Global Pyrolysis Oil Market Report, Size & Forecast 2026-2033

Global Pyrolysis Oil Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 4.12 Billion |

| Market Size (2033) | USD 9.87 Billion |

| CAGR (2026???2033) | 11.5% |

| Largest Segment | Waste Plastic-Derived Pyrolysis Oil |

| Fastest Growing Segment | Chemical Recycling Feedstock Applications |

| Leading Application | Fuel and Petrochemical Feedstock Production |

| Key Growth Driver | Rising demand for sustainable fuels and increasing focus on waste plastic management |

| Key Technology Trends | Catalytic pyrolysis, chemical recycling technologies, modular reactor systems, advanced oil upgrading techniques |

| Major End-Use Industries | Petrochemicals, Refining, Power Generation, Industrial Heating, Waste Management |

| Key Market Opportunity | Expansion of circular economy initiatives and advanced recycling infrastructure |

| Regional Leader | Europe |

| Fastest Growing Region | Asia-Pacific |

| Sustainability Focus | Conversion of waste plastics, biomass, and rubber into valuable fuels and feedstocks, supporting waste reduction and resource recovery |

Global Pyrolysis Oil Market Size & Forecast

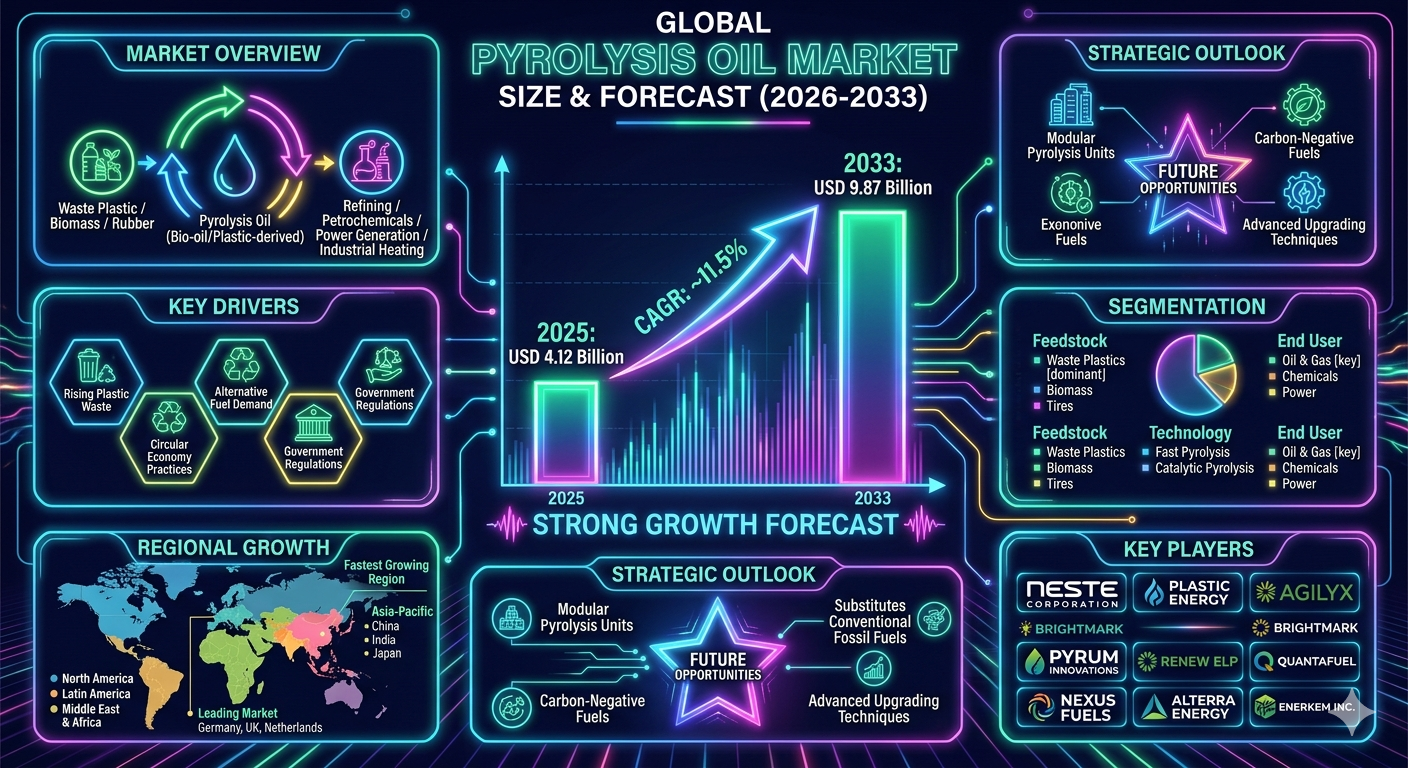

The global pyrolysis oil market is projected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 4.12 billion in 2025 and is expected to reach nearly USD 9.87 billion by 2033, expanding at a CAGR of around 11.5%. The market growth is driven by rising demand for sustainable fuels, increasing emphasis on waste plastic management, growing adoption of circular economy practices, and expanding investments in chemical recycling and advanced thermal conversion technologies worldwide. Pyrolysis oil, also known as bio-oil or plastic-derived oil depending on feedstock, is produced through the thermal decomposition of organic materials such as waste plastics, biomass, and rubber in the absence of oxygen. It serves as a substitute fuel and feedstock for refining, petrochemical production, power generation, and industrial heating applications. The market is undergoing rapid transformation due to technological advancements in chemical recycling, catalytic pyrolysis processes, modular reactor systems, and improved oil upgrading techniques that enhance fuel quality and commercial viability. Additionally, increasing regulatory pressure on plastic waste reduction and rising crude oil price volatility are accelerating adoption of pyrolysis-based circular fuel solutions globally.

