Malaysia Dairy Market Size & Forecast 2026-2033

Malaysia Dairy Market Forecast Snapshot: 2026???2033

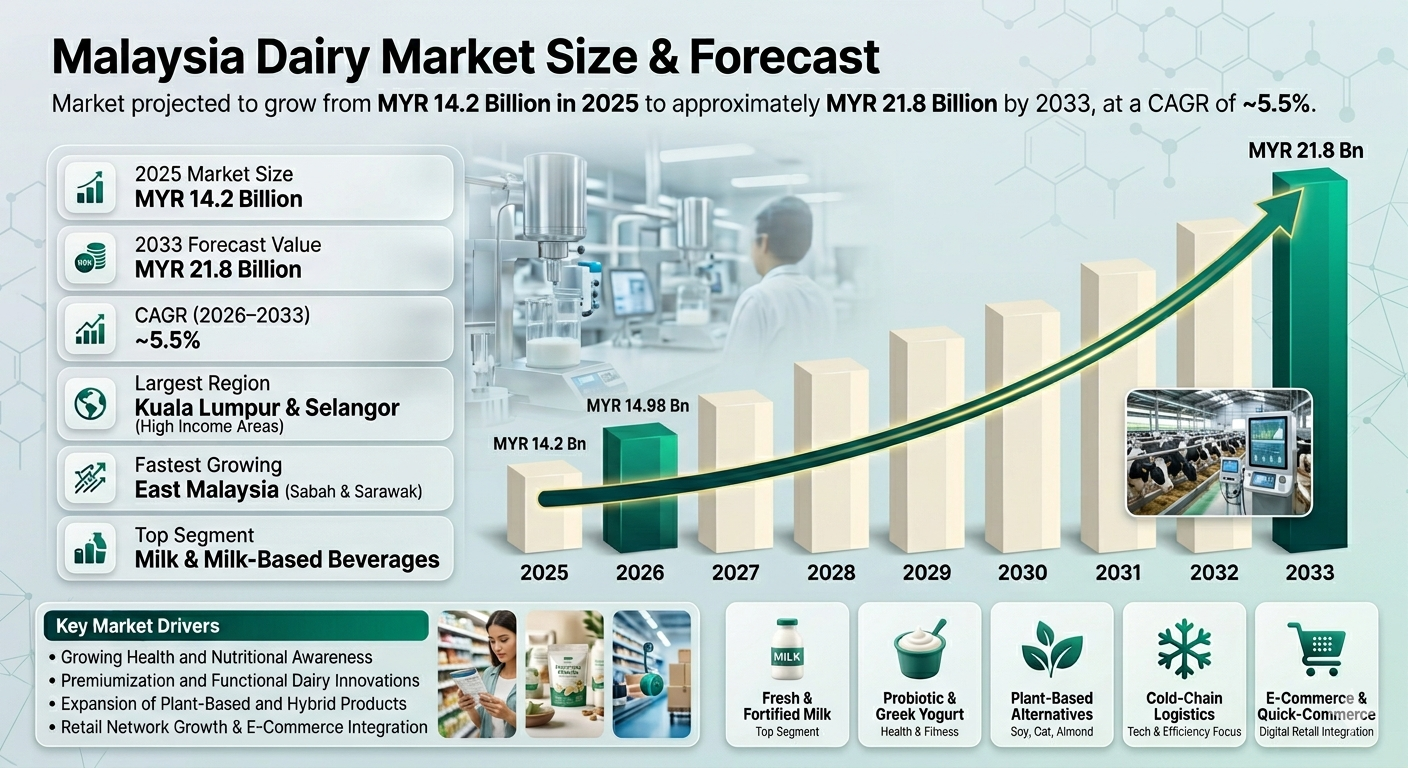

| Metric | Value |

| 2025 Market Size | MYR 14.2 Billion |

| 2033 Market Size | ~MYR 21.8 Billion |

| CAGR (2026???2033) | ~5.5% |

| Largest Region | Kuala Lumpur & Selangor |

| Fastest Growing Region | East Malaysia (Sabah & Sarawak) |

| Top Segment | Milk & Milk-Based Beverages |

| Key Trend | Functional Dairy Products, Plant-Based Alternatives & Premiumization |

| Future Focus | Digital Retail Integration, Sustainable Farming, and Value-Added Dairy |

Malaysia Dairy Market Overview

The Malaysia Dairy Market is buzzing. Driven by people wanting healthier and tastier options, the market is growing steadily. Urban folks are going for functional and fortified dairy products like yogurt with probiotics and low-fat milk. Dairy favourites like milk, yogurt, cheese, butter, cream, and ice cream are doing well. Plus, there's a plant-based boom with soy milk, almond milk, oat milk, and more for the health-conscious crowd.According to Pheonix Research, the Malaysia Dairy Market was valued at MYR 14.2 billion in 2025 and is projected to reach ~MYR 21.8 billion by 2033, growing at a CAGR of ~5.5% during 2026???2033.

Urban areas like Kuala Lumpur, Selangor, and Penang dominate dairy consumption due to higher income levels, modern retail presence, and digital commerce adoption. Meanwhile, East Malaysia (Sabah and Sarawak) is emerging as a high-growth region owing to expanding retail penetration, rising health awareness, and increasing demand for infant formula and fortified dairy.

The Malaysia dairy ecosystem is becoming increasingly premium, health-focused, and innovation-driven, with growth opportunities in functional dairy, probiotic yogurt, fortified milk, and sustainable dairy farming.

