Global Acute Myeloid Leukemia Drugs Market Report, Size & Forecast 2026 - 2033

Global Acute Myeloid Leukemia (AML) Drugs Market Forecast Snapshot: 2026–2033

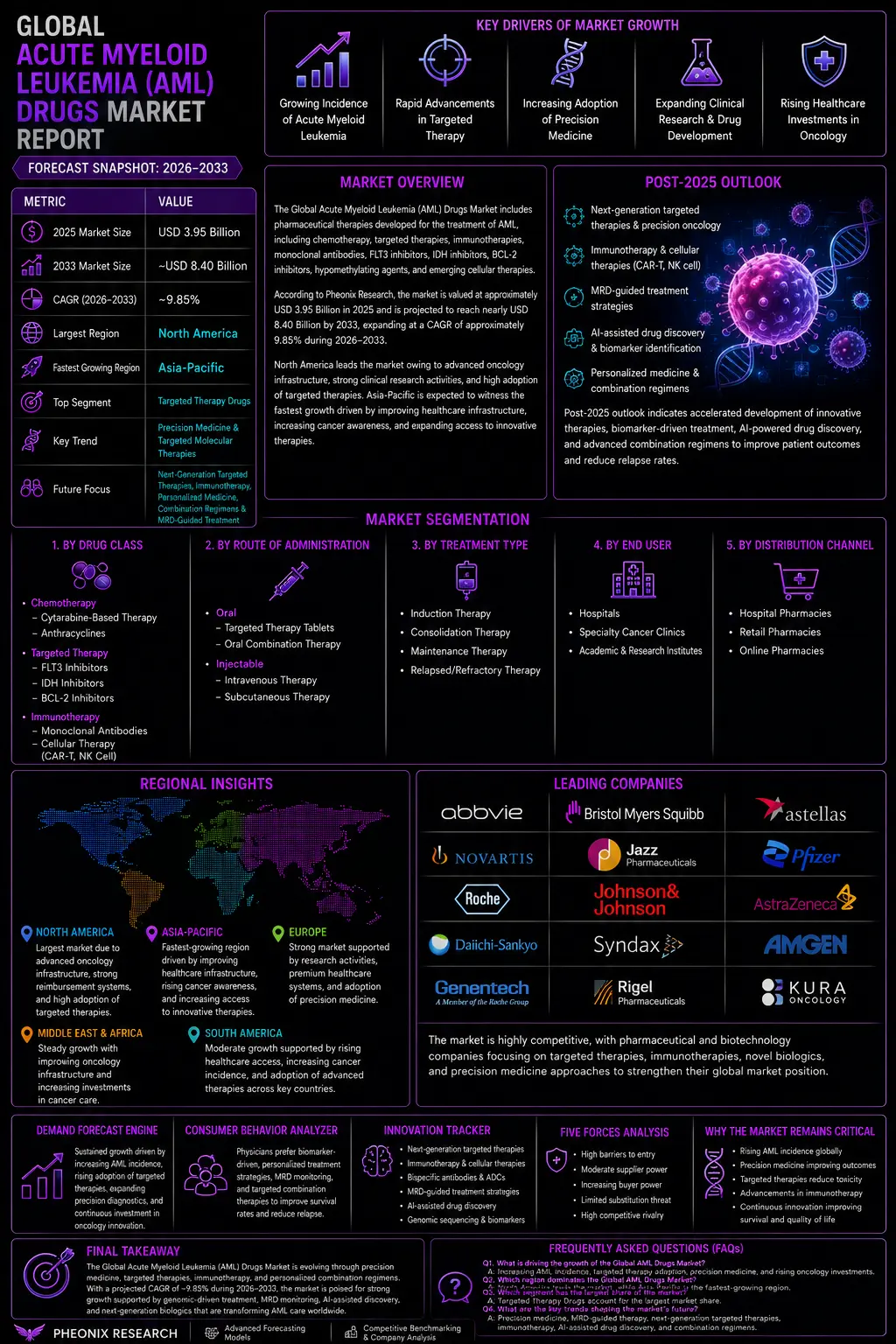

| Metric | Value |

|---|---|

| 2025 Market Size | USD 3.95 Billion |

| 2033 Market Size | ~USD 8.40 Billion |

| CAGR (2026–2033) | ~9.85% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Targeted Therapy Drugs |

| Key Trend | Precision Medicine & Targeted Molecular Therapies |

| Future Focus | Next-Generation Targeted Therapies, Immunotherapy, Personalized Medicine, Combination Regimens & MRD-Guided Treatment |

Global Acute Myeloid Leukemia (AML) Drugs Market Overview

The Global Acute Myeloid Leukemia (AML) Drugs Market comprises pharmaceutical therapies developed for the treatment of acute myeloid leukemia, an aggressive hematologic malignancy characterized by the rapid proliferation of abnormal myeloid cells in the bone marrow and blood. The market includes chemotherapy drugs, targeted therapies, immunotherapies, monoclonal antibodies, FLT3 inhibitors, IDH inhibitors, BCL-2 inhibitors, hypomethylating agents, stem cell transplantation support therapies, and emerging cellular therapies. The AML treatment landscape has undergone significant transformation over the past decade with the introduction of precision medicine, genomic profiling, targeted therapies, and personalized treatment strategies. Improved molecular diagnostics, increasing understanding of genetic mutations such as FLT3, IDH1, IDH2, TP53, and NPM1, together with advances in combination therapies, are enabling more effective and individualized treatment approaches. According to Pheonix Research, the Global Acute Myeloid Leukemia Drugs Market is valued at approximately USD 3.95 billion in 2025 and is projected to reach nearly USD 8.40 billion by 2033, expanding at a CAGR of approximately 9.85% during 2026–2033. North America dominates the market due to advanced oncology infrastructure, high adoption of targeted therapies, favorable reimbursement systems, strong clinical research activities, and the presence of leading pharmaceutical companies. Asia-Pacific is expected to witness the fastest growth owing to improving healthcare infrastructure, increasing cancer awareness, expanding access to innovative oncology therapies, and growing investments in precision medicine across China, Japan, India, and South Korea. The Post-2025 outlook indicates accelerated development of next-generation targeted therapies, bispecific antibodies, CAR-T cell therapies, antibody-drug conjugates (ADCs), measurable residual disease (MRD)-guided treatment strategies, AI-assisted drug discovery, and personalized genomic medicine.Global Acute Myeloid Leukemia (AML) Drugs Market

Key Drivers of Global Acute Myeloid Leukemia (AML) Drugs Market Growth

1. Growing Incidence of Acute Myeloid Leukemia

The increasing prevalence of AML, particularly among the aging population, continues to drive demand for innovative therapeutic options capable of improving survival outcomes while minimizing treatment-related toxicity.2. Rapid Advancements in Targeted Therapy

