Global Industrial Ethanol Market Report, Size & Forecast 2026-2033

Global Industrial Ethanol Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 118.50 Billion |

| Market Size (2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 192.80 Billion |

| CAGR (2026???2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? 6.28% |

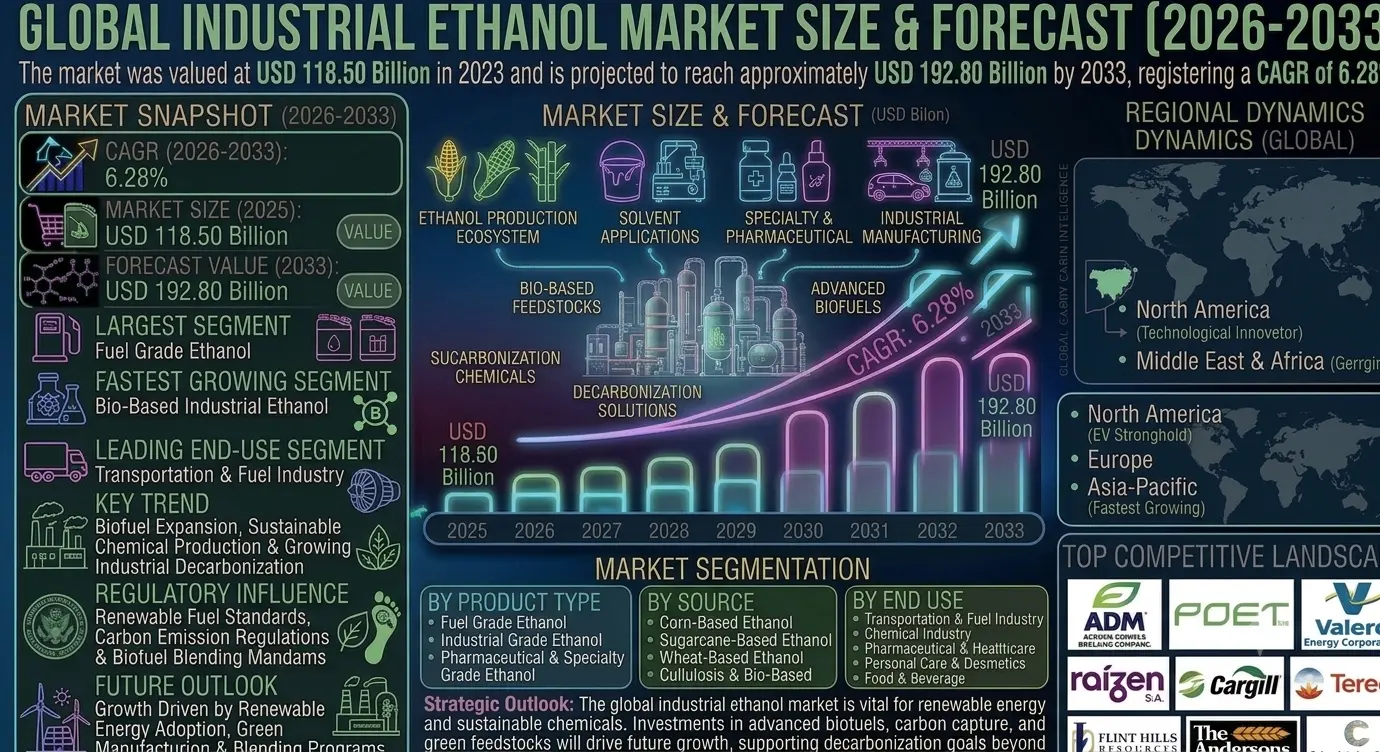

| Largest Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Fuel Grade Ethanol |

| Fastest Growing Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Bio-Based Industrial Ethanol |

| Leading End-Use Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Transportation & Fuel Industry |

| Key Trend | ?? ?? ?? ?? ?? ?? ?? ??Biofuel Expansion, Sustainable Chemical Production & Growing Industrial Decarbonization Initiatives |

| Regulatory Influence | ?? ?? ?? ?? ?? ?? ?? Renewable Fuel Standards, Carbon Emission Regulations & Biofuel Blending Mandates |

| Future Outlook | Growth Driven by Renewable Energy Adoption, Green Manufacturing Practices & Increasing Ethanol Blending Programs |

Global Industrial Ethanol Market Size & Forecast

The Global Industrial Ethanol Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 118.50 billion in 2025 and is projected to reach approximately USD 192.80 billion by 2033, registering a CAGR of 6.28%. Market growth is primarily driven by increasing demand for renewable fuels, rising adoption of ethanol-based industrial chemicals, growing environmental concerns, and supportive government regulations promoting biofuel usage. Industrial ethanol is increasingly being utilized across fuel, chemical, pharmaceutical, personal care, food processing, and manufacturing sectors due to its versatility and sustainable characteristics.Global Industrial Ethanol Market Overview

Industrial ethanol is a bio-based alcohol produced primarily from agricultural feedstocks such as corn, sugarcane, wheat, and other biomass sources. It is widely used as a fuel additive, industrial solvent, chemical intermediate, disinfectant, and ingredient in various manufacturing processes. The market serves multiple industries including transportation, chemicals, pharmaceuticals, cosmetics, food processing, paints & coatings, and industrial manufacturing. Growing focus on sustainability and carbon emission reduction is accelerating the adoption of industrial ethanol globally.Structural Drivers of Market Growth

