Global Remote Sensing Technology for Agriculture Market Report, Size & Forecast 2026 – 2033

| Metric | Value |

|---|---|

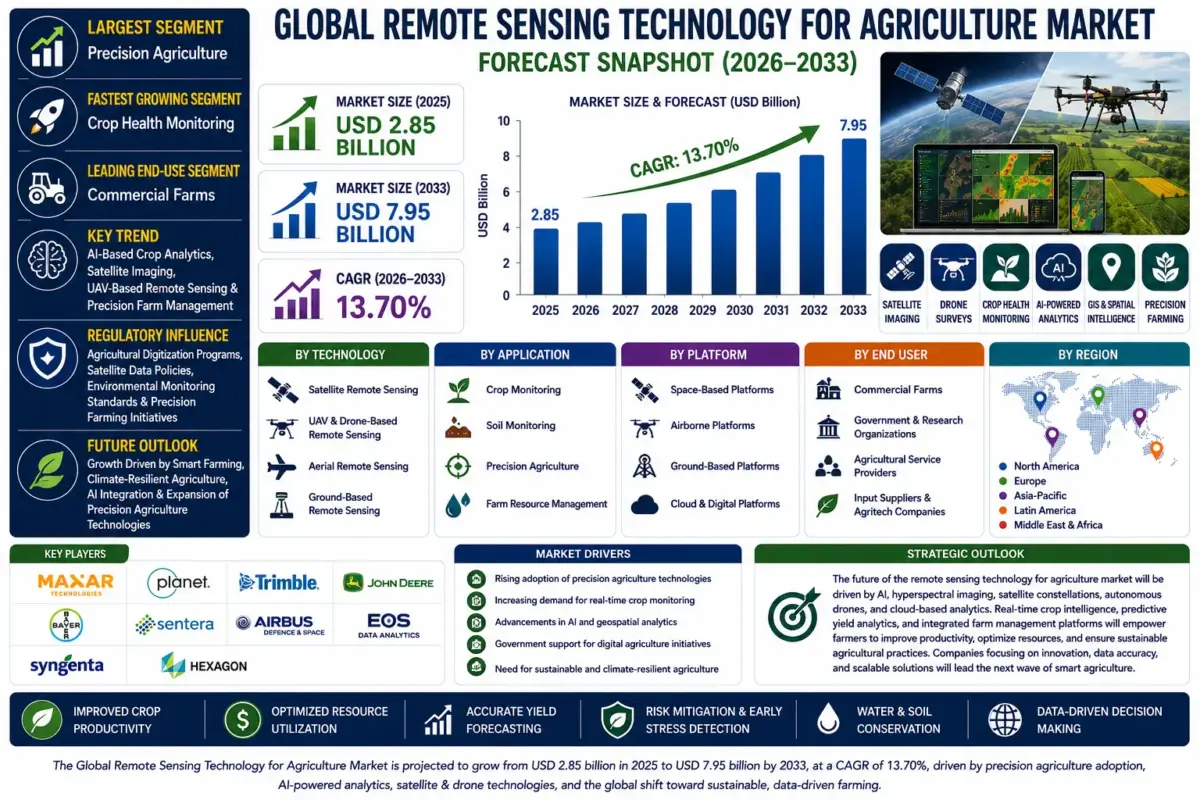

| Market Size (2025) | USD 2.85 Billion |

| Market Size (2033) | USD 7.95 Billion |

| CAGR (2026–2033) | 13.70% |

| Largest Segment | Precision Agriculture |

| Fastest Growing Segment | Crop Health Monitoring |

| Leading End-Use Segment | Commercial Farms |

| Key Trend | AI-Based Crop Analytics, Satellite Imaging, UAV-Based Remote Sensing & Precision Farm Management |

| Regulatory Influence | Agricultural Digitization Programs, Satellite Data Policies, Environmental Monitoring Standards & Precision Farming Initiatives |

| Future Outlook | Growth Driven by Smart Farming, Climate-Resilient Agriculture, AI Integration & Expansion of Precision Agriculture Technologies |

Global Remote Sensing Technology for Agriculture Market Size & Forecast

The Global Remote Sensing Technology for Agriculture Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 2.85 billion in 2025 and is projected to reach approximately USD 7.95 billion by 2033, registering a CAGR of 13.70%. Market growth is primarily driven by increasing adoption of precision agriculture, growing demand for real-time crop monitoring, rising utilization of satellite and drone-based imaging technologies, and expanding investments in digital agriculture. The need to improve agricultural productivity while optimizing resource utilization is further accelerating market expansion.Global Remote Sensing Technology for Agriculture Market Overview

Remote sensing technology for agriculture utilizes satellites, unmanned aerial vehicles (UAVs), aircraft, sensors, and geospatial analytics to monitor crop health, soil conditions, vegetation, irrigation, and environmental changes. These technologies provide high-resolution imagery and actionable insights that enable farmers, agribusinesses, research institutions, and government agencies to improve farm productivity, reduce operational costs, and support sustainable agricultural practices. Integration of artificial intelligence, cloud computing, GIS, and machine learning is transforming remote sensing into a core component of modern precision farming.Structural Drivers of Market Growth

1. Increasing Adoption of Precision Agriculture

Farmers are increasingly utilizing precision farming technologies to optimize irrigation, fertilizer application, crop monitoring, and resource management. Market Implications: Demand for remote sensing platforms supporting precision agriculture continues to increase globally.2. Growing Demand for Crop Health Monitoring

Satellite imagery, drones, and multispectral sensors enable early detection of crop stress, diseases, nutrient deficiencies, and pest infestations. Market Implications: Advanced crop monitoring technologies are improving agricultural productivity and reducing crop losses.3. Expansion of AI and Geospatial Analytics

Artificial intelligence, GIS platforms, and predictive analytics are improving image interpretation, yield forecasting, and farm decision-making. Market Implications: AI-powered remote sensing solutions are enhancing precision farming capabilities.4. Government Support for Digital Agriculture

Governments worldwide are promoting digital farming initiatives, satellite data accessibility, and sustainable agricultural practices. Market Implications: Public investments are accelerating adoption of remote sensing technologies across the agricultural sector.Global Remote Sensing Technology for Agriculture Market Segmentation

1. By Technology

1.1 Satellite Remote Sensing

1.1.1 Optical Satellite Imaging 1.1.1.1 Multispectral Imaging 1.1.1.1.1 Crop Health Monitoring 1.1.1.1.2 Vegetation Index Analysis 1.1.1.1.3 Soil Moisture Assessment 1.1.1.1.4 Crop Yield Estimation 1.1.2 Hyperspectral Satellite Imaging 1.1.3 Synthetic Aperture Radar (SAR) 1.1.4 Thermal Satellite Imaging1.2 UAV & Drone-Based Remote Sensing

1.2.1 Multirotor Drones 1.2.2 Fixed-Wing Drones 1.2.3 Hybrid UAV Systems 1.2.4 Autonomous Drone Platforms1.3 Aerial Remote Sensing

1.3.1 Aircraft-Based Imaging 1.3.2 Helicopter-Based Surveys 1.3.3 LiDAR Mapping 1.3.4 Thermal Aerial Imaging1.4 Ground-Based Remote Sensing

