U.S. Nasal Spray Market Size and Share Analysis 2026-2033

U.S. Nasal Spray Market Size & Forecast

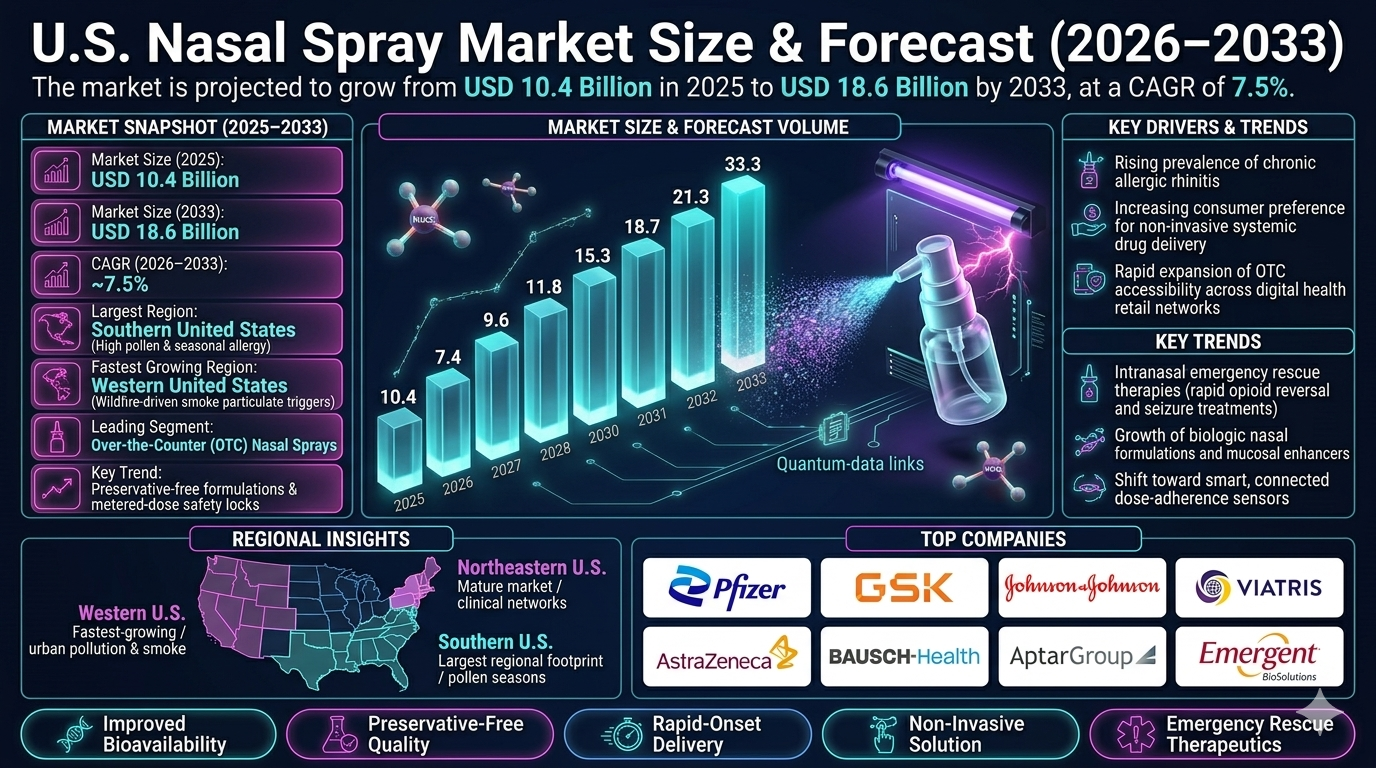

The U.S. nasal spray market is projected to witness robust growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 10.4 billion in 2025 and is expected to reach nearly USD 18.6 billion by 2033, expanding at a CAGR of around 7.5%. The market growth is driven by the rising prevalence of allergic rhinitis, sinusitis, respiratory disorders, increasing consumer preference for non-invasive drug delivery systems, and growing innovation in nasal drug formulations. Nasal sprays are drug delivery systems designed to administer medications directly through the nasal cavity for local or systemic therapeutic effects. These products are widely used for allergy relief, nasal congestion, sinus infections, migraine treatment, hormone delivery, pain management, and vaccine administration. The market is witnessing significant transformation due to advancements in preservative-free formulations, metered-dose delivery systems, biologic nasal therapies, and intranasal vaccine technologies. Additionally, increasing seasonal allergies, rising air pollution exposure, expanding over-the-counter product availability, and growing demand for rapid-onset therapeutics are accelerating market growth across the United States.

U.S. Nasal Spray Market Overview

The U.S. nasal spray market forms a vital segment of the pharmaceutical drug delivery and respiratory therapeutics industry. It plays an essential role in managing allergic conditions, chronic sinus disorders, respiratory infections, neurological therapies, and preventive healthcare applications. The market includes decongestant nasal sprays, saline nasal sprays, corticosteroid nasal sprays, antihistamine sprays, migraine nasal sprays, opioid reversal sprays, and specialty prescription intranasal formulations. Healthcare providers and pharmaceutical manufacturers are increasingly adopting advanced spray technologies to improve bioavailability, patient compliance, and therapeutic efficiency. Technological innovation in intranasal delivery systems, mucosal absorption enhancers, and smart dosing mechanisms is reshaping product development across the industry. Major market participants include Pfizer Inc., GlaxoSmithKline plc, Johnson & Johnson, Viatris Inc., AstraZeneca plc, Bausch Health Companies Inc., AptarGroup Inc., Emergent BioSolutions Inc., Cipla USA, and Hikma Pharmaceuticals PLC.Key Drivers of U.S. Nasal Spray Market Growth

Rising Prevalence of Allergic Rhinitis and Sinus Disorders

The increasing incidence of seasonal allergies, chronic sinusitis, and nasal congestion is significantly driving demand for nasal spray products. Changing environmental conditions and rising allergen exposure are contributing to increased product adoption.Growing Preference for Non-Invasive Drug Delivery

Nasal sprays offer rapid drug absorption and convenient administration without the need for injections. This has made intranasal drug delivery increasingly attractive for both prescription and over-the-counter therapeutic applications.Expansion of Over-the-Counter Product Availability

