Global Tyre Retreading Market size , share & Forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

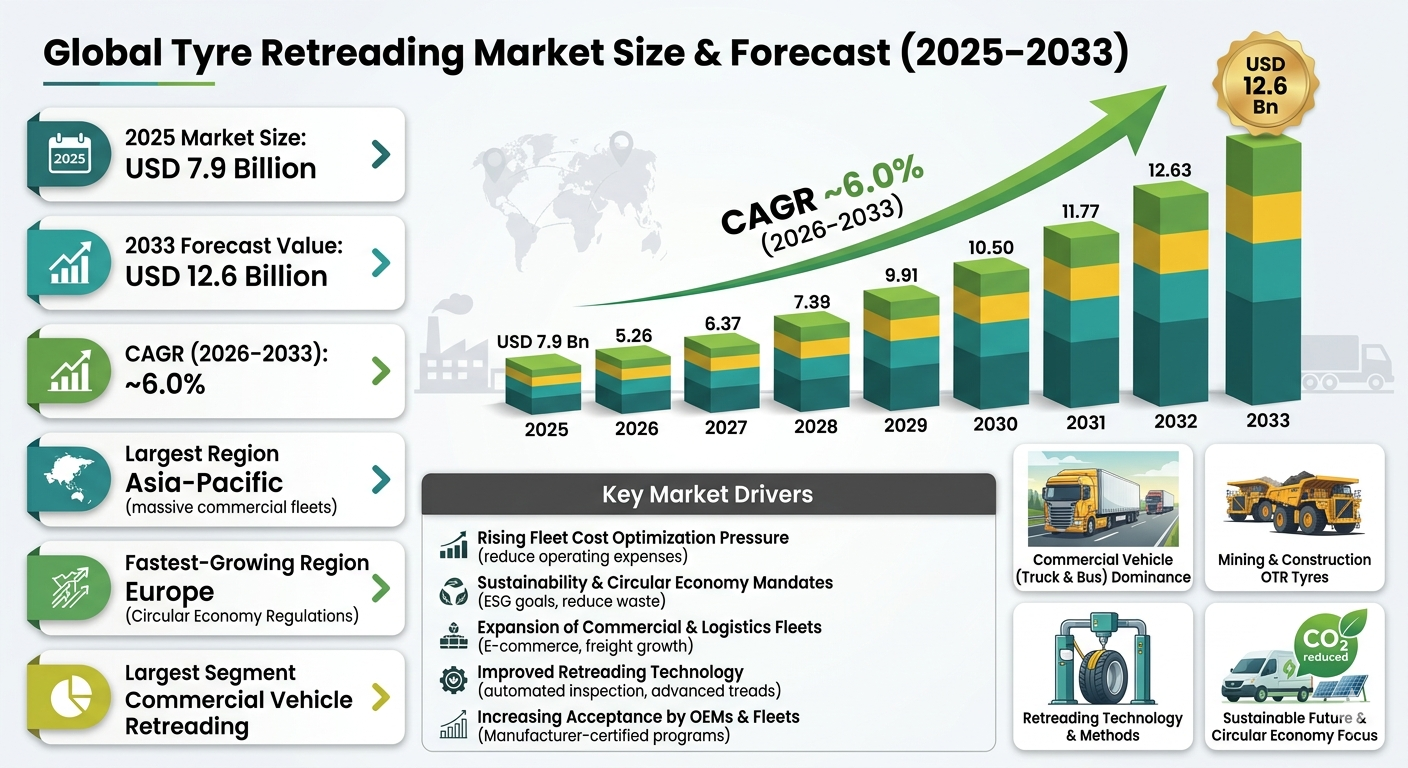

| 2025 Market Size | USD 7.9 Billion |

| 2033 Market Size | USD 12.6 Billion |

| CAGR (2026???2033) | ~6.0% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Commercial vehicle retreading |

| Fastest-Growing Segment | Multi-life & OEM-certified retreading |

| Key Trend | Circular economy & TCO optimization |

Global Tyre Retreading Market Overview

The Global Tyre Retreading Market is all about giving worn tyres a second life by swapping out the tread while keeping the original casing???super cost-efficient.?? It???s big in commercial vehicles, aviation, off-road gear, buses, and fleets where tyres can be a major expense. Instead of buying new every time, retreading saves money and reduces waste.

Retreading saves 30???50% compared to new tyres, uses way less raw material, and cuts carbon emissions???so it???s both wallet-friendly and eco-smart . Fleet operators love it because it slashes total cost of ownership and helps hit sustainability goals. It???s basically a win-win: cheaper for business, better for the planet.

The Global Tyre Retreading Market is dominated by commercial vehicle and OTR tyre retreading, where durable casings and predictable wear patterns make multi-life usage feasible. Passenger vehicle retreading remains limited due to safety perception and regulatory constraints in some regions, while truck, bus, aviation, and mining tyres often undergo multiple retreading cycles.

According to the Pheonix Demand Forecast Engine, the Global Tyre Retreading Market size is valued at USD 7.9 billion in 2025 and is projected to reach USD 12.6 billion by 2033, expanding at a CAGR of ~6.0% during the forecast period (2026???2033).

