Global Urban Farming Market Size and Share Analysis 2026-2033

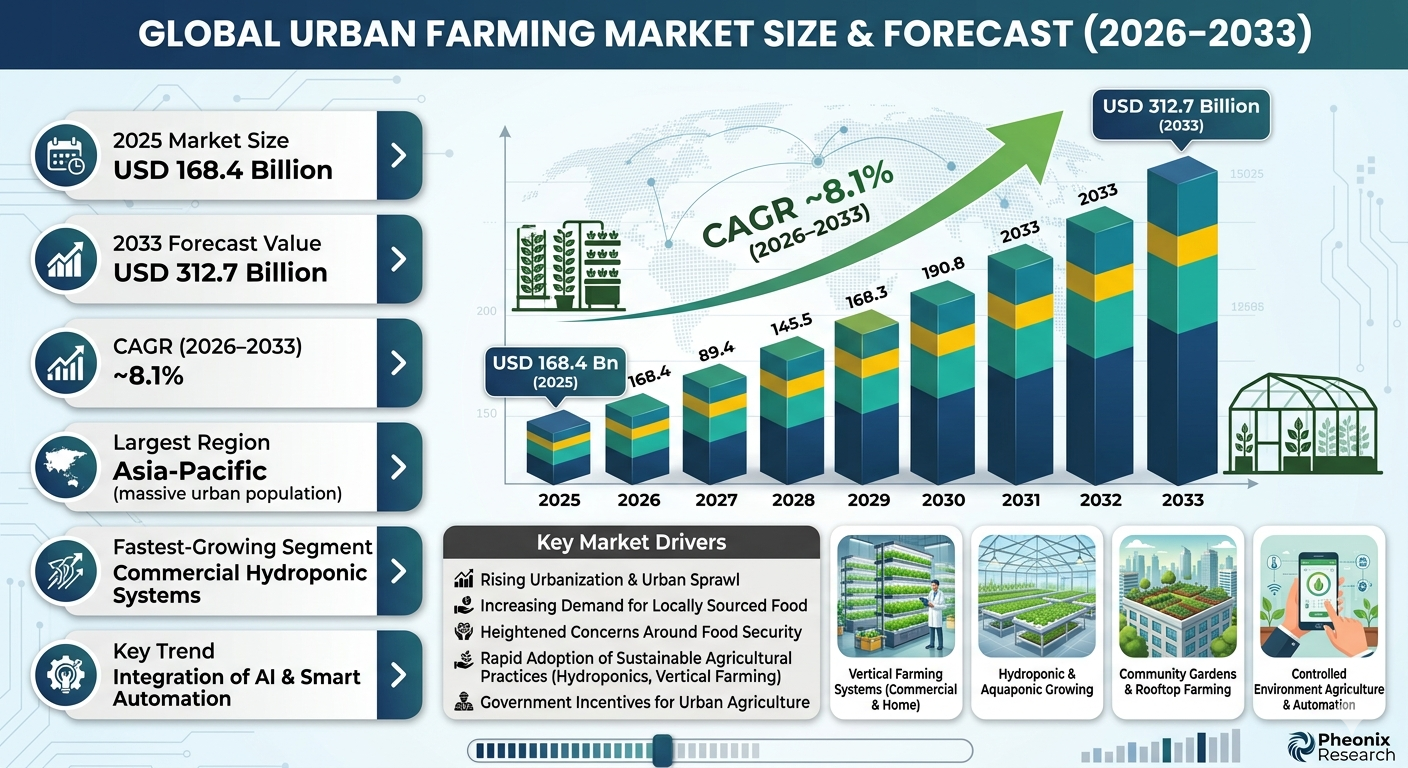

Global Urban Farming Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 168.4 Billion |

| Market Size (2033) | USD 312.7 Billion |

| CAGR (2026???2033) | 8.1% |

| Largest Segment | Vertical Farming Systems |

| Fastest Growing Segment | AI-Enabled Controlled Environment Agriculture (CEA) |

| Leading End-Use Segment | Commercial Urban Farming Operations |

| Key Trend | Integration of Smart Farming Technologies with Urban Infrastructure and Vertical Farming Models |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Primary Growth Driver | Rising Urbanization and Demand for Sustainable Local Food Production |

Global Urban Farming Market Size & Forecast

The global urban farming market is projected to witness strong and sustained growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 168.4 billion in 2025 and is expected to reach nearly USD 312.7 billion by 2033, expanding at a CAGR of around 8.1%. This growth is driven by increasing urbanization, rising demand for locally produced food, growing concerns regarding food security, and rapid adoption of sustainable agricultural practices within urban environments. Urban farming is emerging as a critical solution to address challenges associated with population growth, limited arable land, climate change, and long food supply chains. The market includes a wide range of farming methods such as vertical farming, rooftop farming, hydroponics, aquaponics, indoor farming, and community gardens integrated into urban infrastructure. Technological advancements in controlled environment agriculture (CEA), LED grow lighting, climate control systems, AI-powered farm monitoring, and automated irrigation systems are significantly improving productivity and resource efficiency in urban farming operations. These innovations are enabling year-round crop production with minimal land and water usage. In addition, increasing consumer preference for fresh, pesticide-free, and locally sourced produce is supporting the expansion of urban farming initiatives globally. Governments, municipalities, and private investors are increasingly supporting urban agriculture projects to strengthen food resilience and reduce environmental impact.Global Urban Farming Market Overview

The urban farming market encompasses agricultural activities conducted within or around urban areas using advanced cultivation techniques and controlled environments. The market combines traditional farming concepts with modern agricultural technologies to optimize food production in densely populated regions. Urban farming systems are designed to maximize production efficiency while minimizing transportation costs, carbon emissions, and dependency on conventional agricultural land. These systems often utilize vertical structures, hydroponic nutrient systems, aquaponics, aeroponics, and smart greenhouse technologies. Key industry participants include AeroFarms, Plenty Unlimited, Gotham Greens, Bowery Farming, BrightFarms, Infarm, and numerous regional urban agriculture startups focusing on indoor farming and vertical farming technologies. The market is highly innovation-driven, supported by investments from venture capital firms, food retailers, technology companies, and sustainability-focused organizations. Urban agriculture is increasingly being integrated into smart city initiatives and sustainable urban development programs worldwide.Key Drivers of Global Urban Farming Market Growth

