Global Wine Market size and share Analysis 2026-2033

Global Wine Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

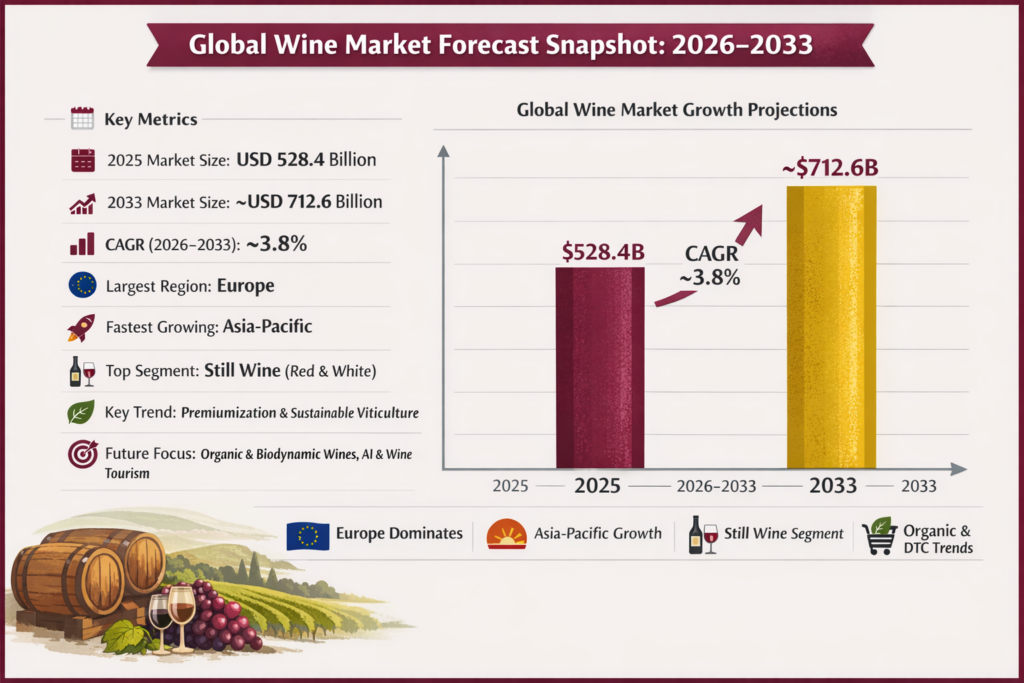

| 2025 Market Size | USD 528.4 Billion |

| 2033 Market Size | ~USD 712.6 Billion |

| CAGR (2026–2033) | ~3.8% |

| Largest Region | Europe |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Still Wine (Red & White) |

| Key Trend | Premiumization, Sustainable Viticulture & DTC Expansion |

| Future Focus | Organic & Biodynamic Wines, AI-Driven Retail Analytics & Wine Tourism |

Global Wine Market Overview

The Global Wine Market is undergoing steady structural evolution, supported by changing consumer lifestyles, premiumization trends, expanding wine culture in emerging economies, and the growing integration of digital retail channels. Wine categories—including red, white, rosé, sparkling, and fortified wines—continue to evolve into premium-driven, experience-oriented beverage ecosystems aligned with modern consumption preferences.

According to Pheonix Research, the Global Wine Market is valued at USD 528.4 billion in 2025 and is projected to reach approximately USD 712.6 billion by 2033, registering a CAGR of ~3.8% (2026–2033). This revenue forecast reflects stable global demand, premium product innovation, expansion of direct-to-consumer channels, and sustained wine tourism growth across mature and developing markets.

Europe holds the largest market share, supported by historic wine-producing nations such as France, Italy, and Spain, strong export networks, and established consumption patterns. Asia-Pacific is emerging as the fastest-growing region, driven by urbanization, rising disposable income, growing wine education, and increasing adoption among younger consumers.

The Post-2025 outlook for the Wine Market highlights continued premiumization, organic and biodynamic production practices, AI-powered supply chain optimization, digital retail growth, and experiential wine tourism as key long-term growth drivers.

Key Drivers of Global Wine Market Growth

1. Premiumization & Evolving Consumer Preferences

Consumers are increasingly shifting toward premium, aged, and limited-edition wines, prioritizing quality, authenticity, and origin over volume consumption.

2. Expansion of Direct-to-Consumer & Online Channels

Winery memberships, subscription wine boxes, and online wine marketplaces are improving accessibility, personalization, and higher-margin sales models.

3. Sustainable & Organic Viticulture

Growing environmental awareness is accelerating adoption of organic, biodynamic, and low-intervention wine production methods.

4. Wine Tourism & Experiential Consumption

Vineyard tours, curated tastings, and immersive wine experiences are strengthening brand loyalty and premium positioning.

5. Growth in Emerging Markets

Asia-Pacific and Latin America are witnessing rising wine adoption due to increasing disposable incomes and Western lifestyle influence.