Asia-Pacific represents the largest retreading market due to cost sensitivity and massive commercial fleets, while Europe is the fastest-growing region, supported by sustainability regulations and circular economy policies.

Key Drivers of Global Tyre Retreading Market Growth

Rising Fleet Cost Optimization Pressure

Fuel, tyres, and maintenance are major cost centers for fleets, making retreading a preferred solution to reduce operating expenses.

Sustainability & Circular Economy Mandates

Retreading reduces waste, raw material usage, and CO??? emissions, aligning with ESG and regulatory goals.

Expansion of Commercial & Logistics Fleets

Growth in freight transport, e-commerce, and public transportation increases demand for cost-efficient tyre lifecycle management.

Improved Retreading Technology

Advanced tread compounds, automated buffing, and inspection technologies have improved retread performance and safety.

Increasing Acceptance by OEMs & Fleets

OEM???approved retreading programs and fleet warranties are boosting market growth , improving confidence and adoption across operators.

Global Tyre Retreading Market Segmentation

1. By Vehicle Category

1.1 Commercial Vehicles??

1.1.1 Trucks

1.1.1.1 Long-Haul Trucks1.1.1.2 Regional & Distribution Trucks

1.1.2 Buses

1.1.2.1 City Buses

1.1.2.2 Intercity & Coach Buses

1.2 Off-the-Road (OTR) Vehicles

1.2.1 Construction Equipment

1.2.1.1 Dump Trucks1.2.1.2 Loaders

1.2.2 Mining Equipment

1.2.2.1 Haul Trucks

1.2.2.2 Underground Mining Vehicles

1.3 Aviation??

1.3.1 Commercial Aircraft

1.3.1.1 Narrow-Body Aircraft 1.3.1.2 Wide-Body Aircraft1.3.2 Military & Cargo Aircraft

1.4 Passenger Vehicles

1.4.1 Taxis & Fleet Cars

??1.4.1.1 Corporate Fleet Vehicles

??1.4.1.2 Limited Adoption Compared to Commercial Vehicles

2. By Retreading Method

2.1 Pre-Cure Retreading??

2.1.1 Cold-Cure Retreading

??2.1.1.1 Molded Tread Strips

??2.1.1.2 Cushion Gum Bonding

2.1.2 Patterned Pre-Cure Treads

??2.1.2.1 Highway Tread Patterns

??2.1.2.2 Regional Tread Patterns

2.2 Mold-Cure Retreading

2.2.1 Hot-Cure Retreading

2.2.1.1 Customized Tread Designs

??2.2.2 Full-Mold Retreading

2.2.2.1 OEM-Style Tread Replication

3. By Tyre Type

3.1 Radial Tyres (Dominant Segment)

3.1.1 Steel-Belted Radial Tyres

3.1.1.1 Truck & Bus Radial Tyres

3.1.2 Fabric-Belted Radial Tyres

3.2 Bias (Cross-Ply) Tyres

3.2.1 Heavy-Duty Bias Tyres

3.2.1.1 OTR & Mining Tyres

4. By Number of Retread Cycles

4.1 Single-Life Retread

4.1.1 Entry-Level Fleet Retreads

4.2 Multi-Life Retread (Fastest-Growing Segment)

4.2.1 Two-Life Retread Tyres

4.2.1.1 Regional Transport Fleets

4.2.2 Three-Life Retread Tyres

4.2.2.1 Long-Haul & Mining Operations

5. By Sales & Service Model

5.1 Independent Retreading Facilities

5.1.1 Local Retreaders

5.1.1.1 Small- & Mid-Scale Operators

5.2 OEM & Brand-Owned Retreading (Fastest-Growing Segment)

5.2.1 Manufacturer-Certified Retreading Programs

5.2.1.1 Michelin Remix

5.2.1.2 Bridgestone Bandag

5.3 Fleet-Owned Retreading Facilities

5.3.1 In-House Fleet Retreading

5.3.1.1 Mining & Logistics Majors

6. By Geography

6.1 Asia-Pacific (Largest Region)

China

India

Japan

Southeast Asia

6.2 Europe (Fastest-Growing Region)

Germany

France

U.K.

Italy

6.3 North America

United States

Canada

6.4 Latin America

Brazil

Mexico

6.5 Middle East & Africa

Regional Insights of Global Tyre Retreading Market

Asia-Pacific ??? Largest Market

High cost sensitivity, expanding logistics fleets, and widespread acceptance of retreaded truck tyres drive strong demand.

Europe ??? Fastest Growing

Circular economy regulations, landfill restrictions, and OEM-certified retreading programs support rapid growth.

North America

Strong trucking industry, long-haul transport, and brand-backed retreading networks dominate demand.

Latin America

Economic pressures and expanding freight activity support retreading adoption.

Middle East & Africa

Mining, construction, and extreme operating conditions make retreading economically attractive.

Leading Companies in the Global Tyre Retreading Market

Bridgestone Corporation (Bandag)

Michelin (Michelin Remix)

Goodyear Tire & Rubber Company

Continental AG

Marangoni

Treadsetters

Kal Tire

Vipal Rubber

Marathon Tyres

Bridgestone Corporation (Bandag) is the largest company in the Global Tyre Retreading Market

Why the Tyre Retreading Market Is Critical

-

Enables significant cost savings for fleets

-

Reduces tyre waste and raw material usage

-

Supports ESG, sustainability, and circular economy goals

-

Extends tyre casing lifecycle and improves asset utilization

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Tracks fleet growth, mileage accumulation, and retread penetration.

