U.K. Oat Milk Market, Size & Forecast 2026-2033

U.K. Oat Milk Market Forecast Snapshot: 2026???2033

| Metric | Value |

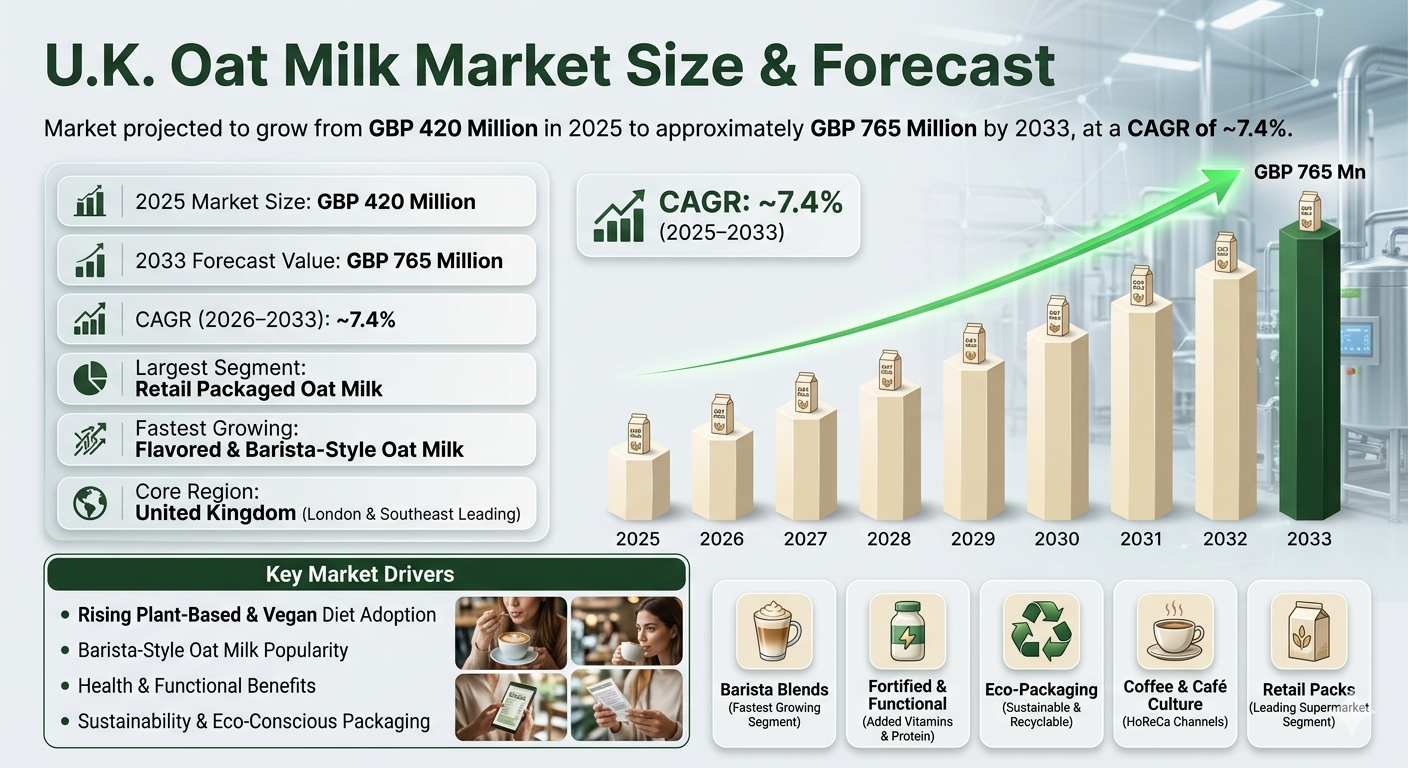

| 2025 Market Size | GBP 420 Million |

| 2033 Market Size | ~GBP 765 Million |

| CAGR (2026???2033) | ~7.4% |

| Largest Segment | Retail Packaged Oat Milk |

| Fastest Growing Segment | Flavored & Barista-Style Oat Milk |

| Key Trend | Plant-Based Innovation & Sustainability Focus |

| Future Focus | Functional Ingredients, Premium Barista Blends, and Eco-Friendly Packaging |

U.K. Oat Milk Market Overview

U.K. Oat Milk Market Overview

The UK Oat Milk Market is growing fast. People are choosing oat milk because it's a great option for those who follow plant-based diets, have lactose intolerance, or care about the environment. Oat milk is popular due to its creamy texture, versatility in coffee, tea, and recipes, and low environmental impact compared to dairy milk. Major players in the market include Oatly, Alpro, Innocent, and Tesco's own brand. The market is expected to keep growing as consumers seek sustainable and healthy alternatives to traditional dairy.According to Pheonix Research, the U.K. Oat Milk Market was valued at GBP 420 million in 2025 and is projected to reach GBP 765 million by 2033, reflecting a CAGR of ~7.4% during 2026???2033.

