Global Clinical Laboratory Services Market Report, Size & Forecast 2026-2033

Global Clinical Laboratory Services Market Forecast Snapshot (2026–2033)

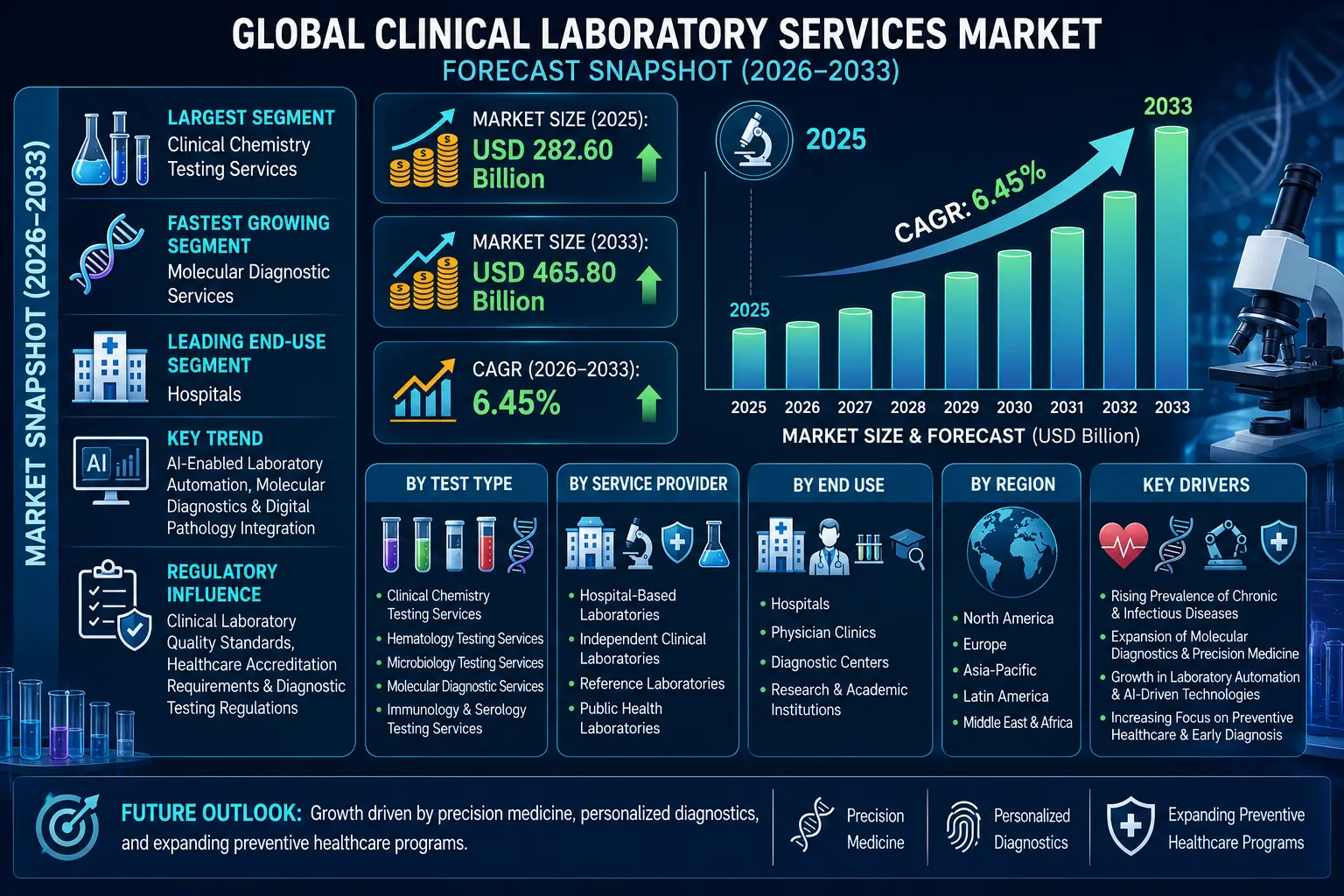

| Metric | Value |

|---|---|

| Market Size (2025) | USD 282.60 Billion |

| Market Size (2033) | USD 465.80 Billion |

| CAGR (2026–2033) | 6.45% |

| Largest Segment | Clinical Chemistry Testing Services |

| Fastest Growing Segment | Molecular Diagnostic Services |

| Leading End-Use Segment | Hospitals |

| Key Trend | AI-Enabled Laboratory Automation, Molecular Diagnostics & Digital Pathology Integration |

| Regulatory Influence | Clinical Laboratory Quality Standards, Healthcare Accreditation Requirements & Diagnostic Testing Regulations |

| Future Outlook | Growth Driven by Precision Medicine, Personalized Diagnostics & Expanding Preventive Healthcare Programs |

Global Clinical Laboratory Services Market & Forecast

The Global Clinical Laboratory Services Market is expected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at USD 282.60 billion in 2025 and is projected to reach approximately USD 465.80 billion by 2033, registering a CAGR of 6.45%. Market growth is primarily driven by increasing prevalence of chronic and infectious diseases, rising demand for early disease diagnosis, expanding preventive healthcare programs, growing adoption of molecular diagnostics, and continuous advancements in laboratory automation and digital pathology technologies.Global Clinical Laboratory Services Market Overview

Clinical laboratory services encompass diagnostic testing performed on blood, urine, tissue, and other biological specimens to support disease diagnosis, treatment selection, patient monitoring, and preventive healthcare. Services include clinical chemistry, hematology, microbiology, immunology, molecular diagnostics, pathology, cytology, and genetic testing. These services are extensively utilized by hospitals, physician offices, diagnostic laboratories, research institutions, and public health organizations worldwide.Structural Drivers of Market Growth

1. Rising Prevalence of Chronic and Infectious Diseases

Increasing incidence of diabetes, cardiovascular diseases, cancer, infectious diseases, and autoimmune disorders is driving demand for routine laboratory testing. Market Implications: Clinical laboratories continue expanding testing capabilities to support timely diagnosis and disease monitoring.2. Expansion of Molecular Diagnostics and Precision Medicine

Genomic testing, biomarker analysis, and personalized medicine are transforming laboratory diagnostics. Market Implications: Advanced molecular testing services are becoming a major growth driver across healthcare systems.3. Growing Adoption of Laboratory Automation

Automation technologies are improving testing accuracy, reducing turnaround times, and increasing laboratory efficiency. Market Implications: AI-enabled laboratory systems are optimizing workflow management and diagnostic performance.4. Increasing Focus on Preventive Healthcare

Governments and healthcare providers are encouraging routine health screening and early disease detection. Market Implications: Preventive diagnostic testing is expanding laboratory service volumes globally.Market Segmentation Analysis

By Test Type

- Clinical Chemistry Testing Services Largest segment driven by routine blood chemistry analysis for disease diagnosis and health monitoring.

