Global Premium Wine Market Report Analysis , Size and Forecast 2026-2033

Global Premium Wine Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

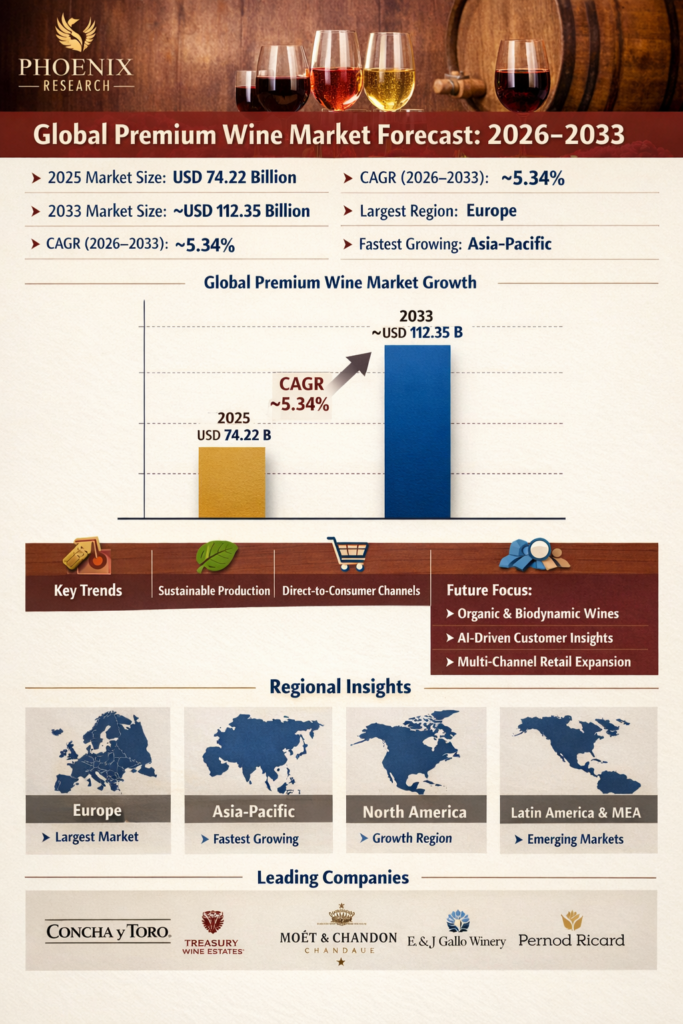

| 2025 Market Size | USD 74.22 Billion |

| 2033 Market Size | ~USD 112.35 Billion |

| CAGR (2026–2033) | ~5.34% |

| Largest Region | Europe |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Red & Sparkling Wines |

| Key Trend | Premiumization, Sustainable Production & Direct-to-Consumer Channels |

| Future Focus | Organic & Biodynamic Wines, AI-Driven Customer Insights, Multi-Channel Retail Expansion |

Global Premium Wine Market Overview

The Global Premium Wine Market includes high-quality red, white, rosé, and sparkling wines, sold across retail, e-commerce, direct-to-consumer channels, fine-dining restaurants, wine clubs, and exclusive tasting experiences.

Premium wine consumption is driven by rising disposable income, growing wine culture in emerging markets, increased interest in wine pairing with gourmet cuisine, and the convenience of online and subscription-based wine platforms.

According to Pheonix Research, the Global Premium Wine Market was valued at USD 74.22 billion in 2025 and is projected to reach approximately USD 112.35 billion by 2033, registering a CAGR of ~5.34% during 2026–2033.

Europe dominates the market, supported by established wine-producing countries like France, Italy, and Spain. Asia-Pacific is the fastest-growing region due to rising wine consumption in China, India, and Southeast Asia, fueled by urbanization, premium lifestyle trends, and tourism.

The Post-2025 outlook emphasizes premiumization, sustainable viticulture practices, AI-powered marketing and inventory management, expansion of direct-to-consumer channels, and experiential wine tourism as key growth drivers.

Key Drivers of Global Premium Wine Market Growth

1. Premiumization and Evolving Consumer Preferences

Global consumers are increasingly gravitating toward fine, aged, and limited-edition wines. The growing interest in wine pairing with gourmet cuisine and immersive tasting experiences is fueling demand for premium offerings worldwide.

2. Growth of Direct-to-Consumer and Online Channels

E-commerce platforms, subscription-based services, and winery-direct sales are expanding accessibility to premium wines. These channels enable higher margins, personalized experiences, and seamless delivery, driving adoption across diverse markets.

3. Rise of Sustainable and Organic Wine Production

Heightened health consciousness and environmental awareness are boosting demand for organic, biodynamic, and low-sulfite wines. Sustainable production practices enhance brand reputation, foster consumer trust, and strengthen long-term loyalty.

4. Expansion in Emerging Markets and Tourism-Driven Growth

Rapidly developing wine cultures in Asia-Pacific, Latin America, and the Middle East are accelerating consumption. Urbanization, rising disposable incomes, and tourism-driven demand are key factors driving market expansion in these regions.

5. Influence of Celebrity and Sommelier Endorsements

Collaborations with renowned chefs, sommeliers, and celebrities elevate the perception of exclusivity and quality. Such endorsements increase brand visibility, enhance prestige, and attract high-end consumer segments globally.

