Global Artificial Intelligence in Agriculture Market Size and Share Analysis 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

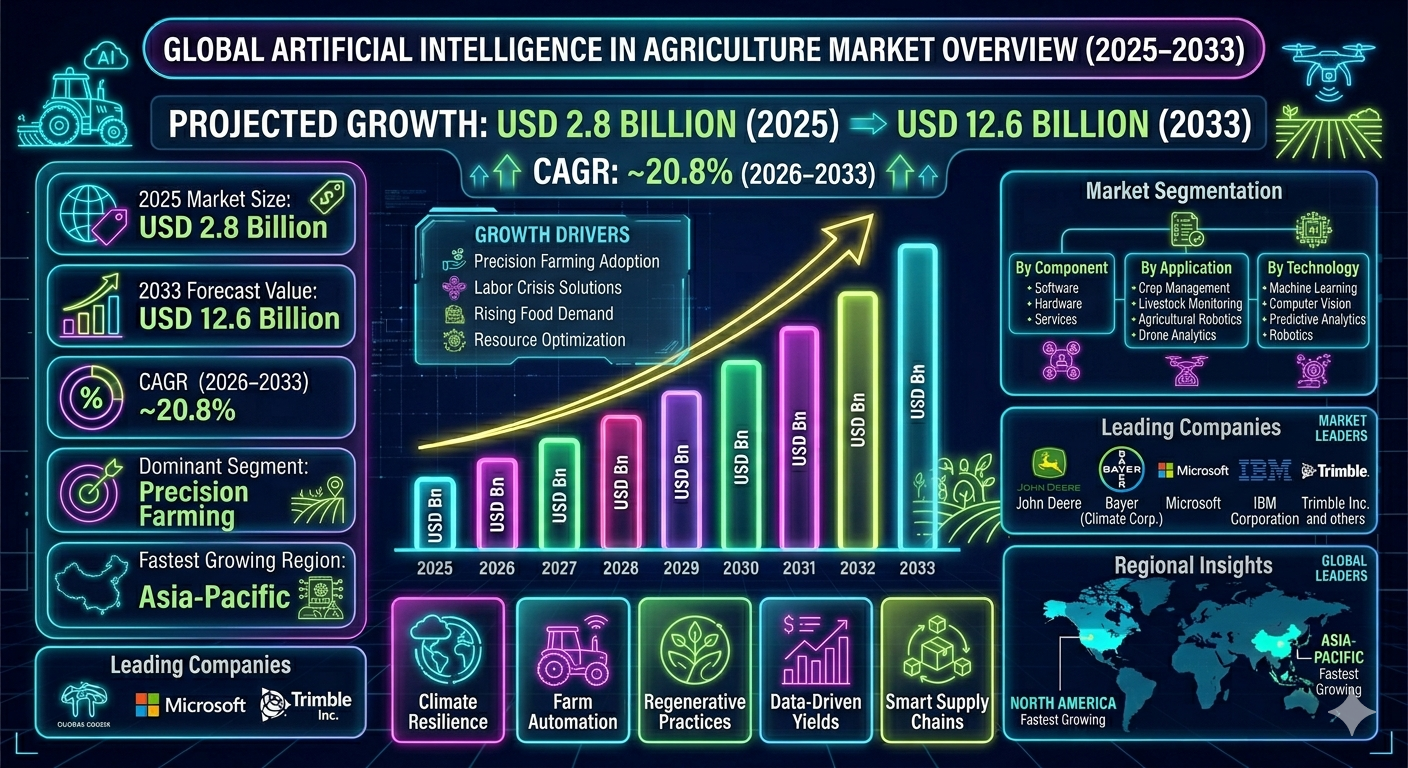

| Market Size (2025) | USD 2.8 Billion |

| Market Size (2033) | USD 12.6 Billion |

| CAGR (2026???2033) | 20.8% |

| Largest Segment | Precision Farming Solutions |

| Fastest Growing Segment | Agricultural Robotics and Autonomous Farming Systems |

| Leading End-Use Segment | Large Commercial Farms and Agribusiness Enterprises |

| Key Trend | Integration of AI with IoT, Drones, and Autonomous Smart Farming Platforms |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Primary Growth Driver | Rising Demand for Precision Agriculture and Resource Optimization Technologies |

Global Artificial Intelligence in Agriculture Market Size & Forecast

The global artificial intelligence (AI) in agriculture market is projected to witness strong and accelerated growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 2.8 billion in 2025 and is expected to reach nearly USD 12.6 billion by 2033, expanding at a CAGR of around 20.8%. This rapid growth is driven by increasing adoption of precision farming technologies, rising global food demand, labor shortages in agriculture, and the need for higher crop productivity with optimized resource utilization. The integration of AI technologies in agriculture is transforming traditional farming practices into data-driven, automated, and highly efficient systems. AI-powered solutions are being widely used for crop monitoring, soil analysis, predictive analytics, livestock management, weed detection, irrigation optimization, and supply chain forecasting. In addition, the increasing penetration of IoT-enabled sensors, drones, satellite imaging, and machine learning algorithms is enabling real-time decision-making for farmers. These technologies are improving yield quality, reducing operational costs, and minimizing environmental impact through efficient use of water, fertilizers, and pesticides. Government initiatives promoting smart agriculture, digital farming subsidies, and agritech investments are further accelerating market expansion globally. Venture capital funding in agritech startups is also rising, supporting innovation in AI-based agricultural platforms and farm automation systems.Global Artificial Intelligence in Agriculture Market Overview

