Global kidney disease market Size and Share Analysis 2026-2033

Global kidney disease market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 23.5 Billion |

| Market Size (2033) | USD 45.8 Billion |

| CAGR (2026???2033) | 8.7% |

| Largest Segment | Hemodialysis Services and Equipment |

| Fastest Growing Segment | Home Dialysis and Remote Monitoring Solutions |

| Leading End-Use Segment | Dialysis Centers |

| Key Trend | Shift Toward Home-Based Renal Care and Digital Nephrology Platforms |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Primary Growth Driver | Rising Global Prevalence of Diabetes, Hypertension, and Chronic Kidney Disease |

Global Kidney Disease Market Size & Forecast

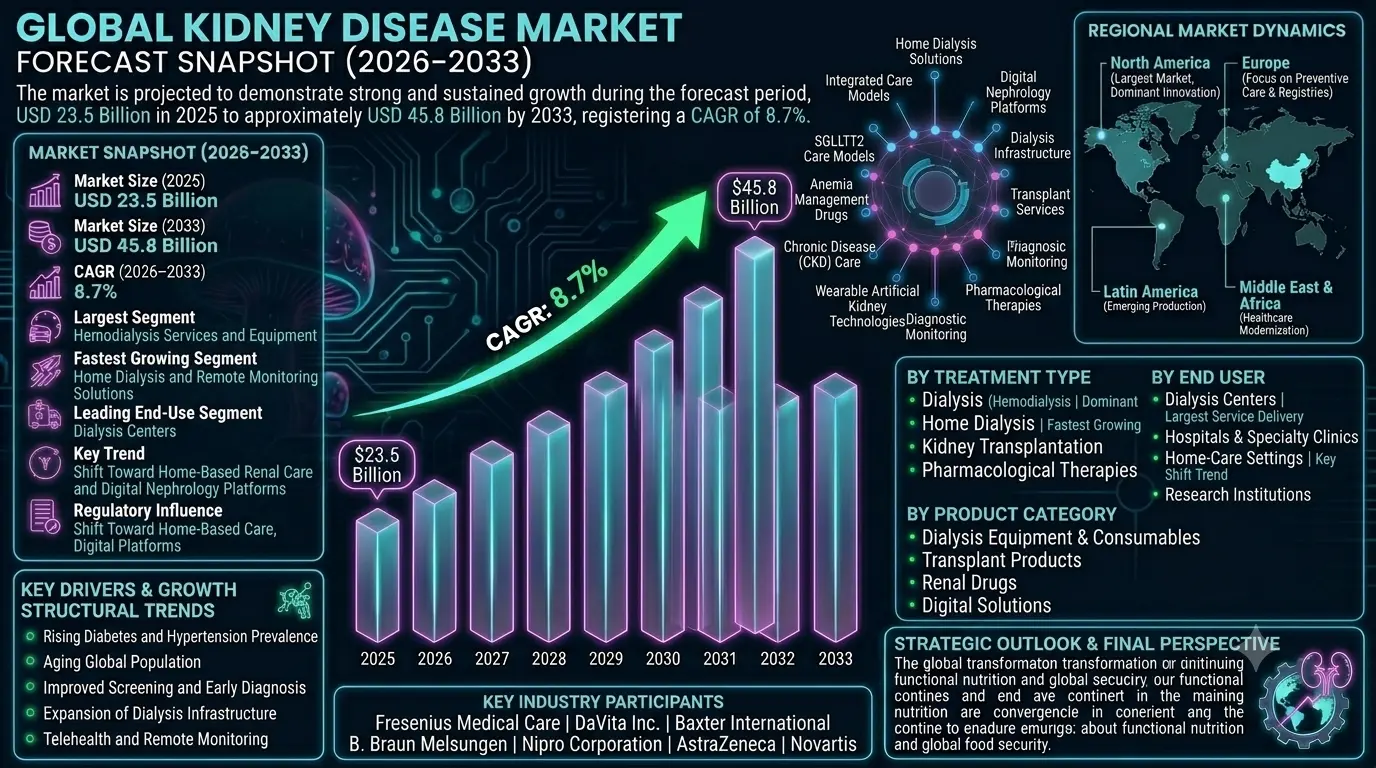

The global kidney disease market is projected to demonstrate strong and sustained growth during the forecast period from 2026 to 2033. Valued at approximately USD 23.5 billion in 2025, the market is expected to reach nearly USD 45.8 billion by 2033, expanding at a CAGR of around 8.7%. This growth reflects the increasing global burden of chronic kidney disease (CKD) and end-stage renal disease (ESRD), alongside expanding access to diagnosis and long-term renal care. The market covers a broad continuum of care, including early diagnostic testing, nephrology consultations, dialysis services, kidney transplantation, pharmacological treatments, home-care management, and digital monitoring solutions. Rising prevalence of diabetes and hypertension, which are the primary risk factors for kidney failure, continues to be the central driver of market expansion globally. In addition, aging populations, improved disease awareness, and wider implementation of routine screening programs are enabling earlier diagnosis of kidney disorders. This is significantly increasing the treated patient pool and driving demand for both in-center and home-based dialysis solutions. Technological advancements in portable dialysis systems, wearable devices, and telemedicine-based nephrology care are further improving treatment accessibility and patient outcomes. According to Pheonix Demand Forecast Engine, the global kidney disease market size is estimated at USD 23.5 billion in 2025 and is projected to reach USD 45.8 billion by 2033, growing at a CAGR of approximately 8.7% during the forecast period (2026???2033).

