Global Surfactant Market Size and Share Analysis 2026-2033

Global Surfactant Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 48.7 Billion |

| Market Size (2033) | USD 72.9 Billion |

| CAGR (2026???2033) | 5.2% |

| Largest Type Segment | Anionic Surfactants |

| Fastest Growing Type Segment | Bio-based Surfactants |

| Largest Source Segment | Synthetic Surfactants |

| Fastest Growing Source Segment | Bio-based Surfactants |

| Largest Application Segment | Household Detergents |

| Fastest Growing Application Segment | Personal Care Products |

| Leading End User Segment | Consumer Goods Manufacturers |

| Dominant Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

| Key Growth Driver | Increasing Demand for Household Cleaning and Personal Care Products |

| Emerging Opportunity | Development of Sustainable and Bio-based Surfactant Technologies |

Global Surfactant Market Size & Forecast

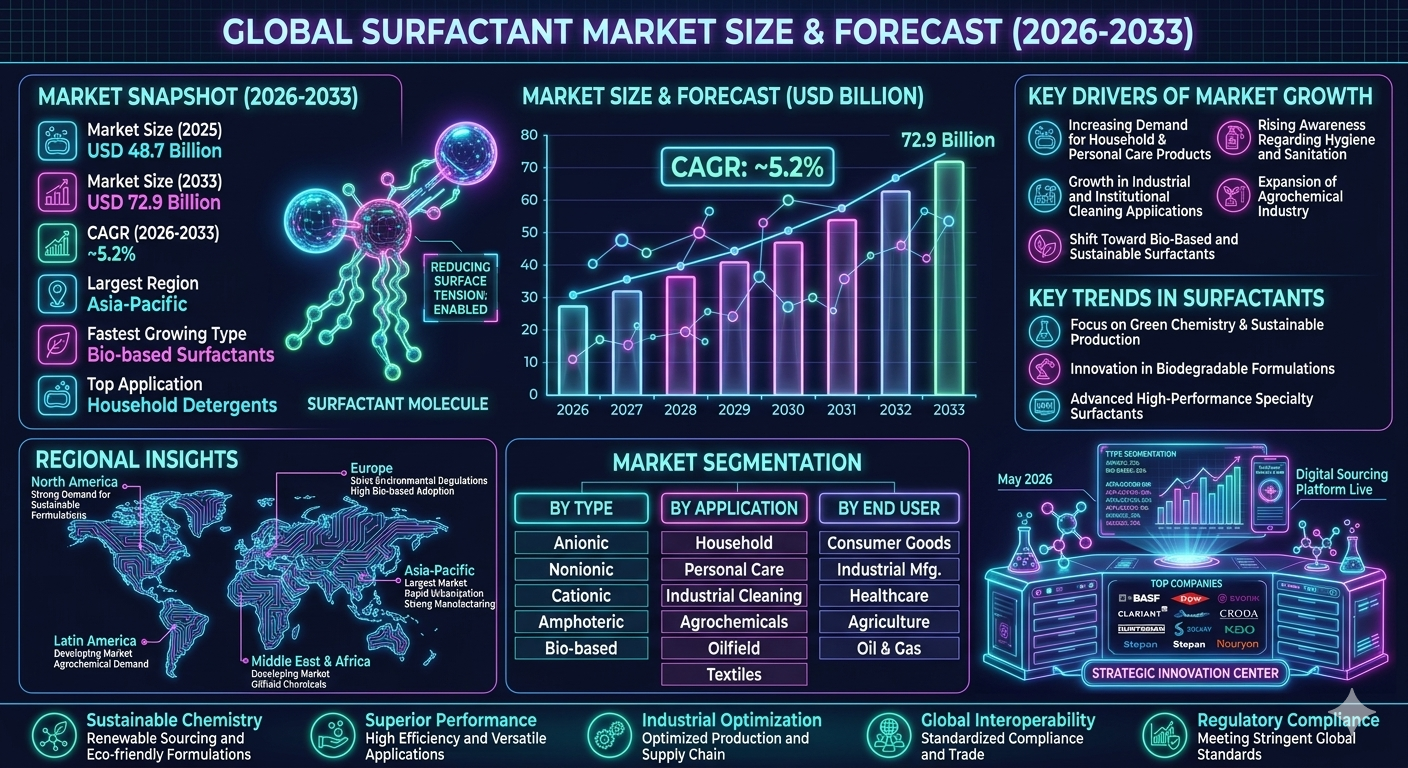

The global surfactant market is projected to witness strong and consistent growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 48.7 billion in 2025 and is expected to reach nearly USD 72.9 billion by 2033, expanding at a CAGR of around 5.2%. This growth is driven by rising demand from household detergents, personal care products, industrial cleaning applications, agrochemicals, oilfield chemicals, and expanding industrial manufacturing activities worldwide. Surfactants, also known as surface-active agents, are chemical compounds that reduce surface tension between liquids, solids, and gases. They are widely used in cleaning products, emulsifiers, wetting agents, foaming agents, dispersants, and detergents across numerous industrial and consumer applications. The market is benefiting from increasing consumption of personal hygiene products, growing urbanization, rising awareness regarding sanitation and cleanliness, and strong demand for high-performance industrial cleaning solutions. Technological advancements in bio-based and environmentally friendly surfactants are also reshaping the industry landscape. Additionally, rising demand for sustainable and biodegradable chemicals is encouraging manufacturers to invest in green surfactant technologies and renewable raw material sourcing strategies.

Global Surfactant Market Overview

The surfactant market forms a critical segment of the global specialty chemicals industry. Surfactants are extensively utilized in household detergents, shampoos, soaps, cosmetics, pharmaceuticals, food processing, agriculture, paints & coatings, textile processing, and enhanced oil recovery operations. The market includes synthetic surfactants and bio-based surfactants, with synthetic variants currently dominating due to large-scale industrial applications and cost efficiency. However, bio-based surfactants are gaining rapid traction due to increasing environmental regulations and consumer preference for sustainable products. Major industry participants include BASF SE, Dow Inc., Evonik Industries, Clariant AG, Croda International, Huntsman Corporation, Solvay, Kao Corporation, and Stepan Company. The industry is highly competitive and innovation-driven, with companies focusing on product performance, sustainability, regulatory compliance, and raw material optimization.Key Drivers of Global Surfactant Market Growth

Increasing Demand for Household and Personal Care Products

Growing consumption of detergents, shampoos, soaps, skincare products, and household cleaners is significantly driving surfactant demand globally.Rising Awareness Regarding Hygiene and Sanitation

Consumers and industries are increasingly prioritizing hygiene and cleaning standards, particularly in healthcare, hospitality, and residential sectors.Growth in Industrial and Institutional Cleaning Applications

Industrial manufacturing facilities, food processing plants, and commercial institutions are increasingly using advanced surfactant-based cleaning solutions.Expansion of Agrochemical Industry

Surfactants are widely used in pesticides, herbicides, and agricultural formulations to improve dispersion and effectiveness.Shift Toward Bio-Based and Sustainable Surfactants

Environmental concerns and regulatory pressures are accelerating demand for biodegradable and renewable surfactant formulations.Global Surfactant Market Segmentation

By Type

The market is segmented into anionic surfactants, nonionic surfactants, cationic surfactants, amphoteric surfactants, and bio-based surfactants. Anionic surfactants account for the largest market share due to extensive use in detergents and cleaning products.By Source

The market includes synthetic surfactants and bio-based surfactants. Synthetic surfactants dominate currently, while bio-based variants are witnessing rapid growth.By Application

