Global Compressed Natural Gas (CNG) Market Report, Size & Forecast 2026-2033

Global Compressed Natural Gas (CNG) Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 105.6 Billion |

| Market Size (2033) | USD 172.4 Billion |

| CAGR (2026???2033) | 6.4% |

| Largest Segment | Transportation Fuel |

| Fastest Growing Segment | Commercial Vehicle CNG Applications |

| Leading Application | Passenger Vehicles and Public Transportation |

| Key Growth Driver | Increasing demand for cleaner transportation fuels and supportive government policies |

| Key Technology Trends | Expansion of CNG refueling infrastructure, advanced high-pressure storage cylinders, dual-fuel engine technologies |

| Major End-Use Industries | Transportation, Logistics, Public Transit, Industrial Applications |

| Key Market Opportunity | Growing investments in natural gas distribution networks and low-emission mobility solutions |

| Regional Leader | Asia-Pacific |

| Fastest Growing Region | Middle East & Africa |

| Sustainability Focus | Reduction of greenhouse gas emissions and urban air pollution through cleaner fuel adoption |

Global Compressed Natural Gas (CNG) Market Size & Forecast

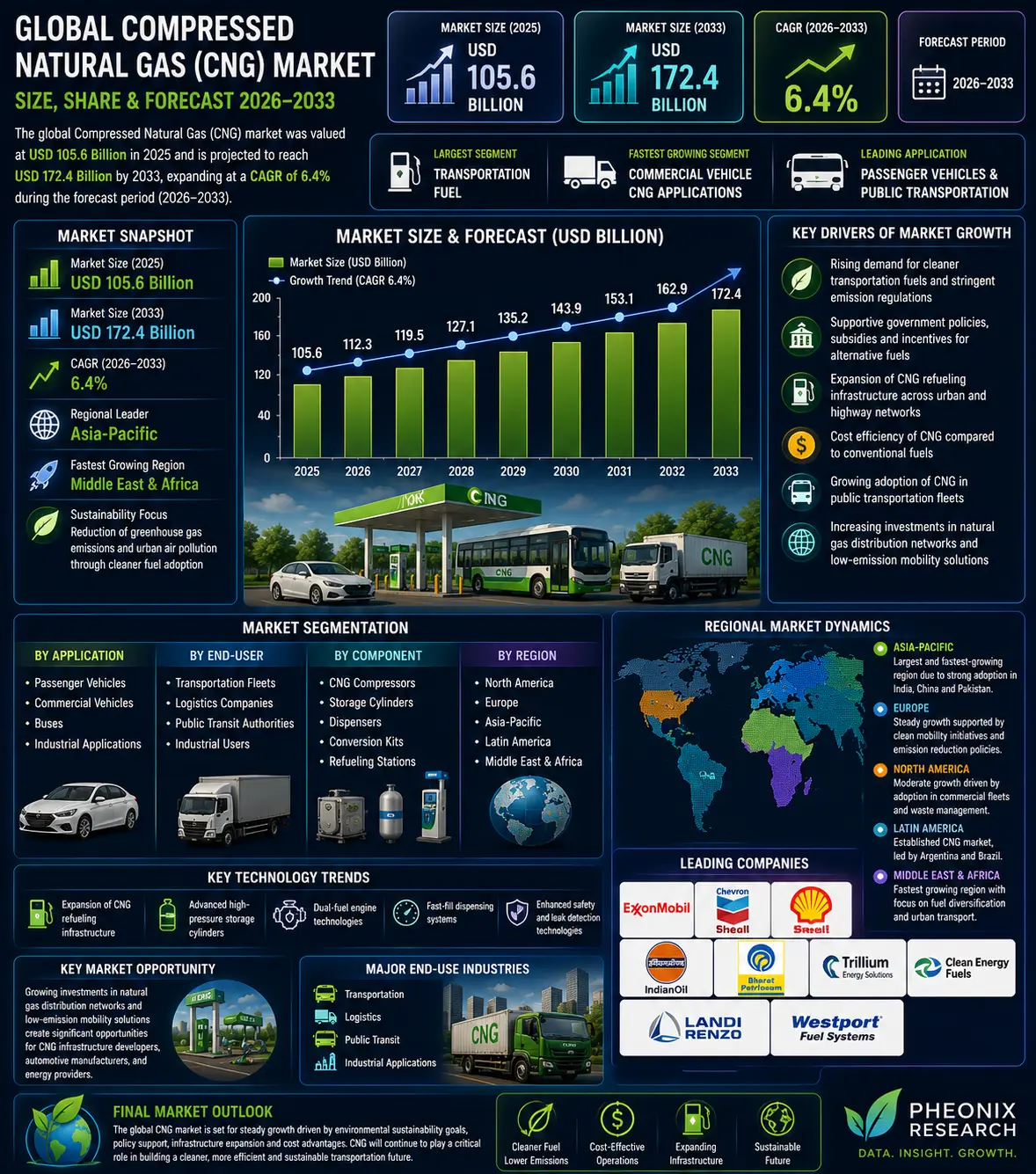

The global Compressed Natural Gas (CNG) market is projected to witness steady and sustainable growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 105.6 billion in 2025 and is expected to reach nearly USD 172.4 billion by 2033, expanding at a CAGR of around 6.4%. The market growth is driven by increasing demand for cleaner transportation fuels, rising concerns over greenhouse gas emissions, supportive government policies for alternative fuels, and expanding natural gas distribution infrastructure across emerging and developed economies. Compressed Natural Gas (CNG) is a cleaner-burning alternative fuel derived primarily from methane, stored at high pressure for use in vehicles and industrial applications. It is widely used in passenger vehicles, commercial fleets, buses, three-wheelers, and light-duty transport systems as a cost-effective and environmentally friendly alternative to gasoline and diesel. The market is undergoing gradual transformation through the expansion of CNG refueling infrastructure, advancements in high-pressure storage cylinders, and integration of dual-fuel engine technologies that enhance fuel efficiency and operational flexibility. Additionally, increasing urban air pollution concerns and global decarbonization targets are accelerating the adoption of CNG vehicles and infrastructure investments worldwide.Global Compressed Natural Gas (CNG) Market Overview

