Global Antacids Market Report, Size & Forecast 2026-2033

Global Antacids Market Size & Forecast

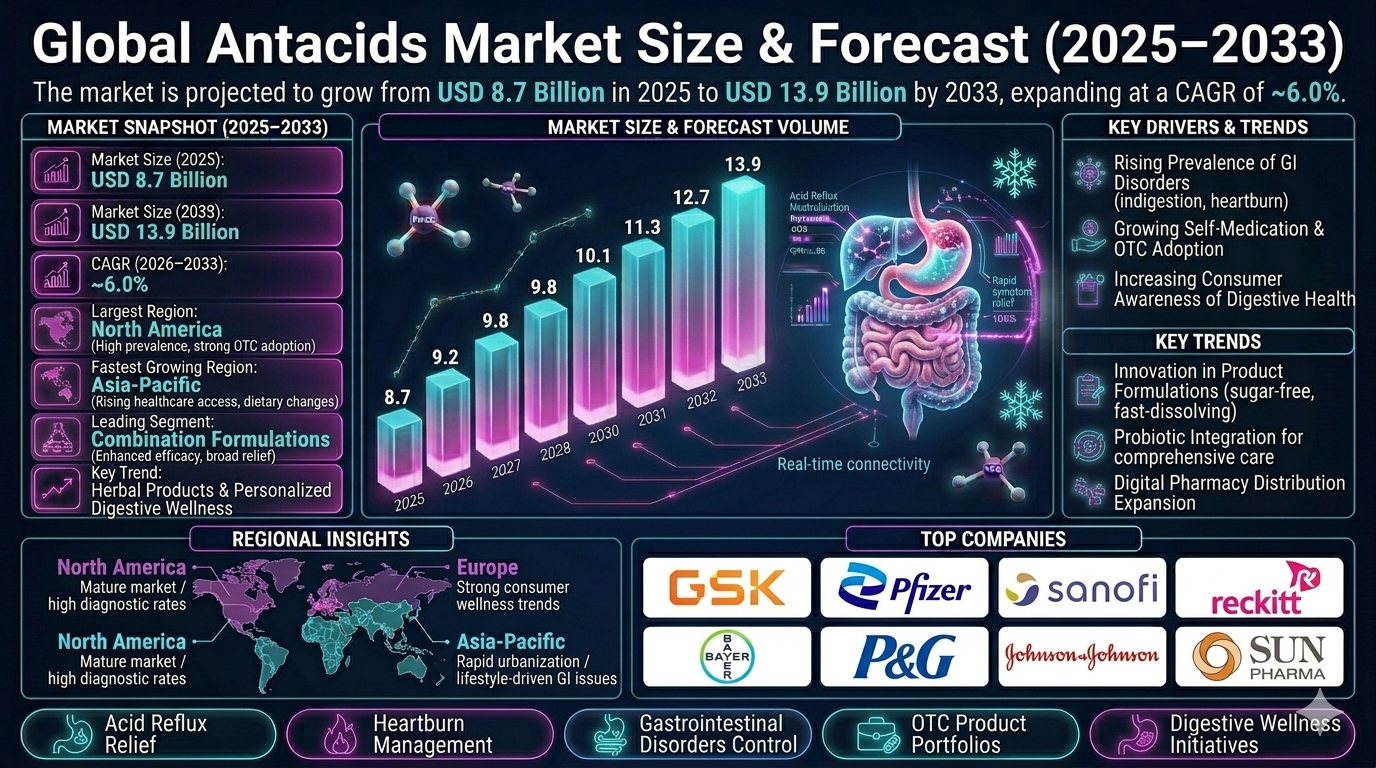

The global antacids market is projected to witness steady growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 8.7 billion in 2025 and is expected to reach nearly USD 13.9 billion by 2033, expanding at a CAGR of around 6.0%. The market growth is driven by the increasing prevalence of gastrointestinal disorders, rising consumer awareness regarding digestive health, growing self-medication trends, and expanding over-the-counter (OTC) pharmaceutical accessibility across developed and emerging markets. Antacids are medications used to neutralize stomach acid and provide relief from acid reflux, heartburn, indigestion, gastritis, and other acid-related gastrointestinal conditions. These products are widely available in tablet, liquid, chewable, powder, and suspension formulations for both prescription and OTC use. The market is experiencing significant transformation through formulation innovation, rapid-acting therapeutic combinations, sugar-free and herbal product development, and expanding digital pharmaceutical distribution channels. Additionally, changing dietary habits, increasing consumption of processed foods, rising stress levels, and sedentary lifestyles are contributing to growing global demand for antacid products.

Global Antacids Market Overview

The antacids market forms a vital segment of the global gastrointestinal therapeutics and consumer healthcare industry. These products play an essential role in managing acid-related digestive disorders while supporting preventive digestive care. The market includes acid-neutralizing agents such as calcium carbonate, magnesium hydroxide, aluminum hydroxide, sodium bicarbonate, and combination formulations. Manufacturers are increasingly focusing on enhanced product efficacy, faster symptom relief, improved taste profiles, convenient dosage forms, and clean-label digestive health formulations. Technological advancements in pharmaceutical formulation science, extended-release combinations, and personalized digestive health solutions are reshaping market dynamics. Major market participants include GlaxoSmithKline plc, Pfizer Inc., Sanofi S.A., Reckitt Benckiser Group plc, Bayer AG, Procter & Gamble, Johnson & Johnson, Prestige Consumer Healthcare, Haleon, and Sun Pharmaceutical Industries Ltd.Key Drivers of Global Antacids Market Growth

Rising Prevalence of Gastrointestinal Disorders

The increasing incidence of acid reflux, gastroesophageal reflux disease (GERD), indigestion, and gastritis is driving global demand for antacid products. Changing dietary habits and sedentary lifestyles are contributing significantly to digestive health concerns.Growing Self-Medication and OTC Adoption

