Global Sustainable & Green Tyres Market size, Share & Forecast 2026-2033

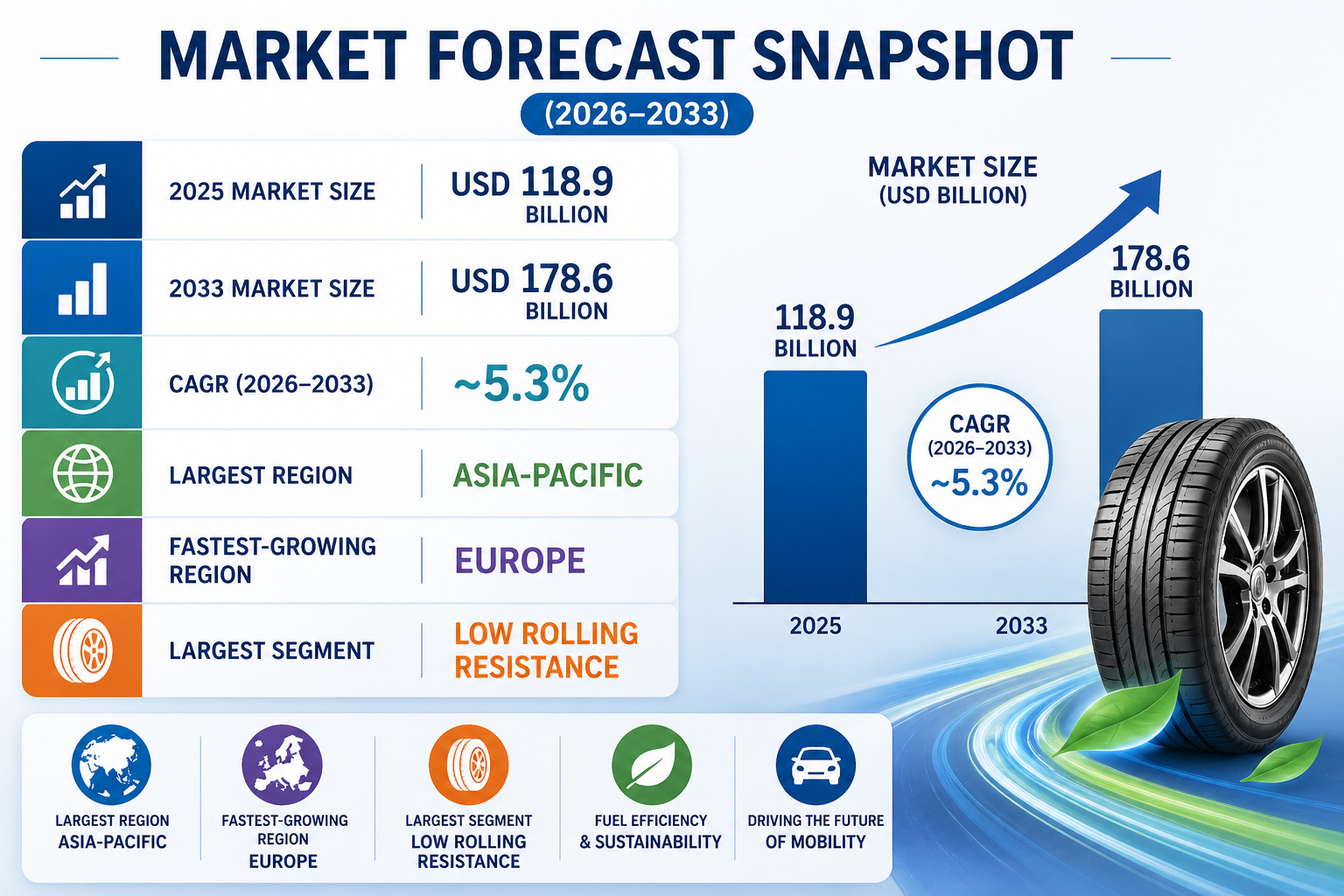

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| 2025 Market Size | USD 118.9 Billion |

| 2033 Market Size | USD 178.6 Billion |

| CAGR (2026???2033) | ~5.3% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Low rolling resistance tyres |

| Fastest-Growing Segment | EV-specific green tyres |

| Key Trend | Bio-based materials & circular tyres |

Global Sustainable & Green Tyres Market Overview

The Global Sustainable & Green Tyres Market is all about making tyres eco-friendly from start to finish . They use greener materials, low-emission factories, and design tyres that save energy while driving. Even at the end of life, these tyres are easier to recycle or dispose of safely. It???s a big step toward cutting pollution and waste in the tyre world.

These tyres typically incorporate bio-based and renewable materials, such as natural rubber, bio-silica, soybean oil, recycled carbon black, and sustainable fillers. In addition, green tyres are engineered with low rolling resistance compounds that help improve fuel efficiency in internal combustion engine (ICE) vehicles and extend driving range in electric vehicles (EVs). Noise reduction, longer tread life, and recyclability are also core design objectives.

The Global Sustainable & Green Tyres Market covers everything from cars, trucks, bikes, EVs, to heavy off-road gear, both for new vehicles and replacements . With governments, manufacturers, fleets, and drivers all pushing for greener options, these eco-friendly tyres are shifting from niche luxury to everyday standard. It???s like the whole tyre world going green, one ride at a time.

According to the Pheonix Demand Forecast Engine, the Global Sustainable & Green Tyres Market size is valued at USD 118.9 billion in 2025 and is projected to reach USD 178.6 billion by 2033, expanding at a CAGR of ~5.3% during 2026???2033.

Asia-Pacific is the largest market, driven by massive vehicle production and replacement demand, while Europe is the fastest-growing region, supported by stringent environmental regulations, EV penetration, and sustainability mandates.

Key Drivers of Global Sustainable & Green Tyres Market Growth

Stringent Environmental & Emission Regulations

Governments worldwide enforce fuel-efficiency and CO??? rules, pushing low rolling resistance tyres, driving market growth and making eco rides mainstream.

Rising Electric Vehicle Adoption

EVs benefit significantly from green tyres due to reduced rolling resistance, lower noise, and improved range, making sustainable tyres a preferred OEM choice.