- Hematology Testing Services Includes complete blood count (CBC), coagulation testing, and blood disorder diagnostics.

- Microbiology Testing Services Supports detection of bacterial, viral, fungal, and parasitic infections.

- Molecular Diagnostic Services Fastest-growing segment driven by genetic testing, PCR technologies, and precision medicine applications.

- Immunology & Serology Testing Services Used for immune system evaluation, infectious disease diagnosis, and autoimmune disease detection.

By Service Provider

- Hospital-Based Laboratories Largest segment due to integrated diagnostic services and high patient volumes.

- Independent Clinical Laboratories Provide specialized and routine testing services across healthcare providers.

- Reference Laboratories Offer advanced molecular, genetic, and specialized diagnostic testing.

- Public Health Laboratories Support disease surveillance, outbreak monitoring, and public health initiatives.

By End Use

- Hospitals Largest segment driven by inpatient and outpatient diagnostic testing requirements.

- Physician Clinics Increasing laboratory testing for primary care and specialty medical services.

- Diagnostic Centers Provide comprehensive laboratory services and preventive health screening programs.

- Research & Academic Institutions Utilize laboratory services for clinical studies, biomarker research, and translational medicine.

Regional Market Dynamics

North America

Leading region supported by advanced healthcare infrastructure, widespread laboratory automation, favorable reimbursement systems, and high diagnostic testing volumes.Europe

Driven by universal healthcare systems, growing precision medicine initiatives, and increasing adoption of advanced laboratory technologies.Asia-Pacific

Fastest-growing region supported by expanding healthcare infrastructure, rising healthcare expenditure, increasing chronic disease burden, and growing demand for diagnostic services.Latin America

Growing market driven by improving access to healthcare, expanding diagnostic laboratory networks, and increasing preventive health programs.Middle East & Africa

Emerging market supported by healthcare modernization, government investments in laboratory infrastructure, and growing demand for diagnostic testing services.Competitive Landscape

The Global Clinical Laboratory Services Market is highly competitive with international diagnostic service providers, hospital laboratory networks, and specialized testing companies focusing on laboratory automation, molecular diagnostics, and digital healthcare integration.Key Companies Operating in the Market Include:

- Labcorp Holdings Inc.

- Quest Diagnostics Incorporated

- Sonic Healthcare Limited

- Eurofins Scientific SE

- SYNLAB International GmbH

- Mayo Clinic Laboratories

- ARUP Laboratories

- Unilabs AB

- Fulgent Genetics, Inc.

- Charles River Laboratories International, Inc.

Strategic Outlook

The future of the clinical laboratory services market will be driven by advances in molecular diagnostics, artificial intelligence, digital pathology, laboratory automation, and precision medicine. Laboratories are increasingly adopting cloud-based laboratory information management systems (LIMS), AI-assisted diagnostic algorithms, and robotic automation to improve operational efficiency and diagnostic accuracy. Integration of genomics, biomarker testing, and personalized healthcare will continue expanding service offerings. Growing demand for preventive healthcare, companion diagnostics, infectious disease surveillance, and decentralized laboratory testing will further accelerate market growth. Organizations investing in advanced diagnostic technologies, digital transformation, and laboratory network expansion will strengthen their competitive position in the evolving healthcare landscape.Final Market Perspective

The Global Clinical Laboratory Services Market remains a fundamental pillar of modern healthcare delivery. Rising demand for accurate diagnostics, expanding precision medicine applications, and continuous innovation in laboratory technologies are creating substantial long-term growth opportunities. Companies delivering high-quality, automated, and technologically advanced laboratory services will be well-positioned to capitalize on the increasing global demand for diagnostic healthcare solutions.Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Growth Highlights

