Global Driving Simulator Market size and share Analysis 2026-2033

Global Driving Simulator Market Forecast Snapshot: 2026???2033

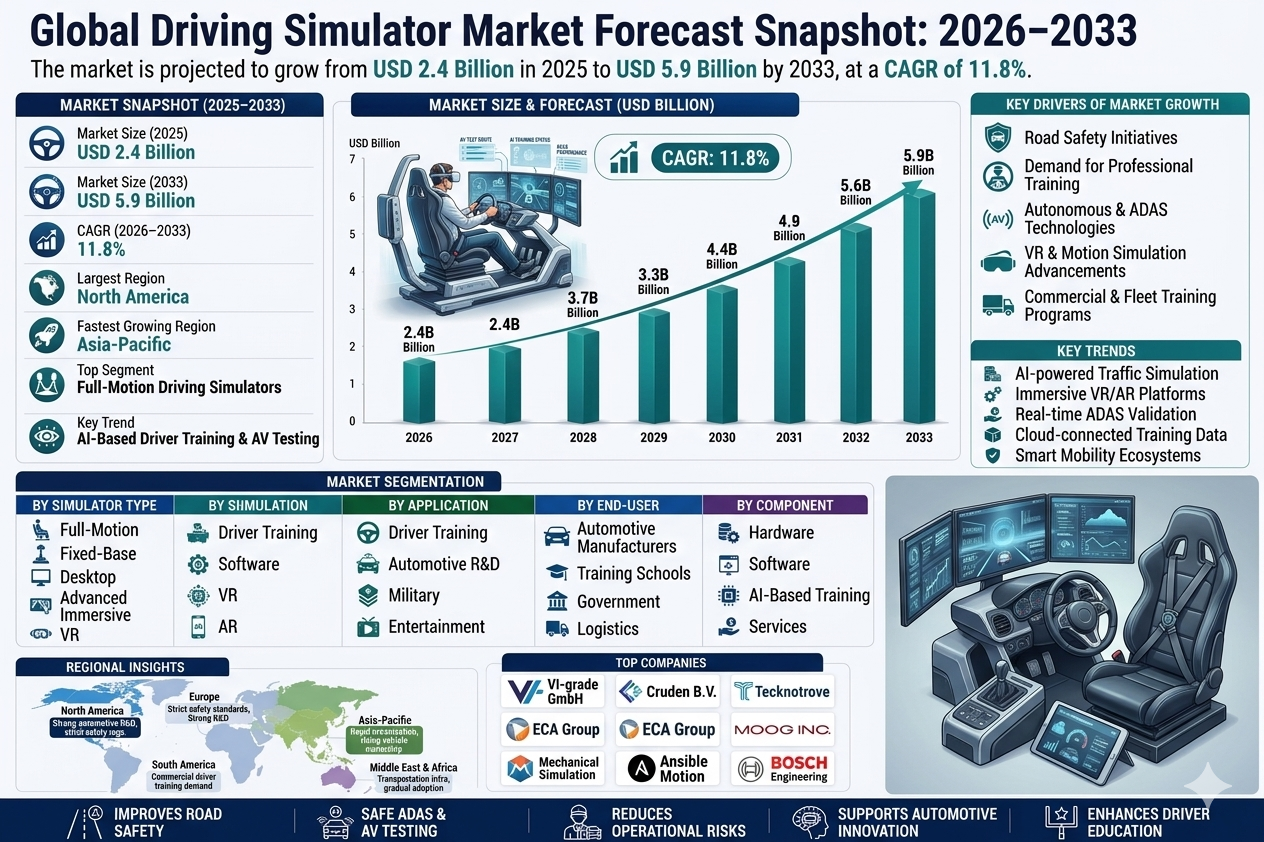

| Metric | Value |

| 2025 Market Size | USD 2.4 Billion |

| 2033 Market Size | USD 5.9 Billion |

| CAGR (2026???2033) | 11.8% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Full-Motion Driving Simulators |

| Key Trend | AI-Based Driver Training & Autonomous Vehicle Testing |

| Future Focus | VR/AR Simulation, ADAS Testing, and Smart Mobility Training |

Global Driving Simulator Market Overview

The Global Driving Simulator Market is speeding ahead.Driving simulators are revving up, with car makers, driving schools, and transport authorities using them to boost safety, training, and vehicle testing. These simulators recreate real-world roads virtually, making training safer and more effective, driven by safety, easy training, and simple testing ??? all contributing to a safer driving experience.According to Pheonix Research, the Global Driving Simulator Market is valued at USD 2.4 billion in 2025 and is projected to reach USD 5.9 billion by 2033, registering a CAGR of 11.8% during 2026???2033. Market growth is driven by rising road safety initiatives, increasing demand for professional driver training, and expanding use of simulation technology in autonomous vehicle and ADAS testing.

