Global Tyre Replacement Market size, share & Forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

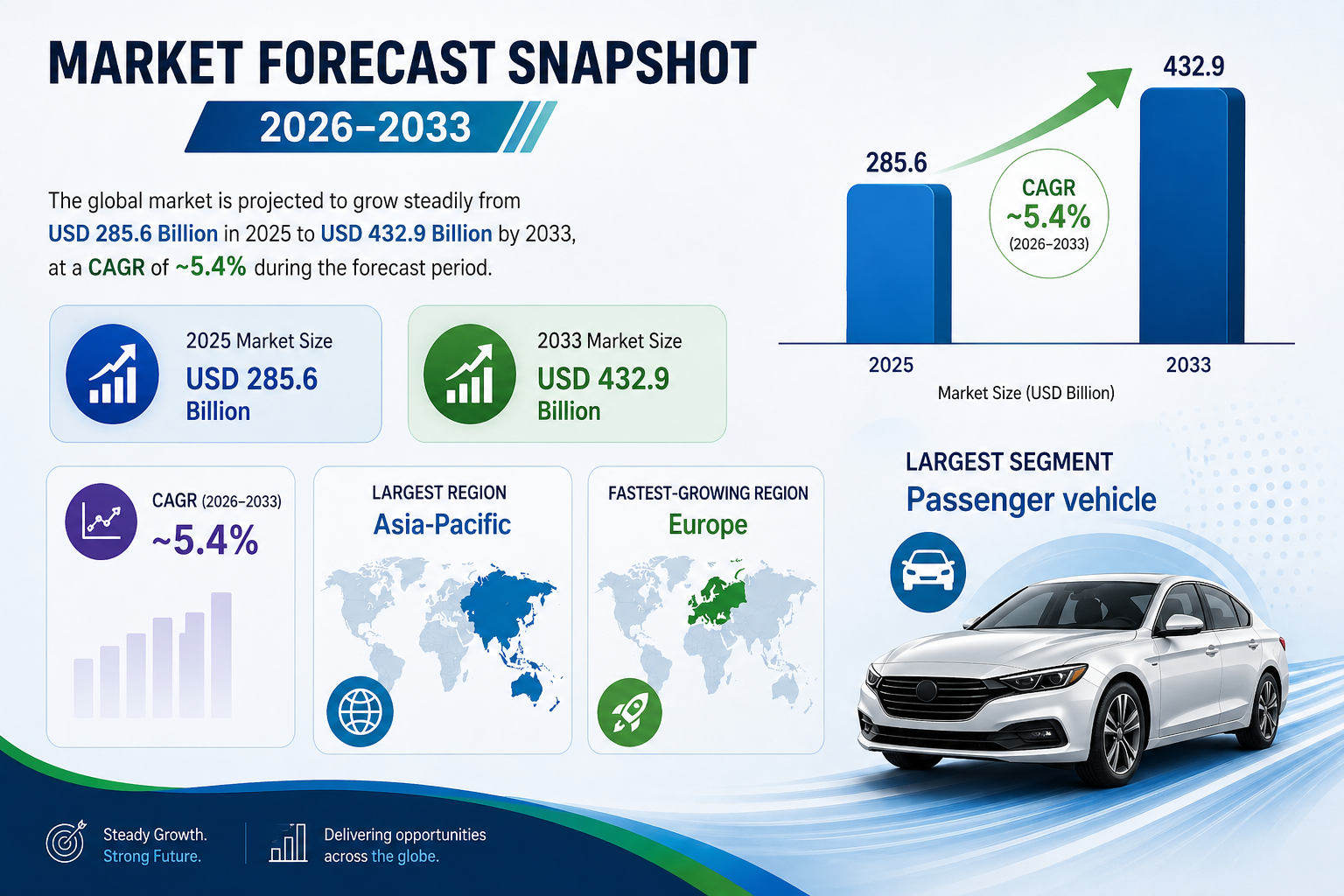

| 2025 Market Size | USD 285.6 Billion |

| 2033 Market Size | USD 432.9 Billion |

| CAGR (2026???2033) | ~5.4% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Passenger vehicle replacement tyres |

| Fastest-Growing Segment | EV replacement tyres |

| Key Trend | Premiumization & EV-focused replacement |

Global Tyre Replacement Market Overview

The Global Tyre Replacement Market is basically the biggest money-maker in the tyre world . It covers all those tyres people buy when the old ones wear out, get damaged, or just get too old???think cars, trucks, bikes, off-road gear, even EVs. Unlike OEM sales, which bounce with new car production, replacement demand stays steady, driven by how many vehicles are on the road, how much they???re driven, road conditions, and safety rules. So, it???s a solid, ongoing market that keeps rolling no matter what.

Tyres wear out like clockwork, so replacing them is a must-buy, not a maybe . With more cars on the road and people keeping vehicles longer, the replacement market dominates tyre sales worldwide. It???s a steady, recurring demand that keeps the industry rolling.

The Global Tyre Replacement Market is where premiumization, tech upgrades, and better margins shine . Instead of just swapping like-for-like, folks now go for higher-performance tyres with better durability, fuel efficiency, noise reduction, safety, and EV compatibility. It???s a sweet spot for innovation and profits, making replacements more than just a routine fix.

According to the Pheonix Demand Forecast Engine, the Global Tyre Replacement Market size is valued at USD 285.6 billion in 2025 and is projected to reach USD 432.9 billion by 2033, expanding at a CAGR of ~5.4% during the forecast period (2026???2033).

