Global Ethanol Fuel Blending Market Report, Size & Forecast 2026-2033

Global Ethanol Fuel Blending Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 82.40 Billion |

| Market Size (2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 141.30 Billion |

| CAGR (2026???2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? 6.97% |

| Largest Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??E10 Fuel Blends |

| Fastest Growing Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??E20 Fuel Blends |

| Leading End-Use Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Passenger Vehicles |

| Key Trend | ?? ?? ?? ?? ??Higher Ethanol Blending Mandates, Decarbonization Initiatives & Expansion of Biofuel Infrastructure |

| Regulatory Influence | ?? ?? ?? ?? ??Renewable Fuel Standards, National Ethanol Blending Programs & Carbon Emission Reduction Policies |

| Future Outlook | Growth Driven by Energy Security Goals, Sustainable Transportation & Increasing Government Support for Biofuels |

Global Ethanol Fuel Blending Market Size & Forecast

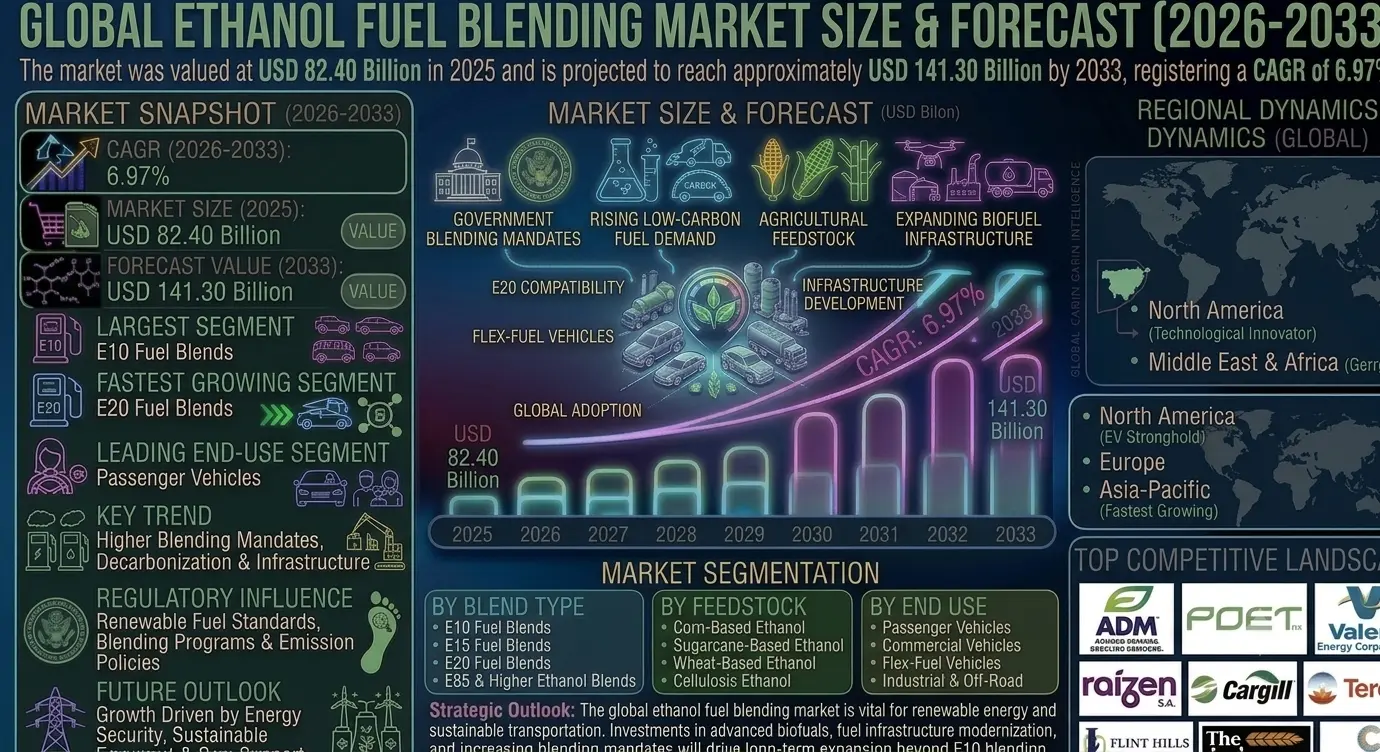

The Global Ethanol Fuel Blending Market is expected to witness robust growth during the forecast period from 2026 to 2033. The market was valued at USD 82.40 billion in 2025 and is projected to reach approximately USD 141.30 billion by 2033, registering a CAGR of 6.97%. Market growth is primarily driven by increasing adoption of renewable fuels, implementation of higher ethanol blending mandates, rising concerns regarding greenhouse gas emissions, and growing efforts to reduce dependence on fossil fuel imports. Governments worldwide are promoting ethanol blending as a strategic solution to improve energy security and support sustainable transportation systems.Global Ethanol Fuel Blending Market Overview

Ethanol fuel blending involves mixing ethanol with gasoline in various proportions such as E10, E15, E20, E25, E85, and higher blends. Ethanol serves as an oxygenate that improves fuel combustion efficiency and reduces harmful vehicle emissions. The market includes ethanol producers, petroleum refiners, fuel distributors, government agencies, automotive manufacturers, and fuel retail networks. Increasing adoption of biofuels and advancements in flex-fuel vehicle technologies are supporting the expansion of ethanol blending programs globally.Structural Drivers of Market Growth

1. Government Ethanol Blending Mandates

Many countries are implementing mandatory ethanol blending targets to reduce carbon emissions and lower reliance on imported petroleum products. Market Implications: Ethanol producers and fuel distributors are expanding infrastructure and supply chains to meet growing blending requirements.2. Rising Demand for Low-Carbon Transportation Fuels

Increasing environmental concerns and climate change mitigation efforts are driving the adoption of cleaner transportation fuel alternatives. Market Implications: Ethanol blending is becoming a key strategy for reducing transportation sector emissions.3. Growing Agricultural Feedstock Availability

Expanding production of corn, sugarcane, and other ethanol feedstocks is supporting increased ethanol manufacturing capacity. Market Implications: Stable feedstock supply is enhancing market growth and improving long-term fuel blending sustainability.4. Expansion of Biofuel Infrastructure

Investments in ethanol production facilities, storage terminals, and fuel distribution networks are improving market accessibility. Market Implications: Enhanced infrastructure is accelerating the adoption of higher ethanol blends across multiple regions.Market Segmentation Analysis

By Blend Type

- E10 Fuel Blends Largest segment due to widespread adoption and compatibility with most conventional gasoline-powered vehicles.