Casing Life Assessment Model

Evaluates casing durability and multi-life retreading potential.

Fleet TCO Optimization Engine

Quantifies cost-per-kilometer advantages of retreading.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate

-

Supplier Power: Low???Moderate

-

Threat of New Entrants: Moderate

-

Threat of Substitutes: Low

-

Competitive Rivalry: Moderate

Final Takeaway of Global Tyre Retreading Market

The Global Tyre Retreading Market is transitioning from a purely cost-driven practice to a strategic, sustainability-led fleet solution. With rising logistics activity, tighter margins, and regulatory pressure to reduce environmental impact, retreading will remain a vital growth lever through 2033. Manufacturers and service providers that invest in OEM-certified programs, advanced inspection technology, and fleet-integrated service models will capture the greatest long-term value.

Competitive Landscape

Global Tyre Retreading Competitive Intensity & Market Structure Overview

The Global Tyre Retreading Market is characterized by a cost-efficiency-driven, sustainability-focused, and fleet-centric competitive landscape, where commercial economics, casing quality, and lifecycle optimization define market success. Unlike new tyre markets that rely heavily on OEM production and consumer upgrades, the retreading market is structurally centered on maximizing tyre asset utilization across commercial vehicles, aviation, mining, and heavy-duty fleets. The market operates through a hybrid structure comprising independent retreaders, OEM-certified retreading networks, and fleet-owned in-house retreading facilities. Competitive intensity is moderate to high, shaped by technology quality, casing durability, regulatory compliance, and trust in retread performance. While independent operators maintain strong regional relevance, OEM-backed programs are increasingly strengthening market share through quality assurance and fleet confidence. Market concentration is moderate, with major global tyre manufacturers leveraging brand-backed retreading ecosystems such as Bandag and Michelin Remix, while local and regional retreaders continue to compete aggressively in cost-sensitive markets. The market’s strategic foundation is increasingly tied to circular economy policies, total cost of ownership (TCO) optimization, and sustainable fleet management.

Global Tyre Retreading Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Bridgestone Corporation (Bandag): Global market leader with one of the most established retreading ecosystems, strong fleet partnerships, and advanced commercial retread programs. Michelin (Michelin Remix): Premium retreading innovator focused on OEM-certified multi-life casing programs and sustainability-led fleet optimization. Goodyear Tire & Rubber Company: Strong presence in commercial fleet retreading with integrated service networks and performance-focused solutions. Continental AG: Technology-driven player with emphasis on casing quality, digital inspection, and fleet lifecycle solutions. Marangoni: Specialized retreading technology provider with strong international footprint in tread materials and systems. Vipal Rubber: Major independent retread material supplier with broad global presence in pre-cure tread markets. Kal Tire: Strong OTR and mining retreading specialist with operational strength in extreme-duty sectors. Treadsetters: Regional commercial retreading player focused on fleet and transport economics. Marathon Tyres: Value-oriented participant serving cost-sensitive fleet and regional transport segments.

Key Competitive Intensity & Market Structure Signals in Global Tyre Retreading Market

A major structural signal is the dominance of commercial vehicle fleets, where tyre operating costs significantly impact profitability. This makes retreading a strategic fleet management tool rather than a discretionary purchase. Another critical signal is the growing shift toward OEM-certified retreading programs, which improve trust, warranty protection, and standardized performance. This trend is increasing consolidation around major brand-backed ecosystems. Casing durability has become a strategic differentiator, as higher-quality original tyres support multiple retread cycles and stronger lifetime economics. This is intensifying focus on casing management technologies and inspection systems. Sustainability and circular economy mandates are reshaping market dynamics, particularly in Europe, where waste reduction and resource efficiency policies are accelerating adoption of retreaded tyres.

Strategic Implications of Competitive Intensity & Market Structure in Global Tyre Retreading Market

Manufacturers and retread providers must prioritize casing lifecycle management, as durable, retread-friendly tyre architecture directly influences profitability and competitive advantage. OEM-certified retreading is becoming a strategic growth pillar, offering stronger brand trust, better fleet retention, and premium pricing opportunities compared to purely independent operators. Technology investments in automated inspection, buffing precision, tread quality, and digital fleet monitoring are increasingly necessary to improve safety perception and operational consistency. Fleet integration strategies are critical, particularly for logistics, mining, and bus operators seeking predictable cost-per-kilometer optimization. Providers that bundle retreading with broader fleet tyre management services will secure stronger long-term contracts.

Global Tyre Retreading Competitive Intensity & Market Structure Forward Outlook

The Global Tyre Retreading Market is expected to witness sustained expansion as cost pressures, sustainability mandates, and fleet optimization priorities intensify globally. Competitive intensity will increasingly shift from price-only competition toward quality assurance, OEM certification, and digital lifecycle management capabilities. Market consolidation is likely to strengthen around major global tyre brands and organized retreading ecosystems, while smaller independent operators may remain competitive in regional, price-sensitive niches. In the long term, the market will be shaped by three strategic pillars: OEM-certified retreading, multi-life casing optimization, and circular economy integration. Companies that align with these trends will lead the Global Tyre Retreading Market through 2033.