Global Pyrolysis Oil Market Overview

The pyrolysis oil market represents a rapidly emerging segment within the global waste-to-energy, circular economy, and alternative fuels industry. It plays a critical role in converting end-of-life plastics and biomass waste into valuable liquid hydrocarbons that can be reused across industrial and energy sectors. The market includes plastic pyrolysis oil, biomass pyrolysis oil, tire-derived oil, and upgraded refinery-compatible synthetic crude substitutes. Pyrolysis oil is increasingly being used in refineries, petrochemical plants, cement industries, industrial boilers, and power generation facilities as a lower-carbon alternative to conventional fossil fuels. Technological advancements in reactor design, catalytic upgrading, distillation processes, and emission control systems are significantly improving product quality and scalability. Major market participants include Neste Corporation, Plastic Energy, Agilyx, Brightmark, Pyrum Innovations, ReNew ELP, Quantafuel, Nexus Fuels, Alterra Energy, and Enerkem Inc.Key Drivers of Global Pyrolysis Oil Market Growth

Rising Plastic Waste and Environmental Concerns

The increasing global accumulation of plastic waste is driving demand for advanced recycling and waste-to-fuel technologies. Pyrolysis provides an effective solution for reducing landfill dependency and environmental pollution.Expansion of Circular Economy Initiatives

Governments and industries are increasingly promoting circular economy models that prioritize material reuse and resource efficiency. Pyrolysis oil plays a key role in closing the loop for plastic and hydrocarbon waste streams.Growing Demand for Alternative Fuels

Rising energy demand and volatility in crude oil prices are encouraging adoption of alternative fuel sources such as pyrolysis oil. Industries are seeking cost-effective and lower-carbon fuel substitutes.Technological Advancements in Chemical Recycling

Innovations in catalytic pyrolysis, hydroprocessing, and oil upgrading are improving yield quality and reducing impurities. This is enhancing commercial scalability and refinery compatibility.Supportive Government Regulations

Policies targeting plastic waste reduction, extended producer responsibility (EPR), and carbon emission reductions are supporting market growth. Regulatory frameworks are encouraging investments in pyrolysis infrastructure.Global Pyrolysis Oil Market Segmentation

By Feedstock

The market is segmented into waste plastics, biomass, tires, and mixed waste streams. Waste plastics represent the dominant feedstock segment due to high availability and recycling urgency.By Technology

The market includes slow pyrolysis, fast pyrolysis, and catalytic pyrolysis. Fast and catalytic pyrolysis technologies are gaining traction due to higher efficiency and better oil quality.By Application

Applications include fuel for industrial heating, power generation, refinery feedstock, marine fuel, and petrochemical production. Refinery and petrochemical applications are emerging as high-value segments.By End User

End users include oil & gas companies, chemical manufacturers, power plants, cement industries, and waste management companies. Oil & gas companies represent a key demand segment due to integration with refining systems.Regional Market Dynamics

Europe

Europe leads the global pyrolysis oil market due to strong environmental regulations, advanced recycling infrastructure, and aggressive circular economy policies. Countries such as Germany, the Netherlands, Finland, and the United Kingdom are key contributors.North America

North America is witnessing strong growth supported by rising investments in chemical recycling and waste-to-energy technologies. The United States is the primary market with increasing commercial plant deployments.Asia-Pacific

Asia-Pacific is the fastest-growing region due to high plastic waste generation, expanding industrial base, and increasing energy demand. China, India, Japan, and South Korea are major growth markets.Latin America

Latin America is gradually emerging with growing interest in waste management solutions and alternative fuels. Brazil and Mexico are leading regional contributors.Middle East & Africa

The region is witnessing moderate growth driven by diversification of energy sources and investments in circular economy projects. Gulf countries are increasingly exploring waste-to-fuel technologies.Competitive Landscape

The global pyrolysis oil market is highly innovative and technology-driven, with companies competing through process efficiency, feedstock flexibility, oil quality, and scalability. Key players include Neste Corporation, Plastic Energy, Agilyx, Brightmark, Pyrum Innovations, ReNew ELP, Quantafuel, Nexus Fuels, Alterra Energy, and Enerkem Inc. Companies are increasingly investing in advanced catalytic systems, modular pyrolysis plants, refinery partnerships, and upgrading technologies to improve product quality and commercial adoption. Strategic collaborations with petrochemical companies, waste management firms, and government bodies are strengthening market positioning.Strategic Outlook

The strategic outlook for the global pyrolysis oil market remains highly positive due to rising demand for sustainable fuels and circular economy integration. Future opportunities include advanced chemical recycling integration, refinery-grade circular feedstocks, decentralized modular pyrolysis units, and carbon-negative fuel production systems. Scaling production efficiency, improving oil quality standards, and strengthening supply chain integration will be critical for long-term growth. Companies investing in technology innovation, feedstock diversification, and downstream integration are expected to gain competitive advantage.Final Market Perspective

The global pyrolysis oil market is emerging as a key enabler of circular economy transformation and sustainable fuel development worldwide.technology Rising environmental concerns, regulatory support, and technological advancements will continue to drive strong market expansion throughout the forecast period. Organizations that successfully combine innovation, scalability, and integration with existing energy systems will remain strongly positioned in the evolving global pyrolysis oil market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Pyrolysis Oil Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Pyrolysis Oil

