Global Leak Detection Market Report, Size & Forecast 2026-2033

Global Leak Detection Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 3.85 Billion |

| Market Size (2033) | USD 7.24 Billion |

| CAGR (2026???2033) | 8.2% |

| Largest Segment | Pipeline Leak Detection Systems |

| Fastest Growing Segment | IoT-Enabled Smart Leak Detection Solutions |

| Leading Application | Oil & Gas Pipeline Monitoring |

| Key Growth Driver | Increasing demand for industrial safety systems and pipeline monitoring infrastructure |

| Key Technology Trends | IoT-enabled monitoring, AI-powered predictive analytics, cloud-based diagnostics, smart sensor technologies |

| Major End-Use Industries | Oil & Gas, Water Utilities, Chemical Processing, Manufacturing, Energy & Utilities |

| Key Market Opportunity | Expansion of asset integrity management and smart infrastructure monitoring systems |

| Regional Leader | North America |

| Fastest Growing Region | Asia-Pacific |

| Sustainability & Innovation Focus | Prevention of environmental hazards, reduction of resource losses, enhanced regulatory compliance, and predictive maintenance capabilities |

Global Leak Detection Market Size & Forecast

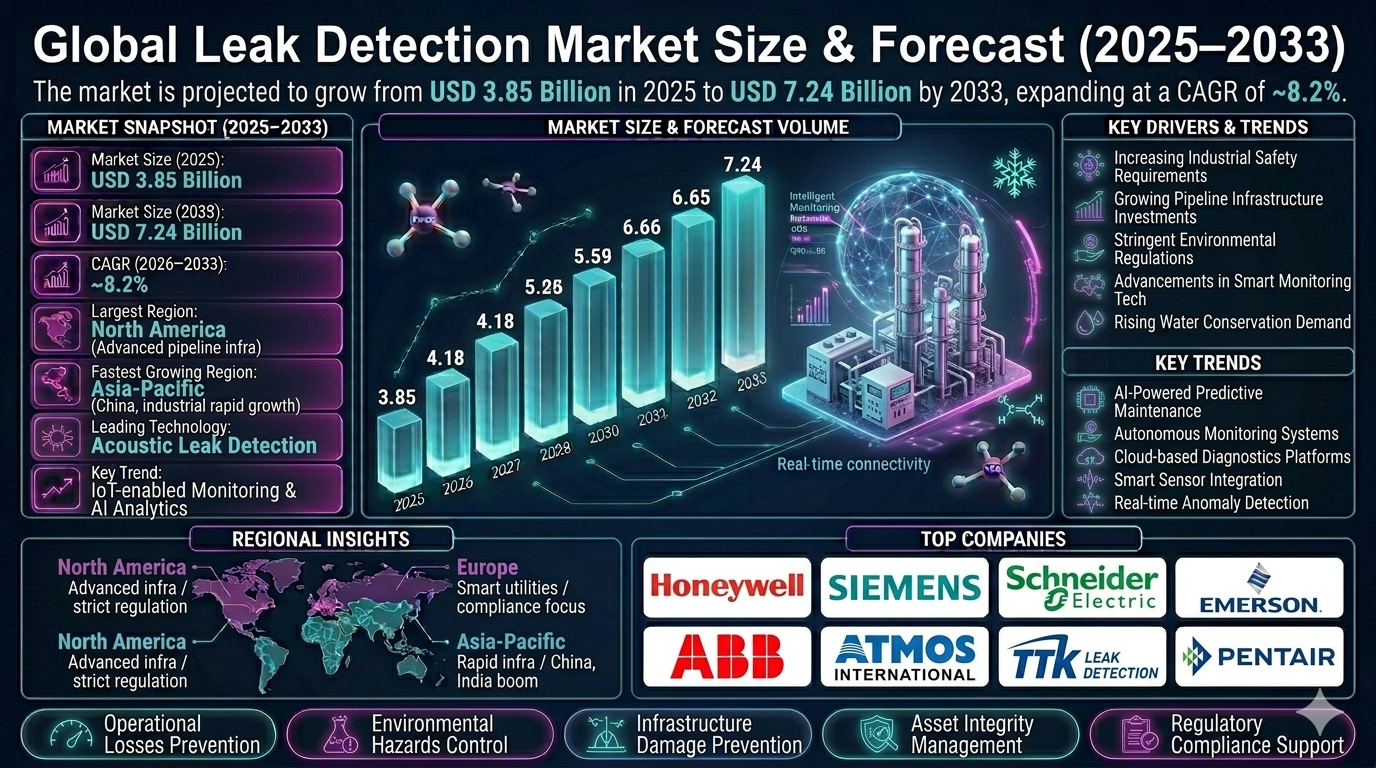

The global leak detection market is projected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 3.85 billion in 2025 and is expected to reach nearly USD 7.24 billion by 2033, expanding at a CAGR of around 8.2%. The market growth is driven by increasing demand for industrial safety systems, growing investments in pipeline monitoring infrastructure, rising environmental regulations, and the rapid adoption of advanced sensing technologies across oil & gas, water utilities, chemical processing, and manufacturing sectors. Leak detection systems are critical monitoring solutions designed to identify, locate, and report leaks in pipelines, storage tanks, processing equipment, and utility distribution systems. These systems help prevent operational losses, environmental hazards, infrastructure damage, and safety incidents. The market is undergoing rapid transformation through the integration of IoT-enabled monitoring, AI-powered predictive analytics, cloud-based diagnostics, and smart sensor technologies. Additionally, increasing focus on sustainability, asset integrity management, and regulatory compliance is accelerating market expansion globally.