Key Drivers of Malaysia Dairy Market Growth

1. Growing Health and Nutritional Awareness

Malaysian consumers are increasingly prioritizing health and wellness, fueling demand for protein-rich, fortified, low-lactose, and probiotic dairy products. This trend is particularly strong among urban populations, fitness enthusiasts, and parents seeking high-quality nutrition for children.2. Premiumization and Functional Dairy Innovations

Rising disposable income and a shift toward healthier lifestyles are driving the adoption of premium dairy offerings such as Greek yogurt, A2 milk, fortified beverages, and specialty cheeses. Functional innovations that support immunity, digestion, and overall wellness are becoming key purchase motivators.3. Expansion of Plant-Based and Hybrid Dairy Products

The growing flexitarian and vegan consumer base is creating opportunities for plant-based milk alternatives (soy, almond, oat) and hybrid dairy products. These offerings cater to lactose-sensitive consumers while aligning with sustainability and ethical consumption trends.4. Retail Network Growth and E-Commerce Integration

The penetration of modern retail channels ??? including supermarkets, hypermarkets, convenience stores, and online grocery platforms ??? is enhancing product accessibility and enabling seamless purchase experiences. E-commerce and subscription-based models are increasingly important in reaching tech-savvy consumers.5. Technological Advancements and Cold-Chain Optimization

Investments in smart dairy processing, cold-chain logistics, and AI-enabled demand forecasting are improving product quality, reducing waste, and enhancing operational efficiency. These innovations support the growing supply of fresh, functional, and specialty dairy products across Malaysia.Malaysia Dairy Market Segmentation

