Global Yogurt Market Report, Size & Forecast 2026-2033

Global Yogurt Market Forecast Snapshot: 2026???2033

| Metric | Value |

| 2025 Market Size | USD 115.4 Billion |

| 2033 Market Size | ~USD 168.9 Billion |

| CAGR (2026???2033) | ~4.9% |

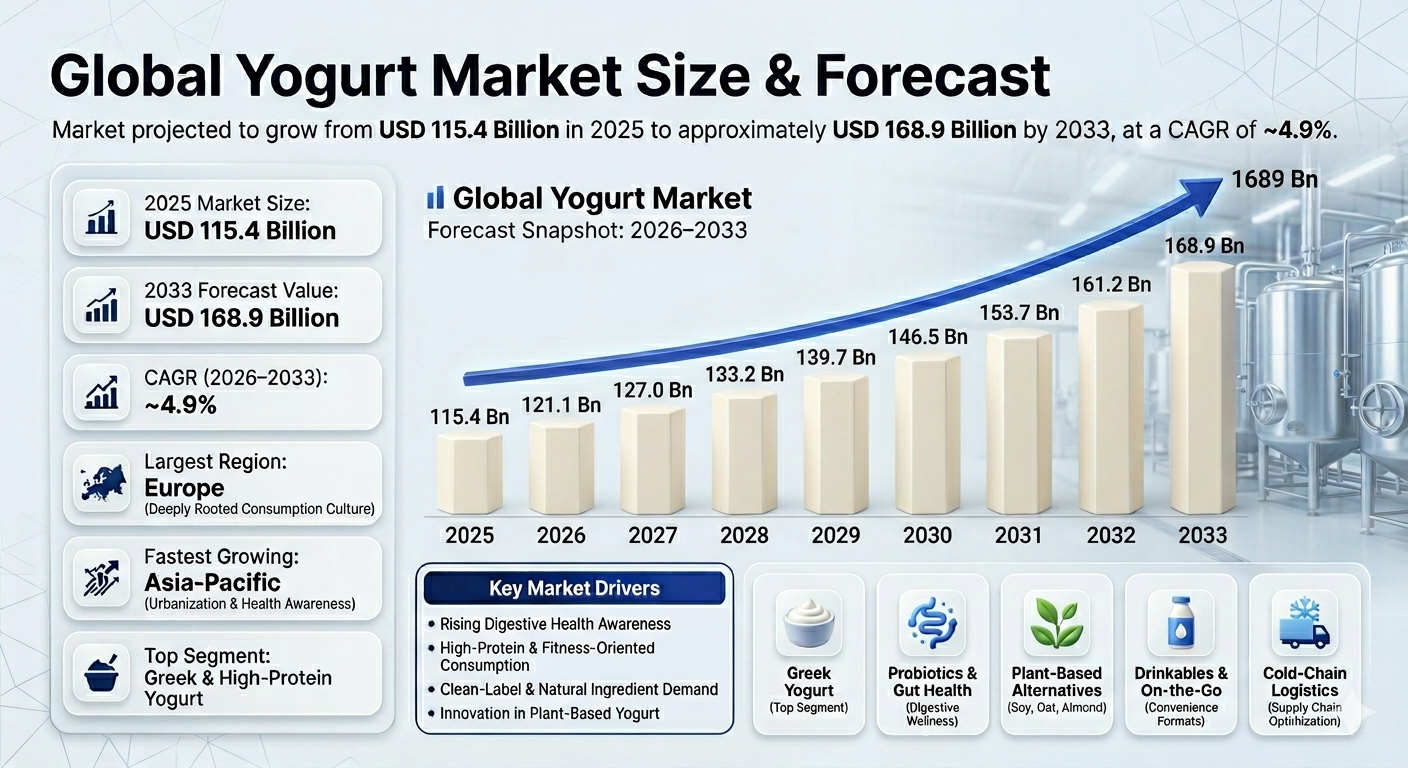

| Largest Region | Europe |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Greek & High-Protein Yogurt |

| Key Trend | Probiotic Innovation, High-Protein Formulations & Clean-Label Positioning |

| Future Focus | Functional Fortification, Plant-Based Yogurt Alternatives & Sustainable Packaging |

Global Yogurt Market Overview

The Global Yogurt Market represents one of the most dynamic segments within the broader dairy industry. Yogurt has evolved from a traditional fermented dairy product into a premium, functional, and protein-rich health food consumed across age groups.Yogurt products are widely available across supermarkets, convenience stores, specialty health outlets, caf??s, and online grocery platforms. Modern consumers increasingly view yogurt as a convenient source of probiotics, protein, calcium, and digestive health support.

The market has undergone substantial transformation. Once dominated by plain and flavored varieties, yogurt now includes Greek yogurt, Skyr, plant-based alternatives, probiotic-enhanced formulations, and high-protein variants catering to fitness-conscious consumers.

According to Pheonix Research, the Global Yogurt Market is valued at USD 115.4 Billion in 2025 and is projected to reach approximately USD 168.9 Billion by 2033, reflecting a CAGR of ~4.9% (2026???2033).

Europe remains the largest regional market due to strong consumption culture and premium product penetration. Asia-Pacific is the fastest-growing region, driven by urbanization, health awareness, and rising middle-class income levels.

Post-2025 market dynamics highlight accelerated demand for probiotic blends, lactose-free variants, plant-based yogurt alternatives, personalized nutrition formats, and AI-optimized cold-chain logistics.

Key Drivers of Global Yogurt Market Growth

Rising Digestive Health Awareness

Consumers increasingly recognize probiotics as essential for gut health, immunity, and overall wellness, boosting demand for functional yogurt.

High-Protein & Fitness-Oriented Consumption

Greek yogurt and high-protein variants are gaining traction among fitness enthusiasts and health-conscious adults.

Clean-Label & Natural Ingredient Demand

Organic, preservative-free, non-GMO, and low-sugar yogurt formulations are attracting premium consumers.

Expansion of Retail & E-Commerce Channels

Omnichannel availability across supermarkets and digital platforms improves accessibility and subscription-based repeat purchases.

Innovation in Plant-Based Yogurt

Almond, soy, coconut, oat, and cashew-based yogurts are expanding the consumer base beyond traditional dairy users.

