Global Plant-Based Meat Market size and share Analysis 2026-2033

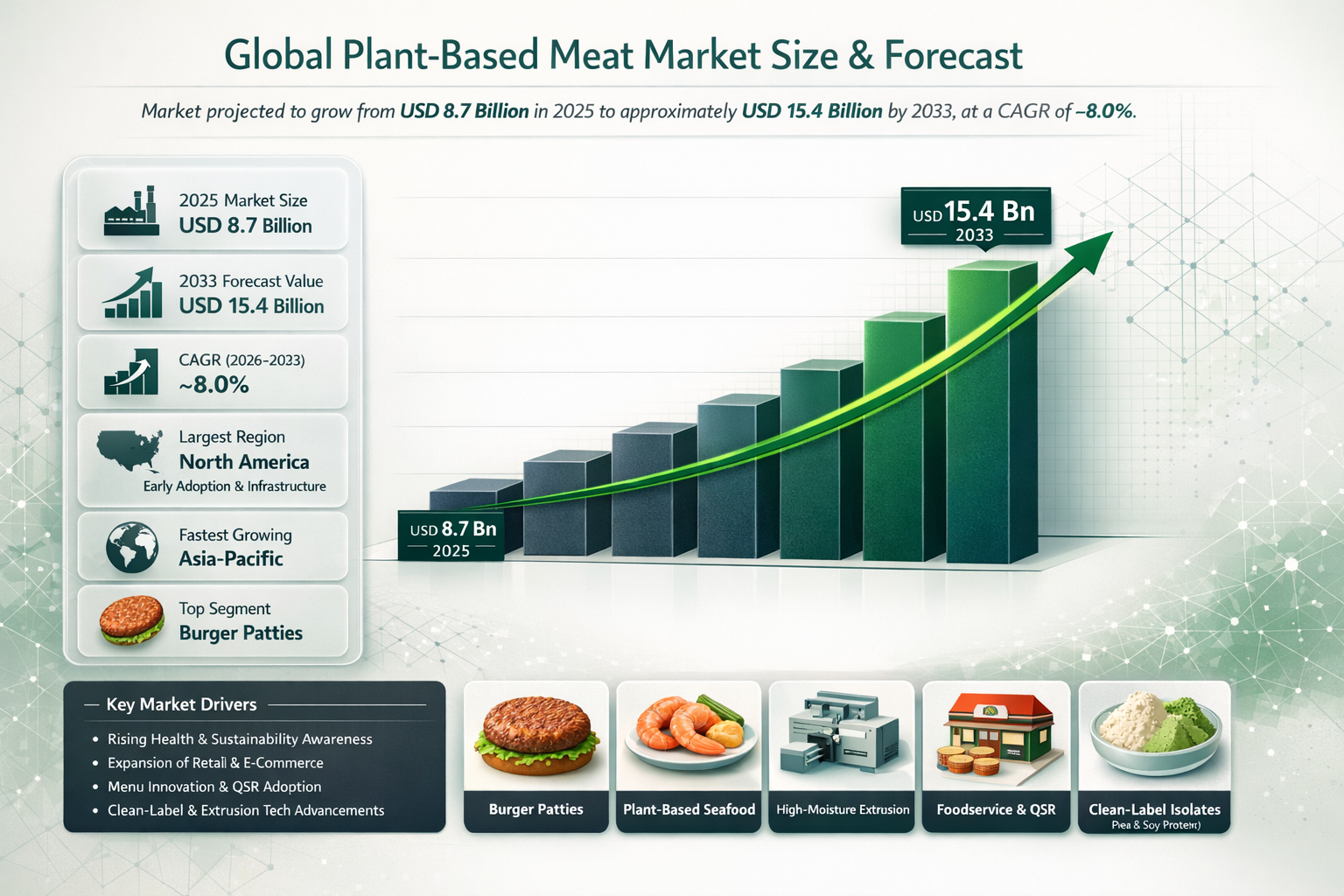

Global Plant-Based Meat Market Forecast Snapshot: 2026???2033

| Metric | Value |

| 2025 Market Size | USD 8.7 Billion |

| 2033 Market Size | USD 15.4 Billion |

| CAGR (2026???2033) | ~8.0% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Plant-Based Meat Alternatives ??? Burger Patties |

| Key Trend | Clean-Label, High-Protein & Sustainable Protein Innovation |

| Future Focus | Product Innovation, Supply Chain Scaling, and Plant-Based Diversification |

Global Plant-Based Meat Market Overview

The Global Plant-Based Meat Market is booming! Plant-based meats are taking over, driven by health-conscious folks, eco-friendly vibes, and the need for sustainable protein. From burgers to nuggets, sausages, and more, plant-based meats are popping up on menus and shelves everywhere, fueled by better food choices, less environmental impact, and tastier innovations.

