Global Radio Pharmaceuticals Market Report, Size & Foerecast 2026-2033

Global Radio Pharmaceuticals Market Report, Size, Share and Forecast 2026???2033

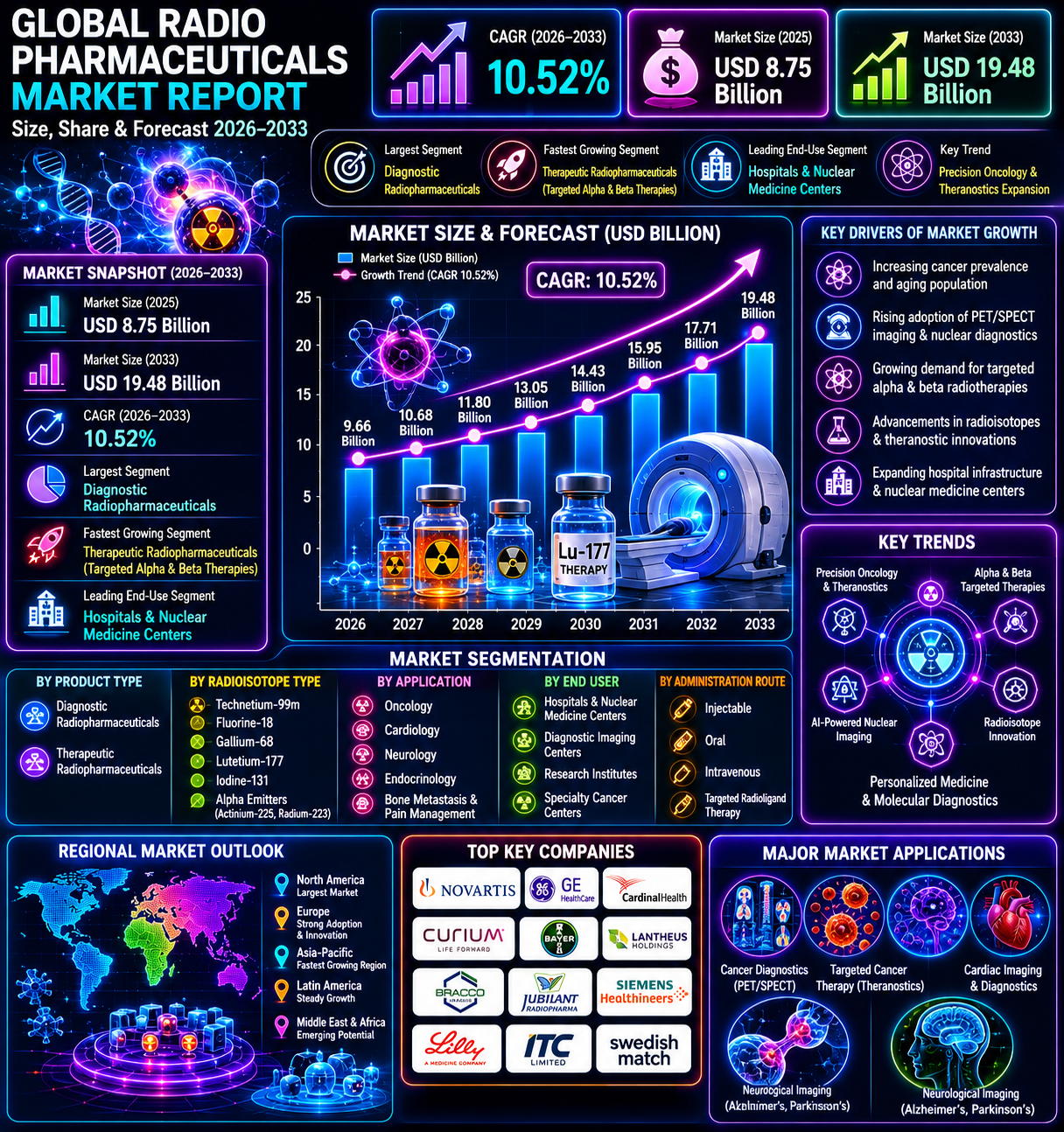

Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 8.75 Billion |

| Market Size (2033) | USD 19.48 Billion |

| CAGR (2026???2033) | 10.52% |

| Largest Segment | Diagnostic Radiopharmaceuticals |

| Fastest Growing Segment | Therapeutic Radiopharmaceuticals (Targeted Alpha & Beta Therapies) |

| Leading End-Use Segment | Hospitals & Nuclear Medicine Centers |

| Key Trend | Precision Oncology & Theranostics Expansion |

| Regulatory Influence | Radioisotope Safety Standards, Nuclear Medicine Regulations & Clinical Trial Compliance |

| Future Outlook | Growth Driven by Cancer Diagnostics, Targeted Therapy & Isotope Innovation |

Market Size & Forecast

The Global Radio Pharmaceuticals Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 8.75 billion in 2025 and is projected to reach approximately USD 19.48 billion by 2033, registering a CAGR of 10.52%. The market growth is primarily driven by increasing cancer prevalence, rising cardiovascular and neurological disorders, growth in precision medicine, expanding PET/SPECT imaging adoption, and increasing use of targeted radioligand therapies. Radiopharmaceuticals are increasingly critical in molecular imaging, oncology diagnostics, nuclear cardiology, neurological disease detection, prostate cancer treatment, and theranostic medicine. Growing adoption of radioisotopes, targeted alpha therapy, beta-emitting agents, and personalized treatment planning is accelerating market expansion. In addition, increasing healthcare investment, isotope production innovation, and demand for non-invasive targeted diagnostics are supporting long-term industry growth.Global Radio Pharmaceuticals Market Overview

Radiopharmaceuticals are radioactive compounds used in nuclear medicine for disease diagnosis, imaging, and targeted therapeutic applications. The market includes diagnostic radiopharmaceuticals, therapeutic radiopharmaceuticals, PET tracers, SPECT tracers, alpha emitters, beta emitters, and theranostic agents. These products are widely used across oncology, cardiology, neurology, endocrinology, bone metastasis treatment, and targeted cancer therapeutics. The market is shifting from conventional imaging agents toward targeted radioligand therapies, theranostics, AI-integrated nuclear diagnostics, and precision molecular medicine.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in targeted radioligand therapies, PET tracers, isotope engineering, theranostics, and AI-assisted molecular imaging is accelerating commercialization. Advanced isotope production and next-generation oncology tracers are improving diagnostic precision and therapeutic outcomes.Market Implications

