Global Tyre Distribution & Retail Market Size, Share & Forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

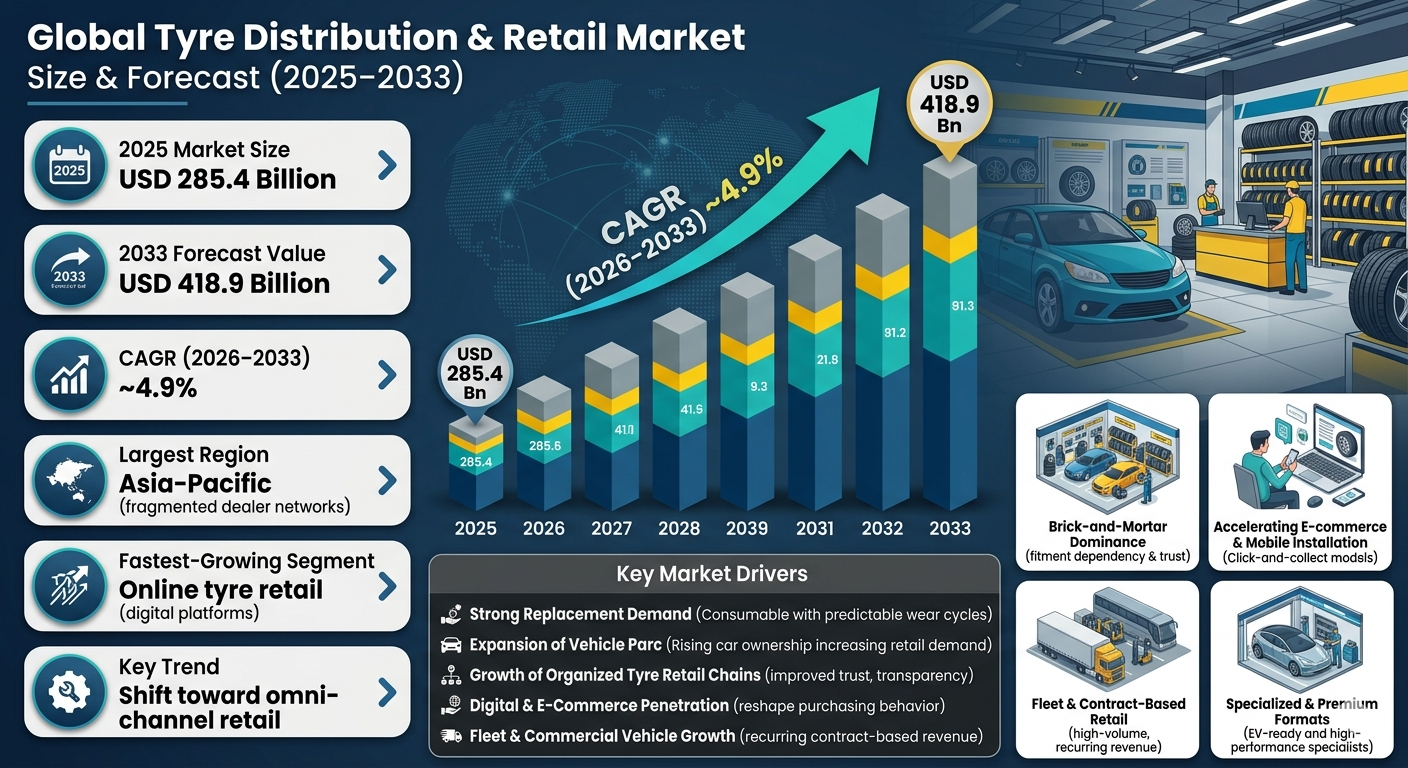

| 2025 Market Size | USD 285.4 Billion |

| 2033 Market Size | USD 418.9 Billion |

| CAGR (2026???2033) | ~4.9% |

| Largest Segment | Independent tyre dealers |

| Fastest-Growing Segment | Online tyre retail |

| Largest Region | Asia-Pacific |

| Key Trend | Shift toward omni-channel retail |

Global Tyre Distribution & Retail Market Overview

The Global Tyre Distribution & Retail Market is basically how tyres get from factories to you???through shops, dealers, online stores, and fleet services . It includes brand outlets, independent sellers, wholesalers, and even e-commerce sites, making buying tyres super convenient. This whole network keeps the automotive aftermarket running smoothly.

Tyres get replaced a lot, so the Global Tyre Distribution & Retail Market is where the real value happens . Shoppers count on retailers for stock, fitment, balancing, alignment, warranties, and after-sales help. With more cars on the road and fancy tech like EV, run-flat, and smart tyres, pro retail networks are more important than ever. Plus, online platforms and fast delivery options are making it easier to get tyres quickly, boosting customer satisfaction. Retailers who offer expert advice and service stand out in this competitive space.

According to the Pheonix Demand Forecast Engine, the Global Tyre Distribution & Retail Market size is valued at USD 285.4 billion in 2025 and is projected to reach USD 418.9 billion by 2033, expanding at a CAGR of ~4.9% during 2026???2033. Growth is driven by rising replacement demand, expansion of organized retail, and accelerating online tyre sales.

Asia-Pacific dominates the market due to massive vehicle parc and fragmented dealer networks, while Europe is the fastest-growing region due to organized retail chains, premium tyre penetration, and digital platforms.

Key Drivers of Global Tyre Distribution & Retail Market Growth

Strong Replacement Demand

Tyres are consumables with predictable wear cycles, making replacement sales the largest and most stable revenue stream.

Expansion of Vehicle Parc

Rising passenger and commercial vehicle ownership directly increases retail tyre demand.

Growth of Organized Tyre Retail Chains

Brand-owned outlets and franchise networks are driving market growth , improving customer trust, service quality, and pricing transparency.

Digital & E-Commerce Penetration

Online tyre platforms, mobile fitment services, and omnichannel models are reshaping purchasing behavior.

Fleet & Commercial Vehicle Growth

Logistics, ride-hailing, and leasing fleets rely on long-term retail and service contracts.

