Global Tubeless Tyres Market size, share & forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

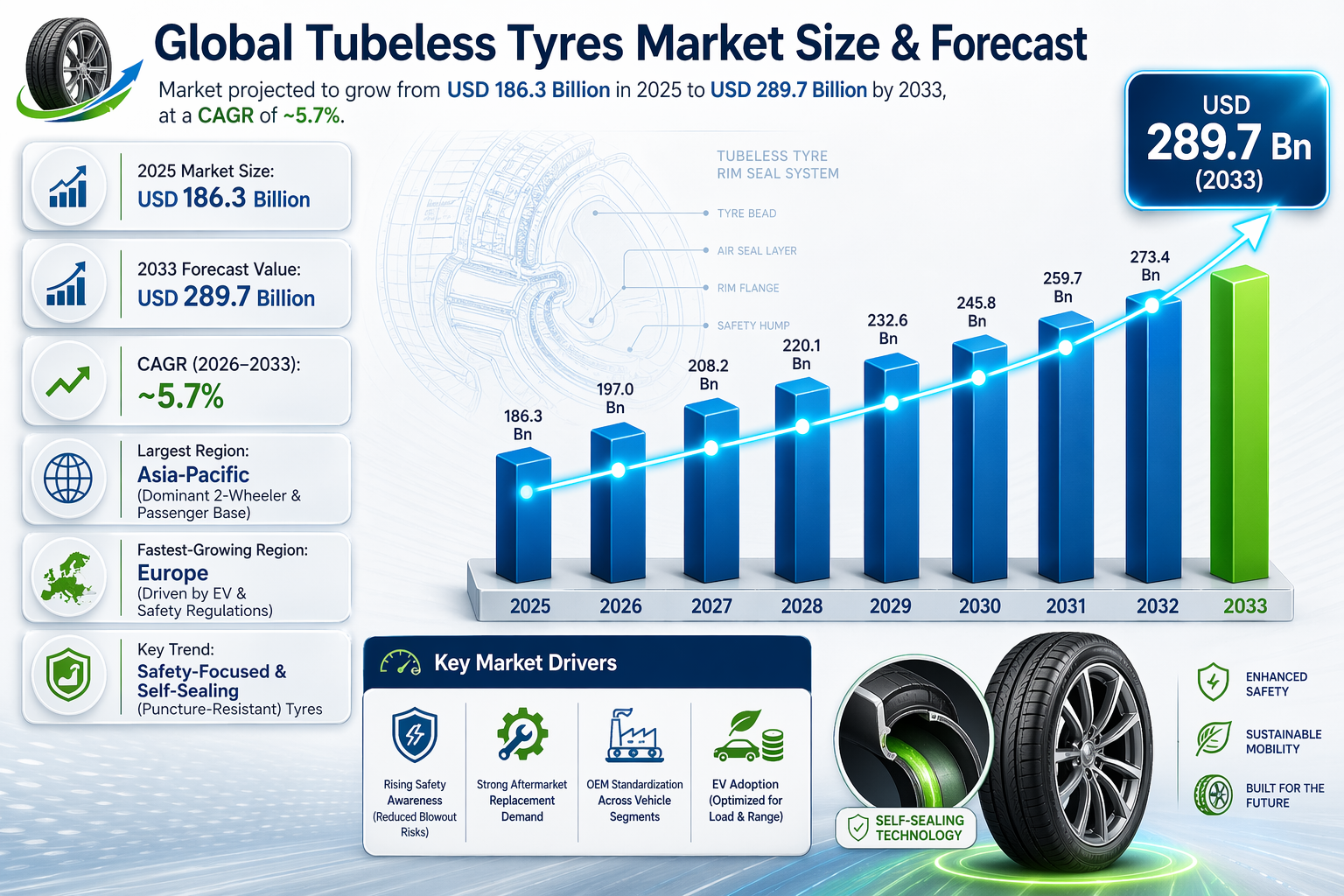

| 2025 Market Size | USD 186.3 Billion |

| 2033 Market Size | USD 289.7 Billion |

| CAGR (2026???2033) | ~5.7% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Passenger vehicle tubeless tyres |

| Fastest-Growing Segment | EV & two-wheeler tubeless tyres |

| Key Trend | Safety-focused & self-sealing tyres |

Global Tubeless Tyres Market Overview

The Global Tubeless Tyres Market is all about tyres that don???t need an inner tube???they seal airtight with the rim. You???ll see them on cars, SUVs, bikes, trucks, off-road machines, and even electric vehicles . They are safer, more fuel-efficient, need less maintenance, and give a smoother ride than old-school tube tyres.

Tubeless tyres are a game-changer???they cut down the risk of sudden air loss, handle heat better, and even let you keep rolling for a bit after a puncture . That???s why they???re becoming the top pick for both new cars and replacements. Plus, with better rubber, rim designs, and puncture-sealing tech, they???re getting even tougher and more reliable. It???s no surprise they???re taking over from old tube tyres across all vehicle types.

The Global tubeless tyres market is expanding steadily, driven by rising vehicle production, growing consumer awareness of safety benefits, and increasing penetration in emerging markets. Replacement demand remains the dominant revenue contributor due to routine tyre wear, while OEM adoption continues to rise as tubeless tyres become the industry standard.

According to the Pheonix Demand Forecast Engine, the Global Tubeless Tyres Market size??is estimated at USD 186.3 billion in 2025 and is projected to reach USD 289.7 billion by 2033, growing at a CAGR of ~5.7% during the forecast period (2026???2033).

Asia-Pacific represents the largest market due to high vehicle volumes and two-wheeler dominance, while Europe is the fastest-growing region driven by safety regulations, EV penetration, and premium vehicle demand.