1.4.1 Field Sensors 1.4.2 IoT-Enabled Monitoring Systems 1.4.3 Mobile Remote Sensing Platforms 1.4.4 Smart Weather Stations2. By Application

2.1 Crop Monitoring

2.1.1 Crop Health Assessment 2.1.1.1 Vegetation Monitoring 2.1.1.1.1 NDVI Analysis 2.1.1.1.2 Disease Detection 2.1.1.1.3 Nutrient Deficiency Analysis 2.1.1.1.4 Growth Stage Monitoring 2.1.2 Crop Stress Detection 2.1.3 Yield Forecasting 2.1.4 Harvest Planning2.2 Soil Monitoring

2.2.1 Soil Moisture Monitoring 2.2.2 Soil Fertility Mapping 2.2.3 Soil Salinity Assessment 2.2.4 Soil Erosion Monitoring2.3 Precision Agriculture

2.3.1 Variable Rate Application 2.3.2 Irrigation Management 2.3.3 Fertilizer Optimization 2.3.4 Precision Spraying2.4 Farm Resource Management

2.4.1 Land Use Mapping 2.4.2 Water Resource Management 2.4.3 Field Boundary Mapping 2.4.4 Livestock Monitoring3. By Platform

3.1 Space-Based Platforms

3.1.1 Commercial Satellites 3.1.1.1 Earth Observation Satellites 3.1.1.1.1 High-Resolution Satellites 3.1.1.1.2 Medium-Resolution Satellites 3.1.1.1.3 Weather Satellites 3.1.1.1.4 CubeSats 3.1.2 Government Satellite Programs 3.1.3 Private Satellite Constellations 3.1.4 Low Earth Orbit (LEO) Satellites3.2 Airborne Platforms

3.2.1 Drones 3.2.2 Aircraft 3.2.3 Helicopters 3.2.4 High-Altitude Platforms3.3 Ground-Based Platforms

3.3.1 Fixed Monitoring Stations 3.3.2 Mobile Sensor Systems 3.3.3 Tractor-Mounted Sensors 3.3.4 Autonomous Field Robots3.4 Cloud & Digital Platforms

3.4.1 GIS Platforms 3.4.2 Cloud Analytics Platforms 3.4.3 AI-Based Decision Support Systems 3.4.4 Farm Management Software Integration4. By End User

4.1 Commercial Farms

4.1.1 Large-Scale Farms 4.1.1.1 Precision Farming Operations 4.1.1.1.1 Row Crop Farms 4.1.1.1.2 Plantation Farms 4.1.1.1.3 Horticulture Farms 4.1.1.1.4 Greenhouse Operations 4.1.2 Agribusiness Companies 4.1.3 Agricultural Cooperatives 4.1.4 Contract Farming Organizations4.2 Government & Research Organizations

4.2.1 Agricultural Research Institutes 4.2.2 Government Agriculture Departments 4.2.3 Environmental Agencies 4.2.4 Meteorological Organizations4.3 Agricultural Service Providers

4.3.1 Precision Agriculture Service Providers 4.3.2 Drone Service Companies 4.3.3 GIS & Mapping Providers 4.3.4 Agronomy Consultants4.4 Input Suppliers & Agritech Companies

4.4.1 Seed Companies 4.4.2 Fertilizer Manufacturers 4.4.3 Crop Protection Companies 4.4.4 Digital Agriculture Solution Providers5. By Region

5.1 North America 5.2 Europe 5.3 Asia-Pacific 5.4 Latin America 5.5 Middle East & AfricaRegional Market Dynamics

North America

Leading region supported by widespread adoption of precision agriculture, advanced satellite infrastructure, strong investment in agricultural technology, and high utilization of AI-powered farm management solutions.Europe

Driven by sustainable agriculture initiatives, digital farming policies, environmental monitoring programs, and increasing adoption of geospatial technologies.Asia-Pacific

Fastest-growing region supported by expanding agricultural modernization, government-backed smart farming initiatives, increasing drone adoption, and rising demand for food security.Latin America

Growing market driven by large-scale commercial farming, expanding precision agriculture adoption, and increasing investment in crop monitoring technologies.Middle East & Africa

Emerging market supported by water conservation initiatives, climate-smart agriculture programs, and growing investments in agricultural digitalization.Competitive Landscape

The Global Remote Sensing Technology for Agriculture Market is highly competitive with satellite imaging companies, agricultural technology providers, drone manufacturers, geospatial analytics firms, and precision farming solution providers focusing on AI-driven analytics, remote monitoring, and integrated digital agriculture platforms.Key Companies Operating in the Market Include:

- Maxar Technologies Inc.

- Planet Labs PBC

- Trimble Inc.

- John Deere

- Bayer AG (Climate FieldView)

- Sentera Inc.

- Airbus Defence and Space

- EOS Data Analytics

- Syngenta Group

- Hexagon AB

Strategic Outlook

The future of the remote sensing technology for agriculture market will be driven by artificial intelligence, hyperspectral imaging, satellite constellations, autonomous drones, cloud-based analytics, and precision farm management platforms. Organizations are increasingly investing in real-time crop intelligence, predictive yield analytics, automated field monitoring, and digital advisory solutions to improve farm productivity and sustainability. Integration with IoT devices, weather forecasting systems, and farm management software will further strengthen data-driven agricultural decision-making. Growing emphasis on climate-resilient agriculture, resource conservation, carbon farming, and sustainable food production will continue creating significant market opportunities. Companies focusing on AI-powered geospatial analytics, advanced remote sensing technologies, and integrated precision agriculture solutions will strengthen their competitive position in the global agricultural technology market.Final Market Perspective

The Global Remote Sensing Technology for Agriculture Market is becoming a vital component of modern smart farming and precision agriculture. Rising demand for data-driven farming, increasing adoption of satellite and drone technologies, expanding digital agriculture initiatives, and continuous advancements in AI and geospatial analytics are expected to support sustained market growth throughout the forecast period. Organizations delivering intelligent, scalable, and high-precision remote sensing solutions will be well-positioned to capitalize on long-term opportunities across the global agricultural technology ecosystem.Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Growth Highlights

