Global Autonomous & Future Mobility Tyres Market size,share & forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

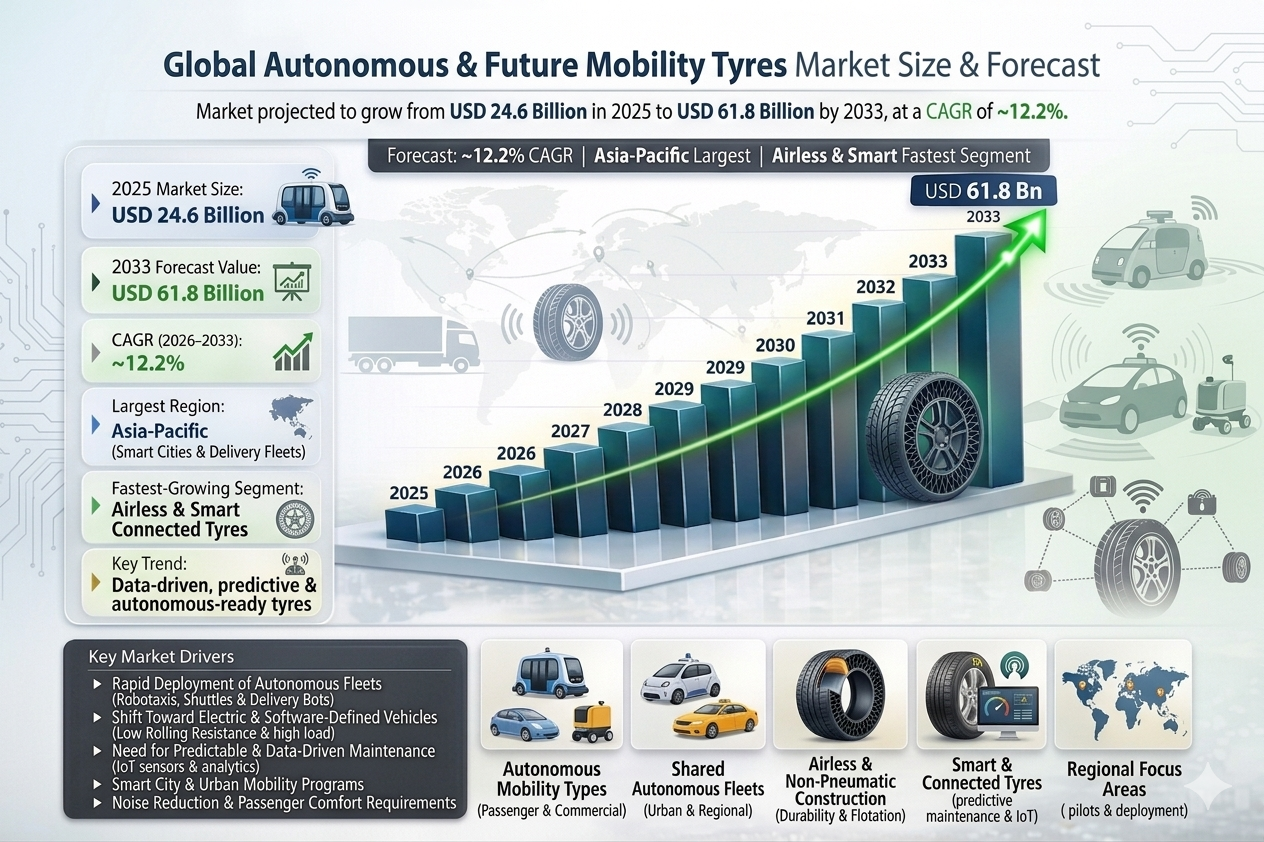

| 2025 Market Size | USD 24.6 Billion |

| 2033 Market Size | USD 61.8 Billion |

| CAGR (2026???2033) | ~12.2% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Segment | Airless & smart connected tyres |

| Key Trend | Data-driven, predictive & autonomous-ready tyres |

Global Autonomous & Future Mobility Tyres Market Overview

The Global Autonomous & Future Mobility Tyres Market is all about tyres built for self-driving cars, robotaxis, autonomous shuttles, delivery bots, and next-gen electric rides . These tyres go beyond grip and toughness???they???re made for nonstop use, super low noise, and even help sensors work better. Plus, they???re designed for predictive maintenance and digital connectivity, so they can ???talk??? to the vehicle and warn about wear or issues . As autonomous mobility grows, these smart tyres become a key part of the whole system.

Tyres are no longer just rubber???they???re turning into smart, data-generating parts of a vehicle???s brain . As cars shift from human drivers to software control, tyres need to keep up with longer operating hours and super-precise sensor systems. They have to deliver consistent performance, predictable wear, and real-time health updates to keep everything running smoothly . It???s like the tyre???s got a voice now, telling the car when it???s tired or needs attention.

The Global Autonomous & Future Mobility Tyres Market includes tyres supplied to autonomous vehicle OEMs, robotaxi manufacturers, smart city mobility platforms, and fleet operators, as well as replacement tyres for high-utilization autonomous fleets. With autonomous mobility increasingly tied to electric powertrains, these tyres are also optimized for higher vehicle weight, lower rolling resistance, and ultra-low acoustic output.

According to the Pheonix Demand Forecast Engine, the Global Autonomous & Future Mobility Tyres Market size is estimated at USD 24.6 billion in 2025 and is projected to reach USD 61.8 billion by 2033, expanding at a CAGR of ~12.2% during the forecast period (2026???2033).

North America leads early adoption due to robotaxi pilots and autonomous freight trials, while Asia-Pacific represents the largest long-term growth opportunity, driven by smart cities, autonomous delivery fleets, and government-backed mobility innovation.

Key Drivers of Global Autonomous & Future Mobility Tyres Market Growth

Rapid Deployment of Autonomous Fleets

Robotaxis, shuttles, and delivery bots run 24/7, so their tyres wear out super fast . That nonstop grind fuels huge replacement demand, driving steady market growth.

