Global Ceramics Market Report, Size, Share and Forecast 2026–2033

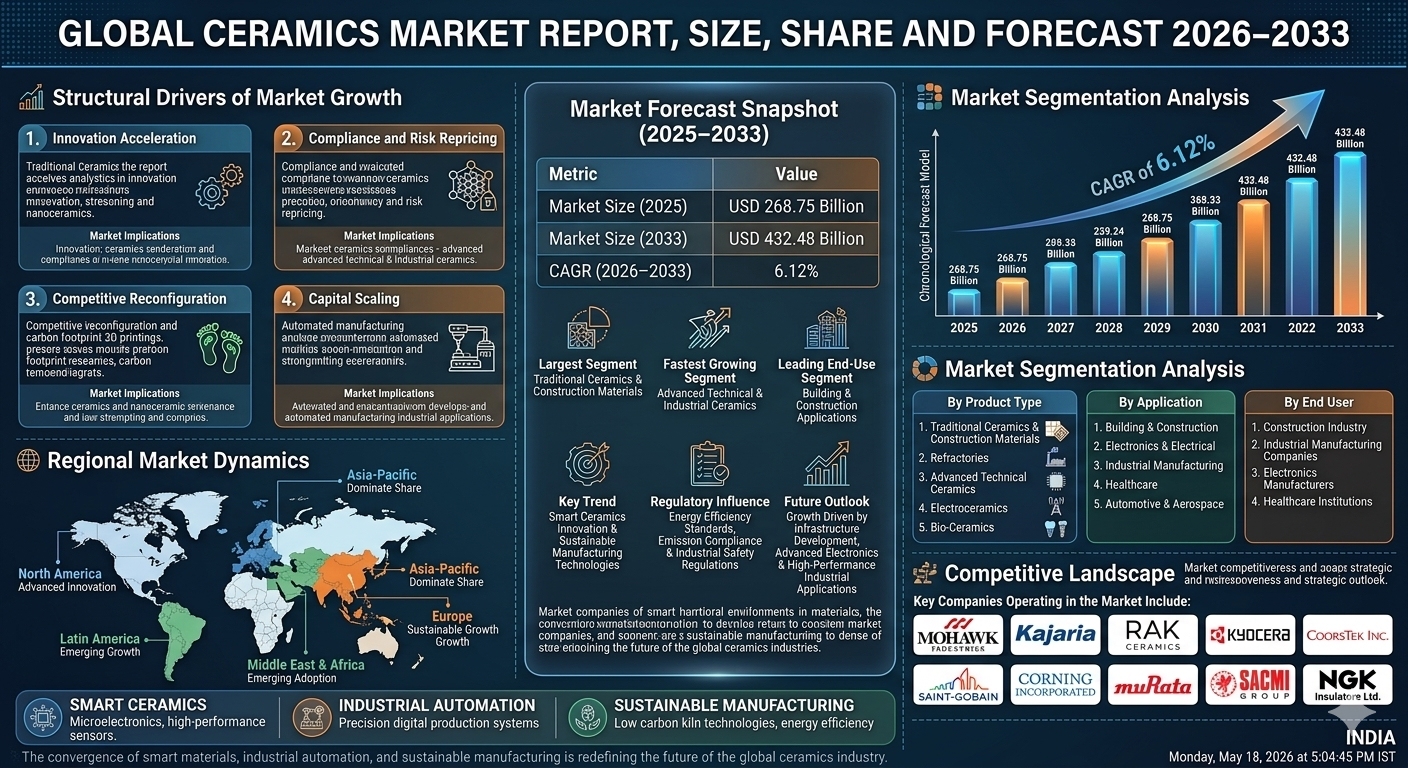

Global Ceramics Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 268.75 Billion |

| Market Size (2033) | USD 432.48 Billion |

| CAGR (2026???2033) | 6.12% |

| Largest Segment | Traditional Ceramics & Construction Materials |

| Fastest Growing Segment | Advanced Technical & Industrial Ceramics |

| Leading End-Use Segment | Building & Construction Applications |

| Key Trend | Smart Ceramics Innovation & Sustainable Manufacturing Technologies |

| Regulatory Influence | Energy Efficiency Standards, Emission Compliance & Industrial Safety Regulations |

| Future Outlook | Growth Driven by Infrastructure Development, Advanced Electronics & High-Performance Industrial Applications |

