Global Connected & Intelligent Tyres Market size, share & forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

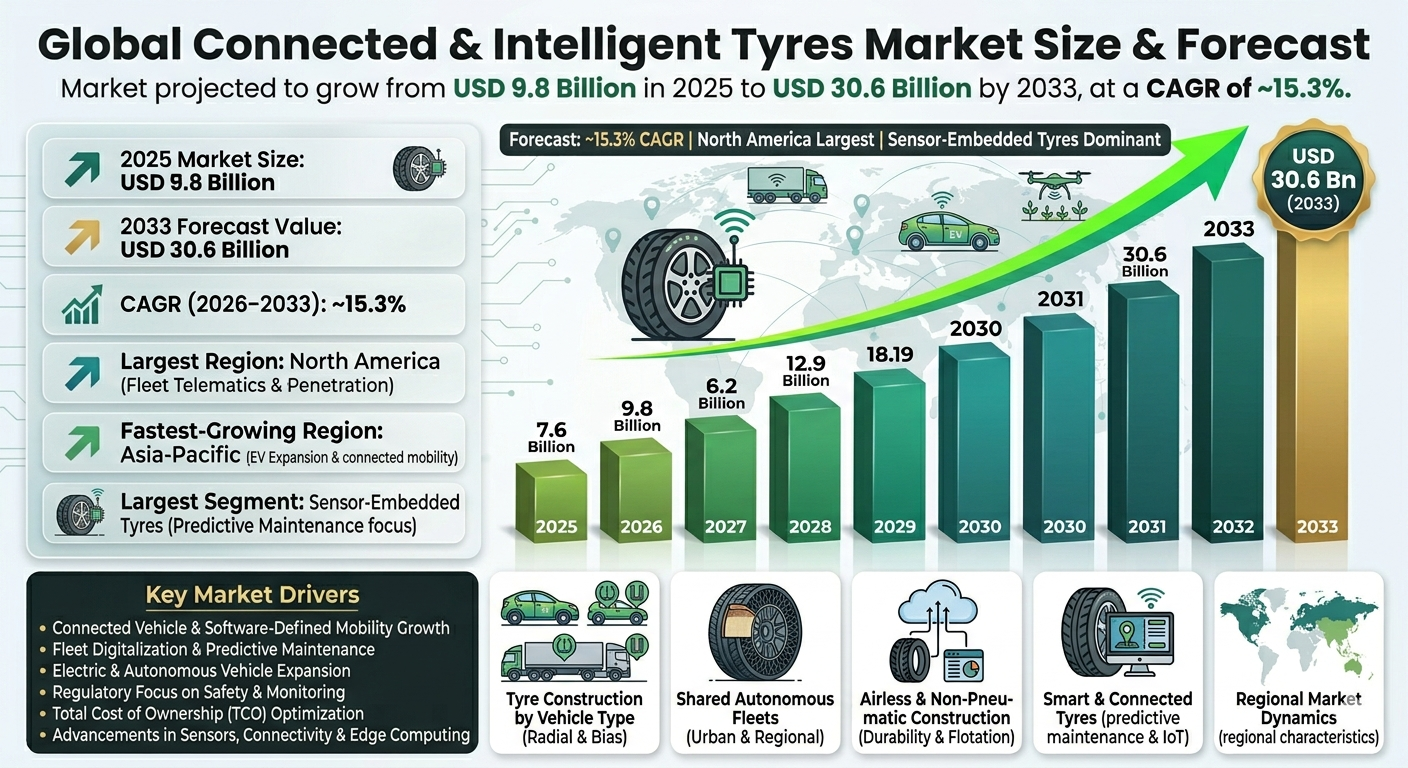

| 2025 Market Size | USD 9.8 Billion |

| 2033 Market Size | USD 30.6 Billion |

| CAGR (2026???2033) | ~15.3% |

| Largest Region | North America |

| Fastest-Growing Region | Asia-Pacific |

| Largest Segment | Sensor-embedded tyres |

| Fastest-Growing Segment | EV & autonomous vehicle tyres |

| Key Trend | Tyres evolving into connected data platforms |

Global Connected & Intelligent Tyres Market Overview

The Global Connected & Intelligent Tyres Market brings tyres with a brain and a voice . They constantly track pressure, temperature, tread wear, load, road grip, and vehicle movement. All that data gets sent in real time to the car or driver, making rides safer and smoother. It???s a smart upgrade for everyday driving.

Connected tyres are like smart sidekicks for cars, trucks, EVs, self-driving rides, and even heavy off-road machines . They help keep things safe, catch problems before they happen, save energy, and make fleets run smoother. By linking up with the car???s computer, telematics, and cloud systems, they turn tyres into key players in modern, software-driven mobility. Basically, tyres aren???t just rubber anymore???they???re part of the car???s brain.

OEMs increasingly deploy connected tyres as part of ADAS, TPMS, fleet management, and autonomous driving stacks, while aftermarket adoption is accelerating across logistics, mining, public transport, and shared mobility fleets.

According to the Pheonix Demand Forecast Engine, the Global Connected & Intelligent Tyres Market size is valued at USD 9.8 billion in 2025 and is projected to reach USD 30.6 billion by 2033, growing at a CAGR of ~15.3% during 2026???2033.

North America is the largest market, driven by fleet telematics and connected vehicle penetration, while Asia-Pacific is the fastest-growing region, supported by EV expansion, smart manufacturing, and connected mobility investments.

Key Drivers of Global Connected & Intelligent Tyres Market Growth

Connected Vehicle & Software-Defined Mobility Growth

Vehicles increasingly rely on real-time data, making tyres an active data source rather than a passive component.

