Global Transplant Diagnostics Market Report, Size and Forecast 2026-2033

Global Transplant Diagnostics Market Report, Size, Share and Forecast 2026–2033

Market Forecast Snapshot (2025–2033)

| Metric | Value |

|---|---|

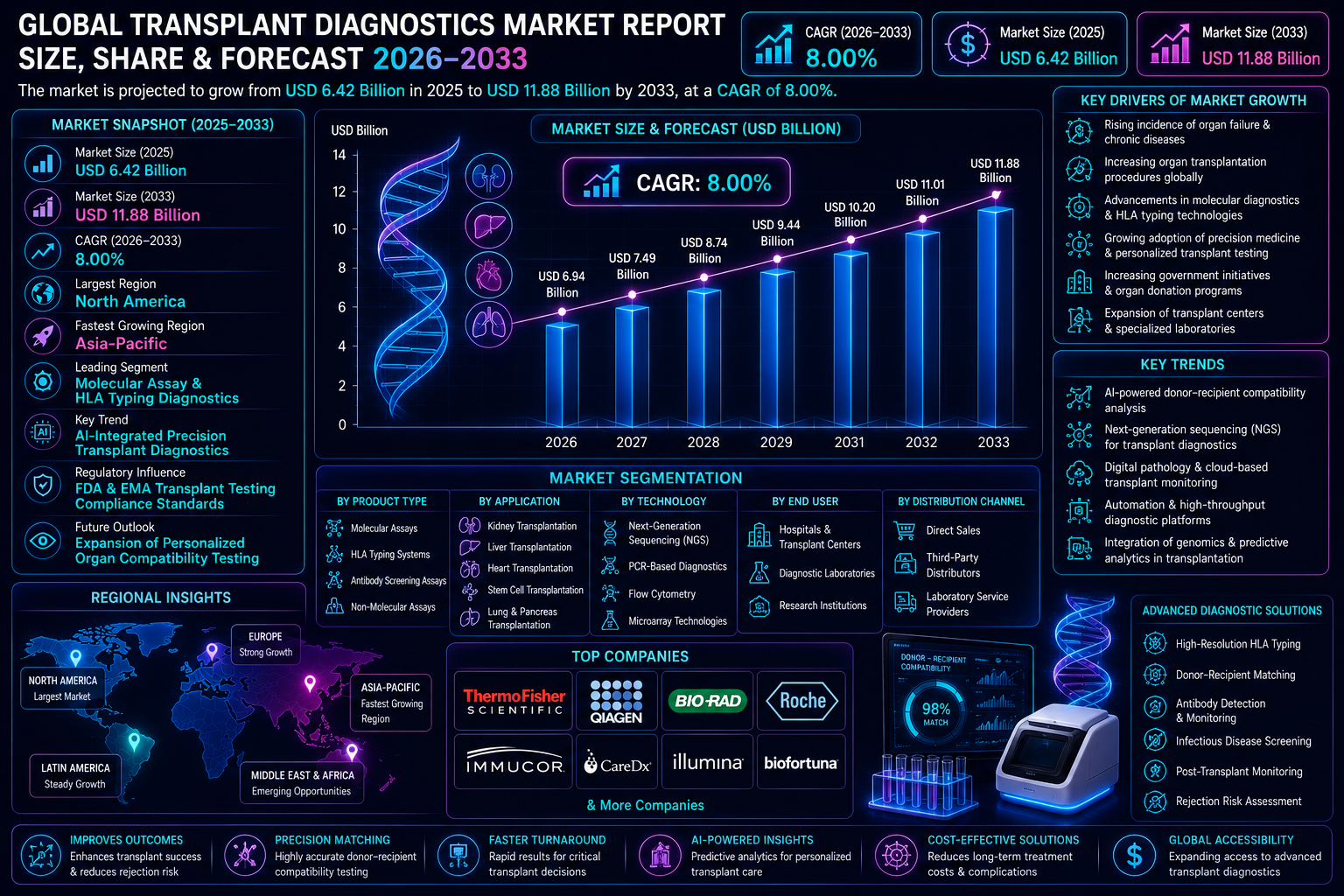

| Market Size (2025) | USD 6.42 Billion |

| Market Size (2033) | USD 11.88 Billion |

| CAGR (2026–2033) | 8.00% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Leading Segment | Molecular Assay & HLA Typing Diagnostics |

| Key Trend | AI-Integrated Precision Transplant Diagnostics |

| Regulatory Influence | FDA & EMA Transplant Testing Compliance Standards |

| Future Outlook | Expansion of Personalized Organ Compatibility Testing |

Market Size & Forecast

The Global Transplant Diagnostics Market is projected to experience strong and sustained growth during the forecast period from 2026 to 2033. The market was valued at USD 6.42 billion in 2025 and is anticipated to reach approximately USD 11.88 billion by 2033, expanding at a CAGR of 8.00% throughout the forecast timeline. The market’s growth is being driven by increasing organ transplantation procedures, rising prevalence of chronic diseases leading to organ failure, and advancements in molecular diagnostic technologies. The growing incidence of kidney failure, liver disorders, cardiovascular diseases, and autoimmune conditions has significantly increased demand for organ transplantation globally. As transplantation procedures continue to rise, healthcare providers are increasingly adopting advanced transplant diagnostics solutions to improve donor-recipient compatibility, reduce rejection risks, and optimize transplant outcomes. Technological advancements in molecular diagnostics, next-generation sequencing (NGS), PCR-based testing, and AI-driven compatibility analysis are significantly improving transplantation success rates. Additionally, increasing adoption of precision medicine and personalized healthcare approaches is further accelerating the use of advanced transplant diagnostics globally. Growing awareness regarding organ donation programs, expanding healthcare infrastructure, and favorable government initiatives supporting transplantation services are also contributing significantly to market growth.Global Transplant Diagnostics Market Overview

The Transplant Diagnostics Market plays a critical role in organ transplantation procedures by enabling accurate donor-recipient matching, post-transplant monitoring, and rejection risk assessment. Transplant diagnostic solutions include molecular assays, HLA typing technologies, antibody screening systems, and infectious disease testing platforms. The market encompasses a broad range of diagnostic applications including kidney transplantation, liver transplantation, heart transplantation, lung transplantation, stem cell transplantation, and tissue compatibility testing. The market remains moderately consolidated with several global diagnostics companies actively investing in advanced immunogenetics technologies, AI-driven transplant analytics, and precision diagnostic platforms. Companies are increasingly focusing on expanding molecular testing capabilities and improving transplant outcome prediction technologies. Regulatory agencies worldwide continue to strengthen standards related to transplantation safety, organ compatibility testing, and infectious disease screening. Increasing demand for highly sensitive and rapid transplant diagnostics solutions is encouraging innovation across the market. The integration of digital pathology, genomic analysis, cloud-based transplant monitoring, and AI-assisted compatibility analysis is transforming transplant diagnostics workflows and improving clinical decision-making globally.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid advancements in molecular diagnostics, genomic sequencing, and AI-assisted transplant analytics are significantly accelerating innovation within the transplant diagnostics market. Technologies such as next-generation sequencing (NGS), digital PCR, and high-resolution HLA typing are improving donor-recipient matching accuracy and reducing rejection risks. The growing adoption of automated diagnostic systems and cloud-based transplant monitoring platforms is also enhancing workflow efficiency and improving turnaround times for transplantation procedures.Market Implications

Companies investing in precision diagnostics, AI-based transplant analytics, and high-throughput sequencing technologies are expected to gain substantial competitive advantages as healthcare systems increasingly prioritize personalized transplantation strategies.2. Compliance and Risk Repricing