Applications include household detergents, personal care products, industrial cleaning, agrochemicals, oilfield chemicals, textiles, paints & coatings, pharmaceuticals, and food processing.By End User

End users include consumer goods manufacturers, industrial manufacturers, healthcare companies, agriculture sector participants, and oil & gas companies.By Distribution Channel

The market includes direct sales, distributors, specialty chemical suppliers, and online industrial procurement platforms.Regional Market Dynamics

Asia-Pacific dominates the global surfactant market due to strong industrial manufacturing, rising consumer goods demand, and rapid urbanization in China, India, Japan, and Southeast Asia. North America represents a significant market driven by strong demand for personal care products, industrial cleaning chemicals, and sustainable surfactant formulations. Europe is witnessing steady growth due to stringent environmental regulations and increasing adoption of bio-based surfactants. Latin America is gradually expanding with rising demand for household cleaning products and agricultural chemicals. Middle East & Africa is emerging as a developing market supported by industrial growth, oilfield chemical demand, and expanding consumer goods industries.Competitive Landscape

The global surfactant market is highly competitive and fragmented, with the presence of multinational chemical manufacturers and regional specialty chemical producers. Key players include BASF SE, Dow Inc., Evonik Industries, Clariant AG, Croda International, Huntsman Corporation, Solvay, Kao Corporation, Stepan Company, and Nouryon. Companies are increasingly focusing on sustainable surfactant development, bio-based feedstocks, and high-performance specialty formulations to strengthen competitiveness. Strategic acquisitions, partnerships, and investments in green chemistry technologies are becoming increasingly common as companies seek to expand market share and comply with evolving environmental regulations.Strategic Outlook

The strategic outlook for the surfactant market remains highly positive due to expanding applications across consumer goods, industrial manufacturing, agriculture, and energy sectors. Future growth opportunities lie in bio-based surfactants, low-toxicity formulations, specialty industrial surfactants, and advanced emulsification technologies. Manufacturers are expected to continue investing in sustainable chemistry, renewable raw materials, and high-efficiency production processes to align with global environmental standards.Final Market Perspective

The global surfactant market remains a vital component of the specialty chemicals industry, supporting essential applications across cleaning, personal care, agriculture, healthcare, and industrial manufacturing sectors. As consumer preferences shift toward sustainability and industries increasingly prioritize environmental compliance, demand for innovative and eco-friendly surfactant solutions will continue to rise. Companies that combine technological innovation, product performance, and sustainability strategies will remain strongly positioned in the evolving global surfactant market.Table of Contents

- 1. Executive Summary

- 1.1 Global Surfactant Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Surfactants

- 2.2 Scope of the Study

- 2.3 Evolution of the Specialty Chemicals Industry

- 2.4 Surfactant Value Chain & Supply Infrastructure

- 2.5 Raw Materials & Feedstock Landscape

- 2.6 Sustainability & Regulatory Environment

- 2.7 Technology & Formulation Innovation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Demand for Household Cleaning Products

- 4.1.2 Increasing Consumption of Personal Care Products

- 4.1.3 Expansion of Industrial & Institutional Cleaning Applications

- 4.1.4 Growing Demand from Agrochemical Industry

- 4.1.5 Rising Focus on Hygiene & Sanitation Standards

- 4.2 Restraints

- 4.2.1 Volatility in Petrochemical Raw Material Prices

- 4.2.2 Stringent Environmental Regulations

- 4.2.3 Toxicity Concerns Related to Synthetic Surfactants

- 4.2.4 High Production Costs for Bio-Based Surfactants

- 4.3 Opportunities

- 4.3.1 Expansion of Bio-Based & Biodegradable Surfactants

- 4.3.2 Growth in Green Chemistry Technologies

- 4.3.3 Emerging Market Industrialization

- 4.3.4 Specialty Surfactants for Advanced Industrial Applications

- 4.4 Challenges

- 4.4.1 Supply Chain Disruptions in Chemical Feedstocks

- 4.4.2 Regulatory Compliance Across Global Markets

- 4.4.3 Competitive Pricing Pressures

- 4.4.4 Sustainability Transition Challenges

- 4.1 Drivers

- 5. Global Surfactant Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Raw Material Utilization Trends

- 5.6 Production Capacity & Consumption Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Type

- 6.1.1 Anionic Surfactants

- 6.1.1.1 Household Detergent Applications

- 6.1.1.1.1 Laundry Cleaning Solutions

- 6.1.1.1.1.1 High-Foaming Detergent Formulations

- 6.1.1.1.1 Laundry Cleaning Solutions

- 6.1.1.1 Household Detergent Applications

- 6.1.2 Nonionic Surfactants

- 6.1.2.1 Personal Care & Cosmetics

- 6.1.2.1.1 Skin & Hair Care Products

- 6.1.2.1.1.1 Mild Cleansing Formulations

- 6.1.2.1.1 Skin & Hair Care Products

- 6.1.2.1 Personal Care & Cosmetics

- 6.1.3 Cationic Surfactants

- 6.1.3.1 Fabric Softeners & Disinfectants

- 6.1.3.1.1 Industrial Cleaning Applications

- 6.1.3.1.1.1 Antimicrobial Surface Cleaning Solutions

- 6.1.3.1.1 Industrial Cleaning Applications

- 6.1.3.1 Fabric Softeners & Disinfectants

- 6.1.4 Amphoteric Surfactants

- 6.1.4.1 Personal Care Products

- 6.1.4.2 Specialty Industrial Formulations

- 6.1.5 Bio-Based Surfactants

- 6.1.1 Anionic Surfactants

- 6.2 By Source

- 6.2.1 Synthetic Surfactants

- 6.2.2 Bio-Based Surfactants

- 6.3 By Application

- 6.3.1 Household Detergents

- 6.3.2 Personal Care Products

- 6.3.3 Industrial & Institutional Cleaning

- 6.3.4 Agrochemicals

- 6.3.5 Oilfield Chemicals

- 6.3.6 Paints & Coatings

- 6.3.7 Pharmaceuticals

- 6.3.8 Food Processing

- 6.4 By End User

- 6.4.1 Consumer Goods Manufacturers

- 6.4.2 Industrial Manufacturers

- 6.4.3 Healthcare Companies

- 6.4.4 Agriculture Sector

- 6.4.5 Oil & Gas Industry

- 6.5 By Distribution Channel

- 6.5.1 Direct Sales

- 6.5.2 Chemical Distributors

- 6.5.3 Specialty Chemical Suppliers

- 6.5.4 Online Industrial Procurement Platforms

- 6.1 By Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Sustainability & Bio-Based Innovation Analysis

- 8.4 Strategic Partnerships & Acquisitions

- 8.5 Manufacturing Capacity & Expansion Strategies

- 9. Company Profiles

- 9.1 BASF SE

- 9.2 Dow Inc.

- 9.3 Evonik Industries

- 9.4 Clariant AG

- 9.5 Croda International

- 9.6 Huntsman Corporation

- 9.7 Solvay

- 9.8 Kao Corporation

- 9.9 Stepan Company

- 9.10 Nouryon

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Raw Material Price & Feedstock Analyzer

- 10.3 Sustainable Surfactant Innovation Tracker

- 10.4 Industrial Application Trend Monitoring System

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Bio-Based Surfactant Production

- 11.2 Investment in Green Chemistry Technologies

- 11.3 Advanced Specialty Surfactant Development

- 11.4 Sustainable Supply Chain Optimization

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Surfactant Market Competitive Intensity & Market Structure Overview

The Global Surfactant Market is highly competitive and innovation-driven, characterized by the presence of multinational chemical manufacturers, specialty ingredient suppliers, regional producers, and emerging bio-based surfactant companies. Market competition is primarily influenced by product performance, pricing strategies, sustainability initiatives, raw material availability, and regulatory compliance across multiple end-use industries.