The growing availability of FLT3 inhibitors, IDH inhibitors, BCL-2 inhibitors, and mutation-specific therapies has significantly improved treatment outcomes and expanded precision medicine approaches in AML management.3. Increasing Adoption of Precision Medicine

Comprehensive genomic profiling and molecular diagnostics enable physicians to select personalized treatment regimens based on individual genetic mutations, driving demand for targeted AML therapies.4. Expanding Clinical Research & Drug Development

Continuous investment in oncology research, clinical trials, and innovative biologics is accelerating the approval of novel AML drugs, combination therapies, and immunotherapeutic approaches.5. Growing Healthcare Investments in Oncology

Governments, healthcare providers, and pharmaceutical companies continue increasing investments in oncology infrastructure, cancer screening, precision diagnostics, and innovative treatment access, supporting sustained market growth.Global Acute Myeloid Leukemia (AML) Drugs Market Segmentation

1. By Drug Class

1.1 Chemotherapy 1.1.1 Cytarabine-Based Therapy 1.1.1.1 Standard Cytarabine 1.1.1.2 High-Dose Cytarabine 1.1.2 Anthracyclines 1.1.2.1 Daunorubicin 1.1.2.2 Idarubicin 1.2 Targeted Therapy 1.2.1 FLT3 Inhibitors 1.2.1.1 Midostaurin 1.2.1.2 Gilteritinib 1.2.2 IDH Inhibitors 1.2.2.1 Ivosidenib 1.2.2.2 Enasidenib 1.2.3 BCL-2 Inhibitors 1.2.3.1 Venetoclax 1.2.3.2 Combination Therapy 1.3 Immunotherapy 1.3.1 Monoclonal Antibodies 1.3.1.1 CD33 Targeted Therapy 1.3.1.2 Bispecific Antibodies 1.3.2 Cellular Therapy 1.3.2.1 CAR-T Therapy 1.3.2.2 NK Cell Therapy2. By Route of Administration

2.1 Oral 2.1.1 Targeted Therapy Tablets 2.1.1.1 FLT3 Inhibitors 2.1.1.2 IDH Inhibitors 2.1.2 Oral Combination Therapy 2.1.2.1 Maintenance Therapy 2.1.2.2 Personalized Treatment 2.2 Injectable 2.2.1 Intravenous Therapy 2.2.1.1 Chemotherapy 2.2.1.2 Monoclonal Antibodies 2.2.2 Subcutaneous Therapy 2.2.2.1 Biologics 2.2.2.2 Supportive Care3. By Treatment Type

3.1 Induction Therapy 3.1.1 Intensive Chemotherapy 3.1.1.1 Newly Diagnosed AML 3.1.1.2 High-Risk Patients 3.2 Consolidation Therapy 3.2.1 High-Dose Therapy 3.2.1.1 Stem Cell Preparation 3.2.1.2 Disease Remission 3.3 Maintenance Therapy 3.3.1 Targeted Maintenance 3.3.1.1 Oral Agents 3.3.1.2 Long-Term Disease Control 3.4 Relapsed/Refractory Therapy 3.4.1 Salvage Treatment 3.4.1.1 Targeted Therapy 3.4.1.2 Combination Regimens4. By End User

4.1 Hospitals 4.1.1 Oncology Hospitals 4.1.1.1 Hematology Centers 4.1.1.2 Cancer Institutes 4.2 Specialty Cancer Clinics 4.2.1 Outpatient Oncology 4.2.1.1 Personalized Medicine Centers 4.2.1.2 Day Care Infusion Centers 4.3 Academic & Research Institutes 4.3.1 Clinical Research Centers 4.3.1.1 Drug Development 4.3.1.2 Clinical Trials5. By Distribution Channel

5.1 Hospital Pharmacies 5.1.1 Oncology Pharmacy 5.1.1.1 Inpatient Treatment 5.1.1.2 Specialty Drug Dispensing 5.2 Retail Pharmacies 5.2.1 Community Pharmacies 5.2.1.1 Oral AML Therapies 5.2.1.2 Supportive Medications 5.3 Online Pharmacies 5.3.1 Digital Pharmacy Platforms 5.3.1.1 Home Delivery5.3.1.2 Specialty Prescription Services

Regional Insights of Global Acute Myeloid Leukemia (AML) Drugs Market

North America – Largest Market

North America dominates the Global Acute Myeloid Leukemia (AML) Drugs Market owing to its advanced oncology infrastructure, widespread adoption of targeted therapies, strong reimbursement policies, and extensive clinical research activities. The United States leads the regional market through continuous approvals of novel AML drugs, increasing utilization of genomic testing, and the presence of major pharmaceutical and biotechnology companies actively developing next-generation leukemia therapies. High awareness among healthcare professionals and favorable regulatory pathways further strengthen regional market leadership.Asia-Pacific

Asia-Pacific is projected to register the fastest growth during the forecast period, supported by improving healthcare infrastructure, increasing cancer diagnosis rates, expanding access to precision medicine, and rising healthcare expenditure across China, Japan, India, South Korea, and Australia. Government initiatives promoting oncology research, expanding health insurance coverage, and increasing availability of targeted therapies are accelerating market growth throughout the region.Europe

Europe represents a significant market driven by strong oncology research, favorable healthcare reimbursement systems, and increasing adoption of personalized medicine. Germany, France, the United Kingdom, Italy, and Spain continue investing in molecular diagnostics, innovative leukemia therapies, and clinical trials to improve patient outcomes while supporting rapid commercialization of advanced AML treatment options.Middle East & Africa

The Middle East & Africa market is gradually expanding due to improving cancer care infrastructure, increasing investments in specialty oncology centers, growing awareness of hematologic malignancies, and expanding availability of advanced therapeutic options. Countries including the UAE, Saudi Arabia, South Africa, and Israel continue strengthening access to precision oncology and innovative cancer treatments.South America

South America is witnessing steady market growth supported by improving oncology healthcare services, increasing government initiatives for cancer management, and rising adoption of targeted leukemia therapies. Brazil, Argentina, Chile, and Colombia continue investing in specialized hematology centers and expanding access to innovative AML treatments.Leading Companies in the Global Acute Myeloid Leukemia (AML) Drugs Market

- AbbVie Inc.

- Bristol Myers Squibb Company

- Astellas Pharma Inc.

- Novartis AG

- Jazz Pharmaceuticals plc

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson

- AstraZeneca PLC

- Daiichi Sankyo Company, Limited

- Syndax Pharmaceuticals, Inc.

- Amgen Inc.

- Genentech, Inc.

- Rigel Pharmaceuticals, Inc.