Asia-Pacific is the largest market due to its massive vehicle parc and two-wheeler dominance, while Europe is the fastest-growing region driven by premium tyre replacement, EV penetration, and stringent safety regulations.

Key Drivers of Global Tyre Replacement Market Growth

Expanding Global Vehicle Parc

Rising vehicle ownership across emerging and developed markets is fueling market growth , increasing the base of vehicles requiring regular tyre replacement .

Recurring Wear & Tear Cycles

Tyres have limited tread life, making replacement unavoidable regardless of economic cycles.

Longer Vehicle Lifespans

Improved vehicle durability keeps cars, trucks, and two-wheelers operational for longer periods, boosting lifetime replacement frequency.

Shift Toward Premium & Value-Added Tyres

Consumers increasingly replace tyres with higher-performance, fuel-efficient, and technology-enabled alternatives.

Electric Vehicle Adoption

EVs accelerate tyre wear due to higher torque and weight, increasing replacement frequency and demand for EV-specific tyres.

Road Safety & Regulatory Enforcement

Mandatory tread depth, tyre inspection norms, and safety checks are driving market growth , directly supporting replacement demand.

Global Tyre Replacement Market Segmentation

1. By Vehicle Category

1.1 Passenger Vehicles (Largest Segment)

1.1.1 Passenger Cars

1.1.1.1 Hatchbacks

1.1.1.2 Sedans

1.1.2 SUVs & Crossovers

1.1.2.1 Compact SUVs

1.1.2.2 Mid-size & full-size SUVs

1.1.3 MPVs & Passenger Vans

1.2 Two-Wheelers

1.2.1 Motorcycles

1.2.1.1 Commuter motorcycles

1.2.1.2 Premium motorcycles

1.2.2 Scooters

1.2.2.1 ICE scooters

1.2.2.2 Electric scooters

1.3 Commercial Vehicles

1.3.1 Light Commercial Vehicles (LCVs)

1.3.1.1 Delivery vans

1.3.1.2 Pickup trucks

1.3.2 Medium & Heavy Commercial Vehicles

1.3.2.1 Long-haul trucks

1.3.2.2 Buses

1.4 Off-the-Road (OTR) Vehicles

1.4.1 Construction Equipment

1.4.1.1 Loaders

1.4.1.2 Excavators

1.4.2 Agricultural Machinery

1.4.2.1 Tractors

1.4.2.2 Harvesters

2. By Tyre Construction

2.1 Radial Tyres (Largest & Fastest-Growing)

2.1.1 Steel-Belted Radial Tyres

2.1.1.1 Passenger vehicle radials

2.1.1.2 Commercial vehicle radials

2.1.2 Fabric-Belted Radial Tyres

2.1.2.1 Polyester radial tyres

2.1.2.2 Nylon radial tyres

2.2 Bias (Cross-Ply) Tyres

2.2.1 Nylon Bias Tyres

2.2.1.1 Heavy-duty bias tyres

2.2.2 Polyester Bias Tyres

2.2.2.2 Cost-focused bias tyres

3. By Sales Channel

3.1 Authorized Dealer Networks (Largest Segment)

3.1.1 Manufacturer-Branded Stores

3.1.1.1 OEM-authorized outlets

3.1.2 Franchise Dealer Networks

3.2 Independent Tyre Retailers

3.2.1 Multi-Brand Tyre Shops

3.2.1.1 Local retailers

3.2.2 Service & Fitment Centers

3.3 Fleet Service Providers

3.3.1 Contracted Fleet Replacement

3.3.1.1 Mileage-based tyre contracts

3.3.2 Tyre-as-a-Service (TaaS)

3.4 Online & E-Commerce Platforms (Fastest-Growing)

3.4.1 Direct-to-Consumer Sales

3.4.1.1 Online tyre marketplaces

3.4.2 App-Based Booking & Installation

4. By Tyre Technology

4.1 Conventional Replacement Tyres

4.2 Low Rolling Resistance Tyres

4.2.1 Fuel-efficient replacement tyres

4.3 EV-Optimized Replacement Tyres

4.3.1 Low-noise, high-load tyres

4.4 Run-Flat & Self-Sealing Tyres

4.4.1 Puncture-resistant tyres

4.5 Smart & Connected Tyres

4.5.1 Sensor-enabled replacement tyres

5. By Geography

5.1 Asia-Pacific (Largest Region)

China

India

Japan

Southeast Asia

5.2 Europe (Fastest-Growing Region)

Germany

France

U.K.

Italy

5.3 North America

U.S.

Canada

5.4 Latin America

Brazil

Mexico

5.5 Middle East & Africa

Regional Insights of Global Tyre Replacement Market

Asia-Pacific ??? Largest Market

Massive vehicle parc, high two-wheeler penetration, varied road conditions, and price-sensitive replacement cycles drive dominant demand.

Europe ??? Fastest Growing

Premium tyre replacement, EV-specific tyres, winter tyre regulations, and strict safety standards support accelerated growth.

North America

Large SUV and truck parc, long-distance driving, and strong aftermarket infrastructure sustain stable demand.

Latin America

Growing vehicle ownership and aging fleets increase replacement frequency.

Middle East & Africa

Harsh road and climate conditions accelerate tyre wear, boosting replacement demand.

Leading Companies in the Global Tyre Replacement Market

Michelin

Bridgestone Corporation

Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A.

