Global Urticaria Market Report, Size and Forecast 2026-2033

Global Urticaria Market Report, Size, Share and Forecast 2026–2033

Market Forecast Snapshot (2025–2033)

| Metric | Value |

|---|---|

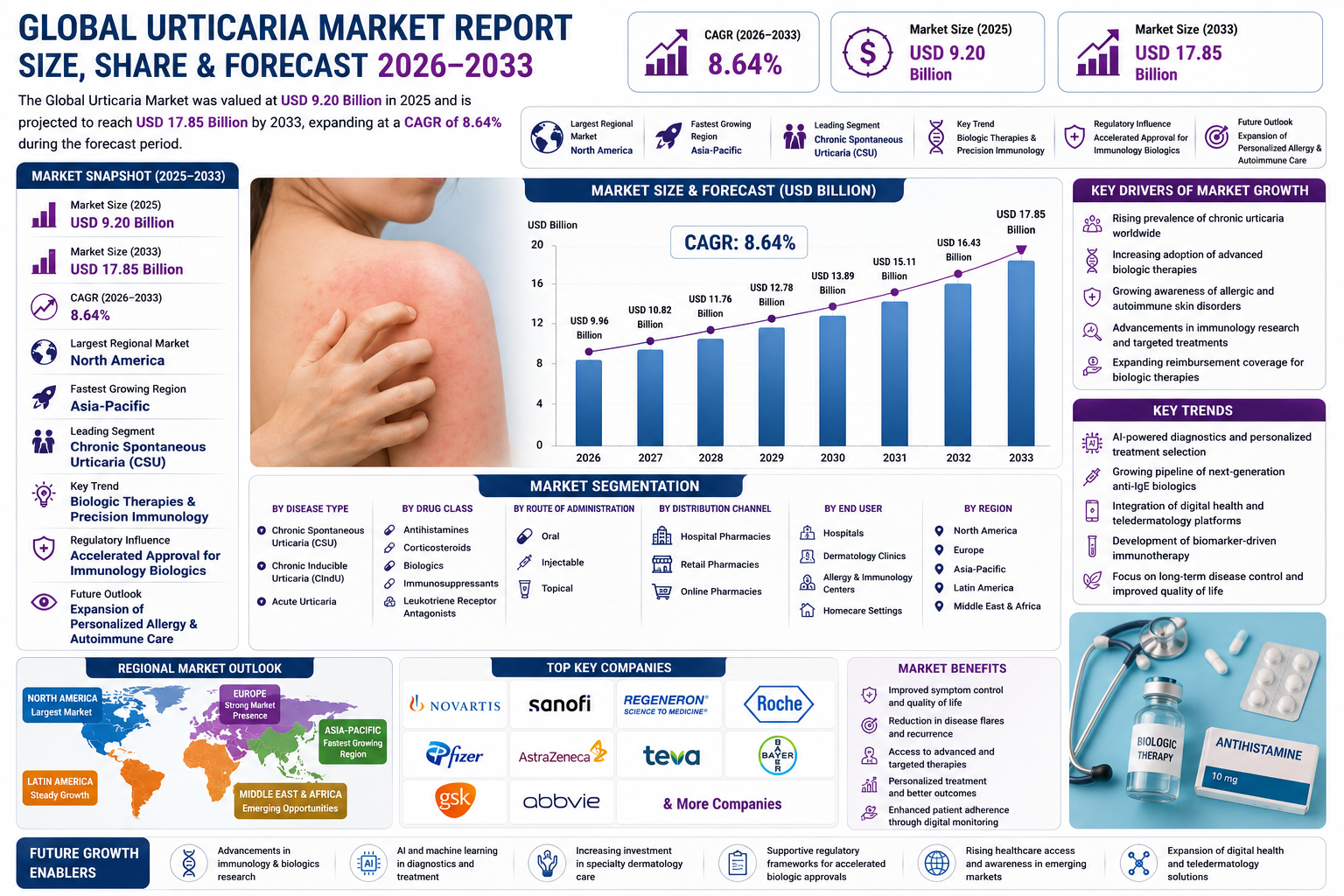

| Market Size (2025) | USD 9.20 Billion |

| Market Size (2033) | USD 17.85 Billion |

| CAGR (2026–2033) | 8.64% |

| Largest Regional Market | North America |

| Fastest Growing Region | Asia-Pacific |

| Leading Segment | Chronic Spontaneous Urticaria (CSU) |

| Key Trend | Biologic Therapies & Precision Immunology |

| Regulatory Influence | Accelerated Approval for Immunology Biologics |

| Future Outlook | Expansion of Personalized Allergy & Autoimmune Care |

Market Size & Forecast

The Global Urticaria Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 9.20 billion in 2025 and is projected to reach approximately USD 17.85 billion by 2033, expanding at a CAGR of 8.64%. The market growth is primarily driven by the rising prevalence of chronic urticaria, increasing awareness regarding allergic and autoimmune skin disorders, and growing adoption of advanced biologic therapies. The increasing burden of chronic spontaneous urticaria (CSU) and chronic inducible urticaria (CIndU) globally is creating substantial demand for effective long-term treatment solutions. The market is also benefiting from advancements in immunology research, targeted monoclonal antibody therapies, and personalized medicine approaches. Increasing diagnosis rates, improved healthcare access, and expanding reimbursement coverage for biologics are further supporting market growth. Additionally, pharmaceutical companies are heavily investing in next-generation anti-IgE therapies, mast cell stabilizers, and immune-modulating biologics, significantly reshaping the competitive landscape.Global Urticaria Market Overview

Urticaria, commonly referred to as hives, is a dermatological and immunological condition characterized by itchy wheals, swelling, redness, and inflammatory skin reactions. The disease may occur acutely or chronically and is often associated with allergic triggers, autoimmune disorders, infections, medications, or environmental stimuli. The urticaria treatment market includes antihistamines, corticosteroids, leukotriene receptor antagonists, immunosuppressants, biologics, and emerging targeted therapies. The growing transition from conventional symptomatic treatments toward targeted immunological therapies is transforming disease management strategies globally. Biologic therapies targeting IgE pathways, mast cells, and inflammatory cytokines are increasingly becoming central components of chronic urticaria management. The emergence of precision immunology and biomarker-driven therapeutic strategies is further accelerating innovation across the market. Moreover, digital health integration, AI-assisted diagnostics, and teledermatology platforms are improving patient access to urticaria management and long-term monitoring services.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid advancements in immunotherapy, monoclonal antibody development, and biologic drug research are significantly accelerating market commercialization. Pharmaceutical companies are increasingly focusing on targeted therapies capable of delivering improved efficacy with reduced adverse effects. The growing adoption of anti-IgE biologics and personalized immunomodulatory treatments is expanding the therapeutic landscape.Market Implications

Companies investing in next-generation biologics and precision immunology platforms are expected to strengthen long-term competitive positioning.2. Compliance and Risk Repricing

Regulatory agencies are increasingly supporting accelerated approval pathways for innovative immunology and rare disease therapies. However, stringent safety evaluations and pharmacovigilance requirements continue influencing biologic development timelines. The growing emphasis on long-term treatment efficacy and adverse event monitoring is shaping clinical trial standards and post-market surveillance practices.Market Implications