Key Drivers of Global Tubeless Tyres Market Growth

Rising Safety Awareness

Tubeless tyres reduce blowout risk and enable gradual air loss, improving vehicle safety and control.

Strong Replacement Demand

??People always need new tyres, so shops stay busy. That steady demand keeps the market showing solid growth.

OEM Standardization of Tubeless Tyres

Most modern passenger vehicles and two-wheelers are now factory-fitted with tubeless tyres.

Fuel Efficiency & Lower TCO

Less rolling resistance means better mileage and lower long-term costs . You get more distance per tank, saving money over time. This efficiency boost fuels market growth.

Electric Vehicle Adoption

EVs require tubeless tyres optimized for load, noise reduction, and energy efficiency.

Growth in Two-Wheeler & Urban Mobility

High penetration in motorcycles and scooters accelerates market expansion in emerging economies.

Global Tubeless Tyres Market Segmentation??

1. By Vehicle Category

1.1 Passenger Vehicles

1.1.1 Hatchbacks

1.1.1.1 Entry-level compact hatchbacks

1.1.1.2 Premium hatchbacks

1.1.2 Sedans

1.1.2.1 Mid-size sedans

1.1.2.2 Full-size sedans

1.1.2.3 Luxury sedans

1.1.3 SUVs & Crossovers

1.1.3.1 Compact SUVs

1.1.3.2 Mid-size SUVs

1.1.3.3 Full-size SUVs

1.2 Two-Wheelers??

1.2.1 Motorcycles

1.2.1.1 Commuter motorcycles

1.2.1.2 Sports & performance motorcycles

1.2.1.3 Adventure & touring motorcycles

1.2.2 Scooters

1.2.2.1 Entry-level scooters

1.2.2.2 Premium scooters

1.2.2.3 Electric scooters

1.3 Commercial Vehicles

1.3.1 Light Commercial Vehicles (LCVs)

1.3.1.1 Pickup trucks

1.3.1.2 Cargo vans

1.3.1.3 Last-mile delivery vehicles

1.3.2 Medium & Heavy Commercial Vehicles (M&HCVs)

1.3.2.1 Medium-duty trucks

1.3.2.2 Heavy-duty trucks

1.3.2.3 Intercity & coach buses

1.4 Off-the-Road (OTR) Vehicles

1.4.1 Construction Equipment

1.4.1.1 Loaders

1.4.1.2 Excavators

1.4.1.3 Dump trucks

1.4.2 Agricultural Machinery

1.4.2.1 Tractors

1.4.2.2 Harvesters

1.4.2.3 Farm utility vehicles

2. By Tyre Construction

2.1 Radial Tubeless Tyres

2.1.1 Steel-Belted Radial Tubeless Tyres

2.1.1.1 Single steel belt

2.1.1.2 Double steel belt

2.1.1.3 Multi-layer steel belt

2.1.2 Fabric-Belted Radial Tubeless Tyres

2.1.2.1 Polyester radial tubeless

2.1.2.2 Nylon radial tubeless

2.2 Bias Tubeless Tyres

2.2.1 Nylon Bias Tubeless Tyres

2.2.1.1 Two-ply nylon

2.2.1.2 Multi-ply nylon

2.2.2 Polyester Bias Tubeless Tyres

2.2.2.1 Light-duty bias tyres

2.2.2.2 Heavy-duty bias tyres

3. By Seasonality

3.1 Summer Tubeless Tyres

3.1.1 Performance Summer Tyres

3.1.1.1 High-speed stability tyres

3.1.1.2 Sports & UHP applications

3.1.2 Touring Summer Tyres

3.1.2 1 Comfort-focused tyres

3.1.2.2 Long-tread-life tyres

3.2 Winter Tubeless Tyres

3.2.1 Studded Winter Tyres

3.2.1.1 Extreme snow & ice applications

3.2.2 Studless Winter Tyres

3.2.2.1 Ice-grip compound tyres

3.2.2.2 Snow-optimized tread tyres

3.3 All-Season Tubeless Tyres??

3.3.1 Standard All-Season Tyres

3.3.1.1 Daily commuter vehicles

3.3.2 Performance All-Season Tyres

3.3.2.1 Performance sedans & SUVs

4. By Sales Channel

4.1 OEM (Original Equipment Manufacturer)

4.1.1 Passenger Vehicle OEM Fitment

4.1.1.1 Hatchback & sedan OEMs

4.1.1.2 SUV & crossover OEMs

4.1.2 Two-Wheeler OEM Fitment

4.1.2.1 Motorcycle OEMs

4.1.2.2 Scooter OEMs

4.1.3 Commercial Vehicle OEM Fitment

4.1.3.1 LCV manufacturers

4.1.3.2 Truck & bus OEMs

4.2 Aftermarket / Replacement

4.2.1 Authorized Dealer Networks

4.2.1.1 Brand-owned dealerships

4.2.2 Independent Tyre Retailers

4.2.2.1 Regional & local tyre shops

4.2.3 Multi-Brand Service Centers

4.2.3.1 Auto service chains

4.2.4 Online & E-Commerce Platforms

4.2.4.1 OEM-backed online stores

4.2.4.2 Third-party marketplaces

5. By Rim Size

5.1 Below 14 Inches

5.1.1 Two-Wheelers

5.1.1.1 Scooters

5.1.1.2 Entry-level motorcycles

5.1.2 Entry-Level Compact Cars

5.2 14???16 Inches

5.2.1 Mass-Market Passenger Vehicles

5.2.1.1 Hatchbacks

5.2.1.2 Compact sedans

5.3 16???18 Inches (Largest Segment)