The market is primarily driven by increased consumption in coffee shops and home use, expanding retail presence, and rising adoption of premium barista blends. Retail-packaged oat milk dominates in terms of volume, while flavored and fortified variants are witnessing the fastest growth. The post-2025 outlook indicates further premiumization, adoption of functional ingredients (protein, vitamins, minerals), AI-enabled supply chain optimization, and eco-conscious packaging, reflecting evolving consumer expectations for health, taste, and sustainability.Key Drivers of U.K. Oat Milk Market Growth

Rising Plant-Based & Vegan Diet Adoption

Growing interest in plant-based nutrition supports increased oat milk consumption.Lactose intolerance and dairy-free preference among millennials and Gen Z are key contributors.Barista-Style Oat Milk Popularity

Specialty coffee shops and cafes drive demand for creamy, froth-friendly oat milk.Flavored and fortified variants enable differentiation and premium positioning.Health & Functional Benefits

Low saturated fat, cholesterol-free content, and fortified nutrients appeal to health-conscious consumers.Functional ingredients such as protein, calcium, and vitamins enhance adoption.Retail Expansion & E-Commerce Penetration

Supermarkets, hypermarkets, convenience stores, and online grocery platforms facilitate wider availability.Subscription-based and direct-to-consumer channels boost accessibility.Sustainability & Eco-Conscious Packaging

Oat milk production generates lower carbon footprint than dairy milk. Brands emphasizing recyclable and plant-based packaging resonate with environmentally conscious consumers.U.K. Oat Milk Market Segmentation??