Manufacturers investing in theranostic compounds, targeted isotopes, and high-precision nuclear therapies are expected to strengthen market competitiveness.2. Compliance and Risk Repricing

Radiation safety standards, nuclear medicine regulations, isotope transport rules, GMP manufacturing, and clinical validation requirements strongly shape the market. Healthcare systems are increasingly emphasizing controlled handling, safety monitoring, and regulated therapeutic use.Market Implications

Companies offering compliant, safe, clinically validated, and scalable radiopharmaceutical solutions are likely to gain stronger market adoption.3. Competitive and Value-Chain Reconfiguration

Pharmaceutical companies, isotope producers, nuclear medicine suppliers, cyclotron operators, and theranostics developers are expanding product portfolios. Isotope scarcity, logistics complexity, and targeted therapy specialization are reshaping value-chain dynamics.Market Implications

Firms focusing on isotope supply stability, vertical integration, and advanced therapeutic radioligands may gain stronger margins.4. Capital and Capacity Scaling

Rising investment in isotope production facilities, nuclear medicine centers, cyclotron infrastructure, and oncology radiotherapy programs is supporting market expansion. Governments and private players are strengthening radiopharma manufacturing capabilities globally.Market Implications

Manufacturers scaling isotope production, targeted therapy development, and precision oncology infrastructure are expected to capture future opportunities.Market Segmentation Analysis

By Product Type

1. Diagnostic Radiopharmaceuticals

This remains the largest segment due to widespread PET and SPECT imaging demand.2. Therapeutic Radiopharmaceuticals

Fastest-growing segment due to targeted cancer treatment expansion.By Radioisotope Type

1. Technetium-99m

Largest isotope segment due to broad diagnostic use.2. Fluorine-18

Strong growth in PET imaging applications.3. Gallium-68

Growing rapidly in prostate and neuroendocrine imaging.4. Lutetium-177

Critical in targeted radioligand therapy.5. Iodine-131

Widely used in thyroid disease treatment.6. Alpha Emitters (Actinium-225, Radium-223)

High-growth precision oncology segment.By Application

1. Oncology

Largest application segment due to cancer diagnosis and targeted treatment.2. Cardiology

Used in myocardial perfusion and cardiac imaging.3. Neurology

Used in Alzheimer???s, Parkinson???s, and brain imaging.4. Endocrinology

Strong use in thyroid diagnostics and treatment.5. Bone Metastasis & Pain Management

Growing therapeutic use.By End User

1. Hospitals & Nuclear Medicine Centers

Largest segment due to advanced imaging and treatment infrastructure.2. Diagnostic Imaging Centers

Growing due to PET/SPECT demand.3. Research Institutes

Important for isotope development and trials.4. Specialty Cancer Centers

Rapidly growing in precision oncology treatment.Regional Market Dynamics

North America

North America dominates the global radiopharmaceuticals market due to advanced nuclear medicine infrastructure, oncology adoption, and strong isotope R&D.Europe

Europe remains a major market supported by theranostics growth, cancer treatment innovation, and strong healthcare regulation.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rising cancer burden, healthcare modernization, and expanding nuclear medicine facilities.Latin America

Latin America is gradually expanding due to imaging infrastructure growth and oncology investments.Middle East & Africa

The region is witnessing emerging growth due to hospital expansion and radiology service adoption.Competitive Landscape

The Global Radio Pharmaceuticals Market is moderately consolidated with pharmaceutical manufacturers, isotope producers, and nuclear medicine companies competing globally. Key companies operating in the market include:- Novartis AG

- GE HealthCare

- Cardinal Health

- Curium Pharma

- Bayer AG

- Lantheus Holdings

- Bracco Imaging

- Jubilant Radiopharma

- Siemens Healthineers

- Eli Lilly (Point Biopharma)

Strategic Outlook

The future of the radiopharmaceuticals market will be shaped by theranostics, alpha-emitter therapies, targeted oncology, AI-based nuclear imaging, and isotope production innovation. Rising demand for personalized oncology, non-invasive molecular imaging, and precision-targeted therapies is expected to support long-term expansion. Advanced radioligand therapies, isotope engineering, and oncology-centered diagnostics are likely to create major growth opportunities.Final Market Perspective

The Global Radio Pharmaceuticals Market remains one of the fastest-growing segments within nuclear medicine, oncology therapeutics, and precision diagnostics. Rising demand for targeted imaging, cancer therapy, and personalized medicine continues driving long-term market growth. Companies capable of delivering compliant, high-precision, scalable, and advanced theranostic solutions will be best positioned to capture future opportunities. The convergence of isotope innovation, molecular diagnostics, and targeted radiotherapy is expected to redefine the future of the global radiopharmaceuticals industry.Table of Contents

Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Growth Highlights

1.3 Largest Segment Analysis

1.4 Fastest Growing Segment Analysis

1.5 Regional Outlook

1.6 Competitive Landscape Snapshot

1.7 Future Market Outlook

2. Global Radio Pharmaceuticals Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Radio Pharmaceuticals Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Pricing & Revenue Structure Analysis