1.3 Demand-Supply Overview

1.4 Key Strategic Insights

1.5 Analyst Viewpoint

2. Market Overview

2.1 Introduction to Clinical Laboratory Services Market

2.2 Industry Value Chain Analysis

2.3 Market Evolution & Historical Trends

2.4 Macro-Economic Impact Analysis

2.5 Rising Demand for Early Disease Diagnosis & Preventive Healthcare

2.6 AI-Enabled Laboratory Automation, Molecular Diagnostics & Digital Pathology Integration

3. Global Clinical Laboratory Services Market Forecast Snapshot (USD Billion), 2026–2033

3.1 2025 Market Size

3.2 2033 Market Size

3.3 CAGR (2026–2033)

3.4 Largest Region

3.5 Fastest Growing Region

3.6 Largest Segment

3.7 Key Trend

3.8 Future Outlook

4. Key Drivers of Market Growth

4.1 Rising Prevalence of Chronic & Infectious Diseases

4.2 Expansion of Molecular Diagnostics & Precision Medicine

4.3 Growing Adoption of Laboratory Automation

4.4 Increasing Focus on Preventive Healthcare

4.5 Advancements in AI-Driven Laboratory Information Systems

5. Market Challenges

5.1 Stringent Regulatory & Quality Compliance Requirements

5.2 Shortage of Skilled Laboratory Professionals

5.3 High Capital Investment for Advanced Laboratory Infrastructure

5.4 Data Security & Interoperability Challenges

6. Market Segmentation by Test Type (USD Billion), 2026–2033

6.1 Clinical Chemistry Testing Services

6.1.1 Routine Clinical Chemistry Tests

6.1.1.1 Blood Glucose Testing

6.1.1.2 Lipid Profile Testing

6.1.1.3 Liver Function Tests

6.1.1.4 Kidney Function Tests

6.2 Hematology Testing Services

6.2.1 Blood Disorder Testing

6.2.1.1 Complete Blood Count (CBC)

6.2.1.2 Coagulation Testing

6.2.1.3 Hemoglobin Analysis

6.2.1.4 Bone Marrow Testing

6.3 Microbiology Testing Services

6.3.1 Infectious Disease Testing

6.3.1.1 Bacterial Testing

6.3.1.2 Viral Testing

6.3.1.3 Fungal Testing

6.3.1.4 Parasitic Testing

6.4 Molecular Diagnostic Services

6.4.1 Genomic & Molecular Testing

6.4.1.1 PCR Testing

6.4.1.2 Next-Generation Sequencing (NGS)

6.4.1.3 Genetic Testing

6.4.1.4 Companion Diagnostics

6.5 Immunology & Serology Testing Services

6.5.1 Immune System Diagnostics

6.5.1.1 Autoimmune Disease Testing

6.5.1.2 Allergy Testing

6.5.1.3 Infectious Disease Serology

6.5.1.4 Immunoassays

7. Market Segmentation by Service Provider (USD Billion), 2026–2033

7.1 Hospital-Based Laboratories

7.1.1 Integrated Hospital Laboratories

7.1.1.1 Inpatient Testing

7.1.1.2 Outpatient Testing

7.1.1.3 Emergency Laboratory Services

7.1.1.4 Critical Care Diagnostics

7.2 Independent Clinical Laboratories

7.2.1 Standalone Laboratory Networks

7.2.1.1 Routine Diagnostics

7.2.1.2 Preventive Health Screening

7.2.1.3 Home Sample Collection

7.2.1.4 Specialized Testing

7.3 Reference Laboratories

7.3.1 Advanced Diagnostic Laboratories

7.3.1.1 Molecular Testing

7.3.1.2 Genetic Testing

7.3.1.3 Esoteric Testing

7.3.1.4 Biomarker Analysis

7.4 Public Health Laboratories

7.4.1 Government Laboratory Services

7.4.1.1 Disease Surveillance

7.4.1.2 Outbreak Investigation

7.4.1.3 Population Screening

7.4.1.4 Public Health Research

8. Market Segmentation by End Use (USD Billion), 2026–2033

8.1 Hospitals

8.1.1 Public Hospitals

8.1.2 Private Hospitals

8.1.3 Multi-Specialty Hospitals

8.1.4 Academic Medical Centers

8.2 Physician Clinics

8.2.1 Primary Care Clinics

8.2.2 Specialty Clinics

8.2.3 Group Practices

8.2.4 Ambulatory Care Centers

8.3 Diagnostic Centers

8.3.1 Independent Diagnostic Centers

8.3.2 Preventive Health Centers

8.3.3 Imaging & Laboratory Centers

8.3.4 Multi-Specialty Diagnostic Networks

8.4 Research & Academic Institutions

8.4.1 Universities

8.4.2 Biomedical Research Institutes

8.4.3 Clinical Research Organizations (CROs)

8.4.4 Government Research Centers

9. Market Segmentation by Region (USD Billion), 2026–2033

9.1 North America

9.2 Europe

9.3 Asia-Pacific

9.4 Latin America

9.5 Middle East & Africa

10. Regional Market Analysis

10.1 North America – Market Leader

10.2 Asia-Pacific – Fastest Growing Region

10.3 Europe – Advanced Diagnostic & Precision Medicine Market

10.4 Latin America – Expanding Laboratory Infrastructure

10.5 Middle East & Africa – Emerging Diagnostic Healthcare Market

11. Competitive Landscape

11.1 Market Share Analysis

11.2 Competitive Positioning Matrix

11.3 Strategic Developments (M&A, Product Launches, Partnerships)

11.4 Innovation Benchmarking

11.5 Laboratory Accreditation & Regulatory Compliance Assessment

12. Company Profiles

12.1 Labcorp Holdings Inc.

12.2 Quest Diagnostics Incorporated

12.3 Sonic Healthcare Limited

12.4 Eurofins Scientific SE

12.5 SYNLAB International GmbH

12.6 Mayo Clinic Laboratories

12.7 ARUP Laboratories

12.8 Unilabs AB

12.9 Fulgent Genetics, Inc.

12.10 Charles River Laboratories International, Inc.

13. Strategic Intelligence & AI-Driven Insights

13.1 Pheonix Demand Forecast Engine

13.2 Clinical Laboratory Services Intelligence Dashboard

13.3 AI-Powered Diagnostic Workflow Analytics

13.4 Predictive Laboratory Capacity & Testing Intelligence Engine

13.5 Laboratory Quality Compliance & Regulatory Monitoring System

14. Investment & Growth Opportunities

14.1 Molecular Diagnostic Laboratory Expansion

14.2 AI-Enabled Laboratory Automation Solutions

14.3 Digital Pathology & Precision Medicine Platforms

14.4 Preventive Healthcare & Population Screening Programs

14.5 Laboratory Network Expansion Across Emerging Markets

15. Why the Global Clinical Laboratory Services Market Remains Critical

15.1 Increasing Burden of Chronic & Infectious Diseases

15.2 Growing Adoption of Precision Medicine

15.3 Continuous Innovation in Molecular Diagnostics & Laboratory Automation

15.4 Expansion of Preventive Healthcare Programs

15.5 Long-Term Growth Across Global Diagnostic Healthcare Markets

16. Appendix

17. About Pheonix Research

18. Disclaimer

Competitive Landscape

Global Clinical Laboratory Services Market Competitive Intensity & Market Structure Overview

The Global Clinical Laboratory Services Market is highly competitive and characterized by the presence of multinational diagnostic service providers, hospital laboratory networks, reference laboratories, specialty testing companies, and healthcare diagnostics organizations. Competitive intensity is driven by testing accuracy, turnaround time, laboratory automation, molecular diagnostic capabilities, geographic reach, regulatory compliance, and integrated digital laboratory services.

Companies compete across a broad range of diagnostic services including clinical chemistry, hematology, microbiology, immunology, molecular diagnostics, pathology, genetic testing, and specialized reference laboratory services. Increasing demand for precision medicine, preventive healthcare, and advanced diagnostic testing is intensifying competition while encouraging continuous investment in laboratory technologies and service expansion.

The market structure is evolving toward highly automated, AI-enabled, and digitally connected laboratory ecosystems. Market participants are investing in laboratory automation, molecular diagnostics, cloud-based laboratory information management systems (LIMS), digital pathology, artificial intelligence, and strategic acquisitions to strengthen operational efficiency, testing capacity, and competitive positioning.

Global Clinical Laboratory Services Market Competitive Intensity & Market Structure Current Scenario

Leading Global Clinical Laboratory Services Companies

- Labcorp Holdings Inc.: One of the world’s leading laboratory service providers offering comprehensive diagnostic testing, drug development support, genomic testing, and advanced laboratory solutions through an extensive global network.

- Quest Diagnostics Incorporated: A major diagnostic information services provider recognized for its broad clinical testing portfolio, advanced laboratory infrastructure, and strong presence across routine and specialized diagnostics.

- Sonic Healthcare Limited: A global laboratory medicine company operating extensive pathology and diagnostic laboratory networks across multiple countries with a focus on quality testing services.

- Eurofins Scientific SE: A leading provider of laboratory testing services specializing in clinical diagnostics, life sciences, genomic analysis, and specialized laboratory solutions.

- SYNLAB International GmbH: An international diagnostics company delivering clinical laboratory services, pathology, and specialized testing through an extensive European laboratory network.

- Mayo Clinic Laboratories: A renowned reference laboratory offering highly specialized diagnostic testing, precision medicine services, and advanced clinical laboratory expertise.