North America currently dominates the market due to strong investments in automotive R&D, the presence of major simulator technology providers, and strict driver safety regulations. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, supported by rapid urbanization, increasing vehicle ownership, and growing demand for driver education and transport training infrastructure.

The post-2025 outlook indicates greater integration of AI-powered simulation environments, VR/AR immersive driving platforms, and real-time traffic simulation systems, positioning driving simulators as a critical technology for next-generation mobility and intelligent transportation systems.

Key Drivers of Global Driving Simulator Market Growth

1. Increasing Focus on Road Safety and Driver Training

Governments and transportation authorities are promoting simulator-based training to reduce road accidents and improve driver skills before real-world driving.

2. Rising Adoption in Automotive Research & Development

Automotive manufacturers increasingly use driving simulators for vehicle testing, performance validation, and autonomous driving development.

3. Growth of Autonomous and ADAS Technologies

Simulation platforms enable safe testing of advanced driver assistance systems (ADAS) and autonomous driving algorithms in complex traffic scenarios.

4. Technological Advancements in VR and Motion Simulation

Integration of virtual reality, high-resolution graphics, and motion platforms is enhancing realism and training effectiveness.

5. Expansion of Commercial and Fleet Driver Training Programs

Logistics companies, transportation fleets, and public transit agencies are adopting simulators to train drivers efficiently and reduce operational risks.