Global Leak Detection Market Overview

The leak detection market forms an essential segment of the industrial monitoring, safety, and infrastructure protection industry. It supports critical operations across oil & gas pipelines, water distribution networks, chemical plants, power generation facilities, and commercial infrastructure. The market includes fixed leak detection systems, portable leak detectors, software analytics platforms, fiber optic sensing systems, acoustic leak detection technologies, and infrared monitoring solutions. Industries are increasingly adopting intelligent leak detection systems to improve operational reliability, minimize resource wastage, and reduce downtime. Technological advancements in ultrasonic sensing, thermal imaging, real-time wireless communication, and AI-driven anomaly detection are significantly improving leak detection accuracy and response times. Major market participants include Honeywell International Inc., Siemens AG, Schneider Electric, Emerson Electric Co., ABB Ltd., Atmos International, TTK Leak Detection, Pentair plc, Perma-Pipe International Holdings, and FLIR Systems.Key Drivers of Global Leak Detection Market Growth

Increasing Industrial Safety Requirements

Industries are prioritizing leak detection systems to enhance worker safety, reduce hazardous incidents, and protect critical infrastructure. Leak prevention has become a strategic necessity across high-risk industrial environments.Growing Pipeline Infrastructure Investments

Expansion of oil & gas pipelines, water transmission systems, and industrial utility networks is driving demand for advanced leak detection technologies. Infrastructure modernization projects are supporting strong market growth.Stringent Environmental Regulations

Governments worldwide are implementing strict environmental compliance standards for emissions control, fluid containment, and resource conservation. These regulations are increasing adoption of automated leak monitoring systems.Advancements in Smart Monitoring Technologies

IoT connectivity, AI-powered predictive maintenance, and cloud-based diagnostics are transforming traditional leak detection into intelligent monitoring ecosystems. These technologies improve detection precision and operational efficiency.Rising Demand for Water Conservation Solutions

Water scarcity concerns are driving utilities to deploy leak detection solutions for reducing non-revenue water losses and improving distribution efficiency. This is particularly significant in urban infrastructure projects.Global Leak Detection Market Segmentation

By Technology

The market is segmented into acoustic leak detection, fiber optic sensing, ultrasonic detection, infrared thermography, mass balance systems, and vapor sensing technologies. Acoustic and fiber optic systems account for a significant market share due to high sensitivity and real-time monitoring capabilities.By Component

The market includes hardware, software, and services. Hardware dominates the market due to widespread deployment of sensors, detectors, and monitoring devices.By Application

Applications include pipelines, storage tanks, process equipment, water distribution systems, HVAC systems, and commercial infrastructure. Pipeline monitoring represents the largest application segment globally.By End User

End users include oil & gas, water & wastewater utilities, chemical processing, power generation, manufacturing, and commercial infrastructure. Oil & gas remains the dominant end-user segment due to critical safety and environmental monitoring requirements.Regional Market Dynamics

North America

North America dominates the global leak detection market due to advanced pipeline infrastructure, stringent regulatory frameworks, and widespread adoption of industrial automation technologies. The United States remains the leading contributor to regional market growth.Europe

Europe holds a significant market share supported by environmental compliance initiatives, smart infrastructure investments, and advanced industrial safety standards. Germany, the United Kingdom, and France are major regional markets.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid industrialization, expanding pipeline networks, water infrastructure modernization, and increasing investments in smart monitoring systems. China, India, Japan, and South Korea are key contributors.Middle East & Africa

The Middle East is witnessing strong growth due to expanding oil & gas production infrastructure and increasing focus on operational safety. Saudi Arabia and the UAE lead regional demand.Latin America

Latin America is gradually expanding due to pipeline modernization projects and growing industrial safety awareness. Brazil and Mexico are leading regional markets.Competitive Landscape

The global leak detection market is highly competitive and technology-driven, with established industrial automation companies and specialized monitoring solution providers competing through innovation, reliability, and service capabilities. Key players include Honeywell International Inc., Siemens AG, Schneider Electric, Emerson Electric Co., ABB Ltd., Atmos International, TTK Leak Detection, Pentair plc, Perma-Pipe International Holdings, and FLIR Systems. Companies are increasingly investing in AI-powered analytics, wireless monitoring platforms, and predictive maintenance technologies. Strategic collaborations with infrastructure operators, utilities, and industrial manufacturers are strengthening market positioning.Strategic Outlook

The strategic outlook for the global leak detection market remains highly positive due to rising infrastructure investments and increasing demand for industrial risk management solutions. Future growth opportunities include autonomous monitoring systems, digital twin integration, advanced predictive diagnostics, and smart city water management applications. Growing emphasis on sustainability, regulatory compliance, and asset optimization will continue shaping market development. Manufacturers investing in digital innovation, sensing accuracy, and integrated monitoring ecosystems are expected to strengthen competitive advantage.Final Market Perspective

The global leak detection market continues to play a critical role in industrial safety, environmental protection, and infrastructure efficiency worldwide. Rising demand for intelligent monitoring systems, regulatory compliance solutions, and predictive maintenance technologies will continue driving market growth throughout the forecast period. Organizations that successfully combine technological innovation, operational reliability, and integrated digital monitoring capabilities will remain strongly positioned in the evolving global leak detection market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Leak Detection Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Leak Detection Systems

- 2.2 Scope of the Study

- 2.3 Evolution of Leak Monitoring Technologies

- 2.4 Leak Detection Value Chain & Ecosystem

- 2.5 Regulatory & Compliance Landscape

- 2.6 Industrial Safety & Environmental Standards

- 2.7 Technology Innovation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Industrial Safety Requirements