?? ?? ?? 1. By Product Type

1.1 Retail Packaged Oat Milk

1.1.1 Standard Oat Milk

1.1.1.1 Original / Unsweetened

1.1.1.2 Low-Fat / Reduced-Calorie

1.1.1.3 Flavored Standard (Vanilla, Chocolate, etc.)

1.1.2 Barista-Style Oat Milk

1.1.2.1 Whole Barista Oat Milk

1.1.2.2 Low-Fat Barista Oat Milk

1.1.2.3 Organic Barista Oat Milk

1.1.3 Flavored / Sweetened Oat Milk

1.1.3.1 Vanilla Flavored

1.1.3.2 Chocolate Flavored

1.1.3.3 Seasonal / Limited Edition Flavors

1.2 Functional & Fortified Oat Milk

1.2.1 Protein-Enriched Oat Milk

1.2.1.1 Plant Protein Blend

1.2.1.2 Added Pea Protein

1.2.1.3 Multi-Protein Fortified

1.2.2 Vitamin & Mineral Fortified

1.2.2.1 Calcium Fortified

1.2.2.2 Vitamin D & B12 Fortified

1.2.2.3 Iron & Zinc Fortified

1.2.3 Organic & Clean Label Oat Milk

1.2.3.1 Certified Organic

1.2.3.2 Non-GMO & Chemical-Free

1.2.3.3 Eco-Friendly / Sustainable Packaging

1.3 Bulk / Institutional Oat Milk

1.3.1 Foodservice Packs

1.3.1.1 1L / 2L Retail Packs for Caf??s

1.3.1.2 Bulk 5L / 10L Packs for Restaurants

1.3.1.3 Ready-to-Use Beverage Bases

1.3.2 HoReCa (Hotel, Restaurant, Caf??) Oat Milk

1.3.2.1 Premium Barista Oat Milk

1.3.2.2 Standard Caf?? Oat Milk

1.3.2.3 Specialty Flavored Oat Milk

1.3.3 Industrial Ingredients

1.3.3.1 Oat Milk Powder

1.3.3.2 Concentrated Oat Extracts

1.3.3.3 Ready-to-Mix Oat Base for Food Processing

?? ?? ?? ?? ?? 2. By Distribution Channel

2.1 Supermarkets & Hypermarkets

2.1.1 National Chains (Tesco, Sainsbury???s, ASDA)

2.1.2 Regional / Local Supermarkets

2.1.3 Discount Retailers (Aldi, Lidl)

2.2 Convenience Stores

2.2.1 Urban Convenience Chains

2.2.2 Independent Local Stores

2.2.3 Petrol Station / Transit Stores

2.3 Online Retail / E-Commerce

2.3.1 Direct-to-Consumer Brand Websites

2.3.2 E-Commerce Marketplaces (Amazon, Ocado)

2.3.3 Subscription / Delivery Services (Milk Delivery, Specialty Boxes)

2.4 Specialty & Health Stores

2.4.1 Organic & Natural Food Retailers

2.4.2 Vegan & Plant-Based Retailers

2.4.3 Boutique / Premium Health Stores

2.5 Foodservice & HoReCa Channels

2.5.1 Coffee Chains & Caf??s

2.5.2 Hotels & Restaurants

2.5.3 Catering & Event Services

?? ?? ?? ?? ?? ??3. By End-User

3.1 Individual Consumers

3.1.1 Millennials & Gen Z

3.1.1.1 Urban Professionals

3.1.1.2 Social Media & Trend-Driven Consumers

3.1.2 Health-Conscious Adults

3.1.2.1 Fitness Enthusiasts

3.1.2.2 Diet-Specific Consumers (Keto, Vegan, Lactose-Free)

3.1.3 Families & Lactose-Intolerant Consumers

3.1.3.1 Parents Purchasing for Children

3.1.3.2 Lactose-Intolerant Adults

3.2 Corporate & Institutional Clients

3.2.1 Coffee Chains & Caf??s

3.2.1.1 National Coffee Chains

3.2.1.2 Independent Specialty Caf??s

3.2.2 Hotels & Restaurants

3.2.2.1 Boutique / Luxury Hotels

3.2.2.2 Chain Restaurants & Fast Casual

3.2.3 Healthcare & Educational Institutions

3.2.3.1 Hospitals & Clinics

3.2.3.2 Schools, Colleges & Universities

?? ?? ?? ?? ?? ??4. By Region

4.1 United Kingdom ??? Core Market

4.2 Europe ??? Influence & Imports

Regional Insights of the U.K. Oat Milk Market

London & Southeast ??? Premium and Urban Adoption

London and Southeast England lead the U.K. oat milk market, driven by high consumer awareness, a strong caf?? culture, and the presence of premium grocery retailers. These regions exhibit the highest consumption rates, reflecting early adoption of plant-based and specialty dairy alternatives.

Midlands & Northern England ??? Expanding Mass-Market Segment

Oat milk adoption in the Midlands and Northern England is growing rapidly, fueled by the expansion of supermarkets, retail chains, and mainstream distribution networks. These regions represent significant growth potential as oat milk becomes increasingly accessible to everyday households.

Scotland & Wales ??? Niche Premium and Sustainable Growth

Scotland and Wales show steady growth, supported by environmentally conscious consumers and lifestyle-driven purchasing patterns. Urban centers and younger demographics are the primary adopters, contributing to a niche but sustainable market expansion in these regions.

Leading Companies in the U.K. Oat Milk Market

Oatly AB

Alpro (Danone)

Plenish

Minor Figures

Rude Health

Oat-ly Good

Provamel

The Collective Dairy Alternative

Oatly AB remains one of the largest and most recognized oat milk brands in the U.K., leveraging strong retail presence, caf?? partnerships, innovative product lines including barista-style and flavored oat milk, and a focus on sustainability and clean-label initiatives.

Strategic & Technological Insights??

Pheonix Demand Forecast Engine highlights steady market growth driven by rising adoption of oat milk across retail, caf??, and HoReCa channels, supported by increasing consumer awareness of plant-based and health-focused alternatives. The Consumer Behavior Analyzer identifies a growing preference for fortified, functional, and barista-style oat milk among Millennials, Gen Z, and health-conscious adults, alongside increasing demand for sustainable and clean-label products. The Innovation Tracker emphasizes product fortification (vitamins, calcium, protein, probiotics), barista and culinary integration, eco-friendly packaging solutions, and renewable production practices as key competitive differentiators. Porter???s Five Forces Analysis reveals moderate to high competitive rivalry, evolving supplier dynamics for sustainable oat sourcing, and significant opportunities for brands leveraging functional innovation, premium caf?? partnerships, and e-commerce strategies to differentiate in the U.K. market.Why the U.K. Oat Milk Market Remains Critical

-

Promotes healthy, dairy-free, and plant-based lifestyles.

-

Supports sustainability and eco-friendly consumption habits.

-

Encourages product innovation and premiumization in plant-based beverages.