Global Driving Simulator Market Segmentation

?? ?? ??1.By Simulator Type

1.1 Full-Motion Driving Simulators

1.1.1 Hydraulic Motion Platforms

1.1.1.1 Multi-Axis Motion Systems

1.1.1.1.1 Automotive R&D Simulation

1.1.1.1.2 Advanced Driver Training

1.1.2 Electric Motion Platforms

1.1.2.1 Precision Motion Systems

1.1.2.1.1 High-End Training Simulators

1.1.2.1.2 Autonomous Vehicle Testing

1.2 Fixed-Base Driving Simulators

1.2.1 Desktop Simulation Systems

1.2.1.1 Educational Driving Simulators

1.2.1.1.1 Driving Schools

1.2.1.1.2 Training Institutes

1.2.2 Console-Based Simulators

1.2.2.1 Semi-Professional Training Systems

1.2.2.1.1 Corporate Driver Training

1.2.2.1.2 Fleet Driver Training

1.3 Advanced Immersive Simulators

1.3.1 Virtual Reality (VR) Driving Simulators

1.3.1.1 Head-Mounted Display Systems

1.3.1.1.1 Individual Driver Training

1.3.1.1.2 Research Simulation

1.3.2 Augmented Reality (AR) Simulators

1.3.2.1 Mixed Reality Driving Systems

1.3.2.1.1 ADAS Testing

1.3.2.1.2 Smart Mobility Research

?? ??2.By Component

2.1 Hardware

2.1.1 Motion Platforms

2.1.1.1 Hydraulic Motion Systems

2.1.1.2 Electric Motion Systems

2.1.2 Display Systems

2.1.2.1 Multi-Screen Displays

2.1.2.2 360-Degree Dome Displays

2.1.3 Control Systems

2.1.3.1 Steering & Pedal Systems

2.1.3.2 Force Feedback Controls

2.2 Software

2.2.1 Simulation Software Platforms

2.2.1.1 Traffic Scenario Simulation

2.2.1.2 Weather & Environment Simulation

2.2.2 AI-Based Training Systems

2.2.2.1 Driver Behavior Analysis

2.2.2.2 Performance Assessment Systems

2.3 Services

2.3.1 Simulator Installation & Integration

2.3.1.1 Training Center Setup

2.3.1.2 Automotive R&D Integration

2.3.2 Maintenance & Support Services

2.3.2.1 Hardware Maintenance

2.3.2.2 Software Updates

?? ?? 3.By Application

3.1 Driver Training

3.1.1 Professional Driver Training

3.1.1.1 Commercial Vehicle Training

3.1.1.2 Public Transport Training

3.1.2 Driving Schools

3.1.2.1 Beginner Driver Education

3.1.2.2 Advanced Driving Courses

3.2 Automotive Research & Development

3.2.1 Vehicle Performance Testing

3.2.1.1 Engine & Powertrain Simulation

3.2.1.2 Vehicle Dynamics Testing

3.2.2 Autonomous Vehicle Development

3.2.2.1 Self-Driving Algorithm Testing

3.2.2.2 AI Driving Model Training

3.3 Military & Defense Training

3.3.1 Tactical Vehicle Training

3.3.2 Armored Vehicle Simulation

3.4 Entertainment & Gaming

3.4.1 Racing Simulation Centers

3.4.2 Esports Driving Simulation

?? ??4.By End-User

4.1 Automotive Manufacturers

4.1.1 Vehicle Development Centers

4.1.2 Autonomous Vehicle Research Labs

4.2 Driver Training Schools

4.2.1 Commercial Driving Schools

4.2.2 Public Driver Education Institutes

4.3 Government & Transportation Authorities

4.3.1 Road Safety Agencies

4.3.2 Public Transport Training Centers

4.4 Logistics & Fleet Operators

4.4.1 Truck Driver Training Programs

4.4.2 Delivery Fleet Training Systems

?? 5.By Region

5.1 North America

5.2 Europe

5.3 Asia-Pacific

5.4 Middle East & Africa

5.5 South America

Regional Insights of Global Driving Simulator Market

North America ??? Largest Market

North America dominates the market due to strong automotive R&D investments, advanced driver safety regulations, and widespread adoption of simulation technologies in driver training and vehicle development.

Asia-Pacific ??? Fastest Growing Market

Rapid urbanization, increasing vehicle ownership, and growing investments in transportation training infrastructure are driving strong growth across China, India, Japan, and South Korea.

Europe

Europe???s market growth is supported by strict road safety regulations, strong automotive manufacturing presence, and increasing research into autonomous vehicle technologies.

Middle East & Africa

Rising investment in transportation infrastructure and driver training programs is gradually expanding simulator adoption in the region.

South America

Growing demand for commercial driver training and road safety initiatives is supporting steady market development.

Leading Companies in Global Driving Simulator Market

-

Tecknotrove Simulator System Pvt. Ltd.

-

ECA Group

-

Moog Inc.

-

Mechanical Simulation Corporation

-

Ansible Motion Ltd.

-

Bosch Engineering GmbH

These companies are focusing on advanced simulation technologies, immersive VR-based training environments, and AI-driven driver behavior analysis to strengthen their competitive positioning in the market.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine identifies increasing adoption of simulator-based driver training, autonomous vehicle testing, and automotive R&D investments as primary long-term growth drivers. Innovation Tracker highlights VR/AR simulation platforms, AI-based driver behavior analytics, and real-time traffic environment modeling as major competitive differentiators. Infrastructure Investment Analyzer indicates rising global investment in driver training infrastructure and automotive simulation laboratories. Porter???s Five Forces Analysis reveals moderate supplier power, high technology barriers for new entrants, and strong competition among established simulator technology providers.Why the Global Driving Simulator Market is Critical

-

Improves driver safety through realistic training environments.

-

Enables safe testing of autonomous and ADAS technologies.

-

Reduces training costs and operational risks for transport operators.

-

Supports automotive innovation and vehicle development.

-

Enhances driver education and road safety awareness.

Final Takeaway of Global Driving Simulator Market

The Global Driving Simulator Market is rapidly evolving into a technology-driven ecosystem supporting driver training, automotive research, and intelligent mobility development. The Driving Simulator Market CAGR 2026???2033 of 11.8% reflects strong expansion driven by road safety initiatives, autonomous vehicle development, and advanced simulation technologies.

Companies that invest in AI-driven simulation platforms, immersive VR/AR training environments, and autonomous vehicle testing capabilities will be well positioned for long-term competitive advantage.

At Pheonix Research, our advanced forecasting frameworks provide in-depth revenue forecasts, regional insights, technology benchmarking, and strategic intelligence, enabling stakeholders to capitalize on the evolving global driving simulator market with confidence.

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on??LinkedIn??and??X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7436301705400557568

X : https://x.com/Pheonix_Insight/status/2030537524821807142?s=20

Competitive Landscape

Global Driving Simulator Market Competitive Intensity & Market Structure Overview

The Global Driving Simulator Market is characterized by a highly technology-driven and innovation-intensive competitive landscape, shaped by the convergence of automotive engineering, simulation software, and immersive digital technologies. The market is evolving rapidly as demand rises for safer driver training, autonomous vehicle testing, and advanced mobility research platforms.