The AI in agriculture market represents the integration of advanced computational technologies with traditional farming systems to improve productivity, sustainability, and profitability. It spans multiple applications including crop management, precision farming, livestock monitoring, agricultural robotics, and supply chain optimization. The market is characterized by rapid technological adoption and increasing collaboration between agritech companies, software developers, hardware manufacturers, and agricultural organizations. Leading technology providers are developing AI-driven platforms that combine machine learning, computer vision, and predictive analytics to support farmers in decision-making processes. Key industry participants include IBM Corporation, Microsoft, John Deere, Bayer AG (Climate Corporation), Trimble Inc., Deere & Company, AGCO Corporation, and emerging agritech startups specializing in AI-based farming solutions. These companies are focusing on integrated smart farming ecosystems that connect data collection, analysis, and automated execution systems. The shift toward digital agriculture is also being supported by increasing smartphone penetration in rural areas and improved internet connectivity, enabling farmers to access AI-based advisory services and mobile farming applications.Key Drivers of Global Artificial Intelligence in Agriculture Market Growth

Rising Global Food Demand

Increasing global population and changing dietary patterns are driving higher food demand. AI helps farmers improve crop yields, reduce losses, and optimize production efficiency to meet rising food requirements.Adoption of Precision Farming Techniques

Precision agriculture powered by AI enables farmers to monitor field variability and apply inputs such as water, fertilizers, and pesticides in a targeted manner, improving productivity and reducing waste.Labor Shortages in Agriculture

Many regions are experiencing declining agricultural labor availability. AI-driven automation, robotics, and smart machinery are helping bridge this gap by reducing dependence on manual labor.Climate Change and Resource Optimization

Unpredictable weather patterns and environmental challenges are increasing the need for intelligent farming systems. AI helps optimize irrigation, predict weather impacts, and improve climate resilience in agriculture.Advancements in IoT and Data Analytics

The integration of IoT sensors, drones, satellite imaging, and big data analytics is enhancing the accuracy of AI systems, enabling real-time monitoring and predictive insights for agricultural operations.Global Artificial Intelligence in Agriculture Market Segmentation

By Component

The market is segmented into software, hardware, and services. Software solutions dominate due to widespread use of AI platforms, analytics tools, and farm management systems. Hardware includes drones, sensors, robotics, and automated machinery.By Application

Applications include precision farming, crop monitoring, livestock monitoring, drone analytics, soil management, agricultural robotics, and supply chain management. Precision farming remains the largest segment due to high adoption rates globally.By Technology

The market includes machine learning, computer vision, predictive analytics, natural language processing, and robotics. Machine learning and computer vision are the most widely used technologies in modern agriculture systems.By Deployment Mode

Deployment is categorized into cloud-based and on-premise solutions. Cloud-based platforms dominate due to scalability, real-time data access, and lower infrastructure costs.By End User

End users include farmers, agribusiness companies, agricultural cooperatives, research institutions, and government agencies. Large agribusinesses and commercial farms are the leading adopters of AI technologies.Regional Market Dynamics

North America leads the global AI in agriculture market due to strong adoption of precision farming, advanced agritech infrastructure, and high investment in agricultural automation technologies in the United States and Canada. Europe is witnessing steady growth driven by sustainable farming initiatives, strict environmental regulations, and increasing adoption of smart agriculture practices across countries such as Germany, France, and the Netherlands. Asia-Pacific is the fastest-growing region, fueled by large agricultural economies such as China and India, rising food demand, government digital farming programs, and increasing agritech startup activity. Latin America is emerging as a key market due to expanding large-scale farming operations in Brazil and Argentina, along with growing adoption of precision agriculture technologies. Middle East & Africa is gradually adopting AI-based agricultural systems to address water scarcity, improve food security, and enhance farming efficiency in arid regions.Competitive Landscape

The global artificial intelligence in agriculture market is highly competitive and rapidly evolving, with a mix of established technology companies, agricultural equipment manufacturers, and innovative startups. Key players include IBM Corporation, Microsoft, John Deere, Bayer AG (Climate Corporation), Trimble Inc., AGCO Corporation, and Cisco Systems, along with numerous agritech startups. Companies are focusing on developing integrated smart farming ecosystems that combine AI, IoT, robotics, and data analytics. Strategic partnerships between technology providers and agricultural firms are increasing to enhance product capabilities and market reach. John Deere is leading in agricultural machinery automation with AI-enabled tractors and equipment, while Bayer???s Climate Corporation focuses on digital farming platforms and predictive analytics. Technology giants like Microsoft and IBM are providing cloud-based AI infrastructure for agricultural applications. Barriers to entry include high technology development costs, need for specialized agricultural data, and limited digital infrastructure in developing regions. However, rapid innovation is creating opportunities for new entrants in niche AI agricultural solutions.Strategic Outlook

The strategic outlook for the AI in agriculture market is highly positive, driven by the convergence of digital technology and sustainable farming needs. The future of agriculture will increasingly depend on autonomous farming systems, AI-driven decision-making platforms, and real-time data analytics. Growth opportunities lie in expanding AI applications in climate-smart agriculture, regenerative farming practices, and supply chain optimization. Integration of AI with robotics and autonomous machinery is expected to significantly transform large-scale farming operations. Increased government support, venture capital investment, and public-private partnerships will further accelerate innovation in agritech ecosystems. Companies that combine AI capabilities with practical agricultural solutions will gain a strong competitive advantage.Final Market Perspective

The global artificial intelligence in agriculture market is entering a transformative phase, reshaping traditional farming into a highly efficient, data-driven, and sustainable industry. AI is playing a critical role in addressing global food security challenges, improving productivity, and reducing environmental impact. As technology adoption accelerates, the market will continue to evolve toward fully automated and intelligent farming systems. Companies investing in integrated AI platforms, precision agriculture tools, and smart farming ecosystems are expected to lead the next wave of agricultural innovation.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Artificial Intelligence in Agriculture Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Digital Farming Transformation

- 2.4 Agritech Ecosystem & Value Chain Structure

- 2.5 Impact of Precision Farming Adoption

- 2.6 Sustainability & Climate-Smart Agriculture Trends

- 2.7 Technology & Innovation Landscape (AI, IoT, Robotics)