Shift Toward Electric & Software-Defined Vehicles

Autonomous platforms are predominantly electric, requiring tyres with low rolling resistance, high load-bearing capacity, and reduced vibration.

Need for Predictable & Data-Driven Maintenance

Fleet operators want tyres that predict wear, so they can fix issues before breakdowns . This cuts downtime, boosts uptime, and keeps fleets rolling smooth . It???s a smart move driving market growth.

Smart City & Urban Mobility Programs

Government investments in autonomous public transport, campus mobility, and last-mile delivery accelerate tyre demand.

Noise Reduction & Passenger Comfort Requirements

Without engine noise, tyre noise becomes dominant???driving adoption of acoustic and vibration-dampening tyre technologies.

Global Autonomous & Future Mobility Tyres Market Segmentation??

1. By Mobility Type

1.1 Autonomous Passenger Vehicles??

1.1.1 Robotaxis

1.1.1.1 Urban robotaxi fleets

1.1.1.2 Inter-city autonomous taxi services

1.1.2 Privately Owned Autonomous Cars

1.1.2.1 Premium autonomous passenger cars

1.1.2.2 Mass-market autonomous vehicles

1.2 Autonomous Commercial Vehicles

1.2.1 Autonomous Delivery Vans

1.2.1.1 Last-mile delivery vans

1.2.1.2 Mid-mile logistics vans

1.2.2 Autonomous Trucks

1.2.2.1 Autonomous regional haul trucks

1.2.2.2 Autonomous long-haul freight trucks

1.3 Shared & On-Demand Autonomous Mobility

1.3.1 Ride-Hailing Autonomous Fleets

1.3.1.1 App-based shared autonomous cars

1.3.1.2 Subscription-based autonomous mobility

1.3.2 Autonomous Shuttles & Pods

1.3.2.1 Urban public transport shuttles

1.3.2.2 Campus & industrial park pods

2. By Tyre Construction & Design

2.1 Radial Tyres??2.1.1 Steel-Belted Radial Tyres

2.1.1.1 Single steel-belt radial tyres

2.1.1.2?? Multi-layer steel-belt radial tyres

2.1.2 Fabric-Belted Radial Tyres

2.1.2.1 Polyester fabric radial tyres

2.1.2.2 Nylon fabric radial tyres

2.2 Airless & Non-Pneumatic Tyres (Fastest-Growing Segment)

2.2.1 Polymer Lattice Tyres

2.2.1.1 Thermoplastic lattice tyres

2.2.1.2 Elastomer-based lattice tyres

2.2.2 Composite Airless Tyres

2.2.2.1 Fiber-reinforced composite tyres

2.2.2.2 Hybrid polymer-composite tyres

2.3 Solid Tyres

2.3.1 Industrial Solid Tyres

2.3.1.1 Warehouse autonomous robots

2.3.1.2 Factory AGVs

2.3.2 Low-Speed Autonomous Platform Tyres

2.3.2.1 Sidewalk delivery robots

2.3.2.2 Indoor mobility platforms

3. By Autonomy Level

3.1 Level 2???3 (ADAS-Enabled Vehicles)

3.1.1 Passenger Vehicles

3.1.1.1 ADAS-equipped sedans

3.1.1.2 ADAS-equipped SUVs

3.1.2 Commercial Vehicles

3.1.2.1 Semi-autonomous delivery vans

3.2 Level 4 Autonomous Vehicles??

3.2.1 Autonomous Passenger Platforms

3.2.1.1 Robotaxis

3.2.1.2 Autonomous shared shuttles

3.2.2 Autonomous Commercial Platforms

3.2.2.1 Driverless delivery vehicles

3.2.2.2 Autonomous logistics vehicles

3.3 Level 5 Fully Autonomous Vehicles

3.3.1 Universal Autonomous Platforms

3.3.1.1 Fully driverless passenger vehicles

3.3.1.2 Fully autonomous freight platforms

4. By Tyre Technology

4.1 Low Rolling Resistance Tyres

4.1.1 EV-Optimized Compound Tyres

4.1.1.1 Energy-efficient tread compounds

4.1.1.2 Lightweight structural designs

4.2 Smart & Connected Tyres (Core Segment)

4.2.1 Sensor-Embedded Tyres

4.2.1.1 Pressure monitoring sensors

4.2.1.2 Temperature & load sensors

4.2.2 Connected Tyre Systems

4.2.2.1 Vehicle-to-Tyre (V2T) communication

4.2.2.2 Cloud-based tyre analytics platforms

4.3 Noise & Vibration Suppression Tyres

4.3.1 Acoustic Comfort Tyres

4.3.1.1 Acoustic foam-lined tyres

4.3.1.2 Resonance-canceling tyre designs

4.3.2 Ride Comfort Optimized Tyres

4.3.2.1 Low-vibration tread patterns

4.3.2.2 Soft-compound comfort tyres

4.4 Self-Healing & Maintenance-Free Tyres

4.4.1 Self-Sealing Tyres

4.4.1.1 Sealant-based puncture protection

4.4.1.2 Gel-infused tread technologies

4.4.2 Puncture-Resistant Tyres

4.4.2.1 Reinforced sidewall tyres

4.4.2.2 Multi-layer protective carcass tyres

5. By Sales Channel

5.1 OEM (Original Equipment Manufacturer)

5.1.1 Autonomous Passenger Vehicle OEMs

5.1.1.1 Robotaxi manufacturers

5.1.1.2 Autonomous car OEMs

5.1.2 Autonomous Commercial Vehicle OEMs

5.1.2.1 Autonomous truck OEMs

5.1.2.2 Autonomous delivery vehicle OEMs

5.2 Fleet & Mobility Operators (Largest Segment)

5.2.1 Autonomous Mobility Fleet Operators

5.2.1.1 Robotaxi service providers

5.2.1.2 Shared autonomous shuttle operators

5.2.2 Tyre-as-a-Service (TaaS) Models

5.2.2.1 Subscription-based tyre supply

5.2.2.2 Usage-based tyre replacement contracts

5.3 Aftermarket / Replacement

5.3.1 Authorized Autonomous Tyre Dealers

5.3.1.1 OEM-certified tyre distributors

5.3.2 Independent Replacement Channels

5.3.2.1 Multi-brand tyre retailers

5.3.2.2 Specialized autonomous vehicle service centers

6. By Geography

6.1 North America

6.1.1 U.S.

6.1.2 Canada

6.2 Asia-Pacific (Largest Growth Potential)

6.2.1 China

6.2.2 Japan

6.2.3 South Korea

6.3 Europe

6.3.1 Germany

6.3.2 France

6.3.3 U.K.

Regional Insights of Global Autonomous & Future Mobility Tyres Market

North America

Leads in early commercialization, driven by robotaxi pilots, autonomous trucking corridors, and advanced fleet analytics adoption.

Asia-Pacific

The largest long-term market, supported by smart city deployments, autonomous delivery robots, and strong government backing in China, Japan, and South Korea.