Competitive intensity remains strong due to the extensive application range of surfactants in household detergents, personal care products, industrial cleaning, agrochemicals, oilfield chemicals, textiles, paints & coatings, and pharmaceuticals. Companies are continuously focusing on improving formulation efficiency, environmental compatibility, and cost optimization to strengthen market positioning.

The market structure is moderately fragmented, with large global chemical corporations dominating high-volume production while regional and niche manufacturers focus on customized formulations and specialty surfactant applications. Integrated supply chain capabilities, manufacturing scale, and access to raw materials remain major competitive advantages within the industry.

Global Surfactant Market Competitive Intensity & Market Structure Current Scenario

Leading Surfactant Manufacturers & Specialty Chemical Companies

BASF SE: One of the global leaders in surfactants and specialty chemicals, offering extensive product portfolios for household, industrial, and personal care applications with strong focus on sustainable chemistry solutions.

Dow Inc.: Major player in industrial and consumer surfactants with advanced formulation technologies and strong global manufacturing presence.

Evonik Industries: Focused on specialty surfactants and high-performance additives for personal care, industrial cleaning, and agricultural applications.

Clariant AG: Known for specialty and bio-based surfactant innovations targeting sustainable consumer and industrial markets.

Croda International: Strong presence in premium personal care and cosmetic surfactants with emphasis on renewable and environmentally friendly ingredients.

Huntsman Corporation: Active in industrial surfactants, performance chemicals, and specialty formulations for cleaning and manufacturing sectors.

Solvay: Major supplier of specialty surfactants and advanced chemical solutions for industrial, consumer, and energy applications.

Kao Corporation: Significant player in household and personal care surfactants with strong integration into consumer product manufacturing.

Stepan Company: Specialized surfactant manufacturer with strong product offerings across detergents, agriculture, and industrial cleaning applications.

Nouryon: Expanding its specialty surfactant portfolio through sustainable chemistry initiatives and advanced industrial formulations.

Key Competitive Intensity & Market Structure Signals in Global Surfactant Market

One of the most significant competitive signals in the market is the accelerating shift toward bio-based and biodegradable surfactants. Regulatory pressure regarding environmental sustainability and rising consumer preference for eco-friendly products are forcing manufacturers to invest heavily in renewable feedstocks and green chemistry technologies.

Another major competitive factor is raw material integration and feedstock optimization. Companies with strong access to petrochemical feedstocks, oleochemicals, and renewable raw materials are gaining cost advantages and improving supply chain resilience amid raw material price volatility.

Innovation in specialty surfactant formulations is becoming increasingly important, particularly for premium personal care products, industrial cleaning systems, pharmaceutical formulations, and agrochemical applications. High-performance multifunctional surfactants are enabling manufacturers to differentiate their product offerings in mature market segments.

The market is also witnessing rising competition in low-toxicity and regulatory-compliant formulations. Companies operating in Europe and North America are increasingly focusing on REACH compliance, low-VOC formulations, and safer chemical alternatives to strengthen regulatory positioning and customer trust.

Digitalization and process optimization are further reshaping market competition. Advanced manufacturing technologies, AI-driven process monitoring, and automated production systems are helping companies improve operational efficiency, reduce waste generation, and optimize product quality consistency.

Strategic Implications of Competitive Intensity & Market Structure in Global Surfactant Market

Large multinational chemical companies continue to strengthen competitive positioning through vertical integration strategies involving feedstock sourcing, surfactant production, downstream formulation capabilities, and global distribution networks. This integration improves operational efficiency and reduces supply chain risks.

Strategic acquisitions and partnerships are increasingly shaping the market structure, particularly in the bio-based surfactant segment where established chemical companies are acquiring sustainable chemistry startups and specialty ingredient manufacturers to accelerate product innovation.

Product differentiation is becoming a key strategic priority as competition intensifies across mature detergent and cleaning product categories. Manufacturers are increasingly focusing on premium specialty surfactants with enhanced foaming, emulsification, dispersing, and wetting properties.

Regional manufacturing expansion remains a major strategic trend, especially in Asia-Pacific where rising industrialization, urbanization, and consumer goods production continue to drive large-scale surfactant demand growth. Companies are expanding local production capacities to improve cost competitiveness and regional supply capabilities.

Sustainability has become a core strategic requirement across the surfactant industry. Companies are prioritizing carbon reduction initiatives, renewable feedstock utilization, water-efficient manufacturing systems, and biodegradable formulations to align with global environmental standards and evolving customer expectations.

Global Surfactant Market Competitive Intensity & Market Structure Forward Outlook

The Global Surfactant Market is expected to become increasingly sustainability-focused and technology-driven over the forecast period. Competitive dynamics will continue shifting toward bio-based chemistry, advanced specialty formulations, and environmentally responsible production systems.

Bio-based surfactants are expected to witness rapid expansion as consumer goods manufacturers, personal care brands, and industrial users increasingly prioritize sustainable ingredients and green supply chains. This transition will create new competitive opportunities for companies specializing in renewable chemical technologies.

Technological advancements in surfactant synthesis, formulation science, and process engineering will further intensify competition, particularly in high-value applications such as pharmaceuticals, advanced industrial cleaning, enhanced oil recovery, and premium cosmetics.

Asia-Pacific will remain the dominant production and consumption region due to strong industrial manufacturing activity, expanding consumer goods industries, and rising demand for cleaning and hygiene products. Meanwhile, North America and Europe will continue leading innovation in sustainable and specialty surfactant technologies.

Overall, the surfactant market is expected to maintain strong long-term growth supported by expanding applications across consumer, industrial, healthcare, and agricultural sectors. Companies that successfully combine large-scale manufacturing capabilities, sustainable innovation, advanced specialty formulations, and efficient supply chain management will remain strongly positioned in the Global Surfactant Market through 2033.

Value Chain

Global Surfactant Market Value Chain & Supply Chain Evolution Overview

The Global Surfactant Market value chain is undergoing significant transformation as manufacturers increasingly shift toward sustainable chemical production, bio-based feedstocks, advanced formulation technologies, and integrated specialty chemical ecosystems. The evolution of the market is being driven by rising global demand for household cleaning products, personal care formulations, industrial detergents, agrochemicals, oilfield chemicals, and high-performance specialty surfactants used across multiple industrial sectors. Growing environmental concerns, stricter chemical regulations, and increasing consumer preference for biodegradable products are accelerating innovation across the surfactant industry and reshaping global supply chain strategies.

Surfactants play a critical role in reducing surface tension and enabling emulsification, foaming, wetting, dispersing, and cleaning functions in a wide range of products. As demand expands across consumer goods, industrial manufacturing, healthcare, agriculture, and energy industries, the value chain has evolved from traditional bulk chemical manufacturing into a more specialized, performance-driven, and sustainability-focused ecosystem. Manufacturers are increasingly investing in renewable raw materials, green chemistry technologies, and advanced formulation science to improve product efficiency while reducing environmental impact.

The upstream segment of the surfactant supply chain relies heavily on petrochemical derivatives, oleochemicals, natural oils, fatty alcohols, ethylene oxide, and other specialty chemical intermediates used in surfactant synthesis. Global suppliers of crude oil derivatives, palm oil, coconut oil, and renewable feedstocks play a critical role in determining production costs, supply stability, and sustainability performance. At the same time, rising volatility in raw material prices and growing pressure to reduce carbon emissions are encouraging companies to diversify sourcing strategies and strengthen local supply resilience.

