Global Environmental Consulting Services Market Report, Size & Forecast 2026-2033

Global Environmental Consulting Services Market Report, Size, Share and Forecast 2026???2033

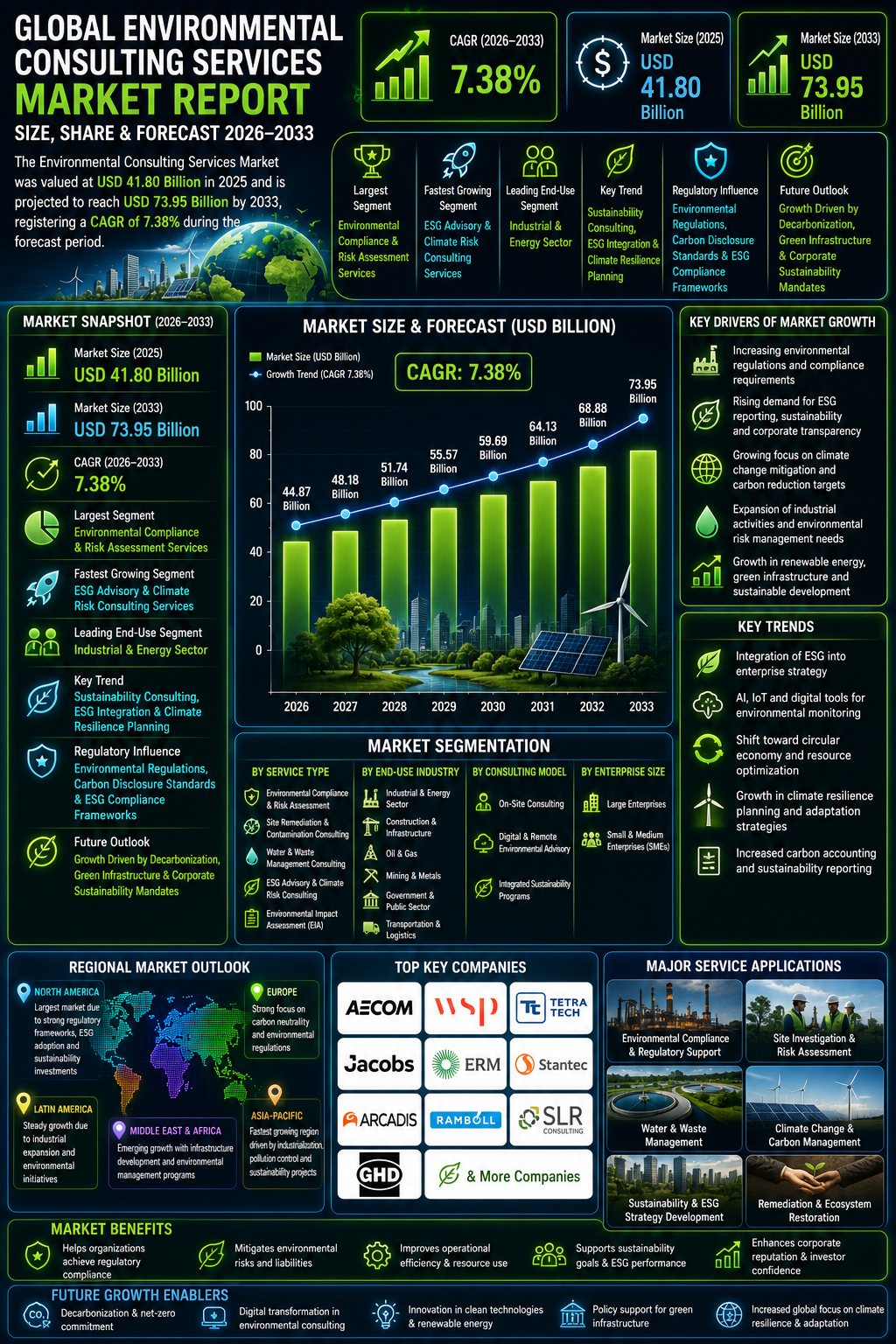

Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 41.80 Billion |

| Market Size (2033) | USD 73.95 Billion |

| CAGR (2026???2033) | 7.38% |

| Largest Segment | Environmental Compliance & Risk Assessment Services |

| Fastest Growing Segment | ESG Advisory & Climate Risk Consulting Services |

| Leading End-Use Segment | Industrial & Energy Sector |

| Key Trend | Sustainability Consulting, ESG Integration & Climate Resilience Planning |

| Regulatory Influence | Environmental Regulations, Carbon Disclosure Standards & ESG Compliance Frameworks |

| Future Outlook | Growth Driven by Decarbonization, Green Infrastructure & Corporate Sustainability Mandates |

Market Size & Forecast

The Environmental Consulting Services Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 41.80 billion in 2025 and is projected to reach approximately USD 73.95 billion by 2033, registering a CAGR of 7.38%. The market growth is primarily driven by rising environmental regulations, increasing ESG reporting requirements, climate change mitigation efforts, industrial pollution control needs, carbon reduction targets, and growing corporate sustainability strategies. Environmental consulting services are increasingly critical for environmental compliance, site remediation, sustainability planning, water resource management, ecological risk assessments, air quality monitoring, waste reduction, and carbon accounting. In addition, growth in renewable energy projects, infrastructure modernization, smart city planning, and climate resilience programs is supporting long-term market expansion.Global Environmental Consulting Services Market Overview