Regulatory frameworks surrounding transplantation safety, infectious disease testing, and organ compatibility diagnostics are becoming increasingly stringent. Healthcare providers and diagnostics manufacturers must comply with evolving standards established by regulatory agencies including the U.S. Food and Drug Administration and the European Medicines Agency. Manufacturers are investing heavily in clinical validation studies, quality assurance programs, and laboratory automation systems to ensure compliance with transplant testing standards and patient safety protocols.Market Implications

Companies with strong regulatory expertise and validated diagnostic platforms will strengthen their market positions while improving adoption among transplantation centers and healthcare providers.3. Competitive and Value-Chain Reconfiguration

The market is witnessing increasing competition driven by convergence between molecular diagnostics, genomics, AI healthcare platforms, and transplant informatics. Strategic collaborations between diagnostics companies, transplant centers, biotechnology firms, and genomic sequencing providers are reshaping the transplant diagnostics ecosystem. The expansion of precision medicine and personalized healthcare initiatives is also redistributing value-chain dynamics and creating opportunities for integrated transplant diagnostics platforms.Market Implications

The integration of AI, cloud-based healthcare systems, and genomic diagnostics will continue redefining competitive advantages within the transplant diagnostics market.4. Capital and Capacity Scaling

Increasing investments in molecular diagnostics laboratories, transplant centers, genomic sequencing infrastructure, and AI healthcare technologies are supporting rapid market scalability. Governments and healthcare institutions are expanding transplantation programs and investing in advanced diagnostics infrastructure to improve transplant success rates. Healthcare providers are also increasing investments in laboratory automation, digital pathology systems, and real-time transplant monitoring platforms to optimize clinical workflows.Market Implications

Companies investing in scalable diagnostic technologies, laboratory automation, and high-throughput molecular testing platforms are expected to capture long-term growth opportunities.Market Segmentation Analysis

By Product Type

1. Molecular Assays

Molecular diagnostics assays dominate the market due to increasing demand for highly accurate donor-recipient compatibility testing.2. HLA Typing Systems

High-resolution HLA typing technologies remain critical for transplantation compatibility assessment.3. Antibody Screening Assays

Antibody detection and monitoring systems are increasingly used for rejection risk assessment.4. Non-Molecular Assays

Serological and immunological testing methods continue to support transplantation workflows globally.By Application

1. Kidney Transplantation

Kidney transplantation remains the leading application segment due to rising global incidence of chronic kidney disease.2. Liver Transplantation

Increasing liver failure cases and hepatitis prevalence are driving demand for liver transplant diagnostics.3. Heart Transplantation

Advanced transplant diagnostics are increasingly utilized for cardiac transplant compatibility testing.4. Stem Cell Transplantation

Hematopoietic stem cell transplantation is witnessing growing demand for high-resolution immunogenetics testing.5. Lung & Pancreas Transplantation

Specialized compatibility diagnostics are increasingly supporting complex organ transplantation procedures.By Technology

1. Next-Generation Sequencing (NGS)

NGS technologies are rapidly gaining adoption due to superior precision and high-throughput compatibility analysis.2. PCR-Based Diagnostics

PCR technologies remain widely used for HLA typing and infectious disease screening.3. Flow Cytometry

Flow cytometry systems support crossmatching and antibody screening applications.4. Microarray Technologies

Microarray platforms are increasingly utilized for genomic compatibility analysis.By End User

1. Hospitals & Transplant Centers

Large transplantation hospitals remain primary adopters of advanced transplant diagnostics solutions.2. Diagnostic Laboratories

Independent diagnostic laboratories play a critical role in compatibility testing and transplant monitoring.3. Research Institutions

Academic and clinical research centers increasingly utilize transplant diagnostics technologies for immunogenetics research.By Distribution Channel

1. Direct Sales

Direct manufacturer sales dominate due to specialized diagnostic equipment requirements.2. Third-Party Distributors

Regional distributors support market expansion and healthcare accessibility.3. Laboratory Service Providers

Integrated laboratory service providers are increasingly offering transplant diagnostic testing solutions.Regional Market Dynamics

North America

North America dominates the Global Transplant Diagnostics Market due to advanced healthcare infrastructure, high transplantation procedure volumes, strong reimbursement systems, and rapid adoption of molecular diagnostics technologies. The United States remains the largest contributor due to increasing organ transplantation activities and precision medicine initiatives.Europe

Europe is witnessing substantial growth driven by increasing organ donation awareness, advanced transplantation programs, and supportive healthcare policies. Germany, France, the UK, and Spain remain major contributors to regional market growth.Asia-Pacific

Asia-Pacific is projected to witness the fastest growth during the forecast period due to improving healthcare infrastructure, rising chronic disease prevalence, expanding transplantation services, and increasing healthcare investments across China, India, Japan, and South Korea.Latin America

The Latin American market is gradually expanding due to increasing transplantation awareness and improving access to advanced diagnostic services.Middle East & Africa

The market in the Middle East & Africa is experiencing moderate growth supported by healthcare modernization initiatives and growing transplantation infrastructure investments.Competitive Landscape

The Global Transplant Diagnostics Market is highly innovation-driven with companies focusing on molecular diagnostics, AI-assisted transplant analytics, genomic sequencing technologies, and laboratory automation systems. Key companies operating in the market include:- Thermo Fisher Scientific

- QIAGEN

- Bio-Rad Laboratories

- F. Hoffmann-La Roche Ltd.

- Immucor

- CareDx

- Illumina

- Biofortuna

Strategic Outlook

The future of the Transplant Diagnostics Market will be shaped by increasing integration of AI healthcare systems, genomic medicine, precision diagnostics, and cloud-based transplant monitoring technologies. Healthcare systems are increasingly prioritizing personalized transplantation strategies to improve clinical outcomes and reduce transplant rejection rates. The growing adoption of next-generation sequencing, digital pathology, and predictive analytics will continue transforming transplantation workflows globally. Additionally, increasing investments in organ donation programs and transplantation infrastructure are expected to create strong long-term growth opportunities. Companies capable of balancing technological innovation, regulatory compliance, clinical accuracy, and cost efficiency will strengthen their market positioning significantly.Final Market Perspective

The Global Transplant Diagnostics Market is entering a transformative growth phase driven by increasing transplantation procedures, advancements in molecular diagnostics, and rising demand for personalized healthcare solutions. The convergence of genomics, AI, and precision medicine is fundamentally reshaping transplant diagnostics globally. As healthcare systems continue prioritizing transplant safety, compatibility accuracy, and long-term patient outcomes, advanced transplant diagnostics technologies are expected to become increasingly essential within modern healthcare infrastructure. Companies investing in next-generation diagnostics platforms, laboratory automation, and digital healthcare ecosystems will be best positioned to capitalize on the market’s future growth potential.Table of Contents

Executive Summary

1.1 Market Forecast Snapshot (2026–2033)

1.2 Global Transplant Diagnostics Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Regulatory Influence & Transplant Testing Compliance Trends