Global Premium Wine Market Segmentation

1. By Wine Type

1.1 Red Wine

1.1.1 Cabernet Sauvignon

1.1.1.1 Single Vineyard Cabernet

1.1.1.2 Blended Cabernet

1.1.1.3 Aged Barrel Cabernet

1.1.2 Merlot

1.1.2.1 Classic Merlot

1.1.2.2 Reserve / Estate Merlot

1.1.2.3 Blended Merlot Wines

1.1.3 Pinot Noir

1.1.3.1 Old World Pinot Noir

1.1.3.2 New World Pinot Noir

1.1.3.3 Premium Pinot Noir Blends

1.1.4 Syrah / Shiraz

1.1.4.1 Syrah Single Vineyard

1.1.4.2 Shiraz Reserve

1.1.4.3 Syrah Blends

1.1.5 Blends & Other Premium Reds

1.1.5.1 Bordeaux Blends

1.1.5.2 Rhône Blends

1.1.5.3 Other Regional Blends

1.2 White Wine

1.2.1 Chardonnay

1.2.1.1 Oaked Chardonnay

1.2.1.2 Unoaked Chardonnay

1.2.1.3 Reserve / Estate Chardonnay

1.2.2 Sauvignon Blanc

1.2.2.1 Classic Sauvignon Blanc

1.2.2.2 Premium Single Vineyard

1.2.2.3 Blended Sauvignon Blanc

1.2.3 Riesling

1.2.3.1 Dry Riesling

1.2.3.2 Semi-Sweet Riesling

1.2.3.3 Ice Wine Riesling

1.2.4 Pinot Grigio

1.2.4.1 Italian Pinot Grigio

1.2.4.2 New World Pinot Grigio

1.2.4.3 Premium Pinot Grigio Blends

1.2.5 Premium White Blends

1.2.5.1 Chardonnay + Sauvignon Blanc Blends

1.2.5.2 Other White Regional Blends

1.2.5.3 Estate / Reserve White Blends

1.3 Rosé Wine

1.3.1 Light Rosé

1.3.1.1 Provence Style

1.3.1.2 Dry Rosé

1.3.1.3 Summer Blend Rosé

1.3.2 Premium Blush Rosé

1.3.2.1 Reserve Rosé

1.3.2.2 Barrel-Aged Blush Rosé

1.3.2.3 Limited Edition Rosé

1.3.3 Sparkling Rosé

1.3.3.1 Classic Sparkling Rosé

1.3.3.2 Brut Rosé

1.3.3.3 Vintage Sparkling Rosé

1.4 Sparkling & Champagne

1.4.1 Classic Champagne

1.4.1.1 Non-Vintage Champagne

1.4.1.2 Vintage Champagne

1.4.1.3 Prestige Cuvée

1.4.2 Prosecco

1.4.2.1 DOCG Prosecco

1.4.2.2 Spumante Prosecco

1.4.2.3 Rosé Prosecco

1.4.3 Cava

1.4.3.1 Traditional Cava

1.4.3.2 Reserve Cava

1.4.3.3 Limited Edition Cava

1.4.4 Premium Sparkling Varietals

1.4.4.1 Blanc de Blancs

1.4.4.2 Blanc de Noirs

1.4.4.3 Luxury Vintage Sparkling

1.5 Fortified & Dessert Wines

1.5.1 Port & Sherry

1.5.1.1 Tawny Port

1.5.1.2 Ruby Port

1.5.1.3 Sherry Fino / Oloroso

1.5.2 Late Harvest Wines

1.5.2.1 Single Vineyard Late Harvest

1.5.2.2 Blended Late Harvest Wines

1.5.2.3 Ice Wine Varieties

1.5.3 Ice Wine

1.5.3.1 Riesling Ice Wine

1.5.3.2 Vidal Ice Wine

1.5.3.3 Limited Edition Ice Wines

1.5.4 Vermouth & Specialty Dessert Wines

1.5.4.1 Sweet Vermouth

1.5.4.2 Dry Vermouth

1.5.4.3 Dessert Wine Blends

2. By Distribution Channel

2.1 On-Trade / Hospitality

2.1.1 Fine Dining Restaurants

2.1.1.1 Michelin-Star Wine Lists

2.1.1.2 Sommelier-Selected Wines

2.1.1.3 Wine Pairing Experiences

2.1.2 Hotel & Resort Wine Bars

2.1.2.1 Resort Exclusive Labels

2.1.2.2 Signature Wine Menus

2.1.2.3 Wine Tastings & Events

2.1.3 Wine Tasting Rooms & Vineyards

2.1.3.1 Estate Tasting Rooms

2.1.3.2 Vineyard Tours

2.1.3.3 VIP Wine Clubs

2.2 Off-Trade / Retail

2.2.1 Supermarkets & Hypermarkets

2.2.1.1 Premium Shelf Wines

2.2.1.2 Limited Edition Packs

2.2.1.3 Promotional Wines

2.2.2 Specialty Wine Stores

2.2.2.1 Boutique Wine Shops

2.2.2.2 Sommelier Curated Wines

2.2.2.3 Rare & Collectible Wines

2.2.3 Duty-Free & Travel Retail

2.2.3.1 Airport Exclusive Wines

2.2.3.2 Travel Retail Limited Editions

2.2.3.3 Gift & Collector Packs

2.3 Direct-to-Consumer (DTC)

2.3.1 Winery Membership Programs

2.3.1.1 Subscription-Based Wine Clubs

2.3.1.2 VIP Tasting Memberships

2.3.1.3 Estate Limited Releases

2.3.2 Online Wine Clubs & Subscriptions

2.3.2.1 Personalized Wine Boxes

2.3.2.2 Curated Tasting Selections

2.3.2.3 Seasonal Wine Collections

2.3.3 App-Based Wine Retail & Delivery

2.3.3.1 Direct Winery-to-Consumer Apps

2.3.3.2 Third-Party Wine Delivery Apps

2.3.3.3 Subscription-Based App Delivery

2.4 E-Commerce

2.4.1 Third-Party Platforms

2.4.1.1 Online Retailers & Marketplaces

2.4.1.2 Subscription Platforms

2.4.1.3 Premium Wine Aggregators

2.4.2 Brand-Owned E-Stores

2.4.2.1 Direct Wine Sales Portals

2.4.2.2 Limited Edition Online Releases

2.4.2.3 Loyalty Member Exclusive Sales

2.4.3 Marketplace & Aggregator Channels

2.4.3.1 Wine Auction Platforms

2.4.3.2 Global Wine Marketplaces

2.4.3.3 Influencer-Endorsed Wine Drops

3. By End-User

3.1 Individual Consumers

3.1.1 Millennials & Gen Z Wine Enthusiasts

3.1.1.1 Urban Professionals

3.1.1.2 Social Media-Focused Consumers

3.1.1.3 Experience-Oriented Wine Drinkers

3.1.2 Urban Professionals & Affluent Consumers