OEM Sustainability Commitments

Automotive OEMs are committing to net-zero targets, pushing tyre suppliers to deliver low-carbon, recyclable, and bio-based tyre solutions.

Fuel Efficiency & Total Cost of Ownership (TCO) Benefits

Green tyres improve mileage, reduce fuel consumption, and last longer, offering long-term cost savings for consumers and fleets.

Growing Consumer Awareness

Eco-conscious buyers now choose certified, recyclable tyres, driving market growth and greener rides.

Advancements in Material Science

Innovations in bio-polymers, sustainable fillers, and recycled materials enable high-performance green tyres without compromising safety or durability.

Global Sustainable & Green Tyres Market Segmentation

1. By Tyre Type

1.1 Low Rolling Resistance Tyres??

Designed to minimize energy loss, improve fuel efficiency, and extend EV driving range.

1.1.1 Fuel-Efficient Compound Tyres

1.1.1.1 Silica-rich tread compounds

1.1.1.2 Optimized tread block geometry

1.1.1.3 Reduced hysteresis rubber formulations

1.1.2 EV-Optimized Low-Energy Tyres

1.1.2.1 High-load-bearing EV tyres

1.1.2.2 Noise-reduction focused tread design

1.1.2.3 Range-optimized green tyres

1.2 Bio-Based & Renewable Material Tyres

Focused on reducing dependence on fossil-derived materials.

1.2.1 Natural Rubber-Dominant Tyres

1.2.1.1 Sustainably harvested natural rubber

1.2.1.2 Certified plantation-sourced rubber

1.2.2 Bio-Oil & Plant-Based Compound Tyres

1.2.2.1 Soybean oil???based compounds

1.2.2.2 Plant-derived plasticizers

1.2.2.3 Reduced petroleum oil content

1.3 Recycled & Circular Economy Tyres

Aligned with circular economy and end-of-life recycling strategies.

1.3.1 Recycled Carbon Black Tyres

1.3.1.1 Pyrolysis-derived carbon black

1.3.1.2 Low-carbon footprint reinforcement

1.3.2 Tyres Using Reclaimed Rubber

1.3.2.1 Recovered rubber compounds

1.3.2.2 Partial recycled-content green tyres

1.4 Energy-Efficient & Long-Life Tyres

Engineered to maximize lifecycle efficiency.