- 4.1.2 Growing Pipeline Infrastructure Investments

- 4.1.3 Stringent Environmental Regulations

- 4.1.4 Advancements in Smart Monitoring Technologies

- 4.1.5 Rising Demand for Water Conservation Solutions

- 4.2 Restraints

- 4.2.1 High Initial Installation Costs

- 4.2.2 Integration Challenges with Legacy Infrastructure

- 4.2.3 Technical Complexity in Large-Scale Deployments

- 4.2.4 Limited Skilled Workforce Availability

- 4.3 Opportunities

- 4.3.1 IoT-Enabled Smart Leak Monitoring Systems

- 4.3.2 Digital Twin Integration for Predictive Diagnostics

- 4.3.3 Expansion in Smart City Water Infrastructure

- 4.3.4 AI-Driven Real-Time Anomaly Detection

- 4.4 Challenges

- 4.4.1 False Alarm Management

- 4.4.2 Cybersecurity Risks in Connected Monitoring Systems

- 4.4.3 Sensor Calibration & Maintenance Requirements

- 4.4.4 Data Processing & Interpretation Complexity

- 4.1 Drivers

- 5. Global Leak Detection Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Technology Adoption Trends

- 5.5 Deployment & Monitoring Analysis

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Technology

- 6.1.1 Acoustic Leak Detection

- 6.1.2 Fiber Optic Sensing

- 6.1.3 Ultrasonic Detection

- 6.1.4 Infrared Thermography

- 6.1.5 Mass Balance Systems

- 6.1.6 Vapor Sensing Technologies

- 6.2 By Component

- 6.2.1 Hardware

- 6.2.2 Software

- 6.2.3 Services

- 6.3 By Application

- 6.3.1 Pipelines

- 6.3.2 Storage Tanks

- 6.3.3 Process Equipment

- 6.3.4 Water Distribution Systems

- 6.3.5 HVAC Systems

- 6.3.6 Commercial Infrastructure

- 6.4 By End User

- 6.4.1 Oil & Gas

- 6.4.2 Water & Wastewater Utilities

- 6.4.3 Chemical Processing

- 6.4.4 Power Generation

- 6.4.5 Manufacturing

- 6.4.6 Commercial Infrastructure

- 6.1 By Technology

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Middle East & Africa

- 7.5 Latin America

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Technology Benchmarking

- 8.3 Product Portfolio Analysis

- 8.4 Strategic Partnerships & Acquisitions

- 8.5 Innovation & Digital Transformation Strategies

- 9. Company Profiles

- 9.1 Honeywell International Inc.

- 9.2 Siemens AG

- 9.3 Schneider Electric

- 9.4 Emerson Electric Co.

- 9.5 ABB Ltd.

- 9.6 Atmos International

- 9.7 TTK Leak Detection

- 9.8 Pentair plc

- 9.9 Perma-Pipe International Holdings

- 9.10 FLIR Systems

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Leak Detection Demand Forecast Engine

- 10.2 Infrastructure Risk Monitoring Analyzer

- 10.3 Predictive Maintenance Intelligence Tracker

- 10.4 Regulatory Compliance Monitoring Dashboard

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Autonomous Monitoring Systems

- 11.2 Investment in AI-Powered Diagnostics

- 11.3 Integration with Smart Infrastructure Platforms

- 11.4 Strengthening Cybersecurity in Monitoring Networks

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Leak Detection Market Competitive Intensity & Market Structure Overview

The global leak detection market is highly technology-driven and moderately consolidated, characterized by strong competition among industrial automation leaders, infrastructure monitoring specialists, sensing technology providers, and software analytics companies. Competitive intensity is shaped by technological innovation, sensing accuracy, system reliability, integration capabilities, regulatory compliance expertise, and service support networks.

The market structure includes multinational industrial automation corporations, specialized leak monitoring solution providers, pipeline integrity management firms, and emerging digital monitoring technology companies. Market participants compete through product innovation, advanced sensor deployment, AI-powered analytics, and integrated monitoring ecosystem development.

Rising industrial safety requirements, increasing infrastructure modernization projects, stricter environmental regulations, and growing adoption of intelligent asset monitoring systems are intensifying competition across the global leak detection market.

Global Leak Detection Market Competitive Intensity & Market Structure Current Scenario

Leading Leak Detection Solution Providers

Honeywell International Inc.: Global industrial technology leader offering advanced leak detection systems integrated with industrial automation and predictive maintenance platforms.

Siemens AG: Major industrial automation company providing smart leak monitoring solutions supported by digital industrial infrastructure capabilities.

Schneider Electric: Leading provider of industrial monitoring systems with strong focus on energy management and infrastructure protection technologies.

Emerson Electric Co.: Significant market participant delivering process monitoring and intelligent sensing solutions for industrial leak detection applications.

ABB Ltd.: Prominent automation company leveraging digital monitoring systems and advanced sensor technologies for infrastructure integrity management.

Atmos International: Specialized leak detection company recognized for pipeline monitoring software and real-time leak localization technologies.

TTK Leak Detection: Established provider focused on liquid leak detection systems for industrial, commercial, and data center applications.

Pentair plc: Major industrial solutions provider offering fluid management and leak detection technologies across infrastructure sectors.

Perma-Pipe International Holdings: Specialized infrastructure monitoring company focused on pipeline leak detection and containment systems.

FLIR Systems: Technology-driven company offering thermal imaging and infrared monitoring solutions for advanced leak detection applications.

Key Competitive Intensity & Market Structure Drivers

Increasing regulatory pressure regarding environmental protection, emissions control, and industrial safety compliance is driving demand for advanced leak detection technologies.

Rapid expansion of oil & gas pipelines, water utility infrastructure, and industrial processing facilities is intensifying competition among solution providers.

Technological advancements in fiber optic sensing, acoustic monitoring, thermal imaging, and AI-based anomaly detection are creating strong product differentiation opportunities.

The growing adoption of IoT-enabled monitoring platforms and cloud-based predictive diagnostics is accelerating market transformation toward intelligent monitoring ecosystems.

Rising focus on operational efficiency, asset integrity management, and resource conservation is encouraging end users to adopt advanced leak detection solutions.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly investing in AI-powered predictive analytics and autonomous monitoring systems to improve detection speed and reduce false alarms.