Midstream operations involve surfactant synthesis, blending, formulation development, quality testing, packaging, and specialty customization for different industrial and consumer applications. Major chemical manufacturers such as BASF SE, Dow Inc., Evonik Industries, Clariant AG, Croda International, Huntsman Corporation, Solvay, Kao Corporation, and Stepan Company are continuously expanding production capabilities and investing in research and development to create high-performance and environmentally friendly surfactant solutions. These companies increasingly focus on specialty formulations designed for low toxicity, high biodegradability, improved foaming characteristics, and compatibility with evolving regulatory standards.

The downstream segment includes distribution networks, industrial chemical suppliers, FMCG manufacturers, personal care brands, industrial cleaning companies, agrochemical producers, pharmaceutical firms, textile processors, and oilfield service providers. Distribution structures are highly globalized and involve direct B2B contracts, specialty chemical distributors, formulation partners, and regional supply networks serving multiple industries simultaneously. The increasing complexity of global supply chains, environmental compliance standards, and sustainability reporting requirements is encouraging companies to adopt digital supply chain monitoring systems and integrated procurement strategies.

Despite strong market growth, the surfactant industry continues to face challenges related to fluctuating feedstock prices, environmental regulations, supply chain disruptions, waste management concerns, and increasing pressure to reduce dependence on petroleum-derived chemicals. In addition, geopolitical instability, transportation constraints, and sustainability certification requirements are influencing sourcing decisions and operational strategies across the global surfactant ecosystem.

Global Surfactant Market Value Chain & Supply Chain Evolution Current Scenario

The current surfactant market ecosystem is characterized by increasing investment in bio-based surfactant production, expansion of specialty chemical manufacturing facilities, and rising integration of sustainability initiatives into product development strategies. Chemical manufacturers are actively developing renewable surfactants derived from plant-based oils, sugar-based feedstocks, and biodegradable raw materials to align with tightening environmental regulations and changing consumer preferences.

Household detergents and personal care applications continue to dominate global surfactant demand, supported by rising urbanization, increasing hygiene awareness, and growing consumption of cleaning and cosmetic products worldwide. Industrial cleaning applications are also expanding rapidly as manufacturing companies, food processing facilities, healthcare institutions, and commercial establishments increasingly prioritize sanitation and operational cleanliness standards.

Agrochemical and oilfield applications remain significant contributors to market demand due to the role of surfactants in improving pesticide effectiveness, drilling fluid performance, and enhanced oil recovery operations. At the same time, pharmaceutical and healthcare industries are increasingly using specialized surfactants in drug formulations, emulsification systems, and medical cleaning products.

Manufacturers are also increasingly adopting digital manufacturing systems, process automation technologies, and AI-driven formulation optimization tools to improve operational efficiency, reduce waste generation, and accelerate product development cycles. Sustainability certifications, traceability systems, and responsible sourcing practices are becoming more important across procurement and production operations as customers demand greater transparency regarding environmental impact and raw material origins.

However, the current market environment remains highly sensitive to fluctuations in petrochemical feedstock prices, supply disruptions in natural oil markets, transportation costs, and changing environmental regulations. Manufacturers are therefore investing heavily in supply diversification, regional production expansion, and circular economy initiatives to strengthen long-term operational resilience.

Key Value Chain & Supply Chain Evolution Signals in Global Surfactant Market

One of the strongest transformation signals in the surfactant market is the rapid transition toward bio-based and biodegradable surfactant formulations. Regulatory pressure to reduce environmental toxicity and growing consumer demand for sustainable household and personal care products are encouraging chemical manufacturers to accelerate investments in renewable feedstocks and green chemistry technologies.

Another important market signal is the increasing integration of digital technologies into chemical manufacturing and supply chain management. Advanced analytics, AI-powered formulation systems, digital inventory management, and predictive maintenance technologies are helping companies optimize production efficiency, reduce operational downtime, and improve product consistency across global manufacturing facilities.

The growing emphasis on specialty surfactants designed for high-performance industrial applications is also reshaping the market landscape. Industries such as healthcare, electronics manufacturing, advanced coatings, pharmaceuticals, and oil & gas are demanding more customized surfactant solutions with enhanced chemical stability, low toxicity, and improved environmental compatibility.

Sustainability reporting and traceability systems are becoming increasingly important across the supply chain as global brands seek to meet ESG commitments and comply with evolving chemical safety regulations. Manufacturers are therefore implementing responsible sourcing programs, lifecycle analysis systems, and carbon reduction strategies to improve environmental performance throughout the surfactant value chain.

In addition, strategic partnerships between surfactant producers, FMCG companies, agricultural chemical firms, and industrial manufacturers are increasing as companies seek long-term supply security, product innovation collaboration, and integrated sustainability initiatives. These collaborations are supporting faster commercialization of next-generation surfactant technologies and strengthening supply chain resilience globally.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Surfactant Market

Leading surfactant manufacturers such as BASF SE, Dow Inc., Evonik Industries, Clariant AG, Croda International, Huntsman Corporation, Solvay, Kao Corporation, Stepan Company, and Nouryon are strengthening market competitiveness through sustainability-focused product innovation, capacity expansion, and advanced specialty chemical development. Competitive differentiation increasingly depends on environmental performance, feedstock diversification, formulation expertise, production efficiency, and the ability to meet evolving global regulatory standards.

Companies capable of combining large-scale manufacturing capabilities with renewable feedstock integration and specialty formulation expertise are expected to maintain stronger long-term market positioning. There is also growing emphasis on localized production strategies aimed at reducing transportation costs, minimizing supply disruptions, and improving responsiveness to regional market demand.

Strategic investments in bio-refineries, renewable chemical technologies, and low-emission production systems are becoming critical for long-term growth as sustainability requirements continue to intensify across global industries. Chemical companies are increasingly prioritizing circular economy initiatives, waste reduction programs, and energy-efficient manufacturing systems to strengthen operational sustainability and improve ESG performance.

At the same time, partnerships with FMCG companies, personal care brands, industrial cleaning firms, and agricultural chemical producers are becoming increasingly important for accelerating product development and securing long-term supply agreements. These collaborations support co-development of customized surfactant formulations optimized for specific end-use applications and evolving consumer requirements.

Manufacturers are also investing in digital procurement systems, real-time supply chain monitoring, and predictive demand forecasting tools to improve operational agility and reduce the impact of raw material volatility. As supply chains become increasingly globalized and interconnected, companies with strong sourcing flexibility and integrated logistics capabilities are expected to gain competitive advantages.

Global Surfactant Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the surfactant market value chain is expected to become increasingly sustainable, technology-driven, and performance-oriented as industries accelerate the transition toward environmentally responsible specialty chemicals. Bio-based surfactants are expected to gain substantial market share due to rising regulatory restrictions on conventional petrochemical-based surfactants and increasing consumer demand for eco-friendly cleaning and personal care products.

Advanced manufacturing technologies including AI-assisted chemical formulation, automated process control systems, digital twin production models, and predictive analytics are expected to improve production efficiency and accelerate innovation across surfactant manufacturing operations. Companies will increasingly adopt intelligent manufacturing systems capable of optimizing raw material usage, reducing waste generation, and lowering energy consumption.

