Global Next Generation Sequencing (NGS) Market Report, Size & Forecast 2026-2033

Global Next-Generation Sequencing (NGS) Market Forecast Snapshot (2026???2033)

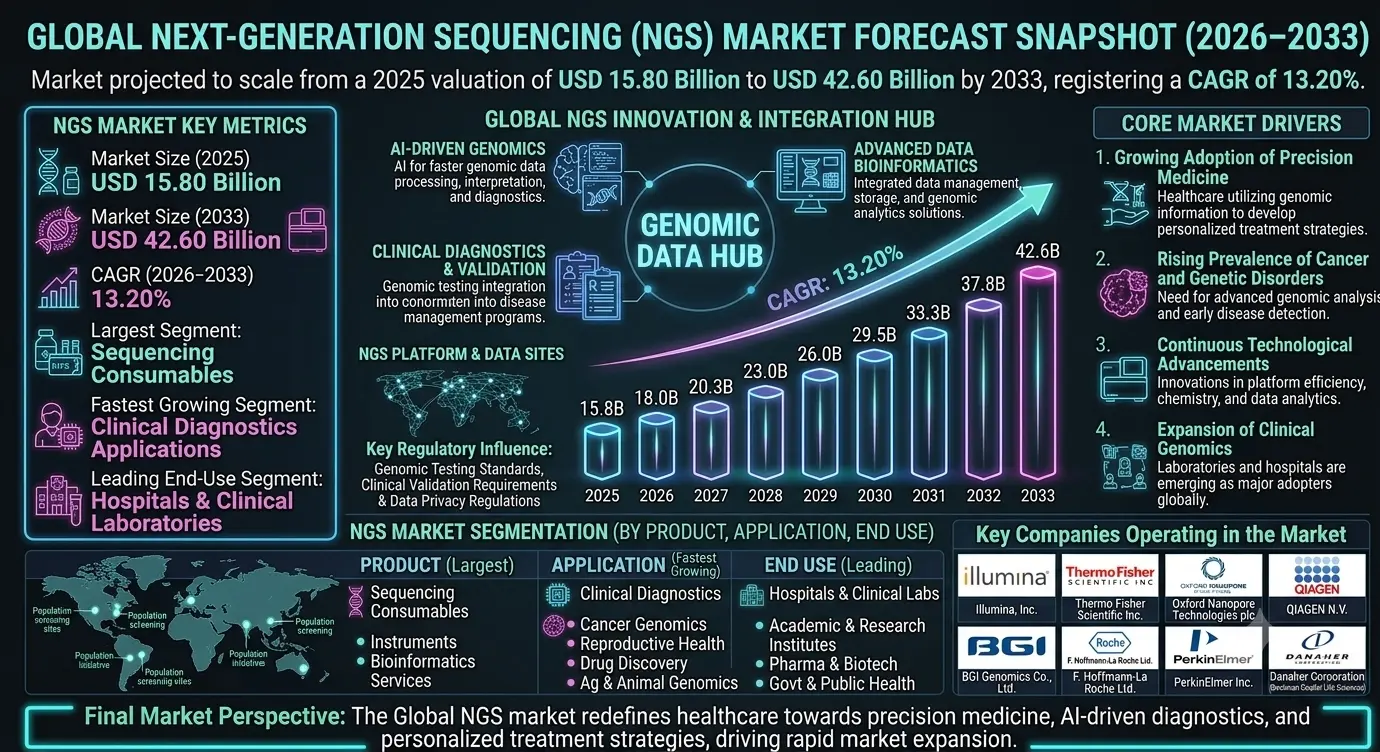

| Metric | Value |

|---|---|

| Market Size (2025) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 15.80 Billion |

| Market Size (2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 42.60 Billion |

| CAGR (2026???2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??13.20% |

| Largest Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Sequencing Consumables |

| Fastest Growing Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Clinical Diagnostics Applications |

| Leading End-Use Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Hospitals & Clinical Laboratories |

| Key Trend | ?? ?? ?? ?? ??Precision Medicine, AI-Driven Genomics & Expansion of Clinical Sequencing Applications |

| Regulatory Influence | ?? ?? ?? ??Genomic Testing Standards, Clinical Validation Requirements & Data Privacy Regulations |

| Future Outlook | Growth Driven by Personalized Medicine, Cancer Genomics & Advancements in Sequencing Technologies |

Global Next-Generation Sequencing (NGS) Market Size & Forecast

The Global Next-Generation Sequencing (NGS) Market is expected to witness robust growth during the forecast period from 2026 to 2033. The market was valued at USD 15.80 billion in 2025 and is projected to reach approximately USD 42.60 billion by 2033, registering a CAGR of 13.20%. Market growth is primarily driven by increasing adoption of precision medicine, rising demand for genomic testing, expanding cancer research activities, and continuous technological advancements in sequencing platforms. The declining cost of genome sequencing and increasing integration of NGS into clinical diagnostics are further accelerating market expansion globally.Global Next-Generation Sequencing (NGS) Market Overview

Next-Generation Sequencing (NGS) refers to advanced sequencing technologies that enable rapid and high-throughput analysis of DNA and RNA. NGS is widely used in clinical diagnostics, oncology, reproductive health, infectious disease testing, agricultural genomics, and drug discovery. The technology provides comprehensive genetic insights with greater speed, scalability, and accuracy compared to traditional sequencing methods. Growing investments in genomics research and increasing applications in personalized healthcare continue to strengthen market growth.Structural Drivers of Market Growth