- Kura Oncology, Inc.

Why the Global Acute Myeloid Leukemia (AML) Drugs Market Remains Critical

- Rising incidence of AML among aging populations continues to increase demand for innovative treatment options.

- Precision medicine and genomic profiling are transforming AML diagnosis and personalized treatment selection.

- Targeted therapies significantly improve clinical outcomes while reducing treatment-related toxicity compared to conventional chemotherapy.

- Continuous research in immunotherapy, cellular therapy, and molecular oncology is expanding therapeutic opportunities for relapsed and refractory AML patients.

- Increasing healthcare investments and regulatory support continue accelerating the development and commercialization of novel AML therapies worldwide.

Strategic Intelligence and AI-Backed Insights – Global Acute Myeloid Leukemia (AML) Drugs Market

Pheonix Demand Forecast Engine identifies sustained market growth driven by increasing adoption of targeted therapies, expanding molecular diagnostic testing, rising investment in oncology research, growing utilization of combination therapies, and continuous approval of innovative leukemia drugs across major healthcare markets. The Consumer Behavior Analyzer highlights increasing physician preference for personalized treatment strategies based on genetic profiling, measurable residual disease (MRD) monitoring, biomarker-driven therapy selection, and individualized combination treatment regimens designed to improve long-term patient outcomes. The Innovation Tracker emphasizes FLT3 inhibitors, IDH inhibitors, BCL-2 inhibitors, bispecific antibodies, antibody-drug conjugates (ADCs), CAR-T cell therapies, measurable residual disease (MRD)-guided treatment, artificial intelligence-assisted drug discovery, genomic sequencing, and precision oncology platforms as the technologies expected to redefine AML treatment over the coming decade. Five Forces Analysis indicates high barriers to entry due to stringent regulatory requirements, extensive clinical trial investments, specialized oncology expertise, and complex biologics development. Supplier power remains moderate owing to multiple pharmaceutical innovators, while buyer power is increasing as healthcare providers prioritize clinically differentiated therapies with demonstrated survival benefits. Competitive rivalry remains high as leading pharmaceutical companies compete through innovation, strategic collaborations, regulatory approvals, and expanding oncology pipelines.Final Takeaway of Global Acute Myeloid Leukemia (AML) Drugs Market

The Global Acute Myeloid Leukemia (AML) Drugs Market is entering a new era of precision oncology driven by targeted therapies, molecular diagnostics, immunotherapy, and personalized medicine. The projected CAGR of approximately 9.85% during 2026–2033 reflects growing global demand for innovative therapies capable of improving survival outcomes, reducing relapse rates, and delivering more individualized treatment approaches for AML patients. Future market expansion will be supported by continued advances in genomic medicine, AI-assisted drug discovery, measurable residual disease (MRD)-guided therapy, antibody-drug conjugates, bispecific antibodies, cellular immunotherapies, and combination treatment strategies. As healthcare systems increasingly embrace precision medicine and biomarker-driven treatment protocols, pharmaceutical companies will continue accelerating innovation across the AML therapeutic landscape. Organizations that successfully integrate advanced molecular diagnostics, targeted drug development, immunotherapy platforms, companion diagnostics, and personalized treatment strategies will be well positioned to achieve sustainable competitive advantage in the rapidly evolving oncology market. At Pheonix Research, our advanced forecasting models deliver comprehensive Global Acute Myeloid Leukemia (AML) Drugs Market revenue forecasts, competitive benchmarking, regional opportunity analysis, and strategic intelligence—enabling pharmaceutical companies, biotechnology firms, healthcare providers, investors, and research organizations to capitalize on the Post-2025 outlook with confidence and data-driven decision-making.Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Market Highlights

1.3 Market Size & Forecast (2026–2033)

1.4 Largest Regional Market Analysis

1.5 Fastest Growing Regional Market Analysis

1.6 Largest Segment Analysis

1.7 Competitive Landscape Snapshot

1.8 Future Market Outlook

2. Global Acute Myeloid Leukemia (AML) Drugs Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Acute Myeloid Leukemia (AML) Drugs Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Drug Development & Commercialization Pathway