Global Yogurt Market Segmentation

?? ?? ?? ??1. By Product Type

1.1 Traditional Yogurt

1.1.1 Plain Yogurt

1.1.1.1 Full-Fat

1.1.1.2 Low-Fat

1.1.1.3 Non-Fat

1.1.1.4 Organic Plain Yogurt

1.1.2 Flavored Yogurt

1.1.2.1 Fruit-Flavored

1.1.2.2 Dessert-Inspired Flavors

1.1.2.3 Kids??? Yogurt

1.1.2.4 Limited-Edition Flavors

1.2 Greek & High-Protein Yogurt

1.2.1 Traditional Greek Yogurt

1.2.1.1 Full-Fat Greek

1.2.1.2 Low-Fat Greek

1.2.1.3 Non-Fat Greek

1.2.1.4 Organic Greek Yogurt

1.2.2 Skyr & Icelandic Yogurt

1.2.2.1 Plain Skyr

1.2.2.2 Flavored Skyr

1.2.2.3 High-Protein Skyr

1.2.2.4 Fitness-Focused Variants

1.3 Probiotic & Functional Yogurt

1.3.1 Digestive Health Yogurt

1.3.1.1 Lactobacillus-Enriched

1.3.1.2 Bifidobacterium Blends

1.3.1.3 Prebiotic + Probiotic

1.3.1.4 Gut Microbiome Support

1.3.2 Immunity-Boosting Yogurt

1.3.2.1 Vitamin D Fortified

1.3.2.2 Zinc-Enriched

1.3.2.3 Multivitamin Yogurt

1.3.2.4 Herbal-Infused Yogurt

1.4 Plant-Based Yogurt Alternatives

1.4.1 Almond-Based Yogurt

1.4.2 Soy-Based Yogurt

1.4.3 Coconut-Based Yogurt

1.4.4 Oat-Based Yogurt

1.4.5 Cashew & Mixed Nut Yogurt

1.5 Drinkable Yogurt

1.5.1 Probiotic Drinkable Yogurt

1.5.2 High-Protein Drinkables

1.5.3 Kids??? Yogurt Drinks

1.5.4 On-the-Go Functional Beverages

?? ?? ?? ?? ?? ??2 . By Application

2.1 Retail Consumption

2.1.1 Supermarkets & Hypermarkets

2.1.1.1 Product Category Placement

2.1.1.1.1 Traditional Yogurt Section

2.1.1.1.2 Greek & High-Protein Yogurt Shelves

2.1.1.1.3 Probiotic & Functional Yogurt Zone

2.1.1.1.4 Plant-Based Yogurt Refrigerated Area

2.1.1.2 Packaging & Format Availability

2.1.1.2.1 Single-Serve Cups

2.1.1.2.2 Multi-Pack Family Formats

2.1.1.2.3 Drinkable Yogurt Bottles

2.1.1.2.4 Bulk & Value Packs

2.1.1.3 Merchandising Strategy

2.1.1.1.1 Eye-Level Shelf Positioning

2.1.1.1.2 End-Cap Promotions

2.1.1.1.3 Seasonal Flavor Displays

2.1.1.1.4 Private Label Yogurt Placement

2.1.1.4 Consumer Targeting

2.1.1.4.1 Health-Conscious Adults

2.1.1.4.2 Families & Children

2.1.1.4.3 Fitness & Protein Consumers

2.1.1.4.4 Premium & Organic Buyers

2.1.2 Convenience Stores

2.1.2.1 On-the-Go Consumption

2.1.2.1.1 Single-Serve Yogurt Cups

2.1.2.1.2 Drinkable Yogurt Bottles

2.1.2.1.3 Spoon-Free Yogurt Packs

2.1.2.1.4 Ready-to-Eat Protein Yogurt

2.1.2.2 Product Placement Strategy

2.1.2.2.1 Near Checkout Counters

2.1.2.2.2 Adjacent to Functional Beverages

2.1.2.2.3 Chiller Display Units

2.1.2.2.4 Impulse Purchase Sections

2.1.2.3 Pricing & Promotion

2.1.2.3.1 Premium Single-Serve Pricing

2.1.2.3.2 Combo Deals with Snacks

2.1.2.3.3 Limited-Time Flavor Launches

2.1.2.3.4 Trial & Mini Packs

2.1.3 Specialty Health Stores

2.1.3.1 Health-Focused Product Segments

2.1.3.1.1 Probiotic & Gut Health Yogurt

2.1.3.1.2 High-Protein & Fitness Yogurt

2.1.3.1.3 Organic & Clean-Label Yogurt

2.1.3.1.4 Plant-Based & Dairy-Free Yogurt

2.1.3.2 Premium & Educational Positioning

2.1.3.2.1 Clinically Backed Yogurt Formulations

2.1.3.2.2 Nutritionist-Recommended Brands

2.1.3.2.3 Ingredient Transparency Labels

2.1.3.2.4 Functional Benefit Communication

2.1.3.3 Consumer Engagement

2.1.3.3.1 In-Store Sampling Programs

2.1.3.3.2 Health Advisor Consultations

2.1.3.3.3 Wellness Workshops

2.1.3.3.4 Loyalty & Membership Discounts

2.1.4 Online Grocery Platforms

2.1.4.1 Digital Shelf Optimization

2.1.4.1.1 Search-Based Product Visibility

2.1.4.1.2 Sponsored Yogurt Listings

2.1.4.1.3 AI-Driven Product Recommendations

2.1.4.1.4 Personalized Yogurt Discovery

2.1.4.2 Product Assortment

2.1.4.2.1 Full-Portfolio Brand Availability

2.1.4.2.2 Exclusive Online-Only Variants

2.1.4.2.3 Subscription-Friendly Multipacks

2.1.4.2.4 Imported & Premium Yogurt Brands

2.1.4.3 Fulfillment & Logistics

2.1.4.3.1 Cold-Chain Delivery

2.1.4.3.2 Same-Day & Next-Day Delivery

2.1.4.3.3 Temperature-Controlled Packaging

2.1.4.3.4 Return & Replacement Policies

2.2 Foodservice & HoReCa

2.2.1 Hotels

2.2.1.1 Breakfast & Buffet Applications

2.2.1.1.1 Plain & Flavored Yogurt Stations

2.2.1.1.2 Yogurt Parfait Bars

