Global Audio Critical Communication Market Report, Size, Share and Forecast 2026–2033

Global Audio Critical Communication Market Forecast Snapshot (2026???2033)

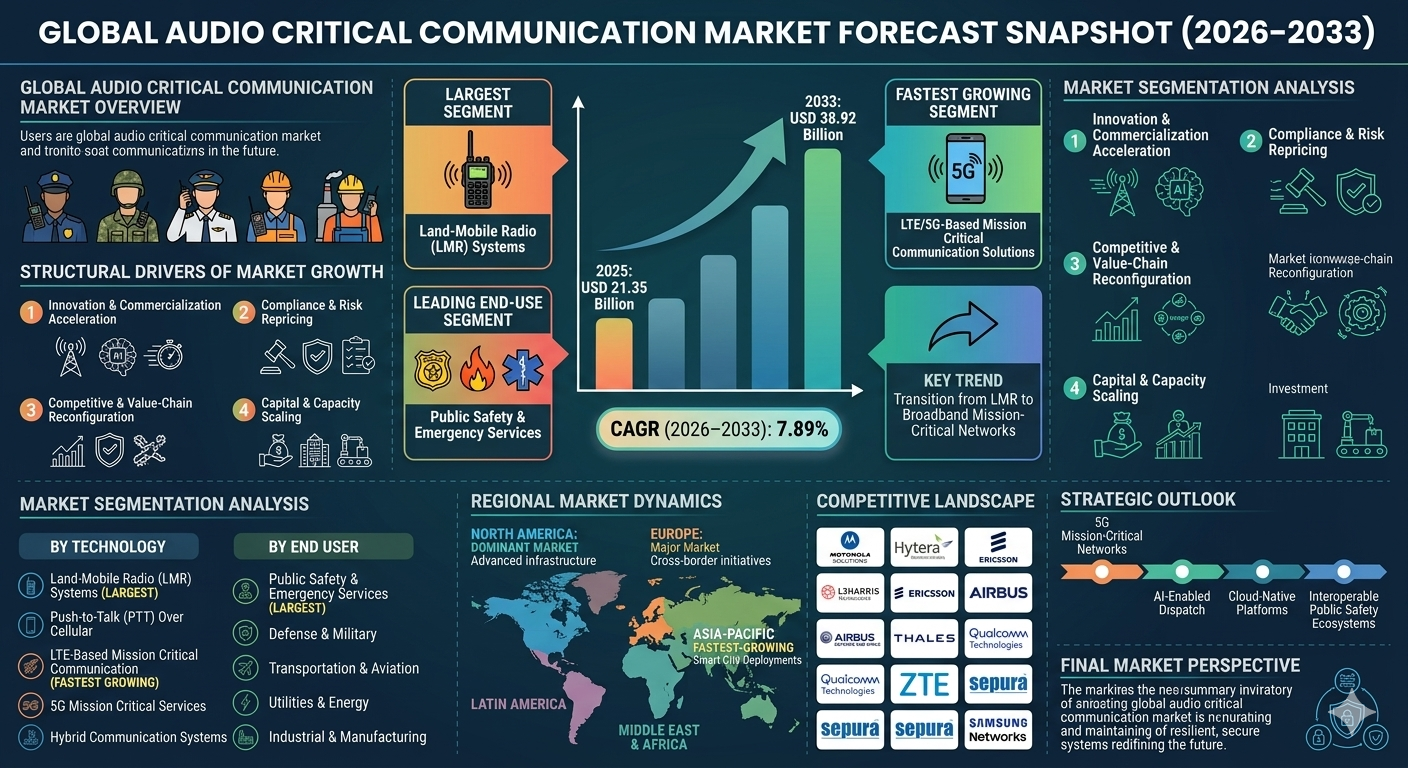

| Metric | Value |

|---|---|

| Market Size (2025) | USD 21.35 Billion |

| Market Size (2033) | USD 38.92 Billion |

| CAGR (2026???2033) | 7.89% |

| Largest Segment | Land-Mobile Radio (LMR) Systems |

| Fastest Growing Segment | LTE/5G-Based Mission Critical Communication Solutions |

| Leading End-Use Segment | Public Safety & Emergency Services |

| Key Trend | Transition from LMR to Broadband Mission-Critical Networks |

| Regulatory Influence | Public Safety Communication Standards, Spectrum Allocation Policies & Emergency Response Protocols |

| Future Outlook | Growth Driven by Digital Public Safety Infrastructure, 5G Adoption & Interoperable Communication Systems |

Global Audio Critical Communication Market

Market Size & Forecast

The Global Audio Critical Communication Market is expected to witness steady expansion during the forecast period from 2026 to 2033. The market was valued at USD 21.35 billion in 2025 and is projected to reach approximately USD 38.92 billion by 2033, registering a CAGR of 7.89%. The market growth is primarily driven by increasing demand for reliable real-time communication in emergency response, public safety modernization programs, transportation safety systems, and industrial mission-critical operations. Audio critical communication systems are essential for ensuring uninterrupted voice communication in mission-critical environments such as law enforcement, fire services, military operations, airports, utilities, and industrial plants. The increasing shift toward broadband-enabled communication networks is accelerating market transformation. In addition, rising investments in smart cities, disaster management systems, and national security infrastructure are supporting long-term market expansion.

