Global Petrochemicals Market Report, Size & Forecast 2026-2033

Global Petrochemicals Market Size & Forecast

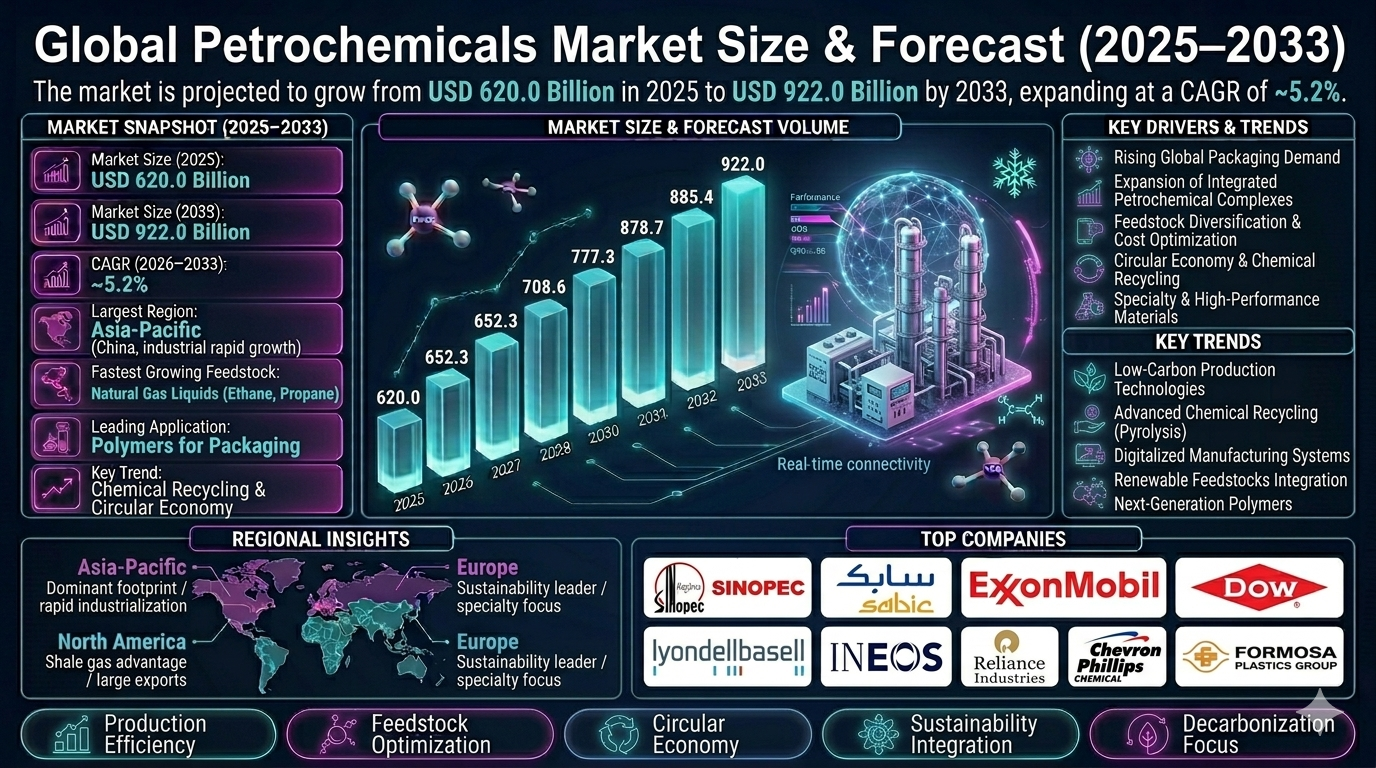

The global petrochemicals market is projected to witness substantial growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 620.0 billion in 2025 and is expected to reach nearly USD 922.0 billion by 2033, expanding at a CAGR of around 5.2%. The market growth is driven by increasing demand for polymers and specialty chemicals, rapid industrialization, rising packaging consumption, expanding downstream manufacturing industries, and growing investments in integrated refining and petrochemical production complexes worldwide. Petrochemicals are chemical products derived primarily from petroleum and natural gas feedstocks. These include olefins, aromatics, methanol, polymers, synthetic rubbers, and specialty chemicals used across packaging, automotive, construction, healthcare, electronics, and consumer goods industries. The market is experiencing significant transformation through feedstock diversification, digitalized manufacturing systems, low-carbon production technologies, and chemical recycling innovation. Additionally, rising global demand for sustainable plastics, lightweight materials, and advanced industrial chemicals is accelerating market expansion.

Global Petrochemicals Market Overview

The petrochemicals market forms a foundational segment of the global industrial chemicals sector, supporting essential manufacturing processes across nearly every major industry. The market includes olefins, aromatics, methanol derivatives, polymers, synthetic elastomers, and specialty performance chemicals. Manufacturers are increasingly focusing on production efficiency, feedstock optimization, circular economy integration, and advanced process automation to improve competitiveness. Technological innovation in steam cracking, propane dehydrogenation, chemical recycling, catalyst optimization, and process electrification is reshaping industry dynamics. Major market participants include Sinopec, SABIC, ExxonMobil Chemical, BASF SE, Dow Inc., LyondellBasell Industries, INEOS Group, Reliance Industries Limited, Chevron Phillips Chemical, and Formosa Plastics Group.Key Drivers of Global Petrochemicals Market Growth

Rising Global Packaging Demand

The growing need for flexible packaging, food packaging, industrial packaging, and consumer product protection is driving strong demand for petrochemical-derived polymers. Packaging remains the largest application segment globally.Expansion of Integrated Petrochemical Complexes

