Global New Energy Vehicles (NEV) Market Report, Size, Share and Forecast 2026–2033

Global New Energy Vehicles (NEV) Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

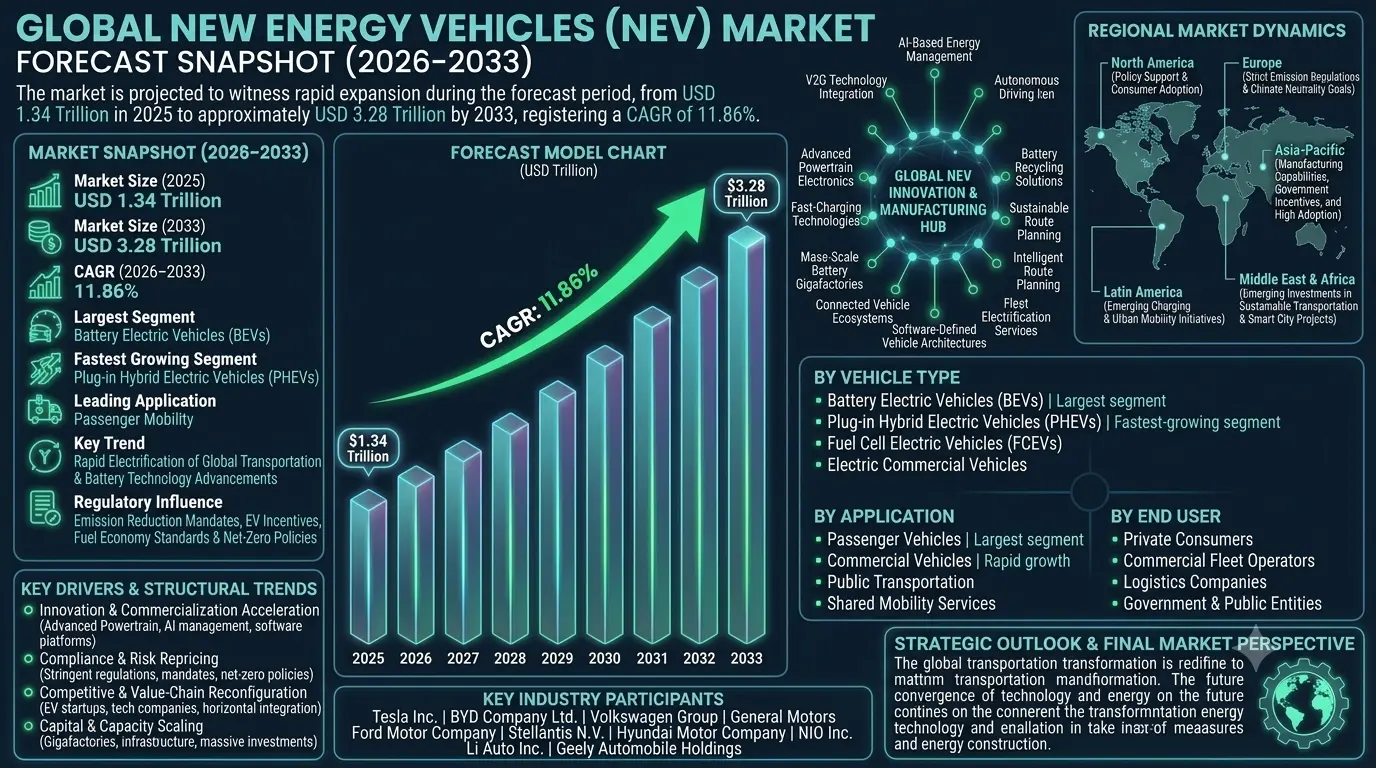

| Market Size (2025) | USD 1.34 Trillion |

| Market Size (2033) | USD 3.28 Trillion |

| CAGR (2026???2033) | 11.86% |

| Largest Segment | Battery Electric Vehicles (BEVs) |

| Fastest Growing Segment | Plug-in Hybrid Electric Vehicles (PHEVs) |

| Leading Application | Passenger Mobility |

| Key Trend | Rapid Electrification of Global Transportation & Battery Technology Advancements |

| Regulatory Influence | Emission Reduction Mandates, EV Incentives, Fuel Economy Standards & Net-Zero Policies |

| Future Outlook | Growth Driven by EV Infrastructure Expansion, Battery Innovation & Government Electrification Policies |

Global New Energy Vehicles (NEV) Market Size & Forecast

The Global New Energy Vehicles (NEV) Market is expected to witness rapid expansion during the forecast period from 2026 to 2033. The market was valued at USD 1.34 trillion in 2025 and is projected to reach approximately USD 3.28 trillion by 2033, registering a CAGR of 11.86%. The market growth is primarily driven by accelerating global decarbonization efforts, rising fuel prices, government EV incentives, and increasing consumer shift toward sustainable mobility solutions. New Energy Vehicles include battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and fuel cell electric vehicles (FCEVs), all of which are contributing to the transition away from internal combustion engine (ICE) vehicles. Expanding charging infrastructure, advancements in lithium-ion and solid-state batteries, and increasing investments from automakers are further accelerating market growth.

