Global Hydraulics Market Report, Size & Forecast 2026-2033

Global Hydraulics Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 42.8 Billion |

| Market Size (2033) | USD 67.9 Billion |

| CAGR (2026???2033) | 5.9% |

| Largest Segment | Hydraulic Equipment & Components |

| Fastest Growing Segment | Electro-Hydraulic Systems |

| Leading Application | Construction and Heavy Equipment Machinery |

| Key Growth Driver | Increasing industrial automation and rising demand for heavy construction equipment |

| Key Technology Trends | Electro-hydraulic technologies, IoT-enabled condition monitoring, energy-efficient hydraulic systems, smart fluid power solutions |

| Major End-Use Industries | Construction, Agriculture, Manufacturing, Aerospace, Mining, Marine, Automotive, Energy |

| Key Market Opportunity | Expansion of industrial automation and infrastructure development projects |

| Regional Leader | Asia-Pacific |

| Fastest Growing Region | Middle East & Africa |

| Sustainability & Innovation Focus | Development of energy-efficient hydraulic systems, predictive maintenance technologies, and intelligent motion control solutions |

Global Hydraulics Market Size & Forecast

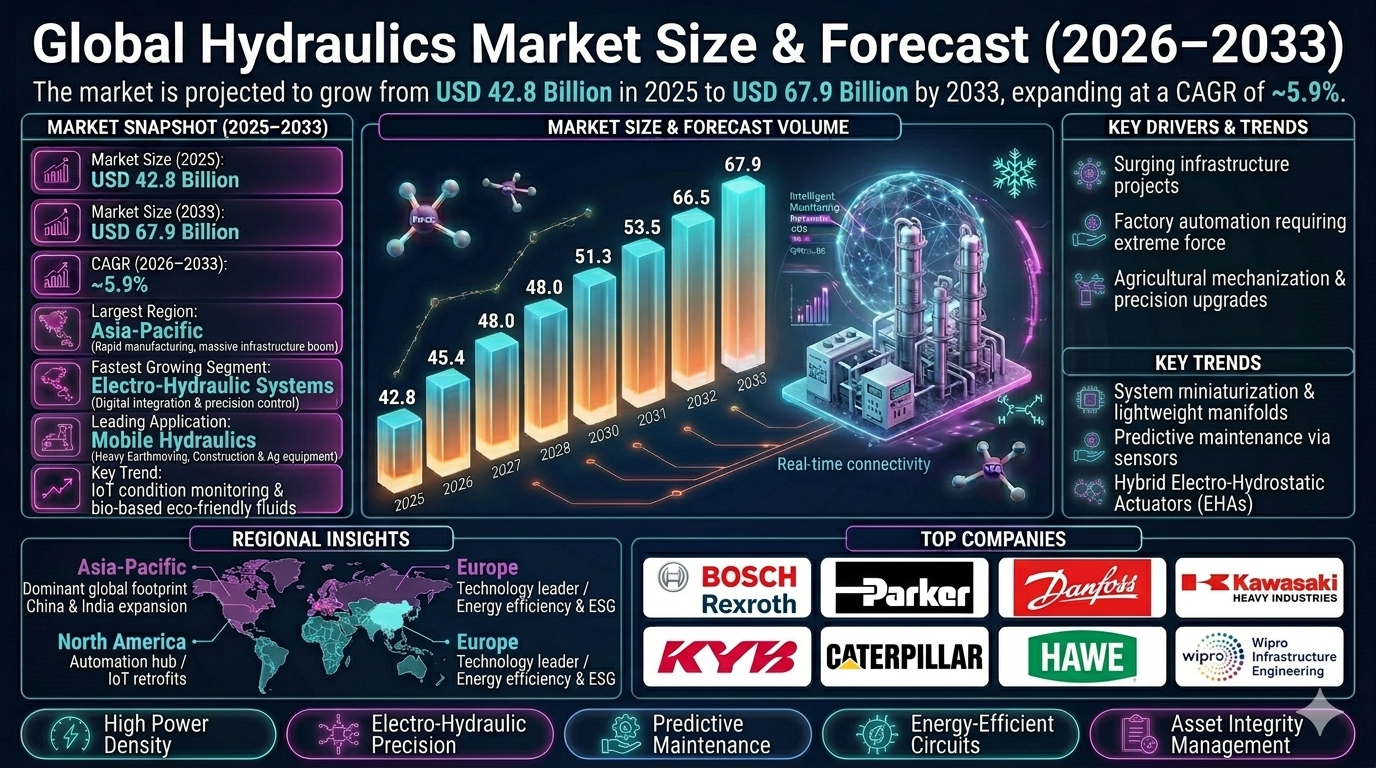

The global hydraulics market is projected to witness significant growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 42.8 billion in 2025 and is expected to reach nearly USD 67.9 billion by 2033, expanding at a CAGR of around 5.9%.

The market growth is driven by increasing industrial automation, rising demand for heavy construction equipment, expanding manufacturing activities, and growing investments in advanced fluid power systems across industrial and mobile applications. Hydraulic systems use pressurized fluid to generate, control, and transmit power for machinery and equipment. These systems are widely utilized across construction, agriculture, aerospace, mining, marine, automotive, manufacturing, and energy industries due to their high power density, operational precision, and reliability. The market is experiencing significant transformation through the integration of electro-hydraulic technologies, IoT-enabled condition monitoring, energy-efficient hydraulic systems, and advanced smart fluid power solutions. Additionally, rising infrastructure development, industrial modernization, and the increasing need for efficient motion control systems are accelerating market expansion globally.