Large-scale refinery-to-chemical integration projects are improving supply chain efficiency, lowering operational costs, and increasing production flexibility. These projects are strengthening global petrochemical production capacity.Feedstock Diversification and Cost Optimization

Producers are increasingly leveraging ethane, propane, naphtha, recycled feedstocks, and renewable raw materials to improve production economics. This diversification enhances resilience against crude oil price volatility.Growth of Circular Economy and Chemical Recycling

Increasing investments in pyrolysis, depolymerization, and feedstock recycling technologies are enabling sustainable material recovery and circular polymer production. This supports regulatory compliance and sustainability targets.Rising Demand for Specialty and High-Performance Materials

Automotive electrification, medical device innovation, lightweight construction, and advanced electronics are increasing demand for specialty petrochemical materials. Higher-value product development is supporting industry profitability.Global Petrochemicals Market Segmentation

By Product

The market is segmented into olefins, aromatics, methanol & derivatives, polymers, synthetic rubbers & elastomers, and specialty chemicals. Olefins dominate the market due to their critical role in downstream polymer production.By Feedstock

The market includes naphtha, natural gas liquids, coal-based feedstocks, bio-based feedstocks, and recycled feedstock inputs. Natural gas liquids are witnessing significant growth due to favorable economics.By End-Use Industry

End-use industries include packaging, automotive, construction, electronics, healthcare, agriculture, and textiles. Packaging accounts for the largest market share globally.By Production Process

The market includes steam cracking, catalytic cracking, propane dehydrogenation, methanol-to-olefins, and advanced recycling conversion technologies. Steam cracking remains the dominant production technology.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global petrochemicals market due to rapid industrialization, expanding manufacturing capacity, and rising domestic demand. China, India, Japan, and South Korea are major contributors. China remains the largest regional producer and consumer.North America

North America holds a significant market share supported by abundant shale gas resources, low-cost ethane feedstocks, and advanced petrochemical infrastructure. The United States remains a major export-oriented production hub.Europe

Europe focuses on specialty chemicals, sustainability initiatives, and circular economy integration. Germany, France, and the Netherlands are major regional markets.Middle East & Africa

The Middle East continues to expand as a major petrochemical export hub due to abundant hydrocarbon feedstock availability and integrated production complexes. Saudi Arabia and the UAE lead regional growth.Latin America

Latin America is gradually expanding due to industrial development, regional manufacturing growth, and infrastructure investments. Brazil and Mexico remain key regional markets.Competitive Landscape

The global petrochemicals market is highly competitive and capital-intensive, with major players competing through production scale, feedstock integration, process efficiency, and technological innovation. Key companies include Sinopec, SABIC, ExxonMobil Chemical, BASF SE, Dow Inc., LyondellBasell Industries, INEOS Group, Reliance Industries Limited, Chevron Phillips Chemical, and Formosa Plastics Group. Sinopec remains the largest company in the global petrochemicals market due to its integrated refining and petrochemical production footprint. Companies are increasingly investing in circular production technologies, digitalized plant systems, and specialty product innovation.Strategic Outlook

The strategic outlook for the global petrochemicals market remains highly positive due to increasing industrial demand and sustainability-driven transformation. Future opportunities include low-carbon petrochemical production, chemical recycling, renewable feedstocks, specialty polymer development, and electrified processing technologies. Growing emphasis on decarbonization and circular plastics will significantly shape future market evolution. Manufacturers investing in process optimization, feedstock flexibility, and advanced material innovation are likely to strengthen competitive positioning.Final Market Perspective

The global petrochemicals market remains an essential backbone of modern industrial production and material innovation. Rising demand for polymers, specialty chemicals, sustainable materials, and advanced manufacturing solutions will continue driving market growth throughout the forecast period. Organizations that successfully combine production efficiency, sustainability integration, and downstream value creation will remain strongly positioned in the evolving global petrochemicals market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Petrochemicals Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Petrochemicals

- 2.2 Scope of the Study

- 2.3 Evolution of Petrochemical Manufacturing

- 2.4 Petrochemical Value Chain & Ecosystem

- 2.5 Feedstock Landscape & Raw Material Analysis

- 2.6 Regulatory & Sustainability Framework

- 2.7 Technology Innovation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Global Packaging Demand

- 4.1.2 Expansion of Integrated Petrochemical Complexes

- 4.1.3 Feedstock Diversification & Cost Optimization

- 4.1.4 Growth of Circular Economy & Chemical Recycling

- 4.1.5 Rising Demand for Specialty & High-Performance Materials

- 4.2 Restraints

- 4.2.1 Volatility in Crude Oil & Natural Gas Prices

- 4.2.2 Stringent Environmental Regulations

- 4.2.3 High Capital Investment Requirements

- 4.2.4 Supply Chain & Feedstock Availability Constraints

- 4.3 Opportunities

- 4.3.1 Renewable Feedstock Integration

- 4.3.2 Low-Carbon Production Technologies

- 4.3.3 Advanced Chemical Recycling Solutions

- 4.3.4 Expansion of Specialty Polymer Applications

- 4.4 Challenges

- 4.4.1 Decarbonization Pressures

- 4.4.2 Waste Management & Plastic Circularity

- 4.4.3 Energy-Intensive Production Processes

- 4.4.4 Global Overcapacity Risks

- 4.1 Drivers

- 5. Global Petrochemicals Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Production & Consumption Analysis