Rapid Urbanization and Population Growth

Rising urban populations are increasing pressure on food supply systems. Urban farming provides localized food production solutions that reduce transportation dependency and improve access to fresh produce in densely populated cities.Growing Demand for Sustainable Agriculture

Consumers and governments are increasingly prioritizing environmentally sustainable food production methods. Urban farming minimizes land use, reduces water consumption, and lowers carbon emissions associated with long-distance food transportation.Advancements in Controlled Environment Agriculture

Innovations in LED lighting, climate control systems, hydroponics, and automation technologies are improving crop yields and enabling year-round cultivation in urban environments.Increasing Preference for Locally Grown Produce

Consumers are increasingly demanding fresh, pesticide-free, and locally sourced vegetables and herbs. Urban farming supports shorter supply chains and improved food quality.Government Support and Smart City Initiatives

Governments and municipalities are supporting urban farming through subsidies, zoning reforms, sustainability programs, and investments in smart agriculture infrastructure.Global Urban Farming Market Segmentation

By Farming Type

The market is segmented into vertical farming, indoor farming, rooftop farming, hydroponics, aquaponics, aeroponics, and community farming. Vertical farming is currently the dominant segment due to its high productivity and efficient land utilization.By Component

The market includes hardware systems, software platforms, and services. Hardware components such as LED grow lights, climate control systems, sensors, irrigation systems, and automated farming equipment account for a significant share of the market.By Crop Type

Crops include leafy greens, herbs, microgreens, tomatoes, strawberries, peppers, and specialty vegetables. Leafy greens dominate due to fast growth cycles and strong demand from urban consumers and restaurants.By Application

Applications include commercial farming, residential farming, institutional farming, and community agriculture projects. Commercial urban farming operations represent the largest revenue-generating segment.By End User

End users include commercial growers, restaurants, supermarkets, households, educational institutions, and government organizations. Commercial retailers and food service providers are increasingly partnering with urban farming companies for fresh produce supply.Regional Market Dynamics

North America holds a major share of the global urban farming market due to strong technological adoption, high investment activity, and growing demand for sustainable local food production in the United States and Canada. Europe is witnessing steady growth supported by strict sustainability regulations, smart city initiatives, and increasing consumer demand for organic and locally sourced produce. Asia-Pacific is the fastest-growing region due to rapid urbanization, rising population density, and increasing food security concerns in countries such as China, Japan, Singapore, and India. Latin America is gradually adopting urban farming systems as cities seek sustainable solutions for food distribution and resource management. Middle East & Africa is emerging as a promising market due to water scarcity challenges and increasing investment in controlled environment agriculture technologies for food security.Competitive Landscape

The global urban farming market is highly competitive and innovation-focused, with participation from agritech startups, vertical farming companies, greenhouse technology providers, and food retailers. Key players include AeroFarms, Plenty Unlimited, Bowery Farming, Gotham Greens, BrightFarms, Infarm, and Freight Farms. Companies are investing heavily in automation, AI-powered farm management systems, energy-efficient LED technologies, and scalable vertical farming infrastructure to improve operational efficiency and profitability. Strategic collaborations with supermarkets, restaurants, and logistics providers are becoming increasingly common as urban farming companies expand distribution networks and strengthen supply chain integration. Competition is centered around yield optimization, energy efficiency, sustainability, and ability to scale production within urban environments. Continuous innovation remains a key differentiator in the market.Strategic Outlook

The strategic outlook for the urban farming market remains highly positive as cities increasingly prioritize food resilience, sustainability, and local food production. Urban farming is expected to become an integral component of future smart city ecosystems. Future growth opportunities lie in AI-driven crop optimization, robotic harvesting systems, renewable energy integration, and modular farming infrastructure designed for urban spaces. Increasing investments in vertical farming startups, climate-resilient agriculture, and sustainable food systems are expected to accelerate market innovation and commercialization over the forecast period.Final Market Perspective

The global urban farming market is positioned for long-term expansion driven by rapid urbanization, rising sustainability awareness, and growing demand for local food production systems. Urban agriculture is transforming how cities approach food security, environmental sustainability, and resource efficiency. As technological advancements continue to improve productivity and cost efficiency, urban farming is expected to become a mainstream agricultural model in modern cities. Companies that combine scalable farming technologies with sustainable production practices will be well-positioned to lead the future of urban agriculture globally.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Urban Farming Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Future Strategic Outlook

- 2. Introduction & Market Overview

- 2.1 Definition of Urban Farming

- 2.2 Scope of the Study

- 2.3 Evolution of Urban Agriculture

- 2.4 Urban Food Supply Ecosystem

- 2.5 Sustainability & Smart City Integration

- 2.6 Regulatory & Government Support Landscape

- 2.7 Technology & Innovation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rapid Urbanization & Population Growth

- 4.1.2 Increasing Demand for Sustainable Agriculture

- 4.1.3 Advancements in Controlled Environment Agriculture

- 4.1.4 Rising Demand for Locally Grown Produce

- 4.1.5 Government Support & Smart City Initiatives

- 4.2 Restraints

- 4.2.1 High Initial Infrastructure Costs

- 4.2.2 Energy Consumption Challenges

- 4.2.3 Technical Skill Limitations

- 4.2.4 Limited Profitability in Early Stages

- 4.3 Opportunities

- 4.3.1 Expansion of Vertical Farming Projects

- 4.3.2 AI & Automation Integration

- 4.3.3 Renewable Energy-Powered Farming Systems

- 4.3.4 Emerging Markets & Urban Food Security Programs

- 4.4 Challenges

- 4.4.1 Scalability Constraints

- 4.4.2 Regulatory & Zoning Restrictions

- 4.4.3 Supply Chain & Distribution Complexity

- 4.4.4 Competition from Conventional Agriculture

- 4.1 Drivers

- 5. Global Urban Farming Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Revenue Distribution by Region

- 5.4 Segment Revenue Analysis

- 5.5 Technology Adoption Trends

- 5.6 Sustainability Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Farming Type