- ARUP Laboratories: A leading reference laboratory supporting hospitals, academic medical centers, and healthcare providers with advanced diagnostic and molecular testing services.

- Unilabs AB: A major diagnostics provider offering laboratory testing, pathology, imaging, and related healthcare diagnostic services across international markets.

- Fulgent Genetics, Inc.: A specialized diagnostics company focused on genomic testing, precision medicine, molecular diagnostics, and genetic analysis solutions.

- Charles River Laboratories International, Inc.: A global life sciences organization providing specialized laboratory testing, research services, and preclinical support for pharmaceutical and biotechnology industries.

Key Competitive Intensity & Market Structure Drivers

Growing demand for molecular diagnostics, precision medicine, and personalized healthcare is intensifying competition among clinical laboratory service providers worldwide.

Artificial intelligence, laboratory automation, robotic sample processing, and digital pathology technologies are becoming key competitive differentiators for improving operational efficiency and diagnostic accuracy.

Increasing investments in genomics, biomarker testing, and high-throughput laboratory platforms are enabling companies to expand specialized diagnostic capabilities and strengthen market leadership.

Expansion of integrated laboratory networks, reference testing services, and cloud-based laboratory information management systems is improving workflow efficiency and supporting scalable diagnostic operations.

Strategic partnerships, laboratory acquisitions, and investments in advanced testing technologies are accelerating global market expansion while increasing competition across clinical diagnostics and laboratory services.

Strategic Implications of Competitive Intensity & Market Structure

Organizations with extensive laboratory networks, advanced molecular diagnostic capabilities, and comprehensive testing portfolios are expected to maintain strong competitive advantages.

Investment in AI-enabled diagnostics, laboratory automation, digital pathology, and integrated healthcare information systems is becoming increasingly important for long-term market leadership.

Companies focusing on precision diagnostics, preventive healthcare services, and next-generation genomic testing are likely to strengthen revenue growth and market share.

Strategic collaborations with hospitals, physician networks, research institutions, biotechnology companies, and healthcare systems are improving testing accessibility, innovation, and operational scalability.

Businesses capable of delivering accurate diagnostics, rapid turnaround times, regulatory compliance, technological innovation, and integrated laboratory services will be best positioned to compete effectively in the evolving global clinical laboratory services market.

Global Clinical Laboratory Services Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global clinical laboratory services market is expected to become increasingly technology-driven, data-centric, and precision medicine-focused as demand for advanced diagnostics continues to expand globally.

Future competition will be shaped by AI-assisted diagnostics, molecular testing innovations, digital pathology platforms, automated laboratory workflows, cloud-based laboratory information management systems, and precision medicine technologies.

Market participants are expected to increase investments in genomics, biomarker discovery, laboratory automation, predictive analytics, and integrated digital diagnostic ecosystems to strengthen competitive positioning.

Over the forecast period, organizations that successfully combine diagnostic accuracy, operational efficiency, technological innovation, regulatory compliance, and scalable laboratory infrastructure will be best positioned to lead the evolving global clinical laboratory services market.

Value Chain

Global Clinical Laboratory Services Market Value Chain & Supply Chain Evolution Overview

The Global Clinical Laboratory Services Market operates through a highly integrated healthcare value chain encompassing test ordering, patient specimen collection, sample transportation, laboratory processing, diagnostic analysis, quality assurance, result reporting, and clinical decision support. The market includes clinical chemistry, hematology, microbiology, immunology, molecular diagnostics, pathology, genetic testing, and specialized laboratory services delivered through hospitals, independent laboratories, reference laboratories, and public health institutions.

The industry is driven by the increasing prevalence of chronic and infectious diseases, rising demand for precision diagnostics, expansion of preventive healthcare programs, and continuous advancements in laboratory automation and molecular testing technologies. Healthcare providers are increasingly investing in digital laboratory infrastructure to improve testing efficiency, diagnostic accuracy, and patient outcomes.

The adoption of laboratory information management systems (LIMS), automated analyzers, robotic sample handling, digital pathology platforms, and molecular diagnostic technologies has significantly enhanced operational efficiency across the laboratory value chain. Organizations are strengthening laboratory networks while improving turnaround times, workflow automation, and regulatory compliance.

Advancements in artificial intelligence, laboratory automation, cloud-based informatics, next-generation sequencing, digital pathology, and predictive analytics are transforming the industry’s value chain while improving diagnostic precision, laboratory productivity, and healthcare delivery.

Global Clinical Laboratory Services Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Test Ordering & Patient Registration: Physician consultation, electronic test ordering, patient registration, insurance verification, and laboratory scheduling.

- Specimen Collection & Sample Transportation: Collection of blood, urine, tissue, and other biological specimens followed by secure transportation to diagnostic laboratories.

- Laboratory Processing & Diagnostic Testing: Sample preparation, clinical chemistry, hematology, microbiology, immunology, molecular diagnostics, pathology, and genetic testing.

- Quality Assurance & Regulatory Compliance: Internal quality control, laboratory accreditation, validation procedures, proficiency testing, and compliance with clinical laboratory standards.

- Data Analysis & Diagnostic Reporting: Interpretation of laboratory results, AI-assisted diagnostics, laboratory information management systems (LIMS), and secure report generation.

- Clinical Decision Support & Healthcare Integration: Integration of laboratory findings with electronic health records (EHRs), physician consultation, treatment planning, and patient monitoring.

- End User Healthcare Services: Delivery of diagnostic services to hospitals, physician clinics, diagnostic centers, research institutions, and public health organizations.

Company-to-Stage Mapping

- Test Ordering & Patient Registration: Hospitals, physician practices, outpatient clinics, healthcare information system providers, and EHR platform vendors.

- Specimen Collection & Sample Transportation: Hospital collection centers, independent diagnostic laboratories, specimen logistics providers, and healthcare courier services.

- Laboratory Processing & Diagnostic Testing: Labcorp Holdings Inc., Quest Diagnostics Incorporated, Sonic Healthcare Limited, Eurofins Scientific SE, SYNLAB International GmbH, Mayo Clinic Laboratories, ARUP Laboratories, Unilabs AB, and Fulgent Genetics, Inc.

- Quality Assurance & Regulatory Compliance: Clinical laboratory accreditation organizations, quality management providers, laboratory compliance specialists, and regulatory agencies.

- Data Analysis & Diagnostic Reporting: Laboratory information management system (LIMS) providers, AI-powered diagnostic software developers, digital pathology companies, and healthcare IT providers.

- Clinical Decision Support & Healthcare Integration: Hospitals, physicians, healthcare providers, EHR vendors, and clinical decision support platform providers.