3.1.2.1 Corporate Entertaining

3.1.2.2 Home Wine Cellars

3.1.2.3 Fine Dining Occasions

3.1.3 Wine Collectors & Connoisseurs

3.1.3.1 Investment-Grade Wines

3.1.3.2 Rare & Vintage Collections

3.1.3.3 Auction Participation

3.2 Corporate & Institutional

3.2.1 Corporate Gifting & Hospitality

3.2.1.1 Executive Gift Packages

3.2.1.2 Corporate Wine Tastings

3.2.1.3 Event Hosting & Sponsorship

3.2.2 Event & Conference Wine Services

3.2.2.1 Banquet & Catering Wines

3.2.2.2 Wine Pairing Experiences

3.2.2.3 Premium Wine Rentals & Bars

3.2.3 Hotel & Restaurant Procurement

3.2.3.1 Fine Dining Restaurants

3.2.3.2 Luxury Resorts & Hotels

3.2.3.3 Specialty Wine Bars

4.by Region

1. Europe – Largest Market

2. Asia-Pacific – Fastest Growing Region

3. North America

4. Latin America

5. Middle East & Africa

Regional Insights of Global Premium Wine Market

Europe – Largest Market

Europe continues to dominate premium wine consumption, driven by historical vineyards, strong export networks, and consumer appreciation for aged, high-quality wines. France, Italy, and Spain lead production, while urban centers across Germany, the UK, and Scandinavia drive on-trade demand.

Asia-Pacific – Fastest Growing Region

China, Japan, South Korea, and India are experiencing surging demand for premium wines, fueled by rising disposable incomes, expanding wine culture, and online wine retail. Urban professional segments and wine clubs are key growth drivers.

North America

The U.S. and Canada represent significant growth markets, with increased adoption of Napa and Sonoma wines, sparkling varieties, and subscription-based wine services. Premiumization, wine tourism, and food pairing culture support revenue expansion.

Latin America

Brazil, Mexico, and Chile show rising adoption of imported wines, wine tourism, and premium lifestyle products. Growth is concentrated in major cities and affluent consumer segments.

Middle East & Africa

Premium wine growth is concentrated in urban hubs such as Dubai, Johannesburg, and Riyadh, driven by luxury hospitality, tourism, and high-net-worth consumer spending.

Leading Companies in the Global Premium Wine Market

-

Pernod Ricard (Jacob’s Creek, Mumm)

-

Domaine de la Romanée-Conti

-

Moët & Chandon

-

Champagne Louis Roederer

-

Vega Sicilia

-

Penfolds

-

Torres

The market is highly fragmented, with both global conglomerates and boutique vineyard operators competing for premium positioning.E. & J. Gallo Winery is the largest company among the listed wine producers.

Why the Global Premium Wine Market Remains Critical

-

Rising global interest in fine wines and wine culture ensures steady demand.

-

AI-based customer segmentation, demand forecasting, and inventory management enhance operational efficiency.

-

Direct-to-consumer channels and subscription models improve margin and customer loyalty.

-

Sustainable viticulture and organic certification strengthen brand positioning.

-

Multi-channel presence (retail, hospitality, online) enables market scalability.

Strategic Intelligence and AI-Backed Insights – Global Premium Wine Market

- Pheonix Demand Forecast Engine: Steady growth supported by premiumization, emerging markets adoption, and online wine retail expansion.

- Consumer Behavior Analyzer: Rising preference for organic, biodynamic, and exclusive aged wines; emphasis on wine education, tasting experiences, and authenticity.

- Innovation Tracker: Automation in wine production, AI-powered vineyard monitoring, smart logistics, personalized recommendations, and loyalty-based engagement are key differentiators.

- Porter’s Five Forces Analysis: High rivalry due to fragmented boutique and global brands; moderate supplier power for premium grapes; differentiation through authenticity, origin, and sustainable practices.

Final Takeaway of Global Premium Wine Market

The Global Premium Wine Market is steadily evolving into a premium-driven, experience-oriented, and technology-enabled beverage ecosystem. The projected CAGR of ~5.34% during 2026–2033 reflects stable growth supported by rising global demand for aged and limited-edition wines, sparkling and Champagne offerings, and health-conscious, sustainably produced varietals.

Growth will be defined by a dual-engine model:

- High-margin experiential segments, including aged reds, Champagne, limited editions, wine tourism, curated tastings, and exclusive cellar offerings.