Sumitomo Rubber Industries

Hankook Tire

Yokohama Rubber Company

Apollo Tyres

MRF

Michelin is the largest company in the Global Tyre Replacement Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Models vehicle parc growth, mileage accumulation, and replacement cycles.

Replacement Cycle Optimization Model

Tracks tread wear rates by vehicle type and region.

EV Tyre Wear Analyzer

Evaluates accelerated replacement demand from EV torque and weight.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate

-

Supplier Power: Moderate

-

Threat of New Entrants: Low

-

Threat of Substitutes: Low

-

Competitive Rivalry: High

Why the Tyre Replacement Market Is Critical

-

Largest revenue contributor in the global tyre industry

-

Non-discretionary, recurring demand

-

Strong pricing power through premium upgrades

-

Direct link to road safety and vehicle efficiency

Final Takeaway of Global Tyre Replacement Market

The Global Tyre Replacement Market is the backbone of the global tyre industry, offering stable volumes, recurring revenue, and strong margins. As vehicles stay on roads longer and EVs reshape tyre wear dynamics, replacement demand will continue to expand. Manufacturers that focus on premium replacement products, EV-ready portfolios, digital retail channels, and fleet-focused solutions will dominate the market through 2033.

Competitive Landscape

Global Tyre Replacement Competitive Intensity & Market Structure Overview

The Global Tyre Replacement Market is characterized by a highly mature, volume-driven, and brand-dominant competitive landscape, where global tyre manufacturers compete alongside strong regional players and an extensive aftermarket distribution ecosystem. Unlike OEM-focused segments, this market is primarily demand-driven by vehicle parc size, mileage accumulation, and replacement cycles rather than new vehicle production.

The market structure is heavily skewed toward replacement demand through authorized dealer networks, independent retailers, fleet service providers, and rapidly growing online channels. Competitive intensity is high, as players compete on pricing, product performance, durability, fuel efficiency, and increasingly, EV compatibility and premiumization.

Market concentration remains strong at the top, with Tier 1 global manufacturers holding significant share, but fragmentation exists at the regional and local distribution level. Fleet contracts and organized retail channels are becoming increasingly important in shaping competitive positioning and long-term customer retention.

Global Tyre Replacement Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global leader with strong premium replacement portfolio, advanced fuel-efficient tyres, and extensive retail and fleet network penetration.

Bridgestone Corporation: Dominant global player with broad product range, strong distribution strength, and leadership in commercial and passenger replacement segments.

Goodyear Tire & Rubber Company: Strong presence in North America and Europe with focus on high-performance and EV-ready replacement tyres.

Continental AG: Technology-driven manufacturer with strong positioning in premium, safety-focused, and LRR replacement tyres.

Pirelli & C. S.p.A.: Premium segment specialist focused on luxury and performance vehicle replacement tyres with strong OEM legacy influence.

Sumitomo Rubber Industries: Strong Asia-focused player with expanding global footprint in passenger and commercial replacement tyres.

Hankook Tire: Fast-growing global challenger with aggressive expansion in premium replacement and EV tyre categories.

Yokohama Rubber Company: Known for performance-oriented and durable replacement tyre solutions across passenger and SUV segments.

MRF: Leading regional powerhouse in Asia, especially strong in price-competitive replacement tyre segments.

Apollo Tyres: Emerging global player with strong presence in commercial and passenger replacement tyre markets.

Key Competitive Intensity & Market Structure Signals in Global Tyre Replacement Market

A key structural signal in the market is the dominance of replacement demand over OEM sales, making distribution networks and retail penetration critical competitive advantages. Companies with strong dealer ecosystems and fleet contracts tend to secure more stable long-term revenues.

Another major signal is the growing premiumization trend, where consumers increasingly upgrade to higher-performance tyres during replacement cycles. This is boosting demand for fuel-efficient, low rolling resistance, EV-compatible, and noise-reducing tyres.

The rise of electric vehicles is reshaping replacement dynamics, as EVs accelerate tyre wear due to higher torque and vehicle weight, increasing replacement frequency and driving demand for EV-specific tyre solutions.

Digital transformation is also reshaping competition, with online tyre sales, app-based booking, and tyre-as-a-service (TaaS) models gaining traction, particularly in urban markets and fleet operations.

Strategic Implications of Competitive Intensity & Market Structure in Global Tyre Replacement Market

Manufacturers must prioritize strengthening aftermarket distribution networks, as replacement demand is primarily controlled through retail and fleet channels rather than OEM integration. Control over last-mile availability directly impacts market share.

Product differentiation through premiumization is becoming essential, with increasing demand for EV-optimized, fuel-efficient, and durable tyres. Companies that fail to upgrade product portfolios risk margin compression in commoditized segments.

Fleet-focused strategies are gaining importance, as large commercial operators increasingly adopt contract-based tyre management models, offering long-term recurring revenue opportunities for suppliers.

Digital sales channels and direct-to-consumer platforms are emerging as a structural shift, requiring manufacturers to integrate online retail strategies with traditional dealer networks to maintain competitiveness.

Global Tyre Replacement Competitive Intensity & Market Structure Forward Outlook

The Global Tyre Replacement Market is expected to remain the largest and most stable revenue-generating segment in the tyre industry, supported by continuous vehicle parc expansion and recurring replacement cycles.

Competitive intensity will remain high, but differentiation will increasingly shift from price-based competition to technology, sustainability, and EV-specific performance capabilities.

Market consolidation among global Tier 1 manufacturers is expected to strengthen, while regional players will continue to compete aggressively in cost-sensitive segments, particularly in emerging markets.