3.5 Isotope Supply Chain & Nuclear Medicine Infrastructure Overview

3.6 Product & Therapeutic Landscape

3.6.1 Diagnostic Radiopharmaceuticals

3.6.1.1 PET Imaging Agents

3.6.1.1.1 SPECT Imaging Agents

3.6.1.1.1.1 Molecular Imaging Expansion

3.6.1.1.1.2 Precision Diagnostic Innovation

3.6.2 Therapeutic Radiopharmaceuticals

3.6.2.1 Targeted Alpha Therapies

3.6.2.1.1 Targeted Beta Therapies

3.6.2.1.1.1 Oncology Radioligand Treatment Growth

3.6.2.1.1.2 Advanced Therapeutic Precision

3.6.3 Theranostic Agents

3.6.3.1 Integrated Diagnostic-Therapeutic Solutions

3.6.3.1.1 Personalized Cancer Management

3.6.3.1.1.1 Multi-Target Oncology Applications

3.6.3.1.1.2 Future Precision Medicine Trends

3.6.4 AI-Integrated Nuclear Imaging

3.6.4.1 Smart Diagnostic Workflows

3.6.4.1.1 Predictive Oncology Imaging

3.6.4.1.1.1 Imaging Automation Growth

3.6.4.1.1.2 Clinical Efficiency Improvement

3.7 Regulatory Landscape

3.7.1 Radioisotope Safety Standards

3.7.1.1 Nuclear Medicine Regulations

3.7.1.1.1 Clinical Trial Compliance

3.7.1.1.1.1 GMP & Radiopharma Manufacturing Standards

3.7.1.1.1.2 Isotope Transport & Handling Compliance

3.8 Market Trends & Innovation Outlook

3.8.1 Precision Oncology Expansion

3.8.1.1 Targeted Radioligand Innovation

3.8.1.1.1 Alpha & Beta Isotope Development

3.8.1.1.1.1 AI-Based Molecular Imaging

3.8.1.1.1.2 Personalized Theranostic Growth

4. Global Radio Pharmaceuticals Market Dynamics

4.1 Market Drivers

4.1.1 Rising Cancer Prevalence

4.1.1.1 Oncology Diagnostic Demand

4.1.1.1.1 Targeted Therapy Expansion

4.1.1.1.1.1 Precision Medicine Growth

4.1.2 Growth in PET/SPECT Imaging Adoption

4.1.2.1 Imaging Infrastructure Expansion

4.1.2.1.1 Diagnostic Efficiency Improvement

4.1.2.1.1.1 Clinical Imaging Demand

4.1.3 Rising Use of Radioligand Therapies

4.1.3.1 Targeted Oncology Treatment

4.1.3.1.1 Therapeutic Accuracy Enhancement

4.1.3.1.1.1 Personalized Therapy Expansion

4.1.4 Isotope Production Innovation

4.1.4.1 Cyclotron & Reactor Development

4.1.4.1.1 Stable Supply Enhancement

4.1.4.1.1.1 Manufacturing Scalability Growth

4.1.5 Demand for Non-Invasive Diagnostics

4.1.5.1 Molecular Imaging Solutions

4.1.5.1.1 Disease Detection Accuracy

4.1.5.1.1.1 Long-Term Healthcare Integration

4.2 Market Restraints

4.2.1 High Production & Infrastructure Costs

4.2.2 Short Isotope Half-Life Challenges

4.2.3 Regulatory Complexity

4.2.4 Supply Chain Constraints in Isotope Logistics

4.3 Market Opportunities

4.3.1 Theranostics Expansion

4.3.2 Alpha-Emitter Therapeutic Innovation

4.3.3 Emerging Oncology Applications

4.3.4 AI-Based Nuclear Diagnostics

4.4 Market Challenges

4.4.1 Isotope Scarcity

4.4.2 Specialized Distribution Complexity

4.4.3 Clinical Validation Requirements

4.4.4 Nuclear Safety Compliance Burden

5. Global Radio Pharmaceuticals Market Size Analysis (USD Billion), 2026???2033

5.1 Revenue Forecast Analysis

5.2 CAGR Analysis

5.3 Demand-Supply Analysis

5.4 Segment Contribution Analysis

5.5 Pricing Trend Analysis

6. Global Radio Pharmaceuticals Market Segmentation Analysis

6.1 By Product Type

6.1.1 Diagnostic Radiopharmaceuticals

6.1.2 Therapeutic Radiopharmaceuticals

6.2 By Radioisotope Type

6.2.1 Technetium-99m

6.2.2 Fluorine-18

6.2.3 Gallium-68

6.2.4 Lutetium-177

6.2.5 Iodine-131

6.2.6 Alpha Emitters (Actinium-225, Radium-223)

6.3 By Application

6.3.1 Oncology

6.3.2 Cardiology

6.3.3 Neurology

6.3.4 Endocrinology

6.3.5 Bone Metastasis & Pain Management

6.4 By End User

6.4.1 Hospitals & Nuclear Medicine Centers

6.4.2 Diagnostic Imaging Centers

6.4.3 Research Institutes

6.4.4 Specialty Cancer Centers

7. Regional Market Analysis

7.1 North America

7.1.1 U.S.

7.1.2 Canada

7.1.3 Mexico

7.2 Europe

7.2.1 Germany

7.2.2 U.K.

7.2.3 France

7.2.4 Italy

7.2.5 Spain

7.2.6 Rest of Europe

7.3 Asia-Pacific

7.3.1 China

7.3.2 Japan

7.3.3 India

7.3.4 South Korea

7.3.5 Australia

7.3.6 Rest of Asia-Pacific

7.4 Latin America

7.4.1 Brazil

7.4.2 Argentina

7.4.3 Rest of Latin America

7.5 Middle East & Africa

7.5.1 GCC Countries

7.5.2 South Africa

7.5.3 Rest of Middle East & Africa

8. Competitive Landscape

8.1 Market Share Analysis

8.2 Competitive Intensity Overview

8.3 Strategic Developments

8.4 Product Innovation & Isotope Expansion

8.5 Partnerships, Mergers & Acquisitions

8.6 Nuclear Medicine Positioning Analysis

9. Company Profiles

9.1 Novartis AG

9.2 GE HealthCare

9.3 Cardinal Health

9.4 Curium Pharma

9.5 Bayer AG

9.6 Lantheus Holdings

9.7 Bracco Imaging

9.8 Jubilant Radiopharma

9.9 Siemens Healthineers

9.10 Eli Lilly (Point Biopharma)

10. Strategic Intelligence & Pheonix AI Insights

10.1 Pheonix Market Growth Forecast Engine

10.2 Radiopharma Innovation Trend Analyzer

10.3 Isotope Supply Risk Tracker

10.4 Precision Oncology Opportunity Mapping

10.5 Automated Porter???s Five Forces Analysis

11. Future Outlook & Strategic Recommendations

11.1 Theranostics Expansion Strategies

11.2 Isotope Supply Optimization

11.3 Targeted Therapy Innovation Growth

11.4 Precision Oncology Scaling Opportunities

11.5 Long-Term Market Outlook (2033+)

12. Appendix

12.1 Abbreviations

12.2 Research References

12.3 Data Sources

13. About Pheonix

14. Market Research

15. Disclaimer

Competitive Landscape

Global Radiopharmaceuticals Market Competitive Intensity & Market Structure Overview