Value Chain

Global Tyre Retreading Market Value Chain & Supply Chain Evolution Overview

The Global Tyre Retreading Market value chain is evolving from a traditional cost-saving aftermarket practice into a strategic circular economy ecosystem centered on lifecycle extension, fleet efficiency, and sustainability optimization. Retreading transforms worn tyres into reusable assets by preserving the casing and replacing the tread, significantly reducing raw material consumption, lowering carbon emissions, and improving total cost of ownership (TCO) for fleets. This positions tyre retreading as a critical component of commercial mobility economics and ESG-aligned transportation systems. The retreading value chain spans casing procurement, inspection and testing, tread compound development, retreading process technologies, OEM-certified retread programs, fleet lifecycle management, and end-of-life casing recovery. Unlike new tyre manufacturing, retreading places exceptional emphasis on casing quality, durability analytics, and multi-life asset utilization. Upstream supply chain operations depend heavily on high-quality used tyre casings, rubber compounds, tread materials, bonding agents, inspection systems, and retreading machinery. Leading players such as Bridgestone (Bandag), Michelin Remix, Goodyear, and Marangoni are increasingly building integrated retreading ecosystems combining casing management, OEM certification, and fleet service partnerships. Manufacturing focuses on casing inspection, buffing, tread application, curing, and quality assurance. Advanced retreading increasingly uses automated inspection technologies, shearography, RFID tracking, digital casing analytics, and OEM-grade tread engineering to improve safety, performance, and repeatability. Distribution is primarily fleet-driven, including logistics operators, trucking fleets, bus fleets, mining companies, aviation operators, and OTR users. OEM-certified retreading networks are expanding rapidly as trust, warranty coverage, and lifecycle economics become increasingly important. Supply chain challenges include casing availability, quality consistency, safety perception, regulatory compliance, retread acceptance barriers in passenger segments, and balancing retread affordability with premium performance expectations.

Global Tyre Retreading Market Value Chain & Supply Chain Evolution Current Scenario

The current market is shaped by growing fleet cost pressures, sustainability mandates, logistics expansion, and circular economy priorities. Upstream, high-quality casing preservation is becoming increasingly strategic, with fleet operators and OEM programs focusing on maximizing casing durability from first-life tyre selection onward. Retreading technologies are shifting toward automation, precision inspection, digital traceability, and OEM-certified quality systems that enhance trust and performance. Commercial vehicle fleets remain the dominant market, particularly in trucking, buses, aviation, mining, and OTR applications where predictable tyre wear and casing reuse economics are strongest. OEM and branded retreading programs are increasingly replacing fragmented local retreaders in premium segments due to stronger quality assurance, warranty support, and lifecycle management. Sustainability reporting and ESG compliance are increasingly strengthening retreading’s strategic role as fleets seek measurable carbon and waste reduction.

Key Value Chain & Supply Chain Evolution Signals in Global Tyre Retreading Market

Several major structural trends are reshaping the tyre retreading ecosystem. First, circular economy integration is elevating retreading from cost optimization to sustainability infrastructure. Second, OEM-certified retreading programs are expanding rapidly, improving trust, standardization, and premium adoption. Third, digital casing analytics and predictive lifecycle management are improving retread eligibility and maximizing casing utilization. Fourth, fleet-integrated service contracts are driving retreading adoption through cost-per-kilometer optimization. Fifth, sustainability regulations and landfill reduction policies are increasing strategic demand for retreaded tyres.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Tyre Retreading Market

Leading companies such as Bridgestone Bandag, Michelin Remix, Goodyear, Continental, and Marangoni are strengthening market leadership through integrated casing ecosystems, certified retreading networks, and fleet partnerships. Supply chain resilience increasingly depends on casing availability, inspection precision, and consistent tread quality. Companies with strong OEM trust, digital inspection capabilities, and fleet service integration are better positioned to capture premium retreading opportunities. Multi-life retreading capabilities are emerging as a major competitive differentiator, particularly for long-haul trucking, aviation, and mining sectors. Long-term competitiveness will increasingly rely on combining affordability, safety, sustainability, and lifecycle data transparency.

Global Tyre Retreading Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the tyre retreading value chain is expected to become more digitized, OEM-integrated, and sustainability-driven. Manufacturers will increasingly prioritize multi-life retreading, predictive casing intelligence, advanced automation, and circular fleet service ecosystems. Fleet partnerships will deepen as logistics, freight, and aviation sectors increasingly focus on cost optimization and ESG outcomes. OEM-certified retreading programs will expand globally, particularly in premium trucking, mining, and commercial vehicle categories. Digital traceability, RFID-enabled lifecycle monitoring, and AI-powered casing analysis will become increasingly important for maximizing retread value. Ultimately, the future retreading value chain will evolve from simple tread replacement toward lifecycle-managed tyre asset optimization ecosystems.

