Global Industrial Automation Market Report, Size & Forecast 2026 - 2033

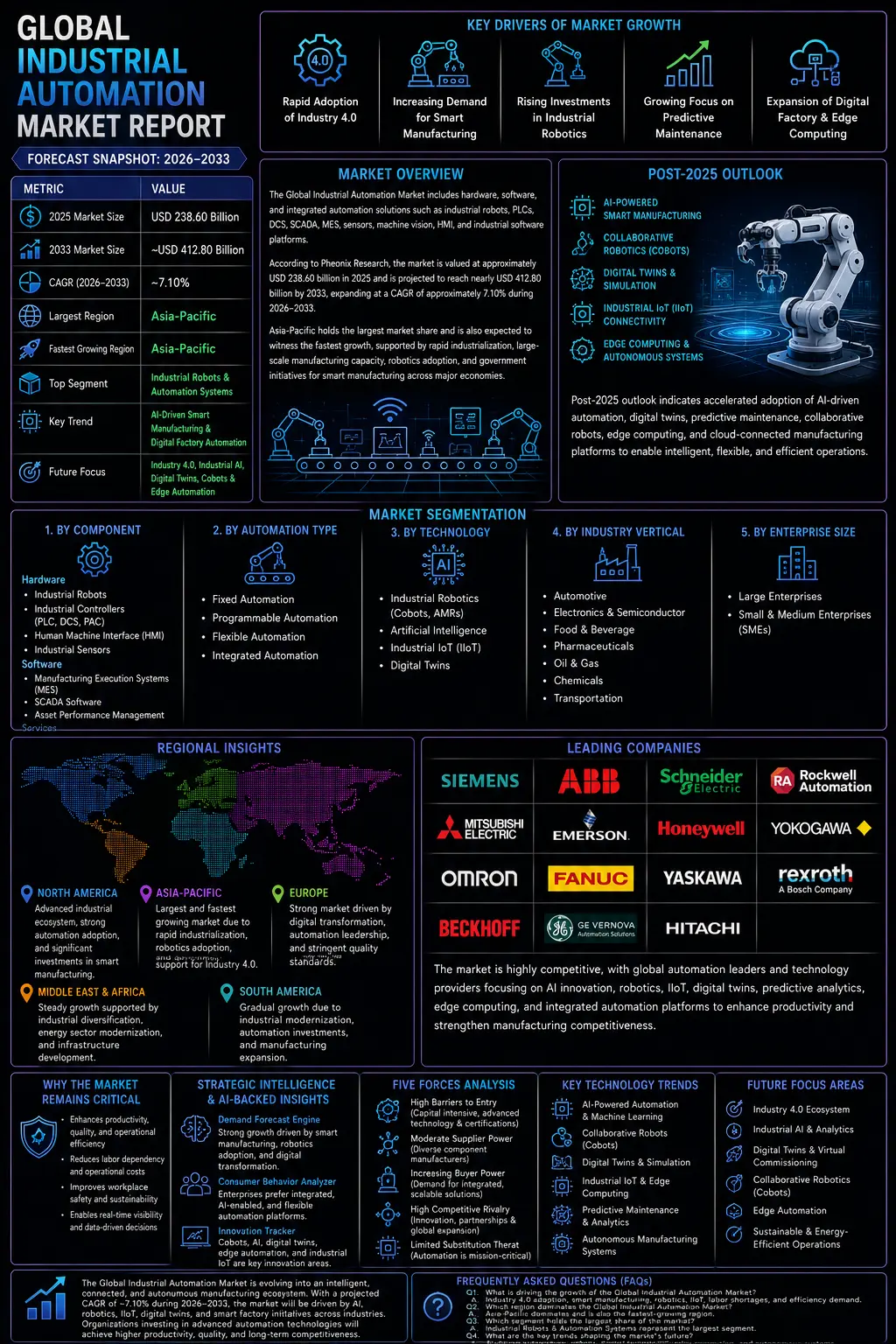

Global Industrial Automation Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

| 2025 Market Size | USD 238.60 Billion |

| 2033 Market Size | ~USD 412.80 Billion |

| CAGR (2026–2033) | ~7.10% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Industrial Robots & Automation Systems |

| Key Trend | AI-Driven Smart Manufacturing & Digital Factory Automation |

| Future Focus | Industry 4.0, Industrial AI, Digital Twins, Collaborative Robots (Cobots) & Edge Automation |

Global Industrial Automation Market Overview

The Global Industrial Automation Market comprises hardware, software, and integrated automation solutions designed to optimize manufacturing operations, industrial production, logistics, process industries, and critical infrastructure. The market includes industrial robots, programmable logic controllers (PLCs), distributed control systems (DCS), supervisory control and data acquisition (SCADA), manufacturing execution systems (MES), industrial sensors, machine vision, motion control systems, human-machine interfaces (HMIs), and industrial software platforms. Industrial automation has become the foundation of modern manufacturing as industries increasingly adopt smart factories, connected production systems, artificial intelligence, Industrial Internet of Things (IIoT), and advanced robotics to improve operational efficiency, product quality, workplace safety, and production flexibility. Automation technologies enable manufacturers to reduce labor dependency, minimize downtime, optimize energy consumption, and achieve real-time production visibility across industrial operations. According to Pheonix Research, the Global Industrial Automation Market is valued at approximately USD 238.60 billion in 2025 and is projected to reach nearly USD 412.80 billion by 2033, expanding at a CAGR of approximately 7.10%during 2026–2033. Asia-Pacific accounts for the largest market share owing to rapid industrialization, extensive manufacturing capacity, large-scale adoption of robotics, and government initiatives supporting smart manufacturing across China, Japan, South Korea, and India. The region is also expected to witness the fastest growth, driven by expanding electronics production, automotive manufacturing, semiconductor investments, and increasing deployment of Industry 4.0 technologies. The Post-2025 outlook indicates accelerated adoption of AI-powered industrial automation, collaborative robotics, digital twins, predictive maintenance, industrial edge computing, autonomous manufacturing systems, cloud-connected production environments, and intelligent factory management platforms.Global Industrial Automation Market

Key Drivers of Global Industrial Automation Market Growth

1. Rapid Adoption of Industry 4.0

Manufacturers worldwide are increasingly implementing Industry 4.0 technologies including Industrial IoT, artificial intelligence, digital twins, cloud computing, and connected production systems to enhance productivity, improve operational visibility, and enable intelligent manufacturing.2. Increasing Demand for Smart Manufacturing

Growing pressure to improve manufacturing efficiency, product quality, operational flexibility, and cost optimization is encouraging industries to deploy advanced industrial automation solutions across production facilities.3. Rising Investments in Industrial Robotics

Automotive, electronics, pharmaceuticals, food & beverage, logistics, and semiconductor industries continue to increase investments in industrial robots and collaborative robots to automate repetitive tasks, improve production speed, and address skilled labor shortages.4. Growing Focus on Predictive Maintenance

Manufacturers are increasingly utilizing AI-powered predictive maintenance, industrial analytics, machine learning, and real-time equipment monitoring to minimize unplanned downtime, improve equipment utilization, and extend asset lifecycle.5. Expansion of Digital Factory & Edge Computing

The integration of industrial edge computing, cloud-based manufacturing platforms, autonomous production systems, and real-time operational intelligence is transforming factory automation and enabling decentralized decision-making across manufacturing operations.Global Industrial Automation Market Segmentation

