Global Radial vs Bias Tyres Market size , share & forecast 2026-2033

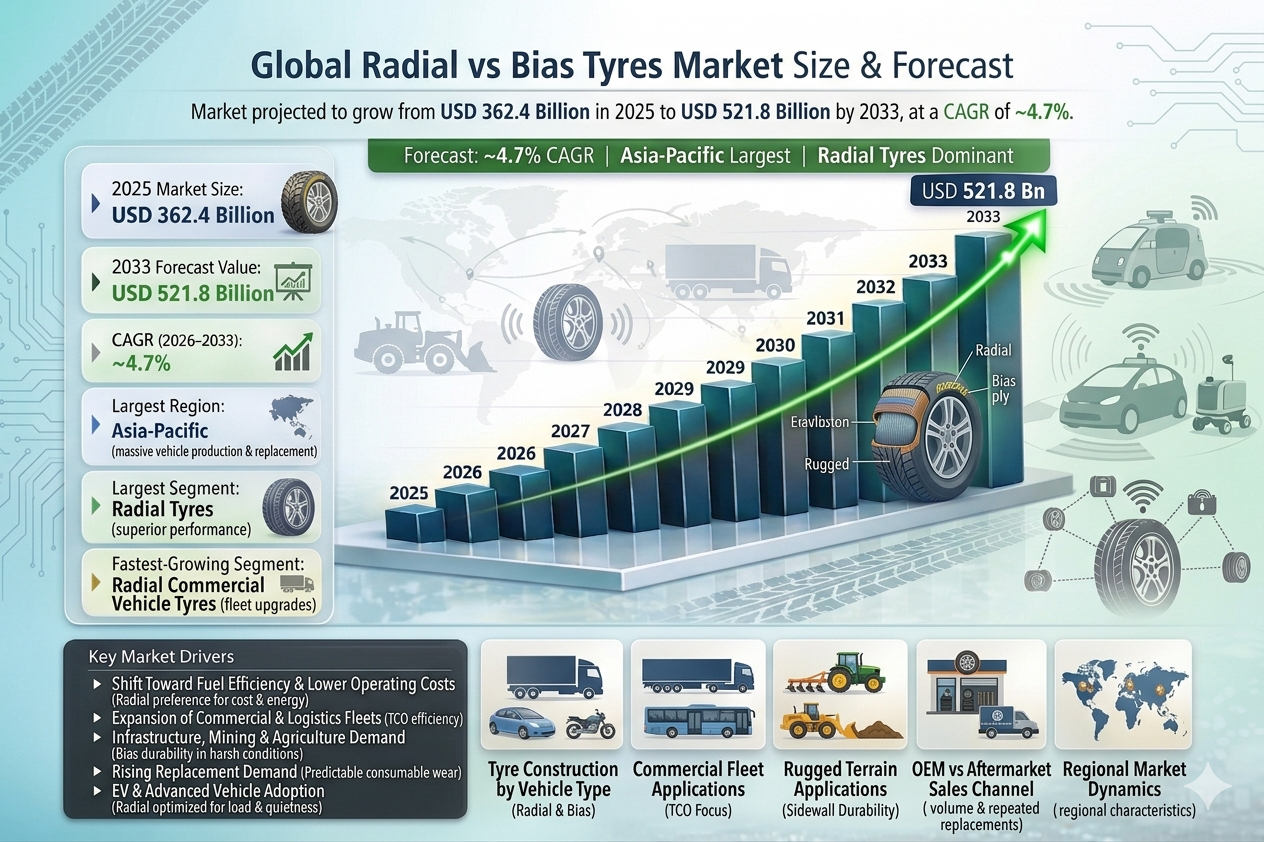

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| 2025 Market Size | USD 362.4 Billion |

| 2033 Market Size | USD 521.8 Billion |

| CAGR (2026???2033) | ~4.7% |

| Largest Segment | Radial tyres |

| Fastest-Growing Segment | Radial commercial vehicle tyres |

| Largest Region | Asia-Pacific |

| Key Trend | Shift from bias to radial for TCO efficiency |

Global Radial vs Bias Tyres Market Overview

The Global Radial vs Bias Tyres Market breaks down tyres by how they???re built ??? radial or bias (cross-ply) ??? and each has its own vibe. Radial tyres are tougher, last longer, and handle better, so they???re popular for cars, trucks, and heavy machinery . Bias tyres are cheaper, simpler, and great for rough, low-speed jobs like farming or industrial use . Both types serve different vehicles and needs, from passenger cars to off-road beasts.

The Global Radial vs Bias Tyres Market covers tyres sold as original equipment for new vehicles and, more importantly, through the aftermarket, where most of the volume comes from repeated replacements . As the number of vehicles on roads grows and infrastructure, mining, farming, and EVs expand, demand for both radial and bias tyres shifts and evolves. Radial tyres dominate for durability and performance, while bias tyres hold their ground in cost-sensitive, rugged applications.

According to the Pheonix Demand Forecast Engine, the Global Radial vs Bias Tyres Market size is valued at USD 362.4 billion in 2025 and is projected to reach USD 521.8 billion by 2033, expanding at a CAGR of ~4.7% during 2026???2033. Growth is strongly skewed toward radial tyres, while bias tyres maintain stable demand in niche and emerging-market applications.