Market-Specific Value Chain

- Casing Procurement & Recovery: Used tyre collection, casing inspection, fleet casing management, OEM casing selection

- Research & Development: Retread compounds, tread design, casing durability analytics, inspection technology, multi-life optimization

- Retreading Manufacturing: Buffing, tread application, curing, automated inspection, OEM-certified retread production

- Fleet & OEM Integration: Commercial fleets, trucking, aviation, mining, OEM retread certification programs

- Distribution & Service: Independent retreaders, OEM retread networks, fleet contracts, lifecycle service providers

- End-of-Life & Circular Economy Services: Final recycling, casing disposal, reclaimed rubber recovery, sustainability reporting

Company-to-Stage Mapping

- Casing Procurement & Recovery: Bridgestone Bandag, Michelin Remix, Goodyear Tire & Rubber Company, Kal Tire

- Research & Development: Michelin, Bridgestone Corporation, Continental AG, Marangoni

- Retreading Manufacturing: Bridgestone Bandag, Michelin Remix, Vipal Rubber, Marathon Tyres

- Fleet & OEM Integration: Bridgestone Corporation, Michelin, Goodyear Tire & Rubber Company, Kal Tire

- Distribution & Service: Treadsetters, Vipal Rubber, independent retreading facilities, OEM-certified retread networks

- End-of-Life & Circular Economy Services: Michelin, Bridgestone Corporation, recycling ecosystem partners, reclaimed rubber processors

Investment Activity

Global Tyre Retreading Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Tyre Retreading Market are being shaped by rising fleet cost pressures, circular economy mandates, ESG priorities, and increasing demand for total cost of ownership (TCO) optimization across commercial transport ecosystems. Between 2026 and 2033, capital allocation is expected to increasingly prioritize OEM-certified retreading platforms, advanced casing inspection technologies, multi-life tyre programs, automated retreading systems, and sustainable fleet lifecycle management infrastructure.

The market is highly cost-efficiency and operational performance driven, requiring continuous investment in casing durability analytics, automated buffing systems, tread engineering, digital inspection tools, and scalable retread service networks. Leading players such as Bridgestone (Bandag), Michelin (Remix), Goodyear, Continental, and Marangoni are significantly expanding investments in certified retreading ecosystems, fleet-integrated retread contracts, and circular tyre lifecycle solutions.

A major structural transformation influencing investment patterns is the shift of retreading from a low-cost aftermarket alternative into a strategic sustainability and asset optimization solution. This evolution is directing funding toward premium retreading quality, lifecycle extension, and integrated tyre service ecosystems that maximize casing utilization and operational savings.

Global Tyre Retreading Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by logistics fleet expansion, e-commerce transportation growth, rising raw material costs, and global sustainability regulations. Fleet operators and OEM-backed retreading providers are increasingly prioritizing long-term lifecycle contracts over one-time tyre purchases.

- Asia-Pacific: Leads global investment activity due to cost-sensitive commercial fleets, expanding freight demand, and broad retread adoption across logistics and public transportation sectors.

- Europe: Fastest-growing investment region, driven by circular economy mandates, landfill restrictions, sustainability frameworks, and premium OEM-certified retreading programs.

- North America: Strong investment momentum supported by large trucking networks, long-haul fleet economics, and established brand-backed retreading ecosystems.

- Latin America & Middle East & Africa: Emerging growth markets fueled by freight expansion, mining operations, and economic pressure to optimize tyre lifecycle costs.

Key Investment & Funding Dynamics Signals in Global Tyre Retreading Market

- Rising fleet TCO optimization pressure is increasing capital inflows into retread infrastructure, casing life extension systems, and lifecycle management solutions.

- Growing sustainability mandates are accelerating investments in circular tyre systems that reduce waste, raw material consumption, and carbon emissions.

- Expansion of OEM-certified retreading programs is driving funding into premium retread quality assurance, warranty systems, and dealer network integration.

- Advancements in automated casing inspection, digital tread design, and predictive maintenance are creating technology-led investment opportunities.

- Increasing adoption of multi-life retreading strategies is strengthening investor confidence in long-term recurring revenue models.

Strategic Implications of Investment & Funding Dynamics in Global Tyre Retreading Market

- The investment landscape strongly favors players with durable casing technologies, certified retreading quality systems, and fleet contract integration capabilities.

- Strategic partnerships with logistics operators, mining fleets, public transport systems, and OEM tyre brands are becoming critical growth drivers.

- Technological differentiation increasingly centers on casing analytics, retread safety validation, and multi-life performance optimization.

- Regional diversification remains essential, with Asia-Pacific leading cost-led adoption, Europe driving sustainability innovation, and North America emphasizing scale and operational efficiency.

- Perception barriers, regulatory compliance, and casing quality consistency remain strategic priorities for sustained capital deployment.

Global Tyre Retreading Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Tyre Retreading Market is expected to attract steady and strategic investment as retreading becomes a critical pillar of commercial fleet sustainability, circularity, and operational efficiency.

Future capital allocation will increasingly prioritize AI-enabled casing diagnostics, multi-life retread systems, OEM-backed premium retreading ecosystems, fleet-as-a-service models, and carbon-reduction focused tyre lifecycle programs.

- Asia-Pacific: Will remain the dominant investment hub due to large commercial fleet volumes, cost pressures, and growing logistics demand.

- Europe: Will continue leading innovation in sustainability-led retreading systems, circular economy frameworks, and premium certified retread solutions.

- North America: Will expand investments in long-haul fleet retreading, mining applications, and advanced service network integration.