Consumers are increasingly opting for self-care and over-the-counter digestive relief solutions for mild gastrointestinal symptoms. This trend is supporting widespread market expansion.Increasing Consumer Awareness of Digestive Health

Greater public awareness regarding digestive wellness and preventive healthcare is encouraging early symptom management. This is strengthening product adoption across multiple age groups.Expansion of E-commerce and Digital Pharmacy Platforms

Online pharmacies and digital healthcare platforms are increasing product accessibility and enabling broader consumer reach. This is accelerating sales growth globally.Innovation in Product Formulations

Manufacturers are introducing sugar-free, herbal, fast-dissolving, flavored, and combination antacid products to improve consumer convenience and compliance. Product differentiation is driving competitive growth.Global Antacids Market Segmentation

By Drug Type

The market is segmented into calcium-based antacids, magnesium-based antacids, aluminum-based antacids, sodium bicarbonate-based antacids, and combination formulations. Combination formulations dominate the market due to enhanced efficacy and broader symptom relief.By Dosage Form

The market includes tablets, chewable tablets, liquids, suspensions, powders, and effervescent formulations. Chewable tablets account for a significant market share due to convenience and rapid action.By Distribution Channel

Distribution channels include hospital pharmacies, retail pharmacies, online pharmacies, and supermarkets. Retail pharmacies remain the dominant distribution channel globally.By Application

Applications include heartburn relief, acid reflux treatment, indigestion management, gastritis treatment, and ulcer-related symptom relief. Heartburn and acid reflux treatment account for the largest application segment.Regional Market Dynamics

North America

North America dominates the global antacids market due to high prevalence of digestive disorders, strong OTC healthcare adoption, and advanced pharmaceutical distribution infrastructure. The United States remains the leading regional market.Europe

Europe holds a significant market share supported by strong consumer awareness, regulatory approvals for OTC digestive care products, and growing digestive wellness trends. Germany, the United Kingdom, and France are key contributors.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rising healthcare access, increasing urbanization, dietary changes, and growing pharmaceutical consumption. China, India, Japan, and South Korea are major regional markets.Latin America

Latin America is witnessing steady growth due to increasing healthcare awareness and expanding retail pharmaceutical infrastructure. Brazil and Mexico remain key regional contributors.Middle East & Africa

The Middle East & Africa market is gradually expanding due to improving healthcare access and rising consumer demand for OTC healthcare products. GCC countries are leading regional market development.Competitive Landscape

The global antacids market is highly competitive, characterized by strong participation from multinational pharmaceutical companies and consumer healthcare brands. Key players include GlaxoSmithKline plc, Pfizer Inc., Sanofi S.A., Reckitt Benckiser Group plc, Bayer AG, Procter & Gamble, Johnson & Johnson, Prestige Consumer Healthcare, Haleon, and Sun Pharmaceutical Industries Ltd. Companies are increasingly investing in product reformulation, flavor enhancement, digital marketing strategies, and expanded OTC product portfolios. Strategic acquisitions and partnerships with pharmacy distribution networks are strengthening competitive positioning.Strategic Outlook

The strategic outlook for the global antacids market remains positive due to growing digestive health awareness and expanding OTC pharmaceutical consumption. Future growth opportunities include herbal antacid formulations, personalized digestive health solutions, probiotic-integrated products, and digital digestive wellness platforms. Increasing focus on clean-label ingredients and sugar-free therapeutic options will shape future product innovation. Manufacturers investing in formulation science, digital distribution, and consumer-centric branding are expected to strengthen market leadership.Final Market Perspective

The global antacids market continues to play an essential role in digestive healthcare management worldwide. Rising prevalence of gastrointestinal disorders, increasing self-medication trends, and expanding healthcare accessibility will continue driving market growth throughout the forecast period. Organizations that successfully combine therapeutic effectiveness, product innovation, and consumer convenience will remain strongly positioned in the evolving global antacids market.Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Market Highlights

1.3 Growth Outlook Analysis

1.4 Largest Segment Overview

1.5 Fastest Growing Segment Overview

1.6 Regional Market Insights

1.7 Competitive Landscape Snapshot

1.8 Future Market Outlook

2. Global Antacids Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Antacids Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Pricing Structure Analysis