The market structure is moderately consolidated, with a group of specialized simulation technology providers and engineering firms dominating high-end automotive R&D and full-motion simulator deployments. At the same time, a growing number of regional and niche players are competing in cost-effective and training-focused simulator segments.

Competitive intensity is increasing due to rapid advancements in AI-based simulation, VR/AR integration, and real-time environment modeling. Vendors are competing not only on hardware capabilities but also on software intelligence, realism, scalability, and total cost of ownership (TCO).

Global Driving Simulator Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

VI-grade GmbH: Simulation Technology Leader. Known for high-end automotive simulation platforms and advanced driving simulator solutions for OEM R&D applications.

Cruden B.V.: Professional Simulator Provider. Specializes in high-performance driving simulators for motorsport, automotive development, and research applications.

Tecknotrove Simulator System Pvt. Ltd.: Emerging Market Leader. Strong presence in driver training simulators for commercial, defense, and public transport sectors.

ECA Group: Simulation & Training Specialist. Provides advanced simulation systems for defense, industrial, and transportation training applications.

Moog Inc.: Motion Control Technology Provider. Leader in precision motion platforms and simulation systems for high-fidelity driving environments.

Mechanical Simulation Corporation: Software-Focused Player. Known for vehicle dynamics simulation software and automotive testing platforms.

Ansible Motion Ltd.: Advanced Simulation Innovator. Focuses on high-end driver-in-the-loop simulators and autonomous vehicle testing systems.

Bosch Engineering GmbH: Automotive Engineering Leader. Integrates simulation technologies with ADAS and autonomous vehicle development solutions.

Key Competitive Intensity & Market Structure Signals in Global Driving Simulator Market

A key competitive signal is the increasing integration of AI and data analytics into simulation platforms. Vendors are developing intelligent systems capable of analyzing driver behavior, predicting risk scenarios, and optimizing training outcomes, significantly enhancing value proposition.

The growing demand for autonomous vehicle and ADAS testing is reshaping the competitive landscape. High-fidelity simulators capable of replicating complex real-world driving conditions are becoming essential, favoring technologically advanced players.

Another major signal is the rapid adoption of VR/AR-based immersive simulation environments. These technologies are lowering entry barriers for training-focused solutions while simultaneously increasing competition among providers offering cost-effective yet realistic simulators.

Additionally, government and fleet-driven demand for driver safety training is expanding the market, creating opportunities for mid-tier and regional players to compete in standardized training solutions.

Strategic Implications of Competitive Intensity & Market Structure in Global Driving Simulator Market

Companies are increasingly shifting toward integrated simulation ecosystems that combine hardware, software, and analytics into unified platforms. This approach enhances customer value and strengthens long-term partnerships with automotive OEMs and training institutions.

Total cost of ownership (TCO) is becoming a critical decision factor, particularly in driver training and fleet applications, where cost efficiency and scalability are prioritized alongside performance.

Investment in AI-driven simulation, digital twin environments, and real-time traffic modeling is emerging as a key strategic differentiator. Companies that lead in these technologies are gaining a competitive edge in autonomous vehicle development and advanced mobility research.

Partnerships with automotive manufacturers, government agencies, and mobility solution providers are playing a crucial role in expanding market reach and accelerating technology adoption.

Global Driving Simulator Market Competitive Intensity & Market Structure Forward Outlook

The market is expected to remain highly competitive, with increasing convergence between simulation technology providers, automotive OEMs, and software companies. Strategic collaborations and acquisitions will play a key role in strengthening technological capabilities and market positioning.

AI-powered simulation, immersive VR/AR environments, and cloud-based training platforms will define the next phase of competition, particularly in autonomous driving and smart mobility applications.

Emerging markets will offer strong growth opportunities for cost-effective and scalable simulator solutions, intensifying competition in training and education segments.

In the long term, the market will be defined by three core competitive pillars: simulation realism, AI-driven intelligence, and scalable training ecosystems. Companies that align with these pillars while maintaining strong innovation pipelines and global partnerships will lead the Global Driving Simulator Market through 2033.

Value Chain

Global Driving Simulator Market Value Chain & Supply Chain Evolution Overview

The Global Driving Simulator Market value chain is evolving from traditional hardware-centric simulation systems toward integrated, software-driven, and AI-enabled simulation ecosystems. This transformation is driven by increasing demand for advanced driver training, autonomous vehicle testing, and real-time mobility simulation. Driving simulators are becoming critical tools across automotive R&D, transportation safety, and intelligent mobility development.