5.3.1 Sedans

5.3.2 Compact & Mid-Size SUVs

5.4 Above 18 Inches (Fastest-Growing)

5.4.1 Premium SUVs

5.4.2 Performance & Luxury Vehicles

6. By Tyre Technology

6.1 Conventional Tubeless Tyres

6.2 Self-Sealing Tubeless Tyres

6.2.1 Sealant-Based Puncture-Resistant Tyres

6.2.1.1 Passenger vehicles

6.2.1.2 Two-wheelers

6.3 Low Rolling Resistance Tyres

6.3.1 Fuel-Efficient Compound Tyres

6.3.2 EV-Optimized Tubeless Tyres

6.4 Run-Flat Tubeless Tyres

6.4.1 Self-Supporting Run-Flat Tyres

6.4.2 Reinforced Sidewall Tyres

6.5 Smart & Connected Tubeless Tyres

6.5.1 Embedded Pressure & Temperature Sensors

6.5.2 IoT-Enabled Tyre Monitoring Systems

7. By Propulsion Type

7.1 Internal Combustion Engine (ICE) Vehicles

7.1.1 Petrol vehicles

7.1.2 Diesel vehicles

7.2 Electric Vehicles??

7.2.1 Battery Electric Vehicles (BEVs)

7.2.1.1 Passenger EVs

7.2.2.2 Electric two-wheelers

7.2.2 Plug-in Hybrid Electric Vehicles (PHEVs)

8. By Geography

8.1 Asia-Pacific

8.1.1 China

8.1.2 India

8.1.3 Japan

8.1.4 Southeast Asia

8.2 Europe

8.2.1 Germany

8.2.2 France

8.2.3 U.K.

8.2.4 Italy

8.3 North America

8.3.1 U.S.

8.3.2 Canada

8.4 Latin America

8.4.1 Brazil

8.4.2 Mexico

8.5 Middle East & Africa

Regional Insights of Global Tubeless Tyres Market

Asia-Pacific ??? Largest Market

High two-wheeler volumes, expanding passenger vehicle parc, and strong replacement demand drive market leadership.

Europe ??? Fastest Growing

Stringent safety norms, premium vehicle penetration, and EV adoption accelerate tubeless tyre demand.

North America

SUV dominance, long-distance driving, and aftermarket maturity support steady growth.

Latin America

Rising vehicle ownership and improving road infrastructure boost tubeless tyre adoption.

Middle East & Africa

Demand driven by extreme-climate performance requirements and expanding vehicle fleets.

Leading Companies in the Global Tubeless Tyres Market

-

Goodyear Tire & Rubber Company

-

Continental AG

-

Pirelli & C. S.p.A.

-

Sumitomo Rubber Industries

-

Hankook Tire

-

Yokohama Rubber Company

-

Apollo Tyres

-

CEAT Limited

Michelin and Bridgestone are the largest company in the Global Tubeless Tyres Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Analyzes vehicle parc growth, replacement cycles, and tubeless penetration trends.

EV Tyre Requirement Analyzer

Evaluates demand for low-noise, high-load, and energy-efficient tubeless tyres.

Raw Material Sensitivity Model

Tracks rubber, silica, and oil price volatility impacting margins.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate ??? fragmented aftermarket, strong OEMs

-

Supplier Power: Moderate ??? rubber and chemical inputs

-

Threat of New Entrants: Low ??? capital and technology barriers

-

Threat of Substitutes: Low ??? tubeless tyres becoming standard

-

Competitive Rivalry: High ??? global majors vs regional brands

Why the Global Tubeless Tyres Market Remains Critical

-

Enhances road safety and puncture resistance

-

Reduces maintenance and lifecycle costs

-

Improves fuel efficiency and EV range

-

Strong recurring replacement demand

-

Core technology for modern vehicle platforms

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Analyzes vehicle parc growth, replacement cycles, and tubeless penetration trends.

EV Tyre Requirement Analyzer

Evaluates demand for low-noise, high-load, and energy-efficient tubeless tyres.

Raw Material Sensitivity Model

Tracks rubber, silica, and oil price volatility impacting margins.

Automated Porter???s Five Forces (Concise)

-

Buyer Power: Moderate ??? fragmented aftermarket, strong OEMs

-

Supplier Power: Moderate ??? rubber and chemical inputs

-

Threat of New Entrants: Low ??? capital and technology barriers

-

Threat of Substitutes: Low ??? tubeless tyres becoming standard

-

Competitive Rivalry: High ??? global majors vs regional brands

Final Takeaway of Global Tubeless Tyres Market

The Global Tubeless Tyres Market is transitioning from a premium feature to an industry standard across vehicle categories. Driven by safety advantages, fuel efficiency benefits, and EV compatibility, tubeless tyres are rapidly replacing tube-type alternatives worldwide. Manufacturers that invest in advanced sealing technologies, EV-optimized designs, and strong aftermarket networks will be best positioned to lead the market through 2033.

Competitive Landscape

Global Tubeless Tyres Competitive Intensity & Market Structure Overview

The Global Tubeless Tyres Market is characterized by a highly competitive and structurally evolving ecosystem, driven by the rapid transition from tube-type tyres to tubeless technology across passenger vehicles, two-wheelers, and commercial fleets. The market is dominated by global tyre manufacturers that leverage strong OEM partnerships while competing aggressively in the high-volume replacement segment.

The market operates on a dual-structure model where OEM fitment ensures consistent demand and brand positioning, while the aftermarket drives volume growth due to frequent replacement cycles. Competitive intensity remains high as manufacturers compete on safety features, durability, fuel efficiency, and total cost of ownership (TCO).