- E15 Fuel Blends Increasingly adopted in markets promoting higher renewable fuel content.

- E20 Fuel Blends Fastest-growing segment driven by government blending targets and advancements in vehicle compatibility.

- E85 & Higher Ethanol Blends Used primarily in flex-fuel vehicles and specialized transportation applications.

By Feedstock

- Corn-Based Ethanol Largest segment supported by extensive production infrastructure in major ethanol-producing countries.

- Sugarcane-Based Ethanol Widely utilized in countries with strong sugarcane cultivation and biofuel programs.

- Wheat-Based Ethanol Used as an alternative feedstock in selected regions.

- Cellulosic Ethanol Emerging segment driven by advancements in second-generation biofuel technologies.

By End Use

- Passenger Vehicles Largest segment due to high gasoline consumption and widespread implementation of ethanol blending programs.

- Commercial Vehicles Growing adoption of blended fuels for fleet operations and transportation services.

- Flex-Fuel Vehicles Fast-growing segment capable of utilizing higher ethanol blend concentrations.

- Industrial & Off-Road Applications Utilizes blended fuels in specialized machinery and equipment operations.

Regional Market Dynamics

North America

Leading market driven by strong renewable fuel standards, extensive ethanol production capacity, and established fuel blending infrastructure.Europe

Supported by carbon reduction targets, renewable energy directives, and increasing demand for sustainable transportation fuels.Asia-Pacific

Fastest-growing region due to expanding ethanol blending programs, rising fuel demand, and government initiatives promoting energy security.Latin America

Major market led by Brazil's advanced ethanol industry and widespread use of flex-fuel vehicles.Middle East & Africa

Emerging market supported by diversification of transportation fuel sources and growing renewable energy investments.Competitive Landscape

The Global Ethanol Fuel Blending Market is characterized by the presence of ethanol manufacturers, energy companies, agricultural processors, fuel distributors, and biofuel technology providers. Market participants compete through production efficiency, feedstock management, distribution capabilities, and strategic partnerships. Key Companies Operating in the Market Include:- Archer Daniels Midland Company (ADM)

- POET LLC

- Valero Energy Corporation

- Green Plains Inc.

- Ra??zen S.A.

- Cargill Incorporated

- Tereos Group

- Flint Hills Resources

- The Andersons, Inc.

- CropEnergies AG

Strategic Outlook

The future of the ethanol fuel blending market will be shaped by increasing renewable fuel mandates, advancements in ethanol production technologies, and global efforts to reduce transportation-related carbon emissions. Governments are expected to continue strengthening biofuel policies and increasing blending targets to support energy diversification and sustainability objectives. Investments in advanced biofuels, cellulosic ethanol production, and fuel infrastructure modernization will further enhance market growth prospects. Automotive manufacturers are also adapting vehicle technologies to accommodate higher ethanol blend compatibility, creating additional demand opportunities. As countries seek cleaner and more secure energy solutions, ethanol fuel blending is expected to remain a critical component of sustainable transportation strategies worldwide.Final Market Perspective

The Global Ethanol Fuel Blending Market plays a crucial role in supporting renewable energy adoption, reducing greenhouse gas emissions, and improving energy security. Rising government support, expanding production capacity, and increasing demand for sustainable transportation fuels are creating significant growth opportunities across the industry. Companies that invest in advanced production technologies, feedstock diversification, and efficient fuel distribution networks will be well-positioned to capitalize on the long-term expansion of the global ethanol fuel blending ecosystem.Table of Contents

Table of Contents

- Executive Summary

- Global Ethanol Fuel Blending Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends in Renewable Transportation Fuels

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Ethanol Fuel Blending

- Scope of the Global Ethanol Fuel Blending Market

- Evolution of Ethanol-Blended Fuel Programs

- Role of Ethanol in Sustainable Transportation

- Value Chain Analysis of the Ethanol Fuel Blending Ecosystem

- Regulatory Influence (Renewable Fuel Standards, National Ethanol Blending Programs & Carbon Emission Policies)

- Transition Toward Higher Ethanol Blend Adoption and Biofuel Expansion

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Government Ethanol Blending Mandates

- Rising Demand for Low-Carbon Transportation Fuels

- Growing Agricultural Feedstock Availability

- Expansion of Biofuel Infrastructure

- Market Restraints

- Feedstock Price Volatility

- Infrastructure Compatibility Limitations

- Competition from Electric Mobility Solutions

- Market Opportunities

- Expansion of E20 and Higher Blend Programs

- Growth in Cellulosic Ethanol Production

- Emerging Biofuel Markets in Developing Economies

- Advancements in Flex-Fuel Vehicle Technologies

- Market Challenges

- Supply Chain and Feedstock Availability Risks

- Regulatory and Policy Uncertainty

- Public Awareness and Adoption Challenges

- Structural Drivers of Market Growth

- Global Ethanol Fuel Blending Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Biofuel Consumption Trends

- Blend Adoption Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Blend Type

- E10 Fuel Blends (Largest Segment)

- E15 Fuel Blends

- E20 Fuel Blends (Fastest-Growing Segment)

- E85 & Higher Ethanol Blends

- By Feedstock

- Corn-Based Ethanol (Largest Segment)

- Sugarcane-Based Ethanol

- Wheat-Based Ethanol

- Cellulosic Ethanol

- By End Use

- Passenger Vehicles (Largest Segment)

- Commercial Vehicles

- Flex-Fuel Vehicles (Fastest-Growing Segment)

- Industrial & Off-Road Applications

- By Blend Type

- Regional Market Analysis

- North America (Largest Regional Market)

- Europe

- Asia-Pacific (Fastest-Growing Regional Market)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- Production Capacity Expansion Strategies

- Partnerships, Acquisitions & Biofuel Infrastructure Investments

- Company Profiles

- Archer Daniels Midland Company (ADM)

- POET LLC

- Valero Energy Corporation

- Green Plains Inc.