The growing accessibility of OTC nasal sprays through pharmacies, supermarkets, and e-commerce platforms is supporting market expansion. Consumers increasingly prefer self-administered solutions for common respiratory and allergy-related conditions.Advancements in Specialty Intranasal Therapies

Innovations in migraine treatment, hormone replacement, central nervous system drug delivery, and emergency rescue therapies are expanding market opportunities. Intranasal biologics and peptide-based therapies are emerging as high-growth segments.Increasing Focus on Emergency and Rapid-Onset Therapeutics

Products such as naloxone nasal sprays and emergency seizure therapies are witnessing strong demand due to their rapid therapeutic response. These solutions play an increasingly important role in emergency medical care.U.S. Nasal Spray Market Segmentation

By Product Type

The market is segmented into decongestant sprays, saline sprays, steroid sprays, antihistamine sprays, migraine sprays, opioid reversal sprays, and specialty therapeutic sprays. Corticosteroid and decongestant sprays account for significant market share due to high usage frequency.By Prescription Type

The market includes prescription nasal sprays and over-the-counter nasal sprays. Over-the-counter products dominate due to high consumer accessibility and widespread use for allergy relief.By Application

Applications include allergy treatment, sinusitis management, pain management, migraine therapy, hormone delivery, emergency care, and vaccination delivery. Allergy treatment represents the largest application segment.By Distribution Channel

Distribution channels include retail pharmacies, hospital pharmacies, online pharmacies, supermarkets, and specialty clinics. Retail pharmacies remain the dominant distribution channel across the U.S. market.Regional Market Dynamics

Northeastern United States

This region represents a significant market due to high seasonal allergy prevalence, advanced healthcare infrastructure, and strong consumer healthcare awareness.Southern United States

The Southern region is witnessing strong growth due to rising respiratory health concerns, high pollen exposure, and growing retail healthcare accessibility.Midwestern United States

Steady demand is supported by expanding healthcare access, increasing allergy diagnosis rates, and pharmaceutical distribution networks.Western United States

The Western region is experiencing strong adoption due to urban pollution concerns, wildfire-related respiratory issues, and advanced pharmaceutical innovation hubs.Competitive Landscape

The U.S. nasal spray market is highly competitive and innovation-driven, with pharmaceutical companies competing through formulation innovation, delivery efficiency, product safety, and regulatory approvals. Key companies include Pfizer Inc., GlaxoSmithKline plc, Johnson & Johnson, Viatris Inc., AstraZeneca plc, Bausch Health Companies Inc., AptarGroup Inc., Emergent BioSolutions Inc., Cipla USA, and Hikma Pharmaceuticals PLC. Companies are increasingly investing in preservative-free formulations, advanced spray mechanisms, biologic intranasal therapies, and consumer-friendly packaging solutions. Strategic partnerships between pharmaceutical firms, device manufacturers, and healthcare distributors are shaping the market landscape.Strategic Outlook

The strategic outlook for the U.S. nasal spray market remains highly positive due to rising therapeutic applications and growing innovation in intranasal drug delivery. Future opportunities include intranasal vaccines, CNS-targeted therapies, digital adherence monitoring systems, and personalized nasal drug delivery solutions. Advancements in biologics delivery and smart dispensing technologies are expected to further expand the market. Manufacturers investing in differentiated formulations, regulatory approvals, and next-generation drug delivery platforms are likely to strengthen their competitive positioning.Final Market Perspective

The U.S. nasal spray market is evolving rapidly as healthcare providers and consumers increasingly adopt efficient, convenient, and non-invasive therapeutic solutions. Growing allergy prevalence, rising respiratory health concerns, and expanding intranasal therapeutic applications will continue driving market expansion throughout the forecast period. Companies that successfully combine product innovation, regulatory compliance, and patient-centric delivery technologies will remain strongly positioned in the evolving U.S. nasal spray market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 U.S. Nasal Spray Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Key Market Highlights

- 1.4 Growth Drivers Overview

- 1.5 Segment Performance Summary

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Market Outlook

- 2. Introduction & Market Overview

- 2.1 Definition of Nasal Spray Therapeutics

- 2.2 Market Scope & Coverage

- 2.3 Evolution of Intranasal Drug Delivery Systems

- 2.4 Value Chain Analysis

- 2.5 Regulatory Landscape in the U.S.

- 2.6 Technology Innovation Trends

- 2.7 Key Therapeutic Applications Overview

- 3. Research Methodology

- 3.1 Primary Research Approach

- 3.2 Secondary Research Sources

- 3.3 Market Estimation Framework

- 3.4 Forecasting Model (2026???2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Prevalence of Allergic Rhinitis & Sinusitis

- 4.1.2 Increasing Preference for Non-Invasive Drug Delivery

- 4.1.3 Expansion of OTC Product Availability

- 4.1.4 Advancements in Specialty Intranasal Therapies

- 4.1.5 Growing Demand for Rapid-Onset Emergency Treatments

- 4.2 Restraints

- 4.2.1 Side Effects & Mucosal Irritation Concerns

- 4.2.2 Regulatory Compliance Challenges

- 4.2.3 Product Misuse & Overdependence Risks

- 4.2.4 Pricing Pressure in OTC Segment

- 4.3 Opportunities

- 4.3.1 Intranasal Biologics & Peptide Therapies

- 4.3.2 Vaccine Delivery via Nasal Route

- 4.3.3 CNS-Targeted Drug Delivery Innovations

- 4.3.4 Smart & Metered-Dose Spray Technologies

- 4.4 Challenges

- 4.4.1 Formulation Stability Issues

- 4.4.2 Device-Drug Integration Complexity

- 4.4.3 Competition from Alternative Delivery Methods

- 4.4.4 Supply Chain Constraints in Pharmaceutical Inputs

- 4.1 Drivers

- 5. U.S. Nasal Spray Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Revenue Growth Trends