Environmental consulting services involve professional advisory, technical, compliance, and risk management solutions aimed at helping organizations manage environmental impact, sustainability obligations, and regulatory compliance. The market includes environmental impact assessments (EIA), contamination & remediation consulting, waste management consulting, climate advisory, ESG consulting, biodiversity planning, water treatment advisory, and carbon footprint management services. These services are widely used across industrial manufacturing, oil & gas, mining, construction, utilities, transportation, chemicals, real estate, and public infrastructure sectors. The market is shifting from traditional environmental compliance toward ESG advisory, carbon neutrality consulting, digital environmental monitoring, climate resilience strategy, and circular economy consulting.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in environmental monitoring software, AI-driven emissions analytics, digital twin sustainability modeling, remote sensing, GIS-based environmental mapping, and climate risk platforms is accelerating consulting efficiency. Advanced predictive tools and automation are improving environmental assessment accuracy.Market Implications

Consulting firms investing in digital sustainability analytics, AI-enabled compliance monitoring, and climate intelligence solutions are expected to strengthen market competitiveness.2. Compliance and Risk Repricing

Global environmental regulations, carbon accounting mandates, ESG disclosure rules, water safety standards, industrial emissions limits, and biodiversity protection laws are strongly shaping the market. Organizations are increasingly focusing on environmental risk mitigation and regulatory preparedness.Market Implications

Companies offering compliant, data-driven, and risk-focused environmental solutions are likely to gain stronger market trust.3. Competitive and Value-Chain Reconfiguration

Engineering firms, environmental consultants, ESG specialists, sustainability platforms, and risk-advisory companies are increasingly expanding service portfolios. Mergers, digital partnerships, and integrated sustainability offerings are reshaping market economics.Market Implications

Firms focusing on ESG consulting, energy transition advisory, and end-to-end sustainability strategy may gain stronger margins.4. Capital and Capacity Scaling

Rising investment in green infrastructure, renewable energy, carbon capture, waste recycling, environmental remediation, and smart city development is supporting market expansion. Governments and corporations are increasing sustainability spending.Market Implications

Consultants scaling climate advisory, industrial compliance, and environmental technology integration are expected to capture future opportunities.Market Segmentation Analysis

By Service Type

1. Environmental Compliance & Risk Assessment

This remains the largest segment due to strict industrial regulations and compliance demand.2. Site Remediation & Contamination Consulting

Strong growth due to industrial clean-up and land redevelopment.3. Water & Waste Management Consulting

Critical for utilities and sustainability planning.4. ESG Advisory & Climate Risk Consulting

Fastest-growing segment due to carbon disclosure and investor pressure.5. Environmental Impact Assessment (EIA)

Widely used in infrastructure and industrial approvals.By End-Use Industry

1. Industrial & Energy Sector

Largest segment due to emissions, compliance, and pollution management.2. Construction & Infrastructure

Strong demand from EIA and green project development.3. Oil & Gas

Important for remediation and regulatory advisory.4. Mining & Metals

Used for land, water, and biodiversity assessments.5. Government & Public Sector

Growing due to sustainability and urban environmental planning.6. Transportation & Logistics

Increasing focus on carbon footprint and environmental compliance.By Consulting Model

1. On-Site Consulting

Largest due to inspections, remediation, and project execution.2. Digital & Remote Environmental Advisory

Fast-growing due to monitoring platforms and analytics.3. Integrated Sustainability Programs

Growing for enterprise ESG transformation.By Enterprise Size

1. Large Enterprises

Dominates due to ESG reporting and compliance complexity.2. Small & Medium Enterprises (SMEs)

Growing due to sustainability regulation expansion.Regional Market Dynamics

North America

North America dominates the environmental consulting services market due to strong ESG adoption, environmental regulations, infrastructure modernization, and corporate sustainability investment.Europe

Europe remains a major market supported by carbon neutrality goals, climate regulations, and circular economy initiatives.Asia-Pacific

Asia-Pacific is the fastest-growing region due to industrialization, pollution management, renewable energy expansion, and sustainability-driven infrastructure growth.Latin America

Latin America is gradually expanding due to mining activity, environmental protection initiatives, and industrial compliance demand.Middle East & Africa

The region is witnessing emerging growth due to water management, energy transition, and environmental infrastructure projects.Competitive Landscape

The Environmental Consulting Services Market is moderately fragmented with engineering firms, sustainability consultants, environmental specialists, and risk advisory companies competing globally. Key companies operating in the market include:- AECOM

- WSP Global

- Tetra Tech

- Jacobs Solutions

- ERM (Environmental Resources Management)

- Stantec

- Arcadis

- Ramboll Group

- SLR Consulting

- GHD Group

Strategic Outlook

The future of the environmental consulting services market will be shaped by ESG transformation, climate resilience planning, AI-based environmental analytics, carbon neutrality strategies, biodiversity consulting, and sustainability reporting. Rising demand for decarbonization, renewable energy transitions, smart city planning, and environmental risk mitigation is expected to support long-term expansion. Climate-tech integration, carbon accounting, and enterprise sustainability consulting are likely to create major growth opportunities.Final Market Perspective

The Environmental Consulting Services Market remains one of the fastest-growing segments within sustainability, infrastructure, and regulatory advisory industries. Rising ESG mandates, environmental regulations, industrial transformation, and climate adaptation needs continue driving long-term market growth. Companies capable of delivering scalable, data-driven, compliant, and sustainability-focused consulting services will be best positioned to capture future opportunities. The convergence of climate intelligence, digital environmental monitoring, and ESG integration is expected to redefine the future of the global environmental consulting industry.Table of Contents

Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Growth Highlights

1.3 Largest Segment Analysis

1.4 Fastest Growing Segment Analysis

1.5 Regional Outlook

1.6 Competitive Landscape Snapshot

1.7 Future Market Outlook

2. Global Environmental Consulting Services Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Environmental Consulting Services Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Pricing & Revenue Structure Analysis

