Global Digital Transformation Market Report, Size & Forecast 2026-2033

Market Forecast Snapshot (2026???2033)

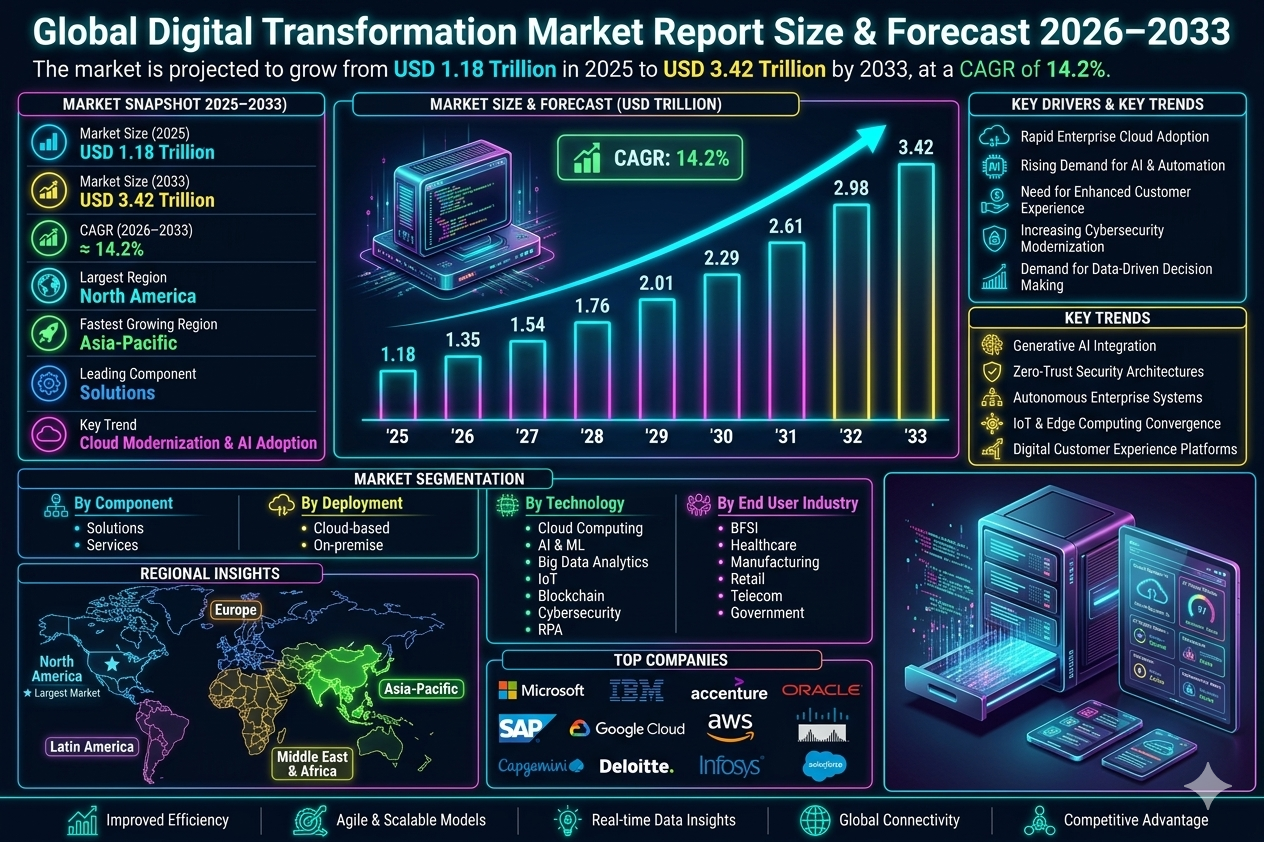

| Metric | Value |

|---|---|

| Market Size (2025) | USD 1.18 Trillion |

| Market Size (2033) | USD 3.42 Trillion |

| CAGR (2026???2033) | 14.2% |

| Largest Segment | Cloud Computing & Enterprise Software Solutions |

| Fastest Growing Segment | Artificial Intelligence & Intelligent Automation Solutions |

| Leading End-Use Segment | BFSI & Healthcare |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Key Market Trend | Generative AI Integration, Cloud-Native Transformation, and Hyperautomation |

| Primary Growth Driver | Rapid Enterprise Digitization and Increasing Cloud & AI Investments |

Global Digital Transformation Market Size & Forecast

The global digital transformation market is projected to witness exceptional growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 1.18 trillion in 2025 and is expected to reach nearly USD 3.42 trillion by 2033, expanding at a CAGR of around 14.2%. The market growth is driven by rapid enterprise digitization, increasing cloud adoption, rising investments in artificial intelligence and automation technologies, expanding demand for data-driven decision-making, and the growing need for agile business models across industries worldwide. Digital transformation refers to the strategic integration of digital technologies across business processes, operations, customer experiences, and organizational models to improve efficiency, innovation, scalability, and competitive advantage. It encompasses cloud computing, artificial intelligence, machine learning, big data analytics, Internet of Things (IoT), blockchain, cybersecurity, robotic process automation, and digital customer engagement platforms. The market is undergoing rapid evolution through the integration of intelligent automation, hyper-personalization technologies, advanced analytics, and cloud-native architectures that enable organizations to modernize legacy systems and accelerate innovation cycles. Additionally, increasing demand for remote operations, digital-first customer engagement, and operational resilience is significantly accelerating digital transformation initiatives globally.