- 5.4 Demand-Supply Analysis

- 5.5 Product Penetration Trends

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Product Type

- 6.1.1 Decongestant Nasal Sprays

- 6.1.2 Saline Nasal Sprays

- 6.1.3 Corticosteroid Nasal Sprays

- 6.1.4 Antihistamine Nasal Sprays

- 6.1.5 Migraine Nasal Sprays

- 6.1.6 Opioid Reversal Nasal Sprays

- 6.1.7 Specialty Therapeutic Nasal Sprays

- 6.2 By Prescription Type

- 6.2.1 Prescription-Based Nasal Sprays

- 6.2.2 Over-the-Counter (OTC) Nasal Sprays

- 6.3 By Application

- 6.3.1 Allergy Treatment

- 6.3.2 Sinusitis Management

- 6.3.3 Migraine Therapy

- 6.3.4 Pain Management

- 6.3.5 Hormone Delivery

- 6.3.6 Emergency Care

- 6.3.7 Vaccination Delivery

- 6.4 By Distribution Channel

- 6.4.1 Retail Pharmacies

- 6.4.2 Hospital Pharmacies

- 6.4.3 Online Pharmacies

- 6.4.4 Supermarkets & Drug Stores

- 6.4.5 Specialty Clinics

- 6.1 By Product Type

- 7. Regional Market Analysis

- 7.1 Northeastern United States

- 7.2 Southern United States

- 7.3 Midwestern United States

- 7.4 Western United States

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Key Player Benchmarking

- 8.3 Product Portfolio Analysis

- 8.4 Strategic Developments

- 8.5 Innovation & Pipeline Analysis

- 9. Company Profiles

- 9.1 Pfizer Inc.

- 9.2 GlaxoSmithKline plc

- 9.3 Johnson & Johnson

- 9.4 Viatris Inc.

- 9.5 AstraZeneca plc

- 9.6 Bausch Health Companies Inc.

- 9.7 AptarGroup Inc.

- 9.8 Emergent BioSolutions Inc.

- 9.9 Cipla USA

- 9.10 Hikma Pharmaceuticals PLC

- 10. Strategic Insights & Market Outlook

- 10.1 Intranasal Drug Delivery Innovation Trends

- 10.2 Biologics & Specialty Therapy Expansion

- 10.3 Digital & Smart Nasal Spray Technologies

- 10.4 Future Therapeutic Applications

- 10.5 Long-Term Market Outlook (2033+)

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of OTC & Self-Care Products

- 11.2 Investment in Advanced Formulations

- 11.3 Growth of Emergency Therapeutic Sprays

- 11.4 Adoption of AI-Driven Drug Delivery Systems

- 11.5 Personalized Intranasal Therapy Development

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

U.S. Nasal Spray Market Competitive Intensity & Market Structure Overview

The U.S. nasal spray market is highly competitive and innovation-driven, with strong participation from global pharmaceutical companies, specialty drug manufacturers, generic drug players, and medical device-enabled drug delivery firms. Competition is primarily shaped by formulation innovation, therapeutic differentiation, regulatory approvals, brand strength, and the effectiveness of drug delivery technologies.

The market structure is moderately consolidated, with a mix of large multinational pharmaceutical companies dominating branded prescription products and a highly competitive over-the-counter (OTC) segment characterized by generic brands and retail-driven competition. Continuous product innovation and lifecycle extension strategies are key competitive tools across the market.

Rising prevalence of respiratory disorders, increasing allergy cases, and growing demand for non-invasive and fast-acting drug delivery systems are intensifying competition across both prescription and OTC nasal spray categories in the United States.

U.S. Nasal Spray Market Competitive Intensity & Market Structure Current Scenario

Leading Nasal Spray & Pharmaceutical Companies

Pfizer Inc.: A major pharmaceutical leader involved in respiratory and specialty therapeutics, with strong capabilities in prescription nasal drug development and commercialization.

GlaxoSmithKline plc: Key player in allergy and respiratory care, offering a strong portfolio of nasal spray products and inhalation therapies.

Johnson & Johnson: Significant participant in consumer healthcare and OTC respiratory products, including widely used nasal spray formulations.

AstraZeneca plc: Focused on respiratory therapeutics and advanced drug delivery systems, including nasal and inhalation-based therapies.

Viatris Inc.: Major generic pharmaceutical company supplying cost-effective nasal spray products across prescription and OTC segments.

Bausch Health Companies Inc.: Active in consumer health and specialty pharmaceuticals with nasal and allergy-related treatment offerings.

AptarGroup Inc.: Leading drug delivery systems provider specializing in nasal spray devices, metered-dose technologies, and advanced dispensing solutions.

Emergent BioSolutions Inc.: Key player in emergency nasal therapeutics, including opioid overdose reversal nasal spray technologies.

Cipla USA: Important generic pharmaceutical supplier with growing presence in respiratory and nasal drug delivery markets.

Hikma Pharmaceuticals PLC: Strong provider of injectable and respiratory generics, including nasal spray formulations for the U.S. market.

Key Competitive Intensity & Market Structure Drivers

The increasing prevalence of allergic rhinitis, sinusitis, and chronic respiratory conditions is significantly intensifying competition among pharmaceutical companies to expand nasal spray portfolios.

Over-the-counter product availability and retail pharmacy penetration are driving price-based competition, particularly in decongestant and saline spray segments.

Innovation in drug delivery technologies such as metered-dose systems, preservative-free formulations, and intranasal biologics is becoming a key competitive differentiator.

Growing demand for emergency therapeutic sprays, including opioid reversal and seizure management products, is creating high-value niche competition among specialty pharmaceutical firms.

Regulatory approvals, clinical efficacy, and safety profiles play a critical role in shaping market positioning, especially for prescription-based nasal therapeutics.

Strategic Implications of Competitive Intensity & Market Structure

Pharmaceutical companies are increasingly focusing on product differentiation through advanced formulations, improved absorption technologies, and extended product lifecycles.

Strategic collaborations between drug manufacturers and device technology providers are strengthening innovation in nasal spray delivery systems and patient-friendly dosing mechanisms.

Expansion of OTC distribution through retail pharmacies, e-commerce platforms, and supermarket channels is intensifying competition in consumer healthcare segments.

Investment in biologic nasal therapies, intranasal vaccines, and CNS-targeted drug delivery systems is opening new high-growth competitive frontiers.

Generic competition is increasing pressure on pricing strategies, particularly for mature decongestant and antihistamine nasal spray products.