1. By Component

1.1 Hardware 1.1.1 Industrial Robots 1.1.1.1 Articulated Robots 1.1.1.2 SCARA Robots 1.1.1.3 Cartesian Robots 1.1.1.4 Delta Robots 1.1.2 Industrial Controllers 1.1.2.1 Programmable Logic Controllers (PLC) 1.1.2.2 Distributed Control Systems (DCS) 1.1.2.3 Programmable Automation Controllers (PAC) 1.1.3 Human Machine Interface (HMI) 1.1.3.1 Touchscreen HMI 1.1.3.2 Operator Panels 1.1.3.3 Industrial Displays 1.1.4 Industrial Sensors 1.1.4.1 Proximity Sensors 1.1.4.2 Pressure Sensors 1.1.4.3 Temperature Sensors 1.1.4.4 Vision Sensors1.2 Software

1.2.1 Manufacturing Execution Systems (MES) 1.2.1.1 Production Monitoring 1.2.1.2 Production Scheduling 1.2.2 SCADA Software 1.2.2.1 Process Monitoring 1.2.2.2 Remote Control 1.2.3 Asset Performance Management 1.2.3.1 Predictive Analytics 1.2.3.2 Condition Monitoring 1.3 Services 1.3.1 Professional Services 1.3.1.1 Consulting 1.3.1.2 System Integration 1.3.1.3 Installation 1.3.2 Managed Services 1.3.2.1 Maintenance 1.3.2.2 Remote Monitoring2. By Automation Type

2.1 Fixed Automation 2.1.1 Assembly Lines 2.1.1.1 High-Volume Manufacturing 2.1.1.2 Continuous Production 2.2 Programmable Automation 2.2.1 Batch Manufacturing 2.2.1.1 Flexible Production 2.2.1.2 Process Manufacturing 2.3 Flexible Automation 2.3.1 Smart Manufacturing 2.3.1.1 AI-Based Production 2.3.1.2 Adaptive Manufacturing 2.4 Integrated Automation 2.4.1 End-to-End Factory Automation 2.4.1.1 Enterprise Integration 2.4.1.2 Digital Factory Operations3. By Technology

3.1 Industrial Robotics 3.1.1 Collaborative Robots (Cobots) 3.1.1.1 Assembly 3.1.1.2 Packaging 3.1.1.3 Material Handling 3.1.2 Autonomous Mobile Robots (AMRs) 3.1.2.1 Warehouse Automation 3.1.2.2 Factory Logistics 3.2 Artificial Intelligence 3.2.1 Machine Learning 3.2.1.1 Predictive Maintenance 3.2.1.2 Process Optimization 3.2.2 Computer Vision 3.2.2.1 Quality Inspection 3.2.2.2 Defect Detection 3.3 Industrial Internet of Things (IIoT) 3.3.1 Connected Devices 3.3.1.1 Smart Sensors 3.3.1.2 Edge Gateways 3.4 Digital Twins 3.4.1 Equipment Digital Twins 3.4.1.1 Machine Simulation 3.4.1.2 Virtual Commissioning4. By Industry Vertical

4.1 Automotive 4.1.1 Vehicle Manufacturing 4.1.1.1 Passenger Vehicles 4.1.1.2 Commercial Vehicles 4.2 Electronics & Semiconductor 4.2.1 Semiconductor Manufacturing 4.2.1.1 Wafer Fabrication 4.2.1.2 Chip Packaging 4.3 Food & Beverage 4.3.1 Food Processing 4.3.1.1 Packaging 4.3.1.2 Quality Inspection 4.4 Pharmaceuticals 4.4.1 Drug Manufacturing 4.4.1.1 Packaging 4.4.1.2 Laboratory Automation 4.5 Oil & Gas 4.5.1 Refining 4.5.1.1 Pipeline Monitoring 4.5.1.2 Process Automation 4.6 Chemicals 4.6.1 Specialty Chemicals 4.6.1.1 Continuous Processing 4.6.1.2 Batch Processing5. By Enterprise Size

5.1 Large Enterprises 5.1.1 Global Manufacturing Companies 5.1.1.1 Multi-Plant Operations 5.1.1.2 Smart Factory Networks 5.2 Small & Medium Enterprises (SMEs) 5.2.1 Industrial SMEs 5.2.1.1 Component Manufacturers 5.2.1.2 Contract ManufacturersRegional Insights of Global Industrial Automation Market

North America

North America represents one of the most technologically advanced industrial automation markets, supported by widespread adoption of Industry 4.0, smart manufacturing, artificial intelligence, Industrial Internet of Things (IIoT), and digital factory initiatives. The United States leads regional growth owing to substantial investments in automotive manufacturing, aerospace, pharmaceuticals, logistics automation, semiconductor production, and warehouse robotics. Increasing labor shortages and the need for resilient supply chains continue to accelerate automation adoption across industries.Asia-Pacific – Largest & Fastest Growing Market

Asia-Pacific dominates the Global Industrial Automation Market and is projected to remain the fastest-growing region throughout the forecast period. China, Japan, South Korea, India, Taiwan, and Southeast Asian countries continue to expand manufacturing capacity through large-scale investments in industrial robotics, semiconductor fabrication, electronics production, electric vehicle manufacturing, and smart factories. Government initiatives such as "Made in China 2025," India's manufacturing modernization programs, Japan's Society 5.0 strategy, and South Korea's smart factory roadmap are significantly accelerating industrial automation deployment across the region.Europe

Europe maintains a strong market position driven by advanced manufacturing capabilities, industrial digitalization, sustainability initiatives, and stringent production quality standards. Germany remains the regional leader due to its highly automated automotive and machinery industries, while France, Italy, the United Kingdom, and the Nordic countries continue expanding investments in robotics, industrial software, energy-efficient manufacturing systems, and digital production technologies.Middle East & Africa

The Middle East & Africa market is experiencing steady growth supported by industrial diversification initiatives, smart manufacturing investments, energy sector modernization, and infrastructure development. Countries including the UAE, Saudi Arabia, Qatar, and South Africa are increasingly deploying industrial automation technologies to improve operational efficiency across manufacturing, petrochemicals, utilities, mining, and logistics sectors.South America

South America continues to witness gradual automation adoption driven by modernization of manufacturing facilities, food processing industries, mining operations, oil & gas production, and agricultural processing plants. Brazil, Argentina, Chile, and Colombia remain key contributors as industrial enterprises increasingly invest in automation solutions to improve productivity, reduce operational costs, and enhance competitiveness.Leading Companies in the Global Industrial Automation Market

- Siemens AG

- ABB Ltd.

- Schneider Electric SE

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- Honeywell International Inc.

- Yokogawa Electric Corporation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- Bosch Rexroth AG

- Beckhoff Automation GmbH & Co. KG

- General Electric (GE Vernova Automation Solutions)

- Hitachi, Ltd.

Why the Global Industrial Automation Market Remains Critical

- Smart manufacturing initiatives continue to transform global production systems through intelligent automation and connected operations.

- Rising labor shortages and increasing production costs encourage manufacturers to deploy robotics and automated production technologies.

- AI, Industrial IoT, digital twins, and predictive maintenance improve operational efficiency while minimizing downtime.

- Automation enhances workplace safety, product quality, production flexibility, and overall manufacturing competitiveness.

- Industrial automation supports sustainable manufacturing through optimized energy consumption, reduced waste generation, and improved resource utilization.