Fleet Digitalization & Predictive Maintenance

Fleet operators use tyre intelligence to cut downtime, fuel use, and accidents, fueling market growth?? and boosting efficiency.

Electric & Autonomous Vehicle Expansion

EVs and AVs require continuous tyre data for torque management, load sensing, traction control, and safety validation.

Regulatory Focus on Safety & Monitoring

Mandatory TPMS, vehicle safety norms, and emissions regulations accelerate adoption.

Total Cost of Ownership (TCO) Optimization

Connected tyres extend life and improve fuel efficiency, driving market growth?? and lowering operational costs.

Advancements in Sensors, Connectivity & Edge Computing

Low-power sensors, 5G, and edge analytics enable scalable deployment.

Global Connected & Intelligent Tyres Market Segmentation

1. By Intelligence & Connectivity Type

1.1 Sensor-Embedded Tyres??

1.1.1 Pressure Sensors

1.1.1.1 Direct TPMS sensors

1.1.1.2 In-tyre pressure modules

1.1.2 Temperature Sensors

1.1.2.1 Heat buildup monitoring

1.1.2.2 High-load applications

1.1.3 Tread Wear & Deformation Sensors

1.1.3.1 Embedded wear indicators

1.1.3.2 Predictive replacement alerts

1.2 Fully Connected Tyres??

1.2.1 Vehicle-to-Tyre (V2T) Communication

1.2.2 Tyre-to-Cloud (T2C) Connectivity

1.2.3 Tyre-to-Infrastructure (T2I) Integration

2. By Vehicle Category

2.1 Passenger Vehicles

2.1.1 Hatchbacks & Compact Cars

2.1.2 Sedans

2.1.2.1 Mid-size sedans

2.1.2.2 Luxury sedans

2.1.3 SUVs & Crossovers

2.1.3.1Compact SUVs

2.1.3.2 Mid-size SUVs

2.1.3.3 Premium SUVs

2.2 Commercial Vehicles

2.2.1 Light Commercial Vehicles (LCVs)

2.2.1.1 Urban delivery vans

2.2.1.2 E-commerce fleets

2.2.2 Medium & Heavy Commercial Vehicles

2.2.2.1 Long-haul trucks

2.2.2.2 Buses

2.2.2.3 Logistics fleets

2.3 Electric Vehicles (Fastest-Growing Vehicle Segment)

2.3.1 Battery Electric Vehicles (BEVs)

2.3.2 Plug-in Hybrid Electric Vehicles (PHEVs)

2.4 Off-the-Road (OTR) Vehicles

2.4.1 Construction Equipment

2.4.2 Mining Vehicles

2.4.3 Agricultural Machinery

3. By Connectivity Technology

3.1 Bluetooth & Short-Range Connectivity

3.1.1 Vehicle ECU Integration

3.2 RFID-Enabled Tyres

3.2.1 Passive RFID Tyres

3.2.2 Active RFID Tyres

3.3 Cellular-Connected Tyres (Fastest-Growing)

3.3.1 LTE-Enabled Tyres

3.3.2 5G-Enabled Tyres

3.4 Edge & Cloud-Integrated Tyres

3.4.1 Edge Processing Tyres

3.4.2 Cloud-Based Fleet Analytics

4. By Sales Channel

4.1 OEM (Original Equipment Manufacturer) (Largest Segment)

4.1.1 Passenger Vehicle OEM Fitment

4.1.2 EV OEM Fitment

4.1.3 Commercial Fleet OEM Fitment

4.2 Aftermarket & Retrofit Solutions

4.2.1 Fleet Retrofit Systems

4.2.2 Authorized Tyre Dealers

4.2.3 Telematics & Mobility Service Providers

5. By Application

5.1 Safety & Compliance

5.1.1 TPMS & Regulatory Compliance

5.2 Predictive Maintenance (Largest Application)

5.2.1 Tyre Failure Prediction

5.2.2 Wear & Load Optimization

5.3 Fuel Efficiency & Energy Optimization

5.3.1 Rolling Resistance Management

5.4 Autonomous & ADAS Enablement (Fastest-Growing)

5.4.1 Road Condition Detection

5.4.2 Traction & Stability Feedback

6. By Geography

6.1 North America (Largest Market)

-

U.S.

-

Canada

6.2 Asia-Pacific (Fastest-Growing Region)

-

China

-

Japan

-

South Korea

-

India

6.3 Europe

-

Germany

-

France

-

U.K.

6.4 Latin America

-

Brazil

-

Mexico

6.5 Middle East & Africa

Regional Insights of Global Connected & Intelligent Tyres Market

North America ??? Largest Market

Advanced fleet telematics adoption, connected vehicle penetration, and strong OEM integration.

Asia-Pacific ??? Fastest-Growing

EV acceleration, smart manufacturing, and connected mobility investments drive rapid growth.

Europe

Strong regulatory focus on safety, emissions, and connected vehicle standards.

Latin America

Gradual adoption led by logistics and public transport fleets.

Middle East & Africa

Mining, construction, and extreme-condition applications dominate demand.

Leading Companies in the Global Connected & Intelligent Tyres Market

-

Goodyear Tire & Rubber Company

-

Continental AG

-

Pirelli & C. S.p.A.

-

Hankook Tire

-

Yokohama Rubber Company

-

Sumitomo Rubber Industries

-

Nokian Tyres

-

Sensata Technologies (sensor ecosystem partner)

Michelin are?? Bridgestone are the largest company in the Global Connected & Intelligent Tyres Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Tracks connected vehicle growth, EV penetration, and fleet digitization.