Global Ceramics Market Size & Forecast

The Global Ceramics Market is expected to witness steady expansion during the forecast period from 2026 to 2033. The market was valued at USD 268.75 billion in 2025 and is projected to reach approximately USD 432.48 billion by 2033, registering a CAGR of 6.12%. The market growth is primarily driven by rising construction activity, expanding infrastructure investments, increasing demand for advanced industrial materials, and growing applications across electronics, healthcare, and automotive sectors. Ceramic products are increasingly critical for construction, insulation, electronics components, biomedical devices, and high-temperature industrial applications. Rising adoption of lightweight technical ceramics, additive manufacturing, and energy-efficient production systems is accelerating market growth. In addition, rapid urbanization, smart infrastructure development, and technological innovation in material science are supporting long-term market expansion.Global Ceramics Market Overview

Ceramics are inorganic, non-metallic materials manufactured through high-temperature processing and used across structural, decorative, and advanced technical applications. The market includes traditional ceramics, tiles, sanitaryware, refractories, advanced ceramics, bio-ceramics, and electroceramics. Ceramic products are widely utilized across construction, electronics, healthcare, automotive, aerospace, and industrial manufacturing sectors. The market is shifting from conventional ceramic manufacturing toward advanced engineered ceramics, digital production systems, sustainable kiln technologies, and precision-performance applications.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in nanoceramics, 3D-printed ceramics, lightweight composites, and high-performance electroceramics is accelerating product development. Advanced material engineering is improving thermal resistance, mechanical durability, and conductivity performance.Market Implications

Companies investing in technical ceramic innovation, additive manufacturing, and smart material solutions are expected to strengthen market leadership.2. Compliance and Risk Repricing

Energy efficiency regulations, carbon emission reduction targets, workplace safety standards, and industrial environmental compliance requirements are influencing production modernization. Governments are increasingly promoting cleaner manufacturing processes and sustainable material sourcing.Market Implications

Firms offering compliant, energy-efficient, and environmentally responsible ceramic solutions are likely to gain stronger market trust.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as traditional ceramic manufacturers, advanced materials companies, construction suppliers, and industrial technology firms expand product offerings. Integrated raw material sourcing and technology-driven manufacturing processes are altering value-chain economics.Market Implications

Companies focusing on product diversification, automation, and technical ceramic specialization may gain stronger margins.4. Capital and Capacity Scaling

Rising investment in automated kilns, digital production facilities, technical ceramic research centers, and advanced processing infrastructure is supporting market expansion. Infrastructure development and industrial modernization are also increasing demand.Market Implications

Operators scaling advanced manufacturing capabilities and production efficiency are expected to capture future opportunities.Market Segmentation Analysis

By Product Type

1. Traditional Ceramics & Construction Materials

This remains the largest segment due to widespread use in tiles, bricks, and sanitaryware applications.2. Refractories

Widely used in high-temperature industrial processing applications.3. Advanced Technical Ceramics

Fastest-growing due to increasing industrial and electronics applications.4. Electroceramics

Growing demand for electronic component manufacturing.5. Bio-Ceramics

Strong growth driven by medical implants and dental applications.By Application

1. Building & Construction

Largest segment due to infrastructure and residential development demand.2. Electronics & Electrical

Strong growth driven by miniaturized component manufacturing.3. Industrial Manufacturing

Widely used in wear-resistant and thermal-resistant systems.4. Healthcare

Growing demand for medical and dental ceramic solutions.5. Automotive & Aerospace