?? ?? ?? ??1. By Product Type

1.1 Milk & Milk-Based Beverages

1.1.1 Fresh Milk

1.1.1.1 Whole Milk

1.1.1.2 Low-Fat Milk

1.1.1.3 Skimmed Milk

1.1.2 Flavored & Sweetened Milk

1.1.2.1 Chocolate & Cocoa Milk

1.1.2.2 Fruit-Flavored Milk

1.1.2.3 Specialty Blends

1.1.3 Functional & Fortified Milk

1.1.3.1 Protein-Enriched Milk

1.1.3.2 Vitamin & Mineral Fortified Milk

1.1.3.3 Lactose-Free / A2 Milk

1.2 Yogurt & Fermented Dairy Products

1.2.1 Regular Yogurt

1.2.1.1 Plain Yogurt

1.2.1.2 Flavored Yogurt

1.2.2 Greek & Skyr Yogurt

1.2.2.1 High-Protein Greek Yogurt

1.2.2.2 Low-Fat Skyr Variants

1.2.3 Probiotic & Functional Yogurt

1.2.3.1 Digestive Health Yogurt

1.2.3.2 Immunity-Boosting Yogurt

1.3 Cheese & Dairy Spreads

1.3.1 Hard Cheese (Cheddar, Gouda, Parmesan)

1.3.2 Soft Cheese (Cream Cheese, Ricotta, Cottage Cheese)

1.3.3 Processed Cheese & Spreads

1.4 Butter & Cream

1.4.1 Unsalted Butter

1.4.2 Salted Butter

1.4.3 Cream Products (Heavy / Whipping, Sour Cream)

1.5 Ice Cream & Frozen Dairy Desserts

1.5.1 Traditional Ice Cream

1.5.2 Gelato & Sorbet

1.5.3 Dairy-Based Frozen Yogurt

1.6 Dairy-Based Ingredients

1.6.1 Milk Powder (Whole & Skimmed)

1.6.2 Whey & Protein Powders

1.6.3 Condensed & Cream-Based Ingredients

?? ?? ?? ?? ?? ??2. By Application

2.1 Retail Consumption

2.1.1 Supermarkets & Hypermarkets

2.1.1.1 Premium Dairy Sections

2.1.1.1.1 Greek Yogurts & High-Protein Products

2.1.1.1.2 Fortified Milk & Nutritional Beverages

2.1.1.1.3 Specialty Cheeses & Artisan Dairy

2.1.1.2 Value & Mass-Market Dairy Aisles

2.1.1.2.1 Standard Milk & Milk-Based Beverages

2.1.1.2.2 Flavored Yogurts & Packaged Desserts

2.1.1.2.3 Processed Cheeses & Spreads

2.1.2 Convenience Stores

2.1.2.1 Grab-and-Go Dairy Packs

2.1.2.1.1 Single-Serve Yogurts

2.1.2.1.2 Flavored Milk Bottles

2.1.2.2 Refrigerated Snacks & Beverages

2.1.2.2.1 Protein Shakes & Smoothies

2.1.2.2.2 Dairy-Based Dessert Cups

2.1.3 Specialty Health Stores

2.1.3.1 Functional & Therapeutic Dairy

2.1.3.1.1 Lactose-Free Milk & Yogurt

2.1.3.1.2 Probiotic Supplements

2.1.3.2 Organic & Clean-Label Dairy

2.1.3.2.1 A2 Milk

2.1.3.2.2 Plant-Based Dairy Hybrids

2.1.4 Online Grocery Platforms

2.1.4.1 Subscription-Based Dairy Delivery

2.1.4.1.1 Fresh Milk Subscriptions

2.1.4.1.2 Curated Yogurt & Cheese Boxes

2.1.4.2 E-Commerce Marketplaces

2.1.4.2.1 Retailer-Hosted Online Stores

2.1.4.2.2 Brand-Owned Digital Platforms

2.2 Foodservice

2.2.1 Hotels

2.2.1.1 Fine Dining & Buffet Services

2.2.1.1.1 Artisanal Cheese Platters

2.2.1.1.2 Specialty Yogurt Offerings

2.2.1.2 In-Room & Mini-Bar Dairy Products

2.2.1.2.1 Packaged Milk & Creamers

2.2.1.2.2 Dessert Yogurts

2.2.2 Restaurants

2.2.2.1 Menu-Integrated Dairy Ingredients

2.2.2.1.1 Cheese-Based Dishes

2.2.2.1.2 Dairy Sauces & Dressings

2.2.2.2 Beverage-Centric Applications

2.2.2.2.1 Milkshakes & Lassis

2.2.2.2.2 Cream-Based Coffees

2.2.3 Caf??s & Smoothie Bars

2.2.3.1 Yogurt & Smoothie Drinks

2.2.3.1.1 Greek Yogurt Blends

2.2.3.1.2 Plant-Based Dairy Smoothies

2.2.3.2 Specialty Coffee & Dairy Integration

2.2.3.2.1 Dairy Foam & Lattes

2.2.3.2.2 Creamer & Milk Alternatives

2.2.4 Institutional Catering

2.2.4.1 School & College Canteens

2.2.4.1.1 Packaged Milk Programs

2.2.4.1.2 Yogurt & Dairy Snacks

2.2.4.2 Corporate & Hospital Catering

2.2.4.2.1 Nutritional Dairy Beverages

2.2.4.2.2 Fortified Milk & Desserts

2.3 Preventive & Functional Nutrition

2.3.1 Digestive Wellness Programs

2.3.1.1 Probiotic Yogurts

2.3.1.1.1 Adult Digestive Support

2.3.1.1.2 Pediatric Probiotic Formulas

2.3.1.2 Fermented Dairy Beverages

2.3.1.2.1 Kefir-Based Drinks

2.3.1.2.2 Live-Culture Milk Drinks

2.3.2 Fitness Nutrition

2.3.2.1 High-Protein Dairy

2.3.2.1.1 Whey-Enriched Yogurts

2.3.2.1.2 Protein Shakes & Meal Supplements

2.3.2.2 Functional Beverages

2.3.2.2.1 Electrolyte & Recovery Drinks

2.3.2.2.2 Dairy-Based Sports Smoothies

2.3.3 Pediatric Nutrition

2.3.3.1 Infant & Toddler Formulas

2.3.3.1.2 Fortified Cow Milk Formulas

2.3.3.2 Early Childhood Yogurts & Snacks

2.3.3.2.1 Flavored Yogurt Cups

2.3.3.2.2 Calcium-Fortified Desserts

2.3.4 Senior Health Diets

2.3.4.1 Bone Health Supplements

2.3.4.1.1 High-Calcium Milk

2.3.4.1.2 Fortified Dairy Snacks

2.3.4.2 Easy-Digestion Dairy Products

2.3.4.2.1 Lactose-Free Beverages

2.3.4.2.2 Probiotic Yogurts for Seniors

?? ?? ?? ?? ?? 3. By Distribution Channel

3.1 Offline Retail

3.1.1 Supermarkets & Hypermarkets

3.1.1.1 Premium Dairy Sections

3.1.1.1.1 Greek Yogurts & High-Protein Options

3.1.1.1.2 Fortified & Functional Milk Beverages

3.1.1.1.3 Artisanal Cheeses & Specialty Products

3.1.1.2 Mass-Market Dairy Aisles

3.1.1.2.1 Standard Milk Varieties (Full-Cream, Low-Fat, Skimmed)

3.1.1.2.2 Flavored Yogurts & Packaged Desserts

3.1.1.2.3 Processed Cheese & Spreads

3.1.1.3 In-Store Promotions & Sampling

3.1.1.3.1 Taste Test Zones

3.1.1.3.2 Promotional Bundles & Offers

3.1.2 Convenience Stores

3.1.2.1 Ready-to-Drink Dairy Packs

3.1.2.1.1 Single-Serve Yogurts & Drinks

3.1.2.1.2 Flavored Milk Bottles & Mini Cartons

3.1.2.2 Refrigerated Snacks & Health Options

3.1.2.2.1 Protein-Rich Dairy Drinks

3.1.2.2.2 Low-Sugar Yogurt Cups

3.1.2.3 Quick Grab-and-Go Packs

3.1.2.3.1 Travel-Size Dairy Snacks

3.1.2.3.2 On-the-Go Cheese Portions

3.1.3 Specialty Organic Stores

3.1.3.1 Organic & Natural Dairy

3.1.3.1.1 A2 Milk Varieties

3.1.3.1.2 Plant-Based & Hybrid Dairy Products