The Global Radiopharmaceuticals Market is characterized by a moderately consolidated and technology-intensive competitive structure, where specialized pharmaceutical companies, isotope producers, nuclear medicine suppliers, and theranostics innovators compete through isotope access, regulatory expertise, clinical efficacy, and precision oncology capabilities. Competition is primarily driven by radioisotope production capacity, theranostics innovation, clinical validation, nuclear medicine infrastructure, logistics efficiency, oncology specialization, and targeted therapy differentiation.

The market is led by key players such as Novartis AG, GE HealthCare, Cardinal Health, Curium Pharma, Bayer AG, Lantheus Holdings, Bracco Imaging, Jubilant Radiopharma, Siemens Healthineers, and Eli Lilly (Point Biopharma), which compete through radioligand therapy portfolios, diagnostic tracers, isotope manufacturing, PET/SPECT ecosystem strength, and oncology-focused innovation.

Growing demand across oncology, cardiology, neurology, endocrinology, bone metastasis management, molecular imaging, targeted alpha therapies, and theranostics is intensifying competition. Companies are increasingly investing in Lutetium-177, Gallium-68, Actinium-225, PET tracers, AI-based nuclear imaging, cyclotron infrastructure, isotope engineering, and precision radiotherapy platforms.

Global Radiopharmaceuticals Market Competitive Landscape

Leading Company Profiles

- Novartis AG ??? Major global leader in radioligand therapy, oncology theranostics, and targeted nuclear medicine innovation.

- GE HealthCare ??? Strong player in diagnostic imaging agents, PET/SPECT ecosystems, and nuclear medicine solutions.

- Cardinal Health ??? Key supplier in radiopharmaceutical distribution, nuclear pharmacy networks, and isotope logistics.

- Curium Pharma ??? Specialized leader in nuclear medicine, diagnostic tracers, and therapeutic radiopharmaceuticals.

- Bayer AG ??? Strong presence in oncology therapeutics and targeted radiopharmaceutical development.

- Lantheus Holdings ??? Significant player in diagnostic radiopharmaceuticals and imaging-focused innovation.

- Bracco Imaging ??? Major imaging diagnostics company with nuclear medicine and contrast agent expertise.

- Jubilant Radiopharma ??? Important provider of radiopharmaceutical manufacturing and isotope supply services.

- Siemens Healthineers ??? Strong ecosystem player in molecular imaging, PET/SPECT platforms, and precision diagnostics.

- Eli Lilly (Point Biopharma) ??? Expanding in precision oncology radioligand therapies and advanced targeted isotopes.

Key Competitive Intensity Signals

- Competition in therapeutic radiopharmaceuticals and radioligand oncology therapies is rapidly intensifying.

- Isotope supply security (Lutetium-177, Gallium-68, Actinium-225) remains a major competitive barrier.

- Regulatory complexity and nuclear safety compliance create high entry barriers.

- Theranostics and precision oncology integration are becoming core technology differentiators.

- Vertical integration between isotope production, nuclear pharmacies, and therapy development strengthens margins.

- PET/SPECT imaging expansion is reinforcing recurring diagnostic demand.

- Strategic hospital and oncology-center partnerships improve long-term prescription and treatment adoption.

Strategic Implications

- Companies with strong isotope production and logistics infrastructure can maintain supply stability advantages.

- Theranostics and targeted alpha/beta therapies may remain the strongest long-term growth differentiators.

- Regulatory and clinical validation strength can significantly improve commercialization success.

- Oncology-centered precision radiotherapy platforms may create premium-margin opportunities.

- Partnerships with hospitals, cancer centers, and nuclear medicine facilities can strengthen long-term market penetration.

Forward Outlook

The Global Radiopharmaceuticals Market is expected to remain moderately consolidated with very high competitive intensity, supported by precision oncology growth, isotope innovation, and theranostics expansion.

Future competition will increasingly focus on:

- Therapeutic radiopharmaceuticals and radioligand therapies

- Alpha-emitter and beta-emitter innovation

- Isotope production and supply-chain security

- PET/SPECT diagnostic tracer expansion

- AI-based molecular imaging and precision diagnostics

- Theranostics integration

- Oncology-focused targeted nuclear therapies

The convergence of precision medicine, isotope engineering, theranostics, molecular imaging, oncology therapeutics, and nuclear medicine infrastructure will continue reshaping the long-term competitive landscape.

Value Chain

Global Radiopharmaceuticals Market Value Chain & Supply Chain Evolution Overview

The Global Radiopharmaceuticals Market operates through a highly specialized nuclear medicine and precision therapeutics ecosystem supported by isotope production, radiochemical synthesis, sterile pharma manufacturing, regulated transport, clinical distribution, and hospital-based therapeutic deployment. The market is increasingly shaped by theranostics, targeted radioligand therapies, PET/SPECT imaging growth, and isotope innovation.

The value chain depends heavily on radioisotope sourcing, cyclotron/reactor infrastructure, GMP sterile production, time-sensitive logistics, radiation safety systems, and precision oncology treatment networks.

Supply chain complexity is very high due to short isotope half-lives, radiation safety compliance, cold/controlled transport, specialized nuclear infrastructure, sterile handling, clinical validation, and hospital-linked delivery coordination.

Global Radiopharmaceuticals Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

1. Radioisotope & Nuclear Input Sourcing

Cyclotron-produced isotopes, reactor-based isotopes, enriched target materials, radionuclides, shielding materials, sterile APIs, and specialty reagents.