Global NEV Market Overview

New Energy Vehicles (NEVs) are automobiles powered partially or fully by electricity and alternative energy sources, designed to reduce carbon emissions and dependency on fossil fuels. The market includes battery electric cars, plug-in hybrids, electric buses, electric trucks, fuel cell vehicles, and associated charging and battery ecosystem services. NEVs are widely adopted across passenger transportation, commercial fleets, logistics, public transit systems, and shared mobility platforms. The market is transitioning from early-stage adoption to mass-market penetration driven by technological maturity and regulatory support.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid advancements in battery energy density, fast-charging technologies, power electronics, and electric drivetrains are transforming the NEV ecosystem. Automakers are increasingly integrating AI-based energy management systems and software-defined vehicle architectures.Market Implications

Companies investing in battery innovation, EV platforms, and intelligent mobility systems are expected to strengthen global leadership.2. Compliance and Risk Repricing

Stringent emission regulations, zero-emission vehicle mandates, carbon taxation policies, and fuel efficiency standards are driving NEV adoption worldwide. Governments are implementing aggressive electrification targets for public transport and commercial fleets.Market Implications

Firms aligning with sustainability regulations and producing compliant zero-emission vehicles are likely to gain stronger market advantage.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as traditional automakers, EV startups, and technology companies compete for dominance across the electric mobility value chain. Battery manufacturing, charging infrastructure, and software ecosystems are becoming critical competitive differentiators.Market Implications

Companies with strong vertical integration across battery, software, and vehicle manufacturing may gain long-term market control.4. Capital and Capacity Scaling

Massive investments in EV manufacturing plants, battery gigafactories, and global charging infrastructure are accelerating market expansion. Governments and private investors are heavily funding electrification projects worldwide.Market Implications

Organizations scaling production capacity and global supply chains are expected to capture future demand surges.Market Segmentation Analysis

By Vehicle Type

1. Battery Electric Vehicles (BEVs)

Largest segment driven by zero-emission policies and declining battery costs.2. Plug-in Hybrid Electric Vehicles (PHEVs)

Fastest-growing segment offering flexible transition from ICE to full EV adoption.3. Fuel Cell Electric Vehicles (FCEVs)

Emerging segment supported by hydrogen infrastructure development.4. Electric Commercial Vehicles

Strong adoption in logistics, delivery, and public transport fleets.By Application

1. Passenger Vehicles

Largest segment due to mass consumer adoption and government incentives.2. Commercial Vehicles

Rapid growth driven by fleet electrification and logistics transformation.3. Public Transportation

Increasing deployment of electric buses in urban mobility systems.4. Shared Mobility Services

Growing integration of EVs in ride-hailing and car-sharing platforms.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global NEV market due to strong manufacturing capabilities, government incentives, and high EV adoption rates, particularly in China.Europe

Europe is a major market driven by strict emission regulations and aggressive climate neutrality goals.North America

North America is witnessing strong growth due to policy support, infrastructure expansion, and increasing consumer adoption.Latin America

Latin America is gradually expanding due to improving charging infrastructure and urban mobility initiatives.Middle East & Africa

The region is emerging with growing investments in sustainable transportation and smart city projects.Competitive Landscape

The Global NEV Market is highly competitive with automakers, battery manufacturers, and technology firms expanding aggressively worldwide.Key Companies Operating in the Market Include:

- Tesla Inc.

- BYD Company Ltd.

- Volkswagen Group

- General Motors

- Ford Motor Company

- Stellantis N.V.

- Hyundai Motor Company

- NIO Inc.

- Li Auto Inc.

- Geely Automobile Holdings

Strategic Outlook

The future of the NEV market will be shaped by battery innovation, charging infrastructure expansion, autonomous driving integration, and software-defined vehicle ecosystems. Solid-state batteries, ultra-fast charging networks, and vehicle-to-grid (V2G) technologies will significantly enhance efficiency and adoption. The shift toward electrified, connected, and autonomous mobility is expected to redefine the global automotive industry.Final Market Perspective

The Global New Energy Vehicles Market stands at the center of the global transportation transformation. Rising environmental concerns, policy mandates, and technological breakthroughs continue to drive long-term exponential growth. Companies capable of delivering scalable, affordable, and high-performance electric mobility solutions will be best positioned to capture future opportunities. The convergence of electrification, digitalization, and energy transition is expected to reshape the future of global transportation systems.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global New Energy Vehicles (NEV) Market Snapshot (2026???2033)

- 1.2 Market Size & Growth Overview

- 1.3 Key Market Highlights

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Performance Summary

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Market Introduction & Overview

- 2.1 Definition of New Energy Vehicles (NEV)

- 2.2 Scope of the Global NEV Market

- 2.3 Evolution of Electric Mobility

- 2.4 NEV Value Chain Analysis

- 2.5 Regulatory & Policy Framework

- 2.6 Role of NEVs in Global Decarbonization

- 2.7 Transition from ICE Vehicles to Electric Mobility

- 3. Research Methodology

- 3.1 Primary Research Approach

- 3.2 Secondary Research Sources

- 3.3 Market Size Estimation Methodology

- 3.4 Forecasting Assumptions (2026???2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Market Drivers

- 4.1.1 Rapid Electrification of Global Transportation

- 4.1.2 Advancements in Battery Technology

- 4.1.3 Government EV Incentives & Subsidies

- 4.1.4 Rising Fuel Prices & Energy Transition

- 4.1.5 Expansion of Charging Infrastructure

- 4.2 Market Restraints

- 4.2.1 High Initial Cost of EVs

- 4.2.2 Limited Charging Infrastructure in Emerging Regions

- 4.2.3 Battery Raw Material Supply Constraints

- 4.3 Market Opportunities

- 4.3.1 Development of Solid-State Batteries

- 4.3.2 Growth in EV Fleet Electrification

- 4.3.3 Expansion of Smart Mobility Services

- 4.3.4 Integration of Vehicle-to-Grid (V2G) Systems

- 4.4 Market Challenges

- 4.4.1 Battery Recycling & Sustainability Issues

- 4.4.2 Supply Chain Volatility for Critical Minerals

- 4.4.3 Standardization of Charging Systems

- 4.1 Market Drivers

- 5. Global New Energy Vehicles (NEV) Market Size & Forecast (USD Trillion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Demand & Adoption Trends