Global Tyre Distribution & Retail Market Segmentation

1. By Distribution Channel

1.1 Exclusive Brand Outlets

1.1.1 Manufacturer-Owned Stores

?? ?? ?? ??1.1.1.1 Flagship brand showrooms

?? ?? ?? ??1.1.1.1 Company-operated service centers

1.1.2 Authorized Brand Experience Centers

?? ?? ?? 1.1.1.1 Premium customer experience hubs

?? ?? ?? 1.1.1.1 EV-focused and smart-tyre retail outlets

1.2 Independent Tyre Dealers

1.2.1 Local Multi-Brand Retailers

?? ?? ?? 1.2.1.1?? Neighborhood tyre shops

?? ?? ?? 1.2.1.2 Single-location family-owned stores

1.2.2 Regional Dealership Networks

?? ?? ?? 1.2.2.1 Multi-city independent dealer chains

?? ?? ?? 1.2.2.2 Regional wholesale-retail hybrids

1.2.3 Service-Oriented Dealers

?? ?? ?? 1.2.3.1 Tyre + alignment specialists

?? ?? ?? 1.2.3.2 Tyre + mechanical service retailers

1.3 Franchise & Organized Retail Chains

1.3.1 National Tyre Retail Chains

?? ?? ?? 1.3.1.1 Large-format tyre supermarkets

?? ?? ?? 1.3.1.2 Multi-brand organized retail outlets

1.3.2 Authorized Franchise Partners

?? ?? ?? 1.3.2.1 Brand-franchised service centers

?? ?? ?? 1.3.2.2 OEM-backed retail franchises

1.3.3 Fleet-Focused Retail Chains

?? ?? ?? 1.3.3.1?? Dedicated fleet tyre service providers

?? ?? ?? 1.3.3.2 Contract-based commercial tyre retailers

1.4 Wholesalers & Distributors

1.4.1 Regional Bulk Distributors

?? ?? ?? 1.4.1.1 High-volume tyre distributors

?? ?? ?? 1.4.1.2 Import-export focused distributors

1.4.2 B2B Supply Channels

?? ?? ?? 1.4.2.1 Dealer-to-dealer supply

?? ?? ?? 1.4.2.2 Fleet and industrial bulk supply

1.4.3 Private Label Distributors

?? ?? ?? 1.4.3.1 Distributor-owned tyre brands

?? ?? ?? 1.4.3.2 White-label tyre supply networks

1.5 Online & E-Commerce Platforms (Fastest-Growing Segment)

1.5.1 Pure-Play Online Tyre Retailers

?? ?? ?? 1.5.1.1 Marketplace-only tyre platforms

?? ?? ?? 1.5.1.2 Direct-to-consumer tyre brands

1.5.2 Omnichannel Retailers

?? ?? ??1.5.2.1 Online ordering with offline fitment

?? ?? ??1.5.2.2 Click-and-collect tyre retail models

1.5.3 Mobile & On-Demand Fitment Platforms

?? ?? ?? 1.5.3.1 Home tyre installation services

?? ?? ?? 1.5.3.2 Fleet mobile tyre service platforms

2. By Vehicle Category

2.1 Passenger Vehicles (Largest Segment)

2.1.1 Hatchbacks

?? ?? ?? 2.1.1.1 Entry-level compact cars

?? ?? ?? 2.1.1.2 Premium compact vehicles

2.1.2 Sedans

?? ?? ?? 2.1.2.1 Mid-size sedans

?? ?? ?? 2.1.2.2 Full-size sedans

2.1.3 SUVs & Crossovers

?? ?? ??2.1.3.1 Compact SUVs

?? ?? ??2.1.3.2 Mid-size SUVs

?? ?? ??2.1.3.3 Full-size & premium SUVs

2.2 Commercial Vehicles

2.2.1 Light Commercial Vehicles (LCVs)

?? ?? ?? ??2.2.1.1 Delivery vans

?? ?? ?? ??2.2.1.2 Pickup trucks

2.2.2 Medium Commercial Vehicles

?? ?? ?? 2.2.2.1 Regional freight trucks

?? ?? ?? 2.2.2.2 Urban distribution vehicles

2.2.3 Heavy-Duty Commercial Vehicles

?? ?? ?? 2.2.3.1 Long-haul trucks

?? ?? ?? 2.2.3.2 Buses & coaches

2.3 Two-Wheelers & Three-Wheelers

2.3.1 Motorcycles

?? ?? ?? 2.3.1.1 Commuter motorcycles

?? ?? ?? 2.3.1.2 Premium & sports motorcycles

2.3.2 Scooters

?? ?? ?? 2.3.2.1 ICE scooters

?? ?? ?? 2.3.2.2 Electric scooters

2.3.3 Three-Wheelers

?? ?? ?? 2.3.3.1 Passenger auto-rickshaws

?? ?? ?? 2.3.3.2 Cargo three-wheelers

2.4 Off-the-Road (OTR) Vehicles

2.4.1 Construction Equipment

?? ?? ?? 2.4.1.1 Loaders

?? ?? ?? 2.4.1.2 Excavators

2.4.2 Mining Vehicles

?? ?? ??2.4.2.1 Dump trucks

?? ?? ??2.4.2.2 Haul trucks

2.4.3 Agricultural Machinery

?? ?? ?? 2.4.3.1 Tractors

?? ?? ?? 2.4.3.2 Harvesters

3. By Sales Type

3.1 OEM-Linked Retail

3.1.1 Dealer-Based Replacement

?? ?? ??3.1.1.1 OEM dealer tyre replacement

?? ?? ??3.1.1.2 Warranty-linked tyre sales

3.1.2 Authorized Service Centers

?? ?? 3.1.2.1 Brand-certified service outlets

?? ?? 3.1.2.2 OEM-supported multi-brand centers

3.2 Aftermarket / Replacement (Largest Segment)

3.2.1 Walk-In Retail Customers

?? ?? ?? 3.2.1.1 Individual vehicle owners

?? ?? ?? 3.2.1.2 Casual replacement buyers

3.2.2 Fleet Replacement Contracts

?? ?? ?? 3.2.2.1 Logistics & transport fleets

?? ?? ?? 3.2.2.2 Ride-hailing & leasing fleets

3.2.3 Subscription & Managed Services

?? ?? ?? 3.2.3.1 Tyre-as-a-service models

?? ?? ?? 3.2.3.2 Mileage-based replacement contracts

4. By Price Category

4.1 Economy Tyres

4.1.1 Entry-Level Budget Tyres

?? ?? ??4.1.1.1 Low-cost domestic brands

?? ?? ??4.1.1.2 Price-sensitive replacement tyres

4.2 Mid-Range Tyres

4.2.1 Balanced Performance Tyres

?? ?? ?? 4.2.1.1 Value-for-money brands

?? ?? ?? 4.2.1.2 Mass-market replacement tyres

4.3 Premium Tyres

4.3.1 High-Performance Tyres

?? ?? ?? 4.3.1.1 Sports & luxury vehicle tyres

4.3.2 EV-Ready & Smart Tyres

?? ?? ?? 4.3.2.1 Low-noise EV tyres

?? ?? ?? 4.3.2.2 Sensor-enabled tyres

5. By Retail Format

5.1 Physical / Offline Retail

Dominates due to mandatory fitment, service dependency, and strong customer trust.