Strategic Intelligence and AI-Backed Insights – Global Industrial Automation Market

Pheonix Demand Forecast Engine identifies sustained market expansion driven by increasing smart factory investments, rapid deployment of industrial robotics, growing digital transformation initiatives, expanding semiconductor manufacturing, and widespread Industry 4.0 adoption across global manufacturing industries. The Consumer Behavior Analyzer highlights increasing enterprise preference for integrated automation ecosystems that combine robotics, AI-powered analytics, Industrial Internet of Things (IIoT), manufacturing execution systems (MES), predictive maintenance, cloud connectivity, and real-time operational intelligence to improve production efficiency and profitability. The Innovation Tracker emphasizes collaborative robots (cobots), autonomous mobile robots (AMRs), artificial intelligence, machine vision, edge computing, digital twins, Industrial IoT platforms, autonomous manufacturing, industrial metaverse applications, and low-code industrial automation software as the technologies expected to shape the next generation of intelligent manufacturing. Five Forces Analysis indicates high barriers to entry due to significant capital requirements, advanced engineering capabilities, industrial certifications, and extensive system integration expertise. Supplier power remains moderate because of diversified component manufacturers, while buyer power is increasing as industrial customers seek interoperable, scalable, and future-ready automation platforms. Competitive rivalry remains intense as leading vendors compete through AI innovation, robotics portfolios, software integration, strategic acquisitions, and comprehensive digital manufacturing ecosystems.Final Takeaway of Global Industrial Automation Market

The Global Industrial Automation Market is rapidly evolving into a highly intelligent, interconnected, and autonomous manufacturing ecosystem. The projected CAGR of approximately 7.10% during 2026–2033 reflects continued investments in smart manufacturing, industrial robotics, artificial intelligence, Industrial Internet of Things (IIoT), and digital transformation across virtually every major industrial sector. Future market growth will be driven by AI-enabled autonomous production systems, collaborative robotics, digital twins, edge computing, cloud-connected manufacturing platforms, predictive maintenance, industrial analytics, and intelligent process optimization. As manufacturers increasingly prioritize operational resilience, supply chain flexibility, sustainability, and workforce productivity, industrial automation will become an essential pillar of next-generation manufacturing strategies. Organizations that successfully integrate robotics, AI-powered decision-making, Industrial IoT, machine vision, cybersecurity, and digital factory technologies will be well positioned to achieve long-term competitive advantages through higher productivity, improved product quality, optimized operational costs, and greater manufacturing agility. At Pheonix Research, our advanced forecasting models deliver comprehensive Global Industrial Automation Market revenue forecasts, competitive benchmarking, regional opportunity analysis, and strategic intelligence—enabling automation vendors, manufacturers, industrial enterprises, investors, and technology providers to capitalize on the Post-2025 outlook with confidence and data-driven decision-making.Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Market Highlights

1.3 Market Size & Forecast (2026–2033)

1.4 Largest Regional Market Analysis

1.5 Fastest Growing Regional Market Analysis

1.6 Largest Segment Analysis

1.7 Competitive Landscape Snapshot

1.8 Future Market Outlook

2. Global Industrial Automation Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Industrial Automation Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Automation Architecture & Manufacturing Workflow Analysis