1.4.1 Extended Tread-Life Tyres

1.4.1.1 Wear-resistant tread compounds

1.4.1.2 High-mileage commercial tyres

1.4.2 Wear-Optimized Green Tyres

1.4.2.1 Uniform wear technology

1.4.2.2 Reduced replacement frequency

2. By Vehicle Category

2.1 Passenger Vehicles (Largest Segment)

2.1.1 Hatchbacks

2.1.1.1 Entry-level compact vehicles

2.1.1.2 Urban mobility-focused green tyres

2.1.2 Sedans

2.1.2.1 Mid-size sedans

2.1.2.2 Premium and executive sedans

2.1.3 SUVs & Crossovers

2.1.3.1 Compact SUVs

2.1.3.2 Mid-size SUVs

2.1.3.3 Full-size SUVs

2.2 Commercial Vehicles

2.2.1 Light Commercial Vehicles (LCVs)

2.2.1.1 Delivery vans

2.2.1.2 Urban logistics vehicles

2.2.2 Medium-Duty Trucks

2.2.2.1 Regional freight vehicles

2.2.2.2 Distribution trucks

2.2.3 Heavy-Duty Trucks & Buses

2.2.3.1 Long-haul trucks

2.2.3.2 Intercity and city buses

2.3 Electric Vehicles (Fastest-Growing Segment)

2.3.1 Battery Electric Vehicles (BEVs)

2.3.1.1 Electric passenger cars

2.3.1.2 Electric SUVs

2.3.2 Plug-in Hybrid Electric Vehicles (PHEVs)

2.3.2.1 Passenger PHEVs

2.3.2.2 Fleet PHEVs

2.4 Two-Wheelers & Three-Wheelers

2.4.1 Motorcycles

2.4.1.1 Commuter motorcycles

2.4.2.2 Premium motorcycles

2.4.2 Scooters

2.4.2.1 ICE scooters

2.4.2.2 Electric scooters

2.4.3 Electric Two-Wheelers

2.4.3.1 Urban electric mobility tyres

2.4.3.2 Range-optimized two-wheeler tyres

2.5 Off-the-Road (OTR) Vehicles

2.5.1 Agricultural Machinery

2.5.1.1 Tractors

2.5.1.2 Harvesters

2.5.2 Construction Equipment

2.5.2.1 Loaders

2.5.2.2 Excavators

3. By Sales Channel

3.1 OEM (Original Equipment Manufacturer)

3.1.1 Passenger Vehicle OEM Fitment

3.1.1.1 ICE vehicle OEMs

3.1.1.2 Hybrid vehicle OEMs

3.1.2 EV OEM Fitment

3.1.2.1 Electric passenger vehicle OEMs

3.1.2.2 Electric commercial vehicle OEMs

3.1.3 Commercial Fleet OEM Contracts

3.1.3.1 Truck OEM agreements

3.1.3.2 Bus OEM supply contracts

3.2 Aftermarket / Replacement (Largest Segment)

3.2.1 Authorized Tyre Dealer Networks

3.2.1.1 Branded dealership chains

3.2.1.2 Manufacturer-authorized outlets

3.2.2 Independent Retailers

3.2.2.1 Multi-brand tyre shops

3.2.2.2 Local tyre distributors

3.2.3 Fleet Service Providers

3.2.3.1 Fleet maintenance contracts

3.2.3.2 Tyre management services

3.2.4 Online & E-Commerce Platforms

3.2.4.1 Direct-to-consumer tyre sales

3.2.4.2 Digital tyre marketplaces

4. By Material Type

4.1 Natural & Bio-Based Rubber

4.1.1 Sustainably Sourced Natural Rubber

4.1.1.1 FSC-certified rubber

4.1.1.2 Responsible plantation rubber

4.1.2 Bio-Synthetic Rubber Blends

4.1.2.1 Bio-polymer enhanced rubber

4.1.2.2 Reduced fossil-based elastomers

4.2 Sustainable Fillers & Reinforcements

4.2.1 Silica-Based Compounds

4.2.1.1 Wet-grip optimized silica

4.2.1.2 Low rolling resistance silica4.2.2 Bio-Silica from Rice Husk Ash

4.2.2.1 Agricultural waste-derived silica

4.2.2.2 Low-carbon reinforcement fillers

4.3 Recycled Materials

4.3.1 Recycled Carbon Black

4.3.1.1 Pyrolysis-based carbon black

4.3.1.2 Circular material recovery systems

4.3.2 Reclaimed Rubber Content

4.3.2.1 End-of-life tyre rubber reuse

4.3.2.2 Partial recycled compound tyres

4.4 Low-Impact Chemicals & Oils

4.4.1 Soybean & Plant-Based Oils

4.4.1.1 Renewable plasticizers

4.4.1.2 Low-PAH oils

4.4.2 Low-Aromatic Process Oils

4.4.2.1 Reduced toxic emissions

4.4.2.2 Compliance with global regulations

5. By Geography

5.1 Asia-Pacific (Largest Region)

-

China

-

India

-

Japan

-

Southeast Asia

5.2 Europe (Fastest-Growing Region)

-

Germany

-

France

-

U.K.

-

Italy

5.3 North America

-

U.S.

-

Canada

5.4 Latin America

-

Brazil

-

Mexico

5.5 Middle East & Africa

Regional Insights of Global Sustainable & Green Tyres Market

Asia-Pacific ??? Largest Market

High vehicle production volumes, strong replacement demand, and growing adoption of fuel-efficient tyres in China and India support market dominance.

Europe ??? Fastest-Growing Region

Strict CO??? regulations, EU tyre labeling rules, EV adoption, and sustainability-focused consumers drive rapid growth of green tyres.

North America

Rising EV sales, fleet fuel-efficiency targets, and OEM sustainability initiatives support steady market expansion.

Latin America

Gradual adoption driven by fuel cost sensitivity and improving regulatory frameworks.

Middle East & Africa

Green tyre adoption remains nascent but is increasing in premium passenger vehicles and commercial fleets.

Leading Companies in the Global Sustainable & Green Tyres Market

-

Goodyear Tire & Rubber Company

-

Pirelli & C. S.p.A.

-

Hankook Tire

-

Yokohama Rubber Company

-

Sumitomo Rubber Industries

-

Apollo Tyres

-

Nokian Tyres

Michelin is the largest company in the Global Sustainable & Green Tyres Market

Why the Sustainable & Green Tyres Market Is Critical

-

Direct impact on fuel efficiency and EV range

-

Major contributor to automotive carbon reduction

-

Enables circular economy and recycling initiatives

-

Aligns tyre manufacturers with OEM ESG goals

-

Balances performance, cost savings, and environmental responsibility

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Analyzes vehicle parc growth, EV penetration, and fuel-efficiency regulations.

Sustainability Penetration Model

Tracks adoption of green tyres across regions and vehicle categories.

Raw Material Sustainability Index

Monitors availability, cost, and carbon footprint of bio-based and recycled inputs.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate ??? OEMs and fleets influence pricing

-

Supplier Power: Moderate ??? sustainable material sourcing constraints

-

Threat of New Entrants: Low ??? R&D and certification barriers

-

Threat of Substitutes: Low ??? performance must meet safety standards

-

Competitive Rivalry: High ??? global majors competing on sustainability credentials

Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| 2025 Market Size | USD 118.9 Billion |

| 2033 Market Size | USD 178.6 Billion |

| CAGR (2026???2033) | ~5.3% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Low rolling resistance tyres |

| Fastest-Growing Segment | EV-specific green tyres |

| Key Trend | Bio-based materials & circular tyres |

Final Takeaway

The Global Sustainable & Green Tyres Market is transitioning from an eco-friendly alternative to a core pillar of the global tyre industry. As regulations tighten and EV adoption accelerates, sustainable tyres will become the default choice rather than a premium option. Manufacturers that invest in bio-based materials, circular production models, and energy-efficient tyre designs will be best positioned to lead the market through 2033.

Competitive Landscape

Global Sustainable & Green Tyres Competitive Intensity & Market Structure Overview

The Global Sustainable & Green Tyres Market is characterized by a sustainability-led, innovation-intensive competitive landscape, where tyre manufacturers compete not only on durability, safety, and cost, but increasingly on environmental performance, carbon footprint reduction, circularity, and material innovation. Competitive differentiation is rapidly shifting toward low rolling resistance technologies, bio-based raw materials, recycled inputs, and lifecycle sustainability. The market structure is evolving from traditional tyre manufacturing toward ESG-integrated mobility solutions, with OEMs, regulatory bodies, fleet operators, and environmentally conscious consumers all influencing product development. OEM fitment remains a critical competitive gateway due to automaker sustainability targets and fuel-efficiency requirements, while the aftermarket represents a major volume opportunity as green tyres increasingly transition from premium alternatives to mainstream replacements. Market concentration remains relatively high, with major global tyre manufacturers leveraging R&D capabilities, sustainable sourcing networks, and manufacturing scale to dominate. However, competition is intensifying as regional manufacturers, material innovators, and circular economy specialists increasingly enter the value chain through bio-materials, recycled compounds, and green production technologies.

Global Sustainable & Green Tyres Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global sustainability leader with strong focus on bio-based materials, circular tyre development, and low rolling resistance innovation. Bridgestone Corporation: Major green mobility player emphasizing sustainable materials, carbon reduction, and premium EV-compatible tyre solutions. Goodyear Tire & Rubber Company: Innovation-focused manufacturer investing in soybean oil compounds, sustainable feedstocks, and fuel-efficient tyre platforms. Continental AG: Advanced sustainability-driven company integrating recyclable materials, low-emission manufacturing, and premium green tyre technologies. Pirelli & C. S.p.A.: Premium performance player emphasizing FSC-certified natural rubber, EV-focused green tyres, and sustainability branding. Hankook Tire: Growing global competitor with increasing investment in eco-materials and EV sustainability solutions. Yokohama Rubber Company: Focused on environmental tyre development with energy efficiency and sustainable material integration. Nokian Tyres: Strong sustainability-centric player recognized for low rolling resistance and environmentally optimized tyre innovation.