1.3 Demand-Supply Overview

1.4 Key Strategic Insights

1.5 Analyst Viewpoint

2. Market Overview

2.1 Introduction to Global Remote Sensing Technology for Agriculture Market

2.2 Industry Value Chain Analysis

2.3 Market Evolution & Historical Trends

2.4 Macro-Economic Impact Analysis

2.5 Digital Agriculture & Precision Farming Transformation

2.6 AI-Based Crop Analytics, Satellite Imaging, UAV-Based Remote Sensing & Precision Farm Management

3. Global Remote Sensing Technology for Agriculture Market Forecast Snapshot (USD Billion), 2026–2033

3.1 2025 Market Size

3.2 2033 Market Size

3.3 CAGR (2026–2033)

3.4 Largest Region

3.5 Fastest Growing Region

3.6 Largest Segment

3.7 Key Trend

3.8 Future Outlook

4. Key Drivers of Market Growth

4.1 Increasing Adoption of Precision Agriculture

4.2 Growing Demand for Crop Health Monitoring

4.3 Expansion of AI & Geospatial Analytics

4.4 Government Support for Digital Agriculture

4.5 Integration of Satellite Imaging, UAVs & Cloud-Based Farm Intelligence Platforms

5. Market Challenges

5.1 High Deployment & Technology Integration Costs

5.2 Limited Connectivity & Digital Infrastructure in Rural Areas

5.3 Data Privacy, Satellite Data Accessibility & Regulatory Compliance

5.4 Technical Skill Gaps & Adoption Barriers Among Farmers

6. Market Segmentation by Technology (USD Billion), 2026–2033

6.1 Satellite Remote Sensing

6.1.1 Optical Satellite Imaging

6.1.1.1 Multispectral Imaging

6.1.1.1.1 Crop Health Monitoring

6.1.1.1.2 Vegetation Index Analysis

6.1.1.1.3 Soil Moisture Assessment

6.1.1.1.4 Crop Yield Estimation

6.1.2 Hyperspectral Satellite Imaging

6.1.3 Synthetic Aperture Radar (SAR)

6.1.4 Thermal Satellite Imaging

6.2 UAV & Drone-Based Remote Sensing

6.2.1 Multirotor Drones

6.2.2 Fixed-Wing Drones

6.2.3 Hybrid UAV Systems

6.2.4 Autonomous Drone Platforms

6.3 Aerial Remote Sensing

6.3.1 Aircraft-Based Imaging

6.3.2 Helicopter-Based Surveys

6.3.3 LiDAR Mapping

6.3.4 Thermal Aerial Imaging

6.4 Ground-Based Remote Sensing

6.4.1 Field Sensors

6.4.2 IoT-Enabled Monitoring Systems

6.4.3 Mobile Remote Sensing Platforms

6.4.4 Smart Weather Stations

7. Market Segmentation by Application (USD Billion), 2026–2033

7.1 Crop Monitoring

7.1.1 Crop Health Assessment

7.1.1.1 Vegetation Monitoring

7.1.1.1.1 NDVI Analysis

7.1.1.1.2 Disease Detection

7.1.1.1.3 Nutrient Deficiency Analysis

7.1.1.1.4 Growth Stage Monitoring

7.1.2 Crop Stress Detection

7.1.3 Yield Forecasting

7.1.4 Harvest Planning

7.2 Soil Monitoring

7.2.1 Soil Moisture Monitoring

7.2.2 Soil Fertility Mapping

7.2.3 Soil Salinity Assessment

7.2.4 Soil Erosion Monitoring

7.3 Precision Agriculture

7.3.1 Variable Rate Application

7.3.2 Irrigation Management

7.3.3 Fertilizer Optimization

7.3.4 Precision Spraying

7.4 Farm Resource Management

7.4.1 Land Use Mapping

7.4.2 Water Resource Management

7.4.3 Field Boundary Mapping

7.4.4 Livestock Monitoring

8. Market Segmentation by Platform (USD Billion), 2026–2033

8.1 Space-Based Platforms

8.1.1 Commercial Satellites

8.1.1.1 Earth Observation Satellites

8.1.1.1.1 High-Resolution Satellites

8.1.1.1.2 Medium-Resolution Satellites

8.1.1.1.3 Weather Satellites

8.1.1.1.4 CubeSats

8.1.2 Government Satellite Programs

8.1.3 Private Satellite Constellations

8.1.4 Low Earth Orbit (LEO) Satellites

8.2 Airborne Platforms

8.2.1 Drones

8.2.2 Aircraft

8.2.3 Helicopters

8.2.4 High-Altitude Platforms

8.3 Ground-Based Platforms

8.3.1 Fixed Monitoring Stations

8.3.2 Mobile Sensor Systems

8.3.3 Tractor-Mounted Sensors

8.3.4 Autonomous Field Robots

8.4 Cloud & Digital Platforms

8.4.1 GIS Platforms

8.4.2 Cloud Analytics Platforms

8.4.3 AI-Based Decision Support Systems

8.4.4 Farm Management Software Integration

9. Market Segmentation by End User (USD Billion), 2026–2033

9.1 Commercial Farms

9.1.1 Large-Scale Farms

9.1.1.1 Precision Farming Operations

9.1.1.1.1 Row Crop Farms

9.1.1.1.2 Plantation Farms

9.1.1.1.3 Horticulture Farms

9.1.1.1.4 Greenhouse Operations

9.1.2 Agribusiness Companies

9.1.3 Agricultural Cooperatives

9.1.4 Contract Farming Organizations

9.2 Government & Research Organizations

9.2.1 Agricultural Research Institutes

9.2.2 Government Agriculture Departments

9.2.3 Environmental Agencies

9.2.4 Meteorological Organizations

9.3 Agricultural Service Providers

9.3.1 Precision Agriculture Service Providers

9.3.2 Drone Service Companies

9.3.3 GIS & Mapping Providers

9.3.4 Agronomy Consultants

9.4 Input Suppliers & Agritech Companies

9.4.1 Seed Companies

9.4.2 Fertilizer Manufacturers

9.4.3 Crop Protection Companies

9.4.4 Digital Agriculture Solution Providers

10. Market Segmentation by Region (USD Billion), 2026–2033

10.1 North America

10.2 Europe

10.3 Asia-Pacific

10.4 Latin America

10.5 Middle East & Africa

11. Regional Market Analysis

11.1 North America – Market Leader

11.2 Asia-Pacific – Fastest Growing Region

11.3 Europe – Sustainable Agriculture & Precision Farming Market

11.4 Latin America – Expanding Commercial Farming & Crop Monitoring Technologies

11.5 Middle East & Africa – Emerging Climate-Smart Agriculture Market

12. Competitive Landscape

12.1 Market Share Analysis

12.2 Competitive Positioning Matrix

12.3 Strategic Developments (M&A, Product Launches, Partnerships)

12.4 Innovation Benchmarking

12.5 AI, Satellite Imaging & Precision Agriculture Technology Assessment

13. Company Profiles

13.1 Maxar Technologies Inc.

13.2 Planet Labs PBC

13.3 Trimble Inc.

13.4 John Deere

13.5 Bayer AG (Climate FieldView)

13.6 Sentera Inc.

13.7 Airbus Defence and Space

13.8 EOS Data Analytics

13.9 Syngenta Group

13.10 Hexagon AB

14. Strategic Intelligence & AI-Driven Insights

14.1 Pheonix Demand Forecast Engine

14.2 Agricultural Remote Sensing Analytics Dashboard

14.3 AI-Powered Crop Intelligence & Yield Prediction

14.4 Precision Agriculture Optimization Engine

14.5 Smart Farming & Geospatial Intelligence Platform

15. Investment & Growth Opportunities

15.1 Precision Agriculture Technologies

15.2 AI-Based Crop Analytics & Predictive Farming

15.3 Satellite Imaging & UAV-Based Remote Sensing Solutions

15.4 Cloud-Based Agricultural Intelligence Platforms

15.5 Climate-Resilient Agriculture & Digital Farming Infrastructure

16. Why the Global Remote Sensing Technology for Agriculture Market Remains Critical

16.1 Increasing Adoption of Precision Agriculture

16.2 Rising Demand for Real-Time Crop Monitoring

16.3 AI-Driven Agricultural Intelligence & Precision Farm Management

16.4 Growing Focus on Sustainable & Climate-Resilient Farming

16.5 Long-Term Growth Across Smart Agriculture & Digital Farming Markets

17. Appendix

18. About Pheonix Research

19. Disclaimer

Competitive Landscape

Global Remote Sensing Technology for Agriculture Market Competitive Intensity & Market Structure Overview

The Global Remote Sensing Technology for Agriculture Market is highly competitive and characterized by the presence of satellite imaging companies, agricultural technology providers, drone manufacturers, geospatial analytics firms, precision farming solution providers, and digital agriculture platform developers. Competitive intensity is driven by artificial intelligence-powered analytics, satellite imaging capabilities, UAV technologies, geospatial intelligence, cloud-based analytics platforms, precision agriculture expertise, and integration with digital farm management ecosystems.