Driving simulators combine high-performance hardware, immersive visualization systems, advanced software platforms, and AI-based analytics to replicate real-world driving environments. The value chain extends beyond manufacturing into simulation software development, AI modeling, sensor integration, and data-driven performance analytics.

The upstream supply chain relies on precision components such as motion platforms, display systems, VR/AR devices, sensors, processors, and control systems. Software development, including simulation engines, physics modeling, and AI-based driver behavior analysis, plays a central role in value creation.

Manufacturing focuses on system integration, combining hardware and software into fully functional simulator platforms. Companies are increasingly investing in modular simulator architectures, scalable solutions, and high-fidelity simulation environments.

Distribution includes direct sales to automotive OEMs, driving schools, research institutions, and government agencies, along with system integration partnerships. Service-based models such as simulation-as-a-service and software licensing are also emerging.

Key supply chain challenges include high system costs, integration complexity, continuous software upgrades, and the need for real-time simulation accuracy and reliability.

Global Driving Simulator Market Value Chain & Supply Chain Evolution Current Scenario

The current market ecosystem is shaped by increasing adoption of simulation technologies across driver training, automotive R&D, and autonomous vehicle development.

Upstream suppliers are focusing on high-performance hardware components, immersive display technologies, and advanced computing systems to support realistic simulations.

Software providers are developing AI-driven simulation platforms, real-time traffic modeling systems, and advanced analytics tools for driver performance evaluation.

Manufacturers are integrating motion systems, VR/AR technologies, and simulation software into unified platforms for diverse applications.

End users such as automotive companies, training institutes, and government agencies are increasingly adopting simulators to improve safety, reduce costs, and enhance testing capabilities.

Cloud-based simulation platforms, remote training systems, and digital twin technologies are emerging as key trends in the ecosystem.

Key Value Chain & Supply Chain Evolution Signals in Global Driving Simulator Market

Several key trends are reshaping the market landscape.

First, AI-driven simulation and analytics are transforming driver training and vehicle testing processes.

Second, VR and AR technologies are enhancing simulation realism and immersive training experiences.

Third, autonomous vehicle development is significantly increasing demand for advanced simulation platforms.

Fourth, cloud-based simulation and remote training solutions are expanding accessibility and scalability.

Fifth, modular and scalable simulator systems are enabling flexible deployment across different end-user segments.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Driving Simulator Market

Leading companies such as VI-grade, Cruden, Moog Inc., and Bosch Engineering are strengthening their market positions through advanced simulation technologies, AI integration, and high-fidelity system design.

Competitive advantage increasingly depends on software capabilities, simulation accuracy, system integration expertise, and ability to deliver scalable and customizable solutions.

Companies with strong capabilities in AI modeling, real-time simulation, and VR/AR integration are better positioned to capture high-value market segments.

Strategic collaborations with automotive OEMs, research institutions, and government agencies are becoming critical for long-term growth.

Balancing system cost, performance, and scalability remains essential, particularly for expanding adoption in training and emerging markets.

Global Driving Simulator Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to become increasingly software-driven, AI-powered, and cloud-enabled.

Simulation platforms will evolve toward fully autonomous, self-learning systems capable of real-time adaptation and predictive analytics.

Integration of digital twins, real-world data, and connected vehicle ecosystems will enhance simulation accuracy and relevance.

Cloud-based simulation-as-a-service models will expand, enabling remote access and scalable deployment.

VR/AR immersive environments and advanced motion systems will further enhance realism and training effectiveness.

Ultimately, the driving simulator market will evolve into a critical pillar of intelligent mobility ecosystems, supporting safety, innovation, and autonomous transportation development.

Market-Specific Value Chain

- Component & Technology Supply: Motion platforms, VR/AR devices, sensors, processors, display systems, control hardware

- Software & AI Development: Simulation engines, physics modeling, AI driver behavior analytics, traffic simulation software

- System Integration & Manufacturing: Simulator assembly, hardware-software integration, testing and validation

- Deployment & Integration: Automotive OEM integration, training center setup, R&D lab deployment

- Distribution & Commercialization: Direct sales, system integrators, global distribution networks, SaaS models

- Aftermarket & Lifecycle Services: Maintenance, software updates, simulation upgrades, technical support, performance analytics

Company-to-Stage Mapping

- Component & Technology Supply: Moog Inc., Bosch Engineering GmbH, Siemens (automation & control components)

- Software & AI Development: Mechanical Simulation Corporation, VI-grade GmbH, Cruden B.V.

- System Integration & Manufacturing: Tecknotrove Simulator System Pvt. Ltd., ECA Group, Ansible Motion Ltd.