U.S. Nasal Spray Market Competitive Intensity & Market Structure Forward Outlook

The U.S. nasal spray market is expected to remain highly competitive as innovation in intranasal drug delivery and expanding therapeutic applications continue to reshape the industry landscape.

Future competition will increasingly focus on biologic nasal therapies, intranasal vaccines, digital adherence solutions, and precision drug delivery systems targeting neurological and systemic conditions.

Advancements in smart dispensing technologies, preservative-free formulations, and combination therapies are expected to further differentiate leading market participants.

The OTC segment is expected to remain price-sensitive, while the prescription segment will be driven by innovation, clinical efficacy, and regulatory approvals.

Overall, companies that successfully combine drug innovation, advanced delivery technologies, regulatory strength, and strong consumer healthcare branding will remain strongly positioned in the evolving U.S. nasal spray market.

Value Chain

U.S. Nasal Spray Market Value Chain & Supply Chain Evolution Overview

The U.S. nasal spray market value chain is evolving rapidly as rising respiratory disease burden, increasing allergy prevalence, and growing demand for non-invasive drug delivery systems reshape pharmaceutical development and healthcare consumption patterns. Nasal sprays have become a widely adopted therapeutic modality across allergy treatment, sinusitis management, migraine therapy, emergency care, hormone delivery, and neurological applications due to their rapid onset of action, ease of administration, and improved patient compliance compared to traditional oral and injectable drug delivery systems.

The value chain encompasses active pharmaceutical ingredient (API) sourcing, formulation development, drug delivery device manufacturing, fill-finish pharmaceutical processing, packaging, regulatory approval pathways, distribution networks, and end-user healthcare delivery systems. The ecosystem integrates pharmaceutical manufacturers, contract development and manufacturing organizations (CDMOs), device engineering firms, packaging solution providers, healthcare distributors, pharmacies, hospitals, and digital healthcare platforms.

Leading companies such as Pfizer Inc., GlaxoSmithKline plc, Johnson & Johnson, Viatris Inc., AstraZeneca plc, Bausch Health Companies Inc., Emergent BioSolutions Inc., Cipla USA, Hikma Pharmaceuticals PLC, and AptarGroup Inc. are investing heavily in intranasal drug delivery innovation, advanced spray technologies, biologic formulation development, and next-generation therapeutic applications to expand clinical effectiveness and market reach.

Upstream supply chain activities include API manufacturing, pharmaceutical-grade excipient production, device component engineering (nasal pumps, valves, and metered-dose systems), and sterile formulation ingredient sourcing. Midstream operations focus on drug formulation, stability testing, clinical validation, regulatory compliance (FDA pathways), and manufacturing scale-up. Downstream processes involve packaging, cold chain or ambient distribution, pharmacy networks, hospital procurement systems, and direct-to-consumer retail channels.

Operational priorities across the nasal spray value chain increasingly emphasize formulation stability, dose precision, patient safety, regulatory compliance, device reliability, and scalable manufacturing efficiency. However, the market continues to face challenges related to stringent FDA regulations, complex clinical validation requirements, supply chain dependencies for pharmaceutical ingredients, device compatibility issues, and increasing pressure for preservative-free and environmentally sustainable formulations.

U.S. Nasal Spray Market Value Chain & Supply Chain Evolution Current Scenario

The current U.S. nasal spray market is being shaped by rising demand for OTC allergy medications, increasing incidence of respiratory disorders, growing adoption of self-administered treatments, and rapid innovation in intranasal drug delivery technologies. Seasonal allergies, pollution exposure, and chronic sinus conditions continue to drive consistent demand across both prescription and over-the-counter segments.

Retail pharmacies remain the dominant distribution channel, supported by widespread consumer access, strong physician recommendations, and increasing pharmacy-based healthcare services. Online pharmacies and e-commerce platforms are also gaining traction, driven by convenience, subscription-based medication models, and direct-to-consumer healthcare trends.

Pharmaceutical companies are increasingly investing in preservative-free formulations, metered-dose spray technologies, improved nasal absorption systems, and device-driven drug delivery innovations to enhance therapeutic performance and patient experience. Device manufacturers such as AptarGroup play a critical role in enabling precision dosing and improving usability across nasal spray products.

Emergency and specialty nasal spray applications are expanding rapidly, particularly opioid reversal sprays (naloxone), seizure rescue therapies, and emerging intranasal migraine treatments. These high-impact therapeutic areas are strengthening the clinical importance of nasal drug delivery systems in emergency medicine and neurology.

At the same time, manufacturers are focusing on regulatory compliance, supply chain reliability, and product differentiation through advanced formulations and combination therapies. The increasing complexity of intranasal biologics and peptide-based therapies is also influencing manufacturing and distribution strategies across the ecosystem.

Key Value Chain & Supply Chain Evolution Signals in U.S. Nasal Spray Market

One of the most significant transformation signals is the increasing shift toward biologic and specialty intranasal therapies. The nasal route is being explored for delivering peptides, hormones, vaccines, and central nervous system (CNS)-targeted drugs, expanding the therapeutic scope of nasal spray products beyond traditional allergy and congestion treatments.

Another key signal is the rapid growth of emergency-use intranasal medications, particularly naloxone nasal sprays for opioid overdose reversal. This segment has gained strong policy and public health support, significantly increasing market penetration across healthcare and community settings.

The expansion of OTC nasal spray availability is also reshaping market dynamics. Consumers are increasingly self-managing mild respiratory conditions, supported by strong pharmacy retail infrastructure and growing digital healthcare access.

Technological innovation in drug delivery systems is a major market driver. Advances in metered-dose technologies, dry powder nasal sprays, preservative-free formulations, and mucosal absorption enhancers are improving drug efficacy, safety, and patient compliance.

Digital health integration is emerging as an additional transformation signal. Smart adherence monitoring, connected drug delivery systems, and digital prescription tracking are beginning to influence long-term pharmaceutical delivery models in the U.S. healthcare ecosystem.

Regulatory tightening by the U.S. FDA around formulation safety, device accuracy, and bioequivalence standards is also shaping innovation pathways and increasing the importance of clinical validation and quality manufacturing systems.