- Ra??zen S.A.

- Cargill Incorporated

- Tereos Group

- Flint Hills Resources

- The Andersons, Inc.

- CropEnergies AG

- Strategic Outlook

- Future of Renewable Fuel Blending Programs

- Expansion of Biofuel Production Capacity

- Growth of Cellulosic and Advanced Ethanol Technologies

- Rising Adoption of Higher Ethanol Blend Fuels

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Ethanol Fuel Blending Market Competitive Intensity & Market Structure Overview

The Global Ethanol Fuel Blending Market is highly competitive and strategically important within the renewable fuels and transportation energy ecosystem. The market consists of ethanol producers, agricultural processing companies, integrated energy firms, fuel distributors, biofuel technology providers, and infrastructure operators competing through production capacity, feedstock efficiency, regulatory compliance, distribution networks, and sustainability performance.

Competition is primarily influenced by government blending mandates, renewable fuel standards, feedstock availability, production economics, and long-term supply agreements with fuel retailers and petroleum refiners. Market participants are increasingly focusing on capacity expansion, advanced ethanol technologies, supply chain optimization, and carbon reduction initiatives to strengthen competitive positioning.

The market structure is evolving toward larger integrated biofuel ecosystems supported by strategic partnerships between ethanol manufacturers, agricultural suppliers, refiners, automotive companies, and government agencies. Growing adoption of higher ethanol blends and investments in next-generation biofuel infrastructure are further reshaping competitive dynamics globally.

Global Ethanol Fuel Blending Market Competitive Intensity & Market Structure Current Scenario

Leading Global Ethanol Fuel Blending Companies

- Archer Daniels Midland Company (ADM): One of the world’s largest ethanol producers with extensive feedstock sourcing capabilities, large-scale production facilities, and global distribution networks.

- POET LLC: A leading biofuel producer recognized for large ethanol production capacity, innovation in renewable fuels, and investments in advanced biofuel technologies.

- Valero Energy Corporation: Operates significant ethanol production assets and leverages integrated refining and fuel distribution operations to strengthen market competitiveness.

- Green Plains Inc.: Focuses on ethanol production efficiency, renewable fuel innovation, and value-added agricultural processing solutions.

- Ra??zen S.A.: A major sugarcane ethanol producer with strong market leadership in Brazil and extensive fuel distribution infrastructure.

- Cargill Incorporated: Utilizes its global agricultural supply chain expertise to support ethanol production, feedstock management, and biofuel distribution activities.

- Tereos Group: A prominent producer of sugar-based ethanol serving transportation fuel and industrial biofuel markets across multiple regions.

- Flint Hills Resources: Operates large-scale ethanol manufacturing facilities and maintains strong relationships across fuel supply chains.

- The Andersons, Inc.: Active in ethanol production, grain sourcing, and renewable fuel supply management through vertically integrated operations.

- CropEnergies AG: A leading European bioethanol producer focused on sustainable fuel solutions and renewable energy market expansion.

Key Competitive Intensity & Market Structure Drivers

Government ethanol blending mandates and renewable fuel regulations remain the most influential competitive factors, creating strong demand visibility while encouraging production expansion and infrastructure investment.

Feedstock availability, agricultural productivity, and raw material pricing significantly influence profitability and competitive positioning among market participants.

Increasing adoption of E20 and higher ethanol blends is driving competition among producers seeking to secure long-term supply contracts and strengthen distribution capabilities.

Investments in advanced ethanol technologies, cellulosic ethanol production, and carbon reduction initiatives are becoming important differentiators in an increasingly sustainability-focused market environment.

Growing collaboration between ethanol producers, fuel retailers, automotive manufacturers, and government agencies is strengthening market integration and creating barriers to entry for smaller competitors.

Strategic Implications of Competitive Intensity & Market Structure

Companies with large-scale production facilities, diversified feedstock sourcing strategies, and integrated distribution networks are expected to maintain significant competitive advantages.

Investment in advanced biofuel technologies, operational efficiency improvements, and carbon management solutions is becoming increasingly important for long-term market leadership.

Strategic partnerships across agricultural, energy, automotive, and infrastructure sectors are helping companies secure stable demand and strengthen market positioning.

Organizations capable of maintaining regulatory compliance while optimizing production economics are expected to achieve superior profitability and market resilience.

Expansion into emerging ethanol blending markets and higher-blend fuel segments is creating new growth opportunities for established industry participants.

Global Ethanol Fuel Blending Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global ethanol fuel blending market is expected to become increasingly policy-driven, sustainability-focused, and technologically advanced as governments continue prioritizing renewable transportation fuels.

Future competition will be shaped by advancements in cellulosic ethanol technologies, feedstock diversification strategies, carbon capture integration, and infrastructure modernization programs.

Market participants are expected to increase investments in production expansion, supply chain optimization, advanced biofuel development, and strategic partnerships to strengthen competitive positioning.

Over the forecast period, companies that successfully combine production scale, feedstock security, regulatory alignment, technological innovation, sustainability performance, and efficient distribution capabilities will be best positioned to lead the evolving global ethanol fuel blending market.

Value Chain

Global Ethanol Fuel Blending Market Value Chain & Supply Chain Evolution Overview

The Global Ethanol Fuel Blending Market operates through an integrated value chain consisting of feedstock cultivation, ethanol production, fuel blending operations, storage, distribution, retail fuel networks, and end-user consumption. The industry connects agricultural producers, biofuel manufacturers, petroleum companies, automotive manufacturers, government agencies, and transportation users.

The market is strongly influenced by renewable fuel policies, ethanol blending mandates, carbon reduction targets, agricultural productivity, and advancements in flex-fuel vehicle technologies. Increasing global focus on energy security and sustainable transportation is accelerating the adoption of ethanol-blended fuels.