The CNG market forms a key segment of the global alternative fuels and clean mobility ecosystem. It plays an important role in reducing carbon emissions, improving air quality, and diversifying energy sources in the transportation sector. The market includes CNG-powered passenger vehicles, commercial fleets, heavy-duty transport systems, CNG fueling stations, storage cylinders, compressors, and distribution infrastructure. Automotive manufacturers and energy providers are increasingly collaborating to expand CNG ecosystems and improve fuel accessibility in urban and semi-urban regions. Technological advancements in high-capacity storage tanks, fast-fill dispensing systems, and leak detection technologies are improving safety and operational efficiency. Major market participants include ExxonMobil Corporation, Chevron Corporation, Royal Dutch Shell plc, Gazprom, Indian Oil Corporation, Bharat Petroleum Corporation Limited (BPCL), Trillium Energy Solutions, Clean Energy Fuels Corp., Landi Renzo S.p.A., and Westport Fuel Systems Inc.Key Drivers of Global CNG Market Growth

Rising Demand for Cleaner Transportation Fuels

Growing environmental concerns and stringent emission regulations are driving the shift toward low-emission fuels such as CNG. CNG produces significantly lower levels of carbon dioxide, nitrogen oxides, and particulate matter compared to conventional fuels.Government Policies and Incentives

Many governments are promoting CNG adoption through subsidies, tax benefits, and investments in fueling infrastructure. Regulatory support is significantly accelerating market penetration in developing economies.Expansion of CNG Refueling Infrastructure

The rapid expansion of CNG stations across urban and highway networks is improving accessibility and supporting vehicle adoption. Infrastructure development is a key enabler of long-term market growth.Cost Efficiency Compared to Conventional Fuels

CNG offers lower fuel costs compared to gasoline and diesel, making it attractive for commercial fleet operators and public transportation systems. This cost advantage is driving widespread adoption in price-sensitive markets.Growing Adoption in Public Transportation Fleets

CNG buses, taxis, and three-wheelers are increasingly being deployed to reduce urban pollution and operational costs. Public transport electrification strategies in many countries include CNG as a transitional fuel.Global CNG Market Segmentation

By Application

The market is segmented into passenger vehicles, commercial vehicles, buses, and industrial applications. Commercial vehicles and public transport buses account for a significant share due to high fuel consumption patterns.By End-User

End users include transportation fleets, logistics companies, public transit authorities, and industrial users. Fleet operators represent the largest end-user segment globally.By Component

The market includes CNG compressors, storage cylinders, dispensers, conversion kits, and refueling stations. CNG refueling infrastructure holds a major share due to ongoing expansion programs.By Region

The market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific dominates the global CNG market due to strong adoption in India, China, and Pakistan.Regional Market Dynamics

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region in the CNG market due to strong government support, rapid urbanization, and high fuel demand in transportation sectors. India and China are leading global CNG adoption with extensive infrastructure expansion programs.Europe

Europe maintains steady growth supported by clean mobility initiatives and emission reduction policies. Countries such as Italy, Germany, and Spain have established CNG vehicle ecosystems.North America

North America shows moderate growth driven by adoption in commercial fleets and waste management vehicles. The United States remains the key regional contributor.Latin America

Latin America is an established CNG market, particularly in Argentina and Brazil, supported by early infrastructure development. Growth continues through fleet expansion and fuel cost advantages.Middle East & Africa

The region is witnessing gradual adoption due to increasing focus on fuel diversification and urban transport modernization. Natural gas-rich countries are promoting domestic CNG usage.Competitive Landscape

The global CNG market is moderately consolidated, with participation from energy companies, automotive OEMs, and infrastructure providers. Key players include ExxonMobil Corporation, Chevron Corporation, Shell plc, Gazprom, Indian Oil Corporation, Bharat Petroleum Corporation Limited (BPCL), Clean Energy Fuels Corp., Trillium Energy Solutions, Landi Renzo S.p.A., and Westport Fuel Systems Inc. Companies are investing in CNG station expansion, advanced fuel storage systems, and dual-fuel engine technologies to improve efficiency and safety. Strategic partnerships between oil & gas companies, governments, and fleet operators are accelerating infrastructure development.Strategic Outlook

The strategic outlook for the global CNG market remains positive, supported by ongoing transition toward cleaner fuels and hybrid mobility solutions. Future opportunities include biomethane blending, smart CNG dispensing systems, AI-based fleet optimization, and integration with hydrogen-ready infrastructure. Despite growing electrification trends, CNG is expected to remain a key transitional fuel in heavy-duty and cost-sensitive transportation segments. Companies investing in infrastructure expansion, fuel efficiency technologies, and integrated energy solutions are expected to strengthen competitive positioning.Final Market Perspective

The global CNG market continues to play a crucial role in the transition toward cleaner and more sustainable transportation systems worldwide. Rising environmental concerns, supportive policies, and cost advantages will continue to drive steady market growth throughout the forecast period. Organizations that successfully combine infrastructure scale, fuel innovation, and strategic partnerships will remain strongly positioned in the evolving global CNG market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Compressed Natural Gas (CNG) Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Compressed Natural Gas (CNG)

- 2.2 Scope of the Study

- 2.3 Evolution of Alternative Fuel Technologies

- 2.4 CNG Value Chain & Ecosystem Analysis

- 2.5 Regulatory & Environmental Compliance Landscape

- 2.6 Clean Mobility Transition Trends

- 2.7 Technology Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Demand for Cleaner Transportation Fuels

- 4.1.2 Government Policies and Incentives

- 4.1.3 Expansion of CNG Refueling Infrastructure

- 4.1.4 Cost Efficiency Compared to Conventional Fuels

- 4.1.5 Growing Adoption in Public Transportation Fleets

- 4.2 Restraints

- 4.2.1 High Initial Infrastructure Investment

- 4.2.2 Limited Refueling Accessibility in Rural Areas

- 4.2.3 Vehicle Conversion Costs

- 4.2.4 Competition from Electric Mobility

- 4.3 Opportunities

- 4.3.1 Biomethane Blending Integration

- 4.3.2 Smart CNG Dispensing Systems

- 4.3.3 Hydrogen-Ready CNG Infrastructure

- 4.3.4 Fleet Optimization Through Digital Platforms

- 4.4 Challenges

- 4.4.1 Infrastructure Deployment Delays

- 4.4.2 Safety and Storage Challenges

- 4.4.3 Regulatory Variability Across Regions

- 4.4.4 Long-Term Energy Transition Uncertainty

- 4.1 Drivers

- 5. Global Compressed Natural Gas (CNG) Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Vehicle Adoption Analysis