While Tier 1 players maintain strong control over OEM supply chains, the aftermarket remains fragmented, with regional and mid-tier manufacturers competing on pricing, accessibility, and localized distribution networks, especially in emerging markets.

Global Tubeless Tyres Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global Tyre Leader. Strong in premium tubeless, EV-compatible, and self-sealing tyre technologies.

Bridgestone Corporation: Global Tyre Manufacturer. Extensive OEM partnerships and advanced safety-focused tubeless solutions.

Goodyear Tire & Rubber Company: Innovation-Driven Player. Focus on smart tyres, run-flat, and fuel-efficient tubeless designs.

Continental AG: Technology-Focused Manufacturer. Leader in sensor-enabled and connected tubeless tyre systems.

Pirelli & C. S.p.A.: Premium Segment Specialist. Focus on high-performance and luxury vehicle tubeless tyres.

Sumitomo Rubber Industries: Strong presence in Asia-Pacific with balanced OEM and aftermarket portfolio.

Hankook Tire: Fast-growing global player with expanding EV and premium tubeless tyre offerings.

Yokohama Rubber Company: Known for durable, fuel-efficient, and performance-oriented tubeless tyres.

Apollo Tyres: Competitive player in cost-efficient tubeless tyres across emerging markets.

CEAT Limited: Strong presence in two-wheeler and passenger vehicle tubeless tyre segments in developing regions.

Key Competitive Intensity & Market Structure Signals in Global Tubeless Tyres Market

A major structural signal is the rapid standardization of tubeless tyres across OEM platforms, significantly reducing the relevance of tube-type tyres. This transition intensifies competition among manufacturers to secure OEM contracts and maintain long-term supply agreements.

The aftermarket remains the largest and most competitive segment, driven by high replacement frequency. Consumers and fleet operators prioritize safety, durability, and fuel efficiency, pushing manufacturers to differentiate through self-sealing, run-flat, and low rolling resistance technologies.

Another key signal is the rising influence of electric vehicles and two-wheelers, which demand tubeless tyres optimized for load capacity, noise reduction, and energy efficiency. This is accelerating innovation and competition in EV-compatible tyre segments.

Regional dynamics also play a critical role, with Asia-Pacific witnessing intense price-based competition due to high volumes and cost-sensitive consumers, while Europe focuses on premium, safety-driven, and regulation-compliant tyre solutions.

Strategic Implications of Competitive Intensity & Market Structure in Global Tubeless Tyres Market

Manufacturers are shifting from product-centric strategies to technology-driven and safety-focused offerings. Companies investing in self-sealing, run-flat, and smart tyre technologies are gaining a competitive advantage in both OEM and aftermarket segments.

Total cost of ownership (TCO) is becoming a key decision factor, with customers valuing longer tyre life, reduced maintenance, and improved fuel efficiency over upfront pricing. This trend favors premium and technologically advanced tubeless tyres.

Electrification is reshaping competitive strategies, as EV-compatible tubeless tyres become a critical growth segment. Manufacturers that fail to innovate in low-noise, high-load, and energy-efficient designs risk losing relevance in future mobility markets.

Additionally, digital integration through smart tyre monitoring systems and IoT-enabled solutions is emerging as a new competitive frontier, especially in fleet and high-value vehicle segments.

Global Tubeless Tyres Competitive Intensity & Market Structure Forward Outlook

The Global Tubeless Tyres Market is expected to remain highly competitive with increasing consolidation among leading players and continued fragmentation in regional aftermarket channels.

OEM standardization of tubeless tyres will further strengthen the position of Tier 1 manufacturers, while regional players will continue to compete in price-sensitive and high-volume markets.

Technological advancements in safety, puncture resistance, and smart connectivity will define the next phase of competition. Companies investing in EV-ready and self-sealing technologies will capture significant market share.

In the long term, the market will be shaped by three core competitive pillars: safety innovation, lifecycle cost efficiency, and EV compatibility. Manufacturers aligning with these trends while maintaining strong distribution and OEM partnerships will lead the Global Tubeless Tyres Market through 2033.

Value Chain

Global Tubeless Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain of the Global Tubeless Tyres Market are highly integrated, spanning raw material sourcing, advanced manufacturing, OEM partnerships, distribution networks, and aftermarket service ecosystems. This market operates through a dual-demand structure’OEM fitment for new vehicles and a dominant replacement cycle driven by continuous tyre wear across passenger vehicles, two-wheelers, and commercial fleets. Tubeless tyres require higher precision engineering compared to tube-type tyres, particularly in airtight sealing, bead design, and advanced rubber compounds. This increases dependency on quality raw materials, manufacturing consistency, and strong OEM alignment, making the value chain more technology-driven and quality-focused. Upstream supply is anchored in natural rubber, synthetic rubber, carbon black, silica, steel cords, and specialty sealant compounds used in self-sealing tyres. Leading players such as Michelin, Bridgestone, Goodyear, and Continental maintain global sourcing networks and long-term supplier contracts to manage input cost volatility and ensure consistent material quality. Manufacturing focuses on airtight construction, precision bead fitting, heat resistance, and durability optimization. Increasingly, companies are integrating self-sealing layers, run-flat technologies, and EV-compatible compounds to enhance safety and performance. Automation and quality control systems are critical to maintaining defect-free production at scale. Distribution is a mix of OEM supply agreements and extensive aftermarket networks, including authorized dealers, independent retailers, service centers, and digital platforms. The aftermarket dominates revenue due to predictable replacement cycles, especially in high-usage segments such as two-wheelers and commercial vehicles. Supply chain challenges include raw material price fluctuations, logistics inefficiencies, and rising regulatory pressures related to sustainability and emissions. Additionally, manufacturers face increasing expectations to develop EV-compatible tyres, low rolling resistance designs, and environmentally sustainable materials.