Global Audio Critical Communication Market Overview

Audio critical communication refers to secure, high-reliability voice communication systems used in mission-critical environments where failure is not an option. The market includes land-mobile radio (LMR) systems, push-to-talk (PTT) over cellular, LTE/5G mission-critical services, dispatch systems, integrated communication platforms, and interoperable emergency networks. These systems are widely used across public safety agencies, defense organizations, transportation authorities, utilities, oil & gas operations, and industrial facilities. The market is shifting from traditional narrowband radio systems toward broadband-enabled, IP-based, and AI-enhanced communication ecosystems that support data, video, and voice integration.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in 5G mission-critical communications, AI-assisted dispatch systems, cloud-based control platforms, and interoperable communication networks is transforming operational efficiency. Advanced communication technologies are improving response times, coordination, and situational awareness in emergency environments.Market Implications

Companies investing in broadband mission-critical platforms, secure communication protocols, and integrated command systems are expected to strengthen market leadership.2. Compliance and Risk Repricing

Public safety communication regulations, spectrum management policies, national security standards, and emergency response compliance frameworks are influencing system modernization. Governments are increasingly mandating interoperable and resilient communication infrastructure.Market Implications

Firms offering compliant, secure, and interoperable communication solutions are likely to gain stronger government and enterprise adoption.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as telecom providers, defense contractors, communication equipment manufacturers, and software vendors expand mission-critical offerings. Convergence of telecom, IT, and public safety communication ecosystems is reshaping value-chain structures.Market Implications

Companies focusing on integrated LTE/5G communication ecosystems and unified dispatch platforms may gain stronger long-term contracts.4. Capital and Capacity Scaling

Rising investments in 5G infrastructure, public safety networks, command centers, and digital communication modernization programs are supporting market expansion. Governments worldwide are upgrading legacy radio systems to broadband-enabled platforms.Market Implications

Operators scaling secure broadband infrastructure and mission-critical network deployments are expected to capture future opportunities.Market Segmentation Analysis

By Technology

1. Land-Mobile Radio (LMR) Systems

This remains the largest segment due to established public safety infrastructure.2. Push-to-Talk (PTT) Over Cellular

Growing adoption due to smartphone integration and flexibility.3. LTE-Based Mission Critical Communication

Fastest-growing segment driven by broadband transition.4. 5G Mission Critical Services

Emerging segment enabling ultra-low latency communication.5. Hybrid Communication Systems

Used for interoperability between legacy and modern systems.By End User

1. Public Safety & Emergency Services

Largest segment due to critical operational requirements.2. Defense & Military

Strong demand for secure and resilient communication systems.3. Transportation & Aviation

Used for real-time operational coordination.4. Utilities & Energy

Essential for field communication and infrastructure monitoring.5. Industrial & Manufacturing

Growing adoption for workplace safety and coordination.Regional Market Dynamics

North America

North America dominates the market due to advanced public safety infrastructure, early 5G adoption, and strong defense communication investments.Europe

Europe remains a major market supported by cross-border emergency communication initiatives and digital public safety programs.Asia-Pacific

Asia-Pacific is the fastest-growing region due to smart city deployments, infrastructure modernization, and expanding public safety networks.Latin America

Latin America is gradually expanding due to modernization of emergency response systems and telecom upgrades.Middle East & Africa

The region is witnessing emerging growth driven by smart city projects and national security investments.Competitive Landscape

The Global Audio Critical Communication Market is highly competitive with telecom providers, defense contractors, and communication technology firms expanding globally.Key Companies Operating in the Market Include:

- Motorola Solutions

- Hytera Communications

- L3Harris Technologies

- Ericsson

- Airbus Defence and Space

- Thales Group

- Qualcomm Technologies

- ZTE Corporation

- Sepura Limited

- Samsung Networks

Strategic Outlook

The future of the audio critical communication market will be shaped by 5G mission-critical networks, AI-enabled dispatch systems, cloud-native communication platforms, and fully interoperable public safety ecosystems. The transition from legacy LMR systems to broadband-enabled communication infrastructure will significantly enhance operational efficiency and situational awareness. The rise of smart cities, digital emergency response systems, and integrated defense communication networks is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Audio Critical Communication Market remains a foundational segment within public safety, defense, and industrial communication ecosystems. Rising demand for reliable, secure, and real-time communication continues driving long-term market growth. Companies capable of delivering resilient, interoperable, and next-generation broadband communication systems will be best positioned to capture future opportunities. The convergence of 5G, AI, and mission-critical networking is expected to redefine the future of global critical communication infrastructure.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Audio Critical Communication Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Audio Critical Communication Market