1. Growing Adoption of Precision Medicine

Healthcare providers are increasingly utilizing genomic information to develop personalized treatment strategies tailored to individual patient profiles. Market Implications: Demand for NGS-based diagnostics and companion diagnostic solutions is expected to increase significantly across healthcare systems.2. Rising Prevalence of Cancer and Genetic Disorders

The increasing burden of cancer and hereditary diseases is driving the need for advanced genomic analysis and molecular diagnostics. Market Implications: NGS technologies are becoming critical tools for early disease detection, biomarker discovery, and targeted therapy selection.3. Continuous Technological Advancements in Sequencing Platforms

Innovations in sequencing chemistry, automation, bioinformatics, and data analysis are improving sequencing efficiency and reducing costs. Market Implications: Technology providers are expanding adoption across research, clinical, and commercial applications.4. Expansion of Clinical Genomics and Molecular Diagnostics

Healthcare institutions are increasingly integrating genomic testing into routine diagnostic workflows and disease management programs. Market Implications: Clinical laboratories and hospitals are emerging as major adopters of NGS technologies worldwide.Market Segmentation Analysis

By Product

- Sequencing Consumables Largest segment due to recurring demand for reagents, sample preparation kits, and sequencing cartridges.

- Sequencing Instruments Includes high-throughput and benchtop sequencing platforms used in research and diagnostics.

- Bioinformatics Services Provides data processing, interpretation, storage, and genomic analytics solutions.

By Application

- Cancer Genomics Major application area supporting tumor profiling, biomarker identification, and targeted therapy development.

- Clinical Diagnostics Fastest-growing segment driven by increasing adoption of genomic testing in healthcare settings.

- Reproductive Health Includes prenatal testing, carrier screening, and newborn genetic screening applications.

- Drug Discovery & Development Supports pharmaceutical research, biomarker discovery, and precision medicine initiatives.

- Agricultural & Animal Genomics Used for crop improvement, livestock breeding, and agricultural biotechnology research.

By End Use

- Hospitals & Clinical Laboratories Largest segment due to increasing implementation of genomic testing in routine clinical practice.

- Academic & Research Institutes Significant users of NGS technologies for genomics and life science research.

- Pharmaceutical & Biotechnology Companies Utilize NGS for drug discovery, clinical trials, and companion diagnostics development.

- Government & Public Health Organizations Support population genomics, disease surveillance, and public health initiatives.

Regional Market Dynamics

North America

Leading region due to advanced healthcare infrastructure, strong genomics research funding, and widespread adoption of precision medicine technologies.Europe

Driven by government-supported genomics programs, growing cancer research initiatives, and increasing clinical sequencing adoption.Asia-Pacific

Fastest-growing region supported by expanding healthcare investments, increasing genomic research activities, and rising awareness of personalized medicine.Latin America

Growing market driven by improving healthcare infrastructure and increasing access to advanced molecular diagnostic technologies.Middle East & Africa

Emerging market supported by healthcare modernization programs, genomic research investments, and growing demand for advanced diagnostics.Competitive Landscape

The Global Next-Generation Sequencing (NGS) Market is highly competitive with leading genomics companies, biotechnology firms, and healthcare technology providers investing heavily in innovation, platform development, and bioinformatics capabilities. Key Companies Operating in the Market Include:- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- Pacific Biosciences of California, Inc.

- Oxford Nanopore Technologies plc

- QIAGEN N.V.

- Agilent Technologies, Inc.

- BGI Genomics Co., Ltd.

- F. Hoffmann-La Roche Ltd.

- PerkinElmer Inc.

- Danaher Corporation (Beckman Coulter Life Sciences)

Strategic Outlook

The future of the NGS market will be shaped by increasing adoption of precision medicine, expansion of clinical genomics, and continuous technological innovation. Artificial intelligence and advanced bioinformatics tools are expected to improve genomic interpretation, accelerate diagnostics, and enhance treatment personalization. Sequencing costs are expected to decline further, making genomic testing more accessible across healthcare systems. Growing applications in oncology, rare disease diagnostics, infectious disease surveillance, and reproductive health will continue to create substantial growth opportunities. Additionally, government-funded genomics initiatives and population-scale sequencing programs are expected to accelerate market development and broaden the clinical utility of NGS technologies.Final Market Perspective

The Global Next-Generation Sequencing (NGS) Market represents one of the most transformative segments of modern healthcare and life sciences. Increasing demand for genomic insights, personalized medicine, and advanced molecular diagnostics is driving rapid market expansion. As sequencing technologies become more affordable, scalable, and clinically relevant, organizations investing in innovation, bioinformatics, and precision healthcare solutions will be well-positioned to capitalize on long-term opportunities within the evolving global genomics ecosystem.Table of Contents

Table of Contents

- Executive Summary

- Global Next-Generation Sequencing (NGS) Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends in Precision Medicine & Clinical Genomics

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Next-Generation Sequencing (NGS)

- Scope of the Global NGS Market

- Evolution of Genomic Sequencing Technologies

- Role of NGS in Modern Healthcare & Life Sciences

- Value Chain Analysis of the NGS Ecosystem

- Regulatory Influence (Genomic Testing Standards, Clinical Validation Requirements & Data Privacy Regulations)

- Transition Toward AI-Driven Genomics & Clinical Sequencing Applications

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Growing Adoption of Precision Medicine