Key Competitive Intensity & Market Structure Signals in Global Sustainable & Green Tyres Market

A major structural signal is the increasing importance of sustainability compliance as a core competitive variable. Environmental regulations, tyre labeling systems, and carbon reduction mandates are making sustainability performance a strategic necessity rather than optional branding. Another critical signal is the growing shift toward bio-based and circular raw material ecosystems. Competition increasingly extends upstream into sustainable rubber sourcing, recycled carbon black, plant-based oils, and circular production systems, creating new supply chain advantages for companies with early access to scalable sustainable inputs. Electric vehicle adoption is also accelerating competitive intensity, as EVs require tyres that combine sustainability with low rolling resistance, high durability, and noise reduction. This is driving a convergence between green tyre innovation and EV-specific product development. Brand positioning is becoming increasingly important, with sustainability certifications, carbon-neutral initiatives, and lifecycle transparency influencing both OEM procurement and consumer purchasing behavior.

Strategic Implications of Competitive Intensity & Market Structure in Global Sustainable & Green Tyres Market

Manufacturers must increasingly integrate sustainability into every stage of the value chain’from material sourcing and manufacturing to product design and end-of-life recovery. Competitive advantage will depend on balancing environmental responsibility with cost competitiveness and performance. OEM partnerships remain strategically critical, particularly as automakers pursue net-zero targets and require tyre suppliers to align with broader ESG and emissions goals. Investment in advanced material science is essential, especially in bio-polymers, sustainable fillers, recycled compounds, and low-impact chemical processing, as these technologies are becoming core drivers of product differentiation. Circular economy models such as tyre recycling, retreading, reclaimed rubber integration, and carbon recovery are expected to become major long-term strategic pillars, particularly in regions with strict environmental regulation.

Global Sustainable & Green Tyres Competitive Intensity & Market Structure Forward Outlook

The Global Sustainable & Green Tyres Market is expected to experience sustained competitive acceleration as sustainability becomes central to both mobility and industrial manufacturing strategy. Competitive intensity will remain high as global tyre leaders race to secure environmental leadership while balancing regulatory compliance and profitability. Market consolidation is likely to strengthen among Tier 1 manufacturers, particularly through sustainable raw material partnerships, recycling ecosystem expansion, and ESG-driven innovation investments. The aftermarket will increasingly transform into a high-volume green replacement ecosystem, supported by consumer awareness, fleet TCO benefits, and fuel-efficiency economics. Over the long term, the market will be defined by three major competitive pillars: sustainable material leadership, circular economy integration, and EV-compatible green performance. Manufacturers that successfully align environmental innovation with scalable production and OEM sustainability mandates will lead the Global Sustainable & Green Tyres Market through 2033.

Value Chain

Global Sustainable & Green Tyres Market Value Chain & Supply Chain Evolution Overview

The Global Sustainable & Green Tyres Market value chain is rapidly transforming from traditional fossil-fuel-dependent tyre production into a sustainability-first, circular, and ESG-integrated ecosystem. This evolution is driven by rising adoption of bio-based materials, renewable feedstocks, recycled raw materials, low-emission manufacturing technologies, and end-of-life circularity systems. Sustainable and green tyres are no longer positioned solely as eco-friendly alternatives’they are increasingly strategic assets for fuel efficiency, EV optimization, regulatory compliance, and long-term carbon reduction. Green tyres increasingly utilize renewable and environmentally optimized inputs such as FSC-certified natural rubber, soybean oil, rice husk ash-derived bio-silica, recycled carbon black, reclaimed rubber, and low-impact processing oils. As a result, the value chain now extends beyond conventional tyre manufacturing to include sustainable agriculture, advanced material science, recycling ecosystems, carbon transparency, and lifecycle emissions management. The upstream supply chain depends on sustainable raw material sourcing, renewable chemical innovation, recycled feedstock processing, and supplier traceability. Major tyre manufacturers such as Michelin, Bridgestone, Continental, Goodyear, and Pirelli are strengthening supply networks around certified natural rubber, circular materials procurement, renewable chemistry partnerships, and ESG-compliant sourcing strategies. Manufacturing is evolving toward energy-efficient production, renewable-powered facilities, lower emissions, advanced compounding technologies, and product designs that optimize rolling resistance, tread life, acoustic performance, and recyclability. Sustainable tyre factories are increasingly integrating renewable energy, waste minimization systems, and circular material loops to align with net-zero objectives. Distribution spans OEM and aftermarket channels, with the aftermarket remaining dominant due to global replacement cycles, while OEM demand is accelerating as automakers increasingly integrate sustainable tyres into ICE, hybrid, and EV platforms to support broader decarbonization commitments. Key supply chain challenges include sustainable material cost premiums, limited renewable feedstock scalability, recycling infrastructure gaps, supplier traceability complexity, and balancing sustainability innovation with cost competitiveness, safety, and durability standards.

Global Sustainable & Green Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The current sustainable tyre ecosystem is shaped by environmental regulations, EV adoption, OEM ESG commitments, fuel-efficiency mandates, and growing consumer preference for sustainable mobility products. Upstream suppliers are increasingly focused on renewable feedstocks, sustainable rubber cultivation, pyrolysis-based recycled carbon black, and bio-synthetic compounds to reduce fossil dependency and carbon intensity. Manufacturing strategies are shifting toward low-carbon facilities, renewable energy integration, sustainable chemistry, advanced rolling resistance optimization, and circular production models. OEM integration is accelerating as vehicle manufacturers prioritize sustainable tyre fitments that improve fuel economy, extend EV range, and align with lifecycle carbon targets. The aftermarket remains the largest revenue channel, supported by replacement demand for long-life, low-rolling-resistance, and fuel-saving tyres among consumers and commercial fleets. Lifecycle traceability, ESG certifications, and digital sustainability disclosures are becoming increasingly important as procurement standards evolve across OEM and consumer channels.