1. Rising Demand for Renewable Fuels

Governments worldwide are implementing ethanol blending mandates and renewable fuel programs to reduce dependence on fossil fuels. Market Implications: Ethanol producers are expanding production capacity to meet growing demand from transportation fuel applications.2. Increasing Focus on Sustainable Industrial Chemicals

Industries are shifting toward bio-based raw materials and environmentally friendly chemical production processes. Market Implications: Industrial ethanol is gaining importance as a renewable feedstock for chemical manufacturing.3. Expansion of Industrial and Manufacturing Applications

Industrial ethanol is increasingly used as a solvent, cleaning agent, and process ingredient across diverse manufacturing sectors. Market Implications: Demand from industrial end-users continues to diversify beyond traditional fuel applications.4. Government Policies Supporting Decarbonization

Stringent carbon reduction targets and environmental regulations are encouraging the use of low-carbon biofuels and sustainable materials. Market Implications: Regulatory support is expected to strengthen long-term market growth and investment activity.Market Segmentation Analysis

By Product Type

- Fuel Grade Ethanol Largest segment driven by widespread use in gasoline blending programs and renewable transportation fuel initiatives.

- Industrial Grade Ethanol Used extensively in solvents, chemical processing, cleaning products, and industrial manufacturing applications.

- Pharmaceutical & Specialty Grade Ethanol High-purity ethanol utilized in healthcare, pharmaceuticals, cosmetics, and specialty industrial applications.

By Source

- Corn-Based Ethanol Largest segment due to established production infrastructure and abundant feedstock availability in major producing regions.

- Sugarcane-Based Ethanol Widely adopted in countries with strong sugarcane production capabilities and biofuel programs.

- Wheat-Based Ethanol Utilized in several regions as an alternative feedstock for ethanol production.

- Cellulosic & Bio-Based Industrial Ethanol Fastest-growing segment driven by advancements in second-generation biofuel technologies and sustainability goals.

By End Use

- Transportation & Fuel Industry Largest segment due to extensive ethanol blending requirements and renewable fuel adoption.

- Chemical Industry Uses ethanol as a feedstock for producing chemicals, solvents, and intermediates.

- Pharmaceutical & Healthcare Industry Utilizes ethanol in drug formulations, sanitizers, disinfectants, and healthcare products.

- Personal Care & Cosmetics Industry Growing demand for ethanol in perfumes, skincare products, and cosmetic formulations.

- Food & Beverage Processing Used in flavor extraction, food processing, and specialty ingredient applications.

Regional Market Dynamics

North America

Leading market driven by large-scale ethanol production capacity, strong renewable fuel standards, and extensive corn-based ethanol infrastructure.Europe

Supported by stringent carbon reduction targets, renewable energy policies, and growing demand for sustainable industrial chemicals.Asia-Pacific

Fastest-growing region due to expanding industrialization, rising energy demand, and increasing government support for ethanol blending programs.Latin America

Major market led by Brazil's sugarcane-based ethanol industry and strong biofuel adoption initiatives.Middle East & Africa

Emerging market supported by diversification of energy sources, industrial development, and growing interest in renewable fuels.Competitive Landscape

The Global Industrial Ethanol Market is highly competitive with the presence of biofuel producers, agricultural processing companies, chemical manufacturers, and renewable energy firms. Companies compete through production efficiency, feedstock optimization, sustainability initiatives, and strategic capacity expansion projects. Key Companies Operating in the Market Include:- Archer Daniels Midland Company (ADM)

- POET LLC

- Valero Energy Corporation

- Green Plains Inc.

- Ra??zen S.A.

- Tereos Group

- Cargill Incorporated

- Flint Hills Resources

- The Andersons, Inc.

- Cristal Union Group

Strategic Outlook

The future of the industrial ethanol market will be shaped by increasing adoption of renewable fuels, advancements in bio-based production technologies, and expanding industrial applications. Investments in cellulosic ethanol production, carbon capture technologies, and sustainable feedstock development are expected to improve production efficiency and environmental performance. Industrial ethanol will continue to play a critical role in supporting global decarbonization objectives and renewable energy transitions. Growing demand for sustainable chemicals, green solvents, and bio-based manufacturing inputs is expected to create additional opportunities beyond fuel applications. Companies focusing on innovation, operational efficiency, and sustainable production practices will be well-positioned to benefit from long-term market expansion.Final Market Perspective

The Global Industrial Ethanol Market represents a vital segment of the renewable energy and industrial chemicals industry. Rising demand for sustainable fuels, environmentally friendly industrial inputs, and low-carbon manufacturing solutions is creating substantial growth opportunities worldwide. As governments and industries continue to prioritize sustainability and carbon reduction, industrial ethanol is expected to remain a key component of the global transition toward a more renewable and resource-efficient economy.Table of Contents

Table of Contents

- Executive Summary

- Global Industrial Ethanol Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends & Renewable Fuel Developments

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Industrial Ethanol

- Scope of the Global Industrial Ethanol Market

- Evolution of Bio-Based Ethanol Production

- Role of Industrial Ethanol in Renewable Energy & Industrial Applications

- Value Chain Analysis of the Industrial Ethanol Ecosystem

- Regulatory Influence (Renewable Fuel Standards, Carbon Emission Regulations & Biofuel Blending Mandates)

- Transition Toward Sustainable Fuels, Green Chemicals & Industrial Decarbonization