Asia-Pacific is the largest regional market, supported by high vehicle production volumes, a massive replacement tyre base, strong agricultural activity, and growing infrastructure and mining investments in China, India, and Southeast Asia.

Europe is the fastest-growing region, driven by rapid radial tyre penetration, fleet modernization, stringent fuel-efficiency regulations, and increasing adoption of electric and premium vehicles.

Key Drivers of Global Radial vs Bias Tyres Market Growth

Shift Toward Fuel Efficiency & Lower Operating Costs

Radial tyres offer lower rolling resistance and longer service life, making them increasingly preferred by fleet operators and cost-conscious consumers.

Expansion of Commercial & Logistics Fleets

Freight, e-commerce, and fleet upgrades are pushing more trucks, buses, and LCVs to switch to radial tyres . They last longer, handle better, and save fuel. That shift???s driving solid market growth.

Infrastructure, Mining & Agriculture Demand

Bias tyres stay essential for heavy machinery, off-road, and farm gear , with tough sidewalls that handle bumps and impacts. Their durability keeps demand steady, driving solid market growth.

Rising Replacement Demand

Tyres are consumables with predictable wear cycles, making aftermarket replacement the largest revenue contributor for both radial and bias segments.

EV & Advanced Vehicle Adoption

Electric vehicles require radial tyres optimized for load, noise reduction, and energy efficiency, accelerating structural migration away from bias tyres.

Global Radial vs Bias Tyres Market Segmentation

1. By Tyre Construction

1.1 Radial Tyres??

1.1.1 Steel-Belted Radial Tyres

1.1.1.1 Single steel-belt radial tyres

1.1.1.2 Double steel-belt radial tyres

1.1.1.3 Multi-layer steel-belt radial tyres

1.1.2 Fabric-Belted Radial Tyres

1.1.2.1 Polyester radial tyres

1.1.2.2 Nylon radial tyres

Key Advantages:

Longer tread life, improved fuel economy, better heat dissipation, enhanced ride comfort

1.2 Bias (Cross-Ply) Tyres

1.2.1 Nylon Bias Tyres

1.2.1.1 Heavy-duty bias tyres

1.2.1.2 Load-focused bias tyres

1.2.2 Polyester Bias Tyres

1.2.2.1 Cost-efficient bias tyres

1.2.2.2 Rugged terrain tyres

Key Advantages:

Strong sidewalls, high load tolerance, low upfront cost, suitability for harsh environments

2. By Vehicle Category

2.1 Passenger Vehicles

2.1.1 Hatchbacks

2.1.2 Sedans

2.1.3 SUVs & crossovers

2.2 Commercial Vehicles

2.2.1 Light Commercial Vehicles (LCVs)

2.2.1.1 Delivery vans

2.2.1.2 Pickup trucks

2.2.2 Medium & Heavy Commercial Vehicles

2.2.2.1 Trucks

2.2.2.2 Buses

2.3 Off-the-Road (OTR) Vehicles

2.3.1 Construction equipment

2.3.2 Mining vehicles

2.4 Agricultural Vehicles

2.4.1 Tractors

2.4.2 Harvesters

2.5 Two-Wheelers & Three-Wheelers

2.5.1 Motorcycles

2.5.2 Scooters

2.5.3 Auto-rickshaws

3. By Sales Channel

3.1 OEM (Original Equipment Manufacturer)

3.1.1 Passenger vehicle OEM fitment

3.1.2 Commercial vehicle OEM fitment

3.1.3 Agricultural & industrial OEMs

3.2 Aftermarket / Replacement??

3.2.1 Authorized tyre dealers

3.2.2 Independent retailers

3.2.3 Fleet service centers

3.2.4 Online tyre platforms

4. By Price & Performance Category

4.1 Economy Tyres

4.1.1 Low-cost bias tyres

4.1.2 Entry-level radial tyres

4.2 Mid-Range Tyres

4.2.1 Balanced durability and performance

4.3 Premium Tyres

4.3.1 High-performance radial tyres

4.3.2 Long-life fleet tyres

5. By Geography

5.1 Asia-Pacific??

5.1.1 China

5.1.2 India

5.1.3 Japan

5.1.4 Southeast Asia

5.2 Europe??

5.2.1 Germany

5.2.2 France

5.2.3 U.K.

5.2.4 Italy

5.3 North America

5.3.1 U.S.

5.3.2 Canada

5.4 Latin America

5.4.1 Brazil

5.4.2 Mexico

5.5 Middle East & Africa

5.5.1 UAE

5.5.2 Saudi Arabia

5.5.3 South Africa

Regional Insights

Asia-Pacific ??? Largest Market

High vehicle production, strong agricultural usage, and a large replacement market support demand for both radial and bias tyres. Radial penetration is accelerating in China and India.

Europe ??? Radial-Dominated Market

Stringent fuel-efficiency regulations, EV adoption, and premium vehicle demand have made radial tyres the industry standard.

North America

Strong commercial fleets, long-haul trucking, and replacement-driven demand favor radial tyres, while bias tyres persist in select industrial uses.

