and strategic battery industry policies. Japan and South Korea also maintain strict quality and environmental standards for battery-grade materials due to their advanced battery manufacturing sectors.

Latin America and Africa are increasingly strengthening mining governance frameworks and environmental oversight for manganese extraction activities, while also encouraging foreign investments in battery mineral processing infrastructure.

Key Regulatory & Policy Environment Signals in Global Electrolytic Manganese Dioxide Market

- Battery Supply Chain Localization Policies: Governments are promoting domestic battery material production to reduce dependence on foreign supply chains and strengthen energy security.

- Environmental Compliance Standards: EMD production facilities are subject to strict regulations related to emissions control, wastewater treatment, and industrial waste management.

- Critical Mineral and Mining Regulations: Manganese extraction and processing activities are increasingly regulated under responsible mining and sustainable sourcing frameworks.

- Battery Recycling and Circular Economy Policies: Governments are implementing regulations encouraging recycling of battery materials and recovery of critical minerals.

- Electric Vehicle and Clean Energy Incentives: EV adoption policies and renewable energy investments are indirectly accelerating demand for battery-grade EMD materials.

- Worker Safety and Hazardous Material Handling Standards: Strict industrial safety regulations govern handling, transportation, and storage of manganese compounds and chemical processing materials.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is significantly reshaping operational strategies and investment priorities across the electrolytic manganese dioxide market. Manufacturers are increasingly investing in environmentally sustainable refining technologies, wastewater recycling systems, and energy-efficient production facilities to comply with tightening environmental regulations.

Battery supply chain localization initiatives in North America and Europe are creating new opportunities for regional EMD production capacity expansion and strategic partnerships with battery manufacturers and EV companies.

Stricter sustainability regulations and responsible sourcing requirements are encouraging companies to improve traceability, reduce carbon intensity, and align with ESG (Environmental, Social, and Governance) standards across the battery materials value chain.

The expansion of battery recycling policies is also expected to influence long-term raw material procurement strategies by increasing the availability of recycled manganese materials within circular battery ecosystems.

Additionally, regulatory incentives supporting clean energy technologies and EV manufacturing are improving long-term demand visibility for high-purity battery-grade EMD products globally.

Global Electrolytic Manganese Dioxide Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global electrolytic manganese dioxide market is expected to become increasingly sustainability-focused, supply-chain-oriented, and strategically aligned with global energy transition goals.

Governments are likely to introduce stricter environmental regulations for mineral extraction, chemical refining, and industrial emissions while simultaneously expanding incentives for localized battery material manufacturing and low-carbon production technologies.

Battery recycling mandates, carbon reduction targets, and responsible sourcing frameworks are expected to become more influential in shaping market competitiveness and supplier qualification requirements.

The continued expansion of EV manufacturing, renewable energy storage systems, and critical mineral security initiatives will further strengthen policy support for high-purity manganese-based battery materials.

Technological advancements in sustainable mining, green chemical processing, and closed-loop battery recycling systems are also expected to play a growing role in future regulatory frameworks.

Overall, the regulatory and policy environment will remain a major strategic driver for the electrolytic manganese dioxide market, with companies investing in sustainable production processes, advanced purification technologies, and compliance-ready supply chains expected to maintain strong long-term competitive advantages.