Global Kidney Disease Market Overview

The kidney disease market encompasses a comprehensive healthcare ecosystem designed to manage acute kidney injury (AKI), chronic kidney disease (CKD), and end-stage renal disease (ESRD). It includes diagnostic services, dialysis treatment infrastructure, transplant services, drug therapies, and digital health platforms that support long-term patient management. The market is highly structured around long-term care needs, as kidney diseases typically require continuous treatment and monitoring. Dialysis remains the dominant treatment modality, while kidney transplantation is the preferred long-term solution but constrained by donor availability. Pharmacological advancements and regenerative medicine research are also gaining momentum in slowing disease progression. Key industry participants include Fresenius Medical Care, DaVita Inc., Baxter International, B. Braun Melsungen, Nipro Corporation, and Nikkiso Co., along with pharmaceutical companies such as AstraZeneca and Novartis, which are actively involved in nephrology drug development. The market is characterized by a mix of large integrated dialysis providers and specialized medical device manufacturers. Regulatory frameworks and reimbursement systems play a critical role in shaping market access and treatment affordability. Government-funded healthcare programs, especially in developed regions, significantly support dialysis and transplant services, while emerging economies are investing in expanding renal care infrastructure.Key Drivers of Global Kidney Disease Market Growth

Rising Diabetes and Hypertension Prevalence

Diabetes and hypertension are the leading causes of CKD worldwide. The continuous rise in these chronic conditions significantly increases the number of patients progressing to renal failure, thereby driving long-term demand for dialysis and kidney care services.Aging Global Population

Older populations are more susceptible to kidney dysfunction due to reduced renal function and higher prevalence of comorbidities. This demographic shift is expanding the global CKD patient base, particularly in developed regions.Improved Screening and Early Diagnosis

Wider adoption of eGFR testing, urine albumin screening, and routine health checkups is enabling earlier detection of kidney disease. This is increasing the number of diagnosed patients entering treatment pathways earlier in disease progression.Expansion of Dialysis Infrastructure

Investments in dialysis centers, home dialysis programs, and mobile treatment units are improving access to care. Expansion in both public and private healthcare systems is a major growth enabler for the market.Advancements in Pharmacological Therapies

New drug classes such as SGLT2 inhibitors, anemia management drugs, and anti-fibrotic agents are improving disease management and slowing progression, contributing to longer treatment cycles and expanded therapeutic adoption.Telehealth and Remote Monitoring

Remote patient monitoring and tele-nephrology platforms are enhancing chronic disease management. These solutions reduce hospital visits, improve patient compliance, and support the growth of home-based care models.Global Kidney Disease Market Segmentation

By Disease Type

Chronic Kidney Disease (CKD), Acute Kidney Injury (AKI), Diabetic Nephropathy, Hypertensive Nephropathy, Polycystic Kidney Disease (PKD), and Glomerular Diseases represent the primary disease categories. CKD and ESRD account for the largest share due to long-term treatment requirements.By Treatment Type

The market includes dialysis (hemodialysis and peritoneal dialysis), kidney transplantation, pharmacological therapies, and emerging regenerative treatments. Hemodialysis remains the dominant segment, while home dialysis is the fastest-growing category.By Diagnosis & Monitoring

Diagnostic methods include imaging (ultrasound, CT, MRI), laboratory tests (serum creatinine, eGFR, urinalysis), biomarker testing, and remote monitoring systems. Digital monitoring is gaining importance in chronic care management.By End User

Hospitals, dialysis centers, specialty renal clinics, home-care settings, and research institutions form the key end-user segments. Dialysis centers represent the largest service delivery channel globally.By Product Category

Dialysis equipment, transplant-related products, CKD and AKI drugs, and digital renal care solutions form the major product categories. Consumables such as dialyzers and bloodlines generate recurring revenue streams.By Geography

The market spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, each with distinct healthcare infrastructure maturity and disease burden patterns.Regional Market Dynamics

North America remains the largest market due to high CKD awareness, advanced dialysis infrastructure, strong reimbursement systems, and widespread access to transplantation services. Asia-Pacific is the fastest-growing region, driven by rising diabetes prevalence, increasing healthcare investments, and expanding dialysis capacity in countries such as China, India, and Japan. Europe focuses on preventive care, structured CKD registries, and growing adoption of home dialysis solutions supported by public healthcare systems. Latin America is expanding its dialysis infrastructure, with Brazil and Mexico leading regional adoption through public-private healthcare investments. Middle East & Africa is witnessing gradual growth supported by healthcare modernization, specialist renal center development, and rising medical tourism activity.Competitive Landscape

The global kidney disease market is highly consolidated in dialysis services and moderately competitive in pharmaceuticals and medical devices. Key players include Fresenius Medical Care, DaVita Inc., Baxter International, B. Braun Melsungen, Nipro Corporation, and Nikkiso Co., alongside pharmaceutical innovators such as AstraZeneca and Novartis. Fresenius Medical Care holds the leading position globally due to its extensive dialysis clinic network, vertically integrated supply chain, and strong presence in consumables and services. DaVita Inc. follows as a major service provider with a strong focus on outpatient dialysis care. Companies are increasingly focusing on home dialysis solutions, digital health integration, and next-generation renal therapies to differentiate offerings. Strategic partnerships between device manufacturers and pharmaceutical firms are also expanding integrated care models. High capital requirements, strict regulatory frameworks, and complex reimbursement systems create significant barriers to entry, reinforcing the dominance of established global players.Strategic Outlook

The strategic direction of the kidney disease market is centered on expanding access to care, improving treatment efficiency, and reducing long-term healthcare costs. Home dialysis, remote monitoring, and AI-driven patient management systems are expected to play a major role in future care delivery models. Pharmacological innovation, particularly in kidney-protective therapies, is expected to slow disease progression and reduce dependency on dialysis over the long term. However, the growing patient pool will continue to sustain strong demand for dialysis infrastructure and consumables. Emerging opportunities lie in regenerative medicine, wearable artificial kidney technologies, and integrated digital nephrology platforms. Companies that combine device innovation, pharmaceutical development, and digital healthcare ecosystems will gain a competitive advantage.Final Market Perspective

The global kidney disease market is a structurally resilient and high-growth healthcare segment driven by rising chronic disease prevalence and expanding healthcare access. While dialysis remains the core revenue driver, the future of the market will increasingly shift toward home-based care, preventive therapies, and digital health integration. Long-term transformation will be shaped by advances in regenerative medicine and disease-modifying therapies that may reduce dependence on dialysis. However, due to persistent risk factors such as diabetes, hypertension, and aging populations, the market will continue to experience strong and sustained demand globally.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Kidney Disease Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Kidney Disease Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Care Pathway & Treatment Ecosystem (Diagnosis???Dialysis???Transplant???Home Care)

- 2.5 Impact of Epidemiology Trends (Diabetes, Hypertension & Aging Population)

- 2.6 Regulatory & Reimbursement Landscape

- 2.7 Technology & Innovation Landscape (Dialysis Tech, Telehealth, Regenerative Medicine)