- 5.5 Infrastructure Deployment Trends

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Application

- 6.1.1 Passenger Vehicles

- 6.1.2 Commercial Vehicles

- 6.1.3 Buses

- 6.1.4 Industrial Applications

- 6.2 By End User

- 6.2.1 Transportation Fleets

- 6.2.2 Logistics Companies

- 6.2.3 Public Transit Authorities

- 6.2.4 Industrial Users

- 6.3 By Component

- 6.3.1 CNG Compressors

- 6.3.2 Storage Cylinders

- 6.3.3 Dispensers

- 6.3.4 Conversion Kits

- 6.3.5 Refueling Stations

- 6.4 By Distribution Model

- 6.4.1 Public Refueling Infrastructure

- 6.4.2 Private Fleet Refueling Stations

- 6.4.3 Mobile Refueling Systems

- 6.1 By Application

- 7. Market Segmentation by Geography

- 7.1 Asia-Pacific

- 7.2 Europe

- 7.3 North America

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Infrastructure Benchmarking

- 8.3 Technology Portfolio Analysis

- 8.4 Strategic Partnerships & Collaborations

- 8.5 Fuel Innovation Strategies

- 9. Company Profiles

- 9.1 ExxonMobil Corporation

- 9.2 Chevron Corporation

- 9.3 Shell plc

- 9.4 Gazprom

- 9.5 Indian Oil Corporation

- 9.6 Bharat Petroleum Corporation Limited (BPCL)

- 9.7 Clean Energy Fuels Corp.

- 9.8 Trillium Energy Solutions

- 9.9 Landi Renzo S.p.A.

- 9.10 Westport Fuel Systems Inc.

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Clean Mobility Forecast Engine

- 10.2 Fuel Infrastructure Analytics Dashboard

- 10.3 Fleet Transition Intelligence Tracker

- 10.4 Alternative Fuel Adoption Analyzer

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Urban Refueling Infrastructure

- 11.2 Investment in Advanced Storage Technologies

- 11.3 Integration with Renewable Natural Gas Systems

- 11.4 Strengthening Fleet Conversion Programs

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Compressed Natural Gas (CNG) Market Competitive Intensity & Market Structure Overview

The global Compressed Natural Gas (CNG) market is moderately consolidated and infrastructure-intensive, characterized by strong competition among integrated energy companies, gas distribution utilities, alternative fuel technology providers, automotive fuel system manufacturers, and fueling infrastructure developers. Competitive intensity is driven by infrastructure scale, distribution network reach, fuel pricing competitiveness, storage technology innovation, and strategic partnerships across transportation ecosystems.

The market structure consists of multinational oil and gas companies, regional natural gas distributors, CNG refueling station operators, vehicle conversion technology providers, and automotive OEM partners. Competition is shaped by access to natural gas supply, station deployment capabilities, advanced storage systems, dual-fuel technology integration, and regional regulatory alignment.

Rising demand for cleaner transportation fuels, expanding government-backed infrastructure programs, and increasing adoption of low-emission mobility solutions are intensifying competition across the global CNG market.

Global Compressed Natural Gas (CNG) Market Competitive Intensity & Market Structure Current Scenario

Leading Global CNG Companies

ExxonMobil Corporation: Major global energy company with extensive natural gas production capabilities and expanding clean fuel initiatives.

Chevron Corporation: Leading integrated energy provider focused on alternative fuel investments and natural gas infrastructure development.

Shell plc: Global energy leader with strong investments in CNG fueling networks and low-carbon mobility solutions.

Gazprom: Major natural gas supplier with extensive CNG distribution capabilities and significant transportation fuel infrastructure investments.

Indian Oil Corporation: Leading South Asian energy company aggressively expanding CNG station infrastructure and urban mobility fuel networks.

Bharat Petroleum Corporation Limited (BPCL): Significant CNG infrastructure developer focused on urban and intercity fueling expansion.

Clean Energy Fuels Corp.: Specialized clean transportation fuel company with extensive CNG and renewable natural gas fueling operations.

Trillium Energy Solutions: Key alternative fuel infrastructure provider serving commercial transportation fleets.

Landi Renzo S.p.A.: Leading manufacturer of CNG conversion systems and fuel management technologies.

Westport Fuel Systems Inc.: Major provider of advanced alternative fuel engine technologies and CNG fuel system integration solutions.

Key Competitive Intensity & Market Structure Drivers

The increasing global focus on reducing transportation-related emissions is significantly intensifying competition among CNG infrastructure and fuel solution providers.

Government subsidies, regulatory incentives, and clean mobility mandates are accelerating infrastructure deployment and market expansion.

Rapid urbanization and rising commercial transportation demand are strengthening the need for scalable and efficient CNG fueling ecosystems.

Technological advancements in high-pressure storage cylinders, leak detection systems, and fast-fill dispensing infrastructure are creating strong product differentiation opportunities.

The growing role of public transport and fleet conversion programs is increasing demand for reliable and cost-efficient CNG solutions.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly investing in large-scale refueling station expansion to strengthen regional market access and competitive positioning.

Strategic partnerships between gas suppliers, automotive OEMs, and fleet operators are becoming essential for ecosystem development.

Advanced storage technology and dual-fuel system innovation are emerging as key differentiators for vehicle performance and safety enhancement.

Biomethane integration and renewable natural gas blending are creating new competitive opportunities within decarbonization-focused transportation markets.

Digital fleet management, AI-based fuel optimization, and smart dispensing systems are enhancing operational efficiency and customer retention.

Global Compressed Natural Gas (CNG) Market Competitive Intensity & Market Structure Forward Outlook

The global CNG market is expected to remain highly competitive as governments and fleet operators continue transitioning toward cleaner fuel alternatives.

Future competition will increasingly focus on renewable natural gas integration, smart fueling infrastructure, hybrid fuel system compatibility, and digital mobility ecosystem connectivity.

Asia-Pacific is expected to remain the dominant competitive region due to aggressive infrastructure expansion and strong policy support.

Advancements in lightweight storage systems, hydrogen-compatible fueling infrastructure, and intelligent energy management platforms are expected to reshape market dynamics.

Overall, companies that successfully combine infrastructure scale, technological innovation, fuel supply reliability, and strategic ecosystem partnerships will remain strongly positioned in the evolving global Compressed Natural Gas (CNG) market.