1.8 Strategic Outlook Through 2033

Introduction & Market Overview

2.1 Definition of the Transplant Diagnostics Market

2.2 Market Size & Forecast (2026–2033)

2.3 Industry Evolution & Market Development

2.4 Supply Chain & Distribution Infrastructure

2.5 Impact of Organ Transplantation Trends & Precision Medicine

2.6 Regulatory & Compliance Landscape (FDA, EMA & Organ Transplant Testing Standards)

2.7 Technology & Innovation Landscape (NGS, AI Diagnostics, PCR & Digital Pathology)

Research Methodology

3.1 Primary Research

3.2 Secondary Research

3.3 Market Size Estimation Model

3.4 Forecast Assumptions (2026–2033)

3.5 Data Validation & Triangulation

Market Dynamics

4.1 Drivers

4.1.1 Rising Organ Transplantation Procedures Globally

4.1.2 Increasing Prevalence of Chronic Organ Failure Diseases

4.1.3 Growing Adoption of Precision Medicine & Personalized Healthcare

4.1.4 Advancements in Molecular & Genomic Diagnostics

4.1.5 Increasing Investments in Transplant Infrastructure & Organ Donation Programs

4.2 Restraints

4.2.1 High Cost of Advanced Molecular Diagnostic Technologies

4.2.2 Limited Organ Donation Availability

4.2.3 Regulatory Complexity & Compliance Burdens

4.2.4 Limited Access to Advanced Diagnostics in Emerging Markets

4.3 Opportunities

4.3.1 Expansion of AI-Assisted Compatibility Testing

4.3.2 Growth of Next-Generation Sequencing (NGS) Applications

4.3.3 Increasing Adoption of Cloud-Based Transplant Monitoring Platforms

4.3.4 Emerging Market Expansion Across Asia-Pacific & Latin America

4.4 Challenges

4.4.1 Complexity of Donor-Recipient Matching

4.4.2 Data Privacy & Genomic Information Security Risks

4.4.3 High Infrastructure & Laboratory Automation Costs

4.4.4 Variability in Global Transplantation Policies & Standards

Transplant Diagnostics Market Analysis (USD Billion), 2026–2033

5.1 Market Size Overview

5.2 CAGR Analysis

5.3 Regional Revenue Distribution

5.4 Segment Revenue Analysis

5.5 Distribution Channel Analysis

5.6 Clinical & Healthcare Impact Analysis

Market Segmentation (USD Billion), 2026–2033

6.1 By Product Type

6.1.1 Molecular Assays

6.1.1.1 PCR-Based Molecular Testing Systems

6.1.1.1.1 High-Sensitivity Compatibility Assays

6.1.1.1.1.1 AI-Assisted Molecular Diagnostic Platforms

6.1.2 HLA Typing Systems

6.1.2.1 High-Resolution HLA Typing Technologies

6.1.2.1.1 Genomic Compatibility Testing Platforms

6.1.2.1.1.1 Precision Immunogenetics Systems

6.1.3 Antibody Screening Assays

6.1.3.1 Donor-Specific Antibody Detection Systems

6.1.3.1.1 Crossmatching Diagnostic Platforms

6.1.3.1.1.1 Rejection Risk Assessment Technologies

6.1.4 Non-Molecular Assays

6.1.4.1 Serological Testing Systems

6.1.4.1.1 Immunological Compatibility Assays

6.1.4.1.1.1 Conventional Transplant Screening Platforms

6.2 By Application

6.2.1 Kidney Transplantation

6.2.1.1 Renal Compatibility Testing

6.2.1.1.1 Kidney Donor Matching Platforms

6.2.1.1.1.1 Post-Transplant Rejection Monitoring Systems

6.2.2 Liver Transplantation

6.2.2.1 Hepatic Compatibility Diagnostics

6.2.2.1.1 Liver Donor Screening Systems

6.2.2.1.1.1 Liver Rejection Risk Assessment Platforms

6.2.3 Heart Transplantation

6.2.3.1 Cardiac Organ Compatibility Testing

6.2.3.1.1 Heart Transplant Immunogenetics Systems

6.2.3.1.1.1 Post-Cardiac Transplant Monitoring Technologies

6.2.4 Stem Cell Transplantation

6.2.4.1 Hematopoietic Stem Cell Matching

6.2.4.1.1 Bone Marrow Compatibility Testing

6.2.4.1.1.1 Advanced Immunogenetics Analysis Systems

6.2.5 Lung & Pancreas Transplantation

6.2.5.1 Thoracic & Pancreatic Organ Compatibility Testing

6.2.5.1.1 Specialized Organ Rejection Monitoring Systems

6.2.5.1.1.1 Multi-Organ Transplant Diagnostics Platforms

6.3 By Technology

6.3.1 Next-Generation Sequencing (NGS)

6.3.1.1 High-Throughput Genomic Sequencing Systems

6.3.1.1.1 Precision HLA Sequencing Platforms

6.3.1.1.1.1 AI-Driven Genomic Compatibility Analytics

6.3.2 PCR-Based Diagnostics

6.3.2.1 Real-Time PCR Testing Systems

6.3.2.1.1 Molecular Compatibility Assays

6.3.2.1.1.1 Infectious Disease Screening PCR Platforms

6.3.3 Flow Cytometry

6.3.3.1 Crossmatching & Antibody Screening Systems

6.3.3.1.1 Immunophenotyping Platforms

6.3.3.1.1.1 Advanced Cellular Compatibility Analysis Systems

6.3.4 Microarray Technologies

6.3.4.1 Genomic Microarray Platforms

6.3.4.1.1 Multiplex Compatibility Analysis Systems

6.3.4.1.1.1 High-Resolution Immunogenetics Platforms

6.4 By End User

6.4.1 Hospitals & Transplant Centers

6.4.1.1 Multi-Specialty Transplant Hospitals

6.4.1.1.1 Organ Transplantation Units

6.4.1.1.1.1 Advanced Immunogenetics Laboratories

6.4.2 Diagnostic Laboratories

6.4.2.1 Independent Molecular Diagnostics Laboratories

6.4.2.1.1 Specialized Transplant Testing Facilities

6.4.2.1.1.1 High-Throughput Compatibility Testing Centers

6.4.3 Research Institutions

6.4.3.1 Academic Immunogenetics Research Centers

6.4.3.1.1 Transplant Biology Research Programs

6.4.3.1.1.1 Genomic Medicine Research Laboratories

6.5 By Distribution Channel

6.5.1 Direct Sales

6.5.1.1 Manufacturer-Integrated Diagnostic Systems

6.5.1.1.1 Institutional Procurement Contracts

6.5.1.1.1.1 Enterprise Laboratory Solutions

6.5.2 Third-Party Distributors

6.5.2.1 Regional Diagnostics Equipment Suppliers

6.5.2.1.1 Molecular Testing Distribution Networks

6.5.2.1.1.1 Healthcare Diagnostics Partnerships

6.5.3 Laboratory Service Providers

6.5.3.1 Specialized Transplant Testing Service Networks

6.5.3.1.1 Outsourced Molecular Diagnostic Services

6.5.3.1.1.1 Integrated Clinical Testing Platforms

Market Segmentation by Geography

7.1 North America

7.2 Europe

7.3 Asia-Pacific

7.4 Latin America

7.5 Middle East & Africa

Competitive Landscape

8.1 Market Share Analysis

8.2 Product Portfolio Benchmarking

8.3 Product Positioning Mapping

8.4 Strategic Partnerships & Genomic Diagnostics Ecosystems

8.5 Competitive Intensity & Innovation Benchmarking

Company Profiles

9.1 Thermo Fisher Scientific

9.2 QIAGEN

9.3 Bio-Rad Laboratories

9.4 F. Hoffmann-La Roche Ltd.

9.5 Immucor

9.6 CareDx

9.7 Illumina

9.8 Biofortuna

Strategic Intelligence & Pheonix AI Insights

10.1 Pheonix Demand Forecast Engine

10.2 Supply Chain & Infrastructure Analyzer

10.3 Technology & Innovation Tracker

10.4 Product Development Insights

10.5 Automated Porter’s Five Forces Analysis

Future Outlook & Strategic Recommendations

11.1 Expansion of AI-Assisted Transplant Compatibility Testing

11.2 Growth of Personalized Genomic Diagnostics

11.3 Increasing Adoption of Cloud-Based Monitoring Platforms

11.4 Laboratory Automation & Workflow Optimization Strategies

11.5 Long-Term Market Outlook (2033+)

Appendix

About Pheonix Research

Disclaimer

Competitive Landscape

Global Transplant Diagnostics Market Competitive Intensity & Market Structure Overview

The Global Transplant Diagnostics Market is characterized by a moderately consolidated structure with high competitive intensity, driven by the increasing convergence of molecular diagnostics, genomics, AI-powered healthcare analytics, and precision medicine technologies. The market is dominated by a group of established global diagnostics companies with strong expertise in immunogenetics, molecular sequencing, and transplantation compatibility testing.