Latin America

Cost sensitivity sustains bias tyre usage, though radial adoption is growing with fleet modernization.

Middle East & Africa

Bias tyres remain relevant in construction, mining, and extreme operating conditions.

Leading Companies in the Global Radial vs Bias Tyres Market

-

Goodyear Tire & Rubber Company

-

Continental AG

-

Pirelli & C. S.p.A.

-

Sumitomo Rubber Industries

-

Hankook Tire

-

Yokohama Rubber Company

-

Toyo Tires

-

Apollo Tyres

Michelin is the largest company in the Global Radial vs Bias Tyres Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Analyzes vehicle parc growth, fleet replacement cycles, infrastructure activity, and agricultural mechanization trends.

Radial Penetration Model

Tracks migration rates from bias to radial tyres by vehicle type and region.

Fleet TCO Optimization Engine

Evaluates cost-per-kilometer advantages driving radial tyre adoption.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate ??? fleet consolidation increases negotiation power

-

Supplier Power: Moderate ??? raw material volatility impacts margins

-

Threat of New Entrants: Low ??? capital-intensive manufacturing

-

Threat of Substitutes: Low ??? no functional alternatives

-

Competitive Rivalry: High ??? global majors vs regional price players

Final Takeaway

The Global Radial vs Bias Tyres Market is undergoing a structural transformation, with radial tyres steadily replacing bias tyres across most vehicle categories due to superior efficiency, durability, and lifecycle economics. While bias tyres retain relevance in heavy-duty, off-road, and cost-sensitive applications, their long-term growth remains limited. Manufacturers that invest in advanced radial technologies, EV-compatible designs, and fleet-focused solutions will capture the majority of value through 2033.

Competitive Landscape

Global Radial vs Bias Tyres Market Competitive Intensity & Market Structure Overview

The Global Radial vs Bias Tyres Market is characterized by a structurally stable yet highly competitive landscape, shaped by the ongoing transition from bias (cross-ply) to radial tyre technology. The market operates on a dual-technology structure where radial tyres dominate mainstream automotive and commercial applications, while bias tyres retain relevance in niche, rugged, and cost-sensitive segments. Competitive intensity is high due to the scale of the global tyre industry and the gradual but irreversible shift toward radialization. Manufacturers compete on durability, fuel efficiency, lifecycle cost, and performance optimization, particularly in fleet and commercial vehicle segments where total cost of ownership (TCO) is a key decision factor. The market is moderately consolidated, with Tier 1 global players controlling a significant share of radial tyre production and OEM contracts. However, the bias tyre segment remains fragmented, with strong participation from regional and low-cost manufacturers serving agriculture, mining, and off-road applications.

Global Radial vs Bias Tyres Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global Tyre Manufacturer. Leader in radial tyre innovation, fuel-efficient designs, and premium fleet solutions. Bridgestone Corporation: Global Tyre Manufacturer. Strong presence across radial and specialty tyres with extensive OEM partnerships. Goodyear Tire & Rubber Company: Tyre Manufacturer. Focused on high-performance radial tyres and connected fleet solutions. Continental AG: Technology-Driven Tyre Manufacturer. Strong in smart tyres and advanced radial engineering. Pirelli & C. S.p.A.: Premium Tyre Manufacturer. Focused on high-performance radial tyres and luxury vehicle segments. Sumitomo Rubber Industries: Tyre Manufacturer. Strong in both radial and bias segments across Asia-Pacific. Hankook Tire: Fast-Growing Global Player. Expanding radial tyre portfolio across passenger and commercial vehicles. Yokohama Rubber Company: Tyre Manufacturer. Known for durable and fuel-efficient radial tyres. Toyo Tires: Performance-Oriented Manufacturer. Strong in radial tyre innovation and mid-premium segments. Apollo Tyres: Cost-Competitive Global Player. Strong presence in both radial and bias tyres across emerging markets.

Key Competitive Intensity & Market Structure Signals in Radial vs Bias Tyres

A key structural signal is the accelerating shift from bias to radial tyres across most vehicle categories. Fleet operators and OEMs increasingly prioritize fuel efficiency, longer tread life, and reduced operating costs, all of which favor radial technology. OEM contracts play a critical role in shaping market structure. Automakers predominantly specify radial tyres for new vehicles, reinforcing their dominance and limiting growth opportunities for bias tyres in mainstream segments. The replacement market continues to be the largest revenue contributor, where competition intensifies between premium radial brands and low-cost bias alternatives, particularly in price-sensitive regions. Another important signal is the persistence of bias tyres in specific applications such as agriculture, construction, mining, and off-road environments. Their strong sidewalls and lower upfront cost ensure continued demand despite technological limitations. Regional dynamics also influence competition, with developed markets largely radial-dominated, while emerging markets continue to exhibit a mixed adoption pattern driven by cost considerations and operating conditions.