Value Chain

Global Compressed Natural Gas (CNG) Market Value Chain & Supply Chain Evolution Overview

The global Compressed Natural Gas (CNG) market value chain is undergoing significant transformation as clean mobility initiatives, natural gas infrastructure expansion, alternative fuel adoption, and transportation decarbonization strategies reshape the broader global energy ecosystem. CNG has emerged as a critical transitional fuel that supports lower-emission transportation while offering cost-effective energy solutions for passenger vehicles, commercial fleets, public transportation systems, and industrial mobility applications.

The CNG market value chain spans natural gas extraction, processing and purification, compression infrastructure development, high-pressure storage system manufacturing, fueling station deployment, vehicle conversion technologies, distribution network integration, fleet deployment, and long-term energy optimization services. This interconnected ecosystem includes upstream gas producers, midstream transmission operators, compression equipment manufacturers, storage cylinder developers, fueling infrastructure providers, automotive OEMs, fleet operators, public transportation authorities, and downstream service providers.

Major companies including ExxonMobil Corporation, Chevron Corporation, Shell plc, Gazprom, Indian Oil Corporation, Bharat Petroleum Corporation Limited (BPCL), Trillium Energy Solutions, Clean Energy Fuels Corp., Landi Renzo S.p.A., and Westport Fuel Systems Inc. are actively investing in fueling infrastructure expansion, advanced storage systems, dual-fuel powertrain innovation, digital fleet optimization, and integrated clean fuel distribution platforms to strengthen market leadership.

Upstream supply chain activities depend on natural gas extraction, purification, transmission pipelines, gas treatment systems, and regional feedstock distribution infrastructure. Midstream operations focus on gas compression, cylinder manufacturing, refueling station construction, equipment assembly, pressure regulation systems, safety testing, and network integration. Downstream activities include fuel dispensing, vehicle conversion and deployment, fleet operations management, station maintenance, digital monitoring, and long-term energy efficiency optimization.

Operational priorities across the CNG value chain increasingly emphasize fuel accessibility, pressure system safety, storage efficiency, distribution reliability, station network scalability, leak prevention, digital monitoring, and lifecycle operational efficiency. However, the market continues to face challenges related to infrastructure capital requirements, station accessibility limitations, natural gas price volatility, regulatory complexity, and long-term competition from electrification technologies.

Global Compressed Natural Gas (CNG) Market Value Chain & Supply Chain Evolution Current Scenario

The current CNG market is being shaped by rising urban air quality concerns, supportive government clean fuel policies, increasing commercial fleet adoption, and expanding natural gas distribution infrastructure. Transportation operators are increasingly adopting CNG as a cost-efficient lower-emission fuel alternative to gasoline and diesel.

Asia-Pacific currently dominates the global CNG market due to strong policy support, extensive refueling infrastructure development, large transportation demand, and significant adoption across public mobility systems. India, China, and Pakistan remain the leading regional markets.

Europe maintains a strong market position supported by emission reduction targets, mature natural gas distribution systems, and established CNG vehicle ecosystems. North America continues to expand through commercial fleet and waste management vehicle adoption.

Commercial vehicles and public transport buses remain the dominant application segments due to high fuel consumption intensity and strong cost-efficiency advantages.

Fleet operators are increasingly integrating digital fuel management systems and predictive maintenance platforms to optimize operational performance across CNG-powered transportation networks.

Key Value Chain & Supply Chain Evolution Signals in Global Compressed Natural Gas (CNG) Market

One of the most significant transformation signals is the rapid expansion of CNG refueling infrastructure. Governments and private energy operators are increasingly investing in fast-fill and high-capacity station networks to improve accessibility.

Advanced high-pressure cylinder technologies are significantly improving storage efficiency, reducing vehicle weight, and enhancing operational safety.

Dual-fuel and bi-fuel engine technologies are becoming increasingly important, enabling operational flexibility and smoother integration into mixed-fuel transportation ecosystems.

Digital station monitoring and smart dispensing systems are emerging as critical innovations for improving operational efficiency, safety management, and predictive maintenance capabilities.

Biomethane integration is becoming a major strategic evolution signal, enabling lower-carbon fuel pathways and stronger alignment with long-term decarbonization targets.

Hydrogen-ready gas infrastructure development is emerging as an important long-term investment trend across advanced CNG distribution networks.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Compressed Natural Gas (CNG) Market

Leading CNG market participants are increasingly prioritizing infrastructure scale, digital fuel management, advanced storage innovation, and integrated mobility partnerships to maintain competitive advantage. Competitive differentiation increasingly depends on fueling accessibility, network reliability, operational efficiency, and lifecycle service integration.

Companies capable of delivering integrated end-to-end CNG ecosystems combining fuel production, station deployment, vehicle conversion technologies, and digital fleet optimization are expected to capture premium market opportunities.

Strategic collaborations between gas producers, infrastructure developers, vehicle manufacturers, municipal transit authorities, and commercial fleet operators are becoming essential for accelerating market penetration.

Fleet-as-a-service and fuel supply agreement models are emerging as important recurring revenue structures that improve long-term customer retention.

Digital fuel analytics and predictive maintenance capabilities are becoming increasingly important strategic differentiators as fleet operators seek operational intelligence and efficiency optimization.

Manufacturers and fuel providers are increasingly localizing refueling infrastructure near major transport corridors and logistics hubs to improve service density and strengthen regional market competitiveness.

Global Compressed Natural Gas (CNG) Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the CNG value chain is expected to become more digitally integrated, sustainability-oriented, and increasingly connected to broader clean fuel ecosystems. CNG will continue evolving as a critical transitional energy platform supporting transportation decarbonization.

Advanced compression and dispensing technologies will continue improving station efficiency, reducing operational costs, and enhancing fueling speed.

Biomethane blending and renewable natural gas integration will become increasingly central to future CNG infrastructure development.

AI-powered fleet optimization systems will enable real-time fuel consumption monitoring, route optimization, and predictive maintenance across CNG vehicle fleets.

Hydrogen-compatible infrastructure pathways will create future interoperability opportunities between CNG and emerging hydrogen mobility ecosystems.

Distributed fueling station intelligence platforms will enable centralized monitoring, automated maintenance scheduling, and network-wide operational optimization.

Ultimately, the future CNG value chain will evolve into a highly connected, digitally optimized, and lower-carbon transitional mobility ecosystem capable of supporting cleaner transportation infrastructure across both developed and emerging global markets.