2. Radiochemical Synthesis & Product Development

PET tracers, SPECT tracers, alpha emitters, beta emitters, theranostic compounds, radioligands, and targeted isotope engineering.

3. Sterile Manufacturing & Packaging

GMP sterile formulation, vial filling, radiolabeling, shielding-based packaging, contamination control, and pharmaceutical-grade manufacturing.

4. Regulatory Validation & Nuclear Compliance

Radiation safety standards, nuclear medicine compliance, transport approvals, dosimetry validation, pharmacovigilance, and clinical trial controls.

5. Distribution & Clinical Supply Networks

Specialized radiopharma distributors, hospital supply systems, nuclear transport logistics, imaging center procurement, cancer center delivery, and time-sensitive therapeutic distribution.

6. End-Use Clinical & Diagnostic Ecosystem

Hospitals, nuclear medicine centers, oncology centers, imaging labs, diagnostic centers, and research institutes.

Key Value Chain Evolution Signals

1. Growth of Theranostics

Integrated diagnostic + therapeutic radioligands are expanding rapidly.

2. Isotope Scarcity & Supply Stability

Reliable isotope production is a major strategic advantage.

3. Short Half-Life Logistics

Time-critical delivery strongly shapes supply chains.

4. Precision Oncology Expansion

Cancer-focused radiotherapies are increasing demand.

5. Nuclear Infrastructure Investment

Cyclotrons and isotope plants are scaling globally.

6. AI-Integrated Imaging

Digital nuclear diagnostics improve treatment precision.

Strategic Implications

1. Isotope Control

Stable upstream isotope access improves resilience.

2. Vertical Nuclear Integration

Integrated production + distribution improves margins.

3. Time-Sensitive Logistics

Fast hospital-linked delivery is critical.

4. Clinical Compliance Leadership

Radiation-safe validated workflows improve adoption.

5. Oncology Ecosystem Partnerships

Hospitals and cancer centers strengthen demand penetration.

Forward Outlook

The market is expected to evolve toward a more precision-oncology and theranostics-driven ecosystem through:

- Alpha-emitter therapy expansion

- PET/SPECT innovation

- Cyclotron capacity growth

- Targeted radioligand therapies

- AI-based nuclear diagnostics

- Hospital-linked isotope delivery

- Advanced theranostic compounds

Investment Activity

Global Radio Pharmaceuticals Market Investment & Funding Dynamics Overview

The Global Radio Pharmaceuticals Market is witnessing strong investment momentum driven by precision oncology expansion, theranostics adoption, isotope innovation, and increasing demand for targeted molecular diagnostics and radioligand therapies. Pharmaceutical companies, isotope producers, nuclear medicine providers, oncology research firms, and radiotherapy developers are actively investing in isotope production facilities, cyclotron infrastructure, targeted alpha and beta therapies, PET/SPECT tracers, and advanced theranostic platforms.

Investment activity is accelerating due to rising cancer prevalence, expanding nuclear medicine applications, personalized oncology demand, and adoption of targeted radiopharmaceutical therapies. The growing shift toward precision molecular imaging, AI-assisted nuclear diagnostics, radioligand treatment development, and next-generation isotope engineering is significantly influencing capital allocation across the market.

Additionally, expanding investments in radiopharma manufacturing, oncology-focused clinical trials, nuclear medicine centers, and isotope supply-chain modernization are strengthening long-term growth opportunities globally.

Global Radio Pharmaceuticals Market Investment & Funding Dynamics Current Scenario

Currently, the Global Radio Pharmaceuticals Market demonstrates rising investment activity with high capital intensity due to isotope production complexity, cyclotron facilities, radiation-safe manufacturing, specialized logistics, and regulatory-compliant clinical infrastructure. Major players are heavily investing in targeted radioligand therapies, PET tracers, alpha-emitter compounds, theranostic agents, and precision oncology treatment systems.

The market is attracting strong funding into isotope engineering, targeted cancer therapeutics, molecular imaging platforms, AI-driven nuclear diagnostics, and specialty oncology applications. Rising healthcare investments and expanding cancer-focused nuclear medicine programs are further supporting investment flow.

The industry is witnessing active merger, partnership, and acquisition activity as pharmaceutical firms, isotope suppliers, theranostics developers, and nuclear medicine providers pursue vertical integration, pipeline expansion, and precision-oncology ecosystem growth.

Key Investment & Funding Dynamics Signals in Global Radio Pharmaceuticals Market

- Rising demand for precision oncology, PET/SPECT imaging, and targeted radioligand therapies is accelerating long-term investments.

- Expansion of cyclotron infrastructure, isotope production facilities, and nuclear medicine centers is increasing capital deployment.

- Growing focus on theranostics, alpha/beta therapies, and personalized cancer diagnostics is strengthening innovation-led funding.

- Strategic investments in AI-integrated imaging, isotope engineering, and advanced radioligand therapies are reshaping treatment priorities.

- Partnerships between pharmaceutical companies, isotope producers, hospitals, and oncology centers are improving supply-chain and therapeutic ecosystem stability.

- Increasing regulatory focus on radioisotope safety, GMP compliance, nuclear medicine handling, and clinical validation is supporting investor confidence.

- Rising demand for scalable, high-precision, and clinically validated radiopharmaceutical solutions is accelerating R&D and infrastructure spending.

Strategic Implications of Investment & Funding Dynamics in Global Radio Pharmaceuticals Market

- Continuous investment in theranostics, targeted isotopes, and precision oncology platforms is essential for long-term competitiveness.

- High capital intensity requires strong allocation toward isotope manufacturing, nuclear safety infrastructure, logistics, and clinical development.

- Companies capable of delivering safe, scalable, and advanced radiopharmaceutical solutions will strengthen market positioning significantly.

- Strategic M&A and vertical integration are accelerating isotope security, product expansion, and therapeutic specialization.

- Investments in alpha-emitter therapies, molecular imaging, and oncology radioligand innovation will remain major priorities.

- Compliance with radiation safety, clinical-trial, transport, and GMP standards is critical for long-term adoption.