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Rising Demand for Renewable Fuels

- Increasing Focus on Sustainable Industrial Chemicals

- Expansion of Industrial & Manufacturing Applications

- Government Policies Supporting Decarbonization

- Market Restraints

- Volatility in Agricultural Feedstock Prices

- Competition from Alternative Renewable Fuels

- Infrastructure Limitations in Emerging Markets

- Market Opportunities

- Growth of Cellulosic Ethanol Production

- Expansion of Bio-Based Chemical Manufacturing

- Increasing Ethanol Blending Targets Worldwide

- Development of Carbon-Neutral Industrial Processes

- Market Challenges

- Feedstock Availability & Supply Chain Risks

- Regulatory Uncertainty Across Regions

- Balancing Fuel and Industrial Ethanol Demand

- Structural Drivers of Market Growth

- Global Industrial Ethanol Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Ethanol Production & Consumption Trends

- Fuel vs Industrial Application Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Product Type

- Fuel Grade Ethanol (Largest Segment)

- Industrial Grade Ethanol

- Pharmaceutical & Specialty Grade Ethanol

- By Source

- Corn-Based Ethanol (Largest Segment)

- Sugarcane-Based Ethanol

- Wheat-Based Ethanol

- Cellulosic & Bio-Based Industrial Ethanol (Fastest-Growing Segment)

- By End Use

- Transportation & Fuel Industry (Largest Segment)

- Chemical Industry

- Pharmaceutical & Healthcare Industry

- Personal Care & Cosmetics Industry

- Food & Beverage Processing

- By Product Type

- Regional Market Analysis

- North America (Largest Regional Market)

- Europe

- Asia-Pacific (Fastest-Growing Region)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- Biofuel Production & Sustainability Strategies

- Capacity Expansion, Partnerships & Feedstock Optimization Initiatives

- Company Profiles

- Archer Daniels Midland Company (ADM)

- POET LLC

- Valero Energy Corporation

- Green Plains Inc.

- Ra??zen S.A.

- Tereos Group

- Cargill Incorporated

- Flint Hills Resources

- The Andersons, Inc.

- Cristal Union Group

- Strategic Outlook

- Future of Renewable Fuel & Ethanol Blending Programs

- Expansion of Cellulosic & Advanced Ethanol Technologies

- Growth of Bio-Based Industrial Chemical Applications

- Role of Ethanol in Industrial Decarbonization Strategies

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Industrial Ethanol Market Competitive Intensity & Market Structure Overview

The Global Industrial Ethanol Market is highly competitive and moderately consolidated, characterized by the presence of large biofuel producers, agricultural processing companies, renewable energy firms, chemical manufacturers, and integrated agribusiness corporations. Competitive intensity is driven by production capacity, feedstock availability, operational efficiency, product quality, sustainability initiatives, regulatory compliance, and distribution network strength.

Companies compete across multiple application segments including fuel ethanol, industrial solvents, chemical intermediates, pharmaceutical-grade ethanol, personal care ingredients, and specialty industrial products. The increasing adoption of renewable fuels and bio-based industrial chemicals is intensifying competition among market participants globally.

The market structure is evolving toward sustainability-focused and technology-driven production models. Producers are investing in advanced fermentation technologies, cellulosic ethanol production, carbon capture solutions, feedstock diversification, and capacity expansion projects to strengthen market positioning and improve profitability.

Global Industrial Ethanol Market Competitive Intensity & Market Structure Current Scenario

Leading Global Industrial Ethanol Companies

- Archer Daniels Midland Company (ADM): One of the world’s largest ethanol producers with extensive corn processing infrastructure and a diversified portfolio of biofuel and industrial ethanol products.

- POET LLC: A leading biofuel company recognized for large-scale ethanol production, innovation in renewable fuels, and investments in next-generation bio-based technologies.

- Valero Energy Corporation: Operates significant ethanol production facilities and leverages integrated energy operations to support large-scale fuel ethanol supply.

- Green Plains Inc.: A major ethanol producer focused on operational efficiency, sustainable production practices, and value-added bio-based product development.

- Ra??zen S.A.: One of the leading sugarcane-based ethanol producers globally, benefiting from strong feedstock availability and extensive biofuel distribution capabilities.

- Tereos Group: A diversified agribusiness company with strong ethanol production operations across sugar and grain-based feedstock markets.

- Cargill Incorporated: A global agricultural and industrial processing company supplying ethanol and bio-based products to multiple industrial sectors.

- Flint Hills Resources: A significant ethanol producer with integrated production assets and strong participation in renewable fuel markets.

- The Andersons, Inc.: Active in grain processing and ethanol production with a focus on operational optimization and feedstock management.

- Cristal Union Group: A prominent European ethanol producer leveraging sugar beet feedstocks and sustainable production technologies.

Key Competitive Intensity & Market Structure Drivers

Growing government support for renewable fuel programs and ethanol blending mandates is intensifying competition among producers seeking to expand market share in transportation fuel applications.

Increasing demand for sustainable industrial chemicals and bio-based manufacturing inputs is encouraging companies to diversify product portfolios beyond traditional fuel ethanol markets.

Feedstock availability, pricing volatility, and agricultural supply chain management remain critical competitive factors influencing production economics and profitability.

Investments in advanced biofuel technologies, including cellulosic ethanol and low-carbon production processes, are creating differentiation opportunities for market participants.