Market-Specific Value Chain

- Natural Gas Extraction & Processing: Gas production, purification, treatment, transmission, and feedstock preparation for compression and distribution.

- Compression Infrastructure & Equipment Manufacturing: Compressor systems, pressure regulation technologies, storage cylinder manufacturing, dispensing hardware, and fueling station engineering.

- Station Deployment & Network Integration: Refueling station construction, pipeline connectivity, digital monitoring integration, safety system deployment, and regional network expansion.

- Vehicle Conversion & Fleet Deployment: CNG vehicle manufacturing, dual-fuel system integration, conversion kit installation, fleet onboarding, and operational deployment.

- Fuel Distribution & Operational Optimization: Fuel dispensing, station management, digital analytics, predictive maintenance, and fleet performance monitoring.

- Long-Term Clean Mobility Integration: Renewable gas blending, AI fleet intelligence, hydrogen-ready infrastructure adaptation, and low-carbon transportation optimization.

Company-to-Stage Mapping

- Natural Gas Extraction & Processing: ExxonMobil Corporation, Chevron Corporation, Shell plc, Gazprom.

- Compression Infrastructure & Equipment Manufacturing: Landi Renzo S.p.A., Westport Fuel Systems Inc., CNG equipment engineering providers.

- Station Deployment & Network Integration: Indian Oil Corporation, Bharat Petroleum Corporation Limited (BPCL), Trillium Energy Solutions.

- Vehicle Conversion & Fleet Deployment: Automotive OEM partners, fleet conversion technology providers.

- Fuel Distribution & Operational Optimization: Clean Energy Fuels Corp., commercial fueling network operators.

- Long-Term Clean Mobility Integration: Renewable natural gas platform developers, smart mobility infrastructure innovators, integrated alternative fuel ecosystem providers.

Investment Activity

Global Compressed Natural Gas (CNG) Market Investment & Funding Dynamics Overview

The global Compressed Natural Gas (CNG) market is witnessing steady investment growth driven by rising demand for cleaner transportation fuels, expanding natural gas distribution infrastructure, supportive regulatory frameworks, and increasing focus on low-emission mobility solutions. Between 2026 and 2033, capital allocation is expected to accelerate across CNG refueling networks, advanced storage systems, compression technologies, and dual-fuel vehicle conversion infrastructure.

The CNG market represents a strategically important segment within the broader clean mobility, alternative fuels, and energy transition ecosystem. Energy companies, infrastructure investors, institutional funds, transportation-focused private equity firms, and public-sector development agencies are actively increasing investments to strengthen CNG distribution capabilities and support fleet-level adoption.

A major structural investment trend is the expansion of integrated CNG mobility ecosystems combining refueling stations, pipeline connectivity, fleet conversion services, and smart fuel management systems. This transition is driving capital deployment toward scalable fueling infrastructure and advanced gas compression technologies.

Growing convergence between CNG infrastructure, smart mobility systems, biomethane integration, and hybrid transportation solutions is creating broader cross-sector investment opportunities.

Current Investment & Funding Landscape

- Asia-Pacific: Leads global investment activity due to large-scale CNG infrastructure expansion and strong public transportation conversion programs.

- North America: Strong investment focus on commercial fleet fueling infrastructure and heavy-duty transportation applications.

- Europe: Attracting investments through clean mobility policies and alternative fuel infrastructure deployment.

- Latin America: Continued investment growth supported by mature vehicle conversion ecosystems.

- Middle East & Africa: Emerging investments focused on domestic gas utilization and transport modernization.

Key Investment Drivers

- Rising global focus on low-emission transportation fuels.

- Increasing government incentives and infrastructure subsidies.

- Expansion of urban public transportation modernization programs.

- Cost advantages over gasoline and diesel for fleet operators.

- Growing investments in natural gas distribution networks.

- Increasing commercial fleet conversion initiatives.

- Integration of biomethane and renewable gas solutions.

- Rising pressure to reduce urban air pollution.

Strategic Investment Areas

- CNG Refueling Infrastructure: Expansion of urban and highway fueling station networks.

- Compression Technologies: High-efficiency compressors and fast-fill dispensing systems.

- Storage Solutions: Lightweight high-pressure composite storage cylinders.

- Vehicle Conversion Technologies: Advanced dual-fuel and dedicated CNG conversion systems.

- Fleet Management Platforms: Digital monitoring and fuel optimization systems.

- Renewable CNG Integration: Biomethane blending and renewable gas infrastructure.

Strategic Investment Implications

- Infrastructure scale remains a major determinant of investor confidence.

- Regions with strong regulatory incentives attract higher long-term capital inflows.

- Fleet conversion partnerships significantly improve commercial viability.

- Technology advancements in storage and dispensing improve return-on-investment potential.

- Renewable gas compatibility is becoming an important valuation factor.

- Public-private partnerships are accelerating infrastructure deployment timelines.

Forward Investment Outlook

The global CNG market is expected to remain a stable investment segment throughout the forecast period as governments and private operators continue expanding alternative fuel ecosystems.

Future funding activity is likely to prioritize smart refueling networks, renewable CNG integration, AI-enabled fuel optimization systems, and large-scale commercial fleet transition programs.

- Asia-Pacific: Will continue dominating capital inflows through large-scale infrastructure expansion.

- North America: Will focus on commercial transport and heavy-duty fleet modernization.

- Europe: Will maintain investment through low-carbon mobility initiatives.

- Emerging Markets: Will attract strategic investment through natural gas monetization programs.

Overall, the CNG market remains a resilient investment opportunity positioned at the intersection of clean mobility, energy transition, and cost-efficient transportation infrastructure development.

Technology & Innovation

Global Compressed Natural Gas (CNG) Market Technology & Innovation Landscape Overview

The Global Compressed Natural Gas (CNG) Market is undergoing significant technological transformation driven by advancements in high-pressure storage systems, smart refueling infrastructure, fuel system integration technologies, and digital monitoring solutions. Innovation is increasingly focused on improving fuel storage efficiency, enhancing vehicle performance, strengthening operational safety, and enabling more intelligent natural gas distribution networks.

Modern CNG technologies are evolving toward highly efficient and digitally connected clean fuel ecosystems capable of supporting advanced transportation requirements, real-time infrastructure monitoring, and optimized fleet fuel management. These innovations are improving fuel accessibility, lowering operational costs, and accelerating adoption across commercial transportation and public transit systems.