Increasing use in lightweight and high-performance components.By End User

1. Construction Industry

Largest segment due to extensive ceramic material usage.2. Industrial Manufacturing Companies

Strong demand for advanced process applications.3. Electronics Manufacturers

Growing demand for precision ceramic components.4. Healthcare Institutions

Used for specialized biomedical applications.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global ceramics market due to large-scale manufacturing, rapid urbanization, and strong construction activity.North America

North America remains a major market supported by advanced ceramics innovation and industrial modernization.Europe

Europe is witnessing strong growth driven by sustainable production technologies and high-value industrial ceramics.Latin America

Latin America is gradually expanding due to infrastructure development and construction sector growth.Middle East & Africa

The region is witnessing emerging adoption driven by urban infrastructure projects and industrial expansion.Competitive Landscape

The Global Ceramics Market is highly competitive with traditional ceramic producers, advanced materials manufacturers, and industrial technology companies expanding globally.Key Companies Operating in the Market Include:

- Mohawk Industries

- Kajaria Ceramics

- RAK Ceramics

- Kyocera Corporation

- CoorsTek Inc.

- Saint-Gobain Ceramics

- Corning Incorporated

- Murata Manufacturing

- SACMI Group

- NGK Insulators Ltd.

Strategic Outlook

The future of the ceramics market will be shaped by advanced technical ceramic innovation, digital manufacturing systems, lightweight material engineering, and sustainable kiln technologies. 3D printing, nanoceramics, and smart ceramics for electronics and healthcare will significantly improve market competitiveness. The rise of infrastructure modernization, electronics miniaturization, and high-performance industrial applications is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Ceramics Market remains a major segment within construction, industrial manufacturing, and advanced material ecosystems. Rising demand for infrastructure materials, technical ceramics, and energy-efficient manufacturing continues driving long-term market growth. Companies capable of delivering scalable, high-performance, sustainable, and technologically advanced ceramic solutions will be best positioned to capture future opportunities. The convergence of smart materials, industrial automation, and sustainable manufacturing is expected to redefine the future of the global ceramics industry.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Ceramics Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Ceramics

- 2.2 Scope of the Study

- 2.3 Evolution of Ceramic Manufacturing Technologies

- 2.4 Advanced Materials Ecosystem Analysis

- 2.5 Regulatory & Industrial Compliance Framework

- 2.6 Smart Manufacturing & Sustainability Trends

- 2.7 Product Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026???2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Global Infrastructure Development

- 4.1.2 Growing Demand for Advanced Industrial Materials

- 4.1.3 Expansion of Electronics & Semiconductor Applications

- 4.1.4 Advancements in Technical Ceramic Manufacturing

- 4.1.5 Increasing Adoption of Sustainable Production Technologies

- 4.2 Restraints

- 4.2.1 High Energy Consumption in Manufacturing

- 4.2.2 Raw Material Price Volatility

- 4.2.3 Capital-Intensive Production Infrastructure

- 4.2.4 Stringent Environmental Compliance Requirements

- 4.3 Opportunities

- 4.3.1 Growth in Smart Ceramics Applications

- 4.3.2 Expansion of Biomedical Ceramic Solutions

- 4.3.3 Additive Manufacturing Integration

- 4.3.4 Emerging Demand in Electric Vehicles & Aerospace

- 4.4 Challenges

- 4.4.1 Complex Manufacturing Processes

- 4.4.2 Scaling Advanced Ceramic Production

- 4.4.3 Technology Adoption Barriers

- 4.4.4 Global Supply Chain Disruptions

- 4.1 Drivers

- 5. Global Ceramics Market Analysis (USD Billion), 2026???2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Product Innovation Trends