-

Enhances availability across retail, caf??, and online channels.

-

Integrates nutrition, taste, and lifestyle trends to drive consumer loyalty.

Final Takeaway of U.K. Oat Milk Market

The U.K. Oat Milk Market is steadily evolving into a functional, sustainable, and digitally integrated plant-based beverage ecosystem. The market???s CAGR 2026???2033 reflects robust growth driven by rising health consciousness, premium barista adoption, and innovative product offerings such as fortified, flavored, and clean-label oat milk.

Companies that effectively integrate product innovation, e-commerce and retail expansion, barista and HoReCa partnerships, and sustainable production practices will be best positioned for long-term value creation.

At Pheonix Research, our advanced forecasting models deliver comprehensive U.K. Oat Milk revenue projections, competitive benchmarking, and strategic intelligence ??? enabling stakeholders to capitalize on post-2025 market opportunities with data-backed confidence and growth-focused strategies.

?????? Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on??LinkedIn,?? and??X??for continuous intelligence and market coverage. LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7432099387507384321 X : https://x.com/Pheonix_Insight/status/2026338392460722622?s=20Table of Contents

1. Market Forecast Snapshot (2026???2033)

1.1 2025 Market Size ??? GBP 420 Million

1.2 2033 Market Size ??? ~GBP 765 Million

1.3 CAGR (2026???2033) ??? ~7.4%

1.4 Largest Segment ??? Retail Packaged Oat Milk

1.5 Fastest Growing Segment ??? Flavored & Barista-Style Oat Milk

1.6 Key Trend ??? Plant-Based Innovation & Sustainability Focus

1.7 Future Focus ??? Functional Ingredients, Premium Barista Blends, Eco-Friendly Packaging

2. U.K. Oat Milk Market Overview

2.1 Market Definition & Scope

2.2 Evolution of the U.K. Oat Milk Industry

2.3 Plant-Based & Vegan Consumer Adoption

2.4 Premiumization & Barista-Style Oat Milk Growth

2.5 E-Commerce & Retail Expansion

2.6 Post-2025 Market Outlook

3. Key Drivers of U.K. Oat Milk Market Growth

3.1 Rising Plant-Based & Vegan Diet Adoption

3.2 Popularity of Barista-Style Oat Milk

3.3 Health & Functional Benefits (Protein, Vitamins, Minerals)

3.4 Retail Expansion & E-Commerce Penetration

3.5 Sustainability & Eco-Conscious Packaging

3.6 Product Innovation & Flavored Variants

4. Market Segmentation by Product Type

4.1 Retail Packaged Oat Milk

4.1.1 Standard Oat Milk

4.1.1.1 Original / Unsweetened

4.1.1.2 Low-Fat / Reduced-Calorie

4.1.1.3 Flavored Standard (Vanilla, Chocolate, etc.)

4.1.2 Barista-Style Oat Milk

4.1.2.1 Whole Barista Oat Milk

4.1.2.2 Low-Fat Barista Oat Milk

4.1.2.3 Organic Barista Oat Milk

4.1.3 Flavored / Sweetened Oat Milk

4.1.3.1 Vanilla Flavored

4.1.3.2 Chocolate Flavored

4.1.3.3 Seasonal / Limited Edition Flavors

4.2 Functional & Fortified Oat Milk

4.2.1 Protein-Enriched Oat Milk

4.2.1.1 Plant Protein Blend

4.2.1.2 Added Pea Protein

4.2.1.3 Multi-Protein Fortified

4.2.2 Vitamin & Mineral Fortified

4.2.2.1 Calcium Fortified

4.2.2.2 Vitamin D & B12 Fortified

4.2.2.3 Iron & Zinc Fortified

4.2.3 Organic & Clean Label Oat Milk

4.2.3.1 Certified Organic

4.2.3.2 Non-GMO & Chemical-Free

4.2.3.3 Eco-Friendly / Sustainable Packaging

4.3 Bulk / Institutional Oat Milk

4.3.1 Foodservice Packs

4.3.1.1 1L / 2L Retail Packs for Caf??s

4.3.1.2 Bulk 5L / 10L Packs for Restaurants

4.3.1.3 Ready-to-Use Beverage Bases

4.3.2 HoReCa (Hotel, Restaurant, Caf??) Oat Milk

4.3.2.1 Premium Barista Oat Milk

4.3.2.2 Standard Caf?? Oat Milk

4.3.2.3 Specialty Flavored Oat Milk

4.3.3 Industrial Ingredients

4.3.3.1 Oat Milk Powder

4.3.3.2 Concentrated Oat Extracts

4.3.3.3 Ready-to-Mix Oat Base for Food Processing