According to Pheonix Research, the Global Plant-Based Meat Market is valued at USD 8.7 billion in 2025 and is projected to reach USD 15.4 billion by 2033, registering a CAGR of ~8.0% during 2026???2033. Growth is being driven by evolving consumer preferences, rapid product innovation, and expansion of modern retail and foodservice channels.

North America currently dominates due to strong consumer awareness, advanced retail infrastructure, and early adoption of plant-based alternatives. Meanwhile, Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable incomes, and increasing awareness of sustainable protein options. Post-2025 Outlook: The market is expected to see deeper integration of functional ingredients, AI-driven product personalization, sustainable sourcing strategies, and expanded foodservice adoption, positioning plant-based meat as a strategically important growth category rather than a niche trend.Key Drivers of Global Plant-Based Meat Market Growth

Rising Health & Sustainability Awareness

Growing consumer concern over the health and environmental impacts of conventional meat is driving increased adoption of plant-based alternatives.

Expansion of Retail & E-Commerce Channels

??Supermarkets, hypermarkets, and online grocery platforms are enhancing accessibility, improving distribution, and expanding market reach for plant-based meat products.

Menu Innovation & Foodservice Adoption

Quick-service restaurants, full-service eateries, and hotels are increasingly incorporating plant-based meat options???such as burgers, nuggets, strips, and ethnic dishes???catering to flexitarian and health-conscious consumers.

Technological Advancements & Product Development

Innovations in protein isolates, high-moisture extrusion, and clean-label formulations are improving taste, texture, and nutritional profiles, making plant-based meat more appealing and realistic.

Regulatory Support & Market Approvals

Favorable food safety regulations, labeling standards, and market approvals across North America, Europe, and Asia are enabling large-scale commercial production and facilitating rapid market growth.