Renewable feedstocks derived from plant oils, biomass, sugar-based materials, and waste recycling systems are expected to play a much larger role in future surfactant production strategies. Chemical manufacturers will continue investing in sustainable sourcing partnerships and bio-refinery infrastructure to secure long-term access to renewable raw materials and reduce exposure to petrochemical price volatility.

Specialty surfactants designed for pharmaceutical, healthcare, industrial automation, advanced coatings, electronics manufacturing, and agricultural applications are expected to represent major growth opportunities over the forecast period. Demand for highly customized formulations with enhanced performance characteristics, regulatory compliance, and sustainability attributes will continue to expand across industrial sectors.

Ultimately, the future surfactant value chain will evolve into a highly integrated global specialty chemical ecosystem combining renewable chemistry, digital manufacturing, intelligent supply chain systems, advanced formulation science, and sustainability-driven innovation. Companies capable of balancing performance, scalability, regulatory compliance, and environmental responsibility will remain strongly positioned in the evolving global surfactant market.

Market-Specific Value Chain

- Raw Material & Feedstock Supply: Petrochemical derivatives, oleochemicals, fatty alcohols, ethylene oxide, palm oil, coconut oil, renewable plant-based feedstocks, and specialty chemical intermediates.

- Surfactant Manufacturing & Chemical Processing: Chemical synthesis, surfactant blending, formulation development, specialty chemical processing, quality testing, and industrial-scale production operations.

- Specialty Formulation & Product Customization: Performance optimization, biodegradable formulation development, industrial customization, personal care formulations, and high-performance specialty surfactant engineering.

- Distribution & Industrial Supply Networks: Chemical distributors, bulk industrial supply channels, regional specialty chemical suppliers, B2B procurement systems, and global logistics operations.

- End-Use Industry Integration: Household detergents, personal care products, industrial cleaning, agrochemicals, pharmaceuticals, oilfield chemicals, textiles, paints & coatings, and food processing applications.

- Sustainability & Regulatory Compliance Systems: ESG reporting, environmental certification, waste management, biodegradable chemistry initiatives, and sustainable sourcing programs.

Company-to-Stage Mapping

- Raw Material & Feedstock Supply: Wilmar International, Cargill, IOI Corporation, petrochemical feedstock suppliers, renewable oil producers.

- Surfactant Manufacturing & Chemical Processing: BASF SE, Dow Inc., Evonik Industries, Huntsman Corporation, Solvay, Stepan Company.

- Specialty Formulation & Product Customization: Croda International, Clariant AG, Kao Corporation, Nouryon, specialty formulation developers.

- Distribution & Industrial Supply Networks: Brenntag, Univar Solutions, regional chemical distributors, industrial procurement providers.

- End-Use Industry Integration: Unilever, Procter & Gamble, Henkel, Colgate-Palmolive, agrochemical manufacturers, industrial cleaning product companies.

- Sustainability & Regulatory Compliance Systems: Global ESG compliance organizations, sustainable chemistry certification agencies, environmental monitoring firms.

Investment Activity

Global Surfactant Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Surfactant Market are being significantly influenced by rising global demand for household cleaning products, personal care formulations, industrial detergents, agrochemicals, and specialty chemical applications. Between 2026 and 2033, capital investments are expected to accelerate across sustainable surfactant production technologies, bio-based feedstock integration, advanced manufacturing infrastructure, and environmentally compliant specialty chemical formulations.

The surfactant industry remains highly innovation-driven and capital-intensive, requiring continuous investments in production facilities, chemical processing technologies, raw material optimization systems, and regulatory compliance infrastructure. Major companies including BASF SE, Dow Inc., Evonik Industries, Clariant AG, Croda International, Solvay, Huntsman Corporation, Kao Corporation, and Stepan Company are increasing funding toward high-performance surfactants, renewable feedstocks, and next-generation green chemistry solutions to strengthen competitive positioning and long-term profitability.

A major transformation influencing investment patterns is the increasing shift toward sustainable and biodegradable surfactants. Regulatory pressure regarding environmental safety, wastewater treatment standards, and reduction of toxic chemical discharge is encouraging both public and private investments into bio-based surfactants, plant-derived raw materials, low-carbon production technologies, and circular chemical manufacturing systems.

Global Surfactant Market Investment & Funding Dynamics Current Scenario

Currently, investment activity in the surfactant market is strongly supported by rising global consumption of detergents, soaps, shampoos, cosmetics, industrial cleaners, and agrochemical products. Expansion of consumer goods manufacturing, increasing hygiene awareness, and growing industrial cleaning requirements continue to drive large-scale investments in specialty chemical production capacity and advanced formulation technologies.

- Asia-Pacific: Dominates global investment activity due to rapid industrialization, rising consumer goods production, expanding personal care markets, and increasing chemical manufacturing capacity across China, India, Japan, and Southeast Asia.

- North America: Continues attracting strong investments focused on sustainable surfactant development, specialty industrial chemicals, and advanced bio-based surfactant technologies supported by environmental compliance initiatives.

- Europe: Witnessing major funding activity driven by stringent environmental regulations, green chemistry initiatives, and increasing adoption of biodegradable and renewable surfactant formulations.

- Middle East & Latin America: Emerging as developing investment regions supported by industrial expansion, rising household product demand, and increasing investments in downstream specialty chemical manufacturing infrastructure.

Key Investment & Funding Dynamics Signals in Global Surfactant Market

- Growing global demand for household detergents, personal hygiene products, and industrial cleaning agents is accelerating investments in surfactant production expansion and specialty formulation development.

- Rising environmental regulations and sustainability requirements are driving strong funding toward biodegradable surfactants, renewable feedstocks, and eco-friendly chemical manufacturing technologies.

- Expansion of the agrochemical and oilfield chemicals industries is increasing capital allocation toward specialty surfactants designed for emulsification, dispersion, and enhanced performance applications.

- Technological advancements in bio-based surfactant synthesis, enzymatic processing, and green chemistry are attracting strategic investments from chemical manufacturers and sustainability-focused investors.

- Digital transformation across specialty chemical manufacturing is supporting investments in AI-based production optimization, smart process monitoring, predictive maintenance systems, and energy-efficient manufacturing infrastructure.

Strategic Implications of Investment & Funding Dynamics in Global Surfactant Market

- The investment landscape increasingly favors companies with strong capabilities in sustainable chemistry, renewable raw material sourcing, and environmentally compliant surfactant manufacturing technologies.

- Bio-based surfactants are emerging as a major strategic investment segment due to rising consumer preference for natural ingredients and increasing regulatory pressure on synthetic chemicals.

- Vertical integration strategies involving raw material sourcing, specialty formulation development, and downstream consumer product manufacturing are becoming increasingly important for long-term profitability and supply chain stability.

- Strategic acquisitions, research partnerships, and technology collaborations are accelerating as companies seek to strengthen innovation capabilities and expand global specialty surfactant portfolios.

- Raw material price volatility, particularly in petrochemical feedstocks and natural oils, continues influencing investment priorities, encouraging companies to diversify sourcing strategies and improve operational efficiency.

Global Surfactant Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Surfactant Market is expected to attract robust long-term investment driven by increasing demand for sustainable consumer products, industrial cleaning solutions, agrochemical formulations, and specialty chemical applications worldwide.

Future capital allocation will prioritize bio-based surfactant technologies, low-emission chemical production systems, advanced formulation capabilities, renewable feedstock processing, and digitalized manufacturing operations designed to improve sustainability and production efficiency.

- Asia-Pacific: Will remain the leading investment region supported by large-scale consumer goods production, expanding industrial manufacturing, and rising demand for personal care and cleaning products.