- Deployment & Integration: VI-grade GmbH, Cruden B.V., Bosch Engineering GmbH

- Distribution & Commercialization: Global simulator providers, system integrators, regional distributors

- Aftermarket & Lifecycle Services: Moog Inc., VI-grade GmbH, Cruden B.V., service partners

Investment Activity

Global Driving Simulator Market Investment & Funding Dynamics Overview

Investment in the Global Driving Simulator Market is accelerating rapidly, fueled by increasing focus on road safety, expansion of autonomous vehicle development, and growing adoption of simulation technologies across training and R&D applications. Between 2026 and 2033, capital allocation is expected to concentrate on full-motion simulators, AI-based training platforms, VR/AR immersive environments, and advanced automotive simulation systems.

The market is evolving into a high-tech, innovation-driven segment attracting investments from automotive OEMs, technology providers, government bodies, and private investors. Leading companies such as VI-grade, Cruden, Moog Inc., Bosch Engineering, and Ansible Motion are investing heavily in high-fidelity simulation systems, real-time data integration, and AI-driven analytics to enhance realism and performance.

A major shift shaping investment flows is the growing reliance on simulation for autonomous vehicle testing and ADAS validation. This is directing funding toward highly sophisticated, scalable simulation platforms capable of replicating complex real-world driving conditions in a controlled environment.

Global Driving Simulator Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is being driven by rising demand for professional driver training, automotive R&D expansion, and increasing integration of simulation technologies into safety and testing frameworks.

- North America: Leads investment due to strong automotive R&D ecosystem, early adoption of simulation technologies, and significant funding in autonomous vehicle development.

- Asia-Pacific: Fastest-growing investment region supported by rapid urbanization, increasing vehicle ownership, and expansion of driver training infrastructure.

- Europe: Strong investment focus on automotive innovation, safety regulations, and autonomous driving research.

- Middle East & Africa: Emerging investment landscape driven by transportation modernization and driver training initiatives.

Key Investment & Funding Dynamics Signals in Global Driving Simulator Market

- Rising investment in AI-based driver behavior analysis and performance assessment systems.

- Growing funding for VR/AR-based immersive simulation technologies to enhance training realism.

- Automotive OEMs increasing investment in simulation for autonomous and ADAS testing.

- Expansion of commercial driver training programs driving demand for scalable simulator solutions.

- Integration of real-time data and advanced analytics is attracting technology-focused investments.

Strategic Implications of Investment & Funding Dynamics in Global Driving Simulator Market

- Companies with strong capabilities in AI, VR/AR, and motion simulation technologies are attracting higher investment.

- Partnerships between automotive manufacturers and simulation technology providers are increasing.

- Investment strategies are shifting toward scalable, modular simulation platforms.

- Regional expansion into Asia-Pacific is becoming critical for long-term growth.

- Continuous innovation in simulation realism and data analytics is essential for competitive positioning.

Global Driving Simulator Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Driving Simulator Market is expected to attract sustained and high-value investment as simulation becomes a core component of driver training, vehicle testing, and smart mobility development.

Future investments will focus on AI-driven simulation platforms, VR/AR immersive environments, autonomous vehicle testing systems, and integrated mobility simulation ecosystems.

- North America: Will continue leading investments in advanced simulation technologies and autonomous vehicle testing platforms.

- Asia-Pacific: Will dominate future growth driven by expanding training infrastructure and automotive market expansion.

- Europe: Will emphasize innovation in safety, regulatory compliance, and autonomous mobility research.

Technological advancements in real-time simulation, digital twins, and AI-based traffic modeling will further influence funding strategies across the market.

Overall, the market will remain a high-growth, innovation-led investment segment through 2033, supported by its critical role in enhancing road safety, enabling autonomous mobility, and advancing automotive R&D. Companies that lead in simulation accuracy, scalability, and AI integration will shape the future competitive landscape.

Technology & Innovation

Global Driving Simulator Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Driving Simulator Market is rapidly evolving toward highly immersive, AI-driven, and data-centric simulation ecosystems. Driving simulators are transitioning from basic training tools into advanced platforms capable of replicating complex real-world driving environments for training, testing, and research applications.

Innovation intensity in this market is high, driven by advancements in artificial intelligence, virtual reality (VR), augmented reality (AR), motion simulation systems, and real-time physics-based modeling. Leading companies such as VI-grade GmbH, Cruden B.V., Moog Inc., Bosch Engineering, and Tecknotrove are investing in next-generation simulators that combine high-fidelity visuals, precise motion feedback, and intelligent analytics.