Global Wine Market Segmentation

1. By Wine Type

1.1 Red Wine

1.1.1 Cabernet Sauvignon

1.1.1.1 Premium Reserve Cabernet

1.1.1.2 Single-Vineyard Cabernet

1.1.1.3 Oak-Aged Cabernet

1.1.1.4 Organic & Biodynamic Cabernet

1.1.2 Merlot

1.1.2.1 Estate Bottled Merlot

1.1.2.2 Blended Merlot

1.1.2.3 Barrel-Aged Merlot

1.1.2.4 Limited-Edition Merlot

1.1.3 Pinot Noir

1.1.3.1 Cool-Climate Pinot Noir

1.1.3.2 Single-Origin Pinot Noir

1.1.3.3 Organic Pinot Noir

1.1.3.4 Luxury Vintage Pinot Noir

1.1.4 Syrah / Shiraz

1.1.4.1 Old-World Syrah

1.1.4.2 New-World Shiraz

1.1.4.3 Reserve Shiraz

1.1.4.4 Small-Batch Syrah

1.1.5 Regional & Premium Blends

1.1.5.1 Bordeaux Blends

1.1.5.2 Rhône Blends

1.1.5.3 Super Tuscans

1.1.5.4 Proprietary Premium Blends

1.2 White Wine

1.2.1 Chardonnay

1.2.1.1 Unoaked Chardonnay

1.2.1.2 Oak-Aged Chardonnay

1.2.1.3 Single-Vineyard Chardonnay

1.2.1.4 Organic & Sustainable Chardonnay

1.2.2 Sauvignon Blanc

1.2.2.1 Marlborough Style

1.2.2.2 Old-World Sauvignon Blanc

1.2.2.3 Reserve Sauvignon Blanc

1.2.2.4 Limited-Release Sauvignon Blanc

1.2.3 Riesling

1.2.3.1 Dry Riesling

1.2.3.2 Off-Dry Riesling

1.2.3.3 Sweet Riesling

1.2.3.4 Late Harvest Riesling

1.2.4 Pinot Grigio

1.2.4.1 Italian Pinot Grigio

1.2.4.2 Premium Estate Pinot Grigio

1.2.4.3 Organic Pinot Grigio

1.2.4.4 Aromatic Reserve Pinot Grigio

1.2.5 Premium White Blends

1.2.5.1 Rhône-Style White Blends

1.2.5.2 Aromatic White Blends

1.2.5.3 Barrel-Fermented Blends

1.2.5.4 Boutique White Blends

1.3 Rosé Wine

1.3.1 Dry Rosé

1.3.1.1 Provence Style

1.3.1.2 Estate Dry Rosé

1.3.1.3 Organic Rosé

1.3.1.4 Limited-Edition Seasonal Rosé

1.3.2 Premium Rosé

1.3.2.1 Barrel-Aged Rosé

1.3.2.2 Single-Vineyard Rosé

1.3.2.3 Luxury Rosé

1.3.2.4 Collector’s Rosé

1.3.3 Sparkling Rosé

1.3.3.1 Champagne Rosé

1.3.3.2 Prosecco Rosé

1.3.3.3 Cava Rosé

1.3.3.4 Premium Vintage Sparkling Rosé

1.4 Sparkling & Champagne

1.4.1 Champagne

1.4.1.1 Non-Vintage Champagne

1.4.1.2 Vintage Champagne

1.4.1.3 Prestige Cuvée

1.4.1.4 Blanc de Blancs / Blanc de Noirs

1.4.2 Prosecco

1.4.2.1 Prosecco DOC

1.4.2.2 Prosecco DOCG

1.4.2.3 Extra Dry / Brut Variants

1.4.2.4 Premium Millesimato

1.4.3 Cava

1.4.3.1 Traditional Cava

1.4.3.2 Reserva & Gran Reserva

1.4.3.3 Organic Cava

1.4.3.4 Boutique Cava

1.4.4 Luxury Vintage Sparkling

1.4.4.1 Estate Vintage Sparkling

1.4.4.2 Limited Production Sparkling

1.4.4.3 Organic Vintage Sparkling

1.4.4.4 Collector’s Edition Sparkling

1.5 Fortified & Dessert Wines

1.5.1 Port

1.5.1.1 Ruby Port

1.5.1.2 Tawny Port

1.5.1.3 Vintage Port

1.5.1.4 Late Bottled Vintage (LBV)

1.5.2 Sherry

1.5.2.1 Fino

1.5.2.2 Amontillado

1.5.2.3 Oloroso

1.5.2.4 Pedro Ximénez

1.5.3 Late Harvest Wines

1.5.3.1 Botrytized Wines

1.5.3.2 Noble Rot Wines

1.5.3.3 Sweet Reserve Wines

1.5.3.4 Premium Dessert Selections

1.5.4 Ice Wine

1.5.4.1 Canadian Ice Wine

1.5.4.2 German Eiswein

1.5.4.3 Estate Ice Wine

1.5.4.4 Limited Vintage Ice Wine

2. By Distribution Channel

2.1 On-Trade / Hospitality

2.1.1 Fine Dining Restaurants

2.1.1.1 Michelin-Starred Establishments

2.1.1.2 Premium Independent Restaurants

2.1.1.3 Chef-Led Boutique Dining

2.1.1.4 Wine-Pairing Tasting Menu Programs

2.1.2 Hotels & Resorts

2.1.2.1 Luxury 5-Star Hotels

2.1.2.2 Boutique & Lifestyle Hotels

2.1.2.3 Resort & Destination Properties

2.1.2.4 All-Inclusive & Event Venues

2.1.3 Wine Bars & Tasting Rooms

2.1.3.1 Urban Wine Bars

2.1.3.2 Vineyard Tasting Rooms

2.1.3.3 Themed & Experiential Wine Lounges

2.1.3.4 Pop-Up & Seasonal Wine Events

2.2 Off-Trade / Retail

2.2.1 Supermarkets & Hypermarkets

2.2.1.1 Premium Imported Wine Shelves

2.2.1.2 Private Label & Store Brands

2.2.1.3 Promotional & Discounted Packs

2.2.1.4 Seasonal & Festive Collections

2.2.2 Specialty Wine Stores

2.2.2.1 Independent Boutique Retailers

2.2.2.2 Organic & Biodynamic Wine Shops

2.2.2.3 Collector & Fine Wine Merchants

2.2.2.4 Regional / Artisanal Focused Stores

2.2.3 Duty-Free & Travel Retail

2.2.3.1 Airport Duty-Free Stores

2.2.3.2 Cruise & Ferry Retail

2.2.3.3 Cross-Border Retail Outlets

2.2.3.4 Limited-Edition Travel Exclusives

2.3 Direct-to-Consumer (DTC)

2.3.1 Winery Membership Programs

2.3.1.1 Tiered Membership Clubs

2.3.1.2 Quarterly / Annual Shipment Plans

2.3.1.3 Exclusive Member-Only Releases

2.3.1.4 VIP Event & Vineyard Access

2.3.2 Subscription Wine Clubs

2.3.2.1 Curated Regional Selections

2.3.2.2 Sommelier-Curated Premium Boxes

2.3.2.3 Themed & Seasonal Collections

2.3.2.4 Personalized AI-Driven Selections

2.3.3 Estate Limited Releases

2.3.3.1 Small-Batch Micro-Lots

2.3.3.2 Single-Vineyard Allocations

2.3.3.3 Pre-Release & En Primeur Offers

2.3.3.4 Collector Allocation Programs

2.4 E-Commerce

2.4.1 Online Retail Platforms

2.4.1.1 National Online Liquor Retailers

2.4.1.2 Cross-Border Wine Platforms

2.4.1.3 Flash Sale & Discount Platforms

2.4.1.4 Premium Digital Marketplaces

2.4.2 Brand-Owned E-Stores

2.4.2.1 Winery Official Websites

2.4.2.2 Mobile Commerce Applications

2.4.2.3 Virtual Tasting & Purchase Platforms

2.4.2.4 Limited Digital-Only Releases

2.4.3 Global Wine Marketplaces

2.4.3.1 Auction-Based Platforms

2.4.3.2 Collector & Rare Wine Exchanges

2.4.3.3 B2B Wholesale Marketplaces

2.4.3.4 Investment-Grade Wine Platforms

3. By End-User

3.1 Individual Consumers

3.1.1 Millennials & Gen Z

3.1.1.1 Social & Experiential Consumers