- 2.2 Scope of the Study

- 2.3 Evolution of Mission-Critical Communication Systems

- 2.4 Communication Infrastructure Ecosystem Analysis

- 2.5 Regulatory & Spectrum Allocation Framework

- 2.6 Public Safety Communication Trends

- 2.7 Broadband Mission-Critical Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Public Safety Infrastructure Modernization

- 4.1.2 Rising Demand for Real-Time Communication

- 4.1.3 Transition from LMR to LTE/5G Networks

- 4.1.4 Smart City Communication Deployment

- 4.1.5 Defense & Emergency Communication Investments

- 4.2 Restraints

- 4.2.1 High Infrastructure Deployment Costs

- 4.2.2 Legacy System Integration Complexity

- 4.2.3 Spectrum Allocation Constraints

- 4.2.4 Cybersecurity Risks

- 4.3 Opportunities

- 4.3.1 5G Mission-Critical Communication Expansion

- 4.3.2 Cloud-Based Dispatch Platforms

- 4.3.3 AI-Powered Emergency Coordination

- 4.3.4 Interoperable Communication Ecosystems

- 4.4 Challenges

- 4.4.1 Cross-Network Interoperability

- 4.4.2 Security & Data Privacy Requirements

- 4.4.3 Regulatory Standardization Across Regions

- 4.4.4 Migration from Legacy Systems

- 4.1 Drivers

- 5. Global Audio Critical Communication Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Technology Adoption Trends

- 5.5 End-User Demand Analysis

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Technology

- 6.1.1 Land-Mobile Radio (LMR) Systems

- 6.1.2 Push-to-Talk (PTT) Over Cellular

- 6.1.3 LTE-Based Mission Critical Communication

- 6.1.4 5G Mission Critical Services

- 6.1.5 Hybrid Communication Systems

- 6.2 By End User

- 6.2.1 Public Safety & Emergency Services

- 6.2.2 Defense & Military

- 6.2.3 Transportation & Aviation

- 6.2.4 Utilities & Energy

- 6.2.5 Industrial & Manufacturing

- 6.1 By Technology

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Technology Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Product Innovation Analysis

- 8.5 Competitive Positioning Strategies

- 9. Company Profiles

- 9.1 Motorola Solutions

- 9.2 Hytera Communications

- 9.3 L3Harris Technologies

- 9.4 Ericsson

- 9.5 Airbus Defence and Space

- 9.6 Thales Group

- 9.7 Qualcomm Technologies

- 9.8 ZTE Corporation

- 9.9 Sepura Limited

- 9.10 Samsung Networks

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Mission-Critical Communication Forecast Engine

- 10.2 Public Safety Network Analytics Dashboard

- 10.3 Emergency Response Optimization Tracker

- 10.4 Technology Opportunity Analyzer

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of LTE/5G Critical Networks

- 11.2 AI-Driven Dispatch System Adoption

- 11.3 Strengthening Interoperability Standards

- 11.4 Secure Broadband Infrastructure Investments

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Audio Critical Communication Market Competitive Intensity & Market Structure Overview

The global audio critical communication market is highly competitive and moderately consolidated, dominated by established telecom infrastructure providers, defense communication specialists, and mission-critical system integrators. Competitive intensity is primarily driven by technological migration from LMR to LTE/5G networks, system reliability requirements, interoperability standards, cybersecurity capabilities, and long-term government procurement contracts.

The market structure is characterized by legacy land-mobile radio (LMR) system providers coexisting with next-generation broadband communication solution vendors. Increasing convergence between telecom operators, defense contractors, and software-defined communication platforms is reshaping competitive boundaries.

Rising demand for real-time emergency response communication, smart city deployments, and national security modernization programs is significantly intensifying competition across the global audio critical communication market.

Global Audio Critical Communication Market Competitive Intensity & Market Structure Current Scenario

Leading Global Audio Critical Communication Companies

Motorola Solutions: Global leader in mission-critical communication systems with strong dominance in public safety and LMR-to-broadband transition solutions.

Hytera Communications: Major global competitor offering a wide portfolio of digital radio and broadband communication solutions.

L3Harris Technologies: Key defense and aerospace communication provider specializing in secure mission-critical systems.

Ericsson: Leading telecom infrastructure provider expanding into 5G mission-critical communication networks and private 5G solutions.

Airbus Defence and Space: Strong player in secure government communication systems and TETRA-based public safety networks.

Thales Group: Major defense technology company offering integrated secure communication and command systems.

Qualcomm Technologies: Key enabler of 5G chipset and communication technologies supporting mission-critical broadband connectivity.

ZTE Corporation: Telecom equipment provider expanding into broadband and emergency communication infrastructure.

Sepura Limited: Specialist in digital radio communication systems widely used in public safety and transportation sectors.

Samsung Networks: Emerging competitor in 5G infrastructure and private network solutions for mission-critical applications.

Key Competitive Intensity & Market Structure Drivers

Transition from LMR systems to LTE and 5G-based mission-critical networks is accelerating technological competition.

