Global Tyre Recycling & Circular Economy Market size, share & Forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

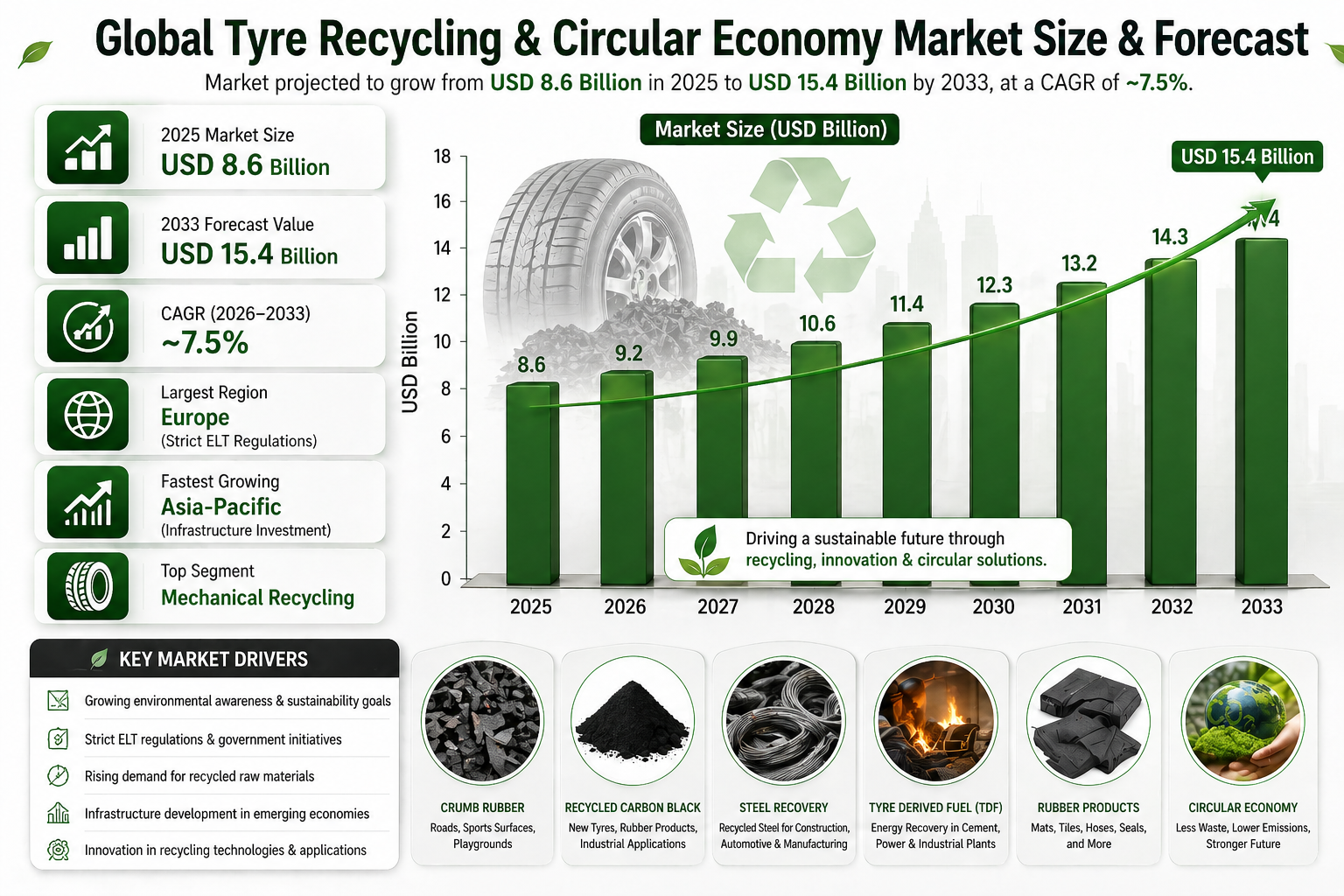

| 2025 Market Size | USD 8.6 Billion |

| 2033 Market Size | USD 15.4 Billion |

| CAGR | ~7.5% |

| Largest Region | Europe |

| Fastest-Growing Region | Asia-Pacific |

| Largest Segment | Mechanical recycling |

| Fastest-Growing Segment | Pyrolysis & closed-loop recycling |

| Key Trend | Tyre-to-tyre circularity |

Global Tyre Recycling & Circular Economy Market Overview

The Global Tyre Recycling & Circular Economy Market is all about turning old, worn-out tyres into something useful again???think recycling, material recovery, and reuse . With around 1.8???2 billion tyres hitting end-of-life every year, managing that waste is a huge environmental and regulatory challenge. Instead of just dumping them, companies are finding ways to extract value, like making rubber crumbs, fuel, or even new products. It???s a growing, eco-friendly industry that???s becoming super important worldwide.

Old-school tyre disposal like landfilling and random stockpiling is pretty much dead in developed countries???too risky with fires, pollution, and space issues . Now, governments and tyre makers treat tyres as valuable resources, not trash, pushing circular economy ideas. They???re recycling and repurposing tyres into new products, fuel, or materials. It???s a smarter, greener way to handle tyre waste and keep the planet cleaner.

The Global Tyre Recycling & Circular Economy Market is turning old tyres into treasure???rubber granules, recycled carbon black, steel, fibres, oils, and gas???used in construction, cars, infrastructure, energy, and manufacturing . Cool tech like pyrolysis and devulcanization upgrades waste into high-value materials. Instead of trash, tyres become raw materials for new products.

According to the Pheonix Demand Forecast Engine, the Global Tyre Recycling & Circular Economy Market size is valued at USD 8.6 billion in 2025 and is projected to reach USD 15.4 billion by 2033, expanding at a CAGR of ~7.5% during 2026???2033.