Global Plant-Based Meat Market Segmentation

?? ?? 1. By Product Type

1.1 Plant-Based Meat Alternatives

1.1.1 Burger Patties

1.1.1.1 Soy-Based Patties

1.1.1.2 Pea-Protein Patties

1.1.1.3 Wheat-Protein (Seitan) Patties

1.1.1.4 Mixed Protein Blends

1.1.1.5 Premium Gourmet Patties

1.1.2 Sausages & Hot Dogs

1.1.2.1 Breakfast Sausages

1.1.2.2 Smoked Sausages

1.1.2.3 Hot Dogs

1.1.2.4 Spicy & Regional Variants

1.1.3 Nuggets & Strips

1.1.3.1 Breaded Nuggets

1.1.3.2 Grilled Strips

1.1.3.3 Frozen Ready-to-Cook Formats

1.1.3.4 High-Protein Snack Bites

1.1.4 Minced & Ground Meat Alternatives

1.1.4.1 Plant-Based Ground Beef

1.1.4.2 Plant-Based Minced Chicken

1.1.4.3 Plant-Based Meat Crumbles

1.1.4.4 Ready Meal Integration Formats

1.2 Plant-Based Seafood Alternatives

1.2.1 Fillets & Steaks

1.2.1.1 Fish Fillets

1.2.1.2 Shrimp Alternatives

1.2.1.3 Crab & Lobster Alternatives

1.2.2 Nuggets & Patties

1.2.2.1 Fish Sticks & Nuggets

1.2.2.2 Crab Cakes & Patties

1.3 Plant-Based Deli & Ready-to-Cook Products

1.3.1 Sliced & Cold Cuts

1.3.1.1 Vegan Ham

1.3.1.2 Vegan Turkey Slices

1.3.1.3 Plant-Based Bacon

1.3.2 Marinated & Pre-Cooked Meals

1.3.2.1 Ready-to-Grill Kebabs

1.3.2.2 Frozen Plant-Based Meals

?? ?? ??2. By Distribution Channel

2.1 Retail

2.1.1 Supermarkets & Hypermarkets

2.1.1.1 National Chains

2.1.1.2 Private Label Products

2.1.1.3 Refrigerated Sections

2.1.2 Health & Organic Stores

2.1.2.1 Specialty Retailers

2.1.2.2 Vegan Specialty Stores

2.2 Online

2.2.1 E-commerce Platforms

2.2.1.1 Marketplace Platforms

2.2.1.2 Grocery Delivery Apps

2.2.2 Brand-Owned Websites

2.2.2.1 Direct-to-Consumer (DTC)

2.2.2.2 Subscription Programs

2.3 Foodservice

2.3.1 Quick-Service Restaurants (QSR)

2.3.1.1 Burger Chains

2.3.1.2 Nuggets & Strips Menu

2.3.2 Full-Service Restaurants

2.3.2.1 Casual Dining

2.3.2.2 Premium Dining

2.3.3 Institutional Catering

2.3.3.1 Schools & Universities

2.3.3.2 Hospitals & Corporate Campuses

?? ?? ??3. By End-User

3.1 Individual Consumers

3.1.1 Vegans

3.1.1.1 Ethical Vegans

3.1.1.2 Environmental Vegans

3.1.2 Flexitarians

3.1.2.1 Occasional Plant-Based Consumers

3.1.2.2 Health-Driven Flexitarians

3.1.3 Health-Conscious Consumers

3.1.3.1 Fitness-Oriented

3.1.3.2 Weight Management

3.2 Food Manufacturers

3.2.1 Processed Meat Producers

3.2.1.1 Vegan Meat Snack Manufacturers

3.2.1.2 Ready Meal Manufacturers

3.3 Foodservice Operators

3.3.1 QSR Chains

3.3.1.1 International Chains

3.3.1.2 Regional Chains

3.3.2 Hotels & Caf??s

3.3.2.1 Premium Hotels

3.3.2.2 Caf?? Chains

?? ??4.By Region

4.1 North America 4.2 Europe 4.3 Asia-Pacific 4.4 Middle East & Africa 4.5. South AmericaRegional Insights of the Global Plant-Based Meat Market

North America ??? Largest Market

The U.S. drives regional dominance, supported by early adoption of plant-based meats, high disposable income, strong consumer awareness, and advanced retail and distribution networks.

Asia-Pacific ??? Fastest Growing Market

Rapid market expansion is fueled by urbanization, rising middle-class populations, growing awareness of meat alternatives, and increasing penetration of modern retail channels across China, India, Japan, and Southeast Asia.

Europe

Growth is underpinned by stringent sustainability policies, a rising vegan and flexitarian population, and regulatory frameworks that enable large-scale commercialization of plant-based meat products.

Middle East & Africa

Market development is supported by increasing health consciousness, expansion of premium retail formats, and growing imports of international plant-based meat brands.

South America

Adoption is driven by rising health awareness, an expanding middle-class consumer base, and increased integration of plant-based meat into foodservice and quick-service restaurant channels.

Leading Companies

-

Nestl?? S.A. (Plant-Based Division)

-

Tyson Foods (Alternative Protein Division)

-

Maple Leaf Foods (Greenleaf Foods)

-

Danone S.A. (Plant-Based Division)

-

Eat Just, Inc.

-

The Hain Celestial Group

-

Oatly Group AB

-

Unilever PLC (Plant-Based Portfolio)

Beyond Meat, Inc.?? is the largest company in the Plant-Based Meat Market.These companies are driving innovation through product diversification, clean-label offerings, and advanced production technologies. Market leadership is increasingly determined by scalability, sustainability initiatives, and consumer acceptance in key global regions.

Strategic Intelligence & AI-Driven Insights

Pheonix Demand Forecast Engine: Projects strong, sustained double-digit growth across key segments including burger patties, nuggets, and high-protein plant-based snacks.

Consumer Behavior Analyzer: Identifies flexitarians and health-conscious consumers as the primary adopters, highlighting a broader shift toward sustainable and functional protein alternatives.

Innovation Tracker: Tracks advancements in fermentation-based proteins, hybrid formulations, clean-label products, and AI-enabled supply chain optimization, supporting scalability and efficiency.

Porter???s Five Forces Analysis: Reveals moderate supplier bargaining power, intense competitive rivalry, and significant growth opportunities for brands that differentiate through premium quality, sustainability, and technological integration.

Why the Global Plant-Based Meat Market is Critical

-

Rising demand for sustainable, high-protein alternatives to conventional meat.

-

Increasing integration into QSR menus, retail, and ready-to-eat products.

-

Innovation in product development, flavor profiles, and texture realism driving adoption.

-

Regulatory approvals, sustainability mandates, and urbanization boosting market growth.