3.5 Smart Factory Infrastructure Overview

3.6 Industrial Automation Technology Landscape

3.6.1 Hardware

3.6.1.1 Industrial Robots

3.6.1.1.1 Industrial Controllers

3.6.1.1.1.1 Human Machine Interfaces (HMI)

3.6.1.1.1.2 Industrial Sensors

3.6.2 Software

3.6.2.1 Manufacturing Execution Systems (MES)

3.6.2.1.1 SCADA Software

3.6.2.1.1.1 Asset Performance Management

3.6.2.1.1.2 Industrial Analytics Platforms

3.6.3 Services

3.6.3.1 Professional Services

3.6.3.1.1 Managed Services

3.6.3.1.1.1 System Integration

3.6.3.1.1.2 Remote Monitoring & Maintenance

4. Regulatory Landscape

4.1 Industrial Safety & Automation Standards

4.2 Machine Safety Regulations

4.3 Industrial Communication & Interoperability Standards

4.4 Environmental & Energy Efficiency Regulations

4.5 Industrial Cybersecurity & Data Governance Standards

5. Market Trends & Innovation Outlook

5.1 AI-Driven Smart Manufacturing

5.2 Industry 4.0 Adoption

5.3 Digital Twins & Virtual Commissioning

5.4 Collaborative Robots (Cobots)

5.5 Industrial Internet of Things (IIoT)

5.6 Edge Computing & Edge Automation

5.7 Autonomous Mobile Robots (AMRs)

5.8 Cloud-Based Manufacturing Platforms

6. Global Industrial Automation Market Dynamics

6.1 Market Drivers

6.1.1 Rapid Adoption of Industry 4.0

6.1.2 Increasing Demand for Smart Manufacturing

6.1.3 Rising Investments in Industrial Robotics

6.1.4 Growing Focus on Predictive Maintenance

6.1.5 Expansion of Digital Factory & Edge Computing

6.2 Market Restraints

6.2.1 High Initial Capital Investment

6.2.2 Complex Integration with Legacy Systems

6.2.3 Shortage of Skilled Automation Professionals

6.2.4 High Maintenance & Upgrade Costs

6.3 Market Opportunities

6.3.1 AI-Powered Factory Automation

6.3.2 Collaborative Robotics (Cobots)

6.3.3 Smart Manufacturing in Emerging Economies

6.3.4 Industrial IoT Expansion

6.3.5 Cloud-Based Industrial Automation Platforms

6.4 Market Challenges

6.4.1 Industrial Cybersecurity Risks

6.4.2 Interoperability Between Automation Platforms

6.4.3 Supply Chain Disruptions for Automation Components

6.4.4 Workforce Upskilling & Change Management

7. Global Industrial Automation Market Size Analysis (USD Billion), 2026–2033

7.1 Revenue Forecast Analysis

7.2 CAGR Analysis

7.3 Investment Trend Analysis

7.4 Automation Adoption Analysis

7.5 Production Efficiency & ROI Assessment

8. Global Industrial Automation Market Segmentation Analysis

8.1 By Component

8.1.1 Hardware

8.1.2 Software

8.1.3 Services

8.2 By Automation Type

8.2.1 Fixed Automation

8.2.2 Programmable Automation

8.2.3 Flexible Automation

8.2.4 Integrated Automation

8.3 By Technology

8.3.1 Industrial Robotics

8.3.2 Artificial Intelligence

8.3.3 Industrial Internet of Things (IIoT)

8.3.4 Digital Twins

8.4 By Industry Vertical

8.4.1 Automotive

8.4.2 Electronics & Semiconductor

8.4.3 Food & Beverage

8.4.4 Pharmaceuticals

8.4.5 Oil & Gas

8.4.6 Chemicals

8.5 By Enterprise Size

8.5.1 Large Enterprises

8.5.2 Small & Medium Enterprises (SMEs)

9. Regional Market Analysis

9.1 Asia-Pacific

9.1.1 China

9.1.2 Japan

9.1.3 South Korea

9.1.4 India

9.1.5 Taiwan

9.1.6 Rest of Asia-Pacific

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 Germany

9.3.2 U.K.

9.3.3 France

9.3.4 Italy

9.3.5 Nordic Countries

9.3.6 Rest of Europe

9.4 Middle East & Africa

9.4.1 GCC Countries

9.4.2 South Africa

9.4.3 Rest of Middle East & Africa

9.5 South America

9.5.1 Brazil

9.5.2 Argentina

9.5.3 Rest of South America

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Intensity Overview

10.3 Strategic Developments

10.4 Product Innovation & Digital Factory Platforms

10.5 Partnerships, Acquisitions & Collaborations

10.6 Vendor Positioning Analysis

11. Company Profiles

11.1 Siemens AG

11.2 ABB Ltd.

11.3 Schneider Electric SE

11.4 Rockwell Automation, Inc.

11.5 Mitsubishi Electric Corporation

11.6 Emerson Electric Co.

11.7 Honeywell International Inc.

11.8 Yokogawa Electric Corporation

11.9 Omron Corporation

11.10 FANUC Corporation

11.11 Yaskawa Electric Corporation

11.12 Bosch Rexroth AG

11.13 Beckhoff Automation GmbH & Co. KG

11.14 GE Vernova Automation Solutions

11.15 Hitachi, Ltd.

12. Strategic Intelligence & Pheonix AI Insights

12.1 Pheonix Demand Forecast Engine

12.2 Consumer Behavior Analyzer

12.3 Innovation Tracker

12.4 Smart Factory Opportunity Dashboard

12.5 Automated Porter’s Five Forces Analysis

13. Future Outlook & Strategic Recommendations

13.1 Industry 4.0 Implementation Roadmap

13.2 AI-Driven Manufacturing Strategy

13.3 Digital Factory Transformation Framework

13.4 Industrial Edge & IIoT Deployment Strategy

13.5 Long-Term Market Outlook (2033+)

14. About Pheonix Market Research

15. Disclaimer

Competitive Landscape

Global Industrial Automation Market Competitive Intensity & Market Structure Overview

The Global Industrial Automation Market is highly competitive and characterized by the presence of industrial automation providers, robotics manufacturers, industrial software developers, control system suppliers, sensor manufacturers, industrial communication technology companies, and digital transformation solution providers. Competitive intensity is driven by the rapid adoption of Industry 4.0, Industrial Internet of Things (IIoT), artificial intelligence (AI), machine learning, digital twins, cloud manufacturing, edge computing, and advanced robotics across manufacturing industries.

Companies compete across multiple automation segments including industrial control systems (ICS), programmable logic controllers (PLCs), distributed control systems (DCS), supervisory control and data acquisition (SCADA), manufacturing execution systems (MES), industrial robotics, collaborative robots (cobots), industrial AI platforms, machine vision systems, industrial cybersecurity, and predictive maintenance solutions. Increasing demand for smart factories, autonomous manufacturing, operational efficiency, workforce optimization, and sustainable industrial operations is intensifying competition while accelerating technological innovation throughout the automation ecosystem.

The market structure is evolving toward integrated automation ecosystems combining industrial hardware, intelligent software, AI-powered analytics, cloud connectivity, industrial edge computing, digital twins, and cybersecurity into unified manufacturing platforms. Market participants are investing heavily in AI-enabled automation, industrial IoT infrastructure, robotics software, industrial cloud platforms, advanced sensing technologies, and strategic partnerships to strengthen market positioning while enabling manufacturers to achieve greater productivity, flexibility, and resilience.

Global Industrial Automation Market Competitive Intensity & Market Structure Current Scenario

Leading Global Industrial Automation Companies

Siemens AG: A global industrial technology leader providing industrial automation systems, digital factory solutions, PLCs, SCADA, digital twin platforms, industrial software, AI-powered manufacturing, and smart infrastructure technologies.

ABB Ltd.: A leading provider of industrial robotics, electrification, motion control, distributed control systems, AI-enabled automation platforms, collaborative robots, and intelligent manufacturing solutions.

Schneider Electric SE: A global automation and energy management company offering industrial control systems, EcoStruxure digital platforms, industrial software, smart manufacturing technologies, and industrial IoT solutions.

Rockwell Automation, Inc.: An industrial automation specialist delivering PLCs, industrial control systems, manufacturing execution systems, industrial AI, digital transformation solutions, and factory automation platforms.

Mitsubishi Electric Corporation: A global automation company providing factory automation equipment, PLCs, motion control systems, robotics, industrial software, and intelligent manufacturing technologies.

Emerson Electric Co.: A leading automation provider offering process automation systems, distributed control systems, industrial software, predictive maintenance, measurement technologies, and digital transformation solutions.

Honeywell International Inc.: A technology company delivering industrial automation, process control systems, industrial cybersecurity, smart manufacturing software, and connected industrial operations.

FANUC Corporation: A global robotics manufacturer specializing in industrial robots, CNC systems, factory automation, AI-enabled robotic solutions, and precision manufacturing technologies.

Yaskawa Electric Corporation: A leading supplier of industrial robots, servo systems, motion control technologies, intelligent automation platforms, and advanced manufacturing solutions.

Omron Corporation: An industrial automation company providing sensors, machine vision systems, PLCs, industrial safety systems, autonomous mobile robots, and smart factory automation technologies.

Key Competitive Intensity & Market Structure Drivers

Increasing adoption of Industry 4.0, smart factories, and digital manufacturing initiatives is intensifying competition among industrial automation providers across global manufacturing industries.

Growing deployment of industrial AI, Industrial Internet of Things (IIoT), machine vision, collaborative robots, digital twins, and predictive maintenance solutions is creating significant technological differentiation among market participants.

Rising demand for manufacturing efficiency, labor optimization, quality improvement, real-time production monitoring, and autonomous factory operations is strengthening competitive intensity while accelerating innovation in automation platforms.

Strategic collaborations among automation companies, robotics manufacturers, cloud service providers, semiconductor companies, AI software developers, industrial cybersecurity firms, and manufacturing enterprises are accelerating product innovation, expanding digital capabilities, and improving operational performance.

Continuous investment in industrial AI, cloud manufacturing platforms, industrial edge computing, robotics, industrial cybersecurity, machine vision, and integrated automation ecosystems is enabling companies to improve operational efficiency, customer value, and long-term competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Companies offering comprehensive industrial automation platforms, integrated hardware-software ecosystems, and AI-enabled manufacturing technologies are expected to maintain significant competitive advantages.

Investment in industrial AI, predictive analytics, digital twins, industrial IoT connectivity, collaborative robotics, and industrial cybersecurity is becoming increasingly important for sustaining long-term market leadership.

Organizations focusing on expanding intelligent automation capabilities, improving software interoperability, strengthening cloud-based manufacturing solutions, and enhancing production flexibility are likely to increase revenue growth and market share.

Strategic partnerships with manufacturing companies, cloud technology providers, semiconductor manufacturers, system integrators, industrial software developers, and research institutions are supporting innovation, global expansion, and next-generation automation development.

Businesses capable of combining technological innovation, industrial engineering expertise, software intelligence, operational scalability, cybersecurity, and integrated automation ecosystems will be best positioned to compete effectively in the evolving global industrial automation market.

Global Industrial Automation Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global industrial automation market is expected to become increasingly AI-driven, software-defined, and Industry 4.0-oriented as manufacturers accelerate investments in intelligent production systems and digital transformation.

Future competition will be shaped by industrial artificial intelligence, collaborative robotics (cobots), autonomous manufacturing, Industrial IoT, digital twins, cloud manufacturing, edge computing, machine vision, industrial cybersecurity, and predictive maintenance technologies.