Strategic partnerships with pipeline operators, water utilities, industrial manufacturers, and infrastructure management companies are becoming essential for market expansion.

Integrated digital platforms combining leak detection, predictive maintenance, and real-time asset monitoring are emerging as critical competitive differentiators.

Cloud-based diagnostics, wireless connectivity, and remote monitoring capabilities are enabling stronger customer value propositions.

Companies are prioritizing service-based business models, including monitoring-as-a-service and predictive analytics subscriptions, to strengthen recurring revenue streams.

Global Leak Detection Market Competitive Intensity & Market Structure Forward Outlook

The global leak detection market is expected to remain highly competitive as industrial sectors increasingly prioritize infrastructure safety, operational resilience, and environmental sustainability.

Future competition will increasingly center on autonomous monitoring systems, digital twin integration, advanced predictive diagnostics, and fully connected industrial monitoring ecosystems.

Asia-Pacific and the Middle East are expected to emerge as major competitive growth regions due to expanding industrial infrastructure and rising investment in smart monitoring technologies.

Innovation in machine learning-based anomaly detection, edge computing, and real-time wireless sensing is expected to reshape future market dynamics.

Overall, companies that successfully combine sensing precision, digital intelligence, infrastructure integration, and scalable service capabilities will remain strongly positioned in the evolving global leak detection market.

Value Chain

Global Leak Detection Market Value Chain & Supply Chain Evolution Overview

The global leak detection market value chain is evolving rapidly as industries increasingly prioritize operational safety, environmental protection, infrastructure reliability, and intelligent asset monitoring across critical industrial ecosystems. Leak detection systems have become essential components of industrial safety and asset integrity management, enabling real-time identification, localization, and response to leaks across pipelines, storage tanks, utility networks, process equipment, and commercial infrastructure.

The market value chain spans sensor material development, electronics manufacturing, software platform engineering, system integration, monitoring infrastructure deployment, analytics processing, maintenance services, and end-user operational monitoring. This ecosystem connects sensing technology developers, semiconductor manufacturers, industrial automation firms, cloud platform providers, infrastructure operators, system integrators, engineering service providers, and industrial end-users.

Major companies including Honeywell International Inc., Siemens AG, Schneider Electric, Emerson Electric Co., ABB Ltd., Atmos International, TTK Leak Detection, Pentair plc, Perma-Pipe International Holdings, and FLIR Systems are continuously investing in AI-powered analytics, IoT-enabled monitoring platforms, cloud-based diagnostics, fiber optic sensing, and predictive maintenance technologies to strengthen operational efficiency and market competitiveness.

Upstream supply chain operations depend on semiconductor fabrication, advanced sensor materials, optical fiber manufacturing, thermal imaging components, embedded electronics production, and industrial communications hardware. Midstream activities focus on leak detection system assembly, software integration, cloud connectivity architecture, calibration, testing, and deployment engineering. Downstream operations include infrastructure installation, system monitoring services, maintenance support, and operational performance optimization.

Operational priorities across the leak detection value chain increasingly emphasize sensing accuracy, response speed, cybersecurity resilience, predictive intelligence, remote accessibility, regulatory compliance, and interoperability with broader industrial monitoring ecosystems. However, the market continues to face challenges related to infrastructure integration complexity, high deployment costs, legacy system compatibility, cybersecurity risks, and varying regulatory standards across regions.

Global Leak Detection Market Value Chain & Supply Chain Evolution Current Scenario

The current leak detection market is being shaped by rapid industrial automation, expanding pipeline and utility infrastructure, rising environmental compliance requirements, and increasing deployment of smart industrial monitoring systems. Industrial operators are increasingly replacing conventional manual inspection methods with intelligent automated monitoring solutions capable of continuous leak detection and predictive diagnostics.

North America currently dominates the global leak detection market due to advanced pipeline infrastructure, strong regulatory enforcement, extensive industrial automation adoption, and significant investment in infrastructure modernization. The United States remains the leading regional contributor supported by extensive oil & gas operations and smart utility deployment.

Europe maintains a strong market position driven by strict environmental regulations, sustainability initiatives, and increasing adoption of digital industrial monitoring technologies. Asia-Pacific is emerging as the fastest-growing region due to rapid industrialization, expanding water and energy infrastructure, and growing investments in smart utility systems.

Manufacturers are increasingly integrating AI-powered anomaly detection, cloud-based analytics dashboards, real-time wireless connectivity, and edge computing capabilities into leak detection platforms to improve operational responsiveness and monitoring accuracy.

Water conservation initiatives are significantly accelerating adoption of leak detection technologies across municipal water distribution systems as utilities seek to reduce non-revenue water losses and improve infrastructure efficiency.

Key Value Chain & Supply Chain Evolution Signals in Global Leak Detection Market

One of the most significant transformation signals is the rapid shift toward intelligent IoT-enabled leak monitoring ecosystems. Connected sensors and cloud-integrated platforms are enabling continuous remote monitoring and real-time operational visibility across distributed infrastructure networks.

Another major signal is the increasing integration of artificial intelligence and predictive analytics into leak detection systems. AI-powered platforms can identify abnormal operational patterns, forecast failure risks, and significantly improve proactive maintenance strategies.

The expansion of fiber optic sensing technology is also reshaping the market. Distributed fiber optic monitoring offers high sensitivity, long-distance coverage, and real-time event localization for large-scale pipeline and utility applications.

Environmental compliance requirements are becoming increasingly stringent, driving stronger adoption of automated leak monitoring solutions across industries such as oil & gas, chemicals, and water utilities.

Digital twin integration is emerging as an important market signal, allowing operators to simulate infrastructure behavior, analyze leak scenarios, and optimize maintenance planning through virtual asset modeling.