- 5.5 Application Demand Analysis

- 5.6 Future Growth Projections

- 6. Market Segmentation (USD Billion), 2026???2033

- 6.1 By Product Type

- 6.1.1 Traditional Ceramics & Construction Materials

- 6.1.2 Refractories

- 6.1.3 Advanced Technical Ceramics

- 6.1.4 Electroceramics

- 6.1.5 Bio-Ceramics

- 6.2 By Application

- 6.2.1 Building & Construction

- 6.2.2 Electronics & Electrical

- 6.2.3 Industrial Manufacturing

- 6.2.4 Healthcare

- 6.2.5 Automotive & Aerospace

- 6.3 By End User

- 6.3.1 Construction Industry

- 6.3.2 Industrial Manufacturing Companies

- 6.3.3 Electronics Manufacturers

- 6.3.4 Healthcare Institutions

- 6.1 By Product Type

- 7. Market Segmentation by Geography

- 7.1 Asia-Pacific

- 7.2 North America

- 7.3 Europe

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Innovation Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Manufacturing Capacity Analysis

- 8.5 Brand Positioning Strategies

- 9. Company Profiles

- 9.1 Mohawk Industries

- 9.2 Kajaria Ceramics

- 9.3 RAK Ceramics

- 9.4 Kyocera Corporation

- 9.5 CoorsTek Inc.

- 9.6 Saint-Gobain Ceramics

- 9.7 Corning Incorporated

- 9.8 Murata Manufacturing

- 9.9 SACMI Group

- 9.10 NGK Insulators Ltd.

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Ceramic Innovation Forecast Engine

- 10.2 Smart Manufacturing Analytics Dashboard

- 10.3 Industrial Demand Intelligence Tracker

- 10.4 Product Performance Opportunity Analyzer

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Investment in Advanced Technical Ceramics

- 11.2 Expansion of Sustainable Manufacturing Systems

- 11.3 Strengthening Digital Production Infrastructure

- 11.4 Development of Smart Ceramic Applications

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Ceramics Market Competitive Intensity & Market Structure Overview

The global ceramics market is highly competitive and moderately consolidated, characterized by strong competition among traditional ceramic manufacturers, advanced materials companies, industrial component suppliers, and specialized technical ceramic producers. Competitive intensity is driven by manufacturing scale, product innovation, raw material sourcing capabilities, energy-efficient production systems, application-specific customization, and regulatory compliance across industrial sectors.

The market structure includes large multinational ceramic producers with diversified product portfolios alongside regional manufacturers specializing in construction ceramics, sanitaryware, refractories, and advanced engineered ceramic solutions. Competition is increasingly shaped by smart ceramics development, precision manufacturing technologies, additive manufacturing capabilities, and sustainable kiln modernization.

Rising infrastructure development, increasing adoption of advanced industrial materials, rapid electronics expansion, and growing demand for high-performance thermal-resistant components are significantly intensifying competition across the global ceramics market.

Global Ceramics Market Competitive Intensity & Market Structure Current Scenario

Leading Global Ceramics Companies

Mohawk Industries: Leading global ceramic flooring and construction materials manufacturer with strong international production capabilities.

Kajaria Ceramics: Major ceramic tile producer with extensive market presence and diversified product offerings.

RAK Ceramics: Prominent ceramic solutions provider specializing in tiles, sanitaryware, and construction applications.

Kyocera Corporation: Global leader in advanced technical ceramics for electronics, automotive, and industrial applications.

CoorsTek Inc.: Major technical ceramics manufacturer focused on engineered high-performance ceramic components.

Saint-Gobain Ceramics: Established industrial ceramics producer offering advanced refractory and engineered ceramic solutions.

Corning Incorporated: Leading innovator in specialty glass-ceramic and high-performance material technologies.

Murata Manufacturing: Key electroceramics producer specializing in advanced electronic ceramic components.

SACMI Group: Major ceramic manufacturing technology provider supporting automated production systems.

NGK Insulators Ltd.: Strong participant specializing in industrial ceramics, insulation systems, and environmental applications.