3.5 Product Formulation Landscape

3.6 Distribution & Retail Infrastructure Analysis

3.7 OTC Pharmaceutical Industry Overview

3.8 Consumer Digestive Health Trends

3.9 Technological Advancements in Antacid Formulations

4. Global Antacids Market Dynamics

4.1 Market Drivers

4.1.1 Rising Prevalence of Gastrointestinal Disorders

4.1.1.1 Increasing GERD & Acid Reflux Cases

4.1.1.1.1 Lifestyle & Dietary Impact

4.1.2 Growing Self-Medication & OTC Adoption

4.1.2.1 Consumer Preference for OTC Healthcare

4.1.2.1.1 Expanding Pharmacy Accessibility

4.1.3 Increasing Consumer Awareness of Digestive Health

4.1.3.1 Preventive Healthcare Trends

4.1.3.1.1 Rising Wellness-Oriented Consumption

4.1.4 Expansion of E-commerce & Digital Pharmacies

4.1.4.1 Online OTC Drug Accessibility

4.1.4.1.1 Digital Healthcare Penetration

4.1.5 Innovation in Product Formulations

4.1.5.1 Sugar-Free & Herbal Antacids

4.1.5.1.1 Fast-Acting Combination Therapies

4.2 Market Restraints

4.2.1 Side Effects Associated with Excessive Usage

4.2.2 Availability of Alternative GI Therapies

4.2.3 Stringent Pharmaceutical Regulations

4.2.4 Product Recall & Safety Challenges

4.3 Market Opportunities

4.3.1 Herbal & Natural Digestive Care Products

4.3.2 Personalized Digestive Health Solutions

4.3.3 Probiotic-Integrated Antacid Products

4.3.4 Growth in Emerging OTC Markets

4.4 Market Challenges

4.4.1 Intense Competitive Pricing Pressure

4.4.2 Consumer Preference Shifts Toward Preventive Care

4.4.3 Counterfeit OTC Pharmaceutical Products

4.4.4 Regulatory Compliance Complexity

5. Global Antacids Market Size Analysis (USD Billion), 2026???2033

5.1 Revenue Forecast Analysis

5.2 CAGR Analysis

5.3 Demand-Supply Analysis

5.4 Pricing Trend Analysis

5.5 Consumption Pattern Analysis

5.6 Market Share Analysis

6. Global Antacids Market Segmentation Analysis

6.1 By Drug Type

6.1.1 Calcium-Based Antacids

6.1.2 Magnesium-Based Antacids

6.1.3 Aluminum-Based Antacids

6.1.4 Sodium Bicarbonate-Based Antacids

6.1.5 Combination Formulations

6.2 By Dosage Form

6.2.1 Tablets

6.2.2 Chewable Tablets

6.2.3 Liquids

6.2.4 Suspensions

6.2.5 Powders

6.2.6 Effervescent Formulations

6.3 By Distribution Channel

6.3.1 Hospital Pharmacies

6.3.2 Retail Pharmacies

6.3.3 Online Pharmacies

6.3.4 Supermarkets & Hypermarkets

6.4 By Application

6.4.1 Heartburn Relief

6.4.2 Acid Reflux Treatment

6.4.3 Indigestion Management

6.4.4 Gastritis Treatment

6.4.5 Ulcer-Related Symptom Relief

7. Regional Market Analysis

7.1 North America

7.1.1 U.S.

7.1.2 Canada

7.1.3 Mexico

7.2 Europe

7.2.1 Germany

7.2.2 U.K.

7.2.3 France

7.2.4 Italy

7.2.5 Spain

7.2.6 Rest of Europe

7.3 Asia-Pacific

7.3.1 China

7.3.2 Japan

7.3.3 India

7.3.4 South Korea

7.3.5 Australia

7.3.6 Rest of Asia-Pacific

7.4 Latin America

7.4.1 Brazil

7.4.2 Mexico

7.4.3 Rest of Latin America

7.5 Middle East & Africa

7.5.1 GCC Countries

7.5.2 South Africa

7.5.3 Rest of Middle East & Africa

8. Competitive Landscape

8.1 Market Share Analysis

8.2 Competitive Benchmarking

8.3 Strategic Developments

8.4 Product Innovation Analysis

8.5 Mergers & Acquisitions

8.6 OTC Brand Positioning Analysis

8.7 Distribution Network Strategies

9. Company Profiles

9.1 GlaxoSmithKline plc

9.2 Pfizer Inc.

9.3 Sanofi S.A.

9.4 Reckitt Benckiser Group plc

9.5 Bayer AG

9.6 Procter & Gamble

9.7 Johnson & Johnson

9.8 Prestige Consumer Healthcare

9.9 Haleon

9.10 Sun Pharmaceutical Industries Ltd.

10. Strategic Intelligence & Pheonix AI Insights

10.1 Pheonix Market Forecast Engine

10.2 OTC Consumer Trend Analysis

10.3 Digestive Health Opportunity Mapping

10.4 Pharmaceutical Retail Intelligence

10.5 Competitive Positioning Dashboard

10.6 Regulatory Risk Assessment Framework

11. Future Outlook & Strategic Recommendations

11.1 OTC Market Expansion Strategies

11.2 Product Innovation & Formulation Development

11.3 Digital Pharmacy Growth Strategies

11.4 Clean-Label & Herbal Product Adoption

11.5 Long-Term Market Outlook (2033+)

12. Appendix

12.1 Abbreviations

12.2 Research References

12.3 Data Sources

12.4 Methodology Validation

13. About Pheonix

14. Market Research

15. Disclaimer

Competitive Landscape

Global Antacids Market Competitive Intensity & Market Structure Overview

The global antacids market is highly competitive and moderately fragmented, characterized by strong participation from multinational pharmaceutical companies, consumer healthcare brands, generic drug manufacturers, and regional over-the-counter digestive health product providers. Competitive intensity is shaped by product efficacy, brand trust, formulation innovation, distribution reach, pricing strategies, and consumer accessibility.

The market structure includes established branded pharmaceutical manufacturers, OTC consumer health companies, private-label producers, and emerging natural digestive wellness product developers. Companies compete through product differentiation, formulation advancement, retail pharmacy penetration, and digital healthcare engagement strategies.

Rising digestive health awareness, increasing self-medication trends, expanding OTC pharmaceutical access, and continuous product innovation are intensifying competition across the global antacids market.

Global Antacids Market Competitive Intensity & Market Structure Current Scenario

Leading Global Antacid Market Participants

GlaxoSmithKline plc (Haleon): Major global digestive healthcare leader with strong OTC antacid brands and broad consumer healthcare distribution capabilities.

Pfizer Inc.: Established pharmaceutical company with strong presence in gastrointestinal therapeutics and consumer healthcare product development.

Sanofi S.A.: Significant market participant offering digestive health solutions supported by extensive pharmaceutical distribution networks.

Reckitt Benckiser Group plc: Leading consumer healthcare company recognized for strong digestive wellness product branding and retail market penetration.

Bayer AG: Major global pharmaceutical company with established digestive care solutions and broad international market access.

Procter & Gamble: Prominent consumer health company competing through strong consumer trust and healthcare product innovation.

Johnson & Johnson: Important participant with broad healthcare capabilities supporting digestive health product portfolios.

Prestige Consumer Healthcare: Strong OTC healthcare company focused on accessible digestive care products and retail pharmacy expansion.

Haleon: Dedicated consumer health company with significant digestive wellness market leadership and global product visibility.

Sun Pharmaceutical Industries Ltd.: Key global generic pharmaceutical manufacturer expanding digestive therapeutics offerings across emerging and developed markets.