Companies compete across multiple remote sensing segments including satellite remote sensing, UAV and drone-based monitoring, aerial imaging, ground-based sensing, crop health monitoring, soil analysis, precision agriculture, yield forecasting, and farm resource management. Growing adoption of smart farming, rising demand for real-time agricultural intelligence, increasing climate-related challenges, and expanding investments in digital agriculture are intensifying competition while encouraging continuous innovation in remote sensing technologies.

The market structure is evolving toward AI-powered crop analytics, hyperspectral imaging, autonomous drone platforms, cloud-based geospatial intelligence, predictive agricultural analytics, IoT-enabled field monitoring, and integrated precision farming platforms. Market participants are investing heavily in advanced imaging technologies, machine learning algorithms, digital agriculture platforms, and strategic partnerships to strengthen market positioning and improve agricultural productivity.

Global Remote Sensing Technology for Agriculture Market Competitive Intensity & Market Structure Current Scenario

Leading Global Remote Sensing Technology for Agriculture Companies

- Maxar Technologies Inc.: A leading satellite imagery and geospatial intelligence company providing high-resolution Earth observation data, agricultural monitoring solutions, and advanced geospatial analytics.

- Planet Labs PBC: A global Earth observation company delivering high-frequency satellite imagery, crop monitoring services, environmental intelligence, and precision agriculture analytics.

- Trimble Inc.: A leading precision agriculture technology provider offering GNSS solutions, remote sensing technologies, farm management software, and geospatial analytics platforms.

- John Deere: A global agricultural equipment manufacturer integrating precision farming technologies, AI-enabled crop monitoring, remote sensing capabilities, and digital farm management solutions.

- Bayer AG (Climate FieldView): A digital agriculture platform provider offering satellite imagery, field analytics, crop performance monitoring, predictive insights, and precision farming decision support.

- Sentera Inc.: A precision agriculture company specializing in drone-based remote sensing, multispectral imaging, crop health analytics, and field intelligence solutions.

- Airbus Defence and Space: A satellite imaging and geospatial solutions provider delivering Earth observation services, agricultural monitoring, environmental intelligence, and precision farming support.

- EOS Data Analytics: A geospatial analytics company providing satellite-based crop monitoring, vegetation analysis, yield forecasting, and digital agriculture intelligence platforms.

- Syngenta Group: A global agricultural technology company integrating digital farming platforms, remote sensing technologies, agronomic analytics, and crop management solutions.

- Hexagon AB: A technology company offering geospatial intelligence, remote sensing solutions, precision agriculture technologies, positioning systems, and agricultural data analytics.

Key Competitive Intensity & Market Structure Drivers

Increasing adoption of precision agriculture, growing demand for crop health monitoring, and expanding investments in smart farming technologies are intensifying competition among remote sensing technology providers worldwide.

Advancements in artificial intelligence, machine learning, hyperspectral imaging, satellite constellations, UAV technologies, and cloud-based geospatial analytics are becoming major competitive differentiators across the market.

Growing demand for precision crop management, predictive yield forecasting, soil monitoring, irrigation optimization, and climate-resilient farming is strengthening market competitiveness while improving agricultural productivity.

Strategic collaborations among satellite companies, agritech providers, drone manufacturers, research institutions, government agencies, and digital agriculture platform providers are accelerating innovation, expanding solution capabilities, and enhancing farm decision-making.

Continuous investment in AI-powered analytics, autonomous drone systems, cloud-based farm intelligence platforms, IoT-enabled monitoring, precision agriculture technologies, and integrated digital farming ecosystems is enabling companies to improve operational efficiency and long-term competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Companies with comprehensive remote sensing platforms, advanced geospatial analytics capabilities, and integrated digital agriculture ecosystems are expected to maintain significant competitive advantages.

Investment in artificial intelligence, satellite imaging, drone technologies, predictive analytics, IoT-enabled monitoring, and cloud-based farm intelligence platforms is becoming increasingly important for long-term market leadership.

Organizations focusing on expanding precision agriculture capabilities, improving crop intelligence, strengthening predictive analytics, and enhancing digital farming experiences are likely to increase revenue growth and market share.

Strategic partnerships with agritech companies, satellite operators, drone manufacturers, government agencies, agricultural cooperatives, and research institutions are supporting innovation, operational efficiency, and international market expansion.

Businesses capable of combining technological innovation, geospatial intelligence, agricultural expertise, operational scalability, and integrated precision farming solutions will be best positioned to compete effectively in the evolving global remote sensing technology for agriculture market.

Global Remote Sensing Technology for Agriculture Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global remote sensing technology for agriculture market is expected to become increasingly AI-driven, digitally connected, and precision agriculture-focused as demand for intelligent farming solutions continues to expand globally.

Future competition will be shaped by AI-based crop analytics, hyperspectral imaging, autonomous drone fleets, next-generation satellite constellations, cloud-native geospatial platforms, and predictive agricultural intelligence technologies.

Market participants are expected to increase investments in digital agriculture infrastructure, real-time crop monitoring platforms, advanced remote sensing technologies, automated field intelligence, and integrated precision farming ecosystems to strengthen competitive positioning.

Over the forecast period, companies that successfully combine technological innovation, agricultural expertise, geospatial intelligence, operational scalability, and comprehensive remote sensing solutions will be best positioned to lead the evolving global remote sensing technology for agriculture market.

Value Chain

Global Remote Sensing Technology for Agriculture Market Value Chain & Supply Chain Evolution Overview

The Global Remote Sensing Technology for Agriculture Market operates through an integrated agricultural technology value chain comprising satellite data acquisition, UAV and sensor manufacturing, geospatial imaging, AI-powered analytics, cloud platform integration, precision agriculture software development, farm advisory services, system deployment, digital farm management, and customer support. The ecosystem includes satellite operators, drone manufacturers, sensor developers, geospatial analytics providers, cloud platform vendors, agritech companies, precision farming solution providers, agricultural cooperatives, research institutions, government agencies, and commercial farms collaborating to deliver intelligent remote sensing solutions across modern agriculture.