Global Tubeless Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The current supply chain landscape of the Global Tubeless Tyres Market is stable but undergoing steady transformation driven by safety standardization, electrification, and growing demand for advanced tyre technologies. At the upstream level, volatility in rubber and petrochemical inputs continues to impact production costs. Manufacturers are responding with diversified sourcing strategies, long-term procurement contracts, and material innovation to reduce dependency on traditional inputs. Manufacturing is increasingly focused on high-performance tubeless designs, including self-sealing tyres, run-flat systems, and EV-optimized tyres with low rolling resistance and noise reduction capabilities. Companies are also investing in automation and digital quality control to enhance production efficiency and consistency. OEM integration is strengthening as tubeless tyres become the standard across passenger vehicles and two-wheelers. Automakers are aligning closely with tyre manufacturers to ensure compatibility with safety regulations, fuel efficiency targets, and EV performance requirements. The aftermarket remains the largest revenue contributor, supported by strong replacement demand across all vehicle categories. Consumers and fleet operators are increasingly prioritizing safety, durability, and long-term cost efficiency, driving demand for premium tubeless tyres. Digital transformation is gradually influencing distribution channels, with online tyre sales platforms, digital inventory systems, and service scheduling tools improving accessibility and customer experience.

Key Value Chain & Supply Chain Evolution Signals in Global Tubeless Tyres Market

Several structural trends are shaping the evolution of the tubeless tyre value chain. First, OEM standardization of tubeless tyres is accelerating globally, making them the default choice for most vehicle categories and reducing the relevance of tube-type alternatives. Second, safety-focused innovation is driving the adoption of self-sealing and run-flat technologies, enhancing product value and differentiation. Third, the rise of electric vehicles is pushing demand for specialized tubeless tyres with low rolling resistance, high load capacity, and noise reduction features. Fourth, the dominance of the aftermarket segment continues due to predictable wear cycles, reinforcing the importance of distribution networks and service infrastructure. Finally, digitalization is improving supply chain efficiency through online sales platforms, inventory optimization, and data-driven demand forecasting.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Tubeless Tyres Market

Leading companies such as Michelin, Bridgestone, Goodyear, and Continental leverage strong OEM relationships, global manufacturing footprints, and advanced R&D capabilities to maintain competitive advantage. The increasing technological complexity of tubeless tyres’especially with self-sealing, run-flat, and EV-compatible features’raises entry barriers, favoring established global players. Aftermarket dominance creates opportunities for recurring revenue through replacement cycles, while also emphasizing the importance of brand loyalty and distribution reach. Cost management remains critical, as manufacturers balance raw material price volatility with investments in advanced technologies and sustainability initiatives. The transition toward electric mobility presents both a challenge and opportunity, requiring continuous innovation in tyre design while unlocking high-growth premium segments.

Global Tubeless Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the tubeless tyres value chain is expected to become more technology-driven, efficient, and sustainability-focused. Manufacturers will increasingly invest in EV-optimized tyres, self-sealing technologies, and sustainable materials such as bio-based rubber and recycled components. Circular economy practices, including recycling and retreading (where applicable), will gain importance. The aftermarket segment will continue to dominate, supported by growing global vehicle parc and consistent replacement demand across two-wheelers, passenger vehicles, and commercial fleets. Digital distribution channels will expand further, with e-commerce platforms, direct-to-consumer models, and integrated service solutions becoming more prominent. Overall, the future value chain will be defined by safety innovation, EV compatibility, and lifecycle optimization, with companies that align product performance with cost efficiency and sustainability gaining long-term competitive advantage.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, carbon black, silica, steel cord, sealant compounds sourcing

- Research & Development: Self-sealing tyres, run-flat technology, EV-compatible designs, low rolling resistance engineering

- Manufacturing: Airtight tyre production, bead design, curing, and high-precision quality testing

- OEM Integration: Supply of tubeless tyres for passenger vehicles, two-wheelers, commercial vehicles, and EV platforms

- Distribution & Retail: Authorized dealers, independent retailers, service centers, and online platforms

- Aftermarket Services: Replacement tyres, puncture repair, maintenance services, and digital tyre monitoring solutions

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Apollo Tyres

- Distribution & Retail: Goodyear Tire & Rubber Company, Apollo Tyres, CEAT Limited, Yokohama Rubber Company

- Aftermarket Services: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

Investment Activity

Global Tubeless Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Tubeless Tyres Market are driven by the rapid transition from tube-type to tubeless tyre technologies, supported by rising safety awareness, increasing vehicle production, and growing adoption of electric mobility. Between 2026 and 2033, capital allocation is expected to focus on advanced sealing technologies, low rolling resistance compounds, and EV-optimized tubeless tyre designs.

The market exhibits moderate to high capital intensity, requiring investments in precision manufacturing, airtight bead design, advanced rubber compounds, and smart tyre integration. Leading players such as Michelin, Bridgestone, Goodyear, and Continental are investing heavily in R&D and expanding global production capacity to meet rising demand across passenger vehicles, two-wheelers, and commercial fleets.

A major structural shift influencing investments is the increasing demand for safety-enhanced tyres, including self-sealing and run-flat technologies. These innovations are attracting funding aimed at improving puncture resistance, durability, and overall driving reliability.

Global Tubeless Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly aligned with OEM standardization of tubeless tyres across most vehicle categories. Automakers are increasingly integrating tubeless tyres as default fitment, driving consistent demand for advanced tyre solutions.