5.1.1 Exclusive Brand Retail Stores

?? ?? ?? 5.1.1.1 Manufacturer-owned flagship outlets

?? ?? ?? 5.1.1.2 Brand-certified service & experience centers

5.1.2 Independent Brick-and-Mortar Retailers

?? ?? ?? 5.1.2.1 Local multi-brand tyre shops

?? ?? ?? 5.1.2.2 Family-owned neighborhood retailers

5.1.3 Franchise & Chain Retail Stores

?? ?? ?? 5.1.3.1 National organized tyre retail chains

?? ?? ?? 5.1.3.2 Authorized franchise service centers

5.1.4 Fleet Service Retail Centers

?? ?? ?? 5.1.4.1 Dedicated fleet tyre depots

?? ?? ?? 5.1.4.2 Commercial vehicle service hubs

5.2 Digital / Online Retail (Fastest-Growing Segment)

Driven by convenience, price transparency, and urban consumer adoption.

5.2.1 Pure-Play Online Tyre Platforms

?? ?? ?? 5.2.1.1 Marketplace-based tyre sellers

?? ?? ?? 5.2.1.2 Direct-to-consumer tyre brands

5.2.2 Brand-Owned E-Commerce Stores

?? ?? ?? 5.2.2.1 Manufacturer direct online sales

?? ?? ?? 5.2.2.2 Online booking with dealer fitment

5.2.3 Omnichannel Retail Models

?? ?? ?? 5.2.3.1 Click-and-collect tyre retail

?? ?? ?? 5.2.3.2 Online ordering + offline installation

5.2.4 Mobile & On-Demand Retail Services

?? ?? ?? 5.2.4.1 Home tyre installation vans

?? ?? ?? 5.2.4.2 Emergency & roadside tyre replacement

5.3 Fleet & Contract-Based Retail

High-volume, recurring revenue retail model.

5.3.1 Logistics & Transport Fleet Retail

?? ?? ?? 5.3.1.1 Truck & bus fleet tyre contracts

?? ?? ?? 5.3.1.2Long-haul commercial vehicle programs

5.3.2 Leasing & Mobility Fleet Retail

?? ?? ?? 5.3.2.1 Ride-hailing fleet tyre management

?? ?? ?? 5.3.2.2 Vehicle leasing replacement contracts

5.3.3 Subscription-Based Retail Models

?? ?? ?? 5.3.3.1 Tyre-as-a-Service (TaaS)

?? ?? ?? 5.3.3.2 Mileage-based replacement programs

5.4 Specialized & Premium Retail Formats

High-margin, niche-focused retail channels.

5.4.1 EV-Focused Tyre Retailers

?? ?? ?? 5.4.1.1 EV-only service centers

?? ?? ?? 5.4.1.2 Low-noise & efficiency-optimized tyre specialists

5.4.2 Performance & Luxury Tyre Boutiques

?? ?? ?? 5.4.2.1 Sports car and luxury vehicle tyre retailers

?? ?? ?? 5.4.2.2 High-performance fitment specialists

5.4.3 OTR & Industrial Tyre Retailers

?? ?? ?? 5.4.3.1 Mining & construction tyre specialists

?? ?? ?? 5.4.3.2 Agricultural machinery tyre dealers

6. By Geography

6.1 Asia-Pacific (Largest Region)

6.1.1 China

6.1.2 India

6.1.3 Japan

6.1.4 Southeast Asia

6.2 Europe (Fastest-Growing Region)

6.2.1 Germany

6.2.2 France

6.2.3 U.K.

6.2.4 Italy

6.3 North America

6.3.1 United States

6.3.2 Canada

6.4 Latin America

6.4.1 Brazil

6.4.2 Mexico

6.5 Middle East & Africa

6.5.1 GCC Countries

6.5.2 South Africa

Leading Companies in the Global Tyre Distribution & Retail Market

-

Goodyear Tire & Rubber Company

-

Continental AG

-

Pirelli & C. S.p.A.

-

Sumitomo Rubber Industries

-

Apollo Tyres

-

Yokohama Rubber Company

-

Les Schwab Tire Centers

-

Mavis Tire Supply

Michelin is the largest company in the Global Tyre Distribution & Retail Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Tracks vehicle parc growth, replacement cycles, and retail penetration rates.

Retail Channel Profitability Model

Analyzes margins across offline, franchise, and online tyre retail.

Omnichannel Adoption Index

Measures digital maturity and consumer shift toward online tyre buying.

Why the Tyre Distribution & Retail Market Is Critical

-

Primary revenue generator in the global tyre value chain

-

Controls customer access, brand loyalty, and pricing power

-

Critical for EV tyre adoption and advanced tyre technologies

-

Acts as the service interface between manufacturers and end users

Final Takeaway

The Global Tyre Distribution & Retail Market is a structurally resilient, replacement-driven market undergoing rapid transformation. While traditional dealers remain dominant, digital platforms, franchise chains, and fleet-focused retail models are reshaping competition. Companies that invest in omnichannel strategies, service-led differentiation, and EV-ready retail infrastructure will capture the most value through 2033.

Competitive Landscape

Global Tyre Distribution & Retail Competitive Intensity & Market Structure Overview

The Global Tyre Distribution & Retail Market is characterized by a highly fragmented yet strategically evolving competitive structure, where independent dealers currently dominate volume, while organized retail chains, franchise networks, and digital commerce platforms are reshaping long-term market dynamics. As the primary customer-facing layer of the tyre value chain, distribution and retail networks control product accessibility, replacement monetization, service quality, and brand loyalty.