- Scalable retail and direct-to-consumer (DTC) formats, including e-commerce delivery, online wine subscriptions, and winery membership programs.

This balanced structure enables both premium positioning and broad market accessibility. Operators that successfully integrate AI-driven customer insights, enhance sustainable vineyard practices, expand international direct-to-consumer rollouts, and strengthen omnichannel distribution (retail, on-trade, DTC, and online) will be best positioned for sustainable long-term value creation.

At Pheonix Research, our advanced forecasting models provide in-depth Global Premium Wine Market revenue forecasts, competitive benchmarking, and strategic intelligence — enabling stakeholders to capitalize on the post-2025 market outlook with data-backed precision and actionable growth strategies.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7430468268567736320

X : https://x.com/Pheonix_Insight/status/2024707980361699547?s=20

Table of Contents

1. Executive Summary

1.1 Global Market Snapshot (2025–2033)

1.2 Key Growth Highlights & Strategic Insights

1.3 Largest and Fastest-Growing Regions

1.4 Dominant and Emerging Market Segments

1.5 High-Potential Opportunity Areas

2. Global Premium Wine Market Overview

2.1 Market Definition and Scope

2.2 Evolution of the Global Premium Wine Industry

2.3 Value Chain & Supply Ecosystem

2.4 Business Models (Retail, DTC, Hospitality, Wine Clubs)

2.5 Pricing Analysis and Premium Tier Strategies

2.6 Regulatory Landscape and Quality Certifications

3. Market Forecast Snapshot (2026–2033)

3.1 Market Size 2025: USD 74.22 Billion

3.2 Market Size 2033: ~USD 112.35 Billion

3.3 CAGR (2026–2033): ~5.34%

3.4 Largest Region: Europe

3.5 Fastest-Growing Region: Asia-Pacific

3.6 Top Segments: Red Wine & Sparkling Wine

3.7 Key Trend: Premiumization, Sustainable Production & DTC Channels

3.8 Future Focus: Organic & Biodynamic Wines, AI-Driven Insights, Multi-Channel Retail Expansion

4. Market Dynamics

4.1 Key Growth Drivers

4.2 Market Restraints and Barriers

4.3 Emerging Opportunities

4.4 Industry Challenges

4.5 Macroeconomic and Trade Impact

5. Market Segmentation by Wine Type (USD Billion), 2026–2033

5.1 Red Wine

5.1.1 Cabernet Sauvignon

5.1.1.1 Single Vineyard Cabernet

5.1.1.2 Blended Cabernet

5.1.1.3 Aged Barrel Cabernet

5.1.2 Merlot

5.1.2.1 Classic Merlot

5.1.2.2 Reserve / Estate Merlot

5.1.2.3 Blended Merlot

5.1.3 Pinot Noir

5.1.3.1 Old World Pinot Noir

5.1.3.2 New World Pinot Noir

5.1.3.3 Premium Pinot Noir Blends

5.1.4 Syrah / Shiraz

5.1.4.1 Syrah Single Vineyard

5.1.4.2 Shiraz Reserve

5.1.4.3 Syrah Blends

5.1.5 Blends & Other Premium Reds

5.1.5.1 Bordeaux Blends

5.1.5.2 Rhône Blends

5.1.5.3 Other Regional Blends

5.2 White Wine

5.2.1 Chardonnay

5.2.1.1 Oaked Chardonnay

5.2.1.2 Unoaked Chardonnay

5.2.1.3 Reserve / Estate Chardonnay

5.2.2 Sauvignon Blanc

5.2.2.1 Classic Sauvignon Blanc

5.2.2.2 Premium Single Vineyard

5.2.2.3 Blended Sauvignon Blanc

5.2.3 Riesling

5.2.3.1 Dry Riesling

5.2.3.2 Semi-Sweet Riesling

5.2.3.3 Ice Wine Riesling

5.2.4 Pinot Grigio

5.2.4.1 Italian Pinot Grigio

5.2.4.2 New World Pinot Grigio

5.2.4.3 Premium Pinot Grigio Blends

5.2.5 Premium White Blends

5.2.5.1 Chardonnay + Sauvignon Blanc Blends

5.2.5.2 Other Regional White Blends

5.2.5.3 Estate / Reserve Blends

5.3 Rosé Wine

5.3.1 Light Rosé

5.3.1.1 Provence Style

5.3.1.2 Dry Rosé

5.3.1.3 Summer Blend

5.3.2 Premium Blush Rosé

5.3.2.1 Reserve Rosé

5.3.2.2 Barrel-Aged Blush Rosé

5.3.2.3 Limited Edition

5.3.3 Sparkling Rosé

5.3.3.1 Classic Sparkling Rosé

5.3.3.2 Brut Rosé

5.3.3.3 Vintage Sparkling

5.4 Sparkling & Champagne

5.4.1 Classic Champagne

5.4.1.1 Non-Vintage Champagne

5.4.1.2 Vintage Champagne

5.4.1.3 Prestige Cuvée

5.4.2 Prosecco

5.4.2.1 DOCG Prosecco

5.4.2.2 Spumante Prosecco

5.4.2.3 Rosé Prosecco

5.4.3 Cava

5.4.3.1 Traditional Cava

5.4.3.2 Reserve Cava

5.4.3.3 Limited Edition

5.4.4 Premium Sparkling Varietals

5.4.4.1 Blanc de Blancs

5.4.4.2 Blanc de Noirs

5.4.4.3 Luxury Vintage

5.5 Fortified & Dessert Wines

5.5.1 Port & Sherry

5.5.1.1 Tawny Port

5.5.1.2 Ruby Port

5.5.1.3 Sherry Fino / Oloroso

5.5.2 Late Harvest Wines

5.5.2.1 Single Vineyard

5.5.2.2 Blended Late Harvest

5.5.2.3 Ice Wine Varieties

5.5.3 Ice Wine

5.5.3.1 Riesling Ice Wine

5.5.3.2 Vidal Ice Wine

5.5.3.3 Limited Edition Ice Wines

5.5.4 Vermouth & Specialty Dessert Wines