- North America: Will continue focusing on specialty surfactants, sustainable chemical innovation, and advanced industrial cleaning technologies supported by regulatory modernization.

- Europe: Will strengthen investments in circular chemical systems, green surfactant technologies, and environmentally sustainable manufacturing infrastructure.

Sustainability and carbon reduction initiatives are expected to increasingly reshape investment priorities across the surfactant industry. Companies are anticipated to accelerate funding toward renewable raw materials, biodegradable product development, waste reduction technologies, and environmentally optimized chemical processing systems.

Overall, the market is expected to maintain strong long-term expansion due to its essential role across household cleaning, personal care, agriculture, healthcare, and industrial manufacturing applications. Companies that successfully combine technological innovation, sustainable production capabilities, raw material optimization, and global supply chain efficiency will remain strongly positioned to lead the Global Surfactant Market through 2033.

Technology & Innovation

Global Surfactant Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Surfactant Market is evolving rapidly as chemical manufacturers increasingly focus on sustainable formulations, bio-based feedstocks, advanced performance chemistry, and environmentally responsible production technologies. Innovation across the market is centered around biodegradable surfactants, green chemistry processes, high-efficiency emulsification systems, multifunctional surfactant formulations, and advanced manufacturing technologies designed to improve product performance while reducing environmental impact.

The growing global emphasis on sustainability and environmental compliance is significantly reshaping the surfactant industry. Manufacturers are increasingly investing in renewable raw materials such as plant oils, sugar-based compounds, and naturally derived feedstocks to develop eco-friendly surfactants with lower toxicity and improved biodegradability. These innovations are helping companies align with stringent environmental regulations while meeting rising consumer demand for sustainable cleaning and personal care products.

Advanced formulation technologies are also becoming a major innovation area within the surfactant market. Companies are developing multifunctional surfactants capable of delivering improved foaming, wetting, dispersing, emulsifying, and conditioning performance across multiple industrial and consumer applications. These next-generation formulations are helping improve product efficiency while reducing overall chemical consumption in cleaning and industrial processing operations.

Digitalization and automation are increasingly transforming surfactant manufacturing processes. Chemical producers are adopting AI-driven process optimization systems, automated production monitoring platforms, predictive maintenance technologies, and advanced quality control analytics to improve operational efficiency, consistency, and cost management across manufacturing facilities.

In addition, nanotechnology and specialty chemistry innovations are expanding surfactant applications in pharmaceuticals, agriculture, oilfield chemicals, and advanced industrial formulations. Nano-emulsion technologies and precision surfactant systems are enabling improved active ingredient delivery, enhanced chemical stability, and better surface interaction capabilities in high-performance applications.

The innovation landscape is also shifting toward low-carbon production methods and circular economy initiatives. Manufacturers are increasingly adopting energy-efficient synthesis technologies, waste reduction systems, recyclable packaging solutions, and carbon footprint optimization strategies to strengthen sustainability across the entire surfactant value chain.

Global Surfactant Market Technology & Innovation Landscape Current Scenario

Currently, the global surfactant market is experiencing accelerated innovation driven by environmental regulations, rising sustainability expectations, and increasing demand for high-performance specialty formulations. Major chemical manufacturers such as BASF SE, Dow Inc., Evonik Industries, Clariant AG, Croda International, Huntsman Corporation, Solvay, Kao Corporation, Stepan Company, and Nouryon are actively investing in advanced surfactant technologies and green chemistry solutions.

Bio-based surfactants are emerging as one of the fastest-growing innovation segments within the market. Companies are increasingly developing surfactants derived from renewable feedstocks including coconut oil, palm oil, sugar derivatives, and microbial fermentation processes. These products are gaining traction across household cleaning, personal care, and industrial applications due to their improved biodegradability and lower environmental impact.

Advanced industrial surfactants are also witnessing strong development, particularly in agrochemicals, enhanced oil recovery, paints & coatings, textile processing, and pharmaceutical formulations. Manufacturers are designing specialized surfactants capable of operating under extreme temperatures, varying pH conditions, and complex industrial environments while maintaining high stability and performance efficiency.

Artificial intelligence and advanced analytics are increasingly being integrated into chemical manufacturing operations to optimize surfactant synthesis, formulation development, and supply chain management. AI-powered systems are helping manufacturers improve raw material utilization, reduce production waste, and accelerate new product development cycles.

Digital procurement platforms and integrated chemical supply chain systems are also becoming more common across the surfactant industry. These technologies are improving procurement transparency, inventory management, logistics coordination, and customer engagement across global chemical distribution networks.

In addition, companies are expanding research into sulfate-free, low-toxicity, and skin-friendly surfactants for personal care and cosmetic applications. These innovations are supporting growing consumer demand for premium and environmentally conscious beauty and hygiene products worldwide.

Key Technology & Innovation Trends in Global Surfactant Market

- Bio-Based Surfactant Development: Renewable and biodegradable surfactants derived from plant-based and natural feedstocks.

- Green Chemistry Manufacturing: Sustainable production technologies reducing emissions, waste generation, and environmental impact.

- Multifunctional Surfactant Formulations: Advanced products delivering enhanced emulsification, wetting, foaming, and dispersing performance.

- AI-Driven Process Optimization: Intelligent systems improving manufacturing efficiency, quality control, and resource management.

- Nanotechnology-Based Surfactants: Precision formulations supporting advanced pharmaceutical, industrial, and agricultural applications.

- Low-Toxicity & Sulfate-Free Solutions: Safer surfactant formulations for personal care, cosmetics, and healthcare products.

- Advanced Industrial Cleaning Chemistry: High-performance surfactants designed for industrial sanitation and institutional cleaning applications.

- Enhanced Oil Recovery Surfactants: Specialized chemical systems improving oil extraction efficiency in energy operations.

- Digital Supply Chain Integration: Smart procurement and logistics systems improving surfactant distribution and inventory management.

- Energy-Efficient Production Technologies: Manufacturing systems reducing energy consumption and operational costs.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally transforming the surfactant market by improving sustainability, product efficiency, manufacturing optimization, and regulatory compliance across the global specialty chemicals industry. Companies that successfully integrate advanced chemistry, renewable feedstocks, and digital manufacturing technologies are strengthening their competitive positioning within increasingly environmentally conscious markets.

For chemical manufacturers, investment in bio-based surfactants, green chemistry technologies, and intelligent production systems has become a major strategic priority. Organizations leveraging sustainable product portfolios and energy-efficient manufacturing processes are improving regulatory compliance, enhancing brand reputation, and expanding opportunities within premium consumer and industrial segments.

The growing adoption of AI and digital analytics is also improving operational performance across surfactant production facilities. Intelligent systems are enabling faster product development, better demand forecasting, optimized raw material utilization, and reduced manufacturing waste, helping companies improve profitability and supply chain resilience.

At the same time, increasing demand for customized and specialty surfactant formulations is driving innovation across pharmaceutical, agricultural, oilfield, and industrial processing applications. Manufacturers capable of delivering application-specific performance solutions are gaining strong advantages in high-value specialty chemical markets.

However, challenges such as volatile raw material prices, environmental compliance costs, sustainable feedstock availability, and evolving global chemical regulations continue to impact market dynamics. Companies must continue investing in R&D, sustainable sourcing strategies, and advanced manufacturing technologies to maintain long-term competitiveness.