5. Market Segmentation by Distribution Channel

5.1 Supermarkets & Hypermarkets

5.1.1 National Chains (Tesco, Sainsbury???s, ASDA)

5.1.2 Regional / Local Supermarkets

5.1.3 Discount Retailers (Aldi, Lidl)

5.2 Convenience Stores

5.2.1 Urban Convenience Chains

5.2.2 Independent Local Stores

5.2.3 Petrol Station / Transit Stores

5.3 Online Retail / E-Commerce

5.3.1 Direct-to-Consumer Brand Websites

5.3.2 E-Commerce Marketplaces (Amazon, Ocado)

5.3.3 Subscription / Delivery Services (Milk Delivery, Specialty Boxes)

5.4 Specialty & Health Stores

5.4.1 Organic & Natural Food Retailers

5.4.2 Vegan & Plant-Based Retailers

5.4.3 Boutique / Premium Health Stores

5.5 Foodservice & HoReCa Channels

5.5.1 Coffee Chains & Caf??s

5.5.2 Hotels & Restaurants

5.5.3 Catering & Event Services

6. Market Segmentation by End-User

6.1 Individual Consumers

6.1.1 Millennials & Gen Z

6.1.1.1 Urban Professionals

6.1.1.2 Social Media & Trend-Driven Consumers

6.1.2 Health-Conscious Adults

6.1.2.1 Fitness Enthusiasts

6.1.2.2 Diet-Specific Consumers (Keto, Vegan, Lactose-Free)

6.1.3 Families & Lactose-Intolerant Consumers

6.1.3.1 Parents Purchasing for Children

6.1.3.2 Lactose-Intolerant Adults

6.2 Corporate & Institutional Clients

6.2.1 Coffee Chains & Caf??s

6.2.1.1 National Coffee Chains

6.2.1.2 Independent Specialty Caf??s

6.2.2 Hotels & Restaurants

6.2.2.1 Boutique / Luxury Hotels

6.2.2.2 Chain Restaurants & Fast Casual

6.2.3 Healthcare & Educational Institutions

6.2.3.1 Hospitals & Clinics

6.2.3.2 Schools, Colleges & Universities

7. Market Segmentation by Region

7.1 United Kingdom ??? Core Market

7.2 Europe ??? Influence & Imports

8. Regional Insights

8.1 London & Southeast ??? Premium and Urban Adoption

8.2 Midlands & Northern England ??? Expanding Mass-Market Segment

8.3 Scotland & Wales ??? Niche Premium and Sustainable Growth

9. Competitive Landscape

9.1 Market Share Analysis

9.2 Competitive Positioning Matrix

9.3 Retail & HoReCa Expansion Strategies

9.4 Barista-Style & Flavored Oat Milk Innovation

9.5 Pricing, Sustainability & Premiumization Strategies

10. Leading Companies

10.1 Oatly AB

10.2 Alpro (Danone)

10.3 Plenish

10.4 Minor Figures

10.5 Rude Health

10.6 Oat-ly Good

10.7 Provamel

10.8 The Collective Dairy Alternative

11. Strategic Intelligence & AI-Backed Insights

11.1 Pheonix Demand Forecast Engine

11.2 Consumer Behavior & Trend Analytics

11.3 Innovation Tracker ??? Functional, Barista, Sustainable Packaging

11.4 Porter???s Five Forces Analysis

12. Sustainability & Regulatory Landscape

12.1 Eco-Friendly Packaging & Carbon Footprint Reduction

12.2 Plant-Based Ingredient Sourcing Standards

12.3 Food Safety & Health Regulations

12.4 Responsible Consumption & Labeling

13. Market Significance??

13.1 Promotion of Plant-Based & Health-Conscious Lifestyles

13.2 Contribution to Retail, Caf?? & HoReCa Ecosystem

13.3 Employment & Supply Chain Impact

13.4 Integration of Innovation, Sustainability & Consumer Trends

13.5 Repeat Purchase & Brand Loyalty

14. Final Takeaway

14.1 Growth Outlook (2026???2033)

14.2 Dual-Engine Growth Model (Retail Packaged vs. Barista & Functional)

14.3 Premiumization & Mass-Market Expansion Strategy

14.4 E-Commerce, Caf?? & HoReCa Integration

14.5 Strategic Recommendations for Stakeholders

15. Appendix.????

16. About Us?? ??

17. Disclaimer????

Competitive Landscape

Competitive Landscape of the U.K. Oat Milk Market

Executive Framing

The U.K. Oat Milk Market is moderately consolidated, led by prominent players such as Oatly AB, Alpro (Danone), Minor Figures, Plenish, and Rude Health. These companies dominate through strong brand positioning, caf?? partnerships, retail penetration, and continuous innovation in barista-style and functional oat milk offerings.