- 5.5 Technology Adoption Trends

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Product

- 6.1.1 Olefins

- 6.1.2 Aromatics

- 6.1.3 Methanol & Derivatives

- 6.1.4 Polymers

- 6.1.5 Synthetic Rubbers & Elastomers

- 6.1.6 Specialty Chemicals

- 6.2 By Feedstock

- 6.2.1 Naphtha

- 6.2.2 Natural Gas Liquids

- 6.2.3 Coal-Based Feedstocks

- 6.2.4 Bio-Based Feedstocks

- 6.2.5 Recycled Feedstock Inputs

- 6.3 By End-Use Industry

- 6.3.1 Packaging

- 6.3.2 Automotive

- 6.3.3 Construction

- 6.3.4 Electronics

- 6.3.5 Healthcare

- 6.3.6 Agriculture

- 6.3.7 Textiles

- 6.4 By Production Process

- 6.4.1 Steam Cracking

- 6.4.2 Catalytic Cracking

- 6.4.3 Propane Dehydrogenation

- 6.4.4 Methanol-to-Olefins

- 6.4.5 Advanced Recycling Conversion Technologies

- 6.1 By Product

- 7. Market Segmentation by Geography

- 7.1 Asia-Pacific

- 7.2 North America

- 7.3 Europe

- 7.4 Middle East & Africa

- 7.5 Latin America

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Production Capacity Benchmarking

- 8.3 Technology Innovation Analysis

- 8.4 Strategic Partnerships & Capacity Expansion

- 8.5 Sustainability & Circular Economy Strategies

- 9. Company Profiles

- 9.1 Sinopec

- 9.2 SABIC

- 9.3 ExxonMobil Chemical

- 9.4 BASF SE

- 9.5 Dow Inc.

- 9.6 LyondellBasell Industries

- 9.7 INEOS Group

- 9.8 Reliance Industries Limited

- 9.9 Chevron Phillips Chemical

- 9.10 Formosa Plastics Group

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Global Demand Forecast Engine

- 10.2 Feedstock Cost Optimization Analyzer

- 10.3 Circular Economy Integration Tracker

- 10.4 Carbon Emissions Monitoring Dashboard

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Low-Carbon Production Technologies

- 11.2 Investment in Chemical Recycling Infrastructure

- 11.3 Strengthening Feedstock Flexibility

- 11.4 Development of Specialty Material Portfolios

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Petrochemicals Market Competitive Intensity & Market Structure Overview

The global petrochemicals market is highly consolidated, capital-intensive, and strategically competitive, characterized by the presence of large integrated oil, gas, and chemical corporations competing on production scale, feedstock access, process efficiency, downstream integration, and sustainability-driven innovation.

The market structure is dominated by multinational petrochemical producers, national oil companies, and regional integrated refining-to-chemical operators. These participants leverage extensive infrastructure, feedstock security, advanced process technologies, and global supply chain capabilities to maintain market leadership.

Increasing global polymer demand, rapid expansion of integrated petrochemical complexes, rising investments in circular economy technologies, and evolving sustainability regulations are significantly intensifying competition across the global petrochemicals market.

Global Petrochemicals Market Competitive Intensity & Market Structure Current Scenario

Leading Global Petrochemical Companies

Sinopec: The largest global petrochemical producer with extensive refining integration, diversified product portfolio, and strong manufacturing footprint across Asia.

SABIC: Major Middle Eastern petrochemical leader with strong feedstock advantages, integrated production assets, and growing specialty chemical capabilities.

ExxonMobil Chemical: Global leader with advanced refining-petrochemical integration and strong process innovation capabilities.

BASF SE: Diversified chemical manufacturer focused on specialty petrochemicals, process optimization, and sustainability-oriented product innovation.

Dow Inc.: Major global producer with strong downstream polymer integration and advanced materials innovation expertise.

LyondellBasell Industries: Leading polyolefins and petrochemical producer recognized for large-scale integrated operations and circular plastics investments.

INEOS Group: Significant petrochemical operator with broad olefins, aromatics, and polymer production assets across multiple geographies.

Reliance Industries Limited: Major Asian integrated refining and petrochemical producer with strong domestic and export-oriented production capacity.

Chevron Phillips Chemical: Key global producer with strong North American feedstock advantage and advanced polymer production technologies.

Formosa Plastics Group: Major Asian petrochemical player with vertically integrated production and strong regional market influence.

Key Competitive Intensity & Market Structure Drivers

Feedstock availability and pricing remain primary competitive differentiators, particularly for companies benefiting from low-cost natural gas liquids, ethane, and integrated refinery operations.

The expansion of refinery-to-chemical integration projects is increasing production efficiency and intensifying competition among large-scale petrochemical manufacturers.

Technological advancements in steam cracking optimization, propane dehydrogenation, process electrification, and digital plant automation are becoming increasingly critical for competitive positioning.

Growing regulatory pressure surrounding carbon emissions and plastic waste management is driving competition in sustainable production technologies and circular material solutions.

Rising downstream demand for specialty polymers, advanced elastomers, and high-performance materials is encouraging product portfolio diversification.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are aggressively investing in integrated petrochemical complexes to improve operational efficiency, reduce production costs, and strengthen feedstock flexibility.

Strategic expansion into specialty chemicals and high-value downstream materials is becoming essential for margin enhancement and market differentiation.

Investments in chemical recycling, renewable feedstock integration, and circular plastics production are increasingly shaping long-term competitive strategies.

Digital transformation through AI-based plant optimization, predictive maintenance, and real-time operational analytics is enhancing process efficiency and reliability.

Strategic partnerships across the value chain, including collaborations with packaging, automotive, and consumer goods manufacturers, are strengthening market resilience.

Global Petrochemicals Market Competitive Intensity & Market Structure Forward Outlook

The global petrochemicals market is expected to remain highly competitive as industrial demand continues expanding alongside increasing sustainability expectations.

Future competition will increasingly focus on low-carbon petrochemical production, advanced recycling technologies, bio-based feedstock utilization, and electrified manufacturing systems.