Digital fleet analytics, predictive casing management, and lifecycle sustainability measurement tools will increasingly shape funding priorities across the market.

Overall, the market will maintain stable growth through 2033, supported by its essential role in cost reduction, sustainability, and commercial tyre lifecycle optimization. Companies that align OEM certification, advanced retreading technology, fleet partnerships, and circular economy integration will be best positioned to capture long-term value in the evolving global tyre ecosystem.

Technology & Innovation

Global Tyre Retreading Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global tyre retreading market is increasingly centered on lifecycle extension, casing optimization, sustainability, and fleet total cost of ownership (TCO) enhancement. Unlike new tyre manufacturing, retreading innovation focuses on maximizing the economic and structural value of existing tyre casings while improving safety, performance consistency, and environmental efficiency. As fleets prioritize cost reduction and ESG alignment, retreading is evolving from a low-cost alternative into a strategic circular economy solution. Innovation intensity in the tyre retreading market is moderate to high, driven by advances in casing inspection systems, automated buffing, precision tread application, advanced curing processes, and OEM-certified retread programs. Major players such as Bridgestone Corporation (Bandag), Michelin (Michelin Remix), Goodyear Tire & Rubber Company, Continental AG, and Marangoni are investing in retread quality standardization and multi-life tyre programs to improve performance parity with new tyres. A major technological shift is the emergence of intelligent casing management and multi-life retreading ecosystems, where advanced diagnostics, digital tyre history tracking, and predictive casing analysis enable safer and more efficient repeat retreading cycles. Simultaneously, sustainable tread compounds, automated manufacturing systems, and retread certification standards are strengthening confidence among fleets, logistics operators, and industrial users.

Global Tyre Retreading Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global tyre retreading market is focused on enhancing retread reliability, extending casing lifespan, and improving cost-per-kilometer performance. Manufacturers and retread service providers are prioritizing technologies that ensure retreaded tyres deliver safety, durability, and operational consistency comparable to premium new tyres. Advanced casing inspection technologies are a major innovation pillar. Shearography, X-ray scanning, ultrasonic diagnostics, and AI-assisted casing analytics are increasingly used to detect structural weaknesses before retreading, significantly improving safety standards and reducing failure rates. Automated buffing and precision tread application systems are transforming production consistency. CNC-controlled buffing machines, robotic tread builders, and advanced bonding systems reduce human error and improve tread uniformity, particularly in high-volume commercial tyre retreading. Multi-life retreading innovation is accelerating through stronger casing materials and better casing lifecycle analytics. Commercial truck, bus, mining, and aviation tyres are increasingly designed for multiple retread cycles, significantly lowering lifecycle cost and reducing raw material demand. OEM-certified retreading programs are reshaping market perception by offering standardized performance, warranty-backed solutions, and quality assurance. Programs such as Michelin Remix and Bridgestone Bandag are elevating retread adoption beyond price-sensitive markets. Sustainable material innovation is also expanding, with improved tread compounds, recycled rubber integration, lower-emission curing systems, and circular manufacturing models supporting broader ESG goals. Digital fleet integration is emerging as a growing innovation area, where tyre tracking software, RFID tagging, and predictive maintenance platforms help fleets optimize retread timing and casing utilization.

Key Technology & Innovation Landscape Signals in Global Tyre Retreading Market

- Advanced Casing Inspection Systems: AI, shearography, and X-ray technologies are improving safety and retread eligibility assessment.

- OEM-Certified Retreading Programs: Brand-backed retread ecosystems are strengthening trust and premium adoption.

- Multi-Life Tyre Platforms: Increased focus on tyres engineered for multiple retread cycles.

- Automated Retreading Facilities: Robotics and precision manufacturing improve consistency and throughput.

- Digital Tyre Lifecycle Tracking: RFID and data platforms support casing history and predictive retread scheduling.

- Sustainable Compound Innovation: Lower-emission materials and recycled rubber integration enhance ESG alignment.

- Fleet TCO Optimization: Retreading increasingly positioned as a strategic operating model rather than a simple replacement strategy.

Strategic Implications of Technology & Innovation Landscape in Global Tyre Retreading Market

The evolving technology landscape has major strategic implications for retreaders, tyre manufacturers, commercial fleets, and industrial operators. Technology-led retreading is transforming from a secondary market into a core fleet lifecycle management strategy. Manufacturers investing in stronger casing design, retread compatibility, and OEM-certified service networks can capture greater value across multiple tyre life cycles rather than relying solely on new tyre sales. This creates recurring revenue opportunities and deeper fleet integration. For fleets, advanced retreading technologies significantly improve TCO by reducing tyre procurement costs, extending asset life, and lowering downtime. Companies that integrate predictive casing management and digital tyre monitoring can optimize operational efficiency at scale. Automation and quality assurance are raising competitive barriers, favoring larger retread providers with advanced facilities, certification systems, and technology partnerships. Sustainability is becoming a central strategic driver, with retreading increasingly aligned with circular economy mandates, carbon reduction goals, and resource conservation initiatives. This enhances retreading’s strategic value for fleets pursuing ESG compliance. OEM-backed retreading is also shifting customer perception, positioning retreaded tyres as premium lifecycle solutions rather than budget compromises.