A major technological shift is the integration of AI-powered driver behavior analysis and autonomous driving simulation. These systems enable real-time evaluation of driver performance, predictive risk assessment, and training optimization, while also supporting development and validation of ADAS and self-driving algorithms.

Simultaneously, advancements in cloud computing, edge processing, and digital twin technology are enabling scalable simulation environments, remote access capabilities, and continuous software updates, enhancing flexibility and deployment efficiency.

Global Driving Simulator Market Technology & Innovation Landscape Current Scenario

Currently, the market is focused on enhancing realism, interactivity, and scalability of simulation platforms. Companies are prioritizing technologies that improve user immersion while expanding application areas across driver training, automotive R&D, and autonomous vehicle development.

AI-driven simulation software is emerging as a key innovation pillar, enabling dynamic traffic scenarios, adaptive learning environments, and real-time performance analytics. These systems can simulate unpredictable driving conditions, enhancing both training effectiveness and testing accuracy.

Motion simulation technologies are advancing through multi-axis platforms, force feedback systems, and high-precision actuators, providing realistic vehicle dynamics and physical feedback to users.

VR and AR-based immersive simulators are gaining traction, offering 360-degree visualization, interactive environments, and enhanced situational awareness for drivers and researchers.

Sensor integration and real-time data processing are also improving environmental simulation capabilities, allowing accurate modeling of weather conditions, road surfaces, and traffic behaviors.

Cloud-based simulation platforms are enabling remote collaboration, large-scale scenario testing, and shared simulation environments across geographically distributed teams.

Key Technology & Innovation Trends in Global Driving Simulator Market

- AI-Based Driver Behavior Analytics: Real-time performance assessment, risk prediction, and adaptive training systems.

- VR/AR Immersive Simulation: 360-degree environments enhancing realism and user engagement.

- Advanced Motion Platforms: Multi-axis systems delivering precise physical feedback and vehicle dynamics.

- Autonomous Vehicle Simulation: Testing and validation of self-driving algorithms and ADAS technologies.

- Real-Time Traffic & Environment Modeling: Dynamic simulation of complex driving scenarios.

- Cloud-Based Simulation Platforms: Remote access, collaborative testing, and scalable deployment.

- Digital Twin Integration: Virtual replication of real vehicles and driving environments.

- Edge Computing for Low Latency: Faster processing and real-time responsiveness in simulations.

Strategic Implications of Technology & Innovation

Technological advancements are transforming driving simulators into critical infrastructure for both training and automotive innovation. Companies investing in AI-driven analytics, immersive simulation technologies, and scalable platforms are likely to gain a strong competitive edge.

For automotive manufacturers, advanced simulators significantly reduce development costs and time-to-market by enabling virtual testing of vehicle systems and autonomous technologies.

In driver training, simulation technologies improve safety outcomes, reduce operational risks, and enable standardized skill development across diverse driver populations.

However, high initial investment costs, system complexity, and the need for continuous software upgrades present challenges for widespread adoption, particularly among smaller training providers.

Regulatory bodies and governments are increasingly recognizing simulation-based training as a critical component of road safety strategies, further supporting market growth.

Global Driving Simulator Market Technology & Innovation Forward Outlook

Looking ahead, the Global Driving Simulator Market is expected to evolve toward fully intelligent, autonomous, and hyper-realistic simulation ecosystems. Future simulators will increasingly integrate AI, machine learning, and real-time data analytics to deliver adaptive and personalized training experiences.

The adoption of digital twin technology will enable precise replication of real-world vehicles and infrastructure, enhancing testing accuracy for automotive R&D and smart mobility solutions.

VR and AR technologies will continue to advance, providing deeper immersion and more interactive simulation environments, particularly for complex urban and autonomous driving scenarios.

Cloud and edge computing will play a critical role in enabling large-scale simulation networks, real-time collaboration, and continuous system optimization.

In conclusion, the Global Driving Simulator Market is transitioning into a highly advanced, AI-powered, and immersive simulation ecosystem. Companies that lead in AI integration, motion simulation, VR/AR technologies, and autonomous testing platforms will shape the future of driver training and mobility innovation through 2033.

Regulatory Landscape

Global Driving Simulator Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Driving Simulator Market is evolving as governments, transportation authorities, and safety organizations increasingly integrate simulation technologies into formal driver training, testing, and automotive validation frameworks. Driving simulators are gaining recognition as critical tools for enhancing road safety, reducing accident risks, and enabling controlled testing of advanced vehicle technologies.