The market operates through a multi-channel ecosystem comprising independent tyre dealers, exclusive brand outlets, franchise chains, wholesalers, fleet service providers, and increasingly omnichannel e-commerce platforms. While offline retail remains dominant due to fitment, balancing, and after-sales service dependency, online tyre retail is the fastest-growing segment, supported by digital purchasing behavior, price transparency, and click-to-fitment convenience.

Competitive intensity is high due to pricing competition, replacement-driven recurring demand, and increasing premiumization. Leading tyre manufacturers are strengthening direct retail ecosystems, while independent dealers continue to leverage local trust, regional accessibility, and service-led differentiation. Fleet and subscription models are also creating recurring high-value contract opportunities.

Global Tyre Distribution & Retail Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global market leader with strong retail and franchise ecosystems, premium positioning, omnichannel investments, and extensive replacement market penetration.

Bridgestone Corporation: Major global player with broad dealer networks, service-led retail infrastructure, and strong fleet-focused distribution capabilities.

Goodyear Tire & Rubber Company: Strong replacement and retail presence with growing investments in digital platforms and fleet service models.

Continental AG: Premium tyre retail participant focused on technology integration, EV tyre readiness, and organized dealer partnerships.

Pirelli & C. S.p.A.: Premium and luxury-focused retail specialist with strong performance tyre distribution in developed markets.

Sumitomo Rubber Industries: Broad regional distribution strength with growing organized retail participation.

Apollo Tyres: Expanding aftermarket and franchise-led retail footprint, particularly in emerging markets.

Les Schwab Tire Centers & Mavis Tire Supply: Strong retail-focused specialists with high customer retention through service-centric business models.

Key Competitive Intensity & Market Structure Signals in Global Tyre Distribution & Retail Market

A major structural signal is the continued dominance of independent tyre dealers, particularly across Asia-Pacific and fragmented emerging markets, where localized service, price sensitivity, and customer trust remain critical competitive advantages.

Another major market signal is the rapid rise of online tyre retail and omnichannel strategies. Consumers increasingly expect digital discovery, price comparison, online booking, and offline installation, pushing retailers toward integrated sales models.

Fleet and contract-based retail are becoming strategically important due to recurring, predictable revenue streams from logistics, leasing, and ride-hailing operators.

Premiumization is reshaping competitive intensity, as retailers increasingly differentiate through EV-ready tyres, smart tyres, alignment services, financing, and subscription offerings rather than pure product sales.

Retail digitization and data-driven inventory management are also becoming critical competitive levers, particularly for organized chains seeking efficiency and customer retention.

Strategic Implications of Competitive Intensity & Market Structure in Global Tyre Distribution & Retail Market

Manufacturers must increasingly control or influence downstream retail infrastructure to secure brand visibility, pricing discipline, and premium product adoption. Exclusive stores, franchise models, and digital channels are becoming strategic necessities.

Independent dealers must compete through service excellence, localized trust, and diversified offerings, as larger organized players expand scale and digital reach.

Online and omnichannel retail models represent one of the largest strategic growth opportunities, particularly in urban markets where convenience and price transparency are accelerating digital tyre purchasing.

Fleet retail models, tyre-as-a-service (TaaS), and subscription programs are reshaping revenue models from transactional to lifecycle-based relationships.

Retailers aligned with EV adoption, premium tyres, and advanced service ecosystems will capture disproportionate long-term value as replacement trends evolve.

Global Tyre Distribution & Retail Competitive Intensity & Market Structure Forward Outlook

The Global Tyre Distribution & Retail Market is expected to remain structurally resilient due to non-discretionary replacement demand, but competition will increasingly shift from simple distribution scale toward channel sophistication, service integration, and omnichannel capability.

Independent dealers are likely to remain volume leaders in many emerging markets, though organized chains and franchise networks will steadily gain share through branding, standardization, and customer experience.

Online tyre retail will witness the fastest structural transformation, especially through click-and-fitment, mobile fitment, and direct-to-consumer models.

EV replacement tyres, premiumization, and digital service ecosystems will become major profitability drivers, while fleet and subscription retail models are expected to strengthen recurring cash flow opportunities.

Through 2033, the market will be defined by five competitive pillars: independent dealer resilience, organized retail expansion, digital commerce acceleration, fleet lifecycle integration, and premium EV-focused retail transformation. Companies that align with these structural shifts will lead the Global Tyre Distribution & Retail Market.

Value Chain

Global Tyre Distribution & Retail Market Value Chain & Supply Chain Evolution Overview

The Global Tyre Distribution & Retail Market value chain is evolving from a fragmented, dealer-dominated aftermarket structure into a digitally connected, omnichannel, and service-driven mobility retail ecosystem. Traditionally dependent on independent tyre shops and wholesale distributors, the market is now shifting toward organized retail chains, franchise networks, OEM-backed outlets, and online tyre platforms that integrate sales, fitment, and after-sales services into a unified experience.

The value chain spans tyre manufacturers, regional distributors, wholesalers, authorized dealers, independent retailers, e-commerce platforms, fleet service providers, and end consumers. Increasing vehicle ownership, rising replacement demand, and growing premiumization are reshaping how tyres are marketed, sold, and serviced across global regions.

Upstream supply dynamics are driven by tyre manufacturers producing diverse portfolios for passenger vehicles, commercial fleets, EVs, and specialty applications. These products flow through multi-layer distribution networks where pricing, availability, branding, and service quality are determined by channel efficiency and retail penetration.

Manufacturers and distributors are increasingly focusing on strengthening retail ecosystems through exclusive brand outlets, franchised service centers, and digital-first retail platforms. This is enabling better inventory control, improved customer experience, and higher brand loyalty in a highly competitive aftermarket environment.

At the downstream level, tyre retail is becoming service-centric rather than product-centric, with fitment, alignment, balancing, warranty services, and fleet maintenance contracts becoming core revenue drivers alongside tyre sales.

Global Tyre Distribution & Retail Market Value Chain & Supply Chain Evolution Current Scenario

The current market is shaped by strong replacement demand, rapid urbanization, rising vehicle parc, and accelerating digital adoption in tyre purchasing behavior.