- 5.4 Pricing Analysis

- 5.5 Investment Trends

- 5.6 Future Market Outlook

- 6. Market Segmentation Analysis (2026???2033)

- 6.1 By Vehicle Type

- 6.1.1 Battery Electric Vehicles (BEVs) (Largest Segment)

- 6.1.2 Plug-in Hybrid Electric Vehicles (PHEVs) (Fastest-Growing Segment)

- 6.1.3 Fuel Cell Electric Vehicles (FCEVs)

- 6.1.4 Electric Commercial Vehicles

- 6.2 By Application

- 6.2.1 Passenger Vehicles (Largest Segment)

- 6.2.2 Commercial Vehicles

- 6.2.3 Public Transportation

- 6.2.4 Shared Mobility Services

- 6.1 By Vehicle Type

- 7. Regional Market Analysis

- 7.1 Asia-Pacific (Largest Market)

- 7.2 Europe

- 7.3 North America

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Competitive Benchmarking

- 8.3 Strategic Developments

- 8.4 EV Innovation & Technology Strategies

- 8.5 Partnerships, Expansion & Investment Analysis

- 9. Company Profiles

- 9.1 Tesla Inc.

- 9.2 BYD Company Ltd.

- 9.3 Volkswagen Group

- 9.4 General Motors

- 9.5 Ford Motor Company

- 9.6 Stellantis N.V.

- 9.7 Hyundai Motor Company

- 9.8 NIO Inc.

- 9.9 Li Auto Inc.

- 9.10 Geely Automobile Holdings

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 NEV Demand Forecast Model

- 10.2 Battery Technology Adoption Analysis

- 10.3 Charging Infrastructure Growth Tracker

- 10.4 EV Ecosystem Competitiveness Assessment

- 10.5 Porter???s Five Forces Analysis (Automated Insight Model)

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of EV Infrastructure

- 11.2 Growth of Solid-State Battery Technology

- 11.3 Acceleration of Fleet Electrification

- 11.4 Integration of Autonomous & Connected Mobility

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Market Research

- 14. Disclaimer

Competitive Landscape

Global New Energy Vehicles (NEV) Market Competitive Intensity & Market Structure Overview

The Global New Energy Vehicles (NEV) market is highly competitive and rapidly evolving, characterized by intense rivalry among traditional automotive OEMs, dedicated electric vehicle manufacturers, battery technology leaders, and emerging mobility technology firms. Competition is primarily driven by technological innovation, cost efficiency in battery production, software capabilities, supply chain control, and global manufacturing scale.

Market participants are increasingly shifting from conventional vehicle manufacturing to integrated mobility ecosystems that combine electric drivetrains, battery technologies, charging infrastructure, autonomous driving capabilities, and connected vehicle software platforms. This transition is redefining competitive boundaries across the global automotive industry.

The competitive structure is transitioning from traditional OEM dominance toward a dual-layer ecosystem dominated by vertically integrated EV leaders and software-driven mobility companies. Strategic alliances, joint ventures, and battery partnerships are becoming critical for maintaining competitive positioning.

Global NEV Market Competitive Intensity & Current Market Structure

Leading Global NEV Manufacturers & Ecosystem Players

Tesla Inc.: A global leader in electric mobility and software-defined vehicles, known for its strong battery technology integration, autonomous driving capabilities, and direct-to-consumer business model.

BYD Company Ltd.: A dominant player in both electric passenger and commercial vehicles with strong vertical integration across batteries, EV platforms, and energy solutions.

Volkswagen Group: A traditional automotive giant transitioning aggressively into electric mobility with large-scale EV platform investments and global electrification strategy.

General Motors: A key North American OEM focusing on electric trucks, SUVs, and next-generation EV platforms under its Ultium battery architecture.

Ford Motor Company: Expanding its EV portfolio with strong focus on electric trucks, commercial EVs, and fleet electrification solutions.

Stellantis N.V.: Leveraging multi-brand strategy to accelerate EV adoption across Europe and North America.

Hyundai Motor Company: Rapidly expanding EV lineup with strong focus on affordability, hydrogen fuel cell technology, and global market penetration.

NIO Inc.: A premium Chinese EV manufacturer focusing on smart mobility, battery swapping technology, and premium EV ecosystems.

Li Auto Inc.: Specializing in extended-range electric vehicles with strong growth in the Chinese EV market.

Geely Automobile Holdings: A diversified automotive group with strong investments in EV brands, smart mobility platforms, and global partnerships.

Key Competitive Drivers in the NEV Market

Battery technology innovation is the most critical competitive factor, with companies racing to improve energy density, reduce charging time, and lower production costs through gigafactory expansion and supply chain optimization.

Software-defined vehicles and AI-powered mobility systems are emerging as key differentiators, enabling advanced features such as autonomous driving, predictive maintenance, and intelligent energy management.

Control over charging infrastructure and energy ecosystems is becoming a strategic advantage, with companies investing heavily in fast-charging networks and vehicle-to-grid integration technologies.

Government policies, emission regulations, and subsidy frameworks are significantly influencing competitive positioning, particularly in Europe, China, and North America.

Strategic partnerships between automakers, battery manufacturers, and technology companies are reshaping the competitive landscape and accelerating innovation cycles.