Final Takeaway of Global Plant-Based Meat Market

The Global Plant-Based Meat Market is transitioning from a niche segment to a mainstream protein pillar within the sustainable food ecosystem. With a projected CAGR of ~8.0% (2026???2033), growth is driven by rising consumer health awareness, environmental sustainability concerns, regulatory support, technological innovation, and expanded retail and foodservice penetration.

Companies that focus on product innovation, fermentation-based proteins, hybrid formulations, automation, and supply chain scalability are well-positioned to capture long-term value. Strategic partnerships, investment in R&D, and alignment with environmental sustainability goals will remain key competitive differentiators in the post-2025 landscape.

At Pheonix Research, our advanced forecasting models deliver in-depth market revenue analysis, competitive benchmarking, and strategic intelligence, enabling stakeholders to capitalize on emerging opportunities with data-backed confidence and sustainable growth strategies.???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on??LinkedIn??and??X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433034201727393793

X : https://x.com/Pheonix_Insight/status/2027271963111235595?s=20

Table of Contents

1. Executive Summary

1.1 Market Forecast Snapshot (2026???2033)

1.1.1 2025 Market Size ??? USD 8.7 Billion

1.1.2 2033 Market Size ??? USD 15.4 Billion

1.1.3 CAGR (2026???2033) ??? ~8.0%

1.2 Key Highlights

1.2.1 Largest Region ??? North America

1.2.2 Fastest Growing Region ??? Asia-Pacific

1.2.3 Dominant Segment ??? Plant-Based Burger Patties

1.2.4 Key Trend ??? Clean-Label, High-Protein & Sustainable Protein Innovation

1.2.5 Future Focus ??? Product Innovation, Supply Chain Scaling, and Plant-Based Diversification

1.3 Strategic Insights

1.3.1 Structural Shift Toward Plant-Forward Diets

1.3.2 Innovation-Led Competitive Landscape

1.3.3 Retail & Foodservice Expansion

1.3.4 Long-Term Investment Attractiveness

2. Global Plant-Based Meat Market Overview

2.1 Market Definition & Scope

2.2 Evolution of the Plant-Based Meat Industry

2.3 Consumer Adoption Trends: Flexitarian & Health-Conscious Diets

2.4 Technological Advancements: Fermentation, Extrusion & Hybrid Formulations

2.5 Regulatory & Labeling Landscape

2.6 Post-2025 Market Outlook

3. Key Drivers of Market Growth

3.1 Rising Health & Sustainability Awareness

3.2 Expansion of Retail & E-Commerce Channels

3.3 Menu Innovation & Foodservice Adoption

3.4 Technological Advancements & Product Development

3.5 Regulatory Support & Market Approvals

3.6 ESG & Sustainability Initiatives

4. Market Segmentation by Product Type

4.1 Plant-Based Meat Alternatives

4.1.1 Burger Patties

4.1.1.1 Soy-Based Patties

4.1.1.2 Pea-Protein Patties

4.1.1.3 Wheat-Protein (Seitan) Patties

4.1.1.4 Mixed Protein Blends

4.1.1.5 Premium Gourmet Patties

4.1.2 Sausages & Hot Dogs

4.1.2.1 Breakfast Sausages

4.1.2.2 Smoked Sausages

4.1.2.3 Hot Dogs

4.1.2.4 Spicy & Regional Variants

4.1.3 Nuggets & Strips

4.1.3.1 Breaded Nuggets

4.1.3.2 Grilled Strips

4.1.3.3 Frozen Ready-to-Cook Formats

4.1.3.4 High-Protein Snack Bites

4.1.4 Minced & Ground Meat Alternatives

4.1.4.1 Plant-Based Ground Beef

4.1.4.2 Plant-Based Minced Chicken

4.1.4.3 Plant-Based Meat Crumbles

4.1.4.4 Ready Meal Integration Formats

4.2 Plant-Based Seafood Alternatives

4.2.1 Fillets & Steaks

4.2.1.1 Fish Fillets

4.2.1.2 Shrimp Alternatives

4.2.1.3 Crab & Lobster Alternatives

4.2.2 Nuggets & Patties

4.2.2.1 Fish Sticks & Nuggets

4.2.2.2 Crab Cakes & Patties

4.3 Plant-Based Deli & Ready-to-Cook Products

4.3.1 Sliced & Cold Cuts

4.3.1.1 Vegan Ham

4.3.1.2 Vegan Turkey Slices

4.3.1.3 Plant-Based Bacon

4.3.2 Marinated & Pre-Cooked Meals

4.3.2.1 Ready-to-Grill Kebabs