- End User Healthcare Services: Hospitals, diagnostic centers, physician clinics, research institutions, academic laboratories, and public health agencies.

Key Value Chain & Supply Chain Evolution Signals in Global Clinical Laboratory Services Market

Expansion of Molecular Diagnostic Testing

Healthcare providers are increasingly adopting molecular diagnostics and genomic testing to enable precision medicine and earlier disease detection.

Growing Adoption of AI-Enabled Laboratory Automation

Artificial intelligence, robotic automation, and smart laboratory systems are improving workflow efficiency, testing accuracy, and turnaround times.

Integration of Digital Pathology Platforms

Digital pathology technologies are enhancing remote diagnostics, collaboration among specialists, and efficient pathology workflows.

Increasing Implementation of Cloud-Based Laboratory Informatics

Cloud-enabled LIMS and integrated healthcare data platforms are improving laboratory connectivity, data management, and operational visibility.

Expansion of Preventive Healthcare and Screening Programs

Governments and healthcare providers are increasing investments in routine diagnostic screening to support early disease detection and population health management.

Strengthening Laboratory Quality and Regulatory Compliance

Clinical laboratories continue investing in quality management systems, accreditation programs, and standardized testing protocols to ensure diagnostic reliability.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Advanced Laboratory Automation

Automation technologies can improve laboratory productivity, reduce manual errors, and increase testing capacity.

Expansion of Molecular and Precision Diagnostic Capabilities

Organizations investing in advanced molecular testing platforms can strengthen service offerings and support personalized healthcare.

Strengthening Laboratory Information Management Systems

Integrated LIMS platforms improve workflow efficiency, regulatory compliance, and secure management of diagnostic data.

Enhancement of AI-Driven Diagnostic Decision Support

Artificial intelligence can improve interpretation of laboratory data, optimize workflows, and support faster clinical decision-making.

Optimization of Laboratory Logistics and Sample Management

Efficient specimen transportation, automated sample tracking, and inventory optimization improve operational performance and service reliability.

Leveraging Integrated Healthcare Ecosystems

Seamless integration between laboratories, hospitals, physicians, and digital health platforms can improve care coordination and patient outcomes.

Global Clinical Laboratory Services Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the clinical laboratory services value chain is expected to become increasingly automated, digitally connected, and precision-driven. Continued advances in molecular diagnostics, artificial intelligence, digital pathology, laboratory automation, and cloud-based healthcare informatics will further transform laboratory operations worldwide.

Key Future Developments Include:

- Expansion of AI-assisted laboratory automation and intelligent diagnostic workflows.

- Increasing adoption of molecular diagnostics, genomics, and precision medicine testing.

- Greater implementation of cloud-based laboratory information management systems (LIMS).

- Broader deployment of digital pathology and remote diagnostic technologies.

- Growing integration of predictive analytics and clinical decision support platforms.

- Strengthening of global laboratory networks supporting preventive healthcare and personalized medicine.

As the market evolves, competitive advantage will increasingly depend on laboratory automation, diagnostic accuracy, digital integration, regulatory compliance, operational efficiency, and comprehensive testing capabilities.

Companies that successfully integrate advanced diagnostic technologies, AI-powered laboratory platforms, scalable testing infrastructure, and connected healthcare ecosystems will be well-positioned to achieve long-term growth in the Global Clinical Laboratory Services Market.

Investment Activity

Global Clinical Laboratory Services Market Investment & Funding Dynamics Overview (2026–2033)

The Global Clinical Laboratory Services Market is experiencing robust investment activity driven by increasing demand for advanced diagnostic testing, expanding molecular diagnostics, growing adoption of laboratory automation, and rising investments in precision medicine. Clinical laboratory service providers, diagnostic technology companies, healthcare organizations, private equity firms, venture capital investors, and strategic healthcare investors are actively investing in AI-enabled laboratory automation, molecular diagnostic capabilities, digital pathology platforms, laboratory information management systems (LIMS), and high-throughput diagnostic infrastructure.

Investment momentum is accelerating as healthcare providers seek to improve diagnostic accuracy, reduce turnaround times, enhance laboratory efficiency, and expand specialized testing capabilities. Capital allocation is increasingly focused on automated laboratory workflows, genomics platforms, biomarker testing, cloud-based laboratory management systems, robotic sample processing, and digital healthcare integration.

Additionally, growing investments in preventive healthcare programs, decentralized diagnostic networks, companion diagnostics, infectious disease surveillance, precision medicine initiatives, and laboratory network expansion are creating significant long-term opportunities across the global clinical laboratory services ecosystem.

Current Investment & Funding Landscape

The current investment environment reflects strong participation from global diagnostic service providers, healthcare systems, life sciences companies, institutional investors, venture capital firms, and strategic healthcare technology partners. Industry participants are investing heavily in laboratory modernization, molecular testing platforms, digital pathology technologies, laboratory automation systems, advanced analytics, and high-capacity diagnostic infrastructure.

Funding is increasingly directed toward AI-powered diagnostic workflows, next-generation sequencing (NGS), precision diagnostics, cloud-enabled laboratory operations, laboratory network expansion, and integrated digital healthcare platforms to improve operational performance and strengthen long-term market competitiveness.

Strategic collaborations among clinical laboratories, hospitals, diagnostic technology providers, biotechnology companies, research institutions, and healthcare IT vendors are accelerating innovation, expanding testing capabilities, and supporting the adoption of next-generation laboratory services worldwide.

Key Investment & Funding Dynamics Signals

- Growing demand for molecular diagnostics, genomic testing, and precision medicine is driving substantial investment in advanced laboratory technologies.

- Expansion of AI-enabled laboratory automation and digital pathology platforms is attracting increased funding for intelligent diagnostic workflows.

- Rising investment in robotic sample processing, laboratory information management systems (LIMS), and cloud-based laboratory infrastructure is improving operational efficiency and testing capacity.

- Increasing capital deployment toward biomarker testing, companion diagnostics, and high-throughput laboratory platforms is strengthening specialized diagnostic capabilities.

- Strategic funding for preventive healthcare programs, decentralized diagnostic services, and laboratory network expansion is supporting broader healthcare accessibility.

- Growing collaboration between clinical laboratories, hospitals, biotechnology companies, research institutions, and healthcare technology providers is accelerating diagnostic innovation.

- Expansion into emerging healthcare markets with increasing diagnostic demand and healthcare infrastructure investments is creating attractive long-term investment opportunities.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in laboratory automation, molecular diagnostics, and digital healthcare technologies will remain essential for sustaining long-term competitive advantage.

- Capital allocation toward AI-powered diagnostics, genomics platforms, predictive analytics, and integrated laboratory ecosystems will strengthen service quality and operational efficiency.