2.2.1.1.3 Probiotic & Low-Fat Options

2.2.1.1.4 Plant-Based Yogurt Alternatives

2.2.1.2 Wellness & Premium Offerings

2.2.1.2.1 Organic & Clean-Label Yogurt

2.2.1.2.2 Protein-Rich Yogurt for Fitness Guests

2.2.1.2.3 Customized Yogurt Bowls

2.2.1.2.4 Spa & Wellness Menu Integration

2.2.2 Restaurants

2.2.2.1 Culinary Applications

2.2.2.1.1 Yogurt-Based Sauces & Dressings

2.2.2.1.2 Marinades & Cooking Ingredients

2.2.2.1.3 Desserts & Yogurt-Based Sweets

2.2.2.1.4 Fusion & Ethnic Cuisine

2.2.2.2 Health-Oriented Menus

2.2.2.2.1 Low-Calorie Menu Integration

2.2.2.2.2 High-Protein Menu Items

2.2.2.2.3 Probiotic-Rich Dishes

2.2.2.2.4 Plant-Based Menu Options

2.2.3 Caf??s & Smoothie Bars

2.2.3.1 Beverage & Bowl Applications

2.2.3.1.1 Yogurt Smoothies

2.2.3.1.2 Protein Shake Bases

2.2.3.1.3 Yogurt Bowls & Parfaits

2.2.3.1.4 Frozen Yogurt Creations

2.2.3.2 Customization & Add-Ons

2.2.3.2.1 Protein Boosters

2.2.3.2.2 Superfood Toppings

2.2.3.2.3 Functional Ingredients (Seeds, Fiber)

2.2.3.2.4 Plant-Based Yogurt Bases

2.2.4 Institutional Catering

2.2.4.1 Educational Institutions

2.2.4.1.1 School Nutrition Programs

2.2.4.1.2 College & University Cafeterias

2.2.4.1.3 Child-Friendly Yogurt Formats

2.2.4.1.4 Fortified Yogurt Options

2.2.4.2 Healthcare Facilities

2.2.4.2.1 Hospital Patient Diets

2.2.4.2.2 Digestive Health Support

2.2.4.2.3 Low-Sugar & Lactose-Free Yogurt

2.2.4.2.4 Protein-Enriched Clinical Nutrition

2.3 Preventive & Functional Nutrition

2.3.1 Digestive Wellness Programs

2.3.1.1 Probiotic & Prebiotic Yogurt

2.3.1.2 Gut Microbiome Support Products

2.3.1.3 Lactose-Free Digestive Solutions

2.3.1.4 Clinically Formulated Yogurt

2.3.2 Fitness Nutrition

2.3.2.1 High-Protein Yogurt

2.3.2.2 Post-Workout Recovery Products

2.3.2.3 Low-Fat & Low-Sugar Variants

2.3.2.4 Functional Additive Blends

2.3.3 Pediatric Nutrition

2.3.3.1 Calcium & Vitamin-Enriched Yogurt

2.3.3.2 Mild-Flavored & Low-Sugar Formulations

2.3.3.3 Kid-Friendly Packaging

2.3.3.4 Immunity-Boosting Yogurt

2.3.4 Senior Health Diets

2.3.4.1 Bone Health Yogurt (Calcium + Vitamin D)

2.3.4.2 Digestive Support Yogurt

2.3.4.3 High-Protein Easy-to-Digest Products

2.3.4.4 Low-Sodium & Low-Sugar Options

?? ?? ?? ?? ?? ??3. By Distribution Channel

3.1 Offline Retail

3.1.1 Supermarkets & Hypermarkets

3.1.1.1 National Retail Chains

3.1.1.2 Regional & Local Chains

3.1.1.3 Premium & Gourmet Supermarkets

3.1.1.4 Private Label Yogurt Brands

3.1.2 Convenience Stores

3.1.2.1 Urban Convenience Chains

3.1.2.2 Transit & Travel Hubs

3.1.2.3 Gas Station Stores

3.1.2.4 Campus & Office Locations

3.1.3 Specialty Organic Stores

3.1.3.1 Organic Food Chains

3.1.3.2 Health & Wellness Retailers

3.1.3.3 Vegan & Plant-Based Stores

3.1.3.4 Imported Premium Yogurt Retail

3.1.4 Traditional Grocery

3.1.4.1 Independent Neighborhood Stores

3.1.4.2 Wet Markets (Developing Regions)

3.1.4.3 Small Format Family Retail

3.1.4.4 Local Dairy Outlets

3.2 Online Channels

3.2.1 E-Commerce Marketplaces

3.2.1.1 One-Time Purchase

3.2.1.2 Subscription Purchase

3.2.1.3 Bulk Purchase Discounts

3.2.1.4 Influencer-Driven Promotions

3.2.2 Brand-Owned Websites

3.2.2.1 Direct-to-Consumer Sales

3.2.2.2 Exclusive Product Launches

3.2.2.3 Personalized Nutrition Tools

3.2.2.4 Loyalty & Referral Programs

3.2.3 Subscription Models

3.2.3.1 Weekly Yogurt Delivery

3.2.3.2 Family Subscription Packs

3.2.3.3 Fitness-Oriented Subscriptions

3.2.3.4 Auto-Replenishment Programs

3.2.4 Quick-Commerce Grocery Apps

3.2.4.1 10???30 Minute Delivery Platforms

3.2.4.2 Urban Micro-Fulfillment Centers

3.2.4.3 Impulse Yogurt Purchases

3.2.4.4 Dynamic Pricing Algorithms

4. By Region

4.1 Europe

4.2 North America

4.3 Asia-Pacific

4.4 Latin America

4.5 Middle East & Africa

Leading Companies in the Global Yogurt Market

Chobani LLC

Lactalis Group

General Mills (Yoplait)

Arla Foods

Fonterra Co-operative Group

Meiji Holdings

Amul (GCMMF)

Danone remains a dominant player globally, particularly in probiotic and functional yogurt segments.