Cybersecurity is becoming a critical consideration as leak detection systems become more connected and cloud-enabled. Manufacturers are increasingly investing in secure industrial communication protocols and cyber-resilient system architectures.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Leak Detection Market

Leading market participants are increasingly prioritizing intelligent sensing innovation, digital platform integration, predictive analytics capabilities, and service-oriented monitoring models to strengthen competitive positioning. Competitive differentiation increasingly depends on system reliability, analytics sophistication, scalability, and ease of infrastructure integration.

Companies capable of delivering end-to-end intelligent monitoring ecosystems with advanced analytics and real-time decision support are expected to capture premium market opportunities as industries prioritize predictive maintenance and operational resilience.

Strategic partnerships between leak detection technology providers, industrial automation companies, cloud infrastructure firms, and engineering service providers are becoming increasingly important for expanding system interoperability and accelerating deployment across complex industrial environments.

Recurring service-based business models including remote monitoring subscriptions, predictive diagnostics platforms, and managed maintenance services are becoming central revenue drivers for leading vendors.

Sustainability-focused infrastructure modernization initiatives are creating strong opportunities for leak detection providers, particularly in water management, pipeline decarbonization, and smart city infrastructure development.

Cybersecurity investment is becoming a critical strategic requirement as industrial operators increasingly demand secure digital monitoring ecosystems capable of protecting sensitive infrastructure data.

Global Leak Detection Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the leak detection value chain is expected to become increasingly autonomous, AI-driven, and deeply integrated with broader industrial digital ecosystems. Intelligent monitoring systems will evolve beyond reactive detection toward predictive and self-optimizing operational intelligence platforms.

Advanced sensing technologies including next-generation fiber optics, nanosensors, distributed acoustic sensing, and thermal anomaly detection systems are expected to significantly improve detection precision and infrastructure coverage.

AI-driven predictive diagnostics will increasingly enable automated failure forecasting, maintenance scheduling optimization, and infrastructure health assessment across critical industrial assets.

Digital twin integration will become more widespread, enabling infrastructure operators to simulate operational behavior, assess leak propagation scenarios, and improve strategic maintenance planning.

Cloud-native monitoring platforms and edge computing architectures will continue to improve remote accessibility, data processing speed, and distributed infrastructure visibility.

Water conservation and sustainability initiatives are expected to accelerate leak detection deployment across urban utility networks, smart city infrastructure, and municipal water systems globally.

Ultimately, the future leak detection value chain will evolve into an intelligent, predictive, and highly connected industrial monitoring ecosystem capable of delivering autonomous infrastructure protection, operational optimization, and real-time asset resilience across critical global infrastructure networks.

Market-Specific Value Chain

- Sensor Components & Electronics Manufacturing: Semiconductor fabrication, optical fiber production, thermal imaging components, acoustic sensors, embedded electronics, and communication hardware.

- Detection System Engineering & Software Development: Leak detection algorithms, AI analytics platforms, cloud connectivity systems, cybersecurity integration, and digital monitoring software architecture.

- System Assembly & Industrial Integration: Device manufacturing, system calibration, testing, industrial automation integration, and infrastructure compatibility engineering.

- Infrastructure Deployment & Installation: Pipeline installation support, utility network integration, field deployment, commissioning services, and engineering implementation.

- Monitoring, Analytics & Operational Management: Real-time monitoring platforms, predictive diagnostics, remote analytics services, digital twin integration, and maintenance optimization.

- Long-Term Infrastructure Optimization: Autonomous monitoring systems, sustainability analytics, predictive asset integrity management, and continuous infrastructure resilience improvement.

Company-to-Stage Mapping

- Sensor Components & Electronics Manufacturing: Semiconductor manufacturers, fiber optic suppliers, thermal imaging component providers, industrial sensor developers.

- Detection System Engineering & Software Development: Honeywell, Siemens, Schneider Electric, Emerson Electric, ABB.

- System Assembly & Industrial Integration: Perma-Pipe International Holdings, TTK Leak Detection, industrial systems integrators.

- Infrastructure Deployment & Installation: Engineering service firms, utility contractors, industrial automation deployment specialists.

- Monitoring, Analytics & Operational Management: Atmos International, FLIR Systems, cloud analytics providers, predictive monitoring platform companies.

- Long-Term Infrastructure Optimization: AI monitoring firms, digital twin technology providers, smart infrastructure analytics companies.

Investment Activity

Global Leak Detection Market Investment & Funding Dynamics Overview

Investment activity in the global leak detection market is accelerating rapidly due to increasing industrial safety requirements, expanding pipeline infrastructure modernization programs, rising environmental compliance mandates, and growing adoption of AI-powered monitoring systems. Between 2026 and 2033, capital allocation is expected to increasingly target intelligent sensing platforms, IoT-enabled leak monitoring systems, predictive analytics software, digital twin integration, and autonomous infrastructure monitoring technologies.

The leak detection market is becoming a strategically critical segment of the industrial monitoring, safety technology, and infrastructure protection ecosystem. Industrial automation companies, utility operators, private equity firms, infrastructure investors, and industrial technology innovators are increasing funding toward advanced leak detection solutions to improve operational reliability, regulatory compliance, and asset protection.

A major structural transformation shaping investment dynamics is the transition from conventional reactive leak detection approaches toward proactive, real-time, digitally connected monitoring ecosystems. This shift is driving substantial funding into smart sensor networks, cloud-based diagnostics platforms, edge analytics systems, and AI-driven anomaly detection technologies.

The market is also benefiting from rising investments in water conservation technologies, pipeline digitalization, wireless infrastructure monitoring systems, and advanced acoustic and fiber optic sensing solutions. Growing emphasis on operational sustainability and infrastructure resilience is reshaping long-term investment priorities.