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Prevalence of Diabetes & Hypertension

- 4.1.2 Aging Global Population

- 4.1.3 Improved CKD Screening & Early Diagnosis

- 4.1.4 Expansion of Dialysis Infrastructure & Home Dialysis

- 4.1.5 Advancements in Nephrology Pharmacotherapy

- 4.1.6 Telehealth & Remote Patient Monitoring Adoption

- 4.1.7 Government & Reimbursement Support Programs

- 4.2 Restraints

- 4.2.1 High Cost of Dialysis & Transplant Care

- 4.2.2 Limited Access in Low-Income Regions

- 4.2.3 Organ Donor Shortage

- 4.2.4 Infrastructure Gaps in Emerging Economies

- 4.3 Opportunities

- 4.3.1 Growth of Home Dialysis & Portable Devices

- 4.3.2 Expansion of Nephroprotective Drug Pipeline

- 4.3.3 AI-Based Kidney Disease Monitoring

- 4.3.4 Regenerative & Bioartificial Kidney Technologies

- 4.4 Challenges

- 4.4.1 High Capital Requirements for Dialysis Infrastructure

- 4.4.2 Clinical Complexity of CKD Progression Management

- 4.4.3 Supply Chain Constraints for Dialysis Consumables

- 4.4.4 Regulatory Approval Complexity for Novel Therapies

- 4.1 Drivers

- 5. Kidney Disease Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Treatment Modality Analysis

- 5.6 Healthcare System Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Disease Type

- 6.1.1 Chronic Kidney Disease (CKD)

- 6.1.2 Acute Kidney Injury (AKI)

- 6.1.3 Diabetic Nephropathy

- 6.1.4 Hypertensive Nephropathy

- 6.1.5 Polycystic Kidney Disease (PKD)

- 6.1.6 Glomerular Diseases

- 6.2 By Treatment Type

- 6.2.1 Dialysis

- 6.2.1.1 Hemodialysis

- 6.2.1.2 Peritoneal Dialysis

- 6.2.2 Kidney Transplantation

- 6.2.3 Pharmacological Treatment

- 6.2.4 Regenerative & Emerging Therapies

- 6.2.1 Dialysis

- 6.3 By Diagnosis & Monitoring

- 6.3.1 Imaging

- 6.3.2 Laboratory Tests

- 6.3.3 Biomarker Tests

- 6.3.4 Remote Monitoring Systems

- 6.4 By End User

- 6.4.1 Hospitals

- 6.4.2 Dialysis Centers

- 6.4.3 Specialty Renal Clinics

- 6.4.4 Home-Care Settings

- 6.4.5 Research & Academic Institutes

- 6.5 By Product Category

- 6.5.1 Dialysis Equipment & Consumables

- 6.5.2 Transplant-related Products

- 6.5.3 CKD & AKI Drugs

- 6.5.4 Digital & Connected Solutions

- 6.1 By Disease Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Service & Care Delivery Positioning

- 8.4 Supply Chain & Healthcare Partnerships

- 8.5 Competitive Intensity & Market Consolidation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Renal Infrastructure Mapping System

- 10.3 Telehealth & RPM Adoption Analyzer

- 10.4 Clinical Trial & Pipeline Tracker

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Home Dialysis Ecosystem

- 11.2 Growth of Nephroprotective Drug Adoption

- 11.3 Digital Kidney Care Transformation

- 11.4 Regenerative & Bioartificial Kidney Development

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Kidney Disease Market Competitive Intensity & Market Structure Overview

The Global Kidney Disease Market is characterized by a highly consolidated yet service-intensive competitive structure, dominated by large dialysis service providers, global medical device manufacturers, and a growing set of pharmaceutical and digital health companies. The market operates within a long-term chronic care framework, where recurring treatment demand, reimbursement systems, and infrastructure scale define competitive advantage.

Competitive intensity is high due to the essential and non-discretionary nature of renal care, particularly dialysis and end-stage renal disease (ESRD) management. Leading players compete on scale of dialysis networks, cost efficiency, consumable supply chains, treatment outcomes, and integration of digital monitoring and home-care solutions.

The market structure is moderately consolidated in dialysis services, where a few global players control a significant share of treatment capacity, while pharmaceuticals, diagnostics, and medical device segments remain more fragmented with strong multinational participation and regional suppliers.

Global Kidney Disease Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Fresenius Medical Care: Global Market Leader. Dominates dialysis services, consumables, and renal care infrastructure with extensive global clinic networks.

DaVita Inc.: Leading Dialysis Service Provider. Strong presence in the U.S. with expanding international renal care operations and outpatient dialysis centers.

Baxter International: Major Renal Care Device Company. Strong portfolio in peritoneal dialysis systems, hemodialysis equipment, and renal therapy solutions.

B. Braun Melsungen AG: Integrated Medical Technology Provider. Active in dialysis machines, consumables, and hospital-based renal care systems.

Nipro Corporation: Renal Device Manufacturer. Strong global footprint in dialysis machines, dialyzers, and blood management systems.

Nikkiso Co., Ltd.: Dialysis Equipment Specialist. Focused on advanced hemodialysis systems and water treatment technologies for renal care.

Toray Medical Co., Ltd.: Membrane Technology Leader. Known for high-performance dialysis membranes and filtration technologies.

AstraZeneca: Pharmaceutical Leader. Key player in nephroprotective therapies, particularly SGLT2 inhibitors for CKD management.

Otsuka Pharmaceutical: Renal Pharma Contributor. Focused on electrolyte balance, CKD management, and supportive renal therapies.

Amgen / Johnson & Johnson: Biologics and supportive therapies providers, historically strong in anemia management and renal-related biologics.

Novo Nordisk / Novartis: Expanding presence in CKD-related metabolic and cardiometabolic therapies through pipeline and partnerships.

Key Competitive Intensity & Market Structure Signals in Global Kidney Disease Market

A key competitive signal in the market is the dominance of integrated renal care ecosystems, where leading providers control dialysis clinics, consumables supply, and patient management services. Scale, vertical integration, and reimbursement negotiation power are critical competitive levers.

Another major structural factor is the growing shift toward home dialysis and remote patient monitoring. This is reshaping competition by enabling device manufacturers and digital health companies to enter traditional service-heavy segments, increasing cross-industry convergence.