Key Competitive Intensity & Market Structure Drivers

Growing demand for advanced technical ceramics is intensifying competition around material engineering and performance innovation.

Energy efficiency regulations and emission reduction standards are accelerating investment in sustainable ceramic manufacturing technologies.

Rapid infrastructure development is strengthening competition across construction ceramics and sanitaryware production.

Electronics miniaturization is increasing demand for precision electroceramic components and specialized manufacturing capabilities.

Additive manufacturing and smart ceramic technologies are reshaping product development competitiveness.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly investing in automated kilns, AI-driven production optimization, and digital ceramic manufacturing systems.

Strategic partnerships with electronics, healthcare, and automotive industries are becoming essential for technical ceramic market expansion.

Vertical integration across raw material sourcing and processing infrastructure is strengthening cost competitiveness.

Sustainable manufacturing modernization and low-emission kiln technologies are emerging as major competitive differentiators.

Research investment in nanoceramics, bio-ceramics, and lightweight composite materials is strengthening innovation leadership.

Global Ceramics Market Competitive Intensity & Market Structure Forward Outlook

The global ceramics market is expected to remain highly competitive as infrastructure modernization and advanced industrial applications continue accelerating.

Future competition will increasingly focus on smart ceramics, additive manufacturing integration, lightweight engineered materials, and precision high-performance ceramic solutions.

Asia-Pacific will remain the dominant competitive region, while North America and Europe are expected to witness strong growth in technical ceramic innovation.

Advancements in nanoceramics, sustainable production systems, and digital manufacturing platforms are expected to significantly reshape market dynamics.

Overall, companies that successfully combine scalable manufacturing, advanced material innovation, sustainability integration, and cross-industry application expertise will remain strongly positioned in the evolving global ceramics market.

Value Chain

Global Ceramics Market Value Chain & Supply Chain Evolution Overview

The Global Ceramics Market value chain is evolving from conventional mineral-based manufacturing systems into a technologically advanced, highly automated, and sustainability-driven materials ecosystem. This transformation is being driven by rising infrastructure development, increasing demand for advanced industrial materials, expanding electronics applications, and growing adoption of energy-efficient manufacturing technologies.

The ceramics value chain is becoming increasingly integrated through digital manufacturing systems, precision engineering, advanced kiln technologies, and material science innovation. Manufacturers are focusing on enhancing product performance, thermal resistance, durability, and environmental efficiency to meet expanding industrial and construction requirements.

The upstream segment begins with raw material sourcing, including clay, kaolin, feldspar, silica, alumina, zirconia, and other specialty minerals. These materials are sourced from mining operations and mineral processing facilities globally, with increasing emphasis on purity, consistency, and sustainable extraction practices.

The operational core of the value chain includes mineral refining, powder processing, forming, shaping, glazing, firing, sintering, surface finishing, and precision engineering. Automation, digital kiln controls, AI-based quality monitoring, and additive manufacturing are increasingly improving production efficiency and reducing waste.

The downstream segment includes ceramic component distribution, construction material supply chains, industrial system integration, electronics manufacturing partnerships, and specialized application deployment across healthcare, automotive, aerospace, and industrial sectors.

Overall, the ceramics value chain is transitioning into a highly engineered, performance-driven, and digitally optimized ecosystem where material precision, manufacturing efficiency, sustainability, and technical specialization define competitive advantage.

Global Ceramics Market Value Chain & Supply Chain Evolution Current Scenario

The current market structure reflects a dual ecosystem combining traditional ceramic production systems with rapidly expanding advanced technical ceramic manufacturing platforms.

Traditional ceramics remain dominant in construction applications such as tiles, sanitaryware, and building materials, while advanced ceramics are witnessing strong growth across electronics, industrial manufacturing, and healthcare applications.

Manufacturing processes are increasingly adopting automated forming systems, robotic handling, digital kiln management, and precision quality control technologies to improve operational consistency.