3.5 AML Treatment Landscape

3.6 Therapeutic Landscape

3.6.1 Chemotherapy

3.6.1.1 Cytarabine-Based Therapy

3.6.1.1.1 Anthracyclines

3.6.1.1.1.1 Standard Induction Therapy

3.6.1.1.1.2 High-Dose Chemotherapy

3.6.2 Targeted Therapy

3.6.2.1 FLT3 Inhibitors

3.6.2.1.1 IDH Inhibitors

3.6.2.1.1.1 BCL-2 Inhibitors

3.6.2.1.1.2 Combination Targeted Therapy

3.6.3 Immunotherapy

3.6.3.1 Monoclonal Antibodies

3.6.3.1.1 Bispecific Antibodies

3.6.3.1.1.1 CAR-T Cell Therapy

3.6.3.1.1.2 NK Cell Therapy

3.6.4 Precision Medicine

3.6.4.1 Genomic Profiling

3.6.4.1.1 Companion Diagnostics

3.6.4.1.1.1 MRD Monitoring

3.6.4.1.1.2 Personalized Treatment Planning

4. Regulatory Landscape

4.1 Oncology Drug Approval Framework

4.2 Precision Medicine & Companion Diagnostic Regulations

4.3 Clinical Trial & Drug Development Guidelines

4.4 Reimbursement & Market Access Policies

4.5 Pharmacovigilance & Patient Safety Regulations

5. Market Trends & Innovation Outlook

5.1 Precision Medicine & Molecular Profiling

5.2 Next-Generation Targeted Therapies

5.3 Immunotherapy & Cellular Therapies

5.4 Measurable Residual Disease (MRD)-Guided Treatment

5.5 AI-Assisted Drug Discovery

5.6 Antibody-Drug Conjugates (ADCs)

5.7 Bispecific Antibodies

5.8 Personalized Combination Therapy Regimens

6. Global Acute Myeloid Leukemia (AML) Drugs Market Dynamics

6.1 Market Drivers

6.1.1 Growing Incidence of Acute Myeloid Leukemia

6.1.2 Rapid Advancements in Targeted Therapy

6.1.3 Increasing Adoption of Precision Medicine

6.1.4 Expanding Clinical Research & Drug Development

6.1.5 Growing Healthcare Investments in Oncology

6.2 Market Restraints

6.2.1 High Cost of Targeted Therapies

6.2.2 Limited Accessibility in Developing Regions

6.2.3 Treatment-Related Toxicity & Adverse Effects

6.2.4 Stringent Regulatory Approval Processes

6.3 Market Opportunities

6.3.1 Expansion of Personalized Medicine

6.3.2 Development of Next-Generation Biologics

6.3.3 Emerging Cellular Immunotherapies

6.3.4 AI-Driven Drug Discovery Platforms

6.3.5 Expansion into Emerging Healthcare Markets

6.4 Market Challenges

6.4.1 Drug Resistance & Disease Relapse

6.4.2 Complex Clinical Trial Design

6.4.3 Biomarker Identification & Validation

6.4.4 Affordability & Reimbursement Challenges

7. Global Acute Myeloid Leukemia (AML) Drugs Market Size Analysis (USD Billion), 2026–2033

7.1 Revenue Forecast Analysis

7.2 CAGR Analysis

7.3 Drug Class Revenue Analysis

7.4 Pipeline & Commercialization Trends

7.5 Investment & R&D Analysis

8. Global Acute Myeloid Leukemia (AML) Drugs Market Segmentation Analysis

8.1 By Drug Class

8.1.1 Chemotherapy

8.1.2 Targeted Therapy

8.1.3 Immunotherapy

8.2 By Route of Administration

8.2.1 Oral

8.2.2 Injectable

8.3 By Treatment Type

8.3.1 Induction Therapy

8.3.2 Consolidation Therapy

8.3.3 Maintenance Therapy

8.3.4 Relapsed/Refractory Therapy

8.4 By End User

8.4.1 Hospitals

8.4.2 Specialty Cancer Clinics

8.4.3 Academic & Research Institutes

8.5 By Distribution Channel

8.5.1 Hospital Pharmacies

8.5.2 Retail Pharmacies

8.5.3 Online Pharmacies

9. Regional Market Analysis

9.1 North America

9.1.1 United States

9.1.2 Canada

9.1.3 Mexico

9.2 Europe

9.2.1 Germany

9.2.2 France

9.2.3 United Kingdom

9.2.4 Italy

9.2.5 Spain

9.2.6 Rest of Europe

9.3 Asia-Pacific

9.3.1 China

9.3.2 Japan

9.3.3 India

9.3.4 South Korea

9.3.5 Australia

9.3.6 Rest of Asia-Pacific

9.4 Middle East & Africa

9.4.1 GCC Countries

9.4.2 South Africa

9.4.3 Israel

9.4.4 Rest of Middle East & Africa

9.5 South America

9.5.1 Brazil

9.5.2 Argentina

9.5.3 Chile

9.5.4 Rest of South America

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Benchmarking

10.3 Strategic Developments

10.4 Oncology Pipeline & Innovation Analysis

10.5 Partnerships, Licensing & Acquisitions

10.6 Competitive Positioning Matrix

11. Company Profiles

11.1 AbbVie Inc.

11.2 Bristol Myers Squibb Company

11.3 Astellas Pharma Inc.

11.4 Novartis AG

11.5 Jazz Pharmaceuticals plc

11.6 Pfizer Inc.

11.7 F. Hoffmann-La Roche Ltd.

11.8 Johnson & Johnson

11.9 AstraZeneca PLC

11.10 Daiichi Sankyo Company, Limited

11.11 Syndax Pharmaceuticals, Inc.

11.12 Amgen Inc.

11.13 Genentech, Inc.

11.14 Rigel Pharmaceuticals, Inc.

11.15 Kura Oncology, Inc.

12. Strategic Intelligence & Pheonix AI Insights

12.1 Pheonix Demand Forecast Engine

12.2 Consumer Behavior Analyzer

12.3 Innovation Tracker

12.4 AML Drug Pipeline Intelligence Dashboard

12.5 Precision Oncology Opportunity Analysis

12.6 Porter’s Five Forces Analysis

13. Future Outlook & Strategic Recommendations

13.1 Precision Medicine Adoption Roadmap

13.2 Next-Generation Targeted Therapy Strategy

13.3 Immunotherapy & Combination Therapy Outlook

13.4 Personalized Oncology Treatment Framework

13.5 Long-Term Market Outlook (2033+)

14. About Pheonix Market Research

15. Disclaimer

Competitive Landscape

Global Acute Myeloid Leukemia (AML) Drugs Market Competitive Intensity & Market Structure Overview

The Global Acute Myeloid Leukemia (AML) Drugs Market is highly competitive and characterized by the presence of multinational pharmaceutical companies, biotechnology firms, oncology drug developers, precision medicine innovators, immunotherapy companies, molecular diagnostics providers, and clinical research organizations. Competitive intensity is driven by rapid advancements in targeted therapies, immunotherapies, precision oncology, genomic profiling, biomarker-driven drug development, artificial intelligence-assisted drug discovery, and personalized treatment strategies.

Companies compete across multiple therapeutic segments including chemotherapy, targeted therapies, FLT3 inhibitors, IDH inhibitors, BCL-2 inhibitors, hypomethylating agents, monoclonal antibodies, bispecific antibodies, CAR-T cell therapies, antibody-drug conjugates (ADCs), and combination treatment regimens. Increasing AML incidence, rising adoption of precision medicine, expanding genomic diagnostics, growing clinical research activities, and continuous regulatory approvals are intensifying competition while accelerating innovation across the AML therapeutic landscape.

The market structure is evolving toward precision oncology ecosystems integrating molecular diagnostics, companion diagnostics, targeted drug development, genomic sequencing, AI-powered drug discovery, measurable residual disease (MRD) monitoring, immunotherapy platforms, and personalized medicine into comprehensive AML treatment strategies. Market participants are investing heavily in next-generation targeted therapies, biologics, cellular therapies, biomarker-driven clinical trials, and strategic collaborations to strengthen market positioning while improving patient survival outcomes.

Global Acute Myeloid Leukemia (AML) Drugs Market Competitive Intensity & Market Structure Current Scenario

Leading Global Acute Myeloid Leukemia (AML) Drug Companies

AbbVie Inc.: A global biopharmaceutical company specializing in targeted oncology therapies, BCL-2 inhibitors, combination regimens, hematologic malignancy treatments, and precision medicine solutions.

Bristol Myers Squibb Company: A leading oncology company developing immunotherapies, targeted leukemia treatments, cellular therapies, and innovative hematology drug platforms.

Astellas Pharma Inc.: A global pharmaceutical company focused on targeted AML therapies, FLT3 inhibitors, precision oncology, and personalized cancer treatment solutions.

Novartis AG: A multinational pharmaceutical company offering targeted therapies, cellular immunotherapies, oncology biologics, and advanced precision medicine platforms.

Jazz Pharmaceuticals plc: A specialty biopharmaceutical company developing innovative leukemia therapies, hematology treatments, and next-generation oncology medicines.

Pfizer Inc.: A global pharmaceutical leader providing targeted oncology drugs, precision medicine solutions, biologics, and innovative hematologic cancer therapies.