Increasing demand for interoperable communication systems across emergency services is pushing vendors toward integrated platform development.

Government procurement cycles and long-term infrastructure contracts are reinforcing consolidation among established players.

Rising cybersecurity threats are intensifying the need for secure, encrypted, and resilient communication systems.

Expansion of smart cities and digital public safety initiatives is driving adoption of broadband-enabled communication ecosystems.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly investing in LTE/5G mission-critical platforms to replace legacy narrowband radio infrastructure.

Strategic partnerships between telecom operators and public safety agencies are becoming essential for large-scale deployment.

Software-defined communication systems and cloud-based dispatch platforms are emerging as key differentiation factors.

Defense-grade encryption, network redundancy, and ultra-reliable low-latency communication capabilities are becoming critical competitive requirements.

Vertical integration across hardware, software, and network services is strengthening long-term contract stability and market positioning.

Global Audio Critical Communication Market Competitive Intensity & Market Structure Forward Outlook

The global audio critical communication market is expected to remain highly competitive as governments and enterprises accelerate modernization of public safety and emergency communication systems.

Future competition will increasingly focus on 5G standalone mission-critical networks, AI-enabled dispatch intelligence, cloud-native communication platforms, and fully interoperable multi-agency communication ecosystems.

North America and Europe will continue to dominate in terms of advanced deployment, while Asia-Pacific will experience the fastest competitive expansion driven by smart city infrastructure and public safety modernization programs.

Advancements in private 5G networks, edge computing integration, and unified communication platforms will significantly reshape market competition dynamics.

Overall, companies that successfully combine secure communication infrastructure, broadband innovation, government partnerships, and scalable interoperable systems will remain strongly positioned in the evolving global audio critical communication market.

Value Chain

Global Audio Critical Communication Market Value Chain & Supply Chain Evolution Overview

The Global Audio Critical Communication Market value chain is evolving from traditional land-mobile radio (LMR)-centric infrastructure into a broadband-enabled, software-defined, and highly interoperable communication ecosystem. This transformation is being driven by the increasing need for real-time, secure, and uninterrupted voice communication across mission-critical environments such as public safety, defense, transportation, utilities, and industrial operations. Governments and enterprises are actively modernizing legacy systems to support LTE and 5G-based mission-critical communication networks.

The value chain is becoming more integrated and technology-intensive, combining hardware manufacturing, telecom infrastructure deployment, software platform development, cloud-based communication services, and cybersecurity frameworks. The convergence of telecom, IT, and public safety systems is reshaping how critical communication networks are designed, deployed, and managed globally.

The upstream segment includes radio device manufacturing, antenna systems, semiconductor components, chipset development, telecom equipment production, and network infrastructure hardware. Key suppliers include telecom OEMs, defense electronics manufacturers, and communication chipset developers that enable reliable and secure communication devices and network systems.

The core operational layer consists of mission-critical network deployment, system integration, command center infrastructure, dispatch platforms, LTE/5G network management, and interoperability solutions. This stage is increasingly driven by software-defined networking, cloud-native communication platforms, and AI-assisted dispatch optimization systems that enhance response coordination and operational efficiency.

The downstream segment includes public safety agencies, defense organizations, transportation authorities, utility providers, industrial enterprises, and emergency response units. These end users rely on integrated communication systems for real-time coordination, crisis response, field operations, and infrastructure management.

Overall, the audio critical communication value chain is transitioning into a highly digital, broadband-enabled, and intelligence-driven ecosystem where reliability, interoperability, security, and low-latency performance define competitive advantage.

Global Audio Critical Communication Market Value Chain & Supply Chain Evolution Current Scenario

The current market structure reflects a transitional ecosystem where legacy LMR systems coexist with emerging LTE and 5G mission-critical communication platforms. Many public safety agencies continue to rely on established narrowband radio systems due to reliability and coverage advantages, while simultaneously adopting broadband solutions for enhanced data and multimedia communication capabilities.

System integration and interoperability remain key challenges as organizations attempt to connect legacy infrastructure with modern IP-based communication systems. Hybrid communication models are increasingly being deployed to ensure seamless connectivity across different technologies and operational environments.

Telecom operators and equipment manufacturers are actively investing in mission-critical communication capabilities, including push-to-talk over cellular (PTT), real-time video communication, and AI-assisted dispatch systems. These technologies are improving situational awareness and response coordination across emergency and industrial operations.

Despite rapid modernization, challenges such as spectrum allocation constraints, cybersecurity risks, high infrastructure costs, and regulatory complexities continue to influence deployment timelines and adoption rates across regions.

Key Value Chain & Supply Chain Evolution Signals in Global Audio Critical Communication Market

Transition from LMR to broadband networks is fundamentally reshaping the communication infrastructure landscape, enabling richer data integration and real-time multimedia communication capabilities.

5G mission-critical communication deployment is enhancing ultra-low latency communication, enabling faster emergency response and improved operational coordination.