Independent tyre dealers continue to dominate volume sales, especially in Asia-Pacific and emerging markets, while organized retail chains and OEM-backed outlets are gaining share in developed regions due to improved service standards and brand trust.

Online tyre retail is expanding rapidly, supported by e-commerce platforms, price transparency, home installation services, and omnichannel models that connect digital ordering with offline fitment centers.

Fleet operators are increasingly relying on contract-based tyre supply models, including mileage-based replacement programs, managed tyre services, and long-term service agreements that optimize cost per kilometer.

Supply chain efficiency, inventory optimization, and regional distribution networks remain critical, as tyre availability and timely fitment directly influence customer satisfaction and retention.

Key Value Chain & Supply Chain Evolution Signals in Global Tyre Distribution & Retail Market

Several structural shifts are redefining the global tyre retail ecosystem.

- Omnichannel Retail Integration: Combination of physical stores, online platforms, and mobile fitment services into unified customer journeys.

- Retail Consolidation: Growth of organized chains and franchise networks reducing market fragmentation.

- Digital Marketplace Expansion: Increased price transparency and competition through online tyre platforms.

- Fleet-Centric Models: Rising adoption of contract-based tyre supply and lifecycle management services.

- Premiumization & EV Shift: Higher demand for EV-compatible, premium, and performance-oriented tyres.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Tyre Distribution & Retail Market

Leading companies such as Michelin, Bridgestone, Goodyear, Continental, and Pirelli are strengthening their competitive position through integrated retail ecosystems, brand-owned outlets, and digital commerce platforms.

Control over distribution networks is becoming a key competitive advantage, enabling better pricing power, stronger customer relationships, and improved brand loyalty.

Independent retailers are under pressure to modernize operations through digital inventory systems, service bundling, and partnerships with manufacturers and online platforms.

Fleet contracts and subscription-based tyre services are emerging as high-value growth areas, offering predictable revenue streams and long-term customer retention.

Digital transformation across retail channels is improving demand forecasting, customer targeting, and service efficiency, making data-driven retail strategies increasingly important.

Global Tyre Distribution & Retail Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the tyre distribution and retail value chain is expected to become more consolidated, digitalized, and service-oriented.

Omnichannel retail models will dominate, integrating online sales, offline fitment, mobile installation, and subscription-based tyre services into unified platforms.

Organized retail chains and OEM-backed networks will continue gaining market share, particularly in urban and premium vehicle segments.

Online tyre retail will expand further due to convenience, price comparison tools, and increasing consumer comfort with digital purchasing.

Fleet and commercial tyre service contracts will become a major growth pillar, driven by logistics expansion and cost optimization needs.

Ultimately, the value chain will evolve from a fragmented distribution system into a digitally connected, customer-centric, and service-led tyre mobility ecosystem.

Market-Specific Value Chain

- Tyre Manufacturing Supply: Passenger, commercial, EV, and specialty tyres supplied by global and regional manufacturers

- Distribution & Wholesale: Regional distributors, importers, bulk suppliers, and logistics partners managing inventory flow

- Retail Channels: Independent dealers, franchise outlets, brand stores, and organized retail chains

- Digital Commerce: Online tyre marketplaces, brand e-stores, and omnichannel platforms

- Fitment & Service Ecosystem: Installation centers, mobile fitment units, alignment and balancing services

- Fleet & Contract Services: Managed tyre programs, subscription models, and mileage-based replacement services

Company-to-Stage Mapping

- Manufacturing Supply: Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A.

- Distribution & Wholesale: Apollo Tyres, Yokohama Rubber Company, Sumitomo Rubber Industries, regional distributors

- Retail Channels: Michelin retail networks, Bridgestone dealerships, MRF retail outlets, independent tyre dealers

- Digital Commerce: Online tyre platforms, manufacturer e-commerce stores, omnichannel retailers

- Fitment & Service Ecosystem: Franchise service centers, independent workshops, mobile tyre installation providers

- Fleet & Contract Services: Goodyear fleet programs, Bridgestone fleet services, Michelin fleet solutions, logistics service providers

Investment Activity

Global Tyre Distribution & Retail Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Tyre Distribution & Retail Market are being shaped by the market’s transition from fragmented dealer-led ecosystems toward omnichannel, digitally integrated, and service-centric retail infrastructure. Between 2026 and 2033, capital deployment is expected to increasingly prioritize organized retail chains, e-commerce platforms, franchise expansion, last-mile fitment services, and EV-ready tyre retail capabilities. As tyre replacement remains a recurring, non-discretionary demand category, investors view tyre distribution and retail as a stable cash-flow segment with strong aftermarket monetization potential. Funding is increasingly directed toward retail digitization, online-to-offline (O2O) platforms, inventory analytics, warehouse automation, and customer lifecycle retention systems. Major global players such as Michelin, Bridgestone, Goodyear, Continental, Apollo Tyres, and Pirelli are actively investing in retail network modernization, franchise ecosystems, direct-to-consumer platforms, and service-led retail expansion to secure stronger downstream control over pricing, customer loyalty, and premium product penetration. A major structural shift is the growing role of EV-specific tyres, premium replacement products, and smart tyre fitment services, which is pushing investments toward technician training, EV service bays, digital diagnostics, and omnichannel customer experience models.

Global Tyre Distribution & Retail Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is being driven by replacement tyre demand stability, rising vehicle parc expansion, and increasing consumer preference for organized and digital tyre purchasing channels. Asia-Pacific leads global investment volume due to its massive vehicle population, fragmented but rapidly consolidating dealer landscape, and large-scale replacement market opportunity across passenger, two-wheeler, and commercial segments. Europe is the fastest-growing investment region, supported by premium retail formats, franchise network expansion, tyre labeling regulations, EV penetration, and rapid omnichannel retail transformation. North America remains a strong investment hub due to mature replacement cycles, large fleet contracts, organized retail chains, and digital tyre commerce growth. Latin America and Middle East & Africa are emerging investment markets where dealer formalization, digital platform penetration, and commercial fleet growth are gradually improving retail investment attractiveness.

