Global Agricultural Tyres Market size, share & forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

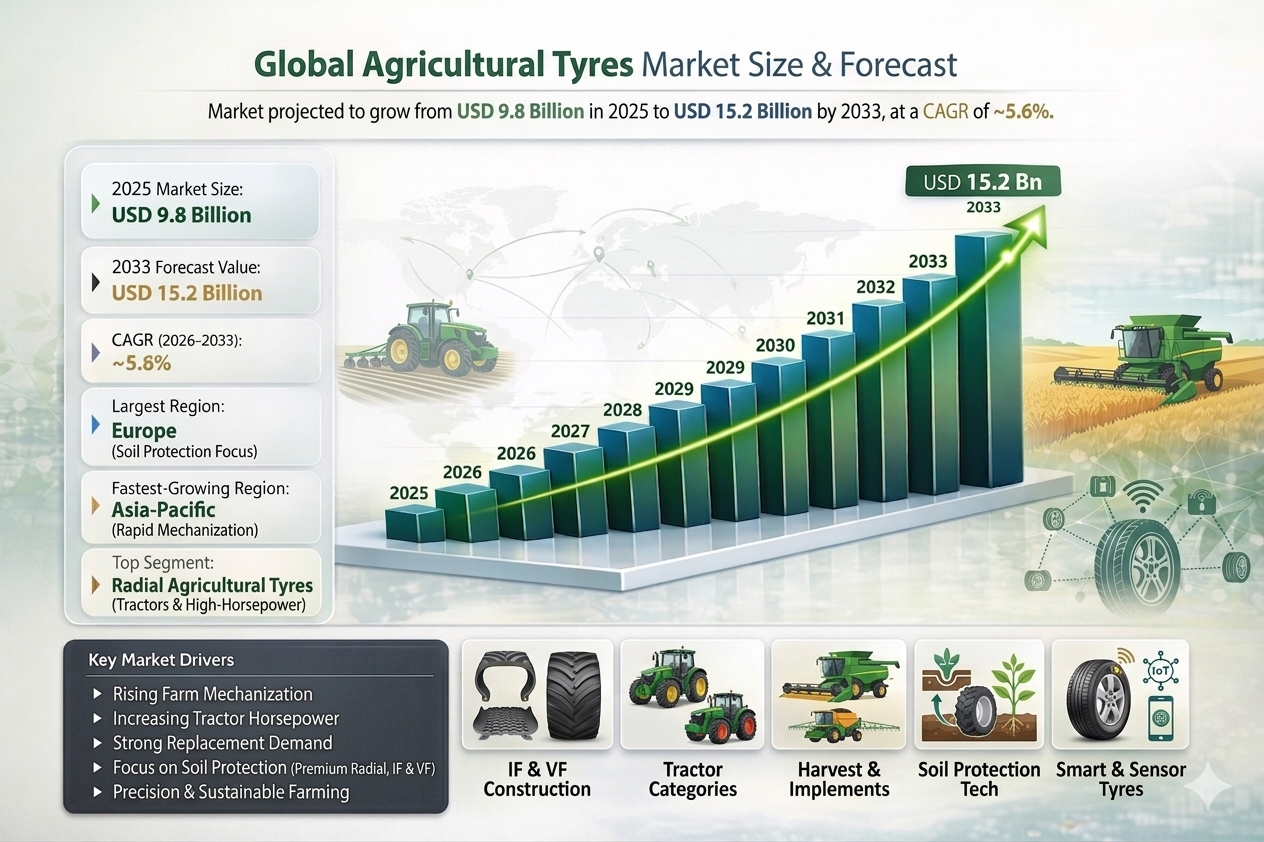

| 2025 Market Size | USD 9.8 Billion |

| 2033 Market Size | USD 15.2 Billion |

| CAGR (2026???2033) | ~5.6% |

| Largest Region | Europe |

| Fastest-Growing Region | Asia-Pacific |

| Largest Segment | Radial agricultural tyres |

| Fastest-Growing Segment | IF & VF high-flexion tyres |

| Key Trend | Soil-protection & high-load tyres |

Global Agricultural Tyres Market Overview

The Global Agricultural Tyres Market is all about tyres built for tough farm life . They go on tractors, harvesters, sprayers, and other equipment, handling heavy loads and soft, uneven fields . These tyres give strong grip and help avoid crushing the soil, which keeps crops healthy. They also save fuel and make machines last longer, making them super important for farmers.

Unlike on-road tyres, agricultural tyres must balance traction, flotation, durability, and soil protection. Modern farming practices increasingly demand tyres that reduce soil damage, support higher horsepower machinery, and enable efficient operations across both field and road use. The market includes OEM tyres supplied with new agricultural machinery and a large replacement aftermarket, driven by wear from intensive seasonal usage.

The Global Agricultural Tyres Market is growing steadily . More farms are using machines, food demand is rising, and big tractors need tougher tyres . New tech like radial, IF, and VF tyres gives better grip and protects soil. Precision farming and eco-friendly practices are pushing designs for less soil compaction and higher efficiency

According to the Pheonix Demand Forecast Engine, the Global Agricultural Tyres Market size?? is estimated at USD 9.8 billion in 2025 and is projected to reach USD 15.2 billion by 2033, growing at a CAGR of ~5.6% during the forecast period (2026???2033).