Manufacturers maintaining strong clinical validation and regulatory compliance frameworks are likely to gain faster commercialization advantages.3. Competitive and Value-Chain Reconfiguration

The urticaria market is witnessing increasing strategic collaborations between pharmaceutical companies, immunology research institutes, and biotechnology firms. Competitive dynamics are shifting toward advanced biologics, biosimilars, and combination immunotherapies. Patent expirations and biosimilar development activities are also reshaping pricing structures and competitive positioning.Market Implications

Companies focusing on differentiated biologic portfolios and strategic licensing agreements are expected to strengthen market share.4. Capital and Capacity Scaling

Growing investments in biologics manufacturing, immunology research infrastructure, and specialty dermatology care networks are accelerating market expansion. Pharmaceutical companies are expanding production capabilities for monoclonal antibodies and immune-targeted therapies. The increasing integration of specialty pharmacy distribution systems is also improving treatment accessibility globally.Market Implications

Manufacturers investing in biologics scalability and specialty care infrastructure are expected to capture substantial long-term opportunities.Market Segmentation Analysis

By Disease Type

1. Chronic Spontaneous Urticaria (CSU)

CSU dominates the market due to its high prevalence and growing demand for long-term biologic therapies.2. Chronic Inducible Urticaria (CIndU)

CIndU is gaining increasing clinical attention due to growing awareness and diagnostic improvements.3. Acute Urticaria

Acute urticaria continues representing a major patient population requiring short-term treatment interventions.By Drug Class

1. Antihistamines

Second-generation antihistamines remain first-line treatment options due to favorable safety profiles.2. Corticosteroids

Corticosteroids continue being utilized for short-term symptom management during severe flare-ups.3. Biologics

Biologic therapies are rapidly becoming the fastest-growing segment due to superior efficacy in refractory chronic urticaria cases.4. Immunosuppressants

Immunosuppressive therapies are utilized in complex autoimmune-associated urticaria conditions.5. Leukotriene Receptor Antagonists

Adjunctive therapies continue supporting multi-pathway disease management approaches.By Route of Administration

1. Oral

Oral medications dominate due to convenience and broad utilization across antihistamine therapies.2. Injectable

Injectable biologics are experiencing strong growth due to increasing adoption of monoclonal antibody treatments.3. Topical

Topical therapies continue supporting symptomatic relief applications.By Distribution Channel

1. Hospital Pharmacies

Hospital pharmacies remain major distribution channels for biologic and specialty immunology therapies.2. Retail Pharmacies

Retail pharmacies dominate antihistamine and oral therapy distribution.3. Online Pharmacies

Online pharmacy adoption is increasing due to digital healthcare expansion and chronic disease management convenience.By End User

1. Hospitals

Hospitals remain primary treatment centers for severe and chronic urticaria management.2. Dermatology Clinics

Specialized dermatology clinics are increasingly driving biologic treatment adoption.3. Allergy & Immunology Centers

Allergy and immunology centers continue playing critical roles in precision diagnosis and advanced therapy administration.4. Homecare Settings

Home-administered biologics and telehealth monitoring are expanding across chronic care management.Regional Market Dynamics

North America

North America dominates the global urticaria market due to advanced biologic adoption, strong reimbursement frameworks, and high immunology research investments.Asia-Pacific

Asia-Pacific represents the fastest-growing region due to rising allergy prevalence, expanding healthcare access, and increasing biologic therapy adoption.Europe

Europe continues experiencing stable growth supported by advanced dermatology care infrastructure and strong regulatory support for biologics.Latin America

Latin America is gradually expanding due to improving healthcare access and increasing awareness regarding chronic skin disorders.Middle East & Africa

The Middle East & Africa region is witnessing emerging growth driven by improving specialty healthcare services and expanding immunology treatment access.Competitive Landscape

The Global Urticaria Market is highly competitive with major pharmaceutical and biotechnology companies focusing on biologics, immunotherapies, and targeted inflammatory pathway treatments. Key companies operating in the market include:- Novartis

- Sanofi

- Regeneron Pharmaceuticals

- Roche

- Pfizer

- AstraZeneca

- Teva Pharmaceutical Industries

- Bayer

- GlaxoSmithKline

- AbbVie

Strategic Outlook

The future of the urticaria market will be heavily influenced by precision immunology, biomarker-based therapeutics, AI-driven disease management, and next-generation biologics. Companies are increasingly investing in therapies targeting IgE, mast cells, interleukins, and inflammatory signaling pathways. The integration of digital health monitoring, teledermatology, wearable allergy tracking, and personalized treatment algorithms is expected to improve long-term patient outcomes and treatment adherence. Additionally, the development of biosimilars, combination immunotherapies, and extended-duration biologics may significantly reshape future market competition and accessibility.Final Market Perspective

The Global Urticaria Market is entering a transformative growth phase driven by increasing prevalence of chronic allergic disorders, advancements in immunology research, and rapid biologic therapy adoption. The transition from conventional symptomatic treatment toward targeted immune-modulating therapies is significantly improving disease management outcomes. Manufacturers capable of delivering clinically validated, personalized, and biologically advanced treatment solutions will be best positioned to capitalize on long-term market opportunities. The convergence of immunology, biotechnology, digital health, and precision medicine is expected to redefine the future landscape of urticaria treatment globally.Table of Contents