Strategic Implications of Competitive Intensity

Companies with strong vertical integration across battery production, EV manufacturing, and software ecosystems are expected to dominate long-term market share due to cost advantages and supply chain control.

Investment in next-generation technologies such as solid-state batteries, ultra-fast charging, and autonomous driving systems will be critical for sustaining competitive advantage.

Manufacturers that successfully scale global production while maintaining cost efficiency will be best positioned to capture mass-market EV demand.

Expansion into emerging markets and diversification into commercial EV fleets, logistics, and shared mobility services will further enhance competitive positioning.

Global NEV Market Competitive Outlook

The competitive landscape of the NEV market is expected to intensify significantly over the forecast period, driven by rapid technological disruption, aggressive capital investment, and global electrification policies.

Traditional automakers will continue to face pressure from agile EV startups and technology-driven mobility companies that prioritize software integration and platform-based ecosystems.

Over the forecast period, leadership in the NEV market will be defined by companies that successfully combine battery innovation, scalable manufacturing, intelligent software systems, and global infrastructure integration.

The convergence of electrification, digital transformation, and energy transition will fundamentally reshape the global automotive competitive structure.

Value Chain

Global New Energy Vehicles (NEV) Market Value Chain & Supply Chain Evolution Overview

The Global New Energy Vehicles (NEV) Market is undergoing a fundamental transformation driven by accelerating electrification of transportation, stringent emission reduction mandates, rapid advancements in battery technologies, and large-scale investments in charging infrastructure. The NEV value chain spans raw material sourcing, battery manufacturing, powertrain development, vehicle assembly, software integration, charging infrastructure deployment, distribution, and end-user mobility services. This interconnected ecosystem is reshaping the global automotive industry and redefining mobility systems.

A key characteristic of the NEV value chain is the deep integration of energy systems, semiconductor technologies, battery chemistry innovation, and software-defined vehicle platforms. Automakers and technology companies are increasingly converging to develop intelligent electric mobility solutions supported by AI-driven energy management, connected vehicle systems, and autonomous driving capabilities.

Supply chain complexity is increasing due to heavy dependence on critical raw materials such as lithium, cobalt, nickel, and rare earth elements, along with geopolitical risks, battery manufacturing constraints, and global logistics dependencies. Market participants must coordinate across mining companies, battery manufacturers, EV OEMs, charging infrastructure providers, software developers, and energy utilities while ensuring scalability, cost efficiency, and sustainability compliance.

The industry is experiencing rapid vertical integration, with automakers investing in battery gigafactories, charging networks, and software ecosystems to secure supply chain control and reduce dependency on external suppliers. The value chain is evolving into a digitally connected, energy-integrated, and highly automated mobility ecosystem.

Global NEV Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Material Extraction: Mining of lithium, nickel, cobalt, graphite, and rare earth materials required for battery production.

- Battery Manufacturing: Cell production, battery pack assembly, energy storage optimization, and thermal management systems.

- Powertrain & Component Manufacturing: Electric motors, power electronics, inverters, drivetrains, and semiconductor systems.

- Vehicle Manufacturing & Assembly: Design, chassis integration, EV platform development, and final vehicle assembly.

- Software & Connectivity Integration: Battery management systems (BMS), AI-based energy optimization, infotainment systems, and autonomous driving software.

- Charging Infrastructure & Energy Systems: Fast-charging networks, home charging solutions, grid integration, and vehicle-to-grid (V2G) systems.

- Distribution & Mobility Services: Dealership networks, direct-to-consumer sales, fleet leasing, ride-hailing integration, and subscription-based mobility models.

- End User Utilization: Passenger vehicles, commercial fleets, public transportation systems, and shared mobility platforms.

Company-to-Stage Mapping

- Raw Material Extraction: Albemarle Corporation, SQM, Glencore, CATL supply partners, and global mining companies.

- Battery Manufacturing: CATL, LG Energy Solution, Panasonic Energy, BYD, Samsung SDI.

- Powertrain & Component Manufacturing: Bosch, Denso, Hitachi Astemo, Infineon Technologies, and EV component suppliers.

- Vehicle Manufacturing & Assembly: Tesla, BYD, Volkswagen Group, General Motors, Ford, Hyundai Motor Company.

- Software & Connectivity Integration: Tesla software division, NVIDIA, Qualcomm, Mobileye, and automotive OS developers.

- Charging Infrastructure & Energy Systems: ChargePoint, Tesla Supercharger Network, ABB, Siemens, Shell Recharge.

- Distribution & Mobility Services: OEM dealer networks, fleet operators, Uber, Lyft, leasing companies, and EV subscription platforms.

- End User Utilization: Private consumers, commercial logistics fleets, public transport agencies, and shared mobility users.

Key Value Chain & Supply Chain Evolution Signals in Global NEV Market

Expansion of Battery Gigafactories

Massive investments in gigafactories are increasing global battery production capacity, reducing costs, and improving supply chain localization.

Acceleration of Vertical Integration by Automakers

Automakers are increasingly controlling battery production, software systems, and charging infrastructure to secure competitive advantage.

Advancement in Solid-State and Next-Gen Batteries

Next-generation battery technologies are improving energy density, safety, and charging speed, reshaping EV performance benchmarks.

Rapid Expansion of Charging Infrastructure Networks

Global deployment of fast-charging and ultra-fast charging stations is reducing range anxiety and supporting mass EV adoption.

Integration of AI and Software-Defined Vehicles

AI-powered energy management, predictive maintenance, and autonomous driving systems are transforming vehicle intelligence.