Europe and Asia-Pacific dominate demand due to strong agricultural output, while North America remains a key technology-driven market for premium and high-flexion tyres.

Key Drivers of Global Agricultural Tyres Market Growth

Rising Farm Mechanization

With fewer farm workers available, more farmers are turning to tractors and machines to get the job done . That shift is boosting demand for agricultural tyres big time . As mechanization spreads, tyre sales see steady growth, keeping farms running smoothly and productively.

Increasing Tractor Horsepower

Larger and more powerful machines require advanced tyres with higher load-bearing capacity and improved traction.

Strong Replacement Demand

Agricultural tyres experience significant wear due to seasonal field operations, creating consistent aftermarket demand.

Focus on Soil Protection

Radial, IF, and VF tyres help reduce soil compaction, improving crop yields and driving adoption of premium products.

Precision & Sustainable Farming

Modern farming techniques require tyres that support efficiency, fuel savings, and reduced environmental impact.

Global Agricultural Tyres Market Segmentation

1. By Tyre Construction

1.1 Radial Tyres??

1.1.1 Standard Radial Tyres

1.1.1.1 Improved traction and fuel efficiency

1.1.1.2 Longer service life

1.1.2 IF & VF Radial Tyres??

1.1.2.1 Higher load at lower pressure

1.1.2.2 Reduced soil compaction

1.2 Bias (Cross-Ply) Tyres

1.2.1 Nylon Bias Tyres

1.2.1.1 Cost-effective

1.2.1.2 Suitable for low-horsepower equipment

1.2.2 Polyester Bias Tyres

1.2.2.1 Improved durability

1.2.2.2 Better sidewall strength

2. By Equipment Type

2.1 Tractors (Largest Segment)

2.1.1 Utility Tractors

2.1.2 Row Crop Tractors

2.1.3 High-Horsepower Tractors

2.2 Harvesters

2.2.1 Combine Harvesters

2.2.2 Forage Harvesters

2.3 Agricultural Implements

2.3.1 Trailers

2.3.2 Sprayers

2.3.3 Seeders & planters

3. By Tyre Position

3.1 Front Tyres

Used primarily for steering control, directional stability, and load distribution in agricultural machinery.

3.1.1 Ribbed Front Tyres

3.1.1.1 Designed for precise steering

3.1.1.2 Minimal soil disturbance

3.1.2 Lug-Type Front Tyres

3.1.2.1 Used in 4WD tractors

3.1.2.2 Enhanced traction support

3.2 Rear Tyres

Rear tyres provide primary traction and carry the majority of machine load during farming operations.

3.2.1 Drive & Traction Rear Tyres

3.2.1.1 High torque transmission

3.2.1.2 Pulling heavy implements

3.2.2 High Load Rear Tyres

3.2.2.1 Designed for heavy-duty equipment

4. By Sales Channel

4.1 OEM (Original Equipment Manufacturer)

Tyres supplied directly with new agricultural machinery.

4.1.1 Tractor OEM Fitment

4.1.1.1 Factory-installed tyres

4.1.2 Harvester & Equipment OEM Fitment

4.1.2.1 Specialized tyre requirements

4.2 Aftermarket / Replacement (Largest Segment)

Driven by seasonal wear, intensive usage, and damage from field conditions.

4.2.1 Authorized Dealer Networks

4.2.1.1 OEM-aligned service providers

4.2.2 Independent Tyre Retailers

4.2.2.1 Cost-sensitive replacement demand

4.2.3 Farm Equipment Service Centers

4.2.3.1 Integrated maintenance services

4.2.3.2 Fleet and cooperative customers

5. By Tyre Technology

5.1 Conventional Agricultural Tyres

Traditional designs focused on durability and affordability.

5.1.1 Standard Bias Tyres

5.1.1.1 Low-cost solutions

5.1.2 Standard Radial Tyres

5.1.2.1 Improved fuel efficiency

5.1.2.2 Longer tread life

5.2 High-Flexion Tyres

Advanced tyres designed to carry higher loads at lower inflation pressure.

5.2.1 IF (Increased Flexion) Tyres

5.2.1.1 ~20% higher load capacity

5.2.2 VF (Very High Flexion) Tyres

5.2.2.1 ~40% higher load capacity

5.3 Low Soil Compaction Tyres

Designed to protect soil structure and improve crop yield.

5.3.1 Wide-Base Tyres

5.3.1.1 Larger footprint

5.3.2.2 Reduced ground pressure

5.3.2 Flotation Tyres

5.3.2.1 Very low inflation pressure

5.4 Smart & Sensor-Enabled Tyres (Emerging)

Digitally enhanced tyres for modern precision farming.

5.4.1 Pressure Monitoring Tyres

5.4.1.1 Real-time tyre pressure data

5.4.2 Load Optimization Tyres

5.4.2.1 Adaptive load management

6. By Geography

6.1 Europe (Largest Region)

6.1.1 Germany

6.1.2 France

6.1.3 Italy

6.1.4 U.K.

6.2 Asia-Pacific

6.2.1 China

6.2.2 India

6.2.3 Japan

6.2.4 Australia

6.3 North America

6.3.1 U.S.

6.3.2 Canada

6.4 Latin America

6.4.1 Brazil

6.4.2 Argentina

6.5 Middle East & Africa

Regional Insights of Global Agricultural Tyres Market

Europe ??? Largest Market

High adoption of advanced radial and VF tyres, strong farm mechanization, and strict soil protection regulations drive market leadership.