Global Hydraulics Market Overview

The hydraulics market forms a critical segment of the global fluid power and industrial machinery industry. Hydraulic systems are essential for heavy-duty motion control applications requiring force amplification, precision control, and high operational efficiency. The market includes hydraulic pumps, motors, cylinders, valves, accumulators, reservoirs, filtration systems, and electro-hydraulic control systems. Manufacturers are increasingly focusing on system miniaturization, digital control integration, predictive maintenance capabilities, and energy-efficient hydraulic architecture. Technological innovation in proportional control valves, variable displacement pumps, intelligent actuators, and digital hydraulic systems is reshaping the industry landscape. Major market participants include Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation, Danfoss Power Solutions, Kawasaki Heavy Industries, KYB Corporation, Caterpillar Inc., HAWE Hydraulik, Wipro Infrastructure Engineering, and HYDAC International.Key Drivers of Global Hydraulics Market Growth

Growing Construction and Infrastructure Development

Rapid urbanization and large-scale infrastructure projects are driving strong demand for hydraulic-powered construction equipment such as excavators, loaders, cranes, and lifting systems. This is significantly boosting market growth worldwide.Rising Industrial Automation

Industries are increasingly deploying hydraulic systems for automated manufacturing processes, material handling, and industrial machinery applications. Hydraulics offer superior force control and precision for complex automation tasks.Increasing Demand in Agricultural Equipment

Modern agricultural machinery relies heavily on hydraulic systems for steering, lifting, harvesting, and precision farming operations. Mechanization in agriculture is driving market expansion.Technological Advancements in Electro-Hydraulic Systems

The integration of electronics, sensors, and digital controls is improving hydraulic system performance, monitoring, and energy efficiency. Smart hydraulics are enhancing predictive maintenance and operational reliability.Expansion of Renewable Energy Applications

Hydraulic technologies are increasingly used in wind turbines, hydroelectric systems, and industrial energy management applications. This is creating new growth opportunities for the market.Global Hydraulics Market Segmentation

By Component

The market is segmented into pumps, motors, cylinders, valves, accumulators, filters, reservoirs, and accessories. Hydraulic pumps account for a major market share due to their critical role in system performance.By Type

The market includes open-loop hydraulics, closed-loop hydraulics, and electro-hydraulic systems. Electro-hydraulic systems are witnessing rapid growth due to digital integration advantages.By Application

Applications include mobile hydraulics, industrial hydraulics, aerospace hydraulics, marine hydraulics, and specialized hydraulic systems. Mobile hydraulics dominate the market due to extensive use in construction and agricultural equipment.By End User

End users include construction, agriculture, manufacturing, mining, aerospace, marine, automotive, and energy sectors. Construction remains the dominant end-user segment globally.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global hydraulics market due to rapid industrialization, infrastructure expansion, and growing manufacturing activities. China, India, Japan, and South Korea are major regional contributors. China remains the largest market due to its extensive construction and industrial machinery sectors.North America

North America holds a significant market share supported by advanced manufacturing infrastructure, automation adoption, and strong construction activity. The United States leads regional market growth.Europe

Europe remains a key market driven by industrial automation, advanced machinery manufacturing, and sustainability-focused hydraulic innovation. Germany, France, and Italy are major contributors.Middle East & Africa

The Middle East is witnessing growth due to infrastructure development, mining activity, and energy sector investments. Saudi Arabia and the UAE are leading regional markets.Latin America

Latin America is gradually expanding due to growing mining operations, agricultural mechanization, and industrial modernization. Brazil and Mexico are key regional contributors.Competitive Landscape

The global hydraulics market is highly competitive, with major players competing through product innovation, system efficiency, digital integration, and aftermarket service capabilities. Key companies include Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation, Danfoss Power Solutions, Kawasaki Heavy Industries, KYB Corporation, Caterpillar Inc., HAWE Hydraulik, Wipro Infrastructure Engineering, and HYDAC International. Companies are increasingly investing in smart hydraulic technologies, lightweight system designs, energy-efficient components, and connected diagnostics platforms. Strategic partnerships with OEMs and industrial automation providers are strengthening market positioning.Strategic Outlook

The strategic outlook for the global hydraulics market remains highly positive due to increasing industrial automation and infrastructure investments. Future growth opportunities include intelligent hydraulic systems, digital fluid power management, predictive maintenance analytics, and electrified hydraulic solutions. Growing emphasis on energy efficiency, system reliability, and operational intelligence will significantly shape future market evolution. Manufacturers investing in electro-hydraulic integration, digital diagnostics, and advanced material engineering are expected to strengthen competitive advantage.Final Market Perspective

The global hydraulics market remains essential to industrial productivity, heavy machinery performance, and advanced motion control applications worldwide. Rising construction activity, industrial automation, agricultural mechanization, and technological advancements will continue driving market growth throughout the forecast period. Organizations that successfully combine engineering innovation, digital integration, and operational efficiency will remain strongly positioned in the evolving global hydraulics market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Hydraulics Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Hydraulic Systems

- 2.2 Scope of the Study

- 2.3 Evolution of Fluid Power Technologies

- 2.4 Hydraulic Value Chain & Ecosystem

- 2.5 Raw Materials & Component Supply Landscape

- 2.6 Regulatory & Energy Efficiency Standards

- 2.7 Technology Innovation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Growing Construction & Infrastructure Development

- 4.1.2 Rising Industrial Automation

- 4.1.3 Increasing Demand in Agricultural Equipment

- 4.1.4 Technological Advancements in Electro-Hydraulic Systems

- 4.1.5 Expansion of Renewable Energy Applications

- 4.2 Restraints

- 4.2.1 High Maintenance & Operational Costs

- 4.2.2 Oil Leakage & Environmental Concerns

- 4.2.3 Volatility in Raw Material Prices

- 4.2.4 Complexity of System Integration

- 4.3 Opportunities

- 4.3.1 Intelligent Hydraulic Monitoring Systems

- 4.3.2 Electrified Hydraulic Solutions

- 4.3.3 Digital Predictive Maintenance Platforms

- 4.3.4 Lightweight & Energy-Efficient Hydraulic Components

- 4.4 Challenges

- 4.4.1 Energy Losses in Conventional Systems

- 4.4.2 Skilled Workforce Shortages

- 4.4.3 Transition to Sustainable Fluid Technologies

- 4.4.4 Competition from Electric Actuation Systems

- 4.1 Drivers

- 5. Global Hydraulics Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Production & Consumption Analysis