3.1.1.2 Organic & Sustainable Wine Seekers

3.1.1.3 Digital-First Buyers

3.1.1.4 Trend-Driven & Limited-Edition Buyers

3.1.2 Affluent Urban Professionals

3.1.2.1 Premium Everyday Consumers

3.1.2.2 Corporate Entertainers

3.1.2.3 Luxury & Fine Wine Buyers

3.1.2.4 International & Imported Wine Buyers

3.1.3 Wine Collectors & Connoisseurs

3.1.3.1 Investment-Grade Collectors

3.1.3.2 Vintage & Rare Wine Enthusiasts

3.1.3.3 Auction Participants

3.1.3.4 Cellar Portfolio Builders

4. By Region

4.1 Europe

4.2 Asia-Pacific

4.3 North America

4.4 Latin America

4.5 Middle East & Africa

Regional Insights of the Global Wine Market

Europe – Largest Global Wine Market

Europe continues to dominate both global wine production and consumption, supported by historic vineyards, established appellation systems, strong export networks, and deeply rooted cultural integration of wine. Countries such as France, Italy, and Spain lead in premium and luxury segments, while Western and Northern Europe maintain strong on-trade and retail demand. Sustainability initiatives and organic certifications are further strengthening the region’s premium positioning.

Asia-Pacific – Fastest Growing Market

Asia-Pacific is the fastest-growing regional market, fueled by rapid urbanization, expanding middle-class populations, and increasing exposure to Western dining and lifestyle trends. Rising disposable incomes and growing wine education are accelerating demand across China, Japan, India, South Korea, and Southeast Asia. E-commerce platforms and digital wine clubs are playing a critical role in driving accessibility and premium adoption.

North America

North America remains a significant revenue contributor, led by the United States and Canada. Growth is driven by premium Napa and Sonoma wines, expanding direct-to-consumer (DTC) subscription services, wine tourism, and increasing demand for organic and sustainable wine varieties. Digital retail integration continues to enhance consumer engagement and margin optimization.

Latin America

Latin America is experiencing steady expansion, particularly in Brazil, Mexico, Argentina, and Chile. Growth is supported by rising urban affluence, expanding tourism, and increasing interest in premium imported and locally produced wines. The region also benefits from strong export potential and growing wine culture awareness.

Middle East & Africa

Market growth in the Middle East & Africa is concentrated in luxury hospitality hubs and high-income metropolitan centers such as Dubai and Johannesburg. Premium wine demand is largely driven by tourism, expatriate populations, and upscale dining establishments, with expansion opportunities emerging through luxury retail and hospitality infrastructure development.

Leading Companies in the Global Wine Market

-

Treasury Wine Estates

-

Pernod Ricard

-

Moët Hennessy

-

Torres

-

Penfolds

-

Champagne Louis Roederer

-

Domaine de la Romanée-Conti

E. & J. Gallo Winery remains one of the largest global wine producers in terms of scale and distribution reach.It operates across multiple price segments and has a strong international presence, supplying wines to markets around the world.

Strategic Intelligence & AI-Driven Insights

Pheonix Demand Forecast Engine – Projects stable long-term growth supported by sustained premiumization, geographic expansion in emerging markets, and rising global demand for higher-margin wine categories. The model identifies strong revenue resilience in premium and DTC segments despite macroeconomic fluctuations.

Consumer Behavior Analyzer – Detects accelerating consumer preference for organic, biodynamic, low-intervention, and limited-edition wines. Data signals growing demand for authenticity, origin transparency, sustainability credentials, and experiential consumption among Millennials and Gen Z.

Innovation Tracker – Highlights increasing investments in AI-powered vineyard monitoring, precision viticulture, climate-adaptive grape cultivation, smart inventory systems, and automated logistics optimization to enhance yield quality and operational efficiency.

Porter’s Five Forces Analysis – Reflects high competitive rivalry due to fragmented global producers, moderate supplier power in premium grape sourcing, strong brand-based differentiation, and evolving competitive advantage through sustainability practices, digital engagement, and heritage positioning.

Why the Global Wine Market Remains Critical

-

Strong global cultural integration and lifestyle association

-

Growing premium and collectible wine segment

-

Sustainable production enhances brand value

-

AI-powered analytics improve supply chain efficiency

-

Multi-channel distribution supports scalability

Final Takeaway of the Global Wine Market

The Global Wine Market is evolving into a premium-centric, sustainability-led, and digitally integrated ecosystem. The projected CAGR of ~3.8% (2026–2033) underscores stable and resilient growth, driven by premiumization, expanding direct-to-consumer (DTC) models, rising demand for organic and biodynamic wines, and shifting global consumption patterns.

Future market leadership will be defined by companies that successfully leverage AI-powered vineyard analytics, optimize supply chain efficiency, expand omnichannel distribution (retail, on-trade, DTC, and e-commerce), and elevate experiential wine tourism and brand storytelling.