AI-enabled dispatch and control systems are optimizing emergency response workflows, resource allocation, and incident management efficiency.

Cloud-native communication platforms are enabling scalable, flexible, and remotely managed critical communication networks across geographies.

Interoperability and hybrid systems are becoming essential for integrating legacy radio systems with next-generation broadband communication networks.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Audio Critical Communication Market

The evolving audio critical communication value chain presents significant strategic opportunities for telecom operators, defense contractors, communication technology providers, and software platform developers. Competitive advantage is increasingly determined by system reliability, interoperability capabilities, cybersecurity strength, and ability to deliver integrated broadband communication ecosystems.

Companies investing in LTE/5G mission-critical communication platforms, AI-driven dispatch systems, and cloud-based network management solutions are expected to strengthen their market positioning. The shift toward broadband-enabled public safety infrastructure is also creating long-term government and enterprise contracts for advanced communication solution providers.

Strategic partnerships between telecom companies, public safety agencies, and technology vendors are becoming critical for large-scale deployment of interoperable communication systems. These collaborations are enabling faster modernization of legacy infrastructure and improved integration across emergency response networks.

Organizations capable of delivering secure, scalable, and fully interoperable communication solutions will be best positioned to capture long-term growth opportunities in this evolving ecosystem.

Global Audio Critical Communication Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the audio critical communication value chain is expected to evolve into a fully broadband-enabled, AI-integrated, and cloud-native communication ecosystem. LTE and 5G mission-critical networks will gradually replace legacy LMR systems, enabling unified voice, video, and data communication across public safety and industrial operations.

AI-powered communication systems will enhance predictive analytics, incident response optimization, and real-time decision support for emergency services and defense operations. This will significantly improve situational awareness and operational efficiency in high-risk environments.

Interoperable global communication frameworks will become more prominent as governments invest in cross-border emergency response coordination and standardized communication protocols. This will enhance international cooperation during large-scale emergencies and disasters.

Ultimately, the future audio critical communication value chain will be defined by convergence of 5G networks, AI-driven intelligence systems, cloud-native infrastructure, and fully interoperable public safety communication ecosystems.

Market-Specific Value Chain

- Hardware & Device Manufacturing: LMR radios, LTE/5G devices, antennas, chipsets, communication terminals

- Network Infrastructure: Telecom towers, base stations, 5G core networks, spectrum systems

- Software & Platform Development: Dispatch systems, PTT platforms, AI communication analytics, network management software

- System Integration & Deployment: Command centers, interoperability systems, hybrid communication networks

- End Users: Public safety agencies, defense forces, transportation authorities, utilities, industrial operators

- Service Providers: Telecom operators, managed service providers, communication solution vendors

- Support & Maintenance: Cybersecurity services, network maintenance providers, system upgrade vendors

Investment Activity

Global Audio Critical Communication Market Investment & Funding Dynamics Overview

The Global Audio Critical Communication Market is witnessing strong investment momentum driven by modernization of public safety infrastructure, rapid adoption of broadband mission-critical networks, expansion of smart city programs, and increasing demand for secure real-time communication systems. Telecom providers, defense contractors, network equipment manufacturers, and software vendors are actively investing in 5G mission-critical communication platforms, interoperable dispatch systems, cloud-native command centers, and secure broadband communication infrastructure.

Investment activity is accelerating due to growing demand for LTE/5G mission-critical services, hybrid LMR-broadband systems, push-to-talk over cellular solutions, and AI-enabled emergency response communication platforms. The transition from legacy radio systems to broadband-enabled communication ecosystems is significantly reshaping capital allocation across the market.

Additionally, increasing investments in next-generation public safety networks, encrypted communication systems, smart dispatch platforms, and integrated emergency response infrastructure are strengthening long-term growth opportunities globally.

Global Audio Critical Communication Market Investment & Funding Dynamics Current Scenario

Currently, the global audio critical communication market is experiencing rising investment activity due to large-scale government spending on public safety modernization, defense communication upgrades, and national emergency response systems. Leading companies are heavily investing in 5G-enabled mission-critical networks, AI-assisted dispatch systems, cloud-based communication platforms, and interoperable communication architectures.

The market is attracting strong funding into telecom infrastructure providers, defense communication technology firms, public safety software developers, and broadband mission-critical solution innovators.

The industry is witnessing active government contracts, defense procurement programs, strategic alliances, and cross-industry partnerships as stakeholders pursue network modernization and interoperability enhancements.

Key Investment & Funding Dynamics Signals in Global Audio Critical Communication Market

- Rising demand for LTE/5G mission-critical communication systems is accelerating broadband infrastructure investments.

- Expansion of public safety modernization and smart city programs is increasing government-led capital deployment.

- Growing adoption of AI-powered dispatch and command center systems is strengthening technology-focused funding.

- Strategic investments in interoperable communication platforms and hybrid LMR-broadband systems are reshaping operational priorities.

- Partnerships between telecom operators, defense contractors, and communication technology vendors are improving ecosystem scalability.