Strategic Implications of Competitive Intensity & Market Structure in Radial vs Bias Tyres

The competitive landscape is driving manufacturers to accelerate investment in radial tyre technology, including innovations in low rolling resistance, durability, and EV compatibility. Companies that lead in radial performance are positioned to capture long-term market share. Total cost of ownership (TCO) is becoming the central decision-making metric, particularly for fleet operators. This shift benefits radial tyres due to their longer lifespan and fuel-saving capabilities, despite higher upfront costs. Bias tyre manufacturers are increasingly focusing on niche positioning strategies, targeting rugged applications, low-speed operations, and emerging markets where cost sensitivity remains high. Electrification and regulatory pressures are further reinforcing radial dominance, as EVs and fuel-efficiency standards demand advanced tyre performance that bias technology cannot effectively deliver. Additionally, manufacturers are expanding into value-added services such as retreading, fleet management, and connected tyre solutions to differentiate in an otherwise mature and competitive market.

Radial vs Bias Tyres Competitive Intensity & Market Structure Forward Outlook

The Radial vs Bias Tyres Market is expected to witness continued structural transformation, with radial tyres steadily increasing their share across all major vehicle categories and geographies. Market consolidation is likely to strengthen among Tier 1 players, particularly in the radial segment, while smaller regional players will continue to dominate the fragmented bias tyre market. Technological advancements, including EV-specific radial tyres and smart tyre systems, will further widen the performance gap between radial and bias constructions. Regulatory trends focused on emissions, fuel efficiency, and safety will accelerate radial adoption globally, particularly in commercial vehicle and fleet segments. In the long term, the market will be defined by radial tyre dominance, niche resilience of bias tyres, and increasing integration of performance, efficiency, and digital monitoring capabilities. Manufacturers that align with radial innovation and evolving mobility requirements will lead the market through 2033.

Value Chain

Global Radial vs Bias Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain of the Global Radial vs Bias Tyres Market is highly structured and globally integrated, spanning raw material sourcing, tyre manufacturing, OEM integration, distribution networks, and aftermarket services. The market operates across two parallel product ecosystems’radial and bias tyres’each with distinct manufacturing processes, demand patterns, and application areas. This dual-structure market supports both OEM fitment for new vehicles and a dominant replacement-driven aftermarket, where predictable wear cycles generate continuous demand. While radial tyres dominate modern automotive and commercial vehicle segments, bias tyres remain critical in off-road, agricultural, and cost-sensitive applications, creating a diversified and resilient supply chain. Upstream activities are driven by natural rubber, synthetic rubber, carbon black, silica, steel cords, and textile reinforcements such as nylon and polyester. Radial tyres require more advanced material inputs, particularly steel belts and silica compounds, while bias tyres rely more on layered fabric reinforcements. Leading manufacturers maintain global sourcing strategies and supplier partnerships to manage input cost volatility. Manufacturing varies significantly between the two segments. Radial tyre production is technology-intensive, focusing on precision engineering, fuel efficiency, heat dissipation, and durability. In contrast, bias tyre manufacturing is relatively simpler and cost-efficient, emphasizing ruggedness, sidewall strength, and impact resistance for harsh environments. Distribution is divided between OEM supply chains and extensive aftermarket networks. OEM demand is closely tied to vehicle production trends, while aftermarket distribution’through dealers, retailers, and fleet service providers’accounts for the majority of revenue. Fleet operators, agricultural users, and industrial buyers play a critical role in sustaining demand across both tyre types. Key supply chain challenges include raw material price fluctuations, increasing regulatory pressure on fuel efficiency and emissions, and the ongoing transition from bias to radial tyres, which requires manufacturing upgrades and capital investment.

Global Radial vs Bias Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The current supply chain landscape is defined by a structural shift toward radial tyres, driven by performance, efficiency, and lifecycle cost advantages. This transition is reshaping manufacturing priorities, supplier relationships, and distribution strategies. At the upstream level, demand for advanced materials such as silica and steel belts is increasing due to higher radial tyre production. Meanwhile, bias tyre supply chains remain stable, particularly in emerging markets and off-road applications. Manufacturers such as Michelin, Bridgestone, Goodyear, and Continental are expanding radial tyre production capacity while gradually optimizing or phasing down bias tyre lines in certain segments. Investments are focused on automation, EV-compatible designs, and high-durability radial technologies. OEM integration is increasingly aligned with radial tyre adoption, particularly in passenger vehicles, commercial fleets, and electric vehicles. Bias tyres continue to be supplied to specialized OEM segments such as agriculture, construction, and mining equipment. The aftermarket remains the largest and most stable demand channel, supported by predictable replacement cycles. Fleet operators are increasingly shifting toward radial tyres to reduce total cost of ownership, further accelerating the structural transition. Digital transformation is also influencing the supply chain, with growing adoption of fleet analytics, tyre performance monitoring, and predictive maintenance systems’primarily in radial tyre segments.