3.5 Service Delivery & Sustainability Consulting Infrastructure Overview

3.6 Service Landscape

3.6.1 Environmental Compliance & Risk Assessment Services

3.6.1.1 Industrial Compliance Audits

3.6.1.1.1 Environmental Risk Modeling

3.6.1.1.1.1 Pollution Control Strategy Development

3.6.1.1.1.2 Regulatory Preparedness Solutions

3.6.2 Site Remediation & Contamination Consulting

3.6.2.1 Soil & Groundwater Remediation

3.6.2.1.1 Industrial Cleanup Programs

3.6.2.1.1.1 Land Restoration Solutions

3.6.2.1.1.2 Environmental Hazard Mitigation

3.6.3 Water & Waste Management Consulting

3.6.3.1 Water Resource Planning

3.6.3.1.1 Waste Reduction Strategies

3.6.3.1.1.1 Circular Economy Integration

3.6.3.1.1.2 Sustainable Resource Utilization

3.6.4 ESG Advisory & Climate Risk Consulting

3.6.4.1 Carbon Disclosure & ESG Reporting

3.6.4.1.1 Climate Risk Assessment

3.6.4.1.1.1 Sustainability Strategy Development

3.6.4.1.1.2 Corporate Net-Zero Planning

3.6.5 Environmental Impact Assessment (EIA)

3.6.5.1 Infrastructure & Industrial Impact Studies

3.6.5.1.1 Biodiversity & Ecological Assessment

3.6.5.1.1.1 Project Approval Compliance

3.6.5.1.1.2 Long-Term Ecosystem Monitoring

4. Regulatory Landscape

4.1 Environmental Regulations

4.1.1 Carbon Disclosure Standards

4.1.1.1 ESG Compliance Frameworks

4.1.1.1.1 Emissions & Water Safety Standards

4.1.1.1.2 Biodiversity Protection Laws

5. Market Trends & Innovation Outlook

5.1 Sustainability Consulting Growth

5.1.1 ESG Integration Expansion

5.1.1.1 AI-Based Environmental Analytics

5.1.1.1.1 Climate Resilience Planning

5.1.1.1.2 Digital Environmental Monitoring

6. Global Environmental Consulting Services Market Dynamics

6.1 Market Drivers

6.1.1 Rising Environmental Regulations

6.1.1.1 Compliance Demand Expansion

6.1.1.1.1 Industrial Risk Management

6.1.1.1.1.1 Regulatory Advisory Growth

6.1.2 Growth in ESG Reporting Requirements

6.1.2.1 Corporate Sustainability Pressure

6.1.2.1.1 Investor-Driven ESG Adoption

6.1.2.1.1.1 Carbon Disclosure Expansion

6.1.3 Climate Change Mitigation Efforts

6.1.3.1 Net-Zero Transition Support

6.1.3.1.1 Climate Advisory Services

6.1.3.1.1.1 Long-Term Resilience Planning

6.1.4 Renewable Energy & Green Infrastructure Growth

6.1.4.1 Clean Energy Projects

6.1.4.1.1 Sustainable Urban Development

6.1.4.1.1.1 Environmental Planning Expansion

6.1.5 Demand for Pollution & Resource Management

6.1.5.1 Industrial Waste Control

6.1.5.1.1 Water Conservation Solutions

6.1.5.1.1.1 Circular Sustainability Strategies

6.2 Market Restraints

6.2.1 High Consulting Costs

6.2.2 Complex Cross-Border Regulations

6.2.3 Project Delays in Environmental Approvals

6.2.4 Data Collection & Compliance Challenges

6.3 Market Opportunities

6.3.1 ESG Advisory Expansion

6.3.2 Digital Environmental Monitoring Platforms

6.3.3 Smart City Sustainability Consulting

6.3.4 Carbon Accounting & Net-Zero Strategies

6.4 Market Challenges

6.4.1 Regulatory Complexity

6.4.2 Skilled Workforce Shortage

6.4.3 Environmental Data Accuracy Issues

6.4.4 Long-Term Project Execution Risks

7. Global Environmental Consulting Services Market Size Analysis (USD Billion), 2026???2033

7.1 Revenue Forecast Analysis

7.2 CAGR Analysis

7.3 Demand-Supply Analysis

7.4 Segment Contribution Analysis

7.5 Pricing Trend Analysis

8. Global Environmental Consulting Services Market Segmentation Analysis

8.1 By Service Type

8.1.1 Environmental Compliance & Risk Assessment

8.1.2 Site Remediation & Contamination Consulting

8.1.3 Water & Waste Management Consulting

8.1.4 ESG Advisory & Climate Risk Consulting

8.1.5 Environmental Impact Assessment (EIA)

8.2 By End-Use Industry

8.2.1 Industrial & Energy Sector

8.2.2 Construction & Infrastructure

8.2.3 Oil & Gas

8.2.4 Mining & Metals

8.2.5 Government & Public Sector

8.2.6 Transportation & Logistics

8.3 By Consulting Model

8.3.1 On-Site Consulting

8.3.2 Digital & Remote Environmental Advisory

8.3.3 Integrated Sustainability Programs

8.4 By Enterprise Size

8.4.1 Large Enterprises

8.4.2 Small & Medium Enterprises (SMEs)

9. Regional Market Analysis

9.1 North America

9.1.1 U.S.

9.1.2 Canada

9.1.3 Mexico

9.2 Europe

9.2.1 Germany

9.2.2 U.K.

9.2.3 France

9.2.4 Italy

9.2.5 Spain

9.2.6 Rest of Europe

9.3 Asia-Pacific

9.3.1 China

9.3.2 Japan

9.3.3 India

9.3.4 South Korea

9.3.5 Australia

9.3.6 Rest of Asia-Pacific

9.4 Latin America

9.4.1 Brazil

9.4.2 Argentina

9.4.3 Rest of Latin America

9.5 Middle East & Africa

9.5.1 GCC Countries

9.5.2 South Africa

9.5.3 Rest of Middle East & Africa

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Intensity Overview

10.3 Strategic Developments

10.4 ESG & Sustainability Consulting Innovation

10.5 Partnerships, Mergers & Acquisitions

10.6 Environmental Advisory Positioning Analysis

11. Company Profiles

11.1 AECOM

11.2 WSP Global

11.3 Tetra Tech

11.4 Jacobs Solutions

11.5 ERM (Environmental Resources Management)

11.6 Stantec

11.7 Arcadis

11.8 Ramboll Group

11.9 SLR Consulting

11.10 GHD Group

12. Strategic Intelligence & Pheonix AI Insights

12.1 Pheonix Market Growth Forecast Engine

12.2 ESG & Sustainability Trend Analyzer

12.3 Regulatory Risk Tracker

12.4 Climate Consulting Opportunity Mapping

12.5 Automated Porter???s Five Forces Analysis

13. Future Outlook & Strategic Recommendations

13.1 ESG Consulting Expansion Strategies

13.2 Climate Resilience Advisory Growth

13.3 Carbon Accounting & Net-Zero Scaling

13.4 Digital Environmental Monitoring Adoption