Global Tyre Retreading Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the global tyre retreading market is expected to become more technology-driven, digitally integrated, and sustainability-focused. Retreading will increasingly function as an intelligent lifecycle management system rather than a simple cost-saving process. AI-enabled casing diagnostics, predictive wear analytics, and RFID-based lifecycle management are expected to become standard, enabling safer and more profitable multi-life tyre ecosystems. OEM-certified retreading programs will likely expand significantly, particularly in commercial vehicles, aviation, and industrial segments where quality assurance and lifecycle economics are critical. Automation in retreading plants will continue to improve throughput, precision, and scalability, strengthening retread competitiveness against new tyre economics. Material innovation will further enhance retread performance through stronger compounds, advanced tread technologies, and lower-carbon manufacturing processes. In conclusion, the Global Tyre Retreading Market is transitioning from traditional cost-focused refurbishment into a technologically advanced circular mobility solution. Companies that lead in casing intelligence, automation, OEM certification, and sustainability integration will be best positioned to dominate the next phase of retreading market growth through 2033.

Market Risk

Global Tyre Retreading Market Risk Factors & Disruption Threats Overview

The Global Tyre Retreading Market operates at the intersection of fleet cost optimization, circular economy economics, and industrial sustainability, making it a strategically important segment within the broader tyre value chain. While retreading benefits from strong commercial fleet demand, ESG momentum, and lower total cost of ownership (TCO), the market carries a moderate strategic risk profile due to casing quality dependency, safety perception challenges, regulatory inconsistency, and technological disruption from premium long-life tyres. A major structural risk is casing availability and durability. Retreading viability depends entirely on the quality and recoverability of used tyre casings, particularly in commercial fleets. Poor road conditions, overloaded vehicles, inconsistent maintenance, and low-quality original tyres can significantly reduce retreadable casing supply. Safety perception remains another critical disruption factor. While OEM-certified and technologically advanced retreads offer reliable performance, market adoption in certain regions continues to face skepticism around durability, failure risk, and performance consistency’particularly outside commercial applications. Regulatory fragmentation also creates strategic complexity. Different countries maintain varying policies on retread standards, fleet acceptance, passenger vehicle legality, and aviation certification, creating uneven market scalability. In addition, premium original tyre manufacturers are increasingly designing longer-life, fuel-efficient, and retread-compatible products, which can both support and disrupt independent retreading economics depending on ecosystem control.

Global Tyre Retreading Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects stable growth supported by logistics expansion, freight mobility, mining operations, and rising fleet operating cost pressures. However, the market remains highly sensitive to operational quality and fleet confidence. Commercial truck and bus retreading remain the dominant demand centers globally, particularly in cost-sensitive and fleet-intensive markets. OEM-certified retreading programs are gaining momentum, increasing trust, standardization, and lifecycle optimization while placing pressure on smaller independent retreaders. Casing shortages in some regions are emerging due to increased use of lower-cost imported tyres with weaker retread potential. At the same time, sustainability regulations and circular economy mandates are strengthening retreading’s strategic relevance, particularly in Europe and North America.

Key Risk Factors & Disruption Threats Signals in Global Tyre Retreading Market

A major disruption signal is the acceleration of OEM-controlled retreading ecosystems, where tyre majors increasingly integrate casing design, retread certification, and fleet lifecycle management. Advanced inspection technologies’including AI-based casing diagnostics, digital casing history, and automated buffing systems’are reshaping operational efficiency and safety validation. Fleet digitization and tyre-as-a-service (TaaS) models are also creating new competitive frameworks by integrating retreading into broader asset optimization strategies. Environmental policy tightening around landfill bans, waste tyre disposal, and carbon reduction targets is further strengthening structural demand for retreading solutions. Conversely, the increasing penetration of ultra-durable premium tyres and sustainability-focused new tyre designs may alter replacement-retread economics in select applications.

Strategic Implications of Risk Factors & Disruption Threats in Global Tyre Retreading Market

Retreading providers must prioritize casing quality assurance, digital inspection systems, and performance consistency to defend credibility and expand fleet penetration. OEM partnerships and certification programs will become increasingly essential for scaling trust, warranty support, and premium market participation. Independent retreaders may need to consolidate, specialize, or technologically upgrade to remain competitive against brand-owned retread ecosystems. Investment in circular economy positioning, ESG compliance, and measurable carbon reduction outcomes will become major differentiators in fleet procurement. Geographic expansion should prioritize freight-heavy, mining-intensive, and regulation-supportive markets where retreading economics remain strongest.

Global Tyre Retreading Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Tyre Retreading Market is expected to evolve from a cost-saving aftermarket service into a strategically integrated fleet lifecycle solution. Growth will increasingly depend on technology sophistication, OEM ecosystem participation, and sustainability alignment. Commercial vehicle and multi-life retreading are likely to remain the highest-value segments, particularly across logistics, mining, aviation, and public transport. Europe’s regulatory framework and Asia-Pacific’s cost sensitivity will continue to shape market expansion differently but powerfully. Digital casing intelligence, predictive maintenance, and fleet-integrated retread optimization are expected to redefine competitive advantage. Overall, the market will remain highly relevant but operationally demanding, with long-term winners defined by casing control, technological precision, OEM trust, and scalable circular economy execution.