Market participants are expected to increase investments in intelligent automation software, robotics platforms, AI-powered production optimization, industrial cloud infrastructure, advanced sensing technologies, and connected manufacturing ecosystems to strengthen competitive positioning.

Over the forecast period, companies that successfully combine artificial intelligence, industrial automation expertise, robotics engineering, software innovation, digital manufacturing platforms, and scalable end-to-end automation solutions will be best positioned to lead the evolving global industrial automation market.

Value Chain

Global Industrial Automation Market Value Chain & Supply Chain Evolution Overview

The Global Industrial Automation Market operates through a highly integrated industrial technology value chain comprising component manufacturing, automation hardware production, industrial software development, system integration, quality assurance, distribution, installation & commissioning, industrial operations, predictive maintenance, and lifecycle support. The ecosystem includes automation equipment manufacturers, robotics companies, industrial software developers, semiconductor suppliers, sensor manufacturers, system integrators, cloud service providers, OEMs, industrial enterprises, distributors, and maintenance service providers working collaboratively to enable intelligent, connected, and autonomous manufacturing environments.

The market is being driven by rapid Industry 4.0 adoption, increasing deployment of Industrial Internet of Things (IIoT), artificial intelligence, robotics, digital twins, cloud manufacturing, and predictive maintenance solutions. Organizations are investing heavily in smart factories, AI-powered industrial platforms, industrial cybersecurity, edge computing, and autonomous production systems to improve productivity, operational efficiency, flexibility, and sustainability.

The integration of artificial intelligence, industrial robotics, machine vision, cloud computing, digital twins, advanced sensors, industrial communication networks, edge computing, and predictive analytics has significantly strengthened the industrial automation value chain. Companies are expanding strategic collaborations among automation vendors, software providers, semiconductor manufacturers, system integrators, industrial enterprises, and cloud technology companies to accelerate digital transformation across manufacturing industries.

Advancements in collaborative robotics, AI-enabled automation platforms, industrial edge intelligence, digital manufacturing ecosystems, autonomous production systems, industrial cybersecurity, and smart factory technologies are transforming the supply chain while improving production efficiency, operational reliability, manufacturing scalability, and overall industrial competitiveness across the global automation ecosystem.

Global Industrial Automation Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

Component & Technology Development:

Industrial electronics, semiconductors, sensors, PLC components, industrial communication devices, motion control technologies, robotics engineering, AI algorithms, machine vision technologies, embedded systems, and industrial software development.

Automation Equipment Manufacturing:

Industrial robots, PLCs, DCS, SCADA systems, HMI panels, industrial sensors, servo motors, drives, machine vision systems, safety systems, industrial controllers, and automation hardware manufacturing.

Software Development & System Integration:

Manufacturing execution systems (MES), industrial AI platforms, predictive maintenance software, industrial analytics, digital twins, cloud manufacturing platforms, cybersecurity software, production planning systems, and enterprise integration.

Quality Assurance & Regulatory Compliance:

Industrial safety validation, functional safety testing, cybersecurity certification, product quality assurance, ISO compliance, energy efficiency validation, factory acceptance testing, and regulatory certification.

Supply Chain, Distribution & Deployment:

Global component sourcing, warehouse management, industrial equipment distribution, OEM supply, channel partner networks, logistics coordination, inventory management, and project delivery.

Installation, Commissioning & Industrial Operations:

System installation, factory automation deployment, equipment commissioning, industrial networking, production optimization, operator training, technical consulting, and operational support.

Lifecycle Services & Predictive Maintenance:

Remote monitoring, preventive maintenance, predictive analytics, equipment upgrades, spare parts management, industrial cybersecurity services, technical support, and asset lifecycle optimization.

End User Applications:

Deployment across automotive manufacturing, electronics & semiconductors, pharmaceuticals, food & beverage, chemicals, oil & gas, mining, utilities, logistics & warehousing, aerospace, renewable energy, and consumer goods manufacturing.

Company-to-Stage Mapping

Component & Technology Development:

Siemens AG, ABB Ltd., Schneider Electric SE, Mitsubishi Electric Corporation, Omron Corporation, Keyence Corporation, Beckhoff Automation GmbH & Co. KG, semiconductor suppliers, industrial electronics manufacturers, and AI software developers.

Automation Equipment Manufacturing:

ABB Ltd., FANUC Corporation, Yaskawa Electric Corporation, KUKA AG, Rockwell Automation, Siemens AG, Bosch Rexroth AG, Emerson Electric Co., Honeywell International Inc., Delta Electronics, and Yokogawa Electric Corporation.

Software Development & System Integration:

Siemens AG, Schneider Electric SE, Rockwell Automation, Emerson Electric Co., Honeywell International Inc., Advantech Co., Ltd., industrial software providers, cloud service providers, and industrial system integrators.

Supply Chain, Distribution & Deployment:

Industrial equipment distributors, OEM partners, automation solution providers, logistics companies, warehouse operators, regional distribution partners, and industrial channel networks.

Installation, Commissioning & Industrial Operations:

System integrators, automation engineering firms, industrial contractors, OEM service providers, manufacturing consultants, technical service organizations, and industrial enterprises.

Lifecycle Services & Predictive Maintenance:

Siemens AG, ABB Ltd., Schneider Electric SE, Rockwell Automation, Emerson Electric Co., Honeywell International Inc., industrial maintenance providers, remote monitoring companies, and predictive analytics solution providers.

Quality Assurance & Regulatory Compliance:

Industrial certification agencies, functional safety organizations, ISO certification bodies, industrial cybersecurity firms, quality assurance laboratories, and regulatory compliance organizations.

End User Applications:

Automotive manufacturers, electronics companies, pharmaceutical manufacturers, food & beverage processors, chemical companies, oil & gas operators, mining companies, utilities, logistics providers, aerospace manufacturers, and consumer goods producers.

Key Value Chain & Supply Chain Evolution Signals in Global Industrial Automation Market

Expansion of Industry 4.0 & Smart Factory Adoption

Manufacturers are increasingly integrating AI, IIoT, robotics, cloud manufacturing, and digital twins to enable intelligent and autonomous production systems.

Growing Deployment of Industrial AI

Artificial intelligence is improving predictive maintenance, production scheduling, quality inspection, anomaly detection, and autonomous process optimization across industrial facilities.

Increasing Adoption of Collaborative Robotics

Collaborative robots (cobots) are enabling flexible, safe, and cost-effective automation, particularly among small and medium-sized manufacturers.

Advancement of Digital Twin & Edge Computing Technologies

Digital twins and industrial edge computing are improving real-time production monitoring, simulation, predictive analytics, and operational efficiency.

Strengthening Industrial Cybersecurity

Organizations are investing in industrial network security, endpoint protection, identity management, and secure communication protocols to safeguard connected manufacturing systems.

Expansion of Integrated Automation Ecosystems

Automation vendors are developing unified platforms that combine hardware, software, AI, cloud services, and industrial networking into comprehensive smart manufacturing solutions.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Intelligent Automation Technologies

Advanced robotics, industrial AI, digital twins, IIoT platforms, and edge computing strengthen manufacturing flexibility, productivity, and operational excellence.

Expansion of Smart Manufacturing Infrastructure

Modern factories equipped with connected production systems, intelligent controllers, cloud platforms, and digital analytics improve scalability and production efficiency.