In the long term, the market will be shaped by three core pillars: premiumization of replacement tyres, EV-driven wear acceleration, and digital transformation of tyre retail and fleet management ecosystems. Manufacturers aligning with these trends will secure sustainable growth through 2033.

Value Chain

Global Tyre Replacement Market Value Chain & Supply Chain Evolution Overview

The Global Tyre Replacement Market value chain is evolving from a traditional volume-driven aftermarket ecosystem into a technologically advanced, digitally integrated, premium-focused mobility support network. Unlike OEM tyre sales that depend heavily on vehicle production cycles, the replacement market is built around recurring demand driven by tyre wear, road safety compliance, vehicle longevity, and growing global vehicle parc expansion. This makes replacement tyres the most resilient and commercially critical revenue stream in the global tyre industry.

The replacement tyre value chain spans raw material sourcing, tyre design and manufacturing, wholesale distribution, dealer networks, retail fitment centers, digital commerce platforms, fleet contracts, and end-of-life recycling ecosystems. Increasingly, the market is shifting from simple tyre replacement toward premiumization, where consumers and fleets prioritize durability, fuel efficiency, EV compatibility, smart monitoring, and total cost of ownership optimization.

Upstream supply chain dynamics remain dependent on natural rubber, synthetic rubber, carbon black, silica, steel cords, textile reinforcements, and specialty compounds. However, manufacturers are increasingly integrating sustainable materials, recycled compounds, and EV-specific engineering to meet replacement market demand for performance and regulatory alignment.

Manufacturing strategies increasingly focus on producing differentiated replacement portfolios, including premium passenger tyres, EV replacement tyres, run-flat tyres, smart tyres, low rolling resistance tyres, and region-specific durability solutions. Production flexibility is becoming critical as manufacturers balance mass-market affordability with premium and EV-focused growth segments.

Distribution remains the defining competitive battleground, with authorized dealer networks, independent retailers, wholesalers, e-commerce platforms, and fleet service providers all playing strategic roles. Digital tyre marketplaces, online-to-offline booking, and tyre-as-a-service models are rapidly transforming how consumers and fleets purchase replacement tyres.

Supply chain challenges include fluctuating raw material costs, counterfeit tyre risks, logistics complexity, inventory optimization, regional regulatory compliance, and balancing premium product innovation with affordability across price-sensitive markets.

Global Tyre Replacement Market Value Chain & Supply Chain Evolution Current Scenario

The current market is shaped by growing global vehicle parc expansion, longer vehicle ownership cycles, EV adoption, premiumization trends, and regulatory safety enforcement.

Upstream, manufacturers are strengthening sourcing resilience for natural rubber, silica, steel, and sustainable compounds while increasingly adapting portfolios for EV wear patterns and premium performance demands.

Manufacturing strategies are prioritizing high-margin replacement products, region-specific tread technologies, winter tyres, fuel-efficient designs, and digital quality monitoring systems.

Distribution networks are increasingly omnichannel, combining authorized dealerships, independent retailers, online sales platforms, mobile fitment, and subscription-based fleet programs.

Fleet replacement and commercial contracts are becoming increasingly important due to logistics expansion, urban delivery growth, and cost-per-kilometer optimization requirements.

Lifecycle management, recycling systems, retreading programs, and sustainable disposal are gaining strategic relevance as ESG priorities influence aftermarket purchasing behavior.

Key Value Chain & Supply Chain Evolution Signals in Global Tyre Replacement Market

Several major structural shifts are reshaping the tyre replacement ecosystem.

First, premiumization is increasing average selling prices as consumers increasingly choose fuel-efficient, durable, and technology-enhanced replacement tyres.

Second, EV replacement tyres are emerging as a major growth category due to higher wear rates, torque loads, and demand for low-noise, high-load solutions.

Third, digital retail channels are transforming purchasing journeys through online marketplaces, app-based installation, and direct-to-consumer models.

Fourth, fleet-focused tyre lifecycle services are expanding through predictive maintenance, contract replacement, and tyre-as-a-service offerings.

Fifth, sustainability and circular economy integration are becoming increasingly important through retreading, recycling, and material recovery systems.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Tyre Replacement Market

Leading players such as Michelin, Bridgestone, Goodyear, Continental, and Pirelli are strengthening their positions through premium replacement portfolios, dealer ecosystem expansion, EV-specific products, and digital commerce strategies.

Supply chain resilience increasingly depends on inventory agility, regional dealer penetration, logistics optimization, and counterfeit prevention.

Companies with strong aftermarket branding, consumer trust, advanced fitment networks, and premium innovation are better positioned to capture replacement market share.

Digital transformation is becoming a critical differentiator, particularly through predictive tyre replacement, connected tyre services, and e-commerce integration.

Long-term competitiveness will increasingly rely on balancing premium product margins with scalable affordability across diverse global markets.

Global Tyre Replacement Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the tyre replacement value chain is expected to become more premiumized, EV-centric, digitally connected, and sustainability-integrated.

Manufacturers will increasingly prioritize EV replacement tyres, connected replacement ecosystems, predictive wear analytics, and higher-margin specialty tyres.

Dealer ecosystems will continue evolving toward omnichannel engagement, integrating physical retail, online booking, mobile installation, and subscription-based replacement services.

Fleet and commercial replacement programs will expand significantly as logistics, delivery, and shared mobility sectors prioritize uptime and cost efficiency.