Global Digital Transformation Market Overview

The digital transformation market represents one of the fastest-growing segments of the global enterprise technology ecosystem. Organizations across sectors are increasingly adopting digital strategies to improve operational agility, optimize costs, enhance customer experiences, and build future-ready business infrastructures. The market includes cloud transformation, business process automation, digital workplace solutions, cybersecurity modernization, enterprise mobility, advanced analytics, AI-powered applications, and digital customer experience platforms. Digital transformation initiatives are increasingly becoming central to enterprise competitiveness, enabling organizations to respond effectively to evolving market dynamics and technological disruption. Technological advancements in generative AI, edge computing, 5G connectivity, quantum-ready architectures, low-code platforms, and intelligent automation are significantly reshaping the market landscape. Major market participants include Microsoft Corporation, IBM Corporation, Accenture plc, Oracle Corporation, SAP SE, Google Cloud, Amazon Web Services (AWS), Cisco Systems, Capgemini, Deloitte, and Infosys Limited.Key Drivers of Global Digital Transformation Market Growth

Rapid Enterprise Cloud Adoption

Organizations are increasingly migrating workloads to cloud-based environments to improve scalability, flexibility, and operational efficiency. Cloud modernization is a core driver of digital transformation investments.Rising Demand for Artificial Intelligence and Automation

Businesses are adopting AI, machine learning, and robotic process automation to improve productivity and decision-making. Automation is significantly enhancing operational efficiency across industries.Growing Need for Enhanced Customer Experience

Digital customer engagement platforms are enabling organizations to deliver personalized and seamless user experiences. This is driving widespread digital transformation across consumer-facing sectors.Increasing Cybersecurity Modernization

As digital operations expand, organizations are investing heavily in cybersecurity frameworks and zero-trust architectures. Cyber resilience has become essential to digital transformation success.Demand for Data-Driven Decision Making

Advanced analytics and business intelligence tools are empowering enterprises to leverage real-time insights for strategic planning. Data monetization is becoming a critical competitive differentiator.Global Digital Transformation Market Segmentation

By Component

The market is segmented into solutions and services. Solutions dominate the market due to widespread enterprise software adoption.By Deployment Mode

The market includes cloud-based and on-premise deployment models. Cloud-based deployment is the fastest-growing segment due to scalability and cost efficiency.By Technology

The market includes cloud computing, artificial intelligence, big data analytics, IoT, blockchain, cybersecurity, and robotic process automation. Cloud computing and AI account for the largest market share.By End User Industry

End-user industries include BFSI, healthcare, manufacturing, retail, telecom, government, education, and transportation. BFSI and healthcare represent major adoption sectors globally.Regional Market Dynamics

North America

North America dominates the global digital transformation market due to advanced technology infrastructure, high enterprise IT spending, and strong innovation ecosystems. The United States remains the leading regional market.Europe

Europe maintains significant market share supported by digital modernization initiatives, smart manufacturing adoption, and enterprise cloud migration. Germany, the United Kingdom, and France are key contributors.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid digitalization, government smart infrastructure initiatives, and increasing enterprise technology investments. China, India, Japan, South Korea, and Southeast Asia are major growth markets.Latin America

Latin America is experiencing steady growth driven by digital banking, e-commerce expansion, and cloud adoption. Brazil and Mexico are leading regional contributors.Middle East & Africa

The region is witnessing increasing digital transformation investments through smart city initiatives and public sector modernization programs. UAE and Saudi Arabia are major emerging markets.Competitive Landscape

The global digital transformation market is highly competitive and innovation-driven, with technology giants, consulting firms, and cloud service providers competing through integrated solutions and strategic partnerships. Key players include Microsoft Corporation, IBM Corporation, Accenture plc, Oracle Corporation, SAP SE, Google Cloud, Amazon Web Services, Cisco Systems, Capgemini, Deloitte, and Infosys Limited. Companies are investing heavily in AI innovation, cloud-native platforms, digital consulting capabilities, and cybersecurity solutions. Strategic acquisitions, ecosystem collaborations, and industry-specific solution development are strengthening market positioning.Strategic Outlook

The strategic outlook for the global digital transformation market remains exceptionally strong due to ongoing enterprise modernization and technological convergence. Future opportunities include generative AI integration, autonomous enterprise systems, digital twins, immersive customer experiences, and decentralized cloud infrastructure. Organizations prioritizing agile transformation frameworks, cybersecurity resilience, and data intelligence will remain competitive. Technology providers investing in industry-specific digital platforms and AI-powered transformation services are expected to lead future growth.Final Market Perspective

The global digital transformation market continues to redefine how organizations operate, innovate, and compete across industries worldwide. Accelerating cloud adoption, AI integration, and digital-first business models will continue driving strong market expansion throughout the forecast period. Companies that successfully combine technological innovation, strategic agility, and customer-centric transformation will remain strongly positioned in the evolving global digital transformation market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Digital Transformation Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Digital Transformation