- 5.5 Technology Adoption Trends

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Component

- 6.1.1 Hydraulic Pumps

- 6.1.2 Hydraulic Motors

- 6.1.3 Hydraulic Cylinders

- 6.1.4 Hydraulic Valves

- 6.1.5 Accumulators

- 6.1.6 Filters

- 6.1.7 Reservoirs

- 6.1.8 Accessories

- 6.2 By Type

- 6.2.1 Open-Loop Hydraulics

- 6.2.2 Closed-Loop Hydraulics

- 6.2.3 Electro-Hydraulic Systems

- 6.3 By Application

- 6.3.1 Mobile Hydraulics

- 6.3.2 Industrial Hydraulics

- 6.3.3 Aerospace Hydraulics

- 6.3.4 Marine Hydraulics

- 6.3.5 Specialized Hydraulic Systems

- 6.4 By End User

- 6.4.1 Construction

- 6.4.2 Agriculture

- 6.4.3 Manufacturing

- 6.4.4 Mining

- 6.4.5 Aerospace

- 6.4.6 Marine

- 6.4.7 Automotive

- 6.4.8 Energy

- 6.1 By Component

- 7. Market Segmentation by Geography

- 7.1 Asia-Pacific

- 7.2 North America

- 7.3 Europe

- 7.4 Middle East & Africa

- 7.5 Latin America

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Technology Innovation Analysis

- 8.4 Strategic Partnerships & Acquisitions

- 8.5 Digital Transformation & Sustainability Strategies

- 9. Company Profiles

- 9.1 Bosch Rexroth AG

- 9.2 Parker Hannifin Corporation

- 9.3 Eaton Corporation

- 9.4 Danfoss Power Solutions

- 9.5 Kawasaki Heavy Industries

- 9.6 KYB Corporation

- 9.7 Caterpillar Inc.

- 9.8 HAWE Hydraulik

- 9.9 Wipro Infrastructure Engineering

- 9.10 HYDAC International

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Hydraulic Demand Forecast Engine

- 10.2 Industrial Equipment Utilization Analyzer

- 10.3 Smart Fluid Power Monitoring Tracker

- 10.4 Energy Efficiency Optimization Dashboard

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Electro-Hydraulic Solutions

- 11.2 Investment in Predictive Maintenance Platforms

- 11.3 Development of Sustainable Hydraulic Fluids

- 11.4 Integration of Digital Diagnostics & IoT Systems

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Hydraulics Market Competitive Intensity & Market Structure Overview

The global hydraulics market is highly competitive and moderately consolidated, characterized by the presence of established fluid power manufacturers, industrial automation companies, and specialized hydraulic system providers competing on engineering innovation, product efficiency, digital integration, reliability, and aftermarket service capabilities.

The market structure consists of multinational hydraulic component manufacturers, integrated industrial equipment suppliers, OEM-focused solution providers, and regional hydraulic technology specialists. Competitive positioning is shaped by product performance, technological advancement, customization capabilities, service network reach, and strategic partnerships with industrial machinery manufacturers.

Growing industrial automation, rising infrastructure development, expanding mobile equipment demand, and increasing adoption of intelligent electro-hydraulic systems are intensifying competition across the global hydraulics market.

Global Hydraulics Market Competitive Intensity & Market Structure Current Scenario

Leading Global Hydraulics Companies

Bosch Rexroth AG: Global leader in hydraulic drive and control technologies with strong expertise in industrial automation and digital fluid power systems.

Parker Hannifin Corporation: Major hydraulic solutions provider offering a broad portfolio of motion and control technologies across industrial and mobile applications.

Eaton Corporation: Prominent player known for advanced hydraulic components, energy-efficient systems, and integrated fluid power solutions.

Danfoss Power Solutions: Leading provider of mobile and industrial hydraulic systems focused on digitalization and electrified fluid power technologies.

Kawasaki Heavy Industries: Significant manufacturer recognized for high-performance hydraulic pumps, motors, and industrial motion control systems.

KYB Corporation: Strong global participant specializing in hydraulic equipment for automotive, construction, and industrial machinery applications.

Caterpillar Inc.: Major integrated equipment manufacturer with strong hydraulic system capabilities supporting heavy machinery operations.

HAWE Hydraulik: Specialized hydraulic technology company known for precision-engineered compact hydraulic solutions.

Wipro Infrastructure Engineering: Important regional hydraulic systems provider with expanding global manufacturing presence.

HYDAC International: Established hydraulic engineering company focused on filtration, fluid management, and intelligent hydraulic monitoring systems.

Key Competitive Intensity & Market Structure Drivers

The growing adoption of industrial automation and smart manufacturing systems is increasing demand for digitally integrated hydraulic technologies.

Rapid infrastructure development and expanding construction equipment demand are intensifying competition in mobile hydraulic system innovation.

Technological advancements in electro-hydraulic controls, variable displacement systems, and predictive maintenance capabilities are creating strong product differentiation opportunities.

Energy efficiency regulations and sustainability initiatives are driving investment in low-energy hydraulic architectures and intelligent fluid management systems.

The increasing need for customized hydraulic solutions across agriculture, mining, aerospace, and marine industries is encouraging product specialization.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly investing in electro-hydraulic integration and smart digital control systems to improve system precision and operational efficiency.

Strategic partnerships with OEMs, automation platform providers, and heavy equipment manufacturers are becoming critical for market expansion.