Key Value Chain & Supply Chain Evolution Signals in Global Sustainable & Green Tyres Market

Several transformative forces are reshaping the sustainable tyre value chain. First, bio-based materials and renewable compounds are increasingly replacing petroleum-derived tyre chemistry, expanding the strategic importance of sustainable sourcing ecosystems. Second, circular economy integration is accelerating through tyre recycling, reclaimed rubber, recycled carbon black, and material recirculation systems. Third, EV growth is intensifying demand for tyres that combine sustainability with low rolling resistance, noise reduction, and range optimization. Fourth, ESG mandates and carbon regulations are transforming sustainability from optional differentiation into a strategic operational necessity. Fifth, lifecycle carbon transparency and traceable sourcing are becoming increasingly influential in OEM partnerships, investor confidence, and brand competitiveness.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Sustainable & Green Tyres Market

Industry leaders including Michelin, Bridgestone, Continental, Goodyear, and Pirelli are increasingly differentiating through sustainable sourcing, advanced bio-material science, and circular manufacturing capabilities. Competitive resilience increasingly depends on access to renewable materials, recycling ecosystems, supplier transparency, and ESG-certified sourcing frameworks. Manufacturers with advanced R&D capabilities in sustainable compounds, low rolling resistance engineering, and circular design are better positioned to capture premium OEM contracts and regulatory-driven growth. Long-term success will increasingly rely on lifecycle sustainability metrics, emissions reductions, material circularity, and digital traceability systems. Affordability remains a critical strategic challenge, requiring companies to scale green innovation while maintaining mainstream pricing accessibility.

Global Sustainable & Green Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the sustainable tyre value chain is expected to become increasingly renewable, circular, low-carbon, and digitally traceable. Tyre manufacturers will increasingly prioritize fully recyclable tyre structures, renewable raw materials, advanced bio-polymers, low-carbon factories, and circular lifecycle management. OEM partnerships will deepen as automakers integrate sustainable tyres into EV, hybrid, and carbon-neutral mobility strategies. The aftermarket will remain a major growth engine, supported by consumer demand for energy savings, lower operating costs, and environmentally responsible products. Recycling infrastructure, reclaimed material ecosystems, blockchain-enabled traceability, and sustainable procurement technologies will become central competitive differentiators. Ultimately, the market’s future value chain will evolve from product-centric tyre manufacturing into lifecycle-managed, sustainability-led mobility ecosystems.

Market-Specific Value Chain

- Sustainable Raw Material Procurement: FSC-certified natural rubber, bio-silica, soybean oil, recycled carbon black, reclaimed rubber, renewable fillers, sustainable oils

- Research & Development: Low rolling resistance technologies, EV-specific green tyres, bio-based compounds, sustainable chemistry, circular tyre design

- Manufacturing: Low-emission factories, renewable energy integration, sustainable compounding, energy-efficient production, waste minimization systems

- OEM Integration: ICE vehicles, EVs, hybrid vehicles, commercial fleets, OEM sustainability partnerships

- Distribution & Retail: OEM channels, aftermarket replacement, authorized dealers, e-commerce, fleet service providers

- End-of-Life & Circular Economy Services: Tyre recycling, pyrolysis systems, reclaimed rubber recovery, circular material reintegration, sustainable disposal

Company-to-Stage Mapping

- Sustainable Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Pirelli & C. S.p.A.

- Distribution & Retail: Apollo Tyres, Nokian Tyres, Goodyear Tire & Rubber Company, Yokohama Rubber Company

- End-of-Life & Circular Economy Services: Michelin, Bridgestone Corporation, Continental AG, recycling ecosystem partners

Investment Activity

Global Sustainable & Green Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Sustainable & Green Tyres Market are being driven by accelerating sustainability mandates, stricter fuel-efficiency regulations, growing EV adoption, and increasing pressure on automotive supply chains to reduce carbon intensity. Between 2026 and 2033, capital allocation is expected to increasingly prioritize bio-based materials, low rolling resistance technologies, circular tyre production systems, recycled raw material ecosystems, and EV-specific green tyre innovation. The market is highly material science and sustainability intensive, requiring continuous investment in renewable rubber sources, bio-silica compounds, recycled carbon black, soybean oil formulations, advanced tread optimization, and low-emission manufacturing systems. Leading tyre manufacturers such as Michelin, Bridgestone, Goodyear, Continental, Pirelli, and Hankook are significantly expanding sustainability-focused R&D budgets while scaling green production capacity and circular economy initiatives. A major structural transformation influencing investment flows is the shift from conventional petroleum-heavy tyre manufacturing toward low-carbon, recyclable, and resource-efficient tyre ecosystems. This transition is directing funding into sustainable material sourcing, carbon footprint reduction, lifecycle optimization, and closed-loop recycling infrastructure.

Global Sustainable & Green Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by tightening environmental regulations, OEM decarbonization strategies, fuel-efficiency mandates, and rising global EV production. Partnerships between tyre manufacturers, material science innovators, recycling technology providers, and automotive OEMs are becoming central to long-term sustainability positioning.

- Asia-Pacific: Leads global investment activity due to high-volume vehicle production, extensive tyre manufacturing infrastructure, and expanding demand for cost-efficient fuel-saving tyres.

- Europe: Fastest-growing investment region, driven by aggressive CO reduction policies, EU sustainability regulations, premium EV adoption, and circular economy leadership.

- North America: Strong investment momentum supported by EV expansion, fleet fuel-efficiency goals, and rising ESG commitments across OEM ecosystems.

- Latin America & Middle East & Africa: Emerging investment markets supported by fuel-cost sensitivity, gradual regulatory modernization, and increasing sustainable mobility awareness.

Key Investment & Funding Dynamics Signals in Global Sustainable & Green Tyres Market

- Rising demand for low rolling resistance tyres is increasing capital inflows into energy-efficient compound development and advanced tread engineering.

- Growing EV production is accelerating funding into green tyres optimized for range extension, heavier battery loads, and lower cabin noise.

- Bio-based material innovation is attracting strategic investment in renewable feedstocks such as natural rubber, plant oils, rice husk silica, and sustainable fillers.

- Circular economy expansion is driving investment in tyre recycling technologies, reclaimed rubber systems, pyrolysis infrastructure, and recycled carbon black platforms.

- OEM net-zero commitments are reshaping supplier investment priorities toward low-carbon production, lifecycle sustainability, and ESG-aligned innovation.