The industry is being driven by increasing adoption of precision agriculture, rising demand for real-time crop monitoring, expanding utilization of satellite and drone-based imaging, growing investments in digital agriculture, and increasing emphasis on sustainable farming practices. Agricultural stakeholders are increasingly investing in AI-powered crop analytics, multispectral imaging, GIS platforms, cloud-based farm management systems, and predictive agricultural intelligence to improve productivity, optimize resource utilization, and strengthen climate-resilient farming.

The integration of artificial intelligence, machine learning, geospatial information systems (GIS), IoT-enabled field sensors, cloud computing, satellite constellations, UAV technologies, hyperspectral imaging, predictive analytics, and digital farm management platforms has significantly optimized the agricultural remote sensing value chain. Organizations are strengthening collaboration between satellite data providers, agritech companies, drone service providers, agricultural consultants, and commercial farming enterprises while expanding intelligent precision agriculture ecosystems.

Advancements in AI-based crop analytics, hyperspectral imaging, autonomous UAV platforms, cloud-native geospatial analytics, precision irrigation technologies, digital decision support systems, and real-time environmental monitoring are transforming supply chain operations while improving farm productivity, crop health assessment, resource efficiency, sustainability, and agricultural decision-making across the global remote sensing technology ecosystem.

Global Remote Sensing Technology for Agriculture Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Satellite, Sensor & Hardware Development: Development and manufacturing of Earth observation satellites, UAVs, multispectral and hyperspectral sensors, LiDAR systems, thermal imaging devices, IoT field sensors, weather stations, GPS modules, and agricultural monitoring equipment.

- Data Acquisition, Platform Integration & Analytics: Satellite imaging, drone-based surveys, aerial mapping, GIS integration, cloud computing, AI-powered image processing, predictive analytics, farm management software integration, and geospatial data visualization.

- Precision Agriculture & Farm Intelligence: Crop health monitoring, vegetation analysis, soil assessment, irrigation management, yield forecasting, pest detection, fertilizer optimization, field mapping, and precision farm management.

- Quality Assurance & Regulatory Compliance: Satellite data validation, sensor calibration, image accuracy verification, environmental monitoring, agricultural data governance, system certification, and compliance with agricultural digitization programs, satellite data policies, environmental monitoring standards, and precision farming initiatives.

- Deployment, Integration & Professional Services: Precision agriculture consulting, UAV deployment, GIS implementation, cloud platform deployment, agronomy consulting, technical integration, operator training, and digital agriculture implementation services.

- Operations, Maintenance & Customer Support: Cloud platform management, AI model optimization, software updates, technical support, remote monitoring, predictive maintenance, agronomic advisory services, and lifecycle platform management.

- End User Applications: Deployment of remote sensing technologies across commercial farms, agribusiness companies, agricultural cooperatives, government agriculture departments, research institutions, environmental agencies, agronomy service providers, and digital agriculture solution providers.

Company-to-Stage Mapping

- Satellite, Sensor & Hardware Development: Satellite manufacturers, drone manufacturers, multispectral sensor developers, IoT device manufacturers, imaging technology companies, GPS solution providers, and agricultural equipment manufacturers.

- Data Acquisition, Platform Integration & Analytics: Maxar Technologies Inc., Planet Labs PBC, Trimble Inc., Airbus Defence and Space, EOS Data Analytics, Hexagon AB, Bayer AG (Climate FieldView), John Deere, Sentera Inc., and Syngenta Group.

- Precision Agriculture & Farm Intelligence: AI analytics providers, GIS solution providers, precision agriculture software companies, agritech firms, farm management platform providers, agricultural data analytics companies, and remote sensing technology vendors.

- Deployment, Integration & Professional Services: Precision agriculture consultants, drone service providers, GIS implementation partners, agronomy consultants, cloud integration companies, agricultural technology service providers, and digital farming consultants.

- Operations, Maintenance & Customer Support: Maxar Technologies Inc., Planet Labs PBC, Trimble Inc., John Deere, Bayer AG (Climate FieldView), EOS Data Analytics, cloud service providers, and agricultural technology support organizations.

- Quality Assurance & Regulatory Compliance: Agricultural regulatory authorities, satellite data agencies, environmental monitoring organizations, certification bodies, agricultural research institutes, data governance authorities, and quality assurance organizations.

- End User Applications: Commercial farms, agricultural cooperatives, agribusiness companies, government agriculture departments, research institutions, environmental agencies, precision agriculture service providers, and agritech solution providers.

Key Value Chain & Supply Chain Evolution Signals in Global Remote Sensing Technology for Agriculture Market

Expansion of AI-Based Precision Agriculture

Agricultural organizations are increasingly deploying artificial intelligence for crop health analysis, yield prediction, irrigation optimization, disease detection, and precision farm management to improve agricultural productivity and operational efficiency.

Growing Adoption of Satellite and UAV-Based Monitoring

Commercial satellites, drone platforms, multispectral imaging, hyperspectral sensing, and thermal imaging technologies are enabling continuous farm monitoring, early crop stress detection, and high-resolution agricultural intelligence.

Rapid Integration of Cloud-Based Geospatial Platforms

Cloud-native GIS platforms, AI-powered analytics engines, digital farm management software, and remote sensing dashboards are enabling centralized agricultural data management and real-time decision support.

Increasing Investment in Smart Farming Infrastructure

IoT-enabled field sensors, weather monitoring systems, precision irrigation technologies, autonomous drones, and connected agricultural equipment are improving farm automation and resource optimization.

Strengthening Predictive Agricultural Analytics

Machine learning, geospatial analytics, digital twins, and predictive crop intelligence are enabling proactive farm planning, yield forecasting, environmental monitoring, and sustainable agricultural management.

Expansion of Climate-Smart Agriculture Solutions

Governments and agribusiness organizations are investing in climate-resilient farming technologies, carbon farming initiatives, water conservation programs, and sustainable precision agriculture platforms to strengthen long-term food security.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Intelligent Agricultural Technologies

Artificial intelligence, satellite imaging, UAV technologies, predictive analytics, and geospatial intelligence improve agricultural productivity, crop monitoring, resource efficiency, and operational decision-making.

Expansion of Cloud-Based Agricultural Ecosystems

Cloud-native analytics platforms, GIS integration, digital farm management systems, and AI-powered advisory services strengthen agricultural visibility while supporting scalable precision farming operations.

Strengthening Precision Agriculture Capabilities

Advanced sensing technologies, autonomous drones, precision irrigation, variable-rate application systems, and digital crop intelligence improve farming efficiency while reducing resource consumption.

Optimization of Agricultural Data Intelligence

Real-time satellite monitoring, sensor integration, predictive analytics, environmental data platforms, and AI-driven insights improve agricultural planning and farm productivity.

Enhancement of Regulatory and Environmental Compliance

Digital monitoring systems, satellite-based environmental assessment, precision farming technologies, and standardized agricultural data platforms improve compliance with sustainability initiatives and agricultural digitization programs.

Leveraging Sustainable Smart Farming Strategies

Climate-resilient agriculture, water conservation, precision resource management, carbon farming initiatives, and integrated digital agriculture ecosystems enable sustainable farming while strengthening long-term agricultural competitiveness.