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Global Food Demand

- 4.1.2 Adoption of Precision Farming Techniques

- 4.1.3 Labor Shortages in Agriculture

- 4.1.4 Climate Change & Resource Optimization

- 4.1.5 Advancements in IoT & Data Analytics

- 4.2 Restraints

- 4.2.1 High Implementation & Technology Costs

- 4.2.2 Limited Digital Infrastructure in Rural Areas

- 4.2.3 Data Privacy & Ownership Concerns

- 4.2.4 Lack of Technical Awareness Among Farmers

- 4.3 Opportunities

- 4.3.1 Expansion of Smart Farming Ecosystems

- 4.3.2 Growth of Agritech Startups & Innovation

- 4.3.3 AI in Climate-Smart Agriculture

- 4.3.4 Autonomous Farming & Robotics Integration

- 4.4 Challenges

- 4.4.1 Integration Complexity of AI Systems

- 4.4.2 Fragmented Agricultural Data Sources

- 4.4.3 High Dependency on Connectivity

- 4.4.4 Resistance to Technological Adoption

- 4.1 Drivers

- 5. Artificial Intelligence in Agriculture Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Technology Adoption Trends

- 5.6 Agricultural Productivity Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Component

- 6.1.1 Software Solutions

- 6.1.2 Hardware (Sensors, Drones, Robotics)

- 6.1.3 Services (Consulting & Integration)

- 6.2 By Application

- 6.2.1 Precision Farming

- 6.2.2 Crop Monitoring

- 6.2.3 Livestock Monitoring

- 6.2.4 Drone & Satellite Analytics

- 6.2.5 Soil Management

- 6.2.6 Agricultural Robotics

- 6.2.7 Supply Chain Optimization

- 6.3 By Technology

- 6.3.1 Machine Learning

- 6.3.2 Computer Vision

- 6.3.3 Predictive Analytics

- 6.3.4 Natural Language Processing

- 6.3.5 Robotics & Automation

- 6.4 By Deployment Mode

- 6.4.1 Cloud-Based Solutions

- 6.4.2 On-Premise Solutions

- 6.5 By End User

- 6.5.1 Farmers & Individual Growers

- 6.5.2 Agribusiness Companies

- 6.5.3 Agricultural Cooperatives

- 6.5.4 Research Institutions

- 6.5.5 Government Agencies

- 6.1 By Component

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Technology Integration Mapping

- 8.4 Strategic Partnerships & Collaborations

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Smart Farming Infrastructure Analyzer

- 10.3 AI & Agritech Innovation Tracker

- 10.4 Precision Agriculture Adoption Insights

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Autonomous Farming Expansion

- 11.2 AI-Driven Crop Optimization Systems

- 11.3 Robotics & Farm Automation Growth

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Artificial Intelligence in Agriculture Market Competitive Intensity & Market Structure Overview

The Global Artificial Intelligence in Agriculture Market is characterized by a rapidly evolving, technology-intensive competitive ecosystem where agritech startups, industrial machinery leaders, and global technology giants are converging. The market is transitioning from traditional precision farming solutions to fully integrated AI-powered agricultural ecosystems combining machine learning, robotics, IoT, and predictive analytics.

Competitive intensity is high and accelerating due to strong innovation cycles, rising venture capital inflows, and increasing demand for scalable smart farming solutions. Companies compete on algorithm accuracy, platform integration, hardware-software interoperability, scalability across farm sizes, and real-time decision-making capabilities.

The market structure is moderately consolidated at the top layer, dominated by global technology firms and agricultural machinery leaders, while the mid and lower tiers remain fragmented with numerous agritech startups offering niche AI solutions such as crop imaging, soil intelligence, and farm automation tools.

Global Artificial Intelligence in Agriculture Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

John Deere: Global leader in AI-enabled agricultural machinery. Strong focus on autonomous tractors, smart equipment, and precision farming systems integrated with real-time field intelligence.

Bayer AG (Climate Corporation): Major digital agriculture player offering predictive analytics platforms, climate modeling tools, and data-driven crop management solutions.

IBM Corporation: Leading provider of AI and cloud infrastructure for agriculture, specializing in predictive analytics, weather intelligence, and farm data platforms.

Microsoft Corporation: Key enabler of cloud-based agricultural AI systems through Azure, supporting smart farming applications, IoT integration, and data-driven decision platforms.

Trimble Inc.: Focused on precision agriculture technologies, GPS-based farm management systems, and AI-driven field optimization tools.

AGCO Corporation: Agricultural machinery company integrating AI and automation into smart farming equipment and connected farm ecosystems.

Granular (Corteva Agriscience): Digital farm management platform specializing in operational planning, analytics, and farm profitability optimization.

CropX Technologies: Agritech innovator focused on soil intelligence, irrigation optimization, and sensor-based farm analytics.

John Deere Precision Ag Division: Advanced AI-driven farming solutions integrating robotics, autonomous machines, and predictive field insights.

FarmWise: Emerging robotics company specializing in AI-powered weeding and autonomous field management systems.

Key Competitive Intensity & Market Structure Signals in Global Artificial Intelligence in Agriculture Market

A major competitive signal is the shift toward fully integrated digital farming ecosystems. Companies are no longer competing on standalone tools but on end-to-end platforms combining hardware, software, data analytics, and automation.

Another key trend is the increasing dominance of machine learning and computer vision technologies in crop monitoring, disease detection, and yield prediction. Firms with superior data models and agricultural datasets are gaining significant competitive advantage.

The rise of autonomous farming equipment is reshaping competition in agricultural machinery, with companies racing to develop self-driving tractors, robotic harvesters, and AI-powered spraying systems.

Strategic partnerships between technology companies and agribusiness firms are intensifying, enabling faster commercialization of AI solutions and expanding market reach across developed and emerging economies.

Data ownership and platform ecosystems are becoming critical competitive assets, as companies that control large-scale agricultural datasets strengthen their long-term AI model accuracy and market positioning.

Strategic Implications of Competitive Intensity & Market Structure in Global Artificial Intelligence in Agriculture Market

The market is shifting from product-based competition to ecosystem-based competition, where companies integrate software platforms, smart hardware, and cloud analytics into unified agricultural solutions.

