Global Automotive Embedded Systems in Automobile Market Report, Size & Forecast 2026 - 2033

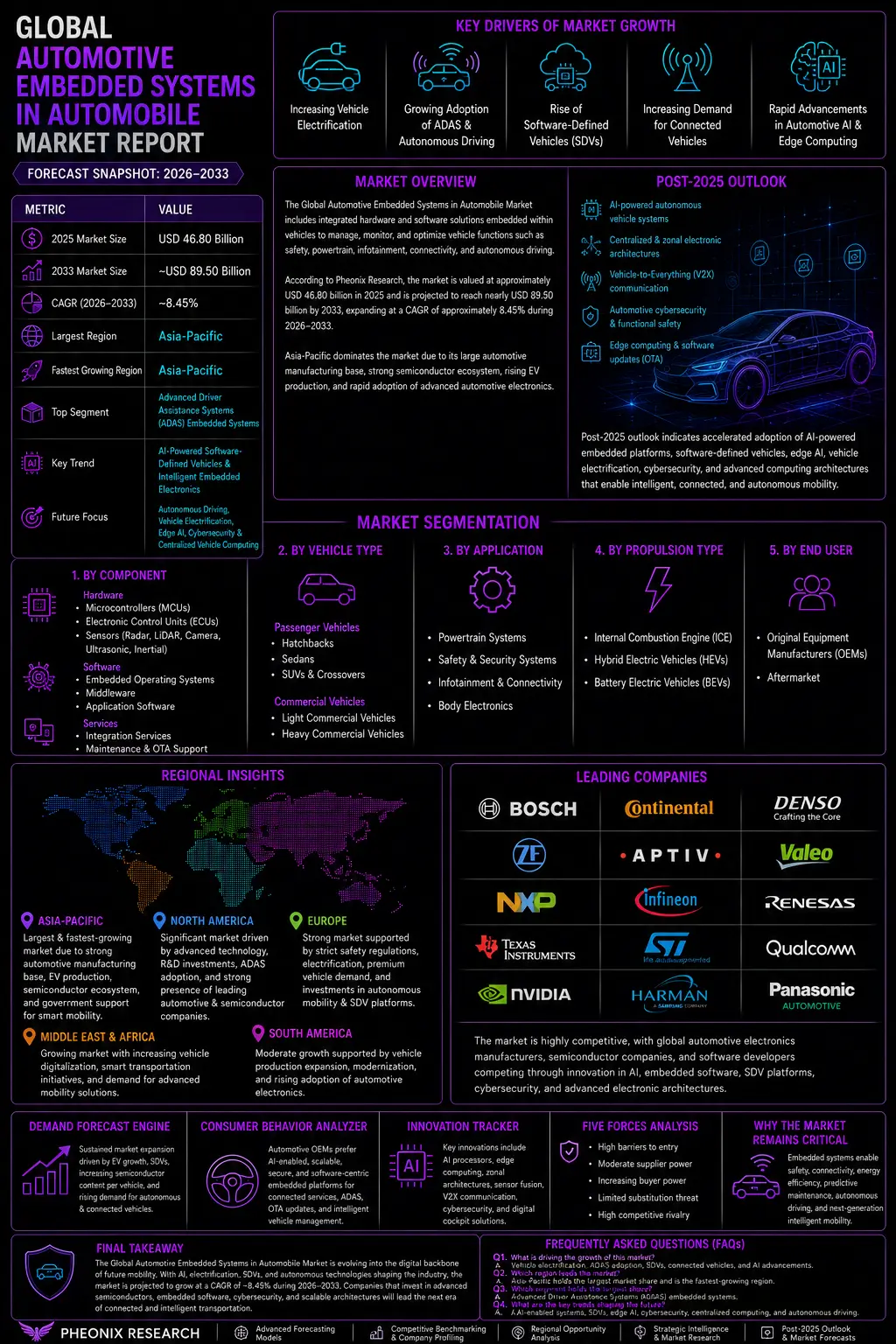

Global Automotive Embedded Systems in Automobile Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

| 2025 Market Size | USD 46.80 Billion |

| 2033 Market Size | ~USD 89.50 Billion |

| CAGR (2026–2033) | ~8.45% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Advanced Driver Assistance Systems (ADAS) Embedded Systems |

| Key Trend | AI-Powered Software-Defined Vehicles & Intelligent Embedded Electronics |

| Future Focus | Autonomous Driving, Vehicle Electrification, Edge AI, Automotive Cybersecurity & Centralized Vehicle Computing |

Global Automotive Embedded Systems in Automobile Market Overview

The Global Automotive Embedded Systems in Automobile Market comprises integrated hardware and software solutions embedded within vehicles to manage, monitor, and optimize vehicle functions. These systems include electronic control units (ECUs), microcontrollers, sensors, actuators, infotainment processors, telematics modules, advanced driver assistance systems (ADAS), powertrain controllers, battery management systems (BMS), body electronics, and vehicle communication networks. Embedded systems serve as the digital intelligence behind modern automobiles by enabling real-time control, safety, connectivity, diagnostics, energy management, and autonomous driving capabilities. Rapid advancements in vehicle electrification, connected mobility, autonomous driving technologies, software-defined vehicles (SDVs), and artificial intelligence are transforming the automotive industry into a software-centric ecosystem. Modern passenger and commercial vehicles now integrate hundreds of embedded processors and millions of lines of software code to support intelligent transportation, predictive maintenance, enhanced safety, infotainment, and over-the-air (OTA) software updates. According to Pheonix Research, the Global Automotive Embedded Systems in Automobile Market is valued at approximately USD 46.80 billion in 2025 and is projected to reach nearly USD 89.50 billion by 2033, expanding at a CAGR of approximately 8.45% during 2026–2033. Asia-Pacific dominates the market owing to its large automotive manufacturing base, increasing electric vehicle production, expanding semiconductor ecosystem, and rapid adoption of advanced automotive electronics across China, Japan, South Korea, and India. The region is also expected to remain the fastest-growing market due to government support for electric mobility, smart transportation infrastructure, and connected vehicle technologies. The Post-2025 outlook indicates accelerated adoption of AI-powered embedded platforms, centralized vehicle computing architectures, software-defined vehicles, zonal electronic architectures, edge computing, vehicle-to-everything (V2X) communication, automotive cybersecurity, and autonomous driving technologies.Global Automotive Embedded Systems in Automobile Market

Key Drivers of Global Automotive Embedded Systems in Automobile Market Growth

1. Increasing Vehicle Electrification

The rapid adoption of electric vehicles (EVs), hybrid electric vehicles (HEVs), and plug-in hybrid electric vehicles (PHEVs) is significantly increasing demand for embedded controllers, battery management systems, motor control units, and intelligent power electronics.2. Growing Adoption of ADAS & Autonomous Driving

Automakers continue integrating advanced driver assistance systems including adaptive cruise control, lane-keeping assist, automatic emergency braking, parking assistance, and autonomous driving technologies, creating substantial demand for high-performance embedded computing platforms.3. Rise of Software-Defined Vehicles (SDVs)