F. Hoffmann-La Roche Ltd.: A leading biotechnology and diagnostics company delivering precision oncology, companion diagnostics, targeted biologics, and personalized cancer treatment platforms.

Johnson & Johnson: A global healthcare company investing in hematology research, targeted therapies, immuno-oncology, and next-generation oncology drug development.

AstraZeneca PLC: A multinational biopharmaceutical company focused on targeted oncology, antibody-drug conjugates, precision medicine, and biomarker-driven treatment strategies.

Daiichi Sankyo Company, Limited: A global pharmaceutical company specializing in antibody-drug conjugates (ADCs), targeted oncology therapies, and advanced hematology research.

Syndax Pharmaceuticals, Inc.: A biotechnology company developing innovative targeted therapies, epigenetic treatments, and next-generation AML drug candidates.

Amgen Inc.: A biotechnology leader providing biologics, immunotherapies, targeted oncology platforms, and advanced hematologic cancer treatment solutions.

Genentech, Inc.: A biotechnology innovator focused on personalized oncology, targeted biologics, companion diagnostics, and molecularly guided cancer therapies.

Rigel Pharmaceuticals, Inc.: A specialty biopharmaceutical company developing targeted therapies for hematologic malignancies and rare blood disorders.

Kura Oncology, Inc.: A clinical-stage biotechnology company advancing precision oncology through mutation-targeted therapies and innovative AML drug development.

Key Competitive Intensity & Market Structure Drivers

Increasing incidence of acute myeloid leukemia, expanding aging populations, and growing demand for effective precision therapies are intensifying competition among global pharmaceutical and biotechnology companies.

Rapid advancements in targeted therapies, immunotherapies, genomic sequencing, molecular diagnostics, AI-assisted drug discovery, biomarker identification, and companion diagnostics are creating significant technological differentiation among market participants.

Growing adoption of personalized medicine, measurable residual disease (MRD) monitoring, mutation-specific therapies, combination treatment regimens, and next-generation biologics is strengthening competitive intensity while accelerating therapeutic innovation.

Strategic collaborations among pharmaceutical companies, biotechnology firms, research institutions, diagnostic companies, academic medical centers, and regulatory agencies are accelerating clinical development, expanding treatment pipelines, and improving commercialization opportunities.

Continuous investment in targeted oncology, immunotherapy, CAR-T cell therapies, antibody-drug conjugates, genomic medicine, biomarker research, and AI-driven drug discovery is enabling companies to improve clinical outcomes, strengthen product portfolios, and maintain long-term competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Companies offering comprehensive oncology portfolios, targeted therapies, precision medicine platforms, and integrated diagnostic capabilities are expected to maintain significant competitive advantages.

Investment in genomic sequencing, biomarker-driven drug development, immunotherapy, measurable residual disease (MRD) monitoring, AI-assisted drug discovery, and companion diagnostics is becoming increasingly important for sustaining long-term market leadership.

Organizations focusing on expanding precision oncology pipelines, improving treatment efficacy, accelerating regulatory approvals, and strengthening personalized medicine capabilities are likely to increase market share and revenue growth.

Strategic partnerships with biotechnology companies, diagnostic developers, academic research institutions, healthcare providers, and clinical research organizations are supporting innovation, pipeline expansion, and global commercialization.

Businesses capable of combining pharmaceutical innovation, molecular diagnostics, precision medicine expertise, immunotherapy development, regulatory excellence, and scalable oncology commercialization strategies will be best positioned to compete effectively in the evolving Global Acute Myeloid Leukemia (AML) Drugs Market.

Global Acute Myeloid Leukemia (AML) Drugs Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the Global Acute Myeloid Leukemia (AML) Drugs Market is expected to become increasingly precision-driven, biomarker-focused, and immunotherapy-oriented as healthcare systems accelerate adoption of personalized oncology and targeted treatment approaches.

Future competition will be shaped by next-generation targeted therapies, bispecific antibodies, CAR-T cell therapies, antibody-drug conjugates (ADCs), measurable residual disease (MRD)-guided treatment, AI-assisted drug discovery, genomic sequencing, companion diagnostics, and personalized combination regimens.

Market participants are expected to increase investments in precision oncology platforms, targeted biologics, cellular immunotherapies, molecular diagnostics, AI-powered research, biomarker discovery, and advanced clinical development programs to strengthen competitive positioning.

Over the forecast period, companies that successfully combine pharmaceutical innovation, precision medicine, molecular diagnostics, immunotherapy expertise, advanced biologics, and personalized treatment strategies will be best positioned to lead the evolving Global Acute Myeloid Leukemia (AML) Drugs Market.

Value Chain

Global Acute Myeloid Leukemia (AML) Drugs Market Value Chain Analysis

1. Drug Discovery, Target Identification & Early Research

The value chain begins with pharmaceutical companies, biotechnology firms, academic institutions, and research organizations conducting disease biology research, genomic profiling, biomarker discovery, molecular target identification, AI-assisted drug discovery, and preclinical development. Advances in precision medicine, immunotherapy, and companion diagnostics continue to accelerate innovation in AML therapeutics.

2. API Manufacturing & Biopharmaceutical Production

Manufacturers produce active pharmaceutical ingredients (APIs), biologics, monoclonal antibodies, targeted therapy compounds, excipients, and drug delivery components under stringent Good Manufacturing Practice (GMP) standards. This stage includes formulation development, sterile manufacturing, quality control, and scale-up for commercial production.

3. Clinical Development, Regulatory Approval & Commercial Manufacturing

Drug developers conduct Phase I–III clinical trials, safety evaluations, efficacy studies, pharmacovigilance planning, regulatory submissions, and manufacturing validation. Regulatory agencies review data for approval, while commercial-scale production ensures consistent product quality, compliance, and supply continuity.

4. Distribution, Specialty Pharmacy & Healthcare Delivery

Approved AML drugs are distributed through specialty distributors, hospital pharmacies, oncology pharmacies, and healthcare networks. Cold chain logistics, inventory management, reimbursement coordination, and specialty drug distribution ensure timely availability of therapies to hospitals, cancer centers, and specialty clinics.

5. Patient Treatment, Monitoring & Lifecycle Management

Healthcare providers administer AML therapies, monitor treatment response through genomic testing and measurable residual disease (MRD) assessment, manage adverse events, optimize personalized treatment regimens, and provide long-term patient follow-up. Pharmaceutical companies support lifecycle management through post-marketing surveillance, label expansion, real-world evidence generation, and next-generation therapy development.