- Increasing regulatory emphasis on public safety communication standards, spectrum allocation policies, and emergency response compliance is supporting investor confidence.

- Rising demand for secure and resilient communication infrastructure is accelerating R&D spending.

Strategic Implications of Investment & Funding Dynamics in Global Audio Critical Communication Market

- Continuous investment in 5G mission-critical networks and broadband communication infrastructure is essential for long-term competitiveness.

- Capital allocation toward secure communication systems and interoperable platforms will strengthen market positioning.

- Companies delivering reliable, scalable, and government-compliant communication solutions are expected to gain stronger market share.

- Strategic partnerships and long-term government contracts will accelerate network modernization and deployment scale.

- Investments in AI-enabled emergency response systems and cloud-native dispatch platforms will remain major priorities.

- Compliance with public safety regulations, spectrum policies, and defense communication standards will remain critical for sustained growth.

- Organizations scaling broadband mission-critical ecosystems are expected to capture substantial future opportunities.

Global Audio Critical Communication Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Audio Critical Communication Market is expected to maintain strong investment growth driven by 5G adoption, digital public safety transformation, smart city expansion, and defense communication modernization.

Future capital deployment will increasingly focus on fully interoperable communication networks, AI-driven dispatch systems, cloud-native public safety platforms, and next-generation broadband mission-critical infrastructure.

The convergence of telecom, AI, and public safety ecosystems is expected to become a major long-term innovation priority.

In conclusion, the Global Audio Critical Communication Market represents a high-value infrastructure investment landscape where broadband transformation, secure communication systems, interoperability, and mission-critical networking innovation will define future capital strategies.

Technology & Innovation

Global Audio Critical Communication Market Technology & Innovation Landscape Overview

The global audio critical communication market is undergoing a significant technological transition driven by the evolution from legacy Land-Mobile Radio (LMR) systems toward advanced LTE and 5G-based mission-critical communication networks. This transformation is enabling secure, high-reliability, and low-latency communication across public safety, defense, transportation, and industrial environments where uninterrupted connectivity is essential.

Modern communication ecosystems are increasingly integrating IP-based voice systems, broadband push-to-talk (PTT) services, cloud-native dispatch platforms, and AI-assisted communication management tools. These advancements are improving coordination efficiency, response times, and situational awareness in mission-critical operations such as emergency response, disaster management, and security enforcement.

The market is also witnessing growing deployment of interoperable communication frameworks, hybrid LMR-LTE systems, and unified command-and-control platforms that enable seamless communication between legacy infrastructure and next-generation broadband networks. This interoperability is a key enabler of large-scale public safety modernization programs globally.

Global Audio Critical Communication Market Technology & Innovation Current Scenario

Currently, innovation in the market is focused on enabling the transition toward fully broadband-enabled, software-defined, and AI-enhanced mission-critical communication systems. Traditional narrowband radio communication is being progressively replaced by integrated digital platforms that support voice, video, and data exchange in real time.

LTE-based mission-critical communication systems are gaining strong traction due to their ability to support high-speed, secure, and scalable connectivity for emergency services and enterprise users. These systems are increasingly deployed alongside 5G networks to enable ultra-reliable low-latency communication (URLLC) for critical operations.

Push-to-talk over cellular (PTT) solutions are also expanding rapidly, offering flexible, smartphone-based communication capabilities that extend beyond traditional radio coverage. These solutions are particularly valuable for transportation, utilities, and field workforce coordination.

AI-enabled dispatch systems are emerging as a key innovation layer, enabling automated incident prioritization, intelligent resource allocation, and real-time decision support for emergency response teams. Additionally, cloud-based communication platforms are improving scalability, resilience, and remote accessibility across distributed operations.

Edge computing integration is further enhancing system responsiveness by enabling local processing of critical communication data, reducing latency, and ensuring uninterrupted connectivity even in network-constrained environments.

Key Technology & Innovation Trends in the Global Audio Critical Communication Market

- LTE & 5G Mission-Critical Networks: Enabling ultra-reliable, low-latency broadband communication for emergency and defense applications.

- Push-to-Talk Over Cellular (PTT): Providing flexible, mobile-based instant communication across wide coverage areas.

- AI-Driven Dispatch Systems: Enhancing emergency response coordination and real-time decision-making.

- Cloud-Native Communication Platforms: Supporting scalable, resilient, and remotely accessible communication infrastructure.

- Hybrid LMR-LTE Systems: Ensuring interoperability between legacy radio and modern broadband systems.

- Edge Computing Integration: Reducing latency and improving reliability in mission-critical communication environments.

- Interoperable Command Platforms: Enabling seamless coordination across agencies and jurisdictions.

- Software-Defined Communication Networks: Increasing flexibility and adaptability of communication infrastructure.

- Secure Encryption Protocols: Strengthening data protection and communication security in sensitive operations.

- Integrated Voice, Video & Data Systems: Enhancing situational awareness through unified communication channels.