Key Competitive Intensity & Market Structure Drivers

The increasing prevalence of acid reflux, GERD, indigestion, and lifestyle-related digestive disorders is driving strong product demand and intensifying market competition.

Growing consumer preference for self-medication and OTC digestive health management is strengthening retail competition across branded and generic product categories.

Innovation in sugar-free formulations, herbal combinations, fast-acting solutions, and consumer-friendly dosage forms is creating strong product differentiation.

The expansion of e-commerce pharmacies and digital healthcare platforms is increasing market accessibility and accelerating competitive digital engagement strategies.

Consumer demand for clean-label digestive health products and wellness-oriented formulations is encouraging manufacturers to diversify product portfolios.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly investing in rapid-action formulations, taste enhancement, and differentiated delivery formats to improve consumer adoption.

Strategic partnerships with pharmacy chains, online healthcare platforms, and retail distributors are becoming essential for strengthening market reach.

Brand positioning through digestive wellness education, digital marketing, and preventive healthcare campaigns is emerging as a major competitive strategy.

Companies are prioritizing product portfolio expansion through herbal formulations, combination therapies, and personalized digestive wellness offerings.

Acquisitions, licensing agreements, and OTC product portfolio diversification are strengthening competitive positioning across regional markets.

Global Antacids Market Competitive Intensity & Market Structure Forward Outlook

The global antacids market is expected to remain highly competitive as digestive health awareness, consumer self-care trends, and OTC pharmaceutical accessibility continue to expand globally.

Future competition will increasingly focus on personalized digestive care, clean-label innovation, probiotic-integrated formulations, and digital consumer health engagement.

Asia-Pacific is expected to emerge as a major competitive growth region due to rising healthcare access, urbanization, and increasing digestive health awareness.

Technological advancements in pharmaceutical formulation science and consumer-focused therapeutic innovation are expected to significantly reshape market dynamics.

Overall, companies that successfully combine therapeutic effectiveness, consumer convenience, strong retail presence, and digital health innovation will remain strongly positioned in the evolving global antacids market.

Value Chain

Global Antacids Market Value Chain & Supply Chain Evolution Overview

The global antacids market value chain is undergoing steady transformation as digestive health awareness, self-medication adoption, over-the-counter pharmaceutical accessibility, and consumer-centric formulation innovation continue reshaping the broader gastrointestinal therapeutics ecosystem. Antacids remain essential healthcare products for managing acid reflux, heartburn, indigestion, gastritis, and other acid-related digestive disorders, supporting both preventive digestive care and rapid symptom relief across global consumer healthcare markets.

The antacids value chain spans active pharmaceutical ingredient sourcing, excipient production, formulation development, manufacturing, packaging, distribution, retail pharmacy access, digital healthcare platforms, and end-consumer therapeutic use. This interconnected ecosystem includes chemical ingredient suppliers, pharmaceutical manufacturers, formulation scientists, packaging companies, pharmacy networks, digital health platforms, logistics providers, and healthcare consumers.

Major companies including GlaxoSmithKline plc, Pfizer Inc., Sanofi S.A., Reckitt Benckiser Group plc, Bayer AG, Procter & Gamble, Johnson & Johnson, Prestige Consumer Healthcare, Haleon, and Sun Pharmaceutical Industries Ltd. are actively investing in rapid-action formulations, improved dosage convenience, sugar-free product development, flavor optimization, and digital distribution strategies to strengthen competitive positioning.

Upstream supply chain operations depend on sourcing acid-neutralizing active ingredients such as calcium carbonate, magnesium hydroxide, aluminum hydroxide, sodium bicarbonate, pharmaceutical excipients, flavoring agents, sweeteners, and packaging materials. Midstream activities focus on formulation engineering, blending, tablet compression, liquid suspension manufacturing, stability testing, quality assurance, and regulatory compliance validation. Downstream operations include wholesale pharmaceutical distribution, retail pharmacy supply, e-commerce fulfillment, direct-to-consumer healthcare sales, and consumer usage monitoring.

Operational priorities across the antacids value chain increasingly emphasize product efficacy, fast symptom relief, formulation stability, taste enhancement, regulatory compliance, shelf-life optimization, consumer convenience, and broad therapeutic accessibility. However, the market continues to face challenges related to pricing pressure, raw material availability, regulatory complexity, consumer preference shifts toward natural alternatives, and intense competition from adjacent gastrointestinal therapeutic categories.

Global Antacids Market Value Chain & Supply Chain Evolution Current Scenario

The current antacids market is being shaped by increasing digestive health concerns, changing dietary patterns, growing stress-related gastrointestinal disorders, and expanding consumer demand for rapid, convenient self-care solutions. Consumers are increasingly relying on OTC antacids for immediate symptom management without requiring physician consultation for mild acid-related conditions.

North America currently dominates the global antacids market due to high digestive disorder prevalence, strong OTC medication adoption, mature pharmacy infrastructure, and widespread digestive health awareness. The United States remains the largest contributor to regional demand.

Europe maintains a strong market position supported by established consumer healthcare markets, favorable regulatory pathways for OTC digestive therapeutics, and increasing consumer focus on preventive wellness solutions. Asia-Pacific is emerging as the fastest-growing regional market due to rising healthcare access, urban dietary changes, and expanding retail pharmaceutical infrastructure.

Manufacturers are increasingly introducing chewable tablets, fast-dissolving formulations, flavored suspensions, sugar-free options, and combination digestive care solutions to improve consumer compliance and therapeutic convenience.

The rise of digital pharmacies and direct-to-consumer healthcare platforms is significantly transforming pharmaceutical distribution models, improving accessibility and strengthening product visibility across emerging and mature markets.

Key Value Chain & Supply Chain Evolution Signals in Global Antacids Market

One of the most significant transformation signals is the growing consumer preference for fast-acting and convenient dosage formats. Rapid-dissolving chewables, liquid suspensions, and on-the-go sachet formats are increasingly reshaping product development strategies.