Current Market Reality

The market is highly dynamic, driven by plant-based adoption, sustainability concerns, and increasing demand for dairy alternatives. Retail-packaged oat milk remains the dominant segment, while barista-style and flavored variants are witnessing rapid growth due to caf?? culture expansion and premiumization trends.

Private label brands (Tesco, Aldi, Lidl) are intensifying price competition, while premium brands differentiate through clean-label ingredients, functional fortification, and eco-friendly packaging.

Key Signals and Evidence

- Strong growth in barista-style oat milk across caf??s and foodservice channels.

- Rising demand for flavored, fortified, and functional oat milk variants.

- Expansion of private label offerings increasing pricing pressure.

- High consumer preference for sustainable and low-carbon footprint products.

- Growth of e-commerce, subscription models, and direct-to-consumer channels.

Strategic Implications

- Barista Channel Expansion: Strengthen partnerships with coffee chains and independent caf??s.

- Product Innovation: Focus on functional, flavored, and premium oat milk variants.

- Sustainability Leadership: Invest in eco-friendly packaging and low-carbon production.

- Private Label Competition: Differentiate through branding, quality, and clean-label positioning.

- Omnichannel Growth: Expand across retail, e-commerce, and subscription-based delivery models.

Forward Outlook

The U.K. Oat Milk Market is projected to reach approximately GBP 765 million by 2033, growing at a CAGR of ~7.4%. Growth will be driven by increasing plant-based consumption, premium barista adoption, and expanding retail and digital distribution channels.

Future competition will center around functional ingredient integration, AI-driven supply chains, sustainable packaging innovations, and premium product positioning, with brands competing on taste, nutrition, and environmental impact.

Value Chain

U.K. Oat Milk Market: Value Chain & Market Dynamics

Executive Framing

The U.K. oat milk market operates within a sustainability-driven, health-focused, and innovation-led value chain, fueled by rising consumer demand for plant-based alternatives, lactose-free nutrition, and environmentally responsible products. Oat milk has evolved into a mainstream dairy alternative with premium, functional, and barista-oriented offerings.

The market follows a hybrid operational model, where large-scale beverage manufacturers leverage automated production, standardized formulations, and strong retail distribution, while emerging brands focus on clean-label innovation, premium positioning, and direct-to-consumer (DTC) models.

Key challenges include oat sourcing variability, processing costs, shelf-life management, and increasing demand for sustainable and recyclable packaging.

Current Market Reality

The oat milk value chain exhibits moderate complexity, driven by ingredient sourcing, processing requirements, and omnichannel distribution. Leading players such as Oatly, Alpro, and Plenish operate with strong brand positioning, caf?? partnerships, and integrated retail + HoReCa presence.

Upstream sourcing involves oats, water, enzymes, stabilizers, and fortification ingredients such as vitamins and minerals, with increasing emphasis on sustainable and locally sourced oats.

Midstream operations include oat processing, enzymatic treatment, blending, homogenization, fortification, and packaging, with innovation focused on barista-style formulations, flavored variants, and functional fortification.

Downstream distribution spans supermarkets, convenience stores, specialty retailers, online platforms, and caf??/HoReCa channels, ensuring widespread accessibility and repeat consumption.

Key Signals and Evidence

- Market growth from GBP 420 million (2025) to ~GBP 765 million (2033) at a CAGR of ~7.4%.

- Rising adoption of plant-based and dairy-free beverages across consumer segments.

- Strong demand for barista-style oat milk in caf??s and coffee chains.

- Increasing popularity of functional and fortified oat milk variants.

- Growing emphasis on sustainability and eco-friendly packaging solutions.

Buyer power remains moderate-to-high due to wide brand availability and product differentiation, while supplier power is moderate, influenced by oat sourcing and input cost fluctuations.

Strategic Implications

Companies must balance product quality, sustainability, and cost efficiency to remain competitive. Established players are focusing on retail expansion, caf?? partnerships, and premium product positioning.

Emerging brands can differentiate through clean-label formulations, functional innovation, localized sourcing, and DTC strategies.