Aftermarket service capabilities, predictive diagnostics, and condition monitoring platforms are emerging as major competitive differentiators.

Investment in lightweight materials, compact system design, and advanced fluid engineering is helping manufacturers improve system performance and efficiency.

Digital transformation through IoT-enabled monitoring, remote diagnostics, and AI-based maintenance analytics is reshaping long-term competitive strategies.

Global Hydraulics Market Competitive Intensity & Market Structure Forward Outlook

The global hydraulics market is expected to remain highly competitive as industries increasingly prioritize automation, energy efficiency, and intelligent motion control systems.

Future competition will focus on electro-hydraulic innovation, digital fluid power management, autonomous machinery integration, and predictive system optimization.

Asia-Pacific is expected to remain the dominant competitive growth region due to rapid industrialization and infrastructure expansion, while North America and Europe will lead advanced hydraulic technology innovation.

Electrification trends, AI-powered monitoring systems, and sustainable fluid power technologies are expected to significantly reshape market dynamics.

Overall, companies that successfully combine engineering excellence, digital innovation, operational reliability, and advanced service ecosystems will remain strongly positioned in the evolving global hydraulics market.

Value Chain

Global Hydraulics Market Value Chain & Supply Chain Evolution Overview

The global hydraulics market value chain is evolving rapidly as industrial automation, infrastructure modernization, advanced machinery manufacturing, and digital fluid power innovation reshape the broader motion control and industrial equipment ecosystem. Hydraulic systems remain foundational to heavy-duty power transmission and motion control applications, enabling efficient force generation, operational precision, and high-performance functionality across construction, manufacturing, agriculture, mining, aerospace, marine, and energy sectors.

The hydraulics value chain spans raw material sourcing, component manufacturing, precision engineering, system assembly, digital integration, OEM equipment deployment, aftermarket servicing, and lifecycle performance optimization. This interconnected ecosystem includes metal and alloy suppliers, seal and fluid manufacturers, electronics developers, hydraulic component manufacturers, industrial machinery OEMs, systems integrators, maintenance providers, and industrial end-users.

Major companies including Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation, Danfoss Power Solutions, Kawasaki Heavy Industries, KYB Corporation, Caterpillar Inc., HAWE Hydraulik, Wipro Infrastructure Engineering, and HYDAC International are investing heavily in electro-hydraulic integration, intelligent control systems, predictive diagnostics, lightweight system architecture, and energy-efficient hydraulic technologies to strengthen market leadership.

Upstream supply chain operations depend on specialty steel production, precision machining materials, hydraulic fluids, elastomer seals, filtration media, sensors, semiconductors, and industrial electronics. Midstream activities focus on hydraulic pump and valve manufacturing, system design, software integration, actuator assembly, testing, and quality assurance. Downstream operations include equipment integration, field installation, maintenance services, system upgrades, and operational monitoring.

Operational priorities across the hydraulics value chain increasingly emphasize energy efficiency, precision control, system reliability, digital diagnostics, modular scalability, and predictive maintenance integration. However, the market continues to face challenges related to raw material cost fluctuations, system complexity, hydraulic fluid sustainability concerns, integration with electrified systems, and increasing pressure for lower-emission industrial solutions.

Global Hydraulics Market Value Chain & Supply Chain Evolution Current Scenario

The current hydraulics market is being shaped by expanding infrastructure development, accelerating industrial automation, increased agricultural mechanization, and rising demand for digitally integrated heavy machinery systems. Industries are increasingly upgrading conventional hydraulic architectures with electro-hydraulic controls and intelligent monitoring systems to improve efficiency and reduce operational downtime.

Asia-Pacific currently dominates the global hydraulics market due to rapid industrialization, large-scale construction activity, growing manufacturing output, and strong machinery production capabilities. China remains the largest regional market supported by robust construction equipment demand and industrial modernization initiatives.

North America maintains a strong market position due to advanced manufacturing infrastructure, significant automation deployment, and sustained investment in construction and agricultural equipment modernization. Europe continues to emphasize energy-efficient hydraulic innovation, precision machinery engineering, and sustainable industrial automation systems.

Manufacturers are increasingly integrating IoT sensors, digital pressure monitoring systems, variable displacement technologies, and cloud-connected diagnostics platforms into hydraulic solutions to improve operational intelligence and lifecycle performance.

The market is also witnessing increasing demand for compact and lightweight hydraulic systems designed for advanced mobile applications, robotics integration, and hybrid industrial machinery platforms.

Key Value Chain & Supply Chain Evolution Signals in Global Hydraulics Market

One of the most significant transformation signals is the rapid shift toward electro-hydraulic systems. The integration of electronics and hydraulic power is enabling improved control precision, energy optimization, and enhanced operational responsiveness across industrial and mobile applications.

Another major signal is the increasing deployment of IoT-enabled condition monitoring solutions. Connected hydraulic systems equipped with smart sensors are enabling predictive maintenance, real-time diagnostics, and remote performance monitoring.

Energy efficiency has become a defining market trend. Manufacturers are increasingly developing variable speed drives, load-sensing systems, and optimized fluid control architectures to reduce energy consumption and improve operational sustainability.

Advanced material engineering is also reshaping the value chain. Lightweight alloys, advanced sealing materials, and improved filtration technologies are enhancing system durability while reducing equipment weight and maintenance frequency.

The convergence of hydraulics with automation and robotics is creating new market opportunities, particularly in advanced manufacturing environments requiring precise force control and integrated digital operation.

Sustainability pressures are driving increased interest in biodegradable hydraulic fluids, low-leakage designs, and environmentally optimized fluid power systems.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Hydraulics Market

Leading hydraulic system manufacturers are increasingly prioritizing digital integration, energy-efficient system architecture, and intelligent diagnostics capabilities to maintain competitive advantage. Competitive differentiation increasingly depends on system performance, reliability, operational intelligence, and lifecycle cost efficiency.