Europe currently leads the market due to strict ELT regulations and high recycling penetration, while Asia-Pacific is the fastest-growing region, driven by rising tyre consumption, regulatory tightening, and investment in recycling infrastructure.

Key Drivers of Global Tyre Recycling & Circular Economy Market Growth

Rising End-of-Life Tyre Generation

Global vehicle parc expansion and shorter tyre replacement cycles are driving market growth , increasing ELT volumes year-on-year.

Stringent Environmental Regulations

Landfill bans, extended producer responsibility (EPR) laws, and waste management directives are accelerating recycling adoption.

Shift Toward Circular Economy Models

OEMs and governments are prioritizing closed-loop systems that reintegrate recycled tyre materials into new tyres and products.

Advancements in Recycling Technologies

Innovations in pyrolysis, devulcanization, and rCB production are improving economic viability and material quality.

Growing Demand for Sustainable Raw Materials

Recycled rubber and rCB are driving market growth , helping manufacturers reduce carbon footprint and dependence on virgin materials.

Global Tyre Recycling & Circular Economy Market Segmentation

1. By Recycling Process

1.1 Mechanical Recycling??

1.1.1 Ambient Grinding

?? ?? ??1.1.1.1 Rubber crumb production

?? ?? ??1.1.1.2 Steel separation

1.1.2 Cryogenic Grinding

?? ?? ??1.1.2.1 Fine rubber powder

?? ?? ??1.1.2.2 High-purity granulates

1.2 Pyrolysis

1.2.1 Thermal Pyrolysis

?? ?? ?? 1.2.1.1 Pyrolysis oil recovery

?? ?? ?? 1.2.1.2 Syngas generation

1.2.2 Advanced / Continuous Pyrolysis

?? ?? ??1.2.2.1 Recovered carbon black (rCB)

?? ?? ??1.2.2.2 High-efficiency reactors

1.3 Devulcanization

1.3.1 Mechanical Devulcanization

?? ?? ?? 1.3.1.1 Reclaimed rubber compounds

1.3.2 Chemical & Microwave Devulcanization

?? ?? ?? 1.3.2.1 High-quality rubber recovery

1.4 Energy Recovery

1.4.1 Tire-Derived Fuel (TDF)

?? ?? ??1.4.1.1 Cement kilns

?? ?? ??1.4.1.2 Industrial boilers

2. By Recovered Material Type

2.1 Recycled Rubber??

2.1.1 Rubber Crumb & Granules

?? ?? ?? 2.1.1.1 Playground surfaces

?? ?? ?? 2.1.1.2 Sports flooring

2.1.2 Rubber Powder

?? ?? ?? 2.1.2.1 Asphalt modification

?? ?? ?? 2.1.2.2 Molded rubber goods

2.2 Recovered Carbon Black??

2.2.1 Semi-Reinforcing rCB

?? ?? ?? 2.2.1.1 Tyres & rubber products

2.2.2 Specialty-Grade rCB

?? ?? ?? 2.2.2.1 Plastics & coatings

2.3 Recovered Steel

2.3.1 High-Carbon Steel

?? ?? ?? 2.3.1.1 Construction & metal recycling

2.4 Recovered Oils & Gases

2.4.1 Pyrolysis Oil

?? ?? ?? 2.4.1.1 Industrial fuel

?? ?? ?? 2.4.1.2 Chemical feedstock

3. By Application

3.1 Construction & Infrastructure

3.1.1 Asphalt & Road Construction

?? ?? ?? 3.1.1.1 Rubber-modified asphalt

3.1.2 Civil Engineering

?? ?? ?? 3.1.2.1 Shock absorption layers

3.2 Automotive & Tyre Manufacturing

3.2.1 Tyre Compounds

?? ?? ?? 3.2.1.1 Partial virgin material replacement

3.2.2 Automotive Components

?? ?? ?? 3.2.2.1 Mats, seals, gaskets

3.3 Sports & Leisure Surfaces

3.3.1 Playgrounds

?? ?? ?? 3.3.3.1 Safety flooring

3.3.2 Athletic Tracks

?? ?? ?? 3.3.2.2 Synthetic turf infill

3.4 Industrial & Energy Use

3.4.1 Cement Manufacturing

?? ?? ?? 3.4.1.1 Alternative fuels

4. By Tyre Source

4.1 Passenger Vehicle Tyres??

4.1.1 Passenger Cars

?? ?? ??4.1.1.1 Urban recycling streams

4.2 Commercial Vehicle Tyres

4.2.1 Truck & Bus Tyres

?? ?? ?? 4.2.1.1 High material recovery value

4.3 Off-the-Road (OTR) Tyres

4.3.1 Mining & Construction Tyres

?? ?? ?? 4.3.1.1 Large-scale recycling

5. By Circular Economy Model

5.1 Open-Loop Recycling??

5.1.1 Downcycled Applications

?? ?? ?? 5.1.1.1 Flooring, mats, fuel

5.2 Closed-Loop Recycling??

5.2.1 Tyre-to-Tyre Recycling

?? ?? ?? ??5.2.1.1 rCB reintegration

?? ?? ?? ??5.2.1.2 Reclaimed rubber compounds

5.3 Extended Producer Responsibility (EPR) Systems

5.3.1 OEM-Led Collection Programs

?? ?? ?? 5.3.1.1 Manufacturer-funded recycling

6. By Geography

6.1 Europe (Largest Region)

Germany

France

U.K.

Italy

6.2 Asia-Pacific (Fastest-Growing Region)

China

India

Japan

Southeast Asia

6.3 North America

U.S.

Canada

6.4 Latin America

Brazil

Mexico

6.5 Middle East & Africa

Regional Insights

Europe

Strong ELT regulations, landfill bans, and mature EPR systems make Europe the global leader in tyre recycling efficiency.