Retreading, recycling, and circular aftermarket services will gain increasing strategic importance, especially in commercial and sustainability-focused markets.

Ultimately, the tyre replacement value chain will evolve from product-centric replacement cycles toward lifecycle-managed, data-enabled, and customer-retention-focused mobility ecosystems.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, carbon black, silica, steel belts, textile reinforcements, sustainable compounds

- Research & Development: Premium replacement tyres, EV replacement tyres, low rolling resistance, durability engineering, smart tyre technology

- Manufacturing: Mass-market tyres, premium tyres, EV tyres, retread solutions, regional product customization

- Distribution & Wholesale: Global wholesalers, regional distributors, logistics providers, inventory management systems

- Retail & Fitment: Authorized dealers, independent retailers, online platforms, fleet service providers, mobile installation

- End-of-Life & Circular Economy Services: Retreading, recycling, reclaimed rubber, disposal systems, sustainability programs

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG

- Research & Development: Michelin, Pirelli & C. S.p.A., Continental AG, Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Sumitomo Rubber Industries, Yokohama Rubber Company

- Distribution & Wholesale: Apollo Tyres, MRF, Goodyear Tire & Rubber Company, Yokohama Rubber Company

- Retail & Fitment: Michelin dealer networks, Bridgestone retail systems, independent tyre retailers, digital tyre marketplaces

- End-of-Life & Circular Economy Services: Michelin, Bridgestone Corporation, Continental AG, retreading & recycling ecosystem partners

Investment Activity

Global Tyre Replacement Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Tyre Replacement Market are being driven by the structural shift toward a larger global vehicle parc, increasing vehicle ownership duration, rising EV penetration, and growing demand for premium, performance-oriented replacement tyres. Between 2026 and 2033, capital allocation is expected to increasingly focus on retail network expansion, EV-specific replacement tyre portfolios, digital distribution channels, fleet service ecosystems, and advanced tyre lifecycle management solutions.

The market is highly cash-flow stable and volume-driven, making it one of the most attractive segments for long-term investment within the tyre industry. Leading manufacturers such as Michelin, Bridgestone, Goodyear, Continental, Pirelli, and Hankook are significantly investing in aftermarket dominance strategies, direct-to-consumer platforms, and intelligent tyre service ecosystems to capture recurring replacement demand.

A key structural transformation shaping investment flows is the premiumization of replacement demand, where consumers are increasingly shifting from basic replacements to high-performance, EV-compatible, fuel-efficient, low-noise, and smart-connected tyres. This is directing funding toward innovation-led replacement products and value-added service ecosystems.

Global Tyre Replacement Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by expanding global vehicle ownership, aging vehicle fleets, rising safety compliance enforcement, and increasing EV adoption. Strong aftermarket ecosystems and multi-brand retail expansion remain central to current funding strategies.

- Asia-Pacific: Leads global investment activity due to massive vehicle parc size, high two-wheeler penetration, and strong price-sensitive replacement demand.

- Europe: Fastest-growing investment region, driven by premium tyre demand, EV adoption, winter tyre regulations, and strict safety compliance frameworks.

- North America: Strong investment momentum supported by large SUV and truck parc, high mileage usage, and established aftermarket infrastructure.

- Latin America & Middle East & Africa: Emerging markets seeing gradual investment growth driven by aging fleets, harsh operating conditions, and expanding vehicle ownership.

Key Investment & Funding Dynamics Signals in Global Tyre Replacement Market

- Rising global vehicle parc is generating sustained long-term investment into replacement distribution networks and service infrastructure.

- Premiumization trend is driving capital inflows into high-performance, EV-ready, and fuel-efficient replacement tyre portfolios.

- EV adoption is increasing investment in specialized replacement tyres designed for higher torque, weight load, and accelerated wear cycles.

- Digital retail transformation is accelerating funding into e-commerce platforms, app-based tyre booking systems, and direct-to-consumer sales channels.

- Fleet modernization and Tyre-as-a-Service (TaaS) models are unlocking recurring revenue investment opportunities in managed tyre lifecycle services.

Strategic Implications of Investment & Funding Dynamics in Global Tyre Replacement Market

- The investment landscape strongly favors manufacturers with strong aftermarket control, distribution networks, and brand loyalty in replacement cycles.

- Strategic expansion into digital platforms and omnichannel retail is becoming essential for capturing fragmented replacement demand.

- Technological differentiation is shifting toward EV-compatible tyres, smart tyres, run-flat systems, and long-life performance compounds.

- Regional diversification remains critical, with Asia-Pacific leading volume, Europe driving premiumization, and North America sustaining fleet-driven demand.

- Supply chain efficiency, pricing optimization, and dealer network control remain key investment priorities in maintaining profitability.

Global Tyre Replacement Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Tyre Replacement Market is expected to attract steady and resilient investment as replacement demand continues to serve as the backbone of the global tyre industry.

Future capital allocation will increasingly prioritize EV-specific replacement tyres, smart tyre ecosystems, digital retail expansion, predictive tyre wear analytics, and integrated fleet service platforms.

- Asia-Pacific: Will remain the dominant investment hub due to massive vehicle population, strong replacement cycles, and cost-driven demand.

- Europe: Will continue leading premium replacement innovation and EV-focused aftermarket transformation.

- North America: Will expand investments in fleet replacement services, SUV/truck tyre demand, and digital aftermarket platforms.

Digital transformation, subscription-based tyre models, and AI-driven replacement cycle prediction will increasingly shape future funding strategies across the market.