Rising environmental regulations and decarbonization targets are accelerating innovation in carbon reduction strategies, renewable energy integration, and sustainable production practices.

Strategic Implications of Competitive Intensity & Market Structure

Companies with large-scale production facilities, reliable feedstock sourcing capabilities, and diversified end-use exposure are expected to maintain significant competitive advantages.

Investment in advanced biofuel technologies, production efficiency improvements, and sustainability initiatives is becoming increasingly important for long-term market leadership.

Manufacturers focusing on specialty-grade ethanol products, industrial applications, and value-added bio-based chemicals are likely to strengthen revenue diversification and profitability.

Strategic partnerships across agriculture, energy, chemical, and transportation sectors are helping companies enhance supply chain resilience and market access.

Organizations capable of combining production scale, operational efficiency, sustainability performance, regulatory compliance, and product innovation will be best positioned to compete effectively in the evolving industrial ethanol market.

Global Industrial Ethanol Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global industrial ethanol market is expected to become increasingly sustainability-driven, technology-focused, and integrated with broader renewable energy ecosystems.

Future competition will be shaped by advancements in cellulosic ethanol production, carbon capture technologies, low-emission manufacturing processes, and next-generation bio-based feedstocks.

Market participants are expected to increase investments in production capacity expansion, process optimization, renewable energy integration, and specialty industrial ethanol applications to strengthen competitive positioning.

Over the forecast period, companies that successfully balance production efficiency, sustainability, innovation, feedstock security, and market diversification will be best positioned to lead the evolving global industrial ethanol market.

Value Chain

Global Industrial Ethanol Market Value Chain & Supply Chain Evolution Overview

The Global Industrial Ethanol Market operates through a complex value chain involving feedstock cultivation, raw material procurement, ethanol production, processing, storage, distribution, blending, industrial application, and end-user consumption. Industrial ethanol is widely utilized across transportation fuels, chemical manufacturing, pharmaceuticals, personal care products, food processing, and industrial cleaning applications.

The market is heavily influenced by renewable energy policies, biofuel mandates, feedstock availability, environmental regulations, and technological advancements in ethanol production. Growing global emphasis on decarbonization and sustainable manufacturing practices continues to reshape industry dynamics.

The expansion of bio-based economies, increasing ethanol blending programs, and growing adoption of renewable industrial chemicals have transformed supply chain structures. Manufacturers are increasingly investing in production efficiency, feedstock diversification, and sustainable sourcing strategies to strengthen competitiveness.

Advancements in cellulosic ethanol technologies, carbon capture integration, digital supply chain management, and sustainable feedstock utilization are driving the evolution of the industrial ethanol value chain while improving operational efficiency and environmental performance.

Global Industrial Ethanol Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Feedstock Cultivation & Supply: Production and supply of corn, sugarcane, wheat, sorghum, and biomass feedstocks used for ethanol manufacturing.

- Feedstock Processing: Collection, transportation, storage, milling, and preparation of agricultural raw materials for ethanol production.

- Ethanol Production & Fermentation: Conversion of feedstocks into ethanol through fermentation, distillation, dehydration, and purification processes.

- Quality Control & Storage: Product testing, regulatory compliance verification, storage management, and inventory control.

- Distribution & Logistics: Bulk transportation, terminal operations, pipeline transfers, rail networks, and supply chain coordination.

- Industrial Processing & Blending: Ethanol blending with fuels and integration into chemical, pharmaceutical, personal care, and industrial manufacturing applications.

- End User Consumption: Transportation companies, chemical manufacturers, pharmaceutical firms, personal care brands, food processors, and industrial users.

Company-to-Stage Mapping

- Feedstock Cultivation & Supply: Agricultural producers, farming cooperatives, corn growers, sugarcane producers, wheat suppliers, and biomass feedstock providers.

- Feedstock Processing: Archer Daniels Midland Company (ADM), Cargill Incorporated, The Andersons, Inc., agricultural processors, and grain handling operators.

- Ethanol Production & Fermentation: POET LLC, Green Plains Inc., Ra??zen S.A., Tereos Group, Valero Energy Corporation, and Cristal Union Group.

- Quality Control & Storage: Ethanol storage terminal operators, testing laboratories, certification bodies, and quality assurance providers.

- Distribution & Logistics: Rail operators, bulk transport companies, terminal operators, fuel distributors, and logistics service providers.

- Industrial Processing & Blending: Fuel blenders, chemical manufacturers, pharmaceutical companies, personal care product manufacturers, and industrial processors.

- End User Consumption: Transportation & fuel companies, chemical producers, pharmaceutical manufacturers, cosmetics companies, food processors, and industrial enterprises.

Key Value Chain & Supply Chain Evolution Signals in Global Industrial Ethanol Market

Expansion of Ethanol Blending Programs

Governments across multiple regions are increasing ethanol blending mandates to reduce carbon emissions and strengthen renewable fuel adoption.

Growth of Cellulosic and Advanced Bio-Based Ethanol

Advancements in second-generation ethanol technologies are enabling production from agricultural residues and non-food biomass feedstocks.

Increasing Demand for Sustainable Industrial Chemicals

Manufacturers are increasingly utilizing ethanol as a renewable feedstock for producing environmentally friendly chemicals and solvents.

Digitalization of Supply Chain Operations

Companies are adopting digital monitoring, predictive analytics, and supply chain optimization tools to improve operational efficiency.