Strategic Implications of Value Chain & Supply Chain Evolution in U.S. Nasal Spray Market

Leading pharmaceutical companies are increasingly focusing on next-generation intranasal delivery systems, biologic formulation capabilities, and differentiated therapeutic applications to strengthen competitive positioning in the U.S. nasal spray market. Competitive advantage is increasingly determined by formulation innovation, device precision, regulatory success, and distribution network strength.

Companies capable of developing intranasal biologics, CNS-targeted therapies, and emergency-use nasal medications are expected to capture high-growth opportunities as clinical applications expand beyond conventional respiratory treatments. Strategic investment in R&D and clinical trials is becoming essential for long-term differentiation.

Device-pharma collaboration is a key strategic trend. Partnerships between pharmaceutical manufacturers and drug delivery device companies such as AptarGroup are enabling improved dosing accuracy, patient usability, and product lifecycle innovation.

Supply chain resilience is also becoming increasingly important due to dependence on pharmaceutical-grade raw materials, regulatory bottlenecks, and global manufacturing dependencies. Companies are diversifying production locations and strengthening contract manufacturing partnerships to improve supply stability.

Additionally, companies focusing on OTC market expansion, consumer-friendly packaging, and digital pharmacy distribution channels are gaining stronger retail market penetration and brand visibility across the U.S. healthcare system.

U.S. Nasal Spray Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the U.S. nasal spray value chain is expected to become more technologically advanced, biologically driven, and digitally integrated. Intranasal drug delivery will expand beyond respiratory care into neurology, emergency medicine, hormone therapy, and vaccine administration, significantly broadening market scope.

Advanced formulation technologies such as nanocarrier-based intranasal delivery, sustained-release nasal systems, and targeted CNS drug delivery platforms are expected to redefine therapeutic effectiveness and expand clinical applications.

The integration of digital health technologies, including smart adherence monitoring, connected drug delivery devices, and AI-driven patient management systems, will further enhance treatment outcomes and patient engagement.

Regulatory frameworks will continue to evolve, with increasing emphasis on safety validation, device precision standards, and real-world evidence generation for intranasal therapies. This will drive higher compliance requirements but also improve overall product quality and trust.

OTC expansion is expected to continue, driven by consumer self-care trends, pharmacy retail growth, and increased healthcare awareness. At the same time, specialty prescription nasal sprays will grow rapidly due to expanding therapeutic indications.

Ultimately, the future U.S. nasal spray value chain will evolve into a highly integrated pharmaceutical-device-digital ecosystem focused on precision drug delivery, patient-centric care, emergency response applications, and advanced therapeutic innovation across multiple disease categories.

Market-Specific Value Chain

- API & Pharmaceutical Ingredient Supply: Active pharmaceutical ingredient manufacturing, excipient production, biochemical sourcing, and raw material quality control.

- Formulation & Drug Delivery Development: Nasal spray formulation design, preservative-free systems, biologic integration, stability testing, and dosage optimization.

- Device Engineering & Manufacturing: Metered-dose spray systems, nasal pumps, valves, packaging systems, and drug-device integration technologies.

- Regulatory Approval & Clinical Validation: FDA approval processes, clinical trials, bioequivalence testing, and compliance documentation.

- Distribution & Retail Healthcare Channels: Retail pharmacies, hospital pharmacies, online pharmacies, e-commerce platforms, and healthcare distributors.

- Patient Care & Digital Health Integration: OTC self-care usage, prescription-based treatment, digital adherence monitoring, and connected healthcare ecosystems.

Company-to-Stage Mapping

- API & Pharmaceutical Ingredient Supply: Pfizer API suppliers, global excipient manufacturers, pharmaceutical raw material providers.

- Formulation & Drug Delivery Development: GlaxoSmithKline, AstraZeneca, Johnson & Johnson, Viatris, Bausch Health.

- Device Engineering & Manufacturing: AptarGroup Inc., drug delivery device manufacturers, packaging technology firms.

- Regulatory Approval & Clinical Validation: FDA-regulated pharmaceutical companies, clinical research organizations (CROs), contract manufacturers.

- Distribution & Retail Healthcare Channels: CVS Health, Walgreens, hospital pharmacies, Amazon Pharmacy, retail pharmacy networks.

- Patient Care & Digital Health Integration: Telehealth platforms, digital pharmacy ecosystems, healthcare technology providers.

Investment Activity

U.S. Nasal Spray Market Investment & Funding Dynamics Overview

Investment activity in the U.S. nasal spray market is increasing steadily due to rising prevalence of respiratory disorders, expanding allergy treatment demand, growing adoption of non-invasive drug delivery systems, and rapid innovation in intranasal therapeutic technologies. Between 2026 and 2033, funding is expected to concentrate on advanced nasal drug delivery platforms, biologic intranasal formulations, preservative-free products, and next-generation emergency therapeutic sprays.

The market represents a strategically important segment of the U.S. pharmaceutical and drug delivery ecosystem. Pharmaceutical companies, biotech firms, medical device manufacturers, and healthcare investors are actively increasing capital allocation toward improving intranasal absorption efficiency, enhancing patient compliance, and expanding therapeutic applications beyond traditional allergy and congestion treatments.

A key structural shift influencing investment dynamics is the expansion of intranasal therapies into systemic drug delivery and emergency medicine applications. This includes growing investment in migraine therapies, opioid reversal agents, hormone delivery systems, CNS-targeted treatments, and intranasal vaccine platforms.

The market is also benefiting from increased funding in smart drug delivery technologies, metered-dose spray systems, digital adherence monitoring solutions, and advanced formulation science. Rising demand for rapid-onset therapeutics and self-administered treatment options is further strengthening long-term investment opportunities.

Current Investment & Funding Landscape

Current funding activity in the U.S. nasal spray market is strongly supported by pharmaceutical R&D expansion, growing OTC product commercialization, increasing demand for emergency-use intranasal drugs, and strong retail pharmacy distribution growth. Companies are actively investing in formulation innovation, device engineering, clinical trials, and regulatory approvals for novel intranasal therapies.

- Northeast U.S.: Leading investment activity due to strong pharmaceutical research ecosystems, high allergy prevalence, and advanced healthcare infrastructure.