Table of Contents

1. Executive Summary

1.1 Market Forecast Snapshot (2026–2033)

1.2 Global Urticaria Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

2. Introduction & Market Overview

2.1 Definition of the Urticaria Market

2.2 Market Size & Forecast (2026–2033)

2.3 Industry Evolution & Market Development

2.4 Supply Chain & Specialty Distribution Infrastructure

2.5 Impact of Consumer Healthcare & Allergy Awareness Trends

2.6 Regulatory & Compliance Landscape for Immunology Therapies

2.7 Technology & Innovation Landscape in Biologics & Precision Immunology

3. Research Methodology

3.1 Primary Research

3.2 Secondary Research

3.3 Market Size Estimation Model

3.4 Forecast Assumptions (2026–2033)

3.5 Data Validation & Triangulation

4. Market Dynamics

4.1 Drivers

4.1.1 Rising Prevalence of Chronic Urticaria Disorders

4.1.2 Increasing Adoption of Biologic Therapies

4.1.3 Advancements in Precision Immunology Research

4.1.4 Growing Healthcare Awareness & Diagnosis Rates

4.1.5 Expansion of Specialty Dermatology & Allergy Care Infrastructure

4.2 Restraints

4.2.1 High Cost of Biologic Therapies

4.2.2 Limited Access in Emerging Economies

4.2.3 Regulatory Complexity for Advanced Immunotherapies

4.2.4 Adverse Effects & Long-Term Safety Concerns

4.3 Opportunities

4.3.1 Expansion of Biomarker-Driven Personalized Therapies

4.3.2 Growth of Teledermatology & Digital Health Platforms

4.3.3 Development of Biosimilars & Cost-Effective Biologics

4.3.4 Increasing Penetration Across Emerging Healthcare Markets

4.4 Challenges

4.4.1 Complex Clinical Trial & Approval Processes

4.4.2 Competitive Pressure from Biosimilars

4.4.3 Limited Awareness of Advanced Therapies

4.4.4 Specialty Distribution & Cold Chain Challenges

5. Global Urticaria Market Analysis (USD Billion), 2026–2033

5.1 Market Size Overview

5.2 CAGR Analysis

5.3 Regional Revenue Distribution

5.4 Segment Revenue Analysis

5.5 Distribution Channel Analysis

5.6 Patient Treatment Adoption Analysis

6. Market Segmentation (USD Billion), 2026–2033

6.1 By Disease Type

6.1.1 Chronic Spontaneous Urticaria (CSU)

6.1.1.1 Autoimmune CSU

6.1.1.1.1 Severe Refractory CSU

6.1.1.1.1.1 Anti-IgE Resistant Cases

6.1.1.1.1.2 Long-Term Biologic Managed Cases

6.1.2 Chronic Inducible Urticaria (CIndU)

6.1.2.1 Cold-Induced Urticaria

6.1.2.1.1 Cholinergic Urticaria

6.1.2.1.1.1 Pressure-Induced Urticaria

6.1.2.1.1.2 Solar-Induced Urticaria

6.1.3 Acute Urticaria

6.1.3.1 Allergy-Induced Acute Urticaria

6.1.3.1.1 Drug-Induced Acute Reactions

6.1.3.1.1.1 Infection-Associated Urticaria

6.1.3.1.1.2 Food Allergy-Associated Urticaria

6.2 By Drug Class

6.2.1 Antihistamines

6.2.1.1 First-Generation Antihistamines

6.2.1.1.1 Second-Generation Antihistamines

6.2.1.1.1.1 Long-Acting Antihistamine Therapies

6.2.1.1.1.2 Combination Antihistamine Treatments

6.2.2 Corticosteroids

6.2.2.1 Oral Corticosteroids

6.2.2.1.1 Injectable Corticosteroids

6.2.2.1.1.1 Acute Flare-Up Management Therapies

6.2.2.1.1.2 Severe Symptom Suppression Treatments

6.2.3 Biologics

6.2.3.1 Anti-IgE Biologics

6.2.3.1.1 Monoclonal Antibody Therapies

6.2.3.1.1.1 Mast Cell Targeting Biologics

6.2.3.1.1.2 Cytokine Inhibitor Therapies

6.2.4 Immunosuppressants

6.2.4.1 Cyclosporine-Based Therapies

6.2.4.1.1 Immune-Modulating Drug Therapies

6.2.4.1.1.1 Autoimmune Urticaria Treatments

6.2.4.1.1.2 Severe Chronic Case Management

6.2.5 Leukotriene Receptor Antagonists

6.2.5.1 Combination Therapy Applications

6.2.5.1.1 Inflammatory Pathway Modulation

6.2.5.1.1.1 Adjunctive Allergy Management Therapies

6.2.5.1.1.2 Chronic Symptom Reduction Treatments

6.3 By Route of Administration

6.3.1 Oral

6.3.1.1 Tablet Formulations

6.3.1.1.1 Liquid Oral Formulations

6.3.1.1.1.1 Daily Maintenance Therapies

6.3.1.1.1.2 Rapid Symptom Relief Medications

6.3.2 Injectable

6.3.2.1 Subcutaneous Biologics

6.3.2.1.1 Intravenous Immunotherapies

6.3.2.1.1.1 Long-Acting Injectable Treatments

6.3.2.1.1.2 Specialty Biologic Drug Platforms

6.3.3 Topical

6.3.3.1 Anti-Itch Creams

6.3.3.1.1 Anti-Inflammatory Topical Solutions

6.3.3.1.1.1 Localized Skin Relief Treatments

6.3.3.1.1.2 Dermatological Support Therapies

6.4 By Distribution Channel

6.4.1 Hospital Pharmacies

6.4.1.1 Specialty Biologic Distribution Centers

6.4.1.1.1 Immunology Drug Dispensing Units

6.4.1.1.1.1 Hospital-Based Specialty Care Pharmacies

6.4.1.1.1.2 Advanced Immunotherapy Distribution Systems

6.4.2 Retail Pharmacies

6.4.2.1 Community Pharmacy Networks

6.4.2.1.1 Chronic Allergy Medication Retailing

6.4.2.1.1.1 OTC Antihistamine Distribution

6.4.2.1.1.2 Prescription Urticaria Therapy Channels

6.4.3 Online Pharmacies

6.4.3.1 E-Pharmacy Platforms

6.4.3.1.1 Digital Prescription Management Systems

6.4.3.1.1.1 Home Delivery Immunology Therapies

6.4.3.1.1.2 Subscription-Based Chronic Care Platforms

6.5 By End User

6.5.1 Hospitals

6.5.1.1 Tertiary Care Hospitals

6.5.1.1.1 Immunology Treatment Centers

6.5.1.1.1.1 Advanced Allergy Care Units

6.5.1.1.1.2 Severe Chronic Urticaria Treatment Facilities

6.5.2 Dermatology Clinics

6.5.2.1 Specialized Skin Disorder Clinics

6.5.2.1.1 Chronic Allergy Management Centers

6.5.2.1.1.1 Precision Dermatology Clinics

6.5.2.1.1.2 Biologic Administration Centers

6.5.3 Allergy & Immunology Centers

6.5.3.1 Allergy Diagnostic Facilities

6.5.3.1.1 Advanced Immunotherapy Centers

6.5.3.1.1.1 Personalized Allergy Treatment Clinics

6.5.3.1.1.2 Immune Disorder Management Facilities

6.5.4 Homecare Settings

6.5.4.1 Self-Administered Biologic Care

6.5.4.1.1 Telehealth Allergy Monitoring Systems

6.5.4.1.1.1 Remote Patient Management Platforms

6.5.4.1.1.2 Home-Based Chronic Care Programs

7. Market Segmentation by Geography

7.1 North America

7.2 Europe

7.3 Asia-Pacific

7.4 Latin America

7.5 Middle East & Africa

8. Competitive Landscape

8.1 Market Share Analysis

8.2 Product Portfolio Benchmarking

8.3 Product Positioning Mapping

8.4 Strategic Collaborations & Licensing Partnerships

8.5 Competitive Intensity & Market Fragmentation

9. Company Profiles

9.1 Novartis

9.2 Sanofi

9.3 Regeneron Pharmaceuticals

9.4 Roche

9.5 Pfizer

9.6 AstraZeneca

9.7 Teva Pharmaceutical Industries

9.8 Bayer

9.9 GlaxoSmithKline

9.10 AbbVie

10. Strategic Intelligence & Pheonix AI Insights

10.1 Pheonix Demand Forecast Engine

10.2 Immunology Care Infrastructure Analyzer

10.3 Biologic Innovation & Pipeline Tracker

10.4 Precision Therapy Development Insights

10.5 Automated Porter’s Five Forces Analysis

11. Future Outlook & Strategic Recommendations

11.1 Expansion of Precision Immunology Therapies

11.2 Biologic Innovation & Biosimilar Strategies

11.3 Digital Allergy Management & Telehealth Expansion

11.4 Emerging Market Penetration Strategies

11.5 Long-Term Market Outlook (2033+)

12. Appendix

13. About Pheonix Research

14. Disclaimer

Competitive Landscape

Global Urticaria Market Competitive Intensity & Market Structure Overview

The Global Urticaria Market is characterized by a moderately consolidated structure with high competitive intensity, driven by rapid advancements in biologic therapies, precision immunology, and targeted inflammatory pathway treatments. The market is dominated by large multinational pharmaceutical and biotechnology companies actively competing through innovation in monoclonal antibodies, anti-IgE therapies, and immune-modulating biologics.