Technology adoption such as AI-driven demand forecasting, supply chain optimization, and personalized nutrition insights will enhance operational efficiency and consumer engagement.

Sustainability remains a core focus, with emphasis on low-carbon production, recyclable packaging, and responsible sourcing practices.

Forward Outlook

The U.K. oat milk market is expected to evolve into a premium, functional, and sustainability-centric plant-based beverage ecosystem, supported by changing dietary preferences and environmental awareness.

Key future developments include:

- Expansion of functional and fortified oat milk variants

- Growth in barista-style and premium flavored products

- Adoption of sustainable and innovative packaging solutions

- Increasing use of AI-driven analytics for demand forecasting and supply chain optimization

Companies that successfully integrate innovation, sustainability, and omnichannel distribution will be best positioned for long-term growth.

In conclusion, the U.K. oat milk market is transforming into a consumer-centric, sustainable, and premium-driven ecosystem, where health, taste, and environmental impact define competitive success.

Investment Activity

Investment & Funding Dynamics ??? U.K. Oat Milk Market

Executive Framing

Current Market Reality

Valued at GBP 420 million in 2025 and projected to reach ~GBP 765 million by 2033 (CAGR ~7.4%), the market is driven by strong retail penetration and growing caf?? consumption. Leading companies such as Oatly, Alpro, and Minor Figures are investing heavily in barista-grade products, flavored variants, and sustainable production to strengthen their presence in both retail and HoReCa segments.

Key Signals and Evidence

- Barista & Premium Product Expansion: Increased investments in caf??-focused oat milk formulations and premium variants.

- Sustainable Production & Packaging: Capital directed toward low-emission production processes and recyclable packaging innovation.

- Capacity Expansion: Investment in manufacturing facilities and supply chain optimization to meet rising demand.

- Retail & HoReCa Penetration: Strategic partnerships with supermarkets, coffee chains, and foodservice providers.

- Functional Ingredient Development: Focus on protein, calcium, and vitamin fortification to enhance product differentiation.

- M&A Activity: Ongoing partnerships and selective acquisitions to expand market footprint.

- Digital & D2C Growth: Investments in e-commerce platforms, subscription services, and direct consumer engagement.

Strategic Implications

Companies focusing on premiumization, sustainability, and functional innovation are best positioned to capture long-term growth. Investors are prioritizing brands with strong caf?? integration, retail scalability, and the ability to align with evolving environmental and health-conscious consumer preferences.

Forward Outlook

Between 2026 and 2033, investment activity is expected to remain strong, with a focus on functional oat milk, premium barista blends, and sustainable packaging innovations. Growth opportunities will be driven by expanding caf?? culture, digital retail channels, and increasing demand for eco-conscious products.

Technology & Innovation

U.K. Oat Milk Market: Technology & Innovation

Executive Framing

Innovation in the U.K. Oat Milk Market is driven by advancements in plant-based processing technologies, ingredient fortification, and sustainable production systems. Companies are focusing on enhancing texture, taste, and nutritional value while aligning with environmental sustainability and clean-label consumer expectations.

Current Market Reality

The market is evolving with improved enzymatic processing techniques that enhance creaminess and stability of oat milk. Fortification with vitamins, minerals, and protein is becoming standard, while barista-specific formulations are optimized for frothing and coffee applications. AI and data analytics are increasingly used for supply chain optimization and demand forecasting.

Key Signals and Evidence

- Advanced Processing Technologies: Enzymatic hydrolysis and filtration techniques improve texture, taste, and shelf stability.

- Functional Fortification: Addition of calcium, vitamin D, B12, and protein enhances nutritional profile.

- Barista Optimization: Specialized formulations designed for foam stability and caf??-grade performance.

- Clean-Label & Plant-Based Innovation: Minimal ingredient lists and non-GMO formulations gain traction.

- Sustainable Production & Packaging: Low-carbon processing, recyclable cartons, and eco-friendly packaging solutions.

- AI-Driven Supply Chain: Demand forecasting, inventory planning, and distribution optimization using AI tools.

Strategic Implications

Brands investing in processing innovation, functional fortification, and sustainable practices will strengthen their competitive positioning. Differentiation through barista-quality products and clean-label offerings is essential, while AI integration improves operational efficiency and scalability across retail and foodservice channels.

Forward Outlook

Future innovation will focus on next-generation plant-based formulations, enhanced nutritional fortification, and carbon-neutral production. AI-enabled supply chains, premium barista blends, and sustainable packaging will define the next phase of growth in the U.K. oat milk market.