3.1.3.2 Lactose-Free & Functional Products

3.1.3.2.1 Probiotic Yogurts

3.1.3.2.2 Fortified Functional Beverages

3.1.3.3 Imported & Premium Brands

3.1.3.3.1 European Cheeses

3.1.3.3.2 Artisanal Dairy from Asia-Pacific

3.1.4 Traditional Grocery Stores

3.1.4.1 Local Fresh Milk & Dairy Counters

3.1.4.1.1 Standard Cow Milk

3.1.4.1.2 Goat Milk & Specialty Local Milks

3.1.4.2 Packaged Dairy Products

3.1.4.2.1 Yogurts & Puddings

3.1.4.2.2 Cheese Blocks & Spreads

3.1.4.3 Regional & House Brands

3.1.4.3.1 Localized Flavors & Products

3.1.4.3.2 Budget-Friendly Dairy Options

3.2 Online Channels

3.2.1 E-Commerce Marketplaces

3.2.1.1 Multi-Brand Retailer Platforms

3.2.1.1.1 Lazada & Shopee Dairy Sections

3.2.1.1.2 Marketplace Promotions & Flash Sales

3.2.1.2 Hypermarket Online Stores

3.2.1.2.1 Tesco & AEON Online Milk & Yogurt

3.2.1.2.2 Subscription Bundles

3.2.2 Brand-Owned Websites

3.2.2.1 Direct-to-Consumer Online Stores

3.2.2.1.1 Fresh Milk & Yogurt Subscriptions

3.2.2.1.2 Limited Edition / Seasonal Products

3.2.2.2 Loyalty & Membership Platforms

3.2.2.2.1 Exclusive Online Offers

3.2.2.2.2 Reward Points & Digital Coupons

3.2.3 Subscription Models

3.2.3.1 Regular Milk & Dairy Subscriptions

3.2.3.1.1 Home Delivery of Fresh Milk

3.2.3.1.2 Yogurt / Cheese Subscription Boxes

3.2.3.2 Functional & Nutritional Dairy Plans

3.2.3.2.1 Protein-Focused Deliveries

3.2.3.2.2 Digestive Health / Probiotic Packs

3.2.4 Quick-Commerce Grocery Apps

3.2.4.1 Instant Dairy Deliveries

3.2.4.1.1 GrabFood / Foodpanda Express Milk & Yogurt

3.2.4.1.2 On-Demand Cheese & Dairy Snacks

3.2.4.2 Hyperlocal Brand Partnerships

3.2.4.2.1 Local Farm-to-Door Dairy

3.2.4.2.2 Fresh Milk & Specialty Orders

3.2.4 Quick-Commerce Grocery Apps

?? ?? ?? 4. By End-User

4.1 Infants & Toddlers

4.1.1 Infant Formula Consumers

4.1.2 Pediatric Dietary Support

4.1.3 Allergy-Sensitive Infants

4.2 Health-Conscious Adults

4.2.1 Lactose-Sensitive Consumers

4.2.2 Fitness & Protein-Focused Individuals

4.2.3 Digestive Health Seekers

4.3.1 Bone Health Support

4.3.2 Easy Digestion Diets

4.3.3 Nutrient-Dense Supplementation

4.4 Culinary & Foodservice Sector

4.4.1 Hotels & Restaurants

4.4.2 Artisanal Cheese Producers

4.4.3 Bakery & Confectionery

?? ?? ?? ?? ??5. By Region (Malaysia)

5.1 Peninsular Malaysia

5.2 East Malaysia

5.3 Northern MalaysiaLeading Companies in Malaysia Dairy Market

-

Marigold HL Milk Sdn Bhd

-

Greenfields Malaysia

-

Farm Fresh Milk Sdn Bhd

-

The Laughing Cow / Bel Group

Strategic Intelligence & AI-Backed Insights

The Pheonix Demand Forecast Engine identifies robust growth driven by premium dairy offerings, fortified nutritional products, and plant-based innovations. The Consumer Behavior Analyzer highlights rising consumer preference for lactose-free, high-protein, and probiotic dairy products, reflecting evolving health-conscious trends. The Innovation Tracker underscores key differentiators, including advanced cold-chain logistics, AI-driven demand forecasting, sustainable packaging, and seamless digital retail integration, enabling brands to optimize operations and meet consumer expectations.Porter???s Five Forces Analysis

- High Competitive Rivalry ??? Intense competition among domestic and international dairy players is driving continuous innovation and pricing strategies.

- Moderate Supplier Power ??? Suppliers of raw milk and specialty ingredients exert moderate influence due to diversified sourcing options.

- Moderate Buyer Power ??? Consumers are increasingly health-conscious, demanding functional and premium dairy products, which gives them moderate leverage.

- Moderate Threat of Substitutes ??? Plant-based dairy alternatives (almond, oat, soy yogurts) present a moderate substitution threat.

- Moderate Entry Barriers ??? New entrants face moderate barriers due to regulatory compliance, distribution networks, and brand loyalty requirements.

Why the Malaysia Dairy Market is Critical

- Rising urban middle-class population and health-conscious consumers drive consistent demand.

- Adoption of AI and digital channels enhances operational efficiency and market reach.

- Expansion of premium and functional products aligns with evolving dietary trends.

- Sustainable dairy farming and eco-friendly packaging support regulatory compliance and brand trust.

Final Takeaway of Malaysia Dairy Market

The Malaysia Dairy Market is evolving into a premium, health-focused, and innovation-driven sector. A projected CAGR of 5.5% (2026???2033) highlights strong growth, fueled by functional dairy innovations, expanding urban retail networks, and increasing adoption of plant-based alternatives. Companies that prioritize R&D in functional and fortified dairy, sustainable farming practices, digital distribution channels, and consumer-centric product development will be well-positioned for sustained market leadership. At Pheonix Research, our advanced forecasting models and strategic intelligence tools deliver comprehensive revenue analysis, market insights, and actionable guidance ??? enabling stakeholders to confidently seize opportunities within the dynamic Malaysia Dairy Market.?????? Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on??LinkedIn,?? and??X??for continuous intelligence and market coverage. LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7432439384865656833 X : https://x.com/Pheonix_Insight/status/2026677625570382084?s=20Table of Contents