Asia-Pacific and the Middle East are expected to remain dominant competitive growth regions due to ongoing capacity expansions and favorable feedstock economics.

Circular economy integration and specialty materials innovation are expected to create significant long-term competitive opportunities.

Overall, companies that successfully combine production scale, technological innovation, sustainability integration, and downstream value creation will remain strongly positioned in the evolving global petrochemicals market.

Value Chain

Global Petrochemicals Market Value Chain & Supply Chain Evolution Overview

The global petrochemicals market value chain is undergoing substantial transformation as rising industrial demand, downstream manufacturing expansion, feedstock diversification, and sustainability-driven innovation reshape the global chemical production ecosystem. Petrochemicals remain the foundational building blocks of modern industrial manufacturing, enabling production across packaging, automotive, construction, electronics, healthcare, agriculture, textiles, and consumer goods industries.

The petrochemicals value chain spans hydrocarbon extraction, feedstock processing, refining integration, chemical conversion, polymer production, specialty material manufacturing, downstream industrial processing, and end-user product applications. This interconnected ecosystem links upstream oil and gas producers, refining companies, petrochemical processors, catalyst developers, logistics operators, recycling technology providers, and downstream manufacturers.

Major companies including Sinopec, SABIC, ExxonMobil Chemical, BASF SE, Dow Inc., LyondellBasell Industries, INEOS Group, Reliance Industries Limited, Chevron Phillips Chemical, and Formosa Plastics Group are heavily investing in feedstock optimization, integrated refinery-to-chemical infrastructure, digitalized manufacturing systems, low-carbon production technologies, and circular petrochemical solutions to strengthen long-term competitiveness.

Upstream supply chain activities depend on crude oil extraction, natural gas liquids processing, hydrocarbon transportation, and feedstock storage infrastructure. Midstream operations involve refining, steam cracking, catalytic conversion, propane dehydrogenation, methanol processing, and chemical separation technologies. Downstream activities include polymer manufacturing, specialty chemical conversion, industrial processing, logistics distribution, and end-use product manufacturing integration.

Operational priorities across the petrochemicals value chain increasingly focus on feedstock flexibility, production efficiency, process electrification, digital automation, carbon footprint reduction, and circular material recovery. However, the industry continues to face challenges related to feedstock price volatility, regulatory pressure, decarbonization requirements, infrastructure intensity, and geopolitical supply chain disruptions.

Global Petrochemicals Market Value Chain & Supply Chain Evolution Current Scenario

The current petrochemicals market is being shaped by increasing global consumption of polymers and specialty chemicals, expansion of integrated petrochemical complexes, and accelerated investments in circular production technologies. Demand from packaging, automotive lightweighting, electronics manufacturing, and construction applications continues to drive sustained production growth.

Asia-Pacific dominates the global petrochemicals ecosystem due to strong industrialization, large-scale production infrastructure, and expanding downstream manufacturing demand. China remains the world???s largest producer and consumer, supported by aggressive capacity additions and integrated refining-to-chemicals expansion.

North America benefits from low-cost shale-derived feedstocks and extensive ethane cracking infrastructure, positioning the region as a globally competitive production hub. Europe is increasingly focused on specialty petrochemicals, sustainability-driven process innovation, and circular plastics integration.

The Middle East continues to strengthen its global role through export-oriented integrated petrochemical complexes supported by abundant hydrocarbon resources and strategic industrial diversification initiatives.

Producers are increasingly adopting advanced digital manufacturing systems, predictive analytics, process automation, and catalyst optimization technologies to improve operational efficiency and reduce costs. Simultaneously, chemical recycling infrastructure and renewable feedstock integration are becoming critical strategic priorities.

Key Value Chain & Supply Chain Evolution Signals in Global Petrochemicals Market

One of the most significant transformation signals is the rapid expansion of integrated refinery-to-chemical complexes. These facilities improve feedstock efficiency, maximize product flexibility, and strengthen operational economics by reducing supply chain fragmentation.

Another major signal is the accelerating shift toward feedstock diversification. Producers are increasingly leveraging ethane, propane, methanol, renewable raw materials, and recycled feedstocks to improve resilience against crude oil market volatility.

The growth of chemical recycling technologies is reshaping the value chain. Advanced pyrolysis, depolymerization, and feedstock recycling systems are enabling circular material recovery and reducing reliance on virgin hydrocarbon feedstocks.

Digital transformation is also significantly influencing operational strategies. AI-enabled process optimization, predictive maintenance, digital twin systems, and automated process control are improving plant performance and reducing operational downtime.

Sustainability pressures are driving investments in low-carbon petrochemical production technologies, carbon capture systems, electrified crackers, and renewable energy integration across production facilities.

Demand growth for specialty and performance-oriented materials is another key market signal, with industries such as EV manufacturing, healthcare, electronics, and advanced packaging increasingly requiring high-performance petrochemical derivatives.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Petrochemicals Market

Leading petrochemical companies are increasingly prioritizing integrated production systems, feedstock flexibility, advanced process technologies, and sustainability-focused innovation to strengthen competitive advantage. Competitive differentiation is increasingly determined by operational scale, technology adoption, feedstock economics, and carbon management capabilities.

Companies with integrated refining and petrochemical operations are expected to maintain strong strategic advantages through lower production costs, supply chain resilience, and downstream value capture.

Investment in circular economy infrastructure is becoming a critical strategic imperative. Companies integrating advanced recycling technologies and circular polymer solutions are likely to strengthen regulatory compliance and long-term market relevance.

Strategic partnerships between petrochemical producers, recycling technology firms, catalyst developers, and downstream industrial manufacturers are becoming increasingly important for accelerating innovation and expanding market opportunities.