Key Investment & Funding Dynamics Signals in Global Tyre Distribution & Retail Market

A major investment signal is the rapid shift from independent, price-driven retail toward integrated omnichannel models combining digital purchase, local installation, and mobile fitment services. Expansion of online tyre retail platforms is attracting substantial capital into e-commerce marketplaces, digital logistics, warehouse networks, and click-and-fit business models. Franchise and organized chain retail models are seeing strong funding momentum as brands seek stronger customer retention, pricing consistency, and premiumization opportunities. Fleet-focused retail contracts and tyre-as-a-service (TaaS) models are unlocking recurring B2B investment opportunities in logistics, leasing, and mobility ecosystems. The rise of EV tyres, run-flat products, connected tyres, and premium fitment services is accelerating investment into retail capability upgrades, technician specialization, and smart diagnostics infrastructure.

Strategic Implications of Investment & Funding Dynamics in Global Tyre Distribution & Retail Market

The investment landscape increasingly favors retailers and manufacturers with scalable omnichannel ecosystems, franchise networks, and integrated aftermarket service capabilities. Independent tyre dealers remain volume-dominant, but long-term capital is increasingly flowing toward organized, technology-enabled retail models that can offer superior margins and customer retention. Digital transformation is becoming a major competitive differentiator, with inventory intelligence, online booking systems, AI-driven recommendation tools, and mobile service integration reshaping retail economics. Regional diversification remains essential, with Asia-Pacific focused on volume expansion, Europe on premiumization and regulation-led modernization, and North America on fleet and digital channel optimization. Retail margin pressures, logistics complexity, and inventory management risks continue to influence profitability, making supply chain automation and channel efficiency central to future funding strategies.

Global Tyre Distribution & Retail Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Tyre Distribution & Retail Market is expected to attract sustained investment as tyre replacement demand remains structurally resilient and retail ecosystems modernize globally. Future capital allocation will increasingly prioritize omnichannel commerce, online tyre marketplaces, EV-focused retail infrastructure, subscription-based tyre programs, and predictive aftermarket service ecosystems. Asia-Pacific will remain the largest investment destination due to scale and dealer consolidation, while Europe will lead innovation in premium and EV-ready retail models. North America will continue to focus on digital retail, fleet service contracts, and advanced replacement ecosystems. Retail digitization, AI-enabled customer acquisition, and smart supply chain technologies will further reshape investment patterns, pushing tyre retail from transactional sales toward lifecycle mobility service platforms. Overall, the market’s investment outlook remains highly stable and strategically attractive, supported by recurring replacement demand, retail modernization, and evolving consumer preferences. Companies that align distribution scale with digital transformation, service excellence, and premium product penetration will be best positioned to lead through 2033.

Technology & Innovation

Global Tyre Distribution & Retail Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Tyre Distribution & Retail Market is being reshaped by rapid digital transformation, omnichannel retail expansion, and service-led business model innovation. Traditional tyre retail, once dominated by offline dealerships, is now evolving into a highly integrated ecosystem combining physical stores, e-commerce platforms, fleet service networks, and mobile fitment solutions. A key innovation driver is the shift toward omnichannel retail systems, where customers can research, purchase, and schedule installation across both online and offline platforms. This integration is improving convenience, pricing transparency, and service accessibility while enabling retailers to expand their customer reach beyond geographic limitations. Digital technologies such as AI-driven product recommendation engines, automated inventory management, and predictive demand forecasting are increasingly being adopted by tyre retailers. These tools help optimize stock levels, reduce delivery time, and enhance customer satisfaction by ensuring the right tyre is available at the right location. Fleet-focused innovation is another major area of transformation. Subscription-based tyre services, Tyre-as-a-Service (TaaS) models, and lifecycle management platforms are enabling commercial operators to shift from ownership-based purchases to performance-based contracts. This is significantly improving cost predictability and operational efficiency for logistics and mobility companies.

Global Tyre Distribution & Retail Market Technology & Innovation Landscape Current Scenario

The current innovation environment is centered on digital retail expansion, service automation, and customer experience enhancement. Online tyre marketplaces and brand-owned e-commerce platforms are rapidly gaining traction, offering price comparison tools, installation booking systems, and doorstep delivery services. Omnichannel integration is now a standard strategy among leading retailers, allowing customers to purchase tyres online and complete installation at authorized service centers. This hybrid model is improving conversion rates and strengthening brand loyalty across urban and semi-urban markets. Artificial intelligence and data analytics are increasingly being used to analyze vehicle usage patterns, predict replacement cycles, and personalize tyre recommendations. This is especially valuable in the replacement segment, where timing and product fitment are critical. Mobile tyre installation services and on-demand fitment platforms are also expanding rapidly. These services bring tyre replacement directly to the customer’s location, reducing downtime and improving convenience, particularly in urban and fleet applications. In addition, fleet management platforms are integrating tyre lifecycle tracking, enabling real-time monitoring of wear, pressure, and performance. This helps fleet operators reduce total cost of ownership (TCO) and improve operational efficiency.

Key Technology & Innovation Landscape Signals in Global Tyre Distribution & Retail Market

- Omnichannel Retail Integration: Seamless connection between online ordering and offline installation services.

- AI-Driven Retail Platforms: Intelligent recommendation engines and predictive replacement analytics.

- Tyre-as-a-Service (TaaS) Models: Subscription-based tyre usage and lifecycle management solutions.

- Mobile Fitment & On-Demand Services: Doorstep tyre installation and emergency replacement services.

- Fleet Digitalization Platforms: Real-time monitoring of tyre health, usage, and performance metrics.

- Smart Inventory Management: Automated stock optimization and demand forecasting systems.

- Customer Experience Digitization: Online booking, transparent pricing, and digital warranty tracking.

- Data-Driven Retail Optimization: Analytics-based pricing, promotions, and sales channel strategies.

Strategic Implications of Technology & Innovation Landscape in Global Tyre Distribution & Retail Market

The ongoing technological transformation is redefining competitive dynamics in the tyre retail ecosystem. Traditional independent dealers are under pressure to digitize operations, while organized retail chains and OEM-backed outlets are gaining advantage through scale, technology adoption, and integrated service offerings. Omnichannel capability is becoming a key differentiator, with retailers that combine digital engagement and physical service infrastructure achieving higher customer retention and sales conversion rates. This is also enabling expansion into underserved regions without requiring large physical investments. Subscription-based and fleet-oriented service models are shifting revenue structures from one-time sales to recurring income streams. This is improving business predictability and strengthening long-term customer relationships in the commercial segment. Data analytics and AI integration are also enabling more precise demand planning, reducing inventory inefficiencies, and improving supply chain responsiveness. Retailers leveraging these tools are better positioned to manage seasonal demand fluctuations and regional market variations. Overall, technology adoption is becoming a core competitive requirement rather than an optional enhancement, especially as customer expectations shift toward convenience, transparency, and speed of service.