13.5 Long-Term Market Outlook (2033+)

14. About Pheonix

15. Market Research

16. Disclaimer

Competitive Landscape

Global Environmental Consulting Services Market Competitive Intensity & Market Structure Overview

The Global Environmental Consulting Services Market is characterized by a moderately fragmented and expertise-driven competitive structure, where engineering consultancies, ESG advisory firms, environmental specialists, and infrastructure consulting companies compete through technical expertise, regulatory capabilities, digital sustainability tools, and sector-specific environmental solutions. Competition is primarily driven by environmental compliance knowledge, ESG advisory depth, climate-risk modeling, remediation capabilities, digital monitoring integration, geographic reach, and multidisciplinary consulting strength.

The market is led by major players such as AECOM, WSP Global, Tetra Tech, Jacobs Solutions, ERM (Environmental Resources Management), Stantec, Arcadis, Ramboll Group, SLR Consulting, and GHD Group, which compete through global project execution, sustainability consulting, infrastructure expertise, remediation services, and integrated environmental-risk platforms.

Growing demand across industrial & energy, construction, oil & gas, mining & metals, transportation, utilities, chemicals, public infrastructure, and government sectors is intensifying competition. Companies are increasingly investing in ESG consulting, climate resilience planning, AI-based environmental analytics, carbon accounting, biodiversity advisory, digital environmental monitoring, and decarbonization strategy services.

Global Environmental Consulting Services Market Competitive Landscape

Leading Company Profiles

- AECOM ??? Global leader in infrastructure, environmental consulting, remediation, and sustainability advisory services.

- WSP Global ??? Major engineering and sustainability consulting firm with strong climate-risk and ESG capabilities.

- Tetra Tech ??? Key provider in environmental engineering, water management, and ecological consulting solutions.

- Jacobs Solutions ??? Strong player in environmental compliance, infrastructure sustainability, and digital environmental systems.

- ERM (Environmental Resources Management) ??? Specialized leader in ESG advisory, sustainability strategy, and environmental risk consulting.

- Stantec ??? Significant global consulting company with environmental planning, water solutions, and resilience expertise.

- Arcadis ??? Major player in sustainable infrastructure, remediation, and climate adaptation consulting.

- Ramboll Group ??? Strong presence in environmental engineering, ESG strategy, and renewable energy advisory.

- SLR Consulting ??? Focused on environmental, sustainability, and carbon-risk advisory solutions.

- GHD Group ??? Expanding in engineering, water, environmental risk, and sustainability consulting services.

Key Competitive Intensity Signals

- Competition in ESG advisory and climate-risk consulting is rapidly intensifying.

- Regulatory compliance expertise remains a major barrier to entry.

- Digital sustainability analytics and AI-based monitoring are becoming core service differentiators.

- Large infrastructure and remediation projects create scale-based competitive advantages.

- Carbon accounting, biodiversity planning, and net-zero advisory are expanding premium consulting demand.

- Integrated engineering + environmental advisory models are reshaping competitive positioning.

- Public-sector and industrial contracts strengthen recurring revenue visibility.

Strategic Implications

- Firms with multidisciplinary engineering and ESG expertise can maintain stronger long-term market positioning.

- Digital environmental monitoring and AI-driven compliance tools may become major differentiators.

- Climate resilience and decarbonization consulting can improve premium-margin opportunities.

- Global regulatory alignment and sector specialization can strengthen enterprise trust.

- Strategic acquisitions and sustainability-tech partnerships may improve service scalability.

Forward Outlook

The Global Environmental Consulting Services Market is expected to remain moderately fragmented with high competitive intensity, supported by ESG expansion, climate adaptation needs, industrial sustainability mandates, and green infrastructure growth.

Future competition will increasingly focus on:

- ESG advisory and sustainability transformation

- Climate-risk and resilience planning

- Carbon accounting and decarbonization strategy

- AI-based environmental analytics

- Biodiversity and ecological risk consulting

- Digital monitoring and remote environmental intelligence

- Circular economy and green infrastructure advisory

The convergence of ESG integration, climate intelligence, digital monitoring, environmental compliance, decarbonization, and sustainability consulting will continue reshaping the long-term competitive landscape.

Value Chain

Global Environmental Consulting Services Market Value Chain & Supply Chain Evolution Overview

The Global Environmental Consulting Services Market operates through a knowledge-intensive advisory ecosystem supported by environmental assessments, regulatory expertise, digital monitoring tools, engineering support, sustainability strategy development, and enterprise-level compliance execution. The market is increasingly shaped by ESG integration, climate risk modeling, carbon accounting, and sustainability transformation services.