Regional Insights of the Global Yogurt Market

Europe ??? Largest Market

Europe maintains its leadership position in the global yogurt market, supported by a deeply rooted yogurt consumption culture, strong brand heritage, and continuous premiumization strategies. The region benefits from high penetration of probiotic and functional yogurt products, widespread demand for organic and clean-label variants, and consistent innovation in flavor and texture profiles. Mature retail infrastructure and private-label expansion further reinforce market stability and revenue leadership.

Asia-Pacific ??? Fastest Growing Region

Asia-Pacific is emerging as the fastest-growing regional market, driven by rising health awareness, increasing protein-focused dietary habits, and rapid urbanization. Expanding modern retail networks, e-commerce growth, and strong adoption of drinkable and fortified yogurt products are accelerating market penetration. Localized flavors and affordable product innovations are also supporting volume growth across both developed and emerging economies within the region.

North America

North America demonstrates strong demand for Greek-style, high-protein, and functional yogurt products, aligned with fitness-oriented lifestyles and premium health positioning. Consumer preference for clean-label, low-sugar, and lactose-free options continues to shape product development strategies. Innovation in plant-based yogurt alternatives and subscription-based retail models is further strengthening regional competitiveness.

Latin America

Latin America is witnessing steady growth supported by an expanding middle-class population, rising disposable incomes, and increasing adoption of flavored and affordable yogurt variants. Improved cold-chain logistics and retail modernization are enhancing product accessibility. Manufacturers are focusing on cost-effective formulations and localized taste preferences to capture broader consumer segments.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but consistent expansion, fueled by urbanization, evolving dietary habits, and growing health consciousness. Increasing awareness of probiotic and digestive health benefits is supporting demand, particularly in urban centers. Investments in retail infrastructure and cold storage capabilities are expected to further improve market penetration over the forecast period.

Why the Global Yogurt Market Remains Critical

-

Strong alignment with digestive and preventive healthcare trends

-

Expanding high-protein and fitness nutrition segment

-

Rapid plant-based yogurt innovation

-

Premiumization through organic and clean-label positioning

-

Omnichannel retail and subscription-driven growth

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine projects sustained long-term growth in the global yogurt market, supported by accelerating probiotic innovation, rising protein-centric dietary patterns, and rapid expansion of plant-based alternatives. The model identifies functional positioning and premiumization as core value drivers shaping revenue growth across developed and emerging economies. Consumer Behavior Analyzer reveals a structural shift in purchasing preferences toward clean-label formulations, lactose-free variants, high-protein offerings, and personalized nutrition solutions. Health-conscious millennials, fitness-focused consumers, and aging populations are increasingly prioritizing ingredient transparency, digestive wellness, and immune-support benefits when selecting yogurt products. Innovation Tracker highlights next-generation fermentation technologies, AI-driven demand forecasting systems, sustainable and recyclable packaging formats, plant-based R&D investments, and cold-chain supply chain optimization as critical competitive differentiators. Companies leveraging advanced analytics and precision formulation capabilities are gaining measurable advantages in product development speed, shelf stability, and market responsiveness.Final Takeaway of the Global Yogurt Market

The Global Yogurt Market is transitioning into a functional, protein-driven, and premium health-oriented ecosystem. The projected CAGR of ~4.9% (2026???2033) reflects consistent expansion supported by probiotic demand, high-protein consumption trends, plant-based innovation, and omnichannel retail growth.

Future competitive leadership will be defined by companies investing in fermentation innovation, clean-label formulations, sustainable packaging, digital supply chain optimization, and diversified functional yogurt portfolios.

At Pheonix Research, our advanced forecasting frameworks deliver comprehensive Yogurt Market revenue projections, competitive benchmarking, and AI-backed strategic intelligence ??? empowering stakeholders to capitalize on post-2025 global health and nutrition trends with precision and scalable growth strategies.

?????? Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on??LinkedIn,?? and??X??for continuous intelligence and market coverage. LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7432379202638761984 X : https://x.com/Pheonix_Insight/status/2026617182092931378?s=20Table of Contents