Current Investment & Funding Landscape

Current funding activity in the leak detection market is strongly supported by infrastructure modernization projects, oil & gas safety upgrades, smart water utility investments, and increasing deployment of digital industrial monitoring systems. Companies are actively investing in real-time analytics platforms, wireless leak detection devices, automated alarm systems, and integrated industrial monitoring software.

- North America: Leads global investment activity due to advanced pipeline monitoring infrastructure, stringent environmental regulations, and widespread adoption of industrial automation technologies.

- Europe: Witnessing strong funding growth supported by environmental compliance initiatives, smart utility infrastructure investments, and industrial digitalization programs.

- Asia-Pacific: Emerging as the fastest-growing investment region due to rapid industrialization, water infrastructure modernization, and large-scale pipeline network expansion.

- Middle East: Attracting significant investment driven by expanding oil & gas infrastructure, operational risk management requirements, and industrial safety modernization programs.

Key Investment & Funding Drivers

- Growing industrial safety requirements are increasing investments in advanced monitoring and early-warning leak detection systems.

- Pipeline infrastructure expansion is driving large-scale funding for real-time leak detection technologies.

- Stringent environmental regulations are accelerating investments in automated compliance monitoring solutions.

- Water conservation initiatives are supporting leak detection deployment across urban utility networks.

- Digital transformation is driving capital allocation toward IoT-connected and AI-powered monitoring platforms.

- Advancements in fiber optic and acoustic sensing technologies are creating innovation-focused funding opportunities.

- Rising asset integrity management requirements are strengthening demand for predictive diagnostics systems.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of combining sensing precision with intelligent digital analytics.

- Technology leadership in AI-based anomaly detection and predictive monitoring is becoming a major competitive differentiator.

- Integrated software-hardware leak detection ecosystems are attracting stronger institutional and strategic investment interest.

- Partnerships with utility operators, pipeline owners, and industrial automation providers are strengthening investment attractiveness.

- Companies investing in scalable wireless monitoring platforms are expected to achieve stronger market positioning.

- Regional diversification strategies remain essential for addressing varied regulatory and infrastructure modernization needs.

- Organizations integrating leak detection into broader industrial digitalization ecosystems are likely to capture greater long-term value.

Forward Investment Outlook

The global leak detection market is expected to maintain strong long-term investment momentum due to rising infrastructure protection requirements, expanding industrial automation adoption, and increasing demand for sustainable resource management solutions.

Future funding activity is expected to prioritize autonomous monitoring systems, AI-powered predictive diagnostics, digital twin-enabled infrastructure analytics, smart city water management solutions, and cloud-native industrial safety platforms.

- North America: Will remain the leading investment hub due to regulatory-driven monitoring upgrades and advanced industrial technology adoption.

- Asia-Pacific: Will strengthen its position through infrastructure modernization and expanding utility digitalization initiatives.

- Europe: Will continue emphasizing sustainability-focused leak monitoring and environmental compliance innovation.

Future innovation investments are also expected across edge-enabled monitoring systems, drone-assisted infrastructure inspection, next-generation fiber optic sensing, machine learning-based anomaly detection, and fully autonomous leak response technologies.

The convergence of industrial digitalization, environmental sustainability, and predictive infrastructure management will continue reshaping investment priorities across the leak detection market.

Overall, the market is expected to remain a highly attractive long-term infrastructure technology investment opportunity as industries increasingly prioritize operational reliability, safety, and resource efficiency worldwide.

Technology & Innovation

Leak Detection Market Technology & Innovation Landscape Overview

The global leak detection market is undergoing rapid technological transformation driven by advancements in sensor engineering, artificial intelligence, real-time monitoring systems, and industrial digitalization. The evolution of leak detection technologies is increasingly focused on improving detection accuracy, accelerating incident response, minimizing operational losses, and enabling predictive asset integrity management across critical infrastructure.

Modern leak detection technologies are integrating intelligent sensor networks, edge computing systems, and advanced analytics platforms to deliver continuous monitoring and highly accurate anomaly identification. These innovations are significantly enhancing operational reliability and environmental safety across industrial sectors.

The market is also witnessing strong adoption of IoT-enabled leak monitoring, cloud-connected diagnostics, autonomous surveillance systems, and smart infrastructure intelligence that are redefining industrial safety and resource management.

Leak Detection Market Technology & Innovation Current Scenario

Currently, leak detection innovation is centered around real-time sensing accuracy and predictive anomaly identification. Advanced acoustic and ultrasonic sensors are increasingly deployed to identify subtle pressure fluctuations and sound signatures associated with leaks in pipelines and industrial equipment.

Fiber optic sensing technology is becoming a major innovation area due to its ability to provide continuous distributed monitoring over long distances with exceptional sensitivity to temperature, vibration, and pressure variations.

Artificial intelligence and machine learning algorithms are being widely integrated into leak detection platforms to distinguish genuine leak events from operational noise, reducing false alarms and improving decision-making accuracy.

Thermal imaging and infrared detection systems are increasingly used for non-contact monitoring, enabling rapid leak visualization in hazardous or inaccessible environments.

Cloud-based analytics platforms are improving centralized monitoring by enabling remote diagnostics, predictive maintenance planning, and historical performance trend analysis across distributed infrastructure assets.

Autonomous inspection technologies such as drones and robotic crawlers are also gaining traction for inspecting large-scale pipelines, storage systems, and utility networks where manual inspection is operationally challenging.

Key Technology & Innovation Trends in Leak Detection Market

- IoT-Enabled Sensor Networks: Connected devices enabling continuous real-time infrastructure monitoring.

- AI-Powered Anomaly Detection: Machine learning systems improving leak event identification accuracy.

- Fiber Optic Distributed Sensing: Long-range monitoring with high sensitivity for temperature and pressure changes.

- Ultrasonic Leak Detection: High-frequency acoustic sensing for early leak identification.