- 2.2 Scope of the Study

- 2.3 Evolution of Waste-to-Fuel Technologies

- 2.4 Circular Economy Ecosystem Analysis

- 2.5 Regulatory & Sustainability Framework

- 2.6 Chemical Recycling Industry Trends

- 2.7 Technology Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Plastic Waste Generation

- 4.1.2 Expansion of Circular Economy Initiatives

- 4.1.3 Growing Demand for Alternative Fuels

- 4.1.4 Advancements in Chemical Recycling Technologies

- 4.1.5 Supportive Government Regulations

- 4.2 Restraints

- 4.2.1 High Initial Capital Investment

- 4.2.2 Feedstock Supply Chain Complexity

- 4.2.3 Product Quality Standardization Issues

- 4.2.4 Limited Commercial-Scale Infrastructure

- 4.3 Opportunities

- 4.3.1 Refinery Integration for Circular Feedstocks

- 4.3.2 Decentralized Modular Pyrolysis Plants

- 4.3.3 Carbon-Negative Fuel Production Systems

- 4.3.4 Expansion into Emerging Economies

- 4.4 Challenges

- 4.4.1 Scaling Commercial Production

- 4.4.2 Regulatory Compliance Complexity

- 4.4.3 Emission Control Requirements

- 4.4.4 Technology Optimization Challenges

- 4.1 Drivers

- 5. Global Pyrolysis Oil Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Technology Adoption Trends

- 5.5 Feedstock Utilization Analysis

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Feedstock

- 6.1.1 Waste Plastics

- 6.1.2 Biomass

- 6.1.3 Tires

- 6.1.4 Mixed Waste Streams

- 6.2 By Technology

- 6.2.1 Slow Pyrolysis

- 6.2.2 Fast Pyrolysis

- 6.2.3 Catalytic Pyrolysis

- 6.3 By Application

- 6.3.1 Industrial Heating Fuel

- 6.3.2 Power Generation

- 6.3.3 Refinery Feedstock

- 6.3.4 Marine Fuel

- 6.3.5 Petrochemical Production

- 6.4 By End User

- 6.4.1 Oil & Gas Companies

- 6.4.2 Chemical Manufacturers

- 6.4.3 Power Plants

- 6.4.4 Cement Industries

- 6.4.5 Waste Management Companies

- 6.1 By Feedstock

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Technology Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Capacity Expansion Analysis

- 8.5 Innovation & Commercialization Strategies

- 9. Company Profiles

- 9.1 Neste Corporation

- 9.2 Plastic Energy

- 9.3 Agilyx

- 9.4 Brightmark

- 9.5 Pyrum Innovations

- 9.6 ReNew ELP

- 9.7 Quantafuel

- 9.8 Nexus Fuels

- 9.9 Alterra Energy

- 9.10 Enerkem Inc.

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Circular Fuel Opportunity Forecast Engine

- 10.2 Feedstock Supply Intelligence Dashboard

- 10.3 Refinery Integration Analytics Tracker

- 10.4 Technology Efficiency Opportunity Analyzer

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Investment in Advanced Catalytic Technologies

- 11.2 Expansion of Modular Pyrolysis Infrastructure

- 11.3 Strengthening Refinery Partnerships

- 11.4 Enhancing Feedstock Diversification Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Sports Betting Market Competitive Intensity & Market Structure Overview

The global sports betting market is highly competitive and moderately consolidated, characterized by strong competition among multinational betting operators, digital gaming platforms, casino-entertainment companies, and regional sportsbook providers. Competitive intensity is driven by platform innovation, regulatory compliance, betting experience optimization, customer acquisition strategies, and technological differentiation.

The market structure consists of large international sportsbook operators, regulated online wagering platforms, integrated casino and entertainment groups, fantasy sports companies, and emerging digital-native betting technology providers. Competition is shaped by licensing capabilities, digital infrastructure, payment ecosystem integration, sports media partnerships, and responsible gaming frameworks.

Increasing legalization, rapid digital transformation, rising mobile-first betting adoption, and expanding consumer participation in live sports wagering are intensifying competition across the global sports betting market.

Global Sports Betting Market Competitive Intensity & Market Structure Current Scenario

Leading Global Sports Betting Companies

Flutter Entertainment: Global market leader with an extensive sportsbook portfolio including FanDuel, Paddy Power, and Betfair, supported by advanced digital betting ecosystems.

Bet365 Group Ltd.: Leading online sportsbook operator recognized for strong live betting capabilities, broad global market reach, and advanced platform innovation.

Entain plc: Major betting operator with diversified sportsbook brands and strong international regulatory market presence.

DraftKings Inc.: Prominent digital sports betting platform with strong North American market penetration and advanced mobile-first betting infrastructure.

Caesars Entertainment: Integrated gaming and sportsbook company leveraging casino assets and omnichannel customer engagement strategies.

Kindred Group: Established online gaming and sportsbook provider focused on regulated market expansion and responsible gaming technologies.

MGM Resorts International: Major entertainment and betting operator strengthening digital sports wagering through strategic technology partnerships.

Betsson AB: Strong European digital betting operator with growing international expansion initiatives.

888 Holdings plc: Significant online betting platform provider with diversified digital gaming and sportsbook capabilities.

PointsBet Holdings Ltd.: Innovative sportsbook operator focused on differentiated betting experiences and advanced in-play wagering solutions.