1. Executive Summary

1.1 Global Market Snapshot (2026???2033)

1.2 Key Growth Highlights & Strategic Insights

1.3 Largest and Fastest-Growing Regions

1.4 Dominant and Emerging Market Segments

1.5 High-Potential Opportunity Areas

2. Global Yogurt Market Overview

2.1 Market Definition and Scope

2.2 Evolution of the Global Yogurt Industry

2.3 Industry Value Chain & Supply Ecosystem

2.4 Business Models (Traditional Dairy, Premium, Private Label, DTC, Plant-Based)

2.5 Pricing Structure & Margin Analysis

2.6 Regulatory and Compliance Landscape

3. Market Forecast Snapshot (2026???2033)

3.1 Market Size in 2025: USD 115.4 Billion

3.2 Projected Market Size by 2033: ~USD 168.9 Billion

3.3 Compound Annual Growth Rate (CAGR): ~4.9%

3.4 Largest Regional Market: Europe

3.5 Fastest-Growing Region: Asia-Pacific

3.6 Leading Segment: Greek & High-Protein Yogurt

3.7 Key Industry Trend: Probiotic Innovation, High-Protein & Clean-Label Positioning

3.8 Future Outlook: Functional Fortification, Plant-Based Expansion & Sustainable Packaging

4. Market Dynamics

4.1 Primary Growth Drivers

4.2 Market Restraints & Limitations

4.3 Emerging Opportunities

4.4 Key Industry Challenges

4.5 Impact of Macroeconomic and Regulatory Factors

5. Market Segmentation by Product Type (USD Billion), 2026???2033

5.1 Traditional Yogurt

5.1.1 Plain Yogurt

5.1.1.1 Full-Fat Yogurt

5.1.1.2 Low-Fat Yogurt

5.1.1.3 Non-Fat Yogurt

5.1.1.4 Organic Plain Yogurt

5.1.2 Flavored Yogurt

5.1.2.1 Fruit-Based Flavors

5.1.2.2 Dessert-Inspired Variants

5.1.2.3 Kids??? Yogurt Formats

5.1.2.4 Limited-Edition & Seasonal Flavors

5.2 Greek & High-Protein Yogurt

5.2.1 Traditional Greek Yogurt

5.2.1.1 Full-Fat Greek

5.2.1.2 Low-Fat Greek

5.2.1.3 Non-Fat Greek

5.2.1.4 Organic Greek Variants

5.2.2 Skyr & Icelandic Yogurt

5.2.2.1 Plain Skyr

5.2.2.2 Flavored Skyr

5.2.2.3 High-Protein Skyr

5.2.2.4 Fitness-Oriented Formulations

5.3 Probiotic & Functional Yogurt

5.3.1 Digestive Health Yogurt

5.3.1.1 Lactobacillus-Enriched

5.3.1.2 Bifidobacterium Blends

5.3.1.3 Prebiotic + Probiotic Yogurt

5.3.1.4 Gut Microbiome Support Variants

5.3.2 Immunity-Boosting Yogurt

5.3.2.1 Vitamin D Fortified

5.3.2.2 Zinc-Enriched

5.3.2.3 Multivitamin Blends

5.3.2.4 Herbal-Infused Yogurt

5.4 Plant-Based Yogurt Alternatives

5.4.1 Almond-Based Yogurt

5.4.2 Soy-Based Yogurt

5.4.3 Coconut-Based Yogurt

5.4.4 Oat-Based Yogurt

5.4.5 Cashew & Mixed Nut Yogurt

5.5 Drinkable Yogurt

5.5.1 Probiotic Drinkables

5.5.2 High-Protein Drinkables

5.5.3 Kids??? Yogurt Drinks

5.5.4 Functional On-the-Go Bottles

6. Market Segmentation by Distribution Channel (USD Billion), 2026???2033

6.1 Supermarkets & Hypermarkets

6.1.1 Refrigerated Dairy Aisles

6.1.1.1 Traditional Yogurt Placement

6.1.1.2 Greek & High-Protein Shelf Allocation

6.1.1.3 Probiotic & Functional Yogurt Section

6.1.1.4 Plant-Based Yogurt Refrigeration Units

6.1.1.5 Private Label Yogurt Positioning

6.1.1.6 Promotional & End-Cap Displays

6.1.2 Premium & Organic Sections

6.1.2.1 Certified Organic Yogurt Display

6.1.2.2 Grass-Fed & Non-GMO Product Shelves

6.1.2.3 Clean-Label & Low-Sugar Variants

6.1.2.4 Imported & Specialty Yogurt Brands

6.1.2.5 Sustainable Packaging Focused Products

6.1.2.6 Limited-Edition & Seasonal Premium Lines

6.2 Convenience Stores

6.2.1 Single-Serve Grab-and-Go Cups

6.2.1.1 Ready-to-Eat Yogurt Cups

6.2.1.2 Portion-Controlled Protein Packs

6.2.1.3 Kids??? Yogurt Snack Formats

6.2.1.4 Spoon-Free & Squeeze Packaging

6.2.1.5 Impulse Purchase Placement

6.2.1.6 On-the-Go Breakfast Options

6.2.2 Functional & Protein Beverage Coolers

6.2.2.1 Drinkable Yogurt Bottles

6.2.2.2 High-Protein Functional Drinks

6.2.2.3 Probiotic Beverage Variants

6.2.2.4 Fitness-Focused Recovery Drinks

6.2.2.5 Lactose-Free Drinkable Options

6.2.2.6 Premium Single-Serve Pricing Models

6.3 Online Retail

6.3.1 E-Commerce Grocery Platforms

6.3.1.1 One-Time Purchase Options

6.3.1.2 Bulk Purchase Discounts

6.3.1.3 AI-Driven Product Recommendations

6.3.1.4 Sponsored Brand Listings

6.3.1.5 Cold-Chain Delivery Integration

6.3.1.6 Same-Day & Next-Day Delivery Services

6.3.2 Health & Wellness Marketplaces

6.3.2.1 Organic & Clean-Label Yogurt Listings

6.3.2.2 High-Protein & Functional Portfolio Availability

6.3.2.3 Plant-Based & Vegan Product Categories

6.3.2.4 Subscription Bundle Offers

6.3.2.5 Influencer-Driven Promotions

6.3.2.6 Cross-Selling with Supplements & Superfoods

6.4 Direct-to-Consumer (DTC)

6.4.1 Subscription-Based Yogurt Delivery

6.4.1.1 Weekly & Monthly Subscription Plans

6.4.1.2 Family Pack Delivery Models

6.4.1.3 Fitness-Focused Protein Bundles

6.4.1.4 Auto-Replenishment Services

6.4.1.5 Loyalty & Referral Incentives

6.4.1.6 Data-Driven Personalization Programs

6.4.2 Personalized Nutrition Packs

6.4.2.1 Macro-Targeted Yogurt Plans

6.4.2.2 Gut-Health Focused Bundles

6.4.2.3 Weight Management Packs

6.4.2.4 Pediatric & Senior Nutrition Kits

6.4.2.5 Custom Flavor Selection Options

6.4.2.6 AI-Based Diet Recommendation Systems

6.5 Specialty Health Stores

6.5.1 Organic Retail Chains

6.5.1.1 Certified Organic Yogurt Supply

6.5.1.2 Grass-Fed & Hormone-Free Variants

6.5.1.3 Non-GMO & Clean-Ingredient Products

6.5.1.4 Probiotic-Focused Premium Lines

6.5.1.5 Sustainable & Ethical Brand Positioning

6.5.1.6 Nutritionist-Recommended Products

6.5.2 Vegan & Plant-Based Specialty Stores

6.5.2.1 Almond-Based Yogurt Variants