Leading companies such as Thermo Fisher Scientific, QIAGEN, Bio-Rad Laboratories, F. Hoffmann-La Roche Ltd., and Illumina are shaping market dynamics through advanced molecular assays, next-generation sequencing (NGS), HLA typing systems, and AI-assisted transplant analytics.

Competitive intensity is primarily driven by technological innovation, genomic sequencing capabilities, regulatory compliance, clinical accuracy, laboratory automation, and integration of AI-powered transplant analytics platforms. The increasing adoption of precision transplantation and personalized medicine is further intensifying market competition globally.

Global Transplant Diagnostics Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

- Thermo Fisher Scientific: Global leader in molecular diagnostics, transplant compatibility testing, and genomic analysis platforms.

- QIAGEN: Provider of molecular testing technologies, PCR diagnostics, and transplant genomics solutions.

- Bio-Rad Laboratories: Developer of transplant diagnostics systems, antibody screening technologies, and laboratory automation platforms.

- F. Hoffmann-La Roche Ltd.: Diagnostics company focused on molecular assays, PCR technologies, and precision healthcare platforms.

- Immucor: Specialist in immunogenetics, HLA typing, and transplant compatibility testing solutions.

- CareDx: Provider of AI-assisted transplant monitoring and organ rejection surveillance technologies.

- Illumina: Leader in next-generation sequencing platforms supporting high-resolution transplant compatibility analysis.

- Biofortuna: Developer of HLA typing reagents and transplant diagnostic solutions.

Key Competitive Intensity & Market Structure Signals in Global Transplant Diagnostics Market

Several signals define the competitive dynamics of the market:

- The increasing adoption of next-generation sequencing (NGS), digital PCR, and AI-powered compatibility analysis highlights a highly innovation-driven competitive structure.

- Growing emphasis on precision medicine and personalized transplantation strategies is accelerating investment in advanced molecular diagnostics technologies.

- Regulatory oversight related to transplantation safety, infectious disease testing, and organ compatibility diagnostics is increasing barriers to entry and favoring established diagnostics companies.

- Strategic collaborations between biotechnology firms, transplant centers, genomic sequencing providers, and healthcare AI companies are reshaping the transplant diagnostics ecosystem.

- Competitive differentiation is increasingly based on clinical accuracy, turnaround speed, laboratory automation, genomic analytics capabilities, and AI-assisted compatibility prediction.

- Cloud-based transplant monitoring systems and digital pathology integration are becoming key competitive advantages for advanced diagnostics providers.

- Increasing transplantation procedure volumes globally are driving long-term demand for scalable and automated transplant diagnostics platforms.

Strategic Implications of Competitive Intensity & Market Structure in Global Transplant Diagnostics Market

The competitive structure creates several strategic implications:

- Continuous investment in molecular diagnostics, genomic sequencing, and AI-assisted transplant analytics is essential for maintaining market leadership.

- Regulatory compliance, laboratory accreditation, and clinical validation capabilities are major competitive barriers, strengthening the position of established diagnostics companies.

- Integration of cloud-based healthcare systems, digital pathology, and real-time transplant monitoring platforms is becoming increasingly important for competitive differentiation.

- Strategic partnerships with hospitals, transplant centers, and genomic research institutions are critical for expanding market penetration and improving clinical adoption.

- Companies focusing on high-throughput sequencing technologies, automated diagnostics workflows, and personalized transplant monitoring systems are expected to gain substantial competitive advantages.

- Increasing demand for rapid, highly sensitive, and predictive transplant diagnostics is accelerating innovation in AI-powered compatibility testing.

- Expansion of precision healthcare ecosystems and personalized medicine initiatives will continue reshaping competitive dynamics across the market.

Global Transplant Diagnostics Market Competitive Intensity & Market Structure Forward Outlook

Looking ahead, the Global Transplant Diagnostics Market is expected to maintain its moderately consolidated structure with sustained high competitive intensity, supported by growing transplantation volumes and increasing adoption of precision diagnostics technologies.

- AI-assisted transplant analytics and predictive rejection monitoring systems will become increasingly mainstream across transplantation workflows.

- Next-generation sequencing technologies will continue transforming donor-recipient compatibility analysis and personalized transplant diagnostics.

- Integration of cloud-connected laboratory systems and digital pathology platforms will intensify technology competition across the market.

- Healthcare providers are expected to increasingly adopt automated and high-throughput transplant diagnostics systems to improve workflow efficiency and clinical accuracy.

- Strategic acquisitions, biotechnology collaborations, and genomic healthcare partnerships are expected to accelerate market consolidation and innovation.

- Rising investments in transplantation infrastructure, organ donation programs, and personalized medicine will continue driving long-term market expansion globally.

In conclusion, the Global Transplant Diagnostics Market represents a high-growth, precision medicine-driven, and technologically advanced competitive landscape, where genomic innovation, AI integration, regulatory capability, and laboratory automation will determine long-term market leadership.

Value Chain

Global Transplant Diagnostics Market Value Chain & Supply Chain Evolution Overview

The Global Transplant Diagnostics Market is undergoing rapid transformation driven by advancements in molecular diagnostics, genomic sequencing, AI-powered healthcare systems, and increasing transplantation procedures worldwide. The market’s value chain is characterized by a hybrid operational model supported by a hybrid distribution structure integrating direct manufacturer sales, laboratory service providers, diagnostic distributors, and healthcare institutions. This interconnected framework is reshaping transplant compatibility testing, laboratory workflows, and precision medicine integration across global healthcare systems.

A defining feature of this value chain is the increasing convergence of molecular diagnostics, immunogenetics, genomic medicine, and AI-assisted compatibility analysis. Transplant diagnostics technologies increasingly combine next-generation sequencing (NGS), PCR-based assays, HLA typing systems, antibody screening platforms, cloud-based monitoring systems, and predictive analytics to improve donor-recipient matching accuracy and reduce organ rejection risks.

Supply chain complexity remains high due to stringent regulatory requirements, specialized laboratory infrastructure, genomic sequencing dependencies, and the integration of advanced healthcare technologies. Companies must coordinate across reagent sourcing, sequencing platform manufacturing, laboratory automation systems, software integration, cloud-based healthcare infrastructure, and clinical compliance standards while maintaining high diagnostic precision and workflow efficiency.

Manufacturers and diagnostics providers are increasingly investing in automated molecular testing platforms, AI-enabled transplant analytics, cloud-connected laboratory systems, and scalable genomic sequencing infrastructure to improve operational efficiency and transplantation outcomes. The value chain is evolving into a highly integrated, precision-driven, and data-centric healthcare ecosystem focused on personalized transplantation strategies and long-term patient monitoring.