Key Value Chain & Supply Chain Evolution Signals in Global Radial vs Bias Tyres Market

Several key signals are shaping the evolution of this market’s value chain. First, the ongoing shift from bias to radial tyres is the most significant structural trend, driven by fuel efficiency, durability, and lifecycle cost advantages. Second, increasing fleet focus on total cost of ownership (TCO) is accelerating radial tyre adoption, particularly in commercial vehicle segments. Third, bias tyres continue to maintain relevance in niche applications such as agriculture, construction, and mining, ensuring a dual-market structure. Fourth, OEM standardization is favoring radial tyres, especially in developed markets and electric vehicle platforms. Finally, digitalization and smart tyre technologies are being adopted primarily within radial tyre ecosystems, further widening the technological gap between the two segments.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Radial vs Bias Tyres Market

Leading players such as Michelin, Bridgestone, Continental, and Goodyear are strengthening their competitive positions through investments in radial tyre innovation, global manufacturing networks, and OEM partnerships. The transition toward radial tyres is creating capital-intensive requirements, increasing entry barriers and reinforcing market consolidation among established manufacturers. Bias tyre manufacturers, particularly regional players, continue to compete on cost and durability in price-sensitive and off-road segments, maintaining a stable but limited growth outlook. Fleet operators are playing a central role in shaping demand, increasingly prioritizing radial tyres to optimize fuel efficiency, maintenance costs, and overall operational performance. The growing importance of sustainability and regulatory compliance is further accelerating the shift toward radial tyres, which offer lower emissions and improved energy efficiency.

Global Radial vs Bias Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to become increasingly radial-dominated, with continued decline in bias tyre share across most on-road vehicle segments. Manufacturers will prioritize advanced radial technologies, including EV-compatible tyres, low rolling resistance compounds, and smart tyre systems integrated with digital fleet platforms. Bias tyres will remain relevant in specialized applications, particularly in agriculture, mining, and construction, but their overall market share will gradually decline. The aftermarket will continue to dominate revenue generation, supported by expanding global vehicle parc and predictable replacement cycles. Overall, the future value chain will be defined by efficiency, durability, and technological advancement, with radial tyres capturing the majority of value creation in the global market.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, carbon black, silica, steel cords, and textile reinforcements (nylon, polyester)

- Research & Development: Radial tyre engineering, bias tyre durability optimization, low rolling resistance technologies, and EV-compatible designs

- Manufacturing: Production of steel-belted radial tyres and layered bias tyres with focus on durability, efficiency, and cost optimization

- OEM Integration: Supply to passenger vehicles, commercial vehicles, agricultural machinery, and industrial equipment manufacturers

- Distribution & Sales: Dealer networks, independent retailers, fleet service providers, and online tyre platforms

- Aftermarket Services: Replacement tyres, retreading, maintenance services, and fleet tyre management solutions

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Apollo Tyres

- Distribution & Sales: Goodyear Tire & Rubber Company, Apollo Tyres, JK Tyre & Industries, Yokohama Rubber Company

- Aftermarket Services: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

Investment Activity

Global Radial vs Bias Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Radial vs Bias Tyres Market are primarily driven by the ongoing structural shift from bias (cross-ply) tyres to radial tyre technology. Between 2026 and 2033, capital allocation is expected to increasingly favor radial tyre manufacturing, advanced materials, and performance optimization technologies that enhance fuel efficiency and reduce total cost of ownership (TCO).

The market is moderately capital-intensive, requiring significant investments in manufacturing infrastructure, steel-belt technology, and precision engineering. Leading tyre manufacturers such as Michelin, Bridgestone, Continental, and Goodyear are focusing on expanding radial production capacity while optimizing legacy bias tyre operations for niche applications.

A key transformation shaping investment trends is the growing demand for fuel-efficient, long-lasting tyres across passenger and commercial vehicle segments. This is accelerating funding toward radial tyre innovation, including low rolling resistance compounds, EV-compatible designs, and high-durability fleet solutions.

Global Radial vs Bias Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly aligned with the global transition toward radial tyres, particularly in commercial vehicle and passenger vehicle segments. OEM partnerships and fleet-focused solutions are key areas of capital deployment.

Asia-Pacific dominates as the largest investment hub, driven by high vehicle production volumes, expanding replacement markets, and increasing radial penetration in countries such as China and India.

Europe is the fastest-growing investment region, supported by stringent fuel-efficiency regulations, rapid EV adoption, and a well-established preference for radial tyres across vehicle categories.

North America remains a mature and technology-driven market, with investments focused on premium radial tyres for long-haul trucking, fleet optimization, and EV compatibility.

Latin America and the Middle East & Africa continue to attract selective investments, particularly in cost-effective bias tyre production and gradual radial adoption driven by infrastructure and industrial growth.

Key Investment & Funding Dynamics Signals in Global Radial vs Bias Tyres Market

A major investment signal is the accelerating global shift from bias to radial tyres, driven by superior fuel efficiency, durability, and lifecycle cost advantages.

The expansion of commercial fleets and logistics networks is another critical signal, as fleet operators increasingly prioritize TCO optimization through radial tyre adoption.

Strong replacement demand continues to ensure stable revenue streams, encouraging sustained investment across both radial and bias segments.

The rise of electric vehicles is further reinforcing investment in advanced radial tyre technologies designed for higher loads, lower noise, and improved energy efficiency.

At the same time, continued demand for bias tyres in off-road, agricultural, and industrial applications sustains targeted investments in durable, cost-effective designs.

Strategic Implications of Investment & Funding Dynamics in Global Radial vs Bias Tyres Market

The investment landscape increasingly favors companies with strong radial tyre technology capabilities, creating competitive advantages for established global players.