Asia-Pacific

Rapid vehicle growth, rising ELT volumes, and increased investment in pyrolysis and recycling infrastructure drive the fastest growth.

North America

Well-established recycling networks and growing adoption of rCB in tyre manufacturing.

Latin America & MEA

Emerging regulatory frameworks and growing awareness support long-term growth potential.

Leading Companies in the Global Tyre Recycling & Circular Economy Market

Liberty Tire Recycling

Genan Holding

Pyrum Innovations

Scandinavian Enviro Systems

GreenMantra Technologies

Ecolomondo

Bolder Industries

Recovered Carbon Black International

Liberty Tire Recycling is the largest company in the Global Tyre Recycling & Circular Economy Market

Strategic Intelligence & Pheonix AI Insights

-

ELT Volume Forecast Model ??? Tracks end-of-life tyre generation by region

-

Material Recovery Yield Engine ??? Evaluates rCB and rubber recovery economics

-

Circularity Index Scoring ??? Measures tyre-to-tyre recycling penetration

Porter???s Five Forces (Brief)

-

Buyer Power: Moderate

-

Supplier Power: Low

-

Threat of New Entrants: Moderate

-

Threat of Substitutes: Low

-

Competitive Rivalry: Moderate???High

Why the Tyre Recycling & Circular Economy Market Is Critical

The Tyre Recycling & Circular Economy Market is critical due to the rapidly growing volume of end-of-life tyres and the urgent need for sustainable waste management. With billions of tyres discarded annually, recycling prevents landfill accumulation, environmental pollution, and fire hazards.

This market enables a circular economy transition by recovering valuable materials such as rubber, steel, carbon black, and oils, reducing dependence on virgin raw materials and lowering production costs. It also supports carbon reduction goals, as recycled tyre materials generate significantly lower emissions compared to new material production.

Final Takeaway

The Global Tyre Recycling & Circular Economy Market is transitioning from waste management to a strategic raw-material recovery industry. As regulations tighten and OEMs commit to sustainability targets, advanced recycling technologies such as pyrolysis and devulcanization will redefine value creation. Players that enable high-quality material recovery, OEM integration, and closed-loop recycling will lead the next phase of market growth through 2033.

Competitive Landscape

Global Tyre Recycling & Circular Economy Competitive Intensity & Market Structure Overview

The Global Tyre Recycling & Circular Economy Market is characterized by a regulation-driven, sustainability-focused, and technology-evolving competitive landscape, where environmental compliance, material recovery efficiency, and circular value creation define long-term market leadership. Unlike traditional tyre manufacturing or replacement markets, this sector is structurally built around end-of-life tyre (ELT) collection, processing, and transformation into reusable raw materials, energy products, or closed-loop manufacturing inputs.

The market operates through a multi-layered ecosystem that includes ELT collection systems, mechanical recyclers, pyrolysis operators, devulcanization specialists, and recovered material suppliers. Competitive intensity is moderate to high, with increasing differentiation based on processing technology, recovery yield quality, regulatory alignment, and ability to support tyre-to-tyre circularity.

Market concentration is moderate, with regional leaders dominating ELT collection and mechanical recycling, while advanced pyrolysis and recovered carbon black (rCB) segments remain more fragmented but rapidly evolving. Europe currently leads structural maturity due to regulatory sophistication, while Asia-Pacific is emerging as the next major growth engine due to rising ELT volumes and infrastructure expansion.

Global Tyre Recycling & Circular Economy Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Liberty Tire Recycling: Global market leader with strong ELT collection infrastructure, large-scale recycling capacity, and diversified downstream applications.

Genan Holding: Major international recycler known for advanced mechanical recycling and high-volume material recovery systems.

Pyrum Innovations: Technology-focused leader in advanced pyrolysis and recovered carbon black innovation with growing OEM partnerships.

Scandinavian Enviro Systems: Circular economy specialist focused on tyre-to-tyre recycling and premium-grade recovered carbon black solutions.

GreenMantra Technologies: Advanced materials innovator leveraging recycled polymers and tyre-derived feedstocks for specialty applications.

Ecolomondo: Pyrolysis technology player focused on scalable resource recovery and sustainable industrial feedstocks.

Bolder Industries: High-growth rCB producer focused on premium material recovery and sustainable supply chains.

Recovered Carbon Black International: Specialized player supporting circular carbon black integration across manufacturing sectors.

Key Competitive Intensity & Market Structure Signals in Global Tyre Recycling & Circular Economy Market

A key structural signal is the increasing shift from open-loop recycling toward closed-loop tyre-to-tyre systems, where recovered carbon black, reclaimed rubber, and sustainable feedstocks are reintegrated into tyre manufacturing.

Another major signal is the growing importance of pyrolysis and devulcanization technologies, which are rapidly reshaping competitive differentiation by enabling higher-value material recovery compared to traditional crumb rubber pathways.

Regulatory frameworks such as landfill bans, ELT mandates, and extended producer responsibility (EPR) systems remain critical structural forces, particularly in Europe, where compliance standards significantly influence market participation.

OEM sustainability commitments are also intensifying competition, as tyre manufacturers increasingly seek reliable recycled material streams that align with ESG goals and carbon reduction targets.

Strategic Implications of Competitive Intensity & Market Structure in Global Tyre Recycling & Circular Economy Market

Recycling companies must prioritize technology investment, as higher-value outputs such as rCB, reclaimed rubber, and chemical feedstocks provide stronger profitability than low-margin downcycled applications.

Partnerships with OEMs and tyre manufacturers are becoming increasingly strategic, as closed-loop recycling systems offer long-term demand security and premium positioning.

Scale and ELT sourcing infrastructure remain critical, since consistent feedstock access directly impacts utilization rates, economics, and market competitiveness.