Pharmaceutical innovation is increasingly influencing competitive dynamics, particularly with the expansion of SGLT2 inhibitors and emerging nephroprotective drugs that delay disease progression and potentially reduce dialysis dependency.

Supply chain control over dialysis consumables such as dialyzers, bloodlines, and catheters remains a major competitive advantage, as these products generate recurring revenue and lock-in effects for service providers.

Regulatory frameworks and reimbursement systems significantly shape competition, particularly in North America and Europe, where pricing negotiations, insurance coverage, and public health funding determine market accessibility and profitability.

Strategic Implications of Competitive Intensity & Market Structure in Global Kidney Disease Market

Market leaders are increasingly focusing on integrated renal care models combining dialysis services, pharmaceuticals, diagnostics, and digital health platforms to improve patient outcomes and strengthen long-term retention.

Expansion into home dialysis and decentralized care models is becoming a key strategic priority, driven by cost efficiency, patient convenience, and healthcare system pressure to reduce hospital-based treatments.

Digital transformation, including tele-nephrology, remote monitoring, and AI-assisted disease management, is emerging as a key differentiator in improving clinical outcomes and reducing operational costs.

Pharmaceutical-device partnerships are becoming more common, particularly in CKD management, where drug therapies and dialysis technologies are increasingly integrated to slow disease progression and improve patient quality of life.

In emerging markets, competitive strategies are focused on infrastructure expansion, affordability-driven service models, and government partnerships to increase dialysis accessibility and transplant capacity.

Global Kidney Disease Market Competitive Intensity & Market Structure Forward Outlook

The Global Kidney Disease Market is expected to remain highly structured and service-driven, with continued dominance of large dialysis providers and increasing influence of pharmaceutical innovation and digital health ecosystems.

Market consolidation is expected to continue in dialysis services as scale advantages, reimbursement negotiations, and infrastructure ownership become increasingly critical to profitability and expansion.

Home-based care models and wearable or portable dialysis systems are expected to gradually disrupt traditional center-based care structures, enabling new entrants and technology-focused companies to gain share.

Pharmaceutical breakthroughs in kidney disease progression delay and regenerative therapies may reshape long-term demand dynamics, potentially reducing dependency on traditional dialysis in select patient groups.

Overall, companies that successfully integrate service delivery, consumable supply chains, pharmaceutical innovation, and digital care platforms will define leadership in the evolving Global Kidney Disease Market through 2033.

Value Chain

Global Kidney Disease Market Value Chain & Supply Chain Evolution Overview

The Global Kidney Disease Market value chain spans a highly integrated healthcare ecosystem that includes early diagnosis, clinical management, renal replacement therapies, pharmaceutical interventions, medical devices, home-care solutions, and long-term care coordination services. It represents a critical chronic disease management infrastructure designed to support patients with chronic kidney disease (CKD), acute kidney injury (AKI), and end-stage renal disease (ESRD).

The ecosystem is primarily driven by rising diabetes and hypertension prevalence, aging populations, improved screening programs, and expanding access to renal care services. The value chain is evolving from hospital-centric treatment toward decentralized, patient-centric, and digitally enabled renal care models.

Key industry participants include Fresenius Medical Care, Baxter International, DaVita Inc., B. Braun Melsungen AG, Nipro Corporation, Nikkiso Co., Ltd., and Otsuka, alongside pharmaceutical leaders such as AstraZeneca and Novo Nordisk. These companies operate across dialysis services, medical devices, drug therapies, and renal care infrastructure development.

The upstream supply chain includes dialysis machine manufacturers, dialyzer and consumable producers, pharmaceutical API suppliers, diagnostic reagent providers, and medical device component manufacturers. Midstream operations involve hospitals, dialysis centers, specialty renal clinics, and transplant centers. Downstream includes home-care services, tele-nephrology platforms, and remote patient monitoring ecosystems.

Digital health technologies, AI-driven diagnostics, connected dialysis machines, and remote monitoring platforms are increasingly integrated across the value chain, enabling real-time patient tracking, predictive risk assessment, and improved treatment outcomes.

Key supply chain challenges include high treatment costs, dialysis infrastructure limitations in emerging markets, organ donor shortages, reimbursement disparities, cold-chain logistics for transplant products, and dependency on specialized medical consumables.

Global Kidney Disease Market Value Chain & Supply Chain Evolution Current Scenario

The current kidney disease care ecosystem is characterized by strong reliance on in-center hemodialysis, increasing adoption of peritoneal dialysis, and gradual expansion of home-based treatment models supported by telehealth infrastructure.

Dialysis providers and medical device companies are expanding global networks of treatment centers, while pharmaceutical firms are advancing nephroprotective therapies such as SGLT2 inhibitors, anemia management drugs, and mineral bone disorder treatments.

Hospitals and dialysis chains are increasingly adopting integrated care delivery systems that combine diagnostics, treatment, and monitoring under unified care pathways. This is improving patient outcomes while optimizing operational efficiency.

Remote patient monitoring (RPM), digital kidney health platforms, and IoT-enabled dialysis machines are emerging as critical enablers for decentralized renal care, reducing hospital dependency and improving chronic disease management.

At the same time, transplant ecosystems remain constrained by organ availability, surgical infrastructure, and regulatory frameworks, maintaining sustained demand for dialysis-based therapies globally.

Key Value Chain & Supply Chain Evolution Signals in Global Kidney Disease Market

Several structural trends are reshaping the kidney disease value chain globally.

First, rising CKD prevalence driven by diabetes and hypertension is significantly expanding demand for dialysis services, renal drugs, and diagnostic solutions.

Second, the shift toward home dialysis and decentralized care models is transforming traditional hospital-centric treatment systems.

Third, pharmaceutical innovation in nephroprotective therapies is slowing disease progression and reshaping long-term treatment pathways.

Fourth, digital health integration, including tele-nephrology, AI-based monitoring, and connected dialysis devices, is improving clinical efficiency and reducing hospitalization rates.

Fifth, healthcare policy reforms and reimbursement expansion in emerging markets are driving infrastructure investments in dialysis centers and transplant programs.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Kidney Disease Market

Leading players such as Fresenius Medical Care, DaVita Inc., Baxter International, and B. Braun Melsungen AG are strengthening their positions through vertically integrated care models combining dialysis services, consumables, and digital health platforms.