The automotive industry is transitioning from hardware-centric vehicles to software-defined architectures where centralized embedded computing platforms manage multiple vehicle functions through intelligent software updates and cloud connectivity.4. Increasing Demand for Connected Vehicles

Embedded telematics, vehicle connectivity, V2X communication, infotainment systems, cloud integration, and over-the-air software updates are becoming standard features across modern vehicles, driving continuous innovation in embedded electronics.5. Rapid Advancements in Automotive AI & Edge Computing

Artificial intelligence, machine learning, edge processors, automotive-grade semiconductor technologies, and intelligent sensor fusion are enabling real-time decision-making, predictive diagnostics, enhanced vehicle safety, and autonomous driving capabilities.Global Automotive Embedded Systems in Automobile Market Segmentation

1. By Component

1.1 Hardware 1.1.1 Microcontrollers (MCUs) 1.1.1.1 8-bit MCUs 1.1.1.2 16-bit MCUs 1.1.1.3 32-bit MCUs 1.1.2 Electronic Control Units (ECUs) 1.1.2.1 Powertrain ECU 1.1.2.2 Body Control Module 1.1.2.3 Chassis Control ECU 1.1.2.4 ADAS ECU 1.1.3 Sensors 1.1.3.1 Radar Sensors 1.1.3.2 LiDAR Sensors 1.1.3.3 Camera Sensors 1.1.3.4 Ultrasonic Sensors 1.1.3.5 Inertial Sensors 1.2 Software 1.2.1 Embedded Operating Systems 1.2.1.1 AUTOSAR 1.2.1.2 Linux-Based Automotive Platforms 1.2.2 Middleware 1.2.2.1 Communication Middleware 1.2.2.2 Diagnostic Software 1.2.3 Application Software 1.2.3.1 ADAS Software 1.2.3.2 Infotainment Software 1.2.3.3 Vehicle Control Software 1.3 Services 1.3.1 Integration Services 1.3.1.1 ECU Integration 1.3.1.2 Software Validation 1.3.2 Maintenance & OTA Support 1.3.2.1 Software Updates 1.3.2.2 Remote Diagnostics2. By Vehicle Type

2.1 Passenger Vehicles 2.1.1 Hatchbacks 2.1.1.1 Compact Cars 2.1.1.2 Premium Hatchbacks 2.1.2 Sedans 2.1.2.1 Mid-Size Sedans 2.1.2.2 Luxury Sedans 2.1.3 SUVs & Crossovers 2.1.3.1 Compact SUVs 2.1.3.2 Full-Size SUVs 2.2 Commercial Vehicles 2.2.1 Light Commercial Vehicles 2.2.1.1 Delivery Vans 2.2.1.2 Pickup Trucks 2.2.2 Heavy Commercial Vehicles 2.2.2.1 Heavy Trucks 2.2.2.2 Buses & Coaches3. By Application

3.1 Powertrain Systems 3.1.1 Engine Control 3.1.1.1 Fuel Injection 3.1.1.2 Transmission Control 3.1.2 Battery Management Systems 3.1.2.1 Cell Monitoring3.1.2.2 Thermal Management

3.2 Safety & Security Systems 3.2.1 ADAS 3.2.1.1 Lane Departure Warning 3.2.1.2 Adaptive Cruise Control 3.2.1.3 Automatic Emergency Braking 3.2.2 Airbag Control 3.2.2.1 Occupant Protection 3.2.2.2 Crash Detection 3.3 Infotainment & Connectivity 3.3.1 Navigation Systems 3.3.1.1 GPS Navigation 3.3.1.2 Cloud Navigation 3.3.2 Connected Vehicle Systems 3.3.2.1 Telematics 3.3.2.2 Vehicle-to-Everything (V2X) 3.4 Body Electronics 3.4.1 Climate Control 3.4.1.1 HVAC Controllers 3.4.1.2 Smart Cabin Systems 3.4.2 Lighting Systems 3.4.2.1 Adaptive Lighting 3.4.2.2 Intelligent LED Systems4. By Propulsion Type

4.1 Internal Combustion Engine (ICE) 4.1.1 Gasoline Vehicles 4.1.1.1 Passenger Cars 4.1.1.2 Commercial Vehicles 4.1.2 Diesel Vehicles 4.1.2.1 Heavy Commercial Vehicles 4.1.2.2 Off-Highway Vehicles 4.2 Hybrid Electric Vehicles (HEVs) 4.2.1 Mild Hybrid 4.2.1.1 Passenger Vehicles 4.2.1.2 Commercial Vehicles 4.2.2 Full Hybrid 4.2.2.1 Advanced Hybrid Systems 4.2.2.2 Intelligent Energy Management 4.3 Battery Electric Vehicles (BEVs) 4.3.1 Passenger EVs 4.3.1.1 Urban Mobility 4.3.1.2 Premium EVs 4.3.2 Commercial EVs 4.3.2.1 Electric Buses 4.3.2.2 Electric Trucks5. By End User

5.1 Original Equipment Manufacturers (OEMs) 5.1.1 Passenger Vehicle Manufacturers 5.1.1.1 Global Automotive OEMs 5.1.1.2 Regional Manufacturers 5.1.2 Commercial Vehicle Manufacturers 5.1.2.1 Truck Manufacturers 5.1.2.2 Bus Manufacturers 5.2 Aftermarket 5.2.1 Infotainment Upgrades 5.2.1.1 Navigation Systems 5.2.1.2 Multimedia Systems 5.2.2 Telematics & Diagnostics 5.2.2.1 Fleet Management 5.2.2.2 Vehicle MonitoringRegional Insights of Global Automotive Embedded Systems in Automobile Market

Asia-Pacific – Largest & Fastest Growing Market

Asia-Pacific dominates the Global Automotive Embedded Systems in Automobile Market owing to its extensive automotive manufacturing ecosystem, strong semiconductor supply chain, rapid electric vehicle production, and increasing adoption of connected vehicle technologies. China, Japan, South Korea, and India continue investing heavily in software-defined vehicles (SDVs), autonomous driving technologies, intelligent transportation systems, and advanced automotive electronics. Government initiatives supporting electric mobility, semiconductor manufacturing, and smart mobility further strengthen regional market leadership.North America

North America represents one of the most technologically advanced markets, driven by increasing deployment of autonomous driving technologies, connected vehicles, electric vehicles, and advanced driver assistance systems (ADAS). The United States remains the regional leader due to substantial R&D investments by global automotive OEMs, semiconductor manufacturers, and technology companies developing AI-powered automotive embedded platforms, automotive cybersecurity solutions, and centralized vehicle computing architectures.Europe

Europe continues to hold a significant market share owing to stringent vehicle safety regulations, widespread adoption of premium vehicles, rapid electrification, and strong automotive engineering capabilities. Germany, France, the United Kingdom, Italy, and Sweden are major contributors through continuous investments in intelligent mobility, autonomous driving, embedded software development, and next-generation electronic vehicle architectures.Middle East & Africa

The Middle East & Africa market is steadily expanding due to increasing vehicle digitalization, adoption of connected mobility solutions, investments in smart transportation infrastructure, and growing demand for advanced passenger safety systems. Countries including the UAE, Saudi Arabia, and South Africa are progressively integrating intelligent automotive technologies into their transportation ecosystems.South America

South America is witnessing gradual market growth supported by increasing vehicle production, expanding automotive electronics adoption, rising demand for connected vehicles, and modernization of automotive manufacturing facilities. Brazil and Argentina continue to drive regional demand through increasing investments in vehicle safety systems and embedded electronic technologies.Leading Companies in the Global Automotive Embedded Systems in Automobile Market

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Qualcomm Technologies, Inc.