Leading companies such as Novartis, Sanofi, Regeneron Pharmaceuticals, Roche, and Pfizer are shaping market dynamics through advanced biologic development, immunotherapy pipelines, and precision medicine initiatives.

Competitive intensity is primarily driven by biologic innovation, clinical efficacy, regulatory approvals, biosimilar competition, pricing pressures, and long-term chronic disease management strategies. Increasing investment in next-generation immunology platforms and biomarker-driven therapies is further intensifying global market competition.

Global Urticaria Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

- Novartis: Market leader in chronic spontaneous urticaria biologics with strong expertise in anti-IgE therapies and immunology innovation.

- Sanofi: Major player focusing on inflammatory disease biologics and precision immunology expansion.

- Regeneron Pharmaceuticals: Developer of targeted monoclonal antibody therapies and advanced immunology treatment platforms.

- Roche: Strong participant in immunology diagnostics, biologics development, and precision healthcare ecosystems.

- Pfizer: Expanding immunology portfolio through biologics research and inflammatory disease therapeutics.

- AstraZeneca: Active developer of targeted immunology therapies and autoimmune disease treatments.

- Teva Pharmaceutical Industries: Major supplier of antihistamines and specialty immunology therapeutics globally.

- Bayer: Participant in allergy and inflammatory disease treatment portfolios.

- GlaxoSmithKline: Investing in immunology biologics and respiratory-allergy treatment integration.

- AbbVie: Expanding immune-mediated disease therapies and monoclonal antibody research capabilities.

Key Competitive Intensity & Market Structure Signals in Global Urticaria Market

Several signals define the competitive dynamics of the market:

- Rapid expansion of biologic therapies and monoclonal antibody treatments is reshaping competitive positioning across chronic urticaria management.

- Increasing focus on anti-IgE therapies, mast cell targeting, and cytokine pathway modulation is accelerating immunology innovation.

- Pharmaceutical companies are heavily investing in precision immunology and biomarker-based personalized treatment approaches.

- Regulatory support for accelerated biologic approvals is intensifying competition among next-generation immunotherapy developers.

- Patent expirations and biosimilar development activities are gradually increasing pricing pressure within mature biologic segments.

- Expansion of specialty dermatology clinics, allergy centers, and teledermatology platforms is improving treatment accessibility globally.

- AI-assisted diagnostics, digital monitoring tools, and telehealth integration are increasingly supporting chronic disease management ecosystems.

Strategic Implications of Competitive Intensity & Market Structure in Global Urticaria Market

The competitive structure creates several strategic implications:

- Continuous biologic innovation and clinical differentiation are becoming essential for maintaining long-term market leadership.

- Companies capable of demonstrating superior long-term efficacy, safety profiles, and patient adherence outcomes will strengthen competitive positioning.

- Strategic collaborations between biotechnology firms, immunology researchers, and specialty healthcare providers are increasingly important for accelerating commercialization.

- Expansion of biosimilar portfolios may improve treatment affordability while increasing pricing competition across biologic therapies.

- Precision medicine strategies integrating genomic analysis, biomarkers, and AI-driven treatment optimization will increasingly influence future market competition.

- Specialty pharmacy networks and digital healthcare ecosystems are becoming critical for chronic biologic therapy distribution and patient monitoring.

- Regulatory compliance, pharmacovigilance infrastructure, and clinical validation capabilities remain major competitive barriers within the market.

Global Urticaria Market Competitive Intensity & Market Structure Forward Outlook

Looking ahead, the Global Urticaria Market is expected to maintain its moderately consolidated structure with sustained high competitive intensity, supported by rapid innovation in biologics and precision immunology technologies.

- Next-generation anti-IgE biologics and targeted cytokine inhibitors are expected to significantly expand treatment personalization.

- AI-assisted immunology diagnostics and predictive inflammatory profiling will increasingly support precision therapy selection.

- Growth in biosimilars and extended-duration biologics may improve treatment accessibility and alter competitive pricing structures.

- Teledermatology platforms, wearable allergy monitoring systems, and digital adherence tools will increasingly integrate into chronic disease management ecosystems.

- Pharmaceutical companies are expected to intensify investments in combination immunotherapies and immune pathway targeting technologies.

- Strategic acquisitions, licensing agreements, and biotechnology partnerships are likely to accelerate selective market consolidation.

- The convergence of immunology, biotechnology, AI healthcare systems, and precision medicine will fundamentally reshape the future urticaria treatment landscape.

In conclusion, the Global Urticaria Market represents a high-value, innovation-driven, and biologics-focused competitive ecosystem, where precision immunology, targeted biologic therapies, and digital healthcare integration will determine long-term market leadership.

Value Chain

Global Urticaria Market Value Chain & Supply Chain Evolution Overview

The Global Urticaria Market is undergoing significant transformation driven by rapid advancements in biologic therapies, precision immunology, and personalized autoimmune disease management. The market’s value chain is characterized by a hybrid operational model supported by integrated pharmaceutical distribution systems connecting biologics manufacturing, specialty care infrastructure, hospital networks, and digital healthcare ecosystems.

A defining feature of this value chain is its increasing dependence on advanced biologic therapies, monoclonal antibody manufacturing, and precision immunology research. The transition from conventional antihistamine-based symptomatic treatment toward targeted immune-modulating therapies is reshaping research priorities, production scalability, and specialty treatment delivery models globally.

Supply chain complexity is high due to biologics manufacturing requirements, cold-chain logistics, regulatory compliance standards, specialty pharmacy integration, and long clinical development timelines. The increasing adoption of personalized therapies, biomarker-driven treatment strategies, and AI-assisted disease monitoring is further expanding operational and technological complexity across the value chain.

Pharmaceutical manufacturers are investing heavily in immunology R&D, biologics production scalability, specialty dermatology care networks, and digital health integration to improve treatment accessibility, long-term patient monitoring, and therapeutic precision. The market is evolving into a highly specialized and innovation-driven immunology ecosystem aligned with precision medicine and personalized chronic disease management.

Global Urticaria Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Research & Immunology Discovery: Autoimmune disease research, IgE pathway studies, mast cell biology, inflammatory cytokine analysis, and biomarker identification.

- Drug Development & Clinical Trials: Monoclonal antibody development, biologic therapy trials, pharmacovigilance studies, and precision immunology validation.

- Biologics Manufacturing & Formulation: Large-scale biologics production, sterile injectable formulation, antibody purification, and quality-controlled pharmaceutical manufacturing.

- Regulatory Approval & Compliance: FDA, EMA, and global immunology biologics approvals, safety monitoring, and post-market surveillance systems.

- Distribution & Specialty Pharmacy Networks: Cold-chain logistics, hospital pharmacy systems, specialty biologics distributors, and online pharmacy ecosystems.

- Clinical Administration & Patient Management: Hospitals, dermatology clinics, allergy & immunology centers, teledermatology systems, and homecare biologic administration.