At Pheonix Research, our advanced forecasting frameworks deliver comprehensive Wine Market revenue projections, competitive intelligence, and AI-backed strategic insights — empowering stakeholders to navigate the Post-2025 landscape with data-driven precision, operational agility, and sustainable long-term value creation.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7430551872865808384

X : https://x.com/Pheonix_Insight/status/2024793508293611567?s=20

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2025–2033)

1.2 Key Growth Highlights

1.3 Largest & Fastest Growing Regions

1.4 Dominant Segments

1.5 Strategic Opportunity Areas

1.6 Analyst Recommendations

2. Global Wine Market Overview

2.1 Market Definition & Scope

2.2 Industry Evolution & Historical Trends

2.3 Value Chain Analysis

2.4 Pricing Structure Analysis

2.5 Regulatory & Compliance Landscape

2.6 Taxation & Trade Policies

2.7 Supply Chain & Distribution Ecosystem

3. Market Forecast Snapshot (2026–2033)

3.1 2025 Market Size: USD 528.4 Billion

3.2 2033 Market Size: ~USD 712.6 Billion

3.3 CAGR (2026–2033): ~3.8%

3.4 Largest Region: Europe

3.5 Fastest Growing Region: Asia-Pacific

3.6 Top Segment: Still Wine (Red & White)

3.7 Key Trend: Premiumization, Sustainable Viticulture & DTC Expansion

3.8 Future Focus: Organic Wines, AI-Driven Retail Analytics & Wine Tourism

4. Market Dynamics

4.1 Market Drivers

4.2 Market Restraints

4.3 Emerging Opportunities

4.4 Industry Challenges

4.5 Impact of Macroeconomic Factors

4.6 Technological Advancements in Viticulture

5. Market Segmentation by Wine Type (USD Billion), 2026–2033

5.1 Red Wine

5.1.1 Cabernet Sauvignon

5.1.1.1 Premium Reserve Cabernet

5.1.1.2 Single-Vineyard Cabernet

5.1.1.3 Oak-Aged Cabernet

5.1.1.4 Organic & Biodynamic Cabernet

5.1.2 Merlot

5.1.2.1 Estate Bottled Merlot

5.1.2.2 Blended Merlot

5.1.2.3 Barrel-Aged Merlot

5.1.2.4 Limited-Edition Merlot

5.1.3 Pinot Noir

5.1.3.1 Cool-Climate Pinot Noir

5.1.3.2 Single-Origin Pinot Noir

5.1.3.3 Organic Pinot Noir

5.1.3.4 Luxury Vintage Pinot Noir

5.1.4 Syrah / Shiraz

5.1.4.1 Old-World Syrah

5.1.4.2 New-World Shiraz

5.1.4.3 Reserve Shiraz

5.1.4.4 Small-Batch Syrah

5.1.5 Regional & Premium Blends

5.1.5.1 Bordeaux Blends

5.1.5.2 Rhône Blends

5.1.5.3 Super Tuscans

5.1.5.4 Proprietary Premium Blends

5.2 White Wine

5.2.1 Chardonnay

5.2.1.1 Unoaked Chardonnay

5.2.1.2 Oak-Aged Chardonnay

5.2.1.3 Single-Vineyard Chardonnay

5.2.1.4 Organic & Sustainable Chardonnay

5.2.2 Sauvignon Blanc

5.2.2.1 Marlborough Style

5.2.2.2 Old-World Sauvignon Blanc

5.2.2.3 Reserve Sauvignon Blanc

5.2.2.4 Limited-Release Sauvignon Blanc

5.2.3 Riesling

5.2.3.1 Dry Riesling

5.2.3.2 Off-Dry Riesling

5.2.3.3 Sweet Riesling

5.2.3.4 Late Harvest Riesling

5.2.4 Pinot Grigio

5.2.4.1 Italian Pinot Grigio

5.2.4.2 Premium Estate Pinot Grigio

5.2.4.3 Organic Pinot Grigio

5.2.4.4 Aromatic Reserve Pinot Grigio

5.2.5 Premium White Blends

5.2.5.1 Rhône-Style White Blends

5.2.5.2 Aromatic White Blends

5.2.5.3 Barrel-Fermented Blends

5.2.5.4 Boutique White Blends

5.3 Rosé Wine

5.3.1 Dry Rosé

5.3.1.1 Provence Style

5.3.1.2 Estate Dry Rosé

5.3.1.3 Organic Rosé

5.3.1.4 Limited-Edition Seasonal Rosé

5.3.2 Premium Rosé

5.3.2.1 Barrel-Aged Rosé

5.3.2.2 Single-Vineyard Rosé

5.3.2.3 Luxury Rosé

5.3.2.4 Collector’s Rosé

5.3.3 Sparkling Rosé

5.3.3.1 Champagne Rosé

5.3.3.2 Prosecco Rosé

5.3.3.3 Cava Rosé

5.3.3.4 Premium Vintage Sparkling Rosé

5.4 Sparkling & Champagne

5.4.1 Champagne

5.4.1.1 Non-Vintage

5.4.1.2 Vintage

5.4.1.3 Prestige Cuvée

5.4.1.4 Blanc de Blancs / Blanc de Noirs

5.4.2 Prosecco

5.4.2.1 DOC

5.4.2.2 DOCG

5.4.2.3 Extra Dry / Brut

5.4.2.4 Millesimato

5.4.3 Cava

5.4.3.1 Traditional

5.4.3.2 Reserva & Gran Reserva

5.4.3.3 Organic

5.4.3.4 Boutique

5.4.4 Luxury Vintage Sparkling

5.4.4.1 Estate Vintage

5.4.4.2 Limited Production

5.4.4.3 Organic Vintage

5.4.4.4 Collector’s Edition

5.5 Fortified & Dessert Wines

5.5.1 Port

5.5.1.1 Ruby

5.5.1.2 Tawny

5.5.1.3 Vintage

5.5.1.4 LBV

5.5.2 Sherry

5.5.2.1 Fino

5.5.2.2 Amontillado

5.5.2.3 Oloroso

5.5.2.4 Pedro Ximénez

5.5.3 Late Harvest Wines

5.5.3.1 Botrytized

5.5.3.2 Noble Rot

5.5.3.3 Sweet Reserve

5.5.3.4 Premium Dessert Selection

5.5.4 Ice Wine

5.5.4.1 Canadian Ice Wine

5.5.4.2 German Eiswein

5.5.4.3 Estate Ice Wine

5.5.4.4 Limited Vintage Ice Wine

6. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

6.1 On-Trade / Hospitality

6.1.1 Fine Dining Restaurants

6.1.1.1 Michelin-Starred Establishments

6.1.1.2 Premium Independent Restaurants

6.1.1.3 Chef-Led Boutique Dining

6.1.1.4 Wine-Pairing Tasting Menu Programs

6.1.2 Hotels & Resorts

6.1.2.1 Luxury 5-Star Hotels

6.1.2.2 Boutique & Lifestyle Hotels

6.1.2.3 Resort & Destination Properties

6.1.2.4 All-Inclusive & Event Venues

6.1.3 Wine Bars & Tasting Rooms

6.1.3.1 Urban Wine Bars

6.1.3.2 Vineyard Tasting Rooms

6.1.3.3 Themed & Experiential Wine Lounges

6.1.3.4 Pop-Up & Seasonal Wine Events

6.1.4 Cruise Lines & Premium Travel Catering

6.1.4.1 Luxury Cruise Operators

6.1.4.2 Private Yacht Catering

6.1.4.3 Airline First & Business Class Service