- NVIDIA Corporation

- Harman International Industries

- Panasonic Automotive Systems

Why the Global Automotive Embedded Systems in Automobile Market Remains Critical

- Vehicle electrification continues to increase the number and complexity of embedded electronic systems across passenger and commercial vehicles.

- Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies rely heavily on high-performance embedded computing platforms.

- Connected vehicles require intelligent embedded systems to support telematics, cloud connectivity, over-the-air (OTA) software updates, and Vehicle-to-Everything (V2X) communication.

- Software-defined vehicle (SDV) architectures are transforming automobiles into continuously upgradeable intelligent mobility platforms.

- AI-powered embedded systems enhance vehicle safety, energy efficiency, predictive maintenance, cybersecurity, and overall driving experience.

Strategic Intelligence and AI-Backed Insights – Global Automotive Embedded Systems in Automobile Market

Pheonix Demand Forecast Engine identifies sustained market expansion driven by increasing production of electric vehicles, rapid deployment of software-defined vehicle architectures, growing semiconductor content per vehicle, expanding autonomous driving capabilities, and rising investments in intelligent transportation technologies. The Consumer Behavior Analyzer highlights increasing automotive manufacturer preference for centralized vehicle computing platforms capable of supporting AI-driven driver assistance, connected services, predictive diagnostics, infotainment integration, battery optimization, and secure over-the-air software management throughout the vehicle lifecycle. The Innovation Tracker emphasizes software-defined vehicles (SDVs), zonal electronic architectures, artificial intelligence, edge computing, advanced semiconductor platforms, automotive cybersecurity, digital cockpit solutions, autonomous driving processors, sensor fusion, and Vehicle-to-Everything (V2X) communication as the major technologies shaping the future automotive embedded systems landscape. Five Forces Analysis indicates high barriers to entry due to strict automotive functional safety requirements, extensive semiconductor expertise, software certification standards, and significant research and development investments. Supplier power remains moderate because of the concentration of automotive semiconductor manufacturers, while buyer power is increasing as global OEMs seek scalable, secure, and software-centric embedded platforms. Competitive rivalry remains intense as leading automotive technology companies compete through semiconductor innovation, AI capabilities, embedded software development, and strategic partnerships with global vehicle manufacturers.Final Takeaway of Global Automotive Embedded Systems in Automobile Market

The Global Automotive Embedded Systems in Automobile Market is evolving into the technological backbone of next-generation intelligent mobility. The projected CAGR of approximately 8.45% during 2026–2033 reflects increasing global demand for connected, software-defined, electric, and autonomous vehicles supported by advanced embedded electronics and intelligent computing architectures. Future market growth will be driven by AI-enabled embedded processors, centralized vehicle computing, software-defined vehicle platforms, automotive cybersecurity, autonomous driving technologies, edge AI, intelligent sensor fusion, digital cockpits, and over-the-air software management. As vehicles become increasingly software-centric, embedded systems will play a pivotal role in delivering enhanced safety, energy efficiency, connectivity, personalization, and autonomous functionality. Companies that successfully integrate artificial intelligence, automotive-grade semiconductors, embedded software platforms, cybersecurity, high-performance computing, and scalable electronic architectures will be well positioned to lead the next generation of connected mobility and intelligent transportation. At Pheonix Research, our advanced forecasting models deliver comprehensive Global Automotive Embedded Systems in Automobile Market revenue forecasts, competitive benchmarking, regional opportunity analysis, and strategic intelligence—enabling automotive OEMs, Tier-1 suppliers, semiconductor manufacturers, software developers, investors, and mobility technology providers to capitalize on the Post-2025 outlook with confidence and data-driven decision-making.Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Market Highlights

1.3 Market Size & Forecast (2026–2033)

1.4 Largest Regional Market Analysis

1.5 Fastest Growing Regional Market Analysis

1.6 Largest Segment Analysis

1.7 Competitive Landscape Snapshot

1.8 Future Market Outlook

2. Global Automotive Embedded Systems in Automobile Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Automotive Embedded Systems in Automobile Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Embedded Vehicle Electronics Architecture