The integration of IoT-enabled fueling stations, advanced composite storage cylinders, AI-driven fleet optimization, and leak detection systems is reshaping the CNG market by enhancing operational reliability, safety, and scalability across global clean mobility networks.

Global Compressed Natural Gas (CNG) Market Technology & Innovation Current Scenario

Currently, the CNG market is witnessing strong innovation through the development of lightweight high-pressure composite storage cylinders that improve vehicle range, safety performance, and fuel efficiency while reducing overall system weight.

Fast-fill and smart dispensing technologies are increasingly being deployed at CNG refueling stations to reduce refueling times and improve station throughput for commercial fleet operators.

Dual-fuel engine systems are gaining significant traction as they provide operational flexibility by enabling seamless switching between CNG and conventional fuels based on performance requirements and fuel availability.

IoT-connected fueling infrastructure is improving operational visibility through real-time monitoring of dispenser performance, fuel pressure, system diagnostics, and predictive maintenance scheduling.

Advanced leak detection and pressure monitoring technologies are being integrated into storage and dispensing systems to strengthen safety standards and improve infrastructure reliability.

Additionally, digital fleet management platforms are increasingly being adopted to optimize fuel consumption patterns, route efficiency, and overall CNG vehicle operational performance.

Key Technology & Innovation Trends in Global Compressed Natural Gas (CNG) Market

- Lightweight Composite Storage Cylinders: Advanced materials improving fuel storage efficiency and vehicle range.

- Fast-Fill Refueling Systems: High-speed dispensing technologies reducing vehicle downtime.

- Dual-Fuel Engine Integration: Flexible fuel systems enabling seamless fuel source switching.

- IoT-Connected Refueling Infrastructure: Real-time station monitoring and operational analytics.

- Smart Leak Detection Systems: Advanced safety monitoring for fuel containment integrity.

- AI-Based Fleet Optimization: Intelligent fuel consumption and route management solutions.

- Predictive Maintenance Analytics: Data-driven diagnostics improving station and vehicle uptime.

- Digital Payment & Fuel Management Platforms: Connected transaction and consumption monitoring systems.

- Biomethane Blending Technologies: Renewable natural gas integration supporting decarbonization goals.

- Hydrogen-Ready Infrastructure Development: Future-proof fueling systems supporting multi-fuel transition strategies.

Strategic Implications of Technology & Innovation

Technological innovation is significantly reshaping competitive dynamics in the CNG market by shifting competition toward infrastructure intelligence, fuel system efficiency, operational safety, and integrated clean mobility solutions.

Companies investing in smart refueling systems, advanced storage technologies, and digital fleet optimization platforms are achieving stronger differentiation through improved fuel accessibility, reduced operational costs, and enhanced customer reliability.

The integration of digital monitoring and predictive analytics is enabling operators to optimize infrastructure utilization, reduce maintenance disruptions, and improve fuel distribution efficiency.

Biomethane compatibility and hydrogen-ready infrastructure are creating strategic opportunities for long-term energy transition positioning.

However, challenges including high infrastructure deployment costs, storage system complexity, regulatory compliance requirements, and competition from battery electric mobility remain significant barriers to broader market expansion.

Global Compressed Natural Gas (CNG) Market Technology & Innovation Forward Outlook

Looking ahead, the CNG market is expected to evolve toward highly intelligent, digitally integrated, and multi-fuel-ready clean energy ecosystems capable of supporting advanced transportation decarbonization strategies.

Future innovation is likely to focus on next-generation ultra-light composite tanks, AI-powered fueling network optimization, and autonomous fueling station management systems.

The integration of renewable biomethane and synthetic natural gas is expected to strengthen CNG???s role in low-carbon transportation systems.

Advanced digital twin technologies may enable virtual infrastructure modeling for predictive operational planning and system performance optimization.

Hydrogen-CNG hybrid fueling systems are also expected to emerge as an important transitional innovation supporting future clean mobility convergence.

Overall, the Global Compressed Natural Gas (CNG) Market is entering a new era of clean fuel innovation characterized by intelligent infrastructure, enhanced storage efficiency, digital operational intelligence, and renewable gas integration, positioning the market for sustained technological advancement and long-term strategic relevance.

Market Risk

Global Compressed Natural Gas (CNG) Market Risk Factors & Disruption Threats Overview

The global Compressed Natural Gas (CNG) market is experiencing steady growth driven by rising demand for cleaner transportation fuels, supportive regulatory frameworks, expanding refueling infrastructure, and increasing adoption across commercial and public transportation fleets. Despite favorable long-term market fundamentals, the industry faces several risks and disruption threats related to infrastructure limitations, natural gas price volatility, policy shifts, competing low-emission technologies, safety concerns, and supply chain dependencies.

One of the most significant risks impacting the CNG market is the capital-intensive nature of refueling infrastructure development. Establishing widespread CNG distribution networks requires substantial investment in compression systems, storage facilities, pipeline connectivity, and dispensing stations, which can delay adoption in underdeveloped regions.

Natural gas price volatility represents another major challenge. Fluctuations in global natural gas supply, geopolitical instability, and regional energy market imbalances can affect fuel pricing competitiveness relative to gasoline, diesel, and emerging electric mobility solutions.

Policy and regulatory uncertainty also pose significant risks. While many governments currently support CNG adoption through incentives and infrastructure programs, changing decarbonization priorities favoring full electrification may reduce long-term policy support.

Competition from battery electric vehicles (BEVs), hydrogen fuel cell technologies, and renewable biofuels is intensifying across both passenger and commercial transport segments.

Safety concerns associated with high-pressure storage systems, leak risks, and refueling infrastructure reliability remain critical operational considerations.

Additionally, supply chain disruptions affecting compressors, cylinders, valves, conversion kits, and high-pressure storage components may constrain infrastructure expansion.

Global Compressed Natural Gas (CNG) Market Risk Factors & Disruption Threats Current Scenario

The current CNG market is benefiting from strong deployment across emerging economies where cost-efficient fuel alternatives are essential for reducing transportation expenses and urban emissions.

However, the pace of infrastructure development remains uneven across regions, limiting adoption in areas with inadequate refueling accessibility.

Natural gas market volatility driven by geopolitical events and energy supply constraints has created pricing uncertainty for operators and fleet owners.