Overall, the market will remain one of the most stable and profitable segments through 2033, supported by its recurring demand structure and strong alignment with vehicle safety, performance, and efficiency needs. Companies that dominate premium replacement offerings, EV-ready portfolios, and digital distribution ecosystems will lead the next phase of global tyre industry growth.

Technology & Innovation

Global Tyre Replacement Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global tyre replacement market is evolving rapidly as replacement tyres transition from basic wear-and-replace products into high-value, performance-enhancing mobility solutions. Unlike OEM tyres, replacement tyres increasingly serve as an upgrade opportunity where consumers, fleets, and commercial operators prioritize durability, fuel efficiency, safety, noise reduction, and EV readiness. Innovation is therefore centered not only on replacement necessity but also on product differentiation, premiumization, and lifecycle value optimization.

Innovation intensity in the tyre replacement market is high, driven by advancements in low rolling resistance compounds, EV-specific tread architectures, smart tyre integration, run-flat systems, puncture-resistant technologies, and digital retail ecosystems. Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are aggressively investing in replacement-focused innovation strategies to capture higher-margin aftermarket demand.

A major technological transformation is the emergence of EV-optimized replacement tyres, which require reinforced load-bearing structures, high torque resistance, low rolling resistance, and noise suppression to meet electric vehicle performance demands. Simultaneously, connected tyre technologies, predictive wear monitoring, and tyre-as-a-service (TaaS) models are reshaping replacement cycles from reactive purchases into proactive, data-driven maintenance ecosystems.

Global Tyre Replacement Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global tyre replacement market is centered on durability enhancement, premium product differentiation, fuel economy optimization, and digital purchasing convenience. Manufacturers are increasingly designing replacement tyres that outperform OEM baseline products, encouraging consumers to trade up to higher-value alternatives.

Low rolling resistance technology is one of the most prominent innovation areas, as replacement buyers increasingly prioritize fuel savings and EV range extension. Advanced silica compounds, optimized tread geometry, lightweight construction, and improved sidewall engineering are being widely adopted to reduce energy loss while maintaining wet grip and braking performance.

EV-specific replacement tyres are becoming a critical innovation category due to the rapid expansion of electric vehicles globally. These tyres are engineered for higher torque tolerance, increased weight loads from battery systems, reduced cabin noise, and improved efficiency, making them a premium growth segment within the replacement market.

Run-flat, self-sealing, and puncture-resistant technologies are also gaining traction, particularly in premium passenger vehicles and SUVs. These innovations improve safety, reduce roadside downtime, and create value-added replacement opportunities.

Smart and connected replacement tyres are gradually entering mainstream adoption, particularly in commercial fleets and premium consumer categories. Embedded sensors for pressure, temperature, tread wear, and load monitoring enable predictive maintenance, optimize replacement timing, and improve total cost of ownership.

Digital innovation is equally transforming the market. E-commerce tyre platforms, AI-powered fitment tools, app-based installation scheduling, and omnichannel sales models are modernizing how replacement tyres are sold, selected, and serviced.

Sustainability innovation is also expanding, with increasing integration of bio-based compounds, recycled materials, retreadability enhancements, and circular economy initiatives into replacement tyre portfolios.

Key Technology & Innovation Landscape Signals in Global Tyre Replacement Market

- EV-Optimized Replacement Tyres: Fastest-growing innovation area focused on torque resistance, low noise, and energy efficiency.

- Low Rolling Resistance Expansion: Rising replacement demand for fuel-saving and range-extending tyre technologies.

- Run-Flat & Self-Sealing Systems: Premium safety technologies improving convenience and uptime.

- Smart & Connected Replacement Tyres: Sensor integration supports predictive maintenance and data-driven replacement cycles.

- Digital Retail Innovation: Online marketplaces, AI fitment tools, and app-based installation are transforming replacement sales.

- Retread & Circular Economy Programs: Growing focus on sustainability and lifecycle extension.

- Premiumization Through Performance Upgrades: Replacement tyres increasingly positioned as technology upgrades rather than commodity replacements.

Strategic Implications of Technology & Innovation Landscape in Global Tyre Replacement Market

The evolving technology landscape has major strategic implications for tyre manufacturers, distributors, retailers, and fleet operators. Replacement markets offer stronger margins than OEM supply, making innovation-led premiumization a critical profitability lever.

Manufacturers that successfully position replacement tyres as performance upgrades through fuel efficiency, durability, EV readiness, and safety technologies can command higher ASPs and stronger brand loyalty. This shifts competition away from price-only strategies toward technology differentiation.

The rapid rise of EVs is reshaping replacement product roadmaps, requiring manufacturers to prioritize EV-specific replacement portfolios to capture accelerating wear cycles from heavier, torque-intensive electric vehicles.

Digital commerce transformation is redefining aftermarket distribution. Companies investing in omnichannel sales, AI-assisted selection, and direct-to-consumer platforms can secure stronger customer engagement and data ownership.

Smart tyre technologies and predictive maintenance solutions are gradually enabling subscription and service-based replacement ecosystems, particularly for fleets. This creates recurring revenue opportunities beyond one-time product sales.

Sustainability is also becoming strategically essential, as recycled materials, low-emission production, and circular replacement strategies increasingly align with consumer preferences, fleet ESG goals, and regulatory frameworks.

Global Tyre Replacement Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the global tyre replacement market is expected to become increasingly technology-intensive, digitally enabled, and EV-focused. Replacement tyres will evolve from standard consumables into advanced mobility products that improve efficiency, safety, and connected vehicle functionality.