Europe

Growth driven by safety regulations, sustainability mandates, and integration of autonomous shuttles in public transport systems.

Leading Companies in the Global Autonomous & Future Mobility Tyres Market

-

Goodyear Tire & Rubber Company

-

Continental AG

-

Pirelli & C. S.p.A.

-

Hankook Tire

-

Yokohama Rubber Company

-

Toyo Tires

-

Sumitomo Rubber Industries

-

Specialized autonomous tyre startups

Michelin is the largest company in the Global Autonomous & Future Mobility Tyres Market

Why the Autonomous & Future Mobility Tyres Market Is Critical

-

Tyres become data interfaces, not just consumables

-

Direct impact on autonomous safety and sensor accuracy

-

Enables 24/7 fleet uptime and predictable maintenance

-

Essential for robotaxis, smart cities, and autonomous logistics

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Models autonomous vehicle parc growth, fleet utilization rates, and smart city mobility deployment.

Autonomous Tyre Intelligence Model

Analyzes sensor integration, predictive maintenance adoption, and tyre-as-a-service penetration.

Raw Material & Technology Sensitivity Model

Tracks impact of advanced polymers, composites, and digital integration on tyre cost structures.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: High ??? fleet operators negotiate long-term contracts

-

Supplier Power: Moderate ??? advanced materials and sensors

-

Threat of New Entrants: Low ??? high R&D and OEM certification barriers

-

Threat of Substitutes: Low ??? tyres remain mission-critical

-

Competitive Rivalry: High ??? innovation-led competition

Final Takeaway of Global Autonomous & Future Mobility Tyres Market

The Global Autonomous & Future Mobility Tyres Market represents a structural shift in the tyre industry???from replacement-driven sales to technology-led, fleet-integrated mobility solutions. As autonomous vehicles scale globally, tyres will evolve into intelligent platforms that deliver durability, efficiency, comfort, and real-time data.

Manufacturers that invest in smart tyres, airless designs, predictive analytics, and fleet service models will define leadership in this next-generation mobility market through 2033 and beyond.

Competitive Landscape

Global Autonomous & Future Mobility Tyres Market Competitive Intensity & Market Structure Overview

The Global Autonomous & Future Mobility Tyres Market is characterized by a highly technology-intensive and rapidly evolving competitive ecosystem, driven by the rise of autonomous vehicles, robotaxis, and software-defined mobility platforms. The market is transitioning from traditional tyre supply models to integrated mobility and data-driven tyre ecosystems.

Competitive intensity is high due to the convergence of automotive OEMs, AI mobility platforms, and tyre manufacturers. Unlike conventional tyre markets, competition here is defined by sensor integration capability, predictive maintenance intelligence, airless tyre innovation, and compatibility with autonomous driving systems.

The market shows a moderately consolidated structure at the top, where Tier 1 global manufacturers dominate OEM contracts for autonomous passenger vehicles and commercial fleets. However, the ecosystem is expanding rapidly with the entry of mobility-tech firms and specialized startups focused on smart and airless tyre technologies.

Global Autonomous & Future Mobility Tyres Market?? Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global Tyre Manufacturer. Leader in autonomous-ready tyres, airless mobility solutions, and predictive tyre intelligence systems.

Bridgestone Corporation: Global Tyre Manufacturer. Strong focus on fleet automation integration, smart tyres, and mobility-as-a-service solutions.

Goodyear Tire & Rubber Company: Tyre Manufacturer. Leading in connected tyre ecosystems and autonomous fleet data integration.

Continental AG: Technology-Driven Tyre Manufacturer. Strong in sensor-enabled tyres, V2T communication, and autonomous safety systems.

Pirelli & C. S.p.A.: Premium Tyre Manufacturer. Focused on high-performance autonomous passenger platforms and luxury mobility systems.

Hankook Tire: Fast-Growing Global Player. Expanding into EV-autonomous crossover segment and smart tyre solutions.

Yokohama Rubber Company: Tyre Manufacturer. Known for durable and connected tyre technologies for fleet mobility systems.

Toyo Tires: Innovation-Focused Manufacturer. Expanding presence in autonomous and performance mobility platforms.

Sumitomo Rubber Industries: Strong Asia-Pacific Player. Focused on sensor-integrated and long-life mobility tyres.

Specialized Autonomous Tyre Startups: Emerging innovators. Focused on airless tyres, smart sensing systems, and software-defined tyre platforms.

Key Competitive Intensity & Market Structure Signals in Autonomous Tyres

A key structural shift in the market is the transition from product-based competition to ecosystem-based competition. Tyres are increasingly embedded within autonomous vehicle software systems, making data compatibility and sensor integration a core requirement.

Fleet operators, particularly robotaxi and autonomous logistics providers, are becoming the most powerful buyers. Their demand for uptime optimization, predictive maintenance, and tyre-as-a-service models is reshaping procurement strategies.