Global Transplant Diagnostics Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Material & Reagent Sourcing: Molecular reagents, antibodies, sequencing chemicals, PCR consumables, bioinformatics infrastructure, and laboratory-grade materials

- Manufacturing & Platform Development: Molecular assay production, HLA typing systems, sequencing platform manufacturing, laboratory automation equipment, and diagnostic kit assembly

- Technology Integration: AI-assisted transplant analytics, cloud-based transplant monitoring, genomic sequencing software, digital pathology integration, and laboratory informatics systems

- Regulatory & Compliance Management: FDA and EMA transplant diagnostics compliance, laboratory quality assurance, infectious disease testing protocols, and clinical validation systems

- Distribution: Direct manufacturer sales, diagnostic distributors, laboratory service providers, and healthcare procurement networks

- End User Utilization: Hospitals, transplant centers, diagnostic laboratories, academic institutions, and research organizations

Company-to-Stage Mapping

- Raw Material & Reagent Sourcing: Biotechnology reagent suppliers, genomic consumable manufacturers, laboratory chemical providers

- Manufacturing & Platform Development: Thermo Fisher Scientific, QIAGEN, Bio-Rad Laboratories

- Technology Integration: Illumina, CareDx, F. Hoffmann-La Roche Ltd.

- Regulatory & Compliance Management: FDA, EMA, transplant diagnostic regulatory bodies, laboratory accreditation agencies

- Distribution: Healthcare distributors, laboratory service providers, hospital procurement channels

- End User Utilization: Transplant hospitals, molecular diagnostics laboratories, transplant research institutes

Key Value Chain & Supply Chain Evolution Signals in Global Transplant Diagnostics Market

- Expansion of Next-Generation Sequencing (NGS) Technologies

Increasing adoption of NGS platforms is improving donor-recipient compatibility analysis and high-resolution HLA typing precision. - Growth of AI-Assisted Compatibility Analytics

AI-powered transplant diagnostics and predictive analytics are improving transplant success rates and reducing rejection risks. - Integration of Cloud-Based Transplant Monitoring Platforms

Digital healthcare ecosystems and real-time transplant monitoring systems are transforming clinical workflows and patient management. - Increasing Regulatory Oversight & Compliance Requirements

Regulatory agencies are strengthening standards related to transplantation safety, infectious disease screening, and diagnostic validation. - Laboratory Automation & High-Throughput Diagnostics Expansion

Automation technologies are improving workflow efficiency, scalability, and turnaround times for transplant testing procedures. - Convergence of Precision Medicine & Genomic Healthcare

Personalized medicine initiatives are accelerating adoption of advanced molecular diagnostics and genomic compatibility testing platforms.

Strategic Implications of Value Chain & Supply Chain Evolution

- Investment in Precision Diagnostics & Genomic Infrastructure

Companies investing in NGS, AI-powered analytics, and high-resolution compatibility testing will strengthen long-term competitiveness. - Expansion of Automated & Cloud-Connected Laboratory Systems

Integrated laboratory informatics and cloud monitoring platforms are improving operational scalability and workflow efficiency. - Strengthening Regulatory & Clinical Validation Capabilities

Compliance with evolving transplantation regulations and quality assurance standards is essential for healthcare adoption. - Optimization of Molecular Testing Supply Chains

Efficient reagent sourcing, sequencing capacity management, and laboratory automation are critical for operational stability. - Development of Integrated Transplant Diagnostics Ecosystems

Convergence between diagnostics, genomic medicine, and AI healthcare systems is reshaping transplant care delivery models. - Localization of Diagnostic Infrastructure & Testing Capabilities

Regional laboratory expansion and localized sequencing capabilities improve healthcare accessibility and supply chain resilience.

Global Transplant Diagnostics Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the value chain is expected to evolve into a highly automated, AI-driven, and precision-focused healthcare ecosystem.

Key Future Developments Include:

- Expansion of AI-assisted donor-recipient compatibility analysis and predictive transplant analytics

- Increased adoption of next-generation sequencing and high-resolution HLA typing technologies

- Growth of cloud-connected transplant monitoring and digital pathology systems

- Integration of laboratory automation and high-throughput molecular testing platforms

- Expansion of precision medicine and personalized transplantation ecosystems

As the market evolves, competitive advantage will increasingly depend on the ability to combine genomic innovation, laboratory automation, regulatory compliance, and scalable healthcare infrastructure.

Companies that effectively integrate molecular diagnostics, AI-powered analytics, and cloud-connected transplant monitoring platforms will achieve superior clinical accuracy, operational efficiency, and long-term competitive positioning in the Global Transplant Diagnostics Market.

Investment Activity

Global Transplant Diagnostics Market Investment & Funding Dynamics Overview

The investment and funding landscape within the Global Transplant Diagnostics Market is characterized by steadily rising investment activity and high capital intensity, driven by increasing organ transplantation procedures, expanding precision medicine adoption, and rapid advancements in molecular diagnostics technologies. Structural drivers such as rising chronic disease prevalence, increasing organ failure cases, growing organ donation awareness, and expansion of transplantation infrastructure are attracting substantial long-term capital inflows into the market. Investments are primarily focused on molecular diagnostics platforms, next-generation sequencing (NGS), AI-assisted transplant analytics, laboratory automation systems, and cloud-based transplant monitoring technologies.

A major factor influencing investment dynamics in this market is the growing technological sophistication of transplant diagnostics. Modern transplant compatibility testing increasingly integrates genomic sequencing, AI-driven donor-recipient matching algorithms, high-resolution HLA typing, and predictive analytics for rejection risk assessment. These innovations require substantial investment in R&D, bioinformatics infrastructure, laboratory automation, and digital healthcare integration. As a result, diagnostics companies, biotechnology firms, and healthcare technology providers are heavily investing in advanced immunogenetics and precision transplant diagnostics platforms.

Additionally, increasing regulatory requirements related to transplantation safety, infectious disease screening, and diagnostic accuracy are encouraging investments in clinical validation, quality assurance systems, and compliance-focused laboratory infrastructure. Governments and healthcare institutions are also increasing funding for transplantation programs and precision healthcare initiatives to improve long-term transplant outcomes.

Global Transplant Diagnostics Market Investment & Funding Dynamics Current Scenario

In the current scenario, the Global Transplant Diagnostics Market is witnessing strong and strategically driven investment activity supported by increasing demand for personalized transplantation strategies and high-precision compatibility testing. The market’s high capital intensity reflects significant financial commitments required for genomic sequencing infrastructure, molecular diagnostics laboratories, AI healthcare integration, and advanced laboratory automation systems.

Investment activity is particularly concentrated in next-generation sequencing technologies, molecular assay development, AI-based transplant analytics, antibody screening platforms, and cloud-connected transplant monitoring systems. Companies are allocating substantial capital toward improving diagnostic sensitivity, reducing turnaround times, and enhancing predictive capabilities for donor-recipient compatibility and rejection risk analysis.

The market is also experiencing active merger and acquisition (M&A) activity as molecular diagnostics companies, biotechnology firms, and genomic technology providers seek to strengthen technological capabilities, expand transplant diagnostics portfolios, and improve global market reach. Strategic collaborations between transplant centers, diagnostic laboratories, AI healthcare companies, and genomic sequencing providers are accelerating commercialization and adoption of advanced transplant diagnostics solutions.

Furthermore, the funding ecosystem is increasingly supported by government healthcare investments, institutional healthcare funding, venture capital activity in precision medicine, and increasing investments in laboratory digitization and genomic medicine infrastructure.

Key Investment & Funding Dynamics Signals in Global Transplant Diagnostics Market

The investment and funding dynamics in the Global Transplant Diagnostics Market are shaped by several key signals reflecting the transformation of transplant healthcare delivery. One of the primary signals is the rapid adoption of precision medicine and personalized transplantation strategies, which is driving continuous investment in high-resolution compatibility testing and genomic analytics technologies.

Another major signal is the increasing adoption of next-generation sequencing (NGS) and AI-driven transplant diagnostics platforms. Healthcare providers and diagnostics manufacturers are investing heavily in high-throughput sequencing technologies, automated laboratory systems, and predictive analytics tools to improve transplant success rates and minimize rejection risks.