Investment in Carbon Reduction Technologies

Carbon capture, utilization, and storage (CCUS) technologies are being integrated into ethanol production facilities to support sustainability objectives.

Feedstock Diversification Strategies

Producers are expanding beyond traditional feedstocks to reduce supply risks and improve long-term production sustainability.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Advanced Ethanol Production Technologies

Companies adopting next-generation biofuel technologies can improve efficiency, sustainability, and long-term competitiveness.

Strengthening Feedstock Security

Long-term feedstock procurement agreements and diversified sourcing strategies can reduce supply chain disruptions and price volatility.

Expansion of Industrial End-Use Applications

Growth in chemical, pharmaceutical, and personal care sectors can diversify revenue streams beyond fuel applications.

Enhancement of Sustainability Initiatives

Integrating renewable energy, carbon reduction technologies, and sustainable production practices can strengthen regulatory compliance and market positioning.

Optimization of Distribution Infrastructure

Investments in logistics networks, storage facilities, and transportation systems can improve supply chain efficiency and market accessibility.

Leveraging Regulatory Support Programs

Participation in renewable fuel programs and low-carbon initiatives can create additional growth and investment opportunities.

Global Industrial Ethanol Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the industrial ethanol value chain is expected to become increasingly sustainability-focused, technologically advanced, and integrated with global decarbonization initiatives. Growing demand for renewable fuels and bio-based industrial inputs will continue to reshape supply chain structures worldwide.

Key Future Developments Include:

- Expansion of cellulosic and advanced bio-based ethanol production.

- Increasing adoption of carbon capture and low-emission manufacturing technologies.

- Growth of ethanol utilization in sustainable chemical production.

- Strengthening of global ethanol blending programs and renewable fuel mandates.

- Greater implementation of digital supply chain management systems.

- Expansion of feedstock diversification and circular economy initiatives.

As the market evolves, competitive advantage will increasingly depend on production efficiency, feedstock security, sustainability performance, regulatory compliance, and supply chain resilience.

Companies that successfully integrate advanced production technologies, sustainable sourcing strategies, efficient logistics networks, and diversified end-use applications will be well-positioned to achieve long-term growth in the Global Industrial Ethanol Market.

Investment Activity

Global Industrial Ethanol Market Investment & Funding Dynamics Overview (2026???2033)

The Global Industrial Ethanol Market is experiencing significant investment activity driven by increasing demand for renewable fuels, expanding ethanol blending programs, growing adoption of bio-based industrial chemicals, and accelerating global decarbonization initiatives. Ethanol producers, biofuel companies, agricultural processing firms, chemical manufacturers, renewable energy investors, private equity firms, and infrastructure developers are actively investing in ethanol production capacity expansion, advanced biofuel technologies, feedstock optimization, sustainable manufacturing processes, and low-carbon fuel infrastructure.

Investment momentum is strengthening as governments and industries prioritize carbon emission reduction, renewable energy adoption, and sustainable industrial production. Capital allocation is increasingly focused on cellulosic ethanol facilities, next-generation biofuel technologies, carbon capture systems, production efficiency improvements, supply chain optimization, and green chemical manufacturing platforms.

Additionally, growing investments in bio-based feedstocks, ethanol storage and logistics infrastructure, renewable fuel distribution networks, and sustainable industrial chemical applications are creating substantial long-term opportunities throughout the global industrial ethanol value chain.

Current Investment & Funding Landscape

The current market environment reflects strong investor confidence in renewable energy and sustainable industrial materials. Industry participants are investing heavily in production capacity expansion, advanced fermentation technologies, feedstock diversification strategies, and ethanol processing infrastructure.

Significant funding is being directed toward second-generation ethanol production facilities, biomass conversion technologies, carbon reduction projects, bio-refineries, and integrated renewable energy ecosystems to enhance operational efficiency and environmental sustainability.

Strategic collaborations among biofuel producers, agricultural companies, chemical manufacturers, technology providers, and government agencies are reshaping investment flows and accelerating commercialization of advanced ethanol production technologies.

Key Investment & Funding Dynamics Signals

- Growing demand for renewable transportation fuels is driving large-scale investments in ethanol production capacity and blending infrastructure.

- Expansion of bio-based industrial chemicals and green manufacturing initiatives is attracting substantial capital across the industrial sector.

- Increasing adoption of cellulosic and advanced bio-based ethanol technologies is creating high-growth investment opportunities.

- Rising focus on carbon reduction and sustainability targets is accelerating investments in low-carbon fuel solutions.

- Strategic funding for feedstock optimization, agricultural productivity, and supply chain modernization is improving industry competitiveness.

- Growing investments in carbon capture, utilization, and storage (CCUS) technologies are supporting sustainable ethanol production.

- Expansion of renewable energy infrastructure and bio-refinery projects is generating attractive long-term investment prospects.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in advanced ethanol production technologies and process innovation is essential for maintaining long-term competitiveness.

- Capital allocation toward cellulosic ethanol facilities, feedstock diversification, and production efficiency enhancement will strengthen future growth potential.

- Companies developing low-carbon fuels, sustainable chemicals, and bio-based industrial solutions are expected to secure stronger market opportunities.

- Strategic partnerships between biofuel producers, agricultural suppliers, chemical companies, and technology providers will accelerate market expansion.

- Investments in logistics infrastructure, storage facilities, and renewable fuel distribution networks will improve supply chain resilience and operational efficiency.