Investment in AI model development, satellite imaging integration, drone analytics, and real-time farm monitoring systems is becoming essential for maintaining competitiveness.

Scalability across farm sizes???from smallholder farms to large commercial agribusinesses???is emerging as a key differentiator in global adoption.

Government-backed digital agriculture initiatives and subsidies are accelerating adoption in emerging markets, influencing competitive positioning of global and regional players.

The integration of AI with robotics and autonomous machinery is creating new competitive frontiers, especially in large-scale commercial farming operations.

Global Artificial Intelligence in Agriculture Market Competitive Intensity & Market Structure Forward Outlook

The Global Artificial Intelligence in Agriculture Market is expected to witness increasing consolidation among major technology providers, agricultural machinery companies, and leading agritech platforms.

Platform-based business models will dominate the future landscape, where companies offer integrated AI ecosystems combining analytics, automation, and decision-support systems.

Expansion of autonomous farming technologies will significantly intensify competition, particularly in large-scale agriculture markets such as North America, Europe, and Asia-Pacific.

Data-driven agriculture will become the core competitive foundation, with companies investing heavily in AI training datasets, predictive models, and real-time environmental intelligence systems.

In the long term, the market will be defined by three core pillars: AI-driven automation, integrated digital agriculture platforms, and scalable precision farming ecosystems. Companies that successfully combine hardware innovation, AI intelligence, and cloud-based agricultural platforms will lead the Global Artificial Intelligence in Agriculture Market through 2033.

Value Chain

Global Artificial Intelligence in Agriculture Market Value Chain & Supply Chain Evolution Overview

The Global Artificial Intelligence in Agriculture Market value chain is rapidly evolving from traditional farming support systems into a fully digital, data-driven, and autonomous agricultural ecosystem. This transformation is being driven by rising global food demand, labor shortages, climate variability, precision farming adoption, and the increasing integration of IoT, robotics, and AI-powered analytics across agricultural operations.

AI in agriculture integrates machine learning, computer vision, predictive analytics, drones, satellite imaging, and smart sensors to optimize farming decisions across crop production, soil management, irrigation, livestock monitoring, and supply chain forecasting. The ecosystem is shifting agriculture from reactive farming practices to predictive and automated decision-making systems.

The value chain extends across hardware manufacturing (sensors, drones, robotics), AI software platforms, cloud infrastructure providers, agricultural data analytics companies, agritech startups, and traditional agricultural equipment manufacturers. Leading companies such as John Deere, IBM Corporation, Microsoft, Bayer AG (Climate Corporation), Trimble Inc., and AGCO Corporation are actively shaping the smart farming ecosystem through integrated digital agriculture solutions.

Upstream supply chain components include IoT sensor manufacturers, semiconductor providers, drone hardware producers, satellite imaging systems, and agricultural robotics developers. These inputs are essential for generating high-quality real-time agricultural data used by AI systems.

Midstream components focus on AI software development, cloud computing platforms, data analytics engines, and machine learning models that process agricultural data to deliver actionable insights. These platforms enable predictive farming, yield optimization, pest detection, and climate-adaptive decision-making.

Downstream applications include precision farming operations, farm management systems, livestock monitoring, autonomous machinery execution, and agricultural supply chain optimization platforms. End users include farmers, agribusiness companies, cooperatives, research institutes, and government agricultural bodies.

Key challenges in the value chain include fragmented farm data systems, limited rural digital infrastructure, high implementation costs, data interoperability issues, and cybersecurity risks associated with connected agricultural ecosystems.

Global Artificial Intelligence in Agriculture Market Value Chain & Supply Chain Evolution Current Scenario

The current AI in agriculture ecosystem is characterized by rapid digital adoption, increasing deployment of precision farming technologies, and growing integration of AI with IoT-enabled agricultural devices and smart machinery.

Hardware manufacturers are expanding production of drones, smart sensors, automated tractors, and robotic harvesting systems to support real-time data collection and field automation. These technologies are becoming essential for large-scale commercial farming operations.

Software and cloud providers are strengthening AI platforms that enable predictive analytics, crop health monitoring, soil analysis, and yield forecasting. These systems are increasingly being deployed through cloud-based models for scalability and real-time accessibility.

Agritech companies are forming strategic partnerships with traditional agricultural equipment manufacturers to integrate AI capabilities into existing farming machinery, enabling semi-autonomous and fully autonomous agricultural operations.

Government initiatives supporting digital agriculture, precision farming subsidies, and smart farming infrastructure development are significantly accelerating adoption in both developed and emerging economies.

AI-driven decision-support systems are increasingly being used by farmers to optimize irrigation, fertilizer usage, pest control, and harvesting schedules, improving productivity while reducing environmental impact.

Key Value Chain & Supply Chain Evolution Signals in Global Artificial Intelligence in Agriculture Market

Several transformative trends are reshaping the AI in agriculture value chain globally.

First, precision farming adoption is accelerating demand for AI-powered field monitoring systems, enabling targeted application of agricultural inputs and improving crop yields.

Second, increasing deployment of drones, satellite imaging, and computer vision systems is enhancing real-time crop monitoring and early disease detection capabilities.

Third, labor shortages in agriculture are driving automation through AI-enabled robotics and autonomous farming machinery, reducing reliance on manual labor.

Fourth, climate variability and extreme weather conditions are increasing the use of predictive analytics for crop planning, irrigation optimization, and risk mitigation strategies.

Fifth, integration of IoT-enabled agricultural sensors with AI platforms is enabling continuous data collection and real-time decision-making across farm operations.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Artificial Intelligence in Agriculture Market

Industry leaders such as John Deere, Bayer AG (Climate Corporation), IBM Corporation, Microsoft, Trimble Inc., and AGCO Corporation are strengthening their competitive positioning by integrating AI, IoT, robotics, and cloud-based analytics into end-to-end smart farming ecosystems.

Competitive advantage in this market increasingly depends on AI model accuracy, real-time data processing capability, scalability of digital farming platforms, integration with agricultural machinery, and ability to deliver actionable insights at the farm level.