Companies capable of delivering integrated electro-hydraulic solutions with predictive maintenance capabilities are expected to capture premium growth opportunities as industries prioritize operational uptime and intelligent automation.

Strategic partnerships between hydraulic component manufacturers, industrial automation providers, machinery OEMs, and software platform developers are becoming increasingly important for improving interoperability and accelerating innovation deployment.

Aftermarket service capabilities are emerging as a critical strategic differentiator. Companies offering remote diagnostics, predictive servicing, digital monitoring subscriptions, and lifecycle optimization support are strengthening long-term customer relationships.

Sustainability-focused product innovation is becoming increasingly important as industrial operators seek lower-emission equipment, improved fluid efficiency, and environmentally responsible hydraulic systems.

Regional manufacturing localization strategies are also gaining momentum as companies seek to improve supply chain resilience, reduce lead times, and strengthen responsiveness to local industrial demand.

Global Hydraulics Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the hydraulics value chain is expected to become significantly more intelligent, digitally connected, and energy-efficient. Electro-hydraulic architectures will continue replacing conventional systems across industrial and mobile equipment platforms.

Advanced digital diagnostics and AI-powered predictive maintenance systems are expected to become standard across next-generation hydraulic systems, enabling autonomous performance optimization and failure prevention.

Smart fluid power management platforms integrating cloud analytics, edge computing, and real-time system optimization will increasingly enhance operational efficiency and reduce lifecycle costs.

Material innovation will continue improving hydraulic component performance through lighter alloys, advanced coatings, and high-durability sealing technologies that enhance reliability under extreme operating conditions.

Electrification trends across industrial and mobile equipment will accelerate hybrid hydraulic system development, enabling stronger integration between electric drive systems and fluid power architectures.

Sustainable hydraulic technologies including biodegradable fluids, low-loss circuit designs, and energy recovery systems will gain increasing importance as environmental standards continue to evolve.

Ultimately, the future hydraulics value chain will evolve into a digitally intelligent, highly efficient, and environmentally optimized motion control ecosystem capable of supporting advanced industrial automation, infrastructure development, and precision machinery applications globally.

Market-Specific Value Chain

- Raw Material & Component Inputs: Specialty steel, precision alloys, hydraulic fluids, seals, filtration materials, sensors, semiconductors, and industrial electronics.

- Hydraulic Component Manufacturing: Pumps, motors, cylinders, valves, accumulators, filtration systems, reservoirs, and precision fluid control devices.

- System Engineering & Digital Integration: Electro-hydraulic controls, software integration, embedded electronics, smart sensing systems, and predictive diagnostics architecture.

- OEM Equipment Integration: Construction machinery, agricultural equipment, industrial automation systems, aerospace systems, marine applications, and mining machinery integration.

- Deployment, Monitoring & Aftermarket Services: Installation, field calibration, predictive maintenance, digital monitoring, remote diagnostics, and service lifecycle management.

- Advanced Performance Optimization: AI-driven system optimization, energy recovery systems, sustainability-focused fluid technologies, and intelligent fluid power management.

Company-to-Stage Mapping

- Raw Material & Component Inputs: Specialty metal suppliers, hydraulic fluid manufacturers, industrial electronics producers, seal technology developers.

- Hydraulic Component Manufacturing: Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation, Danfoss Power Solutions, HYDAC International.

- System Engineering & Digital Integration: HAWE Hydraulik, Kawasaki Heavy Industries, smart control system developers, industrial automation software firms.

- OEM Equipment Integration: Caterpillar Inc., agricultural equipment OEMs, aerospace manufacturers, industrial machinery builders.

- Deployment, Monitoring & Aftermarket Services: Wipro Infrastructure Engineering, service integrators, predictive maintenance platform providers.

- Advanced Performance Optimization: AI analytics providers, electro-hydraulic technology innovators, sustainable fluid engineering companies.

Investment Activity

Global Hydraulics Market Investment & Funding Dynamics Overview

Investment activity in the global hydraulics market is accelerating steadily due to increasing industrial automation, expanding infrastructure development, rising demand for advanced heavy machinery systems, and growing adoption of electro-hydraulic technologies. Between 2026 and 2033, capital allocation is expected to increasingly target smart hydraulic systems, digital fluid power technologies, predictive maintenance platforms, energy-efficient hydraulic components, and advanced motion control infrastructure.

The hydraulics market represents a strategically vital segment of the global industrial machinery and fluid power ecosystem. Industrial equipment manufacturers, automation technology providers, infrastructure investors, private equity firms, and engineering solution providers are increasing investments to improve operational efficiency, enhance system intelligence, and strengthen equipment performance capabilities.

A major structural transformation shaping investment dynamics is the transition from conventional mechanical hydraulic systems toward digitally integrated electro-hydraulic architectures. This shift is driving substantial funding into sensor-enabled control systems, AI-driven diagnostics, connected hydraulic platforms, and intelligent energy optimization technologies.

The market is also benefiting from rising investments in industrial automation modernization, lightweight hydraulic component engineering, smart actuator systems, and sustainable fluid power technologies. Increasing emphasis on operational precision, reduced energy consumption, and predictive asset management is reshaping long-term capital deployment strategies.

Current Investment & Funding Landscape

Current funding activity in the hydraulics market is strongly supported by heavy equipment modernization programs, manufacturing automation investments, smart construction equipment development, and industrial digitalization initiatives. Companies are actively investing in electro-hydraulic integration, digital monitoring systems, advanced fluid control technologies, and energy-efficient hydraulic infrastructure.

- Asia-Pacific: Dominates global investment activity due to rapid industrialization, expanding construction equipment production, and large-scale infrastructure development projects.

- North America: Witnessing strong capital deployment driven by industrial automation upgrades, advanced manufacturing systems, and construction equipment modernization.