Asia-Pacific

Rapid mechanization in India and China, government subsidies, and rising food demand support growth.

North America

Large farms, high-horsepower equipment, and strong demand for premium tyres dominate the market.

Latin America

Expansion of commercial farming and export-oriented agriculture fuels tyre demand.

Middle East & Africa

Gradual adoption driven by irrigation-based farming and mechanization initiatives.

Leading Companies in the Global Agricultural Tyres Market

-

Continental AG

-

Trelleborg (Yokohama Group)

-

BKT (Balkrishna Industries)

-

Mitas (Yokohama Group)

-

Goodyear Tire & Rubber Company

-

CEAT Limited

-

Apollo Tyres

-

Nokian Tyres

Michelin and?? Trelleborg are the largest in the Global Agricultural Tyres Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Analyzes farm equipment sales, replacement cycles, crop prices, and mechanization trends.

Soil Impact Optimization Model

Evaluates demand for low-compaction and flotation tyres across regions.

Raw Material Sensitivity Model

Tracks natural rubber, steel cord, and oil price movements affecting margins.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate ??? price-sensitive farmers, limited premium suppliers

-

Supplier Power: Moderate ??? rubber and steel inputs

-

Threat of New Entrants: Low ??? technical expertise and distribution barriers

-

Threat of Substitutes: Low ??? tyres are essential

-

Competitive Rivalry: High ??? global majors and regional specialists

Why the Agricultural Tyres Market Remains Critical

-

Essential input for modern farming

-

Direct impact on crop yield and soil health

-

Strong recurring replacement demand

-

Increasing role in sustainable agriculture

Final Takeaway of Global Agricultural Tyres Market

The Global Agricultural Tyres Market is a steadily growing, technology-driven market shaped by mechanization, sustainability, and productivity demands. Radial, IF, and VF tyres are redefining performance standards by reducing soil compaction and improving efficiency. Manufacturers that focus on premium flexion technologies, durable designs, and strong rural distribution networks will be best positioned to lead the market through 2033.

Competitive Landscape

Agricultural Tyres Competitive Intensity & Market Structure Overview

The Global Agricultural Tyres Market is characterized by a specialized yet competitive structure, driven by technological differentiation, strong OEM relationships, and a highly fragmented replacement landscape. The market operates through a dual-channel model where OEM partnerships with agricultural equipment manufacturers provide stability, while the aftermarket remains the dominant revenue contributor due to seasonal wear and high replacement cycles.

Competitive intensity is shaped by the increasing demand for high-performance tyres that balance traction, durability, and soil protection. Manufacturers compete not only on pricing but also on advanced tyre technologies such as radial construction, IF (Increased Flexion), and VF (Very High Flexion) tyres, which enhance load capacity while minimizing soil compaction.

The market is moderately consolidated among global leaders at the top, particularly in Europe and North America, where premium agricultural practices drive demand for advanced tyres. However, regional players maintain strong positions in cost-sensitive markets across Asia-Pacific and Latin America, where affordability and distribution reach are key competitive factors.

Agricultural Tyres Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global Tyre Manufacturer. Leader in premium radial and VF tyre technologies focused on soil protection and high-load performance.

Bridgestone Corporation: Global Tyre Manufacturer. Strong presence in agricultural OEM partnerships and durable farm tyre solutions.

Continental AG: Technology-Driven Tyre Manufacturer. Focused on smart tyre solutions and precision farming integration.

Trelleborg (Yokohama Group): Agricultural Tyre Specialist. Leader in high-performance farming tyres and soil-efficient solutions.

BKT (Balkrishna Industries): Global Off-Highway Tyre Player. Strong in cost-effective agricultural tyres with global export reach.

Mitas (Yokohama Group): Agricultural Tyre Manufacturer. Known for durable and versatile farm tyre solutions.

Goodyear Tire & Rubber Company: Tyre Manufacturer. Expanding presence in agricultural and off-highway tyre segments.

CEAT Limited: Regional Leader. Strong presence in agricultural tyre markets across India and emerging economies.

Apollo Tyres: Emerging Global Competitor. Focused on affordable and durable agricultural tyre offerings.

Nokian Tyres: Premium Tyre Manufacturer. Known for high-performance tyres in challenging farming and weather conditions.

Key Competitive Intensity & Market Structure Signals in Agricultural Tyres

A major structural signal in the market is the rapid adoption of high-flexion tyre technologies such as IF and VF tyres. These tyres enable higher load capacity at lower pressure, significantly reducing soil compaction and improving crop yield, making them increasingly preferred in advanced farming regions.

OEM partnerships with tractor and agricultural equipment manufacturers play a crucial role in market positioning. Securing OEM fitment contracts ensures long-term demand stability, while replacement demand continues to drive overall market volumes due to intensive seasonal usage.

Another key trend is the growing importance of sustainability and soil health. Farmers are increasingly prioritizing tyres that minimize environmental impact, improve fuel efficiency, and support precision farming practices, pushing manufacturers to innovate continuously.