The expansion of E10, E15, E20, and higher ethanol blend programs has transformed fuel supply chains worldwide. Companies are investing in ethanol production capacity, blending infrastructure, storage facilities, and distribution networks to support increasing demand for renewable transportation fuels.

Technological advancements in advanced biofuels, cellulosic ethanol production, digital fuel management systems, and low-carbon ethanol technologies are reshaping the market value chain while improving efficiency and sustainability.

Global Ethanol Fuel Blending Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Agricultural Feedstock Production: Cultivation and supply of corn, sugarcane, wheat, and biomass feedstocks used for ethanol production.

- Feedstock Collection & Processing: Harvesting, transportation, storage, milling, and preparation of agricultural raw materials for ethanol manufacturing.

- Ethanol Production: Conversion of feedstocks into fuel ethanol through fermentation, distillation, dehydration, and purification processes.

- Fuel Blending Operations: Mixing ethanol with gasoline at different ratios including E10, E15, E20, E85, and higher ethanol blends.

- Storage & Distribution: Transportation, terminal storage, pipeline movement, fuel logistics, and supply chain management.

- Fuel Retailing: Distribution through fuel stations, petroleum retailers, government-supported biofuel networks, and transportation fuel providers.

- End User Consumption: Passenger vehicles, commercial vehicles, flex-fuel vehicles, and industrial transportation users consuming ethanol-blended fuels.

Company-to-Stage Mapping

- Agricultural Feedstock Production: Corn growers, sugarcane producers, agricultural cooperatives, wheat suppliers, and biomass feedstock providers.

- Feedstock Collection & Processing: Archer Daniels Midland Company (ADM), Cargill Incorporated, The Andersons, Inc., agricultural processors, and grain handling companies.

- Ethanol Production: POET LLC, Green Plains Inc., Valero Energy Corporation, Ra??zen S.A., Tereos Group, CropEnergies AG, and Flint Hills Resources.

- Fuel Blending Operations: Petroleum refiners, fuel blending companies, energy corporations, and renewable fuel operators.

- Storage & Distribution: Fuel terminal operators, logistics providers, pipeline operators, rail transportation companies, and fuel distributors.

- Fuel Retailing: Gasoline station networks, petroleum retailers, energy companies, and alternative fuel distributors.

- End User Consumption: Passenger vehicle owners, commercial fleets, transportation companies, logistics operators, and industrial vehicle users.

Key Value Chain & Supply Chain Evolution Signals in Global Ethanol Fuel Blending Market

Expansion of Higher Ethanol Blend Programs

Governments worldwide are increasing ethanol blending targets such as E20 and higher blends to reduce transportation emissions and improve energy independence.

Growth of Advanced Biofuel Technologies

Investment in cellulosic ethanol and second-generation biofuel technologies is enabling production from agricultural residues and non-food biomass sources.

Increasing Integration of Renewable Fuel Infrastructure

Fuel companies are expanding blending facilities, storage terminals, and distribution networks to support higher ethanol adoption.

Development of Flex-Fuel Vehicle Ecosystems

Automotive manufacturers are improving vehicle compatibility with higher ethanol concentrations, supporting broader adoption of ethanol-based transportation fuels.

Digitalization of Fuel Supply Chains

Companies are implementing digital monitoring systems, predictive analytics, and automated inventory management to improve fuel supply efficiency.

Growing Focus on Low-Carbon Ethanol Production

Ethanol producers are adopting renewable energy integration, carbon capture technologies, and sustainable production methods to reduce lifecycle emissions.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Ethanol Production Capacity Expansion

Increasing ethanol demand requires expansion of production facilities, modernization of existing plants, and improved operational efficiency.

Strengthening Feedstock Supply Security

Diversification of agricultural feedstocks and long-term supply agreements can reduce raw material risks and improve production stability.

Expansion of Blending Infrastructure

Investment in storage terminals, fuel stations, and distribution networks will accelerate adoption of higher ethanol blend fuels.

Advancement of Low-Carbon Ethanol Technologies

Companies investing in carbon reduction technologies and advanced biofuel processes can improve sustainability performance and regulatory alignment.

Enhancement of Automotive Compatibility

Collaboration between ethanol producers and automotive manufacturers can support wider adoption of flex-fuel and higher ethanol-compatible vehicles.

Leveraging Government Renewable Fuel Programs

Participation in national ethanol blending initiatives and renewable fuel policies can create long-term market expansion opportunities.

Global Ethanol Fuel Blending Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the ethanol fuel blending value chain is expected to become increasingly integrated, sustainable, and technology-driven. Rising demand for renewable transportation fuels, higher blending mandates, and global decarbonization objectives will continue transforming industry operations.

Key Future Developments Include:

- Expansion of E20 and higher ethanol blending programs globally.

- Increasing adoption of advanced and cellulosic ethanol technologies.

- Growth of renewable fuel infrastructure and blending facilities.

- Greater integration of digital technologies across ethanol supply chains.

- Development of low-carbon ethanol production systems.

- Increasing collaboration between biofuel producers and automotive manufacturers.

- Expansion of sustainable agricultural feedstock management practices.

As the market evolves, competitive advantage will increasingly depend on production scalability, feedstock availability, infrastructure development, sustainability performance, and regulatory compliance.

Companies that successfully integrate advanced ethanol production technologies, efficient fuel distribution networks, sustainable sourcing strategies, and strong industry partnerships will be well-positioned to achieve long-term growth in the Global Ethanol Fuel Blending Market.

Investment Activity

Global Ethanol Fuel Blending Market Investment & Funding Dynamics Overview (2026???2033)

The Global Ethanol Fuel Blending Market is experiencing significant investment activity driven by increasing renewable fuel mandates, rising government support for biofuel adoption, expanding ethanol production capacity, and growing efforts to reduce transportation-related carbon emissions. Biofuel producers, energy companies, agricultural processing firms, infrastructure developers, private equity investors, and institutional funds are actively investing in ethanol production facilities, fuel blending infrastructure, feedstock optimization technologies, storage terminals, and distribution network expansion.