- 6.1.1 Vertical Farming

- 6.1.1.1 Indoor Vertical Farming

- 6.1.1.1.1 Automated Vertical Farming Systems

- 6.1.1.1.1.1 AI-Enabled Vertical Farming

- 6.1.1.1.1 Automated Vertical Farming Systems

- 6.1.1.1 Indoor Vertical Farming

- 6.1.2 Indoor Farming

- 6.1.2.1 Smart Greenhouse Farming

- 6.1.2.1.1 Climate-Controlled Farming

- 6.1.2.1.1.1 Sensor-Based Indoor Farming

- 6.1.2.1.1 Climate-Controlled Farming

- 6.1.2.1 Smart Greenhouse Farming

- 6.1.3 Hydroponics

- 6.1.3.1 Nutrient Film Technique Systems

- 6.1.3.1.1 Deep Water Culture Systems

- 6.1.3.1.1.1 Automated Hydroponic Platforms

- 6.1.3.1.1 Deep Water Culture Systems

- 6.1.3.1 Nutrient Film Technique Systems

- 6.1.4 Aquaponics

- 6.1.4.1 Fish-Integrated Farming Systems

- 6.1.5 Rooftop Farming

- 6.1.5.1 Commercial Rooftop Farms

- 6.1.1 Vertical Farming

- 6.2 By Component

- 6.2.1 Hardware

- 6.2.1.1 LED Grow Lights

- 6.2.1.2 Climate Control Systems

- 6.2.1.3 Irrigation Systems

- 6.2.1.4 Sensors & Monitoring Equipment

- 6.2.2 Software

- 6.2.2.1 Farm Management Platforms

- 6.2.2.2 AI-Based Crop Monitoring Software

- 6.2.3 Services

- 6.2.3.1 Consulting & Integration Services

- 6.2.3.2 Maintenance & Technical Support

- 6.2.1 Hardware

- 6.3 By Crop Type

- 6.3.1 Leafy Greens

- 6.3.2 Herbs

- 6.3.3 Tomatoes

- 6.3.4 Strawberries

- 6.3.5 Peppers

- 6.3.6 Specialty Vegetables

- 6.4 By Application

- 6.4.1 Commercial Farming

- 6.4.2 Residential Farming

- 6.4.3 Institutional Farming

- 6.4.4 Community Agriculture Projects

- 6.5 By End User

- 6.5.1 Commercial Growers

- 6.5.2 Supermarkets & Retail Chains

- 6.5.3 Restaurants & Food Service Providers

- 6.5.4 Educational Institutions

- 6.5.5 Government Organizations

- 6.1 By Farming Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product & Technology Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Investment & Funding Analysis

- 8.5 Competitive Differentiation Strategies

- 9. Company Profiles

- 9.1 AeroFarms

- 9.2 Plenty Unlimited

- 9.3 Bowery Farming

- 9.4 Gotham Greens

- 9.5 BrightFarms

- 9.6 Infarm

- 9.7 Freight Farms

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Smart Farming Infrastructure Analyzer

- 10.3 AI-Based Yield Optimization Tracker

- 10.4 Sustainability & Resource Efficiency Insights

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Smart Urban Agriculture

- 11.2 Investment Opportunities in Vertical Farming

- 11.3 AI & Automation Adoption Strategies

- 11.4 Sustainable Food Infrastructure Development

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Urban Farming Market Competitive Intensity & Market Structure Overview

The Global Urban Farming Market is characterized by a highly innovation-driven and sustainability-focused competitive ecosystem supported by increasing urbanization, rising demand for locally produced food, and rapid adoption of controlled environment agriculture technologies. The market is transitioning from small-scale community farming initiatives toward large-scale commercial urban agriculture operations integrated with smart city infrastructure and advanced automation systems.

Competitive intensity is increasing rapidly as companies compete through technological innovation, yield optimization, energy efficiency, crop diversification, and scalable farming infrastructure. Market participants are focusing heavily on AI-powered crop monitoring, automated irrigation systems, climate-controlled farming environments, and energy-efficient LED grow technologies to strengthen operational efficiency and profitability.

The market structure remains moderately fragmented, with a combination of vertical farming startups, greenhouse technology providers, agritech companies, and commercial food producers competing across regional and global markets. Established players are expanding production facilities and distribution partnerships, while emerging startups continue introducing specialized urban farming solutions and modular cultivation systems.

Global Urban Farming Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

AeroFarms: Vertical Farming Technology Leader. Known for advanced indoor farming systems, aeroponic cultivation technology, and AI-driven crop optimization platforms.

Plenty Unlimited: High-Tech Indoor Farming Company. Focused on scalable vertical farming infrastructure and automated fresh produce production systems.

Bowery Farming: AI-Powered Urban Agriculture Provider. Specializes in smart indoor farming systems integrated with machine learning and data analytics technologies.

Gotham Greens: Commercial Greenhouse Farming Operator. Operates large-scale rooftop greenhouses supplying fresh produce to urban retail markets.

BrightFarms: Controlled Environment Agriculture Specialist. Focused on localized greenhouse farming and direct partnerships with supermarkets and retailers.

Infarm: Modular Urban Farming Innovator. Develops compact in-store and distributed farming systems for urban retail and food service applications.

Freight Farms: Container Farming Solutions Provider. Specializes in hydroponic farming systems built inside modular shipping containers.

Crop One Holdings: Commercial Vertical Farming Company. Expanding large-scale indoor farming operations integrated with sustainable food production models.

Mirai Co.: Japanese Indoor Farming Specialist. Focused on LED-based controlled farming environments and high-efficiency vegetable production systems.

Spread Co. Ltd.: Automated Vertical Farming Company. Known for robotic harvesting systems and highly automated indoor lettuce production facilities.

Key Competitive Intensity & Market Structure Signals in Global Urban Farming Market

One of the strongest competitive signals in the market is the increasing investment in automation and artificial intelligence technologies. Companies are aggressively adopting AI-driven crop management, robotic harvesting systems, predictive analytics, and IoT-enabled monitoring platforms to improve productivity and reduce labor dependency.

The rapid expansion of vertical farming infrastructure is significantly reshaping market competition. Large-scale indoor farming facilities capable of year-round production are becoming key competitive differentiators, particularly in densely populated urban centers with limited agricultural land availability.

Another major market signal is the growing emphasis on sustainability and resource efficiency. Companies are competing through water-saving hydroponic systems, renewable energy integration, waste recycling models, and low-carbon food production strategies to align with environmental goals and regulatory expectations.