6.1.4.4 International Travel Hospitality Programs

6.2 Off-Trade / Retail

6.2.1 Supermarkets & Hypermarkets

6.2.1.1 Premium Imported Wine Shelves

6.2.1.2 Private Label & Store Brands

6.2.1.3 Promotional & Discounted Packs

6.2.1.4 Seasonal & Festive Collections

6.2.2 Specialty Wine Stores

6.2.2.1 Independent Boutique Retailers

6.2.2.2 Organic & Biodynamic Wine Shops

6.2.2.3 Collector & Fine Wine Merchants

6.2.2.4 Regional / Artisanal Focused Stores

6.2.3 Duty-Free & Travel Retail

6.2.3.1 Airport Duty-Free Stores

6.2.3.2 Cruise & Ferry Retail

6.2.3.3 Cross-Border Retail Outlets

6.2.3.4 Limited-Edition Travel Exclusives

6.2.4 Warehouse Clubs & Bulk Retailers

6.2.4.1 Membership-Based Wholesale Clubs

6.2.4.2 Discount Bulk Wine Retailers

6.2.4.3 Private Label Bulk Programs

6.2.4.4 Value-Oriented Premium Multipacks

6.3 Direct-to-Consumer (DTC)

6.3.1 Winery Membership Programs

6.3.1.1 Tiered Membership Clubs

6.3.1.2 Quarterly / Annual Shipment Plans

6.3.1.3 Exclusive Member-Only Releases

6.3.1.4 VIP Event & Vineyard Access

6.3.2 Subscription Wine Clubs

6.3.2.1 Curated Regional Selections

6.3.2.2 Sommelier-Curated Premium Boxes

6.3.2.3 Themed & Seasonal Collections

6.3.2.4 Personalized AI-Driven Selections

6.3.3 Estate Limited Releases

6.3.3.1 Small-Batch Micro-Lots

6.3.3.2 Single-Vineyard Allocations

6.3.3.3 Pre-Release & En Primeur Offers

6.3.3.4 Collector Allocation Programs

6.3.4 Digital Engagement & Virtual Commerce

6.3.4.1 Virtual Tasting Events

6.3.4.2 Live Commerce Wine Launches

6.3.4.3 Influencer & Sommelier Collaborations

6.3.4.4 NFT / Digital Ownership Wine Programs

6.4 E-Commerce

6.4.1 Online Retail Platforms

6.4.1.1 National Online Liquor Retailers

6.4.1.2 Cross-Border Wine Platforms

6.4.1.3 Flash Sale & Discount Platforms

6.4.1.4 Premium Digital Marketplaces

6.4.2 Brand-Owned E-Stores

6.4.2.1 Winery Official Websites

6.4.2.2 Mobile Commerce Applications

6.4.2.3 Virtual Tasting & Purchase Platforms

6.4.2.4 Limited Digital-Only Releases

6.4.3 Global Wine Marketplaces

6.4.3.1 Auction-Based Platforms

6.4.3.2 Collector & Rare Wine Exchanges

6.4.3.3 B2B Wholesale Marketplaces

6.4.3.4 Investment-Grade Wine Platforms

6.4.4 Quick Commerce & App-Based Delivery

6.4.4.1 30–60 Minute Delivery Platforms

6.4.4.2 Urban On-Demand Alcohol Apps

6.4.4.3 Premium Concierge Delivery

6.4.4.4 Subscription-Based Instant Delivery

7. Market Segmentation by End User (USD Billion), 2026–2033

7.1 Individual Consumers

7.1.1 Millennials & Gen Z

7.1.1.1 Social & Experiential Consumers

7.1.1.2 Organic & Sustainable Wine Seekers

7.1.1.3 Digital-First Buyers

7.1.1.4 Trend-Driven & Limited-Edition Buyers

7.1.2 Affluent Urban Professionals

7.1.2.1 Premium Everyday Consumers

7.1.2.2 Corporate Entertainers

7.1.2.3 Luxury & Fine Wine Buyers

7.1.2.4 International & Imported Wine Buyers

7.1.3 Wine Collectors & Connoisseurs

7.1.3.1 Investment-Grade Collectors

7.1.3.2 Vintage & Rare Wine Enthusiasts

7.1.3.3 Auction Participants

7.1.3.4 Cellar Portfolio Builders

7.2 Corporate & Institutional Buyers

7.2.1 Hospitality Groups

7.2.1.1 International Hotel Chains

7.2.1.2 Premium Restaurant Groups

7.2.1.3 Luxury Resort Operators

7.2.1.4 Cruise & Travel Hospitality Groups

7.2.2 Corporate Gifting

7.2.2.1 Festive & Seasonal Corporate Hampers

7.2.2.2 Premium Client Appreciation Gifts

7.2.2.3 Executive & Board-Level Gifting

7.2.2.4 Custom-Branded Wine Labels

7.2.3 Event & Banquet Procurement

7.2.3.1 Weddings & Private Celebrations

7.2.3.2 Corporate Conferences & Summits

7.2.3.3 Luxury Gala Events

7.2.3.4 Government & Diplomatic Events

8. Market Segmentation by Region (USD Billion), 2026–2033

8.1 Europe

8.2 Asia-Pacific

8.3 North America

8.4 Latin America

8.5 Middle East & Africa

9. Regional Insights

9.1 Europe – Largest Market

9.2 Asia-Pacific – Fastest Growing

9.3 North America – Premium & DTC Expansion

9.4 Latin America – Emerging Growth

9.5 Middle East & Africa – Luxury Hospitality Driven

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Benchmarking

10.3 M&A & Strategic Alliances

10.4 Innovation & Product Launch Analysis

11. Company Profiles

11.1 E. & J. Gallo Winery

11.2 Concha y Toro

11.3 Treasury Wine Estates

11.4 Pernod Ricard

11.5 Moët Hennessy

11.6 Torres

11.7 Penfolds

11.8 Champagne Louis Roederer

11.9 Domaine de la Romanée-Conti

12. Strategic Intelligence & AI-Driven Insights

12.1 Pheonix Demand Forecast Engine

12.2 Consumer Behavior Analyzer

12.3 Innovation Tracker

12.4 Porter’s Five Forces Analysis

12.5 Investment & Expansion Outlook

13. Why the Global Wine Market Remains Critical

13.1 Cultural & Lifestyle Integration

13.2 Premium & Collectible Growth

13.3 Sustainability & Organic Expansion

13.4 AI-Driven Operational Optimization

13.5 Omnichannel Distribution Scalability

14. Appendix

15. About Us

16. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Wine Market

Executive Framing