Company-to-Stage Mapping

- Research & Immunology Discovery: Immunology research institutes, biotechnology laboratories, and autoimmune disease research organizations.

- Drug Development & Clinical Trials: Novartis, Sanofi, and Regeneron Pharmaceuticals.

- Biologics Manufacturing & Formulation: Roche, Pfizer, and AstraZeneca.

- Regulatory Approval & Compliance: Global pharmaceutical regulatory agencies, biologics compliance organizations, and pharmacovigilance service providers.

- Distribution & Specialty Pharmacy Networks: Specialty pharmacy providers, hospital pharmacy systems, cold-chain logistics companies, and online healthcare distributors.

- Clinical Administration & Patient Management: Dermatology centers, allergy & immunology clinics, hospitals, and telehealth monitoring providers.

Key Value Chain & Supply Chain Evolution Signals in Global Urticaria Market

- Rapid Expansion of Biologic Therapies

Monoclonal antibodies and targeted immune-modulating therapies are increasingly dominating chronic urticaria treatment strategies. - Growth of Precision Immunology & Biomarker-Based Care

Personalized immunology approaches and biomarker-driven diagnostics are improving treatment efficacy and patient-specific therapy selection. - Increasing Dependence on Specialty Care Infrastructure

Specialty dermatology and immunology networks are becoming central to advanced biologic therapy administration and patient monitoring. - Expansion of Cold-Chain & Specialty Pharmacy Networks

Biologic distribution requires advanced cold-chain logistics and highly controlled specialty pharmacy ecosystems. - Integration of Digital Health & Teledermatology

AI-assisted monitoring, telehealth platforms, and wearable allergy management systems are improving long-term patient engagement. - Biosimilar Competition & Pricing Transformation

Patent expirations and biosimilar entry are reshaping pricing structures and improving treatment accessibility globally. - Accelerated Regulatory Support for Immunology Innovation

Regulatory agencies are increasingly supporting fast-track approval pathways for biologics and rare immunological disease therapies.

Strategic Implications of Value Chain & Supply Chain Evolution

- Investment in Precision Immunology Research

Companies must strengthen biomarker discovery, targeted biologics development, and AI-driven immunology analytics capabilities. - Expansion of Biologics Manufacturing Capacity

Scalable monoclonal antibody production and sterile injectable infrastructure will remain critical for long-term competitiveness. - Strengthening Specialty Distribution Ecosystems

Advanced cold-chain logistics and specialty pharmacy integration are essential for biologics accessibility and patient continuity. - Integration of Digital Disease Management Platforms

Teledermatology, remote patient monitoring, and AI-assisted treatment optimization will increasingly shape patient care ecosystems. - Regulatory Compliance & Pharmacovigilance Prioritization

Strong compliance systems and long-term safety monitoring capabilities will improve market trust and commercialization speed. - Focus on Biosimilars & Cost Accessibility

Companies investing in biosimilar development and affordability strategies will strengthen global market penetration. - Expansion of Personalized Chronic Care Models

Long-term biologic management programs and individualized treatment ecosystems will improve patient retention and clinical outcomes.

Global Urticaria Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the Global Urticaria Market is expected to evolve into a highly specialized, precision-driven, and digitally integrated immunology ecosystem.

Key future developments include:

- Expansion of next-generation anti-IgE and cytokine-targeted biologics.

- Increasing adoption of AI-assisted allergy diagnostics and predictive immunology platforms.

- Growth of home-administered biologics and remote patient monitoring ecosystems.

- Expansion of biosimilar biologics and affordability-focused treatment strategies.

- Integration of wearable allergy monitoring and teledermatology platforms.

- Advancements in biomarker-based personalized therapy optimization.

- Increasing convergence of immunology, biotechnology, and digital healthcare ecosystems.

In conclusion, the Global Urticaria Market represents a rapidly evolving and innovation-intensive healthcare ecosystem where biologic innovation, precision immunology, specialty care integration, and digital disease management will determine long-term competitive leadership and therapeutic advancement.

Investment Activity

Global Urticaria Market Investment & Funding Dynamics Overview

The Global Urticaria Market is witnessing strong investment momentum driven by rapid advancements in biologic therapies, increasing prevalence of chronic spontaneous urticaria (CSU), and expanding adoption of precision immunology approaches. Pharmaceutical companies, biotechnology firms, immunology research organizations, and specialty healthcare providers are increasingly investing in next-generation immune-targeted therapies, monoclonal antibodies, and personalized allergy treatment platforms.

Investment activity is being significantly accelerated by the growing clinical success of biologic therapies targeting IgE pathways, mast cells, interleukins, and inflammatory cytokines. The increasing demand for long-term disease management solutions with improved efficacy and reduced side effects is encouraging substantial capital deployment into immunology R&D and advanced biologics manufacturing infrastructure.

Additionally, expanding healthcare access, rising diagnosis rates, and favorable reimbursement policies for specialty biologics are strengthening long-term investor confidence across the urticaria treatment ecosystem. The increasing convergence of biotechnology, precision medicine, AI-driven diagnostics, and digital healthcare platforms is further reshaping investment strategies globally.

Global Urticaria Market Investment & Funding Dynamics Current Scenario

Currently, the Global Urticaria Market demonstrates rapidly increasing investment activity combined with high capital intensity due to extensive biologics research, clinical development programs, and specialty immunology manufacturing requirements. Pharmaceutical companies are actively investing in monoclonal antibody development, biomarker-driven therapeutics, biosimilar expansion, and personalized immunomodulatory treatment platforms.

Major market participants are significantly increasing funding for anti-IgE biologics, immune-targeted therapies, and next-generation inflammatory pathway inhibitors capable of improving treatment outcomes in chronic and refractory urticaria cases.

The market is also witnessing active merger and acquisition activity as global pharmaceutical companies pursue strategic acquisitions, licensing agreements, and immunology-focused collaborations to strengthen biologics pipelines and expand specialty dermatology portfolios.

In parallel, venture capital firms and institutional healthcare investors are increasingly funding biotechnology companies specializing in precision immunology, autoimmune disease therapeutics, allergy diagnostics, and advanced biologic drug development.

Key Investment & Funding Dynamics Signals in Global Urticaria Market

Several major investment signals are shaping funding activity within the Global Urticaria Market:

- Rapid advancements in biologic therapies, monoclonal antibodies, precision immunology, and inflammatory pathway targeting technologies are accelerating pharmaceutical investments globally.

- Increasing clinical adoption of anti-IgE biologics and personalized immunomodulatory therapies is encouraging large-scale investments into specialty biologics manufacturing and clinical trial infrastructure.

- Expansion of AI-assisted diagnostics, biomarker-driven treatment strategies, digital allergy management platforms, and teledermatology ecosystems is driving investments in digital healthcare integration.

- Strategic investments in biosimilars, extended-duration biologics, and combination immunotherapies are reshaping long-term competitive positioning across the market.

- Growing collaborations between pharmaceutical companies, biotechnology firms, immunology research institutes, and specialty healthcare providers are strengthening innovation ecosystems globally.

- Increasing regulatory support for accelerated biologics approvals and rare immunology therapies is improving commercialization timelines and investor confidence.