Regulatory Landscape

Global Tyre Retreading Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Tyre Retreading Market is increasingly shaping retreading from a cost-saving practice into a strategic pillar of circular economy and sustainable mobility. Governments, transportation authorities, and environmental agencies worldwide are intensifying regulations around waste reduction, raw material efficiency, and lifecycle emissions, creating strong structural support for tyre retreading adoption’particularly across commercial fleets, logistics operators, aviation, and off-the-road sectors. Global regulatory frameworks including UNECE tyre safety standards, national transport safety certifications, and circular economy directives increasingly recognize retreading as a viable sustainability solution when strict casing integrity, tread performance, and safety compliance are maintained. Certified retreaded tyres are being positioned as lower-carbon alternatives to new tyres, particularly in heavy-duty applications where casing durability supports multiple retread cycles. Environmental regulations focused on landfill reduction and end-of-life tyre waste management are also significantly accelerating retreading. Regions such as Europe actively promote tyre reuse and retreading through sustainability mandates, while fleet sustainability targets and ESG compliance frameworks are encouraging broader adoption globally. Emerging markets including India, China, Southeast Asia, and Latin America are strengthening tyre quality regulations and road transport compliance systems. These evolving standards are gradually formalizing the retreading ecosystem, improving safety perceptions, and shifting demand from informal operators toward certified retreading programs.

Global Tyre Retreading Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is defined by a balance between safety oversight and sustainability-driven incentives. Europe remains the most policy-progressive region, where circular economy regulations, landfill restrictions, and fleet decarbonization initiatives strongly support OEM-certified retreading programs. In Europe, retreaded tyres’particularly for trucks and buses’benefit from policy support tied to resource efficiency and carbon reduction. Strict quality controls under UNECE regulations ensure that retreaded tyres meet safety and performance standards, strengthening market confidence. Asia-Pacific remains the largest market, but regulatory maturity varies significantly. Cost advantages continue to drive adoption, while improving fleet safety standards in countries such as India and China are encouraging gradual movement toward standardized and certified retreading practices. North America maintains strong demand through DOT oversight, commercial trucking standards, and established brand-backed retreading networks such as Bandag and Michelin Remix. Safety compliance and operational efficiency are the primary regulatory drivers in this market. Aviation and mining sectors globally are subject to especially stringent inspection and certification protocols, where retreading is accepted only under rigorous performance and structural integrity standards.

Key Regulatory & Policy Environment Signals in Global Tyre Retreading Market

- UNECE Retread Tyre Standards: Establish international safety and performance benchmarks for retreaded commercial vehicle tyres.

- Circular Economy & Waste Reduction Policies: Encourage tyre reuse, landfill diversion, and lifecycle optimization.

- Fleet ESG & Sustainability Mandates: Push operators toward lower-emission tyre lifecycle solutions.

- DOT & National Transport Safety Standards: Regulate retread safety, especially for trucks, buses, and aviation applications.

- OEM Certification Programs: Strengthen quality assurance and improve market confidence through manufacturer-backed retreading.

- Emerging Market Standardization Initiatives: Improve quality oversight and reduce informal or unsafe retreading practices.

Strategic Implications of Regulatory & Policy Environment in Global Tyre Retreading Market

The regulatory landscape is increasingly transforming retreading from a fragmented aftermarket activity into a structured, compliance-driven mobility solution. Safety certifications and environmental mandates are raising standards, increasing the competitive advantage of OEM-backed and technologically advanced retreaders. Independent and low-standard retreaders face rising pressure as regulatory scrutiny intensifies. Manufacturers and service providers must invest in advanced casing inspection, digital tracking, automated buffing systems, and certified tread technologies to remain competitive. Compliance-led innovation is becoming central to growth. Technologies such as RFID-based casing tracking, predictive casing analytics, and AI-powered inspection systems are increasingly important to meet both regulatory and operational requirements. Fleet procurement strategies are also shifting, with major logistics and transport operators prioritizing certified multi-life tyre programs that optimize total cost of ownership while aligning with sustainability and safety regulations. Regional policy differences are shaping supply chains, with localized retreading networks, OEM partnerships, and regulatory alignment becoming essential to ensure competitiveness across developed and emerging markets.

Global Tyre Retreading Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for tyre retreading is expected to strengthen significantly, particularly as circular economy strategies, carbon reduction goals, and fleet sustainability mandates become more aggressive globally. Europe will remain the leading regulatory force, likely expanding lifecycle emissions accountability and sustainability-linked procurement frameworks that further support retreading. Asia-Pacific is expected to see rising formalization and quality standardization as governments balance cost sensitivity with road safety priorities. North America is projected to maintain stable regulatory support through trucking efficiency mandates and expanded fleet ESG strategies, while aviation and mining sectors will continue emphasizing high-certification retread solutions. Advanced technologies such as digital casing passports, smart inspection systems, and OEM-certified multi-life platforms are expected to gain stronger regulatory alignment, improving transparency, safety, and adoption rates. Overall, the regulatory landscape will increasingly position tyre retreading as a critical enabler of fleet cost optimization, sustainability compliance, and circular resource management. Companies that proactively align with evolving safety standards, environmental regulations, and technology-driven certification systems will be best positioned to lead the Global Tyre Retreading Market through 2033.