Asia-Pacific dominates as the largest investment hub, supported by high vehicle production volumes, strong two-wheeler demand, and expanding replacement markets in countries such as China and India.

Europe is the fastest-growing investment region, driven by stringent safety regulations, increasing EV adoption, and strong demand for premium and high-performance tubeless tyres.

North America remains a mature and stable market, with investments focused on SUV and light truck segments, as well as advanced tyre technologies such as run-flat and smart tyres.

Latin America and the Middle East & Africa are witnessing gradual investment growth, supported by increasing vehicle ownership and improving road infrastructure.

Key Investment & Funding Dynamics Signals in Global Tubeless Tyres Market

A key investment signal is the global shift toward tubeless tyres as the industry standard, replacing traditional tube-type tyres across passenger and two-wheeler segments.

Rising safety awareness among consumers is driving demand for self-sealing and puncture-resistant tyres, encouraging investments in advanced material technologies.

Strong replacement demand ensures stable and recurring revenue streams, supporting long-term capital investment across aftermarket channels.

The rapid growth of electric vehicles is accelerating investments in EV-specific tubeless tyres designed for higher loads, reduced noise, and improved energy efficiency.

Technological advancements, including smart and sensor-enabled tyres, are emerging as new investment areas aligned with connected mobility trends.

Strategic Implications of Investment & Funding Dynamics in Global Tubeless Tyres Market

The investment landscape favors companies with strong innovation capabilities in sealing technologies, compound development, and EV compatibility.

OEM partnerships are critical for securing long-term demand, as tubeless tyres are increasingly integrated as standard fitment across vehicle platforms.

The shift toward premium and technology-driven tyres is increasing market differentiation, making R&D investment a key competitive factor.

Regional diversification is essential, with Asia-Pacific driving volume growth, Europe leading regulatory-driven innovation, and North America focusing on high-performance applications.

Raw material price volatility, particularly in rubber and petrochemical derivatives, continues to impact margins and influence investment strategies.

Global Tubeless Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Tubeless Tyres Market is expected to attract sustained investment driven by increasing vehicle parc, rising safety standards, and continued electrification of mobility.

Future capital allocation will prioritize self-sealing technologies, run-flat innovations, EV-optimized tyre designs, and smart tyre integration.

Asia-Pacific will remain the largest investment destination due to its scale and growth potential, while Europe will lead in safety-driven and sustainability-focused innovations.

North America will continue to see strong investments in premium and performance-oriented tubeless tyres, particularly for SUVs and electric vehicles.

Overall, the market will continue its transition toward advanced, safety-focused, and connected tyre solutions, with innovation and efficiency shaping investment strategies through 2033.

Technology & Innovation

Global Tubeless Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Tubeless Tyres Market is driven by safety, efficiency, durability, and evolving vehicle requirements across passenger vehicles, two-wheelers, commercial fleets, and electric mobility. Tubeless tyre technology eliminates the need for an inner tube by creating an airtight seal between the tyre and rim, significantly improving reliability and reducing the risk of sudden air loss.

Innovation intensity in this market is steadily increasing as manufacturers focus on enhancing puncture resistance, fuel efficiency, ride comfort, and lifecycle performance. Leading players such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are investing in advanced sealing technologies, lightweight materials, and EV-compatible designs to strengthen their market position.

A major technological shift is the integration of self-sealing and run-flat capabilities into tubeless tyres. These innovations allow vehicles to continue operating even after minor punctures, significantly improving safety and reducing downtime. Additionally, advancements in compound chemistry and structural design are enabling tubeless tyres to deliver superior performance across a wide range of operating conditions.

Global Tubeless Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the market is dominated by radial tubeless tyres, which offer improved fuel efficiency, heat dissipation, and longer tread life compared to traditional alternatives. Steel-belted radial constructions are widely adopted across passenger vehicles and commercial fleets due to their superior performance characteristics.

Self-sealing tyre technology is gaining strong traction, particularly in passenger vehicles and two-wheelers. These tyres incorporate sealant layers that automatically close punctures, reducing the risk of air leakage and enhancing driver safety.

Run-flat tubeless tyres are another key innovation area, allowing vehicles to travel a limited distance even after complete air loss. Reinforced sidewalls and advanced structural designs enable continued mobility, which is especially valuable in premium and safety-focused vehicle segments.

Low rolling resistance technologies are being widely implemented to improve fuel efficiency and extend electric vehicle driving range. Silica-rich compounds and optimized tread patterns reduce energy loss while maintaining grip and braking performance.

Smart and connected tyre technologies are emerging, with embedded sensors providing real-time data on pressure, temperature, and wear. These capabilities support predictive maintenance and enhance overall vehicle safety and efficiency.

Manufacturing innovation is also advancing, with automation, AI-driven inspection systems, and sustainable material integration improving product consistency and reducing environmental impact.

Key Technology & Innovation Landscape Signals in Global Tubeless Tyres Market

- Self-Sealing Technology: Automatic puncture sealing for enhanced safety and reduced downtime.

- Run-Flat Capabilities: Continued mobility after air loss using reinforced sidewall designs.

- Low Rolling Resistance Compounds: Improved fuel efficiency and extended EV driving range.

- Radial Tubeless Dominance: Superior durability, comfort, and heat management.

- Smart & Connected Tyres: Real-time monitoring of tyre health and performance.

- EV-Optimized Designs: High load-bearing capacity and noise reduction for electric vehicles.

- Sustainable Materials Adoption: Increased use of eco-friendly and recycled compounds.

Strategic Implications of Technology & Innovation Landscape in Global Tubeless Tyres Market

The growing importance of safety and efficiency is driving continuous investment in advanced tubeless tyre technologies. Manufacturers must prioritize innovation in self-sealing, run-flat, and low rolling resistance solutions to meet evolving consumer and regulatory expectations.