Strategic Implications of Investment & Funding Dynamics in Global Sustainable & Green Tyres Market

- The investment landscape strongly favors established tyre manufacturers with robust sustainability roadmaps, advanced material science capabilities, and scalable global supply chains.

- Strategic partnerships with renewable material suppliers, recycling firms, agricultural feedstock ecosystems, and EV OEMs are becoming critical competitive differentiators.

- Innovation leadership is increasingly centered around balancing sustainability with performance, ensuring green tyres deliver fuel savings, durability, and safety without compromise.

- Regional diversification remains essential, with Asia-Pacific leading manufacturing scale, Europe leading sustainability innovation, and North America emphasizing ESG-driven premium demand.

- Raw material volatility, sustainable feedstock availability, and certification compliance remain strategic funding priorities.

Global Sustainable & Green Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Sustainable & Green Tyres Market is expected to attract strong and sustained investment as green tyres evolve from regulatory compliance products into mainstream automotive standards. Future capital allocation will increasingly prioritize next-generation bio-based compounds, carbon-neutral tyre production, EV-specific sustainable tyres, closed-loop recycling systems, and AI-supported lifecycle sustainability optimization.

- Asia-Pacific: Will remain the dominant investment hub through large-scale production, cost competitiveness, and rising green mobility demand.

- Europe: Will continue leading innovation in premium sustainable tyre technologies, circular production, and regulatory-driven material transformation.

- North America: Will expand investments in sustainable premium tyres, fleet efficiency, and EV-compatible green mobility solutions.

Digital sustainability measurement tools, lifecycle carbon accounting, and traceable sourcing technologies will increasingly shape future funding strategies across the value chain. Overall, the market will maintain stable long-term growth through 2033, supported by the strategic role of sustainable tyres in fuel efficiency, EV optimization, and automotive decarbonization. Companies that align sustainability, material innovation, circularity, and OEM partnerships will be best positioned to lead the next generation of tyre industry transformation.

Technology & Innovation

Global Sustainable & Green Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Sustainable & Green Tyres Market is being fundamentally reshaped by environmental sustainability, material science advancements, circular economy integration, and energy-efficiency optimization. Unlike conventional tyre innovation, which primarily focused on durability, grip, and performance, sustainable tyre development emphasizes carbon footprint reduction across the full tyre lifecycle’from raw material sourcing and manufacturing to operational efficiency and end-of-life recyclability. Innovation intensity in this market is rapidly accelerating as tyre manufacturers respond to stricter emissions regulations, rising EV adoption, OEM ESG commitments, and consumer demand for eco-conscious mobility solutions. Leading players such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are heavily investing in bio-based compounds, renewable feedstocks, recycled material integration, low rolling resistance engineering, and closed-loop manufacturing ecosystems. A major technological shift is underway from petroleum-heavy tyre construction toward sustainable materials such as natural rubber from certified plantations, soybean oil, rice husk silica, bio-synthetic elastomers, recycled carbon black, and reclaimed rubber. At the same time, green tyres are increasingly engineered for lower rolling resistance, longer tread life, and enhanced EV efficiency’allowing both ICE vehicles and EVs to reduce energy consumption while improving lifecycle economics. Circular innovation is emerging as a major frontier, with tyre companies investing in pyrolysis, material recovery, retreading technologies, and advanced recycling systems that transform end-of-life tyres into reusable production inputs. This positions sustainable tyres not only as fuel-saving products but also as strategic assets in the broader decarbonization of global mobility.

Global Sustainable & Green Tyres Market Technology & Innovation Landscape Current Scenario

Currently, sustainable tyre innovation is centered on balancing environmental responsibility with commercial-grade performance. Low rolling resistance technologies dominate the market, as they directly improve fuel economy, lower CO emissions, and extend EV battery range. Silica-rich tread compounds, advanced polymer chemistry, lightweight carcass engineering, and optimized tread geometry are widely deployed to minimize energy loss while preserving wet grip, braking safety, and durability. Bio-based material adoption is expanding significantly. Soybean oil, plant-derived plasticizers, FSC-certified natural rubber, and bio-silica derived from agricultural waste are increasingly replacing traditional fossil-based inputs, helping reduce environmental impact without compromising tyre quality. Recycled and circular material integration is also gaining momentum. Manufacturers are scaling the use of recycled carbon black, reclaimed rubber compounds, and pyrolysis-derived materials to lower raw material dependency and support circular production models. EV-specific green tyre innovation is accelerating rapidly. These tyres combine low rolling resistance, acoustic dampening, high-load tolerance, and wear-resistant compounds to meet EV-specific needs while aligning with sustainability objectives. Manufacturing innovation is equally important, with AI-powered process optimization, renewable energy-powered production facilities, water conservation systems, and carbon-neutral factory initiatives becoming increasingly common across leading tyre manufacturers.

Key Technology & Innovation Landscape Signals in Global Sustainable & Green Tyres Market

- Low Rolling Resistance Engineering: Core technology for fuel efficiency, lower emissions, and EV range extension.

- Bio-Based Material Integration: Soybean oil, bio-silica, FSC-certified rubber, and plant-based polymers replacing fossil-derived inputs.

- Recycled Carbon Black & Reclaimed Rubber: Circular economy technologies reducing virgin raw material dependency.

- EV-Specific Green Tyres: High-load, low-noise, and energy-efficient tyre designs tailored for electric mobility.

- Pyrolysis & Circular Manufacturing: End-of-life tyre recycling technologies creating reusable feedstocks.

- AI-Driven Sustainable Manufacturing: Smart production systems reducing waste, emissions, and energy intensity.

- Extended Tread Life Innovation: Longer lifecycle tyres reducing replacement frequency and environmental burden.

Strategic Implications of Technology & Innovation Landscape in Global Sustainable & Green Tyres Market

The sustainable tyre innovation landscape carries major strategic implications for tyre manufacturers, automotive OEMs, regulators, and fleet operators. Continuous investment in sustainable material science is becoming essential not only for regulatory compliance but also for long-term competitive positioning. OEM partnerships are increasingly strategic, as automakers seek tyre suppliers that align with vehicle decarbonization strategies, EV performance goals, and ESG mandates. Sustainable tyres are becoming a critical component of broader vehicle sustainability architecture. Circular manufacturing capabilities may become a major source of competitive advantage. Companies that build scalable recycling, retreading, and material recovery ecosystems can improve cost resilience, reduce supply chain volatility, and strengthen sustainability credentials. Material innovation also directly impacts profitability. Access to scalable bio-based and recycled materials will influence cost structures, supply security, and compliance with future environmental regulations. For fleet operators and consumers, green tyres increasingly offer a dual value proposition’lower operating costs through fuel savings and reduced environmental impact’making sustainability economically compelling rather than purely ethical.