- 2.2 Scope of the Study

- 2.3 Evolution of Enterprise Digitalization

- 2.4 Digital Business Ecosystem Analysis

- 2.5 Regulatory & Governance Framework

- 2.6 Enterprise Technology Adoption Trends

- 2.7 Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rapid Enterprise Cloud Adoption

- 4.1.2 Rising Demand for AI and Automation

- 4.1.3 Growing Need for Enhanced Customer Experience

- 4.1.4 Increasing Cybersecurity Modernization

- 4.1.5 Demand for Data-Driven Decision Making

- 4.2 Restraints

- 4.2.1 High Implementation Costs

- 4.2.2 Legacy Infrastructure Complexity

- 4.2.3 Digital Skills Shortage

- 4.2.4 Data Privacy & Compliance Challenges

- 4.3 Opportunities

- 4.3.1 Generative AI Integration

- 4.3.2 Digital Twin Adoption

- 4.3.3 Industry-Specific Transformation Platforms

- 4.3.4 Expansion in Emerging Markets

- 4.4 Challenges

- 4.4.1 Change Management Complexity

- 4.4.2 Cybersecurity Risks

- 4.4.3 Integration Across Legacy Systems

- 4.4.4 ROI Measurement Difficulties

- 4.1 Drivers

- 5. Global Digital Transformation Market Analysis (USD Trillion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Technology Adoption Trends

- 5.5 Enterprise Investment Analysis

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Trillion), 2026???2033

- 6.1 By Component

- 6.1.1 Solutions

- 6.1.2 Services

- 6.2 By Deployment Mode

- 6.2.1 Cloud-Based

- 6.2.2 On-Premise

- 6.3 By Technology

- 6.3.1 Cloud Computing

- 6.3.2 Artificial Intelligence

- 6.3.3 Big Data Analytics

- 6.3.4 Internet of Things (IoT)

- 6.3.5 Blockchain

- 6.3.6 Cybersecurity

- 6.3.7 Robotic Process Automation

- 6.4 By End User Industry

- 6.4.1 BFSI

- 6.4.2 Healthcare

- 6.4.3 Manufacturing

- 6.4.4 Retail

- 6.4.5 Telecom

- 6.4.6 Government

- 6.4.7 Education

- 6.4.8 Transportation

- 6.1 By Component

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Technology Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Product Innovation Analysis

- 8.5 Digital Platform Positioning Strategies

- 9. Company Profiles

- 9.1 Microsoft Corporation

- 9.2 IBM Corporation

- 9.3 Accenture plc

- 9.4 Oracle Corporation

- 9.5 SAP SE

- 9.6 Google Cloud

- 9.7 Amazon Web Services (AWS)

- 9.8 Cisco Systems

- 9.9 Capgemini

- 9.10 Infosys Limited

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Digital Innovation Forecast Engine

- 10.2 Enterprise Transformation Analytics Dashboard

- 10.3 Technology Adoption Intelligence Tracker

- 10.4 AI-Driven Opportunity Analyzer

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Investment in AI-Powered Transformation

- 11.2 Strengthening Cybersecurity Resilience

- 11.3 Accelerating Cloud-Native Modernization

- 11.4 Expanding Industry-Specific Solutions

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Digital Transformation Market Competitive Intensity & Market Structure Overview

The global digital transformation market is highly competitive and moderately consolidated, characterized by intense competition among global cloud hyperscalers, enterprise software providers, IT consulting firms, cybersecurity companies, and digital transformation service integrators. Competitive intensity is driven by cloud infrastructure capabilities, AI integration, platform scalability, industry-specific digital solutions, ecosystem partnerships, and innovation speed.

The market structure consists of dominant multinational technology providers offering integrated digital transformation ecosystems, alongside specialized consulting firms and niche technology vendors focused on sector-specific modernization solutions. Competition is increasingly shaped by cloud-native architectures, generative AI deployment, automation capabilities, and advanced cybersecurity frameworks.

Rapid enterprise digitization, increasing demand for operational agility, and accelerating adoption of intelligent automation are significantly intensifying competition across the global digital transformation market.

Global Digital Transformation Market Competitive Intensity & Market Structure Current Scenario

Leading Global Digital Transformation Companies

Microsoft Corporation: Market leader with comprehensive cloud, AI, enterprise productivity, and digital infrastructure transformation solutions.

Amazon Web Services (AWS): Dominant cloud infrastructure provider supporting enterprise-scale digital modernization initiatives.

IBM Corporation: Major transformation partner focused on hybrid cloud, AI integration, and enterprise consulting solutions.

Accenture plc: Leading consulting and digital transformation services provider with strong enterprise modernization expertise.

Oracle Corporation: Enterprise software leader offering cloud-native transformation platforms and integrated business applications.

SAP SE: Key provider of digital enterprise resource transformation and intelligent business process automation solutions.

Google Cloud: Rapidly growing cloud and AI transformation platform provider.

Cisco Systems: Major digital infrastructure and secure enterprise networking transformation provider.

Capgemini: Global digital consulting firm specializing in intelligent enterprise transformation.

Infosys Limited: Strong market participant delivering AI-driven digital modernization services.

Key Competitive Intensity & Market Structure Drivers

Accelerating enterprise cloud migration is intensifying competition among platform providers.