- Western U.S.: Strong funding growth driven by biotech innovation hubs, respiratory health challenges linked to pollution and wildfires, and high adoption of advanced therapeutics.

- Southern U.S.: Expanding investments supported by large patient populations, high seasonal allergy incidence, and increasing retail healthcare penetration.

- Midwestern U.S.: Stable investment growth supported by strong pharmaceutical distribution networks and expanding healthcare access.

Key Investment & Funding Drivers

- Rising prevalence of allergic rhinitis and sinus disorders is increasing demand for scalable nasal drug delivery solutions.

- Growing preference for non-invasive therapies is driving investment in intranasal formulation innovation.

- Expansion of OTC nasal spray availability is supporting commercialization-focused funding activity.

- Advancements in biologic intranasal therapies are attracting high-value pharmaceutical R&D investments.

- Increasing demand for emergency treatments such as naloxone sprays is accelerating funding in rapid-response therapeutics.

- Technological improvements in metered-dose and preservative-free systems are enhancing device-focused investment opportunities.

- Rising interest in CNS-targeted intranasal drug delivery is creating new high-growth investment pathways.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of integrating advanced formulation science with precision delivery systems.

- Regulatory approvals and clinical validation remain critical differentiators for attracting institutional funding.

- Strategic collaborations between pharmaceutical companies, device manufacturers, and healthcare distributors are strengthening commercialization pathways.

- OTC expansion strategies are becoming a key driver of revenue scalability and investor interest.

- Companies investing in biologics-compatible nasal delivery platforms are expected to gain stronger long-term positioning.

- Digital health integration, including adherence monitoring and smart dosing systems, is emerging as a future investment frontier.

- Organizations with strong IP portfolios and differentiated intranasal technologies are likely to attract higher valuation multiples.

Forward Investment Outlook

The U.S. nasal spray market is expected to maintain strong long-term investment momentum driven by increasing therapeutic diversification, rising consumer healthcare awareness, and continuous innovation in intranasal drug delivery systems.

Future funding activity is expected to prioritize intranasal vaccines, biologic drug delivery platforms, CNS-targeted therapies, smart inhalation-adjacent systems, and advanced emergency response medications.

- Northeast U.S.: Will remain a leading innovation hub for pharmaceutical R&D and clinical development of intranasal therapies.

- Western U.S.: Will strengthen its role in biotech-driven innovation and advanced drug delivery platform development.

- Southern & Midwestern U.S.: Will continue expanding commercialization and distribution-driven investment opportunities.

Future innovation investments are also expected in nanotechnology-enabled nasal delivery systems, precision dosing technologies, and next-generation biologic stabilization methods.

Overall, the convergence of pharmaceutical innovation, patient-centric care models, and rapid therapeutic delivery requirements will continue shaping investment strategies across the U.S. nasal spray market.

Technology & Innovation

U.S. Nasal Spray Market Technology & Innovation Landscape Overview

The U.S. nasal spray market is undergoing continuous technological advancement driven by innovations in drug formulation science, precision delivery systems, biologics integration, and device engineering. The evolution of intranasal therapeutics is increasingly focused on improving bioavailability, enhancing patient compliance, enabling faster onset of action, and expanding therapeutic applications beyond traditional allergy and congestion treatment.

Modern nasal spray technologies are integrating advanced aerosol engineering, micro-dose metering systems, and optimized particle-size distribution to ensure consistent drug deposition across the nasal mucosa. These improvements are significantly enhancing treatment efficacy for both local and systemic therapies.

The market is also witnessing strong adoption of preservative-free formulations, smart delivery devices, and biologic-compatible nasal systems that support emerging therapies such as peptides, vaccines, and central nervous system (CNS)-targeted drugs.

U.S. Nasal Spray Market Technology & Innovation Current Scenario

Currently, nasal spray innovation is centered around improving drug absorption efficiency and ensuring precise dosing control. Metered-dose spray pumps with advanced valve systems are widely used to deliver consistent and accurate drug quantities, reducing dosage variability and improving treatment reliability.

Preservative-free and multidose sterile packaging systems are becoming more common due to increasing concerns around long-term nasal mucosa safety and patient sensitivity. These systems rely on advanced container design technologies such as airless pump systems and collapsible bag-in-bottle structures.

Biopharmaceutical advancements are enabling the development of intranasal biologics, including peptides, monoclonal antibodies, and vaccines. These formulations require specialized stabilization techniques such as lyophilization, nanoparticle encapsulation, and absorption enhancers to improve nasal uptake.

Intranasal vaccine delivery is gaining attention as a non-invasive alternative to injectable immunization, offering advantages such as improved patient compliance and mucosal immunity activation. This is supported by advancements in adjuvant technology and mucosal immunology research.

Device engineering innovations are improving spray plume geometry, droplet size uniformity, and deposition targeting to ensure optimal drug distribution within the nasal cavity. Computational fluid dynamics (CFD) is increasingly used in design optimization.

Digital health integration is also emerging, with smart nasal spray devices incorporating dose tracking, adherence monitoring, and connectivity features for real-time patient data collection.

Key Technology & Innovation Trends in U.S. Nasal Spray Market

- Metered-Dose Delivery Systems: High-precision pumps ensuring accurate and consistent drug administration.

- Preservative-Free Formulations: Advanced packaging systems eliminating the need for chemical preservatives.

- Biologic Intranasal Therapies: Delivery platforms for peptides, proteins, and monoclonal antibodies.

- Intranasal Vaccine Technology: Needle-free vaccine delivery enabling mucosal immune response activation.

- Nanoparticle Drug Delivery: Enhanced absorption and stability using nano-encapsulation techniques.

- Smart Nasal Spray Devices: Connected systems with dose tracking and adherence monitoring capabilities.

- Advanced Aerosol Engineering: Optimized spray plume and droplet size for improved nasal deposition.

- Mucosal Absorption Enhancers: Chemical and biological enhancers improving drug permeability across nasal tissues.

- Digital Health Integration: App-connected devices enabling patient monitoring and treatment optimization.

- Computational Drug Delivery Modeling: CFD-based simulation improving device design and performance efficiency.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the U.S. nasal spray market by shifting focus from traditional decongestant products to high-value therapeutic and biologic intranasal solutions. Companies investing in advanced delivery technologies are achieving stronger differentiation through improved efficacy, safety, and patient experience.