Regional policy alignment is essential, particularly in markets adopting stricter waste regulations and circular economy mandates. Companies positioned early in high-compliance markets gain structural advantage.

Global Tyre Recycling & Circular Economy Competitive Intensity & Market Structure Forward Outlook

The Global Tyre Recycling & Circular Economy Market is expected to evolve from a waste-management-oriented industry into a strategic raw-material recovery and sustainability ecosystem.

Competitive intensity will increasingly center on advanced processing technologies, circular integration capabilities, and quality of recovered materials rather than purely collection or disposal scale.

Market consolidation is likely in mature recycling segments, while advanced pyrolysis, devulcanization, and tyre-to-tyre recycling may remain innovation-driven battlegrounds with strong growth potential.

In the long term, the market will be shaped by three strategic pillars: closed-loop tyre circularity, advanced material recovery technology, and OEM-aligned sustainability integration. Companies that successfully align with these trends will lead the Global Tyre Recycling & Circular Economy Market through 2033.

Value Chain

Global Tyre Recycling & Circular Economy Market Value Chain & Supply Chain Evolution Overview

The Global Tyre Recycling & Circular Economy Market value chain is evolving from a basic waste disposal system into a structured, technology-driven resource recovery ecosystem. Instead of treating end-of-life tyres as environmental waste, the industry now views them as valuable secondary raw materials that can be reintegrated into manufacturing, infrastructure, energy, and industrial applications. This shift is driven by circular economy policies, stricter environmental regulations, and rising demand for sustainable materials.

The value chain begins with tyre collection, which includes municipal waste systems, tyre retailers, automotive workshops, fleet operators, and dedicated collection agencies. These tyres are then transported to sorting and pre-processing facilities where they are inspected, graded, and categorized based on size, material condition, and potential recovery route. Efficient collection and logistics systems are critical, as they directly impact recycling economics and material recovery efficiency.

The core of the value chain lies in recycling and processing technologies, including mechanical recycling, pyrolysis, devulcanization, and energy recovery systems. Mechanical recycling converts tyres into rubber crumb, granules, and powder, while pyrolysis breaks down tyres into oil, gas, steel, and recovered carbon black (rCB). Devulcanization processes enable partial restoration of rubber properties, allowing reuse in new rubber products, while energy recovery converts tyres into industrial fuel alternatives such as tire-derived fuel (TDF).

Once processed, recovered materials enter downstream industrial markets, where they are used in construction materials, asphalt modification, automotive components, sports surfaces, industrial goods, and chemical feedstocks. Recovered steel is reintegrated into metal industries, while recovered carbon black is increasingly being used as a sustainable alternative to virgin carbon black in tyre manufacturing and plastics.

The supply chain is increasingly influenced by Extended Producer Responsibility (EPR) systems, which require tyre manufacturers and importers to finance or manage end-of-life tyre collection and recycling. This regulatory push is strengthening formal recycling networks while reducing illegal dumping and informal disposal practices.

Global Tyre Recycling & Circular Economy Market Value Chain & Supply Chain Evolution Current Scenario

The current market is characterized by rapid expansion of recycling infrastructure, increasing adoption of advanced pyrolysis technologies, and rising integration of recycled materials into mainstream industrial applications. Europe leads in structured recycling systems due to strict landfill bans and mature EPR frameworks, while Asia-Pacific is expanding rapidly due to rising tyre consumption and growing regulatory enforcement.

Mechanical recycling remains the most widely used process globally due to its cost efficiency and scalability, particularly for producing rubber crumb used in construction and infrastructure applications. However, pyrolysis and closed-loop recycling technologies are gaining momentum due to their ability to produce higher-value outputs such as rCB and pyrolysis oil.

Supply chain integration is improving as recycling companies collaborate more closely with tyre manufacturers, construction firms, and industrial users. This is enabling greater material traceability, improved quality standards, and increased acceptance of recycled inputs in high-performance applications.

At the same time, challenges persist in the form of fragmented collection systems, inconsistent feedstock quality, high capital investment requirements for advanced recycling technologies, and limited awareness in emerging markets.

Despite these challenges, demand for sustainable raw materials is steadily increasing, driven by ESG commitments, carbon reduction targets, and cost advantages over virgin materials.

Key Value Chain & Supply Chain Evolution Signals in Global Tyre Recycling & Circular Economy Market

- Shift Toward Closed-Loop Recycling: Increasing reintegration of recycled materials into new tyre production.

- Growth of Pyrolysis Technology: Expansion of rCB and pyrolysis oil production for industrial applications.

- EPR-Driven Collection Systems: Regulatory frameworks mandating producer responsibility for end-of-life tyres.

- Rising Industrial Demand for Recycled Materials: Construction, automotive, and manufacturing sectors adopting recycled inputs.

- Integration of Circular Economy Models: Transition from linear disposal to multi-cycle material recovery systems.

- Material Quality Standardization: Improved processing technologies ensuring consistent recycled output quality.

- Expansion of Recycling Infrastructure: Increased investment in regional recycling plants and processing facilities.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Tyre Recycling & Circular Economy Market

The evolving value chain is redefining competitive dynamics by shifting focus from waste disposal services to high-value material recovery and industrial supply integration. Companies such as Liberty Tire Recycling, Genan Holding, and Pyrum Innovations are strengthening their positions by investing in advanced recycling technologies and expanding regional processing capacity.

Tyre manufacturers are increasingly participating in closed-loop systems, using recovered carbon black and recycled rubber in new tyre production to meet sustainability targets and reduce raw material dependency.

Construction and infrastructure industries are becoming major demand centers for recycled rubber products, particularly in asphalt modification, shock absorption systems, and civil engineering applications.

Energy-intensive industries such as cement manufacturing are adopting tyre-derived fuel as a cost-effective and lower-carbon alternative to traditional fossil fuels.