Growing adoption of AI and automation technologies is creating strong product differentiation opportunities.

Increasing demand for cybersecurity modernization is strengthening competition around secure digital transformation capabilities.

Industry-specific digital transformation requirements are driving specialized platform innovation.

The need for scalable data analytics and intelligent decision-making systems is reshaping vendor competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Technology providers are increasingly investing in generative AI capabilities and intelligent automation platforms.

Strategic acquisitions and cloud ecosystem partnerships are becoming critical for market expansion.

Industry-focused transformation frameworks are emerging as key competitive differentiators.

Cybersecurity integration and zero-trust architecture deployment are becoming essential market requirements.

Low-code platforms and automation-centric service offerings are reshaping enterprise adoption strategies.

Global Digital Transformation Market Competitive Intensity & Market Structure Forward Outlook

The digital transformation market is expected to remain highly competitive as organizations accelerate enterprise modernization initiatives.

Future competition will increasingly focus on autonomous enterprise systems, digital twins, hyperautomation, and AI-native business platforms.

North America will remain the dominant competitive region, while Asia-Pacific is expected to witness the fastest competitive expansion.

Advancements in generative AI, edge computing, decentralized cloud architecture, and intelligent enterprise orchestration will significantly reshape market dynamics.

Overall, companies that successfully combine AI innovation, scalable cloud ecosystems, cybersecurity resilience, and industry-specific transformation expertise will remain strongly positioned in the evolving global digital transformation market.

Value Chain

Global Digital Transformation Market Value Chain & Supply Chain Evolution Overview

The global digital transformation market value chain is undergoing accelerated evolution as enterprises increasingly modernize legacy systems, adopt cloud-native infrastructures, integrate artificial intelligence, and deploy data-driven operational frameworks to improve competitiveness, agility, and resilience. Digital transformation has evolved from a technology upgrade initiative into a strategic enterprise-wide business reinvention framework that impacts every operational layer across industries.

The digital transformation value chain spans digital strategy consulting, cloud infrastructure deployment, software platform development, data architecture modernization, cybersecurity integration, process automation implementation, systems interoperability enablement, managed services delivery, and continuous innovation optimization. This interconnected ecosystem includes hyperscale cloud providers, enterprise software vendors, AI platform developers, cybersecurity firms, systems integrators, consulting organizations, managed service providers, and downstream enterprise users.

Major companies including Microsoft Corporation, IBM Corporation, Accenture plc, Oracle Corporation, SAP SE, Google Cloud, Amazon Web Services (AWS), Cisco Systems, Capgemini, Deloitte, and Infosys Limited are actively investing in intelligent automation, cloud-native enterprise platforms, generative AI integration, cybersecurity resilience frameworks, and industry-specific digital transformation solutions to strengthen global market leadership.

Upstream activities involve infrastructure architecture design, cloud platform engineering, AI model development, software framework innovation, data governance framework creation, and cybersecurity protocol development. Midstream operations focus on enterprise system integration, process automation deployment, application modernization, workflow orchestration, change management services, and interoperability implementation. Downstream activities include enterprise optimization, operational analytics, digital customer engagement, autonomous decision support, continuous managed services, and long-term innovation lifecycle management.

Operational priorities across the digital transformation value chain increasingly emphasize agility, scalability, interoperability, security, user-centric design, operational resilience, regulatory compliance, and measurable business value generation. However, the market continues to face challenges related to legacy infrastructure complexity, integration costs, organizational resistance to change, cybersecurity risks, digital skills shortages, and fragmented technology ecosystems.

Global Digital Transformation Market Value Chain & Supply Chain Evolution Current Scenario

The current digital transformation market is being shaped by rapid cloud migration, enterprise AI adoption, increasing automation deployment, hybrid workforce enablement, and growing demand for resilient digital operating models.

North America currently dominates the global digital transformation market due to mature enterprise technology adoption, strong innovation ecosystems, high digital investment intensity, and widespread cloud-first enterprise strategies. The United States remains the leading regional market.

Europe maintains a strong market position supported by digital modernization programs, Industry 4.0 deployment, and enterprise sustainability-focused digital investments. Asia-Pacific is emerging as the fastest-growing region due to rapid enterprise digitization, government-led smart infrastructure initiatives, and expanding cloud adoption across developing economies.

Cloud-based transformation solutions remain the dominant deployment model due to operational flexibility, cost optimization, and rapid scalability.

BFSI, healthcare, manufacturing, and retail continue to represent the largest enterprise digital transformation adoption sectors globally.

Key Value Chain & Supply Chain Evolution Signals in Global Digital Transformation Market

One of the most significant transformation signals is the rapid emergence of generative AI-powered enterprise workflows. Organizations are increasingly embedding AI into decision-making, customer engagement, and operational automation systems.

Cloud-native architecture adoption is becoming central to digital transformation strategies as enterprises modernize legacy infrastructure for greater scalability and flexibility.

Low-code and no-code development platforms are significantly accelerating enterprise application deployment and reducing digital development barriers.

Zero-trust cybersecurity frameworks are becoming critical as digital operations expand across distributed enterprise environments.