Global Sustainable & Green Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the Global Sustainable & Green Tyres Market is expected to evolve toward ultra-sustainable, circular, and digitally optimized tyre ecosystems. Bio-based materials are likely to move from partial adoption to mainstream production standards, significantly reducing petroleum dependence. Circular tyre systems will expand beyond recycling into full lifecycle ecosystems that include retreading, reusable feedstocks, and closed-loop supply chains, transforming tyre manufacturing economics. EV adoption will further accelerate sustainable tyre innovation, particularly in low-energy compounds, wear optimization, acoustic engineering, and carbon-neutral production. AI, advanced analytics, and digital twins will increasingly optimize tyre design, lifecycle performance, and sustainable manufacturing efficiency, shortening innovation cycles while reducing environmental burden. In conclusion, the Global Sustainable & Green Tyres Market is undergoing a structural technological transformation where sustainability, material innovation, circularity, and energy efficiency define competitive leadership. Companies that successfully integrate bio-based materials, advanced recycling systems, EV-optimized green engineering, and low-carbon manufacturing will lead the sustainable tyre ecosystem through 2033.

Market Risk

Global Sustainable & Green Tyres Market Risk Factors & Disruption Threats Overview

The Global Sustainable & Green Tyres Market operates at the intersection of environmental innovation, regulatory transformation, and automotive performance evolution. While the market benefits from rising global demand for fuel-efficient, low-emission, and circular mobility solutions, it carries a moderate to high strategic risk profile due to material innovation costs, sustainability compliance pressures, and supply chain restructuring. A major structural risk is the complexity and cost volatility associated with sustainable raw material sourcing. Bio-based rubber, recycled carbon black, bio-silica, soybean oil, and renewable fillers often face supply limitations, certification challenges, and price premiums versus conventional petroleum-derived materials. Another key disruption factor is regulatory acceleration. Global environmental mandates, carbon taxation, and ESG disclosure frameworks are forcing tyre manufacturers to rapidly redesign products and production processes. Companies unable to meet low-carbon manufacturing and circularity expectations risk losing OEM contracts and market relevance. Performance parity remains a persistent challenge. Sustainable tyres must balance rolling resistance, durability, wet grip, and lifecycle economics without sacrificing safety. Any perception of lower performance versus conventional tyres can slow adoption, particularly in fleet and commercial segments. The rapid rise of EVs is further reshaping the competitive environment. EV-specific green tyres require low rolling resistance, higher load-bearing capacity, quiet operation, and sustainable materials simultaneously, increasing R&D intensity and shortening innovation cycles.

Global Sustainable & Green Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong momentum, driven by EV growth, fuel-efficiency regulations, consumer sustainability awareness, and OEM decarbonization goals. However, this expansion is accompanied by rising operational complexity and technology investment requirements. Raw material diversification is a central strategic issue. Manufacturers are increasingly dependent on alternative feedstocks such as FSC-certified rubber, rice husk silica, and recycled compounds, but scalability remains inconsistent across regions. OEM sustainability procurement is intensifying, with automotive manufacturers increasingly prioritizing tyre suppliers that can align with net-zero and circular economy objectives. Supply chain pressures, particularly around sustainable inputs and recycling infrastructure, create risks related to production continuity and margin stability. Meanwhile, consumer demand for green tyres is growing, but purchasing decisions remain sensitive to pricing, performance, and replacement economics, particularly in price-sensitive emerging markets.

Key Risk Factors & Disruption Threats Signals in Global Sustainable & Green Tyres Market

A major disruption signal is the accelerating shift toward circular tyre ecosystems, including recycled materials, retreading innovation, and end-of-life tyre reuse systems. This may significantly alter traditional production and replacement models. Rapid EV expansion is another major signal, increasing demand for tyres that combine sustainability with energy optimization, noise suppression, and battery-weight compatibility. Regulatory tightening in Europe and parts of Asia is creating pressure for standardized environmental disclosures, lifecycle emissions transparency, and sustainable material traceability. OEM-led sustainability mandates are increasing supplier qualification complexity, favoring manufacturers with vertically integrated green material capabilities. Additionally, advances in material science’such as bio-polymers, recycled elastomers, and low-carbon fillers’are rapidly redefining competitive differentiation.

Strategic Implications of Risk Factors & Disruption Threats in Global Sustainable & Green Tyres Market

Manufacturers must prioritize sustainable material innovation while maintaining safety, tread life, and fuel-efficiency standards to ensure mainstream market acceptance. Building resilient sustainable supply chains will be critical, particularly through partnerships in renewable feedstocks, recycling ecosystems, and certified sourcing networks. EV-focused green tyre development should remain a strategic priority, as electrification increasingly defines future tyre demand. Investment in circular manufacturing systems, including recycled material integration and retreadable designs, can create long-term competitive advantages while aligning with ESG mandates. Brand credibility and sustainability transparency will become increasingly important, as both OEMs and consumers demand verifiable environmental performance.

Global Sustainable & Green Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Sustainable & Green Tyres Market is expected to maintain steady structural expansion, supported by decarbonization, EV penetration, and circular economy adoption. However, the market’s disruption profile will increasingly center on material access, technological innovation, and compliance sophistication. Bio-based and recycled materials are likely to move from differentiation to industry expectation, reshaping procurement strategies across the tyre value chain. EV-specific sustainable tyres will emerge as one of the most strategically important growth segments, particularly in Europe and Asia-Pacific. Circular economy frameworks, including tyre recycling, retreading, and low-carbon production, will become increasingly central to competitive positioning. Overall, the market will remain highly attractive but strategically demanding, with long-term success dependent on manufacturers’ ability to integrate sustainability, performance, and cost competitiveness into scalable global tyre platforms.