Increasing Dependence on Critical Raw Material Supply Chains

Supply chain risks related to lithium, cobalt, and nickel sourcing are driving investments in recycling and alternative chemistries.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Battery Technology and Energy Storage

Companies investing in advanced battery chemistries, recycling technologies, and gigafactory expansion will secure long-term competitive advantage.

Strengthening Vertical Integration Across EV Ecosystem

Control over batteries, software, and charging infrastructure will become a key differentiator in global NEV competitiveness.

Expansion of Charging and Energy Infrastructure

Scaling fast-charging networks and grid integration systems will be critical to supporting mass EV adoption.

Optimization of Global Supply Chain Resilience

Diversification of raw material sourcing and regionalized production hubs will reduce geopolitical and logistics risks.

Integration of AI and Digital Mobility Platforms

AI-driven vehicle intelligence and connected mobility ecosystems will significantly enhance operational efficiency and user experience.

Growth of Circular Economy and Battery Recycling Systems

Battery recycling and second-life battery applications will become essential for sustainable supply chain development.

Global NEV Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the NEV value chain is expected to evolve into a fully integrated, electrified, and software-defined mobility ecosystem powered by advanced battery technologies, renewable energy integration, and intelligent transportation systems.

Key Future Developments Include:

- Mass adoption of solid-state batteries and next-generation energy storage systems.

- Expansion of global ultra-fast charging infrastructure networks.

- Increased integration of autonomous driving and AI-powered mobility systems.

- Strengthening of battery recycling and circular supply chain models.

- Greater convergence between automotive, energy, and technology sectors.

- Expansion of vehicle-to-grid (V2G) and smart energy ecosystem integration.

As the market evolves, competitive advantage will increasingly depend on control over battery supply chains, software ecosystems, manufacturing scale, and energy infrastructure integration within a unified mobility platform.

Companies that successfully integrate advanced battery technologies, vertically aligned supply chains, AI-driven vehicle intelligence, and global charging infrastructure will achieve strong long-term positioning in the Global New Energy Vehicles Market.

Investment Activity

Global New Energy Vehicles (NEV) Market Investment & Funding Dynamics Overview

The Global New Energy Vehicles (NEV) Market is witnessing unprecedented investment momentum driven by accelerating electrification of transportation, global decarbonization policies, and rapid advancements in battery and charging technologies. Governments, automotive manufacturers, energy companies, and institutional investors are significantly increasing capital allocation toward EV manufacturing infrastructure, battery gigafactories, charging networks, and smart mobility ecosystems.

Investment activity is being fueled by the transition from internal combustion engines (ICE) to electric mobility platforms, supported by strong policy incentives, emission regulations, and consumer demand for sustainable transportation solutions.

Global NEV Market Investment & Funding Dynamics Current Scenario

Currently, the NEV industry is experiencing massive capital inflows across the entire value chain. Leading automotive OEMs and technology firms are investing heavily in electric vehicle platforms, lithium-ion and solid-state battery development, software-defined vehicle systems, and AI-driven mobility solutions.

Venture capital and private equity funding are actively targeting EV startups, charging infrastructure providers, and battery technology innovators. Strategic partnerships between automakers, energy companies, and technology firms are accelerating commercialization and global expansion.

Additionally, governments worldwide are deploying large-scale funding programs for charging infrastructure development, public transport electrification, and clean energy integration, further strengthening market growth.

Key Investment & Funding Dynamics Signals in Global NEV Market

- Rapid expansion of EV charging infrastructure networks is attracting large-scale infrastructure investments.

- Strong capital inflows into battery innovation, including solid-state and fast-charging technologies.

- Increasing investments in software-defined vehicles, AI-based energy management, and autonomous driving systems.

- Growing focus on fleet electrification across logistics, transportation, and public transit sectors.

- Government-backed incentives and subsidies are accelerating EV adoption and manufacturing expansion.

- Strategic collaborations between automakers, energy providers, and technology companies are reshaping industry ecosystems.

- Rising investor interest in vertical integration across battery production, vehicle manufacturing, and software platforms.

Strategic Implications of Investment & Funding Dynamics in Global NEV Market

- Companies investing in battery technology innovation and scalable EV platforms will gain long-term competitive advantage.

- Expansion of charging infrastructure and energy ecosystem integration will be a key determinant of market leadership.

- Automakers with strong vertical integration across hardware, software, and battery systems will dominate future value chains.

- AI-powered mobility solutions and connected vehicle ecosystems will enhance efficiency and profitability.

- Early investment in solid-state batteries and ultra-fast charging technologies will define next-generation competitiveness.

- Regulatory alignment with net-zero policies and emission reduction mandates will drive funding allocation decisions.

- Companies enabling end-to-end electric mobility ecosystems will capture the highest long-term valuation growth.

Global NEV Market Investment & Funding Dynamics Forward Outlook

The future of the Global NEV Market will be shaped by rapid technological innovation, large-scale infrastructure expansion, and increasing integration of digital and energy systems within mobility platforms.

Future investment flows will concentrate on next-generation batteries, autonomous electric vehicles, AI-driven mobility systems, and vehicle-to-grid (V2G) technologies, enabling deeper integration between transportation and energy ecosystems.

As governments continue to enforce aggressive decarbonization targets, investment in EV manufacturing, charging infrastructure, and smart mobility solutions is expected to accelerate significantly.

In conclusion, the NEV market represents a multi-trillion-dollar transformation opportunity where electrification, digitalization, battery innovation, and energy transition technologies will define future capital deployment, competitive advantage, and global transportation infrastructure development.