Data fabric and unified analytics architectures are enabling increasingly seamless real-time enterprise intelligence generation across operational silos.

Industry-specific digital platforms are becoming more prominent as organizations seek customized transformation frameworks aligned with sector-specific operational requirements.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Digital Transformation Market

Leading digital transformation companies are increasingly prioritizing platform integration, AI-driven automation, cloud ecosystem expansion, and cybersecurity resilience to maintain competitive advantage. Competitive differentiation increasingly depends on ecosystem breadth, implementation expertise, innovation speed, and measurable business outcome delivery.

Companies capable of delivering integrated end-to-end transformation ecosystems combining consulting, cloud modernization, AI intelligence, automation, and managed services are expected to capture premium market opportunities.

Strategic collaborations between cloud providers, consulting firms, AI technology developers, cybersecurity vendors, and industry-specific software providers are becoming essential for accelerating enterprise transformation delivery.

Outcome-based transformation service models are emerging as important commercial structures that improve long-term client retention and recurring revenue streams.

Talent development and digital workforce enablement are becoming increasingly important strategic differentiators as enterprise demand for transformation expertise accelerates.

Localization of digital transformation frameworks to address regional compliance, regulatory, and operational requirements is strengthening global market expansion strategies.

Global Digital Transformation Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the digital transformation value chain is expected to become significantly more autonomous, intelligent, adaptive, and industry-specialized. Enterprise digital transformation will increasingly evolve into self-optimizing operational ecosystems.

Generative AI and autonomous decision systems will continue improving enterprise workflow automation, predictive analytics, and strategic operational intelligence.

Digital twin-enabled enterprise architectures will increasingly support simulation-driven operational optimization and real-time scenario planning.

Decentralized cloud infrastructure and edge intelligence systems will enable faster localized digital operations and reduced latency.

Immersive enterprise experiences using extended reality and advanced collaboration environments will significantly reshape workforce productivity models.

Hyperconnected data ecosystems will expand enterprise-wide interoperability, enabling seamless orchestration across customers, suppliers, partners, and internal systems.

Ultimately, the future digital transformation value chain will evolve into a highly intelligent, autonomous, secure, and continuously adaptive enterprise ecosystem capable of enabling next-generation business reinvention.

Market-Specific Value Chain

- Digital Strategy & Architecture Planning: Transformation consulting, digital maturity assessment, roadmap creation, cloud strategy design, and business model modernization planning.

- Technology Platform Development & Infrastructure Modernization: Cloud migration, enterprise software deployment, AI framework integration, cybersecurity implementation, and infrastructure optimization.

- System Integration & Process Transformation: Workflow automation, application interoperability, enterprise data integration, operational digitization, and business process redesign.

- Enterprise Deployment & Change Management: Implementation services, organizational training, workforce enablement, adoption management, and transformation governance.

- Continuous Analytics & Operational Optimization: Real-time analytics, predictive intelligence, automation refinement, performance monitoring, and operational resilience enhancement.

- Autonomous Enterprise Ecosystem Expansion: AI-driven optimization, digital twin orchestration, adaptive business intelligence, and long-term innovation lifecycle evolution.

Company-to-Stage Mapping

- Digital Strategy & Architecture Planning: Accenture plc, Deloitte, Capgemini, Infosys Limited.

- Technology Platform Development & Infrastructure Modernization: Microsoft Corporation, Amazon Web Services, Google Cloud, Oracle Corporation.

- System Integration & Process Transformation: IBM Corporation, SAP SE, Cisco Systems.

- Enterprise Deployment & Change Management: Global systems integrators and enterprise transformation service providers.

- Continuous Analytics & Operational Optimization: AI analytics platform providers, enterprise automation solution vendors.

- Autonomous Enterprise Ecosystem Expansion: Next-generation AI infrastructure innovators, digital twin platform developers, intelligent enterprise orchestration technology providers.

Investment Activity

Global Digital Transformation Market Investment & Funding Dynamics Overview

The global digital transformation market is witnessing unprecedented investment momentum driven by rapid enterprise modernization, accelerated cloud migration, increasing adoption of artificial intelligence, and growing demand for agile, data-driven business models. Between 2026 and 2033, funding activity is expected to intensify across AI platforms, cloud-native architectures, intelligent automation solutions, advanced analytics ecosystems, and cybersecurity modernization initiatives.

The digital transformation market represents one of the most strategically significant segments within the global enterprise technology ecosystem. Venture capital firms, institutional technology investors, private equity funds, hyperscale cloud providers, and strategic enterprise technology corporations are actively deploying capital toward next-generation digital infrastructure and intelligent business transformation platforms.

A major structural transformation shaping investment dynamics is the transition from isolated digital initiatives to enterprise-wide intelligent transformation ecosystems. This evolution is driving significant capital deployment into integrated cloud infrastructure, automation frameworks, low-code platforms, data intelligence systems, and AI-powered business process optimization technologies.

Growing convergence between artificial intelligence, cloud computing, edge infrastructure, cybersecurity, IoT, digital twins, and enterprise analytics is creating substantial cross-sector investment opportunities across global industries.

Current Investment & Funding Landscape

- North America: Leads global investment activity due to advanced enterprise technology adoption, strong venture capital ecosystems, and hyperscaler innovation.