Regulations across regions are focusing on standardizing simulator-based training, ensuring system accuracy, and validating simulation outputs for driver certification and autonomous vehicle development. Authorities are establishing guidelines to ensure that simulators replicate real-world driving conditions with high fidelity and meet defined performance benchmarks.

Additionally, the growing use of simulators in autonomous vehicle (AV) and ADAS testing is prompting regulatory bodies to incorporate simulation-based validation into approval processes. This shift is driving demand for high-precision, AI-enabled simulation platforms capable of generating reliable and compliant test data.

As adoption increases globally, regulatory alignment remains fragmented, requiring simulator providers and users to comply with diverse national standards related to safety, data handling, and certification.

Global Driving Simulator Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by gradual but increasing formalization of simulator usage in driver training and vehicle testing. North America and Europe are leading in regulatory adoption, with structured frameworks supporting simulator-based driver education and research applications.

In North America, transportation authorities and safety agencies are promoting simulator-based training programs, particularly for commercial drivers, while also supporting simulation in autonomous vehicle testing under controlled regulatory guidelines.

Europe maintains stringent safety and training standards, with regulatory bodies encouraging the integration of simulators into driver licensing programs and automotive R&D. The region also emphasizes compliance with safety, ergonomics, and system validation standards.

Asia-Pacific is experiencing rapid regulatory development, with countries such as China, India, and Japan increasingly adopting simulation technologies in driver training infrastructure and smart mobility initiatives. Government-backed programs are supporting digital training systems to address rising road safety concerns.

In the Middle East & Africa and South America, regulatory frameworks are still emerging, but growing investments in transportation infrastructure and safety initiatives are driving gradual adoption of simulator-based training standards.

Across regions, automotive manufacturers, training institutes, and government agencies are aligning with evolving regulatory expectations by deploying compliant and certified simulation systems.

Key Regulatory & Policy Environment Signals in Global Driving Simulator Market

- Driver Training & Licensing Regulations: Governments are incorporating simulator-based training hours into official licensing and certification programs.

- Simulation Validation Standards: Regulatory bodies require high-fidelity simulation systems that accurately replicate real-world driving scenarios.

- Autonomous Vehicle Testing Frameworks: Increasing acceptance of simulation-based validation for ADAS and self-driving technologies.

- Safety & Performance Compliance: Standards governing ergonomics, system responsiveness, and human-machine interaction.

- Data Privacy & Cybersecurity Regulations: Compliance with data protection laws for driver performance data and cloud-based simulation platforms.

- Industry-Specific Training Mandates: Regulations promoting simulator use in commercial fleet, defense, and public transport training programs.

Strategic Implications of Regulatory & Policy Environment in Global Driving Simulator Market

Regulatory developments are transforming driving simulators from optional training tools into essential components of certified driver education and vehicle validation ecosystems. Companies must invest in compliant, high-fidelity simulation technologies that meet evolving regulatory standards.

The growing acceptance of simulation in autonomous vehicle testing is creating new opportunities for simulator providers, while also increasing the need for advanced scenario modeling, AI-driven analytics, and validation capabilities.

Data privacy and cybersecurity requirements are pushing organizations to integrate secure data management systems within simulation platforms, particularly for cloud-based and AI-driven solutions.

Regulatory-driven adoption in commercial driver training, defense applications, and public transport sectors is expanding the market scope, requiring scalable and customizable simulation solutions.

Vendors offering certified, regulation-compliant, and technologically advanced simulation platforms are gaining competitive advantage, while non-compliant systems face limitations in adoption.

Global Driving Simulator Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for driving simulators is expected to become more structured and globally aligned, particularly in driver training certification and autonomous vehicle validation. Governments will increasingly formalize the role of simulators in reducing road accidents and improving driver competency.

North America and Europe will continue leading regulatory advancements, while Asia-Pacific will accelerate policy development driven by smart mobility initiatives and urban transportation challenges.

Simulation-based validation is expected to become a standard requirement for autonomous vehicle testing, significantly increasing demand for advanced, AI-enabled simulation platforms.

Data security, system accuracy, and compliance certification will become critical regulatory focus areas, driving continuous innovation in simulator technologies.

Overall, the regulatory landscape will play a crucial role in shaping the future of the Global Driving Simulator Market, driving adoption, standardization, and technological advancement. Companies that proactively align with regulatory requirements and invest in compliant, high-performance simulation solutions will be best positioned to lead in the evolving mobility ecosystem.