Strategic partnerships with supermarkets, restaurants, hospitality chains, and food delivery companies are becoming increasingly important for distribution expansion and stable revenue generation. Retail integration is strengthening localized supply chains and improving consumer access to fresh produce.

Investment activity from venture capital firms, technology investors, and sustainability-focused funds continues to accelerate market innovation. Capital inflows are supporting expansion of scalable urban farming systems and commercialization of next-generation agricultural technologies.

Strategic Implications of Competitive Intensity & Market Structure in Global Urban Farming Market

Urban farming companies are increasingly shifting from niche agricultural operations toward fully integrated smart food production ecosystems. Automation, software integration, and supply chain optimization are becoming central to long-term competitive positioning.

Technology leadership is emerging as a critical strategic advantage. Companies investing in AI-based crop analytics, climate optimization algorithms, and energy-efficient farming infrastructure are achieving higher operational scalability and production consistency.

Operational efficiency and energy management are becoming increasingly important due to the high electricity requirements associated with indoor farming systems. Firms focusing on renewable energy integration and low-energy cultivation technologies are improving long-term cost competitiveness.

Product differentiation through premium, pesticide-free, organic, and locally sourced produce is strengthening brand positioning among health-conscious consumers and urban retailers. Consumer preference for fresh and traceable food products continues to support premium pricing opportunities.

Additionally, scalability and infrastructure expansion are becoming key strategic priorities. Companies capable of replicating modular farming systems across multiple urban markets are expected to achieve stronger market penetration and operational growth.

Global Urban Farming Market Competitive Intensity & Market Structure Forward Outlook

The Global Urban Farming Market is expected to remain highly competitive as urban food production increasingly becomes part of broader sustainability and smart city development strategies worldwide.

Technological innovation in automation, robotics, artificial intelligence, and controlled environment agriculture will continue to drive future market competition and operational transformation across the industry.

Vertical farming and hydroponic systems are anticipated to witness significant expansion due to rising demand for year-round crop production, water efficiency, and localized food supply chains.

Government support for sustainable agriculture, urban resilience, and climate-smart infrastructure is expected to accelerate adoption of urban farming technologies across developed and emerging economies.

In the long term, the market will be shaped by three major competitive pillars: scalable automation, sustainable production efficiency, and integrated urban food distribution networks. Companies that successfully combine advanced agricultural technologies with energy-efficient and commercially scalable farming models are expected to lead the Global Urban Farming Market through 2033.

Value Chain

Global Urban Farming Market Value Chain & Supply Chain Evolution Overview

The Global Urban Farming Market value chain is rapidly evolving from traditional localized gardening systems into highly controlled, technology-driven, vertically integrated food production ecosystems. This transformation is being driven by rapid urbanization, food security concerns, climate change pressures, limited arable land availability, and growing demand for sustainable, locally produced food.

Urban farming integrates advanced agricultural technologies such as vertical farming, hydroponics, aquaponics, aeroponics, AI-powered monitoring systems, LED grow lighting, automated irrigation, and climate-controlled cultivation environments. These systems enable efficient year-round crop production within densely populated urban environments while minimizing land, water, and transportation requirements.

The value chain now extends far beyond traditional agriculture into controlled environment agriculture (CEA) infrastructure, smart farming technologies, IoT-enabled sensors, AI analytics platforms, renewable energy integration, urban logistics systems, and direct-to-consumer food distribution networks. Leading companies such as AeroFarms, Plenty Unlimited, Bowery Farming, Gotham Greens, BrightFarms, and Infarm are increasingly building integrated urban agriculture ecosystems.

The upstream supply chain increasingly depends on LED lighting manufacturers, climate control system providers, nutrient solution suppliers, hydroponic equipment manufacturers, IoT sensor developers, robotics companies, and software platform providers.

Midstream operations focus on urban farm construction, controlled environment system integration, automated cultivation systems, AI-powered crop management platforms, and energy-efficient production infrastructure designed for high-density urban food production.

Downstream operations include fresh produce distribution, retailer partnerships, restaurant supply agreements, direct-to-consumer delivery platforms, and urban food logistics optimization. Shorter supply chains and localized distribution models are becoming defining characteristics of the urban farming ecosystem.

Key supply chain challenges include high initial infrastructure costs, energy consumption management, scalability limitations, urban real estate costs, supply chain integration complexity, and maintaining consistent production efficiency across controlled environments.

Global Urban Farming Market Value Chain & Supply Chain Evolution Current Scenario

The current urban farming ecosystem is shaped by rising investments in vertical farming infrastructure, rapid adoption of controlled environment agriculture technologies, and increasing integration of AI-driven farm management systems.

Technology suppliers are expanding production of LED grow lighting systems, climate control technologies, hydroponic infrastructure, and smart irrigation systems to support growing demand for urban agriculture solutions.

Urban farming operators are increasingly integrating AI-powered crop monitoring, IoT-enabled environmental controls, and predictive analytics platforms to optimize yield quality, energy usage, and operational efficiency.

Retailers, restaurants, and food service companies are forming strategic partnerships with urban farming operators to secure reliable access to fresh, locally grown produce with shorter supply chains.

Governments and municipalities are increasingly supporting urban farming through smart city programs, sustainability initiatives, zoning reforms, and food resilience policies aimed at reducing urban food insecurity.

Controlled environment agriculture systems are becoming more scalable and commercially viable due to improvements in automation, renewable energy integration, and precision nutrient management technologies.

Key Value Chain & Supply Chain Evolution Signals in Global Urban Farming Market

Several transformative trends are reshaping the urban farming ecosystem globally.

First, vertical farming expansion is accelerating demand for advanced LED lighting systems, AI-powered crop optimization platforms, and automated cultivation technologies.

Second, rising consumer demand for fresh, pesticide-free, and locally sourced produce is strengthening localized urban food production models.

Third, increasing climate change concerns and food supply disruptions are driving investments in resilient controlled environment agriculture systems.

Fourth, integration of AI, IoT, robotics, and data analytics is improving crop monitoring accuracy, yield optimization, and operational efficiency within urban farming facilities.

Fifth, sustainability-focused urban development and smart city initiatives are increasing adoption of rooftop farming, indoor agriculture, and modular farming systems.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Urban Farming Market

Industry leaders such as AeroFarms, Plenty Unlimited, Bowery Farming, Gotham Greens, BrightFarms, and Infarm are strengthening competitive positioning through scalable vertical farming infrastructure, AI-driven cultivation systems, and integrated food distribution networks.