Intelligent Tyre Adoption Model

Maps sensor penetration by vehicle type and region.

Fleet TCO Optimization Engine

Quantifies fuel savings, uptime improvements, and maintenance reduction.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate ??? fleet consolidation increases leverage

-

Supplier Power: Moderate ??? sensor and semiconductor dependencies

-

Threat of New Entrants: Low ??? high R&D and OEM integration barriers

-

Threat of Substitutes: Low ??? software requires physical data inputs

-

Competitive Rivalry: High ??? global tyre majors compete on intelligence

Why the Connected & Intelligent Tyres Market Is Critical

-

Transforms tyres into real-time data generators

-

Enables predictive maintenance and zero-downtime fleets

-

Essential for EV efficiency and autonomous decision-making

-

Enhances vehicle safety, compliance, and sustainability

-

Positions tyres as core components of software-defined mobility

Final Takeaway

The Global Connected & Intelligent Tyres Market is redefining the role of tyres within the mobility value chain. As vehicles become increasingly connected, electric, and autonomous, intelligent tyres will be indispensable for safety, efficiency, and operational intelligence. Market leaders that integrate sensing, connectivity, analytics, and OEM partnerships will capture disproportionate value through 2033.

Competitive Landscape

Global Connected & Intelligent Tyres Competitive Intensity & Market Structure Overview

The Global Connected & Intelligent Tyres Market is characterized by a highly innovation-driven, technology-centric competitive landscape, where traditional tyre manufacturers increasingly compete alongside sensor technology firms, telematics providers, and software ecosystem partners. Unlike conventional tyre markets, competition is no longer defined solely by durability, pricing, or replacement cycles’it is increasingly shaped by data generation, predictive analytics, connectivity infrastructure, and integration with software-defined mobility platforms. The market structure is strongly influenced by OEM-led deployment, particularly across connected passenger vehicles, electric vehicles, commercial fleets, and autonomous mobility systems. OEM integration remains the dominant route to scale due to vehicle architecture compatibility, ADAS integration, and telematics ecosystem alignment. However, the aftermarket is emerging rapidly through retrofit sensor systems, fleet telematics partnerships, and predictive maintenance solutions. Market concentration is moderately high, with global Tier 1 tyre manufacturers leveraging their manufacturing scale, OEM relationships, and sensor partnerships to maintain leadership. At the same time, the market is gradually opening to specialized technology providers that deliver embedded sensors, cloud analytics, RFID, and tyre intelligence platforms.

Global Connected & Intelligent Tyres Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global intelligent mobility leader. Strong focus on connected tyre ecosystems, predictive fleet solutions, and sustainable smart tyre innovation. Bridgestone Corporation: Major player in connected fleet mobility, combining tyre intelligence with telematics and digital fleet optimization platforms. Goodyear Tire & Rubber Company: Technology-focused innovator emphasizing predictive analytics, fleet management, and autonomous-ready tyre systems. Continental AG: Advanced digital mobility leader with integrated tyre sensors, TPMS, and vehicle electronics expertise. Pirelli & C. S.p.A.: Premium intelligent tyre specialist with strong emphasis on high-performance connected vehicle applications. Hankook Tire: Expanding aggressively in EV and smart tyre categories with sensor-enabled product innovation. Yokohama Rubber Company: Performance-oriented player integrating connected tyre technologies for commercial and premium segments. Sensata Technologies: Key sensor ecosystem partner supporting tyre intelligence hardware and data architecture expansion.

Key Competitive Intensity & Market Structure Signals in Global Connected & Intelligent Tyres Market

A defining structural signal is the transition of tyres from consumable products into real-time data platforms. This fundamentally shifts competition from manufacturing-centric to intelligence-centric, where sensing capability, analytics integration, and software interoperability become critical competitive differentiators. Another major signal is the accelerating role of fleet digitalization. Commercial logistics, mining, and mobility operators increasingly prioritize predictive maintenance, uptime optimization, and fuel savings, intensifying demand for connected tyre systems that directly reduce operational costs. Electric and autonomous vehicle expansion is also reshaping competition. EVs and AVs require continuous tyre data for energy optimization, traction management, and autonomous safety validation, making connected tyres a strategic infrastructure layer rather than optional upgrades. Technology partnerships are becoming increasingly important, with tyre companies collaborating with semiconductor providers, cloud platforms, telematics companies, and smart city ecosystems to strengthen market positioning.

Strategic Implications of Competitive Intensity & Market Structure in Global Connected & Intelligent Tyres Market

Manufacturers must increasingly prioritize ecosystem integration over standalone product sales. Strategic advantage will depend on combining tyre manufacturing with sensors, cloud analytics, predictive software, and OEM platform compatibility. OEM partnerships remain mission-critical, particularly in EV and autonomous segments where tyre intelligence is deeply integrated into vehicle safety and software architecture. Fleet-focused business models such as predictive maintenance subscriptions, tyre-as-a-service, and digital fleet optimization are becoming major strategic priorities due to their recurring revenue potential and high customer retention. R&D investment in low-power sensors, edge computing, AI analytics, and cybersecurity is essential, as competitive advantage increasingly depends on both hardware and software performance.