Another major signal is the rapid emergence of airless and non-pneumatic tyre technologies. These systems are gaining traction in autonomous fleets due to their durability, reduced maintenance needs, and suitability for continuous 24/7 operations.

Data-driven tyre intelligence is becoming a key differentiator. Manufacturers that provide real-time tyre health monitoring, AI-based wear prediction, and cloud-based fleet analytics are gaining strategic advantage in OEM partnerships.

Despite rapid innovation, traditional tyre manufacturers still dominate due to their OEM relationships, global manufacturing scale, and certification capabilities required for autonomous vehicle deployment.

Strategic Implications of Competitive Intensity & Market Structure in Autonomous Tyres

The competitive landscape is pushing manufacturers toward deep integration with autonomous vehicle software ecosystems. Tyres are no longer standalone components but critical data nodes within mobility networks.

Total cost of ownership (TCO) is being redefined through uptime maximization. Autonomous fleets prioritize uninterrupted operations, making predictive maintenance and failure prevention more valuable than initial tyre cost.

Electrification and autonomy together are reshaping product design priorities. Tyres must support heavier vehicles, continuous operation cycles, and extremely precise sensor feedback for safe navigation.

Additionally, the rise of Tyre-as-a-Service (TaaS) models is transforming revenue structures. Manufacturers are shifting from one-time sales to subscription-based mobility contracts tied to usage, performance, and data services.

Airless tyre systems and smart connected platforms are emerging as long-term disruptive forces, forcing traditional manufacturers to accelerate innovation or risk displacement in high-value autonomous segments.

Autonomous & Future Mobility Tyres Competitive Intensity & Market Structure Forward Outlook

The Autonomous Tyres Market is expected to remain highly competitive and innovation-led, with increasing convergence between automotive OEMs, AI mobility firms, and tyre manufacturers.

Market consolidation is likely as leading tyre companies acquire startups specializing in smart sensors, airless designs, and mobility analytics platforms to strengthen their autonomous readiness.

Regulatory frameworks around autonomous safety, data transparency, and mobility reliability will significantly influence product development and certification requirements.

In the long term, the market will be defined by three core pillars: autonomous system integration, airless and maintenance-free tyre architecture, and real-time mobility intelligence. Companies that successfully combine physical tyre engineering with digital mobility ecosystems will lead the Autonomous & Future Mobility Tyres Market through 2033 and beyond.

Value Chain

Global Autonomous & Future Mobility Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain structure of the Global Autonomous & Future Mobility Tyres Market is rapidly evolving from a traditional manufacturing-led model into a highly digital, software-integrated, and mobility ecosystem-driven framework. Unlike conventional tyre markets, this segment is deeply connected with autonomous vehicle OEMs, robotics platforms, smart city infrastructure, and fleet-as-a-service operators. The supply chain operates through an advanced multi-layer ecosystem involving raw material suppliers, advanced polymer and sensor technology providers, tyre manufacturers, autonomous vehicle OEMs, mobility fleet operators, and cloud-based analytics platforms. This integration ensures that tyres are not only physical components but also data-generating mobility assets. Upstream inputs include advanced polymers, silica compounds, synthetic rubber, carbon black, steel reinforcement materials, and increasingly, embedded electronic components such as pressure sensors, temperature sensors, and RFID/IoT modules. Suppliers are expanding partnerships with tyre manufacturers to support smart tyre architectures and airless tyre development. Manufacturing in this market is highly innovation-intensive, focusing on airless tyre systems, sensor-integrated radial designs, low rolling resistance compounds, and noise-reduction technologies. Production processes are increasingly aligned with EV and autonomous vehicle platforms, where consistency, predictability, and data integration are more critical than traditional performance metrics alone. Distribution is heavily concentrated within OEM agreements and fleet mobility partnerships. Autonomous mobility operators such as robotaxi providers, logistics automation companies, and smart city fleets directly procure tyres under long-term service contracts. The aftermarket segment is emerging but remains secondary, driven by early-stage autonomous fleet replacements and pilot deployments. Key supply chain challenges include high R&D costs, integration complexity with vehicle software systems, dependency on semiconductor and sensor supply chains, and evolving global regulatory frameworks for autonomous mobility safety standards.

Global Autonomous & Future Mobility Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The Global Autonomous & Future Mobility Tyres Market is currently in a transition phase, moving from experimental deployments toward early commercialization of autonomous mobility ecosystems. This shift is reshaping supply chain structures across manufacturing, distribution, and service layers. At the upstream level, material suppliers are increasingly collaborating with tyre manufacturers to develop advanced composites, self-healing compounds, and lightweight structures suitable for autonomous platforms. Sensor integration and connectivity components are becoming standard requirements rather than optional enhancements. Manufacturers such as Michelin, Bridgestone, Continental, and Goodyear are investing heavily in smart tyre ecosystems that combine hardware durability with real-time data intelligence. Airless tyre prototypes and predictive maintenance-enabled tyres are being tested in controlled autonomous fleet environments. OEM integration is a critical pillar, with autonomous vehicle developers and electric mobility platforms co-designing tyres alongside vehicle architectures. Tyres are now engineered as part of the vehicle’s sensor and navigation ecosystem, ensuring compatibility with AI-driven driving systems. Fleet operators, particularly robotaxi and autonomous logistics companies, are emerging as direct procurement hubs, bypassing traditional dealership models. This shift is enabling tyre-as-a-service (TaaS) models, where usage-based pricing and predictive maintenance contracts are gaining traction. Digitalization is transforming supply chain operations through AI-based tyre monitoring, cloud analytics platforms, and vehicle-to-tyre (V2T) communication systems, enabling real-time performance tracking and predictive failure prevention.