Global Tyre Distribution & Retail Market Technology & Innovation Landscape Forward Outlook

Between 2026 and 2033, the Global Tyre Distribution & Retail Market is expected to evolve into a fully digitized, service-oriented ecosystem. Omnichannel retail will become the dominant model, with integrated online-offline journeys becoming standard across all major markets. Artificial intelligence, machine learning, and predictive analytics will play a central role in shaping pricing strategies, inventory management, and customer engagement. Retailers will increasingly rely on data-driven decision-making to optimize sales and improve operational efficiency. Mobile fitment services and on-demand delivery models are expected to expand significantly, particularly in urban areas where convenience-driven consumption is rising. Fleet-focused digital platforms will also become more sophisticated, offering end-to-end tyre lifecycle management solutions. Subscription-based tyre services and managed mobility solutions are likely to gain mainstream adoption, particularly in logistics, ride-hailing, and corporate fleet segments. This will further accelerate the shift from product sales to service-based revenue models. Overall, the market is transitioning toward a technology-enabled, customer-centric ecosystem where digital platforms, service innovation, and omnichannel integration define competitive leadership through 2033.

Market Risk

Global Tyre Distribution & Retail Market Risk Factors & Disruption Threats Overview

The Global Tyre Distribution & Retail Market operates within a highly fragmented yet strategically critical aftermarket ecosystem where dealer networks, independent retailers, wholesalers, franchise chains, and digital commerce platforms collectively determine customer access, pricing power, and replacement monetization. While the market benefits from recurring replacement demand, expanding global vehicle parc, and stable aftermarket fundamentals, it carries a moderate strategic risk profile due to margin compression, digital disruption, inventory volatility, and evolving consumer purchasing behavior. A major structural risk is channel disruption caused by the rapid rise of e-commerce and omnichannel retail. Traditional independent dealers and offline retailers face increasing competitive pressure from direct-to-consumer platforms, online marketplaces, and manufacturer-owned digital ecosystems that can bypass conventional distribution layers. Another key disruption factor is pricing transparency and margin erosion. Online comparison tools, aggressive discounting, and private-label expansion are intensifying price competition, reducing retailer profitability, and shifting competitive advantage toward service differentiation rather than pure product sales. Supply chain instability also presents a significant operational threat. Global logistics disruptions, fluctuating freight costs, import tariffs, regional inventory imbalances, and raw material price volatility can materially impact tyre availability, working capital requirements, and retail pricing consistency. The shift toward EVs, smart tyres, and premium tyre technologies adds complexity, as retailers must increasingly support specialized fitment, digital diagnostics, software integration, and customer education’requiring infrastructure investment and workforce capability upgrades.

Global Tyre Distribution & Retail Market Risk Factors & Disruption Threats Current Scenario

The current market reflects strong replacement-led resilience supported by aging vehicle fleets, growing vehicle ownership, and recurring tyre wear cycles. However, this demand stability is increasingly balanced by structural transformation across retail models. Independent tyre dealers remain dominant globally, particularly in Asia-Pacific and emerging markets, but organized franchise chains and digital-first platforms are rapidly gaining share through better pricing transparency, inventory management, and convenience. Omnichannel retail is becoming a core competitive differentiator, as consumers increasingly expect online purchasing, mobile fitment, click-and-collect, and integrated after-sales services. Fleet and subscription-based tyre programs are expanding, especially in logistics and mobility sectors, shifting parts of the market from transactional sales to recurring contract models. At the same time, premiumization trends are reshaping consumer expectations, increasing demand for EV-ready, run-flat, connected, and fuel-efficient tyres while raising retailer complexity.

Key Risk Factors & Disruption Threats Signals in Global Tyre Distribution & Retail Market

A major disruption signal is accelerating digitalization, with online tyre retail and mobile fitment services increasingly reshaping purchasing journeys, especially in urban and digitally mature markets. Retail consolidation is another critical trend, as franchise chains, organized retail groups, and large distributors gain leverage through scale, procurement power, and broader service portfolios. EV adoption represents both opportunity and disruption, as EV-specific tyre requirements may shift customer demand patterns while increasing the importance of specialist retail expertise. Private-label and distributor-owned tyre brands are intensifying competitive pressure by targeting price-sensitive segments with lower-cost alternatives. Consumer preference for convenience, transparent pricing, and integrated service ecosystems is rapidly redefining retailer success factors.

Strategic Implications of Risk Factors & Disruption Threats in Global Tyre Distribution & Retail Market

Retailers must increasingly invest in omnichannel capabilities that combine physical fitment infrastructure with digital sales, inventory visibility, and service scheduling. Service-led differentiation’including alignment, balancing, diagnostics, EV support, and subscription models’will become more important than product-only competition. Supply chain resilience, inventory optimization, and regional distribution flexibility will be essential to mitigate volatility and preserve customer satisfaction. Independent dealers may require franchise partnerships, digital integration, or specialization strategies to defend competitiveness against organized retail expansion. Manufacturers and distributors must strengthen retail ecosystems to preserve brand loyalty, customer retention, and premium positioning.

Global Tyre Distribution & Retail Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Tyre Distribution & Retail Market is expected to remain one of the most stable segments in the tyre value chain, but competitive structures will evolve rapidly. Traditional offline retail will remain essential due to installation and service dependency, but online, mobile, and omnichannel channels will capture disproportionate growth. Retail consolidation is likely to accelerate, particularly in developed markets, while fragmented dealer ecosystems may persist longer in cost-sensitive regions. EV replacement growth, premium tyre penetration, and connected tyre servicing will increasingly redefine retailer infrastructure requirements. Overall, the market will remain highly attractive but operationally transformative, with long-term winners defined by digital maturity, service capability, supply chain resilience, and customer experience leadership.