Another major signal is the rising demand for clean-label and sugar-free formulations. Consumers are increasingly seeking digestive health products aligned with broader wellness and health-conscious consumption trends.

The integration of herbal and natural ingredients is also becoming a key market evolution trend. Manufacturers are increasingly exploring botanical digestive relief solutions and plant-based formulations to appeal to wellness-focused consumers.

Digital pharmaceutical distribution is rapidly expanding, with e-commerce platforms improving product accessibility, subscription models, and personalized healthcare engagement.

Consumer preference for preventive digestive wellness is driving innovation beyond traditional symptom relief, including multifunctional products combining antacid activity with probiotics and digestive support ingredients.

Packaging innovation is becoming increasingly important, with compact, travel-friendly, single-dose, and child-safe packaging formats improving convenience and market differentiation.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Antacids Market

Leading market participants are increasingly prioritizing formulation innovation, brand differentiation, consumer-centric packaging, and omnichannel distribution strategies to maintain competitive advantage. Competitive differentiation increasingly depends on therapeutic speed, product convenience, taste optimization, and retail accessibility.

Companies capable of delivering multifunctional digestive health products with strong consumer branding and rapid therapeutic action are expected to capture premium growth opportunities.

Strategic partnerships between pharmaceutical manufacturers, retail pharmacy chains, digital healthcare platforms, and e-commerce distributors are becoming increasingly important for strengthening market penetration and consumer reach.

Digital consumer engagement strategies including telehealth integration, digestive wellness education campaigns, and targeted digital marketing are becoming critical tools for market expansion.

Innovation in sugar-free, herbal, and personalized digestive health formulations is emerging as a major strategic focus area for manufacturers seeking to align with evolving consumer preferences.

Global supply chain resilience is becoming increasingly important as pharmaceutical manufacturers seek to secure reliable ingredient sourcing and improve responsiveness to regional demand fluctuations.

Global Antacids Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the antacids value chain is expected to become increasingly consumer-personalized, digitally integrated, and innovation-driven. Product development will continue shifting toward multifunctional digestive wellness solutions beyond conventional acid neutralization.

Advanced formulation science will enable faster-acting, extended-release, and precision-targeted digestive therapeutics designed to improve symptom control and user experience.

Natural ingredient integration, probiotic-enhanced formulations, and clean-label digestive care products are expected to gain increasing commercial importance.

Digital health ecosystems will continue transforming pharmaceutical access through telemedicine integration, personalized digestive wellness recommendations, and direct-to-consumer subscription models.

AI-powered consumer behavior analytics and personalized healthcare platforms may increasingly influence product targeting, demand forecasting, and consumer engagement strategies.

Packaging innovations focused on portability, sustainability, and precise dosing convenience will continue strengthening product differentiation across retail and online channels.

Ultimately, the future antacids value chain will evolve into a highly responsive, digitally enabled, consumer-centric digestive healthcare ecosystem capable of delivering personalized symptom management, preventive wellness support, and globally accessible therapeutic convenience.

Market-Specific Value Chain

- Raw Material & API Sourcing: Acid-neutralizing agents, pharmaceutical excipients, flavor compounds, sweeteners, stabilizers, and packaging material procurement.

- Formulation Development & Manufacturing: Product formulation, tablet compression, suspension preparation, flavor optimization, stability testing, and quality control.

- Packaging & Regulatory Compliance: Product packaging, labeling, dosage standardization, regulatory approvals, and market authorization validation.

- Distribution & Retail Access: Wholesale pharmaceutical logistics, retail pharmacy distribution, online pharmacy fulfillment, and supermarket healthcare retail placement.

- Consumer Consumption & Digital Engagement: OTC therapeutic use, digital healthcare education, telehealth integration, and consumer feedback monitoring.

- Lifecycle Innovation & Product Evolution: Personalized digestive wellness solutions, formulation enhancement, clean-label innovation, and next-generation digestive care product development.

Company-to-Stage Mapping

- Raw Material & API Sourcing: Pharmaceutical chemical suppliers, excipient manufacturers, flavoring ingredient producers, packaging suppliers.

- Formulation Development & Manufacturing: GlaxoSmithKline plc, Pfizer Inc., Sanofi S.A., Sun Pharmaceutical Industries Ltd.

- Packaging & Regulatory Compliance: Haleon, Bayer AG, regulatory consulting firms, pharmaceutical packaging companies.

- Distribution & Retail Access: Reckitt Benckiser Group plc, Prestige Consumer Healthcare, pharmacy chains, digital pharmacy platforms.

- Consumer Consumption & Digital Engagement: Retail pharmacy networks, telehealth platforms, consumer healthcare digital marketing providers.

- Lifecycle Innovation & Product Evolution: Johnson & Johnson, Procter & Gamble, digestive health R&D innovators, personalized wellness technology firms.

Investment Activity

Global Antacids Market Investment & Funding Dynamics Overview

Investment activity in the global antacids market is accelerating steadily due to rising prevalence of gastrointestinal disorders, expanding over-the-counter pharmaceutical accessibility, increasing consumer awareness of digestive health, and growing demand for innovative digestive wellness solutions. Between 2026 and 2033, capital allocation is expected to increasingly target formulation innovation, clean-label digestive therapeutics, digital pharmacy expansion, personalized gastrointestinal care platforms, and advanced OTC product development.

The antacids market represents a strategically important segment of the global gastrointestinal therapeutics and consumer healthcare ecosystem. Pharmaceutical companies, consumer health brands, venture-backed wellness firms, and institutional healthcare investors are increasing investments to strengthen product differentiation, expand consumer reach, and capture growing digestive healthcare demand.

A major structural transformation shaping investment dynamics is the shift from conventional acid-neutralizing products toward multifunctional digestive health solutions integrating rapid relief, preventive care, herbal ingredients, and personalized wellness formulations. This transition is driving substantial funding into next-generation digestive therapeutics and clean-label pharmaceutical innovation.