Key Value Chain & Supply Chain Evolution Signals in Global Autonomous & Future Mobility Tyres Market

Several structural signals are reshaping the evolution of this value chain. First, the rise of airless and non-pneumatic tyres is fundamentally changing manufacturing architectures by eliminating traditional pressure-based systems and introducing new material engineering approaches. Second, smart connectivity is transforming tyres into active data nodes within autonomous vehicle ecosystems, enabling predictive maintenance, fleet optimization, and safety assurance. Third, fleet-based procurement models are replacing retail-driven demand, with mobility operators demanding long-term service contracts and performance-linked tyre supply agreements. Fourth, integration with AI-driven autonomous driving systems is increasing the importance of consistency, reliability, and real-time responsiveness in tyre performance. Finally, sustainability and lifecycle optimization are becoming central themes, with manufacturers focusing on recyclable materials, energy-efficient production, and extended tyre life solutions for high-utilization autonomous fleets.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Autonomous & Future Mobility Tyres Market

Leading companies such as Michelin, Bridgestone, Continental, and Goodyear are positioned to benefit from early investments in smart tyre technologies, OEM partnerships, and autonomous mobility collaborations. Their global R&D capabilities and digital integration strategies provide strong competitive advantages. The increasing complexity of autonomous mobility systems is creating significant entry barriers, particularly due to the need for cross-disciplinary expertise in materials science, software integration, and vehicle systems engineering. Fleet operators are shifting toward subscription-based tyre usage models, creating predictable revenue streams for manufacturers while enhancing lifecycle management efficiency across autonomous fleets. Cost structures are increasingly influenced by sensor technology, advanced materials, and software integration, requiring manufacturers to balance innovation investment with scalable production models. The transition to autonomous mobility is creating entirely new product categories, including airless tyres, smart tyres, and predictive maintenance-enabled tyre systems, fundamentally reshaping traditional market boundaries.

Global Autonomous & Future Mobility Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to become fully integrated, digitally connected, and ecosystem-driven, with tyres functioning as intelligent mobility components rather than standalone products. Manufacturers will increasingly prioritize airless tyre commercialization, embedded sensor ecosystems, and AI-driven predictive maintenance platforms to align with autonomous vehicle requirements. The fleet and mobility operator segment will dominate demand, with widespread adoption of tyre-as-a-service models and integrated mobility maintenance platforms. Digital ecosystems will play a central role, enabling real-time tyre performance monitoring, autonomous fleet optimization, and cloud-based mobility analytics. Overall, the future value chain will be defined by intelligence, connectivity, and automation, where companies that successfully integrate tyre engineering with digital mobility systems will lead the market transformation through 2033.

Market-Specific Value Chain

- Raw Material Procurement: Advanced polymers, synthetic rubber, carbon black, steel reinforcement, sensor components, and IoT modules

- Research & Development: Airless tyre design, smart sensor integration, AI-based wear prediction, and low-noise compound engineering

- Manufacturing: Production of radial, airless, and smart tyres with embedded electronic systems and advanced composite structures

- OEM Integration: Supply to autonomous vehicle manufacturers, robotaxi platforms, and electric autonomous commercial fleets

- Fleet & Mobility Distribution: Direct contracts with robotaxi operators, logistics automation firms, and smart city mobility networks

- Aftermarket & Services: Predictive maintenance, tyre-as-a-service models, smart monitoring platforms, and lifecycle optimization services

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire, emerging autonomous mobility startups

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Pirelli & C. S.p.A.

- Fleet & Mobility Distribution: Goodyear, Continental AG, Michelin, specialized autonomous fleet service providers

- Aftermarket & Services: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

Investment Activity

Global Autonomous & Future Mobility Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Autonomous & Future Mobility Tyres Market are being shaped by the rapid development of autonomous driving technologies, expansion of robotaxi networks, and the rise of smart city mobility ecosystems. Between 2026 and 2033, capital deployment is expected to concentrate on smart connected tyres, airless and non-pneumatic tyre systems, predictive maintenance platforms, and advanced sensor-integrated mobility solutions.

The market is highly technology-driven and R&D intensive, requiring continuous investment in advanced materials, polymer lattice structures, composite airless systems, embedded electronics, and vehicle-to-tyre communication technologies. Leading players such as Michelin, Bridgestone, Continental, Goodyear, and Pirelli are actively investing in autonomous mobility tyre platforms and forming strategic partnerships with OEMs and mobility service providers.

A key structural shift influencing investment flows is the transition from individually owned vehicles to shared autonomous mobility fleets. This is accelerating funding into tyre-as-a-service (TaaS) models, where tyres are managed as part of uptime-focused mobility contracts rather than traditional replacement products.

Global Autonomous & Future Mobility Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by pilot deployments of robotaxis, autonomous delivery fleets, and smart urban mobility programs. These applications require high-performance tyres capable of continuous operation, predictable wear behavior, and real-time condition monitoring.

North America leads early-stage investment due to active robotaxi pilots, autonomous freight corridors, and strong venture capital participation in mobility startups.

Asia-Pacific represents the largest long-term investment opportunity, driven by large-scale smart city initiatives, autonomous delivery ecosystems, and government-backed mobility innovation programs in China, Japan, and South Korea.

Europe is experiencing accelerating investment flows supported by sustainability mandates, urban mobility transformation, and integration of autonomous public transport systems.

Key Investment & Funding Dynamics Signals in Global Autonomous & Future Mobility Tyres Market

A key investment signal is the rapid commercialization of Level 4 autonomous vehicles, which is driving demand for highly durable, sensor-enabled, and maintenance-optimized tyres.

The emergence of airless and non-pneumatic tyre technologies is attracting significant capital due to their potential to eliminate punctures, reduce maintenance downtime, and support continuous fleet operations.

Growing adoption of smart tyres with embedded sensors is accelerating investments in vehicle-to-tyre communication systems, real-time analytics platforms, and predictive maintenance ecosystems.

Expansion of shared autonomous mobility services is creating long-term investment opportunities in fleet-based tyre management systems and subscription-based tyre models.

Increasing focus on ride comfort and noise reduction in autonomous vehicles is pushing funding into acoustic engineering, vibration suppression technologies, and advanced tread design innovations.