- Rising Prevalence of Cancer and Genetic Disorders

- Continuous Technological Advancements in Sequencing Platforms

- Expansion of Clinical Genomics and Molecular Diagnostics

- Market Restraints

- High Initial Investment and Infrastructure Costs

- Complexity of Genomic Data Interpretation

- Regulatory and Reimbursement Challenges

- Market Opportunities

- Expansion of Clinical Diagnostics Applications

- Growth of Population Genomics Programs

- Increasing Adoption in Rare Disease Diagnostics

- Advancements in AI-Powered Bioinformatics Solutions

- Market Challenges

- Data Storage and Management Requirements

- Privacy and Ethical Concerns Related to Genomic Information

- Shortage of Skilled Genomics and Bioinformatics Professionals

- Structural Drivers of Market Growth

- Global Next-Generation Sequencing (NGS) Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Sequencing Technology Adoption Trends

- Clinical Genomics Penetration Analysis

- Investment and Funding Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Product

- Sequencing Consumables (Largest Segment)

- Sequencing Instruments

- Bioinformatics Services

- By Application

- Cancer Genomics

- Clinical Diagnostics (Fastest-Growing Segment)

- Reproductive Health

- Drug Discovery & Development

- Agricultural & Animal Genomics

- By End Use

- Hospitals & Clinical Laboratories (Largest Segment)

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Government & Public Health Organizations

- By Product

- Regional Market Analysis

- North America (Largest Regional Market)

- Europe

- Asia-Pacific (Fastest-Growing Region)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- Sequencing Technology, AI & Bioinformatics Strategies

- Partnerships, Acquisitions & Genomics Ecosystem Expansion

- Company Profiles

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- Pacific Biosciences of California, Inc.

- Oxford Nanopore Technologies plc

- QIAGEN N.V.

- Agilent Technologies, Inc.

- BGI Genomics Co., Ltd.

- F. Hoffmann-La Roche Ltd.

- PerkinElmer Inc.

- Danaher Corporation (Beckman Coulter Life Sciences)

- Strategic Outlook

- Future of Precision Medicine and Clinical Genomics

- Expansion of AI-Powered Genomic Analytics

- Growth of Population-Scale Sequencing Programs

- Advancements in Sequencing Accuracy, Speed & Accessibility

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Next-Generation Sequencing (NGS) Market Competitive Intensity & Market Structure Overview

The Global Next-Generation Sequencing (NGS) Market is highly competitive and moderately consolidated, with leading genomics technology providers, life sciences companies, biotechnology firms, and molecular diagnostics developers competing across sequencing platforms, consumables, and bioinformatics solutions. Competitive intensity is primarily driven by sequencing accuracy, throughput capabilities, cost efficiency, clinical validation, bioinformatics integration, and regulatory compliance.

Companies compete across sequencing instruments, consumables, genomic analysis software, clinical sequencing services, oncology diagnostics, reproductive health testing, and precision medicine applications. Increasing demand for personalized healthcare, cancer genomics, and clinical molecular diagnostics is intensifying competition throughout the genomics value chain.

The market structure is evolving from research-focused sequencing applications toward large-scale clinical adoption and integrated genomic healthcare ecosystems. Strategic collaborations among sequencing technology providers, healthcare institutions, pharmaceutical companies, and research organizations are reshaping competitive dynamics across the global genomics industry.

Global Next-Generation Sequencing (NGS) Market Competitive Intensity & Market Structure Current Scenario

Leading Global Next-Generation Sequencing (NGS) Companies

- Illumina, Inc.: The global market leader in next-generation sequencing technologies, offering high-throughput sequencing platforms, consumables, and bioinformatics solutions for research and clinical applications.

- Thermo Fisher Scientific Inc.: A major provider of sequencing instruments, reagents, and genomic analysis solutions supporting clinical diagnostics, research, and pharmaceutical applications.

- Pacific Biosciences of California, Inc.: A leading developer of long-read sequencing technologies focused on highly accurate genomic analysis and advanced molecular research.

- Oxford Nanopore Technologies plc: Known for portable and real-time sequencing platforms, enabling flexible genomic analysis across clinical, research, and field-based applications.

- QIAGEN N.V.: A global provider of sample preparation technologies, molecular testing solutions, and bioinformatics platforms supporting NGS workflows.

- Agilent Technologies, Inc.: Offers genomic analysis tools, sample preparation solutions, and workflow optimization technologies for sequencing applications.

- BGI Genomics Co., Ltd.: A major genomics organization providing sequencing services, genomic research capabilities, and large-scale population genomics programs.

- F. Hoffmann-La Roche Ltd.: Expanding its presence in clinical sequencing and precision diagnostics through integrated molecular testing and genomic healthcare solutions.

- PerkinElmer Inc.: Provides genomic testing technologies, sequencing workflow solutions, and molecular diagnostics capabilities for clinical and research applications.

- Danaher Corporation (Beckman Coulter Life Sciences): Offers advanced genomics tools, laboratory automation technologies, and sequencing workflow solutions supporting life sciences research.

Key Competitive Intensity & Market Structure Drivers

The growing adoption of precision medicine is intensifying competition as healthcare providers increasingly rely on genomic information for personalized treatment planning and disease management.

Continuous advancements in sequencing technologies, including long-read sequencing, ultra-high-throughput platforms, and real-time genomic analysis, are accelerating innovation-based competition.

Increasing demand for cancer genomics, rare disease diagnostics, reproductive health testing, and infectious disease surveillance is expanding commercial opportunities across clinical sequencing applications.