Key Value Chain Participants

- Pharmaceutical and biotechnology companies

- API manufacturers and contract manufacturing organizations (CMOs)

- Clinical research organizations (CROs) and regulatory agencies

- Hospital pharmacies, specialty pharmacies, and distributors

- Hospitals, oncology centers, and hematology clinics

- Diagnostic laboratories and companion diagnostic providers

- Pharmacovigilance and lifecycle management service providers

Value Chain Optimization Opportunities

- AI-assisted drug discovery and precision oncology platforms

- Companion diagnostics and biomarker-driven therapy selection

- Scalable biologics manufacturing and supply chain resilience

- Digital clinical trials and decentralized patient monitoring

- Advanced cold chain logistics and specialty pharmacy optimization

- Personalized medicine supported by genomic profiling and MRD monitoring

- Strategic collaborations for combination therapies and next-generation immunotherapies

Investment Activity

Investment Activity in the Global Acute Myeloid Leukemia (AML) Drugs Market

Investment activity in the Global Acute Myeloid Leukemia (AML) Drugs Market is accelerating as pharmaceutical companies, biotechnology firms, academic research institutions, healthcare organizations, and investors increase capital deployment toward precision medicine, targeted therapies, immunotherapy, cellular therapies, and next-generation oncology drug development. Rising demand for personalized treatment approaches, expanding molecular diagnostics, and continuous innovation in hematologic oncology are driving sustained investment across the AML therapeutics ecosystem.

Leading biopharmaceutical companies are investing heavily in next-generation targeted therapies, FLT3 inhibitors, IDH inhibitors, BCL-2 inhibitors, bispecific antibodies, antibody-drug conjugates (ADCs), CAR-T cell therapies, and AI-assisted drug discovery platforms. These investments are improving treatment efficacy, expanding therapeutic options for relapsed and refractory AML patients, and accelerating the development of personalized treatment regimens.

Pharmaceutical manufacturers are also allocating significant capital toward genomic sequencing technologies, companion diagnostics, measurable residual disease (MRD) monitoring, biomarker discovery, and advanced clinical trial programs. Increasing integration of precision diagnostics with targeted therapeutics is strengthening individualized treatment strategies while improving long-term patient outcomes.

Strategic partnerships, licensing agreements, mergers, acquisitions, and research collaborations among pharmaceutical companies, biotechnology firms, diagnostic developers, contract research organizations, and academic institutions are accelerating innovation across the AML treatment landscape. Investments are increasingly focused on combination therapies, immuno-oncology platforms, and translational research to expand product pipelines and improve clinical success rates.

Governments and healthcare organizations continue supporting oncology innovation through cancer research funding, precision medicine initiatives, regulatory incentives, and expanded healthcare infrastructure. These public-sector investments are facilitating faster clinical development, broader patient access to innovative therapies, and continued advancement in AML drug discovery.

Key Investment Trends

- Rising investment in precision medicine, targeted therapies, and next-generation AML drug development.

- Increasing funding for immunotherapies, CAR-T cell therapies, bispecific antibodies, and antibody-drug conjugates (ADCs).

- Expansion of investment in genomic sequencing, companion diagnostics, biomarker discovery, and measurable residual disease (MRD) monitoring.

- Growing capital allocation toward AI-assisted drug discovery, clinical trials, and personalized oncology platforms.

- Higher investment in combination treatment regimens, molecular diagnostics, and translational cancer research.

- Increasing strategic collaborations among pharmaceutical companies, biotechnology firms, diagnostic developers, research institutions, and healthcare organizations.

- Continued investment in advanced biologics manufacturing, oncology R&D infrastructure, and precision healthcare technologies.

Strategic Investment Outlook

Investment activity is expected to remain robust throughout the forecast period as precision oncology continues transforming AML treatment. Future capital deployment will increasingly focus on targeted molecular therapies, immunotherapy platforms, AI-enabled drug discovery, genomic medicine, MRD-guided treatment strategies, companion diagnostics, and next-generation biologics.

Organizations investing in precision medicine platforms, innovative oncology pipelines, advanced diagnostics, personalized treatment strategies, and next-generation immunotherapies are expected to strengthen their competitive position and capitalize on the long-term growth opportunities emerging across the Global Acute Myeloid Leukemia (AML) Drugs Market.

Technology & Innovation

Global Acute Myeloid Leukemia (AML) Drugs Market Technology & Innovation Landscape Overview

The Global Acute Myeloid Leukemia (AML) Drugs Market is undergoing a significant technological transformation driven by precision oncology, molecular diagnostics, next-generation targeted therapies, immunotherapy, artificial intelligence (AI)-enabled drug discovery, and genomic medicine. Advances in biomarker identification, companion diagnostics, measurable residual disease (MRD) monitoring, and personalized treatment strategies are fundamentally reshaping AML management by enabling more accurate diagnosis, risk stratification, and individualized therapeutic interventions.

The integration of high-throughput genomic sequencing, AI-assisted clinical decision support, digital pathology, and advanced bioinformatics is accelerating the identification of actionable mutations such as FLT3, IDH1, IDH2, TP53, NPM1, and KIT, enabling physicians to select targeted therapies with improved efficacy and reduced toxicity. Simultaneously, innovations in cellular immunotherapy, antibody-drug conjugates (ADCs), bispecific antibodies, and next-generation small-molecule inhibitors are expanding treatment options for newly diagnosed as well as relapsed or refractory AML patients.

Growing investments in translational oncology research, precision medicine platforms, adaptive clinical trials, and digital health technologies are accelerating innovation across pharmaceutical companies, biotechnology firms, academic research centers, and precision oncology developers.

Global Acute Myeloid Leukemia (AML) Drugs Market Technology & Innovation Landscape Current Scenario

The current AML therapeutic landscape is characterized by the rapid adoption of targeted molecular therapies, genomic profiling, companion diagnostics, and biomarker-driven treatment selection. Healthcare providers are increasingly utilizing next-generation sequencing (NGS), liquid biopsy technologies, MRD monitoring, and AI-assisted genomic interpretation to guide personalized treatment decisions and monitor disease progression.

Innovations in targeted inhibitors, combination treatment regimens, immunotherapies, CAR-T cell research, and antibody-based therapeutics are improving clinical outcomes while minimizing treatment-related toxicity. In parallel, AI-driven drug discovery platforms, computational biology, and real-world evidence analytics are accelerating the identification of novel therapeutic targets and optimizing clinical trial design, contributing to a more efficient drug development ecosystem.

Key Technology & Innovation Landscape Trends in the Global Acute Myeloid Leukemia (AML) Drugs Market

- Precision oncology is enabling personalized treatment strategies through comprehensive genomic profiling and mutation-specific therapies.

- Next-generation sequencing (NGS) and companion diagnostics are improving molecular classification, patient stratification, and targeted therapy selection.

- FLT3 inhibitors, IDH1/IDH2 inhibitors, BCL-2 inhibitors, and emerging mutation-specific therapies continue to expand targeted treatment options.