The rising global volume of organ transplantation procedures is also strengthening long-term investment confidence within the market. Increasing kidney, liver, heart, lung, and stem cell transplantation activities are creating sustained demand for advanced compatibility testing and post-transplant monitoring solutions.

Regulatory developments surrounding transplantation safety, infectious disease testing, and laboratory quality standards are creating additional investment momentum. Companies are investing heavily in regulatory approvals, laboratory compliance systems, clinical validation studies, and cybersecurity infrastructure for digital healthcare integration.

Additionally, the growing integration of cloud-based healthcare systems, digital pathology, and AI-assisted transplant monitoring platforms is driving investments in connected healthcare ecosystems and real-time patient monitoring technologies.

Strategic Implications of Investment & Funding Dynamics in Global Transplant Diagnostics Market

The current investment dynamics have significant strategic implications for companies operating in the Global Transplant Diagnostics Market. One of the primary implications is the need for continuous technological innovation and precision diagnostics development to maintain competitive positioning in a rapidly evolving healthcare environment.

High capital intensity requires companies to strategically allocate resources toward genomic sequencing capabilities, laboratory automation, AI software development, cloud integration, and regulatory compliance systems. Companies capable of delivering highly accurate, scalable, and automated transplant diagnostics solutions will strengthen long-term competitive advantages.

The increasing role of M&A activity highlights the growing importance of technological consolidation and ecosystem expansion. Companies are leveraging acquisitions and strategic partnerships to strengthen molecular diagnostics capabilities, expand precision medicine portfolios, and accelerate AI integration within transplant workflows.

Furthermore, the increasing digitization of transplant healthcare systems is reshaping business strategies across the market. Investments in AI-driven compatibility analysis, digital pathology, cloud-based monitoring, and integrated laboratory information systems are enabling improved clinical decision-making and operational efficiency.

Global Transplant Diagnostics Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the investment and funding dynamics in the Global Transplant Diagnostics Market are expected to remain highly positive, driven by increasing transplantation demand, rapid advancements in genomic medicine, and growing adoption of AI-powered precision diagnostics. The continued shift toward personalized healthcare and predictive transplant analytics will attract substantial long-term investments into the market.

Technological innovation will remain a central investment focus, particularly in next-generation sequencing platforms, AI-assisted donor-recipient matching systems, automated molecular diagnostics, digital pathology integration, and real-time transplant monitoring technologies. These advancements are expected to improve diagnostic accuracy, reduce rejection risks, and optimize long-term transplant outcomes.

Future investment trends will also emphasize laboratory automation, healthcare interoperability, cloud-connected diagnostics infrastructure, and scalable precision medicine ecosystems to support broader global adoption of advanced transplant diagnostics solutions.

Additionally, increasing investments in organ donation programs, transplantation infrastructure, and digital healthcare transformation initiatives will continue supporting market expansion across both developed and emerging economies.

In summary, the Global Transplant Diagnostics Market is positioned for sustained long-term investment activity supported by increasing transplantation procedures, precision medicine adoption, and ongoing technological innovation in molecular diagnostics and genomic healthcare. Companies that strategically invest in AI-driven diagnostics, genomic sequencing, laboratory automation, and integrated healthcare ecosystems will be best positioned to capture future market opportunities.

Technology & Innovation

Global Transplant Diagnostics Market Technology & Innovation Landscape Overview

The Global Transplant Diagnostics Market is undergoing rapid technological transformation driven by advancements in molecular diagnostics, genomic sequencing, AI-powered compatibility analytics, and precision medicine platforms. The market is characterized by a high innovation intensity level, reflecting accelerated adoption of advanced immunogenetics technologies and increasing integration of digital healthcare ecosystems into transplantation workflows.

At the center of this transformation are next-generation sequencing (NGS), PCR-based diagnostics, AI-assisted transplant analytics, cloud-based transplant monitoring platforms, digital pathology systems, and high-resolution HLA typing technologies. These innovations are significantly improving donor-recipient compatibility analysis, reducing transplant rejection risks, and enhancing long-term transplant outcomes.

AI-integrated transplant diagnostics platforms are increasingly being used to automate compatibility analysis, predict rejection risks, optimize organ allocation strategies, and improve post-transplant monitoring accuracy. Machine learning algorithms can process large-scale genomic and immunological datasets to support highly personalized transplantation decisions and improve clinical workflow efficiency.

Another major technological advancement is the growing adoption of high-throughput genomic sequencing technologies and automated molecular diagnostics systems. Next-generation sequencing and digital PCR platforms are enabling highly sensitive compatibility testing, improved immunogenetics profiling, and faster turnaround times for transplantation procedures.

The market is also witnessing increasing integration of cloud-connected healthcare systems, digital pathology platforms, and laboratory automation technologies. These systems enable real-time transplant monitoring, remote clinical collaboration, centralized data management, and predictive transplant analytics.

Technological advancements in microarray platforms, flow cytometry systems, biomarker analytics, and AI-driven predictive diagnostics are further reshaping transplantation workflows and supporting expansion of personalized organ compatibility testing globally.

Global Transplant Diagnostics Market Technology & Innovation Landscape Current Scenario

Currently, the Global Transplant Diagnostics Market demonstrates high patent activity and increasing investments in molecular diagnostics, AI healthcare systems, genomic medicine, and laboratory automation technologies.

1. AI-Assisted Compatibility Analysis

AI-driven transplant analytics platforms are improving donor-recipient matching accuracy, rejection prediction, and personalized transplantation planning.

2. Next-Generation Sequencing Expansion

NGS technologies are rapidly becoming central to high-resolution HLA typing and precision immunogenetics diagnostics.

3. High-Throughput Molecular Diagnostics

Automated molecular testing platforms are improving workflow efficiency, scalability, and turnaround times for transplant diagnostics.

4. Cloud-Based Transplant Monitoring

Cloud-connected healthcare systems are enabling centralized transplant data management, remote collaboration, and real-time post-transplant monitoring.

5. Digital Pathology & Biomarker Analytics

Digital pathology systems and biomarker-based diagnostics are improving transplant rejection assessment and long-term patient monitoring.

6. Laboratory Automation Integration

Healthcare providers are increasingly adopting laboratory automation systems to optimize transplant testing workflows and improve operational efficiency.

Key Technology & Innovation Landscape Signals in Global Transplant Diagnostics Market

The market is evolving rapidly through several major innovation signals:

1. Rapid Growth of Precision Transplantation

Healthcare systems are increasingly prioritizing personalized transplantation strategies based on genomic and immunological profiling.

2. AI Integration Across Diagnostics Workflows

AI-assisted predictive analytics and machine learning algorithms are becoming key differentiators in transplant compatibility assessment.

3. Expansion of Genomic Sequencing Technologies

High-resolution sequencing platforms are increasingly replacing conventional transplant compatibility testing methods.

4. Increasing Adoption of Automated Diagnostics

Laboratory automation and high-throughput testing platforms are improving transplant diagnostics scalability and efficiency.

5. Growth of Digital Healthcare Ecosystems

Cloud-based transplant monitoring systems and integrated healthcare data platforms are reshaping transplantation workflows.

6. Rising Demand for Real-Time Monitoring

Healthcare providers are increasingly utilizing continuous post-transplant monitoring and predictive rejection analytics technologies.

Strategic Implications of Technology & Innovation Landscape in Global Transplant Diagnostics Market

The evolving technology landscape is significantly transforming competitive dynamics within the market. Companies are increasingly competing on genomic precision, AI analytics capabilities, laboratory automation, cloud connectivity, and diagnostic sensitivity rather than solely on conventional compatibility testing methods.