- Europe: Attracting significant investment through industrial digitalization, smart manufacturing, and cloud modernization programs.

- Asia-Pacific: Emerging as the fastest-growing investment destination driven by rapid enterprise digitization and government-backed smart infrastructure initiatives.

- Latin America: Witnessing increasing investment activity in cloud migration, digital banking, and enterprise automation.

- Middle East & Africa: Strategic investments are accelerating through smart city initiatives and public-sector digital transformation programs.

Key Investment Drivers

- Accelerating enterprise cloud migration strategies.

- Rising investments in artificial intelligence and intelligent automation.

- Increasing demand for data-driven operational decision-making.

- Growing need for cybersecurity modernization and zero-trust architectures.

- Expansion of remote and hybrid work environments.

- Increasing adoption of customer experience transformation platforms.

- Growing competitive pressure for business agility and operational resilience.

- Rapid emergence of generative AI and autonomous enterprise systems.

Strategic Investment Areas

- Cloud Infrastructure: Multi-cloud, hybrid cloud, and cloud-native enterprise transformation solutions.

- Artificial Intelligence Platforms: Generative AI, machine learning, and predictive analytics systems.

- Intelligent Automation: Robotic process automation and workflow orchestration platforms.

- Cybersecurity Modernization: Zero-trust frameworks and advanced digital security architectures.

- Data Analytics Ecosystems: Real-time business intelligence and enterprise data platforms.

- Digital Customer Experience Platforms: Personalization and omnichannel engagement technologies.

Forward Investment Outlook

The global digital transformation market is expected to remain one of the most attractive technology investment sectors throughout the forecast period due to continued enterprise modernization and rapid technology convergence.

Future funding activity is expected to prioritize generative AI integration, autonomous business systems, edge-cloud convergence, digital twin infrastructure, intelligent workflow orchestration, and decentralized enterprise computing platforms.

- North America: Will continue dominating capital inflows through AI and cloud innovation leadership.

- Europe: Will maintain strong investment activity centered on industrial digitization and enterprise modernization.

- Asia-Pacific: Will experience accelerated funding growth driven by large-scale digital infrastructure deployment.

- Emerging Markets: Will attract strategic investments as enterprise digital maturity increases.

Overall, the digital transformation market represents a high-growth investment opportunity positioned at the intersection of enterprise modernization, intelligent automation, cloud innovation, and next-generation digital business infrastructure.

Technology & Innovation

Global Digital Transformation Market Technology & Innovation Landscape Overview

The global digital transformation market is undergoing rapid technological evolution driven by advancements in artificial intelligence, cloud-native computing, edge intelligence, automation frameworks, advanced analytics, cybersecurity modernization, and next-generation connectivity technologies. The evolution of digital transformation technologies is increasingly focused on enabling intelligent enterprise automation, real-time decision-making, hyper-personalized customer engagement, and highly adaptive business ecosystems across industries worldwide.

Modern digital transformation platforms are integrating AI-powered automation engines, multi-cloud architectures, low-code development environments, digital twins, and API-driven enterprise integration systems to streamline operations and accelerate innovation cycles. These innovations are significantly improving business agility, operational resilience, scalability, and enterprise-wide efficiency.

The market is also witnessing strong adoption of generative AI, autonomous workflows, edge computing infrastructure, intelligent process orchestration, and decentralized digital ecosystems that are redefining enterprise technology infrastructure globally.

Global Digital Transformation Market Technology & Innovation Current Scenario

Currently, innovation in the digital transformation market is centered around cloud-first modernization and intelligent automation deployment. Enterprises are rapidly replacing traditional legacy infrastructures with cloud-native systems to improve scalability, flexibility, and operational responsiveness.

Artificial intelligence and machine learning are being widely integrated into digital transformation frameworks to automate decision processes, enhance predictive capabilities, and optimize enterprise operations.

Generative AI technologies are emerging as a major innovation area, enabling intelligent content generation, automated coding, customer service automation, and business workflow augmentation.

Low-code and no-code development platforms are accelerating enterprise application modernization by enabling faster deployment of digital solutions with reduced development complexity.

Edge computing and real-time analytics systems are increasingly being deployed to support low-latency decision-making across distributed enterprise environments.

Zero-trust cybersecurity architectures and intelligent threat detection systems are becoming foundational technologies for securing digitally transformed enterprises.

Key Technology & Innovation Trends in Global Digital Transformation Market

- Generative AI Integration: Automating enterprise content creation, workflow intelligence, and business augmentation.

- Cloud-Native Enterprise Platforms: Delivering scalable and flexible digital infrastructure modernization.

- Low-Code and No-Code Platforms: Accelerating digital application deployment and process innovation.

- Intelligent Process Automation: Streamlining repetitive workflows through AI-powered automation.

- Edge Computing Solutions: Enabling real-time processing and decentralized digital intelligence.

- Digital Twin Technologies: Supporting virtual simulation and operational optimization.

- Hyperautomation Frameworks: Combining AI, RPA, and analytics for enterprise-wide automation.

- Zero-Trust Cybersecurity Architectures: Strengthening digital resilience and enterprise security.

- API-Driven Integration Platforms: Enabling seamless interoperability across enterprise ecosystems.