- Europe: Attracting substantial funding focused on energy-efficient hydraulic innovation, digital fluid power systems, and precision engineering advancements.

- Middle East & Latin America: Emerging as growing investment regions supported by mining activity, infrastructure projects, and industrial equipment expansion.

Key Investment & Funding Drivers

- Growing construction and infrastructure development is increasing investment in advanced mobile hydraulic systems.

- Industrial automation trends are driving funding for intelligent hydraulic motion control solutions.

- Rising agricultural mechanization is supporting hydraulic equipment modernization investments.

- Electro-hydraulic system adoption is accelerating digital integration-focused capital allocation.

- Demand for predictive maintenance capabilities is increasing investments in connected diagnostics platforms.

- Energy efficiency initiatives are driving funding for low-consumption hydraulic architectures.

- Renewable energy equipment applications are creating new hydraulic technology investment opportunities.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of combining hydraulic engineering excellence with digital control intelligence.

- Technology leadership in electro-hydraulic integration is becoming a critical competitive differentiator.

- OEM partnerships and industrial automation collaborations are strengthening investment attractiveness.

- Companies investing in lightweight, energy-efficient hydraulic systems are expected to achieve stronger market positioning.

- Digital service capabilities and predictive maintenance ecosystems are becoming central to long-term investor confidence.

- Regional diversification strategies remain essential for balancing industrial demand exposure and infrastructure growth opportunities.

- Organizations integrating hydraulics into broader smart machinery ecosystems are likely to capture higher long-term value.

Forward Investment Outlook

The global hydraulics market is expected to maintain strong long-term investment momentum due to rising industrial modernization, expanding automation deployment, and increasing demand for intelligent motion control systems.

Future funding activity is expected to prioritize digital hydraulic control platforms, AI-powered predictive diagnostics, electro-hydraulic actuator systems, smart fluid management technologies, and sustainable hydraulic energy optimization solutions.

- Asia-Pacific: Will remain the leading investment hub due to continued industrial expansion and infrastructure-intensive economic growth.

- North America: Will strengthen its position through advanced automation integration and smart heavy equipment innovation.

- Europe: Will continue emphasizing sustainability-driven hydraulic innovation and precision engineering leadership.

Future innovation investments are also expected across autonomous hydraulic systems, digital twin-enabled fluid power monitoring, advanced material engineering, electrified hydraulic systems, and fully connected machine intelligence platforms.

The convergence of industrial automation, digital engineering, and sustainable equipment innovation will continue reshaping investment priorities across the hydraulics market.

Overall, the market is expected to remain a highly attractive long-term industrial investment opportunity as hydraulics continue to serve as a foundational technology for modern machinery, infrastructure development, and precision industrial motion control worldwide.

Technology & Innovation

Global Hydraulics Market Technology & Innovation Landscape Overview

The Global Hydraulics Market is undergoing rapid technological transformation driven by advancements in electro-hydraulic systems, digital control technologies, intelligent sensors, and energy-efficient fluid power solutions. The industry is increasingly integrating smart monitoring systems, automation capabilities, and connected hydraulic architectures to improve operational efficiency, system precision, reliability, and predictive maintenance capabilities across industrial and mobile applications.

Hydraulic system innovation is focused on enhancing energy efficiency, reducing system complexity, improving motion control accuracy, and enabling real-time performance diagnostics. Manufacturers are increasingly investing in intelligent fluid power technologies to address evolving industrial automation requirements and sustainability objectives.

The growing adoption of Industry 4.0, industrial IoT, advanced control software, and data-driven maintenance systems is reshaping hydraulic system design and operational performance across construction, manufacturing, agriculture, aerospace, mining, and energy sectors.

Global Hydraulics Market Technology & Innovation Current Scenario

Currently, the hydraulics market is witnessing significant innovation through the integration of electro-hydraulic systems that combine traditional hydraulic power with advanced electronic controls for greater responsiveness, precision, and operational efficiency.

IoT-enabled hydraulic monitoring systems are increasingly being deployed to enable real-time system diagnostics, pressure monitoring, temperature analysis, and predictive maintenance planning. These connected systems help reduce downtime and improve equipment lifecycle performance.

Variable displacement pumps and proportional control valves are gaining widespread adoption due to their ability to optimize fluid flow and reduce energy consumption across dynamic operational conditions.

Digital hydraulic control systems are improving machine intelligence by enabling precise motion control, automated adjustments, and system-level optimization in industrial machinery and mobile equipment.

Advanced hydraulic filtration technologies and contamination monitoring systems are also being increasingly adopted to improve fluid cleanliness, extend component lifespan, and enhance overall system reliability.

Additionally, lightweight hydraulic materials, compact actuator designs, and low-noise hydraulic components are gaining importance as manufacturers focus on system miniaturization and improved equipment performance.

Key Technology & Innovation Trends in Global Hydraulics Market

- Electro-Hydraulic Integration: Combining hydraulic power with digital electronics for improved control precision and responsiveness.

- IoT-Enabled Condition Monitoring: Real-time diagnostics for predictive maintenance and operational optimization.

- Variable Displacement Pump Technology: Energy-efficient pump systems adjusting flow according to operational requirements.

- Digital Hydraulic Control Systems: Intelligent software-driven control for enhanced automation and precision.

- Smart Hydraulic Sensors: Pressure, temperature, and flow monitoring sensors enabling real-time performance analysis.

- Proportional and Servo Valve Innovation: Advanced valve technologies delivering precise motion and force control.

- Predictive Maintenance Analytics: AI-driven maintenance systems minimizing unplanned equipment failures.

- Energy-Efficient Hydraulic Architecture: Low-loss designs reducing power consumption and improving sustainability.

- Lightweight Hydraulic Components: Advanced material engineering reducing system weight without compromising performance.