The market is also benefiting from rising investments in e-commerce pharmaceutical platforms, direct-to-consumer digestive wellness products, probiotic-integrated antacid formulations, and AI-enabled consumer health engagement solutions. Growing emphasis on preventive digestive health management is reshaping long-term capital deployment strategies.

Current Investment & Funding Landscape

Current funding activity in the antacids market is strongly supported by OTC product expansion strategies, pharmaceutical formulation advancements, digital pharmacy ecosystem growth, and increasing demand for consumer-centric digestive wellness products. Companies are actively investing in flavor enhancement technologies, rapid-dissolution formulations, sugar-free product development, and digital consumer acquisition platforms.

- North America: Leads global investment activity due to strong OTC healthcare adoption, advanced pharmaceutical retail networks, and high consumer awareness regarding digestive health.

- Europe: Witnessing stable investment growth supported by increasing demand for clean-label formulations, digestive wellness trends, and strong pharmaceutical innovation capabilities.

- Asia-Pacific: Emerging as the fastest-growing investment region due to rising healthcare accessibility, increasing pharmaceutical consumption, and expanding urban consumer markets.

- Latin America & Middle East: Attracting gradual investment growth supported by improving healthcare infrastructure and expanding OTC distribution networks.

Key Investment & Funding Drivers

- Rising gastrointestinal disorder prevalence is increasing investment in advanced antacid therapeutic solutions.

- Growing self-medication trends are driving capital allocation toward OTC digestive care expansion.

- Consumer preference for clean-label and sugar-free products is accelerating formulation-focused investments.

- Expansion of e-commerce and digital pharmacy channels is attracting digital health retail investments.

- Product innovation in rapid-relief and combination therapies is creating strong funding opportunities.

- Increasing digestive wellness awareness is supporting preventive care product development investments.

- Demand for herbal and probiotic-integrated formulations is strengthening natural therapeutic innovation funding.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of combining therapeutic efficacy with consumer-centric product innovation.

- Technology leadership in formulation science and rapid-delivery systems is becoming a major competitive differentiator.

- Digital pharmacy partnerships and omnichannel consumer distribution strategies are strengthening investment attractiveness.

- Companies investing in clean-label digestive health solutions are expected to achieve stronger market positioning.

- Brand trust, regulatory compliance, and consumer accessibility remain central to long-term investor confidence.

- Regional diversification strategies are becoming increasingly important for accessing high-growth consumer healthcare markets.

- Organizations integrating digestive health products into broader wellness ecosystems are likely to capture higher long-term value.

Forward Investment Outlook

The global antacids market is expected to maintain stable long-term investment momentum due to growing digestive health awareness, expanding consumer healthcare spending, and continuous pharmaceutical innovation.

Future funding activity is expected to prioritize personalized digestive wellness solutions, probiotic-integrated antacid formulations, AI-enabled symptom management platforms, digital healthcare engagement tools, and advanced fast-acting therapeutic delivery systems.

- North America: Will remain the leading investment hub due to strong consumer healthcare spending and digital pharmaceutical innovation.

- Asia-Pacific: Will strengthen its position through rapid healthcare market expansion and increasing OTC pharmaceutical accessibility.

- Europe: Will continue emphasizing clean-label innovation and preventive digestive wellness solutions.

Future innovation investments are also expected across microbiome-focused digestive care, smart consumer health tracking integration, herbal therapeutic development, personalized nutrition-linked digestive solutions, and subscription-based wellness platforms.

The convergence of consumer wellness trends, digital healthcare transformation, and pharmaceutical formulation innovation will continue reshaping investment priorities across the antacids market.

Overall, the market is expected to remain a highly attractive long-term consumer healthcare investment opportunity as digestive health management becomes an increasingly central component of global preventive wellness strategies.

Technology & Innovation

Global Antacids Market Technology & Innovation Landscape Overview

The Global Antacids Market is experiencing notable technological transformation driven by advancements in pharmaceutical formulation science, rapid-release drug delivery systems, clean-label ingredient innovation, and digital healthcare integration. Manufacturers are increasingly focusing on improving therapeutic efficacy, faster symptom relief, enhanced patient convenience, and personalized digestive health solutions to meet evolving consumer demands.

Innovation within the antacids market is centered on developing advanced formulations that offer improved acid-neutralizing capacity, prolonged relief duration, reduced side effects, and better palatability. Companies are leveraging pharmaceutical research to create differentiated products that combine convenience, efficacy, and consumer-centric design.

The integration of digital health technologies, smart packaging systems, telehealth accessibility, and AI-driven consumer health analytics is also reshaping product distribution, patient engagement, and treatment optimization across the digestive healthcare ecosystem.

Global Antacids Market Technology & Innovation Current Scenario

Currently, the antacids market is witnessing strong innovation in fast-acting formulations designed to provide immediate acid neutralization and sustained symptom relief for acid reflux, heartburn, and indigestion.

Combination formulations incorporating multiple active ingredients such as calcium carbonate, magnesium hydroxide, and alginate compounds are increasingly being adopted to enhance therapeutic effectiveness and broaden symptom coverage.

Sugar-free, low-sodium, and clean-label antacid products are gaining traction as consumers increasingly prioritize healthier digestive care solutions and seek products suitable for diabetic and health-conscious populations.

Chewable tablets, orally dissolving tablets, flavored liquid suspensions, and effervescent delivery systems are improving product convenience, taste profile, and ease of administration across diverse consumer groups.

Digital pharmacy platforms and e-commerce channels are increasingly integrating AI-powered recommendation systems and personalized wellness insights to guide consumer purchasing decisions and improve product accessibility.

Additionally, pharmaceutical manufacturers are investing in stability-enhancing technologies, microencapsulation techniques, and advanced excipient systems to improve shelf life, formulation consistency, and drug delivery performance.

Key Technology & Innovation Trends in Global Antacids Market

- Rapid-Release Formulation Technology: Fast-dissolving delivery systems enabling quicker acid neutralization and symptom relief.