Global Remote Sensing Technology for Agriculture Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the remote sensing technology for agriculture value chain is expected to become increasingly intelligent, AI-driven, and digitally connected. Continued advancements in satellite constellations, autonomous drones, hyperspectral imaging, cloud-native analytics, geospatial intelligence, and precision farm management platforms will further improve agricultural productivity, sustainability, operational efficiency, and climate resilience.

Key Future Developments Include:

- Expansion of AI-powered crop monitoring and predictive agricultural analytics platforms.

- Increasing adoption of hyperspectral imaging, satellite constellations, and autonomous UAV technologies.

- Greater integration of IoT-enabled field sensors, GIS platforms, cloud analytics, and digital farm management systems.

- Broader deployment of precision irrigation, automated crop intelligence, and climate-smart farming technologies.

- Growing investment in sustainable agriculture infrastructure, carbon farming initiatives, and resource optimization solutions.

- Strengthening collaborations between satellite operators, agritech companies, drone manufacturers, government agencies, agricultural research organizations, and commercial farming enterprises.

As the market evolves, competitive advantage will increasingly depend on intelligent geospatial analytics, AI-powered agricultural intelligence, scalable cloud platforms, advanced sensing technologies, precision agriculture capabilities, sustainable farming innovation, and digitally connected agricultural ecosystems.

Companies that successfully integrate artificial intelligence, satellite imaging, autonomous UAV platforms, cloud-based analytics, precision agriculture technologies, IoT-enabled monitoring systems, and comprehensive digital farming solutions will be well-positioned to achieve long-term growth in the Global Remote Sensing Technology for Agriculture Market.

Investment Activity

Global Remote Sensing Technology for Agriculture Market Investment & Funding Dynamics Overview (2026–2033)

The Global Remote Sensing Technology for Agriculture Market is witnessing strong investment momentum driven by the increasing adoption of precision agriculture, rising demand for real-time crop monitoring, expanding digital agriculture initiatives, and rapid integration of artificial intelligence with geospatial technologies. Satellite imaging companies, agritech firms, drone manufacturers, geospatial analytics providers, venture capital investors, private equity firms, government agencies, and agricultural technology enterprises are actively investing in AI-powered crop analytics, satellite imaging platforms, UAV-based remote sensing solutions, hyperspectral imaging technologies, cloud-based geospatial analytics, and precision farm management systems.

Investment activity is accelerating as agricultural stakeholders focus on improving farm productivity, optimizing resource utilization, enhancing crop health monitoring, and strengthening climate-resilient farming practices. Capital allocation is increasingly directed toward high-resolution satellite constellations, autonomous agricultural drones, IoT-enabled field sensors, GIS platforms, predictive crop analytics, cloud-based farm intelligence platforms, and integrated precision agriculture technologies.

Additionally, growing investments in digital agriculture ecosystems, AI-driven decision support systems, smart irrigation technologies, carbon farming solutions, environmental monitoring platforms, and sustainable precision farming infrastructure are creating substantial long-term opportunities across the global remote sensing technology for agriculture ecosystem.

Current Investment & Funding Landscape

The current investment landscape reflects active participation from satellite operators, agricultural technology companies, UAV manufacturers, geospatial software providers, research institutions, government agencies, institutional investors, and technology-focused venture capital firms. Industry participants are investing heavily in satellite remote sensing platforms, AI-enabled crop monitoring, drone-based agricultural imaging, cloud analytics, digital farm management, and precision agriculture solutions.

Significant funding is being directed toward hyperspectral imaging technologies, Earth observation satellites, UAV automation, AI-powered geospatial analytics, IoT-enabled agricultural monitoring systems, and predictive crop intelligence platforms to improve agricultural productivity and strengthen long-term competitive positioning.

Strategic collaborations among satellite imaging companies, agritech providers, drone manufacturers, cloud platform vendors, agricultural research organizations, government agencies, and farm management software developers are accelerating innovation, improving data interoperability, and expanding intelligent precision farming capabilities worldwide.

Key Investment & Funding Dynamics Signals

- Growing investment in AI-powered crop analytics platforms and precision agriculture technologies is improving farm productivity and resource optimization.

- Expansion of satellite imaging infrastructure, hyperspectral sensors, and cloud-based geospatial analytics platforms is attracting substantial funding across agricultural technology markets.

- Increasing capital allocation toward UAV-based remote sensing, autonomous agricultural drones, IoT-enabled field monitoring, and multispectral imaging systems is strengthening real-time crop intelligence capabilities.

- Rising investment in predictive yield forecasting, GIS platforms, digital farm management systems, and AI-enabled decision support technologies is enhancing agricultural planning and operational efficiency.

- Strategic funding for climate-smart agriculture solutions, smart irrigation technologies, carbon farming platforms, and environmental monitoring systems is supporting long-term agricultural sustainability.

- Growing collaboration between satellite operators, agritech companies, drone manufacturers, cloud technology providers, research institutions, and government agencies is accelerating technology innovation and market expansion.

- Expansion of precision agriculture infrastructure across commercial farms, agricultural cooperatives, research organizations, and digital agriculture service providers is creating attractive long-term investment opportunities globally.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in AI-driven remote sensing technologies, satellite analytics, and precision agriculture platforms will be essential for sustaining long-term competitive advantage.

- Capital allocation toward autonomous drones, geospatial analytics, cloud infrastructure, and real-time agricultural monitoring will strengthen farm productivity and operational efficiency.

- Companies developing integrated digital agriculture ecosystems, advanced crop intelligence platforms, and scalable precision farming solutions are expected to secure stronger competitive positions.

- Strategic partnerships among satellite providers, agritech companies, UAV manufacturers, cloud platform vendors, agricultural enterprises, and technology integrators will accelerate innovation and digital agriculture transformation.

- Investments in artificial intelligence, GIS, IoT, machine learning, remote sensing technologies, and predictive agricultural analytics will enhance decision-making, sustainability, and resource management.

- Compliance with agricultural digitization programs, satellite data policies, environmental monitoring standards, and precision farming initiatives will continue influencing investment decisions.

- Organizations building integrated capabilities across satellite imaging, drone technologies, geospatial analytics, cloud computing, AI-powered farm intelligence, and precision agriculture platforms are expected to capture significant long-term value.

Forward Outlook

Looking ahead, the Global Remote Sensing Technology for Agriculture Market is expected to maintain strong investment momentum driven by expanding precision agriculture, increasing adoption of satellite and drone technologies, accelerating AI integration, and growing demand for climate-resilient farming solutions.

Future capital deployment will increasingly focus on AI-powered crop analytics, hyperspectral imaging, autonomous drone platforms, cloud-based agricultural intelligence, predictive yield analytics, and integrated precision farm management systems.

As governments, agribusinesses, and commercial farms continue investing in agricultural digitalization and smart farming infrastructure, investment activity is expected to expand across satellite constellations, remote sensing platforms, UAV technologies, IoT-enabled monitoring systems, digital agriculture ecosystems, and geospatial analytics platforms.

In conclusion, the Global Remote Sensing Technology for Agriculture Market represents a highly attractive investment landscape where AI-powered crop intelligence, satellite imaging, UAV-based remote sensing, cloud geospatial analytics, and precision agriculture technologies will define future funding priorities, competitive differentiation, and long-term market growth.