- Companies developing scalable laboratory networks, advanced testing portfolios, and interoperable digital platforms are expected to secure stronger long-term growth opportunities.

- Strategic partnerships among diagnostic laboratories, hospitals, biotechnology companies, healthcare IT providers, and research organizations will accelerate technology adoption and global market expansion.

- Investments in cybersecurity, laboratory quality management, workforce training, automation technologies, and digital interoperability will improve operational resilience and regulatory readiness.

- Compliance with clinical laboratory quality standards, healthcare accreditation requirements, diagnostic testing regulations, and healthcare data privacy frameworks will continue influencing investment priorities.

- Organizations building integrated capabilities across laboratory testing, molecular diagnostics, pathology, genomics, digital healthcare, and laboratory automation are expected to capture substantial long-term value.

Forward Outlook

Looking ahead, the Global Clinical Laboratory Services Market is expected to maintain strong investment momentum driven by expanding precision medicine initiatives, increasing laboratory digitalization, growing demand for preventive diagnostics, and continuous advancements in molecular testing technologies.

Future capital deployment will increasingly focus on AI-assisted diagnostics, molecular diagnostic platforms, laboratory robotics, digital pathology, cloud-based laboratory ecosystems, predictive analytics, and personalized diagnostic services.

As healthcare systems continue emphasizing early disease detection, personalized medicine, and operational efficiency, investment activity is expected to expand across clinical laboratory automation, genomics, companion diagnostics, laboratory informatics, decentralized testing, and integrated diagnostic networks.

In conclusion, the Global Clinical Laboratory Services Market represents a highly attractive healthcare investment landscape where artificial intelligence, molecular diagnostics, laboratory automation, precision medicine, digital pathology, and regulatory compliance will define future funding priorities, competitive differentiation, and long-term market expansion.

Technology & Innovation

Global Clinical Laboratory Services Market Technology & Innovation Landscape Overview

The Global Clinical Laboratory Services Market is experiencing rapid technological transformation as innovations in molecular diagnostics, artificial intelligence (AI), laboratory automation, digital pathology, next-generation sequencing (NGS), and bioinformatics reshape modern diagnostic services. Clinical laboratories, hospitals, diagnostic service providers, and healthcare organizations are investing significantly in advanced technologies to improve diagnostic accuracy, accelerate turnaround times, enhance workflow efficiency, and support precision medicine initiatives. These innovations are enabling laboratories to deliver faster, more reliable, and highly personalized diagnostic solutions across a broad range of clinical applications.

The market is also benefiting from advancements in automated laboratory instruments, robotic sample processing, cloud-based laboratory information management systems (LIMS), high-throughput testing platforms, and digital data analytics. These technologies are improving operational productivity, reducing manual errors, optimizing laboratory workflows, and strengthening quality assurance. As demand for early disease detection, preventive healthcare, and personalized medicine continues to increase, technology has become a critical driver of laboratory modernization and long-term market expansion.

Global Clinical Laboratory Services Market Technology & Innovation Current Scenario

Current innovation within the clinical laboratory services market is primarily focused on AI-assisted diagnostics, molecular diagnostic technologies, laboratory automation, digital pathology platforms, and precision medicine testing. Clinical laboratories are increasingly utilizing PCR technologies, next-generation sequencing (NGS), genomic testing, biomarker analysis, and AI-powered image analysis to improve disease detection and clinical decision-making. Artificial intelligence is also enhancing workflow optimization, quality control, predictive diagnostics, and laboratory resource management.

Automation technologies, robotic laboratory systems, integrated laboratory information management systems (LIMS), and cloud-based diagnostic platforms are improving testing efficiency while reducing turnaround times and operational costs. In addition, advances in multiplex testing, point-of-care diagnostics, digital pathology imaging, and advanced bioinformatics are expanding laboratory capabilities across oncology, infectious diseases, genetic disorders, and chronic disease management. These innovations are strengthening the ability of clinical laboratories to deliver high-quality, scalable, and patient-centric diagnostic services.

Key Technology & Innovation Trends in Global Clinical Laboratory Services Market

- AI-Enabled Laboratory Automation: Improving workflow efficiency through intelligent sample processing, automated quality control, and predictive laboratory management.

- Molecular Diagnostic Technologies: Expanding the use of PCR, RT-PCR, and advanced molecular assays for rapid and highly accurate disease detection.

- Next-Generation Sequencing (NGS): Accelerating genomic analysis, precision medicine, inherited disease testing, and oncology diagnostics.

- Digital Pathology Platforms: Enhancing pathology workflows through whole-slide imaging, remote diagnostics, and AI-assisted image interpretation.

- Cloud-Based Laboratory Information Management Systems (LIMS): Supporting secure data management, laboratory integration, and real-time workflow optimization.

- High-Throughput Automated Testing Systems: Increasing laboratory capacity and reducing turnaround times through advanced robotic processing technologies.

- Advanced Bioinformatics Solutions: Enabling efficient interpretation of complex genomic, molecular, and clinical laboratory datasets.

- Multiplex Diagnostic Assays: Supporting simultaneous detection of multiple biomarkers and pathogens to improve diagnostic efficiency.

- Point-of-Care Testing Integration: Expanding rapid diagnostic capabilities through decentralized testing solutions connected with centralized laboratory systems.

- Predictive Analytics & Clinical Decision Support: Leveraging AI and advanced analytics to improve diagnostic accuracy, disease prediction, and personalized patient management.

Strategic Implications of Technology & Innovation

Technological advancements are enabling clinical laboratories and diagnostic service providers to improve testing accuracy, increase operational efficiency, and strengthen competitive positioning. Organizations investing in artificial intelligence, laboratory automation, molecular diagnostics, and digital pathology technologies are enhancing service quality while reducing operational costs and improving patient outcomes. Innovation is supporting faster diagnostics, higher laboratory productivity, improved clinical decision-making, and expanded precision medicine capabilities.

As healthcare systems increasingly prioritize preventive care, personalized medicine, and value-based healthcare, organizations are focusing on integrated diagnostic ecosystems that combine intelligent automation, digital pathology, genomics, cloud computing, and advanced analytics. Companies successfully adopting next-generation laboratory technologies are expected to gain significant competitive advantages. However, laboratory accreditation requirements, diagnostic quality standards, regulatory compliance, cybersecurity, and patient data privacy remain critical considerations influencing technology adoption and commercialization.