- Predictive Analytics Engines: Enhancing strategic decision-making through data intelligence.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the digital transformation market by shifting competition from basic digitization toward intelligent, autonomous, and adaptive enterprise ecosystems.

Organizations investing in AI-driven automation, cloud-native infrastructure, and advanced data intelligence platforms are achieving stronger competitive differentiation through improved productivity, faster innovation cycles, and enhanced customer experiences.

The growing convergence of digital technologies is enabling enterprises to improve operational agility, strengthen business continuity, and unlock new revenue models.

Advanced automation and intelligent orchestration are helping organizations reduce operational complexity while improving process accuracy and responsiveness.

However, integration complexity with legacy systems, cybersecurity vulnerabilities, workforce skill gaps, and high implementation costs remain significant challenges for large-scale digital transformation adoption.

Global Digital Transformation Market Technology & Innovation Forward Outlook

The future of digital transformation technology is expected to evolve toward fully autonomous, AI-orchestrated, and self-optimizing enterprise ecosystems capable of enabling predictive business operations and continuous adaptive innovation.

Emerging innovations include autonomous enterprise platforms, self-learning process automation systems, quantum-ready computing frameworks, immersive digital collaboration environments, and intelligent digital assistants.

Digital twin ecosystems are expected to become more advanced, enabling enterprise-wide simulation for strategic planning and operational optimization.

Decentralized cloud architectures and distributed intelligence frameworks are likely to strengthen enterprise resilience and operational scalability.

Federated AI models may further enhance secure cross-enterprise intelligence sharing while preserving organizational data privacy.

Overall, the global digital transformation market is evolving toward a highly intelligent technology ecosystem combining predictive analytics, autonomous automation, secure cloud-native infrastructure, and connected digital intelligence to redefine enterprise innovation, customer engagement, and operational excellence worldwide.

Market Risk

Global Digital Transformation Market Risk Factors & Disruption Threats Overview

The global digital transformation market is witnessing exceptional growth as enterprises across industries accelerate cloud migration, artificial intelligence adoption, process automation, and digital-first business modernization. Despite its robust expansion trajectory, the market faces significant risks and disruption threats related to cybersecurity vulnerabilities, implementation complexity, legacy system constraints, skills shortages, regulatory uncertainty, and rapidly evolving technology landscapes.

One of the most critical risks impacting the digital transformation market is cybersecurity exposure. As organizations digitize operations and increase connectivity across enterprise ecosystems, the attack surface for cyber threats expands significantly. Ransomware attacks, data breaches, supply chain cyberattacks, and identity-based threats can severely disrupt transformation initiatives.

Legacy infrastructure modernization remains a major challenge. Many enterprises continue to operate on outdated systems that are costly and complex to integrate with modern cloud-native platforms, often delaying transformation outcomes.

High implementation costs and uncertain return on investment create financial risks, particularly for mid-sized organizations with limited transformation budgets.

A growing shortage of skilled digital talent???including cloud architects, AI engineers, cybersecurity specialists, and automation experts???continues to constrain execution capacity across markets.

Regulatory complexity is another substantial disruption factor. Data privacy laws, cross-border data transfer restrictions, industry-specific compliance frameworks, and AI governance regulations create operational uncertainty for multinational digital transformation projects.

Additionally, rapid technological innovation is increasing the risk of platform obsolescence, making long-term technology investment decisions increasingly complex.

Global Digital Transformation Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by aggressive enterprise cloud adoption, increased generative AI experimentation, and rising investments in intelligent automation across sectors.

At the same time, cybersecurity incidents affecting digitally connected enterprises are increasing globally, driving stronger focus on zero-trust security architectures.

Many organizations continue to face challenges in scaling pilot digital transformation initiatives into enterprise-wide operational deployments.

The growing pace of AI innovation is creating uncertainty regarding platform selection, governance frameworks, and long-term strategic alignment.

Budget scrutiny is intensifying as organizations seek measurable business outcomes from large-scale transformation investments.

Competition is increasing rapidly as global technology providers, cloud hyperscalers, consulting firms, and specialized transformation vendors expand their service portfolios.

Global Digital Transformation Market Key Risk Factors & Disruption Threat Signals

- Cybersecurity Vulnerabilities: Rising exposure to ransomware, data breaches, and digital infrastructure attacks.

- Legacy System Constraints: Integration challenges with outdated enterprise technology infrastructure.

- High Transformation Costs: Significant capital and operational expenditure requirements.

- Digital Skills Shortage: Limited availability of qualified transformation and AI specialists.

- Regulatory Uncertainty: Evolving data privacy, AI governance, and cross-border compliance requirements.

- Technology Obsolescence: Rapid innovation cycles reducing long-term platform viability.

- Change Management Resistance: Internal organizational resistance slowing transformation adoption.

- Vendor Lock-In Risks: Dependence on proprietary cloud and software ecosystems.

- Uncertain ROI Measurement: Difficulty quantifying transformation outcomes and business value.

- Operational Disruption During Migration: Risk of downtime and workflow interruption during implementation.

Strategic Implications of Risk Factors

Organizations must prioritize cybersecurity-by-design strategies, integrating zero-trust frameworks and continuous digital risk monitoring into transformation initiatives.