The rise of biologic and vaccine-based nasal formulations is expanding the market beyond respiratory care into preventive healthcare, neurology, and emergency medicine. This is creating new high-growth opportunities for pharmaceutical companies and drug delivery technology providers.

Smart delivery systems and digital adherence technologies are improving patient compliance and enabling real-world treatment monitoring, which is becoming increasingly important in chronic disease management and prescription therapies.

However, regulatory complexity, biologic stability challenges, high development costs, and formulation sensitivity remain key barriers to rapid commercialization of next-generation nasal spray technologies.

U.S. Nasal Spray Market Technology & Innovation Forward Outlook

The future of nasal spray technology in the U.S. is expected to move toward highly advanced, multifunctional, and digitally enabled intranasal delivery systems capable of supporting systemic drug delivery and precision therapeutics.

Emerging innovations include gene therapy delivery via nasal routes, CNS-targeted intranasal drugs for neurological disorders, and AI-assisted formulation design for optimized drug performance.

Intranasal vaccines are expected to gain broader clinical adoption, supported by advances in immunology, antigen stabilization, and mucosal delivery science. This could significantly reshape preventive healthcare strategies.

Integration of artificial intelligence and machine learning in drug formulation and device design is expected to accelerate innovation cycles and improve product optimization across the development pipeline.

Overall, the U.S. nasal spray market is evolving toward a highly sophisticated ecosystem combining pharmaceutical innovation, precision engineering, biologics delivery, and digital health integration to redefine non-invasive drug administration.

Market Risk

Global Nasal Spray Market Risk Factors & Disruption Threats Overview

The global nasal spray market, including the U.S. segment, is experiencing steady expansion driven by rising respiratory disorders, increasing allergy prevalence, and innovation in intranasal drug delivery systems. However, despite strong growth prospects, the industry faces multiple structural risks and disruption threats related to regulatory constraints, competitive substitution, pricing pressure, and evolving healthcare delivery models.

One of the key disruption threats is the growing shift toward alternative drug delivery methods and combination therapies. While nasal sprays offer fast absorption and non-invasive administration, oral solid dosage forms, inhalation therapies, and injectable biologics continue to compete strongly in several therapeutic areas. In some cases, newer biologic formulations may replace intranasal delivery for systemic treatment applications.

Regulatory complexity represents another major risk factor. Nasal sprays, particularly prescription and biologic-based formulations, are subject to stringent FDA requirements in the United States, including clinical efficacy validation, safety profiling, device-drug combination approvals, and post-marketing surveillance. These regulatory pathways can significantly increase time-to-market and development costs.

Product recalls and safety concerns also pose a notable risk to market stability. Issues such as contamination, dosing inconsistency, preservative-related side effects, or device malfunction can lead to regulatory actions and reputational damage. This is especially critical in OTC segments with high consumer exposure.

Intense competition from generic manufacturers and private-label OTC products is another structural challenge. Many nasal spray categories, especially decongestants and saline sprays, face significant pricing pressure due to commoditization, limiting profit margins for branded players.

Supply chain dependencies also create vulnerability in the market. Active pharmaceutical ingredients (APIs), specialized spray pumps, and device components are often sourced globally. Disruptions in packaging materials, pump actuators, or sterile manufacturing inputs can directly impact production continuity.

Another emerging disruption factor is the rapid evolution of digital health and self-care ecosystems. Increased adoption of telemedicine and digital pharmacies is reshaping prescription behavior, while smart health platforms may shift treatment preferences toward integrated respiratory care solutions rather than standalone nasal products.

Environmental and formulation-related pressures are also increasing. Concerns around preservatives, propellants, and plastic-based spray devices are driving demand for eco-friendly, preservative-free, and recyclable packaging solutions, forcing manufacturers to invest in reformulation and redesign.

Global Nasal Spray Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong demand for corticosteroid sprays, antihistamine formulations, and emergency therapeutic sprays such as opioid reversal products. OTC nasal sprays continue to dominate volume consumption, supported by seasonal allergy cycles and self-medication trends.

At the same time, prescription nasal sprays are becoming more specialized, focusing on migraine treatment, hormone delivery, and CNS-related applications. This shift is increasing product differentiation but also raising development complexity and regulatory scrutiny.

Pharmaceutical companies are increasingly investing in preservative-free formulations and advanced metered-dose delivery systems to improve patient compliance and reduce side effects. However, these innovations often come with higher production costs and manufacturing complexity.

E-commerce and retail pharmacy expansion are reshaping distribution dynamics, increasing product accessibility but also intensifying price competition. Online platforms are accelerating brand switching behavior, especially in OTC categories.

Meanwhile, growing environmental concerns and sustainability expectations are pushing manufacturers toward recyclable packaging, reduced plastic usage, and greener propellant alternatives, adding operational pressure to existing production systems.

Global Nasal Spray Market Key Risk Factors & Disruption Threat Signals

- Regulatory Approval Complexity: Strict FDA requirements for prescription sprays and combination drug-device products.

- Product Safety & Recall Risks: Potential contamination, dosing inconsistency, or device malfunction issues.

- Generic Competition Pressure: High commoditization in OTC decongestant and saline spray segments.

- Therapeutic Substitution Risk: Competition from oral drugs, inhalers, and injectable biologics.

- Supply Chain Dependency: Reliance on specialized pumps, APIs, and packaging components.

- Pricing Pressure: Aggressive competition in retail and online pharmacy channels.

- Environmental & Sustainability Pressure: Demand for preservative-free and eco-friendly packaging solutions.

- Manufacturing Complexity: High precision requirements for dose consistency and spray delivery systems.

- Digital Health Substitution Trends: Shift toward integrated respiratory care and telehealth-driven treatment models.

- Seasonal Demand Volatility: Strong dependence on allergy seasons and environmental conditions.

Strategic Implications of Risk Factors

Nasal spray manufacturers must prioritize innovation in preservative-free formulations, precision dosing systems, and next-generation intranasal delivery technologies to maintain competitiveness in both OTC and prescription markets.