Investment momentum is accelerating as countries strengthen energy security strategies and implement higher ethanol blending targets across transportation sectors. Capital allocation is increasingly focused on advanced biofuel technologies, cellulosic ethanol production, fuel logistics modernization, refinery integration projects, and low-carbon fuel development initiatives.

Additionally, growing investments in sustainable feedstock development, carbon reduction technologies, flex-fuel vehicle ecosystems, and next-generation ethanol production platforms are creating substantial long-term opportunities throughout the global ethanol fuel blending value chain.

Current Investment & Funding Landscape

The current investment environment reflects strong interest from governments, renewable energy investors, infrastructure funds, and agricultural stakeholders seeking to support low-carbon transportation solutions. Industry participants are investing heavily in capacity expansion projects, blending infrastructure upgrades, fuel storage systems, and supply chain optimization initiatives.

Significant funding is being directed toward cellulosic ethanol facilities, advanced fermentation technologies, feedstock diversification programs, distribution network modernization, and integrated biofuel production ecosystems to improve efficiency and scalability.

Strategic partnerships among ethanol producers, petroleum refiners, automotive manufacturers, agricultural suppliers, and energy infrastructure companies are reshaping investment flows and accelerating market development worldwide.

Key Investment & Funding Dynamics Signals

- Growing implementation of national ethanol blending mandates and renewable fuel programs is attracting large-scale investment across production and distribution infrastructure.

- Expansion of E20 and higher ethanol blending initiatives is driving capital deployment toward fuel compatibility and supply chain enhancement projects.

- Increasing demand for low-carbon transportation fuels is supporting investments in sustainable ethanol production technologies.

- Rising focus on energy security and reduction of fossil fuel imports is strengthening long-term funding opportunities across biofuel markets.

- Strategic investments in cellulosic ethanol and second-generation biofuel technologies are creating new innovation-driven growth avenues.

- Growing adoption of flex-fuel vehicles and advanced fuel systems is encouraging investment in higher ethanol blend infrastructure.

- Expansion of feedstock cultivation, agricultural processing, and ethanol logistics networks is generating additional capital investment opportunities.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in ethanol production capacity, infrastructure modernization, and advanced processing technologies remains essential for long-term market competitiveness.

- Capital allocation toward cellulosic ethanol development, carbon reduction technologies, and sustainable feedstock programs will strengthen future growth potential.

- Companies investing in integrated biofuel ecosystems, blending facilities, and distribution capabilities are expected to secure stronger market positions.

- Strategic collaborations between energy companies, agricultural producers, technology developers, and government agencies will accelerate market expansion.

- Investments in supply chain resilience, storage infrastructure, and fuel transportation networks will improve operational efficiency and market accessibility.

- Compliance with renewable fuel standards, emission reduction policies, and sustainability regulations will continue influencing funding priorities.

- Organizations building capabilities across production, logistics, technology innovation, and regulatory compliance are expected to capture substantial long-term value.

Forward Outlook

Looking ahead, the Global Ethanol Fuel Blending Market is expected to maintain strong investment momentum supported by expanding biofuel mandates, increasing renewable energy adoption, and growing transportation sector decarbonization efforts.

Future capital deployment will increasingly focus on advanced biofuel technologies, cellulosic ethanol production, blending infrastructure expansion, carbon-efficient manufacturing systems, and integrated renewable fuel ecosystems.

As governments and industries continue prioritizing sustainable transportation and energy diversification, investment activity is expected to expand across ethanol production, agricultural feedstock development, fuel logistics, infrastructure modernization, and low-carbon mobility solutions.

In conclusion, the Global Ethanol Fuel Blending Market represents an attractive renewable energy investment landscape where biofuel expansion, energy security initiatives, infrastructure development, technological innovation, and transportation decarbonization will define future funding priorities, competitive differentiation, and long-term market growth.

Technology & Innovation

Global Ethanol Fuel Blending Market Technology & Innovation Landscape Overview

The Global Ethanol Fuel Blending Market is witnessing significant technological advancements as governments, energy companies, and fuel producers focus on improving ethanol production efficiency, blending capabilities, and sustainable biofuel solutions. Innovations in advanced fermentation technologies, feedstock optimization, cellulosic ethanol production, and fuel compatibility systems are transforming the biofuel industry landscape. Companies are increasingly investing in research and development to enhance ethanol yield, reduce production costs, and develop low-carbon fuel alternatives that support global decarbonization goals. As demand for renewable transportation fuels continues to increase, technology innovation is becoming a key factor driving market competitiveness and long-term growth.

The market is also benefiting from advancements in bio-refinery technologies, digital monitoring systems, carbon reduction solutions, and fuel distribution infrastructure. These innovations are enabling ethanol producers to improve operational efficiency, optimize supply chains, enhance sustainability performance, and support higher ethanol blending levels. The growing adoption of E20 and advanced ethanol blends is further accelerating investments in vehicle compatibility technologies, smart fuel management systems, and next-generation biofuel production processes.

Global Ethanol Fuel Blending Market Technology & Innovation Current Scenario

Current innovation within the global ethanol fuel blending market is primarily focused on advanced ethanol production methods, sustainable feedstock utilization, higher blending compatibility, and carbon-efficient manufacturing processes. Ethanol producers are increasingly adopting advanced fermentation technologies, enzyme optimization techniques, and integrated biorefinery systems to improve production efficiency and reduce environmental impact. Developments in cellulosic ethanol and second-generation biofuels are creating new opportunities to utilize agricultural residues and non-food biomass resources.

Digital transformation is also reshaping ethanol fuel blending operations through artificial intelligence-based production monitoring, predictive analytics, and automated quality control systems. Fuel companies are implementing advanced blending technologies, real-time fuel management solutions, and improved storage infrastructure to support higher ethanol concentration fuels. These innovations are helping industry participants improve reliability, maintain fuel quality standards, and accelerate the transition toward sustainable transportation fuels.

Key Technology & Innovation Trends in Global Ethanol Fuel Blending Market

- Advanced Ethanol Production Technologies: Improving fermentation efficiency, ethanol yield, and production scalability.