Technology & Innovation

Global Remote Sensing Technology for Agriculture Market Technology & Innovation Landscape Overview

The Global Remote Sensing Technology for Agriculture Market is witnessing rapid technological advancement as artificial intelligence (AI), satellite imaging, unmanned aerial vehicles (UAVs), geospatial analytics, cloud computing, and Internet of Things (IoT) technologies transform modern farming practices. Agricultural technology companies, satellite service providers, drone manufacturers, research institutions, and agribusiness organizations are investing in advanced remote sensing solutions to improve crop monitoring, optimize resource utilization, enhance yield forecasting, and support sustainable agriculture. These innovations are enabling farmers to make data-driven decisions while improving productivity, operational efficiency, and environmental stewardship.

The market is also benefiting from advancements in hyperspectral imaging, synthetic aperture radar (SAR), Geographic Information Systems (GIS), machine learning algorithms, cloud-based analytics platforms, and precision agriculture technologies. These innovations are improving image accuracy, accelerating agricultural data analysis, enhancing field-level monitoring, and supporting intelligent farm management. As demand for climate-resilient and precision farming continues to grow, technology is becoming a critical driver of agricultural innovation and long-term market expansion.

Global Remote Sensing Technology for Agriculture Market Technology & Innovation Current Scenario

Current innovation within the remote sensing technology for agriculture market is primarily focused on AI-based crop analytics, satellite imaging, UAV-based remote sensing, precision farm management, and geospatial intelligence. Organizations are increasingly utilizing multispectral and hyperspectral imaging, Earth observation satellites, autonomous drones, and AI-powered analytics to monitor crop health, assess soil conditions, detect diseases, forecast yields, and optimize agricultural operations. Artificial intelligence is playing an expanding role in processing remote sensing data, identifying crop stress, and supporting predictive farm management.

Cloud-based GIS platforms, IoT-enabled field sensors, autonomous drone systems, and advanced decision support platforms are enhancing agricultural productivity through real-time monitoring and large-scale data analysis. In addition, advancements in satellite constellations, digital farm management platforms, LiDAR mapping, and predictive analytics are improving operational efficiency and enabling precision agriculture across commercial farms and agribusinesses. These innovations are strengthening the industry’s ability to deliver intelligent, data-driven agricultural solutions.

Key Technology & Innovation Trends in Global Remote Sensing Technology for Agriculture Market

- AI-Based Crop Analytics: Utilizing artificial intelligence to analyze crop conditions, detect plant stress, and improve agricultural decision-making.

- Satellite Imaging Technologies: Enabling continuous monitoring of crop health, vegetation, soil conditions, and environmental changes through high-resolution Earth observation imagery.

- UAV-Based Remote Sensing: Deploying drones equipped with multispectral, hyperspectral, thermal, and RGB sensors for field-level agricultural monitoring.

- Precision Farm Management: Supporting optimized irrigation, fertilization, pesticide application, and resource utilization through precision agriculture technologies.

- Geospatial Analytics & GIS Platforms: Enhancing agricultural mapping, spatial analysis, land management, and field planning through advanced geospatial intelligence.

- Hyperspectral & Multispectral Imaging: Improving crop health assessment, disease detection, nutrient analysis, and vegetation monitoring with advanced imaging technologies.

- IoT-Enabled Field Monitoring: Integrating connected sensors, smart weather stations, and environmental monitoring systems for real-time farm intelligence.

- Cloud-Based Agricultural Analytics: Delivering scalable analytics, remote accessibility, and centralized agricultural data management through cloud platforms.

- Predictive Yield Analytics: Applying machine learning and predictive models to forecast crop yields, optimize harvest planning, and improve farm productivity.

- Digital Farm Decision Support Systems: Providing real-time recommendations for crop management, irrigation scheduling, and resource optimization using integrated agricultural intelligence platforms.

Strategic Implications of Technology & Innovation

Technological advancements are enabling remote sensing solution providers to improve agricultural intelligence, optimize farm operations, and strengthen competitive positioning. Organizations investing in artificial intelligence, satellite technologies, UAV platforms, cloud analytics, and geospatial intelligence are enhancing crop productivity, reducing resource consumption, and improving farm management efficiency. Innovation is helping companies differentiate through real-time agricultural insights, advanced predictive capabilities, and precision farming solutions.

As digital agriculture continues to expand globally, organizations are increasingly focusing on integrated precision farming ecosystems, cloud-enabled analytics platforms, and AI-powered agricultural decision support systems. Businesses that successfully integrate remote sensing technologies, IoT connectivity, advanced analytics, and farm management software are expected to gain significant competitive advantages. However, agricultural digitization programs, satellite data policies, environmental monitoring standards, and precision farming initiatives remain critical factors influencing technology adoption and deployment.

Global Remote Sensing Technology for Agriculture Market Technology & Innovation Forward Outlook

The future of the Global Remote Sensing Technology for Agriculture Market is expected to be shaped by continued advancements in artificial intelligence, hyperspectral imaging, satellite constellations, autonomous drones, cloud-based analytics, precision agriculture, and digital farm management technologies. Emerging innovations such as AI-powered crop intelligence, autonomous field monitoring, advanced geospatial analytics, digital twins for agriculture, and next-generation Earth observation systems are expected to redefine precision farming. Organizations are likely to increase investments in intelligent agricultural platforms that improve scalability, sustainability, and farm productivity.

As demand for smart farming, climate-resilient agriculture, sustainable food production, and data-driven crop management continues to grow, technology will play an increasingly important role in driving market development. The combination of artificial intelligence, satellite imaging, UAV-based remote sensing, IoT connectivity, cloud analytics, and precision agriculture technologies is expected to create substantial growth opportunities while strengthening the long-term evolution of the global remote sensing technology for agriculture market.

Market Risk

Global Remote Sensing Technology for Agriculture Market Risk Factors & Disruption Threats Overview

The global Remote Sensing Technology for Agriculture market is expanding rapidly as precision agriculture, AI-powered crop analytics, satellite imaging, and UAV-based monitoring become increasingly essential for improving agricultural productivity and sustainability. Despite strong market growth, technology providers, agribusinesses, and agricultural organizations face a range of technological, regulatory, operational, and environmental risks that may influence deployment efficiency and long-term market adoption. Increasing dependence on satellite infrastructure, evolving agricultural data governance policies, cybersecurity concerns, climate variability, and integration complexity across digital farming platforms continue to reshape the competitive landscape. Companies are investing in AI-enabled analytics, cloud-based geospatial platforms, advanced sensor technologies, autonomous drones, and secure agricultural data ecosystems to strengthen operational resilience and support sustainable market growth.

Global Remote Sensing Technology for Agriculture Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by growing adoption of satellite remote sensing, drone-based crop monitoring, geospatial analytics, and precision farming technologies across commercial farms, agribusinesses, research institutions, and government agencies. However, organizations continue to face challenges related to high implementation costs, limited digital infrastructure in rural regions, weather-related imaging limitations, fragmented agricultural datasets, and integration challenges with farm management systems. Compliance with evolving satellite data policies, environmental monitoring standards, agricultural digitization programs, and data privacy regulations has become increasingly important, requiring continuous investment in secure, scalable, and interoperable remote sensing solutions.