Global Clinical Laboratory Services Market Technology & Innovation Forward Outlook

The future of the Global Clinical Laboratory Services Market is expected to be shaped by continued advancements in artificial intelligence, digital pathology, molecular diagnostics, next-generation sequencing, laboratory robotics, and computational biology. Emerging innovations such as AI-assisted disease prediction, integrated multi-omics diagnostics, digital twin technologies, automated molecular laboratories, and cloud-native diagnostic ecosystems are expected to redefine clinical laboratory services. Organizations are likely to increase investments in intelligent diagnostic platforms that improve scalability, testing efficiency, and personalized healthcare delivery.

As demand for precision medicine, preventive healthcare, companion diagnostics, and rapid infectious disease detection continues to grow, technology will play an increasingly important role in driving market development. The integration of artificial intelligence, laboratory automation, molecular science, bioinformatics, and digital healthcare technologies is expected to create substantial growth opportunities while strengthening the long-term evolution of the global clinical laboratory services market.

Market Risk

Global Clinical Laboratory Services Market Risk Factors & Disruption Threats Overview

The Global Clinical Laboratory Services Market operates within the broader healthcare diagnostics, clinical pathology, molecular diagnostics, precision medicine, and laboratory information management ecosystem. While the market benefits from rising demand for diagnostic testing, expanding preventive healthcare programs, and increasing adoption of molecular diagnostics, it also faces several risks related to reimbursement pressures, regulatory compliance, workforce shortages, cybersecurity threats, and rapid technological transformation.

One of the primary structural risks is the growing complexity of healthcare reimbursement policies and cost-containment initiatives. Clinical laboratories are increasingly required to deliver high-quality diagnostic services while operating under declining reimbursement rates and stricter healthcare budget controls, placing pressure on operational profitability and investment capacity.

The market is also highly regulated through laboratory quality standards, healthcare accreditation requirements, diagnostic testing regulations, and patient safety frameworks. Maintaining compliance with evolving regulatory standards requires continuous investments in quality management systems, laboratory validation, personnel training, and documentation.

Another major disruption factor involves shortages of skilled laboratory professionals, pathologists, molecular biologists, and clinical technologists. Increasing testing volumes combined with workforce constraints may affect laboratory turnaround times, testing capacity, and overall service quality.

Additionally, laboratories are increasingly exposed to cybersecurity risks as digital pathology systems, laboratory information management systems (LIMS), cloud-based data platforms, and connected diagnostic equipment process large volumes of sensitive patient information. Cyberattacks or system failures may disrupt laboratory operations while creating regulatory and financial consequences.

Global Clinical Laboratory Services Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by expanding molecular diagnostic testing, growing adoption of AI-enabled laboratory automation, increasing use of digital pathology, and rising demand for precision medicine. Healthcare providers continue investing in advanced laboratory technologies to improve diagnostic accuracy, workflow efficiency, and patient outcomes.

However, the industry remains exposed to reimbursement changes, rising operational costs, shortages of qualified laboratory personnel, supply chain disruptions affecting diagnostic reagents and laboratory consumables, and increasing cybersecurity risks associated with healthcare digitalization. These challenges continue to influence laboratory investment priorities and service delivery models.

Clinical laboratories are increasingly implementing automation technologies, robotic sample handling, artificial intelligence, and cloud-based laboratory information systems to improve productivity, reduce manual errors, and shorten testing turnaround times.

Regulatory authorities continue strengthening oversight regarding laboratory accreditation, diagnostic quality standards, patient data privacy, quality assurance, and clinical testing accuracy, requiring laboratories to maintain robust compliance and quality control frameworks.

At the same time, competitive intensity continues to increase as independent laboratory networks, hospital laboratories, specialized molecular diagnostic providers, and digital health companies expand service portfolios through technological innovation, acquisitions, and strategic collaborations.

Key Risk Factors & Disruption Threat Signals in Global Clinical Laboratory Services Market

A major disruption signal is the accelerating adoption of artificial intelligence, machine learning, and laboratory automation technologies that enable intelligent sample processing, AI-assisted diagnostics, workflow optimization, and predictive laboratory management. Organizations that delay digital transformation may experience declining operational competitiveness.

Another important signal is the rapid expansion of molecular diagnostics, genomic sequencing, biomarker analysis, and personalized medicine, significantly increasing demand for advanced laboratory capabilities and specialized testing services.

The growing convergence of digital pathology, cloud computing, laboratory information management systems, and advanced analytics is transforming laboratory operations into highly connected and data-driven diagnostic ecosystems.

Advancements in high-throughput testing platforms, next-generation sequencing, multiplex molecular diagnostics, and automated specimen processing are continuously improving testing capacity, diagnostic precision, and laboratory efficiency.

Growing emphasis on preventive healthcare, population health management, infectious disease surveillance, and companion diagnostics is encouraging healthcare systems to expand laboratory testing infrastructure and specialized diagnostic services.

The expansion of decentralized testing models, integrated diagnostic networks, telemedicine-supported laboratory services, and strategic partnerships between hospitals and reference laboratories is reshaping business models across the global diagnostics industry.

Strategic Implications of Risk Factors & Disruption Threats in Global Clinical Laboratory Services Market

Clinical laboratory organizations should prioritize investments in artificial intelligence, laboratory automation, molecular diagnostics, digital pathology, and advanced laboratory information management systems to improve testing efficiency, diagnostic quality, and operational scalability.

Companies should strengthen cybersecurity through zero-trust architectures, encryption technologies, continuous network monitoring, secure cloud infrastructure, and comprehensive disaster recovery strategies to safeguard sensitive patient and laboratory data.

Organizations should enhance workforce resilience by investing in laboratory staff training, automation-assisted workflows, digital competency development, and talent retention strategies to address ongoing shortages of qualified professionals.

Investment in diversified supply chains, strategic reagent sourcing, inventory optimization, and long-term supplier partnerships can reduce operational risks associated with shortages of laboratory consumables and diagnostic materials.

Strategic collaborations among hospitals, diagnostic laboratories, biotechnology companies, academic institutions, and healthcare technology providers can accelerate innovation, expand specialized testing capabilities, and strengthen precision medicine initiatives.

Organizations should continuously monitor evolving regulations related to laboratory accreditation, healthcare quality standards, diagnostic testing regulations, patient data privacy, and clinical governance to ensure long-term regulatory compliance and operational resilience.

Global Clinical Laboratory Services Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026–2033, the Global Clinical Laboratory Services Market is expected to maintain steady growth as precision medicine, molecular diagnostics, preventive healthcare, and personalized treatment strategies continue expanding worldwide. However, future market growth will increasingly depend on laboratory automation, workforce modernization, cybersecurity resilience, regulatory adaptability, and digital transformation.

Artificial intelligence, digital pathology, cloud-native laboratory platforms, robotic automation, and predictive analytics are expected to become primary competitive differentiators, enabling laboratories to improve diagnostic accuracy, accelerate turnaround times, and optimize operational performance.