Global Connected & Intelligent Tyres Competitive Intensity & Market Structure Forward Outlook

The Global Connected & Intelligent Tyres Market is expected to experience sustained competitive acceleration as connected vehicles, EVs, and autonomous mobility expand globally. Competitive rivalry will intensify as leading tyre manufacturers transition into mobility intelligence providers. Market consolidation is likely to increase, with Tier 1 tyre players strengthening positions through acquisitions, sensor technology partnerships, telematics alliances, and software ecosystem expansion. The aftermarket will evolve from traditional replacement channels into digitally enabled fleet service ecosystems, creating new opportunities for predictive maintenance, cloud analytics, and retrofit solutions. Over the long term, the market will be defined by three core competitive pillars: data ownership, OEM ecosystem integration, and predictive mobility intelligence. Companies that successfully align tyre hardware with software, fleet analytics, and autonomous mobility systems will lead the Global Connected & Intelligent Tyres Market through 2033.

Value Chain

Global Connected & Intelligent Tyres Market Value Chain & Supply Chain Evolution Overview

The Global Connected & Intelligent Tyres Market value chain is rapidly transforming from a traditional tyre manufacturing ecosystem into a highly integrated mobility intelligence network that combines advanced tyre engineering, embedded electronics, software analytics, wireless communication, and cloud-connected vehicle ecosystems. Connected and intelligent tyres are no longer passive mobility components; they function as real-time sensing platforms that generate actionable vehicle, road, and performance intelligence.

These tyres continuously monitor pressure, temperature, tread wear, deformation, load, traction, road grip, and driving conditions, transmitting data to vehicle ECUs, fleet telematics systems, cloud analytics platforms, and autonomous driving stacks. This evolution expands the value chain beyond tyre manufacturing into semiconductors, sensor ecosystems, connectivity providers, AI analytics, telematics, and mobility software.

The upstream supply chain includes natural rubber, synthetic rubber, carbon black, silica, steel reinforcements, MEMS sensors, RFID chips, Bluetooth modules, cellular communication systems, embedded processors, batteries, and edge computing hardware. Major manufacturers such as Michelin, Bridgestone, Continental, and Goodyear increasingly collaborate with sensor specialists, semiconductor providers, telematics platforms, and cloud infrastructure companies to ensure ecosystem scalability.

Manufacturing requires highly specialized integration of sensor systems, connectivity architecture, durability engineering, and software compatibility without compromising tyre safety, rolling resistance, or structural performance. This adds complexity in sensor encapsulation, battery efficiency, wireless calibration, data accuracy, and lifecycle durability.

OEM channels dominate the market, with connected tyres increasingly embedded into ADAS systems, TPMS, EV performance platforms, autonomous vehicle systems, and software-defined vehicle architectures. At the same time, aftermarket retrofits are expanding across logistics, public transport, mining, agriculture, and industrial fleet operations.

Key supply chain challenges include semiconductor dependencies, connectivity standardization, software interoperability, cybersecurity risks, battery durability, and sustainability pressures related to electronic waste and circular material design.

Global Connected & Intelligent Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The current supply chain environment is defined by rapid digitalization, software-defined mobility, EV expansion, and autonomous vehicle readiness.

Upstream, manufacturers are diversifying sensor, chip, and communication module sourcing strategies to mitigate risks associated with semiconductor shortages and supply chain disruptions.

Manufacturing priorities are shifting toward advanced multi-sensor integration, 5G-ready communication systems, RFID scalability, battery-free sensing technologies, edge analytics, and AI-powered predictive maintenance systems.

OEM integration is accelerating, particularly in premium passenger vehicles, EVs, logistics fleets, and autonomous pilot platforms, where connected tyres are becoming standard operational intelligence assets.

Fleet operators are increasingly deploying connected tyre systems in aftermarket applications to improve uptime, optimize TCO, and enhance predictive maintenance outcomes.

Digital business models are emerging as tyre companies evolve into connected mobility service providers through subscription analytics, fleet intelligence dashboards, and software monetization.

Key Value Chain & Supply Chain Evolution Signals in Global Connected & Intelligent Tyres Market

Several critical trends are reshaping the connected tyre ecosystem.

First, tyres are evolving into intelligent IoT endpoints that actively contribute to software-defined vehicle ecosystems.

Second, EV and autonomous vehicle platforms are significantly increasing demand for real-time tyre intelligence, especially for torque, battery efficiency, traction, and road feedback.

Third, predictive fleet maintenance is creating strong commercial demand for data-driven tyre platforms.

Fourth, cellular connectivity, 5G, and edge computing are improving scalability and enabling faster deployment across mobility sectors.

Fifth, recurring software and analytics revenue streams are becoming increasingly important as tyre manufacturers expand beyond product sales into data ecosystems.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Connected & Intelligent Tyres Market

Leading companies such as Michelin, Bridgestone, Continental, and Goodyear benefit from deep OEM partnerships, advanced sensor ecosystems, software platforms, and global manufacturing scale.

High barriers to entry are created by sensor integration complexity, cloud compatibility, cybersecurity standards, software development requirements, and OEM validation cycles.

Strategic alliances between tyre manufacturers, semiconductor firms, telematics providers, cloud platforms, and mobility software companies are becoming essential for competitive leadership.

Long-term recurring revenue opportunities are expanding through fleet software subscriptions, predictive analytics, connected services, and mobility data monetization.

Cost optimization remains critical, as intelligent tyres require balancing hardware costs, software scalability, durability, and premium pricing pressures.

Global Connected & Intelligent Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the connected and intelligent tyre value chain is expected to become increasingly autonomous-ready, cloud-integrated, and software-centric.

Manufacturers will focus on fully integrated tyres featuring advanced sensor fusion, edge computing, AI analytics, 5G communication, and V2X-enabled tyre ecosystems.

OEM partnerships will deepen further as software-defined vehicles, EVs, and autonomous systems increasingly depend on connected tyre intelligence.

Aftermarket growth will accelerate through retrofit ecosystems, telematics integration, and scalable fleet intelligence platforms.