3.5 Automotive Semiconductor & Software Ecosystem

3.6 Technology Landscape

3.6.1 Electronic Control Units (ECUs)

3.6.1.1 Microcontrollers & Automotive SoCs

3.6.1.1.1 Embedded Operating Systems

3.6.1.1.1.1 AUTOSAR Platforms

3.6.1.1.1.2 Linux-Based Automotive Platforms

3.6.2 Advanced Driver Assistance Systems (ADAS)

3.6.2.1 Sensor Fusion Systems

3.6.2.1.1 Computer Vision & AI Processing

3.6.2.1.1.1 Radar & LiDAR Systems

3.6.2.1.1.2 Camera & Ultrasonic Sensors

3.6.3 Connected Vehicle Systems

3.6.3.1 Telematics Control Units (TCUs)

3.6.3.1.1 Infotainment Platforms

3.6.3.1.1.1 Vehicle-to-Everything (V2X) Communication

3.6.3.1.1.2 Over-the-Air (OTA) Software Updates

3.6.4 Electric Vehicle Embedded Systems

3.6.4.1 Battery Management Systems (BMS)

3.6.4.1.1 Powertrain Controllers

3.6.4.1.1.1 Motor Control Units

3.6.4.1.1.2 Energy Management Systems

4. Regulatory Landscape

4.1 Automotive Functional Safety Standards (ISO 26262)

4.2 Automotive Cybersecurity Regulations (ISO/SAE 21434)

4.3 UNECE Vehicle Software & Cybersecurity Regulations (R155 & R156)

4.4 Autonomous Driving & ADAS Regulatory Frameworks

4.5 Data Privacy, Connected Vehicle & V2X Standards

5. Market Trends & Innovation Outlook

5.1 AI-Powered Software-Defined Vehicles (SDVs)

5.2 Centralized Vehicle Computing Architectures

5.3 Edge AI for Automotive Applications

5.4 Intelligent Sensor Fusion Technologies

5.5 Automotive Cybersecurity Platforms

5.6 Digital Cockpit & Connected Mobility Solutions

5.7 Zonal Electronic Architectures

5.8 High-Performance Automotive Computing (HPC)

6. Global Automotive Embedded Systems in Automobile Market Dynamics

6.1 Market Drivers

6.1.1 Increasing Vehicle Electrification

6.1.2 Growing Adoption of ADAS & Autonomous Driving

6.1.3 Rise of Software-Defined Vehicles (SDVs)

6.1.4 Increasing Demand for Connected Vehicles

6.1.5 Rapid Advancements in Automotive AI & Edge Computing

6.2 Market Restraints

6.2.1 Rising Semiconductor Supply Constraints

6.2.2 High Development & Validation Costs

6.2.3 Increasing Embedded Software Complexity

6.2.4 Functional Safety Compliance Challenges

6.3 Market Opportunities

6.3.1 Centralized Vehicle Computing Platforms

6.3.2 Software-Defined Vehicle Ecosystems

6.3.3 Intelligent Electric Vehicle Platforms

6.3.4 Automotive AI & Edge Computing

6.3.5 Autonomous Mobility Solutions

6.4 Market Challenges

6.4.1 Automotive Cybersecurity Threats

6.4.2 OTA Software Reliability & Validation

6.4.3 Integration Across Multi-Domain Vehicle Architectures

6.4.4 Compliance with Global Automotive Standards

7. Global Automotive Embedded Systems in Automobile Market Size Analysis (USD Billion), 2026–2033

7.1 Revenue Forecast Analysis

7.2 CAGR Analysis

7.3 Automotive Electronics Penetration Analysis

7.4 Technology Adoption Trends

7.5 Investment & Innovation Assessment

8. Global Automotive Embedded Systems in Automobile Market Segmentation Analysis

8.1 By Component

8.1.1 Hardware

8.1.2 Software

8.1.3 Services

8.2 By Vehicle Type

8.2.1 Passenger Vehicles

8.2.2 Commercial Vehicles

8.3 By Application

8.3.1 Powertrain Systems

8.3.2 Safety & Security Systems

8.3.3 Infotainment & Connectivity

8.3.4 Body Electronics

8.4 By Propulsion Type

8.4.1 Internal Combustion Engine (ICE) Vehicles

8.4.2 Hybrid Electric Vehicles (HEVs)

8.4.3 Battery Electric Vehicles (BEVs)

8.5 By End User

8.5.1 Original Equipment Manufacturers (OEMs)

8.5.2 Aftermarket

9. Regional Market Analysis

9.1 Asia-Pacific

9.1.1 China

9.1.2 Japan

9.1.3 South Korea

9.1.4 India

9.1.5 Taiwan

9.1.6 Rest of Asia-Pacific

9.2 North America

9.2.1 United States

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 Germany

9.3.2 France

9.3.3 United Kingdom

9.3.4 Italy

9.3.5 Sweden

9.3.6 Rest of Europe

9.4 Middle East & Africa

9.4.1 GCC Countries

9.4.2 South Africa

9.4.3 Rest of Middle East & Africa

9.5 South America

9.5.1 Brazil

9.5.2 Argentina

9.5.3 Rest of South America

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Benchmarking

10.3 Strategic Developments

10.4 Product & Technology Innovation

10.5 Partnerships, Mergers & Acquisitions

10.6 Competitive Positioning Matrix

11. Company Profiles

11.1 Robert Bosch GmbH

11.2 Continental AG

11.3 Denso Corporation

11.4 ZF Friedrichshafen AG

11.5 Aptiv PLC

11.6 Valeo SA

11.7 NXP Semiconductors N.V.

11.8 Infineon Technologies AG

11.9 Renesas Electronics Corporation

11.10 Texas Instruments Incorporated

11.11 STMicroelectronics N.V.

11.12 Qualcomm Technologies, Inc.

11.13 NVIDIA Corporation

11.14 Harman International Industries

11.15 Panasonic Automotive Systems

12. Strategic Intelligence & Pheonix AI Insights

12.1 Pheonix Demand Forecast Engine

12.2 Consumer Behavior Analyzer

12.3 Innovation Tracker

12.4 Intelligent Mobility Opportunity Dashboard

12.5 Automotive Embedded Value Chain Analysis

12.6 Porter’s Five Forces Analysis

13. Future Outlook & Strategic Recommendations

13.1 Software-Defined Vehicle (SDV) Adoption Roadmap

13.2 AI-Enabled Vehicle Computing Strategy

13.3 Automotive Cybersecurity Best Practices

13.4 Autonomous Driving & Connected Mobility Outlook

13.5 Long-Term Market Outlook (2033+)

14. About Pheonix Market Research

15. Disclaimer

Competitive Landscape

Global Automotive Embedded Systems in Automobile Market Competitive Intensity & Market Structure Overview

The Global Automotive Embedded Systems in Automobile Market is highly competitive and characterized by the presence of automotive electronics manufacturers, Tier-1 automotive suppliers, semiconductor companies, embedded software developers, AI computing providers, automotive cybersecurity firms, sensor manufacturers, and intelligent mobility technology companies. Competitive intensity is driven by the rapid evolution of software-defined vehicles (SDVs), vehicle electrification, artificial intelligence (AI), advanced driver assistance systems (ADAS), centralized vehicle computing, edge AI, and connected mobility technologies.

Companies compete across multiple embedded system segments including electronic control units (ECUs), automotive microcontrollers (MCUs), battery management systems (BMS), automotive processors, ADAS platforms, infotainment systems, telematics modules, digital cockpits, embedded operating systems, vehicle communication networks, automotive cybersecurity, and high-performance computing platforms. Growing demand for autonomous driving, electric vehicles, connected cars, predictive diagnostics, intelligent safety systems, and over-the-air (OTA) software updates is intensifying competition while accelerating innovation throughout the automotive embedded ecosystem.

The market structure is evolving toward centralized vehicle computing architectures integrating AI-powered processors, automotive-grade semiconductors, embedded software, cloud connectivity, edge computing, intelligent sensor fusion, cybersecurity, and zonal electronic architectures into unified software-defined vehicle platforms. Market participants are investing heavily in automotive AI, semiconductor innovation, embedded software platforms, autonomous driving technologies, digital cockpit solutions, and strategic partnerships to strengthen market positioning while enabling safer, smarter, and more connected vehicles.

Global Automotive Embedded Systems in Automobile Market Competitive Intensity & Market Structure Current Scenario

Leading Global Automotive Embedded Systems Companies

Robert Bosch GmbH: A global automotive technology leader providing ECUs, ADAS platforms, embedded software, vehicle control systems, automotive AI, and connected mobility technologies.

Continental AG: A leading automotive supplier offering intelligent vehicle electronics, ADAS systems, embedded software, vehicle networking, digital cockpit solutions, and automotive cybersecurity technologies.

Denso Corporation: A global automotive electronics company specializing in embedded control systems, powertrain electronics, ADAS platforms, thermal management, and connected vehicle technologies.

ZF Friedrichshafen AG: A leading mobility technology provider delivering intelligent vehicle control systems, autonomous driving platforms, embedded software, and advanced chassis electronics.

Aptiv PLC: A global automotive technology company developing software-defined vehicle architectures, centralized vehicle computing, smart sensors, connected vehicle platforms, and autonomous driving technologies.