The convergence of transplant diagnostics with AI healthcare systems, genomic medicine, digital pathology, and cloud-based healthcare ecosystems is creating opportunities for highly integrated and personalized transplantation management platforms.

Healthcare providers are increasingly investing in advanced molecular diagnostics infrastructure, automated testing systems, and predictive transplant analytics to improve transplant success rates and optimize clinical outcomes.

Manufacturers are also investing heavily in cybersecurity, data interoperability, clinical validation, and regulatory compliance due to increasing oversight surrounding transplant safety, genomic data management, and diagnostic reliability.

Strategic collaborations between diagnostics companies, transplant centers, biotechnology firms, genomic sequencing providers, and AI healthcare platforms are accelerating commercialization and reshaping competitive dynamics globally.

Global Transplant Diagnostics Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026–2033, the Global Transplant Diagnostics Market is expected to evolve toward highly connected, AI-driven, and precision-focused transplantation ecosystems.

Future technological developments are likely to include:

1. AI-Powered Predictive Transplant Analytics

Advanced AI systems capable of predicting transplant rejection risks, long-term organ compatibility, and personalized immunosuppression strategies.

2. Expanded Genomic & Multi-Omics Diagnostics

Broader integration of genomics, proteomics, transcriptomics, and biomarker analytics into transplantation workflows.

3. Fully Automated Molecular Diagnostics

Increasing deployment of high-throughput automated laboratory systems for rapid compatibility analysis and transplant monitoring.

4. Cloud-Integrated Transplant Ecosystems

Seamless interoperability between transplant centers, laboratories, healthcare providers, and digital healthcare platforms.

5. Real-Time Remote Monitoring Technologies

Expansion of continuous post-transplant monitoring systems using wearable biosensors and connected healthcare platforms.

6. Personalized Organ Compatibility Testing

Growth of individualized transplantation strategies supported by AI, precision medicine, and advanced immunogenetics technologies.

Overall, companies that successfully combine AI innovation, genomic diagnostics, laboratory automation, cloud connectivity, clinical precision, regulatory compliance, and cost efficiency will be best positioned to lead the next phase of growth within the Global Transplant Diagnostics Market.

Market Risk

Global Transplant Diagnostics Market Risk Factors & Disruption Threats Overview

The Global Transplant Diagnostics Market is influenced by a complex combination of technological, regulatory, clinical, and operational risk factors that shape market stability and long-term growth potential. As transplant diagnostics play a critical role in donor-recipient compatibility assessment, rejection monitoring, and transplantation safety, the market operates within a highly regulated and clinically sensitive environment.

The overall market risk level is moderate-to-high, driven by strict regulatory requirements, high technological complexity, reimbursement variability, and dependence on advanced molecular diagnostic infrastructure. The market also faces operational challenges related to laboratory standardization, test accuracy, organ availability constraints, and healthcare affordability across developing regions.

Geopolitical exposure is moderate, as transplant diagnostics systems rely heavily on globally interconnected supply chains involving reagents, sequencing systems, PCR consumables, laboratory automation equipment, and semiconductor-enabled diagnostic instruments. International trade restrictions, geopolitical tensions, and disruptions in biotechnology supply chains may affect manufacturing continuity, pricing stability, and diagnostic accessibility.

Substitution risk is low-to-moderate, because transplant diagnostics are considered clinically essential for organ compatibility assessment and post-transplant monitoring. However, conventional serological testing methods, manual crossmatching techniques, and emerging AI-driven predictive healthcare models may partially substitute certain advanced molecular diagnostics workflows in cost-sensitive healthcare environments.

Global Transplant Diagnostics Market Risk Factors & Disruption Threats Current Scenario

Currently, the transplant diagnostics market is experiencing rapid technological advancement alongside intensifying regulatory scrutiny and operational complexity. One of the most significant risks involves the high cost and infrastructure requirements associated with advanced molecular diagnostics technologies, including next-generation sequencing (NGS), digital PCR, and automated HLA typing systems.

Healthcare providers and diagnostic laboratories face increasing pressure to balance diagnostic accuracy with cost efficiency. In emerging economies, limited access to advanced transplant infrastructure and reimbursement limitations continue to restrict adoption of high-end transplant diagnostics platforms.

Another major challenge is the increasing complexity of regulatory compliance. Regulatory agencies are tightening standards surrounding transplantation safety, infectious disease screening, genomic testing validation, laboratory accreditation, and patient data protection. These evolving requirements increase operational costs and extend product commercialization timelines.

Supply chain dependency remains another critical risk factor. The market depends heavily on specialized reagents, sequencing consumables, laboratory automation systems, and precision diagnostic instruments. Disruptions in biotechnology manufacturing or logistics networks may delay transplantation workflows and increase diagnostic costs.

Additionally, cybersecurity and healthcare data privacy concerns are becoming increasingly important due to growing integration of cloud-based transplant monitoring systems, AI-driven compatibility analysis, and digital pathology platforms.

Key Risk Factors & Disruption Threats Signals in Global Transplant Diagnostics Market

Several major signals highlight the evolving risk landscape within the market:

- Regulatory Compliance Intensification – Increasing oversight on genomic diagnostics, transplant safety, laboratory accreditation, and AI-assisted diagnostics is raising compliance complexity.

- High Capital & Infrastructure Costs – Advanced transplant diagnostics systems require substantial investment in sequencing platforms, laboratory automation, and skilled personnel.

- Supply Chain Dependency – Reliance on specialized reagents, consumables, semiconductors, and diagnostic instruments creates operational vulnerability.

- Organ Availability Constraints – Limited organ donation rates globally may indirectly impact transplantation procedure volumes and diagnostic demand.

- Cybersecurity & Data Privacy Risks – Cloud-connected transplant monitoring platforms face increasing exposure to healthcare cybersecurity threats.

- Healthcare Reimbursement Variability – Inconsistent reimbursement frameworks for advanced molecular diagnostics may limit adoption in certain healthcare systems.

- Clinical Accuracy & Validation Risks – High sensitivity requirements for donor-recipient matching create pressure for continuous validation and quality assurance.

- Competition from Alternative Diagnostic Methods – Conventional serological testing and lower-cost compatibility assessment techniques continue competing in cost-sensitive regions.

- Workforce & Laboratory Skill Shortages – Shortage of trained molecular diagnostics professionals may limit operational scalability in some regions.

Strategic Implications of Risk Factors & Disruption Threats

These risk factors are significantly reshaping strategic priorities across the transplant diagnostics ecosystem. Companies are increasingly focusing on automation, AI integration, high-throughput sequencing technologies, and workflow standardization to improve efficiency and reduce operational complexity.

Manufacturers are also prioritizing regulatory harmonization, cybersecurity infrastructure, and cloud-based healthcare integration to strengthen compliance and long-term market positioning.

Strategic collaborations between diagnostics companies, transplant centers, genomic sequencing firms, AI healthcare providers, and laboratory service organizations are becoming increasingly important to accelerate technology adoption and improve clinical outcomes.

In addition, companies are investing heavily in scalable molecular diagnostics platforms capable of reducing turnaround times while improving compatibility accuracy and transplant success rates.

Supply chain diversification and localized manufacturing strategies are also emerging as critical priorities to mitigate geopolitical disruptions and logistics instability.

Global Transplant Diagnostics Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026–2033, the transplant diagnostics market is expected to remain innovation-driven while facing increasing regulatory, operational, and technological disruption risks. Precision medicine, genomic healthcare, and AI-assisted transplant analytics will continue transforming the competitive landscape.