5.5.4.1 Sweet Vermouth

5.5.4.2 Dry Vermouth

5.5.4.3 Dessert Wine Blends

6. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

6.1 On-Trade / Hospitality

6.1.1 Fine Dining Restaurants (Michelin, Sommelier, Wine Pairings)

6.1.2 Hotels & Resort Wine Bars

6.1.3 Wine Tasting Rooms & Vineyards

6.2 Off-Trade / Retail

6.2.1 Supermarkets & Hypermarkets

6.2.2 Specialty Wine Stores

6.2.3 Duty-Free & Travel Retail

6.3 Direct-to-Consumer (DTC)

6.3.1 Winery Membership Programs

6.3.2 Online Wine Clubs & Subscriptions

6.3.3 App-Based Wine Retail & Delivery

6.4 E-Commerce

6.4.1 Third-Party Platforms

6.4.2 Brand-Owned E-Stores

6.4.3 Marketplace & Aggregator Channels

7. Market Segmentation by End User (USD Billion), 2026–2033

7.1 Individual Consumers

7.1.1 Millennials & Gen Z Wine Enthusiasts

7.1.1.1 Urban Professionals

7.1.1.2 Social Media-Focused Consumers

7.1.1.3 Experience-Oriented Wine Drinkers

7.1.2 Urban Professionals & Affluent Consumers

7.1.2.1 Corporate Entertaining

7.1.2.2 Home Wine Cellars

7.1.2.3 Fine Dining Occasions

7.1.3 Wine Collectors & Connoisseurs

7.1.3.1 Investment-Grade Wines

7.1.3.2 Rare & Vintage Collections

7.1.3.3 Auction Participation

7.2 Corporate & Institutional

7.2.1 Corporate Gifting & Hospitality

7.2.1.1 Executive Gift Packages

7.2.1.2 Corporate Wine Tastings

7.2.1.3 Event Sponsorship & Brand Collaborations

7.2.2 Event & Conference Wine Services

7.2.2.1 Banquet & Catering Wines

7.2.2.2 Wine Pairing Experiences

7.2.2.3 Premium Wine Rentals & Bars

7.2.3 Hotel & Restaurant Procurement

7.2.3.1 Fine Dining Restaurants

7.2.3.2 Luxury Resorts & Hotels

7.2.3.3 Specialty Wine Bars & Lounges

8. Market Segmentation by Region (USD Billion), 2026–2033

8.1 Europe – Largest Market

8.2 Asia-Pacific – Fastest Growing Region

8.3 North America

8.4 Latin America

8.5 Middle East & Africa

9. Regional Insights

9.1 Europe – Heritage Vineyards & Export Leadership

9.2 Asia-Pacific – Rapid Adoption & Urban Growth

9.3 North America – Napa, Sonoma & Subscription Trends

9.4 Latin America – Emerging Consumption & Wine Tourism

9.5 Middle East & Africa – Premium Lifestyle & Hospitality

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Positioning Matrix

10.3 Mergers, Acquisitions & Strategic Alliances

10.4 Product Launches & Innovation Trends

11. Leading Company Profiles

11.1 Concha y Toro

11.2 Treasury Wine Estates

11.3 Pernod Ricard (Jacob’s Creek, Mumm)

11.4 E. & J. Gallo Winery

11.5 Domaine de la Romanée-Conti

11.6 Moët & Chandon

11.7 Champagne Louis Roederer

11.8 Vega Sicilia

11.9 Penfolds

11.10 Torres

12. Strategic Intelligence & AI-Backed Insights

12.1 AI-Driven Customer Segmentation & Insights

12.2 Demand Forecasting & Market Modeling

12.3 Innovation Tracker: Smart Vineyards & Logistics

12.4 Sustainability & Organic Certification Trends

12.5 Porter’s Five Forces Analysis

12.6 Investment & Expansion Strategy Outlook

13. Why the Global Premium Wine Market Remains Critical

13.1 Rising Global Wine Culture

13.2 Direct-to-Consumer & Subscription Scalability

13.3 Sustainable Viticulture & Brand Differentiation

13.4 Multi-Channel Retail Expansion

14. Appendix

15. About Us

16. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Premium Wine Market

Executive Framing

The Global Premium Wine Market is characterized by high competitive intensity and a fragmented market structure, where heritage-driven European wineries, global beverage conglomerates, and boutique vineyard operators coexist. The market is deeply influenced by brand legacy, terroir authenticity, and premium positioning, making differentiation highly dependent on origin, quality, and storytelling. As consumer preferences shift toward experiential luxury, sustainability, and curated wine experiences, competitive dynamics are increasingly shaped by innovation in direct-to-consumer models, sustainable viticulture, and digital engagement strategies.

Current Market Reality

The premium wine market remains highly fragmented, with no single company holding dominant global control. Leading players such as E. & J. Gallo Winery, Treasury Wine Estates, Pernod Ricard, and Concha y Toro operate alongside prestigious boutique wineries like Domaine de la Romanée-Conti and Champagne Louis Roederer. This creates a dual-structure ecosystem where large-scale distribution capabilities coexist with niche, high-value artisanal production.