Overall, companies that can efficiently integrate collection systems, advanced recycling technologies, and high-value end-user applications will gain a strong competitive advantage in the evolving circular economy landscape.

Global Tyre Recycling & Circular Economy Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to become more technologically advanced, regulation-driven, and fully circular, with increasing emphasis on tyre-to-tyre recycling systems and high-performance material recovery.

Pyrolysis and advanced recycling technologies are expected to become mainstream, supported by improvements in efficiency, scalability, and output quality, particularly for recovered carbon black and synthetic fuels.

Closed-loop systems will expand significantly, enabling greater reintegration of recycled materials into tyre manufacturing and reducing dependence on virgin raw materials.

EPR frameworks and global sustainability regulations will continue to strengthen collection efficiency and formalize recycling supply chains, especially in emerging markets.

Ultimately, the market will transition from fragmented waste management operations to a globally integrated circular materials industry, where end-of-life tyres become a critical input for sustainable industrial production systems.

Market-Specific Value Chain

- Tyre Collection: Retailers, fleets, municipal systems, and scrap aggregators collecting end-of-life tyres

- Logistics & Sorting: Transportation, grading, and classification based on tyre condition and recycling route

- Pre-Processing: Shredding, steel removal, size reduction, and material separation

- Recycling & Processing: Mechanical recycling, pyrolysis, devulcanization, energy recovery

- Material Recovery: Rubber crumb, rCB, steel, oils, gas, and rubber powder production

- Industrial Applications: Construction, automotive, energy, infrastructure, and manufacturing usage

- Circular Reintegration: Closed-loop use in new tyre production and advanced materials

Company-to-Stage Mapping

- Collection & Logistics: Liberty Tire Recycling, regional waste management firms

- Recycling & Processing: Genan Holding, Pyrum Innovations, Scandinavian Enviro Systems

- Material Innovation: GreenMantra Technologies, Bolder Industries, Ecolomondo

- Recovered Carbon Black: Recovered Carbon Black International, specialty rCB producers

- Industrial Application Users: Construction companies, tyre manufacturers, cement producers

- Closed-Loop Integration: Michelin, Bridgestone, Continental AG sustainability programs

Investment Activity

Global Tyre Recycling & Circular Economy Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Tyre Recycling & Circular Economy Market are being driven by accelerating end-of-life tyre (ELT) volumes, stringent environmental regulations, OEM sustainability commitments, and rising global demand for recycled raw materials. Between 2026 and 2033, capital allocation is expected to increasingly prioritize advanced pyrolysis systems, devulcanization technologies, recovered carbon black (rCB) production, tyre-to-tyre circularity platforms, and scalable ELT collection infrastructure.

The market is highly infrastructure- and technology-intensive, requiring sustained investment in material recovery systems, automated sorting networks, chemical recycling technologies, thermal conversion platforms, and circular supply chain ecosystems. Leading players such as Liberty Tire Recycling, Genan, Pyrum Innovations, Scandinavian Enviro Systems, and Bolder Industries are significantly expanding investments in next-generation recycling capacity, OEM partnerships, and recovered material commercialization.

A major structural transformation shaping investment flows is the evolution of tyre recycling from waste disposal into strategic raw material recovery. This shift is directing funding toward closed-loop systems that transform ELTs into reusable rubber, steel, oils, and carbon black capable of re-entering automotive and industrial manufacturing ecosystems.

Global Tyre Recycling & Circular Economy Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by tightening landfill bans, EPR mandates, carbon reduction frameworks, and increasing demand for sustainable feedstocks. Governments, tyre OEMs, and recycling innovators are increasingly collaborating to establish integrated circular economy systems.

- Europe: Leads global investment activity due to mature ELT regulations, advanced EPR systems, landfill restrictions, and strong tyre-to-tyre circularity initiatives.

- Asia-Pacific: Fastest-growing investment region, fueled by rising tyre consumption, increasing ELT volumes, regulatory tightening, and large-scale recycling infrastructure expansion.

- North America: Strong investment momentum supported by established recycling networks, growing rCB commercialization, and expanding sustainability commitments.

- Latin America & Middle East & Africa: Emerging markets seeing gradual investment growth through regulatory modernization, industrial demand, and improving waste management frameworks.

Key Investment & Funding Dynamics Signals in Global Tyre Recycling & Circular Economy Market

- Rising ELT generation is driving long-term capital inflows into scalable collection, sorting, and processing infrastructure.

- Growing demand for recycled carbon black and reclaimed rubber is accelerating investment in advanced pyrolysis and devulcanization technologies.

- OEM sustainability targets are increasing funding into tyre-to-tyre circularity systems that reintegrate recycled materials into new tyre production.

- Government regulations banning landfill disposal are strengthening investor confidence in recycling economics and circular infrastructure expansion.

- Material science innovation is unlocking premium applications for recovered tyre materials across automotive, construction, industrial, and energy sectors.

Strategic Implications of Investment & Funding Dynamics in Global Tyre Recycling & Circular Economy Market

- The investment landscape strongly favors companies with scalable recovery technologies, material purity capabilities, and OEM-grade recycled feedstock integration.

- Strategic partnerships with tyre manufacturers, municipal systems, logistics providers, and industrial buyers are becoming critical competitive differentiators.

- Technological leadership increasingly centers on maximizing recovery yield, improving rCB quality, and enabling true closed-loop tyre manufacturing.

- Regional diversification remains essential, with Europe leading policy-driven innovation, Asia-Pacific driving scale, and North America focusing on commercialization and material economics.

- Feedstock consistency, regulatory complexity, and technology scalability remain key investment risks influencing funding deployment.