The expansion of electric vehicles is reshaping product development strategies. Tyre manufacturers need to develop EV-specific tubeless tyres capable of handling higher loads, reducing noise, and improving energy efficiency.

Strong replacement demand creates opportunities for aftermarket growth, encouraging companies to expand distribution networks and service capabilities. Differentiation through technology and performance is becoming critical in a highly competitive market.

Smart tyre technologies are enabling a shift toward data-driven mobility ecosystems. Predictive maintenance and real-time monitoring are opening new service-based revenue streams beyond traditional tyre sales.

Sustainability is emerging as a core strategic focus, with increasing adoption of recyclable materials, energy-efficient manufacturing processes, and circular economy practices.

Global Tubeless Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the tubeless tyres market is expected to witness continuous innovation focused on safety, efficiency, and connectivity. Self-sealing and run-flat technologies are likely to become standard features across a broader range of vehicle categories.

Electric vehicle growth will further accelerate demand for specialized tubeless tyres optimized for range, load capacity, and noise reduction. Advanced materials and lightweight designs will play a key role in improving performance and sustainability.

Smart tyre systems are expected to gain widespread adoption, enabling real-time diagnostics, predictive maintenance, and integration with connected vehicle platforms.

Manufacturing processes will continue to evolve with increased automation, digitalization, and sustainable practices, improving production efficiency and reducing environmental impact.

In conclusion, the Global Tubeless Tyres Market is transitioning into a technology-driven and safety-focused ecosystem. Companies that invest in advanced sealing technologies, EV-compatible designs, smart connectivity, and sustainable materials will be best positioned to lead the market through 2033.A

Market Risk

Global Tubeless Tyres Market Risk Factors & Disruption Threats Overview

The Global Tubeless Tyres Market operates within a highly competitive and volume-driven automotive ecosystem, supported by rising vehicle production, strong replacement demand, and increasing safety awareness. While the market benefits from its transition into a standard tyre technology, it carries a moderate risk profile due to raw material dependency, pricing pressure, and evolving vehicle technologies. A key structural risk is volatility in raw material prices, particularly natural rubber, synthetic rubber, silica, and petrochemical derivatives. These inputs significantly influence production costs, and fluctuations can directly impact manufacturer margins in a price-sensitive and competitive market. Another major risk factor is intense pricing competition across global and regional players. The aftermarket is highly fragmented, and price-driven purchasing behavior can limit profitability, especially in emerging markets where cost sensitivity is high. Product performance expectations also pose operational risks. Tubeless tyres must ensure airtight sealing, puncture resistance, durability, and compatibility with varying road conditions. Failures in performance can impact brand reputation and increase warranty costs. Additionally, the rapid shift toward electric vehicles (EVs) introduces disruption, requiring tubeless tyres to support higher loads, lower rolling resistance, and reduced noise levels, thereby increasing R&D complexity and cost structures.

Global Tubeless Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects steady growth driven by increasing vehicle parc, rising OEM adoption, and strong replacement cycles. However, the industry faces ongoing challenges from fluctuating input costs, competitive pricing pressures, and evolving performance requirements. Raw material cost inflation continues to impact manufacturing economics, forcing companies to optimize pricing strategies while maintaining product quality and competitiveness. The aftermarket dominates revenue generation, supported by predictable wear cycles. However, increasing penetration of organized retail chains, online platforms, and multi-brand service networks is reshaping distribution dynamics. OEM demand is rising as tubeless tyres become standard across passenger vehicles and two-wheelers. At the same time, EV adoption is creating new performance benchmarks, pushing manufacturers to innovate continuously. Supply chain disruptions, particularly in rubber and chemical inputs, can affect production timelines and inventory management, especially during periods of global economic uncertainty.

Key Risk Factors & Disruption Threats Signals in Global Tubeless Tyres Market

A major disruption signal is the rapid growth of electric mobility. EV-specific requirements such as low rolling resistance, noise reduction, and high load-bearing capacity are reshaping tyre design priorities. Increasing adoption of self-sealing and run-flat technologies is another key signal, indicating a shift toward enhanced safety and convenience-driven product innovation. Digitalization and smart tyre integration are emerging trends, with sensors and IoT-enabled systems enabling real-time monitoring and predictive maintenance capabilities. Rising consumer awareness around safety and fuel efficiency is influencing purchasing decisions, accelerating the shift from tube-type to advanced tubeless tyre solutions. Sustainability pressures are also gaining traction, driving demand for eco-friendly materials, recyclable components, and low-emission manufacturing processes.

Strategic Implications of Risk Factors & Disruption Threats in Global Tubeless Tyres Market

Manufacturers must focus on continuous innovation to enhance safety, durability, and performance, particularly in areas such as self-sealing technologies and EV-compatible designs. Strengthening aftermarket distribution networks and digital sales channels is critical to capture replacement demand and improve customer reach. Strategic partnerships with OEMs are essential, as factory-fitment opportunities continue to expand with increasing vehicle production and standardization of tubeless tyres. Cost optimization and raw material sourcing diversification are necessary to manage margin pressures and ensure supply chain stability. Investment in smart tyre technologies and connected solutions can provide a competitive edge by enabling value-added services such as predictive maintenance and real-time monitoring.