- Rising demand for personalized autoimmune and allergy management solutions is accelerating investments in precision medicine platforms and advanced immunological analytics.

Strategic Implications of Investment & Funding Dynamics in Global Urticaria Market

The evolving investment landscape creates several strategic implications for market participants.

- Continuous investment in precision immunology, biologic drug development, biomarker analytics, and AI-driven disease management platforms is becoming essential for maintaining long-term competitive leadership.

- High capital intensity requires companies to strategically allocate resources toward clinical development programs, biologics manufacturing infrastructure, regulatory compliance systems, and specialty care distribution networks.

- Companies capable of developing high-efficacy targeted therapies with strong safety profiles and personalized treatment capabilities are expected to strengthen market positioning significantly.

- Increasing merger and acquisition activity is accelerating market consolidation and enabling companies to rapidly expand immunology portfolios, biologics pipelines, and specialty dermatology capabilities.

- Strategic investments in specialty pharmacy ecosystems, telehealth integration, and chronic disease management platforms are becoming increasingly important for improving long-term patient access and treatment adherence.

- Regulatory compliance investments and pharmacovigilance infrastructure are emerging as critical strategic priorities due to increasing safety monitoring requirements for biologic therapies.

- Companies investing in scalable monoclonal antibody production systems and biosimilar commercialization capabilities are expected to capture substantial long-term growth opportunities.

Global Urticaria Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Urticaria Market is expected to maintain strong investment growth driven by expanding biologic adoption, advancements in precision immunology, and increasing demand for personalized autoimmune disease management solutions.

Future investment activity will increasingly focus on next-generation monoclonal antibodies, mast cell-targeted therapies, AI-powered allergy diagnostics, biomarker-guided treatment systems, and extended-duration biologics capable of improving long-term disease control.

The market is also expected to witness increasing investments in digital immunology platforms, wearable allergy monitoring systems, cloud-connected disease management ecosystems, and AI-assisted treatment optimization technologies.

Additionally, growing biosimilar development activity and expanding specialty immunology infrastructure across emerging markets are expected to improve long-term treatment accessibility and commercial scalability globally.

In conclusion, the Global Urticaria Market represents a high-growth and innovation-intensive investment landscape where biologics innovation, precision immunology, AI-integrated disease management, and personalized therapeutic platforms will continue shaping future capital deployment strategies worldwide.

Technology & Innovation

Global Urticaria Market Technology & Innovation Landscape Overview

The Global Urticaria Market is undergoing significant technological and therapeutic transformation driven by advancements in precision immunology, biologic drug development, monoclonal antibody engineering, biomarker-based diagnostics, and AI-assisted disease management platforms. The market demonstrates a high innovation intensity level, supported by increasing investments in targeted immune therapies and personalized dermatology care.

The transition from conventional symptomatic treatments toward targeted biologic therapies is fundamentally reshaping urticaria management globally. Advanced immunotherapies targeting IgE pathways, mast cell activation, inflammatory cytokines, interleukins, and immune signaling mechanisms are becoming central to chronic urticaria treatment strategies.

Pharmaceutical companies are increasingly investing in next-generation monoclonal antibodies, anti-IgE biologics, mast cell stabilizers, cytokine inhibitors, and immune-modulating therapeutics designed to improve long-term efficacy while reducing adverse effects associated with conventional corticosteroid therapies.

Technological innovation is also accelerating through the integration of AI-assisted diagnostics, biomarker-driven treatment selection, digital patient monitoring systems, teledermatology platforms, and personalized treatment algorithms. These technologies are improving disease classification, therapy optimization, patient adherence, and long-term symptom management.

The growing adoption of precision medicine and genomic immunology research is enabling the development of highly personalized urticaria therapies tailored to individual immune response profiles and inflammatory biomarkers.

Additionally, advances in biologics manufacturing, biosimilar development, high-throughput immunology screening, and specialty pharmacy distribution systems are improving treatment accessibility and commercialization scalability globally.

The convergence of biotechnology, immunology, dermatology, AI-driven healthcare systems, and digital therapeutics is fundamentally transforming the future innovation landscape of the urticaria treatment market.

Global Urticaria Market Technology & Innovation Landscape Current Scenario

Currently, the Global Urticaria Market demonstrates strong patent activity and accelerating biologic commercialization, particularly across chronic spontaneous urticaria (CSU) and refractory autoimmune-associated urticaria treatment segments.

1. Anti-IgE Biologic Innovation

Biologic therapies targeting IgE-mediated inflammatory pathways are becoming mainstream in chronic urticaria management.

2. Precision Immunology & Biomarker Research

Biomarker-driven treatment strategies are improving patient stratification and therapy personalization.

3. Monoclonal Antibody Development

Advanced monoclonal antibody engineering is expanding next-generation immunotherapy pipelines.

4. AI-Assisted Disease Management

AI-enabled diagnostic systems and treatment optimization platforms are improving long-term disease monitoring and patient outcomes.

5. Teledermatology & Digital Health Integration

Remote dermatology platforms and digital monitoring tools are expanding access to chronic urticaria care globally.

6. Biosimilar & Combination Therapy Expansion

Biosimilar development and multi-pathway immunotherapy combinations are reshaping competitive dynamics and treatment accessibility.

Key Technology & Innovation Landscape Signals in Global Urticaria Market

Several innovation signals are shaping market evolution:

1. Rapid Expansion of Precision Immunology

Targeted immune-modulating therapies are increasingly replacing generalized symptomatic treatments.

2. Increasing Investment in Biologic Therapies

Pharmaceutical companies are heavily investing in next-generation biologics with improved efficacy and safety profiles.

3. Growth of Biomarker-Based Personalized Medicine

Immune profiling and biomarker diagnostics are enabling highly personalized treatment pathways.

4. Rising Integration of AI & Digital Dermatology

AI-assisted monitoring and telehealth ecosystems are improving chronic disease management efficiency.

5. Expansion of Long-Acting Injectable Therapies

Extended-duration biologics are improving treatment adherence and patient convenience.

6. Increasing Focus on Biosimilars & Cost Optimization

Patent expirations and biosimilar commercialization are expected to improve affordability and market accessibility.

Strategic Implications of Technology & Innovation Landscape in Global Urticaria Market

The evolving innovation landscape is significantly transforming competition across the urticaria market. Companies are increasingly competing on biologic efficacy, precision immunology capabilities, biomarker analytics, digital patient management systems, and long-term treatment optimization.

Manufacturers investing in AI-driven immunology platforms, next-generation monoclonal antibodies, and biomarker-based therapeutic strategies are expected to strengthen long-term competitive positioning.

Strategic collaborations between pharmaceutical firms, immunology research institutes, biotechnology companies, and digital health providers are accelerating innovation cycles and reshaping treatment ecosystems globally.

The growing convergence of biotechnology, genomics, dermatology, AI healthcare systems, and digital therapeutics is also creating opportunities for integrated chronic disease management platforms and personalized immune care ecosystems.

Additionally, increasing regulatory support for accelerated biologic approvals and precision medicine initiatives is encouraging rapid commercialization of innovative immunology therapies.

Global Urticaria Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026–2033, the Global Urticaria Market is expected to evolve toward highly personalized, AI-assisted, and precision immunology-driven treatment ecosystems.