Sustainability innovation will expand through recyclable electronics, battery-free sensing, low-energy connectivity systems, and circular manufacturing strategies.

Ultimately, connected and intelligent tyres will evolve from premium safety features into foundational components of the global software-defined mobility infrastructure.

Market-Specific Value Chain

- Raw Material & Electronics Procurement: Rubber, silica, carbon black, steel reinforcements, MEMS sensors, RFID chips, processors, batteries, Bluetooth/LTE/5G modules

- Research & Development: Sensor fusion, embedded systems, predictive analytics, AI, cloud integration, EV optimization, autonomous platform readiness

- Manufacturing: Intelligent tyre production, sensor embedding, wireless calibration, software integration, structural durability validation

- OEM Integration: Passenger vehicles, commercial fleets, EVs, autonomous vehicles, industrial mobility platforms

- Distribution & Connectivity Ecosystem: OEM channels, telematics providers, fleet platforms, cloud service providers, authorized dealers

- Aftermarket & Mobility Intelligence Services: Retrofit solutions, predictive maintenance, fleet dashboards, software subscriptions, data monetization

Company-to-Stage Mapping

- Raw Material & Electronics Procurement: Michelin, Bridgestone Corporation, Continental AG, Sensata Technologies

- Research & Development: Michelin, Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A.

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Hankook Tire

- Distribution & Connectivity Ecosystem: Goodyear Tire & Rubber Company, Nokian Tyres, Apollo Tyres, telematics platform providers

- Aftermarket & Mobility Intelligence Services: Michelin, Continental AG, Bridgestone Corporation, Sensata Technologies

Investment Activity

Global Connected & Intelligent Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Connected & Intelligent Tyres Market are being accelerated by the convergence of connected mobility, fleet digitalization, autonomous vehicle ecosystems, and EV expansion. Between 2026 and 2033, capital allocation is expected to increasingly focus on embedded sensor technologies, cloud-connected tyre ecosystems, predictive analytics platforms, AI-enabled fleet intelligence, and next-generation vehicle-to-tyre communication systems.

The market is highly technology-intensive, requiring sustained investment in MEMS sensors, RFID systems, edge computing modules, telematics integration, software-defined mobility architecture, and advanced data analytics platforms. Major global tyre manufacturers including Michelin, Bridgestone, Goodyear, Continental, and Pirelli are significantly expanding R&D investments, strategic partnerships, and digital mobility portfolios to strengthen connected tyre ecosystems.

A major structural transformation shaping investment patterns is the shift of tyres from passive mechanical products into active data-generating platforms. This transition is directing funding toward intelligent tyre systems capable of supporting predictive maintenance, ADAS integration, autonomous navigation, fleet optimization, and real-time road condition intelligence.

Global Connected & Intelligent Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by rising adoption of connected vehicles, software-defined transportation systems, mandatory safety regulations, and increasing fleet demand for uptime optimization. OEM alliances with connected mobility providers, cloud platforms, and telematics companies remain central to securing long-term technology integration.

- North America: Leads global investment activity due to advanced fleet telematics infrastructure, connected commercial vehicle penetration, and strong autonomous mobility development.

- Asia-Pacific: Fastest-growing investment region, fueled by EV growth, smart manufacturing ecosystems, expanding connected infrastructure, and large-scale automotive production.

- Europe: Strong investment momentum driven by regulatory mandates, advanced safety frameworks, and premium connected vehicle innovation.

- Latin America & Middle East & Africa: Emerging markets attracting gradual investments through logistics modernization, mining fleet digitization, and smart transport adoption.

Key Investment & Funding Dynamics Signals in Global Connected & Intelligent Tyres Market

- Rapid growth of connected and software-defined vehicles is increasing funding into tyre intelligence platforms that provide real-time operational data.

- Expansion of fleet digitalization is driving capital inflows into predictive maintenance technologies, reducing downtime and optimizing fleet TCO.

- Growing EV and autonomous vehicle penetration is accelerating investment in advanced tyre sensing systems for torque sensing, traction control, and environmental mapping.

- Rising demand for cloud-based mobility ecosystems is encouraging investment in tyre-to-cloud and vehicle-to-tyre communication frameworks.

- Sensor miniaturization, 5G integration, and AI-enabled analytics are creating high-growth funding opportunities in next-generation intelligent tyre platforms.

Strategic Implications of Investment & Funding Dynamics in Global Connected & Intelligent Tyres Market

- The investment landscape strongly favors global tyre leaders with advanced digital capabilities, software integration expertise, and deep OEM relationships.

- Partnerships with telematics providers, semiconductor companies, cloud infrastructure players, and autonomous mobility firms are becoming essential for strategic competitiveness.

- Technological differentiation is increasingly centered around predictive intelligence, cloud connectivity, real-time analytics, and autonomous vehicle readiness.

- Regional investment diversification is critical, with North America leading telematics deployment, Asia-Pacific driving manufacturing scale, and Europe advancing safety-led innovation.

- Cybersecurity, semiconductor dependency, and high system integration costs remain strategic challenges requiring sustained capital allocation.

Global Connected & Intelligent Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Connected & Intelligent Tyres Market is expected to attract substantial and sustained investment as tyres become central components of connected, autonomous, and software-defined mobility ecosystems.

Future capital deployment will increasingly prioritize fully connected tyre systems, AI-powered predictive maintenance platforms, smart fleet optimization tools, autonomous vehicle compatibility, and edge-cloud data intelligence.

- North America: Will remain a dominant investment center for fleet telematics, autonomous systems, and software-led tyre innovation.

- Asia-Pacific: Will experience the highest investment acceleration due to connected EV manufacturing, infrastructure scale, and smart mobility adoption.