- Measurable residual disease (MRD) monitoring using highly sensitive molecular assays is supporting early relapse detection and treatment optimization.

- Artificial intelligence and machine learning are accelerating drug discovery, biomarker identification, predictive analytics, and clinical decision support.

- Bispecific antibodies, antibody-drug conjugates (ADCs), and immune-based therapies are expanding precision immuno-oncology approaches in AML.

- CAR-T cell therapies, natural killer (NK) cell therapies, and other cellular immunotherapies are advancing clinical research for relapsed and refractory AML.

- Digital pathology, bioinformatics platforms, and cloud-based genomic analytics are improving diagnostic accuracy and precision medicine workflows.

- Adaptive clinical trial designs, real-world evidence platforms, and digital patient monitoring technologies are accelerating regulatory development and personalized care.

- Multi-omics integration, pharmacogenomics, and AI-enabled predictive modeling are supporting the development of next-generation personalized AML therapies.

Strategic Implications of Technology & Innovation in the Global Acute Myeloid Leukemia (AML) Drugs Market

Continuous investment in precision medicine, molecular diagnostics, AI-driven drug development, immunotherapy platforms, and genomic technologies has become essential for pharmaceutical companies seeking to improve patient outcomes and strengthen competitive positioning.

The convergence of genomic sequencing, companion diagnostics, MRD monitoring, bioinformatics, and AI-powered clinical analytics is enabling healthcare providers to deliver highly individualized treatment regimens while improving therapeutic efficacy and reducing unnecessary toxicity.

Pharmaceutical and biotechnology companies investing in targeted inhibitors, immunotherapies, cellular therapies, companion diagnostics, and biomarker-guided treatment strategies are expected to strengthen their leadership within the rapidly evolving AML therapeutics landscape.

Strategic collaborations among pharmaceutical companies, biotechnology firms, academic medical centers, genomic technology providers, contract research organizations, and regulatory agencies are accelerating innovation while supporting the development of next-generation precision oncology solutions.

Growing investments in AI-assisted drug discovery, gene-editing technologies, personalized immunotherapy, digital clinical trials, and translational oncology research are expected to create substantial long-term growth opportunities across the AML drugs market.

Global Acute Myeloid Leukemia (AML) Drugs Market Technology & Innovation Landscape Forward Outlook

Future innovation in the Global Acute Myeloid Leukemia (AML) Drugs Market will increasingly focus on next-generation targeted inhibitors, AI-guided drug discovery, multi-omics precision oncology, personalized immunotherapies, bispecific antibodies, antibody-drug conjugates (ADCs), CAR-T and NK cell therapies, gene-editing technologies, and highly sensitive MRD-guided treatment strategies. Advances in digital biomarkers, predictive genomics, liquid biopsy platforms, and AI-powered clinical decision support systems are expected to further enhance early diagnosis, treatment personalization, and long-term disease management.

Emerging technologies including single-cell sequencing, spatial transcriptomics, CRISPR-based therapeutic research, digital twins for oncology, and cloud-enabled precision medicine platforms are expected to accelerate therapeutic innovation. As oncology care continues to shift toward biomarker-driven and individualized treatment models, technology-enabled precision therapeutics will remain the foundation of future AML management.

Market Risk

Global Acute Myeloid Leukemia (AML) Drugs Market Risk & Disruption Analysis

The Global Acute Myeloid Leukemia (AML) Drugs Market is experiencing rapid transformation driven by precision oncology, molecular diagnostics, targeted therapies, immunotherapy, and personalized treatment approaches. While continuous innovation in AML therapeutics is expanding treatment options and improving patient outcomes, the market faces challenges related to high drug development costs, regulatory complexity, treatment resistance, reimbursement pressures, and the need for biomarker-driven patient selection.

Pharmaceutical and biotechnology companies are increasingly investing in next-generation targeted therapies, bispecific antibodies, CAR-T cell therapies, antibody-drug conjugates (ADCs), measurable residual disease (MRD)-guided treatment, AI-assisted drug discovery, and companion diagnostics to improve therapeutic efficacy and long-term survival. At the same time, evolving regulatory standards, pricing pressures, and competitive pipeline activity are reshaping commercialization strategies across the AML treatment landscape.

Global Acute Myeloid Leukemia (AML) Drugs Market Current Risk Environment

The AML drugs market is operating within a highly competitive and research-intensive oncology environment. Increasing demand for personalized medicine and mutation-specific therapies is accelerating innovation while also increasing clinical development complexity.

One of the major challenges is the high cost and lengthy timelines associated with oncology drug discovery, clinical trials, and regulatory approvals. Drug developers must demonstrate significant improvements in overall survival, safety, and quality of life before obtaining regulatory clearance.

Treatment resistance and disease relapse remain major clinical concerns, particularly among patients with aggressive genetic mutations, creating continuous demand for more effective combination therapies and novel therapeutic mechanisms.

Healthcare systems are also facing reimbursement challenges as premium-priced targeted therapies, biologics, and cellular therapies increase overall treatment costs. Additionally, expanding use of genomic testing and companion diagnostics requires greater investment in precision oncology infrastructure.

Key Market Risk & Disruption Signals

1. Increasing Complexity of Clinical Development

The growing focus on precision medicine, biomarker-driven therapies, and personalized treatment strategies is making clinical trials more complex, time-consuming, and expensive.

2. Rising Treatment Resistance & Disease Relapse

Resistance to existing therapies and relapse following treatment continue driving demand for next-generation targeted drugs, combination regimens, and innovative immunotherapies.

3. Regulatory & Approval Challenges

Stringent global regulatory requirements for oncology drugs, biologics, companion diagnostics, and cellular therapies continue extending product development timelines and commercialization risks.

4. High Cost of Advanced AML Therapies

Targeted therapies, CAR-T cell therapies, bispecific antibodies, and personalized treatments significantly increase healthcare expenditure and reimbursement challenges.

5. Rapid Advancement in Precision Medicine

Continuous discoveries in molecular profiling, genomic sequencing, and biomarker identification are rapidly changing treatment algorithms and accelerating innovation.

6. Growing Competition from Novel Therapeutic Pipelines

Expanding oncology pipelines, multiple late-stage clinical programs, and increasing pharmaceutical investments are intensifying market competition across targeted therapy segments.

7. Increasing Dependence on Companion Diagnostics

The effectiveness of targeted AML therapies increasingly depends on accurate genomic testing and molecular diagnostics, making diagnostic availability a critical success factor.

8. Expansion of AI-Driven Drug Discovery

Artificial intelligence is accelerating target identification, clinical trial optimization, biomarker discovery, and drug development, disrupting traditional pharmaceutical R&D models.