Strategic Implications of Technology & Innovation

Technological advancements are fundamentally reshaping the competitive structure of the audio critical communication market by shifting it from hardware-centric LMR systems toward software-defined, broadband-enabled communication ecosystems. This shift is enabling greater flexibility, scalability, and intelligence in mission-critical operations.

Companies investing in 5G mission-critical platforms, AI-powered dispatch solutions, and integrated public safety communication networks are gaining significant strategic advantages through improved interoperability, faster response times, and enhanced operational efficiency.

The convergence of telecommunications, cloud computing, and artificial intelligence is enabling the development of fully integrated communication ecosystems capable of supporting voice, data, and video in real time across multiple agencies and sectors.

However, challenges such as high infrastructure costs, complex system integration, cybersecurity risks, and regulatory compliance requirements continue to influence adoption speed, particularly in developing regions.

Global Audio Critical Communication Market Technology & Innovation Forward Outlook

The future of the audio critical communication market is expected to evolve toward fully interoperable, AI-orchestrated, and 5G-native communication ecosystems that enable seamless coordination across public safety, defense, and industrial networks.

Next-generation systems are likely to feature autonomous dispatch optimization, real-time situational intelligence platforms, and ultra-reliable cloud-edge hybrid communication architectures designed for mission-critical resilience.

The ongoing transition from LMR to broadband communication networks will continue to accelerate, supported by global investments in smart city infrastructure, national security modernization, and emergency response digitalization.

Overall, the market is evolving toward a highly secure, intelligent, and interconnected communication environment powered by 5G, AI, cloud computing, and interoperable system architecture, redefining the future of global mission-critical communication infrastructure.

Market Risk

Global Audio Critical Communication Market Risk & Disruption Analysis

The Global Audio Critical Communication Market operates in a mission-critical, highly regulated, and technology-sensitive environment where reliability, security, and interoperability are essential. While the market continues to grow due to digital public safety transformation and 5G adoption, it is exposed to regulatory, technological, operational, and cybersecurity risks that can significantly impact deployment and performance outcomes.

Current Risk Environment

The market faces a complex risk landscape driven by the transition from legacy Land-Mobile Radio (LMR) systems to broadband-enabled LTE and 5G communication networks. This transition introduces integration challenges, infrastructure dependency risks, and high modernization costs for governments and enterprises.

Regulatory dependency remains a major risk factor, as public safety communication systems are governed by strict national security standards, spectrum allocation policies, and emergency response protocols. Any policy change or compliance tightening can directly affect procurement cycles and system deployment timelines.

Cybersecurity risks are also increasing as mission-critical communication systems become more connected and IP-based. Threats such as network intrusion, signal interception, ransomware attacks, and data breaches can disrupt emergency response operations and compromise sensitive communication channels.

Operational risks arise from system interoperability limitations, especially when integrating legacy LMR infrastructure with next-generation LTE/5G platforms. Inconsistent standards across regions further complicate cross-border and multi-agency communication.

The market is also exposed to vendor dependency risks, as a limited number of global players control advanced mission-critical communication technologies, creating concentration risk in procurement and long-term system support.

Key Risk & Disruption Factors

- Legacy System Transition Risk: Migration from LMR to LTE/5G systems creates integration and cost challenges.

- Cybersecurity Threats: Increasing vulnerability to hacking, interception, and ransomware in IP-based communication networks.

- Regulatory Dependency: Strict public safety communication regulations and spectrum allocation policies influence deployment timelines.

- Interoperability Challenges: Difficulty in integrating legacy systems with modern broadband communication platforms.

- High Capital Investment: Large-scale infrastructure upgrades require significant government and enterprise spending commitments.

- Vendor Concentration Risk: Dependence on a limited number of global suppliers for mission-critical technologies.

- Network Reliability Risk: System downtime or connectivity failures can directly impact emergency response operations.

- Technology Obsolescence: Rapid evolution of 5G and AI-based communication systems may shorten technology life cycles.

Strategic Risk Implications

The increasing complexity of mission-critical communication systems is pushing governments and enterprises to prioritize resilient, secure, and interoperable network architectures.

Organizations are investing heavily in cybersecurity frameworks, redundant network infrastructure, and AI-enabled monitoring systems to reduce operational vulnerabilities and ensure uninterrupted communication.

Standardization of communication protocols and global interoperability frameworks is becoming essential to reduce fragmentation and improve cross-agency coordination.

Vendors with strong cybersecurity capabilities, multi-network compatibility, and long-term infrastructure support are gaining competitive advantage in procurement decisions.

Forward Risk Outlook (2026???2033)

- Accelerated Digital Migration: Faster shift from analog LMR systems to broadband LTE/5G networks.

- Rising Cybersecurity Prioritization: Security-first architecture will become mandatory in public safety networks.

- Stronger Regulatory Oversight: Governments will enforce stricter compliance and interoperability standards.

- AI-Driven Network Monitoring: Increased use of AI for predictive maintenance and threat detection.