- Digital Twin Hydraulic Simulation: Virtual system modeling for design optimization and operational forecasting.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping the competitive dynamics of the hydraulics market by shifting industry focus toward intelligent, connected, and energy-efficient fluid power systems.

Manufacturers investing in electro-hydraulic integration, smart diagnostics, and digital control technologies are achieving stronger market differentiation through improved operational performance, lower maintenance costs, and enhanced system reliability.

The integration of predictive analytics and real-time condition monitoring is enabling end users to optimize maintenance schedules, reduce equipment downtime, and improve asset utilization across industrial operations.

Energy-efficient hydraulic solutions are also becoming strategically important as industries increasingly prioritize sustainability, lower emissions, and reduced operational energy consumption.

However, challenges including high implementation costs, system integration complexity, cybersecurity concerns, and compatibility with legacy hydraulic infrastructure remain key barriers to large-scale technology adoption.

Global Hydraulics Market Technology & Innovation Forward Outlook

Looking ahead, the hydraulics market is expected to evolve toward highly intelligent, fully connected, and digitally optimized fluid power ecosystems capable of autonomous performance adjustment and predictive operational control.

Future innovations will increasingly focus on AI-powered hydraulic optimization, self-diagnosing systems, autonomous fluid management, and adaptive electro-hydraulic architectures capable of real-time efficiency tuning.

Digital twin integration is expected to play a growing role in hydraulic system design, simulation, predictive maintenance planning, and operational optimization.

Advanced materials and additive manufacturing technologies are likely to support the development of lighter, more durable, and highly efficient hydraulic components.

Electrified hydraulic systems and hybrid fluid power technologies are also expected to gain momentum as industries transition toward lower-emission machinery and sustainable industrial operations.

Overall, the Global Hydraulics Market is entering a new era of smart fluid power innovation characterized by digital intelligence, predictive diagnostics, energy optimization, and enhanced system automation, positioning hydraulics as a critical enabler of next-generation industrial performance.

Market Risk

Global Hydraulics Market Risk Factors & Disruption Threats Overview

The global hydraulics market continues to expand due to rising industrial automation, growing infrastructure development, increasing construction activity, and strong demand for advanced motion control systems across multiple industries. Despite favorable long-term growth prospects, the market faces several structural risks and disruption threats related to technological shifts, raw material volatility, electrification trends, environmental regulations, and operational complexity.

One of the most significant risks affecting the hydraulics market is the increasing shift toward electromechanical and fully electric actuation systems. In applications where energy efficiency, precision, and reduced maintenance are prioritized, electric alternatives are increasingly replacing conventional hydraulic systems, particularly in automation and compact industrial machinery.

Raw material cost volatility represents another major challenge. Hydraulic components depend heavily on steel, aluminum, specialty alloys, seals, and fluid materials, all of which are exposed to fluctuating global commodity prices and supply chain instability.

Environmental regulations related to hydraulic fluid leakage, emissions reduction, and energy efficiency are also becoming increasingly stringent. Manufacturers must invest in eco-friendly hydraulic fluids, leak-proof system designs, and more energy-efficient architectures to maintain compliance.

System maintenance complexity and fluid contamination risks remain ongoing operational concerns. Hydraulic systems require regular maintenance, leak prevention, fluid cleanliness management, and skilled servicing, which can increase lifecycle costs for end users.

Digital transformation presents both opportunity and disruption risk. As smart diagnostics, IoT-enabled condition monitoring, and predictive maintenance systems become standard, manufacturers that fail to integrate digital capabilities may lose competitive relevance.

Additionally, global economic cycles and capital expenditure fluctuations in construction, mining, agriculture, and industrial manufacturing can significantly impact hydraulic equipment demand.

Global Hydraulics Market Risk Factors & Disruption Threats Current Scenario

The current hydraulics market is experiencing strong demand from infrastructure projects, industrial automation upgrades, and agricultural mechanization initiatives across major economies.

Electro-hydraulic systems are gaining traction as manufacturers seek to combine hydraulic power density with digital precision and energy optimization.

However, increasing competition from electric actuation technologies is influencing design decisions in several industrial applications, particularly in sectors focused on sustainability and compact automation.

Supply chain challenges affecting semiconductors, industrial metals, seals, and electronic control components are creating production delays and pricing pressure for hydraulic system manufacturers.

Rising energy efficiency regulations are encouraging innovation in variable-speed drives, smart pump systems, and low-leakage hydraulic architectures.

The market is also seeing increased investment in condition monitoring platforms and predictive maintenance analytics, reshaping service expectations across industrial users.

Global Hydraulics Market Key Risk Factors & Disruption Threat Signals

- Electromechanical Substitution: Growing adoption of electric actuation systems replacing hydraulic solutions.

- Raw Material Cost Volatility: Fluctuating prices of metals, seals, and specialty materials.

- Environmental Compliance Pressure: Stricter fluid leakage and energy efficiency regulations.

- Maintenance Complexity: High servicing requirements increasing lifecycle operational costs.

- Fluid Contamination Risks: Performance degradation caused by contamination and system leakage.

- Supply Chain Disruptions: Delays in industrial components and electronic control systems.

- Digital Integration Gaps: Slow adoption of IoT-enabled monitoring reducing competitiveness.

- Capital Spending Cyclicality: Economic downturns impacting heavy equipment procurement.

- Skilled Labor Shortages: Limited technical expertise for advanced hydraulic servicing.

- Competitive Pricing Pressure: Increasing rivalry among global fluid power manufacturers.

Strategic Implications of Risk Factors

Hydraulic system manufacturers must prioritize energy-efficient system design and electro-hydraulic integration to address growing competition from electric actuation technologies.

Investment in predictive maintenance capabilities, IoT-enabled monitoring, and intelligent diagnostics will become essential to improve customer value and operational reliability.