4.3.2.2 Frozen Plant-Based Meals

5. Market Segmentation by Distribution Channel

5.1 Retail

5.1.1 Supermarkets & Hypermarkets

5.1.1.1 National Chains

5.1.1.2 Private Label Products

5.1.1.3 Refrigerated Sections

5.1.2 Health & Organic Stores

5.1.2.1 Specialty Health Retailers

5.1.2.2 Vegan Specialty Stores

5.2 Online

5.2.1 E-Commerce Platforms

5.2.1.1 Marketplace Platforms (Amazon, Alibaba, etc.)

5.2.1.2 Grocery Delivery Apps

5.2.2 Brand-Owned Websites

5.2.2.1 Direct-to-Consumer (DTC)

5.2.2.2 Subscription Programs

5.3 Foodservice

5.3.1 Quick-Service Restaurants (QSR)

5.3.1.1 Burger Chains

5.3.1.2 Nuggets & Strips Menu

5.3.2 Full-Service Restaurants

5.3.2.1 Casual Dining

5.3.2.2 Premium Dining

5.3.3 Institutional Catering

5.3.3.1 Schools & Universities

5.3.3.2 Hospitals & Corporate Campuses

6. Market Segmentation by End-User

6.1 Individual Consumers

6.1.1 Vegans

6.1.1.1 Ethical Vegans

6.1.1.2 Environmental Vegans

6.1.2 Flexitarians

6.1.2.1 Occasional Plant-Based Consumers

6.1.2.2 Health-Driven Flexitarians

6.1.3 Health-Conscious Consumers

6.1.3.1 Fitness-Oriented

6.1.3.2 Weight Management

6.2 Food Manufacturers

6.2.1 Processed Meat Producers

6.2.1.1 Vegan Meat Snack Manufacturers

6.2.1.2 Ready Meal Manufacturers

6.3 Foodservice Operators

6.3.1 QSR Chains

6.3.1.1 International Chains

6.3.1.2 Regional Chains

6.3.2 Hotels & Caf??s

6.3.2.1 Premium Hotels

6.3.2.2 Caf?? Chains

7. Market Segmentation by Region

7.1 North America ??? Largest Market

7.2 Asia-Pacific ??? Fastest Growing Region

7.3 Europe

7.4 Middle East & Africa

7.5 South America

8. Regional Insights

8.1 North America ??? U.S. Drives Dominance

8.2 Asia-Pacific ??? Urbanization & Middle-Class Growth

8.3 Europe ??? Sustainability Policies & Vegan Population

8.4 Middle East & Africa ??? Premium Retail Expansion

8.5 South America ??? Health Awareness & Retail Integration

9. Competitive Landscape

9.1 Market Share Analysis

9.2 Competitive Positioning Matrix

9.3 Mergers & Acquisitions

9.4 Innovation & R&D Trends

9.5 Pricing & Premiumization Strategies

10. Leading Companies

10.1 Beyond Meat, Inc.

10.2 Impossible Foods Inc.

10.3 Nestl?? S.A. (Plant-Based Division)

10.4 Tyson Foods (Alternative Protein Division)

10.5 Maple Leaf Foods (Greenleaf Foods)

10.6 Danone S.A. (Plant-Based Division)

10.7 Eat Just, Inc.

10.8 The Hain Celestial Group

10.9 Oatly Group AB

10.10 Unilever PLC (Plant-Based Portfolio)

11. Strategic Intelligence & AI-Driven Insights

11.1 Pheonix Demand Forecast Engine

11.2 Consumer Behavior Analyzer

11.3 Innovation Tracker: Fermentation, Hybrid Proteins, AI Supply Chain

11.4 Porter???s Five Forces Analysis

12. Sustainability & Regulatory Landscape

12.1 Carbon Reduction & ESG Alignment

12.2 Sustainable Sourcing & Supply Chain Transparency

12.3 Regulatory Framework & Labeling Standards

12.4 Responsible Production Practices

13. Market Significance

13.1 Contribution to Sustainable Protein Ecosystem

13.2 Public Health & Nutrition Impact

13.3 Retail & Foodservice Transformation

13.4 Investment & Economic Impact

13.5 Role in Food Security & Supply Diversification

14. Final Takeaway

14.1 Market Growth Outlook (2026???2033)

14.2 Structural Growth Thesis

14.3 Premium & Functional Strategy Roadmap

14.4 Retail, QSR & Foodservice Expansion Strategy

14.5 Strategic Recommendations

15. Appendix

16. About Us

17. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Plant-Based Meat Market

Executive Framing

The Global Plant-Based Meat Market is moderately consolidated, led by prominent players such as Beyond Meat, Impossible Foods, Nestl??, Tyson Foods, and Unilever. These companies compete alongside emerging startups and regional innovators, creating a highly dynamic and innovation-driven competitive environment.