Competitive advantage increasingly depends on energy efficiency, crop yield optimization, automation capability, supply chain integration, scalability of controlled environment systems, and ability to reduce operational costs.

Companies capable of integrating advanced hardware, AI-powered farm management systems, renewable energy solutions, and efficient urban logistics are best positioned to capture long-term market opportunities.

Strategic collaboration between agritech companies, food retailers, smart city developers, logistics providers, and renewable energy firms is becoming increasingly important for ecosystem expansion and operational optimization.

Long-term success will increasingly rely on balancing production scalability, energy management, affordability, sustainability, and consistent crop quality across urban farming ecosystems.

Global Urban Farming Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the urban farming value chain is expected to become increasingly automated, AI-driven, energy-efficient, and integrated with future smart city ecosystems.

Urban farming operators will increasingly prioritize robotic harvesting systems, AI-powered crop optimization platforms, autonomous nutrient management, and renewable energy integration to improve profitability and sustainability.

Controlled environment agriculture systems will continue evolving toward highly modular, scalable, and climate-resilient farming infrastructure capable of operating within diverse urban environments.

Digital twin technologies, predictive crop analytics, and real-time environmental monitoring systems are expected to enhance operational precision and reduce production risks.

Localized food supply ecosystems integrating urban farming, direct-to-consumer delivery, and smart logistics platforms will increasingly reduce dependency on long-distance agricultural supply chains.

Ultimately, the future urban farming value chain will evolve from niche urban agriculture projects into fully integrated, intelligent, and sustainable urban food production ecosystems.

Market-Specific Value Chain

- Core Technology & Input Supply: LED grow lighting, hydroponic systems, nutrient solutions, IoT sensors, climate control systems, automation equipment

- Digital Infrastructure & Software Platforms: AI crop analytics, cloud farm management systems, predictive monitoring software, environmental control platforms

- Urban Farm Infrastructure Development: Vertical farming facilities, indoor farming systems, rooftop farming structures, modular cultivation units

- Automated Cultivation & Crop Management: Irrigation automation, robotic harvesting, nutrient optimization, AI-powered environmental management

- Urban Food Distribution & Logistics: Retail partnerships, direct-to-consumer delivery, restaurant supply networks, local produce logistics

- Sustainability & Resource Optimization: Renewable energy integration, water recycling systems, waste reduction, circular agriculture management

Company-to-Stage Mapping

- Core Technology & Input Supply: LED technology providers, hydroponic equipment manufacturers, IoT sensor developers, climate system suppliers

- Digital Infrastructure & Software Platforms: Agritech software companies, AI analytics providers, cloud infrastructure firms

- Urban Farm Infrastructure Development: AeroFarms, Plenty Unlimited, Bowery Farming, Gotham Greens

- Automated Cultivation & Crop Management: Infarm, BrightFarms, robotics providers, automated farming technology companies

- Urban Food Distribution & Logistics: Supermarket chains, food service distributors, direct-to-consumer delivery partners

- Sustainability & Resource Optimization: Renewable energy firms, water management technology providers, sustainable agriculture solution companies

Investment Activity

Global Urban Farming Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Urban Farming Market are being driven by rapid urbanization, increasing food security concerns, rising demand for locally produced food, and accelerating adoption of sustainable agriculture technologies. Between 2026 and 2033, capital allocation is expected to increase significantly toward vertical farming systems, controlled environment agriculture (CEA), hydroponics, aquaponics, AI-powered crop management platforms, and energy-efficient urban farming infrastructure.

The market is highly technology-driven and requires continuous investment in LED grow lighting, climate control systems, automated irrigation technologies, robotics, IoT-enabled monitoring systems, and smart greenhouse solutions. Leading companies such as AeroFarms, Plenty Unlimited, Bowery Farming, Gotham Greens, BrightFarms, and Infarm are increasing investments in scalable indoor farming operations and next-generation urban agriculture technologies.

A major structural shift influencing investment flows is the growing transition toward localized food production and resilient urban food supply chains. This shift is accelerating funding into high-density farming systems designed to reduce transportation costs, minimize resource consumption, and improve year-round crop production within urban environments.

Global Urban Farming Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by increasing venture capital participation in agritech startups, government sustainability initiatives, and rising commercial demand for fresh, pesticide-free, and locally sourced produce. Strategic partnerships between technology providers, food retailers, municipalities, and urban farming companies are becoming increasingly important for market expansion and infrastructure development.

- North America: Leads global investment activity due to advanced agritech ecosystems, strong venture capital funding, and growing adoption of vertical farming technologies across the United States and Canada.

- Europe: Witnessing strong investment growth driven by sustainability-focused agricultural policies, smart city development programs, and rising consumer demand for organic local produce.

- Asia-Pacific: Fastest-growing investment region supported by rapid urbanization, increasing population density, and strong food security initiatives in countries such as China, Japan, Singapore, and India.

- Middle East & Africa & Latin America: Emerging investment regions due to increasing focus on water-efficient agriculture systems, climate-resilient food production, and urban food sustainability programs.

Key Investment & Funding Dynamics Signals in Global Urban Farming Market

- Rapid expansion of vertical farming and indoor farming operations is increasing investment in automated cultivation systems, smart lighting technologies, and climate-controlled infrastructure.

- Growing demand for sustainable and pesticide-free produce is driving capital inflows into hydroponic, aquaponic, and organic urban farming systems.

- Rising integration of AI, IoT, and data analytics in urban agriculture is encouraging investments in predictive crop monitoring, automated nutrient management, and remote farm control platforms.

- Increasing pressure on urban food supply chains is accelerating funding into localized food production models that reduce transportation dependency and improve food resilience.

- Expansion of renewable energy integration within urban farming systems is creating new investment opportunities in solar-powered greenhouses and energy-efficient farming infrastructure.

Strategic Implications of Investment & Funding Dynamics in Global Urban Farming Market

- The investment landscape strongly favors companies capable of integrating automation, AI, and controlled environment technologies into scalable urban farming ecosystems.

- Strategic partnerships between agritech companies, municipalities, supermarkets, restaurants, and logistics providers are becoming increasingly important for distribution efficiency and long-term market expansion.