Strengthening Supply Chain Resilience

Digital supply chain management, inventory optimization, industrial connectivity, and real-time asset visibility improve operational continuity and manufacturing resilience.

Optimization of Industrial Performance

Predictive maintenance, AI-powered quality control, intelligent scheduling, and autonomous production systems reduce downtime while maximizing equipment utilization.

Enhancement of Regulatory Compliance & Safety

Industrial safety standards, cybersecurity compliance, functional safety validation, and energy efficiency programs strengthen manufacturing reliability and regulatory readiness.

Leveraging AI-Driven Manufacturing Innovation

Artificial intelligence, machine learning, industrial analytics, and predictive decision support accelerate innovation while improving production quality and long-term competitiveness.

Global Industrial Automation Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the industrial automation value chain is expected to become increasingly intelligent, autonomous, software-defined, and digitally connected. Continued advancements in industrial AI, collaborative robotics, IIoT, digital twins, cloud manufacturing, industrial edge computing, and predictive analytics will further improve manufacturing productivity, operational efficiency, flexibility, sustainability, and industrial resilience.

Key Future Developments Include:

- Expansion of AI-powered smart factory and autonomous manufacturing platforms.

- Greater integration of Industrial IoT, digital twins, edge computing, and cloud manufacturing ecosystems.

- Increasing adoption of collaborative robots, autonomous mobile robots (AMRs), and intelligent machine vision systems.

- Broader deployment of predictive maintenance, industrial analytics, and real-time operational intelligence platforms.

- Growing investment in industrial cybersecurity, sustainable manufacturing technologies, and energy-efficient automation systems.

- Strengthening collaborations among automation vendors, robotics manufacturers, industrial software providers, semiconductor companies, cloud technology firms, OEMs, and manufacturing enterprises.

As the market evolves, competitive advantage will increasingly depend on AI-enabled automation, integrated industrial software, smart manufacturing ecosystems, industrial cybersecurity, scalable automation platforms, and end-to-end digital transformation capabilities.

Organizations that successfully integrate robotics, artificial intelligence, Industrial IoT, digital twins, cloud manufacturing, predictive analytics, and advanced automation technologies will be well positioned to achieve long-term leadership in the Global Industrial Automation Market.

Investment Activity

Investment Activity in the Global Industrial Automation Market

Investment activity in the Global Industrial Automation Market is accelerating as manufacturers, industrial technology providers, automation vendors, robotics companies, semiconductor manufacturers, and governments increase capital deployment toward smart factories, Industry 4.0 initiatives, industrial artificial intelligence (AI), Industrial Internet of Things (IIoT), and autonomous manufacturing systems. Growing pressure to improve productivity, address labor shortages, enhance operational efficiency, and strengthen supply chain resilience is driving significant investments across the industrial automation ecosystem.

Leading automation companies are investing heavily in AI-powered manufacturing platforms, collaborative robotics (cobots), digital twin technologies, industrial edge computing, cloud-based manufacturing execution systems (MES), and machine vision solutions to enable intelligent and data-driven production environments. These investments are improving production flexibility, predictive maintenance capabilities, quality control, and real-time operational decision-making.

Industrial manufacturers are also allocating substantial capital toward factory modernization, automated material handling systems, advanced motion control technologies, programmable logic controllers (PLCs), distributed control systems (DCS), supervisory control and data acquisition (SCADA) platforms, and integrated industrial cybersecurity solutions. The growing deployment of 5G-enabled industrial networks and connected production infrastructure is further accelerating investment in digital manufacturing capabilities.

Strategic partnerships, mergers, and acquisitions among automation vendors, robotics manufacturers, cloud service providers, semiconductor companies, AI software developers, and industrial system integrators are strengthening technology portfolios and expanding end-to-end automation solutions. Investment is also increasing in industrial software platforms that integrate AI analytics, predictive maintenance, digital twins, production planning, and asset lifecycle management into unified manufacturing ecosystems.

Governments worldwide continue supporting industrial automation through smart manufacturing initiatives, semiconductor investment programs, digital transformation policies, and advanced manufacturing incentives. These public-sector investments are encouraging enterprises to adopt next-generation automation technologies while improving global manufacturing competitiveness and sustainability.

Key Investment Trends

- Rising investment in Industry 4.0 infrastructure, AI-powered automation, and smart factory transformation.

- Increasing funding for industrial robotics, collaborative robots (cobots), autonomous mobile robots (AMRs), and machine vision systems.

- Expansion of investment in Industrial Internet of Things (IIoT), industrial edge computing, cloud manufacturing, and digital twin platforms.

- Growing capital allocation toward predictive maintenance, industrial AI software, manufacturing execution systems (MES), and advanced analytics.

- Higher investment in industrial cybersecurity, secure industrial networking, and OT/IT convergence solutions.

- Increasing strategic collaborations among automation vendors, semiconductor manufacturers, AI companies, cloud providers, and industrial system integrators.

- Continued investment in energy-efficient manufacturing technologies, sustainable automation systems, and intelligent resource optimization platforms.

Strategic Investment Outlook

Investment activity is expected to remain robust throughout the forecast period as manufacturers continue accelerating digital transformation and intelligent automation initiatives. Future capital deployment will increasingly focus on AI-driven production optimization, autonomous manufacturing, industrial edge AI, digital twins, industrial cybersecurity, collaborative robotics, and fully connected smart factory ecosystems.

Companies investing in integrated automation platforms, scalable industrial software, intelligent robotics, IIoT infrastructure, and sustainable manufacturing technologies are expected to strengthen their competitive position and capitalize on the long-term growth opportunities emerging across the Global Industrial Automation Market.

Technology & Innovation

Global Industrial Automation Market Technology & Innovation Landscape Overview

The Global Industrial Automation Market is experiencing rapid technological evolution driven by the convergence of Artificial Intelligence (AI), Industrial Internet of Things (IIoT), digital twins, industrial robotics, edge computing, cloud manufacturing, and advanced analytics. Manufacturers are increasingly transforming conventional production facilities into intelligent, connected, and autonomous smart factories capable of real-time decision-making, predictive maintenance, and self-optimizing operations. These innovations are improving productivity, operational flexibility, product quality, and resource efficiency across multiple industries.

Technology innovation is reshaping every stage of the manufacturing value chain, from production planning and process automation to quality inspection, asset management, and supply chain integration. AI-powered robotics, machine vision, collaborative robots (cobots), autonomous mobile robots (AMRs), industrial cybersecurity platforms, and cloud-native manufacturing execution systems (MES) are enabling manufacturers to reduce downtime, improve workforce safety, and accelerate digital transformation.

The growing adoption of Industry 4.0 initiatives, software-defined manufacturing, predictive analytics, and connected industrial ecosystems continues to drive innovation across global industrial automation markets.

Global Industrial Automation Market Technology & Innovation Landscape Current Scenario

The current industrial automation landscape is characterized by widespread deployment of AI-enabled production systems, IIoT-connected equipment, industrial edge computing, cloud-based automation platforms, and digital twin technologies. Manufacturers are increasingly integrating operational technology (OT) with information technology (IT) to enable real-time monitoring, autonomous process control, predictive maintenance, and enterprise-wide production optimization.

Industrial AI platforms are being deployed for predictive maintenance, anomaly detection, production scheduling, intelligent quality inspection, and process optimization. Collaborative robots and autonomous mobile robots are expanding automation beyond traditional high-volume manufacturing by enabling flexible, human-machine collaboration across assembly, logistics, packaging, and warehouse operations.