Companies that successfully combine agricultural expertise with advanced AI technologies are better positioned to lead in precision farming, autonomous agriculture, and digital farm management solutions.

Strategic partnerships between technology providers, agritech startups, and agricultural equipment manufacturers are becoming essential for ecosystem expansion and innovation acceleration.

Long-term success will depend on improving data accessibility in rural regions, reducing deployment costs, enhancing interoperability across platforms, and ensuring cybersecurity across connected agricultural systems.

Global Artificial Intelligence in Agriculture Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the AI in agriculture value chain is expected to become increasingly autonomous, predictive, and fully integrated with digital farming ecosystems.

AI-powered precision agriculture platforms will evolve toward fully autonomous farm management systems capable of real-time decision-making across planting, irrigation, fertilization, and harvesting operations.

Integration of edge computing, 5G connectivity, and satellite-based monitoring systems will significantly enhance real-time agricultural intelligence capabilities.

Digital twin technology is expected to play a major role in simulating crop growth patterns, optimizing resource allocation, and improving yield forecasting accuracy.

Autonomous agricultural robotics and AI-driven machinery will continue expanding across large-scale commercial farming operations, reducing labor dependency and improving operational efficiency.

Ultimately, the future value chain will shift agriculture from manual and reactive systems into fully intelligent, data-driven, and autonomous farming ecosystems.

Market-Specific Value Chain

- Data Acquisition & Field Sensing: IoT sensors, drones, satellite imaging, soil monitoring systems, weather stations, agricultural robots

- Data Infrastructure & Connectivity: Cloud platforms, edge computing systems, 5G networks, agricultural data lakes, connectivity solutions

- AI & Analytics Engine Development: Machine learning models, computer vision systems, predictive analytics platforms, crop intelligence algorithms

- Smart Agriculture Platform Integration: Farm management systems, precision agriculture platforms, livestock monitoring systems, decision-support tools

- Automation & Field Execution Systems: Autonomous tractors, robotic harvesters, automated irrigation systems, drone-based spraying systems

- End-User Applications & Optimization: Yield optimization, supply chain forecasting, crop health monitoring, resource efficiency management, sustainability tracking

Company-to-Stage Mapping

- Data Acquisition & Field Sensing: John Deere, Trimble Inc., DJI Agriculture, AGCO Corporation

- Data Infrastructure & Connectivity: Microsoft, IBM Corporation, Cisco Systems, Amazon Web Services (AWS)

- AI & Analytics Engine Development: IBM Corporation, Microsoft, Bayer AG (Climate Corporation), agritech startups

- Smart Agriculture Platform Integration: Bayer AG, John Deere, Trimble Inc., AGCO Corporation

- Automation & Field Execution Systems: John Deere, AGCO Corporation, Kubota Corporation, CNH Industrial

- End-User Applications & Optimization: Agribusiness firms, farming cooperatives, government agriculture departments, large-scale commercial farms

Investment Activity

Global Artificial Intelligence in Agriculture Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Artificial Intelligence (AI) in Agriculture Market are being driven by the urgent need to improve global food security, rising adoption of precision farming technologies, and increasing demand for automation in agriculture due to labor shortages and climate variability. Between 2026 and 2033, capital inflows are expected to accelerate significantly across agritech startups, AI software platforms, agricultural robotics companies, and data-driven farm management solution providers.

The market is witnessing strong participation from venture capital firms, private equity investors, technology conglomerates, and government-backed agricultural modernization programs. Major investments are focused on AI-powered precision farming systems, autonomous machinery, predictive crop analytics, and integrated farm management platforms that combine IoT, satellite imaging, and machine learning technologies.

A key structural shift shaping investment flows is the transition from traditional farming models to fully digitized and AI-enabled agricultural ecosystems. This is driving funding into smart farming infrastructure, cloud-based agricultural platforms, robotics integration, and real-time data analytics systems that optimize yield and resource utilization.

Global Artificial Intelligence in Agriculture Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by rising agritech adoption, increasing food demand pressures, and government initiatives promoting smart agriculture and digital farming ecosystems. Venture capital funding in agritech startups has significantly increased, particularly in AI-driven crop monitoring, autonomous machinery, and predictive agricultural analytics platforms.

- North America: Leads global investment due to advanced agritech infrastructure, strong VC ecosystem, and high adoption of precision farming technologies in the United States and Canada.

- Europe: Focused on sustainable agriculture investments, climate-smart farming solutions, and AI-based environmental monitoring systems driven by strict regulatory frameworks.

- Asia-Pacific: Fastest-growing investment region supported by large agricultural economies, government digital farming programs, and rapid agritech startup expansion in China and India.

- Latin America: Expanding investments in large-scale precision farming, especially in Brazil and Argentina, driven by commercial agriculture modernization.

- Middle East & Africa: Emerging investment region focusing on AI-enabled irrigation systems, water optimization technologies, and food security enhancement programs.

Key Investment & Funding Dynamics Signals in Global Artificial Intelligence in Agriculture Market

- Rising global food demand is driving strong capital inflows into AI-powered precision farming and yield optimization technologies.

- Labor shortages in agriculture are accelerating investments in autonomous machinery, agricultural robotics, and AI-driven automation systems.

- Climate change and resource scarcity are pushing funding toward predictive analytics, weather modeling, and smart irrigation systems.

- Integration of IoT, drones, and satellite imaging with AI platforms is attracting significant investment in real-time agricultural monitoring solutions.

- Rapid growth of agritech startups is fueling venture capital activity in niche AI applications such as soil intelligence, pest detection, and livestock monitoring.

- Government subsidies and digital agriculture programs are strengthening public-sector investments in smart farming infrastructure.

Strategic Implications of Investment & Funding Dynamics in Global Artificial Intelligence in Agriculture Market

- The investment landscape strongly favors technology-first agritech companies offering integrated AI, IoT, and data analytics platforms for end-to-end farm management.