The integration of artificial intelligence, machine learning, and advanced bioinformatics platforms is becoming a major competitive differentiator for genomic data interpretation and clinical decision support.

Regulatory requirements related to genomic testing validation, patient data privacy, and clinical compliance standards are creating barriers to entry while favoring established market participants.

Strategic Implications of Competitive Intensity & Market Structure

Companies with advanced sequencing technologies, strong consumables portfolios, robust bioinformatics capabilities, and established clinical partnerships are expected to maintain significant competitive advantages.

Investment in AI-powered genomic analysis, cloud-based bioinformatics platforms, and clinical workflow integration is becoming essential for long-term market differentiation.

Organizations focusing on reducing sequencing costs, improving turnaround times, and enhancing genomic accuracy are likely to strengthen market adoption across healthcare systems.

Strategic collaborations with hospitals, research institutes, pharmaceutical companies, and public health organizations are enabling market participants to expand clinical utility and commercial reach.

Companies capable of combining technological innovation, clinical validation, regulatory compliance, and scalable genomic solutions will be best positioned to compete effectively in the evolving NGS market.

Global Next-Generation Sequencing (NGS) Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global NGS market is expected to become increasingly innovation-driven as precision medicine, population genomics, and molecular diagnostics continue to expand worldwide.

Future competition will be shaped by advancements in sequencing chemistry, AI-powered genomic interpretation, multi-omics integration, and automated bioinformatics workflows that improve clinical decision-making and research productivity.

NGS providers are expected to increase investments in next-generation sequencing platforms, clinical diagnostics applications, cloud-based analytics, and large-scale genomic data management systems to strengthen market positioning.

Over the forecast period, companies that successfully balance sequencing performance, affordability, regulatory compliance, clinical utility, and bioinformatics innovation will be best positioned to lead the evolving global Next-Generation Sequencing (NGS) market.

Value Chain

Global Next-Generation Sequencing (NGS) Market Value Chain & Supply Chain Evolution Overview

The Global Next-Generation Sequencing (NGS) Market operates through a highly specialized value chain encompassing genomic sample collection, reagent manufacturing, sequencing platform development, bioinformatics analysis, clinical interpretation, and healthcare deployment. The ecosystem connects biotechnology companies, sequencing technology providers, healthcare institutions, research organizations, pharmaceutical companies, and regulatory agencies.

The NGS value chain is rapidly evolving through advancements in sequencing chemistry, automation, artificial intelligence, cloud-based bioinformatics, and precision medicine applications. As genomic testing becomes increasingly integrated into clinical practice, demand for scalable, accurate, and cost-effective sequencing solutions continues to expand globally.

Growing investments in cancer genomics, rare disease diagnostics, population genomics programs, and infectious disease surveillance are strengthening the entire NGS ecosystem while driving innovation across sequencing workflows and data analytics platforms.

Global Next-Generation Sequencing (NGS) Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Sample Collection & Preparation: Collection of blood, tissue, saliva, and other biological samples followed by DNA/RNA extraction, purification, and library preparation.

- Reagents & Consumables Manufacturing: Production of sequencing kits, reagents, enzymes, sample preparation solutions, flow cells, cartridges, and sequencing consumables.

- Sequencing Instrument Development: Design and manufacturing of high-throughput, benchtop, and portable sequencing platforms utilizing advanced sequencing technologies.

- Sequencing Workflow Execution: Processing of prepared samples through sequencing instruments to generate genomic and transcriptomic data.

- Bioinformatics & Data Analysis: Data processing, genome alignment, variant calling, annotation, interpretation, cloud computing, and AI-driven analytics.

- Clinical Interpretation & Reporting: Translation of sequencing results into actionable clinical insights for diagnostics, treatment planning, and disease management.

- Healthcare & Research Deployment: Integration of NGS applications across hospitals, clinical laboratories, pharmaceutical companies, research institutes, and public health programs.

- End User Utilization: Physicians, researchers, pharmaceutical developers, genetic counselors, public health agencies, and patients utilizing genomic insights.

Company-to-Stage Mapping

- Sample Collection & Preparation: QIAGEN N.V., Agilent Technologies, Roche Diagnostics, and laboratory sample preparation solution providers.

- Reagents & Consumables Manufacturing: Illumina, Thermo Fisher Scientific, QIAGEN, Agilent Technologies, and BGI Genomics.

- Sequencing Instrument Development: Illumina, Oxford Nanopore Technologies, Pacific Biosciences, Thermo Fisher Scientific, and BGI Genomics.

- Sequencing Workflow Execution: Clinical laboratories, genomic service providers, academic research centers, and contract research organizations.

- Bioinformatics & Data Analysis: Illumina Informatics, Roche Sequencing Solutions, cloud bioinformatics providers, and AI-driven genomics software companies.

- Clinical Interpretation & Reporting: Hospitals, molecular diagnostic laboratories, genetic testing providers, and clinical genomics specialists.

- Healthcare & Research Deployment: Pharmaceutical companies, biotechnology firms, academic institutions, and public health organizations.

- End User Utilization: Healthcare providers, researchers, government agencies, pharmaceutical developers, and patients.

Key Value Chain & Supply Chain Evolution Signals

- Expansion of Precision Medicine Applications: Increasing use of genomic information for personalized therapies is accelerating demand for NGS technologies.

- Growth of AI-Driven Bioinformatics: Artificial intelligence is improving genomic interpretation, variant analysis, and clinical decision support capabilities.

- Declining Sequencing Costs: Technological advancements are reducing sequencing expenses and improving accessibility across healthcare systems.