Valeo SA: A major automotive supplier providing ADAS technologies, embedded electronics, intelligent lighting systems, power electronics, and smart mobility solutions.

NXP Semiconductors N.V.: A leading automotive semiconductor company supplying automotive processors, secure microcontrollers, radar chipsets, vehicle networking solutions, and AI-enabled embedded platforms.

Infineon Technologies AG: A global semiconductor manufacturer providing automotive microcontrollers, power semiconductors, battery management ICs, cybersecurity chips, and intelligent vehicle electronics.

Renesas Electronics Corporation: A leading supplier of automotive MCUs, embedded processors, AI-enabled controllers, SoCs, and intelligent automotive computing platforms.

Texas Instruments Incorporated: A semiconductor company offering automotive analog ICs, embedded processors, power management technologies, sensor interfaces, and vehicle communication solutions.

STMicroelectronics N.V.: A global semiconductor provider delivering automotive microcontrollers, MEMS sensors, imaging processors, AI technologies, and advanced automotive electronics.

Qualcomm Technologies, Inc.: A technology leader developing Snapdragon Digital Chassis platforms, automotive AI processors, connected vehicle technologies, digital cockpit systems, and autonomous driving platforms.

NVIDIA Corporation: A global AI computing company providing DRIVE platforms, centralized vehicle computing, autonomous driving processors, AI acceleration, and edge computing technologies.

Harman International Industries: A leading automotive technology company offering infotainment systems, connected mobility platforms, telematics, digital cockpit solutions, and embedded automotive software.

Panasonic Automotive Systems: A global automotive electronics company delivering infotainment platforms, connected vehicle solutions, embedded electronics, battery technologies, and intelligent mobility systems.

Key Competitive Intensity & Market Structure Drivers

Increasing adoption of software-defined vehicles (SDVs), connected mobility, electric vehicles, and autonomous driving technologies is intensifying competition among automotive embedded system providers worldwide.

Growing deployment of automotive AI, edge computing, advanced semiconductors, ADAS platforms, centralized vehicle computing, intelligent sensor fusion, and automotive cybersecurity is creating significant technological differentiation among market participants.

Rising demand for vehicle safety, intelligent mobility, connected services, predictive diagnostics, over-the-air software updates, and energy-efficient vehicle architectures is strengthening competitive intensity while accelerating embedded system innovation.

Strategic collaborations among automotive OEMs, Tier-1 suppliers, semiconductor manufacturers, cloud technology companies, AI developers, cybersecurity firms, and mobility technology providers are accelerating product innovation, expanding software capabilities, and improving intelligent vehicle performance.

Continuous investment in AI-enabled processors, automotive-grade semiconductors, software-defined vehicle platforms, embedded software, secure connectivity, digital cockpit technologies, and centralized computing architectures is enabling companies to improve operational efficiency, customer value, and long-term competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Companies offering comprehensive embedded hardware-software platforms, automotive AI capabilities, and integrated intelligent vehicle ecosystems are expected to maintain significant competitive advantages.

Investment in automotive artificial intelligence, software-defined vehicle platforms, centralized computing architectures, advanced semiconductor technologies, cybersecurity, edge AI, and connected mobility solutions is becoming increasingly important for sustaining long-term market leadership.

Organizations focusing on expanding intelligent vehicle computing, improving software interoperability, strengthening OTA software management, and enhancing autonomous driving capabilities are likely to increase revenue growth and market share.

Strategic partnerships with automotive OEMs, semiconductor manufacturers, embedded software developers, cloud technology providers, research institutions, and mobility technology firms are supporting innovation, global expansion, and next-generation vehicle platform development.

Businesses capable of combining semiconductor innovation, embedded software expertise, artificial intelligence, cybersecurity, automotive engineering, and scalable software-defined vehicle architectures will be best positioned to compete effectively in the evolving global automotive embedded systems market.

Global Automotive Embedded Systems in Automobile Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the Global Automotive Embedded Systems in Automobile Market is expected to become increasingly AI-driven, software-defined, and semiconductor-centric as automakers accelerate investments in intelligent mobility and next-generation connected vehicles.

Future competition will be shaped by software-defined vehicles (SDVs), centralized vehicle computing, AI-powered embedded processors, autonomous driving platforms, edge AI, digital cockpit technologies, automotive cybersecurity, intelligent sensor fusion, Vehicle-to-Everything (V2X) communication, and zonal electronic architectures.

Market participants are expected to increase investments in automotive AI platforms, embedded software ecosystems, semiconductor innovation, high-performance computing, secure connectivity, cloud-enabled vehicle services, and intelligent mobility technologies to strengthen competitive positioning.

Over the forecast period, companies that successfully combine artificial intelligence, automotive semiconductor expertise, embedded software innovation, cybersecurity, intelligent vehicle computing, and scalable software-defined vehicle platforms will be best positioned to lead the evolving Global Automotive Embedded Systems in Automobile Market.

Value Chain

Global Automotive Embedded Systems in Automobile Market Value Chain Analysis

1. Semiconductor, IP & Core Technology Development

The value chain begins with semiconductor manufacturers, embedded software developers, AI technology providers, and IP vendors developing automotive-grade microcontrollers (MCUs), system-on-chips (SoCs), embedded processors, memory devices, sensor technologies, AI accelerators, communication chipsets, cybersecurity solutions, and real-time operating systems (RTOS). Continuous investment in functional safety (ISO 26262), AI computing, edge processing, and automotive cybersecurity drives innovation at this stage.

2. Electronic Component & Embedded Module Manufacturing

Specialized suppliers manufacture critical automotive electronic components including electronic control units (ECUs), battery management systems (BMS), radar modules, LiDAR sensors, cameras, ultrasonic sensors, telematics control units (TCUs), infotainment processors, vehicle communication modules, actuators, wiring harnesses, printed circuit boards (PCBs), and power electronics. Strict automotive quality standards and reliability testing ensure long-term performance under demanding vehicle operating conditions.

3. Embedded System Integration & Software Development

Tier-1 automotive suppliers and technology companies integrate hardware with embedded operating systems, AUTOSAR platforms, middleware, AI algorithms, cybersecurity software, diagnostic tools, digital cockpit platforms, ADAS software, OTA update capabilities, and Vehicle-to-Everything (V2X) communication technologies. Extensive software validation, hardware-in-the-loop (HIL) testing, cybersecurity verification, and functional safety certification are conducted before deployment.

4. OEM Manufacturing, Vehicle Integration & Validation

Automotive OEMs integrate embedded systems into passenger vehicles, commercial vehicles, electric vehicles (EVs), and hybrid vehicles during manufacturing. This stage includes vehicle electronics integration, calibration, end-of-line testing, homologation, regulatory compliance, autonomous driving validation, and system interoperability testing to ensure seamless performance across multiple vehicle functions.