The value chain depends on environmental data acquisition, field-based technical assessments, digital analytics, consulting expertise, regulatory interpretation, project execution support, and long-term sustainability monitoring.

Supply chain complexity is moderate to high due to regulatory variability, project-specific customization, multidisciplinary technical workflows, environmental data dependency, field execution coordination, and client-specific compliance requirements.

Global Environmental Consulting Services Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

1. Data Collection & Environmental Input Assessment

Site inspections, emissions data, pollution measurements, GIS mapping, biodiversity studies, water analysis, climate data, and regulatory baseline inputs.

2. Environmental Analysis & Advisory Design

Environmental impact assessments (EIA), contamination analysis, carbon accounting, ESG advisory, climate risk assessment, sustainability planning, and remediation strategy design.

3. Digital Tools & Technical Integration

AI-based monitoring systems, remote sensing, environmental modeling, digital twins, sustainability software, compliance dashboards, and reporting automation.

4. Regulatory Review & Compliance Validation

Environmental permits, emissions compliance, ESG disclosures, water safety audits, waste regulations, carbon reporting, and legal risk assessments.

5. Consulting Delivery & Project Execution Support

On-site consulting, remediation supervision, infrastructure advisory, industrial compliance programs, climate resilience planning, and sustainability transformation implementation.

6. End-Use Industry Deployment

Industrial & energy companies, construction firms, mining, oil & gas, utilities, transportation, chemicals, real estate, and public sector organizations.

Key Value Chain Evolution Signals

1. ESG Consulting Expansion

ESG reporting and sustainability advisory are becoming major revenue drivers.

2. Climate Risk Integration

Climate resilience and carbon-neutrality planning are reshaping consulting models.

3. Digital Environmental Monitoring

AI, IoT, GIS, and remote sensing are improving service precision.

4. Regulatory Complexity Growth

Cross-border environmental and disclosure rules are increasing advisory demand.

5. Integrated Sustainability Services

Firms are moving from compliance-only consulting to end-to-end transformation support.

6. Green Infrastructure Support

Renewable energy and smart-city projects are expanding service opportunities.

Strategic Implications

1. Data & Analytics Strength

Environmental intelligence platforms improve differentiation.

2. Regulatory Expertise

Deep compliance knowledge strengthens long-term contracts.

3. Service Diversification

Integrated ESG + climate + remediation offerings improve margins.

4. Field + Digital Hybrid Delivery

Combining on-site execution with digital monitoring improves scalability.

5. Sector-Specific Specialization

Energy, mining, infrastructure, and industrial consulting create stronger market positioning.

Forward Outlook

The market is expected to evolve toward a more digital, ESG-centric, and climate-driven ecosystem through:

- AI-based environmental analytics

- Carbon accounting automation

- Climate resilience consulting

- ESG reporting integration

- Digital twin sustainability modeling

- Smart infrastructure advisory

- Circular economy consulting

- Renewable energy compliance services

Investment Activity

Global Environmental Consulting Services Market Investment & Funding Dynamics Overview

The Global Environmental Consulting Services Market is witnessing strong investment momentum driven by ESG integration, climate resilience planning, decarbonization mandates, and rising environmental compliance requirements. Engineering firms, sustainability consultants, ESG advisory providers, environmental technology companies, and risk-management specialists are actively investing in digital monitoring platforms, climate-risk analytics, carbon accounting tools, biodiversity advisory capabilities, and integrated sustainability consulting infrastructure.

Investment activity is accelerating due to growing demand for ESG reporting, industrial compliance, pollution control, renewable energy advisory, site remediation, and carbon-neutrality strategies. The increasing shift toward AI-driven environmental analytics, digital sustainability monitoring, climate-tech integration, and circular economy consulting is significantly reshaping capital allocation across the market.

Additionally, expanding investments in green infrastructure, smart city sustainability programs, carbon capture advisory, waste-recycling solutions, and environmental risk platforms are strengthening long-term growth opportunities globally.

Global Environmental Consulting Services Market Investment & Funding Dynamics Current Scenario

Currently, the Global Environmental Consulting Services Market demonstrates rising investment activity with medium capital intensity due to digital-platform expansion, analytics software, sustainability advisory scaling, field operations, and environmental compliance infrastructure requirements. Major players are heavily investing in ESG advisory solutions, AI-based emissions monitoring, climate-risk modeling, digital twin sustainability platforms, and enterprise environmental intelligence systems.

The market is attracting strong funding into carbon accounting, biodiversity consulting, remote environmental monitoring, renewable energy transition advisory, and integrated compliance-management solutions. Rising corporate sustainability mandates and government-backed green infrastructure projects are further supporting investment flow.

The industry is witnessing active merger, partnership, and acquisition activity as engineering firms, ESG specialists, climate-tech providers, and environmental consultants pursue service diversification, digital expansion, and integrated sustainability ecosystems.

Key Investment & Funding Dynamics Signals in Global Environmental Consulting Services Market

- Rising demand for ESG reporting, climate-risk planning, and environmental compliance services is accelerating long-term consulting investments.

- Expansion of digital monitoring systems, carbon-accounting platforms, and sustainability analytics tools is increasing capital deployment.

- Growing focus on renewable energy consulting, decarbonization strategies, and circular economy services is strengthening innovation-led funding.

- Strategic investments in AI-driven environmental analytics, remote sensing, and digital twin sustainability modeling are reshaping service priorities.

- Partnerships between engineering firms, ESG providers, climate-tech companies, and governments are improving ecosystem expansion and project delivery.

- Increasing regulatory focus on carbon disclosure, environmental compliance, water safety, and biodiversity protection is supporting investor confidence.

- Rising demand for scalable, data-driven, and sustainability-focused advisory solutions is accelerating R&D and platform spending.

Strategic Implications of Investment & Funding Dynamics in Global Environmental Consulting Services Market

- Continuous investment in ESG advisory, digital environmental monitoring, and climate intelligence tools is essential for long-term competitiveness.