- Strategic convergence of hardware and software is becoming essential, with AI integrated into drones, tractors, sensors, and autonomous farming equipment.

- Data ownership and agricultural intelligence platforms are emerging as key value drivers, influencing long-term competitive positioning.

- Partnerships between technology giants and agricultural enterprises are accelerating commercialization of AI-driven farming solutions.

- Scalability and cloud-based deployment models are becoming critical investment criteria for agritech funding decisions.

- Emerging markets are offering high-growth investment opportunities due to under-penetration of digital agriculture technologies.

Global Artificial Intelligence in Agriculture Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Artificial Intelligence in Agriculture Market is expected to witness sustained and high-growth investment momentum, driven by increasing global food demand, digital transformation of agriculture, and the shift toward climate-resilient farming systems.

Future capital allocation will increasingly focus on fully autonomous farming systems, AI-powered predictive agriculture platforms, robotics integration, and advanced decision-support systems that enable real-time farm optimization and resource efficiency.

- North America: Will continue leading investments in AI-driven precision agriculture, autonomous machinery, and digital farming platforms.

- Asia-Pacific: Will remain the fastest-growing investment hub due to large-scale agricultural modernization and strong government support for agritech innovation.

- Europe: Will focus on sustainable, climate-smart agriculture and regulatory-compliant AI farming systems.

- Emerging Regions: Latin America and MEA will see increasing investments in smart irrigation, crop intelligence, and food security-driven agricultural technologies.

Digital transformation will be the central force shaping future investment patterns, with AI, machine learning, and IoT convergence enabling fully connected and autonomous agricultural ecosystems.

Overall, the market will continue its strong expansion trajectory as agriculture transitions into a data-driven, automated, and sustainability-focused industry. Companies that integrate AI with scalable agricultural applications and real-world farming systems will dominate the Global Artificial Intelligence in Agriculture Market through 2033.

Technology & Innovation

Global Artificial Intelligence in Agriculture Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Artificial Intelligence (AI) in Agriculture Market is rapidly transforming traditional farming into a fully data-driven, automated, and predictive ecosystem. Innovation is centered around integrating AI with IoT, robotics, satellite imaging, drones, and big data analytics to enable precision agriculture and intelligent farm management systems.

AI technologies are increasingly being embedded across the agricultural value chain, from soil preparation and crop planning to harvesting, logistics, and supply chain optimization. Machine learning algorithms, computer vision systems, and predictive analytics are enabling farmers to make real-time, data-backed decisions that significantly improve yield efficiency and resource utilization.

A major innovation shift is the rise of precision agriculture platforms powered by AI, which analyze field variability and optimize inputs such as water, fertilizers, and pesticides. These systems are reducing environmental impact while increasing crop productivity and profitability for farmers.

The integration of autonomous machinery and agricultural robotics is another key technological advancement. AI-powered tractors, harvesters, and robotic weed control systems are reducing dependency on manual labor while improving operational efficiency at scale.

Additionally, AI-driven remote sensing technologies using drones and satellite imagery are enabling continuous crop monitoring, early disease detection, and yield prediction. These systems are particularly valuable for large-scale commercial farming operations.

Global Artificial Intelligence in Agriculture Market Technology & Innovation Landscape Current Scenario

Currently, the AI in agriculture industry is in a high-growth adoption phase, where digital transformation is accelerating across both developed and emerging agricultural economies. Large agribusinesses are leading adoption, while small and medium farmers are gradually integrating AI-based advisory tools through mobile platforms.

Machine learning and computer vision are the most widely deployed technologies, enabling applications such as crop health monitoring, weed detection, pest identification, and automated yield estimation. These technologies are significantly improving decision-making accuracy and reducing crop losses.

IoT-enabled smart farming systems are widely used to collect real-time data from fields, including soil moisture, temperature, humidity, and nutrient levels. This data is processed using AI models to optimize irrigation schedules and fertilizer application.

Cloud-based AI platforms are becoming the dominant deployment model due to their scalability, cost efficiency, and ability to integrate large datasets from multiple farm sources. These platforms allow farmers and agribusinesses to access real-time insights from any location.

Agricultural drones equipped with AI-based imaging systems are increasingly being used for crop spraying, field mapping, and vegetation analysis. These systems improve accuracy while reducing operational costs and chemical usage.

Livestock monitoring systems powered by AI are also gaining traction, enabling real-time tracking of animal health, behavior, feeding patterns, and disease detection through wearable sensors and computer vision tools.

Key Technology & Innovation Trends in Global Artificial Intelligence in Agriculture Market

- AI-Powered Precision Farming: Real-time optimization of water, fertilizer, and pesticide usage based on field variability analysis.

- Autonomous Agricultural Machinery: AI-driven tractors, harvesters, and robotic systems reducing labor dependency and increasing efficiency.

- Drone & Satellite-Based Crop Monitoring: High-resolution imaging and AI analytics for crop health assessment and yield prediction.

- Machine Learning in Crop Forecasting: Predictive models analyzing weather, soil, and historical data to optimize planting and harvesting cycles.

- Computer Vision for Pest & Disease Detection: Automated identification of crop diseases and pests through image recognition systems.

- IoT-Enabled Smart Farming Systems: Sensor-based real-time monitoring of soil, weather, and crop conditions.

- AI-Driven Livestock Management: Wearable sensors and analytics for animal health monitoring and productivity optimization.

- Cloud-Based Agricultural Platforms: Centralized AI systems enabling scalable farm management and data integration.

Strategic Implications of Technology & Innovation

Technological innovation in the AI in agriculture market is fundamentally reshaping global food production systems by improving efficiency, reducing waste, and enhancing sustainability. The transition from traditional farming to intelligent agriculture is enabling higher productivity with lower environmental impact.

For agribusinesses, AI adoption is becoming a critical competitive factor. Companies leveraging integrated digital farming ecosystems combining AI, IoT, robotics, and analytics are achieving significant advantages in yield optimization and cost reduction.