- Europe: Will continue driving premium innovation in safety-compliant intelligent tyre ecosystems.

Digital transformation will fundamentally reshape market economics, with tyres increasingly positioned as connected mobility assets generating recurring software, analytics, and fleet management revenues.

Overall, the market will maintain a strong growth trajectory through 2033, supported by the strategic evolution of tyres into connected data platforms. Companies that align tyre manufacturing with sensing, software, cloud intelligence, and mobility integration will be best positioned to lead the next generation of transportation innovation.

Technology & Innovation

Global Connected & Intelligent Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape in the global connected & intelligent tyres market is being shaped by software-defined mobility, real-time vehicle intelligence, predictive maintenance, and autonomous transportation evolution. Connected tyres are transforming from traditional consumables into intelligent mobility infrastructure capable of continuously sensing, analyzing, and communicating critical performance data such as pressure, temperature, tread wear, load, grip, and road conditions.

Innovation intensity in this market is exceptionally high as tyre manufacturers, semiconductor companies, telematics providers, and automotive OEMs increasingly collaborate to integrate tyres into connected vehicle ecosystems. Leading players such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A., and advanced sensor ecosystem partners are heavily investing in tyre intelligence platforms that support ADAS, fleet optimization, EV systems, and autonomous driving.

A major technological shift is the transition from standalone TPMS solutions toward fully connected, multi-sensor tyre systems integrated with vehicle-to-tyre (V2T), tyre-to-cloud (T2C), and tyre-to-infrastructure (T2I) communication frameworks. These innovations are redefining tyres as active digital nodes within broader mobility networks, enabling safer, more efficient, and increasingly autonomous transportation systems.

Global Connected & Intelligent Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the connected tyre innovation ecosystem is centered on sensor integration, wireless communication, and predictive analytics. Sensor-embedded tyres dominate current deployment, particularly through TPMS, temperature monitoring, and wear analysis applications.

Low-power sensor technologies, edge computing capabilities, and semiconductor miniaturization are key innovation enablers. These technologies allow tyres to continuously collect and process data while minimizing power consumption and maximizing durability under extreme operating conditions.

Connectivity innovation is rapidly evolving beyond Bluetooth and RFID toward LTE, 5G, and cloud-integrated tyre platforms. This shift is enabling scalable deployment across commercial fleets, passenger vehicles, and autonomous systems.

Predictive maintenance remains one of the most commercially significant innovation areas. Fleet operators increasingly leverage tyre analytics platforms to predict failures, optimize replacement schedules, reduce downtime, and lower total operating costs.

Electric vehicle and autonomous vehicle growth is accelerating innovation in load sensing, torque optimization, traction intelligence, and road condition feedback, making connected tyres strategically important for advanced vehicle system performance.

Manufacturing innovation includes AI-driven sensor calibration, advanced material-electronics integration, and digital twin simulation models that accelerate product development while ensuring performance reliability.

Key Technology & Innovation Landscape Signals in Global Connected & Intelligent Tyres Market

- Multi-Sensor Embedded Architectures: Pressure, temperature, tread wear, grip, and deformation intelligence.

- Vehicle-to-Tyre (V2T) Communication: Direct integration with vehicle systems and control software.

- Tyre-to-Cloud (T2C) Platforms: Real-time fleet management and predictive analytics ecosystems.

- 5G & Cellular Connectivity: High-speed, scalable tyre intelligence communication.

- Edge Computing Integration: Real-time processing directly at tyre or vehicle level.

- Autonomous Vehicle Enablement: Tyres supporting road sensing, traction intelligence, and software safety systems.

- EV Optimization Technologies: Load balancing, torque response, and rolling resistance intelligence.

Strategic Implications of Technology & Innovation Landscape in Global Connected & Intelligent Tyres Market

The connected & intelligent tyre landscape creates major strategic shifts across tyre manufacturing, automotive OEMs, telematics ecosystems, and fleet operations. Tyres are increasingly becoming software-enabled assets that create recurring data and service revenue opportunities.

OEM integration is strategically essential, as connected tyres are becoming embedded into ADAS, EV management systems, and autonomous software platforms. Manufacturers that secure OEM partnerships early will benefit from long-term platform lock-in.

Fleet operators are driving rapid commercialization through demand for predictive maintenance, uptime optimization, and cost-per-kilometer improvements, accelerating the transition from tyre sales to data-enabled mobility services.

Supply chain priorities are shifting toward sensor technology, semiconductors, connectivity modules, and software interoperability, expanding competition beyond traditional tyre engineering.

Cybersecurity and data governance are becoming increasingly important strategic considerations as tyres become connected endpoints within larger mobility networks.

Sustainability implications are also growing, as intelligent tyres improve fuel efficiency, reduce emissions, minimize waste through optimized replacement cycles, and support broader decarbonization goals.

Global Connected & Intelligent Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the connected & intelligent tyres market is expected to evolve toward fully autonomous-ready, AI-powered, and continuously connected tyre ecosystems. Tyres will increasingly function as digital mobility interfaces that support software-defined transportation infrastructure.

Future innovation will focus on advanced road surface analytics, self-learning tyre systems, autonomous safety feedback loops, and expanded vehicle-to-infrastructure integration.

5G, AI, and cloud-native mobility platforms are expected to significantly expand connected tyre capabilities, enabling faster diagnostics, deeper operational intelligence, and enhanced autonomous responsiveness.

Material science innovation will increasingly focus on embedding durable electronics into sustainable, lightweight tyre structures without compromising performance, safety, or recyclability.