Key Competitive Intensity & Market Structure Drivers

The progressive legalization and regulation of sports betting across multiple jurisdictions is significantly intensifying operator competition and geographic expansion.

The rapid shift toward mobile betting applications and digital wagering platforms is increasing competitive pressure around user experience and platform functionality.

Technological advancements in AI-powered odds generation, predictive analytics, and live in-play betting capabilities are creating strong product differentiation.

Strategic sponsorship agreements with sports leagues, teams, broadcasters, and digital media platforms are becoming critical competitive positioning tools.

Growing emphasis on secure payment systems, real-time analytics, and responsible gaming frameworks is shaping long-term market competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Operators are increasingly investing in AI-driven personalization engines and advanced analytics platforms to improve customer retention and wagering engagement.

Strategic acquisitions and cross-border licensing agreements are becoming essential for geographic expansion and regulatory market access.

Partnerships with sports media companies and streaming platforms are strengthening real-time betting integration and customer acquisition capabilities.

Responsible gambling tools, identity verification technologies, and regulatory compliance systems are emerging as major competitive differentiators.

Investment in blockchain-enabled payment systems, cybersecurity infrastructure, and omnichannel betting ecosystems is reshaping strategic market positioning.

Global Sports Betting Market Competitive Intensity & Market Structure Forward Outlook

The global sports betting market is expected to remain highly competitive as legalization expands and digital-first wagering ecosystems continue to evolve globally.

Future competition will increasingly focus on AI-personalized betting experiences, esports betting innovation, immersive live-stream wagering, and blockchain-integrated betting ecosystems.

North America and Asia-Pacific are expected to emerge as major competitive growth regions due to regulatory liberalization, rising sports engagement, and mobile payment adoption.

Advancements in real-time analytics, digital identity verification, and predictive wagering technologies are expected to significantly reshape market dynamics.

Overall, companies that successfully combine technological innovation, regulatory excellence, platform security, and personalized user engagement will remain strongly positioned in the evolving global sports betting market.

Value Chain

Global Pyrolysis Oil Market Value Chain & Supply Chain Evolution Overview

The global pyrolysis oil market value chain is evolving rapidly as circular economy models, chemical recycling technologies, and waste-to-fuel systems gain industrial-scale adoption. The ecosystem connects waste collection networks, preprocessing facilities, pyrolysis technology providers, upgrading and refining units, and end-use industries such as petrochemicals, power generation, marine fuels, and industrial heating.

The value chain is increasingly structured around integrated waste management systems, advanced thermal conversion technologies, catalytic upgrading processes, and downstream refinery integration. Stakeholders include municipal waste management authorities, plastic aggregators, technology licensors, plant operators, oil & gas companies, chemical manufacturers, and industrial energy consumers.

Key companies such as Neste Corporation, Plastic Energy, Agilyx, Brightmark, Quantafuel, ReNew ELP, Pyrum Innovations, Nexus Fuels, Alterra Energy, and Enerkem Inc. are actively developing scalable pyrolysis platforms, modular reactor systems, and refinery-compatible oil upgrading technologies to strengthen commercial viability and improve output quality.

Upstream activities include waste collection, sorting, shredding, contamination removal, and feedstock standardization, which are critical for ensuring consistent pyrolysis output quality. Midstream operations involve thermal decomposition processes, catalytic pyrolysis reactions, vapor condensation systems, and crude pyrolysis oil extraction. Downstream operations focus on upgrading, distillation, hydroprocessing, blending, and integration into refinery or industrial fuel systems.

The supply chain is increasingly influenced by regulatory frameworks such as extended producer responsibility (EPR), plastic waste mandates, carbon reduction policies, and renewable fuel standards. These policies are accelerating investments in decentralized pyrolysis plants and regional waste-to-fuel infrastructure.

However, the market still faces operational challenges including feedstock variability, high capital expenditure requirements, limited large-scale commercial standardization, oil quality inconsistency, and logistical complexity in waste aggregation and processing.

Global Pyrolysis Oil Market Value Chain & Supply Chain Evolution Current Scenario

The current market scenario is characterized by rapid commercialization of chemical recycling technologies, increasing pilot-to-commercial scale transitions, and strong policy-driven demand for circular fuel solutions. Europe leads global deployment due to stringent plastic waste regulations and mature recycling ecosystems, while North America is expanding through private-sector investments and strategic partnerships between technology providers and petrochemical companies.

Asia-Pacific is emerging as a high-growth region due to rising plastic waste generation, expanding industrialization, and increasing government focus on waste-to-energy infrastructure development.

Fast pyrolysis and catalytic pyrolysis technologies are gaining momentum as they offer higher efficiency, improved oil quality, and better compatibility with refinery systems compared to traditional slow pyrolysis methods.

Refinery integration is becoming a key commercialization pathway, where pyrolysis oil is increasingly being processed as a co-feedstock in existing petrochemical and refining operations.

Key Value Chain & Supply Chain Evolution Signals in Global Pyrolysis Oil Market

One of the most significant transformation signals is the shift toward refinery-compatible circular feedstocks, where pyrolysis oil is no longer treated as a standalone fuel but as an integrated petrochemical input.

Another key development is the rise of modular and decentralized pyrolysis units, enabling localized waste processing and reducing transportation costs associated with feedstock logistics.

Technological advancements in catalytic upgrading and hydroprocessing are significantly improving oil stability, reducing impurities, and increasing compatibility with existing refinery infrastructure.

Digitalization of waste tracking systems and AI-driven feedstock sorting technologies are improving supply chain efficiency and feedstock quality consistency.