Pharmaceutical companies including AstraZeneca, Novo Nordisk, and Otsuka are expanding renal care portfolios with SGLT2 inhibitors, anemia treatments, and emerging disease-modifying therapies targeting CKD progression.

Competitive advantage increasingly depends on integrated care delivery capability, dialysis network scale, consumable supply efficiency, digital monitoring adoption, and payer partnerships.

Strategic collaborations between device manufacturers, pharmaceutical companies, hospitals, and telehealth providers are becoming essential for expanding access to affordable and scalable renal care solutions.

Long-term competitiveness will depend on reducing treatment costs, improving home-care adoption, enhancing early diagnosis rates, and integrating AI-driven predictive care models into standard renal treatment pathways.

Global Kidney Disease Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the kidney disease value chain is expected to transition toward a more decentralized, digitally enabled, and preventive care-oriented ecosystem.

Home dialysis adoption is expected to accelerate significantly, supported by portable dialysis machines, remote monitoring systems, and caregiver training programs.

AI-powered diagnostics, predictive analytics, and digital twin models for patient health will enable earlier intervention and improved disease progression management.

Pharmaceutical innovation in kidney-protective therapies is expected to reduce ESRD progression rates, potentially reshaping long-term dialysis demand patterns.

Transplant infrastructure expansion, improved organ preservation technologies, and enhanced donor matching systems are expected to improve transplant accessibility globally.

Ultimately, the kidney disease value chain will evolve into an integrated ecosystem combining medical devices, pharmaceuticals, digital health platforms, and home-based care models to deliver more efficient, accessible, and patient-centric renal care.

Market-Specific Value Chain

- Diagnostics & Early Detection: Laboratory testing (eGFR, creatinine, ACR), imaging systems (ultrasound, CT, MRI), biomarker diagnostics (NGAL, cystatin C, KIM-1)

- Pharmaceutical Development & Therapy: Nephroprotective drugs, SGLT2 inhibitors, ACE/ARB therapies, anemia management drugs, phosphate binders, regenerative medicine pipelines

- Dialysis Equipment & Consumables: Hemodialysis machines, PD cyclers, dialyzers, bloodlines, catheters, water treatment systems

- Clinical Care Delivery: Hospitals, dialysis centers, specialty renal clinics, transplant centers, critical care units

- Home & Remote Care Ecosystem: Home dialysis systems, tele-nephrology platforms, remote patient monitoring (RPM), connected health devices

- Transplant & Long-Term Management: Organ procurement systems, immunosuppressive therapies, post-transplant care, patient monitoring systems

Company-to-Stage Mapping

- Diagnostics & Early Detection: Roche Diagnostics, Siemens Healthineers, Abbott Laboratories

- Pharmaceutical Development & Therapy: AstraZeneca, Novo Nordisk, Otsuka, Novartis, Amgen

- Dialysis Equipment & Consumables: Fresenius Medical Care, Baxter International, Nipro Corporation, Nikkiso Co., Ltd.

- Clinical Care Delivery: DaVita Inc., Fresenius Medical Care, B. Braun Melsungen AG

- Home & Remote Care Ecosystem: Baxter International, emerging telehealth startups, digital nephrology platforms

- Transplant & Long-Term Management: Hospital transplant networks, immunosuppressant developers (Novartis, Astellas, Pfizer)

Investment Activity

Global Kidney Disease Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Kidney Disease Market are being driven by the rapidly increasing burden of chronic kidney disease (CKD) and end-stage renal disease (ESRD), rising diabetes and hypertension prevalence, and expanding demand for dialysis infrastructure and long-term renal care solutions. Between 2026 and 2033, capital allocation is expected to accelerate across dialysis services, home-based care models, renal pharmaceuticals, diagnostic platforms, and next-generation digital kidney health ecosystems.

The market remains highly capital intensive due to the recurring nature of treatment, especially dialysis consumables, equipment replacement cycles, and infrastructure-heavy care delivery systems. Leading players such as Fresenius Medical Care, DaVita, Baxter International, B. Braun, and Nipro Corporation continue to attract sustained investments through integrated care models combining dialysis services, devices, and renal pharmaceuticals.

A major structural shift shaping investment flows is the transition from centralized hospital-based dialysis toward decentralized, home-based dialysis and digitally enabled renal care. This is driving strong funding momentum in tele-nephrology platforms, remote patient monitoring systems, wearable kidney devices, and AI-enabled disease progression analytics.

Global Kidney Disease Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by rising CKD diagnosis rates, expansion of dialysis infrastructure in emerging economies, and increasing healthcare expenditure on chronic disease management. Governments and private healthcare providers are investing heavily in dialysis center expansion, transplant programs, and early-stage screening initiatives to reduce long-term treatment burden.

- North America: Leads global investment due to advanced dialysis infrastructure, strong reimbursement systems (Medicare/private insurers), and high adoption of home dialysis and digital renal care solutions.

- Asia-Pacific: Fastest-growing investment region driven by rising diabetes prevalence, large untreated CKD population, and rapid expansion of dialysis centers in China, India, and Southeast Asia.

- Europe: Focused on preventive nephrology care, home dialysis adoption, transplant program strengthening, and cost-efficient renal care delivery models.

- Latin America: Expanding investments in dialysis infrastructure, especially in Brazil and Mexico, supported by public-private healthcare initiatives.

- Middle East & Africa: Emerging investment region driven by healthcare infrastructure development, medical tourism, and increasing government funding for specialty renal care centers.

Key Investment & Funding Dynamics Signals in Global Kidney Disease Market

- Rising global CKD and ESRD prevalence is driving long-term, recurring investments in dialysis infrastructure and consumable supply chains.

- Expansion of home dialysis (HHD and CAPD) is attracting significant funding into portable dialysis machines, training ecosystems, and home-care support services.

- Strong investment momentum in nephroprotective drug development, including SGLT2 inhibitors, HIF stabilizers, and anti-fibrotic therapies, is reshaping pharmaceutical funding flows.

- Digital transformation is accelerating capital deployment into tele-nephrology platforms, AI-based kidney monitoring tools, and remote patient management systems.