6.5.2.2 Oat-Based Yogurt Formats

6.5.2.3 Soy & Coconut-Based Alternatives

6.5.2.4 Dairy-Free Functional Blends

6.5.2.5 Allergen-Free & Gluten-Free Options

6.5.2.6 Premium Imported Plant-Based Brands

7. Market Segmentation by End User (USD Billion), 2026???2033

7.1 Millennials

7.1.1 Fitness-Oriented Consumers

7.1.1.1 High-Protein Greek Yogurt Buyers

7.1.1.2 Post-Workout Recovery Consumers

7.1.1.3 Low-Fat & Macro-Balanced Diet Followers

7.1.1.4 Protein-Enriched Drinkable Yogurt Users

7.1.1.5 Subscription-Based Nutrition Purchasers

7.1.1.6 Portion-Controlled Meal Replacement Users

7.1.2 Clean-Label & Organic Buyers

7.1.2.1 Organic-Certified Yogurt Consumers

7.1.2.2 Non-GMO & Preservative-Free Product Buyers

7.1.2.3 Low-Sugar & Natural Sweetener Seekers

7.1.2.4 Grass-Fed & Hormone-Free Dairy Preference

7.1.2.5 Sustainable & Recyclable Packaging Supporters

7.1.2.6 Plant-Based Yogurt Adopters

7.2 Generation Z (Gen Z)

7.2.1 Trend-Driven Functional Yogurt Consumers

7.2.1.1 Probiotic & Immunity-Focused Buyers

7.2.1.2 Vitamin & Mineral Fortified Yogurt Users

7.2.1.3 Energy-Boosted & Focus-Oriented Consumers

7.2.1.4 Social Media-Influenced Purchasers

7.2.1.5 Innovative & Aesthetic Packaging Seekers

7.2.1.6 On-the-Go Functional Snack Buyers

7.2.2 Flavor-Experimentation Segment

7.2.2.1 Exotic & Global Flavor Adopters

7.2.2.2 Dessert-Inspired Yogurt Consumers

7.2.2.3 Limited-Edition & Seasonal Buyers

7.2.2.4 Botanical & Herbal-Infused Variant Users

7.2.2.5 Hybrid Functional Flavor Explorers

7.2.2.6 Customizable Yogurt Bowl Consumers

7.3 Wellness & Preventive Health Consumers

7.3.1 Daily Gut-Health Users

7.3.1.1 Lactobacillus-Enriched Yogurt Users

7.3.1.2 Bifidobacterium Blend Consumers

7.3.1.3 Prebiotic + Probiotic (Synbiotic) Users

7.3.1.4 Lactose-Free Yogurt Buyers

7.3.1.5 Senior Digestive Health Consumers

7.3.1.6 Clinically Formulated Yogurt Adopters

7.3.2 High-Protein Diet Followers

7.3.2.1 Keto & Low-Carb Diet Followers

7.3.2.2 Muscle Maintenance Consumers

7.3.2.3 High-Satiety Meal Replacement Users

7.3.2.4 Weight Management Program Participants

7.3.2.5 Clinical & Therapeutic Nutrition Users

7.3.2.6 Performance-Oriented Protein Consumers

7.4 Institutional Buyers

7.4.1 Hotels & Restaurants

7.4.1.1 Breakfast Buffet Yogurt Procurement

7.4.1.2 Bulk Plain & Flavored Yogurt Supply

7.4.1.3 Yogurt-Based Culinary Applications

7.4.1.4 Premium & Organic Menu Integration

7.4.1.5 Plant-Based Yogurt Menu Offerings

7.4.1.6 Wellness-Oriented Hospitality Menus

7.4.2 Caf??s & Smoothie Bars

7.4.2.1 Smoothie Base Utilization

7.4.2.2 Protein Shake Integration

7.4.2.3 Yogurt Bowl Customization

7.4.2.4 Functional Booster Add-Ons

7.4.2.5 Frozen Yogurt Concepts

7.4.2.6 Seasonal Flavor Innovation

7.4.3 Educational & Healthcare Institutions

7.4.3.1 School Nutrition Programs

7.4.3.2 University Cafeteria Supply

7.4.3.3 Hospital Patient Diet Integration

7.4.3.4 Digestive-Support Clinical Usage

7.4.3.5 Calcium & Bone-Health Focused Supply

7.4.3.6 Elder-Care Easy-Digest Yogurt Demand

8. Market Segmentation by Region (USD Billion), 2026???2033

8.1 Europe

8.2 North America

8.3 Asia-Pacific

8.4 Latin America

8.5 Middle East & Africa

9. Regional Insights

9.1 Europe ??? Market Leadership

9.2 Asia-Pacific ??? Accelerated Growth Trajectory

9.3 North America ??? Protein & Functional Dominance

9.4 Latin America ??? Expanding Middle-Class Consumption

9.5 Middle East & Africa ??? Emerging Urban Demand

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Competitive Positioning Matrix

10.3 Mergers, Acquisitions & Strategic Partnerships

10.4 Product Launches & Innovation Trends

11. Company Profiles

11.1 Danone S.A.

11.2 Nestl?? S.A.

11.3 Chobani LLC

11.4 Lactalis Group

11.5 General Mills (Yoplait)

11.6 Arla Foods

11.7 Fonterra Co-operative Group

11.8 Meiji Holdings

11.9 Amul (GCMMF)

12. Strategic Intelligence & AI-Backed Insights

12.1 Impact of Artificial Intelligence on the Yogurt Market

12.2 Demand Forecast Modeling (Pheonix Forecast Engine)

12.3 Sustainability & Packaging Innovation Trends

12.4 Porter???s Five Forces Analysis

12.5 Investment and Expansion Strategy Outlook

13. Why the Global Yogurt Market Remains Critical

13.1 Functional Dairy Transformation

13.2 Premiumization & Margin Expansion Potential

13.3 Plant-Based Scalability & Innovation

13.4 Alignment with Global Wellness & Preventive Health Trends

14. Appendix

15. About Us

16. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Yogurt Market

Executive Framing

The Global Yogurt Market is moderately fragmented with high competitive intensity, led by major multinational players such as Danone S.A., Nestl?? S.A., Chobani LLC, Lactalis Group, and General Mills (Yoplait). These players compete alongside strong regional dairy cooperatives and emerging plant-based yogurt brands.

Current Market Reality

The market is highly dynamic, driven by functional innovation, high-protein demand, and probiotic positioning. Greek and high-protein yogurt dominate premium segments, while traditional yogurt continues to hold strong volume share across global markets.

Private label brands and local dairy producers intensify pricing competition, while global players focus on differentiation through clean-label positioning, plant-based alternatives, and functional fortification.

Key Signals and Evidence

- Strong growth in Greek, Skyr, and high-protein yogurt segments.