Long-term supply chain evolution is also being shaped by increasing corporate sustainability commitments, plastic neutrality targets, and carbon reduction mandates across industries such as FMCG, packaging, and petrochemicals.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Pyrolysis Oil Market

Companies that integrate vertically across waste sourcing, technology development, and refinery partnerships are gaining a strong competitive advantage in the evolving pyrolysis oil ecosystem. Strategic control over feedstock supply and downstream integration is becoming critical for profitability and scalability.

Partnerships between waste management companies and petrochemical giants are accelerating commercialization by ensuring stable feedstock supply and guaranteed off-take agreements for upgraded pyrolysis products.

Investment in advanced catalytic systems, emission control technologies, and high-efficiency reactor designs is essential for improving yield economics and meeting regulatory compliance standards.

Policy alignment with circular economy mandates and extended producer responsibility frameworks is increasingly influencing market entry strategies and investment decisions.

Global Pyrolysis Oil Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the pyrolysis oil value chain is expected to transition from fragmented pilot-scale operations to integrated industrial ecosystems linked directly with global petrochemical supply chains.

Advanced chemical recycling hubs will emerge, combining multiple waste streams into centralized processing facilities optimized for efficiency and scalability.

Artificial intelligence and automation will play a larger role in feedstock classification, process optimization, and predictive maintenance of pyrolysis systems.

Refinery integration will deepen significantly, with pyrolysis oil increasingly functioning as a mainstream circular feedstock within global hydrocarbon supply chains.

Ultimately, the market will evolve into a fully integrated circular hydrocarbon economy where waste plastics and biomass are continuously converted into high-value fuels and chemicals through advanced thermal and catalytic systems.

Market-Specific Value Chain

- Feedstock Sourcing & Waste Aggregation: Municipal waste systems, industrial plastic collection, biomass sourcing, sorting facilities, and preprocessing hubs.

- Preprocessing & Material Preparation: Shredding, drying, contamination removal, and feedstock standardization systems.

- Pyrolysis Conversion Systems: Thermal decomposition units, catalytic reactors, vapor condensation systems, and oil extraction technologies.

- Oil Upgrading & Refining Integration: Hydroprocessing, distillation, impurity removal, and refinery blending operations.

- Distribution & Industrial Application: Fuel supply to petrochemical plants, industrial boilers, marine fuel systems, and power generation facilities.

- Circular Economy Reintegration: Waste loop closure systems, carbon credit integration, sustainability reporting, and regulatory compliance tracking.

Company-to-Stage Mapping

- Feedstock Sourcing & Waste Aggregation: Municipal waste operators, waste management firms, regional recyclers.

- Preprocessing & Material Preparation: Waste sorting technology providers and preprocessing equipment manufacturers.

- Pyrolysis Conversion Systems: Agilyx, Brightmark, Alterra Energy, Nexus Fuels, Pyrum Innovations.

- Oil Upgrading & Refining Integration: Neste Corporation, Quantafuel, ReNew ELP, petrochemical refinery partners.

- Distribution & Industrial Application: Oil & gas companies, cement industries, industrial fuel consumers.

- Circular Economy Reintegration: Sustainability platforms, ESG reporting firms, regulatory bodies, carbon credit systems.

Investment Activity

Global Pyrolysis Oil Market Investment & Funding Dynamics Overview

The global pyrolysis oil market is witnessing accelerating investment activity driven by rising demand for circular economy solutions, increasing pressure to manage plastic waste, and strong growth in chemical recycling and alternative fuel technologies. Between 2026 and 2033, capital deployment is expected to intensify across advanced pyrolysis plants, catalytic upgrading technologies, modular waste-to-fuel systems, and refinery integration infrastructure.

The pyrolysis oil market represents a strategically important segment within the broader waste-to-energy, circular economy, and alternative fuels ecosystem. Venture capital firms, clean-tech investors, energy transition funds, petrochemical companies, and institutional infrastructure investors are increasingly allocating capital toward scalable chemical recycling and waste-to-hydrocarbon conversion technologies.

A major structural shift shaping investment dynamics is the transition from pilot-scale pyrolysis systems toward industrial-scale, refinery-integrated, and continuously operating production facilities. This evolution is driving significant capital flows into process optimization, feedstock preprocessing systems, and oil upgrading technologies that improve commercial viability.

Growing convergence between chemical recycling, petrochemical feedstock demand, ESG-driven investment mandates, and regulatory plastic waste reduction policies is creating strong cross-sector investment momentum.

Current Investment & Funding Landscape

- Europe: Leads global investment activity due to strong circular economy regulations, carbon reduction policies, and advanced recycling infrastructure.

- North America: Witnessing increasing venture capital and corporate investment in chemical recycling and waste-to-fuel projects.

- Asia-Pacific: Emerging as a high-growth investment region driven by high plastic waste generation and rising industrial fuel demand.

- Latin America: Early-stage investments are increasing in waste management and alternative fuel initiatives.

- Middle East & Africa: Strategic investments are focused on energy diversification and circular economy development.

Key Investment Drivers

- Rising global plastic waste generation and environmental pressure.

- Expansion of circular economy and extended producer responsibility (EPR) frameworks.

- Increasing demand for alternative and low-carbon fuels.

- Volatility in crude oil prices supporting alternative feedstock adoption.

- Technological advancements in catalytic pyrolysis and upgrading systems.

- Strong policy support for chemical recycling and waste reduction.

- Growing petrochemical industry demand for recycled feedstocks.