EV replacement tyres are expected to remain the fastest-growing innovation category, supported by rising EV parc expansion, faster wear cycles, and consumer demand for range optimization.

Smart tyre integration will expand significantly, particularly through sensor-enabled replacement products capable of real-time diagnostics, predictive replacement scheduling, and fleet management integration.

Digital transformation will continue accelerating, with e-commerce, AI fitment, virtual consultations, and mobile installation ecosystems becoming central to replacement channel competitiveness.

Material science innovation will further advance sustainability through bio-based compounds, recycled content, longer-life tread compounds, and circular production models, supporting both environmental goals and cost optimization.

In conclusion, the Global Tyre Replacement Market is entering a new era where replacement demand is increasingly defined by premiumization, EV adaptation, digitalization, and intelligent lifecycle management. Companies that integrate advanced product technologies, digital ecosystems, and sustainable innovation into replacement strategies will be best positioned to lead the market through 2033.

Market Risk

Global Tyre Replacement Market Risk Factors & Disruption Threats Overview

The Global Tyre Replacement Market operates as the largest and most stable revenue engine within the broader tyre industry, supported by recurring wear cycles, expanding global vehicle parc, and mandatory safety-driven replacement demand. Despite its structural resilience, the market carries a moderate strategic risk profile due to raw material volatility, pricing pressure, counterfeit product penetration, digital retail disruption, and accelerating EV-related technological shifts. A major structural risk is raw material cost instability. Natural rubber, synthetic rubber, carbon black, steel, silica, and energy inputs remain highly sensitive to geopolitical disruptions, commodity cycles, and supply chain fragmentation, which can materially impact manufacturing margins and aftermarket pricing strategies. Another major disruption factor is the rapid premiumization and EV transformation of replacement demand. EVs create faster wear cycles due to higher torque and vehicle weight, but they also require specialized replacement tyres with low rolling resistance, noise reduction, and reinforced durability. Manufacturers unable to rapidly align product portfolios with EV-specific replacement demand risk competitive erosion. Counterfeit and low-cost unregulated tyre markets remain a major challenge, particularly across emerging economies, where price-sensitive consumers may prioritize affordability over safety and brand trust. This creates margin pressure for premium manufacturers while increasing safety and compliance risks. Digital commerce disruption is also reshaping traditional distribution. Online tyre platforms, app-based fitment ecosystems, and direct-to-consumer channels are reducing dependence on traditional dealer networks, forcing legacy players to redesign go-to-market strategies.

Global Tyre Replacement Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong recurring replacement demand supported by aging vehicle fleets, rising vehicle ownership, and increasing road safety enforcement. However, the market is simultaneously undergoing structural disruption from premiumization, EV growth, and channel transformation. Replacement cycles remain stable globally, but inflationary pressures and consumer cost sensitivity are intensifying competition between premium, mid-tier, and budget tyre brands. OEM-aligned aftermarket ecosystems are expanding, particularly for premium and EV segments, strengthening brand loyalty but increasing channel complexity for independent retailers. Online and omnichannel tyre retail models are accelerating, creating both growth opportunities and pricing transparency pressures. Meanwhile, sustainability regulations and consumer preference shifts toward fuel-efficient, low rolling resistance, and recycled-material tyres are increasingly reshaping replacement purchasing behavior.

Key Risk Factors & Disruption Threats Signals in Global Tyre Replacement Market

A major disruption signal is EV-driven replacement acceleration, as EV tyre wear rates often exceed traditional ICE vehicle wear cycles, reshaping replacement economics and product design priorities. Digital aftermarket platforms are another critical signal, as e-commerce marketplaces and mobile fitment solutions increasingly challenge conventional tyre dealer structures. Regulatory tightening around tyre labeling, tread safety, winter tyre mandates, and sustainability standards is creating additional compliance complexity while also driving premium segment growth. Counterfeit tyre suppression initiatives are strengthening in several markets, potentially benefiting global premium manufacturers while disrupting low-cost grey market channels. Fleet-focused tyre-as-a-service (TaaS), predictive maintenance, and connected tyre ecosystems are also emerging as transformative forces in commercial replacement markets.

Strategic Implications of Risk Factors & Disruption Threats in Global Tyre Replacement Market

Manufacturers must aggressively expand premium, EV-specific, and fuel-efficient replacement portfolios to protect long-term pricing power. Strengthening omnichannel distribution’including dealer integration, e-commerce, and direct-to-consumer capabilities’will be essential for market relevance. Anti-counterfeit technologies, certification systems, and brand trust investments will remain critical in defending both safety credibility and margin integrity. Fleet and mobility service partnerships will become increasingly strategic, particularly as predictive replacement and connected tyre ecosystems expand. Supply chain diversification and material cost optimization will be necessary to preserve profitability amid recurring commodity volatility.

Global Tyre Replacement Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Tyre Replacement Market is expected to remain the dominant profit pool of the tyre industry, but competitive advantage will increasingly depend on technological adaptation, channel modernization, and EV readiness. EV replacement tyres are likely to become one of the fastest-growing and highest-margin segments, particularly in Europe, North America, and parts of Asia-Pacific. Digital retail and integrated fitment ecosystems will continue reshaping purchasing pathways, forcing both manufacturers and distributors to evolve rapidly. Sustainability, circular economy compliance, and fuel-efficiency standards will increasingly influence replacement demand patterns. Overall, the market will remain highly resilient but competitively intense, with long-term winners defined by premium innovation, distribution agility, EV specialization, and strong aftermarket ecosystem control.