- Companies investing in isotope supply resilience, AI-enabled diagnostics, and targeted radiotherapy innovation are expected to capture substantial future opportunities.

Global Radio Pharmaceuticals Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Radio Pharmaceuticals Market is expected to maintain strong investment growth driven by theranostics expansion, targeted oncology, isotope innovation, and personalized molecular medicine.

Future capital deployment will increasingly focus on alpha-emitter therapies, radioligand development, advanced PET tracers, AI-driven nuclear diagnostics, isotope engineering, and precision cancer infrastructure. Integrated oncology-radiopharma ecosystems and scalable isotope supply chains are expected to become major long-term innovation priorities.

In conclusion, the Global Radio Pharmaceuticals Market represents a high-growth, research-intensive investment landscape where theranostics, isotope innovation, oncology precision, and nuclear medicine scalability will define future capital strategies.

Technology & Innovation

Global Radio Pharmaceuticals Market Technology & Innovation Landscape Overview

The Global Radio Pharmaceuticals Market is undergoing rapid technological transformation driven by advancements in theranostics, targeted radioligand therapies, isotope engineering, AI-assisted molecular imaging, precision oncology platforms, cyclotron innovation, and next-generation nuclear medicine systems. The market demonstrates a high innovation intensity level, supported by rising cancer prevalence, increasing adoption of personalized medicine, expanding PET/SPECT imaging demand, and growth in targeted therapeutic applications.

At the center of this transformation is the shift from conventional diagnostic imaging agents toward precision-targeted radiopharmaceutical ecosystems, where radioactive compounds are increasingly used for both diagnosis and therapy (theranostics). Companies are investing heavily in radiolabeled biomarkers, targeted alpha therapies, beta-emitting compounds, and receptor-specific radioligands to improve treatment precision and patient outcomes.

A major innovation area is theranostic and radioligand therapy development, where integrated diagnostic-treatment agents such as lutetium-based and gallium-based compounds are improving personalized oncology treatment planning and disease monitoring.

The market is also witnessing strong advancements in isotope engineering and production technologies, including cyclotron-based isotope generation, reactor-based radioisotope optimization, short half-life isotope handling, and high-purity radionuclide processing.

AI integration remains critical, with increasing adoption of AI-powered PET/SPECT imaging analytics, automated lesion detection, radiotracer optimization, and predictive oncology imaging platforms, helping improve diagnostic speed and precision.

Manufacturers are increasingly innovating in micro-dosing technologies, targeted drug-conjugated radiopharmaceuticals, precision dosimetry systems, and AI-enabled treatment planning software, improving therapeutic accuracy and regulatory compliance.

Additionally, advances in alpha-emitter therapies, beta-emitter compounds, personalized radiotherapy platforms, and isotope logistics optimization are reshaping market competitiveness.

The convergence of nuclear medicine, molecular imaging, isotope science, AI diagnostics, precision oncology, and targeted radiotherapy is redefining the future technology landscape of the global radio pharmaceuticals market.

Global Radio Pharmaceuticals Market Technology & Innovation Landscape Current Scenario

Currently, the Global Radio Pharmaceuticals Market demonstrates high patent activity and strong commercialization across theranostics, isotope production, radioligand therapies, and AI-assisted imaging systems.

1. Theranostic Radiopharmaceutical Innovation

Combined diagnostic and therapeutic isotopes are transforming precision oncology.

2. Targeted Radioligand Therapies

Receptor-specific radiotherapies are improving treatment selectivity and efficacy.

3. Advanced Isotope Production Systems

Cyclotron and reactor-based isotope engineering are improving supply reliability.

4. AI-Powered Molecular Imaging

AI-based PET/SPECT analysis is enhancing diagnostic precision and speed.

5. Alpha & Beta Emitter Technologies

Targeted therapeutic isotopes are becoming major innovation drivers.

6. Precision Dosimetry & Treatment Planning

Advanced software is improving radiation targeting and safety optimization.

Key Technology & Innovation Landscape Signals in Global Radio Pharmaceuticals Market

Several innovation signals are shaping the market:

1. Rising Demand for Precision Oncology

Radiopharmaceuticals are becoming central to personalized cancer care.

2. Expansion of Theranostics

Integrated diagnosis-treatment systems are accelerating clinical adoption.

3. Increasing Targeted Alpha Therapy (TAT) Development

High-precision isotope therapies are strengthening oncology pipelines.

4. Growth of AI-Based Nuclear Imaging

AI tools are improving radiology interpretation and workflow efficiency.

5. Isotope Supply Chain Innovation

Production scalability and transport optimization are becoming critical.

6. Personalized Radiotherapy Planning

Patient-specific dosing systems are improving therapeutic outcomes.

7. Rare-Isotope & High-Purity Radionuclide Research

Novel isotopes are expanding future treatment capabilities.

Strategic Implications of Technology & Innovation Landscape in Global Radio Pharmaceuticals Market

The evolving innovation landscape is significantly reshaping competition across the market. Companies are increasingly competing on isotope precision, radioligand specificity, imaging intelligence, dosimetry accuracy, supply-chain stability, regulatory compliance, and oncology specialization.

Manufacturers investing in theranostics, targeted alpha therapies, cyclotron infrastructure, AI-driven imaging, high-purity isotopes, and personalized radiotherapy platforms are expected to strengthen long-term market positioning.

Strategic collaborations between pharmaceutical companies, isotope producers, hospitals, nuclear medicine centers, AI-imaging firms, oncology developers, and research institutes are accelerating commercialization and transforming precision cancer-care ecosystems globally.

The growing convergence of nuclear medicine, isotope engineering, AI diagnostics, theranostics, precision dosimetry, and targeted radiotherapy is creating strong long-term differentiation opportunities.

Additionally, regulatory emphasis on radioisotope handling safety, nuclear transport compliance, GMP production, clinical validation, and radiation-dosage control is encouraging stronger innovation and trusted healthcare adoption.

Global Radio Pharmaceuticals Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026???2033, the Global Radio Pharmaceuticals Market is expected to evolve toward highly targeted, AI-integrated, and precision-driven nuclear therapeutic ecosystems.