Global Surfactant Market Technology & Innovation Forward Outlook

Looking ahead, the global surfactant market is expected to evolve toward highly sustainable, digitally optimized, and performance-driven chemical ecosystems powered by green chemistry, renewable feedstocks, artificial intelligence, and advanced formulation science. Manufacturers will increasingly focus on developing next-generation surfactants that combine high performance with low environmental impact.

Bio-based and biodegradable surfactants are expected to witness significant expansion as regulatory agencies and consumers continue prioritizing sustainability and environmentally safe products. Companies investing in renewable chemistry technologies and low-carbon manufacturing infrastructure are likely to gain strong competitive advantages in future market landscapes.

Artificial intelligence is expected to play a much larger role in surfactant formulation design, predictive process optimization, and supply chain automation. AI-driven innovation platforms will help accelerate product development while improving manufacturing efficiency and reducing operational costs.

Nanotechnology and advanced molecular engineering are also expected to create new opportunities for high-performance surfactants in pharmaceuticals, agriculture, industrial processing, and energy applications. Precision chemical systems with enhanced stability, targeted delivery capabilities, and multifunctional properties will increasingly support specialized industrial requirements.

Smart manufacturing facilities equipped with automated process controls, digital twins, IoT-enabled monitoring systems, and advanced sustainability analytics are expected to become increasingly common across the surfactant industry. These intelligent production environments will improve efficiency, quality consistency, and environmental performance throughout the manufacturing lifecycle.

In conclusion, the Global Surfactant Market is undergoing a major technological transformation driven by sustainable chemistry innovation, advanced formulation technologies, AI integration, and environmentally responsible manufacturing practices. Companies that successfully combine high-performance surfactant technologies, sustainable production strategies, and digital operational capabilities will lead the future evolution of the global surfactant industry.

Market Risk

Global Surfactant Market Risk Factors & Disruption Threats Overview

The global surfactant market is experiencing steady expansion driven by rising demand from household cleaning products, personal care formulations, industrial applications, agrochemicals, and oilfield chemicals. However, despite favorable long-term demand trends, the market faces a complex risk environment influenced by raw material volatility, environmental regulations, supply chain disruptions, sustainability pressures, and changing consumer preferences. Since surfactants are essential ingredients across multiple industries, fluctuations in production economics or regulatory compliance can significantly impact global manufacturing operations and profitability.

One of the most significant risk factors in the surfactant market is dependence on petrochemical and oleochemical feedstocks. Many surfactants are derived from crude oil-based chemicals or vegetable oils such as palm oil and coconut oil. Fluctuations in crude oil prices, agricultural commodity costs, and feedstock availability directly affect manufacturing expenses and pricing stability. Supply disruptions caused by geopolitical tensions, climate-related agricultural impacts, or trade restrictions can significantly influence raw material procurement and production continuity.

Environmental regulations and sustainability compliance represent another major disruption threat within the market. Governments and regulatory agencies worldwide are implementing stricter standards regarding biodegradability, toxicity, wastewater discharge, and chemical safety. Certain surfactants, particularly non-biodegradable or environmentally persistent compounds, face increasing scrutiny due to their ecological impact on aquatic systems and water treatment infrastructure. Compliance with evolving environmental regulations is increasing operational costs and forcing manufacturers to accelerate investments in green chemistry and sustainable formulations.

Another critical risk factor involves rising consumer awareness regarding product safety, sustainability, and chemical transparency. Consumers are increasingly demanding eco-friendly, sulfate-free, non-toxic, and biodegradable cleaning and personal care products. This shift in purchasing behavior is pressuring manufacturers to reformulate products and reduce reliance on traditional synthetic surfactants. Failure to adapt to changing consumer expectations may result in reduced market competitiveness and reputational risks for established brands.

Additionally, global supply chain instability continues to create operational challenges across the surfactant industry. Transportation bottlenecks, port congestion, geopolitical conflicts, and shortages of specialty chemicals can disrupt manufacturing schedules and delay product deliveries. Since surfactants are integrated into large-scale consumer and industrial supply chains, disruptions can rapidly affect downstream industries including detergents, cosmetics, agriculture, pharmaceuticals, and industrial processing.

Global Surfactant Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong demand growth across household cleaning, personal care, and industrial applications, supported by increasing hygiene awareness and expanding manufacturing activities worldwide. However, manufacturers are simultaneously facing rising input costs, tightening environmental regulations, and growing pressure to transition toward sustainable production models.

Feedstock price volatility remains one of the most pressing challenges in the current market landscape. Crude oil price fluctuations continue to affect petrochemical-derived surfactant production costs, while weather-related disruptions and sustainability controversies surrounding palm oil production are impacting oleochemical supply stability. These cost pressures are influencing pricing strategies and profit margins across the industry.

The market is also experiencing accelerated regulatory scrutiny regarding chemical safety and environmental impact. Governments in Europe and North America are implementing stricter standards related to biodegradable formulations, hazardous chemical restrictions, and wastewater treatment requirements. Manufacturers must increasingly invest in R&D, reformulation initiatives, and regulatory testing to maintain compliance across global markets.

Another important trend in the current scenario is the rapid expansion of bio-based surfactants and green chemistry solutions. While these alternatives support sustainability objectives, they often involve higher production costs, scalability challenges, and limited feedstock availability compared to conventional synthetic surfactants. Balancing sustainability goals with cost competitiveness remains a key industry challenge.

In addition, rising competition among multinational chemical companies and regional specialty chemical producers is intensifying pricing pressure and innovation cycles. Companies are increasingly differentiating through specialty formulations, low-toxicity products, and environmentally certified surfactant solutions to strengthen market positioning.

Global Surfactant Market Key Risk Factors & Disruption Threat Signals

One of the most significant disruption signals in the surfactant market is the accelerating transition toward bio-based and biodegradable surfactants. While this shift creates strong growth opportunities, it also disrupts traditional manufacturing models and increases dependency on agricultural feedstocks and renewable raw material supply chains.

Another major disruption trend is the growing integration of green chemistry and low-carbon manufacturing processes within the specialty chemicals industry. Companies are under increasing pressure to reduce emissions, energy consumption, and environmental waste across production operations. Failure to meet sustainability expectations may result in reduced regulatory approval and declining customer acceptance.

The increasing use of advanced surfactants in specialty applications such as pharmaceuticals, enhanced oil recovery, agrochemicals, and high-performance industrial formulations is also reshaping market dynamics. These applications require highly customized formulations and strict quality standards, increasing technical complexity and regulatory oversight.

Climate-related disruptions represent another emerging risk factor affecting agricultural feedstock supply chains. Extreme weather events, water scarcity, and changing climate conditions may impact the availability and pricing of vegetable oil-based raw materials used in bio-based surfactant production.

In addition, the rise of circular economy initiatives and sustainable packaging trends may influence future product formulation strategies. Companies are increasingly expected to develop environmentally responsible products that align with recyclable packaging systems and reduced environmental impact targets.

Global Surfactant Market Strategic Implications of Risk Factors

To manage feedstock volatility risks, surfactant manufacturers should diversify raw material sourcing strategies and reduce dependency on single-source petrochemical or agricultural supply chains. Investments in alternative renewable feedstocks and localized sourcing models can improve long-term supply resilience.

Sustainability integration will become increasingly essential for maintaining regulatory compliance and market competitiveness. Companies must accelerate investment in biodegradable formulations, low-toxicity chemistries, energy-efficient manufacturing processes, and environmentally certified products to align with global environmental standards.

Manufacturers should also strengthen R&D capabilities focused on specialty surfactants and high-performance formulations for industrial, pharmaceutical, and agricultural applications. Innovation-driven product differentiation will become a critical competitive advantage as standard surfactant markets face increasing commoditization pressure.