Regulatory Landscape

Global Sustainable & Green Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Sustainable & Green Tyres Market is a powerful structural catalyst accelerating the transition from conventional tyre manufacturing toward environmentally responsible, low-emission, and circular tyre ecosystems. Governments, environmental agencies, automotive regulators, and sustainability frameworks worldwide are increasingly emphasizing fuel efficiency, carbon reduction, sustainable material sourcing, recycling, and lifecycle emissions accountability’positioning green tyres as a critical component of future mobility policy. Global regulatory frameworks such as the European Union Tyre Labelling Regulation (EU 2020/740), UNECE tyre performance standards, carbon reduction mandates, Extended Producer Responsibility (EPR) frameworks, and EV efficiency regulations are significantly reshaping tyre manufacturing priorities. These regulations increasingly encourage or require low rolling resistance, lower external noise, sustainable materials, and improved recyclability’core pillars of sustainable and green tyre development. Green tyres inherently align with these regulatory priorities because they improve fuel efficiency, reduce CO emissions, support EV range optimization, and increasingly incorporate renewable or recycled inputs such as natural rubber, bio-silica, soybean oil, recycled carbon black, and reclaimed rubber. As a result, sustainable tyres are evolving from optional eco-products into strategic compliance-driven necessities. Emerging markets including China, India, Brazil, and Southeast Asia are also strengthening fuel economy regulations, tyre labeling systems, sustainability policies, and waste management frameworks. These developments are encouraging broader adoption of sustainable tyre technologies across passenger vehicles, commercial fleets, two-wheelers, and EVs.

Global Sustainable & Green Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by the convergence of environmental sustainability mandates, fuel economy standards, emissions regulations, and circular economy initiatives. Europe remains the global leader in regulatory maturity due to stringent CO targets, advanced tyre labeling systems, ESG frameworks, and aggressive EV transition policies. In Europe, regulations governing rolling resistance, wet grip, external noise, and sustainable manufacturing transparency are strongly influencing both OEM tyre fitment and aftermarket purchasing behavior. Sustainability regulations are also increasingly expanding into tyre lifecycle assessments and recycled content expectations. Asia-Pacific currently leads global production volume but is rapidly evolving from a manufacturing-focused market into a regulation-driven sustainability growth engine. China’s dual-carbon goals, India’s fuel efficiency regulations, and Japan’s advanced automotive sustainability standards are strengthening policy support for green tyre adoption. North America maintains a robust policy environment centered on fuel efficiency standards, EPA emissions requirements, EV policy expansion, and OEM sustainability commitments. While regulation is less centralized than Europe, corporate ESG initiatives and EV adoption are significantly supporting green tyre penetration. The rise of electric mobility globally is further accelerating sustainable tyre policy relevance, as EV-specific regulations increasingly prioritize low rolling resistance, durability, sustainable materials, and acoustic performance.

Key Regulatory & Policy Environment Signals in Global Sustainable & Green Tyres Market

- EU Tyre Labelling Regulation (EU 2020/740): Drives transparency in rolling resistance, wet grip, and noise’favoring green tyre technologies.

- UNECE Tyre Standards: Reinforce performance, efficiency, and sustainability compliance.

- Fuel Economy & CO Emission Regulations: Push demand for low rolling resistance and energy-efficient tyres.

- EV Policy Expansion: Supports range optimization, low-noise tyres, and sustainable material integration.

- Circular Economy & EPR Policies: Encourage tyre recycling, recycled material usage, and end-of-life tyre management.

- Sustainable Material Certification Standards: Promote responsibly sourced natural rubber and bio-based materials.

- Waste Reduction Regulations: Increase demand for recyclable, retreadable, and lower-impact tyre systems.

Strategic Implications of Regulatory & Policy Environment in Global Sustainable & Green Tyres Market

The regulatory landscape is transforming sustainability from a branding advantage into a baseline operational and competitive requirement. Tyre manufacturers are increasingly required to align product development, material sourcing, manufacturing processes, and recycling systems with tightening global environmental standards. Manufacturers heavily dependent on fossil-derived inputs, carbon-intensive production, or weak recycling capabilities may face structural disadvantages as policy increasingly rewards sustainability leadership. This is accelerating investments in bio-material science, renewable compounds, carbon-neutral factories, and circular supply chains. Compliance-led innovation is becoming a core strategic differentiator. Companies investing in low rolling resistance compounds, EV-specific green tyres, bio-based elastomers, sustainable fillers, and recycled carbon black are better positioned to secure OEM partnerships and regulatory advantages. Fleet operators and OEMs are increasingly prioritizing certified sustainable tyres to meet ESG targets, fuel-efficiency standards, and operational cost reduction goals. Procurement decisions are increasingly shaped by lifecycle performance, sustainability certifications, and compliance metrics. Regional regulatory variation is also influencing supply chain localization, certification pathways, and material sourcing strategies, requiring manufacturers to adapt product portfolios based on local sustainability frameworks.

Global Sustainable & Green Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become substantially more stringent, with sustainability moving beyond performance standards toward full lifecycle accountability. Governments are likely to increasingly regulate tyre production emissions, material sourcing transparency, recyclability, and end-of-life management. Europe is expected to remain the global leader through stricter carbon accounting, circular economy expansion, and sustainability transparency requirements. Asia-Pacific is projected to become the largest long-term regulatory growth engine due to rising motorization combined with tightening environmental enforcement. North America is expected to increasingly strengthen policy through EV adoption, corporate ESG standards, and advanced fuel-efficiency frameworks. Future regulatory frameworks are likely to expand toward mandatory recycled content thresholds, sustainable sourcing verification, lifecycle carbon labeling, and circular production benchmarks. These shifts will create major opportunities for manufacturers capable of integrating sustainability at scale. Advanced technologies such as bio-synthetic rubber, carbon-neutral manufacturing, circular tyre ecosystems, advanced retreading, and AI-enabled lifecycle optimization are expected to gain stronger regulatory alignment. Overall, the regulatory and policy environment will be a decisive force shaping the future of the Global Sustainable & Green Tyres Market. Manufacturers that proactively align with evolving environmental mandates, circular economy frameworks, fuel-efficiency standards, and sustainable material innovation while building scalable green production systems will be best positioned to lead this increasingly regulation-driven market through 2033.