- Technological innovation is emerging as a major competitive differentiator, particularly in crop yield optimization, energy efficiency, and automated farm management systems.

- Regional diversification remains essential, with North America leading in technological innovation, Europe focusing on sustainability-driven agriculture, and Asia-Pacific driving large-scale urban farming adoption.

- High infrastructure and energy costs remain major operational challenges, encouraging investments in cost-efficient farming models and renewable energy integration solutions.

Global Urban Farming Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Urban Farming Market is expected to attract strong and sustained investment as cities increasingly prioritize sustainable food systems, climate resilience, and localized agricultural production.

Future capital allocation will prioritize AI-driven crop optimization, robotic harvesting systems, modular vertical farming units, renewable energy-powered greenhouses, and advanced water-efficient farming technologies.

- North America: Will continue leading innovation in automated urban farming systems and AI-based farm analytics.

- Europe: Will remain a major hub for sustainable urban agriculture and smart city farming initiatives.

- Asia-Pacific: Will witness the fastest investment growth due to rapid urban expansion and increasing government focus on food security and agricultural modernization.

Digital transformation will further reshape investment patterns, with increasing focus on connected farming ecosystems, remote crop monitoring, predictive analytics, and fully automated urban agriculture facilities.

Overall, the market is expected to maintain strong long-term growth supported by rising urban populations, sustainability priorities, and technological innovation in controlled environment agriculture. Companies that successfully combine scalable production systems with energy-efficient and technology-driven farming solutions will be best positioned to lead the Global Urban Farming Market through 2033.

Technology & Innovation

Global Urban Farming Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Urban Farming Market is rapidly transforming food production within urban environments through advanced controlled-environment agriculture systems, automation technologies, and data-driven farming models. Innovation is primarily focused on maximizing crop productivity in limited urban spaces while reducing water consumption, transportation dependency, and environmental impact.

Urban farming technologies are increasingly integrating artificial intelligence, IoT-enabled monitoring systems, robotics, hydroponics, aeroponics, aquaponics, and vertical farming infrastructure to enable highly efficient indoor cultivation systems. These innovations are helping urban farms achieve year-round crop production with improved yield consistency and resource optimization.

A major technological shift in the market is the rise of vertical farming systems that utilize stacked cultivation layers combined with LED grow lighting and automated nutrient delivery systems. These systems significantly increase production density while minimizing land requirements in urban areas.

Controlled environment agriculture (CEA) technologies are also becoming increasingly sophisticated through the use of climate control systems, automated irrigation, AI-powered crop analytics, and environmental sensors that optimize growing conditions in real time.

Additionally, innovations in renewable energy integration, water recycling systems, and smart greenhouse technologies are supporting the development of sustainable and energy-efficient urban farming ecosystems capable of operating within densely populated cities.

Global Urban Farming Market Technology & Innovation Landscape Current Scenario

Currently, the urban farming market is experiencing rapid technological adoption driven by increasing food security concerns, urbanization, and sustainability initiatives. Commercial vertical farms and indoor farming facilities are expanding across major metropolitan areas globally.

Hydroponic and aeroponic cultivation systems are among the most widely adopted technologies due to their ability to significantly reduce water usage while improving crop growth efficiency. These soil-free farming systems are becoming standard across modern urban farming operations.

AI-driven farm management platforms are increasingly being used to monitor crop growth, regulate nutrient delivery, manage environmental conditions, and predict yield performance. These systems help improve operational efficiency and reduce labor requirements.

IoT-enabled sensors are widely deployed to collect real-time data related to temperature, humidity, pH levels, nutrient concentration, and light intensity. This data is processed through cloud-based analytics platforms to optimize growing conditions and minimize resource waste.

Automated LED grow lighting systems are also becoming more advanced, utilizing spectrum-optimized lighting technologies that improve photosynthesis efficiency and reduce energy consumption in indoor farms.

Urban farming companies are increasingly utilizing robotics for automated seeding, transplanting, harvesting, and packaging operations to improve scalability and reduce operational costs in commercial facilities.

Key Technology & Innovation Trends in Global Urban Farming Market

- Vertical Farming Systems: Multi-layer indoor farming structures maximizing crop production within limited urban spaces.

- Hydroponics & Aeroponics: Soil-free cultivation technologies improving water efficiency and crop growth rates.

- AI-Powered Farm Management: Intelligent systems optimizing climate control, irrigation, nutrient delivery, and crop health monitoring.

- IoT-Based Environmental Monitoring: Real-time sensor networks tracking temperature, humidity, pH levels, and nutrient conditions.

- Advanced LED Grow Lighting: Spectrum-optimized lighting systems improving plant growth efficiency while reducing energy consumption.

- Automated Irrigation & Nutrient Systems: Precision-controlled delivery systems minimizing water and fertilizer waste.

- Agricultural Robotics: Robotic harvesting, seeding, and packaging systems improving operational scalability.

- Smart Greenhouse Technologies: Integrated climate-controlled farming environments enhancing year-round productivity.

- Renewable Energy Integration: Solar-powered urban farms and energy-efficient infrastructure supporting sustainability goals.

- Cloud-Based Farm Analytics Platforms: Centralized digital systems enabling remote monitoring and predictive farm management.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping the urban farming market by enabling localized, sustainable, and highly efficient food production systems within cities. Advanced farming technologies are reducing dependency on conventional agriculture while improving food accessibility in urban populations.

For commercial urban farming operators, technology adoption has become a critical competitive factor. Companies leveraging integrated ecosystems combining AI, automation, climate control, and analytics are achieving significant advantages in crop yield optimization, resource efficiency, and operational scalability.

The integration of automation and robotics is also helping address labor shortages while improving consistency and reducing production costs in large-scale indoor farming facilities.

At the same time, sustainability-focused innovations such as water recycling systems, renewable energy integration, and low-carbon production models are strengthening the role of urban farming in future smart city infrastructure and climate resilience strategies.

However, high capital investment requirements, energy consumption challenges, and infrastructure limitations remain key barriers to widespread adoption, particularly in developing regions.

Global Urban Farming Market Technology & Innovation Forward Outlook

Looking ahead, the urban farming market is expected to evolve toward highly automated and fully connected agricultural ecosystems powered by AI, robotics, and advanced environmental control technologies. Fully autonomous indoor farms are likely to become increasingly viable as automation technologies mature.