- Expansion of Clinical Genomics: Hospitals and diagnostic laboratories are integrating NGS into routine clinical workflows for disease diagnosis and monitoring.

- Growth of Population Genomics Programs: Government-sponsored sequencing initiatives are driving large-scale adoption of genomic technologies.

- Increasing Adoption of Cloud-Based Data Platforms: Cloud infrastructure is enabling scalable genomic data storage, sharing, and analytics.

Strategic Implications of Value Chain Evolution

- Investment in Sequencing Innovation: Companies developing faster, more accurate, and cost-efficient sequencing platforms can strengthen market leadership.

- Expansion of Bioinformatics Capabilities: Advanced analytics and AI-powered interpretation solutions are becoming critical competitive differentiators.

- Strengthening Clinical Laboratory Integration: Seamless workflow solutions improve adoption across healthcare institutions and diagnostic centers.

- Development of Companion Diagnostics: Integration of NGS into targeted therapy selection creates significant growth opportunities in precision medicine.

- Enhancement of Data Security & Compliance: Robust genomic data governance and privacy protection are essential for regulatory compliance.

- Expansion of Global Genomics Infrastructure: Investments in sequencing capacity and laboratory networks support long-term market growth.

Global Next-Generation Sequencing (NGS) Market Value Chain & Supply Chain Evolution Forward Outlook

- Expansion of AI-powered genomic analysis and clinical decision support systems.

- Continued decline in sequencing costs and increased accessibility of genomic testing.

- Growth of precision medicine and companion diagnostic applications.

- Increasing adoption of cloud-native bioinformatics and genomic data platforms.

- Expansion of population genomics and national sequencing initiatives.

- Development of next-generation long-read and real-time sequencing technologies.

The NGS value chain is expected to become increasingly automated, data-driven, and clinically integrated. Advances in sequencing technologies, bioinformatics, and artificial intelligence will continue transforming genomic research and healthcare delivery worldwide.

Organizations that successfully combine sequencing innovation, bioinformatics expertise, clinical integration, and scalable genomics infrastructure will be best positioned to achieve long-term growth and leadership in the Global Next-Generation Sequencing (NGS) Market.

Investment Activity

Global Next-Generation Sequencing (NGS) Market Investment & Funding Dynamics Overview (2026???2033)

The Global Next-Generation Sequencing (NGS) Market is experiencing strong investment momentum driven by the rapid expansion of precision medicine, increasing adoption of genomic testing, growing oncology research activities, and continuous advancements in sequencing technologies. Venture capital firms, private equity investors, biotechnology companies, pharmaceutical organizations, healthcare institutions, and government agencies are actively investing in advanced sequencing platforms, genomic diagnostics, bioinformatics solutions, AI-powered genomic analytics, and large-scale genomics infrastructure.

Investment activity is accelerating as healthcare systems increasingly integrate genomic testing into clinical workflows and personalized treatment strategies. Capital deployment is focused on high-throughput sequencing technologies, clinical genomics applications, cancer diagnostics, companion diagnostics, and cloud-based genomic data management platforms.

Additionally, growing investments in population genomics programs, molecular diagnostics infrastructure, AI-driven genomic interpretation tools, and next-generation bioinformatics platforms are creating substantial long-term opportunities across the global genomics ecosystem.

Current Investment & Funding Landscape

The current market landscape is characterized by significant funding activity across genomics research, clinical diagnostics, and sequencing technology development. Leading industry participants are expanding investments in sequencing instrument innovation, consumables production, automation technologies, and genomic data analytics capabilities.

Healthcare providers and research institutions are increasingly investing in clinical sequencing laboratories, precision medicine initiatives, cancer genomics programs, and genetic disease screening platforms. At the same time, governments are allocating funding toward national genomics projects and public health sequencing programs.

Strategic partnerships among sequencing technology companies, pharmaceutical firms, academic institutions, healthcare providers, and bioinformatics developers are accelerating innovation and driving commercialization of advanced genomic solutions.

Key Investment & Funding Dynamics Signals

- Growing adoption of precision medicine and personalized healthcare is driving substantial investments in genomic technologies.

- Increasing demand for clinical diagnostics and cancer genomics applications is attracting strong funding across healthcare markets.

- Expansion of AI-powered bioinformatics and genomic data analytics platforms is accelerating technology-focused investments.

- Rising investments in population genomics and national sequencing initiatives are strengthening public-sector funding opportunities.

- Growing utilization of NGS in rare disease diagnostics, reproductive health, and infectious disease surveillance is broadening investment scope.

- Strategic funding for sequencing consumables, automation technologies, and laboratory infrastructure is supporting market scalability.

- Increasing emphasis on genomic data security, interoperability, and regulatory compliance is influencing capital allocation decisions.

Strategic Implications of Investment & Funding Dynamics

- Companies investing in high-throughput sequencing platforms and advanced bioinformatics capabilities are expected to strengthen market leadership.

- Capital allocation toward clinical diagnostics, oncology applications, and precision medicine solutions will remain a major growth priority.

- Organizations developing AI-enabled genomic interpretation and decision-support tools are likely to attract sustained investor interest.

- Strategic collaborations between genomics companies, pharmaceutical firms, healthcare providers, and research institutions will accelerate innovation and commercialization.

- Investments in cloud-based genomic data platforms and scalable sequencing infrastructure will enhance operational efficiency and accessibility.

- Compliance with genomic testing standards, clinical validation requirements, and data privacy regulations will continue shaping funding strategies.