- Dialysis consumables (dialyzers, bloodlines, catheters) continue to attract steady investment due to high-volume recurring demand and long-term service contracts.

- Transplant infrastructure development and immunosuppressant therapies remain key funding areas due to limited organ availability and high unmet clinical need.

Strategic Implications of Investment & Funding Dynamics in Global Kidney Disease Market

- The investment landscape strongly favors integrated renal care providers that combine dialysis services, devices, pharmaceuticals, and digital health platforms under unified care ecosystems.

- Home-based dialysis and decentralized care models are becoming a core strategic focus, reducing hospital dependency while expanding patient reach and cost efficiency.

- Pharma-device convergence is increasing, with companies investing in both renal therapeutics and dialysis technologies to strengthen end-to-end treatment control.

- Data-driven renal care management is emerging as a key competitive advantage, with AI-enabled predictive analytics improving patient outcomes and reducing hospitalization rates.

- Public-private partnerships are critical for scaling dialysis infrastructure in emerging markets where affordability and access remain major challenges.

- Cost containment pressures are driving investments in efficient dialysis technologies, reusable systems, and optimized treatment protocols.

Global Kidney Disease Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Kidney Disease Market is expected to attract sustained and expanding investment driven by the rising global CKD burden and increasing demand for long-term renal care solutions.

Future capital allocation will increasingly focus on home dialysis expansion, AI-driven disease monitoring systems, regenerative kidney therapies, and next-generation nephroprotective drugs aimed at slowing disease progression and reducing dialysis dependency.

- North America: Will continue leading investments in advanced dialysis technologies, home-care models, and digital renal health ecosystems.

- Asia-Pacific: Will remain the fastest-growing investment hub due to large unmet patient populations and expanding healthcare infrastructure.

- Europe: Will focus on preventive care systems, transplant optimization, and sustainable dialysis delivery models.

- Emerging Regions: Latin America and MEA will see accelerated investments in dialysis access expansion and renal specialty care infrastructure.

Digital health transformation will play a central role in reshaping investment strategies, with increased adoption of remote monitoring systems, predictive analytics, and connected dialysis devices improving care efficiency and reducing overall healthcare costs.

Overall, the market will remain structurally resilient and investment-intensive due to the chronic, lifelong nature of kidney disease treatment. Companies that successfully integrate clinical care, digital health, and pharmaceutical innovation will be best positioned to lead the Global Kidney Disease Market through 2033.

Technology & Innovation

Global Kidney Disease Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Kidney Disease Market is rapidly evolving as healthcare systems shift from traditional in-clinic care toward digitally enabled, patient-centric, and predictive renal care ecosystems. Advances in medical devices, biotechnology, and digital health platforms are transforming how chronic kidney disease (CKD) and end-stage renal disease (ESRD) are diagnosed, monitored, and treated.

A major innovation shift is the integration of connected dialysis systems, wearable kidney monitoring devices, and AI-powered clinical decision support tools. These technologies enable real-time patient monitoring, early detection of complications, and improved treatment personalization, significantly enhancing patient outcomes and reducing hospitalization rates.

Pharmaceutical innovation is another key pillar of technological advancement in the market. The emergence of SGLT2 inhibitors, HIF stabilizers, and next-generation nephroprotective therapies is reshaping disease management by slowing CKD progression and reducing dependency on dialysis in early-stage patients. Regenerative medicine research, including stem-cell therapies and bioartificial kidney development, is also gaining momentum as a long-term disruptive innovation area.

On the diagnostics side, biomarker-based testing and AI-enhanced laboratory platforms are improving early detection accuracy. Advanced biomarkers such as NGAL, KIM-1, and cystatin C are enabling clinicians to identify kidney injury at earlier stages compared to traditional creatinine-based methods.

Digital health and remote monitoring technologies are further redefining renal care delivery. Tele-nephrology platforms, IoT-enabled dialysis machines, and cloud-based patient management systems allow continuous monitoring of kidney function, treatment adherence, and fluid balance, especially for home dialysis patients.

Global Kidney Disease Market Technology & Innovation Current Scenario

Currently, the kidney disease market is centered around improving treatment accessibility, enhancing dialysis efficiency, and integrating digital health into chronic care management. In-center hemodialysis remains dominant, but home dialysis and portable treatment systems are gaining strong traction due to convenience and cost-effectiveness.

Connected dialysis machines now integrate with cloud platforms, enabling real-time data sharing between patients, clinicians, and care providers. This improves treatment personalization and reduces complications such as hypotension and infection risks.

Artificial intelligence is increasingly being used for predictive analytics in CKD progression, helping clinicians identify high-risk patients earlier and optimize treatment pathways. Machine learning models are also being used to analyze large-scale patient data for better clinical decision-making.

Wearable kidney monitoring devices are emerging as a new innovation frontier, allowing continuous tracking of vital renal health indicators outside clinical environments. These devices aim to reduce hospital visits while improving long-term disease management.

Additionally, home-based dialysis technologies are evolving with compact, user-friendly systems that allow patients to undergo treatment with minimal clinical supervision. This shift is significantly improving patient quality of life and reducing healthcare system burden.

Key Technology & Innovation Trends in Global Kidney Disease Market

- Connected Dialysis Systems: IoT-enabled machines providing real-time monitoring and remote clinician access.

- AI-Based Predictive Diagnostics: Machine learning models for early detection of CKD progression and complications.

- Wearable Kidney Monitoring Devices: Continuous tracking of hydration, electrolyte balance, and renal function indicators.

- Advanced Biomarker Diagnostics: Use of NGAL, KIM-1, and cystatin C for early-stage kidney injury detection.

- Home Dialysis Innovation: Portable hemodialysis and automated peritoneal dialysis systems.

- Tele-Nephrology Platforms: Remote consultations and digital kidney care management systems.

- Nephroprotective Drug Innovation: SGLT2 inhibitors and HIF stabilizers slowing CKD progression.

- Regenerative Medicine Research: Stem-cell therapy and bioartificial kidney development.

Strategic Implications of Technology & Innovation

Technological advancements are fundamentally transforming the kidney disease market from a hospital-centric model to a distributed, digital-first care ecosystem. This shift is improving accessibility of renal care, particularly in emerging markets where dialysis infrastructure is limited.