- Medium capital intensity requires strong allocation toward software platforms, analytics systems, skilled advisory teams, and sustainability infrastructure.

- Companies capable of delivering compliant, integrated, and data-driven environmental solutions will strengthen market positioning significantly.

- Strategic M&A and digital partnerships are accelerating service diversification and ESG ecosystem expansion.

- Investments in decarbonization consulting, biodiversity planning, and enterprise sustainability transformation will remain major priorities.

- Compliance with ESG frameworks, carbon standards, environmental laws, and risk-mitigation protocols is critical for long-term adoption.

- Companies investing in climate-tech integration, carbon intelligence, and scalable sustainability platforms are expected to capture substantial future growth opportunities.

Global Environmental Consulting Services Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Environmental Consulting Services Market is expected to maintain strong investment growth driven by ESG transformation, climate adaptation, renewable energy transition, and environmental digitization.

Future capital deployment will increasingly focus on AI-based emissions analytics, smart environmental monitoring, carbon-accounting automation, biodiversity intelligence, climate-risk software, and circular economy consulting. Integrated sustainability ecosystems and climate-tech platforms are expected to become major long-term innovation priorities.

In conclusion, the Global Environmental Consulting Services Market represents a high-growth, sustainability-driven investment landscape where ESG integration, climate intelligence, regulatory compliance, and digital environmental transformation will define future capital strategies.

Technology & Innovation

Global Environmental Consulting Services Market Technology & Innovation Landscape Overview

The Global Environmental Consulting Services Market is undergoing significant transformation driven by AI-powered environmental analytics, ESG automation platforms, remote sensing technologies, GIS-based mapping, digital twin sustainability modeling, carbon accounting systems, and climate-risk intelligence tools. The market reflects a moderate innovation intensity level, supported by increasing regulatory complexity, ESG integration mandates, corporate decarbonization strategies, and rising demand for digital sustainability solutions.

Environmental consulting is increasingly shifting from traditional manual advisory services toward technology-enabled predictive environmental intelligence ecosystems, where firms use automation, analytics, and real-time monitoring to improve compliance, risk assessment, and sustainability planning.

A major innovation area is digital environmental monitoring, including IoT-based air and water quality sensors, drone surveillance, satellite-based environmental observation, and smart contamination detection tools. These technologies are improving site inspections, ecological analysis, and industrial emissions visibility.

The market is also witnessing rapid adoption of ESG and carbon management software, helping enterprises automate sustainability reporting, Scope 1/2/3 emissions tracking, climate disclosure, and environmental KPI monitoring.

Another key advancement is AI-based climate-risk modeling and predictive analytics, where machine learning tools are being used for flood-risk forecasting, land-use simulation, biodiversity assessment, and infrastructure resilience planning.

Consulting firms are increasingly integrating cloud-based environmental dashboards, waste optimization software, digital remediation modeling, water-resource simulation, and circular economy analytics to strengthen data-driven advisory capabilities.

The convergence of AI, geospatial intelligence, IoT monitoring, cloud analytics, ESG software, remote sensing, and climate-tech platforms is reshaping the future innovation landscape of the environmental consulting services market.

Global Environmental Consulting Services Market Technology & Innovation Landscape Current Scenario

Currently, the market demonstrates moderate patent activity and strong technology commercialization, particularly across sustainability analytics, digital monitoring, and ESG compliance solutions.

1. AI-Based Environmental Analytics

Predictive emissions modeling and automated compliance tools are improving consulting precision.

2. GIS & Geospatial Mapping

Environmental impact assessments increasingly use digital mapping and remote sensing.

3. ESG Reporting Platforms

Automated carbon and sustainability dashboards are accelerating enterprise adoption.

4. Climate Risk Intelligence

Simulation models for climate resilience and disaster-risk planning are expanding.

5. IoT Environmental Monitoring

Smart sensors are improving real-time pollution, water, and air-quality tracking.

6. Digital Twin Sustainability Tools

Virtual modeling is improving infrastructure and ecosystem planning.

Key Technology & Innovation Landscape Signals in Global Environmental Consulting Services Market

1. Expansion of ESG Automation

Digital compliance and sustainability reporting platforms are scaling rapidly.

2. Growth in Carbon Accounting Technologies

AI-enabled emissions and decarbonization tools are becoming critical.

3. Rising Climate-Tech Integration

Climate simulation and resilience analytics are improving risk forecasting.

4. Smart Environmental Monitoring

IoT, drones, and satellite systems are enhancing field diagnostics.

5. Geospatial Intelligence Growth

GIS and remote sensing tools are strengthening environmental visibility.

6. Circular Economy Analytics

Waste optimization and resource-efficiency software are improving sustainability outcomes.

7. Cloud-Based Environmental Platforms

Centralized environmental data management is improving enterprise scalability.

Strategic Implications of Technology & Innovation Landscape in Global Environmental Consulting Services Market

Technology innovation is becoming a major differentiator in environmental consulting. Companies are increasingly competing through AI-driven analytics, ESG automation, digital compliance ecosystems, geospatial mapping, remote sensing, and predictive environmental modeling.

Firms investing in carbon-accounting software, IoT monitoring, AI risk analytics, sustainability dashboards, digital twins, and cloud-based environmental intelligence systems are expected to strengthen long-term market positioning.

Strategic partnerships between consulting firms, climate-tech startups, ESG software vendors, satellite-data providers, and industrial analytics companies are accelerating commercialization and expanding integrated sustainability ecosystems.

Additionally, increasing regulatory emphasis on carbon disclosure, emissions tracking, biodiversity management, water safety, remediation compliance, and industrial sustainability reporting is encouraging stronger innovation adoption globally.