Despite the presence of global leaders, regional and local manufacturers remain highly competitive in emerging markets, where pricing, accessibility, and after-sales service significantly influence purchasing decisions.

Strategic Implications of Competitive Intensity & Market Structure in Agricultural Tyres

Manufacturers must focus on technology-driven differentiation, particularly in radial, IF, and VF tyre segments, to maintain a competitive edge. These premium solutions are increasingly becoming standard in high-productivity farming environments.

Cost competitiveness remains critical, especially in developing markets. Companies that can balance affordability with durability and performance are better positioned to capture large volumes in price-sensitive regions.

The integration of smart and sensor-enabled tyre technologies presents a new avenue for differentiation. As precision agriculture expands, tyres capable of monitoring pressure, load, and field conditions will become increasingly valuable.

Strong distribution networks and dealer relationships are essential, particularly in rural markets where accessibility and service support heavily influence brand loyalty and repeat purchases.

Agricultural Tyres Competitive Intensity & Market Structure Forward Outlook

The Agricultural Tyres Market is expected to remain moderately consolidated at the top while continuing to exhibit strong regional competition in the aftermarket segment. Demand for advanced tyre technologies will drive gradual premiumization, particularly in developed agricultural economies.

Technological innovation will accelerate, with increased focus on high-flexion tyres, soil-friendly designs, and smart tyre solutions aligned with precision farming practices. Manufacturers investing in R&D and sustainable product development will gain a competitive advantage.

Asia-Pacific is expected to witness intensified competition as mechanization increases and demand for affordable yet efficient tyres rises. Meanwhile, Europe and North America will continue to lead in premium and high-technology tyre adoption.

In the long term, the market will be defined by three key competitive pillars: soil protection efficiency, high-load performance, and technological integration. Companies that successfully align with these trends while maintaining strong OEM partnerships and aftermarket reach will lead the Global Agricultural Tyres Market through 2033.

Value Chain

Global Agricultural Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain structure of the Global Agricultural Tyres Market is specialized and closely aligned with the agricultural machinery ecosystem, farming cycles, and rural distribution networks. The market operates through a multi-tier structure involving raw material suppliers, tyre manufacturers, OEM partnerships with farm equipment companies, distributors, dealers, and end-user farmers and agribusinesses.

This ecosystem supports two primary demand streams: OEM fitment for tractors, harvesters, and agricultural equipment, and a dominant aftermarket driven by seasonal wear and intensive field usage. Given the cyclical nature of farming, supply chain planning, inventory availability, and regional distribution efficiency are critical.

The upstream supply chain depends on natural rubber, synthetic rubber, carbon black, silica, steel cord, and advanced polymer compounds. Leading manufacturers such as Michelin, Trelleborg, Bridgestone, and BKT maintain diversified sourcing strategies and long-term supplier relationships to manage raw material volatility and ensure consistent product quality.

Manufacturing in this segment is focused on durability, traction optimization, and soil protection. Tyres are engineered to balance load-bearing capacity, flotation, and reduced soil compaction. Advanced radial, IF (Increased Flexion), and VF (Very High Flexion) tyres are increasingly prioritized to meet modern farming requirements.

Distribution is highly fragmented and region-specific, involving dealer networks, agricultural equipment distributors, and rural retail channels. The aftermarket segment dominates due to recurring replacement cycles driven by seasonal operations and harsh field conditions.

Key supply chain challenges include raw material price fluctuations, seasonal demand variability, rural logistics constraints, and increasing regulatory focus on sustainability and soil preservation. Additionally, the shift toward precision agriculture and high-horsepower machinery is increasing demand for advanced tyre technologies.

Global Agricultural Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The market is currently experiencing steady transformation driven by mechanization, sustainability goals, and precision farming practices.

Upstream, volatility in rubber and petrochemical inputs continues to impact production costs, prompting manufacturers to adopt multi-region sourcing and long-term procurement strategies.

Manufacturers are focusing on high-performance radial tyres, IF and VF technologies, and flotation designs that reduce soil compaction while improving productivity and fuel efficiency.

OEM integration remains strong, with tractor and agricultural equipment manufacturers increasingly partnering with tyre companies to deliver optimized factory-fit solutions aligned with performance and soil protection requirements.

The aftermarket remains the largest revenue contributor due to predictable replacement cycles linked to seasonal farming activities. Farmers and agribusinesses rely heavily on dealer networks and service providers for tyre replacement and maintenance.

Digital adoption is gradually emerging, with precision farming tools and sensor-enabled tyres enabling better monitoring of pressure, load, and soil impact.

Key Value Chain & Supply Chain Evolution Signals in Global Agricultural Tyres Market

Several structural trends are shaping the evolution of the agricultural tyres value chain.

First, increasing farm mechanization is driving consistent demand for high-performance tyres across developing and developed markets.

Second, the shift toward high-horsepower tractors and advanced machinery is increasing demand for tyres with higher load capacity and durability.

Third, soil protection has become a critical factor, accelerating adoption of radial, IF, and VF tyres that minimize soil compaction.

Fourth, aftermarket dominance continues due to seasonal wear and intensive field usage, reinforcing the importance of dealer networks and service accessibility.