Automotive OEMs are increasingly balancing investment between CNG technologies and electrification strategies, creating potential long-term uncertainty for product development.

Urban clean mobility programs continue to support CNG buses and public fleets, though electrification mandates may gradually intensify competitive pressure.

Technological improvements in cylinder safety, fast-fill systems, and smart monitoring solutions are helping mitigate operational risks.

Global Compressed Natural Gas (CNG) Market Key Risk Factors & Disruption Threat Signals

- Infrastructure Development Delays: Slow expansion of refueling stations limiting vehicle adoption.

- Natural Gas Price Volatility: Supply-demand fluctuations affecting fuel cost competitiveness.

- Regulatory Policy Shifts: Transition toward EV-focused clean mobility strategies reducing support for CNG.

- Competition from Electric Vehicles: Accelerating electrification impacting long-term CNG demand.

- Safety and Leak Risks: Operational concerns related to high-pressure storage systems.

- Supply Chain Constraints: Delays in sourcing cylinders, compressors, and dispensing components.

- Technology Obsolescence Risk: Rapid evolution of alternative fuel technologies.

- Consumer Adoption Challenges: Limited awareness and range concerns in certain markets.

- Pipeline Dependency Risks: Distribution vulnerability linked to gas transmission infrastructure.

- Geopolitical Energy Disruptions: Regional instability affecting natural gas availability.

Strategic Implications of Risk Factors

CNG market participants must prioritize accelerated infrastructure deployment through public-private partnerships and integrated fueling ecosystem development.

Investment in advanced leak detection, storage safety enhancements, and digital refueling monitoring systems will be essential to improve reliability and consumer confidence.

Diversifying supply through biomethane integration and regional gas sourcing strategies can help mitigate fuel price volatility.

Manufacturers and fuel providers should position CNG as a transitional low-emission solution, particularly for heavy-duty transport and commercial fleet applications where electrification remains economically challenging.

Strategic alignment with municipal transit authorities, logistics operators, and industrial fleet managers will strengthen market resilience.

Global Compressed Natural Gas (CNG) Market Forward Risk Outlook

Looking ahead to 2026???2033, the CNG market will continue to play an important transitional role in clean mobility ecosystems, particularly across cost-sensitive and infrastructure-constrained markets.

Future disruption is likely to emerge from rapid EV infrastructure expansion, hydrogen mobility commercialization, renewable gas integration, and digitalized smart fueling systems.

Companies unable to adapt to shifting policy priorities and evolving low-carbon transport technologies may face declining competitiveness.

The strongest opportunities will emerge for organizations developing integrated CNG-biomethane solutions, intelligent refueling infrastructure, and fleet optimization technologies.

Overall, long-term market leadership will depend on infrastructure scalability, fuel diversification, operational safety, and strategic adaptability within evolving global transportation decarbonization frameworks.

Global Compressed Natural Gas (CNG) Market Risk Factors & Disruption Threats Overview

The global Compressed Natural Gas (CNG) market is experiencing steady growth driven by rising demand for cleaner transportation fuels, supportive regulatory frameworks, expanding refueling infrastructure, and increasing adoption across commercial and public transportation fleets. Despite favorable long-term market fundamentals, the industry faces several risks and disruption threats related to infrastructure limitations, natural gas price volatility, policy shifts, competing low-emission technologies, safety concerns, and supply chain dependencies.

One of the most significant risks impacting the CNG market is the capital-intensive nature of refueling infrastructure development. Establishing widespread CNG distribution networks requires substantial investment in compression systems, storage facilities, pipeline connectivity, and dispensing stations, which can delay adoption in underdeveloped regions.

Natural gas price volatility represents another major challenge. Fluctuations in global natural gas supply, geopolitical instability, and regional energy market imbalances can affect fuel pricing competitiveness relative to gasoline, diesel, and emerging electric mobility solutions.

Policy and regulatory uncertainty also pose significant risks. While many governments currently support CNG adoption through incentives and infrastructure programs, changing decarbonization priorities favoring full electrification may reduce long-term policy support.

Competition from battery electric vehicles (BEVs), hydrogen fuel cell technologies, and renewable biofuels is intensifying across both passenger and commercial transport segments.

Safety concerns associated with high-pressure storage systems, leak risks, and refueling infrastructure reliability remain critical operational considerations.

Additionally, supply chain disruptions affecting compressors, cylinders, valves, conversion kits, and high-pressure storage components may constrain infrastructure expansion.

Global Compressed Natural Gas (CNG) Market Risk Factors & Disruption Threats Current Scenario

The current CNG market is benefiting from strong deployment across emerging economies where cost-efficient fuel alternatives are essential for reducing transportation expenses and urban emissions.

However, the pace of infrastructure development remains uneven across regions, limiting adoption in areas with inadequate refueling accessibility.

Natural gas market volatility driven by geopolitical events and energy supply constraints has created pricing uncertainty for operators and fleet owners.

Automotive OEMs are increasingly balancing investment between CNG technologies and electrification strategies, creating potential long-term uncertainty for product development.

Urban clean mobility programs continue to support CNG buses and public fleets, though electrification mandates may gradually intensify competitive pressure.

Technological improvements in cylinder safety, fast-fill systems, and smart monitoring solutions are helping mitigate operational risks.

Global Compressed Natural Gas (CNG) Market Key Risk Factors & Disruption Threat Signals

- Infrastructure Development Delays: Slow expansion of refueling stations limiting vehicle adoption.

- Natural Gas Price Volatility: Supply-demand fluctuations affecting fuel cost competitiveness.

- Regulatory Policy Shifts: Transition toward EV-focused clean mobility strategies reducing support for CNG.

- Competition from Electric Vehicles: Accelerating electrification impacting long-term CNG demand.

- Safety and Leak Risks: Operational concerns related to high-pressure storage systems.

- Supply Chain Constraints: Delays in sourcing cylinders, compressors, and dispensing components.

- Technology Obsolescence Risk: Rapid evolution of alternative fuel technologies.

- Consumer Adoption Challenges: Limited awareness and range concerns in certain markets.

- Pipeline Dependency Risks: Distribution vulnerability linked to gas transmission infrastructure.

- Geopolitical Energy Disruptions: Regional instability affecting natural gas availability.

Strategic Implications of Risk Factors

CNG market participants must prioritize accelerated infrastructure deployment through public-private partnerships and integrated fueling ecosystem development.