Machine vision systems, advanced industrial sensors, industrial 5G connectivity, cybersecurity solutions, and cloud-based manufacturing platforms are further improving production visibility, operational resilience, and intelligent decision-making while supporting scalable smart factory deployment.

Key Technology & Innovation Landscape Trends in the Global Industrial Automation Market

- AI-powered manufacturing platforms are enabling predictive maintenance, autonomous production optimization, intelligent scheduling, and real-time quality control.

- Industrial Internet of Things (IIoT) ecosystems are providing continuous monitoring of machines, production assets, and manufacturing processes through connected sensors and industrial gateways.

- Digital twin technology is allowing manufacturers to simulate production systems, optimize factory performance, and improve asset lifecycle management before physical implementation.

- Collaborative robots (Cobots), autonomous mobile robots (AMRs), and automated guided vehicles (AGVs) are improving production flexibility, workplace safety, and material handling efficiency.

- Machine vision systems powered by AI are enhancing automated inspection, defect detection, robot guidance, and precision manufacturing.

- Edge computing is enabling low-latency industrial analytics, local AI processing, and real-time operational decision-making without dependence on centralized cloud infrastructure.

- Cloud manufacturing platforms and Manufacturing Execution Systems (MES) are improving production planning, enterprise integration, and remote factory management.

- Industrial cybersecurity technologies, including zero-trust architectures, endpoint protection, and threat detection systems, are strengthening protection for connected manufacturing environments.

- Advanced analytics and predictive maintenance software are reducing equipment failures, minimizing unplanned downtime, and improving overall equipment effectiveness (OEE).

- Sustainable automation technologies focused on energy optimization, carbon reduction, intelligent resource management, and circular manufacturing are becoming strategic innovation priorities.

Strategic Implications of Technology & Innovation in the Global Industrial Automation Market

Continued investment in AI, industrial robotics, IIoT, digital twins, and intelligent automation platforms has become essential for manufacturers seeking higher productivity, operational resilience, and long-term competitiveness.

The convergence of industrial software, cloud computing, edge intelligence, and advanced analytics is enabling manufacturers to create fully connected production ecosystems that support autonomous decision-making, flexible manufacturing, and continuous process optimization.

Industrial automation vendors investing in interoperable platforms, AI-driven production management, cybersecurity, and cloud-native manufacturing solutions are expected to strengthen market leadership as smart factory adoption accelerates worldwide.

Strategic collaboration among automation companies, robotics manufacturers, semiconductor providers, industrial software developers, and cloud service providers is accelerating innovation while expanding end-to-end industrial automation ecosystems.

Growing investment in intelligent robotics, digital factory platforms, predictive maintenance, industrial AI, and autonomous manufacturing technologies is expected to create significant opportunities across automotive, electronics, pharmaceuticals, food processing, logistics, and energy industries.

Companies capable of integrating AI, IIoT, robotics, digital twins, cloud manufacturing, and industrial cybersecurity into unified automation platforms will be better positioned to support next-generation manufacturing transformation.

Global Industrial Automation Market Technology & Innovation Landscape Forward Outlook

Future innovation within the Global Industrial Automation Market will increasingly focus on autonomous manufacturing, AI-driven industrial decision-making, software-defined factories, digital twin ecosystems, industrial metaverse applications, and next-generation human-machine collaboration. The continued expansion of industrial 5G, edge AI, cloud-native automation, and intelligent robotics will further accelerate smart factory deployment across global manufacturing industries.

Emerging technologies such as generative AI for industrial engineering, self-learning production systems, quantum-assisted optimization, advanced industrial digital twins, and fully autonomous production environments are expected to redefine manufacturing efficiency over the coming decade. As industries prioritize productivity, sustainability, resilience, and digital transformation, technology-driven automation will remain the primary catalyst shaping the future of global industrial manufacturing.

Market Risk

Global Industrial Automation Market Risk & Disruption Analysis

The Global Industrial Automation Market operates within a moderate-to-high risk environment characterized by rapid technological evolution, cybersecurity threats, semiconductor supply volatility, workforce transformation, and increasingly stringent industrial regulations. While Industry 4.0 adoption, smart factory investments, industrial AI, robotics, and digital manufacturing continue to accelerate market expansion, automation vendors and industrial manufacturers must continuously adapt to evolving technological, operational, and geopolitical disruptions. The market is rapidly transitioning from traditional programmable automation toward AI-powered autonomous manufacturing, Industrial Internet of Things (IIoT), digital twins, cloud manufacturing, edge computing, collaborative robotics (cobots), and predictive analytics. These innovations are transforming industrial production while simultaneously increasing complexity in cybersecurity, interoperability, and digital infrastructure management. At the same time, global semiconductor shortages, supply-chain disruptions, increasing cyberattacks on operational technology (OT), rising implementation costs, skilled labor shortages, and stricter industrial safety and sustainability regulations are reshaping automation investment strategies worldwide.

Global Industrial Automation Market Current Risk Environment

The industrial automation industry is currently navigating a dynamic operating environment where technology adoption is accelerating alongside new categories of operational and strategic risks. One of the most significant risks is industrial cybersecurity. Increasing connectivity between operational technology (OT) and information technology (IT), cloud platforms, IIoT devices, and remote industrial operations has expanded the attack surface for ransomware, malware, and critical infrastructure cyber threats. Another major challenge is global semiconductor and electronic component supply volatility. Industrial controllers, sensors, robotics, drives, and automation hardware remain highly dependent on stable semiconductor availability, making supply disruptions a key risk for manufacturers and automation vendors. The market also faces rapid technological obsolescence, requiring continuous investment in AI software, robotics, digital twins, industrial edge computing, machine vision, and cloud-native automation platforms to remain competitive. In addition, skilled workforce shortages continue affecting automation deployment, programming, maintenance, and systems integration, particularly as advanced automation technologies become more sophisticated. Rising geopolitical tensions, trade restrictions, inflationary pressures, energy price fluctuations, and industrial decarbonization initiatives are further increasing uncertainty across global manufacturing operations.

Key Market Risk & Disruption Signals in Global Industrial Automation Market

1. Industrial Cybersecurity Threats

Growing connectivity across factories, IIoT devices, cloud platforms, and operational networks is increasing exposure to ransomware, data breaches, industrial espionage, and production disruptions.

2. Semiconductor & Electronic Component Supply Risks

Supply shortages of semiconductors, industrial processors, sensors, and electronic components continue impacting automation equipment manufacturing and deployment timelines.

3. AI & Autonomous Manufacturing Disruption

Artificial intelligence, machine learning, autonomous robotics, and self-optimizing production systems are fundamentally transforming traditional industrial automation architectures.

4. Workforce Transformation & Skills Gap

Shortages of automation engineers, robotics specialists, AI professionals, and industrial cybersecurity experts continue limiting implementation capacity across many industries.

5. Industrial Safety & Regulatory Compliance

Functional safety regulations, machine safety standards, cybersecurity compliance, environmental regulations, and energy efficiency requirements continue influencing automation system design and deployment.

6. Industrial IoT & Digital Infrastructure Complexity

Expanding adoption of connected factories, cloud manufacturing, edge computing, and digital twins increases integration complexity and operational dependency on digital ecosystems.