Finally, sustainability and precision agriculture are influencing tyre innovation, including low-pressure systems, flotation designs, and emerging smart tyre technologies.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Agricultural Tyres Market

Leading manufacturers such as Michelin, Trelleborg, Bridgestone, and BKT benefit from strong OEM partnerships, global manufacturing capabilities, and advanced R&D focused on soil-friendly and high-flexion tyre technologies.

The specialized nature of agricultural tyres and the need for strong rural distribution networks create high entry barriers, supporting market consolidation among established players.

Farmers and agribusinesses are increasingly prioritizing total cost of ownership, driving demand for durable tyres with longer life cycles and improved fuel efficiency.

Manufacturers must balance raw material cost pressures with investments in advanced tyre technologies, including IF/VF designs and sustainable materials.

The transition toward precision and sustainable farming presents significant opportunities for innovation in soil protection, load optimization, and digital monitoring solutions.

Global Agricultural Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the agricultural tyres value chain is expected to become more technology-driven, sustainability-focused, and regionally optimized.

Manufacturers will increasingly invest in IF and VF tyre technologies, low-compaction designs, and environmentally sustainable materials to align with modern agricultural practices.

The aftermarket will remain the primary revenue driver, supported by recurring seasonal demand and equipment usage intensity.

Digital integration will expand gradually, with smart tyres and precision farming tools enabling better performance monitoring and resource optimization.

Overall, the future value chain will be shaped by mechanization, soil protection, and efficiency optimization, with innovation and distribution strength determining competitive advantage.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, carbon black, silica, steel cord sourcing

- Research & Development: Radial, IF & VF tyre design, soil protection engineering, flotation technology, smart tyre innovations

- Manufacturing: Compounding, moulding, curing, and durability testing for agricultural tyres

- OEM Integration: Supply of tyres to tractor, harvester, and agricultural equipment manufacturers

- Distribution & Dealer Network: Agricultural equipment dealers, rural distributors, and regional tyre retailers

- Aftermarket Services: Replacement tyres, farm equipment servicing, maintenance, and pressure optimization solutions

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, BKT (Balkrishna Industries)

- Research & Development: Michelin, Trelleborg (Yokohama Group), Nokian Tyres, Mitas (Yokohama Group)

- Manufacturing: Bridgestone Corporation, BKT, Apollo Tyres, CEAT Limited

- OEM Integration: Michelin, Trelleborg, Bridgestone Corporation, Mitas

- Distribution & Dealer Network: BKT, Apollo Tyres, CEAT Limited, Nokian Tyres

- Aftermarket Services: Michelin, Bridgestone Corporation, Trelleborg, BKT

Investment Activity

Global Agricultural Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Agricultural Tyres Market are driven by increasing farm mechanization, rising global food demand, and the transition toward sustainable agricultural practices. Between 2026 and 2033, capital allocation is expected to focus on advanced radial tyre technologies, high-flexion (IF & VF) tyres, and soil-protection solutions that enhance productivity while minimizing environmental impact.

The market demonstrates moderate capital intensity, with investments required in specialized rubber compounds, reinforced casing technologies, and precision tread engineering. Leading players such as Michelin, Bridgestone, Trelleborg, and BKT are continuously investing in R&D and expanding production capabilities to meet the evolving requirements of modern, high-horsepower agricultural machinery.

A key structural shift influencing funding is the growing emphasis on soil health and sustainable farming. This is accelerating investments in low-compaction tyres, flotation designs, and high-load capacity solutions that enable efficient operations without damaging soil structure.

Global Agricultural Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is supported by rising adoption of mechanized farming equipment and increasing demand for productivity-enhancing agricultural technologies. OEM partnerships with tractor and equipment manufacturers are a major focus area for tyre companies.

Europe leads as the largest investment hub, driven by advanced farming practices, high adoption of VF tyres, and strict environmental regulations promoting soil protection and efficiency.

Asia-Pacific is emerging as the fastest-growing investment region due to rapid mechanization in countries such as India and China. Government subsidies and rising farm incomes are encouraging investments in both OEM supply chains and aftermarket distribution networks.

North America remains a strong market for premium agricultural tyres, with investments concentrated in high-performance radial and high-flexion tyres designed for large-scale farming operations.

Latin America and the Middle East & Africa are witnessing gradual investment growth, supported by expanding commercial agriculture and increasing adoption of modern farming equipment.

Key Investment & Funding Dynamics Signals in Global Agricultural Tyres Market

A primary investment signal is the increasing global shift toward farm mechanization, which is driving demand for advanced agricultural tyres capable of supporting high-performance machinery.

The growing adoption of IF and VF tyres is another major signal, as farmers seek solutions that allow higher load capacity at lower inflation pressure while minimizing soil compaction.

Strong replacement demand driven by seasonal usage and harsh field conditions continues to ensure recurring revenue streams, encouraging sustained capital investment.

Sustainability trends, including soil conservation and fuel efficiency, are pushing investments toward innovative tyre designs that enhance productivity while reducing environmental impact.

Emerging digital agriculture practices are also creating opportunities for investment in smart and sensor-enabled tyres that support precision farming.

Strategic Implications of Investment & Funding Dynamics in Global Agricultural Tyres Market

The investment landscape favors established players with strong R&D capabilities and extensive distribution networks, creating high entry barriers for new participants.

OEM collaborations with agricultural equipment manufacturers are critical for securing long-term volume and strengthening market positioning.