Future technological developments are likely to include:

1. Next-Generation Precision Biologics

Advanced biologics targeting multiple inflammatory pathways simultaneously are expected to improve long-term disease control.

2. AI-Driven Personalized Immunology Platforms

AI-enabled immune profiling and predictive treatment algorithms will support personalized therapy optimization.

3. Biomarker-Based Treatment Selection

High-resolution biomarker diagnostics will increasingly guide therapy selection and disease monitoring.

4. Long-Acting Injectable Immunotherapies

Extended-duration biologics will improve treatment adherence and chronic disease management efficiency.

5. Integrated Digital Allergy & Dermatology Ecosystems

Connected digital platforms integrating teledermatology, wearable monitoring, and remote immune management will expand rapidly.

6. Biosimilar Commercialization Expansion

The growing availability of biosimilars is expected to improve affordability and treatment accessibility globally.

7. Combination Immunotherapy Innovation

Multi-target immunological therapies combining biologics, cytokine inhibitors, and immune modulators may redefine treatment paradigms.

Overall, companies capable of combining precision immunology, biologic innovation, AI-assisted disease management, biomarker-driven therapeutics, regulatory compliance, and scalable biologics manufacturing will be best positioned to lead the future evolution of the Global Urticaria Market.

Market Risk

Global Urticaria Market Risk & Disruption Analysis

The Global Urticaria Market operates within a moderate-to-high disruption environment, driven by rapid biologic innovation, evolving immunology research, patent expirations, biosimilar competition, regulatory acceleration for immune-targeted therapies, and increasing adoption of precision medicine. While the market demonstrates strong long-term growth fundamentals due to rising chronic urticaria prevalence and expanding biologic therapy adoption, it remains exposed to pricing pressure, reimbursement complexity, clinical development risks, and competitive therapeutic disruption.

A defining structural characteristic of the market is its growing dependence on biologic therapies and advanced immunomodulatory treatments. As treatment strategies increasingly shift from conventional antihistamines toward monoclonal antibodies and targeted immunology platforms, pharmaceutical companies face rising R&D costs, regulatory scrutiny, pharmacovigilance obligations, and manufacturing complexity associated with biologics commercialization.

The market is also undergoing competitive transformation due to the emergence of biosimilars, next-generation anti-IgE therapies, mast cell-targeted biologics, and AI-assisted precision immunology platforms. Increasing convergence between biotechnology, digital health, genomics, and personalized allergy care is reshaping treatment paradigms and accelerating innovation cycles globally.

Global Urticaria Market Current Risk Environment

The current market environment is characterized by increasing biologic adoption, regulatory acceleration for immunology therapies, and intensifying competition among pharmaceutical and biotechnology companies.

One of the most significant disruption factors involves rising pricing pressure and reimbursement scrutiny surrounding high-cost biologic therapies. Healthcare systems, insurers, and government reimbursement programs are increasingly evaluating cost-effectiveness, long-term efficacy, and treatment accessibility for chronic urticaria biologics, particularly within premium specialty drug categories.

Another major risk area involves biosimilar competition and patent expiration dynamics. As leading monoclonal antibody therapies approach patent cliffs, biosimilar entrants may significantly reshape pricing structures, market share distribution, and long-term profitability for originator biologic manufacturers.

The market also faces clinical development risks associated with immunology therapies, including stringent safety evaluations, adverse event monitoring, and long-term efficacy validation requirements. Regulatory agencies continue strengthening pharmacovigilance standards and post-market surveillance obligations for immune-modulating treatments.

In parallel, rapid innovation in inflammatory pathway targeting, cytokine modulation, mast cell stabilization, and biomarker-driven therapies is intensifying therapeutic competition and shortening innovation cycles across the market.

Additionally, geopolitical instability, biologics manufacturing concentration, API supply dependencies, and specialty drug distribution complexity continue creating operational and supply chain risks globally.

Key Market Risk & Disruption Signals in Global Urticaria Market

1. Rising Biologic Therapy Pricing & Reimbursement Pressure

Healthcare systems and insurers are increasingly scrutinizing high-cost biologic therapies, creating reimbursement and accessibility challenges.

2. Biosimilar Competition & Patent Expiration Risks

Patent expirations of leading biologics are expected to intensify biosimilar competition and pricing disruption across the immunology market.

3. Clinical Development & Safety Validation Complexity

Stringent regulatory requirements for long-term safety monitoring, pharmacovigilance, and biologic efficacy validation continue increasing development risks.

4. Rapid Precision Immunology Innovation

Advancements in anti-IgE therapies, mast cell targeting, cytokine inhibition, and biomarker-driven treatments are accelerating therapeutic disruption.

5. Specialty Drug Manufacturing & Supply Chain Dependencies

Dependence on biologics manufacturing infrastructure, cold-chain logistics, and specialty pharmaceutical supply networks creates operational vulnerability.

6. Digital Health & AI-Driven Disease Management Disruption

Teledermatology, wearable allergy monitoring, AI-assisted diagnostics, and digital therapeutics are reshaping chronic urticaria management ecosystems.

7. Regulatory Acceleration for Immunology Therapies

Accelerated approval pathways for innovative biologics increase commercialization opportunities while intensifying competitive entry rates.

Strategic Implications of Market Risk & Disruption in Global Urticaria Market

The evolving disruption environment creates both substantial growth opportunities and operational risks for pharmaceutical manufacturers, biotechnology firms, and immunology-focused healthcare providers.

One of the most important strategic implications is the increasing need for differentiated biologic innovation and precision immunology capabilities. Companies must continuously invest in next-generation monoclonal antibodies, biomarker-guided therapies, extended-duration biologics, and personalized immune-modulating platforms to maintain long-term competitive positioning.

Manufacturers are also increasingly required to strengthen biologics manufacturing scalability, specialty pharmacy partnerships, cold-chain logistics infrastructure, and post-market safety monitoring capabilities to support growing global treatment demand.

The convergence of immunology, genomics, AI-assisted diagnostics, digital therapeutics, and personalized medicine is reshaping value-chain dynamics across the market. Companies capable of integrating biologics with digital disease management ecosystems and predictive treatment analytics are expected to strengthen long-term market leadership.

Strategic collaborations between pharmaceutical companies, immunology research institutes, AI healthcare providers, and specialty dermatology networks are becoming increasingly important for accelerating innovation and commercialization efficiency.

In addition, biosimilar development strategies, licensing partnerships, and regional biologics manufacturing diversification are expected to become critical for maintaining profitability and improving treatment accessibility globally.

Companies focusing on long-duration therapies, self-administered biologics, homecare treatment models, and AI-enabled patient monitoring systems are likely to achieve stronger patient adherence and recurring revenue opportunities.

Global Urticaria Market Risk & Disruption Forward Outlook

Looking ahead to 2026–2033, the Global Urticaria Market is expected to experience a progressively more biologics-driven, precision-focused, and digitally integrated disruption environment.

1. Expansion of Precision Immunology & Biomarker-Based Therapies

Biomarker-guided treatment selection and personalized immunology platforms are expected to become increasingly central to chronic urticaria management.

2. Accelerating Biosimilar Market Penetration

Biosimilar competition is expected to intensify across major biologic categories, reshaping pricing structures and treatment accessibility globally.