Key Risk Factors & Disruption Threat Signals in Global Remote Sensing Technology for Agriculture Market

Major risk factors include disruptions to satellite communication infrastructure, cybersecurity threats targeting cloud-based agricultural platforms, drone operational restrictions, and inaccurate data collection caused by adverse weather conditions, potentially affecting decision-making and farm productivity. Integration challenges across satellite imagery, UAV platforms, IoT sensors, GIS software, and farm management systems may reduce analytical accuracy and operational efficiency. Regulatory changes concerning drone operations, satellite data accessibility, environmental monitoring requirements, and cross-border geospatial data usage may increase compliance complexity and deployment costs. Furthermore, rapid technological advancements in artificial intelligence, hyperspectral imaging, autonomous drones, predictive analytics, and increasing competition from integrated agritech solution providers represent significant disruption signals capable of reshaping market dynamics.

Strategic Implications of Risk Factors & Disruption Threats in Global Remote Sensing Technology for Agriculture Market

Remote sensing technology providers are strengthening business resilience by investing in AI-powered image analytics, cloud-native geospatial platforms, advanced cybersecurity frameworks, and high-resolution satellite and drone technologies to improve data accuracy and operational reliability. Organizations are expanding integration capabilities with IoT-enabled field sensors, weather forecasting systems, GIS platforms, precision agriculture software, and farm management solutions to enhance end-to-end agricultural intelligence. Strategic investments in predictive crop analytics, automated field monitoring, digital decision-support systems, climate risk assessment, and precision farm management are enabling agricultural stakeholders to improve productivity, optimize resource utilization, and strengthen climate resilience. Partnerships with satellite operators, drone manufacturers, agritech companies, research institutions, and government agencies are further supporting platform scalability and digital agriculture transformation.

Global Remote Sensing Technology for Agriculture Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead, the global Remote Sensing Technology for Agriculture market is expected to maintain strong growth despite evolving technological, regulatory, cybersecurity, and environmental challenges. Continued innovation in artificial intelligence, hyperspectral imaging, satellite constellations, autonomous drones, cloud computing, and geospatial analytics will create significant opportunities for precision agriculture and sustainable farming. However, market participants must continuously monitor changing regulatory requirements, climate-related risks, cybersecurity threats, agricultural data governance standards, and emerging digital farming technologies to minimize operational risks. Organizations that prioritize secure digital infrastructure, advanced analytics, seamless platform integration, regulatory compliance, and data-driven precision agriculture strategies will be well positioned to navigate future disruptions and capitalize on long-term opportunities across the global agricultural technology ecosystem.

Regulatory Landscape

Global Remote Sensing Technology for Agriculture Market Regulatory Landscape Overview

The Global Remote Sensing Technology for Agriculture Market operates within a rapidly evolving regulatory framework shaped by agricultural digitization programs, satellite data policies, environmental monitoring standards, and precision farming initiatives. As remote sensing technologies become increasingly integrated into modern agriculture through satellites, UAVs, geospatial analytics, AI, and cloud-based farm management platforms, regulatory compliance is becoming essential for ensuring responsible data utilization, sustainable farming practices, and efficient agricultural resource management.

Governments and regulatory authorities worldwide are implementing policies that promote digital agriculture, satellite data accessibility, UAV operations, environmental sustainability, climate-resilient farming, and precision agriculture adoption. These regulatory frameworks encourage the deployment of advanced remote sensing technologies while supporting food security, resource optimization, environmental conservation, and sustainable agricultural development.

Key Regulatory Areas Influencing the Market

- Agricultural Digitization Programs: Government initiatives promoting digital farming technologies, smart agriculture platforms, precision farming, and data-driven agricultural decision-making.

- Satellite Data Policies: Regulations governing the acquisition, distribution, accessibility, and commercial utilization of satellite imagery and geospatial data for agricultural applications.

- Environmental Monitoring Standards: Regulatory frameworks supporting environmental conservation, land monitoring, soil management, water resource protection, and ecosystem sustainability.

- Precision Farming Initiatives: National and regional programs encouraging adoption of precision agriculture technologies to improve productivity, optimize resource utilization, and reduce environmental impact.

- Drone & UAV Operational Regulations: Aviation regulations governing the safe deployment of drones for agricultural surveying, crop monitoring, aerial imaging, and precision spraying.

- Data Governance & Cybersecurity Standards: Requirements ensuring secure collection, storage, sharing, and protection of agricultural, geospatial, and farm management data.

- Climate-Smart Agriculture Policies: Regulatory initiatives supporting climate adaptation, sustainable farming practices, carbon management, and resilient agricultural production systems.

Regional Regulatory Landscape

North America maintains comprehensive regulatory frameworks supporting precision agriculture, commercial satellite applications, UAV operations, environmental monitoring, and secure agricultural data management.

Europe emphasizes sustainable agriculture, environmental protection, digital farming initiatives, satellite data accessibility, and climate-focused agricultural policies that encourage advanced remote sensing adoption.

Asia-Pacific is strengthening agricultural modernization through government-backed smart farming programs, digital agriculture initiatives, satellite infrastructure development, and expanding UAV regulations.

Latin America continues promoting precision agriculture through agricultural modernization policies, commercial farming initiatives, environmental monitoring programs, and increasing investment in digital farming technologies.

Middle East & Africa is advancing regulatory support through climate-smart agriculture strategies, water conservation initiatives, food security programs, and investments in agricultural digital transformation.

Regulatory Impact on Market Growth

- Agricultural digitization programs are accelerating adoption of remote sensing technologies for precision farming and farm management.

- Satellite data policies are improving access to geospatial information, enabling broader deployment of agricultural monitoring solutions.

- Environmental monitoring standards are increasing demand for remote sensing technologies supporting sustainable land and water resource management.

- Precision farming initiatives are encouraging investments in AI-powered crop monitoring, soil analysis, and resource optimization platforms.

- Drone operation regulations are supporting the safe expansion of UAV-based agricultural surveying and crop intelligence applications.

- Data governance requirements are driving implementation of secure cloud-based agricultural analytics and digital farm management platforms.

- Climate-smart agriculture policies are promoting long-term investments in advanced remote sensing technologies that improve agricultural resilience and sustainability.

Future Regulatory Outlook

The regulatory environment for the Global Remote Sensing Technology for Agriculture Market is expected to increasingly focus on digital agriculture governance, AI-enabled decision support, satellite data accessibility, UAV operational safety, environmental sustainability, and climate-resilient farming. Governments will continue strengthening policies that encourage adoption of intelligent agricultural technologies while ensuring responsible management of agricultural and geospatial data.

Future regulatory developments are expected to expand support for precision agriculture, AI-driven crop analytics, satellite-enabled farm intelligence, sustainable resource management, climate adaptation initiatives, and integrated digital agriculture ecosystems. Companies delivering compliant, secure, and innovative remote sensing solutions will be well positioned to support evolving regulatory requirements and the continued transformation of global agriculture.