5. Distribution, Deployment & Aftermarket Support

Finished vehicles equipped with embedded systems are distributed through OEM dealer networks and fleet sales channels. Following deployment, manufacturers provide over-the-air (OTA) software updates, predictive diagnostics, remote vehicle monitoring, cybersecurity patches, maintenance support, replacement electronic modules, software upgrades, and lifecycle management services to ensure long-term vehicle performance, safety, and connectivity.

Key Value Chain Participants

- Semiconductor manufacturers and IP providers

- Automotive electronics and embedded component manufacturers

- Tier-1 suppliers and embedded software developers

- Automotive OEMs and vehicle manufacturers

- Vehicle dealerships, fleet operators, and mobility service providers

- Automotive cybersecurity, OTA, and cloud platform providers

- Aftermarket service providers and lifecycle support organizations

Value Chain Optimization Opportunities

- AI-powered embedded computing and centralized vehicle architectures

- Software-defined vehicle (SDV) platforms with continuous OTA updates

- Automotive-grade semiconductor localization and supply chain resilience

- Advanced ADAS, autonomous driving, and sensor fusion technologies

- Edge AI integration for real-time vehicle intelligence and predictive diagnostics

- Cybersecurity-by-design and secure Vehicle-to-Everything (V2X) communication

- Sustainable electronics manufacturing, modular hardware platforms, and predictive lifecycle management

Investment Activity

Investment Activity in the Global Automotive Embedded Systems in Automobile Market

Investment activity in the Global Automotive Embedded Systems in Automobile Market is accelerating as automotive OEMs, Tier-1 suppliers, semiconductor manufacturers, embedded software developers, and technology companies increase capital deployment toward software-defined vehicles (SDVs), advanced driver assistance systems (ADAS), vehicle electrification, autonomous driving technologies, and AI-powered automotive computing platforms. Rising demand for connected mobility, enhanced vehicle safety, and intelligent electronic architectures is driving sustained investment across the automotive embedded systems ecosystem.

Leading automotive technology providers are investing heavily in high-performance automotive-grade semiconductors, centralized vehicle computing platforms, edge AI processors, battery management systems (BMS), sensor fusion technologies, and over-the-air (OTA) software update solutions. These investments are improving vehicle intelligence, real-time decision-making, cybersecurity, energy efficiency, and autonomous driving capabilities while enabling scalable software-centric vehicle architectures.

Automotive manufacturers are also allocating significant capital toward zonal electronic architectures, embedded operating systems, automotive cybersecurity, Vehicle-to-Everything (V2X) communication, digital cockpit platforms, and next-generation infotainment systems. Growing electric vehicle production and increasing semiconductor content per vehicle continue to accelerate investment in advanced embedded electronics and intelligent vehicle control systems.

Strategic partnerships, mergers, acquisitions, and collaborations among automotive OEMs, semiconductor companies, AI developers, cloud service providers, and mobility technology firms are expanding innovation capabilities and strengthening end-to-end automotive software ecosystems. Investments are increasingly focused on AI-enabled driver assistance, predictive diagnostics, intelligent connectivity, and integrated vehicle software platforms that support continuous feature upgrades throughout the vehicle lifecycle.

Governments worldwide continue supporting automotive digitalization through electric mobility initiatives, semiconductor manufacturing incentives, connected vehicle programs, and intelligent transportation infrastructure investments. These public-sector initiatives are encouraging faster adoption of advanced embedded systems while strengthening regional automotive manufacturing competitiveness and technological innovation.

Key Investment Trends

- Rising investment in software-defined vehicles (SDVs), AI-powered embedded platforms, and centralized vehicle computing architectures.

- Increasing funding for advanced driver assistance systems (ADAS), autonomous driving technologies, and intelligent sensor fusion.

- Expansion of investment in automotive-grade semiconductors, edge AI processors, battery management systems (BMS), and vehicle electrification technologies.

- Growing capital allocation toward Vehicle-to-Everything (V2X) communication, connected vehicle platforms, digital cockpits, and over-the-air (OTA) software management.

- Higher investment in automotive cybersecurity, functional safety, secure embedded software, and cloud-connected mobility platforms.

- Increasing strategic collaborations among automotive OEMs, Tier-1 suppliers, semiconductor manufacturers, AI companies, and mobility technology providers.

- Continued investment in next-generation electronic architectures, predictive diagnostics, intelligent vehicle control systems, and smart mobility ecosystems.

Strategic Investment Outlook

Investment activity is expected to remain robust throughout the forecast period as automakers continue accelerating the transition toward software-defined, electric, connected, and autonomous vehicles. Future capital deployment will increasingly focus on AI-driven vehicle computing, centralized electronic architectures, automotive cybersecurity, edge AI, intelligent connectivity, digital cockpit technologies, and scalable embedded software platforms.

Companies investing in high-performance automotive semiconductors, AI-enabled embedded systems, secure software architectures, connected vehicle technologies, and intelligent mobility solutions are expected to strengthen their competitive position and capitalize on the long-term growth opportunities emerging across the Global Automotive Embedded Systems in Automobile Market.

Technology & Innovation

Global Automotive Embedded Systems in Automobile Market Technology & Innovation Landscape Overview

The Global Automotive Embedded Systems in Automobile Market is undergoing a rapid technological transformation driven by software-defined vehicles (SDVs), artificial intelligence (AI), edge computing, advanced semiconductor platforms, zonal electronic architectures, and connected mobility ecosystems. As automobiles evolve into intelligent, software-centric platforms, embedded systems are becoming the core technology enabling real-time vehicle control, autonomous driving, electrification, predictive diagnostics, cybersecurity, and seamless digital experiences.

Innovation across the automotive industry is shifting from distributed electronic control units (ECUs) toward centralized high-performance computing architectures capable of managing multiple vehicle functions through intelligent software. Technologies such as AI-powered driver assistance, over-the-air (OTA) software updates, digital cockpits, sensor fusion, vehicle-to-everything (V2X) communication, and automotive-grade cybersecurity are significantly enhancing vehicle intelligence, operational safety, and user experience.

Growing investments in autonomous driving technologies, electric vehicle electronics, edge AI processors, centralized vehicle computing, and intelligent mobility platforms are accelerating innovation across automotive OEMs, Tier-1 suppliers, semiconductor manufacturers, and embedded software developers.

Global Automotive Embedded Systems in Automobile Market Technology & Innovation Landscape Current Scenario

The current market is characterized by widespread deployment of AI-enabled embedded processors, advanced driver assistance system (ADAS) controllers, battery management systems (BMS), automotive-grade system-on-chip (SoC) platforms, high-speed vehicle networking, and cloud-connected telematics solutions. Automakers are increasingly replacing numerous standalone ECUs with centralized domain controllers and zonal computing architectures to improve software scalability, reduce hardware complexity, and enable continuous software upgrades.

Rapid advancements in automotive operating systems, AI-powered perception algorithms, real-time edge analytics, digital cockpit integration, predictive maintenance, and cybersecurity frameworks are enabling safer, smarter, and more connected vehicles. The growing adoption of 5G connectivity, V2X communication, digital twins, and software lifecycle management platforms is further accelerating digital transformation across the automotive embedded ecosystem.