Regulatory Landscape

Global Tyre Replacement Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Tyre Replacement Market plays a crucial role in ensuring road safety, environmental compliance, and performance standards across millions of in-use vehicles. Since the replacement segment directly impacts the existing global vehicle parc, governments and regulatory bodies continuously enforce stricter tyre safety norms, tread depth requirements, and periodic inspection rules to reduce road accidents and improve mobility safety outcomes. Globally, regulatory frameworks such as UNECE tyre regulations, European Union tyre labelling rules, and U.S. Department of Transportation (DOT) safety standards set mandatory benchmarks for tyre durability, wet grip, rolling resistance, and noise levels. These regulations significantly influence replacement purchasing behavior, pushing consumers and fleet operators toward higher-quality, compliant, and performance-oriented tyres rather than low-cost alternatives. In Europe, strict vehicle inspection regimes (such as periodic technical inspections) enforce minimum tread depth and safety compliance, directly driving recurring replacement demand. Similarly, North America’s NHTSA guidelines and DOT standards ensure consistent enforcement of tyre safety norms, particularly for passenger vehicles, SUVs, and commercial fleets operating under high mileage conditions. Emerging economies including India, China, Brazil, and Southeast Asian nations are strengthening road safety laws, tyre quality certification systems, and vehicle inspection frameworks. These policy shifts are expanding organized replacement markets while reducing the dominance of unregulated or low-quality tyre segments.

Global Tyre Replacement Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is shaped by increasing emphasis on road safety enforcement, environmental sustainability, and fuel efficiency optimization. Governments are increasingly integrating tyre performance metrics into vehicle inspection systems, making replacement tyres a key compliance-driven purchase rather than a discretionary upgrade. In Europe, tyre labelling regulations mandating disclosure of rolling resistance, wet grip, and external noise levels are strongly influencing replacement demand. Consumers are increasingly shifting toward premium tyres that comply with efficiency and sustainability benchmarks, particularly in passenger vehicle and EV segments. Asia-Pacific remains a highly dynamic regulatory environment, where rapid motorization and rising accident rates are prompting governments to tighten safety norms. Countries such as India are implementing stricter tyre quality standards and promoting awareness around tread safety, significantly increasing organized replacement penetration. North America continues to maintain strong compliance frameworks through DOT inspections and safety recall mechanisms. The region’s high vehicle mileage, SUV dominance, and commercial freight activity further reinforce steady replacement demand under regulated safety conditions. The rise of electric vehicles is also reshaping regulatory focus, with increased attention on tyre durability, load-bearing capacity, and low rolling resistance requirements. These factors are accelerating replacement cycles and shifting demand toward EV-optimized tyre solutions.

Key Regulatory & Policy Environment Signals in Global Tyre Replacement Market

- UNECE Tyre Safety Regulations: Establish global standards for durability, structural integrity, and road safety compliance.

- EU Tyre Labelling Regulation: Mandates disclosure of fuel efficiency, wet grip, and noise performance, influencing premium replacement choices.

- DOT & NHTSA Standards (U.S.): Enforce tyre safety, manufacturing quality, and compliance for replacement tyres across vehicle categories.

- Mandatory Vehicle Inspection Laws: Require minimum tread depth and safety compliance, directly driving replacement frequency.

- Fuel Efficiency & Emission Norms: Encourage adoption of low rolling resistance replacement tyres for both ICE vehicles and EVs.

- EV-Specific Performance Guidelines: Promote tyres designed for higher load, torque, and energy efficiency requirements.

Strategic Implications of Regulatory & Policy Environment in Global Tyre Replacement Market

The regulatory landscape is transforming the replacement market from a price-driven segment into a performance- and compliance-driven ecosystem. Safety regulations and inspection mandates are increasing baseline demand, while labelling systems and emission norms are shifting consumer preference toward premium, high-efficiency tyres. Manufacturers are increasingly required to balance cost competitiveness with regulatory compliance, pushing innovation in tread design, compound engineering, and sustainability-focused materials. This is raising entry barriers and strengthening the position of established global tyre brands. Fleet operators are particularly influenced by regulatory compliance and total cost of ownership considerations, leading to higher adoption of premium replacement tyres that offer longer life, better fuel efficiency, and improved safety performance. Regional regulatory variations are also reshaping supply chain strategies, encouraging localization of production, expansion of certified distribution networks, and stronger alignment with national safety and environmental policies.

Global Tyre Replacement Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the tyre replacement market is expected to become increasingly stringent, with stronger enforcement of safety inspections, emissions standards, and tyre performance labelling across major economies. Europe will continue leading in regulatory strictness, particularly through expanded sustainability mandates and enhanced tyre performance transparency requirements. Asia-Pacific will see rapid regulatory expansion as governments prioritize road safety improvements and vehicle compliance enforcement. The growth of electric vehicles will further intensify regulatory focus on tyre efficiency, durability, and noise reduction, reinforcing demand for EV-specific replacement tyres globally. Digitalization of compliance systems, including smart inspections and data-driven vehicle monitoring, is expected to further formalize replacement cycles and strengthen demand predictability across markets. Overall, the regulatory landscape will continue to act as a strong structural driver of replacement demand, ensuring steady market expansion while pushing manufacturers toward higher performance, sustainability, and safety standards. Companies that align closely with evolving regulations and invest in premium, EV-ready, and fuel-efficient tyre technologies will maintain long-term leadership through 2033.