Global Tubeless Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Tubeless Tyres Market is expected to maintain steady growth, supported by increasing vehicle ownership, safety awareness, and EV adoption. However, the risk landscape will become more technology-driven and innovation-intensive. Electric mobility will remain a key disruption factor, requiring continuous advancements in tyre design to meet evolving performance and efficiency standards. The integration of smart technologies and IoT-enabled monitoring systems will reshape competitive dynamics, shifting focus toward intelligent and connected tyre solutions. Sustainability will play a larger role, with manufacturers investing in recyclable materials, low rolling resistance designs, and environmentally friendly production processes. Overall, the market will continue transitioning toward advanced, safety-focused, and performance-driven solutions, with long-term success dependent on innovation, cost efficiency, and strong OEM and aftermarket positioning.

Regulatory Landscape

Global Tubeless Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Tubeless Tyres Market plays a crucial role in accelerating the transition from tube-type tyres to tubeless technologies. As governments and automotive regulators prioritize road safety, fuel efficiency, and environmental sustainability, tubeless tyres are increasingly becoming the preferred standard across passenger vehicles, two-wheelers, and commercial fleets.

Key regulatory frameworks such as the European Union Tyre Labelling Regulation (EU) 2020/740 and UNECE tyre safety standards establish mandatory benchmarks for rolling resistance, wet grip, and external noise. Tubeless tyres inherently align with these requirements due to their lower rolling resistance, improved heat dissipation, and enhanced safety performance, making them highly compliant with global regulatory expectations.

In addition, vehicle safety regulations across major automotive markets increasingly emphasize puncture resistance, stability, and reduced risk of sudden tyre failure. Tubeless tyres, with their ability to maintain air pressure even after minor punctures, are strongly favored under such frameworks, supporting their widespread adoption.

Emerging economies such as India, China, Brazil, and Southeast Asian countries are strengthening tyre quality standards, homologation requirements, and vehicle inspection systems. These initiatives are accelerating the penetration of tubeless tyres, particularly in two-wheelers and entry-level passenger vehicles.

Global Tubeless Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is defined by increasing focus on safety, efficiency, and electrification. Europe leads as the most advanced regulatory region, where tyre labeling and safety compliance significantly influence OEM fitment and aftermarket purchasing decisions.

In Europe, stringent safety and environmental regulations are driving near-complete adoption of tubeless tyres across passenger vehicles and growing penetration in two-wheelers. Noise reduction norms and EV-related performance requirements further support demand for advanced tubeless tyre technologies.

In Asia-Pacific, rapid motorization, high two-wheeler volumes, and government-led safety initiatives are accelerating the shift toward tubeless tyres. Countries such as India are witnessing increasing regulatory emphasis on vehicle safety standards, boosting adoption in both OEM and replacement markets.

North America maintains strong regulatory oversight through DOT and NHTSA frameworks, promoting high-performance and safety-compliant tyre solutions. Tubeless tyres dominate the region due to their reliability, durability, and compatibility with long-distance driving conditions.

The rapid growth of electric vehicles globally is also influencing regulatory trends, as EV-specific requirements such as low rolling resistance, high load-bearing capacity, and noise reduction further reinforce the adoption of tubeless tyre technologies.

Key Regulatory & Policy Environment Signals in Global Tubeless Tyres Market

- EU Tyre Labelling Regulation (EU 2020/740): Promotes fuel efficiency, wet grip, and noise transparency, favoring tubeless tyre adoption.

- UNECE Tyre Safety Standards: Define global benchmarks for durability, performance, and structural integrity.

- Vehicle Safety Regulations: Encourage puncture-resistant and blowout-safe tyre technologies, supporting tubeless tyres.

- Fuel Efficiency & Emission Norms: Drive adoption of low rolling resistance tyres, strengthening tubeless penetration.

- Electric Vehicle Policies: Promote EV-compatible tubeless tyres with enhanced efficiency and noise optimization.

- Emerging Market Certification Programs: Improve tyre quality standards and accelerate transition from tube to tubeless systems.

Strategic Implications of Regulatory & Policy Environment in Global Tubeless Tyres Market

The regulatory environment significantly favors tubeless tyre technologies, accelerating their transition from optional upgrades to standard fitment across vehicle categories. This shift raises entry barriers, requiring manufacturers to invest in advanced materials, airtight sealing technologies, and compliance capabilities.

Manufacturers focusing on tube-type tyres face declining regulatory support and must transition toward tubeless and advanced variants such as self-sealing and run-flat tyres to remain competitive.

Compliance-driven innovation is becoming a key differentiator. Investments in low rolling resistance compounds, puncture-resistant designs, and smart tyre technologies are essential to meet evolving regulatory and consumer expectations.

OEMs and fleet operators are increasingly guided by regulatory labeling systems and safety standards, shifting procurement decisions toward certified, high-performance tubeless tyres that offer improved safety, durability, and efficiency.

Regional regulatory variations are shaping supply chain strategies, encouraging localized production, partnerships with OEMs, and development of market-specific product portfolios to ensure compliance and cost efficiency.

Global Tubeless Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become more stringent and safety-focused, further reinforcing the global dominance of tubeless tyre technologies. Governments will continue tightening safety, fuel efficiency, and emission standards across all vehicle categories.

Europe will continue to lead with advanced safety and sustainability regulations, including lifecycle emissions and tyre performance transparency. Asia-Pacific will accelerate adoption through enhanced safety mandates and rapid motorization.

The expansion of electric vehicles will introduce new regulatory requirements focused on energy efficiency, noise reduction, and load optimization, all of which strongly align with tubeless tyre capabilities.

Advanced technologies such as self-sealing, run-flat, and smart connected tubeless tyres are expected to gain regulatory support, particularly in premium and EV segments.

Overall, the regulatory landscape will act as a strong catalyst driving innovation, standardization, and global adoption of tubeless tyres. Manufacturers that align with evolving safety and sustainability regulations while advancing product innovation will be best positioned to lead the market through 2033.