The shift toward premium and high-flexion tyre technologies is increasing differentiation in the market, making innovation a key competitive factor.

Regional diversification is essential, with Europe leading in technology adoption, Asia-Pacific driving volume growth, and North America focusing on high-performance applications.

Volatility in raw material prices, particularly natural rubber and steel, continues to impact margins, necessitating strategic sourcing and cost optimization initiatives.

Global Agricultural Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Agricultural Tyres Market is expected to attract steady investment driven by increasing mechanization, rising food production needs, and growing adoption of sustainable farming practices.

Future capital allocation will prioritize IF and VF tyre technologies, low-compaction solutions, and high-durability designs capable of supporting next-generation agricultural equipment.

Asia-Pacific will continue to emerge as a key growth region, while Europe will lead innovation in sustainability-driven tyre technologies. North America will remain a strong market for premium and high-performance agricultural tyres.

Digital transformation in agriculture will further influence investment patterns, with increasing focus on smart tyres, data-driven farming solutions, and integrated equipment monitoring systems.

Overall, the market will maintain stable growth supported by its essential role in agricultural productivity. Companies that align innovation with sustainability and performance will be best positioned to lead the market through 2033.

Technology & Innovation

Global Agricultural Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global agricultural tyres market is driven by the need for enhanced traction, soil protection, load-bearing efficiency, and long-term durability. Agricultural tyres operate in highly variable conditions, including soft soil, uneven terrain, and heavy machinery loads, making innovation focused on balancing performance with minimal soil damage.

Innovation intensity in this market is moderate but steadily evolving, with strong advancements in radial construction, high-flexion tyre technologies, and advanced tread design. While traditional tyre architectures remain well-established, innovations in IF (Increased Flexion) and VF (Very High Flexion) tyres, along with improved compound engineering, are significantly enhancing operational efficiency and crop productivity. Leading companies such as Michelin, Bridgestone Corporation, Trelleborg (Yokohama Group), Continental AG, and BKT are focusing on soil-friendly, high-load, and precision farming-compatible tyre solutions.

A major technological shift is the adoption of high-flexion tyres that enable higher load capacity at lower inflation pressures, reducing soil compaction and improving yield outcomes. Additionally, emerging smart tyre technologies are supporting precision agriculture by enabling real-time monitoring of pressure, load, and field performance, helping farmers optimize operations.

Global Agricultural Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global agricultural tyres market is centered on improving soil protection, enhancing durability, and increasing operational efficiency. Manufacturers are refining tread patterns and rubber compounds to provide better grip, reduced slippage, and longer service life under demanding field conditions.

High-flexion tyre technology is a key area of advancement, allowing tyres to carry heavier loads at lower pressures. IF and VF tyres are increasingly adopted as they reduce soil compaction while maintaining traction and productivity, making them essential for modern high-horsepower farming equipment.

Durability-focused innovations are also prominent, with reinforced sidewalls, stronger carcass structures, and wear-resistant compounds designed to withstand rough terrain and seasonal usage patterns. These features help extend tyre lifespan and reduce replacement frequency.

Low soil compaction technologies, including wide-base and flotation tyres, are gaining traction as sustainable farming practices become more important. These tyres distribute weight more evenly, protecting soil structure and improving long-term agricultural productivity.

Smart and sensor-enabled tyre technologies are emerging in precision farming applications. Embedded sensors provide real-time data on tyre pressure and load conditions, enabling better decision-making and improving operational efficiency.

Manufacturing innovation is also advancing, with automation, precision engineering, and sustainable material usage improving product consistency and environmental performance. Increasing use of eco-friendly materials aligns with global sustainability goals.

Key Technology & Innovation Landscape Signals in Global Agricultural Tyres Market

- IF & VF High-Flexion Tyres: Rapid adoption of tyres capable of carrying higher loads at lower pressure to reduce soil compaction.

- Low Soil Compaction Solutions: Growing demand for flotation and wide-base tyres to protect soil health and improve yields.

- Advanced Radial Tyre Technology: Continued dominance of radial tyres offering better traction, fuel efficiency, and durability.

- Smart & Sensor-Enabled Tyres: Emergence of connected tyres supporting precision farming and real-time monitoring.

- Reinforced Structural Engineering: Enhanced carcass and sidewall designs for high-load agricultural machinery.

- Sustainable Material Innovation: Increasing use of eco-friendly and recycled materials in tyre manufacturing.

- Wear-Resistant Compound Development: Improved rubber formulations to extend tyre life and reduce operating costs.

Strategic Implications of Technology & Innovation Landscape in Global Agricultural Tyres Market

The evolving technology landscape has significant strategic implications for manufacturers and agricultural stakeholders. Continuous investment in R&D is essential to develop tyres that enhance productivity while minimizing environmental impact. Companies offering advanced high-flexion and soil-friendly solutions will gain a competitive advantage.

The shift toward precision and sustainable farming is reshaping product development priorities, with increasing demand for tyres that reduce soil compaction, improve fuel efficiency, and support high-performance machinery. This is driving collaboration between tyre manufacturers and agricultural equipment OEMs.

Smart tyre technologies are enabling data-driven farming practices by providing real-time insights into tyre performance and field conditions. This creates opportunities for value-added services and integrated farm management solutions.