- Organizations integrating sequencing technologies, bioinformatics, and clinical applications into comprehensive genomic ecosystems are expected to capture substantial long-term value.

Forward Outlook

Looking ahead, the Global Next-Generation Sequencing (NGS) Market is expected to maintain strong investment growth driven by expanding precision medicine adoption, increasing clinical genomics applications, and ongoing technological innovation. Future capital deployment will increasingly focus on AI-driven genomic analytics, advanced sequencing platforms, molecular diagnostics solutions, and population-scale genomics initiatives.

Investment activity is also expected to increase across cancer genomics, reproductive health testing, rare disease diagnostics, infectious disease surveillance, and cloud-based genomic data ecosystems, creating new opportunities for technology developers and healthcare providers.

As genomic medicine becomes a core component of modern healthcare, funding will continue to expand across sequencing infrastructure, bioinformatics innovation, clinical diagnostics, and precision healthcare platforms.

In conclusion, the Global Next-Generation Sequencing (NGS) Market represents a strategically significant healthcare and life sciences investment landscape where precision medicine, AI-powered genomics, clinical sequencing adoption, and advanced bioinformatics technologies will define future funding priorities, competitive differentiation, and long-term market growth.

Technology & Innovation

Global Next-Generation Sequencing (NGS) Market Technology & Innovation Landscape Overview

The Global Next-Generation Sequencing (NGS) Market is experiencing rapid technological evolution driven by increasing demand for precision medicine, advanced molecular diagnostics, and large-scale genomic research. Continuous innovation in sequencing chemistry, high-throughput platforms, automation technologies, and bioinformatics solutions is significantly improving sequencing speed, accuracy, scalability, and affordability. As healthcare providers, research institutions, and biotechnology companies increasingly rely on genomic insights for disease diagnosis, drug discovery, and personalized treatment strategies, technology innovation has become a critical growth driver across the NGS ecosystem. The market is also benefiting from advancements in artificial intelligence, cloud computing, and data analytics that enable efficient interpretation of complex genomic datasets.

The growing integration of NGS into clinical diagnostics, oncology testing, reproductive health screening, infectious disease surveillance, and population genomics programs is accelerating investment in next-generation sequencing technologies worldwide. Manufacturers and technology providers are focusing on developing user-friendly sequencing platforms, streamlined workflows, and advanced genomic analysis tools that improve accessibility and support broader adoption across healthcare and research environments. These innovations continue to expand the clinical utility and commercial viability of NGS technologies globally.

Global Next-Generation Sequencing (NGS) Market Technology & Innovation Current Scenario

The current technology landscape is characterized by significant advancements in sequencing platforms, automation systems, and genomic data analysis capabilities. High-throughput sequencing instruments are delivering faster turnaround times, improved read accuracy, and greater scalability while reducing operational costs. Long-read sequencing technologies, single-cell sequencing platforms, and targeted sequencing approaches are gaining widespread adoption as researchers and clinicians seek deeper genomic insights for complex diseases and precision medicine applications.

Artificial intelligence and advanced bioinformatics solutions are playing an increasingly important role in genomic interpretation, variant analysis, biomarker discovery, and clinical decision support. Cloud-based genomic data management platforms are enabling secure storage, collaboration, and large-scale analysis of sequencing datasets across institutions and geographic regions. In addition, automation technologies in sample preparation, library construction, and sequencing workflows are improving laboratory efficiency, reducing human error, and supporting the growing demand for clinical and research sequencing services.

Key Technology & Innovation Trends in Global Next-Generation Sequencing (NGS) Market

- High-Throughput Sequencing Platforms: Enhancing sequencing capacity, speed, and cost efficiency for large-scale genomic applications.

- Long-Read Sequencing Technologies: Improving structural variant detection, genome assembly, and complex genomic analysis.

- Single-Cell Sequencing Solutions: Enabling detailed analysis of cellular heterogeneity and disease mechanisms.

- AI-Driven Genomic Analytics: Accelerating genomic interpretation, biomarker discovery, and clinical decision-making.

- Advanced Bioinformatics Platforms: Supporting data processing, visualization, storage, and genomic workflow management.

- Automated Sample Preparation Systems: Increasing laboratory efficiency and reducing manual processing requirements.

- Cloud-Based Genomics Infrastructure: Facilitating large-scale data storage, collaboration, and remote genomic analysis.

- Targeted Sequencing Technologies: Improving diagnostic precision and reducing testing costs for specific applications.

- Clinical Genomics Integration: Expanding the use of NGS in routine healthcare and molecular diagnostics workflows.

- Multi-Omics Data Integration: Combining genomic, transcriptomic, proteomic, and clinical data for comprehensive biological insights.

Strategic Implications of Technology & Innovation

Technological advancements are enabling NGS providers to improve sequencing performance, expand clinical applications, and strengthen competitive positioning within the rapidly evolving genomics market. Organizations investing in advanced sequencing platforms, artificial intelligence capabilities, and integrated bioinformatics solutions are enhancing their ability to deliver faster, more accurate, and clinically actionable genomic insights. Innovation is also helping reduce sequencing costs, making genomic testing more accessible across healthcare systems and research institutions worldwide.

The growing adoption of precision medicine and personalized healthcare is increasing the strategic importance of genomic technologies across the healthcare value chain. Companies that successfully combine sequencing innovation, data analytics expertise, regulatory compliance, and clinical validation capabilities are expected to capture significant growth opportunities. At the same time, data privacy, cybersecurity, regulatory approval processes, and reimbursement challenges remain important considerations for market participants seeking sustainable long-term expansion.