Regulatory Landscape

Global Tyre Distribution & Retail Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Tyre Distribution & Retail Market is increasingly shaped by transportation safety laws, environmental compliance mandates, digital commerce regulations, and evolving automotive aftersales governance frameworks. Governments and transport authorities worldwide are focusing on improving road safety, ensuring tyre quality standards, and enhancing transparency in retail distribution networks, making compliance a critical pillar of tyre retail operations. Regulatory frameworks such as mandatory tyre safety standards, tyre labeling regulations, consumer protection laws, and vehicle inspection requirements are directly influencing how tyres are sold, distributed, and serviced. In many regions, authorities are tightening rules around tread depth, tyre age limits, energy efficiency labeling, and warranty disclosures’ensuring that both independent and organized retailers maintain standardized service quality and product authenticity. Environmental regulations are also playing a growing role in shaping the tyre distribution and retail ecosystem. Extended Producer Responsibility (EPR) policies, waste tyre management laws, and recycling mandates are pushing retailers to participate in collection, return, and recycling systems. This is gradually integrating retail networks into circular economy frameworks where end-of-life tyres are tracked and managed through structured channels. The rise of digital commerce and omnichannel retailing has introduced additional regulatory oversight in areas such as e-commerce taxation, consumer data protection, digital payment compliance, and cross-border trade rules. Online tyre platforms and mobile fitment services must comply with regional consumer protection laws, transparent pricing requirements, and installation safety standards, ensuring consistent service quality across physical and digital channels.

Global Tyre Distribution & Retail Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by a strong focus on road safety enforcement, structured aftermarket governance, and increasing digitization of automotive retail. Asia-Pacific, North America, and Europe each follow distinct but increasingly harmonized regulatory approaches to tyre retail operations, particularly in safety compliance and consumer protection. In North America, regulations such as tyre safety standards, Federal Motor Vehicle Safety Standards (FMVSS), and state-level inspection rules ensure strict compliance in tyre sales and replacement practices. Retailers are required to maintain clear documentation of tyre specifications, warranty terms, and safety certifications, especially for passenger and commercial vehicles. Europe maintains one of the most structured regulatory environments, driven by EU tyre labeling regulations, strict consumer transparency laws, and environmental compliance directives. Retailers must provide standardized information on fuel efficiency, wet grip, and noise levels, while also complying with sustainability and recycling obligations under circular economy policies. In Asia-Pacific, regulatory frameworks are rapidly evolving due to rising vehicle ownership and expanding aftermarket demand. Countries such as China and India are strengthening tyre safety standards, promoting organized retail networks, and improving enforcement of quality certification systems to reduce counterfeit and substandard tyre sales. Digital retail regulation is also gaining momentum globally, with governments introducing policies on e-commerce licensing, online consumer rights, transparent pricing mechanisms, and service accountability for mobile tyre installation and omnichannel retail models.

Key Regulatory & Policy Environment Signals in Global Tyre Distribution & Retail Market

- Tyre Safety & Quality Standards: Mandatory compliance with tread depth, durability, and performance benchmarks across regions.

- Tyre Labeling Regulations: EU and other markets require standardized information on efficiency, safety, and noise levels.

- Consumer Protection Laws: Enforcement of transparent pricing, warranty disclosures, and service accountability.

- Extended Producer Responsibility (EPR): Retail participation in tyre collection, recycling, and waste management systems.

- Digital Commerce Regulations: Governance of online tyre sales, data protection, and e-payment compliance.

- Vehicle Inspection & Road Safety Policies: Mandatory tyre condition checks in periodic vehicle inspections.

- Counterfeit Tyre Prevention Rules: Strict enforcement against illegal and substandard tyre distribution channels.

- Omnichannel Retail Compliance: Integration of offline and online retail under unified consumer protection frameworks.

Strategic Implications of Regulatory & Policy Environment in Global Tyre Distribution & Retail Market

The regulatory landscape is significantly transforming the Global Tyre Distribution & Retail Market by shifting it from a fragmented aftermarket structure toward a more standardized, transparent, and digitally integrated ecosystem. Compliance requirements are increasing operational complexity for small retailers while simultaneously benefiting organized retail chains and OEM-backed distribution networks. Retailers are increasingly required to invest in certification systems, digital inventory tracking, warranty management platforms, and compliance reporting tools. This is driving consolidation in the market, with larger players gaining advantage through scalable infrastructure and regulatory readiness. The rise of omnichannel retail is also being shaped by regulatory expectations around consumer rights, service accountability, and pricing transparency. Online tyre platforms must ensure installation safety compliance, verified service partners, and standardized customer experience across regions. Fleet operators and commercial customers are increasingly prioritizing regulatory-compliant retail partners that can provide documented safety checks, lifecycle tracking, and sustainability reporting. This is creating new opportunities for fleet-focused retail models and subscription-based tyre services. Regional regulatory divergence is also influencing market strategies, requiring global tyre brands to adapt distribution models, pricing structures, and service frameworks according to local compliance requirements.

Global Tyre Distribution & Retail Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, regulatory frameworks are expected to become more unified, digitalized, and sustainability-driven, further reshaping the Global Tyre Distribution & Retail Market. Governments are likely to strengthen enforcement of tyre lifecycle management, digital retail compliance, and road safety monitoring systems. Europe is expected to maintain leadership in regulatory sophistication, particularly in sustainability reporting, tyre labeling, and circular economy integration. North America will continue advancing safety enforcement and digital retail governance, while Asia-Pacific is projected to experience rapid regulatory expansion aligned with vehicle growth and infrastructure modernization. Future regulations are likely to increasingly incorporate digital tracking of tyre sales, AI-based inventory monitoring, automated safety compliance systems, and integration with vehicle telematics platforms. This will enhance transparency across the tyre distribution chain from manufacturing to end-user retail. Sustainability regulations are also expected to intensify, requiring retailers to participate more actively in tyre recycling programs, carbon reporting systems, and circular supply chain initiatives. This will further integrate retail networks into broader environmental governance frameworks. Overall, the regulatory and policy environment will act as a key structural force reshaping competition, accelerating digital transformation, and reinforcing sustainability across the Global Tyre Distribution & Retail Market. Companies that align early with safety standards, omnichannel compliance, digital retail governance, and circular economy policies will be best positioned to achieve long-term growth through 2033.