- Cellulosic Ethanol Innovation: Supporting next-generation biofuel production using agricultural residues and biomass resources.

- Feedstock Optimization Technologies: Enhancing the utilization of corn, sugarcane, wheat, and alternative ethanol feedstocks.

- High-Blending Fuel Technologies: Enabling wider adoption of E20, E25, E85, and advanced ethanol blends.

- Vehicle Compatibility Technologies: Supporting automotive advancements for higher ethanol blend usage.

- Carbon Reduction & Sustainable Production Solutions: Improving lifecycle emissions performance of ethanol production.

- Digital Bio-Refinery Management Systems: Using automation, analytics, and monitoring technologies to optimize operations.

- Smart Fuel Distribution Infrastructure: Improving ethanol storage, transportation, and blending network efficiency.

- Advanced Quality Control Technologies: Ensuring fuel consistency, safety, and compliance with regulatory standards.

- Integrated Biorefinery Solutions: Combining ethanol production with renewable chemicals and energy generation.

Strategic Implications of Technology & Innovation

Technological advancements are enabling ethanol fuel blending companies to improve production economics, enhance sustainability, and meet increasing global demand for renewable transportation fuels. Organizations investing in advanced biofuel technologies, efficient feedstock management, and digital production systems are strengthening their competitive position within the evolving energy sector. Innovation is helping companies overcome challenges related to production efficiency, carbon reduction targets, and increasing regulatory requirements.

As countries continue expanding ethanol blending mandates, manufacturers are focusing on improving supply chain capabilities, developing higher ethanol blend solutions, and increasing compatibility with modern vehicle technologies. Digital technologies are enhancing operational visibility and enabling more efficient fuel management practices. However, factors such as feedstock availability, infrastructure requirements, regulatory compliance, and production costs remain important considerations for industry participants seeking sustainable growth.

Global Ethanol Fuel Blending Market Technology & Innovation Forward Outlook

The future of the global ethanol fuel blending market is expected to be shaped by continued advancements in cellulosic ethanol technologies, carbon-efficient production methods, smart fuel infrastructure, and advanced blending systems. Emerging innovations such as artificial intelligence-driven bio-refinery optimization, renewable carbon technologies, and improved biomass conversion processes are expected to enhance ethanol production efficiency and environmental performance. Companies are likely to increase investments in next-generation biofuels to support global energy transition objectives.

As governments and industries continue prioritizing renewable energy adoption and transportation decarbonization, technology will play an increasingly important role in expanding ethanol fuel blending applications. The combination of advanced production technologies, sustainable feedstock development, digital infrastructure, and improved vehicle compatibility solutions is expected to create new growth opportunities while strengthening the long-term development of the global ethanol fuel blending market.

Market Risk

Global Ethanol Fuel Blending Market Risk Factors & Disruption Threats Overview

The Global Ethanol Fuel Blending Market is a critical component of the renewable energy and transportation fuel ecosystem, supporting carbon reduction initiatives, energy diversification, and fuel security objectives. Despite strong policy support and growing adoption of biofuel blending programs, the market faces several risks related to feedstock availability, regulatory uncertainty, technological shifts, infrastructure limitations, and evolving transportation trends.

One of the most significant structural risks involves dependence on agricultural feedstocks such as corn, sugarcane, wheat, and other biomass resources. Crop yield fluctuations caused by extreme weather events, climate change, water scarcity, and agricultural supply disruptions can impact ethanol production volumes and pricing stability.

The market is also highly dependent on government policies, including renewable fuel standards, blending mandates, tax incentives, and biofuel subsidy programs. Changes in political priorities or regulatory frameworks could significantly influence ethanol demand and long-term investment decisions.

Another major disruption factor is the growing adoption of electric vehicles and alternative low-carbon transportation technologies. As EV penetration increases globally, long-term gasoline consumption growth may slow, potentially affecting ethanol blending volumes in certain markets.

Additionally, infrastructure constraints involving ethanol storage, transportation, fuel distribution systems, and retail fueling stations may limit the adoption of higher ethanol blends in some regions.

Global Ethanol Fuel Blending Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by expanding ethanol blending mandates, increasing investments in renewable fuels, and growing efforts to reduce transportation sector emissions. Governments across major economies are strengthening biofuel policies to improve energy security and reduce dependence on imported fossil fuels.

However, producers and distributors continue to face volatility in feedstock prices, energy costs, logistics expenses, and agricultural commodity markets. These factors can directly affect production economics and profit margins.

Automotive manufacturers are increasingly developing vehicles capable of operating with higher ethanol blend concentrations, but vehicle compatibility challenges remain in certain markets where older vehicle fleets dominate.

Supply chain resilience has become a growing concern due to geopolitical tensions, trade restrictions, transportation bottlenecks, and disruptions affecting global agricultural and energy markets.

At the same time, sustainability scrutiny is increasing, with regulators and environmental organizations evaluating the lifecycle emissions, land use impacts, and resource efficiency of biofuel production systems.

Key Risk Factors & Disruption Threat Signals in Global Ethanol Fuel Blending Market

A major disruption signal is the accelerating adoption of battery electric vehicles and alternative transportation technologies, which may gradually reduce gasoline demand and influence long-term ethanol consumption patterns.

Another important signal is the increasing volatility in agricultural commodity markets. Feedstock shortages, changing crop economics, and climate-related agricultural disruptions can affect ethanol supply and pricing dynamics.

The emergence of advanced biofuels, synthetic fuels, renewable hydrogen, and other low-carbon energy alternatives is creating a more competitive landscape for conventional ethanol blending programs.

Growing environmental concerns regarding land utilization, food-versus-fuel debates, water consumption, and agricultural sustainability are prompting greater regulatory and public scrutiny of ethanol production practices.

Changes in government administrations, renewable energy priorities, and fuel policy frameworks can create uncertainty regarding future blending mandates and industry support mechanisms.

Infrastructure readiness for higher ethanol blends, including fuel storage systems, distribution networks, and retail fueling stations, remains a critical factor influencing market expansion across several regions.