The Global Wine Market is characterized by high competitive intensity and a fragmented market structure, where legacy European producers, global beverage conglomerates, and boutique wineries coexist. The market is deeply rooted in heritage, terroir, and brand storytelling, while simultaneously evolving through premiumization, sustainability, and digital transformation. As consumer preferences shift toward quality, authenticity, and experiential consumption, companies must balance traditional craftsmanship with modern distribution and technology-driven strategies to remain competitive.

Current Market Reality

The global wine market remains highly fragmented, with thousands of producers operating across regions, from large-scale companies such as E. & J. Gallo Winery, Concha y Toro, and Treasury Wine Estates to small boutique vineyards and family-owned wineries. Europe continues to dominate production and exports, while Asia-Pacific is emerging as a key consumption growth engine.

Direct-to-consumer (DTC) channels, subscription-based wine clubs, and e-commerce platforms are reshaping traditional distribution models, enabling wineries to enhance margins and customer engagement. At the same time, sustainability practices, including organic and biodynamic viticulture, are becoming critical differentiators in premium positioning, while wine tourism is strengthening brand loyalty and experiential value.

Key Signals and Evidence

Several signals highlight the evolving competitive dynamics in the global wine market:

- Growing demand for premium, aged, and limited-edition wines across both mature and emerging markets.

- Rapid expansion of direct-to-consumer (DTC) models, including winery memberships and subscription wine clubs.

- Rising adoption of organic, biodynamic, and sustainable wine production practices.

- Increasing investment in AI-driven vineyard management, supply chain optimization, and customer analytics.

- Strong growth in experiential consumption, including wine tourism, tasting events, and vineyard-based experiences.

Strategic Implications

Market participants must adopt integrated strategies combining heritage, innovation, and digital engagement:

- Premium Differentiation: Leveraging origin, vintage quality, and exclusivity to strengthen brand positioning.

- Omnichannel Expansion: Expanding DTC, e-commerce, and retail distribution to maximize reach and margins.

- Sustainability Leadership: Investing in organic, biodynamic, and eco-friendly production methods.

- Experiential Marketing: Enhancing wine tourism, tasting experiences, and brand storytelling.

- Technology Integration: Utilizing AI-driven analytics for demand forecasting, vineyard optimization, and personalized consumer engagement.

Forward Outlook

By 2033, the Global Wine Market is expected to reach approximately USD 712.6 billion, growing at a CAGR of ~3.8%. Europe will continue to lead in production and premium segments, while Asia-Pacific will remain the fastest-growing consumption market, driven by rising incomes and evolving wine culture.

The market will evolve through a dual-structure model, combining high-margin premium and experiential wine segments with scalable retail and DTC distribution channels. Companies that effectively integrate sustainability, digital transformation, and premium storytelling will be best positioned to capture long-term growth in this competitive and globally diverse market.

Value Chain

Global Wine Market: Value Chain & Market Dynamics

Executive Framing

The Global Wine Market is evolving steadily, driven by premiumization, changing consumer lifestyles, and expansion of digital retail channels. Wine categories—including red, white, rosé, sparkling, and fortified wines—are transforming into experience-oriented ecosystems where quality, authenticity, and sustainability increasingly define consumer choice.

The market operates through a hybrid value chain that balances large-scale traditional wine production with niche, innovation-driven wineries. Established producers leverage historic vineyards, international distribution networks, and economies of scale, while emerging brands focus on organic, biodynamic, and limited-edition wines with direct-to-consumer (DTC) and e-commerce distribution. This structure introduces both efficiency and differentiation challenges.

Challenges remain in sourcing premium grapes, maintaining consistent quality across regions, and ensuring regulatory compliance for organic or biodynamic certification. Additionally, expansion of wine tourism and digital platforms necessitates agile operations in logistics, retail, and customer engagement.

Current Market Reality

The Global Wine Market is characterized by moderate complexity, combining large-scale production efficiency with premium and specialty product differentiation. Leading players such as E. & J. Gallo Winery, Concha y Toro, and Treasury Wine Estates dominate upstream procurement and downstream distribution through vertically integrated operations.

Upstream, grape sourcing varies between controlled estate vineyards and third-party growers, influencing consistency, cost, and sustainability. Midstream operations involve vinification, aging, blending, and bottling across red, white, rosé, sparkling, and fortified varieties. Increasing demand for organic, biodynamic, and limited-edition wines drives R&D and specialty production techniques.