AI-driven manufacturing, digital twin validation, and software-over-the-air update capabilities are expected to accelerate innovation cycles and product adaptability.

In conclusion, the Global Connected & Intelligent Tyres Market is transforming tyres into data-centric, software-integrated mobility platforms that directly shape safety, efficiency, autonomy, and sustainability. Companies that successfully combine sensing technologies, connectivity ecosystems, predictive analytics, and scalable OEM partnerships will define competitive leadership through 2033.

Market Risk

Global Connected & Intelligent Tyres Market Risk Factors & Disruption Threats Overview

The Global Connected & Intelligent Tyres Market operates at the intersection of tyre manufacturing, sensor technology, software-defined mobility, and connected vehicle ecosystems. While this market benefits from strong structural growth driven by EVs, fleet digitalization, and autonomous mobility, it carries a high risk profile due to technology complexity, semiconductor dependency, cybersecurity concerns, and rapid innovation cycles. A major structural risk is technology integration complexity. Connected tyres require embedded sensors, data transmission modules, cloud connectivity, and vehicle system compatibility, significantly increasing design, manufacturing, and lifecycle management complexity compared to conventional tyres. Another major disruption threat is semiconductor and electronics supply chain dependency. Sensor chips, wireless modules, and connectivity systems expose manufacturers to component shortages, geopolitical supply disruptions, and rising electronic input costs. Cybersecurity and data privacy risks are also critical. As tyres evolve into connected mobility devices, vulnerabilities in tyre-to-vehicle or tyre-to-cloud systems may create safety, operational, or regulatory challenges. Rapid technological obsolescence presents another challenge. Continuous advancements in AI, edge computing, telematics, and autonomous mobility can shorten product life cycles and increase R&D burdens for manufacturers.

Global Connected & Intelligent Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects rapid expansion, supported by fleet telematics growth, EV adoption, and increasing OEM integration of intelligent tyre systems. However, this growth is accompanied by rising complexity in hardware, software, and data ecosystem management. OEM adoption currently dominates, particularly in premium vehicles, EVs, and commercial fleets, where predictive maintenance and real-time monitoring create measurable value. Fleet operators are increasingly adopting retrofit intelligent tyre systems to optimize uptime, fuel consumption, and maintenance scheduling, accelerating aftermarket opportunities. At the same time, semiconductor supply volatility and rising electronics costs remain persistent challenges, affecting scalability and margin structures. Regulatory developments around vehicle safety, TPMS mandates, and connected mobility standards are supporting adoption while simultaneously increasing compliance requirements.

Key Risk Factors & Disruption Threats Signals in Global Connected & Intelligent Tyres Market

A major disruption signal is the acceleration of software-defined vehicles, where tyres are becoming integrated into broader mobility intelligence platforms rather than standalone components. Growth in autonomous mobility and ADAS deployment is another key signal, significantly increasing demand for real-time tyre-road data and advanced connectivity. Cybersecurity regulations and connected vehicle compliance frameworks are emerging as major strategic considerations, particularly in North America and Europe. Fleet digitalization trends are reshaping procurement behavior, with buyers increasingly prioritizing total mobility intelligence over traditional tyre performance metrics alone. Advancements in edge computing, AI analytics, and 5G infrastructure are also accelerating competitive pressure, favoring companies capable of combining hardware and software leadership.

Strategic Implications of Risk Factors & Disruption Threats in Global Connected & Intelligent Tyres Market

Manufacturers must evolve from product-focused strategies toward integrated mobility technology models that combine tyre performance, sensors, software, and analytics. Investment in semiconductor partnerships, sensor ecosystems, and cybersecurity infrastructure is critical to ensure long-term competitiveness. OEM relationships will remain strategically essential, particularly for EV and autonomous platform integration where tyre intelligence becomes foundational. Aftermarket and fleet retrofit solutions represent a major growth opportunity, especially for logistics, mining, and public transport sectors seeking predictive maintenance capabilities. Data monetization, analytics platforms, and tyre-as-a-service models may emerge as critical competitive differentiators beyond physical tyre sales.

Global Connected & Intelligent Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Connected & Intelligent Tyres Market is expected to remain one of the fastest-growing tyre segments, but it will increasingly function as part of a broader connected mobility ecosystem rather than a traditional tyre category. EV growth, autonomous deployment, and smart fleet infrastructure will remain the largest market accelerators while also intensifying product and software complexity. Cybersecurity, data governance, and interoperability standards will become increasingly important as tyres become active nodes in mobility networks. Competition will likely expand beyond traditional tyre manufacturers to include telematics firms, software providers, and sensor technology companies. Overall, long-term success will depend on manufacturers’ ability to balance durability, sensing intelligence, software integration, cybersecurity, and scalable ecosystem partnerships, positioning connected tyres as strategic data platforms within future mobility.

Regulatory Landscape

Global Connected & Intelligent Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Connected & Intelligent Tyres Market is becoming a foundational force accelerating the transformation of tyres from passive mechanical products into digitally integrated mobility intelligence platforms. Governments, transportation authorities, automotive regulators, and connected infrastructure agencies are increasingly prioritizing advanced safety systems, predictive vehicle diagnostics, emissions optimization, and software-defined mobility’creating a strong policy ecosystem for connected and intelligent tyre adoption. Global regulatory mandates such as Tire Pressure Monitoring System (TPMS) requirements in North America, European Union Tyre Labelling Regulation (EU 2020/740), UNECE vehicle safety frameworks, connected vehicle mandates, and autonomous mobility regulations are significantly expanding the role of tyres as real-time data-generating assets. These policies are increasingly pushing OEMs and fleet operators toward tyres capable of continuous pressure, temperature, wear, traction, and load monitoring. Connected and intelligent tyres align closely with modern regulatory priorities by enhancing road safety, reducing blowout risks, improving energy efficiency, lowering rolling resistance, and enabling compliance with connected transport systems. Their integration into ADAS, fleet telematics, EV systems, and autonomous driving stacks positions them as strategic infrastructure within next-generation mobility policy frameworks. Emerging markets including China, India, Brazil, Southeast Asia, and the Middle East are also modernizing transportation regulations through smart mobility programs, digital fleet oversight, and vehicle safety reforms. These developments are accelerating policy support for connected tyre ecosystems across passenger, logistics, mining, and public transportation sectors.