- Compliance with renewable fuel standards, carbon emission regulations, and sustainability requirements will continue influencing investment decisions.

- Organizations building integrated capabilities across feedstock sourcing, ethanol production, renewable energy integration, and sustainable chemical manufacturing are expected to capture substantial future value.

Forward Outlook

Looking ahead, the Global Industrial Ethanol Market is expected to maintain strong investment momentum driven by renewable energy adoption, biofuel expansion, industrial decarbonization initiatives, and increasing demand for sustainable manufacturing inputs.

Future capital deployment will increasingly focus on advanced bio-refineries, cellulosic ethanol production, carbon capture technologies, renewable fuel infrastructure, and bio-based industrial chemical platforms.

As governments and industries continue prioritizing environmental sustainability and energy transition goals, investment activity is expected to expand across renewable fuels, sustainable chemicals, agricultural feedstock development, and low-carbon industrial production systems.

In conclusion, the Global Industrial Ethanol Market represents a highly attractive renewable energy and industrial chemicals investment landscape where biofuel expansion, sustainability, technological innovation, carbon reduction, and green manufacturing initiatives will define future funding priorities, competitive differentiation, and long-term market growth.

Technology & Innovation

Global Industrial Ethanol Market Technology & Innovation Landscape Overview

The global industrial ethanol market is experiencing continuous technological advancement as manufacturers focus on improving production efficiency, sustainability, and feedstock utilization. Innovations in advanced fermentation technologies, enzyme engineering, biomass conversion processes, and automated production systems are enhancing ethanol yield while reducing operational costs. The industry is increasingly adopting digital monitoring platforms, artificial intelligence-based process optimization tools, and smart manufacturing solutions to improve productivity and quality consistency. Growing demand for renewable fuels and bio-based industrial chemicals is also encouraging investment in next-generation production technologies that support large-scale, environmentally responsible ethanol manufacturing.

Technological progress is further accelerating the adoption of cellulosic ethanol production, carbon reduction initiatives, and integrated biorefinery models that maximize resource utilization. Manufacturers are increasingly leveraging sustainable feedstocks, energy-efficient distillation systems, and advanced purification technologies to meet evolving environmental and industrial requirements. These innovations are helping ethanol producers improve operational performance while supporting global sustainability and decarbonization objectives.

Global Industrial Ethanol Market Technology & Innovation Current Scenario

Current innovation activities within the industrial ethanol market are primarily focused on increasing production efficiency, reducing carbon emissions, and expanding the use of renewable feedstocks. Producers are implementing advanced fermentation technologies, high-performance enzymes, and automated process control systems to optimize ethanol output and improve overall plant productivity. Artificial intelligence and predictive analytics solutions are increasingly being utilized to monitor production parameters, minimize downtime, and improve resource management. At the same time, advancements in biomass processing technologies are supporting the commercialization of second-generation ethanol derived from agricultural residues and non-food feedstocks.

The market is also witnessing increased deployment of carbon capture technologies, energy-efficient manufacturing systems, and integrated production platforms that support both ethanol and bio-based chemical production. These innovations are enabling producers to improve sustainability performance while addressing growing demand from fuel, chemical, pharmaceutical, and industrial end-use sectors.

Key Technology & Innovation Trends in Global Industrial Ethanol Market

- Advanced Fermentation Technologies: Improving ethanol yields, production efficiency, and feedstock conversion rates.

- Cellulosic Ethanol Production: Enabling the utilization of agricultural waste, biomass residues, and non-food feedstocks.

- Artificial Intelligence-Based Process Optimization: Supporting real-time production monitoring and operational efficiency improvements.

- Advanced Enzyme Engineering: Enhancing biomass breakdown and increasing ethanol production performance.

- Carbon Capture & Utilization Technologies: Supporting emission reduction and sustainable manufacturing objectives.

- Smart Manufacturing Systems: Improving automation, process control, and production consistency.

- Energy-Efficient Distillation Solutions: Reducing energy consumption and improving production economics.

- Integrated Biorefinery Platforms: Maximizing value generation through co-production of ethanol and bio-based products.

- Sustainable Feedstock Management: Enhancing traceability, resource utilization, and supply chain efficiency.

- Digital Production Analytics: Supporting predictive maintenance and performance optimization across manufacturing facilities.

Strategic Implications of Technology & Innovation

Technological advancements are transforming the industrial ethanol market into a more sustainable, efficient, and innovation-driven industry. Companies investing in advanced production technologies, digital manufacturing systems, and renewable feedstock solutions are improving operational performance while strengthening their competitive positioning. The integration of biotechnology, automation, artificial intelligence, and carbon management technologies is helping producers address increasing demand for renewable fuels and environmentally responsible industrial products. These innovations are also supporting compliance with evolving regulatory requirements and sustainability targets across major global markets.

As industrial applications for ethanol continue to expand, manufacturers that successfully implement advanced production and sustainability technologies are expected to benefit from improved profitability, enhanced market access, and stronger long-term growth opportunities. However, factors such as capital investment requirements, feedstock availability, and regulatory compliance remain important considerations for industry participants.

Global Industrial Ethanol Market Technology & Innovation Forward Outlook

The future of the industrial ethanol market is expected to be shaped by continued advancements in biomass conversion technologies, low-carbon production systems, artificial intelligence-driven manufacturing, and integrated biorefinery operations. Emerging innovations such as next-generation cellulosic ethanol production, digital twin technologies, advanced microbial engineering, and carbon-negative manufacturing processes are expected to further improve efficiency and sustainability across the value chain. Increasing global emphasis on renewable energy, green manufacturing, and circular economy initiatives will continue to support technology adoption and industry modernization.