Downstream, distribution spans on-trade channels (restaurants, hotels, wine bars), off-trade retail (supermarkets, specialty stores, duty-free), and digital DTC platforms. Omnichannel engagement, including wine clubs and subscription boxes, is reshaping traditional retail dominance and enabling smaller wineries to reach global consumers.

Key Signals and Evidence

- The market is projected to grow from USD 528.4 billion (2025) to ~USD 712.6 billion (2033) at a CAGR of ~3.8%, reflecting steady demand across mature and emerging markets.

- Premiumization trends are driving preference for limited-edition, aged, and single-vineyard wines.

- Organic and biodynamic wine adoption is increasing, influencing upstream vineyard management and sourcing strategies.

- Expansion of wine tourism and digital platforms is enhancing consumer engagement and experiential value.

- Asia-Pacific is emerging as the fastest-growing region due to rising urbanization, disposable income, and wine education.

Market power dynamics indicate moderate supplier influence in premium grape sourcing and high buyer power in commoditized wine segments, especially standard red and white wines.

Strategic Implications

Market participants must navigate the trade-off between scale efficiency and premium differentiation. Large producers leverage historic vineyards, production scale, and distribution reach, while investing in premium, organic, and biodynamic portfolios to capture high-margin segments.

Emerging wineries can gain a competitive advantage through value chain agility, including targeted vineyard sourcing, boutique vinification, limited releases, and DTC distribution. Leveraging technology—such as AI-driven vineyard analytics, demand forecasting, and inventory management—enhances efficiency, quality, and regulatory compliance.

Sustainability and circular supply chain models, including eco-friendly packaging and responsible sourcing, are increasingly critical for regulatory alignment and consumer trust.

Forward Outlook

The Global Wine Market is expected to continue evolving toward a premium, sustainability-focused, and digitally integrated ecosystem. Key trends shaping the near-to-medium term include:

- Expansion of DTC channels, online wine clubs, and subscription-based delivery models

- Increased adoption of organic, biodynamic, and low-intervention wines

- Growth of experiential wine tourism, tastings, and curated vineyard experiences

- Investment in regional production hubs, especially in Asia-Pacific, to meet localized demand and optimize costs

- Enhanced focus on sustainable sourcing, packaging, and supply chain transparency

Wineries that successfully integrate premium production, digital engagement, sustainable practices, and experiential offerings will be best positioned to capture long-term value in the evolving wine market.

Investment Activity

Investment & Funding Dynamics – Global Wine Market

Executive Framing

Current Market Reality

The Global Wine Market, valued at USD 528.4 billion in 2025 and projected to reach ~USD 712.6 billion by 2033 (CAGR ~3.8%), is experiencing stable to moderately rising investment activity. Europe remains the dominant investment hub due to its established vineyard infrastructure, while Asia-Pacific is attracting new capital driven by rising consumption and premium adoption. Investments are largely directed toward sustainable vineyard practices, premium wine production, digital sales channels, and wine tourism infrastructure. Major companies such as E. & J. Gallo Winery, Pernod Ricard, and Treasury Wine Estates continue to invest in portfolio diversification, supply chain optimization, and global expansion.

Key Signals and Evidence

- Premiumization Trend: Increasing demand for high-quality, aged, and limited-edition wines supports consistent capital inflow.

- Sustainable Viticulture: Rising investment in organic, biodynamic, and climate-resilient vineyard practices.

- DTC & E-Commerce Expansion: Growth in online wine retail, subscription services, and winery-direct sales channels.

- Wine Tourism Development: Vineyard experiences, tasting events, and luxury hospitality are attracting infrastructure investments.

- Emerging Market Growth: Asia-Pacific and Latin America are driving new investment opportunities.

- M&A Activity: Ongoing consolidation through acquisitions of boutique wineries and premium brands.

- Technology Integration: AI-powered vineyard monitoring, demand forecasting, and logistics optimization are gaining traction.

Strategic Implications

Companies that focus on premium offerings, sustainability, and digital engagement are better positioned to attract investment and sustain competitive advantage. Investors are prioritizing scalable DTC models, strong brand heritage, and global distribution capabilities. Strategic acquisitions and partnerships enable market consolidation, portfolio diversification, and expansion into high-growth regions, particularly in premium and organic segments.

Forward Outlook

From 2026 to 2033, the Global Wine Market is expected to maintain stable investment momentum. Capital will increasingly flow into sustainable production, premium innovation, and digital retail ecosystems. M&A activity will remain consistent as companies seek to strengthen market positioning and expand global reach. Investors focusing on AI-driven analytics, climate-adaptive viticulture, and experiential wine tourism will unlock long-term value in this mature yet evolving market.

Technology & Innovation

Global Wine Market: Technology & Innovation

Executive Framing

In the global wine market, technology and innovation are evolving alongside deeply rooted traditional practices. While winemaking remains heritage-driven, modern advancements in precision viticulture, AI-powered analytics, and sustainable production are transforming how wine is cultivated, produced, and distributed. Innovation is increasingly centered on improving grape quality, optimizing yield, enhancing supply chain efficiency, and delivering personalized consumer experiences through digital platforms and direct-to-consumer channels.

Current Market Reality

The current wine market reflects a mature technological landscape with incremental innovation. Wineries are adopting AI and IoT-based vineyard monitoring systems to track soil conditions, weather patterns, and vine health, enabling better decision-making and climate resilience. Automation in fermentation, bottling, and logistics ensures consistency and scalability. At the same time, digital transformation through e-commerce, wine apps, and subscription services is reshaping consumer access and engagement. Sustainability remains a core innovation pillar, with increasing adoption of organic and biodynamic practices.

Key Signals and Evidence

- Precision Viticulture: Use of AI, drones, and IoT sensors enhances vineyard management, yield quality, and climate adaptability.

- Sustainable Production: Expansion of organic, biodynamic, and low-intervention winemaking supports environmental goals and premium positioning.

- Digital & DTC Ecosystems: Growth in online wine retail, subscriptions, and virtual tastings improves accessibility and customer engagement.

- Automation & Smart Logistics: Advanced production and inventory systems optimize efficiency and reduce operational costs.

- Data-Driven Consumer Insights: AI analytics enable personalized recommendations, targeted marketing, and demand forecasting.