Sustainability is becoming a central strategic focus, with emphasis on reducing environmental impact through eco-friendly materials, efficient production processes, and soil-preserving tyre designs. Companies aligning with these trends will strengthen their market positioning.

For farmers and fleet operators, advanced tyre technologies directly influence productivity, operational efficiency, and cost management. Adoption of innovative tyre solutions is critical for maximizing yields and minimizing long-term soil degradation.

Global Agricultural Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the global agricultural tyres market is expected to advance toward more efficient, sustainable, and intelligent tyre solutions. High-flexion tyre technologies will continue to dominate, driven by the need for higher productivity and soil preservation.

Smart tyre systems are expected to gain wider adoption, integrating with precision farming platforms to enable real-time monitoring, predictive analytics, and optimized field operations.

Material innovation will continue to evolve, focusing on durable, flexible, and environmentally sustainable compounds that enhance performance while reducing ecological impact.

Manufacturing processes will become increasingly automated and digitally integrated, improving production efficiency, scalability, and product quality. Advanced manufacturing technologies will accelerate innovation cycles.

In conclusion, the Global Agricultural Tyres Market is undergoing steady technological transformation driven by mechanization, sustainability, and precision agriculture. Soil protection, high-load performance, and smart integration will remain the core innovation pillars, with companies that successfully deliver these capabilities best positioned to lead the market through 2033.

Market Risk

Global Agricultural Tyres Market Risk Factors & Disruption Threats Overview

The Global Agricultural Tyres Market operates in a stable yet evolving environment, driven by farm mechanization, rising food demand, and increasing adoption of advanced farming technologies. While the market benefits from steady replacement demand and essential usage, it carries a moderate risk profile due to raw material dependency, seasonal demand variability, and pricing sensitivity among farmers. A key structural risk is volatility in raw material prices, particularly natural rubber, synthetic compounds, and steel cords. Agricultural tyres operate in a price-sensitive ecosystem, where farmers often prioritize cost over premium features, limiting manufacturers’ ability to pass on cost increases. Another disruption factor is the fragmented and price-driven customer base. Unlike fleet markets, agricultural buyers are highly dispersed, making demand less predictable and increasing reliance on dealer networks and seasonal purchasing cycles. Operational risks also arise from harsh working conditions. Agricultural tyres are exposed to uneven terrain, heavy loads, and extreme weather, increasing wear and failure risks and putting pressure on manufacturers to deliver highly durable and reliable products. Additionally, the increasing shift toward high-horsepower machinery and advanced farming practices is reshaping tyre requirements, requiring continuous innovation in load-bearing capacity, traction, and soil protection capabilities.

Global Agricultural Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects steady growth supported by increasing mechanization, government subsidies, and rising global food demand. However, this growth is accompanied by cost pressures, uneven regional demand, and evolving technology requirements. Raw material cost fluctuations continue to impact manufacturing margins, especially in emerging markets where price sensitivity is high and premium tyre adoption is limited. The aftermarket segment dominates due to seasonal usage and high wear rates during peak farming periods. However, demand remains cyclical and dependent on factors such as crop prices, weather conditions, and farm income levels. Supply chain challenges, including sourcing of rubber and logistics in rural areas, can impact product availability and distribution efficiency, particularly in developing markets. At the same time, adoption of advanced tyres such as radial, IF, and VF variants is increasing, particularly in Europe and North America, creating a dual market structure between premium and cost-sensitive segments.

Key Risk Factors & Disruption Threats Signals in Global Agricultural Tyres Market

A major risk signal is the increasing adoption of high-horsepower tractors and heavy agricultural equipment. This trend is driving demand for high-load and high-flexion tyres, requiring continuous product innovation. The shift toward precision and sustainable farming is another key signal. Farmers are increasingly focusing on soil protection and efficiency, accelerating demand for low-compaction and flotation tyres. Volatility in farm incomes due to fluctuating crop prices and climate conditions directly impacts purchasing behavior, influencing both OEM and replacement demand. Technological advancements in agricultural equipment are also influencing tyre design, pushing manufacturers to align with evolving machinery requirements. Additionally, gradual adoption of smart farming technologies is signaling future demand for sensor-enabled tyres capable of providing real-time performance and pressure data.

Strategic Implications of Risk Factors & Disruption Threats in Global Agricultural Tyres Market

Manufacturers must prioritize durability, traction, and soil protection to address the demanding conditions of agricultural operations. Product performance directly impacts farm productivity, making reliability a key differentiator. Expanding rural distribution networks and strengthening dealer relationships are critical to capturing fragmented demand and ensuring market penetration, particularly in emerging economies. Investment in advanced tyre technologies such as IF and VF tyres is essential to align with modern farming requirements and premium market segments. Cost optimization and raw material sourcing strategies are necessary to manage pricing pressures and maintain margins in a highly price-sensitive market. Furthermore, integrating digital and smart features into tyres can provide long-term competitive advantage as precision agriculture adoption increases.