As governments and industries pursue long-term decarbonization goals, industrial ethanol is expected to play an increasingly important role in renewable fuel programs, sustainable chemical production, and bio-based industrial applications. The combination of advanced biotechnology, digital manufacturing platforms, and environmental innovation is expected to create new opportunities for growth while strengthening the market’s position within the global renewable economy.

Market Risk

Global Industrial Ethanol Market Risk Factors & Disruption Threats Overview

The Global Industrial Ethanol Market plays a critical role in renewable fuels, industrial chemicals, pharmaceutical manufacturing, personal care products, and sustainable production processes. While the market benefits from increasing biofuel adoption, industrial decarbonization efforts, and growing demand for renewable feedstocks, it remains exposed to various risks associated with feedstock availability, regulatory changes, commodity price volatility, and evolving energy market dynamics.

One of the most significant structural risks involves dependence on agricultural feedstocks such as corn, sugarcane, wheat, and biomass. Weather disruptions, climate-related events, crop diseases, water shortages, and agricultural supply fluctuations can directly impact feedstock availability and production economics.

The market is also highly sensitive to changes in government biofuel policies, renewable fuel standards, blending mandates, and subsidy programs. Regulatory shifts or reductions in policy support could significantly affect ethanol demand and investment activity across major producing regions.

Another key disruption factor is volatility in energy markets. Changes in crude oil prices, gasoline demand, and alternative fuel economics can influence the competitiveness of ethanol relative to conventional fossil fuels, affecting consumption patterns and producer profitability.

Additionally, growing competition from alternative renewable energy technologies, advanced biofuels, hydrogen-based solutions, and electric mobility adoption may create long-term challenges for fuel-grade ethanol demand in certain markets.

Global Industrial Ethanol Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by increasing demand for renewable transportation fuels, expanding industrial applications, and growing interest in sustainable chemical production. Governments and industries are actively pursuing carbon reduction strategies, supporting ethanol consumption across multiple sectors.

However, producers continue to face challenges related to fluctuating feedstock costs, rising energy prices, transportation expenses, and supply chain uncertainties. These factors can affect production margins and operational efficiency.

Industrial ethanol manufacturers are also navigating increasingly complex regulatory environments involving carbon accounting, sustainability certifications, renewable fuel compliance, and environmental reporting requirements.

Global supply chains remain vulnerable to geopolitical tensions, export restrictions, transportation bottlenecks, and regional trade disputes that may impact feedstock sourcing and ethanol distribution networks.

At the same time, increasing focus on second-generation and cellulosic ethanol technologies is encouraging market participants to invest in advanced production methods that improve sustainability and reduce dependence on conventional agricultural feedstocks.

Key Risk Factors & Disruption Threat Signals in Global Industrial Ethanol Market

A major disruption signal is the increasing volatility of agricultural commodity markets. Feedstock price fluctuations can significantly influence ethanol production costs and affect overall market competitiveness.

Another important signal is the accelerating adoption of electric vehicles and alternative clean transportation technologies, which could gradually reduce long-term demand growth for fuel-grade ethanol in certain regions.

The growing emphasis on environmental sustainability and lifecycle carbon emissions is prompting regulators to implement stricter reporting requirements, sustainability certification standards, and carbon reduction targets.

Rapid technological advancements in advanced biofuels, synthetic fuels, hydrogen energy systems, and renewable energy storage solutions may create competitive pressure for traditional ethanol markets.

Geopolitical uncertainties, trade policy changes, and international supply chain disruptions continue to influence global ethanol trade flows, investment decisions, and production strategies.

Climate change-related risks, including droughts, floods, extreme weather events, and agricultural productivity challenges, are becoming increasingly important considerations for feedstock security and long-term industry stability.

Strategic Implications of Risk Factors & Disruption Threats in Global Industrial Ethanol Market

Manufacturers should diversify feedstock sourcing strategies and invest in alternative raw material development to reduce exposure to agricultural supply fluctuations and commodity price volatility.

Investment in advanced ethanol production technologies, including cellulosic ethanol and next-generation biofuel platforms, will be essential for improving sustainability performance and maintaining long-term competitiveness.

Companies should strengthen supply chain resilience through geographic diversification, strategic inventory management, and long-term supplier agreements to mitigate logistics and sourcing risks.

Continuous monitoring of renewable fuel policies, environmental regulations, and carbon reduction frameworks will remain critical for maintaining regulatory compliance and identifying emerging market opportunities.

Strategic collaborations with agricultural producers, energy companies, industrial manufacturers, and technology providers can support innovation, feedstock security, and operational efficiency improvements.

Organizations should also invest in carbon management initiatives, renewable energy integration, and sustainability reporting capabilities to align with evolving customer and regulatory expectations.

Global Industrial Ethanol Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Industrial Ethanol Market is expected to remain a key component of renewable energy, industrial manufacturing, and sustainable chemical production ecosystems. However, future market performance will increasingly depend on policy stability, technological innovation, and feedstock availability.

Regulatory frameworks supporting renewable fuels and industrial decarbonization are expected to continue driving demand, although compliance requirements may become more stringent across major markets.