1. Executive Summary

1.1 Market Forecast Snapshot (2026???2033)

1.2 Malaysia Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

2. Introduction & Market Overview

2.1 Definition of the Malaysia Dairy Market

2.2 Scope of the Study

2.3 Evolution of Dairy Consumption & Premiumization

2.4 Role of Retail, Foodservice, and E-Commerce Channels

2.5 Rise of Functional, Fortified & Plant-Based Dairy Products

2.6 Technological Advancements in Dairy Processing & Cold-Chain

2.7 Sustainability & Eco-Friendly Packaging Trends

3. Research Methodology

3.1 Primary Research

3.2 Secondary Research

3.3 Market Size Estimation Model

3.4 Forecast Assumptions (2026???2033)

3.5 Data Validation & Triangulation

4. Market Dynamics

4.1 Drivers

4.1.1 Growing Health & Nutritional Awareness

4.1.2 Premiumization & Functional Dairy Innovations

4.1.3 Expansion of Plant-Based & Hybrid Dairy Products

4.1.4 Retail Network Growth & E-Commerce Integration

4.1.5 Technological Advancements & Cold-Chain Optimization

4.2 Restraints

4.2.1 Price Volatility of Raw Milk & Ingredients

4.2.2 Regulatory Compliance & Food Safety Standards

4.2.3 Supply Chain & Storage Limitations

4.3 Opportunities

4.3.1 Functional, Fortified & Probiotic Dairy Expansion

4.3.2 Plant-Based & Hybrid Dairy Innovation

4.3.3 Subscription & Direct-to-Consumer Models

4.3.4 Premium & Value-Added Dairy Segments

4.4 Challenges

4.4.1 Consumer Price Sensitivity

4.4.2 Market Fragmentation & Regional Preferences

4.4.3 Competition from Imported & Plant-Based Products

5. Malaysia Dairy Market Analysis (MYR Billion), 2026???2033

5.1 Market Size Overview

5.2 CAGR Analysis

5.3 Region-Wise Revenue Distribution

5.4 Product-Wise Revenue Split

5.5 Margin & Pricing Trend Analysis

6. Market Segmentation by Product Type (MYR Billion), 2026???2033

6.1 Milk & Milk-Based Beverages

6.1.1 Fresh Milk

6.1.1.1 Whole Milk

6.1.1.2 Low-Fat Milk

6.1.1.3 Skimmed Milk

6.1.2 Flavored & Sweetened Milk

6.1.2.1 Chocolate & Cocoa Milk

6.1.2.2 Fruit-Flavored Milk

6.1.2.3 Specialty Blends

6.1.3 Functional & Fortified Milk

6.1.3.1 Protein-Enriched Milk

6.1.3.2 Vitamin & Mineral Fortified Milk

6.1.3.3 Lactose-Free / A2 Milk

6.2 Yogurt & Fermented Dairy Products

6.2.1 Regular Yogurt

6.2.1.1 Plain Yogurt

6.2.1.2 Flavored Yogurt

6.2.2 Greek & Skyr Yogurt

6.2.2.1 High-Protein Greek Yogurt

6.2.2.2 Low-Fat Skyr Variants

6.2.3 Probiotic & Functional Yogurt

6.2.3.1 Digestive Health Yogurt

6.2.3.2 Immunity-Boosting Yogurt

6.3 Cheese & Dairy Spreads

6.3.1 Hard Cheese (Cheddar, Gouda, Parmesan)

6.3.2 Soft Cheese (Cream Cheese, Ricotta, Cottage Cheese)

6.3.3 Processed Cheese & Spreads

6.4 Butter & Cream

6.4.1 Unsalted Butter

6.4.2 Salted Butter

6.4.3 Cream Products (Heavy / Whipping, Sour Cream)

6.5 Ice Cream & Frozen Dairy Desserts

6.5.1 Traditional Ice Cream

6.5.2 Gelato & Sorbet

6.5.3 Dairy-Based Frozen Yogurt

6.6 Dairy-Based Ingredients

6.6.1 Milk Powder (Whole & Skimmed)

6.6.2 Whey & Protein Powders

6.6.3 Condensed & Cream-Based Ingredients

7. Market Segmentation by Application (MYR Billion), 2026???2033

7.1 Retail Consumption

7.1.1 Supermarkets & Hypermarkets

7.1.1.1 Premium Dairy Sections

7.1.1.1.1 Greek Yogurts & High-Protein Products

7.1.1.1.2 Fortified Milk & Nutritional Beverages

7.1.1.1.3 Specialty Cheeses & Artisan Dairy

7.1.1.2 Value & Mass-Market Dairy Aisles

7.1.1.2.1 Standard Milk & Milk-Based Beverages

7.1.1.2.2 Flavored Yogurts & Packaged Desserts

7.1.1.2.3 Processed Cheeses & Spreads

7.1.2 Convenience Stores

7.1.2.1 Grab-and-Go Dairy Packs

7.1.2.1.1 Single-Serve Yogurts

7.1.2.1.2 Flavored Milk Bottles

7.1.2.2 Refrigerated Snacks & Beverages

7.1.2.2.1 Protein Shakes & Smoothies

7.1.2.2.2 Dairy-Based Dessert Cups

7.1.3 Specialty Health Stores

7.1.3.1 Functional & Therapeutic Dairy

7.1.3.1.1 Lactose-Free Milk & Yogurt

7.1.3.1.2 Probiotic Supplements

7.1.3.2 Organic & Clean-Label Dairy

7.1.3.2.1 A2 Milk

7.1.3.2.2 Plant-Based Dairy Hybrids

7.1.4 Online Grocery Platforms

7.1.4.1 Subscription-Based Dairy Delivery

7.1.4.1.1 Fresh Milk Subscriptions

7.1.4.1.2 Curated Yogurt & Cheese Boxes

7.1.4.2 E-Commerce Marketplaces

7.1.4.2.1 Retailer-Hosted Online Stores

7.1.4.2.2 Brand-Owned Digital Platforms

7.2 Foodservice & HoReCa

7.2.1 Hotels

7.2.1.1 Fine Dining & Buffet Services

7.2.1.1.1 Artisanal Cheese Platters

7.2.1.1.2 Specialty Yogurt Offerings

7.2.2 Restaurants

7.2.2.1 Cheese-Based Dishes & Dairy Sauces

7.2.2.2 Beverage-Centric Applications (Milkshakes, Lassis)

7.2.3 Caf??s & Smoothie Bars

7.2.3.1 Yogurt & Smoothie Drinks

7.2.3.2 Specialty Coffee & Dairy Integration

7.2.4 Institutional Catering

7.2.4.1 School & College Canteens

7.2.4.2 Corporate & Hospital Catering

7.3 Preventive & Functional Nutrition

7.3.1 Digestive Wellness Programs

7.3.1.1 Probiotic Yogurts (Adult & Pediatric)

7.3.1.2 Fermented Dairy Beverages

7.3.2 Fitness Nutrition

7.3.2.1 High-Protein Dairy

7.3.2.2 Functional Beverages

7.3.3 Pediatric Nutrition

7.3.3.1 Infant & Toddler Formulas (Goat & Cow Milk)

7.3.3.2 Early Childhood Yogurts & Snacks

7.3.4 Senior Health Diets

7.3.4.1 Bone Health Supplements

7.3.4.2 Easy-Digestion Dairy Products

8. Market Segmentation by Distribution Channel (MYR Billion), 2026???2033

8.1 Offline Retail

8.1.1 Supermarkets & Hypermarkets

8.1.2 Convenience Stores

8.1.3 Specialty Organic Stores

8.1.4 Traditional Grocery Stores

8.2 Online Channels