Strategic Implications of Risk Factors & Disruption Threats in Global Ethanol Fuel Blending Market

Market participants should diversify feedstock sourcing strategies and invest in agricultural supply chain resilience to reduce exposure to crop-related disruptions and commodity price fluctuations.

Investment in advanced biofuel technologies, including cellulosic ethanol and next-generation feedstock solutions, can help improve sustainability performance and reduce reliance on traditional agricultural resources.

Companies should strengthen partnerships with fuel distributors, retailers, vehicle manufacturers, and government agencies to support infrastructure development and higher blend adoption initiatives.

Continuous monitoring of regulatory developments, renewable fuel standards, and environmental policies will remain essential for managing compliance risks and identifying growth opportunities.

Organizations should invest in lifecycle emissions reduction programs, sustainability certifications, and resource-efficient production technologies to address growing environmental expectations.

Expanding applications beyond traditional fuel blending markets may provide additional diversification opportunities and reduce exposure to long-term transportation sector transitions.

Global Ethanol Fuel Blending Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Ethanol Fuel Blending Market is expected to maintain positive growth momentum as governments continue pursuing energy security objectives, carbon reduction targets, and renewable fuel adoption strategies. However, the market will face increasing pressure from evolving transportation technologies and sustainability expectations.

Regulatory support is expected to remain a primary growth driver, although policy structures may become more performance-based, emphasizing carbon intensity reductions, feedstock sustainability, and environmental accountability.

Technological advancements in ethanol production, feedstock optimization, carbon capture integration, and second-gen

Global Ethanol Fuel Blending Market Risk Factors & Disruption Threats Overview

The Global Ethanol Fuel Blending Market is a critical component of the renewable energy and transportation fuel ecosystem, supporting carbon reduction initiatives, energy diversification, and fuel security objectives. Despite strong policy support and growing adoption of biofuel blending programs, the market faces several risks related to feedstock availability, regulatory uncertainty, technological shifts, infrastructure limitations, and evolving transportation trends.

One of the most significant structural risks involves dependence on agricultural feedstocks such as corn, sugarcane, wheat, and other biomass resources. Crop yield fluctuations caused by extreme weather events, climate change, water scarcity, and agricultural supply disruptions can impact ethanol production volumes and pricing stability.

The market is also highly dependent on government policies, including renewable fuel standards, blending mandates, tax incentives, and biofuel subsidy programs. Changes in political priorities or regulatory frameworks could significantly influence ethanol demand and long-term investment decisions.

Another major disruption factor is the growing adoption of electric vehicles and alternative low-carbon transportation technologies. As EV penetration increases globally, long-term gasoline consumption growth may slow, potentially affecting ethanol blending volumes in certain markets.

Additionally, infrastructure constraints involving ethanol storage, transportation, fuel distribution systems, and retail fueling stations may limit the adoption of higher ethanol blends in some regions.

Global Ethanol Fuel Blending Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by expanding ethanol blending mandates, increasing investments in renewable fuels, and growing efforts to reduce transportation sector emissions. Governments across major economies are strengthening biofuel policies to improve energy security and reduce dependence on imported fossil fuels.

However, producers and distributors continue to face volatility in feedstock prices, energy costs, logistics expenses, and agricultural commodity markets. These factors can directly affect production economics and profit margins.

Automotive manufacturers are increasingly developing vehicles capable of operating with higher ethanol blend concentrations, but vehicle compatibility challenges remain in certain markets where older vehicle fleets dominate.

Supply chain resilience has become a growing concern due to geopolitical tensions, trade restrictions, transportation bottlenecks, and disruptions affecting global agricultural and energy markets.

At the same time, sustainability scrutiny is increasing, with regulators and environmental organizations evaluating the lifecycle emissions, land use impacts, and resource efficiency of biofuel production systems.

Key Risk Factors & Disruption Threat Signals in Global Ethanol Fuel Blending Market

A major disruption signal is the accelerating adoption of battery electric vehicles and alternative transportation technologies, which may gradually reduce gasoline demand and influence long-term ethanol consumption patterns.

Another important signal is the increasing volatility in agricultural commodity markets. Feedstock shortages, changing crop economics, and climate-related agricultural disruptions can affect ethanol supply and pricing dynamics.

The emergence of advanced biofuels, synthetic fuels, renewable hydrogen, and other low-carbon energy alternatives is creating a more competitive landscape for conventional ethanol blending programs.

Growing environmental concerns regarding land utilization, food-versus-fuel debates, water consumption, and agricultural sustainability are prompting greater regulatory and public scrutiny of ethanol production practices.

Changes in government administrations, renewable energy priorities, and fuel policy frameworks can create uncertainty regarding future blending mandates and industry support mechanisms.

Infrastructure readiness for higher ethanol blends, including fuel storage systems, distribution networks, and retail fueling stations, remains a critical factor influencing market expansion across several regions.

Strategic Implications of Risk Factors & Disruption Threats in Global Ethanol Fuel Blending Market

Market participants should diversify feedstock sourcing strategies and invest in agricultural supply chain resilience to reduce exposure to crop-related disruptions and commodity price fluctuations.

Investment in advanced biofuel technologies, including cellulosic ethanol and next-generation feedstock solutions, can help improve sustainability performance and reduce reliance on traditional agricultural resources.

Companies should strengthen partnerships with fuel distributors, retailers, vehicle manufacturers, and government agencies to support infrastructure development and higher blend adoption initiatives.

Continuous monitoring of regulatory developments, renewable fuel standards, and environmental policies will remain essential for managing compliance risks and identifying growth opportunities.

Organizations should invest in lifecycle emissions reduction programs, sustainability certifications, and resource-efficient production technologies to address growing environmental expectations.

Expanding applications beyond traditional fuel blending markets may provide additional diversification opportunities and reduce exposure to long-term transportation sector transitions.

Global Ethanol Fuel Blending Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Ethanol Fuel Blending Market is expected to maintain positive growth momentum as governments continue pursuing energy security objectives, carbon reduction targets, and renewable fuel adoption strategies. However, the market will face increasing pressure from evolving transportation technologies and sustainability expectations.