- Combination Therapeutic Formulations: Multi-ingredient antacids delivering broader digestive symptom management.

- Sugar-Free and Low-Sodium Innovation: Health-conscious formulations supporting broader patient suitability.

- Microencapsulation Technology: Enhanced stability and controlled-release delivery for improved therapeutic performance.

- Orally Dissolving Tablets: Convenient dosage formats improving ease of use and patient compliance.

- Herbal and Natural Ingredient Integration: Plant-based digestive relief solutions supporting clean-label consumer preferences.

- AI-Driven Consumer Health Analytics: Personalized digestive care recommendations based on behavioral insights.

- Digital Pharmacy Integration: Online healthcare platforms expanding product accessibility and consumer engagement.

- Smart Packaging Solutions: Digital-enabled packaging improving dosage guidance and product information access.

- Probiotic-Integrated Antacid Development: Combined acid relief and digestive microbiome support solutions.

Strategic Implications of Technology & Innovation

Technological innovation is reshaping the competitive landscape of the antacids market by enabling manufacturers to differentiate products through faster action, improved convenience, cleaner formulations, and personalized digestive health support.

Companies investing in advanced formulation science, digital distribution ecosystems, and consumer-focused product innovation are achieving stronger market positioning through improved brand loyalty and enhanced consumer trust.

The expansion of digital pharmacy infrastructure and AI-powered health recommendation platforms is enabling more efficient market penetration and direct consumer engagement across global regions.

The increasing demand for healthier, cleaner-label, and multifunctional digestive healthcare solutions is driving innovation in ingredient sourcing, product design, and therapeutic positioning.

However, challenges such as regulatory compliance complexity, formulation stability constraints, ingredient sourcing limitations, and rising product development costs remain key barriers to widespread innovation adoption.

Global Antacids Market Technology & Innovation Forward Outlook

Looking ahead, the antacids market is expected to evolve toward highly personalized, digitally integrated, and multifunctional digestive healthcare solutions.

Future innovation is likely to focus on precision digestive therapeutics supported by AI-powered symptom analysis, personalized product recommendations, and real-time digestive health monitoring.

Advanced drug delivery technologies including nano-formulations, bioresponsive release systems, and extended-release acid-neutralizing compounds are expected to improve therapeutic precision and duration.

Natural ingredient-based and microbiome-supportive formulations are anticipated to gain significant traction as consumers increasingly seek holistic digestive wellness solutions.

Digital health ecosystems integrating telemedicine consultations, mobile digestive wellness applications, and connected pharmacy platforms will further transform product accessibility and patient engagement.

Overall, the Global Antacids Market is entering a new phase of pharmaceutical innovation characterized by rapid-release formulations, personalized digestive care, clean-label therapeutics, and digitally enabled consumer health ecosystems, positioning the market for sustained growth and evolving healthcare relevance.

Market Risk

Global Antacids Market Risk Factors & Disruption Threats Overview

The global antacids market is experiencing sustained growth due to increasing digestive health concerns, rising self-medication trends, expanding over-the-counter availability, and growing awareness regarding gastrointestinal wellness. Despite favorable growth fundamentals, the market faces several risks and disruption threats related to regulatory oversight, evolving treatment alternatives, changing consumer preferences, pricing pressure, and formulation safety concerns.

One of the major risks affecting the antacids market is the increasing preference for alternative gastrointestinal therapies such as proton pump inhibitors (PPIs), H2 receptor antagonists, probiotics, and prescription-based acid management treatments. These alternatives often provide longer-lasting symptom relief and may reduce dependence on conventional antacid products.

Regulatory scrutiny regarding ingredient safety, labeling accuracy, sugar content, sodium levels, and long-term usage warnings is creating compliance challenges for manufacturers. Products containing certain compounds may face reformulation requirements due to evolving health and safety standards.

Consumer awareness regarding excessive antacid consumption and its potential side effects, including mineral imbalance, kidney complications, and rebound acid production, may also impact long-term market demand.

Pricing pressure from generic and private-label brands represents another key challenge. Intense competition within the OTC pharmaceutical segment is compressing margins for established global brands.

Supply chain disruptions affecting pharmaceutical-grade raw materials, excipients, packaging materials, and distribution logistics can create inventory shortages and production delays.

Additionally, changing consumer preferences toward natural digestive wellness products, herbal remedies, and preventive gut health solutions are disrupting traditional antacid product demand.

Global Antacids Market Risk Factors & Disruption Threats Current Scenario

The current antacids market remains stable due to consistent consumer demand for immediate acid relief products and strong retail pharmacy accessibility.

However, healthcare providers are increasingly recommending longer-term therapeutic alternatives for chronic acid reflux management, influencing prescription behavior and consumer purchasing patterns.

Manufacturers are facing heightened pressure to innovate through sugar-free formulations, herbal variants, low-sodium compositions, and combination digestive wellness products.

Digital pharmacies and e-commerce platforms are increasing market accessibility but are also intensifying pricing competition and consumer comparison-based purchasing behavior.

Growing awareness regarding gut microbiome health is encouraging consumers to explore probiotic and holistic digestive care products instead of frequent antacid use.

Regulatory agencies are strengthening product safety evaluations, particularly for pediatric use, prolonged consumption, and ingredient interaction risks.

Global Antacids Market Key Risk Factors & Disruption Threat Signals

- Therapeutic Substitution Risk: Increasing preference for PPIs, H2 blockers, and advanced acid-control medications.

- Regulatory Compliance Pressure: Stricter ingredient labeling, dosage warnings, and safety standards.

- Long-Term Usage Safety Concerns: Health risks associated with prolonged antacid consumption.

- Generic Brand Competition: Pricing pressure from low-cost private-label products.

- Natural Remedy Disruption: Rising consumer shift toward herbal and probiotic digestive solutions.

- Supply Chain Instability: Raw material and pharmaceutical packaging disruptions.

- Changing Consumer Preferences: Demand for clean-label and sugar-free formulations.