Technology & Innovation

Global New Energy Vehicles (NEV) Market Technology & Innovation Landscape Overview

The Global New Energy Vehicles (NEV) Market is undergoing a rapid technological transformation driven by advancements in battery chemistry, electric drivetrains, power electronics, vehicle software platforms, autonomous driving systems, and ultra-fast charging infrastructure. The market demonstrates very high innovation intensity as automakers, battery manufacturers, and technology firms compete to redefine global mobility through electrification and digitalization.

At the core of this transformation is the shift from internal combustion engine (ICE) vehicles to fully electrified and software-defined vehicles. This transition is being enabled by breakthroughs in lithium-ion batteries, solid-state battery development, high-efficiency electric motors, and next-generation thermal management systems.

A major innovation area is battery technology advancement, where improvements in energy density, charging speed, lifecycle durability, and cost reduction are significantly enhancing NEV performance and affordability. Solid-state batteries and silicon-anode technologies are emerging as key next-generation breakthroughs.

The market is also witnessing rapid progress in electric drivetrain engineering, including high-efficiency motors, integrated inverter systems, and advanced power electronics that improve vehicle range, acceleration, and energy optimization.

Automakers are increasingly investing in software-defined vehicle architectures, where centralized computing systems, AI-based energy management, predictive diagnostics, and over-the-air (OTA) updates are transforming vehicles into continuously evolving digital platforms.

Charging infrastructure innovation is another critical pillar, including ultra-fast DC charging, wireless charging systems, smart grid integration, and vehicle-to-grid (V2G) technologies that enable two-way energy flow between vehicles and power networks.

Additionally, autonomous driving and advanced driver assistance systems (ADAS) are becoming integral to NEV development, leveraging LiDAR, radar, computer vision, and AI-based perception systems to enhance safety and automation.

Sustainability-focused innovation is also expanding, including battery recycling technologies, green manufacturing processes, lightweight materials, and circular economy strategies aimed at reducing environmental impact across the EV lifecycle.

The convergence of battery innovation, electric drivetrain optimization, AI-powered vehicle systems, charging infrastructure expansion, and autonomous mobility technologies is redefining the future technology landscape of the global NEV market.

Global NEV Market Technology & Innovation Landscape Current Scenario

Currently, the Global NEV Market is characterized by aggressive R&D investment, rapid commercialization of EV platforms, and strong competition across battery, software, and charging ecosystems. Technology convergence is accelerating across automotive and energy sectors.

1. Lithium-Ion & Next-Gen Battery Innovation

Continuous improvements in lithium-ion batteries, including LFP (lithium iron phosphate), NMC (nickel manganese cobalt), and emerging solid-state technologies, are improving energy density, safety, and cost efficiency.

2. Electric Drivetrain Optimization

Integrated motor-inverter systems, high-efficiency power electronics, and multi-speed EV transmissions are improving performance and extending driving range.

3. Software-Defined Vehicles (SDVs)

Vehicles are increasingly built on centralized computing platforms with AI-driven control systems, enabling continuous updates, predictive maintenance, and personalized driving experiences.

4. Fast-Charging & Ultra-Fast Charging Systems

High-power DC charging networks, battery thermal optimization, and high-voltage architectures (800V+ systems) are reducing charging times significantly.

5. Autonomous Driving & ADAS Integration

Advanced sensors, AI perception systems, and real-time mapping technologies are improving vehicle safety and enabling semi-autonomous driving capabilities.

6. Battery Manufacturing & Gigafactory Expansion

Large-scale gigafactories are improving battery supply chain efficiency, reducing costs, and supporting global EV production scaling.

Key Technology & Innovation Landscape Signals in Global NEV Market

Several major technology trends are shaping the NEV industry:

1. Rapid Battery Technology Evolution

Next-generation batteries, including solid-state and sodium-ion technologies, are expected to redefine energy storage performance.

2. Expansion of EV Charging Ecosystems

Ultra-fast charging networks and smart grid integration are becoming critical enablers of large-scale EV adoption.

3. Shift Toward Software-Defined Mobility

Vehicles are evolving into digital platforms with AI-powered systems and continuous feature upgrades via OTA updates.

4. Increasing Vehicle Electrification Across Segments

Electrification is expanding beyond passenger cars into commercial fleets, buses, and logistics vehicles.

5. Integration of AI in Mobility Systems

Artificial intelligence is being used for energy optimization, predictive maintenance, autonomous driving, and user experience personalization.

6. Vertical Integration of EV Supply Chains

Companies are integrating battery production, vehicle manufacturing, and software ecosystems to strengthen competitiveness.

7. Sustainability & Circular Economy Adoption

Battery recycling, second-life battery applications, and sustainable manufacturing practices are gaining importance.

Strategic Implications of Technology & Innovation Landscape in Global NEV Market

The evolving technology landscape is reshaping competition across the NEV industry. Companies are increasingly competing on battery efficiency, software capabilities, charging infrastructure integration, autonomous driving technologies, and ecosystem control.

Automakers investing in battery innovation, gigafactory expansion, AI-powered vehicle platforms, and fast-charging ecosystems are expected to achieve long-term competitive advantage.

Strategic collaborations between automakers, battery manufacturers, energy providers, semiconductor companies, and software developers are accelerating innovation and market expansion.

The convergence of electrification, digital transformation, and energy system integration is creating a highly interconnected mobility ecosystem.

Additionally, regulatory pressures on emissions reduction, fuel economy standards, and net-zero targets are pushing rapid innovation and large-scale adoption of electric mobility solutions.

Global NEV Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026???2033, the Global NEV Market is expected to undergo transformative technological evolution driven by next-generation batteries, autonomous mobility, and fully connected vehicle ecosystems.