Key Technology & Innovation Landscape Trends in the Global Automotive Embedded Systems in Automobile Market

- Software-defined vehicle (SDV) architectures are transforming vehicles into continuously upgradeable platforms through centralized software management and over-the-air (OTA) updates.

- AI-powered embedded computing is enabling autonomous driving, adaptive driver assistance, predictive maintenance, and intelligent vehicle decision-making.

- Centralized vehicle computing and zonal electronic architectures are replacing traditional distributed ECU designs to improve processing efficiency and software integration.

- Automotive-grade edge AI processors are supporting real-time sensor fusion, object recognition, autonomous navigation, and low-latency decision-making.

- Advanced sensor fusion technologies integrating cameras, radar, LiDAR, ultrasonic sensors, GPS, and inertial measurement units (IMUs) are enhancing vehicle perception and safety.

- Vehicle-to-Everything (V2X) communication and 5G connectivity are improving cooperative driving, traffic management, remote diagnostics, and connected mobility services.

- Automotive cybersecurity solutions incorporating hardware security modules (HSMs), secure boot, intrusion detection systems, and encrypted communication are strengthening vehicle resilience against cyber threats.

- Digital cockpit technologies integrating AI voice assistants, augmented reality head-up displays (AR-HUDs), high-resolution infotainment systems, and personalized user interfaces are enhancing in-vehicle experiences.

- Battery management systems (BMS) utilizing AI algorithms and advanced power electronics are optimizing battery performance, thermal management, charging efficiency, and electric vehicle range.

- Digital twin platforms, predictive analytics, and cloud-based vehicle lifecycle management are improving product development, software validation, fleet monitoring, and predictive maintenance.

Strategic Implications of Technology & Innovation in the Global Automotive Embedded Systems in Automobile Market

Continuous investment in AI, software-defined architectures, edge computing, automotive semiconductors, cybersecurity, and connected mobility technologies has become essential for automakers seeking to deliver intelligent, safe, and future-ready vehicles.

The convergence of centralized computing, cloud connectivity, predictive analytics, and software lifecycle management is enabling manufacturers to accelerate innovation, reduce development complexity, improve vehicle performance, and support continuous feature enhancements throughout the vehicle lifecycle.

Automotive companies investing in high-performance computing platforms, AI-enabled ADAS, automotive operating systems, secure embedded software, V2X communication, and scalable semiconductor architectures are expected to strengthen their competitive positioning in the evolving intelligent mobility landscape.

Strategic collaboration among automotive OEMs, semiconductor manufacturers, embedded software developers, cloud service providers, telecommunications companies, and AI technology firms is accelerating innovation while supporting the development of next-generation connected and autonomous vehicles.

Growing investments in autonomous driving platforms, electric mobility technologies, digital cockpit ecosystems, cybersecurity frameworks, and intelligent transportation infrastructure are expected to generate significant long-term growth opportunities across the automotive embedded systems industry.

Global Automotive Embedded Systems in Automobile Market Technology & Innovation Landscape Forward Outlook

Future innovation in the Global Automotive Embedded Systems in Automobile Market will increasingly focus on AI-native vehicle operating systems, centralized vehicle supercomputers, autonomous driving Level 4 and Level 5 technologies, software-defined mobility platforms, quantum-secure automotive communications, next-generation automotive chipsets, and fully connected intelligent transportation ecosystems. Advanced edge AI, digital twins, generative AI-assisted vehicle software development, and cloud-native automotive platforms are expected to redefine future vehicle architectures.

Emerging technologies such as neuromorphic AI processors, silicon carbide (SiC) and gallium nitride (GaN) power electronics, 6G-enabled V2X communication, autonomous mobility orchestration, predictive digital engineering, and self-healing cybersecurity systems will further accelerate innovation. As vehicles become increasingly software-centric and autonomous, technology-driven embedded systems will remain the foundation of future intelligent mobility and connected transportation ecosystems.

Market Risk

Global Automotive Embedded Systems in Automobile Market Risk & Disruption Analysis

The Global Automotive Embedded Systems in Automobile Market is undergoing rapid transformation as software-defined vehicles (SDVs), artificial intelligence, autonomous driving, electrification, and connected mobility redefine vehicle architecture. While growing semiconductor integration and intelligent electronics continue to accelerate market expansion, manufacturers face increasing risks associated with semiconductor supply constraints, cybersecurity threats, software complexity, regulatory compliance, and rapidly evolving automotive technologies.

Automotive OEMs and Tier-1 suppliers are increasingly investing in AI-enabled embedded computing, centralized electronic architectures, automotive cybersecurity, high-performance processors, edge AI, and over-the-air (OTA) software platforms to address the growing complexity of modern vehicles. At the same time, stricter automotive safety standards, cybersecurity regulations, and software validation requirements are reshaping product development and deployment strategies.

Global Automotive Embedded Systems in Automobile Market Current Risk Environment

The automotive embedded systems industry is operating in an increasingly dynamic technology environment driven by vehicle electrification, autonomous mobility, and digital transformation. Rising software content per vehicle and increasing dependence on semiconductor technologies are creating new operational and technological risks across the automotive value chain.

Supply chain disruptions affecting automotive semiconductors, microcontrollers, memory chips, and electronic components continue to challenge production schedules and vehicle availability.

Cybersecurity has become one of the industry’s most significant concerns as connected vehicles increasingly rely on cloud connectivity, OTA software updates, Vehicle-to-Everything (V2X) communication, and AI-enabled decision-making. Protecting embedded systems from cyberattacks, unauthorized access, and software vulnerabilities has become a critical industry priority.

In addition, growing software complexity and the transition toward centralized vehicle computing architectures are increasing validation, certification, and lifecycle software management requirements.

Key Market Risk & Disruption Signals

1. Semiconductor Supply Chain Volatility

Global shortages of automotive-grade semiconductors, microcontrollers, sensors, and advanced electronic components continue to impact vehicle production and embedded system availability.

2. Increasing Automotive Cybersecurity Risks

Connected vehicles, OTA software updates, cloud connectivity, and V2X communications increase exposure to cyberattacks, software breaches, and unauthorized vehicle access.

3. Rapid Transition to Software-Defined Vehicles (SDVs)

The shift from distributed ECUs to centralized computing architectures is accelerating technology disruption and requiring substantial software redevelopment.

4. Growing Functional Safety & Regulatory Compliance

Compliance with automotive functional safety, cybersecurity, software quality, and vehicle safety regulations is becoming increasingly complex for embedded system developers.

5. Accelerating AI & Autonomous Driving Innovation

Continuous advancements in AI processors, sensor fusion, machine learning, and autonomous driving algorithms are shortening product innovation cycles.

6. Increasing Vehicle Electrification Complexity

Growing EV adoption is significantly increasing demand for intelligent battery management systems, power electronics, motor controllers, and embedded energy management platforms.

7. Software Validation & OTA Update Challenges

Managing millions of software code lines, continuous OTA updates, software interoperability, and lifecycle maintenance presents increasing operational complexity.