Digital manufacturing transformation is emerging as a major competitive factor. Companies leveraging AI-driven process optimization, smart manufacturing systems, and digital plant integration are expected to achieve stronger efficiency gains and operational reliability.

Sustainability leadership is becoming a defining market differentiator. Manufacturers investing in renewable feedstocks, low-emission technologies, and decarbonized process infrastructure are likely to improve long-term positioning as environmental regulations intensify globally.

Global Petrochemicals Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the petrochemicals value chain is expected to become more integrated, digitally optimized, and sustainability-oriented. Rising demand for polymers, specialty chemicals, and lightweight materials will continue driving large-scale production expansion globally.

Feedstock diversification will accelerate as producers increasingly integrate renewable feedstocks, recycled hydrocarbons, and alternative chemical pathways to improve supply flexibility and reduce environmental exposure.

Digital technologies including AI-powered plant optimization, digital twins, autonomous process monitoring, and predictive maintenance systems will increasingly transform operational efficiency across petrochemical facilities.

Chemical recycling is expected to become mainstream, enabling circular polymer production and reducing dependency on virgin feedstocks. Large-scale commercial deployment of advanced recycling systems will significantly reshape supply chain structures.

Low-carbon production technologies such as electrified steam cracking, carbon capture integration, green hydrogen utilization, and renewable energy-powered manufacturing systems will become increasingly important as decarbonization pressures intensify.

Emerging integrated petrochemical hubs across Asia-Pacific, North America, and the Middle East will continue strengthening regional production competitiveness and global supply resilience.

Ultimately, the future petrochemicals value chain will evolve into a more intelligent, circular, low-carbon, and highly integrated industrial ecosystem capable of supporting global manufacturing demand while advancing sustainability and resource efficiency objectives.

Market-Specific Value Chain

- Hydrocarbon Extraction & Feedstock Supply: Crude oil extraction, natural gas liquids processing, feedstock storage, transportation infrastructure, and hydrocarbon logistics.

- Primary Petrochemical Conversion: Refining integration, steam cracking, catalytic cracking, propane dehydrogenation, methanol conversion, and catalyst-driven processing systems.

- Chemical Separation & Intermediate Processing: Olefin and aromatic separation, purification systems, process optimization, and intermediate product stabilization.

- Downstream Chemical & Polymer Manufacturing: Polyolefins, specialty chemicals, synthetic elastomers, methanol derivatives, and advanced material production.

- Industrial Distribution & End-Use Integration: Packaging, automotive, construction, electronics, healthcare, agriculture, and consumer product manufacturing applications.

- Circular Innovation & Sustainability Optimization: Chemical recycling, renewable feedstock integration, carbon capture systems, electrified processing, and low-carbon manufacturing technologies.

Company-to-Stage Mapping

- Hydrocarbon Extraction & Feedstock Supply: ExxonMobil, Shell, Saudi Aramco, Reliance Industries, major upstream hydrocarbon producers.

- Primary Petrochemical Conversion: Sinopec, SABIC, Chevron Phillips Chemical, INEOS Group, ExxonMobil Chemical.

- Chemical Separation & Intermediate Processing: BASF SE, LyondellBasell Industries, process technology licensors, catalyst engineering companies.

- Downstream Chemical & Polymer Manufacturing: Dow Inc., Formosa Plastics Group, Braskem, BASF SE, specialty polymer producers.

- Industrial Distribution & End-Use Integration: Packaging converters, automotive material suppliers, electronics manufacturers, industrial chemical distributors.

- Circular Innovation & Sustainability Optimization: Chemical recycling technology firms, low-carbon process innovators, carbon capture solution providers, renewable feedstock developers.

Investment Activity

Global Petrochemicals Market Investment & Funding Dynamics Overview

Investment activity in the global petrochemicals market is accelerating significantly due to expanding downstream chemical demand, increasing refinery-to-chemical integration projects, rising adoption of circular petrochemical technologies, and growing investments in low-carbon production infrastructure. Between 2026 and 2033, capital allocation is expected to increasingly target integrated petrochemical complexes, advanced recycling systems, feedstock diversification technologies, digitalized production facilities, and sustainable chemical manufacturing platforms.

The petrochemicals market remains one of the most strategically critical segments of the global industrial economy. Energy companies, chemical manufacturers, sovereign wealth funds, infrastructure investors, and institutional capital providers are actively increasing investments to expand production capacity, optimize feedstock utilization, and secure long-term competitiveness in a transforming materials landscape.

A major structural transformation influencing investment dynamics is the global shift from conventional volume-based petrochemical production toward integrated, digitally optimized, and sustainability-driven manufacturing ecosystems. This transition is driving large-scale funding into process electrification, chemical recycling infrastructure, carbon capture integration, and circular feedstock systems.

The market is also benefiting from rising investments in specialty chemicals, renewable feedstock conversion, advanced catalytic process technologies, and AI-enabled plant automation. Growing regulatory pressure around emissions reduction and plastics circularity is reshaping capital deployment strategies globally.

Current Investment & Funding Landscape

Current funding activity in the petrochemicals market is strongly supported by refinery modernization projects, large-scale integrated petrochemical complex construction, advanced cracking technology upgrades, and circular plastics infrastructure development. Companies are actively investing in digital process optimization, feedstock flexibility enhancement, production efficiency upgrades, and low-emission operating systems.

- Asia-Pacific: Dominates global investment activity due to extensive petrochemical capacity expansion, rising domestic industrial demand, and large-scale integrated production infrastructure projects across China, India, South Korea, and Southeast Asia.

- North America: Witnessing strong capital deployment driven by shale-based feedstock advantages, export-oriented production expansion, and digitalized petrochemical facility investments.