Europe continues to dominate production and consumption, driven by legacy wine regions such as France, Italy, and Spain, while Asia-Pacific is emerging as a high-growth consumption hub. Direct-to-consumer (DTC) channels, wine clubs, and online platforms are rapidly transforming distribution, enabling wineries to engage directly with consumers and improve margins. Meanwhile, sustainability initiatives such as organic and biodynamic farming are becoming critical differentiators in premium wine positioning.

Key Signals and Evidence

Several key signals highlight the evolving competitive dynamics in the premium wine market:

- Rising demand for organic, biodynamic, and sustainably produced wines reflecting growing environmental and health awareness.

- Expansion of direct-to-consumer (DTC) models, including wine clubs, subscriptions, and winery memberships.

- Increasing investment in AI-driven customer insights, inventory management, and personalized wine recommendations.

- Growth in experiential consumption, including wine tourism, vineyard tours, and curated tasting experiences.

- Strong premiumization trend with increased demand for aged, limited-edition, and luxury wine offerings.

Strategic Implications

Market participants must adopt a balanced strategy that integrates heritage, innovation, and consumer engagement:

- Premium Differentiation: Emphasizing origin, vintage quality, and exclusivity to maintain premium positioning.

- DTC & Omnichannel Expansion: Strengthening direct sales channels, subscriptions, and e-commerce platforms.

- Sustainability Leadership: Investing in organic, biodynamic, and eco-friendly production practices.

- Experiential Marketing: Leveraging wine tourism, tasting events, and sommelier collaborations to enhance brand value.

- Technology Integration: Utilizing AI for demand forecasting, vineyard monitoring, and personalized customer engagement.

Forward Outlook

By 2033, the Global Premium Wine Market is projected to reach approximately USD 112.35 billion, growing at a CAGR of ~5.34%. Europe will remain the largest market due to its strong production base and heritage, while Asia-Pacific will continue to be the fastest-growing region, driven by rising disposable incomes and evolving wine culture.

The market will evolve through a dual-engine growth model: high-margin experiential and luxury segments, including aged wines, Champagne, and exclusive vineyard offerings, alongside scalable DTC and retail-driven distribution channels. Companies that successfully integrate sustainability, digital transformation, and premium storytelling will be best positioned to capture long-term growth in this competitive and evolving landscape.

Value Chain

Global Premium Wine Market: Value Chain & Market Dynamics

Executive Framing

The Global Premium Wine Market operates within a sophisticated and heritage-driven value chain, where quality, origin, aging, and brand storytelling play critical roles. Unlike mass-market beverages, premium wine production is deeply rooted in terroir, viticulture expertise, and time-intensive processes, creating a unique blend of tradition and modern innovation.

The value chain reflects a hybrid structure, combining estate-based wine production with global distribution, retail networks, and direct-to-consumer (DTC) channels. Large wine conglomerates leverage global supply chains and brand portfolios, while boutique wineries focus on exclusivity, craftsmanship, and limited-edition offerings.

However, the market faces challenges in climate variability affecting grape quality, supply constraints of premium vineyards, regulatory compliance across regions, and the need for sustainable viticulture practices. These factors introduce complexity across sourcing, production, and distribution.

Current Market Reality

The premium wine value chain demonstrates moderate complexity, balancing traditional production processes with modern distribution and digital transformation. Leading players such as E. & J. Gallo Winery, Concha y Toro, and Treasury Wine Estates operate integrated models combining vineyard ownership, production facilities, and global distribution networks.

Upstream activities focus on grape cultivation, vineyard management, and harvesting, where quality, climate conditions, and soil characteristics directly influence output. Increasing adoption of organic and biodynamic farming practices adds additional layers of cost and traceability requirements.

Midstream processes include fermentation, aging (often for years in oak barrels), blending, bottling, and quality control. These stages are highly time-sensitive and capital-intensive, particularly for aged and vintage wines.

Downstream distribution spans on-trade (restaurants, hotels, wine bars), off-trade retail (supermarkets, specialty stores), and rapidly growing e-commerce and DTC channels such as wine clubs and winery memberships. Premium wines also rely heavily on experiential channels such as wine tourism, tastings, and auctions.

Despite strong demand, supply limitations, long production cycles, and regulatory constraints across international markets remain key operational challenges.

Key Signals and Evidence

Key indicators shaping the premium wine value chain include:

- Market expansion from USD 74.22 billion (2025) to ~USD 112.35 billion (2033) at a CAGR of ~5.34%, reflecting steady premium demand.

- Strong growth in red and sparkling wines, driven by global consumption trends and celebratory occasions.

- Increasing adoption of organic, biodynamic, and sustainable wine production, reshaping upstream sourcing and vineyard practices.

- Rapid expansion of DTC channels, wine subscriptions, and e-commerce platforms, enhancing margins and consumer engagement.

- Rising demand in Asia-Pacific, requiring localized distribution strategies and premium positioning.

Supplier power is moderate, particularly for high-quality grapes and aging materials, while buyer power is moderate to high due to brand variety and price sensitivity across segments.

Strategic Implications

The premium wine value chain requires balancing heritage-driven production with modern scalability. Large producers benefit from integrated operations and global reach, while smaller wineries leverage exclusivity and storytelling to command premium pricing.

Digital transformation is becoming a key differentiator, with AI-driven demand forecasting, personalized recommendations, and inventory optimization enhancing efficiency and customer engagement. Additionally, sustainable viticulture, eco-friendly packaging, and carbon footprint reduction are critical for long-term competitiveness.