Global Connected & Intelligent Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is shaped by the convergence of connected mobility policy, vehicle safety digitization, telematics expansion, and electrification. North America currently represents one of the strongest regulatory ecosystems due to TPMS mandates, NHTSA safety standards, fleet telematics maturity, and rising autonomous vehicle policy development. In the United States and Canada, connected vehicle programs and fleet management regulations are increasingly expanding beyond baseline TPMS into predictive maintenance, vehicle health diagnostics, and data-centric fleet optimization, creating favorable conditions for intelligent tyre deployment. Europe remains a major regulatory driver due to strict tyre labeling systems, sustainability mandates, carbon reduction frameworks, and advanced connected mobility standards. EU policy increasingly supports intelligent tyre solutions capable of delivering not only compliance but also enhanced transparency in tyre lifecycle performance, emissions impact, and vehicle efficiency. Asia-Pacific is rapidly emerging as a regulatory growth engine, driven by EV policy expansion, industrial digitization, smart city development, and intelligent transport frameworks. China’s connected vehicle policies, India’s road safety initiatives, and Japan’s mobility technology standards are accelerating the transition toward connected tyre ecosystems. The rise of autonomous mobility regulations globally is also increasing the importance of tyre intelligence, as connected tyres become essential for vehicle-road communication, road surface analytics, traction sensing, and autonomous safety validation.

Key Regulatory & Policy Environment Signals in Global Connected & Intelligent Tyres Market

- Mandatory TPMS Regulations: U.S., EU, China, and other major markets establish foundational smart tyre infrastructure.

- EU Tyre Labelling Regulation (EU 2020/740): Strengthens pressure for tyre transparency, efficiency, and advanced monitoring.

- UNECE Safety Standards: Support tyre durability, digital diagnostics, and intelligent integration.

- Connected Vehicle Policies: Promote vehicle-to-cloud, tyre-to-cloud, and fleet telematics ecosystems.

- EV Regulations: Prioritize rolling resistance, efficiency, and load management’favoring connected tyres.

- Autonomous Mobility Frameworks: Require real-time tyre-road intelligence for advanced vehicle safety.

- Fleet Digital Compliance Standards: Encourage predictive maintenance and operational safety technologies.

- Smart City & Infrastructure Programs: Expand vehicle-to-infrastructure integration opportunities for intelligent tyres.

Strategic Implications of Regulatory & Policy Environment in Global Connected & Intelligent Tyres Market

The regulatory landscape is rapidly elevating connected and intelligent tyres from premium innovation to strategic necessity. Compliance with evolving safety, telematics, and software-defined mobility standards is increasingly becoming essential for OEM competitiveness and fleet operational efficiency. Manufacturers that fail to integrate sensors, software, cloud connectivity, and advanced data architectures risk falling behind as policy increasingly favors intelligent, compliant tyre ecosystems. This shift is driving deeper partnerships among tyre manufacturers, semiconductor providers, telematics firms, AI analytics companies, and mobility software platforms. Compliance-led innovation is becoming a major competitive differentiator. Investments in multi-sensor architectures, RFID, 5G connectivity, edge computing, predictive analytics, and tyre-to-cloud ecosystems are essential for future market leadership. Fleet operators are also reshaping procurement strategies around regulation-aligned intelligent tyres that improve uptime, fuel efficiency, accident prevention, insurance optimization, and sustainability compliance. Regional policy variation is influencing supply chain localization, product certification strategies, and region-specific intelligent tyre portfolios, requiring manufacturers to align product development with local digital mobility mandates.

Global Connected & Intelligent Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become substantially more integrated with connected, electric, and autonomous mobility ecosystems, reinforcing connected tyres as critical infrastructure for next-generation transportation systems. North America is expected to continue advancing through fleet intelligence, software-defined vehicle regulations, and autonomous mobility mandates. Europe will likely remain a leader in sustainability, lifecycle transparency, and connected infrastructure compliance. Asia-Pacific is projected to become the fastest-evolving regulatory region due to EV expansion, smart manufacturing, digital logistics, and government-backed intelligent transportation infrastructure. China and India are expected to be particularly influential in shaping regional policy growth. Future regulatory frameworks are likely to evolve beyond TPMS into full Intelligent Tyre Monitoring Systems (ITMS), incorporating tread wear analytics, road interaction sensing, predictive maintenance, tyre lifecycle transparency, and vehicle-to-infrastructure communication. Advanced technologies such as self-powered sensors, AI-enabled diagnostics, digital twins, 5G tyre ecosystems, and autonomous-ready road condition intelligence are expected to gain increasing regulatory significance. Overall, the regulatory and policy environment will serve as a decisive catalyst for innovation, adoption, and standardization across the Global Connected & Intelligent Tyres Market. Companies that proactively align with evolving safety, digital mobility, EV, fleet intelligence, and autonomous regulations while scaling advanced connectivity ecosystems will be best positioned to lead this rapidly expanding market through 2033.