8. Intensifying Competition in Automotive Electronics

Automotive semiconductor companies, software developers, cloud providers, AI firms, and traditional Tier-1 suppliers are competing aggressively through technological innovation and strategic partnerships.

Strategic Implications of Market Risk & Disruption

1. Investment in Centralized Vehicle Computing

Automotive manufacturers are increasingly replacing multiple distributed ECUs with centralized high-performance computing platforms to simplify vehicle architecture and improve scalability.

2. Expansion of Automotive Cybersecurity Capabilities

Companies are strengthening secure boot systems, encrypted communications, intrusion detection, OTA security, and cybersecurity monitoring to protect connected vehicles.

3. Diversification of Semiconductor Supply Chains

OEMs and suppliers are expanding sourcing strategies, regional semiconductor manufacturing, and long-term supplier partnerships to improve supply resilience.

4. AI-Driven Software Development & Validation

Manufacturers are leveraging AI-assisted software testing, predictive diagnostics, digital twins, and automated validation tools to improve software quality and reduce development time.

Global Automotive Embedded Systems in Automobile Market Risk & Disruption Forward Outlook

1. Software-Defined Vehicles Will Become Industry Standard

Centralized computing platforms and software-centric vehicle architectures will increasingly replace traditional distributed electronic systems.

2. AI Will Drive Intelligent Vehicle Computing

Artificial intelligence will enhance ADAS, autonomous driving, predictive maintenance, energy optimization, and real-time vehicle decision-making.

3. Automotive Cybersecurity Will Become a Core Competitive Requirement

Future embedded systems will incorporate advanced cybersecurity frameworks, secure OTA platforms, hardware security modules, and continuous threat monitoring.

4. Edge AI Will Expand Across Vehicle Platforms

Real-time onboard AI processing will improve autonomous driving performance, sensor fusion, driver monitoring, and intelligent vehicle control.

5. Semiconductor Localization Will Increase

Governments and manufacturers are expected to strengthen domestic semiconductor production and regional supply chains to reduce dependency on global suppliers.

6. OTA Software Ecosystems Will Continue Expanding

Continuous software upgrades, feature-on-demand capabilities, remote diagnostics, and cloud-enabled vehicle management will become standard across modern vehicles.

7. Functional Safety Standards Will Continue to Evolve

Increasing automation and software complexity will drive stricter compliance with automotive functional safety, software reliability, and cybersecurity regulations.

8. Collaboration Across the Automotive Technology Ecosystem Will Accelerate

OEMs, semiconductor manufacturers, AI developers, cloud providers, and embedded software companies will continue expanding strategic partnerships to support next-generation intelligent mobility.

Regulatory Landscape

Global Automotive Embedded Systems in Automobile Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a critical role in shaping the Global Automotive Embedded Systems in Automobile Market by governing the design, development, validation, cybersecurity, functional safety, software lifecycle management, and deployment of embedded electronic systems used in modern vehicles. Governments, automotive regulators, and international standards organizations establish comprehensive frameworks to ensure vehicle safety, software reliability, data security, emissions compliance, and interoperability across increasingly connected and software-defined vehicles.

The market is primarily influenced by ISO 26262 Functional Safety, ISO/SAE 21434 Road Vehicles Cybersecurity Engineering, UNECE WP.29 Cybersecurity Regulation (UN R155), UNECE Software Update Regulation (UN R156), AUTOSAR standards, ASPICE (Automotive SPICE), IEC 61508, General Safety Regulation (GSR), vehicle type-approval frameworks, and regional automotive cybersecurity and data protection regulations. These regulatory frameworks support safe software development, secure over-the-air (OTA) updates, functional safety validation, and the reliable deployment of intelligent automotive electronics.

Global Automotive Embedded Systems in Automobile Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape emphasizes vehicle functional safety, software-defined vehicle (SDV) governance, cybersecurity resilience, OTA software management, and advanced driver assistance system (ADAS) validation. Regulatory agencies are strengthening compliance requirements for connected vehicles, AI-enabled embedded systems, autonomous driving technologies, and automotive cybersecurity to address increasing software complexity and cyber risks.

Automotive manufacturers are increasingly required to implement cybersecurity management systems, software update management systems, secure ECU architectures, functional safety engineering, and continuous software lifecycle monitoring. Regulatory attention is also expanding toward AI-driven vehicle functions, data privacy, V2X communication security, and centralized vehicle computing platforms.

Key Regulatory & Policy Environment Signals in the Global Automotive Embedded Systems in Automobile Market

1. Functional Safety & Vehicle Certification

Automotive regulators continue strengthening functional safety requirements through ISO 26262, ensuring embedded hardware and software systems operate safely under both normal and fault conditions while supporting vehicle type approval.

2. Automotive Cybersecurity & Software Compliance

Global adoption of UNECE WP.29 Regulations (UN R155 & UN R156) and ISO/SAE 21434 is driving stricter cybersecurity management, secure software development, software update governance, and protection against cyber threats throughout the vehicle lifecycle.

3. Software-Defined Vehicle (SDV) & OTA Update Governance

Governments and automotive authorities are introducing policies supporting secure over-the-air software updates, centralized vehicle computing, software version control, and lifecycle software management for increasingly software-centric vehicles.

4. AI, Autonomous Driving & ADAS Regulation

Regulators are expanding oversight of AI-enabled embedded systems, autonomous driving technologies, sensor fusion platforms, and ADAS validation to ensure operational safety, transparency, and human oversight where required.

5. Connected Vehicle & Data Protection Requirements

Increasing deployment of connected vehicles and V2X communication is strengthening regulations covering vehicle data privacy, secure communications, cloud connectivity, telematics security, and cross-border automotive data governance.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging automotive OEMs, semiconductor manufacturers, and embedded software providers to develop functionally safe, cyber-secure, software-defined, and standards-compliant embedded systems capable of supporting connected, electric, and autonomous vehicles. Companies are increasing investment in automotive-grade semiconductors, AI-enabled processors, secure software platforms, OTA infrastructure, cybersecurity engineering, and functional safety certification to comply with evolving global regulations.

Manufacturers capable of delivering certified, secure, interoperable, and software-centric embedded platforms are expected to strengthen their competitive position as intelligent mobility, electrification, and autonomous vehicle deployment continue to accelerate.

Global Automotive Embedded Systems in Automobile Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, regulatory frameworks are expected to place greater emphasis on software-defined vehicle governance, AI safety assurance, automotive cybersecurity resilience, centralized vehicle computing, secure OTA software management, autonomous driving validation, and connected vehicle interoperability. Governments are likely to strengthen certification requirements for AI-enabled automotive systems while expanding regulations covering vehicle software, cybersecurity, and digital mobility infrastructure.

Future policy developments are also expected to promote greater international harmonization of functional safety standards, cybersecurity requirements, autonomous vehicle regulations, and software certification frameworks, supporting the continued evolution of intelligent, connected, and software-defined mobility ecosystems.