Global Agricultural Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Agricultural Tyres Market is expected to grow steadily, supported by increasing mechanization, rising global food demand, and technological advancements in farming practices. However, the risk environment will remain influenced by economic, environmental, and technological factors. Demand for advanced tyres such as radial, IF, and VF variants will continue to rise, driven by the need for higher efficiency and reduced soil compaction. Sustainability and soil preservation will play a larger role in shaping tyre innovation, pushing manufacturers toward eco-friendly and low-impact designs. Emerging markets, particularly in Asia-Pacific, will present strong growth opportunities but will also require cost-effective solutions tailored to price-sensitive customers. Overall, the market will remain stable but competitive, with success dependent on balancing cost efficiency, durability, and technological advancement while adapting to evolving agricultural practices and regional demand dynamics.

Regulatory Landscape

Global Agricultural Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Agricultural Tyres Market plays a vital role in shaping product standards, farm productivity, and environmental sustainability. Agricultural tyres directly influence soil health, fuel efficiency, and operational performance of farm machinery, prompting governments and regulatory bodies to establish frameworks focused on safety, durability, and soil conservation.

Key regulatory frameworks such as the European Union Tyre Labelling Regulation (EU) 2020/740 and UNECE tyre safety standards define performance benchmarks related to rolling resistance, durability, and environmental impact. While agricultural tyres are less consumer-facing than passenger tyres, these standards increasingly influence OEM specifications and premium product development, especially for high-horsepower machinery.

In addition, agricultural and environmental policies are driving adoption of soil-protection technologies. Governments and agricultural agencies are promoting sustainable farming practices, encouraging the use of low-compaction tyres such as radial, IF (Increased Flexion), and VF (Very High Flexion) tyres that minimize soil damage and improve crop yield.

Emerging economies including India, China, and Brazil are strengthening regulatory oversight through farm mechanization programs, equipment subsidies, and quality certification systems. These initiatives are improving tyre standardization, supporting adoption of advanced agricultural tyres, and reinforcing structured replacement demand in rural markets.

Global Agricultural Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is shaped by increasing emphasis on sustainable agriculture, soil conservation, and efficient resource utilization. Europe leads in regulatory maturity, where strict environmental policies and soil protection guidelines strongly influence tyre adoption patterns.

In Europe, regulations and sustainability programs encourage farmers to adopt low soil compaction technologies, accelerating demand for radial and high-flexion tyres. Subsidies and incentives for sustainable farming equipment further support adoption of premium agricultural tyres.

In Asia-Pacific, governments are actively promoting farm mechanization through subsidies and rural development programs. Countries like India and China are focusing on improving agricultural productivity, which is increasing demand for durable, high-performance tyres compatible with modern farm equipment.

North America remains a technology-driven market, where precision farming practices and large-scale mechanized agriculture drive demand for advanced tyre solutions. Regulatory focus on efficiency and sustainability is encouraging adoption of fuel-efficient and long-life tyres.

Globally, increasing adoption of smart farming and connected equipment is beginning to influence regulatory frameworks, introducing early-stage standards for sensor-enabled and performance-optimized agricultural tyres.

Key Regulatory & Policy Environment Signals in Global Agricultural Tyres Market

- EU Tyre Labelling Regulation (EU 2020/740): Influences performance standards related to fuel efficiency and environmental impact.

- UNECE Tyre Safety Standards: Establish benchmarks for durability, load capacity, and structural integrity.

- Soil Conservation Policies: Promote adoption of low-compaction tyres such as radial, IF, and VF tyres.

- Farm Mechanization Subsidy Programs: Encourage adoption of advanced agricultural machinery and compatible tyre technologies.

- Sustainable Agriculture Initiatives: Support use of fuel-efficient and environmentally friendly tyre solutions.

- Rural Infrastructure & Modernization Policies: Improve access to high-quality tyres and support aftermarket growth.

Strategic Implications of Regulatory & Policy Environment in Global Agricultural Tyres Market

The regulatory environment creates moderate entry barriers, favoring established manufacturers with strong R&D capabilities and distribution networks in rural and agricultural markets. Compliance with durability, performance, and environmental standards is becoming increasingly important.

Innovation driven by regulatory and sustainability requirements is shaping competition. Manufacturers are investing in high-flexion tyre technologies, advanced tread designs, and materials that reduce soil compaction while improving load capacity and fuel efficiency.

Farmers and agricultural enterprises are increasingly influenced by government incentives and sustainability guidelines, shifting purchasing decisions toward premium tyres that deliver higher productivity and long-term cost benefits.

Regional variations in agricultural policies are also shaping market strategies, encouraging localization of manufacturing, partnerships with farm equipment OEMs, and expansion of rural distribution and service networks.

Global Agricultural Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory landscape is expected to become more sustainability-focused, driven by global food security concerns, climate change policies, and soil preservation initiatives. Governments will increasingly promote technologies that enhance agricultural productivity while minimizing environmental impact.

Europe is expected to strengthen soil health and environmental compliance regulations, while Asia-Pacific will expand mechanization and subsidy programs to improve farm efficiency. These developments will accelerate adoption of advanced tyre technologies across both regions.

The growing adoption of precision agriculture and smart farming will introduce new regulatory considerations related to data integration, performance monitoring, and optimized equipment usage, creating opportunities for sensor-enabled agricultural tyres.

Overall, the regulatory environment will act as a long-term growth enabler, encouraging innovation in soil-friendly, high-efficiency, and durable tyre solutions. Manufacturers that align with sustainability goals and invest in advanced flexion and smart tyre technologies will be best positioned to lead the Global Agricultural Tyres Market through 2033.