- Middle East: Emerging as a major global investment hub due to refinery-to-chemical integration strategies, hydrocarbon resource availability, and economic diversification programs.

- Europe: Attracting targeted funding focused on sustainability transformation, circular chemical manufacturing, specialty chemical innovation, and decarbonization initiatives.

Key Investment & Funding Drivers

- Growing global packaging and polymer demand is increasing investment in olefins and downstream petrochemical production capacity.

- Expansion of integrated refining and petrochemical complexes is driving large-scale infrastructure capital allocation.

- Feedstock diversification initiatives are accelerating investments in ethane, propane, renewable feedstocks, and recycled material processing systems.

- Circular economy mandates are increasing funding for chemical recycling and advanced polymer recovery technologies.

- Digital transformation is driving investments in AI-enabled process optimization and predictive plant operations.

- Low-carbon production technologies are attracting ESG-focused institutional investment.

- Rising specialty chemical demand is supporting high-value product development and advanced material innovation funding.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of combining production scale with sustainability-focused operational transformation.

- Technology leadership in chemical recycling, process electrification, and advanced catalytic systems is becoming a critical competitive differentiator.

- Vertical integration across refining, petrochemical production, and downstream specialty chemical manufacturing is strengthening investment attractiveness.

- Strategic feedstock security and supply chain resilience are becoming central to long-term investor confidence.

- Companies investing in circular production ecosystems are expected to achieve stronger regulatory and commercial positioning.

- Regional diversification strategies remain essential for balancing feedstock economics and demand exposure.

- Organizations integrating digital plant intelligence and energy-efficient systems are likely to attract stronger operational efficiency-focused capital.

Forward Investment Outlook

The global petrochemicals market is expected to maintain strong long-term investment momentum due to rising industrial material demand, increasing downstream chemical applications, and accelerating sustainability-driven transformation.

Future funding activity is expected to prioritize advanced steam cracking systems, low-carbon production infrastructure, renewable feedstock integration, digitalized process control platforms, circular plastics ecosystems, and carbon capture-enabled petrochemical manufacturing.

- Asia-Pacific: Will remain the largest investment hub due to sustained industrial expansion and aggressive petrochemical infrastructure development.

- Middle East: Will continue strengthening its global role through integrated export-oriented petrochemical expansion strategies.

- North America: Will expand through feedstock-driven production growth and next-generation digital petrochemical facility investments.

Future innovation investments are also expected across electrified cracking systems, AI-driven operational optimization, advanced molecular recycling technologies, bio-based petrochemical feedstocks, and carbon-neutral manufacturing processes.

The convergence of industrial growth, sustainability imperatives, and advanced process innovation will continue reshaping investment priorities across the petrochemicals market.

Overall, the market is expected to remain one of the most capital-intensive and strategically attractive long-term industrial investment sectors, with organizations combining production efficiency, circular economy integration, and technology innovation positioned to lead through 2033.

Technology & Innovation

Propylene Market Technology & Innovation Landscape Overview

The global propylene market is undergoing substantial technological transformation driven by innovations in catalytic processing, feedstock optimization, low-carbon production systems, and digitalized petrochemical operations. The evolution of propylene production technologies is increasingly focused on improving process efficiency, enhancing yield optimization, reducing carbon emissions, and supporting the growing demand for high-purity propylene across downstream industrial applications.

Modern propylene production technologies are integrating advanced catalytic reactors, real-time process monitoring systems, and energy-efficient separation technologies to maximize operational output while minimizing feedstock losses. These advancements are significantly improving production economics and sustainability performance across global petrochemical facilities.

The market is also witnessing strong adoption of propane dehydrogenation innovation, AI-driven plant optimization, carbon capture integration, and circular feedstock utilization strategies that are reshaping the future of propylene manufacturing.

Propylene Market Technology & Innovation Current Scenario

Currently, propylene innovation is centered around improving process efficiency and expanding on-purpose production capabilities. Propane dehydrogenation (PDH) technology has emerged as one of the most significant advancements, enabling dedicated propylene production with higher operational flexibility and reduced dependence on traditional refinery by-product generation.

Advanced catalyst development is improving conversion efficiency, extending catalyst life cycles, and reducing operational downtime. New-generation dehydrogenation catalysts offer improved selectivity and lower energy consumption compared to conventional systems.

Steam cracking optimization technologies are increasingly leveraging advanced heat recovery systems, digital combustion control, and predictive maintenance solutions to enhance production efficiency and operational reliability.

Artificial intelligence and machine learning applications are being deployed for real-time process optimization, feedstock balancing, predictive maintenance scheduling, and yield forecasting across integrated petrochemical complexes.

Carbon reduction technologies such as electrified cracking systems, carbon capture utilization, and low-emission hydrogen integration are gaining strategic importance as producers seek to meet global decarbonization targets.

Bio-based propylene development is also advancing through renewable feedstock conversion technologies, offering sustainable alternatives to fossil-derived production pathways.

Key Technology & Innovation Trends in Propylene Market

- Propane Dehydrogenation (PDH) Systems: Dedicated high-efficiency propylene production with enhanced feedstock flexibility.

- Advanced Catalytic Engineering: Improved catalyst selectivity, durability, and lower energy requirements.

- AI-Driven Process Optimization: Real-time production monitoring and predictive operational control.

- Electrified Steam Cracking: Low-emission thermal cracking systems for sustainable production.

- Carbon Capture Integration: Technologies reducing emissions across propylene manufacturing operations.

- Digital Twin Technology: Virtual process simulation for performance optimization and operational planning.

- Renewable Feedstock Conversion: Bio-based pathways for sustainable propylene production.

- Advanced Heat Recovery Systems: Improved thermal efficiency and reduced operational energy costs.