- Digital Price Transparency: E-commerce competition reducing brand pricing flexibility.

- Product Reformulation Costs: Investment requirements for healthier ingredient alternatives.

- Healthcare Guidance Shifts: Clinical recommendations reducing excessive OTC dependency.

Strategic Implications of Risk Factors

Manufacturers must prioritize formulation innovation focused on safer, cleaner, and consumer-friendly digestive relief solutions to remain competitive.

Investment in sugar-free, low-sodium, herbal, and probiotic-integrated antacid products will become essential to align with evolving health-conscious consumer preferences.

Companies should strengthen regulatory compliance systems and proactively adapt to changing pharmaceutical safety requirements.

Expanding digital pharmacy partnerships and optimizing omnichannel distribution strategies will be critical for sustaining market visibility and competitiveness.

Strategic brand differentiation through rapid-action efficacy, trusted clinical validation, and enhanced consumer education can help offset pricing pressure from generics.

Global Antacids Market Forward Risk Outlook

Looking ahead to 2026???2033, the antacids market will continue to grow, but competition from alternative gastrointestinal therapies and preventive digestive health solutions will intensify.

Future market success will increasingly depend on personalized digestive care products, integrated gut health solutions, and innovation in fast-acting clean-label formulations.

Manufacturers unable to respond to consumer demand for safer and more natural digestive care alternatives may face market share erosion.

Digital healthcare integration, telemedicine recommendations, and online pharmaceutical ecosystems will further influence purchasing behavior and competitive dynamics.

Overall, sustained leadership in the global antacids market will depend on formulation innovation, regulatory agility, digital adaptability, and strong consumer trust.

Regulatory Landscape

Global Antacids Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global antacids market is shaped by pharmaceutical safety standards, over-the-counter (OTC) drug regulations, consumer healthcare labeling requirements, ingredient approval frameworks, and product quality compliance mandates. As antacids are widely used for self-medication and digestive symptom management, regulatory oversight focuses heavily on product efficacy, formulation safety, dosage consistency, and consumer accessibility.

Health authorities across major markets regulate antacid manufacturing, active pharmaceutical ingredient usage, product claims, packaging disclosures, and post-market safety monitoring to ensure consumer protection. Regulatory agencies also oversee advertising standards to prevent misleading therapeutic claims and promote responsible self-medication practices.

Increasing demand for herbal formulations, sugar-free variants, and combination digestive health products is driving evolving regulatory scrutiny related to ingredient transparency, formulation substantiation, and health claim validation.

Global Antacids Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for the antacids market combines established pharmaceutical approval systems with growing oversight for OTC digestive healthcare products, e-commerce pharmaceutical distribution, and consumer wellness labeling standards.

In the United States, antacid regulation is primarily governed by the U.S. Food and Drug Administration (FDA), which oversees OTC monograph compliance, ingredient safety, manufacturing quality standards, and labeling requirements. Products marketed under the OTC monograph system must comply with approved active ingredients, dosage limits, and therapeutic indications.

In Europe, antacid products are regulated under the European Medicines Agency (EMA) and national regulatory authorities. Requirements focus on product registration, pharmacovigilance, quality assurance, and strict compliance with pharmaceutical labeling and advertising standards.

Asia-Pacific markets including China, India, Japan, and South Korea are strengthening OTC pharmaceutical regulations to improve consumer safety, enhance manufacturing quality, and regulate online pharmaceutical sales channels.

Emerging markets across Latin America, the Middle East, and Africa are increasingly aligning with international pharmaceutical quality standards and strengthening digestive healthcare product registration processes.

Key Regulatory & Policy Environment Signals in Global Antacids Market

- OTC Drug Compliance Frameworks: Regulatory authorities continue to strengthen requirements for ingredient approvals, dosage consistency, and consumer safety labeling.

- Pharmaceutical Manufacturing Standards: Good Manufacturing Practice (GMP) compliance remains mandatory for antacid production and quality assurance.

- Labeling and Consumer Disclosure Regulations: Clear dosage instructions, contraindications, ingredient transparency, and warning labels are increasingly emphasized.

- Digital Pharmacy Oversight: Growing regulation of online pharmaceutical sales is influencing antacid distribution practices and authentication requirements.

- Health Claim Validation Standards: Regulatory scrutiny is increasing for digestive wellness, herbal relief, and rapid-action therapeutic claims.

- Sugar-Free and Clean-Label Regulations: Authorities are strengthening disclosure requirements for excipients, sweeteners, and additive-free formulations.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging antacid manufacturers to invest in advanced formulation validation, quality assurance systems, and transparent product labeling strategies. Compliance with OTC standards is essential for maintaining market access and consumer trust.

Stricter oversight of health claims is increasing demand for evidence-based product development, particularly for herbal, probiotic-enhanced, and multifunction digestive health solutions.

Digital pharmacy regulations are reshaping distribution strategies by requiring stronger authentication protocols, prescription validation controls where applicable, and secure online consumer communication.

Regulatory emphasis on clean-label formulations and ingredient transparency is creating opportunities for manufacturers offering simplified, consumer-friendly digestive healthcare solutions.

Global Antacids Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global antacids market is expected to become increasingly focused on product transparency, consumer safety, digital pharmaceutical oversight, and evidence-based digestive health claims.

Health authorities are likely to strengthen post-market surveillance systems, improve adverse event reporting requirements, and tighten compliance standards for rapidly expanding OTC digestive care categories.

Digital health integration may introduce enhanced traceability requirements for online antacid distribution, including authentication technologies and stronger regulatory monitoring of e-commerce pharmacy platforms.

Growing consumer demand for natural digestive health products is expected to drive stricter validation requirements for herbal formulations, probiotic-integrated products, and personalized digestive wellness claims.

Overall, regulatory and policy developments will remain a critical market influence, with companies investing in compliance-driven innovation, transparent ingredient sourcing, and scientifically validated product portfolios expected to maintain long-term competitive advantage.