- Rising ESG-driven capital allocation toward clean technologies.

Strategic Investment Areas

- Advanced Pyrolysis Plants: Large-scale continuous waste-to-oil production facilities.

- Catalytic Upgrading Technologies: Processes improving fuel quality and refinery compatibility.

- Modular Recycling Systems: Decentralized pyrolysis units for distributed waste processing.

- Feedstock Preprocessing: Sorting, cleaning, and optimization of waste plastic inputs.

- Refinery Integration: Blending and co-processing systems for petrochemical applications.

- Emission Control Systems: Technologies improving environmental compliance and efficiency.

Strategic Investment Implications

- Scalability from pilot to industrial deployment is a key investment success factor.

- Oil quality and refinery compatibility significantly influence project valuation.

- Long-term offtake agreements with petrochemical companies enhance funding attractiveness.

- Policy stability and regulatory support are critical for investor confidence.

- Feedstock supply chain reliability strongly impacts project bankability.

- Technology differentiation in yield efficiency and upgrading processes drives competitive advantage.

Forward Investment Outlook

The global pyrolysis oil market is expected to remain one of the fastest-growing segments within the circular economy investment landscape, supported by increasing regulatory pressure on plastic waste and rising demand for alternative hydrocarbon sources.

Future funding activity is expected to prioritize refinery-grade chemical recycling systems, AI-optimized process control technologies, integrated waste-to-fuel platforms, and large-scale industrial deployment of continuous pyrolysis plants.

- Europe: Will continue leading investment due to strong regulatory enforcement and circular economy leadership.

- North America: Will expand investment in commercial-scale chemical recycling infrastructure.

- Asia-Pacific: Will experience rapid growth driven by industrial expansion and waste management demand.

- Emerging Markets: Will attract early-stage investments in decentralized waste-to-fuel systems.

Overall, the pyrolysis oil market represents a high-growth investment opportunity at the intersection of waste management, energy transition, and petrochemical circularity, offering strong long-term capital deployment potential for technology-driven and infrastructure-focused investors.

Technology & Innovation

Global Pyrolysis Oil Market Technology & Innovation Landscape Overview

The global pyrolysis oil market is undergoing significant technological transformation driven by advancements in chemical recycling systems, catalytic cracking technologies, modular reactor engineering, artificial intelligence-enabled process optimization, and advanced oil upgrading solutions. The evolution of pyrolysis technologies is increasingly focused on improving feedstock conversion efficiency, enhancing oil quality, reducing emissions, and enabling scalable circular fuel production across industrial applications.

Modern pyrolysis systems are integrating continuous reactor designs, automated temperature control systems, advanced catalysts, and digital monitoring platforms to optimize thermal decomposition processes and improve commercial viability. These innovations are significantly enhancing process efficiency, increasing product consistency, and reducing operational costs.

The market is also witnessing growing adoption of AI-powered process analytics, carbon capture integration, decentralized modular pyrolysis units, and refinery-grade upgrading technologies that are redefining waste-to-fuel conversion infrastructure worldwide.

Global Pyrolysis Oil Market Technology & Innovation Current Scenario

Currently, innovation in the pyrolysis oil market is centered around reactor efficiency optimization and advanced oil purification technologies. Continuous-feed pyrolysis systems are increasingly replacing traditional batch-based operations due to higher throughput, improved operational stability, and lower maintenance requirements.

Catalytic pyrolysis technologies are gaining widespread adoption as they improve hydrocarbon selectivity, reduce undesirable by-products, and enhance fuel quality for downstream applications.

Artificial intelligence and machine learning are being integrated into pyrolysis systems to enable predictive maintenance, process optimization, and real-time thermal control for maximizing output efficiency.

Advanced oil upgrading techniques, including hydroprocessing, distillation refinement, and desulfurization systems, are improving the compatibility of pyrolysis oil with refinery and petrochemical applications.

Emission control systems and integrated gas recovery technologies are also becoming critical innovation areas to improve environmental compliance and operational sustainability.

Modular and decentralized pyrolysis plants are expanding rapidly, allowing localized waste conversion and reducing feedstock transportation costs across distributed industrial ecosystems.

Key Technology & Innovation Trends in Global Pyrolysis Oil Market

- Catalytic Pyrolysis Systems: Improving conversion efficiency and oil quality through advanced catalyst integration.

- Continuous Reactor Technologies: Enabling higher throughput and operational consistency.

- AI-Powered Process Optimization: Real-time analytics for thermal efficiency and yield maximization.

- Advanced Oil Upgrading Systems: Enhancing refinery-grade product compatibility.

- Modular Pyrolysis Units: Decentralized waste-to-fuel conversion for localized deployment.

- Carbon Capture Integration: Reducing lifecycle emissions from pyrolysis operations.

- Digital Monitoring Platforms: Intelligent system diagnostics and predictive maintenance capabilities.

- Feedstock Pre-Treatment Innovations: Improving conversion consistency and reducing contamination.

- Emission Control Technologies: Supporting regulatory compliance and cleaner processing.

- Hybrid Waste Conversion Systems: Combining pyrolysis with chemical recycling and gasification solutions.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the pyrolysis oil market by shifting competition from basic thermal waste conversion toward high-efficiency, scalable, and refinery-integrated circular fuel ecosystems.

Companies investing in advanced catalytic systems, AI-driven automation, and high-quality upgrading technologies are achieving stronger competitive differentiation through superior fuel performance and improved process economics.

The integration of digital technologies is enabling producers to improve process reliability, optimize feedstock flexibility, and strengthen operational scalability.