Strategic Implications of Market Risk & Disruption

1. Expansion of Precision Oncology Strategies

Pharmaceutical companies are prioritizing mutation-specific therapies, personalized treatment regimens, and biomarker-guided drug development to improve clinical outcomes.

2. Investment in Next-Generation Immunotherapies

Companies are accelerating research into CAR-T cell therapies, bispecific antibodies, antibody-drug conjugates, and cellular therapies to address unmet clinical needs.

3. Strengthening Companion Diagnostic Partnerships

Drug developers are increasingly collaborating with molecular diagnostics companies to improve patient selection and maximize therapeutic effectiveness.

4. AI-Enabled Drug Discovery & Clinical Development

Artificial intelligence is being integrated into drug discovery, genomic analysis, clinical trial design, and predictive analytics to reduce development costs and accelerate innovation.

Global Acute Myeloid Leukemia (AML) Drugs Market Risk & Disruption Forward Outlook

1. Precision Medicine Will Become the Standard of Care

Genomic profiling, molecular diagnostics, and biomarker-driven therapies will increasingly guide individualized AML treatment strategies.

2. Targeted Therapies Will Continue to Expand

Next-generation FLT3 inhibitors, IDH inhibitors, BCL-2 inhibitors, and mutation-specific therapies will strengthen treatment effectiveness and improve survival outcomes.

3. Immunotherapy Will Gain Greater Clinical Adoption

Bispecific antibodies, CAR-T cell therapies, antibody-drug conjugates, and NK-cell therapies are expected to become increasingly important treatment options.

4. AI Will Accelerate Oncology Drug Development

Artificial intelligence will improve drug discovery, biomarker identification, patient stratification, and clinical trial efficiency across AML research.

5. MRD-Guided Treatment Will Improve Disease Management

Measurable residual disease monitoring will enable earlier intervention, personalized maintenance therapy, and improved long-term patient outcomes.

6. Combination Therapy Will Become More Common

Future treatment protocols will increasingly combine targeted therapies, immunotherapies, chemotherapy, and supportive care to overcome resistance and reduce relapse rates.

7. Global Access to Innovative Therapies Will Expand

Improving healthcare infrastructure, oncology investments, and regulatory support in emerging markets will increase patient access to advanced AML treatments.

8. Companion Diagnostics Will Become Essential

Integrated genomic testing and companion diagnostics will become fundamental components of AML diagnosis, treatment selection, and ongoing disease monitoring.

Regulatory Landscape

Global Acute Myeloid Leukemia (AML) Drugs Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a fundamental role in shaping the Global Acute Myeloid Leukemia (AML) Drugs Market by governing the research, clinical development, approval, manufacturing, commercialization, and post-market surveillance of AML therapeutics. Regulatory authorities oversee targeted therapies, chemotherapy agents, immunotherapies, monoclonal antibodies, cellular therapies, and companion diagnostics through rigorous clinical evaluation, pharmaceutical quality standards, pharmacovigilance, and precision medicine frameworks. As personalized oncology advances, regulatory focus is increasingly directed toward biomarker-driven therapies, accelerated approvals, and companion diagnostic integration.

The market is primarily influenced by U.S. FDA oncology regulations, European Medicines Agency (EMA) guidelines, ICH (International Council for Harmonisation) standards, Good Clinical Practice (GCP), Good Manufacturing Practice (GMP), Orphan Drug regulations, companion diagnostic approval frameworks, pharmacovigilance requirements, and regional health technology assessment (HTA) policies. These regulatory frameworks support the safe, effective, and timely development and commercialization of innovative AML therapies.

Global Acute Myeloid Leukemia (AML) Drugs Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape emphasizes accelerated development of targeted oncology therapies, precision medicine, companion diagnostics, real-world evidence generation, and long-term patient safety monitoring. Regulatory agencies continue supporting expedited pathways for innovative AML treatments addressing unmet medical needs while maintaining stringent standards for clinical efficacy, manufacturing quality, and pharmacovigilance.

Healthcare authorities are also strengthening requirements for molecular diagnostics, biomarker validation, post-marketing safety surveillance, risk management plans, and evidence supporting combination therapies and personalized treatment strategies. Increasing attention is being given to integrating genomic testing into treatment decisions and improving patient access to precision oncology medicines.

Key Regulatory & Policy Environment Signals in the Global Acute Myeloid Leukemia (AML) Drugs Market

1. Oncology Drug Approval & Clinical Development

Regulatory agencies continue strengthening clinical evaluation requirements for AML therapies, emphasizing robust efficacy data, overall survival outcomes, safety monitoring, and expedited review pathways for therapies addressing unmet medical needs.

2. Precision Medicine & Companion Diagnostic Regulation

Authorities increasingly require validated companion diagnostics, molecular biomarker testing, and genomic profiling to support personalized treatment selection and safe use of targeted AML therapies.

3. Pharmaceutical Manufacturing & Quality Compliance

Global GMP standards, pharmaceutical quality systems, and manufacturing inspections continue ensuring consistent production quality, product integrity, and regulatory compliance across oncology drug manufacturing.

4. Pharmacovigilance & Post-Marketing Safety Monitoring

Regulators are expanding pharmacovigilance requirements through continuous adverse event reporting, long-term safety monitoring, risk management plans, and real-world evidence collection for approved AML therapies.

5. Orphan Drug & Market Access Policies

Orphan drug incentives, reimbursement evaluations, health technology assessments (HTAs), and pricing frameworks continue supporting innovation while influencing patient access to advanced AML treatments across global healthcare systems.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging pharmaceutical companies and biotechnology developers to accelerate precision oncology innovation while strengthening compliance across clinical development, companion diagnostics, manufacturing quality, and post-market surveillance. Companies are increasing investment in biomarker-driven drug development, genomic medicine, real-world evidence generation, regulatory science, and global clinical programs to meet evolving approval requirements.

Manufacturers capable of delivering clinically validated, precision-targeted, high-quality, and regulatory-compliant AML therapies are expected to strengthen their competitive position as personalized oncology and targeted treatment strategies continue to expand worldwide.

Global Acute Myeloid Leukemia (AML) Drugs Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, regulatory frameworks are expected to place greater emphasis on precision oncology, biomarker-guided approvals, companion diagnostics, accelerated regulatory pathways, real-world evidence integration, and advanced cellular and targeted therapies. Regulatory agencies are likely to strengthen guidance supporting personalized medicine while expanding frameworks governing genomic diagnostics, innovative biologics, and combination treatment regimens.

Future policy developments are also expected to promote greater international harmonization of oncology clinical standards, companion diagnostic regulations, pharmacovigilance systems, and precision medicine frameworks, supporting continued innovation across the AML therapeutic landscape.