Strategic Implications of Investment & Funding Dynamics in Global Autonomous & Future Mobility Tyres Market

The investment landscape strongly favors established tyre manufacturers with advanced R&D capabilities and deep integration with automotive OEMs and autonomous technology developers.

Strategic partnerships between tyre companies, autonomous vehicle manufacturers, and mobility service providers are becoming essential for securing long-term contracts and ecosystem integration.

Technology differentiation is a critical competitive factor, particularly in smart tyre systems, airless structures, and predictive maintenance capabilities.

Regional diversification is essential, with North America leading early adoption, Asia-Pacific driving scale deployment, and Europe focusing on regulatory-compliant and sustainability-driven mobility systems.

High dependence on advanced materials, sensors, and digital infrastructure introduces cost volatility, requiring strategic investment in supply chain resilience and vertical integration.

Global Autonomous & Future Mobility Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Autonomous & Future Mobility Tyres Market is expected to attract strong and sustained investment as autonomous mobility transitions from pilot programs to large-scale commercial deployment.

Future capital allocation will prioritize airless tyre systems, AI-enabled predictive maintenance platforms, ultra-low noise tyre technologies, and fully connected smart tyre ecosystems designed for 24/7 fleet operations.

Asia-Pacific will emerge as the dominant long-term investment hub, while North America will continue to lead early innovation and commercialization. Europe will play a key role in regulatory-driven adoption and sustainable mobility integration.

Digital transformation will fundamentally reshape investment patterns, with increasing focus on tyre intelligence platforms, data-driven fleet optimization, and integrated mobility-as-a-service ecosystems.

Overall, the market will evolve from a product-centric tyre industry to a service- and data-driven mobility infrastructure layer. Companies that successfully combine materials innovation, sensor technology, and fleet service models will lead the market through 2033 and beyond.

Technology & Innovation

Global Autonomous & Future Mobility Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global autonomous & future mobility tyres market is being reshaped by the rise of self-driving vehicles, robotaxis, autonomous delivery systems, and software-defined mobility platforms. These tyres are no longer limited to providing grip and durability; they are evolving into intelligent, connected components that support continuous operation, real-time data exchange, and predictive maintenance. Innovation intensity in this market is extremely high compared to conventional tyre segments. Continuous advancements are being made in airless tyre architectures, smart sensor integration, noise and vibration suppression systems, and ultra-durable compounds designed for 24/7 fleet utilization. Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are actively developing next-generation mobility tyre platforms tailored for autonomous ecosystems. A major technological transformation is the shift toward data-driven tyres that can communicate directly with vehicle systems. These tyres are designed to monitor wear, temperature, pressure, and load conditions in real time, enabling predictive maintenance and minimizing operational downtime. At the same time, airless and non-pneumatic tyre systems are emerging as a disruptive innovation, particularly suited for autonomous delivery robots, low-speed shuttles, and high-utilization urban fleets.

Global Autonomous & Future Mobility Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the autonomous tyre technology landscape is focused on reliability, consistency, and digital integration. With autonomous vehicles operating for extended hours without human intervention, tyres must deliver predictable performance and minimal failure risk across all operating conditions. Smart and connected tyre systems are becoming a core innovation area. Embedded sensors track pressure, temperature, load, and tread wear, transmitting real-time data to fleet management platforms. This enables predictive maintenance models that reduce breakdowns and optimize fleet uptime in autonomous operations. Airless tyre technology is gaining strong momentum, particularly for low-speed autonomous mobility platforms such as delivery bots, industrial AGVs, and campus mobility vehicles. These tyres eliminate puncture risks and significantly reduce maintenance requirements, making them ideal for continuous-use applications. Noise and vibration control is another critical development area. Since autonomous and electric vehicles operate with minimal engine noise, tyre noise becomes more noticeable. Acoustic foam inserts, optimized tread block sequencing, and resonance-canceling designs are being widely integrated to improve passenger comfort. High durability and puncture-resistant tyre designs are essential for autonomous fleets operating in urban environments with unpredictable road conditions. Reinforced sidewalls, multi-layer carcass structures, and self-sealing compounds are increasingly being adopted to ensure uninterrupted operation. Manufacturing innovation is also accelerating, with AI-powered inspection systems, automated production lines, and advanced material engineering improving consistency and reducing defects. Sustainable materials such as bio-based rubber and recycled compounds are also being integrated to align with global decarbonization goals.

Key Technology & Innovation Landscape Signals in Global Autonomous & Future Mobility Tyres Market

- Smart & Connected Tyres: IoT-enabled sensors for real-time monitoring and predictive analytics.

- Airless & Non-Pneumatic Tyres: Puncture-free designs for autonomous robots and low-speed fleets.

- Low Rolling Resistance Technology: Improves energy efficiency for electric autonomous vehicles.

- Noise & Vibration Suppression Systems: Acoustic foam and optimized tread designs for silent cabins.

- Self-Healing & Puncture-Resistant Tyres: Advanced materials for uninterrupted fleet operations.

- High Load-Bearing Structures: Reinforced designs for heavy autonomous EV platforms.

- Vehicle-to-Tyre Communication (V2T): Enables direct data exchange between tyres and autonomous systems.

Strategic Implications of Technology & Innovation Landscape in Global Autonomous & Future Mobility Tyres Market

The evolution of autonomous tyre technologies is creating major strategic shifts across the mobility ecosystem. Tyre manufacturers are no longer just component suppliers’they are becoming technology partners in autonomous vehicle ecosystems. Continuous R&D investment is essential to meet requirements for safety, durability, and real-time data integration. OEM collaboration is becoming increasingly critical as autonomous vehicles require highly customized tyre solutions optimized for sensor performance, load distribution, and continuous operation. This is driving deeper integration between tyre manufacturers, autonomous vehicle developers, and software platforms. Smart tyre systems are enabling a shift toward service-oriented business models such as Tyre-as-a-Service (TaaS), where fleets subscribe to usage-based tyre monitoring, replacement, and maintenance solutions. This is transforming traditional tyre sales into recurring revenue models. Sustainability is also becoming a key strategic pillar, with increasing focus on recyclable materials, low-carbon production processes, and circular lifecycle management. Regulatory pressure and ESG commitments are accelerating adoption of eco-friendly tyre technologies. For autonomous fleet operators, tyres are mission-critical components that directly impact safety, uptime, and operational efficiency. Predictive tyre intelligence significantly reduces downtime and ensures consistent fleet performance in high-utilization environments such as robotaxi networks and autonomous logistics systems.