Global Next-Generation Sequencing (NGS) Market Technology & Innovation Forward Outlook

The future of the Global Next-Generation Sequencing (NGS) Market is expected to be shaped by continued advancements in sequencing technologies, artificial intelligence, multi-omics research, and clinical genomics integration. Emerging innovations are likely to further improve sequencing accuracy, reduce turnaround times, and lower overall testing costs, making genomic analysis more accessible for routine healthcare applications. Increasing adoption of population genomics programs, cancer precision medicine initiatives, and rare disease diagnostics will continue to drive demand for advanced sequencing solutions across global markets.

As healthcare systems increasingly embrace personalized medicine and data-driven clinical decision-making, NGS technologies are expected to become a foundational component of modern diagnostics and therapeutic development. Ongoing investments in bioinformatics, automation, cloud infrastructure, and genomic research are anticipated to unlock new applications and commercial opportunities throughout the genomics ecosystem. Companies that prioritize technological innovation, clinical utility, and scalable genomic solutions will be well-positioned to benefit from the long-term growth potential of the global NGS market.

Market Risk

Global Next-Generation Sequencing (NGS) Market Risk Factors & Disruption Threats Overview

The Global Next-Generation Sequencing (NGS) Market operates within a rapidly evolving genomics and precision medicine ecosystem driven by technological innovation, expanding clinical applications, and increasing investments in healthcare research. While the market benefits from growing adoption of genomic testing, cancer diagnostics, and personalized medicine, it faces significant risks related to regulatory complexity, data privacy concerns, reimbursement challenges, and technological disruption.

A major structural risk is the highly regulated nature of clinical genomics and molecular diagnostics. NGS-based tests must comply with stringent validation, quality assurance, and regulatory approval requirements, which can increase commercialization timelines and development costs.

Another significant disruption factor is the growing volume of genomic data generated through sequencing activities. Data storage, interpretation, cybersecurity, and patient privacy concerns continue to present operational and compliance challenges for healthcare providers and sequencing companies.

The market is also exposed to reimbursement uncertainties and healthcare budget constraints. Limited insurance coverage or inconsistent reimbursement policies for genomic testing may restrict adoption across certain healthcare systems and patient populations.

Additionally, rapid technological advancements create competitive pressures, as emerging sequencing platforms, bioinformatics solutions, and alternative molecular diagnostic technologies may disrupt existing business models and accelerate product obsolescence.

Global Next-Generation Sequencing (NGS) Market Risk Factors & Disruption Threats Current Scenario

The current market is characterized by strong demand for genomic analysis across oncology, rare disease diagnostics, reproductive health, infectious disease surveillance, and drug discovery applications.

Healthcare providers, research institutions, and pharmaceutical companies are increasingly integrating NGS technologies into clinical workflows and research programs to improve diagnostic accuracy and treatment outcomes.

Manufacturers are investing heavily in higher-throughput sequencing systems, automated sample preparation technologies, and advanced bioinformatics platforms to improve efficiency and reduce sequencing costs.

At the same time, regulators are strengthening oversight of genomic testing standards, laboratory quality requirements, and patient data protection frameworks, increasing compliance expectations across the industry.

Competition continues to intensify as established genomics companies, biotechnology firms, diagnostic providers, and emerging technology innovators expand their sequencing capabilities and clinical offerings.

Key Risk Factors & Disruption Threats Signals in Global Next-Generation Sequencing (NGS) Market

A major disruption signal is the increasing integration of artificial intelligence and machine learning technologies into genomic analysis workflows, significantly improving variant interpretation, clinical decision support, and diagnostic accuracy.

Another important signal is the growing adoption of population-scale genomics programs and national sequencing initiatives, creating opportunities while simultaneously increasing regulatory and data governance requirements.

The rise of long-read sequencing technologies and next-generation molecular analysis platforms is reshaping competitive dynamics and expanding the scope of genomic applications.

Growing concerns regarding genomic data privacy, ethical use of genetic information, and cybersecurity risks are influencing policy development and operational practices across healthcare systems.

Increasing demand for decentralized and point-of-care molecular diagnostics may encourage innovation in faster, more accessible sequencing technologies for clinical settings.

Strategic Implications of Risk Factors & Disruption Threats in Global Next-Generation Sequencing (NGS) Market

NGS providers must prioritize regulatory compliance, clinical validation, and quality management systems to ensure successful commercialization and market acceptance.

Investment in advanced bioinformatics, artificial intelligence, and secure genomic data management platforms will be critical for extracting clinical value from large-scale sequencing datasets.

Companies should strengthen cybersecurity frameworks and data privacy controls to protect sensitive genetic information and maintain stakeholder trust.

Collaboration with healthcare providers, research institutions, pharmaceutical companies, and government agencies will be essential for expanding clinical adoption and supporting precision medicine initiatives.

Strategic investments in emerging sequencing technologies, workflow automation, and cost-reduction innovations will help companies remain competitive in a rapidly evolving market environment.

Global Next-Generation Sequencing (NGS) Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Next-Generation Sequencing (NGS) Market is expected to evolve toward broader clinical adoption, enhanced automation, and deeper integration into routine healthcare decision-making.

Regulatory frameworks governing genomic testing, patient privacy, and clinical evidence generation are expected to become more comprehensive, requiring ongoing compliance investments from industry participants.