Healthcare regulators are likely to strengthen oversight regarding laboratory quality, diagnostic validation, patient safety, data privacy, and accreditation standards as advanced diagnostic technologies become increasingly integrated into routine clinical practice. Laboratories will need to expand compliance capabilities while maintaining high-quality testing standards.

Growing adoption of genomic testing, companion diagnostics, infectious disease monitoring, preventive screening programs, and personalized medicine will continue increasing demand for advanced laboratory services capable of supporting increasingly complex diagnostic requirements.

Technological convergence across artificial intelligence, molecular biology, laboratory robotics, digital health platforms, cloud computing, and precision diagnostics will continue reshaping laboratory services while creating new opportunities for innovation, operational efficiency, and patient-centered healthcare.

Overall, the market will remain strongly growth-oriented but increasingly influenced by automation, molecular diagnostics, cybersecurity, workforce development, and regulatory evolution. Long-term market leaders will be defined by their ability to deliver accurate, scalable, secure, and technologically advanced clinical laboratory services that support the future of global diagnostic healthcare.

Regulatory Landscape

Global Clinical Laboratory Services Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Clinical Laboratory Services Market is becoming increasingly stringent as healthcare systems place greater emphasis on diagnostic accuracy, patient safety, laboratory quality, and standardized clinical testing. Regulatory agencies, healthcare authorities, accreditation organizations, and laboratory quality bodies establish comprehensive frameworks governing laboratory operations, diagnostic testing procedures, quality assurance, personnel competency, data management, and post-analytical reporting.

Clinical laboratories, hospital laboratories, independent diagnostic centers, and reference laboratories must comply with extensive regulations covering Good Laboratory Practice (GLP), clinical laboratory quality management systems, accreditation requirements, diagnostic testing standards, biosafety protocols, specimen handling, and patient data protection. Regulatory compliance is essential to ensure reliable diagnostic results, maintain patient confidence, and support effective clinical decision-making across healthcare systems.

As precision medicine, molecular diagnostics, digital pathology, and AI-enabled laboratory automation continue expanding, policymakers are strengthening quality standards while promoting innovation, interoperability, cybersecurity, and equitable access to advanced diagnostic services.

Global Clinical Laboratory Services Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape primarily focuses on laboratory quality assurance, accreditation compliance, diagnostic testing accuracy, biosafety, patient safety, and standardized laboratory procedures. Clinical laboratories are required to demonstrate operational excellence through validated testing methods, quality control programs, and continuous performance monitoring.

Clinical laboratory quality standards establish requirements for test validation, quality assurance, instrument calibration, internal quality control, external proficiency testing, and standardized reporting to ensure consistent diagnostic performance.

Healthcare accreditation requirements govern laboratory infrastructure, personnel qualifications, competency assessments, documentation practices, and operational management to maintain internationally recognized quality benchmarks.

Diagnostic testing regulations oversee specimen collection, transportation, analytical validation, laboratory-developed tests (LDTs), molecular diagnostics, pathology services, and reporting accuracy to support safe and effective patient care.

Healthcare authorities continue strengthening biosafety standards, laboratory information management systems (LIMS), electronic health record (EHR) integration, patient privacy protections, and post-market oversight for in vitro diagnostic technologies and laboratory operations.

Key Regulatory & Policy Environment Signals in Global Clinical Laboratory Services Market

- Clinical Laboratory Quality Standards:

Requirements governing quality assurance, analytical validation, instrument calibration, proficiency testing, standardized operating procedures, and continuous quality improvement. - Healthcare Accreditation Requirements:

Frameworks supporting laboratory accreditation, personnel competency, infrastructure compliance, documentation practices, and quality management systems. - Diagnostic Testing Regulations:

Policies governing molecular diagnostics, pathology services, genetic testing, laboratory-developed tests, specimen management, and diagnostic result accuracy. - Biosafety & Specimen Handling Standards:

Guidelines addressing laboratory biosafety, infection prevention, biological specimen collection, transportation, storage, waste management, and occupational safety. - Patient Data Privacy & Digital Health Regulations:

Requirements supporting secure laboratory information management systems, electronic health records, cybersecurity, patient confidentiality, and digital data governance. - Post-Market Surveillance & Quality Monitoring:

Regulations promoting ongoing laboratory audits, quality assessments, adverse event reporting for diagnostic devices, performance monitoring, and continuous regulatory oversight.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging clinical laboratories, diagnostic service providers, hospitals, and healthcare organizations to strengthen quality management systems, laboratory accreditation programs, workforce training, regulatory compliance capabilities, and digital infrastructure. Regulatory excellence is becoming a key competitive advantage across the diagnostic healthcare industry.

Increasing laboratory quality standards are driving investments in laboratory automation, AI-assisted diagnostics, molecular testing platforms, digital pathology systems, and advanced quality control technologies that improve diagnostic accuracy and operational efficiency.

Healthcare accreditation and diagnostic testing regulations are encouraging laboratories to standardize workflows, enhance staff competency, improve analytical validation procedures, and strengthen laboratory governance across clinical operations.

Growing emphasis on patient data security and digital health compliance is accelerating adoption of secure laboratory information management systems, cloud-enabled diagnostics, cybersecurity frameworks, and interoperable healthcare information systems.

As precision medicine and personalized diagnostics continue expanding, organizations capable of maintaining regulatory compliance, laboratory accreditation, high-quality testing, and digital transformation will be well positioned to strengthen their market leadership and improve patient outcomes.

Global Clinical Laboratory Services Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Clinical Laboratory Services Market is expected to become increasingly comprehensive as precision medicine, molecular diagnostics, AI-enabled laboratory technologies, and digital healthcare ecosystems continue advancing globally.

Healthcare authorities are expected to strengthen laboratory quality standards, analytical validation requirements, proficiency testing programs, biosafety regulations, and quality management systems to support increasingly complex diagnostic services.

Regulatory agencies are likely to place greater emphasis on oversight of molecular diagnostics, genetic testing, laboratory-developed tests, digital pathology platforms, artificial intelligence applications, and automated laboratory workflows to ensure clinical reliability and patient safety.

Policymakers are also expected to encourage greater international harmonization of laboratory standards, secure digital health integration, interoperability, electronic reporting, and enhanced cybersecurity to support efficient and connected diagnostic healthcare systems.

Overall, the future regulatory landscape will be shaped by the convergence of clinical laboratory quality standards, healthcare accreditation requirements, diagnostic testing regulations, biosafety protocols, patient data protection frameworks, digital health governance, and quality management systems. Organizations capable of delivering accurate, compliant, technologically advanced, and patient-centric laboratory services will be best positioned to capitalize on long-term growth opportunities within the global diagnostic healthcare industry.