Current Market Reality

The market is characterized by rapid product innovation, expanding foodservice partnerships, and increasing retail penetration. Burger patties dominate the segment, while nuggets, sausages, and ready-to-cook products are gaining traction. Large multinational companies leverage scale, R&D capabilities, and global distribution, while startups focus on niche innovation and clean-label differentiation.

Competition is intensifying across both B2C (retail and foodservice) and B2B (ingredient supply and co-manufacturing) segments, with companies investing heavily in taste, texture, and nutritional improvements.

Key Signals and Evidence

- Strong expansion of plant-based offerings across QSR chains and foodservice menus globally.

- Continuous innovation in high-moisture extrusion, fermentation-based proteins, and clean-label formulations.

- Growing investments in production scaling and supply chain optimization.

- Rising competition from private label and regional brands.

- Increased focus on sustainability, carbon footprint reduction, and ethical sourcing.

Strategic Implications

- Product Innovation: Enhance taste, texture, and nutritional profiles through advanced food technologies.

- Foodservice Expansion: Strengthen partnerships with QSRs, restaurants, and global chains.

- Scale & Cost Optimization: Invest in large-scale production and efficient supply chains.

- Brand Differentiation: Focus on clean-label, high-protein, and functional positioning.

- Sustainability Leadership: Highlight environmental benefits and sustainable sourcing practices.

Forward Outlook

The Global Plant-Based Meat Market is projected to grow from USD 8.7 billion in 2025 to USD 15.4 billion by 2033, at a CAGR of ~8.0%. North America will continue to lead, while Asia-Pacific will emerge as the fastest-growing region driven by urbanization and increasing demand for sustainable protein alternatives.

Future competition will be shaped by technological innovation, cost competitiveness, product diversification, and global expansion strategies, with companies focusing on scaling production and improving consumer acceptance to drive long-term growth.

Value Chain

Global Plant-Based Meat Market: Value Chain & Market Dynamics

Executive Framing

The Global Plant-Based Meat Market operates within a sustainability-driven, innovation-led, and consumer-centric value chain, fueled by rising demand for alternative protein sources. The market is transitioning from niche vegan offerings to mainstream protein solutions, supported by health awareness, environmental concerns, and evolving dietary preferences.

A hybrid operational model enables large players to scale production while startups drive innovation, clean-label development, and direct-to-consumer engagement.

Current Market Reality

The market exhibits high supply chain complexity, driven by multi-stage processing, ingredient sourcing, and global distribution networks. Companies leverage advanced protein technologies, cold-chain logistics, and omnichannel retail strategies to ensure product quality and accessibility.

Distribution spans retail, foodservice, and e-commerce platforms, supporting both mass-market penetration and premium product positioning.

Key Signals and Evidence

- Market growth from USD 8.7 billion (2025) to USD 15.4 billion (2033) at ~8.0% CAGR.

- Rising adoption of flexitarian and plant-forward diets.

- Expansion of QSR and foodservice plant-based menus.

- Innovation in clean-label, high-protein, and fermented ingredients.

- Growth in e-commerce and direct-to-consumer channels.

Strategic Implications

Market leaders are focusing on product innovation, supply chain scaling, and global expansion. Investments in R&D, fermentation technology, and texture optimization are enhancing product realism and consumer acceptance.

Emerging brands differentiate through premium positioning, sustainability claims, and digital-first strategies, targeting niche consumer segments and building brand loyalty.

Forward Outlook

The market is expected to evolve into a core pillar of the global protein ecosystem, driven by sustainability mandates and technological advancements.

- Expansion of functional and fortified plant-based meat products

- Growth in foodservice and ready-to-eat applications

- Adoption of AI-driven supply chain and production optimization

- Increased focus on sustainable sourcing and clean-label innovation

Companies integrating innovation, scalability, and omnichannel distribution will secure long-term competitive advantage.