Global Autonomous & Future Mobility Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the autonomous tyres market is expected to transition toward fully intelligent, self-monitoring, and maintenance-optimized systems. Airless tyre adoption will expand significantly across urban mobility robots, autonomous shuttles, and industrial platforms. Smart tyre technologies will become standard across Level 4 and Level 5 autonomous vehicles, enabling continuous data flow into AI-driven mobility platforms. This will enhance predictive maintenance accuracy, safety performance, and fleet optimization capabilities. Material innovation will focus on ultra-durable composites, lightweight structures, and advanced elastomers designed for long operational lifespans and reduced environmental impact. These developments will support both performance and sustainability goals. Manufacturing processes will continue to evolve through automation, digital twins, and AI-based quality control systems, improving production efficiency and accelerating innovation cycles across global tyre manufacturing networks. In conclusion, the Global Autonomous & Future Mobility Tyres Market is undergoing a structural transformation from traditional consumables to intelligent mobility infrastructure components. Companies that lead in smart tyre systems, airless technologies, predictive analytics, and sustainable material innovation will define the competitive landscape through 2033 and beyond.

Market Risk

Global Autonomous & Future Mobility Tyres Market Risk Factors & Disruption Threats Overview

The Global Autonomous & Future Mobility Tyres Market operates in a highly technology-dependent and rapidly evolving mobility ecosystem, driven by autonomous vehicles, robotaxis, smart logistics, and shared mobility platforms. While the market is supported by strong long-term growth potential, it carries a high risk and disruption profile due to technological uncertainty, regulatory evolution, and shifting mobility ownership models. A major structural risk is technology uncertainty in autonomous mobility deployment timelines. Since large-scale Level 4 and Level 5 adoption is still evolving, tyre demand forecasting remains complex, with delays in fleet scaling directly impacting OEM and fleet procurement cycles. Another key disruption factor is the increasing shift toward fleet-centric mobility models. As ownership transitions from individuals to large mobility operators, tyre procurement becomes centralized, increasing buyer power and placing significant pricing pressure on manufacturers operating under long-term contracts. Rapid technological integration is also a critical risk driver. Smart tyres, sensor-enabled systems, and connected mobility platforms require continuous R&D investment, shortening product life cycles and increasing the risk of technological obsolescence for conventional tyre designs. The rise of airless and non-pneumatic tyres further disrupts the market structure. These technologies are increasingly relevant in autonomous shuttles, delivery robots, and low-speed mobility platforms where maintenance-free operation and durability are prioritized over traditional pneumatic performance.

Global Autonomous & Future Mobility Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects early-stage commercialization of autonomous mobility, supported by pilot programs in robotaxis, autonomous trucking, and smart city mobility systems. However, adoption remains uneven across regions and use cases. OEMs and fleet operators are prioritizing tyres with low rolling resistance, high durability, and sensor integration. However, cost sensitivity remains high due to uncertain fleet utilization rates and evolving autonomous business models. The aftermarket segment is still developing, as most autonomous fleets operate under warranty or service agreements. This is accelerating the shift toward tyre-as-a-service and managed fleet solutions rather than traditional replacement cycles. Supply chain complexity is increasing due to advanced materials, embedded electronics, and composite structures required for smart and airless tyre systems. This creates dependency on specialized suppliers and increases production risks. At the same time, the convergence of electric and autonomous mobility is reshaping demand patterns, requiring tyres that balance load-bearing capacity, energy efficiency, and ultra-low noise performance.

Global Autonomous & Future Mobility Tyres Market Risk Factors & Disruption Threats Signals

A key risk signal is the rapid scaling of robotaxi and autonomous delivery fleets. While this increases utilization-based demand, it also creates unpredictable wear patterns due to continuous 24/7 operation cycles. Fleet consolidation is another major signal. Large mobility operators and tech platforms are centralizing procurement decisions, increasing negotiating power and shifting the market toward long-term contractual pricing models. The acceleration of airless tyre adoption is a disruptive signal, especially in low-speed autonomous applications such as delivery robots and urban shuttle systems where maintenance-free operation is essential. AI-driven fleet management systems are also reshaping the market, requiring tyres to integrate with predictive analytics platforms for real-time performance monitoring and maintenance prediction. Additionally, regulatory uncertainty around autonomous vehicle safety standards and deployment timelines remains a key factor influencing investment decisions in advanced tyre technologies.

Global Autonomous & Future Mobility Tyres Market Strategic Implications

Manufacturers must transition from product-based offerings to service-oriented ecosystems, with Tyre-as-a-Service (TaaS) models aligned with fleet utilization and performance contracts. Investment in smart tyre technology is essential, including embedded sensors, connectivity systems, and predictive analytics capabilities tailored for autonomous fleets. Development of airless, puncture-resistant, and maintenance-free tyres is increasingly important for low-speed autonomous platforms and high-utilization mobility systems. Strong partnerships with OEMs, robotaxi operators, and mobility platforms are critical, as procurement decisions are becoming centralized and technology-driven. Supply chain resilience and advanced material innovation strategies are required to manage complexity from electronics integration and composite manufacturing processes.