Manufacturers must strategically balance investments between expanding radial tyre capacity and maintaining efficient bias tyre production for niche markets.

OEM partnerships and fleet collaborations are critical for capturing long-term demand and strengthening market positioning in both segments.

Regional diversification remains essential, with Asia-Pacific driving volume growth, Europe leading regulatory-driven adoption, and North America focusing on premium and high-performance applications.

Raw material price volatility, particularly in natural rubber and steel, continues to influence investment decisions, requiring robust sourcing and cost management strategies.

Global Radial vs Bias Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Radial vs Bias Tyres Market is expected to witness sustained investment driven by increasing vehicle parc, infrastructure development, and fleet modernization trends.

Future capital allocation will be heavily skewed toward radial tyre technologies, including EV-optimized designs, smart tyre integration, and advanced compound development.

Asia-Pacific will remain the largest investment destination due to its scale and growth potential, while Europe will continue to lead in regulatory-driven innovation and sustainability-focused tyre technologies.

North America will maintain strong investment momentum in premium radial tyres, particularly for commercial fleets and electric vehicles.

Overall, the market will continue its structural transition toward radial dominance, with innovation, efficiency, and TCO optimization shaping long-term investment strategies through 2033.

Technology & Innovation

Global Radial vs Bias Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Radial vs Bias Tyres Market is centered around structural efficiency, durability, and total cost of ownership (TCO). The fundamental difference between radial and bias tyres lies in their construction, which directly influences performance, lifespan, fuel efficiency, and application suitability across passenger, commercial, and off-road vehicles.

Innovation in this market is primarily driven by the global shift from bias to radial tyre technology. Radial tyres, with their steel-belted construction and flexible sidewalls, are continuously evolving to deliver better fuel economy, heat dissipation, and tread life. Meanwhile, bias tyres are undergoing incremental improvements focused on durability and cost optimization for niche applications such as agriculture, mining, and construction.

Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are investing heavily in advanced radial technologies, including high-performance compounds, lightweight structures, and EV-compatible designs. At the same time, innovation in bias tyres remains focused on enhancing ruggedness and load-bearing capabilities for harsh operating environments.

Global Radial vs Bias Tyres Market Technology & Innovation Landscape Current Scenario

Currently, radial tyre technology dominates the innovation landscape due to its superior performance characteristics and growing adoption across all major vehicle categories. Steel-belted radial tyres are widely used for their ability to improve fuel efficiency, reduce rolling resistance, and extend service life.

Advanced rubber compounds, including silica-enhanced formulations, are being integrated into radial tyres to optimize grip, reduce wear, and enhance energy efficiency. These developments are particularly important for commercial fleets and electric vehicles, where operating costs and range optimization are critical.

Bias tyres, while technologically less advanced, continue to evolve with improvements in sidewall strength, cut resistance, and load tolerance. These tyres remain essential in off-road and heavy-duty applications where durability and resistance to mechanical damage are more important than speed or efficiency.

Retreadability is another key innovation area, especially for radial commercial vehicle tyres. Multi-life casing designs enable multiple retreading cycles, significantly reducing lifecycle costs for fleet operators.

Manufacturing technologies are also advancing, with automation, AI-driven quality control, and improved material processing enhancing consistency, scalability, and cost efficiency across both radial and bias tyre production.

Key Technology & Innovation Landscape Signals in Global Radial vs Bias Tyres Market

- Shift Toward Radial Technology: Increasing adoption due to superior fuel efficiency, durability, and performance.

- Low Rolling Resistance Compounds: Enhancing fuel savings and supporting EV efficiency requirements.

- Steel-Belted Reinforcement: Improving structural integrity and tread life in radial tyres.

- Retreadable Tyre Designs: Multi-life casing technologies reducing total cost of ownership for fleets.

- Enhanced Bias Tyre Durability: Improved sidewall strength and impact resistance for rugged environments.

- EV-Compatible Tyres: Radial designs optimized for high torque, load, and noise reduction.

- Advanced Manufacturing Technologies: Automation and AI-driven quality control improving production efficiency.

Strategic Implications of Technology & Innovation Landscape in Global Radial vs Bias Tyres Market

The ongoing shift from bias to radial tyres is reshaping competitive dynamics and strategic priorities for tyre manufacturers. Investment in radial tyre technology is becoming essential to remain competitive, particularly in the passenger vehicle and commercial fleet segments.

Fleet operators are increasingly prioritizing total cost of ownership, driving demand for durable, fuel-efficient, and retreadable radial tyres. This trend is encouraging manufacturers to focus on lifecycle value rather than upfront pricing.

Bias tyre manufacturers must differentiate through cost competitiveness and application-specific durability, particularly in agriculture, mining, and construction sectors where these tyres continue to hold relevance.

The rise of electric vehicles is further accelerating radial tyre innovation, as EVs require specialized tyres capable of handling higher loads, instant torque, and noise reduction requirements.

Strategic partnerships between tyre manufacturers and OEMs are becoming increasingly important to develop vehicle-specific solutions and ensure early adoption of advanced tyre technologies.

Global Radial vs Bias Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the market is expected to witness continued dominance of radial tyre technology, with ongoing advancements in materials, design, and manufacturing processes further strengthening their performance advantages.