Experiential marketing—including vineyard tourism, tasting events, and sommelier-led experiences—plays a vital role in brand positioning and consumer loyalty within the premium segment.

Forward Outlook

The premium wine market value chain is expected to evolve through a combination of tradition and innovation:

- Expansion of organic and biodynamic wine production aligned with sustainability trends.

- Growth in DTC channels, subscription models, and digital wine platforms.

- Increased investment in AI-driven vineyard management and climate adaptation technologies.

- Rising importance of wine tourism and experiential consumption as revenue drivers.

Companies that can ensure consistent quality, strong brand storytelling, sustainable practices, and omnichannel distribution will secure long-term competitive advantage.

In conclusion, the Global Premium Wine Market is evolving into a premium, experience-driven, and sustainability-focused ecosystem, where value chain excellence, authenticity, and innovation collectively define market leadership.

Investment Activity

Investment & Funding Dynamics – Global Premium Wine Market

Executive Framing

Current Market Reality

The Global Premium Wine Market, valued at USD 74.22 billion in 2025 and projected to reach ~USD 112.35 billion by 2033 (CAGR ~5.34%), is witnessing stable to rising investment activity. Europe remains the dominant region, while Asia-Pacific is the fastest-growing, attracting new capital inflows. Investments are largely directed toward premium vineyard acquisitions, expansion of wine tourism, and strengthening omnichannel distribution including e-commerce and subscription-based wine clubs. Major players such as E. & J. Gallo Winery, Pernod Ricard, and Treasury Wine Estates are actively investing in portfolio expansion, premium branding, and global market penetration.

Key Signals and Evidence

- Premiumization Trend: Rising global demand for aged, limited-edition, and high-quality wines supports sustained capital inflow.

- Sustainable & Organic Production: Investments in biodynamic farming, organic certification, and eco-friendly packaging are increasing.

- DTC & E-Commerce Growth: Expansion of online wine platforms and subscription-based wine clubs is attracting investor attention.

- Wine Tourism & Experiential Consumption: Vineyard tours, tasting experiences, and luxury wine hospitality are key investment areas.

- Emerging Market Expansion: Asia-Pacific markets are driving new investments due to rising disposable incomes and wine adoption.

- M&A Activity: Strategic acquisitions of boutique wineries and premium labels are strengthening brand portfolios.

- Technology Integration: AI-driven vineyard management, demand forecasting, and personalized marketing are gaining traction.

Strategic Implications

Companies focusing on premium quality, sustainable production, and direct consumer engagement are better positioned to attract investment and maintain competitive advantage. Investors are increasingly prioritizing brands with strong heritage, global distribution capabilities, and scalable DTC models. Strategic acquisitions and partnerships enable faster expansion into high-growth regions and enhance portfolio diversification, particularly in premium and sparkling wine categories.

Forward Outlook

From 2026 to 2033, the Global Premium Wine Market is expected to experience steady investment growth. Capital will continue to flow into sustainable vineyard practices, premium product innovation, and digital sales channels. M&A activity will remain active, particularly targeting boutique wineries and emerging premium brands. Investors focusing on AI-driven analytics, wine tourism, and global DTC expansion will capture long-term growth opportunities in this evolving market.

Technology & Innovation

Global Premium Wine Market: Technology & Innovation

Executive Framing

In the global premium wine market, technology and innovation are increasingly shaping production efficiency, product quality, and consumer engagement. While rooted in tradition and terroir, the industry is adopting modern technologies such as AI-driven vineyard management, precision agriculture, and data analytics to enhance yield quality and sustainability. Innovation is also visible in organic and biodynamic wine production, digital marketing strategies, and direct-to-consumer (DTC) platforms. These advancements are essential for maintaining premium positioning, ensuring consistency, and meeting evolving consumer expectations around authenticity, sustainability, and personalization.

Current Market Reality

The current premium wine market reflects a blend of heritage-driven production and modern technological integration. Wineries are increasingly using AI and IoT-based vineyard monitoring systems to optimize irrigation, soil health, and harvest timing. Automation in bottling and quality control ensures consistency at scale. At the same time, digital platforms, wine apps, and subscription-based models are transforming how consumers discover and purchase wines. Sustainability practices, including organic farming, biodynamic cultivation, and eco-friendly packaging, are becoming core differentiators across premium brands.

Key Signals and Evidence

- Precision Viticulture: Adoption of AI, drones, and IoT sensors for vineyard monitoring improves grape quality and yield predictability.

- Sustainable & Organic Innovation: Growth in biodynamic, organic, and low-intervention winemaking aligns with premium consumer demand.

- Digital & DTC Expansion: E-commerce platforms, wine apps, and subscription services enhance accessibility and personalization.

- Smart Production & Automation: Advanced bottling, fermentation control, and quality assurance systems improve efficiency and consistency.

- Data-Driven Consumer Insights: AI-powered analytics support targeted marketing, inventory planning, and customer engagement strategies.

Strategic Implications

For premium wine producers, integrating technology enhances both operational efficiency and brand differentiation. Precision viticulture reduces risks and improves grape quality, while digital channels enable direct consumer relationships and higher margins. Sustainable production practices strengthen brand equity and regulatory compliance. Companies that combine heritage storytelling with modern innovation can better appeal to evolving premium consumers, while also optimizing supply chains and global distribution strategies.