Global Tyre Recycling & Circular Economy Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Tyre Recycling & Circular Economy Market is expected to attract strong and sustained investment as recycled tyre materials become strategic inputs for sustainable manufacturing and carbon reduction.

Future capital allocation will increasingly prioritize closed-loop tyre production, AI-driven material recovery optimization, premium rCB commercialization, advanced chemical recycling, and global ELT infrastructure modernization.

- Europe: Will remain the dominant investment hub due to regulatory leadership, circular economy maturity, and advanced tyre-to-tyre recycling ecosystems.

- Asia-Pacific: Will experience the highest investment acceleration through infrastructure scale-up, ELT volume growth, and industrial recycling adoption.

- North America: Will expand investments in premium material recovery technologies, rCB market development, and sustainability-focused industrial applications.

Digital traceability systems, lifecycle carbon accounting, and circularity scoring frameworks will increasingly shape future funding decisions and strategic partnerships.

Overall, the market will maintain robust growth through 2033, supported by its essential role in waste reduction, raw material security, and industrial decarbonization. Companies that align advanced recycling technology, closed-loop innovation, regulatory integration, and OEM collaboration will be best positioned to lead the next phase of tyre circular economy transformation.

Technology & Innovation

Global Tyre Recycling & Circular Economy Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global tyre recycling & circular economy market is being shaped by the urgent need to transform end-of-life tyres (ELTs) from environmental waste into valuable secondary raw materials. With billions of tyres reaching disposal stage globally, innovation is heavily focused on advanced material recovery, circular reintegration, carbon reduction, and scalable recycling economics rather than traditional waste disposal. Innovation intensity in this market is high and accelerating, supported by breakthroughs in pyrolysis, devulcanization, recovered carbon black (rCB), and closed-loop tyre-to-tyre recycling systems. While mechanical recycling remains the dominant installed base, advanced recycling technologies are reshaping the market by enabling higher-value outputs such as specialty-grade rCB, reclaimed rubber, pyrolysis oil, and sustainable feedstocks for tyre manufacturing. Leading players including Liberty Tire Recycling, Genan Holding, Pyrum Innovations, Scandinavian Enviro Systems, GreenMantra Technologies, and Bolder Industries are investing aggressively in scalable circular technologies. A major technological shift is the transition from open-loop recycling (crumb rubber, fuel, mats) toward closed-loop recycling systems where recovered materials are reintegrated into new tyre production. This shift is being driven by OEM sustainability commitments, stricter environmental regulations, and the need to reduce dependence on virgin carbon black, synthetic rubber, and fossil-based inputs. AI-enabled sorting, automation, and advanced chemical recovery are further improving recovery yields and operational economics.

Global Tyre Recycling & Circular Economy Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global tyre recycling & circular economy market is centered on maximizing material recovery efficiency, improving recovered material quality, and scaling circular business models. Mechanical recycling continues to dominate due to established infrastructure and lower capital intensity, particularly for rubber crumb, granules, and civil engineering applications. Pyrolysis is emerging as the fastest-growing innovation segment, offering the ability to recover oil, syngas, steel, and recovered carbon black from ELTs. Continuous pyrolysis systems are improving scalability, energy efficiency, and product consistency, making them increasingly attractive for industrial adoption. Devulcanization technologies are advancing rapidly, allowing rubber to be chemically or mechanically reprocessed for reuse in higher-value applications. This is particularly important for tyre-to-tyre circularity, where reclaimed rubber can partially replace virgin elastomers. Recovered carbon black (rCB) innovation is a core strategic area, as tyre manufacturers seek sustainable alternatives to virgin carbon black. Improvements in purification, particle consistency, and reinforcement quality are increasing rCB’s suitability for premium tyre and industrial applications. Automation and AI are improving sorting, shredding, and contamination control across recycling facilities. Smart process monitoring enhances operational efficiency while reducing energy consumption and waste. Sustainability-led manufacturing integration is also growing, with tyre OEMs increasingly partnering with recycling firms to secure circular raw material streams and meet ESG targets.

Key Technology & Innovation Landscape Signals in Global Tyre Recycling & Circular Economy Market

- Advanced Pyrolysis Systems: Rapid growth in continuous and high-efficiency pyrolysis technologies for rCB, oil, and syngas recovery.

- Closed-Loop Tyre-to-Tyre Recycling: Increasing investment in systems that reintegrate recycled rubber and rCB into new tyre manufacturing.

- Recovered Carbon Black (rCB) Innovation: Rising focus on premium-grade rCB for tyre and industrial reinforcement applications.

- Devulcanization Advancements: Improved chemical and mechanical methods enabling higher-quality reclaimed rubber.

- AI & Automation Integration: Smart sorting, contamination detection, and process optimization improving material recovery efficiency.

- Sustainable Feedstock Substitution: Growing use of recycled materials to reduce virgin raw material dependency.

- EPR & OEM Circular Partnerships: Stronger collaboration between tyre manufacturers and recyclers to meet sustainability mandates.

Strategic Implications of Technology & Innovation Landscape in Global Tyre Recycling & Circular Economy Market

The evolving technology landscape has major strategic implications for recyclers, tyre manufacturers, material suppliers, and regulators. Companies that invest in high-yield recycling systems and premium recovered materials will gain competitive advantages as the industry transitions from disposal to resource recovery. The shift toward tyre-to-tyre circularity is redefining market economics by positioning ELTs as strategic raw material assets rather than waste streams. This creates long-term opportunities for OEM partnerships, circular supply chains, and ESG leadership. Pyrolysis and devulcanization technologies are becoming critical differentiators, enabling higher margins through premium outputs instead of low-value commodity recycling. Firms that can scale advanced systems while maintaining material consistency will lead next-generation market growth. AI and automation are also reshaping competitiveness by lowering operational costs, improving throughput, and increasing material purity. Smart recycling plants are expected to outperform traditional systems in both economics and sustainability metrics. For tyre manufacturers, access to reliable recycled material streams will become strategically important for regulatory compliance, carbon footprint reduction, and raw material cost diversification.