Artificial intelligence, cloud-based bioinformatics platforms, and advanced data analytics will significantly improve genomic interpretation, diagnostic efficiency, and personalized treatment planning.

Expanding applications in oncology, rare diseases, infectious disease monitoring, reproductive health, and population genomics will continue to support long-term market growth worldwide.

Overall, the market will remain highly growth-oriented but increasingly shaped by regulatory compliance, reimbursement policies, data governance requirements, and technological innovation. Long-term industry leaders will be defined by their ability to deliver accurate, scalable, clinically validated, and cost-effective sequencing solutions while maintaining strong data security and analytical capabilities.

Regulatory Landscape

Global Next-Generation Sequencing (NGS) Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Next-Generation Sequencing (NGS) Market is evolving rapidly as genomic technologies become increasingly integrated into clinical diagnostics, precision medicine, public health programs, and biomedical research. Regulatory agencies, healthcare authorities, and data protection bodies are establishing comprehensive frameworks to ensure the safety, accuracy, reliability, and ethical use of genomic testing technologies.

NGS platform manufacturers, diagnostic laboratories, healthcare providers, biotechnology companies, and research institutions must comply with regulations covering clinical validation, laboratory accreditation, genomic data management, patient consent, privacy protection, quality assurance, and medical device approval requirements. As genomic testing becomes more widely adopted, regulatory compliance is becoming a critical factor for market access and commercial success.

The growing use of precision medicine, cancer genomics, rare disease diagnostics, and population-scale sequencing initiatives is encouraging policymakers to strengthen standards that balance innovation, patient safety, data security, and ethical genomic research practices.

Global Next-Generation Sequencing (NGS) Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is primarily focused on ensuring the clinical validity, analytical accuracy, and quality performance of NGS-based testing solutions. Regulatory authorities are increasingly establishing standards for genomic testing workflows, laboratory procedures, and diagnostic interpretation practices.

Clinical validation requirements are becoming more stringent as NGS technologies are increasingly used in patient diagnosis and treatment decision-making. Laboratories and healthcare organizations must demonstrate test accuracy, reproducibility, and clinical relevance before implementation in routine healthcare settings.

Genomic data privacy and security regulations have become central to market operations due to the highly sensitive nature of genetic information. Organizations handling genomic data must comply with strict requirements governing data storage, patient consent, data sharing, cybersecurity, and confidentiality.

Regulatory agencies are also increasing oversight of companion diagnostics and precision medicine applications to ensure that genomic testing supports safe and effective therapeutic decision-making across various disease areas, particularly oncology.

At the same time, international harmonization efforts are encouraging the development of consistent standards for genomic testing quality, laboratory accreditation, and cross-border genomic research collaboration.

Key Regulatory & Policy Environment Signals in Global Next-Generation Sequencing (NGS) Market

- Genomic Testing Standards:

Regulations governing analytical performance, test accuracy, sequencing quality, and validation of NGS-based diagnostic procedures. - Clinical Validation & Laboratory Accreditation Requirements:

Frameworks ensuring diagnostic reliability, laboratory quality management, and compliance with healthcare testing standards. - Genomic Data Privacy & Security Regulations:

Policies governing the collection, storage, protection, sharing, and ethical use of patient genetic information. - Companion Diagnostic Approval Frameworks:

Regulatory pathways supporting the integration of genomic testing into personalized treatment and targeted therapy programs. - Informed Consent & Ethical Genomics Policies:

Requirements addressing patient consent, genetic counseling, research ethics, and responsible use of genomic information. - Medical Device & Diagnostic Product Regulations:

Standards governing the approval, commercialization, and post-market monitoring of sequencing instruments, reagents, and software solutions.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging NGS technology providers and diagnostic laboratories to invest heavily in quality management systems, clinical validation programs, regulatory compliance infrastructure, and cybersecurity capabilities. Regulatory readiness is becoming a major competitive advantage in both research and clinical genomics markets.

Clinical validation requirements are driving increased collaboration between sequencing companies, healthcare institutions, and regulatory authorities to demonstrate the clinical utility and effectiveness of genomic testing solutions.

Data privacy regulations are encouraging organizations to strengthen genomic data governance frameworks, implement advanced encryption technologies, and develop transparent consent management processes for patients and research participants.

Companion diagnostic regulations are creating new growth opportunities for companies developing integrated genomic testing solutions that support precision medicine and targeted therapy selection.

International regulatory convergence is helping facilitate global genomics research initiatives while simultaneously increasing expectations for standardized testing quality and laboratory performance.

Global Next-Generation Sequencing (NGS) Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Next-Generation Sequencing (NGS) Market is expected to become increasingly comprehensive as genomic testing expands across clinical care, public health, pharmaceutical development, and population genomics programs.

Clinical genomics regulations are likely to evolve toward more standardized frameworks for test validation, interpretation, reporting, and integration into routine healthcare delivery systems.

Genomic data privacy requirements are expected to become more stringent as governments seek to protect sensitive genetic information while supporting responsible research collaboration and innovation.

Regulatory oversight of artificial intelligence and bioinformatics tools used in genomic interpretation is anticipated to increase as AI-driven analytics become more important in precision medicine and diagnostic decision support systems.

Overall, the future regulatory landscape will be defined by the convergence of genomic testing standards, clinical validation requirements, data privacy regulations, ethical genomics policies, and precision medicine frameworks. Companies capable of delivering accurate, secure, compliant, and clinically validated NGS solutions will be best positioned to capitalize on long-term opportunities within the rapidly expanding global genomics market.