Strategic Implications

For wine producers, the integration of technology enhances both operational efficiency and competitive differentiation. Precision agriculture reduces production risks and improves consistency, while digital channels provide higher-margin sales opportunities and direct consumer relationships. Sustainability innovations strengthen regulatory compliance and brand equity. Companies that successfully blend tradition with modern innovation can maintain authenticity while scaling globally and adapting to evolving consumer preferences.

Forward Outlook

The global wine market will continue to see gradual but impactful innovation. Future developments will focus on AI-driven vineyard optimization, climate-resilient grape varieties, expanded adoption of sustainable practices, and enhanced digital consumer experiences. Growth in direct-to-consumer ecosystems and wine tourism integration will further support market expansion. Companies that effectively combine heritage, sustainability, and technology will be best positioned for long-term success in the post-2026 landscape.

Market Risk

Risk Factors and Disruption Threats in the Global Wine Market

Executive Framing

The Global Wine Market represents a large, mature, and culturally embedded segment within the alcoholic beverage industry, characterized by steady growth and strong premiumization trends. With a projected CAGR of ~3.8% from 2026–2033, the market remains resilient but faces structural constraints related to climate dependency, regulatory complexities, shifting consumption patterns, and increasing competition from alternative alcoholic and low-alcohol beverages.

Current Market Reality

Europe dominates global production and consumption, while Asia-Pacific drives incremental growth. However, the industry is highly sensitive to agricultural conditions, including climate change, unpredictable weather patterns, and vineyard yield variability. Additionally, strict alcohol regulations, taxation policies, and trade barriers create operational challenges across regions, while evolving consumer preferences toward low-alcohol and functional beverages are reshaping demand dynamics.

Key Signals and Evidence

Key signals include rising demand for organic and biodynamic wines, growth in direct-to-consumer and e-commerce channels, and increasing interest in wine tourism and premium experiences. At the same time, substitution from craft spirits, beer, RTDs, and non-alcoholic beverages is intensifying competition. Climate-related disruptions and sustainability pressures are also becoming more prominent across major wine-producing regions globally.

Strategic Implications

Producers must invest in climate-resilient viticulture, precision agriculture, and sustainable farming practices to mitigate environmental risks. Strengthening DTC channels, leveraging AI-driven demand forecasting, and enhancing brand storytelling will be essential for maintaining competitiveness. Companies must also navigate complex global regulatory frameworks while optimizing supply chains and expanding into high-growth emerging markets.

Forward Outlook

The Global Wine Market is expected to maintain stable long-term growth, supported by premiumization and expanding global wine culture. However, long-term success will depend on effectively managing climate risks, regulatory pressures, and rising competition from alternative beverage categories.

Regulatory Landscape

Regulatory & Policy Landscape: Global Wine Market

Executive Framing

The Global Wine Market operates within a highly complex and tightly regulated framework, driven by alcohol control laws, international trade policies, geographical indication systems, and evolving sustainability mandates. Regulatory oversight spans the entire value chain—from vineyard cultivation and production to labeling, distribution, marketing, and cross-border trade.

Key regulatory authorities include the European Commission (EU wine regulations), U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB), Food Safety and Standards Authority of India (FSSAI), and various national alcohol control boards. These bodies enforce standards related to origin certification, alcohol content, labeling transparency, taxation, and consumer safety.

Wine, particularly premium and region-specific varieties, is also governed by strict geographical indication (GI) and appellation systems, ensuring authenticity, quality control, and protection of regional heritage.

Current Market Reality

Europe maintains the most advanced regulatory ecosystem, with well-established appellation systems such as AOC (France), DOC/DOCG (Italy), and DO (Spain). These frameworks strictly regulate grape sourcing, production techniques, and labeling, reinforcing premium positioning while increasing compliance requirements.

In North America, regulations focus on labeling, taxation, distribution structures, and interstate shipping laws. The U.S. three-tier system (producer–distributor–retailer) adds operational complexity, although direct-to-consumer (DTC) wine sales are expanding under evolving legal frameworks.

Asia-Pacific markets are highly diverse, with varying import duties, licensing requirements, and labeling standards across countries such as China, India, and Japan. High tariffs and regulatory barriers impact pricing, availability, and market entry strategies for global wine producers.

Globally, sustainability regulations—including organic certification, carbon footprint reduction, and eco-friendly packaging—are increasingly influencing production practices and brand positioning.

Key Signals and Evidence

- Strict geographical indication (GI) and appellation laws governing origin and quality.

- Mandatory labeling requirements including alcohol content, origin, and health warnings.

- High excise duties, tariffs, and cross-border trade restrictions.

- Regulation of advertising, sponsorship, and alcohol marketing practices.

- Expansion of direct-to-consumer (DTC) shipping compliance frameworks.

- Growing emphasis on organic, biodynamic, and sustainable certification standards.

Strategic Implications

Regulatory frameworks significantly influence market structure, acting as both barriers to entry and mechanisms for value creation. Appellation systems enhance brand equity and pricing power but require strict adherence to production standards. Companies must invest in compliance infrastructure, certification processes, and traceability systems to maintain market access and competitiveness.

Trade barriers and taxation policies in emerging markets can limit expansion but also create opportunities for strategic partnerships, localized production, and regional distribution models. Direct-to-consumer channels offer higher margins but require navigation of complex shipping and taxation regulations.

Sustainability compliance is becoming a critical competitive factor, with consumers and regulators increasingly prioritizing environmentally responsible production and transparent sourcing practices.

Forward Outlook

The regulatory landscape is expected to become more stringent, particularly in areas such as sustainability reporting, organic certification, labeling transparency, and responsible alcohol consumption policies. Governments are likely to enforce stricter controls on marketing practices and health-related disclosures.

Global trade dynamics will continue to influence market access, with tariffs, bilateral agreements, and geopolitical factors shaping international wine flows. Digitalization of wine sales will introduce additional regulatory requirements around e-commerce, age verification, and cross-border logistics.

Companies that proactively align with evolving regulatory frameworks, invest in sustainable vineyard practices, and adopt region-specific compliance strategies will be best positioned to sustain long-term growth and premium positioning in the global wine market.