Global Tyre Recycling & Circular Economy Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the global tyre recycling & circular economy market is expected to evolve toward more technologically advanced, circular, and OEM-integrated systems. Closed-loop recycling will likely become a core strategic objective as tyre manufacturers increase recycled-content integration. Pyrolysis is projected to see major commercialization growth, particularly in recovered carbon black and chemical feedstock markets. Advances in reactor design, purification, and emissions control will improve scalability and profitability. Devulcanization is expected to gain stronger industrial relevance as material science improves reclaimed rubber performance for premium applications. This could significantly expand tyre-to-tyre circularity beyond current thresholds. AI-enabled smart recycling plants will become increasingly common, using predictive analytics, robotics, and digital twins to optimize ELT processing and material output. Policy frameworks such as EPR mandates, landfill bans, and recycled-content regulations will continue accelerating innovation and infrastructure investment globally. In conclusion, the Global Tyre Recycling & Circular Economy Market is transitioning from traditional waste management to a strategic materials recovery and sustainability ecosystem. Companies that lead in advanced recycling technology, premium material recovery, and scalable closed-loop integration will be best positioned to dominate the market through 2033.

Market Risk

Global Tyre Recycling & Circular Economy Market Risk Factors & Disruption Threats Overview

The Global Tyre Recycling & Circular Economy Market operates within an increasingly regulation-driven sustainability ecosystem, where end-of-life tyre (ELT) management is transitioning from waste disposal to strategic material recovery. While the market benefits from tightening landfill bans, circular economy mandates, and rising demand for recycled raw materials, it carries a moderate to high strategic risk profile due to recycling technology scalability challenges, commodity value fluctuations, regulatory fragmentation, and output quality consistency constraints. A major structural risk is economic dependency on recovered material value. Markets for recycled rubber, recovered carbon black (rCB), pyrolysis oil, and reclaimed steel are highly sensitive to virgin material pricing, oil prices, and industrial demand cycles. If virgin alternatives become cheaper, recycled product competitiveness can weaken materially. Another major disruption factor is technological scalability. Advanced pyrolysis, devulcanization, and tyre-to-tyre closed-loop systems require significant capital investment, process efficiency, and consistent output quality. Many recycling technologies remain commercially promising but operationally uneven across scale. Regulatory inconsistency also creates disruption complexity. While Europe leads with mature ELT and EPR systems, regulatory enforcement varies significantly across Asia-Pacific, Latin America, and emerging economies, limiting uniform global adoption. Additionally, environmental scrutiny of certain recycling methods’particularly emissions-intensive pyrolysis or poorly regulated energy recovery’can create compliance and reputation risks if sustainability claims fail validation.

Global Tyre Recycling & Circular Economy Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong structural momentum driven by rising ELT volumes, government regulation, and OEM sustainability commitments. However, commercialization outcomes remain uneven across technologies and geographies. Mechanical recycling remains the dominant segment due to established infrastructure, lower capital intensity, and broad downstream applications. Pyrolysis and recovered carbon black are rapidly gaining investment attention, but economic viability still depends on scale efficiency, energy economics, and OEM-grade output consistency. OEMs are increasingly prioritizing tyre-to-tyre circularity, placing pressure on recyclers to deliver material quality suitable for reintegration into premium tyre manufacturing. Meanwhile, infrastructure gaps in collection, sorting, and ELT logistics continue to constrain growth in developing regions.

Key Risk Factors & Disruption Threats Signals in Global Tyre Recycling & Circular Economy Market

A major disruption signal is the acceleration of tyre-to-tyre circularity, where closed-loop recycling is increasingly prioritized over downcycling or fuel recovery. Recovered carbon black (rCB) commercialization is another critical signal, as material science improvements could significantly alter tyre manufacturing supply chains. Extended Producer Responsibility (EPR) regulations are intensifying globally, creating stronger structural support but also raising compliance complexity. Carbon accounting and ESG disclosure frameworks are becoming increasingly influential, requiring measurable lifecycle emissions reductions from recycling operators. At the same time, technological breakthroughs in devulcanization and chemical recycling could materially disrupt traditional crumb rubber and TDF-dominant business models.

Strategic Implications of Risk Factors & Disruption Threats in Global Tyre Recycling & Circular Economy Market

Recycling operators must prioritize technology scalability, output quality improvement, and cost competitiveness to secure long-term relevance. Strategic alignment with OEMs and tyre manufacturers will become increasingly important as closed-loop systems gain traction. Investment in ELT collection logistics, regional processing ecosystems, and certification systems will be essential for scalable growth. Regulatory intelligence and environmental compliance sophistication will remain critical, particularly as sustainability scrutiny intensifies. Companies focused on premium rCB, devulcanized rubber, and tyre-to-tyre applications are likely to capture disproportionate strategic value versus low-margin downcycling models.

Global Tyre Recycling & Circular Economy Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Tyre Recycling & Circular Economy Market is expected to evolve from fragmented waste management infrastructure into a strategic industrial raw material recovery ecosystem. However, market leadership will increasingly depend on technology maturity, circular integration, and regulatory sophistication. Pyrolysis, devulcanization, and premium-grade recovered materials are likely to become the highest-value growth areas, particularly where OEM circular sourcing commitments strengthen. Europe will likely remain the benchmark market for policy-led circularity, while Asia-Pacific could emerge as the largest growth engine through infrastructure expansion. Tyre-to-tyre recycling will increasingly define premium market positioning and long-term competitive advantage. Overall, the market will remain highly attractive but execution-intensive, with long-term winners defined by scalable technology, regulatory compliance, OEM integration, and high-value material recovery leadership.