Future technological developments are likely to include:

1. Solid-State Battery Commercialization

Solid-state batteries will significantly improve energy density, safety, and charging speed, enabling longer-range EVs.

2. Ultra-Fast Charging Infrastructure Expansion

Megawatt-level charging systems will reduce charging times to minutes, improving EV usability and adoption.

3. Advanced Autonomous Driving Systems

AI-powered full autonomy systems will gradually expand across passenger and commercial vehicles.

4. Vehicle-to-Grid (V2G) Integration

NEVs will increasingly act as distributed energy resources, supporting grid stability and energy storage.

5. Fully Software-Defined EV Ecosystems

Vehicles will operate as continuously upgradable digital platforms with subscription-based features and AI services.

6. Next-Gen Lightweight Materials

Advanced composites and structural battery integration will improve efficiency and vehicle range.

7. Circular Battery Economy

Battery recycling, reuse, and closed-loop manufacturing systems will become industry standards.

In conclusion, companies that successfully integrate battery innovation, software-defined vehicle architecture, charging infrastructure development, autonomous driving technologies, and sustainable manufacturing systems will lead the future evolution of the Global New Energy Vehicles (NEV) Market.

Market Risk

Global New Energy Vehicles (NEV) Market: Risk Factors & Disruption Threats Overview

The Global New Energy Vehicles (NEV) Market is undergoing a rapid structural transformation driven by electrification policies, technological innovation, and large-scale capital investment. While the long-term outlook remains strongly positive, the market is exposed to significant risks arising from supply chain dependencies, technological uncertainty, regulatory volatility, and intense global competition.

One of the most critical risk factors is battery supply chain concentration. The NEV ecosystem is heavily dependent on lithium, nickel, cobalt, and rare earth materials, with limited geographic diversification. Any disruption in mining output, geopolitical restrictions, or export controls can lead to price volatility and production constraints.

Technological uncertainty also represents a major disruption threat. Despite rapid progress in lithium-ion technology, next-generation solutions such as solid-state batteries and alternative chemistries remain under development. Delays in commercialization or performance limitations could impact long-term adoption trajectories and capital investment decisions.

High capital intensity and infrastructure dependency further amplify market risk. The expansion of charging networks, battery gigafactories, and grid modernization requires sustained investment from both public and private sectors. Any slowdown in funding or policy support may hinder market scalability and adoption rates.

Regulatory dependency is another key vulnerability. NEV demand is strongly influenced by emission mandates, subsidies, tax incentives, and net-zero commitments. Sudden policy reversals, subsidy reductions, or inconsistent regulatory frameworks across regions may create demand fluctuations and market uncertainty.

Additionally, intense global competition is placing pressure on margins and innovation cycles. Established automakers, EV startups, and vertically integrated technology firms are competing aggressively, leading to pricing pressure, overcapacity risks, and rapid product obsolescence in certain segments.

Global NEV Market: Current Risk Scenario

The current NEV market environment reflects strong demand growth supported by electrification policies and consumer adoption, but also increasing structural stress across supply chains and manufacturing ecosystems.

Battery raw material price volatility remains a key challenge, directly impacting vehicle pricing, manufacturer margins, and long-term procurement strategies. Fluctuations in lithium and cobalt prices continue to create uncertainty for EV production economics.

Charging infrastructure expansion is progressing unevenly across regions, creating adoption disparities. Urban areas are experiencing faster deployment, while rural and developing regions continue to face accessibility constraints.

Automakers are also facing inventory and capacity balancing challenges as demand growth varies across segments such as BEVs and PHEVs, requiring flexible production strategies to avoid overproduction or supply shortages.

Cybersecurity and software dependency risks are also emerging as vehicles become increasingly connected, autonomous, and software-defined, exposing the industry to data security vulnerabilities and system integration challenges.

Key Risk Factors & Disruption Threats Signals

- Battery Raw Material Dependency: Heavy reliance on lithium, nickel, and cobalt exposes the market to price volatility and supply disruptions.

- Infrastructure Gaps: Uneven charging network development limits adoption in emerging and rural markets.

- Technological Transition Risk: Uncertainty around next-generation battery technologies may delay long-term efficiency gains.

- Policy & Subsidy Dependence: Market demand is highly sensitive to government incentives and emission regulations.

- High Capital Requirements: Gigafactory development and charging infrastructure expansion require sustained large-scale investment.

- Intense Market Competition: Price wars and overcapacity risks are increasing due to rapid entry of global EV manufacturers.

- Cybersecurity & Software Risks: Connected vehicle systems introduce vulnerabilities in data protection and system integrity.

Strategic Implications of Risk Factors & Disruption Threats

The evolving risk landscape is forcing NEV manufacturers and ecosystem players to adopt vertically integrated strategies, particularly across battery production, raw material sourcing, and software development. Companies are increasingly investing in securing upstream supply chains to reduce exposure to commodity volatility.

Strategic diversification of battery technologies is becoming essential, with firms investing in solid-state research, alternative chemistries, and recycling capabilities to mitigate long-term material dependency risks.

Governments and private stakeholders are focusing on infrastructure co-investment models to accelerate charging network deployment and reduce financial burden on individual manufacturers.

Additionally, partnerships between automotive companies and technology firms are increasing to strengthen capabilities in autonomous driving, vehicle software, and cybersecurity resilience.

Global NEV Market: Forward Risk Outlook

Looking ahead, the NEV market is expected to maintain strong growth momentum, but risk intensity will remain high due to structural dependency on policy frameworks, raw material supply chains, and technological evolution.