Advanced automation and intelligent monitoring are helping operators reduce downtime, improve output consistency, and lower maintenance costs.

However, high capital investment requirements, feedstock contamination variability, technology standardization challenges, and regulatory approval complexity remain major barriers to widespread adoption.

Global Pyrolysis Oil Market Technology & Innovation Forward Outlook

The future of pyrolysis oil technology is expected to move toward fully automated, AI-optimized, and low-emission circular fuel production systems capable of supporting large-scale sustainable hydrocarbon generation.

Emerging innovations include self-optimizing reactor systems, next-generation nano-catalysts, digital twin process simulation, and autonomous waste sorting integration.

Advanced hydrogen-assisted upgrading technologies may enable the production of ultra-low sulfur synthetic fuels suitable for direct refinery integration.

Decentralized smart pyrolysis networks supported by IoT-enabled control systems are expected to strengthen localized circular economy implementation.

Federated industrial analytics platforms may further enhance operational efficiency by enabling cross-facility process learning while maintaining data security.

Overall, the global pyrolysis oil market is evolving toward a highly intelligent, scalable, and sustainable technology ecosystem combining advanced thermal conversion, digital automation, catalytic innovation, and circular fuel integration to redefine waste valorization and alternative energy production worldwide.

Market Risk

Global Pyrolysis Oil Market Risk Factors & Disruption Threats Overview

The global pyrolysis oil market is expanding rapidly as circular economy initiatives, chemical recycling technologies, and waste-to-fuel solutions gain industrial scale. However, despite strong growth momentum, the market faces a complex set of risks related to technology performance, feedstock variability, regulatory uncertainty, economic viability, and downstream adoption challenges.

A key structural risk lies in the technological maturity of pyrolysis systems. While advancements in catalytic pyrolysis and modular reactor design are improving efficiency, many commercial projects still face challenges in achieving consistent yield quality, energy efficiency, and scalable operations across diverse waste streams.

Feedstock variability is another major constraint. Waste plastic composition differs significantly across regions and collection systems, leading to inconsistent output quality and increased preprocessing requirements. This directly impacts operational stability and profitability.

Economic competitiveness remains a critical concern. Pyrolysis oil must compete with conventional fossil fuels and increasingly with other renewable alternatives. In periods of low crude oil prices, commercial viability can weaken, reducing investment momentum.

Regulatory uncertainty also plays a significant role in shaping market risk. Policies governing chemical recycling classification, carbon accounting methodologies, and fuel blending standards vary widely across regions, creating compliance complexity for global operators.

Downstream adoption challenges persist, particularly in refinery integration. Pyrolysis oil often requires additional upgrading or refining before it can meet petrochemical feedstock specifications, increasing cost and operational complexity for end users.

Environmental compliance and emissions management present additional risks, as pyrolysis processes must continuously meet tightening air quality and carbon emission standards, particularly in developed markets.

Global Pyrolysis Oil Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by accelerating investments in chemical recycling facilities, strategic partnerships with oil & gas companies, and increasing policy support for plastic waste reduction. Pilot and commercial-scale pyrolysis plants are expanding across Europe, North America, and parts of Asia-Pacific.

At the same time, several early-stage projects are experiencing delays due to permitting challenges, financing constraints, and technical performance gaps during scale-up from pilot to industrial operations.

Oil price volatility continues to strongly influence investor sentiment, with project economics becoming more favorable during high crude price cycles and more constrained during downturns.

Competition is intensifying as alternative waste management technologies???such as mechanical recycling, gasification, and advanced depolymerization???compete for the same feedstock and policy incentives.

Despite these challenges, strategic collaborations between pyrolysis companies and petrochemical refiners are improving market credibility and supporting long-term commercialization pathways.

Global Pyrolysis Oil Market Key Risk Factors & Disruption Threat Signals

- Technology Scale-Up Risk: Difficulty in maintaining consistent performance from pilot to industrial-scale operations.

- Feedstock Inconsistency: Variability in plastic waste composition affecting output quality and efficiency.

- Oil Price Sensitivity: Profitability highly dependent on global crude oil price fluctuations.

- Regulatory Fragmentation: Differing definitions and standards for chemical recycling across regions.

- High Capital Intensity: Significant upfront investment required for plant construction and commissioning.

- Refinery Integration Barriers: Need for additional upgrading to meet petrochemical-grade specifications.

- Environmental Compliance Pressure: Strict emissions and lifecycle carbon accounting requirements.

- Competition from Alternative Recycling: Mechanical and enzymatic recycling technologies gaining policy preference in some regions.

- Operational Downtime Risk: Complex feedstock handling and reactor maintenance requirements.

- Offtake Uncertainty: Dependence on long-term purchase agreements with refiners and chemical companies.

Strategic Implications of Risk Factors

To mitigate technology and scale-up risks, companies are increasingly focusing on modular plant designs, standardized reactor systems, and phased capacity expansion strategies.

Improving feedstock preprocessing and developing advanced sorting infrastructure will be critical to stabilizing input quality and enhancing output consistency.

Long-term offtake agreements with petrochemical companies and refiners are becoming essential for securing revenue stability and investor confidence.

Policy alignment and active engagement with regulators will be necessary to standardize chemical recycling definitions and improve market predictability.

Investment in upgrading technologies such as hydroprocessing and refining integration will strengthen the value proposition of pyrolysis oil as a drop-in feedstock.