- Increasing demand for probiotic and digestive health-focused products.

- Rapid expansion of plant-based yogurt alternatives.

- Rising preference for clean-label, organic, and low-sugar formulations.

- Growth of online grocery and subscription-based yogurt delivery models.

Strategic Implications

- Functional Innovation: Invest in probiotic, immunity-boosting, and high-protein formulations.

- Plant-Based Expansion: Develop almond, oat, soy, and coconut-based yogurt alternatives.

- Premiumization Strategy: Focus on Greek, Skyr, and organic yogurt segments.

- Omnichannel Distribution: Strengthen presence across retail, e-commerce, and subscription models.

- Clean-Label Positioning: Emphasize natural ingredients, low sugar, and transparency.

Forward Outlook

The Global Yogurt Market is projected to reach approximately USD 168.9 billion by 2033, growing at a CAGR of ~4.9%. Europe will maintain leadership due to strong consumption patterns, while Asia-Pacific will drive the fastest growth supported by rising health awareness and urbanization.

Future competition will be shaped by probiotic innovation, plant-based diversification, AI-driven supply chains, and sustainable packaging, with brands focusing on health benefits, taste, and convenience to capture evolving consumer demand.

Value Chain

Global Yogurt Market: Value Chain & Market Dynamics

Executive Framing

The global yogurt market operates within a nutrition-driven, functional, and innovation-led value chain, supported by strong demand for probiotic, high-protein, and convenient dairy products. Yogurt has evolved into a premium, health-focused, and functional food category catering to diverse consumer needs.

The market follows an integrated operational model, where leading dairy companies manage end-to-end processes including milk sourcing, fermentation, processing, packaging, and global distribution, ensuring quality, consistency, and scalability.

Key challenges include cold-chain dependency, product perishability, raw milk price fluctuations, and increasing demand for clean-label and plant-based alternatives.

Current Market Reality

The yogurt value chain exhibits high complexity, driven by temperature-sensitive logistics, diverse product formulations, and global distribution networks. Major players such as Danone, Nestl??, and Chobani maintain integrated supply chains and strong omnichannel retail presence.

Upstream sourcing involves raw milk procurement, bacterial cultures, flavoring ingredients, and functional additives, with increasing focus on sustainable and high-quality sourcing.

Midstream operations include fermentation, blending, fortification, packaging, and refrigerated storage, with innovation centered on probiotic strains, high-protein formulations, and plant-based yogurt alternatives.

Downstream distribution spans supermarkets, convenience stores, specialty outlets, online platforms, and HoReCa channels, supported by strong cold-chain logistics.

Key Signals and Evidence

- Market growth from USD 115.4 billion (2025) to ~USD 168.9 billion (2033) at a CAGR of ~4.9%.

- Increasing demand for probiotic, digestive health, and high-protein yogurt products.

- Rapid expansion of plant-based yogurt alternatives across global markets.

- Growth in e-commerce, subscription-based models, and quick-commerce delivery.

- Rising consumer preference for clean-label, organic, and low-sugar formulations.

Buyer power is moderate-to-high due to product variety and brand competition, while supplier power is moderate, influenced by dairy input costs and sourcing conditions.

Strategic Implications

Companies must balance product innovation, cold-chain efficiency, and premium positioning to remain competitive. Leading players are focusing on functional diversification, global expansion, and brand differentiation.

Opportunities exist in high-protein, probiotic, and plant-based yogurt segments, enabling strong value creation and margin growth.

Technology adoption such as AI-driven demand forecasting, fermentation optimization, and digital supply chain management will enhance operational efficiency and reduce waste.

Sustainability initiatives including eco-friendly packaging, ethical sourcing, and reduced carbon footprint are becoming critical for long-term competitiveness.

Forward Outlook

The global yogurt market is expected to evolve into a functional, premium, and health-centric food ecosystem, driven by changing dietary preferences and increasing health awareness.

Key future developments include:

- Expansion of functional and probiotic yogurt products

- Growth in plant-based and dairy-free yogurt alternatives

- Adoption of advanced cold-chain and AI-driven supply chain systems

- Increasing focus on clean-label and sustainable product innovations

Companies that successfully integrate innovation, scalability, and sustainability will be best positioned for long-term growth.

In conclusion, the global yogurt market is transforming into a high-growth, innovation-driven, and health-focused ecosystem, where functionality, convenience, and quality define competitive success.

Investment Activity

Investment & Funding Dynamics ??? Global Yogurt Market

Executive Framing

Current Market Reality

Valued at USD 115.4 billion in 2025 and projected to reach ~USD 168.9 billion by 2033 (CAGR ~4.9%), the market is led by Europe, while Asia-Pacific emerges as the fastest-growing region. Major players such as Danone, Nestl??, and Chobani are investing in high-protein yogurt, probiotic innovation, and plant-based alternatives to strengthen their competitive positioning.

Key Signals and Evidence

- Probiotic & Functional Innovation: Increased funding in gut health, immunity-boosting, and microbiome-focused yogurt products.

- High-Protein Product Expansion: Investments in Greek yogurt, Skyr, and fitness-oriented formulations.

- Plant-Based Yogurt Development: Capital allocation toward almond, oat, soy, and coconut-based alternatives.

- Cold-Chain & Logistics Infrastructure: Expansion of temperature-controlled distribution systems.

- Clean-Label & Premium Positioning: Focus on organic, low-sugar, and natural ingredient formulations.

- M&A Activity: Active acquisitions and partnerships to expand product portfolios and regional presence.

- Digital & Retail Expansion: Investments in e-commerce, subscription models, and omnichannel strategies.

Strategic Implications

Companies investing in functional nutrition, plant-based innovation, and premium product differentiation are best positioned for long-term growth. Investors are prioritizing brands with strong R&D capabilities, diversified portfolios, and scalable global distribution networks.

Forward Outlook

Between 2026 and 2033, investment activity is expected to remain strong, with a focus on personalized nutrition, sustainable packaging, and advanced fermentation technologies. Growth will be driven by increasing health awareness, protein-centric diets, and expansion in emerging markets.