Forward Outlook

The global premium wine market will continue to evolve through a balance of tradition and innovation. Future advancements will focus on AI-driven vineyard optimization, climate-resilient grape cultivation, expansion of organic and biodynamic practices, and enhanced digital consumer engagement. Direct-to-consumer ecosystems and personalized wine experiences will play a critical role in market expansion. Companies that successfully integrate sustainability, technology, and premium storytelling will secure long-term competitive advantage in the post-2026 wine landscape.

Market Risk

Risk Factors and Disruption Threats in the Global Premium Wine Market

Executive Framing

The Global Premium Wine Market represents a mature yet evolving segment within the alcoholic beverages industry, driven by premiumization, experiential consumption, and global wine culture expansion. While the market is projected to grow at a CAGR of ~5.34% from 2026–2033, it faces structural risks related to climate dependency, regulatory complexities, supply variability, and shifting consumer preferences toward alternative premium beverages.

Current Market Reality

Europe dominates the market due to established wine heritage, while Asia-Pacific leads in growth. However, the industry is highly dependent on agricultural conditions, making it vulnerable to climate change, vineyard yield fluctuations, and raw material supply inconsistencies. Additionally, strict alcohol regulations, taxation policies, and cross-border trade barriers create operational challenges for global expansion.

Key Signals and Evidence

Key indicators include rising demand for organic and biodynamic wines, growth in direct-to-consumer and e-commerce channels, and increasing consumer interest in premium and collectible wines. At the same time, substitution from craft spirits, premium beer, and low-alcohol alternatives is intensifying competition. Climate-related disruptions and sustainability pressures are also becoming more evident across major wine-producing regions.

Strategic Implications

Producers must invest in climate-resilient viticulture, sustainable farming practices, and supply chain diversification to mitigate production risks. Expanding DTC channels, leveraging AI-driven consumer insights, and strengthening brand storytelling are critical for maintaining premium positioning. Companies also need to navigate complex regulatory frameworks while optimizing global distribution and pricing strategies.

Forward Outlook

The Global Premium Wine Market is expected to maintain stable growth, supported by premium consumption trends and expanding global wine culture. However, long-term success will depend on managing climate risks, regulatory pressures, and competitive substitution from other premium alcoholic and functional beverage categories.

Regulatory Landscape

Regulatory & Policy Landscape: Global Premium Wine Market

Executive Framing

The Global Premium Wine Market operates within a highly regulated environment shaped by alcohol laws, trade policies, labeling standards, and sustainability mandates. Regulatory oversight is critical due to the nature of alcoholic beverages, requiring strict compliance across production, distribution, marketing, and international trade.

Key regulatory authorities include the European Commission (EU wine regulations), U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB), Food Safety and Standards Authority of India (FSSAI), and similar national bodies worldwide. These institutions govern aspects such as geographical indications (GI), alcohol content labeling, origin certification, import/export duties, and consumer safety.

Premium wines, particularly those linked to protected appellations such as Champagne, Bordeaux, and DOC/DOCG regions, are subject to additional certification and quality control frameworks, reinforcing authenticity and brand value while increasing compliance complexity.

Current Market Reality

Europe maintains the most structured and stringent regulatory framework, with appellation systems (AOC, DOCG, DO) ensuring strict control over grape origin, production methods, and quality standards. These regulations support premium positioning but also limit production flexibility.

In North America, regulatory oversight focuses on labeling, taxation, interstate distribution laws, and direct-to-consumer (DTC) shipping compliance. The U.S. three-tier distribution system adds complexity to market access, although DTC wine sales are expanding with evolving legal frameworks.

Asia-Pacific markets are highly fragmented, with varying import duties, licensing requirements, and labeling standards across countries such as China, India, and Japan. High tariffs and regulatory barriers often impact pricing and accessibility of imported premium wines.

Globally, increasing emphasis on sustainability, organic certification, and environmental compliance is influencing vineyard practices, packaging, and supply chain operations.

Key Signals and Evidence

- Strict geographical indication (GI) and appellation laws protecting origin and authenticity.

- Mandatory alcohol content labeling, health warnings, and ingredient disclosures.

- High excise duties, tariffs, and import/export restrictions across regions.

- Regulation of advertising, promotion, and sponsorship activities.

- Expansion of direct-to-consumer (DTC) wine shipping regulations.

- Growing compliance requirements for organic, biodynamic, and sustainable certifications.

Strategic Implications

Regulatory compliance acts as both a barrier and a value enhancer in the premium wine segment. Appellation and certification frameworks strengthen brand equity and consumer trust but require strict adherence to production standards. Companies must invest in regulatory expertise, traceability systems, and compliance infrastructure to operate efficiently across multiple markets.

High import duties and distribution restrictions in emerging markets can limit penetration but also create opportunities for localized partnerships and regional production strategies. Direct-to-consumer channels offer margin advantages but require compliance with evolving shipping and taxation laws.

Sustainability regulations are increasingly influencing purchasing decisions, making eco-friendly production, organic certification, and transparent sourcing key competitive differentiators.

Forward Outlook

The regulatory landscape is expected to become more stringent, particularly regarding sustainability reporting, organic certification, labeling transparency, and alcohol consumption guidelines. Governments will continue to enforce stricter controls on advertising and public health messaging related to alcohol consumption.

Global trade policies and tariffs will remain key factors influencing cross-border wine distribution, especially in Asia-Pacific and emerging markets. Digital transformation of wine sales will drive new compliance requirements for e-commerce, age verification, and cross-border logistics.

Producers that proactively align with regulatory standards, invest in certification and sustainability initiatives, and adapt to regional compliance frameworks will be best positioned to maintain premium positioning and long-term growth in the global market.