Battery innovation, particularly the commercialization of solid-state technology and improvements in fast-charging systems, will play a key role in reducing long-term operational risks and improving adoption efficiency.

However, regulatory fragmentation across regions and uneven infrastructure development may continue to create market imbalances, especially in emerging economies.

Overall, companies that successfully integrate supply chain resilience, technological innovation, and scalable infrastructure partnerships will be best positioned to navigate disruption risks and sustain long-term competitive advantage in the global NEV market.

Regulatory Landscape

Global New Energy Vehicles (NEV) Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global New Energy Vehicles (NEV) Market is defined by aggressive decarbonization mandates, evolving emission control frameworks, and large-scale government incentives aimed at accelerating the transition from internal combustion engine (ICE) vehicles to electric mobility. Governments across major economies are implementing structured policy ecosystems that combine environmental regulation, industrial policy, and infrastructure investment to support NEV adoption.

These regulations influence every stage of the NEV value chain, including vehicle manufacturing standards, battery safety compliance, charging infrastructure deployment, energy efficiency benchmarks, and end-of-life recycling requirements. As a result, automakers and mobility providers must align product development and supply chain strategies with rapidly tightening global sustainability requirements.

The regulatory landscape is also increasingly shaped by national net-zero commitments, carbon neutrality targets, and energy transition strategies, which are accelerating the shift toward electrified transport systems and reducing reliance on fossil fuel-based mobility.

Global New Energy Vehicles (NEV) Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by strong policy-driven adoption, particularly in Asia-Pacific and Europe, where governments have introduced strict emission reduction targets, zero-emission vehicle (ZEV) mandates, and phased bans on new ICE vehicle sales in future timelines. These policies are significantly accelerating NEV penetration across passenger and commercial vehicle segments.

Financial incentives such as purchase subsidies, tax rebates, reduced registration fees, and toll exemptions continue to play a key role in improving NEV affordability and driving consumer adoption. In parallel, corporate fleet electrification mandates are emerging in several regions, particularly for logistics, public transport, and government-owned vehicle fleets.

Charging infrastructure regulations are also expanding rapidly, with governments enforcing minimum charger installation requirements in residential, commercial, and highway infrastructure projects. Standardization of charging protocols and interoperability frameworks is becoming a regulatory priority to ensure seamless cross-network usability.

Battery safety, recycling, and disposal regulations are gaining increased attention, with authorities mandating strict guidelines for lithium-ion battery handling, second-life applications, and circular economy integration. These regulations are shaping sustainable production practices across the NEV ecosystem.

Additionally, vehicle safety standards, cybersecurity requirements for connected vehicles, and software update compliance rules are becoming more prominent as NEVs increasingly rely on digital and autonomous technologies.

Key Regulatory & Policy Environment Signals in Global NEV Market

- Emission Reduction Mandates: Strict CO??? reduction targets and phased ICE vehicle bans accelerating EV adoption.

- EV Incentive Programs: Subsidies, tax credits, and financial benefits supporting consumer and fleet electrification.

- Charging Infrastructure Policies: Government-led mandates for widespread and standardized charging network deployment.

- Battery Safety & Recycling Regulations: Guidelines promoting safe handling, recycling, and circular economy integration for EV batteries.

- Corporate Fleet Electrification Rules: Requirements for logistics, public transport, and government fleets to transition toward NEVs.

- Vehicle Cybersecurity & Software Compliance: Emerging regulations addressing connected vehicle safety and over-the-air update governance.

Strategic Implications of Regulatory & Policy Environment

The regulatory framework is a primary growth catalyst for the NEV market, effectively reshaping global automotive industry dynamics. Automakers that align early with zero-emission mandates and invest in compliant EV platforms are gaining stronger market positioning and preferential access to incentive-driven markets.

Government incentives and subsidy programs are accelerating mass-market adoption, but are also intensifying competition by lowering entry barriers for new EV manufacturers and technology-driven mobility startups. This is increasing innovation pressure across the value chain.

Charging infrastructure policies are creating new investment opportunities for energy companies, utilities, and technology providers, enabling the development of integrated mobility-energy ecosystems. Standardization requirements are further driving interoperability and ecosystem convergence.

Battery regulations are pushing manufacturers toward sustainable sourcing, improved recycling systems, and advanced battery chemistry innovation, strengthening the long-term sustainability profile of the industry while increasing compliance complexity.

Overall, regulatory compliance is becoming a core competitive differentiator, with companies demonstrating strong alignment with environmental policies, safety standards, and digital mobility regulations expected to secure long-term leadership in the global NEV ecosystem.

Global New Energy Vehicles (NEV) Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the NEV market is expected to become more stringent, standardized, and globally coordinated. Many countries are likely to accelerate ICE phase-out timelines while expanding mandatory EV adoption targets across public and commercial transportation sectors.

Global harmonization of charging standards, battery safety protocols, and recycling regulations is expected to improve cross-border EV interoperability and strengthen global supply chain efficiency. This will also support international expansion of EV manufacturers.

Carbon pricing mechanisms, including carbon taxes and emissions trading systems, are expected to further reinforce the economic advantage of NEVs over traditional vehicles, accelerating demand across both developed and emerging markets.

Regulators are also expected to place greater emphasis on digital vehicle governance, including software security, autonomous driving compliance, and real-time vehicle data management, as NEVs become increasingly software-defined.

Overall, the regulatory trajectory strongly supports long-term NEV market expansion. Companies capable of integrating compliance, sustainability, advanced battery technology, and smart mobility solutions into their core strategies will be best positioned to lead the next phase of global transportation transformation.