Global Environmental Consulting Services Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the market is expected to become increasingly predictive, digital, and automation-driven.

1. AI-Driven Sustainability Intelligence

Advanced predictive environmental decision systems will improve advisory efficiency.

2. Automated Carbon Accounting

Real-time emissions tracking and reporting platforms will become mainstream.

3. Climate Digital Twins

Virtual ecosystem and infrastructure simulations will strengthen resilience planning.

4. Autonomous Monitoring Systems

IoT and remote sensing networks will improve continuous diagnostics.

5. Advanced Geospatial Analytics

Satellite-based predictive environmental mapping will improve land and risk planning.

6. Circular Economy Optimization

AI-based waste reduction and recycling intelligence will expand.

7. Integrated ESG Cloud Ecosystems

Unified environmental compliance and sustainability platforms will reshape enterprise consulting.

In conclusion, the Global Environmental Consulting Services Market represents a technology-enabled sustainability ecosystem, where AI, ESG automation, climate-tech, geospatial analytics, IoT monitoring, and digital environmental intelligence will define future competitive leadership.

Market Risk

Global Environmental Consulting Services Market Risk & Disruption Analysis

The Global Environmental Consulting Services Market operates within a moderate-risk, regulation-intensive, and transformation-driven disruption environment, driven by evolving ESG mandates, climate policy changes, industrial sustainability pressure, carbon disclosure requirements, digital environmental intelligence adoption, and infrastructure-linked advisory demand. While the market demonstrates strong long-term growth due to decarbonization initiatives, corporate sustainability commitments, environmental compliance complexity, and climate resilience investments, it remains exposed to regulatory volatility, project-cycle dependency, macroeconomic spending shifts, and service commoditization risks.

A defining structural characteristic of the market is its dependence on policy-linked and compliance-driven consulting ecosystems, where revenue generation is closely tied to environmental legislation, industrial permitting, ESG disclosures, remediation obligations, and climate-related reporting frameworks. Environmental compliance & risk assessment services remain the dominant segment, while high-growth value is increasingly shifting toward ESG advisory, climate risk consulting, carbon accounting, and digital environmental analytics.

The market is also transitioning from traditional compliance-focused consulting toward integrated sustainability intelligence, AI-driven monitoring, climate resilience planning, biodiversity advisory, and enterprise ESG transformation services, increasing technological and strategic disruption.

Global Environmental Consulting Services Market Current Risk Environment

Currently, the market operates under strong regulatory demand, moderate service fragmentation, and increasing digital transformation.

One of the most significant disruption factors is regulatory and policy volatility. Environmental standards, carbon pricing rules, emissions frameworks, biodiversity protections, ESG disclosures, and regional climate regulations continue evolving, creating both demand and compliance uncertainty.

Another major risk area is macroeconomic and project-cycle sensitivity. Environmental consulting demand is often tied to infrastructure investment, industrial expansion, energy projects, remediation programs, and public-sector sustainability budgets. Economic slowdowns may delay discretionary consulting spend.

The market also faces service commoditization and pricing pressure. Standard compliance assessments, audits, and reporting services may become highly competitive, particularly among mid-tier consulting firms and digital sustainability platforms.

Additionally, technology disruption from AI, remote sensing, automation, and ESG software platforms is reshaping traditional consulting models.

In parallel, geopolitical shifts, energy-transition policy changes, and cross-border ESG reporting fragmentation may affect long-term strategic planning.

Key Market Risk & Disruption Signals in Global Environmental Consulting Services Market

1. Regulatory & ESG Policy Volatility

Changing emissions laws, ESG frameworks, and climate rules directly shape service demand.

2. Project-Cycle & Infrastructure Dependency

Consulting growth is tied to industrial expansion, energy investment, and public infrastructure.

3. Service Commoditization & Margin Pressure

Standard compliance and reporting services may face increasing pricing competition.

4. Technology Disruption & Digital Advisory Shift

AI analytics, GIS, remote monitoring, and automation are transforming consulting delivery.

5. Geopolitical & Energy Transition Exposure

Policy changes around energy, mining, and environmental regulation affect consulting priorities.

6. Cross-Border ESG Fragmentation

Regional sustainability standards and disclosure frameworks create complexity.

7. Skilled Workforce & Domain Expertise Dependency

Demand for climate scientists, ESG specialists, and environmental engineers remains high.

8. Corporate Sustainability Budget Variability

Consulting demand may fluctuate with enterprise ESG investment cycles.

Strategic Implications of Market Risk & Disruption in Global Environmental Consulting Services Market

The evolving disruption environment creates strong advisory growth opportunities alongside increasing specialization pressure.

One of the most important strategic implications is the growing need for integrated environmental intelligence ecosystems. Consulting firms increasingly must combine regulatory expertise, digital tools, sustainability modeling, and climate analytics.

Companies must invest in AI-based emissions monitoring, ESG reporting systems, biodiversity advisory, carbon accounting, remote sensing, and climate-risk simulation platforms to remain competitive.

Vertical integration across compliance advisory, engineering services, ESG analytics, climate-tech partnerships, and enterprise sustainability strategy is becoming increasingly valuable.

The convergence of decarbonization, ESG investing, digital monitoring, and climate resilience planning is also reshaping value chains. Firms with stronger multidisciplinary capabilities, data-driven advisory models, and global regulatory expertise may gain stronger market resilience.

Additionally, renewable energy growth, green infrastructure, circular economy strategies, and industrial transformation may create durable long-term demand.

Companies focusing on ESG consulting, climate advisory, digital environmental analytics, carbon strategy, and integrated sustainability services are expected to strengthen long-term market leadership.

Global Environmental Consulting Services Market Risk & Disruption Forward Outlook

Looking ahead to 2026???2033, the Global Environmental Consulting Services Market is expected to become increasingly digital, compliance-centric, and climate-strategy focused.