Healthcare providers are increasingly adopting hybrid care models combining in-center dialysis, home-based treatment, and remote monitoring to optimize patient outcomes and reduce operational costs.

Pharmaceutical and medical device companies are collaborating more closely with digital health firms to develop integrated renal care solutions that combine diagnostics, treatment, and continuous monitoring into unified platforms.

Regulatory bodies are also supporting innovation through faster approvals for digital health solutions and advanced renal therapeutics, further accelerating market transformation.

Global Kidney Disease Market Technology & Innovation Forward Outlook

The future of the kidney disease market is expected to be defined by AI-driven predictive care, fully automated dialysis systems, and regenerative kidney therapies that could reduce or eliminate long-term dialysis dependence.

Wearable artificial kidney devices and implantable bioengineered solutions are emerging as long-term disruptive technologies with the potential to fundamentally reshape renal care delivery.

Digital health ecosystems integrating patient data, AI analytics, and remote clinical oversight will become standard across developed healthcare systems, enabling proactive and personalized kidney disease management.

In the long term, convergence between biotechnology, medical devices, and digital health platforms will create fully integrated renal care ecosystems, significantly improving survival rates and quality of life for CKD and ESRD patients.

Market Risk

Global Kidney Disease Market Risk Factors & Disruption Threats Overview

The Global Kidney Disease Market operates within a highly critical healthcare segment driven by chronic disease prevalence, long-term treatment dependency, and rising demand for dialysis and transplant services. Despite strong structural growth, the market carries a high clinical, regulatory, and reimbursement risk profile due to escalating healthcare costs, infrastructure limitations, therapy access gaps, and increasing pressure on public and private payers.

One of the primary risk factors is the high treatment cost burden associated with chronic kidney disease (CKD) and end-stage renal disease (ESRD). Long-term dialysis, transplantation procedures, and advanced pharmacological therapies place significant financial pressure on healthcare systems and patients, particularly in emerging economies.

Another major disruption factor is limited organ availability for kidney transplantation, which creates long-term dependency on dialysis-based care models. This imbalance between demand and supply continues to constrain optimal treatment outcomes globally.

Additionally, disparities in healthcare infrastructure and reimbursement coverage across regions significantly impact patient access to early diagnosis, dialysis facilities, and advanced renal therapies, especially in low- and middle-income countries.

Rapid technological evolution in renal care, including home dialysis systems, digital monitoring platforms, and regenerative therapies, is also disrupting traditional care delivery models and forcing providers to adapt quickly to new treatment paradigms.

Global Kidney Disease Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by rising CKD and diabetes prevalence, increasing demand for dialysis services, and growing adoption of home-based and decentralized care models. Healthcare systems are under continuous pressure due to the increasing patient pool requiring long-term renal replacement therapy.

However, capacity constraints in dialysis centers, workforce shortages in nephrology care, and uneven distribution of renal infrastructure are limiting treatment accessibility in several regions.

Reimbursement challenges remain a key concern, as dialysis and transplant-related costs are heavily dependent on government healthcare funding, insurance coverage, and reimbursement frameworks that vary widely across countries.

At the same time, supply chain dependencies for dialysis consumables, machines, and pharmaceutical products are creating operational vulnerabilities, particularly in regions dependent on imports.

Digital transformation is expanding rapidly in kidney care through tele-nephrology and remote patient monitoring, but integration challenges with legacy hospital systems and data interoperability issues continue to slow adoption in some markets.

Key Risk Factors & Disruption Threats Signals in Global Kidney Disease Market

A major disruption signal is the rapid rise in diabetes and hypertension prevalence, which is significantly increasing the global CKD patient population and placing long-term strain on dialysis and transplant infrastructure.

The growing shift toward home dialysis and remote monitoring systems is transforming traditional in-center care models, reducing hospital dependency while increasing demand for portable devices and connected health solutions.

Advancements in nephroprotective drugs such as SGLT2 inhibitors and emerging regenerative therapies are gradually altering disease progression patterns, potentially reducing long-term dialysis demand in certain patient segments.

Healthcare workforce shortages, particularly nephrologists and dialysis technicians, are emerging as a structural constraint, limiting the scalability of renal care services in both developed and developing regions.

Additionally, increasing regulatory scrutiny over dialysis pricing, pharmaceutical costs, and healthcare reimbursement models is intensifying pressure on market profitability and operational sustainability.

Strategic Implications of Risk Factors & Disruption Threats in Global Kidney Disease Market

Market participants must prioritize integrated care models that combine dialysis services, pharmaceutical therapies, and digital health solutions to ensure long-term competitiveness in a highly regulated healthcare environment.

Investment in home dialysis technologies, portable treatment systems, and remote monitoring platforms will be critical to addressing infrastructure bottlenecks and improving patient accessibility.

Companies should strengthen partnerships with healthcare providers, payers, and governments to secure reimbursement support and expand access to renal care services across underserved regions.

Supply chain resilience strategies must be developed to ensure consistent availability of dialysis consumables, devices, and essential renal pharmaceuticals amid global logistics disruptions.

Strategic focus on early diagnosis programs, preventive nephrology care, and AI-enabled disease progression tracking will be essential to reduce long-term treatment burden and improve clinical outcomes.

Global Kidney Disease Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Kidney Disease Market is expected to evolve toward more decentralized, technology-enabled, and patient-centric care delivery systems. However, structural risks related to disease prevalence, healthcare funding, and infrastructure limitations will continue to shape market dynamics.

Home dialysis, tele-nephrology, and AI-driven remote monitoring are expected to become mainstream, significantly transforming traditional hospital-based treatment models and improving care accessibility.

Advancements in regenerative medicine, kidney bioengineering, and disease-modifying therapies hold long-term disruptive potential, potentially reducing dependence on chronic dialysis over time.

At the same time, rising healthcare costs, reimbursement constraints, and unequal global access to renal care will remain persistent challenges affecting market scalability and patient outcomes.

Overall, the market will continue to expand steadily, but long-term success will depend on the ability of stakeholders to balance cost efficiency, technological innovation, infrastructure expansion, and equitable access to life-saving renal therapies.