- Circular Petrochemical Processing: Recycled hydrocarbon feedstock integration for lower environmental impact.

- Smart Refinery Automation: Intelligent plant control systems enhancing yield consistency and reliability.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the propylene market by shifting competition from capacity expansion alone toward process efficiency, sustainability performance, and feedstock flexibility.

Manufacturers investing in next-generation PDH technology and digitalized plant operations are achieving stronger competitive differentiation through higher production reliability, improved cost efficiency, and enhanced environmental compliance.

The rise of circular petrochemical systems and renewable feedstock processing is creating new growth opportunities as industries increasingly prioritize sustainable material supply chains.

However, high capital investment requirements, catalyst development complexity, infrastructure modernization costs, and regulatory compliance challenges remain critical barriers to widespread adoption of advanced propylene production technologies.

Propylene Market Technology & Innovation Forward Outlook

The future of propylene technology is expected to move toward fully digitalized, low-carbon, and highly integrated production ecosystems capable of maximizing efficiency while minimizing environmental impact.

Emerging innovations include autonomous refinery optimization systems, next-generation electrified cracking reactors, AI-powered feedstock flexibility platforms, and advanced carbon-neutral propylene manufacturing pathways.

Bio-propylene and chemically recycled feedstock integration are expected to play increasingly important roles in future production strategies as sustainability regulations intensify globally.

The integration of machine learning, advanced simulation platforms, and smart plant orchestration technologies is expected to accelerate operational innovation across the propylene value chain.

Overall, the global propylene market is evolving toward a highly sophisticated technological ecosystem combining catalytic science, digital engineering, sustainability innovation, and intelligent process automation to redefine petrochemical production efficiency worldwide.

Market Risk

Global Petrochemicals Market Risk Factors & Disruption Threats Overview

The global petrochemicals market continues to expand as a critical backbone of industrial manufacturing, packaging, automotive production, construction materials, and consumer goods applications. Despite strong long-term growth potential, the market faces substantial structural risks and disruption threats driven by environmental regulations, feedstock volatility, overcapacity concerns, geopolitical instability, and accelerating sustainability transformation.

One of the most significant risks impacting the petrochemicals market is crude oil and natural gas feedstock price volatility. Since petrochemical production economics are directly linked to hydrocarbon pricing, fluctuations in global energy markets can significantly affect operating margins, pricing competitiveness, and production planning.

Environmental and regulatory pressure represents another major disruption factor. Governments worldwide are imposing stricter carbon emissions standards, plastic waste reduction mandates, and sustainability regulations that are forcing petrochemical manufacturers to invest heavily in low-carbon technologies, recycling systems, and circular production models.

The growing global shift toward circular economy practices presents long-term demand disruption for virgin petrochemical products. Increasing adoption of recycled polymers, bio-based alternatives, and advanced material substitution could gradually reduce dependence on traditional fossil-based petrochemicals.

Overcapacity risk is also becoming increasingly significant. Large-scale investments in integrated refining and petrochemical complexes, particularly in Asia-Pacific and the Middle East, could create regional supply imbalances and downward pricing pressure.

Geopolitical instability and international trade restrictions remain critical operational threats, particularly for export-oriented producers dependent on cross-border raw material flows and downstream market access.

Additionally, public scrutiny regarding plastic pollution and carbon-intensive manufacturing may influence consumer behavior, regulatory intervention, and corporate sustainability requirements across downstream industries.

Global Petrochemicals Market Risk Factors & Disruption Threats Current Scenario

The current petrochemicals market is characterized by strong demand growth from packaging, automotive, healthcare, and electronics sectors, particularly across emerging economies.

At the same time, producers are facing increasing margin pressure due to fluctuating feedstock costs, energy price inflation, and slower downstream industrial recovery in certain mature markets.

Circular plastics initiatives are accelerating globally, prompting significant investment in chemical recycling technologies, pyrolysis systems, and waste-to-feedstock conversion platforms.

Many leading companies are implementing decarbonization strategies through electrified crackers, carbon capture integration, renewable feedstock adoption, and advanced catalyst optimization.

However, these sustainability transitions require substantial capital investment and operational restructuring, creating financial pressure for smaller and mid-sized market participants.

Regional trade uncertainties and logistics bottlenecks continue to influence feedstock availability and export competitiveness across major petrochemical hubs.

Global Petrochemicals Market Key Risk Factors & Disruption Threat Signals

- Feedstock Price Volatility: Crude oil and natural gas fluctuations impacting production economics.

- Carbon Regulation Pressure: Emissions compliance increasing capital and operational costs.

- Plastic Waste Reduction Policies: Regulatory restrictions affecting downstream polymer demand.

- Circular Economy Disruption: Growth of recycling and bio-based alternatives reducing virgin product dependence.

- Regional Overcapacity Risk: Excess production capacity creating pricing pressure.

- Geopolitical Trade Instability: Cross-border supply chain and export disruption risks.

- High Capital Intensity: Significant investment required for modernization and sustainability upgrades.

- Public Sustainability Scrutiny: Negative perception of petrochemical-derived plastics influencing demand patterns.

- Energy Cost Inflation: Rising utility and process energy costs affecting competitiveness.

- Technology Transition Risk: Slow adoption of low-carbon technologies reducing future market relevance.

Strategic Implications of Risk Factors

Petrochemical manufacturers must prioritize feedstock flexibility and integrated production optimization to mitigate exposure to energy market volatility.

Investment in chemical recycling, renewable feedstock integration, and low-emission process technologies will become essential for maintaining regulatory compliance and long-term competitiveness.

Companies should increasingly diversify product portfolios toward specialty chemicals and high-performance materials that offer stronger margins and lower exposure to commodity pricing pressure.