8.2.1 E-Commerce Marketplaces

8.2.2 Brand-Owned Websites & D2C

8.2.3 Subscription Models

8.2.4 Quick-Commerce Grocery Apps

9. Market Segmentation by End-User (MYR Billion), 2026???2033

9.1 Infants & Toddlers

9.1.1 Infant Formula Consumers

9.1.2 Pediatric Dietary Support

9.1.3 Allergy-Sensitive Infants

9.2 Health-Conscious Adults

9.2.1 Lactose-Sensitive Consumers

9.2.2 Fitness & Protein-Focused Individuals

9.2.3 Digestive Health Seekers

9.3 Geriatric Population

9.3.1 Bone Health Support

9.3.2 Easy Digestion Diets

9.3.3 Nutrient-Dense Supplementation

9.4 Culinary & Foodservice Sector

9.4.1 Hotels & Restaurants

9.4.2 Artisanal Cheese Producers

9.4.3 Bakery & Confectionery

10. Market Segmentation by Region (Malaysia)

10.1 Peninsular Malaysia

10.2 East Malaysia (Sabah & Sarawak)

10.3 Northern Malaysia

11. Competitive Landscape ??? Malaysia

11.1 Market Share Analysis

11.2 Brand Positioning Matrix

11.3 Product Innovation & R&D Focus

11.4 Digital & Cold-Chain Distribution Strategies

11.5 Strategic Expansion Trends

12. Company Profiles

12.1 Dutch Lady Milk Industries Berhad

12.2 F&N Beverages Manufacturing Sdn Bhd

12.3 Marigold HL Milk Sdn Bhd

12.4 Nestl?? Malaysia Berhad

12.5 Greenfields Malaysia

12.6 Farm Fresh Milk Sdn Bhd

12.7 The Laughing Cow / Bel Group

13. Regional Insights

13.1 Kuala Lumpur & Selangor ??? Largest Market

13.2 East Malaysia (Sabah & Sarawak) ??? Fastest Growing

13.3 Penang & Northern Malaysia ??? Steady Growth

14. Strategic Intelligence & Pheonix AI-Backed Insights

14.1 Pheonix Demand Forecast Engine

14.2 Consumer Behavior Analyzer

14.3 Innovation Tracker

14.4 Cold-Chain & Digital Distribution Analytics

14.5 Automated Porter???s Five Forces Analysis

15. Future Outlook & Strategic Recommendations

15.1 Premiumization & Functional Dairy Expansion

15.2 Plant-Based & Hybrid Product Growth

15.3 Digital & E-Commerce Integration

15.4 Sustainable Farming & Eco-Friendly Packaging

15.5 Long-Term Market Outlook (2033+)

16. Appendix

17. About Us

18. Disclaimer

Competitive Landscape

Competitive Landscape of the Malaysia Dairy Market

Executive Framing

The Malaysia Dairy Market is moderately concentrated with strong domestic players such as Dutch Lady Milk Industries Berhad, F&N Beverages Manufacturing Sdn Bhd, and Marigold HL Milk Sdn Bhd, alongside global players like Nestl?? Malaysia and Greenfields Malaysia. Competition is intense in functional and premium dairy segments, with innovation, product differentiation, and digital retail integration being key differentiators.

Current Market Reality

The market is driven by urban demand for functional, fortified, and plant-based dairy alternatives. Milk, yogurt, cheese, butter, and ice cream remain core segments, while plant-based and hybrid dairy offerings are gaining traction among health-conscious and lactose-sensitive consumers. East Malaysia (Sabah & Sarawak) is emerging as a high-growth region due to retail expansion and rising health awareness.

Key Signals and Evidence

- Growing adoption of functional dairy products such as protein-enriched milk and probiotic yogurt.

- Rising penetration of plant-based alternatives (soy, almond, oat milk).

- Expansion of modern retail and e-commerce channels, enabling subscription-based and quick-commerce delivery.

- Investment in AI-driven demand forecasting and cold-chain logistics.

- Premiumization trends with fortified beverages, Greek yogurt, A2 milk, and artisanal cheeses.

Strategic Implications

- Product Innovation: Launch new functional, fortified, and plant-based dairy variants.

- Digital Retail Expansion: Enhance e-commerce, subscription models, and quick-commerce delivery capabilities.

- Premiumization Strategy: Develop high-value segments including Greek yogurt, A2 milk, and artisanal cheeses.

- Sustainable Operations: Strengthen eco-friendly packaging, sustainable farming, and traceable supply chains.

- Regional Growth Targeting: Focus on East Malaysia and urban centers for market penetration.

Forward Outlook

The Malaysia Dairy Market is expected to grow from MYR 14.2 billion in 2025 to ~MYR 21.8 billion by 2033, at a CAGR of ~5.5%. Market growth will be supported by increasing health-consciousness, urban retail expansion, premiumization, functional dairy adoption, and rising popularity of plant-based alternatives.

Companies investing in advanced R&D, AI-backed supply chain optimization, sustainable sourcing, and digital consumer engagement will be best positioned to capture long-term growth and market leadership.

Value Chain

Malaysia Dairy Market: Value Chain & Market Dynamics

Executive Framing

The Malaysia Dairy Market operates within a premium, health-driven, and innovation-focused ecosystem, supported by rising urban health awareness, plant-based alternatives, and functional dairy innovations. Consumers increasingly prefer fortified milk, probiotic yogurt, and low-lactose beverages for digestive health and wellness.

The market follows a hybrid operational model, where leading manufacturers leverage standardized production, quality control, and omnichannel distribution, while emerging brands focus on specialty formulations, organic certifications, and direct-to-consumer digital delivery. This ensures both scalability and personalization.

Key challenges include raw milk supply variability, cold-chain logistics, regulatory compliance, and sustainability pressures.