Bias tyres will remain relevant in niche and heavy-duty applications, but their innovation trajectory will be more incremental compared to radial tyres. The long-term growth outlook for bias tyres is expected to remain stable but limited.

Emerging trends such as smart tyres, sensor integration, and predictive maintenance are expected to further enhance the value proposition of radial tyres, particularly in commercial and connected vehicle ecosystems.

Sustainability will also play a key role in future innovation, with increasing adoption of eco-friendly materials, energy-efficient manufacturing processes, and circular economy practices such as recycling and retreading.

In conclusion, the Global Radial vs Bias Tyres Market is undergoing a structural technological transition, with radial tyres emerging as the dominant innovation platform. Manufacturers that prioritize advanced radial technologies, EV compatibility, and lifecycle cost optimization will lead the market evolution through 2033.

Market Risk

Global Radial vs Bias Tyres Market Risk Factors & Disruption Threats Overview

The Global Radial vs Bias Tyres Market operates in a large-scale, cost-sensitive, and replacement-driven environment, supported by automotive, industrial, agricultural, and logistics sectors. While the market benefits from consistent demand and essential product usage, it carries a moderate risk profile due to raw material volatility, structural technology shifts, and regional demand imbalances. A major structural risk is the ongoing transition from bias to radial tyre technology. While radial tyres dominate due to superior performance and fuel efficiency, this shift creates demand disruption for bias tyre manufacturers, particularly in emerging markets and niche applications. Raw material price volatility remains a critical risk factor, especially for natural rubber, synthetic rubber, and steel cord. Since tyres are material-intensive products, fluctuations directly impact production costs and margins, particularly in price-sensitive aftermarket segments. Another key disruption factor is intense price competition across global and regional players. The presence of low-cost manufacturers, especially in Asia, increases pricing pressure and limits margin expansion for premium brands. Demand cyclicality linked to automotive production, infrastructure development, mining, and agriculture also introduces risk. Economic slowdowns can reduce vehicle usage and delay replacement cycles, directly impacting tyre demand.

Global Radial vs Bias Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects steady growth supported by rising vehicle parc, expanding logistics networks, and ongoing infrastructure and agricultural activities. However, the market is simultaneously undergoing structural transformation toward radialization. Radial tyres continue to gain share across passenger and commercial vehicle segments due to their superior durability, fuel efficiency, and lifecycle cost advantages. This is gradually reducing demand for bias tyres in several applications. The aftermarket segment dominates overall demand, driven by predictable wear cycles and high replacement frequency. However, increasing digitalization and online tyre sales are reshaping traditional distribution networks. Supply chain challenges, particularly in sourcing rubber and steel inputs, continue to impact manufacturing costs and delivery timelines. This creates operational pressure for both global and regional players. At the same time, EV adoption is accelerating the shift toward advanced radial tyres, as electric vehicles require low rolling resistance, high load capacity, and noise optimization.

Key Risk Factors & Disruption Threats Signals in Global Radial vs Bias Tyres Market

A key signal is the rapid increase in radial tyre penetration across commercial and passenger vehicle segments. Fleet operators are prioritizing total cost of ownership (TCO), accelerating the transition away from bias tyres. Emerging market demand patterns present another signal. While bias tyres remain relevant in agriculture, construction, and low-speed applications, their share is gradually declining as radial adoption expands. Fleet consolidation and large-scale procurement strategies are also reshaping the market. Large logistics operators and transport companies are negotiating bulk contracts, increasing buyer power and pricing pressure. Technological advancements in tyre materials and design, including EV-compatible radial tyres, signal a shift toward performance-driven and efficiency-focused products. Additionally, sustainability and fuel-efficiency regulations are influencing tyre selection, favoring radial tyres with lower rolling resistance and reduced environmental impact.

Strategic Implications of Risk Factors & Disruption Threats in Global Radial vs Bias Tyres Market

Manufacturers must accelerate investment in radial tyre technologies, focusing on durability, fuel efficiency, and EV compatibility to align with evolving market demand. At the same time, maintaining a balanced portfolio is important, as bias tyres continue to serve niche applications in agriculture, mining, and construction. Strengthening aftermarket distribution networks and digital sales channels is critical, as replacement demand remains the largest revenue contributor. Cost optimization and supply chain resilience strategies are essential to manage raw material volatility and maintain profitability in a highly competitive pricing environment. Building strong relationships with fleet operators and OEMs is increasingly important, as procurement decisions are becoming more centralized and data-driven.

Global Radial vs Bias Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Radial vs Bias Tyres Market will continue its structural transition toward radial dominance, driven by efficiency, sustainability, and performance advantages. Bias tyres will remain relevant in specific off-road, agricultural, and cost-sensitive applications, but their overall market share is expected to decline gradually. EV growth will further accelerate demand for advanced radial tyres, requiring continuous innovation in materials, tread design, and energy efficiency. Digitalization of tyre sales and fleet management will increase transparency and competition, pushing manufacturers toward value-added services and integrated solutions. Overall, the market will remain stable but highly competitive, with long-term success dependent on technology transition, cost efficiency, and strong positioning in both OEM and aftermarket segments.