Future technological developments are likely to include:

1. Advanced Theranostic Platforms

Integrated diagnosis-treatment isotopes will improve personalized oncology care.

2. Next-Generation Alpha Emitter Therapies

High-potency targeted isotopes may significantly improve cancer treatment precision.

3. AI-Driven Molecular Imaging

Predictive imaging and automated lesion detection will improve diagnostics.

4. High-Efficiency Isotope Production

Cyclotron and decentralized production systems may improve global access.

5. Personalized Dosimetry Systems

Patient-specific radiation planning will improve therapeutic safety.

6. Targeted Drug-Radioligand Conjugates

Precision delivery compounds may strengthen treatment efficacy.

7. Scalable Nuclear Medicine Infrastructure

Expanded hospital and oncology radiopharma ecosystems will improve adoption.

In conclusion, companies capable of combining theranostics, isotope innovation, targeted radioligands, AI-based imaging, precision dosimetry, scalable isotope production, and advanced nuclear medicine platforms will be best positioned to lead the future evolution of the Global Radio Pharmaceuticals Market.

Market Risk

Global Radio Pharmaceuticals Market Risk & Disruption Analysis

The Global Radio Pharmaceuticals Market operates within a high-regulation, high-complexity, and innovation-intensive disruption environment, driven by isotope supply constraints, nuclear safety oversight, precision oncology demand, specialized logistics dependency, clinical validation pressure, and rapid theranostics innovation. While the market demonstrates strong long-term growth due to rising cancer burden, expanding PET/SPECT imaging, targeted radioligand therapies, and precision medicine adoption, it remains exposed to supply-chain fragility, regulatory intensity, infrastructure dependency, and therapy substitution pressure.

A defining structural characteristic of the market is its reliance on time-sensitive isotope-based healthcare ecosystems, where product viability, clinical delivery, and profitability are closely tied to isotope half-life constraints, specialized transport, nuclear handling infrastructure, and GMP-grade production. Diagnostic radiopharmaceuticals remain the largest segment by volume and utilization, while high-growth value is increasingly shifting toward therapeutic radiopharmaceuticals, alpha-emitter therapies, and theranostic platforms.

The market is also evolving from conventional nuclear imaging toward precision theranostics, AI-integrated molecular diagnostics, targeted radioligand therapy, and personalized oncology workflows, increasing technological disruption and capital intensity.

Global Radio Pharmaceuticals Market Current Risk Environment

Currently, the market operates under high clinical demand, specialized operational dependency, and strict nuclear-medical oversight.

One of the most significant disruption factors is radioisotope supply-chain fragility. Production depends on nuclear reactors, cyclotrons, enriched precursor availability, and highly specialized manufacturing facilities. Short isotope half-lives (e.g., Tc-99m, F-18) create critical timing sensitivity and delivery risk.

Another major risk area is regulatory and nuclear safety complexity. Radiopharmaceuticals require strict radiation safety compliance, nuclear transport approvals, sterile GMP production, clinical handling protocols, and environmental monitoring.

The market also faces substitution and treatment competition pressure. In diagnostics, MRI, CT, and molecular diagnostics may reduce demand in select applications. In therapeutics, immunotherapy, biologics, precision oncology drugs, and cell-based therapies may compete with radioligand-based treatments.

Additionally, high capital and infrastructure dependency remain major structural risks. Cyclotrons, isotope reactors, nuclear medicine centers, hot cells, and radiation-shielded logistics create high barriers.

In parallel, geopolitical dependence on isotope-producing nations and cross-border radioactive transport rules may affect supply continuity.

Key Market Risk & Disruption Signals in Global Radio Pharmaceuticals Market

1. Isotope Supply Chain & Half-Life Sensitivity

Short-lived isotopes and specialized production create high operational fragility.

2. Nuclear Safety & Regulatory Oversight

Radiation handling, GMP production, transport, and environmental safety drive high compliance burden.

3. Infrastructure & Capital Intensity

Cyclotrons, reactors, and nuclear medicine centers require significant investment.

4. Substitution from Alternative Diagnostics & Therapies

MRI, CT, biologics, immunotherapy, and cell therapies may affect selective demand.

5. Geopolitical Supply Exposure

Dependence on global isotope production hubs increases strategic vulnerability.

6. Clinical Trial & Validation Pressure

Theranostics and targeted radioligands require strong efficacy and safety evidence.

7. Specialized Logistics & Cold-Chain-Like Timing Complexity

Transport windows are tightly linked to isotope viability.

8. Skilled Workforce & Nuclear Expertise Dependency

Growth depends on trained radiochemists, nuclear physicians, and specialty operators.

Strategic Implications of Market Risk & Disruption in Global Radio Pharmaceuticals Market

The evolving disruption environment creates strong precision-medicine opportunity alongside elevated infrastructure and compliance risk.

One of the most important strategic implications is the increasing need for vertically integrated isotope and theranostic ecosystems. Companies increasingly must combine isotope production, radiochemistry, logistics precision, clinical validation, and oncology specialization.

Manufacturers must invest in cyclotron expansion, isotope diversification, alpha-emitter innovation, AI-driven imaging interpretation, targeted radioligand development, and nuclear GMP scalability to remain competitive.

Vertical integration across isotope production, radiopharma synthesis, hospital partnerships, oncology platforms, and specialty logistics is becoming increasingly valuable.

The convergence of precision oncology, nuclear medicine, AI diagnostics, and theranostic medicine is also reshaping value chains. Companies with stronger isotope access, nuclear infrastructure, and specialty oncology networks may gain long-term strategic advantage.

Additionally, aging populations, cancer prevalence, and personalized oncology expansion may create durable demand.

Companies focusing on theranostics, isotope resilience, alpha/beta therapeutic innovation, regulated nuclear manufacturing, and oncology-centered radiopharma ecosystems are expected to strengthen long-term market leadership.

Global Radio Pharmaceuticals Market Risk & Disruption Forward Outlook

Looking ahead to 2026???2033, the Global Radio Pharmaceuticals Market is expected to become increasingly specialized, vertically integrated, and oncology-focused.