Regulatory Landscape

Global Tyre Recycling & Circular Economy Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Tyre Recycling & Circular Economy Market is a major structural force transforming end-of-life tyres (ELTs) from an environmental burden into a strategic resource stream. Governments, environmental agencies, and international regulatory bodies are intensifying pressure on tyre disposal practices through landfill bans, waste management directives, extended producer responsibility (EPR) systems, and circular economy mandates, significantly accelerating tyre recycling adoption worldwide. Historically, landfill disposal and uncontrolled stockpiling created major environmental and public safety risks, including fire hazards, toxic emissions, and land degradation. As a result, regulatory systems in developed economies increasingly prohibit landfill disposal of ELTs and instead prioritize structured collection, recycling, material recovery, and sustainable reuse frameworks. Europe currently represents the global benchmark for tyre recycling regulation, with robust ELT directives, mandatory producer responsibility systems, and aggressive circular economy targets. These frameworks are driving high recycling penetration and fostering innovation in tyre-derived raw materials such as recycled rubber, recovered carbon black (rCB), pyrolysis oil, and reclaimed steel. Emerging economies including China, India, Southeast Asia, and Latin America are progressively tightening tyre waste management policies, introducing formalized recycling regulations, and investing in domestic recycling ecosystems. This policy evolution is rapidly expanding global tyre recycling infrastructure while reducing dependence on informal or environmentally harmful disposal methods.

Global Tyre Recycling & Circular Economy Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is shaped by three converging priorities: environmental protection, resource circularity, and industrial decarbonization. Europe remains the most mature regulatory market, where landfill bans, ELT collection mandates, and EPR systems have created one of the world’s most advanced tyre recycling ecosystems. In Europe, circular economy policies increasingly favor closed-loop recycling systems, including tyre-to-tyre material reintegration, encouraging advanced technologies such as pyrolysis, devulcanization, and rCB production. Regulatory emphasis is shifting from basic waste management toward higher-value resource recovery. Asia-Pacific is witnessing rapid regulatory acceleration due to rising vehicle ownership, increasing ELT volumes, and growing environmental concerns. Governments in China and India are strengthening waste processing regulations and promoting formal recycling sectors, positioning the region as the fastest-growing market. North America maintains relatively mature recycling networks supported by state-level regulations, sustainability initiatives, and growing corporate ESG commitments. Adoption of recycled tyre materials in industrial, automotive, and infrastructure sectors is increasingly supported by environmental policy frameworks. Global carbon reduction goals are further influencing policy priorities, with tyre recycling now recognized as a strategic contributor to lower lifecycle emissions, reduced virgin material dependency, and broader circular manufacturing objectives.

Key Regulatory & Policy Environment Signals in Global Tyre Recycling & Circular Economy Market

- Extended Producer Responsibility (EPR) Laws: Require manufacturers and importers to support collection, recycling, and proper ELT management.

- Landfill Bans & ELT Disposal Restrictions: Prevent environmentally harmful tyre dumping and accelerate formal recycling ecosystems.

- EU Circular Economy Action Plan: Promotes resource recovery, material circularity, and closed-loop tyre recycling innovation.

- Carbon Reduction & Sustainability Mandates: Encourage recycled raw material integration and lower-emission manufacturing pathways.

- Industrial Waste Processing Regulations: Strengthen compliance requirements for pyrolysis, devulcanization, and waste-to-resource operations.

- Green Public Infrastructure Policies: Support recycled rubber use in roads, construction, and public surfaces.

Strategic Implications of Regulatory & Policy Environment in Global Tyre Recycling & Circular Economy Market

The regulatory environment is decisively transforming tyre recycling from a waste disposal sector into a strategic industrial resource recovery market. Compliance pressures are increasing demand for advanced recycling technologies while simultaneously raising operational standards and capital requirements. Traditional low-value applications such as tyre-derived fuel (TDF) and open-loop recycling are gradually facing greater scrutiny, while high-value closed-loop recycling models are gaining stronger policy support. This shift is favoring players capable of producing high-quality rCB, reclaimed rubber, and tyre-grade recovered materials. OEMs are increasingly aligning with regulatory sustainability frameworks, creating stronger partnerships with recyclers to secure circular raw materials and meet ESG commitments. Tyre manufacturers are progressively viewing ELTs as strategic feedstock rather than waste. Regional policy differences are also reshaping supply chains, with localization of collection systems, processing infrastructure, and recycling technologies becoming essential for regulatory compliance and competitive cost structures. Compliance-led innovation’including digital waste tracking, material traceability systems, and lifecycle carbon accounting’is becoming a key differentiator for market leaders.

Global Tyre Recycling & Circular Economy Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become significantly more stringent and circularity-focused, reinforcing the strategic importance of tyre recycling globally. Governments are likely to expand landfill bans, strengthen EPR frameworks, and introduce more aggressive recycled-content mandates. Europe will likely remain the global leader in policy sophistication, with stronger tyre-to-tyre recycling incentives, lifecycle emissions accounting, and sustainability-linked procurement frameworks. Asia-Pacific is projected to emerge as the largest infrastructure expansion opportunity due to tightening regulation and growing ELT volumes. Advanced recycling technologies such as continuous pyrolysis, chemical devulcanization, and high-purity rCB production are expected to receive stronger regulatory support as governments prioritize industrial decarbonization. OEM integration into recycling ecosystems will likely increase through mandatory recycled material targets and sustainability certifications, further accelerating tyre circularity. Overall, the regulatory landscape will act as a powerful enabler of innovation, infrastructure investment, and material circularity. Companies that proactively align with evolving waste management laws, sustainability mandates, and advanced recycling standards while building scalable closed-loop capabilities will be best positioned to lead the Global Tyre Recycling & Circular Economy Market through 2033.