Modernization roadmaps should emphasize phased migration approaches to reduce operational disruption and improve integration success with legacy environments.

Investing in workforce upskilling, digital talent acquisition, and cross-functional transformation governance will be essential for execution success.

Vendor diversification and open architecture strategies can reduce lock-in risk and improve long-term technology flexibility.

Strong transformation governance frameworks focused on measurable business outcomes will become increasingly critical for sustaining executive and investor confidence.

Global Digital Transformation Market Forward Risk Outlook

Between 2026 and 2033, digital transformation will continue reshaping global enterprise operations, but risk complexity will increase as organizations integrate generative AI, autonomous systems, edge intelligence, and decentralized digital infrastructure.

Future disruption is likely to emerge from accelerated AI regulation, quantum-era cybersecurity threats, platform consolidation, and shifting enterprise technology standards.

Organizations unable to build agile, secure, and adaptive transformation strategies may face reduced competitiveness and innovation stagnation.

The strongest opportunities will emerge for enterprises and technology providers delivering secure, interoperable, AI-enabled, and outcome-driven transformation ecosystems.

Long-term market leadership will depend on balancing technological innovation with operational resilience, cybersecurity excellence, regulatory readiness, and organizational agility.

Regulatory Landscape

Global Digital Transformation Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global digital transformation market is shaped by data protection laws, cybersecurity regulations, cloud governance frameworks, artificial intelligence oversight policies, digital infrastructure modernization programs, and cross-border data transfer regulations. As digital transformation becomes central to enterprise competitiveness and public sector modernization, regulatory oversight is expanding to ensure secure, ethical, resilient, and compliant digital ecosystems.

Digital transformation initiatives involving cloud computing, artificial intelligence, IoT, advanced analytics, automation, and digital platforms are increasingly subject to regulatory requirements related to privacy, operational security, algorithmic accountability, and technology governance.

The accelerating deployment of AI-driven systems, distributed cloud architectures, and connected digital infrastructures is driving policymakers to establish clearer compliance frameworks that address digital trust, operational resilience, responsible innovation, and data sovereignty.

Global Digital Transformation Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for digital transformation is characterized by growing global policy activity aimed at balancing innovation with security, privacy, and ethical technology deployment.

In North America, digital transformation regulation is influenced by cybersecurity standards, sector-specific privacy requirements, cloud compliance mandates, and emerging AI governance frameworks. The United States continues to strengthen digital resilience policies across enterprise and public infrastructure sectors.

In Europe, digital transformation initiatives are governed by robust frameworks including GDPR, the Digital Operational Resilience Act (DORA), AI Act regulations, cybersecurity directives, and cloud compliance requirements that strongly shape enterprise modernization strategies.

Asia-Pacific nations including China, India, Japan, South Korea, and Singapore are accelerating digital governance development through national digital infrastructure programs, cybersecurity laws, cloud localization requirements, and AI regulatory frameworks.

Emerging economies across Latin America, the Middle East, and Africa are implementing digital modernization policies and regulatory reforms to support cloud adoption, smart infrastructure deployment, and digital economy expansion.

Key Regulatory & Policy Environment Signals in Global Digital Transformation Market

- Data Privacy and Protection Regulations: Expanding privacy laws are shaping enterprise digital architecture, customer data handling, and compliance strategies.

- Cybersecurity Compliance Standards: Organizations must comply with increasingly stringent operational security and resilience mandates.

- AI Governance Frameworks: Emerging regulations are addressing transparency, accountability, fairness, and risk management in AI deployment.

- Cloud Governance and Data Sovereignty: National policies are influencing cloud deployment models, localization requirements, and infrastructure strategies.

- Cross-Border Data Transfer Controls: Regulatory restrictions are impacting multinational digital transformation initiatives and global data operations.

- Digital Infrastructure Modernization Policies: Government-led digital transformation programs are accelerating enterprise technology adoption across sectors.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging organizations to prioritize compliance-by-design strategies when implementing cloud, AI, automation, and analytics platforms.

Regulatory pressure is accelerating investment in zero-trust cybersecurity architectures, compliance automation tools, governance frameworks, and secure digital infrastructure modernization.

AI oversight requirements are driving demand for explainable AI systems, transparent algorithmic governance, and responsible innovation frameworks.

Cloud compliance and data localization requirements are influencing infrastructure deployment decisions, encouraging hybrid cloud strategies and regional data center expansion.

International regulatory divergence is increasing complexity for global enterprises, making digital compliance management a critical strategic capability.

Global Digital Transformation Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global digital transformation market is expected to become significantly more structured, technology-specific, and globally influential.

Governments are likely to introduce stronger regulations governing AI ethics, autonomous systems accountability, digital operational resilience, and algorithm transparency.

Cybersecurity and critical infrastructure protection requirements are expected to intensify as digital transformation expands across highly sensitive industries.

Cross-border digital governance frameworks may evolve further, although regional differences in data sovereignty and cloud policy will continue to shape global deployment strategies.

Overall, regulatory and policy developments will remain a major market influence, with organizations investing in compliant digital architectures, secure transformation frameworks, and governance-driven innovation expected to maintain long-term competitive advantage.