Digitalization and advanced process automation can help improve operational efficiency, reduce energy consumption, and support predictive maintenance strategies.

Strategic downstream integration and regional production diversification will also play a critical role in improving supply chain resilience and reducing geopolitical exposure.

Global Petrochemicals Market Forward Risk Outlook

Looking ahead to 2026???2033, the petrochemicals market will remain essential to industrial manufacturing but increasingly shaped by sustainability-driven transformation and technological disruption.

Circular production models, electrified processing systems, and advanced recycling technologies are expected to become major competitive differentiators.

Producers that fail to align with decarbonization requirements and evolving environmental regulations may face declining market relevance and increased compliance burdens.

Regions with strong feedstock access, advanced infrastructure, and proactive sustainability investment are expected to maintain long-term structural advantages.

Overall, future market leadership will depend on operational efficiency, low-carbon innovation, circular economy integration, and strategic downstream value creation.

Regulatory Landscape

Global Petrochemicals Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global petrochemicals market is shaped by industrial chemical safety standards, environmental emissions regulations, carbon reduction mandates, feedstock governance policies, and circular economy initiatives. As one of the most critical industrial sectors globally, petrochemicals are subject to extensive regulatory oversight covering production operations, hazardous material management, energy efficiency, waste disposal, and environmental sustainability.

Governments and regulatory bodies worldwide focus on controlling industrial emissions, ensuring safe transportation and storage of petrochemical products, promoting sustainable feedstock usage, and enforcing strict workplace safety requirements. Regulatory frameworks also increasingly address greenhouse gas reduction, resource efficiency, and plastic waste management due to growing environmental concerns.

In recent years, policy attention has shifted toward low-carbon petrochemical production, chemical recycling, renewable feedstocks, and decarbonization technologies as industries align with international climate commitments and net-zero transition strategies.

Global Petrochemicals Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for petrochemicals combines traditional industrial safety and environmental compliance requirements with emerging sustainability-focused regulations. Production facilities are required to meet rigorous operational safety, process monitoring, emissions reporting, and hazardous substance handling standards.

In the United States, petrochemical operations are regulated under Environmental Protection Agency (EPA) air and water quality regulations, Occupational Safety and Health Administration (OSHA) process safety management standards, and Department of Transportation (DOT) hazardous material transportation rules. Refinery and chemical operators must also comply with Clean Air Act requirements and greenhouse gas reporting obligations.

In Europe, the sector is governed by REACH regulations, the Industrial Emissions Directive (IED), Seveso III Directive, and the European Union Emissions Trading System (EU ETS). The region is also aggressively advancing circular economy legislation aimed at reducing virgin petrochemical dependence and increasing recycled content integration.

Asia-Pacific, particularly China, Japan, South Korea, and India, regulates petrochemical production through industrial emissions control frameworks, chemical safety regulations, and national decarbonization policies. China???s tightening environmental compliance standards are significantly reshaping regional production practices.

Middle Eastern and Latin American petrochemical markets are increasingly strengthening environmental oversight while supporting capacity expansion through industrial diversification programs and export-oriented policy incentives.

Key Regulatory & Policy Environment Signals in Global Petrochemicals Market

- Industrial Emissions Regulations: Tightening restrictions on greenhouse gases, VOC emissions, wastewater discharge, and industrial pollutants are influencing plant modernization strategies.

- Chemical Safety and Hazardous Material Compliance: Strict regulations govern petrochemical production, storage, transport, and worker exposure management.

- Carbon Reduction and Decarbonization Policies: Carbon pricing systems, emissions trading frameworks, and energy transition mandates are reshaping production economics.

- Circular Economy and Plastic Waste Policies: Regulations promoting recycling, recycled content mandates, and plastic waste reduction are impacting downstream demand patterns.

- Feedstock Sustainability Standards: Increasing policy support for renewable and recycled feedstocks is encouraging diversification away from conventional fossil-based inputs.

- Energy Efficiency Compliance: Mandatory industrial energy optimization requirements are accelerating adoption of advanced process control technologies.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is significantly influencing capital allocation, technology investment, and operational strategies across the petrochemicals value chain. Producers are increasingly prioritizing low-emission production technologies, electrified processing systems, and advanced catalyst optimization to remain compliant and competitive.

Environmental compliance pressures are accelerating adoption of carbon capture, utilization and storage (CCUS), feedstock flexibility initiatives, and digitalized process monitoring systems to improve sustainability performance and operational efficiency.

Circular economy regulations are encouraging stronger collaboration between petrochemical manufacturers, recyclers, packaging producers, and downstream converters to create closed-loop material systems and enhance resource recovery capabilities.

At the same time, policy incentives supporting renewable feedstocks and chemical recycling are opening new growth pathways for companies investing in next-generation sustainable petrochemical production platforms.

Global Petrochemicals Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global petrochemicals market is expected to become increasingly carbon-centric, sustainability-driven, and innovation-focused. Governments are likely to implement stricter emissions thresholds while expanding incentives for low-carbon industrial transformation.

Carbon pricing mechanisms, mandatory sustainability disclosures, and circular plastics legislation are expected to play a larger role in shaping competitive dynamics and long-term investment strategies.

Policy support for advanced recycling technologies, renewable feedstock utilization, hydrogen integration, and electrified chemical processing is expected to strengthen across major production regions.

International climate commitments and industrial decarbonization roadmaps will continue driving regulatory alignment around sustainable petrochemical production standards.

Overall, regulatory and policy developments will remain a defining force for the petrochemicals market, with companies investing early in compliance-ready infrastructure, process decarbonization, and circular production capabilities expected to maintain long-term competitive advantage.