- Infrared Thermal Imaging: Visual leak detection through thermal signature analysis.

- Edge Computing Integration: Localized processing for low-latency detection and response.

- Autonomous Inspection Robotics: Robotic crawlers and drones for infrastructure surveillance.

- Cloud-Based Diagnostic Platforms: Centralized monitoring and predictive analytics systems.

- Digital Twin Integration: Virtual asset modeling for predictive leak simulation and maintenance planning.

- Wireless Monitoring Systems: Remote communication technologies for decentralized infrastructure coverage.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the leak detection market by shifting competition from conventional reactive monitoring toward predictive and intelligent infrastructure management solutions.

Companies investing in AI-powered analytics, smart sensing systems, and autonomous inspection capabilities are achieving stronger competitive differentiation through improved accuracy, reduced downtime, and lower operational risk.

The growing integration of digital monitoring ecosystems is creating new opportunities for infrastructure operators to optimize maintenance planning, improve regulatory compliance, and reduce resource loss across industrial networks.

However, high implementation costs, legacy infrastructure integration challenges, cybersecurity concerns, and system interoperability limitations remain critical barriers to large-scale adoption of advanced leak detection technologies.

Leak Detection Market Technology & Innovation Forward Outlook

The future of leak detection technology is expected to move toward fully autonomous, predictive, and AI-orchestrated monitoring ecosystems capable of identifying risks before leaks occur.

Emerging innovations include self-learning sensor systems, AI-driven predictive failure modeling, autonomous drone-based inspection fleets, and next-generation digital twin platforms capable of simulating infrastructure degradation in real time.

Quantum sensing technologies and ultra-sensitive nanomaterial-based detectors may further enhance leak detection precision for complex industrial environments.

Integration of blockchain-secured monitoring records and decentralized industrial communication frameworks may also improve data integrity and regulatory transparency across critical infrastructure systems.

Overall, the global leak detection market is evolving toward a highly intelligent ecosystem combining advanced sensing, predictive analytics, autonomous monitoring, and digital infrastructure intelligence to redefine industrial safety and operational resilience worldwide.

Market Risk

Global Leak Detection Market Risk Factors & Disruption Threats Overview

The global leak detection market is experiencing strong growth due to rising industrial safety requirements, expanding pipeline infrastructure, stricter environmental regulations, and increasing adoption of smart monitoring technologies. Despite favorable growth prospects, the market faces several operational, technological, regulatory, and competitive risks that may influence long-term expansion and profitability.

One of the most significant risks affecting the leak detection market is high implementation and infrastructure integration costs. Advanced leak detection systems often require significant investment in sensors, network connectivity, analytics platforms, and integration with existing industrial monitoring infrastructure, which may limit adoption among cost-sensitive operators.

Technological complexity and system reliability concerns represent another major challenge. False alarms, delayed detection, calibration inaccuracies, and system incompatibility with legacy infrastructure can undermine confidence in leak detection systems and impact operational efficiency.

Cybersecurity vulnerabilities are becoming an increasing disruption threat as leak detection systems become more connected through IoT networks, cloud-based diagnostics, and remote monitoring platforms. Unauthorized access, system breaches, or data manipulation could compromise critical industrial infrastructure and operational safety.

Regulatory uncertainty also presents challenges. While stricter environmental compliance requirements generally support market growth, inconsistent regional standards and evolving certification requirements can increase compliance complexity and delay technology deployment.

Economic fluctuations and capital expenditure constraints can affect investment decisions across major end-use industries such as oil & gas, utilities, manufacturing, and chemical processing, slowing procurement cycles for advanced leak detection systems.

Additionally, supply chain disruptions affecting semiconductors, sensors, communication modules, and specialized monitoring equipment may impact product availability and pricing stability.

Global Leak Detection Market Risk Factors & Disruption Threats Current Scenario

The current leak detection market is characterized by increasing adoption of digital monitoring systems, particularly across oil & gas pipelines, water utilities, and industrial manufacturing facilities.

Demand for AI-powered predictive monitoring and real-time analytics platforms is rising as organizations prioritize proactive infrastructure management and operational risk reduction.

However, implementation challenges remain significant, especially in aging industrial infrastructure where integration with legacy systems can be costly and technically complex.

Cybersecurity concerns are intensifying as industrial operators deploy cloud-connected monitoring networks, creating new risk management priorities across the sector.

At the same time, rising component costs and supply chain volatility are creating pricing pressures for system manufacturers and slowing deployment timelines in certain regions.

Regulatory enforcement related to emissions monitoring, pipeline integrity, and water loss prevention continues to drive demand but also increases compliance requirements for technology providers.

Global Leak Detection Market Key Risk Factors & Disruption Threat Signals

- High Deployment Costs: Significant capital requirements for advanced monitoring infrastructure.

- System Reliability Issues: False alarms and inaccurate detection reducing user confidence.

- Cybersecurity Vulnerabilities: Connected monitoring systems exposed to digital threats.

- Legacy Infrastructure Integration Challenges: Technical barriers to implementation in older systems.

- Regulatory Complexity: Evolving regional compliance and certification requirements.

- Capital Spending Constraints: Economic slowdowns impacting industrial technology investments.

- Supply Chain Disruptions: Shortages of sensors, semiconductors, and communication modules.

- Technology Standardization Gaps: Lack of interoperability across platforms and vendors.

- Skilled Workforce Shortages: Limited technical expertise for deployment and maintenance.

- Competitive Pricing Pressure: Growing market competition compressing profit margins.

Strategic Implications of Risk Factors

Leak detection solution providers must prioritize system accuracy, reliability validation, and interoperability to build stronger market confidence and reduce operational adoption barriers.

Cybersecurity investment will become increasingly essential as digital monitoring platforms expand across critical infrastructure applications.