The growing integration of AI with climate-smart agriculture is also helping farmers adapt to climate variability by enabling predictive weather modeling, adaptive irrigation systems, and resilient crop planning strategies.

However, high implementation costs, lack of digital infrastructure in rural regions, and limited technical expertise among small farmers remain key challenges restricting widespread adoption.

Global Artificial Intelligence in Agriculture Market Technology & Innovation Forward Outlook

Looking ahead, the AI in agriculture market is expected to evolve toward fully autonomous farming ecosystems where AI systems manage end-to-end agricultural operations with minimal human intervention. Autonomous tractors, robotic harvesters, and AI-controlled irrigation systems will become increasingly common.

The convergence of AI, 5G connectivity, and edge computing will significantly enhance real-time decision-making capabilities in agriculture, enabling faster data processing directly at the farm level.

Advanced predictive analytics will play a key role in global food supply chain optimization, helping reduce post-harvest losses and improve distribution efficiency across regions.

Digital twin technology for agriculture is also expected to emerge, enabling virtual modeling of farms to simulate crop performance, resource usage, and environmental impact before real-world implementation.

In conclusion, the Global Artificial Intelligence in Agriculture Market is undergoing a major technological revolution, transitioning agriculture into a smart, autonomous, and highly efficient industry. Companies that integrate AI-driven platforms with practical farming solutions, robotics, and real-time analytics will lead the future of global agricultural innovation.

Market Risk

Global Artificial Intelligence in Agriculture Market Risk Factors & Disruption Threats Overview

The Global Artificial Intelligence (AI) in Agriculture Market is undergoing rapid expansion as farming systems transition toward data-driven, automated, and precision-based operations. Despite strong growth momentum, the market carries a moderate-to-high technology adoption risk profile due to data dependency, infrastructure limitations in rural regions, cybersecurity exposure, high implementation costs, and uneven digital readiness across global agricultural economies.

One of the primary risk factors is limited digital infrastructure in agricultural regions, particularly in developing economies. Inadequate internet connectivity, low sensor penetration, and insufficient cloud adoption can restrict AI deployment scalability and reduce real-time decision-making efficiency.

Another major disruption factor is high initial investment and operational complexity. AI-based agricultural systems require significant capital expenditure for drones, IoT sensors, robotics, and software platforms, making adoption challenging for small and medium-scale farmers.

Additionally, data quality and availability constraints pose a critical challenge. AI models depend on accurate, large-scale agricultural datasets, but fragmented farm records, inconsistent data collection, and lack of standardized systems reduce predictive accuracy and system reliability.

Cybersecurity risks and data privacy concerns are also emerging as key issues, as connected agricultural systems become increasingly vulnerable to hacking, data breaches, and unauthorized access to sensitive farm and supply chain information.

Global Artificial Intelligence in Agriculture Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong adoption of AI-powered precision farming, crop monitoring systems, and predictive analytics platforms, particularly in large commercial farms and developed agricultural economies.

However, adoption remains uneven globally, with large agribusinesses leading deployment while smallholder farmers face barriers due to cost, technical expertise, and infrastructure limitations.

Integration challenges between AI systems and legacy agricultural equipment continue to slow full-scale digital transformation, particularly in regions with traditional farming practices and limited mechanization.

At the same time, increasing dependence on cloud-based platforms and third-party agritech providers is creating vendor lock-in risks, limiting flexibility and increasing long-term operational dependency on specific technology ecosystems.

Regulatory uncertainty surrounding agricultural data ownership, cross-border data sharing, and digital farming standards is also influencing deployment strategies across different regions.

Key Risk Factors & Disruption Threats Signals in Global Artificial Intelligence in Agriculture Market

A major disruption signal is the widening digital divide between large-scale commercial farms and smallholder agricultural producers, which may lead to unequal productivity gains and fragmented market adoption patterns.

Rising concerns around data sovereignty and agricultural data ownership are emerging as governments consider stricter regulations on how farm data is collected, stored, and utilized by AI platforms.

Dependence on high-quality real-time data inputs from IoT devices and satellite systems is another key risk signal, as system inaccuracies or sensor failures can significantly impact AI-driven agricultural decisions.

Rapid technological evolution in autonomous farming equipment and robotics is also disrupting traditional farming models, creating uncertainty around labor displacement and workforce transition in agriculture sectors.

Additionally, increasing climate variability is challenging the reliability of historical datasets used for AI training models, potentially reducing predictive accuracy in extreme weather conditions.

Strategic Implications of Risk Factors & Disruption Threats in Global Artificial Intelligence in Agriculture Market

Market participants must focus on building scalable, low-cost AI solutions tailored for small and medium-scale farmers to bridge the global adoption gap and expand addressable market reach.

Investment in robust data infrastructure, including standardized agricultural data platforms and interoperable IoT ecosystems, will be critical to improving model accuracy and system reliability.

Companies should strengthen cybersecurity frameworks and data protection mechanisms to safeguard agricultural intelligence systems and maintain trust across digital farming networks.

Strategic partnerships between agritech firms, governments, and telecom providers will be essential to expand rural connectivity and support large-scale deployment of AI-enabled farming systems.

Development of hybrid AI models combining satellite imagery, edge computing, and localized farm data will play a key role in improving adaptability across diverse agricultural environments.

Global Artificial Intelligence in Agriculture Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the AI in Agriculture Market is expected to experience rapid technological expansion, but adoption challenges related to infrastructure, affordability, and data governance will continue to influence growth patterns.

AI-driven autonomous farming systems, robotics integration, and predictive agricultural analytics are expected to become mainstream in large-scale commercial farming operations, significantly improving productivity and resource efficiency.

However, widespread adoption among smallholder farmers will depend heavily on cost reduction, government subsidies, and simplified AI platforms designed for low-tech environments.

Emerging regulations on agricultural data ownership and AI governance will play a critical role in shaping market structure and competitive dynamics over the forecast period.