Investment Activity

Investment & Funding Dynamics ??? Global Plant-Based Meat Market

Executive Framing

Current Market Reality

Valued at USD 8.7 billion in 2025 and projected to reach USD 15.4 billion by 2033 (CAGR ~8.0%), the market is led by North America, with Asia-Pacific emerging as the fastest-growing region. Major players such as Beyond Meat, Impossible Foods, Nestl??, and Tyson Foods are heavily investing in clean-label formulations, high-protein innovations, and large-scale production capabilities to meet rising global demand.

Key Signals and Evidence

- Product Innovation & R&D Investment: Development of next-generation plant-based meats with improved taste, texture, and nutritional profiles.

- Manufacturing & Capacity Expansion: Investments in large-scale production facilities and supply chain optimization.

- Clean-Label & Functional Ingredients: Focus on natural, high-protein, and minimally processed formulations.

- Foodservice & QSR Partnerships: Strategic collaborations with restaurants, fast-food chains, and hospitality sectors.

- Retail & E-Commerce Expansion: Increased penetration across supermarkets, online platforms, and direct-to-consumer channels.

- M&A & Strategic Investments: Ongoing acquisitions, partnerships, and venture funding in alternative protein startups.

- Technology Integration: Adoption of extrusion technology, fermentation, and AI-driven supply chain optimization.

Strategic Implications

Companies focusing on scalable production, clean-label innovation, and strong distribution networks are best positioned to capture long-term growth. Investors are prioritizing firms with advanced R&D capabilities, global expansion strategies, and alignment with sustainability and health-driven consumer trends.

Forward Outlook

Between 2026 and 2033, investment activity is expected to remain strong, focusing on next-generation protein technologies, product diversification, and supply chain scalability. Growth will be driven by increasing global demand, foodservice integration, and continued innovation in plant-based formulations.

Technology & Innovation

Global Plant-Based Meat Market: Technology & Innovation

Executive Framing

The Global Plant-Based Meat Market is rapidly evolving, driven by the convergence of food technology, sustainability goals, and shifting consumer dietary preferences. Innovation is centered on improving taste, texture, and nutritional value through advanced protein processing, clean-label formulations, and alternative protein sources. As demand for sustainable and high-protein foods rises, plant-based meat is transitioning into a mainstream global protein solution.

Current Market Reality

The market was valued at USD 8.7 billion in 2025 and is projected to reach USD 15.4 billion by 2033, growing at a CAGR of ~8.0%. North America leads due to strong consumer awareness and established retail infrastructure, while Asia-Pacific is the fastest-growing region driven by urbanization and rising disposable incomes. The market is witnessing strong traction in burger patties, nuggets, and ready-to-cook formats, supported by expanding retail and foodservice channels.

Key Signals and Evidence

- Advanced Processing Technologies: High-moisture extrusion and protein structuring techniques improve meat-like texture and sensory experience.

- Clean-Label & Functional Innovation: Use of natural ingredients, high-protein formulations, and fortified nutrients to meet health-conscious demand.

- Fermentation & Novel Proteins: Development of mycoprotein, precision fermentation, and hybrid protein systems for enhanced nutrition and scalability.

- Foodservice & QSR Expansion: Increasing adoption across quick-service restaurants and global food chains accelerates market penetration.

- Sustainable Supply Chains: Focus on reducing carbon footprint, water usage, and resource intensity compared to traditional meat production.

Strategic Implications

Companies investing in R&D, scalable production technologies, and clean-label innovation will gain a competitive advantage. Strategic partnerships with foodservice chains and retailers enhance market reach, while supply chain optimization improves cost efficiency. Brands that successfully balance taste, nutrition, affordability, and sustainability will capture a larger share of the growing flexitarian and health-conscious consumer base.

Forward Outlook

The market is expected to witness continued innovation through 2033, with a focus on next-generation plant proteins, fermentation-based solutions, and AI-driven product development. Expansion into emerging markets, increased foodservice integration, and advancements in texture and flavor realism will further accelerate adoption. Plant-based meat is set to become a core pillar of the global sustainable protein ecosystem.

Market Risk

Risk Factors and Disruption Threats in the Global Plant-Based Meat Market

Executive Framing

The Global Plant-Based Meat Market is projected to grow from USD 8.7 Billion in 2025 to USD 15.4 Billion by 2033, at a CAGR of ~8.0%. Growth is driven by rising health awareness, sustainability concerns, and increasing demand for alternative protein sources. The market is transitioning from niche adoption to mainstream consumption, supported by continuous product innovation, improved taste and texture, and expanding global distribution networks.