Regulatory support is expected to remain a primary growth driver, although policy structures may become more performance-based, emphasizing carbon intensity reductions, feedstock sustainability, and environmental accountability.

Technological advancements in ethanol production, feedstock optimization, carbon capture integration, and second-generation biofuel development are expected to strengthen industry competitiveness and sustainability credentials.

The pace of electric vehicle adoption will remain a critical variable influencing long-term fuel demand projections and ethanol consumption growth across different geographic markets.

Climate-related risks, agricultural productivity challenges, and resource management concerns are likely to become increasingly important considerations for ethanol producers and policymakers.

Overall, the market is expected to remain strategically important within the global renewable energy landscape, but future success will increasingly depend on policy stability, sustainable feedstock management, technological innovation, infrastructure expansion, and the ability to adapt to changing transportation and energy market dynamics.

eration biofuel development are expected to strengthen industry competitiveness and sustainability credentials.

The pace of electric vehicle adoption will remain a critical variable influencing long-term fuel demand projections and ethanol consumption growth across different geographic markets.

Climate-related risks, agricultural productivity challenges, and resource management concerns are likely to become increasingly important considerations for ethanol producers and policymakers.

Overall, the market is expected to remain strategically important within the global renewable energy landscape, but future success will increasingly depend on policy stability, sustainable feedstock management, technological innovation, infrastructure expansion, and the ability to adapt to changing transportation and energy market dynamics.

Regulatory Landscape

Global Industrial Ethanol Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Industrial Ethanol Market is evolving rapidly as governments, environmental agencies, energy regulators, and industry bodies strengthen policies supporting renewable fuels, sustainable industrial production, and carbon emission reduction initiatives. Industrial ethanol plays a critical role in transportation fuels, chemical manufacturing, pharmaceuticals, personal care products, and industrial processing, making regulatory compliance essential across multiple end-use sectors.

Ethanol producers, feedstock suppliers, fuel distributors, chemical manufacturers, and industrial users must comply with a broad range of regulations related to renewable fuel standards, biofuel blending mandates, environmental sustainability, product quality requirements, transportation safety, and emissions management. Regulatory frameworks increasingly influence production strategies, investment decisions, and international trade activities.

As governments intensify efforts to achieve climate goals and reduce dependence on fossil fuels, industrial ethanol is receiving growing policy support through renewable energy programs, low-carbon fuel initiatives, and sustainable manufacturing incentives.

Global Industrial Ethanol Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is primarily shaped by renewable fuel standards and biofuel blending mandates implemented across major economies. Governments are requiring higher ethanol blending ratios in transportation fuels to reduce greenhouse gas emissions and improve energy security.

Carbon emission regulations are increasingly encouraging industries to adopt renewable and bio-based alternatives to conventional petroleum-derived products. Industrial ethanol is benefiting from policies aimed at supporting low-carbon fuels and sustainable industrial feedstocks.

Product quality and fuel specification standards continue to play a critical role in ensuring ethanol compatibility, performance, and safety across transportation and industrial applications. Regulatory authorities maintain strict requirements governing ethanol purity, composition, and distribution practices.

Environmental compliance regulations are becoming increasingly important as manufacturers face greater scrutiny regarding resource utilization, emissions management, wastewater treatment, and sustainable production practices.

In addition, international trade policies, agricultural regulations, and feedstock sustainability requirements continue to influence ethanol production economics, supply chain dynamics, and global market competitiveness.

Key Regulatory & Policy Environment Signals in Global Industrial Ethanol Market

- Renewable Fuel Standards (RFS):

Policies mandating the use of renewable fuels and supporting ethanol integration into transportation energy systems. - Biofuel Blending Mandates:

Government requirements establishing minimum ethanol blending levels in gasoline and transportation fuels. - Carbon Emission Reduction Regulations:

Frameworks promoting low-carbon fuels, industrial decarbonization, and greenhouse gas reduction initiatives. - Fuel Quality & Product Specification Standards:

Requirements governing ethanol purity, performance characteristics, storage, handling, and fuel compatibility. - Environmental Compliance & Sustainability Policies:

Regulations addressing emissions control, water management, waste reduction, and sustainable production practices. - Feedstock Sustainability & Agricultural Policies:

Guidelines supporting responsible sourcing of corn, sugarcane, wheat, and biomass feedstocks used in ethanol production.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging ethanol producers to invest in advanced production technologies, low-carbon manufacturing processes, and sustainable feedstock sourcing strategies. Regulatory compliance is becoming a key competitive differentiator across global ethanol markets.

Renewable fuel standards and blending mandates are driving capacity expansion projects, infrastructure investments, and long-term supply agreements throughout the ethanol value chain.

Carbon reduction regulations are encouraging manufacturers to adopt cleaner production methods, improve energy efficiency, and invest in carbon capture and emissions management technologies.

Environmental compliance requirements are increasing investments in wastewater treatment systems, resource optimization programs, and sustainability reporting initiatives to meet evolving regulatory expectations.

Feedstock sustainability policies are motivating industry participants to strengthen agricultural partnerships, improve traceability systems, and support responsible biomass sourcing practices that align with environmental objectives.

Global Industrial Ethanol Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Industrial Ethanol Market is expected to become increasingly supportive as governments accelerate renewable energy adoption and industrial decarbonization strategies.

Biofuel blending mandates are likely to expand across both developed and emerging economies, creating stronger demand for fuel-grade ethanol and supporting long-term market growth.

Carbon reduction policies are expected to strengthen further, encouraging broader adoption of bio-based fuels and sustainable industrial inputs while increasing compliance requirements for emissions-intensive industries.

Sustainability regulations will likely place greater emphasis on lifecycle carbon accounting, feedstock traceability, environmental performance monitoring, and responsible production practices throughout the ethanol value chain.

Overall, the future regulatory landscape will be defined by the convergence of renewable fuel standards, biofuel blending mandates, carbon emission regulations, environmental sustainability policies, and feedstock governance frameworks. Companies capable of delivering compliant, low-carbon, sustainable, and scalable ethanol solutions will be best positioned to capitalize on long-term opportunities within the expanding global industrial ethanol market.