3. Greater Integration of AI & Digital Allergy Care

AI-assisted diagnostics, wearable allergy tracking systems, teledermatology platforms, and digital therapeutics will increasingly support long-term disease management.

4. Development of Next-Generation Immune-Modulating Therapies

Emerging therapies targeting mast cells, interleukins, inflammatory cytokines, and immune signaling pathways are expected to intensify innovation cycles.

5. Increasing Homecare & Self-Administration Models

Home-administered biologics and remote patient monitoring systems are expected to significantly expand across chronic urticaria care ecosystems.

6. Rising Regulatory Emphasis on Long-Term Safety Monitoring

Regulatory agencies will likely strengthen post-market surveillance, adverse event monitoring, and real-world evidence requirements for biologic therapies.

7. Expansion of Personalized & Preventive Allergy Care

Precision diagnostics, predictive immunology analytics, and individualized treatment optimization will increasingly shape future therapeutic strategies.

8. Greater Focus on Cost Optimization & Accessibility

Healthcare systems and pharmaceutical companies will increasingly prioritize biosimilars, value-based pricing models, and broader biologic accessibility programs.

In conclusion, the Global Urticaria Market represents a rapidly evolving immunology-driven therapeutic ecosystem, where biologic innovation, precision medicine integration, AI-enabled disease management, regulatory agility, and biosimilar competitiveness will define long-term market leadership.

Regulatory Landscape

Global Urticaria Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a critical role in shaping the Global Urticaria Market as healthcare authorities increasingly focus on biologic therapy safety, immunology drug approvals, pharmacovigilance requirements, and personalized medicine frameworks. Regulatory pathways governing monoclonal antibodies, anti-IgE therapies, immune-modulating biologics, and targeted inflammatory pathway treatments significantly influence product development, commercialization timelines, and market accessibility globally.

The growing transition toward precision immunology and biologic-based urticaria treatment is increasing the importance of stringent clinical validation, long-term safety monitoring, and post-market surveillance. Regulatory agencies are prioritizing therapies capable of addressing chronic spontaneous urticaria (CSU) and treatment-resistant patient populations while ensuring acceptable safety profiles and clinical efficacy standards.

The market is also influenced by evolving policies related to biosimilar approvals, specialty drug reimbursement, rare disease support frameworks, and accelerated pathways for innovative immunological therapies. Governments and healthcare systems are increasingly supporting advanced biologics to improve chronic disease management outcomes and reduce long-term healthcare burdens.

In parallel, increasing integration of digital health monitoring, teledermatology platforms, and AI-assisted allergy diagnostics is gradually expanding the regulatory scope surrounding digital therapeutics and connected healthcare ecosystems within immunology care.

Global Urticaria Market Regulatory & Policy Environment Current Scenario

Currently, the Global Urticaria Market operates under a highly regulated pharmaceutical and biologics framework governed by agencies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and other national healthcare authorities.

One of the most important regulatory trends influencing the market is the increasing use of accelerated approval pathways for biologics and advanced immunotherapies targeting chronic inflammatory and autoimmune diseases. Regulatory agencies are actively supporting innovative therapies addressing unmet clinical needs in chronic urticaria management.

Biologic therapies targeting IgE pathways, mast cells, interleukins, and inflammatory cytokines are subject to extensive clinical trial requirements, pharmacovigilance standards, manufacturing quality controls, and post-approval monitoring obligations.

Another major regulatory development involves increasing oversight of biosimilar development and interchangeability standards. As biologic patents expire, regulators are strengthening approval frameworks to ensure biosimilar efficacy, safety, and immunogenicity comparability.

Reimbursement and pricing policies also play a significant role in market expansion, particularly in developed healthcare systems where biologic therapy affordability and insurance coverage influence patient access.

Additionally, patient safety standards surrounding long-term biologic usage, adverse immune reactions, and immunosuppressive risks continue shaping clinical development and regulatory review processes globally.

Key Regulatory & Policy Environment Signals in Global Urticaria Market

1. Accelerated Approval Support for Immunology Biologics

Regulatory agencies are increasingly utilizing accelerated pathways to support innovative therapies addressing chronic and treatment-resistant urticaria conditions.

2. Growing Emphasis on Long-Term Pharmacovigilance

Biologic therapies require extensive long-term safety monitoring, adverse event reporting, and post-market surveillance frameworks.

3. Expansion of Biosimilar Regulatory Frameworks

Patent expirations are encouraging biosimilar development while regulators strengthen interchangeability and immunogenicity standards.

4. Increasing Focus on Precision Medicine & Biomarker Validation

Personalized immunology approaches are driving increased regulatory attention toward biomarker-driven treatment validation and targeted therapy protocols.

5. Reimbursement & Specialty Drug Access Policies

Government healthcare systems and insurers are increasingly shaping market access through biologic reimbursement policies and specialty pharmacy frameworks.

Strategic Implications of Regulatory & Policy Environment in Global Urticaria Market

The evolving regulatory landscape creates major strategic implications for pharmaceutical manufacturers, biotechnology firms, immunology researchers, and specialty healthcare providers. One of the most important implications is the increasing need for robust clinical evidence, long-term efficacy validation, and comprehensive pharmacovigilance systems.

Manufacturers must invest heavily in biologic manufacturing compliance, specialty clinical trial infrastructure, immunogenicity testing, and regulatory documentation to achieve successful commercialization and global market access.

The growing regulatory support for accelerated immunology approvals is also encouraging increased investment in next-generation biologics, precision immunotherapies, and biomarker-driven treatment platforms.

At the same time, pricing pressure and reimbursement scrutiny may intensify competition between branded biologics and emerging biosimilars. Companies capable of balancing innovation, clinical effectiveness, affordability, and regulatory compliance are expected to gain stronger long-term market positioning.

Additionally, increasing integration of digital health monitoring and AI-assisted allergy management platforms may gradually introduce additional compliance requirements related to patient data security and connected healthcare ecosystems.

Global Urticaria Market Regulatory & Policy Environment Forward Outlook

Looking ahead to 2026–2033, the regulatory environment for urticaria therapies is expected to become increasingly innovation-focused, biologics-oriented, and precision medicine-driven as advanced immunotherapies continue transforming chronic disease management globally.

Future regulatory frameworks are likely to place stronger emphasis on biomarker-based treatment selection, AI-assisted immunology diagnostics, long-term biologic safety monitoring, and personalized therapeutic strategies.

Regulatory agencies may also continue expanding accelerated approval mechanisms for breakthrough immunology therapies while strengthening real-world evidence requirements and post-market safety surveillance obligations.

The growing development of biosimilars and combination immunotherapies is expected to further reshape pricing regulations, reimbursement structures, and competitive market dynamics globally.

Governments and healthcare systems are also likely to increase support for specialty immunology infrastructure, chronic disease management programs, and personalized healthcare initiatives to improve long-term patient outcomes.

Overall, the regulatory and policy environment will remain a critical factor influencing innovation, biologic commercialization, reimbursement access, patient safety, and competitive positioning within the Global Urticaria Market. Companies capable of balancing scientific innovation, regulatory excellence, pharmacovigilance, affordability, and personalized treatment capabilities will be best positioned to capitalize on long-term market growth opportunities.