Market Risk

Executive Framing

The U.K. Oat Milk Market is projected to grow from GBP 420 million in 2025 to ~GBP 765 million by 2033, registering a CAGR of ~7.4%. The market demonstrates strong growth momentum driven by rising plant-based adoption, sustainability concerns, and increasing caf?? integration. While demand remains robust, pricing pressures and competitive intensity contribute to a moderate risk environment.

Current Market Reality

Retail packaged oat milk dominates the market, supported by widespread availability across supermarkets and online platforms. Barista-style oat milk is witnessing rapid growth due to strong demand from caf??s and coffee chains. London and Southeast regions lead in premium adoption, while broader regions are experiencing increasing mass-market penetration.

Key Signals and Evidence

Key trends include rising demand for clean-label and fortified oat milk, expansion of private label offerings, and increased consumer preference for sustainable packaging. However, volatility in raw material sourcing, pricing competition, and evolving regulatory standards around labeling and nutrition claims present ongoing challenges.

Strategic Implications

Market players should focus on product differentiation through functional fortification, premium barista formulations, and flavor innovation. Strengthening partnerships with caf??s, expanding direct-to-consumer channels, and investing in sustainable sourcing and packaging will be critical to maintaining competitive advantage.

Forward Outlook

The market is expected to evolve into a premium, functional, and sustainability-driven beverage segment. Future growth will be supported by innovation in plant-based nutrition, AI-enabled supply chains, and increasing consumer demand for eco-friendly and health-focused dairy alternatives. Companies that balance taste, nutrition, and sustainability will lead long-term market success.

Regulatory Landscape

Regulatory & Policy Landscape: U.K. Oat Milk Market

Executive Framing

The U.K. Oat Milk Market operates under a well-defined regulatory framework governed by food safety, labeling, and plant-based product standards. Regulatory compliance is essential for ensuring product safety, maintaining consumer trust, and enabling widespread retail and foodservice distribution. Authorities such as the U.K. Food Standards Agency (FSA), European Food Safety Authority (EFSA) (legacy influence), and other food regulatory bodies oversee ingredient safety, allergen labeling, nutritional disclosures, and marketing claims.

With the rise of plant-based and functional beverages, oat milk products must also comply with regulations related to clean-label claims, fortification (vitamins, calcium), and sustainability standards. Claims such as ???dairy-free,??? ???vegan,??? ???organic,??? and ???low-sugar??? must meet certification and labeling requirements.

Current Market Reality

Oat milk in the U.K. is regulated as a plant-based beverage, with strict requirements for ingredient transparency, allergen disclosure (gluten cross-contamination risks), and nutritional labeling. Fortified oat milk products must clearly declare added vitamins and minerals such as calcium, vitamin D, and B12.

The growing popularity of barista-style and flavored oat milk variants has increased scrutiny on sugar content, additives, and processing standards. Retail and e-commerce channels must comply with packaging, shelf-life labeling, and traceability requirements. Additionally, sustainability claims related to carbon footprint and eco-friendly packaging are increasingly regulated to prevent greenwashing.

Key Signals and Evidence

- Mandatory nutritional labeling including calories, sugar, and fortified nutrients.

- Allergen disclosure, particularly for gluten sensitivity and cross-contamination risks.

- Certification requirements for vegan, organic, and clean-label claims.

- Regulatory scrutiny on sugar content and flavored oat milk variants.

- Compliance standards for shelf-life, storage, and packaging materials.

- Growing oversight on sustainability claims and eco-friendly packaging.

Strategic Implications

Regulatory compliance plays a critical role in product innovation, particularly in fortified and functional oat milk segments. Companies must invest in ingredient traceability, transparent labeling, and certification to support premium and health-focused positioning.

For retail and HoReCa channels, adherence to packaging, labeling, and storage standards is essential for market expansion. Brands focusing on low-sugar formulations, clean-label positioning, and sustainable packaging can gain a competitive advantage while aligning with evolving regulatory expectations.

Forward Outlook (2026???2033)

The regulatory landscape is expected to tighten around sugar reduction, transparent labeling, and plant-based product standardization. Functional oat milk products with added nutrients will require stronger validation and clearer communication of health benefits.

Sustainability regulations, including recyclable packaging, carbon labeling, and waste reduction, will become more prominent. Companies that proactively align with regulatory trends, invest in clean-label innovation, and adopt eco-friendly practices will be best positioned for long-term growth in the U.K. oat milk market.