The integration of artificial intelligence with predictive analytics and machine learning will further improve crop optimization, disease detection, and resource management efficiency across urban farming systems.

Advanced robotics and autonomous harvesting technologies are expected to significantly improve scalability and reduce labor dependency in commercial vertical farming operations.

The convergence of renewable energy systems, smart grid technologies, and energy-efficient LED infrastructure will play a major role in improving the long-term sustainability and profitability of urban farming facilities.Modular farming systems and container-based urban farms are also expected to gain traction, enabling flexible deployment of localized food production systems across residential, commercial, and institutional environments.

In conclusion, the Global Urban Farming Market is undergoing a major technological transformation driven by automation, AI-powered farming systems, and sustainable agriculture innovations. Companies that successfully combine scalable cultivation technologies, intelligent farm management platforms, and resource-efficient infrastructure will lead the future of urban food production globally.

Market Risk

Global Urban Farming Market Risk Factors & Disruption Threats Overview

The Global Urban Farming Market is rapidly evolving as cities increasingly adopt sustainable food production systems, controlled environment agriculture, and technology-driven farming models. While the market benefits from rising urbanization, food security concerns, and growing demand for locally sourced produce, it carries a moderate-to-high strategic risk profile due to high operational costs, technological dependency, energy consumption challenges, and infrastructure scalability limitations.

One of the primary risk factors is the high capital expenditure associated with urban farming infrastructure. Vertical farming facilities, hydroponic systems, climate control technologies, LED grow lighting, and automated irrigation systems require significant upfront investment, creating financial barriers for new entrants and limiting scalability for smaller operators.

Another major disruption factor involves energy dependency and operational cost volatility. Controlled environment agriculture systems consume substantial electricity for lighting, temperature regulation, and automation processes, making profitability highly sensitive to rising energy prices and utility cost fluctuations.

Supply chain and resource availability challenges also create market uncertainty. Urban farming operations rely heavily on specialized equipment, nutrient solutions, sensors, climate-control systems, and semiconductor-based technologies, making them vulnerable to global supply chain disruptions and component shortages.

Additionally, increasing competition among agritech startups, greenhouse operators, and large-scale vertical farming companies is intensifying pricing pressure and accelerating market consolidation. Companies unable to achieve operational efficiency and scalable production economics may face long-term sustainability challenges.

Global Urban Farming Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong global momentum toward sustainable agriculture, local food production, and climate-resilient farming systems. Governments, municipalities, and private investors are increasingly supporting urban farming initiatives to strengthen food security and reduce dependence on traditional agricultural supply chains.

However, urban farming operators continue to face profitability concerns due to high energy consumption, labor costs, and limited economies of scale compared to conventional agriculture. Many vertical farming startups are under pressure to optimize operational efficiency and reduce production costs to achieve long-term commercial viability.

Technological complexity is also increasing operational risk across the industry. Urban farming systems depend heavily on AI-driven monitoring platforms, automated irrigation systems, environmental sensors, and climate-control infrastructure, creating vulnerability to system failures, cybersecurity threats, and maintenance disruptions.

Meanwhile, rising urban real estate costs and zoning restrictions in major metropolitan areas are limiting expansion opportunities for large-scale urban farming infrastructure. Access to affordable urban space remains a significant operational challenge for many market participants.

At the same time, changing consumer expectations regarding organic certification, sustainability standards, and pesticide-free production are increasing compliance and quality assurance requirements across the market.

Key Risk Factors & Disruption Threats Signals in Global Urban Farming Market

A major disruption signal is the rapid advancement of AI-powered precision farming and robotics integration within urban agriculture systems. Autonomous harvesting, predictive crop analytics, and machine-learning-based environmental optimization are transforming operational models and increasing competitive pressure on traditional farming operators.

Energy sustainability concerns continue to intensify as urban farming facilities require high electricity consumption for indoor cultivation systems. Increasing focus on renewable energy integration and carbon-neutral farming practices is reshaping investment priorities across the market.

The expansion of alternative food technologies such as lab-grown foods, precision fermentation, and advanced greenhouse agriculture is also creating long-term competitive disruption for urban farming operators seeking market differentiation.

Climate change-related risks, including water scarcity, extreme weather events, and heat stress in urban environments, are increasing pressure on operators to adopt resilient farming infrastructure and resource-efficient cultivation systems.

Additionally, tightening food safety regulations, urban environmental policies, and sustainability reporting standards are increasing operational compliance complexity for commercial urban farming companies globally.

Strategic Implications of Risk Factors & Disruption Threats in Global Urban Farming Market

Market participants must prioritize energy efficiency, automation integration, and scalable production systems to remain competitive in the evolving urban farming ecosystem. Investment in low-energy LED technologies, renewable energy solutions, and AI-driven environmental management systems will become increasingly critical for operational sustainability.

Companies should strengthen supply chain resilience by diversifying equipment sourcing strategies and developing localized infrastructure partnerships to reduce dependency on imported agricultural technologies and specialized components.

Urban farming operators must also focus on achieving production cost optimization and improving yield consistency to compete effectively with conventional agriculture and greenhouse farming alternatives.

Strategic collaboration with municipalities, real estate developers, supermarkets, and food service providers will play an important role in expanding market access and strengthening localized distribution networks.

Additionally, investment in sustainable branding, organic certification, water recycling systems, and environmentally responsible farming practices will become essential for maintaining consumer trust and regulatory compliance.

Global Urban Farming Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Urban Farming Market is expected to transition toward highly automated, resource-efficient, and technology-driven agricultural ecosystems. However, long-term market risks will remain closely tied to energy economics, infrastructure scalability, and operational profitability.

AI-driven crop optimization, robotic harvesting systems, smart greenhouse technologies, and renewable-energy-powered vertical farms are expected to redefine competitive dynamics and operational efficiency standards across the industry.

The integration of IoT-enabled monitoring systems, predictive analytics, and climate-adaptive farming infrastructure will significantly improve yield management and resource optimization capabilities.

At the same time, increasing pressure for sustainable food production and carbon reduction targets will accelerate investment in circular agriculture models, water-efficient cultivation technologies, and decentralized urban food systems.

Overall, while the market presents strong long-term growth potential supported by urbanization and food security priorities, sustainable competitive advantage will depend on balancing technological innovation, operational efficiency, energy sustainability, and scalable business models across increasingly complex urban agriculture environments.