Overall, the market???s future will be defined by its ability to balance technological innovation with accessibility, ensuring that AI-driven agriculture contributes effectively to global food security, climate resilience, and sustainable farming transformation.

Regulatory Landscape

Global Artificial Intelligence in Agriculture Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Artificial Intelligence in Agriculture Market is evolving rapidly as governments balance agricultural innovation with food safety, data governance, rural digitalization, and sustainable farming objectives. AI-driven agriculture operates at the intersection of agricultural policy, data privacy regulation, digital infrastructure laws, and environmental sustainability frameworks.

Regulatory authorities such as the U.S. Department of Agriculture (USDA), European Commission (CAP policies), Food and Agriculture Organization (FAO), and national digital governance bodies are actively shaping guidelines for the deployment of AI, IoT, and autonomous systems in farming. These regulations focus on ensuring safe use of AI-driven decision systems, protecting farmer data, and promoting transparent algorithmic use in food production systems.

Data governance and cybersecurity regulations are becoming increasingly important as agricultural systems become more connected through IoT sensors, drones, satellite imaging, and cloud-based farm management platforms. Policies such as GDPR in Europe and emerging agricultural data frameworks in other regions are influencing how agricultural data is collected, stored, and utilized.

At the same time, governments are strongly promoting digital agriculture through subsidies, smart farming initiatives, and agritech funding programs. These policies aim to increase productivity, improve food security, and reduce environmental impact through precision farming and AI-enabled resource optimization systems.

Global Artificial Intelligence in Agriculture Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by strong government support for digital transformation in agriculture, alongside emerging frameworks for AI governance and data protection. North America, particularly the United States, is leading in agritech innovation with supportive USDA programs, precision agriculture subsidies, and strong private sector investment in AI-based farming technologies.

In Europe, the Common Agricultural Policy (CAP) and Green Deal initiatives are driving adoption of sustainable and AI-enabled farming systems. Regulatory focus is centered on environmental sustainability, carbon reduction in agriculture, and responsible use of digital farming technologies.

Asia-Pacific is witnessing rapid policy-driven adoption of AI in agriculture, especially in China and India, where governments are investing heavily in smart farming infrastructure, rural digital connectivity, and AI-based crop monitoring systems to ensure food security for large populations.

Latin America is increasingly adopting digital agriculture policies to enhance large-scale farming efficiency, particularly in Brazil and Argentina, where export-oriented agriculture is a key economic driver. Governments are supporting precision farming and AI-based yield optimization technologies.

The Middle East & Africa region is focusing on AI adoption in agriculture to address water scarcity, desert farming challenges, and food import dependency. Governments are supporting controlled environment agriculture and AI-based irrigation optimization systems.

Across all regions, regulatory frameworks are still in early development stages for AI governance in agriculture, creating a dynamic environment where innovation is advancing faster than policy standardization.

Key Regulatory & Policy Environment Signals in Global Artificial Intelligence in Agriculture Market

- Agricultural Data Privacy & Governance Laws: Regulations are emerging to control how farm-level data from IoT devices, satellites, and AI platforms is collected, stored, and shared.

- Digital Agriculture Subsidy Programs: Governments are funding smart farming adoption through subsidies for precision agriculture tools, sensors, and AI platforms.

- AI Ethics & Algorithm Transparency Policies: Guidelines are being developed to ensure explainability and fairness in AI-based agricultural decision-making systems.

- Sustainable Farming & Climate-Smart Agriculture Regulations: Policies promoting water efficiency, reduced chemical usage, and carbon-neutral farming are driving AI adoption.

- Rural Digital Infrastructure Development: Expansion of broadband, 5G, and IoT connectivity in rural areas is enabling large-scale deployment of AI farming systems.

- Food Security & Agricultural Productivity Mandates: Governments are encouraging AI-based solutions to increase yield efficiency and reduce post-harvest losses.

Strategic Implications of Regulatory & Policy Environment in Global Artificial Intelligence in Agriculture Market

Regulatory support for digital agriculture is accelerating the adoption of AI-powered farming systems, enabling faster commercialization of precision agriculture technologies and smart farming platforms. Government subsidies and funding programs are reducing barriers to entry for agritech adoption among small and medium-scale farmers.

Data governance regulations are shaping the architecture of AI agricultural platforms, encouraging companies to develop secure, transparent, and compliant data ecosystems. This is increasing demand for cloud-based agricultural analytics platforms with strong cybersecurity and data protection features.

Environmental and sustainability policies are driving AI integration into climate-smart agriculture practices, including optimized irrigation, fertilizer usage reduction, and predictive climate risk management. This is positioning AI as a core enabler of sustainable farming systems globally.

Regional policy differences are influencing technology adoption rates, with developed economies focusing on advanced automation and developing economies prioritizing accessibility, affordability, and rural digitization of agriculture services.

Additionally, increasing public-private partnerships are fostering innovation in agritech ecosystems, enabling collaboration between governments, technology providers, and agricultural organizations to scale AI adoption in farming systems.

Global Artificial Intelligence in Agriculture Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Artificial Intelligence in Agriculture Market is expected to become more structured, with stronger frameworks for AI governance, agricultural data regulation, and sustainability compliance.

North America is expected to further strengthen precision agriculture policies, expand federal support for agritech innovation, and enhance data security regulations for farm-level digital systems.

Europe will continue leading in sustainable agriculture regulation, with stricter environmental compliance standards and expanded funding for AI-driven climate-smart farming solutions under the Green Deal framework.

Asia-Pacific is expected to remain the fastest-evolving regulatory region, with large-scale government-led digital agriculture programs in China, India, and Southeast Asia driving widespread AI adoption in farming systems.

Latin America and the Middle East & Africa are expected to strengthen agricultural modernization policies, focusing on food security, water-efficient farming, and AI-based resource optimization systems.

Overall, the regulatory landscape will increasingly support AI integration in agriculture as a key driver of global food security, sustainability, and productivity enhancement. Companies that align with data governance standards, sustainability policies, and government-backed digital agriculture initiatives will be best positioned for long-term growth.