1. Expansion of Therapeutic Radiopharmaceuticals

Targeted alpha and beta therapies will capture growing value.

2. Greater Theranostics Integration

Diagnostic-to-therapy linked treatment models will expand.

3. Higher Isotope Production Investments

Cyclotrons and reactor alternatives may reduce supply fragility.

4. Stronger Nuclear Safety & Compliance Oversight

Radiation safety and GMP requirements will remain strict.

5. Growth in Precision Oncology & Personalized Treatment

Radioligand therapies will gain strategic clinical importance.

6. Broader AI-Driven Imaging & Molecular Diagnostics

Automation may improve nuclear diagnostic efficiency.

7. Competitive Consolidation in Specialty Radiopharma

M&A and strategic oncology partnerships may intensify.

8. Regionalization of Isotope Supply Chains

Local isotope production hubs may improve resilience.

In conclusion, the Global Radio Pharmaceuticals Market represents a high-value, clinically critical, and highly specialized healthcare ecosystem, where isotope resilience, nuclear compliance, clinical precision, theranostic innovation, and infrastructure strength will define long-term competitive success.

Regulatory Landscape

Global Radio Pharmaceuticals Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a highly critical role in shaping the Global Radio Pharmaceuticals Market due to strict oversight around nuclear safety, radioactive material handling, clinical validation, pharmaceutical manufacturing, and therapeutic-use compliance. Regulatory frameworks governing radioisotope production, radiation exposure, transport controls, GMP manufacturing, nuclear medicine licensing, and therapeutic approvals significantly influence commercialization, clinical adoption, and long-term market expansion.

Radiopharmaceuticals are widely used across oncology, cardiology, neurology, endocrinology, molecular imaging, and targeted radioligand therapy. Because these products involve radioactive isotopes and direct patient therapeutic exposure, regulatory scrutiny is exceptionally high across production, logistics, and clinical use.

The market is also influenced by evolving radiation protection standards, isotope traceability, nuclear transport regulations, clinical trial requirements, waste-disposal controls, and theranostic validation frameworks. Governments and healthcare regulators are increasingly balancing precision-medicine innovation with radiation safety, public health protection, and supply-chain security.

In addition, cancer-care modernization, nuclear medicine expansion, and precision oncology investments are strengthening structured regulatory enforcement globally.

Global Radio Pharmaceuticals Market Regulatory & Policy Environment Current Scenario

Currently, the Global Radio Pharmaceuticals Market operates under a highly controlled, safety-intensive, and multi-layered regulatory framework involving nuclear medicine licensing, radiation safety laws, isotope transport regulations, pharmaceutical approvals, GMP compliance, and clinical-use monitoring.

One of the most important regulatory trends is radioactive safety and nuclear medicine oversight. Manufacturers and treatment centers must maintain strict isotope handling, storage, shielding, and exposure-control compliance.

Another major regulatory factor involves therapeutic and diagnostic clinical validation. Radiopharmaceuticals require strong efficacy data, dose safety validation, adverse-event monitoring, and regulated therapeutic approval.

Cross-border isotope transport and nuclear logistics also remain highly important, especially due to short half-lives, hazardous material controls, and jurisdiction-specific radioactive transport laws.

Sector-specific compliance is especially strong in hospitals, nuclear medicine centers, oncology treatment facilities, cyclotron operations, and specialty cancer centers.

Additionally, radioactive waste disposal, isotope traceability, and supply-chain security are creating stronger oversight across the ecosystem.

Key Regulatory & Policy Environment Signals in Global Radio Pharmaceuticals Market

1. Rising Nuclear Safety & Radiation Control Standards

Controlled isotope handling, storage, and exposure monitoring remain critical.

2. Expansion of Clinical Validation & Therapeutic Approval Oversight

Safety, dose precision, and efficacy validation are increasingly important.

3. Growing Cross-Border Radioisotope Transport Complexity

Hazardous transport and jurisdiction-specific nuclear compliance require strict governance.

4. Nuclear Medicine Licensing & Facility Oversight

Hospitals and treatment centers require regulated infrastructure compliance.

5. Waste Management & Isotope Traceability Requirements

Secure disposal and radioactive tracking systems are strengthening.

Strategic Implications of Regulatory & Policy Environment in Global Radio Pharmaceuticals Market

The evolving regulatory environment creates major strategic implications for pharmaceutical manufacturers, isotope producers, nuclear medicine centers, oncology providers, and logistics partners. One major implication is the growing need for highly controlled, traceable, and clinically validated radiopharmaceutical ecosystems.

Companies must invest in radiation safety systems, isotope logistics, GMP manufacturing, nuclear licensing, therapeutic validation, and secure transport frameworks to remain globally competitive.

The increasing convergence of theranostics, targeted oncology, isotope innovation, and precision medicine is also pushing firms toward compliance-led innovation.

Organizations capable of balancing isotope scalability, clinical precision, safety readiness, and regulated accessibility will likely strengthen long-term market positioning.

Additionally, firms with strong cyclotron integration, nuclear supply stability, and oncology-centered compliance capabilities will gain stronger competitive advantages.

Global Radio Pharmaceuticals Market Regulatory & Policy Environment Forward Outlook

Looking ahead to 2026???2033, the regulatory environment for radiopharmaceuticals is expected to become increasingly safety-driven, therapeutically governed, and nuclear-compliance-intensive as precision oncology and theranostics continue expanding.

Future regulations are likely to place stronger emphasis on isotope traceability, radiation minimization, targeted-therapy validation, nuclear transport security, radioactive waste handling, and AI-assisted nuclear diagnostics governance.

Governments may continue strengthening nuclear medicine laws, therapeutic-use approvals, GMP requirements, clinical safety mandates, and radioactive logistics oversight.

The expansion of alpha-emitter therapies, theranostics, personalized oncology, and next-generation isotope engineering may further increase regulatory complexity.

Overall, the regulatory and policy environment will remain a major factor influencing trust, commercialization, clinical scalability, safety validation, and competitive positioning within the Global Radio Pharmaceuticals Market.