Regulatory Landscape

Global Radial vs Bias Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Radial vs Bias Tyres Market plays a decisive role in accelerating the shift from bias to radial tyre technologies. Governments, transport authorities, and environmental agencies are increasingly focusing on fuel efficiency, emissions reduction, road safety, and lifecycle sustainability’areas where radial tyres outperform traditional bias tyres. Key global frameworks such as the European Union Tyre Labelling Regulation (EU) 2020/740 and UNECE tyre performance standards establish mandatory benchmarks for rolling resistance, wet grip, and external noise. These regulations strongly favor radial tyre adoption due to their superior fuel efficiency, durability, and performance characteristics, especially in passenger and commercial vehicle segments. In addition, tightening carbon emission policies and fuel economy regulations across major automotive markets are pushing OEMs and fleet operators toward low rolling resistance tyre solutions. This indirectly accelerates the decline of bias tyres in on-road applications while maintaining their relevance in niche off-road and heavy-duty sectors. Emerging economies such as India, China, and Brazil are also strengthening tyre quality regulations, vehicle inspection norms, and safety certifications. These efforts are improving overall tyre standards and encouraging gradual transition toward radialization in commercial and agricultural vehicle segments.

Global Radial vs Bias Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by strong momentum toward energy efficiency, sustainability, and advanced vehicle performance standards. Europe leads in regulatory maturity, where tyre labeling systems significantly influence both OEM fitment and aftermarket purchasing decisions. In Europe, stringent emission norms and fuel efficiency targets have made radial tyres the dominant standard across nearly all vehicle categories. Noise reduction regulations in urban areas further reinforce demand for advanced radial tyre designs with optimized tread patterns and compounds. In Asia-Pacific, governments are promoting infrastructure development, vehicle safety compliance, and fleet modernization. Countries such as China and India are witnessing rapid radial tyre penetration, supported by regulatory push and increasing awareness of total cost of ownership (TCO) benefits. North America maintains strong oversight through DOT and EPA-aligned frameworks, emphasizing fuel economy and safety performance. These regulations support steady adoption of radial tyres across commercial fleets, while bias tyres remain limited to specific industrial and off-road use cases. The growing adoption of electric vehicles is also reshaping regulatory expectations, as EV-specific requirements such as low rolling resistance, high load capacity, and reduced noise further accelerate the transition toward radial tyre technologies.

Key Regulatory & Policy Environment Signals in Global Radial vs Bias Tyres Market

- EU Tyre Labelling Regulation (EU 2020/740): Drives transparency in fuel efficiency, wet grip, and noise’favoring radial tyre adoption.

- UNECE Tyre Performance Standards: Establish global benchmarks for durability, load capacity, and safety performance.

- Fuel Efficiency & Emission Regulations: Promote low rolling resistance tyres, accelerating radialization across fleets.

- Vehicle Safety & Inspection Programs: Strengthen compliance and quality standards in emerging markets.

- Electric Vehicle Policies: Encourage adoption of EV-compatible radial tyres with enhanced efficiency and noise reduction.

- Infrastructure & Industrial Regulations: Sustain niche demand for bias tyres in construction, mining, and agricultural applications.

Strategic Implications of Regulatory & Policy Environment in Global Radial vs Bias Tyres Market

The regulatory environment is accelerating structural transformation in the tyre industry, clearly favoring radial tyre technologies. This shift raises entry barriers, as manufacturers must invest in advanced R&D, manufacturing capabilities, and compliance infrastructure to meet evolving standards. Bias tyre manufacturers face increasing pressure to either upgrade technology or focus on specialized applications such as off-road, agricultural, and industrial segments where regulatory constraints are relatively lower. For leading tyre manufacturers, compliance-driven innovation has become a key competitive advantage. Investments in low rolling resistance compounds, advanced radial construction, and EV-optimized designs are critical to maintaining market leadership. Fleet operators and OEMs are increasingly guided by regulatory labeling systems and TCO-focused policies, shifting procurement decisions toward high-performance radial tyres that deliver measurable efficiency, durability, and sustainability benefits. Regional regulatory variations are also influencing supply chain strategies, encouraging localized production, strategic partnerships, and tailored product offerings to meet diverse compliance requirements.

Global Radial vs Bias Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become more stringent and sustainability-focused, reinforcing the global transition toward radial tyres. Governments will continue tightening fuel efficiency, emission, and noise standards across vehicle categories. Europe will remain at the forefront, expanding lifecycle carbon footprint regulations and strengthening sustainability reporting requirements. Asia-Pacific will accelerate radial adoption through enhanced safety standards and fleet modernization initiatives. The rise of electric vehicles will further reshape regulatory frameworks, introducing new performance requirements that strongly align with radial tyre capabilities, including energy efficiency, load durability, and acoustic optimization. Bias tyres are expected to retain relevance in niche applications such as mining, construction, and agriculture, but their regulatory support will remain limited compared to radial technologies. Overall, the regulatory landscape will act as a powerful catalyst driving radialization, innovation, and consolidation in the tyre industry. Manufacturers that align with evolving regulatory standards and invest in advanced radial technologies will be best positioned to capture long-term market growth.