7. Supply Chain & Geopolitical Disruptions

Global trade uncertainty, geopolitical conflicts, export controls, logistics bottlenecks, and raw material price volatility continue affecting automation equipment production and industrial investments.

8. Sustainability & Energy Transition Requirements

Growing emphasis on carbon reduction, energy-efficient manufacturing, ESG compliance, and sustainable industrial operations is driving investment toward next-generation automation technologies.

Strategic Implications of Market Risk & Disruption in Global Industrial Automation Market

The evolving industrial automation landscape requires manufacturers and automation vendors to prioritize digital resilience, cybersecurity, operational flexibility, and continuous innovation. One of the most important strategic priorities is investment in AI-powered automation platforms, predictive maintenance software, industrial cybersecurity solutions, cloud-native manufacturing systems, digital twins, and edge computing infrastructure to improve production efficiency and operational resilience. Automation providers must strengthen OT cybersecurity capabilities, industrial AI expertise, semiconductor supply resilience, software interoperability, and lifecycle support services to effectively address evolving customer requirements. Strategic collaboration among automation vendors, semiconductor manufacturers, industrial software developers, robotics companies, cloud providers, and system integrators is becoming increasingly important to accelerate innovation and reduce deployment complexity. The convergence of AI, IIoT, robotics, machine vision, cloud computing, edge analytics, and advanced industrial software is reshaping competitive dynamics. Companies capable of delivering integrated, scalable, secure, and intelligent automation ecosystems are expected to strengthen long-term market leadership. Future competitive differentiation will increasingly depend on AI-enabled production optimization, cybersecurity readiness, digital manufacturing platforms, predictive analytics, flexible automation architectures, and sustainability-focused industrial solutions.

Global Industrial Automation Market Risk & Disruption Forward Outlook

Looking ahead to 2026-2033, the Global Industrial Automation Market is expected to undergo continuous transformation as intelligent manufacturing technologies become central to industrial competitiveness.

1. Expansion of AI-Driven Manufacturing

Artificial intelligence will increasingly automate production planning, quality inspection, predictive maintenance, scheduling, and autonomous decision-making.

2. Growth of Smart Factory Ecosystems

Fully connected factories integrating IIoT, robotics, digital twins, cloud platforms, and real-time analytics will become the standard across advanced manufacturing.

3. Increasing Industrial Cybersecurity Investments

Manufacturers will significantly expand investment in OT security, zero-trust architectures, endpoint protection, and industrial threat monitoring.

4. Wider Adoption of Collaborative Robotics (Cobots)

Cobots will continue expanding across SMEs and flexible production environments due to improved safety, affordability, and ease of deployment.

5. Expansion of Digital Twin Technology

Virtual factory simulation, predictive asset management, process optimization, and equipment lifecycle management will become core industrial capabilities.

6. Greater Edge Computing Deployment

Industrial edge computing will support real-time analytics, low-latency automation, autonomous operations, and AI processing closer to production assets.

7. Stronger Focus on Sustainable Manufacturing

Automation technologies supporting energy optimization, carbon reduction, circular manufacturing, and resource efficiency will become major investment priorities.

8. Integration of Industrial AI with Human Expertise

Future production environments will increasingly combine autonomous AI systems with human decision-making, enabling safer, more flexible, and highly adaptive manufacturing operations. In conclusion, the Global Industrial Automation Market represents a highly innovative, digitally transforming, and strategically critical industrial ecosystem, where artificial intelligence, connected manufacturing, cybersecurity, digital engineering, and sustainability initiatives will define long-term competitive success.

Regulatory Landscape

Global Industrial Automation Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a fundamental role in shaping the Global Industrial Automation Market by ensuring industrial safety, operational reliability, cybersecurity, environmental sustainability, and manufacturing efficiency. Industrial automation solutions operate within a comprehensive framework of international machinery safety standards, functional safety regulations, industrial cybersecurity requirements, electrical equipment standards, and energy efficiency policies that govern the design, deployment, and operation of automated manufacturing systems. The market is primarily influenced by industrial safety standards such as IEC 61508, IEC 62061, ISO 13849, IEC 62443 industrial cybersecurity standards, machinery safety directives, occupational health and safety regulations, and national smart manufacturing initiatives. In addition, evolving ESG policies, carbon reduction programs, digital manufacturing frameworks, and Industry 4.0 strategies are accelerating the adoption of intelligent automation across global manufacturing industries.

Global Industrial Automation Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape emphasizes workplace safety, machine reliability, industrial cybersecurity, interoperability, energy efficiency, and digital manufacturing resilience. Manufacturers and automation solution providers must comply with machinery safety regulations, electrical equipment certifications, cybersecurity requirements, and industrial communication standards while ensuring operational continuity across connected production environments. Governments worldwide are actively promoting industrial modernization through Industry 4.0 programs, smart factory initiatives, digital transformation incentives, and advanced manufacturing policies. Simultaneously, stricter environmental regulations and sustainability targets are encouraging industries to deploy energy-efficient automation systems capable of reducing emissions, optimizing resource utilization, and improving production efficiency. Regulators are also strengthening cybersecurity requirements for industrial control systems (ICS), SCADA platforms, Industrial IoT (IIoT) networks, and connected manufacturing environments to enhance protection against evolving cyber threats.

Key Regulatory & Policy Environment Signals in the Global Industrial Automation Market

1. Industrial Safety & Functional Safety Standards

Compliance with IEC 61508, ISO 13849, IEC 62061, machinery safety regulations, and workplace safety standards remains essential for automation equipment deployment.

2. Industrial Cybersecurity Regulations

Growing adoption of IEC 62443, industrial network security frameworks, and cybersecurity compliance is strengthening protection for connected manufacturing systems.

3. Industry 4.0 & Smart Manufacturing Policies

Government-led smart manufacturing initiatives, digital transformation programs, and advanced manufacturing incentives continue accelerating automation investments.

4. Energy Efficiency & Sustainability Regulations

Carbon reduction targets, industrial energy efficiency standards, and ESG initiatives are encouraging the deployment of sustainable automation technologies.

5. Industrial Communication & Interoperability Standards

Standardized industrial communication protocols and interoperability frameworks support seamless integration of automation equipment across smart factory ecosystems.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging automation vendors to strengthen industrial cybersecurity capabilities, improve functional safety, enhance energy efficiency, and develop interoperable automation platforms. Companies are investing in AI-powered manufacturing systems, Industrial IoT platforms, digital twins, predictive maintenance technologies, and secure industrial communication networks to maintain regulatory compliance while improving operational performance. Manufacturers capable of delivering compliant, secure, energy-efficient, and standards-based automation solutions are expected to strengthen their competitive position and support the long-term transition toward intelligent manufacturing ecosystems.

Global Industrial Automation Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, regulatory frameworks are expected to place greater emphasis on AI governance, industrial cybersecurity resilience, autonomous manufacturing safety, digital factory interoperability, and sustainable industrial operations. Governments are likely to expand smart manufacturing initiatives, strengthen cyber resilience requirements for critical industrial infrastructure, and introduce more comprehensive standards supporting intelligent automation and connected production systems. Future regulatory developments are also expected to encourage greater harmonization of global industrial safety standards, wider adoption of secure Industry 4.0 technologies, and accelerated deployment of energy-efficient smart factories, creating a more resilient, digitally connected, and sustainable industrial automation ecosystem. Regulatory Complexity Level – High Approval Pathway Structure – compliance_driven