Regulatory Landscape

Global Urban Farming Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Urban Farming Market is evolving rapidly as governments, municipalities, and international organizations increasingly prioritize food security, sustainable urban development, climate resilience, and resource-efficient agriculture systems. Urban farming technologies such as vertical farming, hydroponics, aquaponics, rooftop farming, and controlled environment agriculture (CEA) are becoming strategically important components of future smart city infrastructure and sustainable food ecosystems.

Governments worldwide are introducing policies and urban planning frameworks that support localized food production, green infrastructure integration, water conservation, and reduction of carbon emissions associated with traditional agricultural supply chains. Regulations related to land use, zoning, building codes, food safety, water recycling, and energy efficiency are significantly influencing the development and expansion of urban farming projects globally.

Environmental sustainability mandates and climate-focused agricultural policies are further accelerating investment in resource-efficient farming systems. Urban farming is increasingly recognized for its ability to reduce food transportation distances, optimize land utilization, minimize pesticide use, and improve urban environmental resilience.

At the same time, regulatory fragmentation across regions regarding indoor farming standards, renewable energy integration, wastewater reuse, and urban land utilization continues to create operational and compliance challenges for urban farming operators and technology providers. Companies are increasingly developing flexible, standards-compliant urban agriculture systems aligned with regional sustainability and food safety requirements.

Global Urban Farming Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by growing policy support for sustainable agriculture, smart city development, and climate-resilient food systems. North America remains a major innovation hub supported by urban agriculture grants, local food production initiatives, and investments in advanced indoor farming technologies.

Europe is strengthening its regulatory framework through sustainability-focused urban development programs, environmental compliance mandates, and green infrastructure policies. Initiatives under the European Green Deal and circular economy strategies are encouraging adoption of vertical farming, hydroponics, and energy-efficient food production systems.

Asia-Pacific is witnessing rapid regulatory expansion driven by urban population growth, food security concerns, and agricultural modernization programs. Countries such as Singapore, Japan, China, and South Korea are actively supporting urban farming through subsidies, smart farming policies, and investment incentives for controlled environment agriculture technologies.

Middle East & Africa nations are increasingly investing in urban farming technologies to address water scarcity, import dependency, and food security challenges. Governments in the UAE and Saudi Arabia are supporting indoor farming and hydroponic projects through sustainability initiatives and agricultural innovation programs.

Latin America is gradually adopting urban agriculture policies aimed at improving food accessibility, community farming participation, and sustainable urban development. Across all regions, policymakers are increasingly viewing urban farming as a strategic tool for enhancing food resilience and environmental sustainability.

Key Regulatory & Policy Environment Signals in Global Urban Farming Market

- Sustainable Agriculture & Climate Policies: Governments are promoting urban farming as part of broader sustainability and climate resilience strategies to reduce carbon emissions and improve local food systems.

- Urban Zoning & Infrastructure Regulations: Municipal zoning reforms and building regulations are increasingly enabling rooftop farms, vertical farms, and integrated agricultural infrastructure within urban environments.

- Food Safety & Traceability Standards: Regulations related to pesticide usage, indoor cultivation hygiene, and food traceability are shaping urban farming operational standards.

- Water Conservation & Recycling Policies: Water efficiency mandates and wastewater recycling frameworks are accelerating adoption of hydroponic and aquaponic systems.

- Renewable Energy & Energy Efficiency Standards: Policies encouraging renewable energy integration and energy-efficient farming technologies are influencing urban farming infrastructure investments.

- Smart City & Digital Agriculture Initiatives: Urban farming is increasingly integrated into smart city development plans supported by IoT, AI-driven monitoring, and digital resource management systems.

Strategic Implications of Regulatory & Policy Environment in Global Urban Farming Market

Regulatory developments are transforming the urban farming market from a niche agricultural segment into a strategically important component of urban sustainability and food security planning. Companies are increasingly required to align operations with environmental standards, food safety regulations, and energy efficiency requirements.

Policies supporting sustainable agriculture and climate adaptation are encouraging investments in controlled environment agriculture systems capable of minimizing water consumption, reducing land dependency, and lowering transportation-related emissions. This is accelerating demand for AI-driven monitoring systems, automated irrigation technologies, and resource-efficient farming infrastructure.

Urban zoning reforms and smart infrastructure initiatives are also creating new growth opportunities for rooftop farming, modular indoor farms, and mixed-use agricultural developments integrated within urban buildings and commercial spaces.

Water conservation regulations are increasing the strategic importance of hydroponics, aquaponics, and closed-loop irrigation systems. Companies capable of delivering water-efficient and energy-optimized farming technologies are expected to gain strong competitive advantages.

Meanwhile, increasing food traceability requirements and sustainability reporting standards are encouraging urban farming operators to adopt digital platforms for crop monitoring, supply chain transparency, and environmental performance tracking.

Global Urban Farming Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Urban Farming Market is expected to become increasingly sustainability-driven, technology-focused, and integrated with urban development policies. Governments are expected to strengthen support for localized food production systems as part of broader climate adaptation and food security strategies.

North America is expected to continue expanding urban agriculture incentives, sustainability grants, and smart farming investments focused on reducing food supply chain vulnerability and improving urban resilience. Europe will likely remain a global leader in sustainable food system regulation, circular agriculture initiatives, and energy-efficient farming standards.

Asia-Pacific is projected to witness significant policy expansion supporting vertical farming infrastructure, smart greenhouse systems, and AI-enabled urban agriculture technologies. Countries such as Singapore, Japan, and China are expected to remain major innovation centers for high-density urban farming solutions.

Regulations related to carbon neutrality, renewable energy integration, water efficiency, and food safety are expected to become stricter globally, increasing demand for compliant and environmentally optimized urban farming systems.

AI governance, IoT integration standards, and digital agriculture regulations are also expected to evolve rapidly, particularly around automated farm operations, resource optimization algorithms, and urban food traceability systems. This will further accelerate the adoption of intelligent and compliance-ready urban agriculture platforms.

Overall, the regulatory and policy landscape will play a critical role in shaping the future evolution of the Global Urban Farming Market. Companies that proactively align with sustainability mandates, smart city initiatives, and resource-efficient agricultural practices will be best positioned to lead the next generation of urban food production ecosystems.