Manufacturers should focus on modular and scalable system architectures that simplify deployment across both modern and legacy industrial environments.

Strategic partnerships with industrial automation providers, utilities, and infrastructure operators can strengthen integration capabilities and improve market access.

Supply chain diversification and localized component sourcing strategies will be critical for maintaining delivery consistency and cost competitiveness.

Global Leak Detection Market Forward Risk Outlook

Looking ahead to 2026???2033, the leak detection market is expected to remain growth-oriented but increasingly shaped by digital transformation risks, cybersecurity demands, and evolving regulatory frameworks.

Autonomous monitoring systems, digital twins, AI-based anomaly detection, and predictive infrastructure analytics will continue reshaping market expectations.

However, providers that fail to address reliability, cybersecurity, and interoperability challenges may face slower adoption and reduced competitiveness.

Regions investing heavily in smart infrastructure modernization and industrial digitalization are expected to offer the strongest long-term growth opportunities.

Overall, sustained success in the leak detection market will depend on technological resilience, secure connectivity, operational precision, and adaptable deployment strategies.

Regulatory Landscape

Global Leak Detection Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global leak detection market is shaped by industrial safety regulations, environmental protection mandates, infrastructure integrity standards, hazardous material containment laws, and digital monitoring compliance frameworks. Leak detection systems are considered critical infrastructure monitoring solutions due to their role in preventing operational failures, minimizing environmental contamination, and ensuring public and workplace safety.

Governments and regulatory agencies worldwide enforce strict requirements for leak prevention, continuous monitoring, emergency response readiness, and reporting obligations across industries such as oil & gas, water utilities, chemical processing, manufacturing, and energy infrastructure. These regulations are increasingly driving the deployment of advanced leak detection technologies.

Policy priorities are also shifting toward sustainability and resource conservation, with growing regulatory emphasis on water loss reduction, methane emission control, industrial asset integrity, and smart infrastructure modernization. This is accelerating adoption of intelligent leak detection systems integrated with digital monitoring platforms.

Global Leak Detection Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for leak detection combines established industrial operational safety standards with evolving environmental compliance requirements and digital infrastructure monitoring policies. Leak detection systems are increasingly mandated for critical infrastructure assets to reduce risk exposure and improve operational accountability.

In the United States, leak detection regulations are governed by agencies including the Environmental Protection Agency (EPA), Pipeline and Hazardous Materials Safety Administration (PHMSA), Occupational Safety and Health Administration (OSHA), and state-level environmental authorities. Methane emissions monitoring, hazardous liquid pipeline integrity management, and water utility leakage reporting requirements are significant compliance drivers.

In Europe, leak detection deployment is influenced by the Industrial Emissions Directive (IED), Seveso III Directive, Water Framework Directive, and strict environmental monitoring regulations. The European Union is also actively strengthening methane leak reporting requirements for oil and gas operators.

Asia-Pacific countries including China, Japan, South Korea, and India are increasingly tightening industrial safety standards, pipeline monitoring regulations, and water conservation policies. Rapid industrialization and urban infrastructure expansion are driving stronger regulatory oversight of leak prevention technologies.

Middle Eastern and Latin American markets are increasingly aligning with international operational integrity and environmental safety standards, particularly in oil & gas pipeline infrastructure and municipal water distribution systems.

Key Regulatory & Policy Environment Signals in Global Leak Detection Market

- Pipeline Integrity Regulations: Mandatory leak monitoring, inspection intervals, and emergency response requirements are driving adoption across energy infrastructure.

- Environmental Emissions Compliance: Regulations targeting methane leaks, hazardous fluid releases, and industrial contamination are increasing demand for advanced detection systems.

- Water Conservation Policies: Governments are mandating non-revenue water reduction and distribution efficiency improvements through leak monitoring deployment.

- Industrial Safety Standards: Leak prevention and detection are central to workplace safety frameworks across chemical, manufacturing, and processing industries.

- Digital Monitoring and Reporting Requirements: Regulatory agencies increasingly require automated monitoring, real-time alerts, and digital compliance reporting.

- Smart Infrastructure Initiatives: Public policy support for smart cities and intelligent utility networks is accelerating adoption of integrated leak detection technologies.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is significantly influencing technology investments across industrial infrastructure sectors. Operators are increasingly deploying advanced leak detection platforms to ensure compliance, minimize operational disruptions, and reduce environmental liabilities.

Stringent emissions regulations are driving stronger demand for high-precision sensing technologies such as fiber optic monitoring, infrared thermography, and AI-based anomaly detection. Companies that offer compliance-ready monitoring solutions are strengthening their competitive positioning.

Water conservation regulations are accelerating municipal adoption of smart leak detection systems, creating major growth opportunities for digital monitoring solution providers focused on utility infrastructure.

The regulatory push toward digitalization is also encouraging integration of cloud-based diagnostics, predictive analytics, and automated compliance reporting tools, enabling operators to improve response times and operational transparency.

Global Leak Detection Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global leak detection market is expected to become increasingly stringent, data-driven, and sustainability-focused. Governments are likely to strengthen leak reporting obligations, tighten emissions thresholds, and mandate continuous monitoring across critical industrial infrastructure.

Methane reduction commitments, industrial decarbonization policies, and water resource protection regulations are expected to significantly expand deployment requirements for advanced leak detection technologies.

Digital compliance frameworks will likely become more prominent, with regulators requiring automated reporting, remote monitoring integration, and AI-supported anomaly detection for critical infrastructure operators.

Smart city investments and infrastructure resilience initiatives are expected to create new regulatory incentives for leak detection adoption across municipal water, district energy, and urban utility systems.

Overall, regulatory and policy developments will remain a key growth catalyst for the leak detection market, with companies investing in intelligent sensing technologies, compliance automation, and integrated digital monitoring ecosystems expected to maintain long-term competitive advantage.