Current Market Reality

The dairy value chain in Malaysia exhibits moderate complexity, driven by diverse product types, multi-step processing, and multi-channel retail. Leading players such as Dutch Lady, F&N, Marigold, and Nestl?? operate with strong brand equity, broad product portfolios, and integrated online + offline networks.

Upstream sourcing includes fresh cow milk, goat milk, plant-based milk, functional ingredients, and probiotics. Pricing is influenced by raw material costs, production efficiency, and premium positioning.

Midstream operations cover pasteurization, fermentation, yogurt & cheese processing, flavoring, packaging, and cold storage. Innovation focuses on functional dairy products, fortified milk, probiotic yogurts, and plant-based blends.

Downstream distribution spans supermarkets, convenience stores, specialty health outlets, online D2C platforms, subscription services, and HoReCa channels, ensuring strong accessibility and repeat purchases.

Key Signals and Evidence

- Market growth from MYR 14.2 billion (2025) to ~MYR 21.8 billion (2033) at a CAGR of ~5.5%.

- Rising consumer preference for functional, fortified, and plant-based dairy products.

- Urban demand for Greek yogurt, A2 milk, and specialty cheese driving premiumization.

- Expansion of online grocery platforms, subscription dairy deliveries, and digital retail integration.

- Focus on sustainable farming, eco-friendly packaging, and AI-enabled cold-chain logistics.

Strategic Implications

Companies must balance product innovation, operational efficiency, and omnichannel reach to remain competitive. Established players focus on premium dairy expansion, fortified products, and broad retail networks.

Emerging brands can differentiate through plant-based and hybrid offerings, clean-label formulations, and digital-first D2C strategies.

Technology adoption such as AI-driven demand forecasting, cold-chain optimization, and digital consumer engagement will enhance operational efficiency and responsiveness.

Sustainability is increasingly critical, emphasizing responsible sourcing, reduced carbon footprint, and eco-friendly packaging.

Forward Outlook

The Malaysia Dairy Market is expected to evolve into a premium, functional, and health-focused ecosystem, supported by rising preventive nutrition awareness, digital retail adoption, and plant-based trends.

Key future developments include:

- Expansion of functional, fortified, and plant-based dairy products

- Growth in digital-first, subscription, and D2C distribution channels

- Adoption of sustainable and innovative packaging solutions

- Increasing use of AI-driven analytics for forecasting and personalized product recommendations

Companies integrating innovation, operational efficiency, and omnichannel distribution will be best positioned for long-term growth in Malaysia???s dynamic dairy market.

Investment Activity

Investment & Funding Dynamics ??? Malaysia Dairy Market

Executive Framing

Current Market Reality

Valued at MYR 14.2 billion in 2025 and projected to reach ~MYR 21.8 billion by 2033 (CAGR ~5.5%), the market is supported by urban consumption, modern retail penetration, and digital commerce adoption. Leading players including Dutch Lady Milk Industries, F&N Beverages, Marigold HL Milk, and Nestl?? Malaysia are investing in functional, fortified, and plant-based products to expand market share in retail, e-commerce, and foodservice segments.

Key Signals and Evidence

- Functional & Fortified Product Innovation: Expansion of protein-rich, vitamin/mineral fortified, probiotic, and lactose-free dairy.

- Plant-Based & Hybrid Offerings: Investments in soy, almond, oat, and hybrid dairy products targeting flexitarian and vegan consumers.

- Production Capacity Expansion: New manufacturing facilities, cold-chain logistics, and AI-enabled demand forecasting.

- Retail, HoReCa & E-Commerce Penetration: Partnerships with supermarkets, caf??s, online marketplaces, and subscription models.

- Premiumization Trends: Launch of Greek yogurt, A2 milk, specialty cheeses, and high-value dairy blends.

- Sustainability Initiatives: Eco-friendly packaging, sustainable sourcing, and energy-efficient processing.

- M&A & Strategic Partnerships: Selective acquisitions and alliances to strengthen product portfolios and distribution footprint.

Strategic Implications

Companies focusing on functional dairy, premiumization, plant-based innovation, and sustainable operations are best positioned to capture long-term growth. Investors are prioritizing brands with strong digital and retail integration, cold-chain capabilities, and alignment with evolving health-conscious and eco-friendly consumer preferences.

Forward Outlook

Between 2026 and 2033, investment activity is expected to remain robust, targeting functional dairy, fortified milk and yogurt, plant-based innovations, and sustainable packaging. Growth will be driven by rising urban consumption, expansion of caf?? culture, e-commerce adoption, and increasing consumer demand for premium and eco-conscious products.

Technology & Innovation

Malaysia Dairy Market: Technology & Innovation

Executive Framing

The Malaysia Dairy Market is rapidly evolving, driven by consumer demand for healthier, tastier, and premium dairy products. Functional, fortified, and plant-based alternatives are transforming traditional dairy consumption, while digital retail integration and sustainable farming practices are reshaping the supply chain. Innovation spans across probiotic yogurt, A2 and lactose-free milk, fortified beverages, and eco-friendly packaging, enabling brands to differentiate in a competitive and health-conscious landscape.

Current Market Reality

The Malaysia Dairy Market was valued at MYR 14.2 billion in 2025 and is projected to reach ~MYR 21.8 billion by 2033, growing at a CAGR of ~5.5%. Urban regions such as Kuala Lumpur, Selangor, and Penang dominate dairy consumption due to higher income, modern retail penetration, and digital commerce adoption. East Malaysia (Sabah & Sarawak) is emerging as a high-growth region with expanding retail presence and rising health awareness. Key innovations include functional dairy products, plant-based alternatives, and digital supply chain enhancements.

Key Signals and Evidence

- Functional & Fortified Dairy: Growth in probiotic yogurts, high-protein milk, and vitamin/mineral-fortified beverages.

- Plant-Based & Hybrid Innovations: Expansion of soy, almond, oat, and blended dairy products catering to lactose-sensitive and flexitarian consumers.