Investment in advanced leak detection, storage safety enhancements, and digital refueling monitoring systems will be essential to improve reliability and consumer confidence.

Diversifying supply through biomethane integration and regional gas sourcing strategies can help mitigate fuel price volatility.

Manufacturers and fuel providers should position CNG as a transitional low-emission solution, particularly for heavy-duty transport and commercial fleet applications where electrification remains economically challenging.

Strategic alignment with municipal transit authorities, logistics operators, and industrial fleet managers will strengthen market resilience.

Global Compressed Natural Gas (CNG) Market Forward Risk Outlook

Looking ahead to 2026???2033, the CNG market will continue to play an important transitional role in clean mobility ecosystems, particularly across cost-sensitive and infrastructure-constrained markets.

Future disruption is likely to emerge from rapid EV infrastructure expansion, hydrogen mobility commercialization, renewable gas integration, and digitalized smart fueling systems.

Companies unable to adapt to shifting policy priorities and evolving low-carbon transport technologies may face declining competitiveness.

The strongest opportunities will emerge for organizations developing integrated CNG-biomethane solutions, intelligent refueling infrastructure, and fleet optimization technologies.

Overall, long-term market leadership will depend on infrastructure scalability, fuel diversification, operational safety, and strategic adaptability within evolving global transportation decarbonization frameworks.

Regulatory Landscape

Global Compressed Natural Gas (CNG) Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global Compressed Natural Gas (CNG) market is shaped by clean fuel mandates, transportation emission reduction targets, natural gas infrastructure regulations, vehicle safety compliance frameworks, and energy transition policies. As governments worldwide accelerate efforts to decarbonize transportation systems, CNG is increasingly positioned as an important transitional fuel within broader low-emission mobility strategies.

Regulatory oversight for CNG spans vehicle conversion standards, refueling station licensing, storage cylinder safety certifications, natural gas distribution approvals, and environmental compliance requirements. Regulatory authorities establish technical specifications to ensure safe storage, transportation, dispensing, and usage of compressed natural gas across automotive and industrial applications.

Policy development is also being influenced by rising urban air quality concerns, carbon reduction commitments, energy security priorities, and growing integration of renewable natural gas and biomethane into national clean energy frameworks.

Global Compressed Natural Gas (CNG) Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for the CNG market is characterized by strong government support in several high-growth economies, combined with evolving technical and environmental compliance standards.

In Asia-Pacific, countries such as India, China, and Pakistan have implemented extensive policy support including subsidies for CNG vehicle conversion, infrastructure expansion programs, and preferential tax treatment for cleaner gaseous fuels.

In Europe, CNG regulation is aligned with broader clean mobility and emissions reduction directives. Policies focus on alternative fuel infrastructure deployment, stringent vehicle emission standards, and integration of renewable gas into transportation systems.

North America maintains a structured but moderate regulatory framework, with CNG deployment primarily supported through commercial fleet incentives, state-level clean transportation policies, and natural gas infrastructure development initiatives.

Latin America and the Middle East are strengthening policy frameworks to encourage CNG adoption through fuel diversification strategies, while several natural gas-producing economies are promoting domestic CNG utilization as part of broader energy optimization efforts.

Key Regulatory & Policy Framework Areas in Global CNG Market

- Vehicle Emission Regulations: Stringent transportation emission norms are encouraging the shift toward lower-emission fuels such as CNG.

- CNG Vehicle Conversion Standards: Regulatory bodies define technical safety requirements for OEM and aftermarket CNG vehicle conversion systems.

- Refueling Infrastructure Licensing: Governments regulate station construction, dispensing systems, compressor standards, and operational safety protocols.

- Storage Cylinder Safety Compliance: High-pressure storage systems are subject to strict testing, inspection, and certification requirements.

- Alternative Fuel Incentive Policies: Tax benefits, subsidies, and grants support adoption of CNG vehicles and infrastructure expansion.

- Renewable Gas Integration Policies: Emerging regulations support blending biomethane and renewable natural gas into existing CNG distribution networks.

Global CNG Market Regulatory Developments & Regional Policy Trends

In India, aggressive government initiatives including city gas distribution expansion and public transport conversion mandates are significantly strengthening the regulatory foundation for CNG adoption.

In China, national clean air initiatives and urban transportation modernization policies continue to support CNG infrastructure development, particularly in public and commercial fleet segments.

Across Europe, implementation of the Alternative Fuels Infrastructure Regulation (AFIR) is encouraging broader deployment of CNG fueling networks while integrating renewable gas mobility solutions.

In North America, state-level programs in regions such as California and Texas are promoting CNG fleet adoption through emission reduction incentives and low-carbon fuel strategies.

Emerging economies are increasingly adopting international safety and technical standards to ensure safe and scalable deployment of CNG infrastructure.

Strategic Implications of Regulatory Environment

The evolving regulatory landscape is encouraging energy providers and automotive manufacturers to invest in certified storage systems, compliant fueling infrastructure, and advanced vehicle conversion technologies.

Compliance with safety and operational standards is becoming a critical competitive requirement, particularly for infrastructure operators and component manufacturers serving regulated transportation markets.

Government incentive programs are accelerating market penetration, but long-term competitiveness increasingly depends on alignment with renewable gas integration strategies and broader decarbonization frameworks.

Regulatory support for CNG as a transitional clean fuel is strengthening opportunities for fleet operators, public transit systems, and logistics companies seeking cost-effective emission reduction solutions.

Global Compressed Natural Gas (CNG) Market Regulatory Outlook

Between 2026 and 2033, the regulatory environment for the global CNG market is expected to become increasingly integrated with national clean mobility roadmaps and low-carbon transportation policies.

Governments are likely to introduce stricter technical standards for storage, dispensing, and vehicle safety while expanding infrastructure investment support programs.

Renewable natural gas and biomethane policy frameworks are expected to play an increasingly important role in shaping the future of CNG regulation, enhancing sustainability credentials for gaseous transport fuels.

While electrification will continue to influence long-term transportation policy, CNG is expected to maintain strong regulatory relevance as a transitional fuel for heavy-duty, commercial, and cost-sensitive transportation applications.

Overall, regulatory and policy developments will remain central to market expansion, with companies aligned with compliance innovation, infrastructure readiness, and renewable fuel integration expected to achieve sustained competitive advantage.