Technology & Innovation

Global Yogurt Market: Technology & Innovation

Executive Framing

Innovation in the Global Yogurt Market is driven by advancements in fermentation science, probiotic engineering, and functional ingredient integration. Companies are leveraging biotechnology, precision processing, and AI-enabled supply chains to enhance product quality, nutritional value, and consumer personalization.

Current Market Reality

The yogurt industry is rapidly evolving with the adoption of advanced fermentation techniques, high-protein processing methods, and plant-based formulation technologies. Probiotic enrichment, lactose-free variants, and clean-label products are becoming mainstream, while AI-driven cold-chain logistics and demand forecasting are improving efficiency and product availability.

Key Signals and Evidence

- Advanced Fermentation Technologies: Precision fermentation and strain optimization improve probiotic effectiveness and product consistency.

- High-Protein & Functional Innovation: Growth in Greek yogurt, Skyr, and fortified variants targeting fitness and wellness segments.

- Probiotic & Microbiome Research: Increasing focus on gut health with clinically backed probiotic strains and formulations.

- Plant-Based Yogurt Development: Expansion of almond, oat, soy, and coconut-based yogurt alternatives.

- AI-Driven Cold Chain & Supply Chain: Smart logistics ensure freshness, reduce spoilage, and optimize distribution.

- Sustainable Packaging & Clean Labeling: Eco-friendly materials and transparent ingredient sourcing enhance brand differentiation.

Strategic Implications

Companies investing in fermentation innovation, functional fortification, and plant-based R&D will gain competitive advantage. Integration of AI-driven supply chains and sustainable packaging solutions will be critical to improve margins, ensure product quality, and meet evolving consumer expectations.

Forward Outlook

Future innovation will focus on next-generation probiotics, personalized nutrition yogurt, and hybrid dairy-plant formulations. AI-enabled production systems, sustainable packaging, and microbiome-focused products will shape the next phase of growth in the global yogurt market.

Market Risk

Risk Factors and Disruption Threats in the Global Yogurt Market

Executive Framing

The Global Yogurt Market is projected to grow from USD 115.4 billion in 2025 to ~USD 168.9 billion by 2033, at a CAGR of ~4.9%. The market reflects steady expansion driven by rising demand for probiotic, high-protein, and functional dairy products. While growth remains stable, evolving consumer preferences and plant-based competition contribute to a moderate risk landscape.

Current Market Reality

Europe dominates the global yogurt market due to strong consumption habits and premium product penetration, while Asia-Pacific is the fastest-growing region driven by urbanization and health awareness. Greek and high-protein yogurt segments lead demand, supported by fitness and wellness trends.

Key Signals and Evidence

Key signals include increasing demand for digestive health solutions, clean-label and low-sugar products, and rapid expansion of plant-based yogurt alternatives. Innovation in probiotic strains and functional fortification continues to shape competitive dynamics.

Strategic Implications

Market players should prioritize functional innovation, protein enrichment, and diversification into plant-based offerings. Investments in cold-chain logistics, sustainable packaging, and digital retail channels will be essential to maintain competitive advantage.

Forward Outlook

The market is expected to evolve into a premium, health-focused, and innovation-driven segment within the dairy industry. Growth will be supported by probiotic demand, personalized nutrition, and global expansion, with companies focusing on sustainability and product differentiation to capture long-term opportunities.

Regulatory Landscape

Regulatory & Policy Landscape: Global Yogurt Market

Executive Framing

The Global Yogurt Market operates within a comprehensive regulatory framework encompassing food safety, fermentation standards, labeling, and health claim regulations. Compliance is critical to ensure product quality, consumer safety, and global market access. Regulatory authorities such as the U.S. FDA, European Food Safety Authority (EFSA), FSSAI (India), and other national agencies oversee yogurt production, probiotic usage, ingredient standards, and nutritional disclosures.

As yogurt evolves into a functional and high-protein health product, regulatory scrutiny has increased around probiotic claims, protein labeling, sugar content, and clean-label positioning. Plant-based yogurt alternatives are also subject to emerging regulations regarding classification, naming conventions, and ingredient transparency.

Current Market Reality

North America and Europe maintain strict regulations for dairy fermentation, probiotic strains, and labeling requirements. Products must clearly disclose nutritional content, including protein, sugar, fat, and live cultures. Health claims related to digestive health and immunity require scientific validation and regulatory approval.

Asia-Pacific presents a diverse regulatory environment, with countries such as China, India, and Japan enforcing specific standards for fermented dairy products, probiotic formulations, and fortified yogurt. Latin America and the Middle East & Africa are strengthening regulatory frameworks to align with international food safety standards and support growing dairy consumption.

Globally, increasing attention is being given to sugar reduction, clean-label certifications, and sustainable packaging, while plant-based yogurt alternatives are driving new regulatory developments across multiple regions.

Key Signals and Evidence

- Mandatory labeling of protein, sugar, fat content, and live probiotic cultures.

- Regulatory approval required for probiotic and digestive health claims.

- Strict standards for fermentation processes and microbial safety.

- Certification requirements for organic, non-GMO, and clean-label yogurt.

- Increasing scrutiny on sugar content and low-sugar product claims.

- Emerging regulations for plant-based yogurt classification and labeling.

Strategic Implications

Regulatory compliance significantly influences product development, especially in probiotic, high-protein, and functional yogurt segments. Companies must invest in clinical validation, ingredient traceability, and transparent labeling to support health claims and premium positioning.

The expansion of plant-based yogurt alternatives requires alignment with evolving regulatory definitions and labeling standards. Additionally, compliance with sustainability and packaging regulations is becoming essential for maintaining brand credibility and meeting consumer expectations.

Forward Outlook

The regulatory landscape is expected to tighten around probiotic claims, sugar reduction policies, and clean-label transparency. Governments may introduce stricter guidelines for functional food labeling, particularly regarding digestive health and immunity-related claims.

Plant-based yogurt alternatives will face clearer regulatory definitions and labeling frameworks, while sustainability regulations focusing on recyclable packaging and carbon footprint reduction will gain importance. Digital traceability and AI-driven compliance systems are expected to enhance regulatory monitoring and supply chain transparency.

Companies that proactively align with evolving regulations, invest in scientifically backed formulations, and adopt sustainable practices will be best positioned to achieve long-term growth in the global yogurt market.