1. Expansion of ESG & Climate Risk Advisory

Carbon disclosure and investor-driven sustainability services will gain strategic value.

2. Greater AI & Digital Environmental Monitoring

Automation, GIS, and predictive analytics will improve consulting efficiency.

3. Higher Regulatory Complexity & Carbon Oversight

Climate reporting and emissions compliance may tighten globally.

4. Growth in Renewable Energy & Green Infrastructure Consulting

Energy transition projects will remain major growth drivers.

5. Rising Enterprise Sustainability Integration

Consulting will increasingly align with broader ESG transformation programs.

6. Stronger Biodiversity & Nature-Risk Advisory Demand

Ecological impact consulting may expand significantly.

7. Competitive Consolidation & Platform Integration

Large engineering and ESG firms may strengthen digital service ecosystems.

8. Broader Circular Economy & Resource Optimization Focus

Waste reduction, water reuse, and industrial efficiency consulting will grow.

In conclusion, the Global Environmental Consulting Services Market represents a knowledge-intensive, regulation-driven, and digitally transforming advisory ecosystem, where regulatory adaptability, ESG intelligence, climate expertise, digital integration, and multidisciplinary consulting strength will define long-term competitive success.

Regulatory Landscape

Global Environmental Consulting Services Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a highly significant role in shaping the Global Environmental Consulting Services Market due to strong oversight around environmental compliance, carbon disclosure, ESG reporting, industrial emissions, water safety, land-use regulations, and sustainability governance. Regulatory frameworks governing environmental impact assessments, pollution control, climate-risk reporting, biodiversity protection, waste management, and decarbonization standards significantly influence consulting demand, project approvals, and long-term market expansion.

Environmental consulting services are widely used across industrial manufacturing, energy, oil & gas, mining, construction, infrastructure, utilities, transportation, and public-sector planning. As governments and corporations strengthen sustainability mandates, regulatory dependency on environmental advisory services continues increasing.

The market is also influenced by evolving ESG frameworks, climate disclosure standards, carbon neutrality policies, circular economy laws, renewable energy compliance, and environmental risk governance. Governments are increasingly balancing economic development with ecological protection and sustainability obligations.

In addition, green infrastructure spending, climate adaptation programs, and corporate sustainability mandates are strengthening structured regulatory enforcement globally.

Global Environmental Consulting Services Market Regulatory & Policy Environment Current Scenario

Currently, the Global Environmental Consulting Services Market operates under a highly structured, compliance-intensive, and multi-jurisdictional regulatory framework involving environmental laws, emissions reporting, land and water protection standards, ESG disclosures, biodiversity oversight, and industrial risk management.

One of the most important regulatory trends is environmental compliance and industrial emissions oversight. Organizations increasingly require advisory support for air quality, waste disposal, site contamination, and ecological risk mitigation.

Another major regulatory factor involves ESG and carbon disclosure governance. Enterprises are facing stronger pressure to align with sustainability reporting, climate-risk transparency, and carbon-accounting obligations.

Cross-border sustainability and environmental compliance also remain important, especially for multinational projects, infrastructure investments, mining, and energy operations.

Sector-specific compliance is especially strong in oil & gas, construction, industrial plants, utilities, renewable energy, and public infrastructure projects.

Additionally, biodiversity conservation, water management, and land restoration laws are creating stronger regulatory oversight.

Key Regulatory & Policy Environment Signals in Global Environmental Consulting Services Market

1. Rising Environmental Compliance & Industrial Risk Standards

Pollution control, remediation, and emissions monitoring remain critical.

2. Expansion of ESG & Carbon Disclosure Requirements

Climate reporting and sustainability governance are increasingly important.

3. Growing Cross-Border Environmental Governance Complexity

Global projects require jurisdiction-specific environmental compliance.

4. Land, Water & Biodiversity Protection Oversight

Ecological risk and natural-resource regulations are strengthening.

5. Climate Adaptation & Green Infrastructure Policy Support

Sustainability-linked consulting demand is accelerating.

Strategic Implications of Regulatory & Policy Environment in Global Environmental Consulting Services Market

The evolving regulatory environment creates major strategic implications for engineering firms, ESG consultants, environmental specialists, infrastructure advisors, and sustainability platforms. One major implication is the growing need for highly compliant, data-driven, and cross-sector environmental advisory ecosystems.

Companies must invest in digital environmental monitoring, ESG reporting tools, carbon-accounting expertise, regulatory intelligence, and climate-risk frameworks to remain globally competitive.

The increasing convergence of decarbonization, biodiversity governance, industrial compliance, and smart sustainability analytics is also pushing firms toward compliance-led innovation.

Organizations capable of balancing technical expertise, regulatory readiness, environmental precision, and scalable advisory models will likely strengthen long-term market positioning.

Additionally, firms with strong ESG integration, multi-sector environmental compliance, and climate resilience planning strategies will gain stronger competitive advantages.

Global Environmental Consulting Services Market Regulatory & Policy Environment Forward Outlook

Looking ahead to 2026???2033, the regulatory environment for environmental consulting services is expected to become increasingly sustainability-driven, disclosure-focused, and climate-governed as global ESG and decarbonization initiatives continue expanding.

Future regulations are likely to place stronger emphasis on carbon accounting, biodiversity impact reporting, circular economy compliance, climate resilience, water security, and environmental transparency.

Governments may continue strengthening emissions laws, ESG reporting mandates, environmental permitting, remediation requirements, and green infrastructure governance.

The expansion of renewable energy, climate-tech, carbon capture, and sustainability transformation may further increase regulatory complexity.

Overall, the regulatory and policy environment will remain a major factor influencing consulting demand, project scalability, compliance intensity, and competitive positioning within the Global Environmental Consulting Services Market.