Regulatory Landscape

Global Kidney Disease Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Kidney Disease Market is highly structured and continuously evolving, driven by rising chronic kidney disease (CKD) burden, increasing dialysis dependency, and strong government involvement in renal care funding and reimbursement systems. Because kidney disease treatment spans pharmaceuticals, medical devices, dialysis services, and transplant systems, it is governed by a multi-layered regulatory framework involving drug authorities, medical device regulators, and public health agencies.

Regulatory bodies such as the U.S. FDA, European Medicines Agency (EMA), and national health authorities oversee approval of nephrology drugs, dialysis machines, and renal care technologies, while healthcare financing systems and insurance programs strongly influence patient access to long-term treatment. Policies related to dialysis reimbursement, transplant allocation systems, and chronic disease management programs play a central role in shaping market demand.

Globally, governments are increasingly prioritizing early detection and prevention of kidney disease through national screening programs, primary care integration, and public awareness initiatives. This is shifting the regulatory focus from end-stage renal disease (ESRD) treatment toward early intervention, slowing disease progression, and reducing long-term healthcare costs.

At the same time, the market is influenced by strict medical device regulations, clinical trial requirements for nephrology drugs, and stringent safety standards for dialysis equipment and consumables. Regulatory harmonization efforts are gradually improving global approval pathways, but regional differences continue to create compliance complexity for multinational manufacturers and service providers.

Global Kidney Disease Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is defined by strong reimbursement-driven demand, expanding dialysis coverage programs, and increasing regulatory focus on patient safety and treatment outcomes. North America leads in structured reimbursement systems, particularly through Medicare coverage for dialysis and transplant-related care, which ensures broad patient access to renal replacement therapies.

In Europe, kidney disease management is supported by universal healthcare systems, national CKD registries, and strict clinical guidelines for dialysis initiation and transplant eligibility. Regulatory frameworks emphasize cost containment, home dialysis adoption, and improved clinical outcomes through standardized treatment protocols.

Asia-Pacific is rapidly expanding its regulatory and healthcare infrastructure, with countries such as China and India increasing public investment in dialysis centers, transplant programs, and essential nephrology drug access. Governments are also introducing national CKD screening initiatives to address the rising burden of diabetes-related kidney disease.

Latin America is strengthening dialysis reimbursement policies and expanding public-private partnerships to improve access to renal care, while Brazil and Mexico remain key regulatory leaders in regional nephrology infrastructure development.

The Middle East & Africa region is witnessing gradual improvements in renal healthcare regulation, driven by government investments in specialized hospitals, transplant programs, and dialysis infrastructure, often supported by medical tourism and international healthcare collaborations.

Across all regions, regulatory emphasis is increasingly shifting toward early-stage CKD management, home-based dialysis adoption, and integration of digital health technologies into renal care pathways.

Key Regulatory & Policy Environment Signals in Global Kidney Disease Market

- Dialysis Reimbursement & Healthcare Funding Policies: Government insurance systems and reimbursement frameworks are the primary drivers of dialysis and ESRD treatment accessibility.

- Medical Device Approval & Safety Regulations: Strict FDA, CE, and national regulatory approvals govern dialysis machines, consumables, and monitoring devices.

- Nephrology Drug Development Guidelines: Clinical trial regulations for CKD drugs, including SGLT2 inhibitors and emerging nephroprotective therapies, are shaping innovation timelines.

- Organ Transplant Allocation Policies: Ethical frameworks and national registries regulate kidney transplant distribution and donor-recipient matching systems.

- Chronic Disease Screening & Early Detection Programs: Governments are expanding CKD screening mandates using eGFR, urinalysis, and risk-based population monitoring.

- Home Dialysis & Telehealth Regulation: Policies supporting remote patient monitoring, home hemodialysis, and digital nephrology platforms are accelerating decentralized care adoption.

Strategic Implications of Regulatory & Policy Environment in Global Kidney Disease Market

Regulatory frameworks are increasingly shaping the shift from hospital-centric dialysis care toward home-based and digitally enabled renal treatment models. Reimbursement policies that support home dialysis adoption are encouraging manufacturers to develop portable dialysis systems, wearable devices, and patient-friendly treatment solutions.

Drug approval pathways and clinical trial regulations are accelerating innovation in nephrology therapeutics, particularly in areas such as SGLT2 inhibitors, anemia management, and anti-fibrotic therapies. Companies that successfully navigate regulatory requirements are gaining faster market access and stronger clinical adoption.

Medical device compliance standards are driving continuous improvements in dialysis machine safety, efficiency, and connectivity. Manufacturers are investing in AI-enabled monitoring systems, automated dialysis equipment, and integrated care platforms to meet evolving regulatory expectations for patient outcomes and safety.

Government-led CKD screening and prevention programs are expanding the diagnosed patient pool, increasing long-term demand for diagnostic tools, early-stage therapeutics, and preventive care solutions. This is shifting industry focus toward earlier intervention strategies rather than late-stage treatment alone.

Additionally, transplant policies and organ allocation frameworks are influencing long-term dialysis demand, as limited organ availability continues to sustain dependence on renal replacement therapies across global markets.

Global Kidney Disease Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Kidney Disease Market is expected to become more integrated, outcome-driven, and digitally enabled, with a strong emphasis on early detection, home-based care, and cost-efficient treatment models.

North America is expected to further strengthen value-based care models, linking reimbursement to patient outcomes, dialysis efficiency, and reduced hospitalization rates. Regulatory support for home dialysis and tele-nephrology is also expected to expand significantly.

Europe will continue focusing on preventive nephrology care, standardized CKD management protocols, and expanded adoption of home dialysis solutions supported by national healthcare systems and digital health integration policies.

Asia-Pacific will remain the fastest-evolving regulatory region, with increasing government investment in dialysis infrastructure, expanded public screening programs, and growing approval pathways for nephrology drugs and medical devices to address rising CKD prevalence.

Latin America and the Middle East & Africa are expected to gradually strengthen renal healthcare regulations, focusing on expanding dialysis access, improving transplant systems, and increasing collaboration with global healthcare providers and device manufacturers.

Overall, the regulatory landscape will continue to drive innovation toward more accessible, affordable, and technology-enabled kidney care solutions. Companies that align with evolving reimbursement systems, invest in compliant digital health platforms, and develop patient-centric treatment models will be best positioned for long-term growth in the global kidney disease market.