Global Pyrolysis Oil Market Forward Risk Outlook

Between 2026 and 2033, the pyrolysis oil market is expected to transition from early commercialization to broader industrial scaling, driven by tightening plastic waste regulations and increasing demand for low-carbon fuel alternatives.

However, the pace of growth will depend heavily on resolving technology scale-up challenges, improving economic competitiveness versus fossil fuels, and achieving consistent regulatory support across key regions.

The most successful market participants will be those that integrate vertically with waste management systems, petrochemical refiners, and advanced recycling ecosystems.

Over time, pyrolysis oil is expected to become a key transitional solution within the broader circular carbon economy, particularly for hard-to-recycle plastic waste streams.

Regulatory Landscape

Global Pyrolysis Oil Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global pyrolysis oil market is shaped by waste management regulations, circular economy directives, carbon reduction policies, fuel quality standards, and chemical recycling governance frameworks. As pyrolysis oil emerges as a key output of advanced recycling and waste-to-energy systems, regulatory oversight is increasingly focused on environmental compliance, emissions control, product classification, and end-use safety standards.

Pyrolysis oil derived from waste plastics, biomass, and tires operates at the intersection of waste treatment and fuel production, which creates complex regulatory classification challenges. Depending on jurisdiction, it may be regulated as an alternative fuel, recycled chemical feedstock, or waste-derived product, each carrying distinct compliance obligations.

The expansion of chemical recycling technologies, coupled with rising environmental pressure to reduce plastic pollution, is driving governments to develop more structured regulatory frameworks that define acceptable feedstocks, processing standards, and product quality benchmarks for pyrolysis-derived fuels.

Global Pyrolysis Oil Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for pyrolysis oil is fragmented but rapidly evolving, with strong policy momentum in regions prioritizing circular economy transformation and plastic waste reduction.

In Europe, pyrolysis oil is increasingly supported under circular economy and chemical recycling frameworks, with regulatory authorities working toward clearer classification of pyrolysis outputs as recycled content for plastics and fuel applications. The EU???s waste directives and emissions regulations strongly influence plant design, feedstock sourcing, and product validation requirements.

In North America, regulatory classification varies by state and federal frameworks, with increasing acceptance of chemical recycling under advanced recycling definitions. Environmental agencies focus on emissions compliance, facility permitting, and product end-use safety, particularly for refinery integration.

In Asia-Pacific, countries such as China, Japan, and India are gradually strengthening waste-to-energy and plastic recycling policies, but regulatory consistency remains uneven across regions, creating varied approval pathways for commercial pyrolysis operations.

Latin America, the Middle East, and Africa are in earlier stages of regulatory development, with growing interest in waste conversion technologies but limited formalized standards for pyrolysis oil production and commercialization.

Key Regulatory & Policy Environment Signals in Global Pyrolysis Oil Market

- Waste Classification Regulations: Determination of whether feedstock and outputs are classified as waste, recycled material, or fuel impacts permitting and commercialization pathways.

- Circular Economy Policies: Government mandates promoting plastic waste reduction and material recovery are supporting pyrolysis adoption.

- Emissions and Environmental Compliance: Strict air quality, carbon emissions, and industrial pollution controls govern pyrolysis plant operations.

- Fuel Quality and Refinery Standards: Regulatory specifications determine suitability of pyrolysis oil for refining, blending, or direct industrial use.

- Extended Producer Responsibility (EPR): Policies requiring manufacturers to manage plastic waste are driving investment in chemical recycling infrastructure.

- Industrial Facility Permitting: Licensing requirements for chemical recycling and thermal processing plants significantly influence project feasibility and timelines.

Global Pyrolysis Oil Market Regulatory Developments & Regional Policy Trends

In Europe, regulatory momentum is strongest, with increasing alignment between chemical recycling policies and sustainability goals aimed at achieving plastic neutrality and circular material recovery systems.

In the United States, regulatory frameworks are evolving toward clearer recognition of advanced recycling technologies, with growing state-level support for pyrolysis projects and refinery integration partnerships.

In Asia-Pacific, governments are prioritizing plastic waste management strategies, with increasing pilot projects and policy experimentation supporting pyrolysis-based waste-to-fuel solutions.

Emerging economies are gradually adopting international environmental compliance frameworks, particularly those aligned with waste reduction and sustainable industrial development goals.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging pyrolysis oil producers to invest in emissions control technologies, feedstock traceability systems, and product quality upgrading processes to meet increasingly strict environmental and fuel standards.

Regulatory uncertainty around classification and permitting continues to influence project financing, investor confidence, and deployment timelines for large-scale pyrolysis facilities.

Companies capable of aligning with circular economy policies and securing regulatory recognition for chemical recycling outputs are gaining stronger competitive positioning in global markets.

Integration with refinery systems is becoming a key strategic requirement, as regulatory acceptance of pyrolysis oil increasingly depends on downstream compatibility and product consistency standards.

Global Pyrolysis Oil Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global pyrolysis oil market is expected to become more structured, standardized, and environmentally stringent.

Governments are likely to introduce clearer definitions for chemical recycling outputs, improved lifecycle emissions accounting, and stricter verification standards for recycled carbon content.

Extended producer responsibility frameworks are expected to expand globally, significantly increasing demand for pyrolysis-based waste processing infrastructure.

However, regulatory divergence across regions will persist in the short term, particularly regarding classification of pyrolysis oil as fuel versus recycled chemical feedstock.

Overall, regulatory and policy developments will remain a key growth enabler, with companies investing in compliance-ready technologies, emissions-efficient systems, and refinery-integrated production models expected to achieve long-term market advantage.