Advanced biofuel technologies, carbon capture initiatives, and sustainable feedstock development programs are likely to gain greater importance as companies seek to improve environmental performance and operational efficiency.

Competition from alternative low-carbon energy solutions will continue influencing market dynamics, encouraging ethanol producers to diversify applications beyond traditional transportation fuel markets.

Supply chain resilience, sustainability certification, and climate adaptation strategies will become increasingly important as environmental and geopolitical risks continue to evolve.

Overall, the market is expected to maintain positive long-term growth prospects, but success will increasingly depend on the ability of industry participants to manage regulatory complexity, secure feedstock supplies, adopt advanced production technologies, and adapt to the rapidly changing global energy and sustainability landscape.

Regulatory Landscape

Global Industrial Ethanol Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Industrial Ethanol Market is evolving rapidly as governments, environmental agencies, energy regulators, and industry bodies strengthen policies supporting renewable fuels, sustainable industrial production, and carbon emission reduction initiatives. Industrial ethanol plays a critical role in transportation fuels, chemical manufacturing, pharmaceuticals, personal care products, and industrial processing, making regulatory compliance essential across multiple end-use sectors.

Ethanol producers, feedstock suppliers, fuel distributors, chemical manufacturers, and industrial users must comply with a broad range of regulations related to renewable fuel standards, biofuel blending mandates, environmental sustainability, product quality requirements, transportation safety, and emissions management. Regulatory frameworks increasingly influence production strategies, investment decisions, and international trade activities.

As governments intensify efforts to achieve climate goals and reduce dependence on fossil fuels, industrial ethanol is receiving growing policy support through renewable energy programs, low-carbon fuel initiatives, and sustainable manufacturing incentives.

Global Industrial Ethanol Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is primarily shaped by renewable fuel standards and biofuel blending mandates implemented across major economies. Governments are requiring higher ethanol blending ratios in transportation fuels to reduce greenhouse gas emissions and improve energy security.

Carbon emission regulations are increasingly encouraging industries to adopt renewable and bio-based alternatives to conventional petroleum-derived products. Industrial ethanol is benefiting from policies aimed at supporting low-carbon fuels and sustainable industrial feedstocks.

Product quality and fuel specification standards continue to play a critical role in ensuring ethanol compatibility, performance, and safety across transportation and industrial applications. Regulatory authorities maintain strict requirements governing ethanol purity, composition, and distribution practices.

Environmental compliance regulations are becoming increasingly important as manufacturers face greater scrutiny regarding resource utilization, emissions management, wastewater treatment, and sustainable production practices.

In addition, international trade policies, agricultural regulations, and feedstock sustainability requirements continue to influence ethanol production economics, supply chain dynamics, and global market competitiveness.

Key Regulatory & Policy Environment Signals in Global Industrial Ethanol Market

- Renewable Fuel Standards (RFS):

Policies mandating the use of renewable fuels and supporting ethanol integration into transportation energy systems. - Biofuel Blending Mandates:

Government requirements establishing minimum ethanol blending levels in gasoline and transportation fuels. - Carbon Emission Reduction Regulations:

Frameworks promoting low-carbon fuels, industrial decarbonization, and greenhouse gas reduction initiatives. - Fuel Quality & Product Specification Standards:

Requirements governing ethanol purity, performance characteristics, storage, handling, and fuel compatibility. - Environmental Compliance & Sustainability Policies:

Regulations addressing emissions control, water management, waste reduction, and sustainable production practices. - Feedstock Sustainability & Agricultural Policies:

Guidelines supporting responsible sourcing of corn, sugarcane, wheat, and biomass feedstocks used in ethanol production.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging ethanol producers to invest in advanced production technologies, low-carbon manufacturing processes, and sustainable feedstock sourcing strategies. Regulatory compliance is becoming a key competitive differentiator across global ethanol markets.

Renewable fuel standards and blending mandates are driving capacity expansion projects, infrastructure investments, and long-term supply agreements throughout the ethanol value chain.

Carbon reduction regulations are encouraging manufacturers to adopt cleaner production methods, improve energy efficiency, and invest in carbon capture and emissions management technologies.

Environmental compliance requirements are increasing investments in wastewater treatment systems, resource optimization programs, and sustainability reporting initiatives to meet evolving regulatory expectations.

Feedstock sustainability policies are motivating industry participants to strengthen agricultural partnerships, improve traceability systems, and support responsible biomass sourcing practices that align with environmental objectives.

Global Industrial Ethanol Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Industrial Ethanol Market is expected to become increasingly supportive as governments accelerate renewable energy adoption and industrial decarbonization strategies.

Biofuel blending mandates are likely to expand across both developed and emerging economies, creating stronger demand for fuel-grade ethanol and supporting long-term market growth.

Carbon reduction policies are expected to strengthen further, encouraging broader adoption of bio-based fuels and sustainable industrial inputs while increasing compliance requirements for emissions-intensive industries.

Sustainability regulations will likely place greater emphasis on lifecycle carbon accounting, feedstock traceability, environmental performance monitoring, and responsible production practices throughout the ethanol value chain.

Overall, the future regulatory landscape will be defined by the convergence of renewable fuel standards, biofuel blending mandates, carbon emission regulations, environmental sustainability policies, and feedstock governance frameworks. Companies capable of delivering compliant, low-carbon, sustainable, and scalable ethanol solutions will be best positioned to capitalize on long-term opportunities within the expanding global industrial ethanol market.