Strengthening supply chain resilience for pumps, APIs, and sterile packaging components is essential to mitigate production disruptions and maintain consistent product availability.

Companies will increasingly need to differentiate through specialty therapeutic applications such as migraine treatments, CNS drug delivery, and emergency care solutions rather than relying on commoditized allergy relief products.

Investment in digital pharmacy integration, patient adherence tracking, and connected healthcare ecosystems will become more important as healthcare delivery becomes increasingly digital and patient-centric.

Sustainability-focused innovation, including recyclable packaging, reduced chemical preservatives, and environmentally responsible manufacturing processes, will also play a key role in long-term brand positioning and regulatory alignment.

Global Nasal Spray Market Forward Risk Outlook

Looking ahead to 2026???2033, the nasal spray market is expected to evolve into a more specialized, innovation-driven segment of respiratory and systemic drug delivery. Growth will be concentrated in advanced therapeutic areas such as biologic intranasal delivery, emergency care medications, and CNS-targeted therapies.

However, the market will face increasing competition from alternative drug delivery platforms, including inhalation systems, injectable biologics, and oral specialty drugs, which may limit expansion in some traditional segments.

Regulatory scrutiny will continue to intensify, particularly for novel intranasal biologics and combination drug-device products, increasing development timelines and compliance costs.

Overall, while the market outlook remains positive, long-term success will depend on innovation in formulation science, delivery technology, regulatory strategy, and differentiation beyond conventional allergy and congestion treatments.

Regulatory Landscape

U.S. Nasal Spray Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the U.S. nasal spray market is primarily shaped by pharmaceutical drug approval frameworks, over-the-counter (OTC) drug regulations, medical device combination product guidelines, and strict quality and safety standards for intranasal drug delivery systems. As nasal sprays are widely used for both prescription and OTC applications, they fall under a dual regulatory pathway depending on formulation type, therapeutic indication, and delivery mechanism.

Regulatory oversight in this market focuses on drug safety, bioavailability, manufacturing quality, labeling accuracy, clinical efficacy, and post-market surveillance. Increasing innovation in biologic nasal therapies, intranasal vaccines, and opioid reversal sprays has further expanded the scope of regulatory evaluation and compliance requirements.

At the same time, supportive public health policies addressing opioid overdose emergencies, allergy management, respiratory health, and pandemic preparedness are contributing to broader acceptance and faster regulatory pathways for certain nasal spray products in the United States.

U.S. Nasal Spray Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for nasal sprays in the United States is governed by the U.S. Food and Drug Administration (FDA), which regulates these products under either the New Drug Application (NDA), Abbreviated New Drug Application (ANDA), or Over-the-Counter Monograph system depending on product classification.

Prescription nasal sprays, including corticosteroids, antihistamines, migraine treatments, and specialty biologics, require rigorous clinical trials and FDA approval to demonstrate safety, efficacy, and manufacturing consistency. OTC nasal sprays, such as saline and decongestant products, are regulated under monograph guidelines that define acceptable active ingredients, dosage limits, and labeling requirements.

Combination products that integrate drug formulations with advanced delivery devices are regulated under the FDA???s Office of Combination Products, ensuring both pharmaceutical and device components meet applicable safety standards.

Opioid reversal nasal sprays such as naloxone have received significant regulatory support, including expedited approval pathways and public health distribution programs, reflecting the government???s focus on addressing the opioid crisis.

Additionally, nasal spray products intended for emergency use or pandemic response, including intranasal vaccines and antiviral therapies, may qualify for Emergency Use Authorization (EUA) under specific public health conditions.

Key Regulatory & Policy Environment Signals in U.S. Nasal Spray Market

- FDA Drug Approval Pathways: Prescription nasal sprays require NDA/ANDA approvals with clinical validation of safety, efficacy, and pharmacokinetics.

- Over-the-Counter Monograph System: OTC nasal products must comply with established monograph standards for ingredients, labeling, and dosage limits.

- Combination Product Regulations: Drug-device nasal spray systems must meet integrated regulatory requirements for both pharmaceutical and device components.

- Public Health Emergency Policies: Accelerated approvals and distribution programs support products addressing opioid overdose, respiratory outbreaks, and emergency care needs.

- Good Manufacturing Practice (GMP) Standards: Strict manufacturing compliance ensures product consistency, sterility (where applicable), and patient safety.

- Post-Market Surveillance Requirements: Continuous monitoring of adverse events and real-world performance is required for ongoing regulatory compliance.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory framework is significantly influencing innovation strategies in the U.S. nasal spray market. Pharmaceutical companies are increasingly investing in robust clinical trials, advanced formulation testing, and regulatory science capabilities to accelerate product approvals and reduce time-to-market.

The growing complexity of combination products is driving collaboration between drug developers and device manufacturers to ensure integrated compliance and optimized delivery performance.

Supportive policies for opioid reversal therapies and emergency respiratory treatments are expanding market access and encouraging wider distribution through pharmacies, hospitals, and public health programs.

At the same time, stricter requirements for biologic nasal therapies and intranasal vaccines are pushing manufacturers toward more advanced clinical validation, immunogenicity testing, and long-term safety monitoring.

Companies that proactively align with FDA expectations, invest in regulatory intelligence, and build scalable compliance systems are better positioned to navigate approval pathways efficiently and capture market opportunities.

U.S. Nasal Spray Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the U.S. nasal spray market is expected to become more innovation-adaptive, particularly for biologics, digital health-integrated delivery systems, and intranasal vaccines. The FDA is likely to further refine guidance for combination products and AI-supported drug delivery systems.

Accelerated approval pathways for emergency therapeutics, opioid crisis interventions, and pandemic preparedness solutions are expected to continue shaping market expansion and product innovation.

Increased focus on real-world evidence, post-market surveillance, and pharmacovigilance will strengthen long-term safety monitoring requirements across all nasal spray categories.

Regulatory support for non-invasive drug delivery systems is expected to grow, especially for CNS-targeted therapies, peptide-based formulations, and next-generation biologic nasal sprays.

Overall, the regulatory and policy environment will remain a critical driver of innovation, with companies investing in compliance-ready, clinically validated, and technologically advanced nasal spray solutions expected to maintain strong competitive advantage in the U.S. market.