Current Market Reality

North America leads the market due to early adoption, strong brand presence, and advanced retail and foodservice infrastructure. Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and increasing awareness of plant-based diets. Burger patties dominate the product segment, while nuggets, sausages, and ready-to-cook formats are gaining traction across retail and quick-service restaurant channels.

Key Signals and Evidence

Key signals include increasing investments in plant-based innovation, expansion of clean-label and high-protein formulations, and growing partnerships with foodservice chains. Technological advancements such as high-moisture extrusion, fermentation-based proteins, and hybrid formulations are enhancing product quality. Consumer trends show a shift toward flexitarian diets, sustainability-driven purchasing, and demand for convenient, ready-to-eat plant-based meals.

Strategic Implications

Companies should focus on product differentiation through taste, texture, and nutritional value while maintaining clean-label positioning. Investments in supply chain scalability, cost optimization, and sustainable sourcing are critical for long-term competitiveness. Expanding presence in emerging markets, strengthening foodservice partnerships, and leveraging digital retail channels will be essential to capture growing consumer demand.

Forward Outlook

The Global Plant-Based Meat Market is expected to continue strong growth as consumer preferences shift toward sustainable and functional protein alternatives. Future expansion will be driven by innovation in next-generation proteins, wider adoption across emerging markets, and increased integration into mainstream diets. Companies that align with sustainability goals, invest in R&D, and scale production efficiently will secure long-term market leadership.

Regulatory Landscape

Regulatory & Policy Landscape: Global Plant-Based Meat Market

Executive Framing

The Global Plant-Based Meat Market operates within a structured and evolving regulatory framework governed by food safety authorities such as the U.S. Food and Drug Administration (FDA), European Food Safety Authority (EFSA), Food Safety and Standards Authority of India (FSSAI), and other regional regulatory bodies. Plant-based meat products???including burger patties, sausages, nuggets, and seafood alternatives???must comply with food safety, ingredient approval, labeling, and packaging regulations.

Emerging product innovations such as high-protein formulations, clean-label products, fermentation-based proteins, and hybrid plant-based meats are subject to increasing regulatory scrutiny. Claims such as ???vegan,??? ???plant-based,??? ???non-GMO,??? ???high-protein,??? and ???sustainable??? require verification and certification to ensure compliance and prevent misleading consumers.

Current Market Reality

The regulatory environment for plant-based meat is moderately complex, with increasing standardization across developed markets such as North America and Europe. These regions enforce strict labeling, allergen disclosure, and food safety standards, particularly regarding protein sources like soy, pea, and wheat.

Asia-Pacific represents a diverse regulatory landscape, where countries such as China, India, and Japan are actively evolving policies for plant-based food classification, import regulations, and labeling requirements. Additionally, the use of terms like ???meat,??? ???burger,??? or ???sausage??? for plant-based products remains a subject of regulatory debate in several regions, adding complexity for global brands.

Key Signals and Evidence

- Mandatory food safety and hygiene compliance across all plant-based meat products.

- Strict labeling requirements including ingredient disclosure and allergen warnings (soy, gluten, etc.).

- Regulations governing the use of ???meat-related??? terminology for plant-based alternatives.

- Certification requirements for vegan, non-GMO, organic, and clean-label claims.

- Increasing scrutiny on protein content, nutritional claims, and functional ingredients.

- Emerging policies supporting sustainable sourcing and eco-friendly packaging.

Strategic Implications

Regulatory compliance is essential for product approval, market entry, and brand credibility in the plant-based meat sector. Companies must invest in ingredient validation, certification processes, and transparent labeling to meet multi-region regulatory standards.

Brands that proactively address regulatory challenges???such as labeling restrictions, health claim substantiation, and sustainability compliance???can enhance consumer trust and strengthen their competitive positioning. Alignment with global food safety standards also facilitates cross-border expansion and scalability.

Forward Outlook

The regulatory landscape is expected to evolve with clearer definitions for plant-based meat products, stricter labeling guidelines, and enhanced oversight of health and sustainability claims. Governments are likely to introduce more detailed frameworks around alternative proteins, including fermentation-based and hybrid products.

Digital traceability, AI-driven compliance systems, and standardized global certifications will play a growing role in ensuring regulatory adherence. Companies that invest in compliance infrastructure and adapt to evolving policies will be well-positioned for long-term growth.