Future disruption risks are expected to include:

- Stricter genomic diagnostics regulations and validation requirements

- Increasing cybersecurity and patient data protection standards

- Rising costs associated with advanced sequencing technologies

- Supply chain instability affecting molecular diagnostics consumables

- Pressure to improve affordability and reimbursement accessibility

- Shortage of specialized molecular diagnostics professionals

- Rapid technology obsolescence due to continuous innovation cycles

- Growing competition from integrated AI healthcare platforms

- Operational risks related to laboratory automation scalability

At the same time, advancements in AI-powered transplant analytics, predictive rejection monitoring, cloud-connected diagnostics ecosystems, and high-resolution genomic compatibility testing are expected to create substantial long-term growth opportunities.

Overall, the Global Transplant Diagnostics Market represents a strategically critical and clinically essential segment within modern healthcare infrastructure. Companies that successfully balance clinical accuracy, regulatory compliance, technological innovation, affordability, and operational scalability will be best positioned to capture sustainable long-term market growth.

Regulatory Landscape

Global Transplant Diagnostics Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a critical role in shaping the Global Transplant Diagnostics Market as transplantation procedures require highly accurate compatibility testing, infectious disease screening, and post-transplant monitoring to ensure patient safety and successful clinical outcomes. Regulatory frameworks governing transplant diagnostics are becoming increasingly stringent due to the growing complexity of molecular testing technologies, genomic analysis, and AI-assisted compatibility systems.

Regulatory authorities including the U.S. Food and Drug Administration, the European Medicines Agency, and regional healthcare agencies across Asia-Pacific are strengthening standards related to HLA typing, molecular compatibility testing, infectious disease screening, laboratory quality assurance, and genomic diagnostics validation. These regulations are designed to improve transplant safety, minimize organ rejection risks, and ensure clinical reliability across transplantation workflows.

The increasing adoption of next-generation sequencing (NGS), digital PCR, AI-driven transplant analytics, and cloud-based transplant monitoring platforms has expanded regulatory oversight into areas including software validation, cybersecurity compliance, data privacy protection, and interoperability standards. As transplant diagnostics become increasingly integrated with precision medicine ecosystems, regulators are emphasizing transparency, clinical validation, and quality control across diagnostic workflows.

International harmonization efforts surrounding laboratory accreditation, transplant testing standards, and molecular diagnostics quality management are also shaping global commercialization strategies for transplant diagnostics manufacturers.

Global Transplant Diagnostics Market Regulatory & Policy Environment Current Scenario

Currently, the Global Transplant Diagnostics Market operates within a highly regulated healthcare environment characterized by strict clinical validation requirements, laboratory compliance standards, and increasing oversight of genomic and AI-enabled diagnostics technologies.

One of the most important regulatory trends influencing the market is the growing emphasis on molecular diagnostic accuracy and high-resolution HLA typing validation. Regulatory agencies are requiring extensive analytical and clinical performance data to ensure compatibility testing reliability and minimize transplantation risks.

Another major development involves increasing oversight of infectious disease screening within transplantation workflows. Healthcare authorities are continuously updating transplantation safety standards to reduce the risk of donor-derived infections and improve transplant recipient outcomes.

The market is also witnessing growing regulation of AI-powered transplant analytics and cloud-connected diagnostic systems. As digital healthcare integration expands, regulatory agencies are strengthening standards related to software-as-a-medical-device (SaMD), cybersecurity resilience, algorithm transparency, and patient data protection.

Laboratory accreditation and quality assurance requirements are becoming increasingly important across transplant diagnostics operations. Healthcare providers and diagnostic laboratories must comply with strict quality management systems, proficiency testing standards, and laboratory automation validation protocols.

Additionally, governments and healthcare organizations are increasingly supporting organ transplantation infrastructure expansion through favorable healthcare policies, reimbursement frameworks, and national organ donation initiatives, which are further strengthening demand for advanced transplant diagnostics solutions.

Key Regulatory & Policy Environment Signals in Global Transplant Diagnostics Market

1. Expansion of Molecular Diagnostics & Genomic Testing Regulations

Regulatory agencies are increasing oversight of next-generation sequencing, PCR-based diagnostics, and high-resolution HLA typing technologies to improve transplant compatibility accuracy and patient safety.

2. Strengthening Infectious Disease Screening Standards

Authorities are implementing stricter transplantation safety protocols and donor screening requirements to reduce post-transplant infection risks.

3. Increasing Regulation of AI & Digital Healthcare Platforms

AI-assisted transplant analytics, cloud-based monitoring systems, and digital pathology platforms are becoming subject to enhanced software validation, cybersecurity, and interoperability requirements.

4. Growing Focus on Laboratory Quality & Accreditation

Diagnostic laboratories and transplantation centers must comply with increasingly rigorous quality assurance standards, laboratory accreditation requirements, and workflow validation protocols.

5. Expansion of Precision Medicine & Personalized Healthcare Policies

Healthcare systems are increasingly supporting precision transplantation strategies through reimbursement support, genomic medicine initiatives, and advanced diagnostics infrastructure investments.

Strategic Implications of Regulatory & Policy Environment in Global Transplant Diagnostics Market

The evolving regulatory environment creates both significant opportunities and operational challenges for transplant diagnostics companies. One of the most important strategic implications is the increasing need for regulatory expertise across molecular diagnostics validation, genomic testing compliance, laboratory accreditation, and AI healthcare governance.

Manufacturers must invest heavily in clinical validation studies, regulatory approvals, quality management systems, cybersecurity infrastructure, and laboratory automation technologies to maintain market competitiveness and healthcare provider trust.

The growing convergence between transplant diagnostics, genomics, AI healthcare systems, and cloud-based monitoring platforms is also reshaping competitive dynamics across the market. Companies capable of delivering integrated precision diagnostics ecosystems while maintaining strong regulatory compliance are expected to secure long-term strategic advantages.

Increasing regulatory emphasis on transplant safety, compatibility accuracy, and laboratory quality assurance is also encouraging strategic collaborations between diagnostics manufacturers, transplant centers, genomic sequencing providers, and healthcare institutions.

Additionally, evolving reimbursement frameworks and government investments in transplantation infrastructure are expected to improve market accessibility and accelerate adoption of advanced transplant diagnostics technologies globally.

Global Transplant Diagnostics Market Regulatory & Policy Environment Forward Outlook

Looking ahead to 2026–2033, the regulatory environment for transplant diagnostics is expected to become increasingly sophisticated, data-driven, and globally harmonized as healthcare systems continue prioritizing precision transplantation and personalized medicine.

Future regulatory frameworks are likely to place stronger emphasis on AI governance, genomic data management, software validation, laboratory automation oversight, and interoperability across digital healthcare ecosystems. Regulatory agencies may also introduce stricter standards surrounding predictive transplant analytics, real-time monitoring systems, and cloud-connected diagnostics platforms.

The increasing adoption of next-generation sequencing and AI-powered transplant analytics is expected to encourage broader regulatory harmonization between molecular diagnostics standards, digital health frameworks, and precision medicine regulations globally.

Healthcare policymakers are also expected to continue expanding organ donation initiatives, transplantation funding programs, and precision diagnostics reimbursement support to improve transplantation accessibility and clinical outcomes.

Additionally, cybersecurity compliance and patient data privacy regulations are likely to become even more critical as transplant diagnostics systems increasingly rely on cloud infrastructure, AI algorithms, and connected healthcare ecosystems.

Overall, the regulatory and policy environment will remain a foundational factor shaping innovation, commercialization, and competitive dynamics within the Global Transplant Diagnostics Market. Companies capable of balancing technological innovation, regulatory adaptability, clinical accuracy, and scalable diagnostics infrastructure will be best positioned to capture long-term market growth opportunities.