- Infrastructure Modernization Push: Large-scale investments in smart cities and emergency communication systems.

- Vendor Consolidation: Increasing mergers and partnerships to deliver end-to-end communication solutions.

Overall, the Global Audio Critical Communication Market remains highly strategic but risk-intensive, where long-term success depends on cybersecurity strength, regulatory compliance, system interoperability, and the ability to support next-generation mission-critical communication infrastructure.

Regulatory Landscape

Global Audio Critical Communication Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global audio critical communication market is shaped by public safety communication standards, spectrum allocation frameworks, emergency response protocols, national security requirements, and telecommunications compliance regulations. As these systems are mission-critical in nature, governments and regulatory authorities place strong emphasis on ensuring uninterrupted connectivity, interoperability across agencies, secure data transmission, and resilient communication infrastructure capable of functioning during disasters and large-scale emergencies.

Audio critical communication providers must comply with a wide range of regulatory requirements covering radio frequency spectrum licensing, encryption standards, emergency communication interoperability mandates, network reliability benchmarks, and equipment certification protocols. These frameworks ensure that communication systems used by public safety agencies, defense organizations, and industrial operators maintain consistent performance under extreme operational conditions.

The ongoing transition from traditional land-mobile radio (LMR) systems to LTE and 5G-based mission-critical communication networks is accelerating the evolution of regulatory frameworks. Governments are increasingly focusing on broadband public safety networks, standardized interoperability across jurisdictions, and secure cloud-based communication architectures that integrate voice, data, and real-time situational intelligence.

Global Audio Critical Communication Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for the audio critical communication market is primarily governed by national telecommunications authorities, public safety communication agencies, and international spectrum management organizations. These bodies regulate frequency allocation, system certification, and operational reliability standards to ensure that mission-critical communication networks remain stable, secure, and interference-free.

In North America and Europe, regulatory frameworks such as FirstNet (U.S.), ETSI standards, and various national emergency communication programs are driving the modernization of public safety networks. These initiatives emphasize interoperability between agencies, secure LTE-based communication infrastructure, and gradual replacement of legacy narrowband radio systems with broadband-enabled solutions.

Asia-Pacific countries including China, India, Japan, and South Korea are rapidly investing in smart public safety infrastructure and digital emergency communication systems. Regulatory bodies in these regions are strengthening spectrum management policies and promoting integration of 5G technologies into national security and disaster response frameworks.

Defense and military communication systems are subject to strict encryption, cybersecurity, and operational confidentiality regulations, ensuring secure communication channels for sensitive missions and strategic operations across global defense networks.

Key Regulatory & Policy Environment Signals in Global Audio Critical Communication Market

- Spectrum Allocation Policies: Government-controlled frequency management ensures interference-free communication for mission-critical operations.

- Public Safety Communication Standards: Regulations enforce interoperability, reliability, and emergency readiness across agencies and jurisdictions.

- Emergency Response Protocols: Communication systems must support rapid coordination during disasters and large-scale incidents.

- Network Security & Encryption Requirements: Strict cybersecurity standards ensure secure transmission of sensitive voice and data communications.

- Telecommunications Compliance Frameworks: Equipment and infrastructure must meet national and international telecom certification standards.

- Critical Infrastructure Protection Policies: Communication systems supporting defense, utilities, and transport sectors are subject to resilience and redundancy mandates.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is driving significant investments in broadband-enabled public safety networks, interoperable communication platforms, and secure cloud-based dispatch systems. Organizations are increasingly upgrading legacy LMR infrastructure to LTE and 5G-based systems in response to government mandates and spectrum modernization policies.

Spectrum reallocation and digital transformation initiatives are accelerating the convergence of telecom operators, defense contractors, and public safety agencies into integrated communication ecosystems capable of supporting real-time voice, video, and data exchange.

Cybersecurity and encryption requirements are pushing vendors to adopt advanced secure communication protocols, identity-based authentication systems, and end-to-end encrypted mission-critical networks to ensure operational integrity in high-risk environments.

The expansion of smart city initiatives and national emergency response modernization programs is further reinforcing demand for interoperable, resilient, and AI-enabled communication platforms across global markets.

Global Audio Critical Communication Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global audio critical communication market is expected to become increasingly broadband-centric, security-intensive, and interoperability-focused. Governments worldwide are likely to accelerate the transition from legacy radio systems to unified LTE and 5G mission-critical communication infrastructures.

Stricter regulations around emergency response readiness, cross-agency communication interoperability, and national security communication resilience are expected to shape future infrastructure investments and technology adoption strategies.

The integration of AI-powered dispatch systems, cloud-native communication platforms, and real-time analytics may introduce additional regulatory requirements around data governance, system reliability, and automated decision-support transparency in mission-critical environments.

Overall, regulatory and policy developments will remain a core growth driver for the market, with companies investing in secure broadband communication systems, interoperable platforms, and next-generation public safety infrastructure expected to maintain strong long-term competitive advantage.