Manufacturers should strengthen supply chain resilience through diversified sourcing strategies and localized production capabilities to mitigate raw material and component disruptions.

Development of environmentally friendly hydraulic fluids, leak-resistant designs, and low-energy consumption systems will support regulatory compliance and sustainability positioning.

Strategic collaboration with OEMs, automation solution providers, and industrial digitalization partners will be increasingly important for maintaining technological leadership.

Global Hydraulics Market Forward Risk Outlook

Looking ahead to 2026???2033, the hydraulics market will remain essential across heavy-duty industrial and mobile applications but will increasingly evolve toward digitally connected and energy-optimized solutions.

Electro-hydraulic systems, smart fluid power architectures, and AI-enabled condition monitoring are expected to become major differentiators across the market.

Manufacturers that fail to adapt to electrification trends, sustainability demands, and digital service expectations may face declining competitiveness.

Regions with strong infrastructure development, manufacturing modernization, and industrial automation investments are expected to offer the strongest long-term growth opportunities.

Overall, sustained market leadership will depend on engineering innovation, digital transformation, operational efficiency, and adaptability to evolving industrial motion control requirements.

Regulatory Landscape

Global Hydraulics Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global hydraulics market is shaped by industrial machinery safety regulations, environmental compliance standards, energy efficiency mandates, workplace safety frameworks, and equipment performance certification requirements. Hydraulic systems are critical components across industrial, construction, agricultural, aerospace, marine, and manufacturing applications, making regulatory oversight essential for operational reliability, worker safety, and environmental protection.

Governments and industry regulatory bodies worldwide enforce stringent standards for hydraulic equipment design, fluid containment, pressure system integrity, emissions reduction, and operational safety. These policies directly influence hydraulic component manufacturing, deployment practices, maintenance standards, and lifecycle performance management.

The increasing global emphasis on sustainability, industrial efficiency, and equipment digitization is accelerating regulatory focus on energy-efficient hydraulic systems, environmentally safe hydraulic fluids, leak prevention technologies, and smart condition monitoring integration.

Global Hydraulics Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for the hydraulics market combines industrial machinery safety standards with evolving environmental regulations focused on energy consumption, fluid leakage prevention, and sustainable industrial operations.

In North America, hydraulic system regulations are governed by organizations such as the Occupational Safety and Health Administration (OSHA), Environmental Protection Agency (EPA), and American Society of Mechanical Engineers (ASME). Compliance requirements cover pressure vessel standards, fluid safety, equipment reliability, and industrial operational safety.

Europe maintains one of the most stringent regulatory frameworks through the Machinery Directive, Pressure Equipment Directive (PED), Restriction of Hazardous Substances (RoHS), and REACH environmental compliance regulations. These standards drive adoption of safer, more efficient, and environmentally sustainable hydraulic technologies.

Asia-Pacific countries including China, Japan, South Korea, and India are strengthening industrial machinery certification standards and environmental compliance requirements to support manufacturing modernization and infrastructure development.

Emerging markets across Latin America, the Middle East, and Africa are increasingly adopting international industrial machinery and hydraulic safety standards to improve infrastructure reliability and attract industrial investments.

Key Regulatory & Policy Environment Signals in Global Hydraulics Market

- Industrial Machinery Safety Standards: Mandatory compliance for hydraulic system pressure control, mechanical integrity, and worker protection continues to drive product innovation.

- Environmental Fluid Regulations: Restrictions on hazardous hydraulic fluids are increasing demand for biodegradable and environmentally safer hydraulic oils.

- Energy Efficiency Requirements: Regulatory emphasis on reducing industrial energy consumption is encouraging adoption of high-efficiency hydraulic systems.

- Leak Prevention and Containment Standards: Stricter fluid leakage prevention requirements are accelerating demand for advanced sealing and monitoring solutions.

- Digital Equipment Monitoring Policies: Smart industrial monitoring regulations are encouraging integration of predictive maintenance and IoT-enabled diagnostics.

- Equipment Certification Requirements: International certification standards are increasingly becoming mandatory for global market access.

Strategic Implications of Regulatory & Policy Environment

Regulatory developments are encouraging hydraulic system manufacturers to prioritize product innovation, operational efficiency, and compliance-driven engineering design. Companies are increasingly investing in energy-efficient pumps, intelligent control systems, and environmentally friendly hydraulic fluid technologies.

Stringent environmental and leak prevention standards are accelerating adoption of advanced sealing systems, predictive maintenance sensors, and real-time monitoring platforms. These technologies improve operational reliability while ensuring regulatory compliance.

Safety-focused regulatory requirements are also increasing demand for precision-engineered pressure control systems and automated shutdown mechanisms, particularly across high-risk industrial and construction environments.

The global shift toward industrial digitization is creating opportunities for smart electro-hydraulic systems equipped with diagnostics, analytics, and remote monitoring capabilities aligned with digital compliance frameworks.

Global Hydraulics Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global hydraulics market is expected to become increasingly focused on energy optimization, environmental sustainability, digital monitoring integration, and operational safety modernization.

Governments are likely to introduce stricter fluid disposal regulations, stronger equipment efficiency standards, and enhanced industrial machinery safety requirements. These changes will accelerate demand for eco-friendly hydraulic fluids and energy-efficient hydraulic architectures.

Digital compliance frameworks will increasingly encourage adoption of IoT-enabled predictive maintenance, remote system diagnostics, and automated condition monitoring for hydraulic infrastructure.

Industrial decarbonization initiatives and sustainability policies will further support the transition toward electro-hydraulic solutions, low-energy fluid power systems, and lightweight high-performance hydraulic components.

Overall, regulatory and policy developments will remain a major growth catalyst for the hydraulics market, with companies investing in intelligent system design, sustainable fluid technologies, and advanced compliance-ready hydraulic solutions expected to maintain long-term competitive advantage.