Global Autonomous & Future Mobility Tyres Market Forward Outlook

Looking ahead to 2026-2033, the market will evolve into a highly integrated, fleet-driven ecosystem supported by autonomous mobility expansion and smart city development. Airless tyres are expected to gain traction in controlled environments such as urban delivery, campuses, and industrial zones, reshaping traditional demand structures. Smart tyres will become standard in autonomous fleets, enabling predictive maintenance, real-time diagnostics, and integration with AI mobility platforms. Tyre-as-a-Service models will expand, shifting revenue from one-time sales to performance-based contracts linked to fleet uptime and efficiency. Overall, the market will remain highly disruptive but structurally transformative, with leadership dependent on digital integration, advanced materials, and service-based business models.

Regulatory Landscape

Global Autonomous & Future Mobility Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Autonomous & Future Mobility Tyres Market is evolving rapidly alongside advancements in autonomous driving, smart mobility, and connected vehicle ecosystems. Since these tyres directly influence safety, sensor accuracy, vehicle uptime, and operational reliability, regulators are increasingly integrating tyre performance standards into broader autonomous vehicle (AV) governance frameworks. Existing global standards such as the European Union Tyre Labelling Regulation (EU 2020/740) and UNECE tyre safety regulations continue to serve as foundational benchmarks for rolling resistance, wet grip, and external noise. However, autonomous mobility introduces new compliance dimensions, including continuous operation durability, predictive maintenance capability, and compatibility with sensor-integrated vehicle architectures. In addition, autonomous vehicle regulations across key markets are expanding to include requirements for system redundancy, real-time monitoring, and safety assurance protocols. These frameworks indirectly influence tyre innovation, pushing manufacturers toward smart, data-enabled, and self-monitoring tyre technologies that support Level 4 and Level 5 autonomous operations. Sustainability regulations are also becoming more influential, particularly in regions prioritizing carbon neutrality and urban decarbonization. Policies encouraging shared autonomous mobility, electric robotaxis, and low-emission logistics are driving demand for low rolling resistance, long-life, and recyclable tyre solutions designed for high-utilization fleets.

Global Autonomous & Future Mobility Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is shaped by early-stage autonomous mobility deployment, pilot programs, and evolving safety frameworks. North America leads in regulatory experimentation, with autonomous vehicle testing corridors, robotaxi approvals, and freight automation pilots requiring strict safety validation and operational monitoring systems. In Europe, regulatory focus is strongly aligned with safety assurance, sustainability compliance, and urban mobility integration. Smart city initiatives and public transport automation programs are encouraging the adoption of low-noise and high-efficiency tyres suitable for autonomous shuttles and shared mobility systems operating in dense urban environments. Asia-Pacific is advancing rapidly through government-backed smart city initiatives, autonomous delivery programs, and digital infrastructure development. China, Japan, and South Korea are actively supporting autonomous logistics and mobility platforms, indirectly accelerating demand for EV-compatible and sensor-ready tyre technologies. At the same time, regulatory authorities are increasingly focusing on continuous monitoring and predictive safety systems. This shift is encouraging the integration of embedded sensors, Vehicle-to-Tyre (V2T) communication systems, and cloud-based analytics platforms within next-generation autonomous tyres.

Key Regulatory & Policy Environment Signals in Global Autonomous & Future Mobility Tyres Market

- Autonomous Vehicle Safety Frameworks: Require continuous monitoring, redundancy, and system reliability, influencing smart tyre integration.

- UNECE Tyre Safety Standards: Provide baseline safety and durability benchmarks increasingly adapted for high-utilization autonomous fleets.

- EU Tyre Labelling Regulation (EU 2020/740): Supports efficiency, noise reduction, and sustainability compliance in autonomous mobility systems.

- Smart City Mobility Policies: Encourage deployment of autonomous shuttles, robotaxis, and delivery bots using advanced tyre technologies.

- Zero-Emission & Electrification Mandates: Accelerate demand for low rolling resistance and EV-optimized autonomous tyres.

- Data Privacy & Connected Vehicle Regulations: Influence design of tyre sensors and cloud-based analytics systems used in fleet monitoring.

Strategic Implications of Regulatory & Policy Environment in Global Autonomous & Future Mobility Tyres Market

The regulatory environment is significantly reshaping competitive dynamics by increasing entry barriers for traditional tyre manufacturers lacking digital and sensor integration capabilities. Compliance now extends beyond physical performance to include data generation, connectivity, and predictive maintenance compatibility. Manufacturers are increasingly investing in smart tyre ecosystems that integrate embedded sensors, AI-driven analytics, and real-time communication with autonomous driving systems. This convergence of hardware and software is becoming essential for regulatory compliance and fleet integration. Fleet operators and mobility platforms are also becoming more influential in procurement decisions due to their need for uptime optimization and predictive maintenance. As a result, tyre-as-a-service (TaaS) models and long-term fleet partnerships are gaining regulatory and commercial importance. Regional differences in autonomous vehicle regulation are encouraging localized innovation strategies. North America emphasizes operational safety validation, Europe prioritizes sustainability and urban integration, while Asia-Pacific focuses on scalability and smart infrastructure alignment.

Global Autonomous & Future Mobility Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory landscape is expected to become significantly more sophisticated as autonomous mobility scales globally. Governments will increasingly formalize standards for connected mobility components, including smart tyres as critical safety and data infrastructure elements. Europe is expected to expand regulations around lifecycle sustainability, digital safety compliance, and noise reduction in autonomous urban transport systems. North America will continue advancing AV certification frameworks, emphasizing real-world safety validation and fleet reliability standards. Asia-Pacific will likely lead in large-scale deployment regulations, supporting autonomous logistics, smart city transport networks, and delivery automation systems, driving rapid adoption of advanced tyre technologies. Overall, the regulatory and policy environment will act as both a catalyst and a gatekeeper’accelerating innovation while enforcing stricter compliance standards. Manufacturers that successfully integrate durability, connectivity, predictive intelligence, and sustainability into autonomous tyre platforms will be best positioned to lead the Global Autonomous & Future Mobility Tyres Market through 2033 and beyond.