- Digital & E-Commerce Integration: Online subscriptions, DTC delivery models, and hyperlocal grocery apps enhance accessibility and consumer engagement.

- Sustainability & Eco-Friendly Packaging: Adoption of recyclable materials, sustainable farming practices, and optimized cold-chain logistics.

- Premiumization Trends: Increasing demand for specialty cheeses, Greek yogurt, A2 milk, and flavored/functional dairy beverages.

Strategic Implications

Companies that prioritize R&D in functional dairy, plant-based innovations, and sustainable practices are better positioned for competitive advantage. Integration of AI-driven demand forecasting, digital retail platforms, and optimized cold-chain logistics enhances operational efficiency and customer satisfaction. Brands that successfully balance health benefits, taste, and sustainability will strengthen loyalty and capture higher-value market segments.

Forward Outlook

The Malaysia Dairy Market is expected to continue growing at ~5.5% CAGR through 2033. Future developments will emphasize functional and fortified dairy, plant-based alternatives, digital commerce, and eco-friendly operations. Premiumization and innovation in product formulations, coupled with technology-enabled retail and logistics, will drive long-term market expansion and position Malaysia as a dynamic hub for health-oriented dairy solutions.

Market Risk

Risk Factors and Disruption Threats in the Malaysia Dairy Market

Executive Framing

The Malaysia Dairy Market is projected to grow from MYR 14.2 Billion in 2025 to ~MYR 21.8 Billion by 2033, at a CAGR of ~5.5%. Growth is driven by rising health consciousness, increasing demand for functional and fortified dairy products, and expanding adoption of plant-based alternatives, particularly in urban areas and infant nutrition segments.

Current Market Reality

Kuala Lumpur & Selangor hold the largest market share due to higher income levels, modern retail presence, and digital commerce adoption, while East Malaysia (Sabah & Sarawak) is the fastest-growing region fueled by retail penetration and health awareness. Milk & milk-based beverages lead the segment, supported by yogurt, cheese, and dairy-based ingredients. Plant-based options such as soy, almond, and oat milk are gaining traction.

Key Signals and Evidence

Key signals include growing demand for functional dairy, fortified and A2 milk products, and clean-label certifications. Expansion of probiotic yogurts, specialty cheeses, and fortified milk powders indicates structural market growth. Digital retail integration and subscription-based deliveries are further evidence of evolving consumer behaviors and technological adoption.

Strategic Implications

Market participants should focus on premium and functional dairy innovations, plant-based integration, and sustainable farming practices. Investments in cold-chain logistics, e-commerce, digital distribution, and traceable supply chains are critical to maintain competitiveness. Emphasizing health-focused products for infants, adults, and seniors can strengthen market positioning.

Forward Outlook

The Malaysia Dairy Market is expected to continue a health- and innovation-driven expansion. Companies prioritizing functional nutrition, fortified and clean-label dairy products, digital retail integration, and sustainable practices are positioned to capture long-term growth opportunities and lead the market.

Regulatory Landscape

Regulatory & Policy Landscape: Malaysia Dairy Market

Executive Framing

The Malaysia Dairy Market operates under a comprehensive regulatory framework governed by food safety, animal health, labeling, and import/export regulations. Key authorities include the Ministry of Health Malaysia (MOH), the Department of Veterinary Services (DVS), and the Food Safety and Quality Division. Dairy products???such as milk, yogurt, cheese, butter, cream, functional dairy, and plant-based alternatives???must comply with hygiene, pasteurization, fortification, and nutritional labeling standards.

Emerging categories, including A2 milk, lactose-free, probiotic yogurt, fortified beverages, and plant-based hybrid products, face evolving regulatory scrutiny. Claims on health benefits, nutrient fortification, and clean-label positioning require substantiation and certification to maintain compliance and consumer trust.

Current Market Reality

Malaysia maintains moderate to stringent regulatory oversight for dairy safety, product labeling, and fortification compliance. Fresh milk, yogurt, and cheese are monitored for pasteurization, microbial safety, and antibiotic residues, while fortified and functional products are evaluated for accurate nutrient content, health claims, and ingredient transparency.

Digital retail channels and cross-border imports increase the complexity of compliance, as products must meet both domestic and international standards. Non-compliance can result in product recalls, fines, or market access restrictions, making regulatory adherence critical for domestic and export-focused companies.

Key Signals and Evidence

- Mandatory pasteurization, hygiene, and cold-chain compliance for dairy products.

- Nutritional labeling regulations for fat, protein, sugar, and fortification levels.

- Monitoring of antibiotic residues, hormones, and animal health standards.

- Certification requirements for organic, A2, and clean-label dairy products.

- Regulatory oversight of functional claims for probiotics, immunity, and protein enrichment.

- Growing emphasis on sustainability, eco-friendly packaging, and ethical sourcing practices.

Strategic Implications

Regulatory compliance affects production processes, supply chain management, and product launch strategies. Companies must implement robust quality control systems, traceability technologies, and cold-chain infrastructure to ensure compliance with MOH, DVS, and international standards.

Innovation in functional, fortified, and plant-based dairy requires adherence to health claim regulations and nutrient labeling standards. Brands that adopt sustainable sourcing, transparent labeling, and ethical production practices can strengthen consumer trust and gain competitive advantage in both domestic and export markets.

Forward Outlook

The regulatory environment is expected to become increasingly focused on sustainability, fortified nutrition, and health-related claims. Authorities may introduce stricter monitoring of fortification standards, plant-based dairy labeling, and eco-friendly packaging compliance.

Functional dairy products, probiotic yogurts, and plant-based alternatives will face enhanced validation for ingredient claims and nutritional accuracy. Advanced compliance technologies such as digital traceability, blockchain-enabled supply chains, and AI-based monitoring are likely to play a larger role in regulatory adherence.

Companies that proactively align with evolving regulations, invest in sustainable production, and ensure transparent labeling will be well-positioned to capture growth opportunities in Malaysia???s dairy sector.