Digitalization and supply chain optimization technologies can help improve operational resilience and inventory management efficiency. AI-driven demand forecasting, predictive maintenance systems, and automated production monitoring can support cost reduction and minimize disruption risks.

Strategic partnerships with consumer goods companies, agricultural suppliers, and sustainability certification organizations will also become increasingly important for ensuring long-term market access and product credibility within environmentally conscious industries.

Global Surfactant Market Forward Risk Outlook

Looking ahead to 2026???2033, the global surfactant market is expected to continue expanding steadily due to rising demand from consumer goods, industrial manufacturing, healthcare, and agriculture sectors. However, long-term market stability will depend heavily on sustainability transformation, regulatory adaptability, and supply chain resilience.

The industry is expected to witness increasing adoption of bio-based surfactants, green chemistry technologies, and low-carbon manufacturing systems as environmental regulations continue to tighten globally. Companies that successfully balance performance, affordability, and sustainability will strengthen long-term competitive positioning.

Overall, while the global surfactant market presents strong growth opportunities supported by essential end-use applications, sustainable success will depend on effectively managing raw material volatility, environmental compliance pressures, technological innovation, and evolving consumer expectations within an increasingly sustainability-focused global chemicals industry.

Regulatory Landscape

Global Surfactant Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global surfactant market is becoming increasingly stringent and sustainability-focused as governments, environmental agencies, and chemical safety authorities strengthen regulations related to chemical usage, environmental protection, product safety, emissions control, and biodegradable ingredient standards. Surfactants are widely used across detergents, personal care products, industrial cleaning solutions, agrochemicals, pharmaceuticals, and oilfield chemicals, making them subject to extensive regulatory oversight throughout their production, transportation, usage, and disposal lifecycles.

Regulatory bodies worldwide are emphasizing safer chemical formulations and environmentally responsible manufacturing practices to reduce water pollution, hazardous waste generation, and long-term ecological impact associated with conventional synthetic surfactants. This has accelerated the implementation of stricter regulations regarding toxicity levels, biodegradability, aquatic safety, and permissible chemical compositions in surfactant-based products.

Governments are also increasingly encouraging the transition toward bio-based and renewable surfactants through sustainability initiatives, green chemistry programs, and carbon reduction policies. Manufacturers are under growing pressure to replace petroleum-derived feedstocks with renewable raw materials while maintaining product performance, cost efficiency, and large-scale manufacturing capability.

Additionally, evolving consumer product regulations, occupational safety standards, and industrial chemical handling requirements are influencing surfactant formulation strategies across household cleaning products, cosmetics, industrial chemicals, and agricultural applications. Regulatory harmonization between international chemical safety frameworks is becoming increasingly important for multinational surfactant producers operating across global markets.

Global Surfactant Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for the surfactant market is heavily shaped by environmental protection laws, chemical registration frameworks, and sustainability mandates. Developed regions such as Europe and North America maintain strict compliance systems governing surfactant manufacturing, chemical usage, wastewater discharge, and consumer product safety.

In Europe, surfactant manufacturers must comply with REACH (Registration, Evaluation, Authorization and Restriction of Chemicals), CLP regulations, and various environmental directives focused on biodegradability, aquatic toxicity, and chemical risk management. The European Union is strongly promoting green chemistry initiatives and sustainable chemical production, driving rapid adoption of bio-based surfactants and environmentally friendly formulations.

North America maintains strong regulatory oversight through agencies such as the U.S. Environmental Protection Agency (EPA) and Health Canada. Regulatory frameworks focus on chemical safety assessments, industrial emissions management, workplace safety standards, and environmental impact reduction for surfactant production and downstream applications.

Asia-Pacific is witnessing rapid regulatory development due to expanding chemical manufacturing activities and increasing environmental concerns. Countries such as China, Japan, South Korea, and India are strengthening industrial pollution controls, wastewater treatment regulations, and chemical safety frameworks to align with global environmental standards and support sustainable industrial growth.

Latin America, the Middle East, and Africa are gradually improving chemical safety regulations and environmental governance systems, particularly in response to increasing industrialization, expanding consumer goods sectors, and rising global sustainability expectations.

Key Regulatory & Policy Environment Signals in Global Surfactant Market

- Chemical Safety & Registration Regulations: Manufacturers must comply with chemical registration frameworks such as REACH, TSCA, and regional chemical inventory systems governing surfactant production and usage.

- Environmental Protection & Wastewater Regulations: Governments are enforcing stricter wastewater discharge standards and pollution control measures for surfactant manufacturing facilities.

- Biodegradability & Eco-Toxicity Standards: Regulatory agencies are increasing requirements for biodegradable formulations and limiting environmentally harmful surfactant compounds.

- Green Chemistry & Sustainable Manufacturing Policies: Governments are promoting renewable feedstocks, low-carbon production processes, and environmentally friendly surfactant technologies.

- Consumer Product Safety Regulations: Household cleaning products, cosmetics, and personal care formulations containing surfactants are subject to strict labeling, safety, and ingredient disclosure requirements.

- Occupational Health & Industrial Safety Standards: Chemical manufacturing operations must comply with workplace safety, hazardous material handling, and industrial exposure regulations.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is significantly influencing product innovation, manufacturing strategies, and supply chain management across the surfactant industry. Companies are increasingly investing in research and development focused on biodegradable surfactants, renewable feedstocks, and low-toxicity formulations to meet tightening environmental standards and changing consumer expectations.

Compliance with global chemical safety regulations is becoming a major competitive factor, particularly for multinational surfactant producers serving regulated consumer goods, pharmaceutical, and industrial sectors. Manufacturers that maintain strong compliance systems and transparent sustainability reporting are gaining advantages in global markets.

Environmental regulations are also accelerating investments in cleaner production technologies, energy-efficient manufacturing systems, and advanced wastewater treatment infrastructure. This is increasing operational costs in the short term but improving long-term sustainability positioning and regulatory resilience.

The growing demand for green consumer products is encouraging surfactant manufacturers to collaborate closely with personal care, detergent, and industrial cleaning product companies to develop sustainable formulations that comply with evolving environmental and safety regulations while maintaining high performance standards.

Global Surfactant Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global surfactant market is expected to become increasingly sustainability-driven, science-based, and internationally coordinated. Governments are likely to continue strengthening environmental regulations targeting hazardous chemicals, industrial emissions, water pollution, and non-biodegradable surfactant compounds.

Future policies are expected to accelerate the transition toward renewable and bio-based surfactants through carbon reduction initiatives, green chemistry incentives, and stricter sustainability disclosure requirements. Manufacturers will likely face increasing pressure to reduce dependency on fossil fuel-derived feedstocks and improve circular economy integration within chemical production systems.

Water conservation and wastewater treatment regulations are also expected to intensify globally, particularly in regions facing industrial pollution challenges and resource constraints. This will increase demand for environmentally compatible surfactants with lower ecological impact and improved biodegradability profiles.

Digital compliance systems and supply chain traceability requirements may become more important as regulators seek greater transparency regarding chemical sourcing, sustainability metrics, and lifecycle environmental impact assessments. Companies may increasingly adopt AI-driven compliance management and advanced environmental monitoring technologies to meet evolving regulatory obligations.

Overall, the regulatory and policy environment will play a central role in shaping the long-term transformation of the global surfactant market. Companies that successfully align with environmental sustainability goals, chemical safety regulations, and green manufacturing practices will be best positioned to maintain long-term competitiveness and growth in the evolving specialty chemicals industry.