Supply chains remain heavily dependent on mineral sourcing stability, energy-intensive processing systems, and regional manufacturing infrastructure. However, sustainability pressures are accelerating adoption of cleaner production technologies.

Advanced ceramics producers are increasingly integrating R&D-driven production capabilities to meet specialized requirements for thermal resistance, conductivity, wear resistance, and biomedical performance.

Key Value Chain & Supply Chain Evolution Signals in Global Ceramics Market

Smart manufacturing integration is significantly improving production efficiency through AI-driven process control and predictive quality monitoring.

Technical ceramic expansion is driving demand for advanced material engineering and specialized production capabilities.

Sustainable kiln modernization is reducing energy consumption and supporting compliance with carbon emission regulations.

Additive manufacturing adoption is enabling precision ceramic component production for complex industrial applications.

Supply chain digitization is enhancing raw material traceability, production planning, and global distribution efficiency.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Ceramics Market

The evolving ceramics value chain presents significant strategic opportunities for material suppliers, ceramic manufacturers, industrial technology providers, and construction material companies.

Competitive advantage is increasingly determined by material innovation, manufacturing automation, energy efficiency, technical specialization, and global distribution scalability.

Manufacturers investing in advanced ceramic R&D, digital production systems, and sustainable kiln infrastructure are expected to strengthen market leadership.

Strategic collaborations between raw material suppliers, industrial manufacturers, electronics companies, and advanced ceramics developers are becoming critical for market expansion.

Organizations capable of balancing production efficiency, technical performance, regulatory compliance, and sustainability objectives will achieve stronger long-term positioning.

Global Ceramics Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the ceramics value chain is expected to evolve into a highly automated, digitally controlled, and sustainability-focused manufacturing ecosystem.

AI-powered process optimization will enhance firing precision, defect detection, and material performance consistency.

Advanced additive manufacturing technologies will enable customized ceramic solutions for aerospace, biomedical, and electronics applications.

Low-emission kiln systems, renewable energy integration, and circular recycling practices will significantly improve environmental performance.

Material science innovation will enable next-generation smart ceramics with enhanced conductivity, sensing capabilities, and multifunctional performance.

Ultimately, the future ceramics value chain will be defined by advanced engineering, intelligent automation, sustainability integration, and high-performance material innovation.

Market-Specific Value Chain

- Raw Material Sourcing: Clay mines, kaolin processors, silica suppliers, specialty mineral extraction companies

- Material Processing: Mineral refinement plants, powder processing facilities, ceramic compound preparation systems

- Manufacturing & Forming: Pressing systems, molding facilities, extrusion units, additive manufacturing platforms

- Firing & Finishing: Kiln operators, glazing systems, sintering technologies, surface treatment facilities

- Quality Assurance & Engineering: Material testing laboratories, performance validation systems, precision inspection providers

- Distribution & Industrial Integration: Construction suppliers, industrial distributors, electronics component supply chains

- End-Use Applications: Building construction, industrial manufacturing, electronics, healthcare, automotive, aerospace

Investment Activity

Global Ceramics Market Investment & Funding Dynamics Overview

The Global Ceramics Market is witnessing substantial investment momentum driven by expanding infrastructure development, increasing adoption of advanced industrial ceramics, rapid innovation in smart ceramic technologies, and growing demand for sustainable manufacturing systems. Ceramic manufacturers, construction material suppliers, advanced materials companies, electronics producers, and industrial technology firms are actively investing in automated production facilities, smart kiln systems, advanced ceramic R&D centers, additive manufacturing capabilities, and energy-efficient processing infrastructure.

Investment activity is accelerating due to rising demand for high-performance ceramic materials, precision-engineered industrial components, lightweight technical ceramics, and environmentally sustainable production processes. The transition toward digitally integrated ceramic manufacturing and smart material applications is significantly reshaping capital allocation across the market.

Additionally, expanding investments in 3D ceramic printing technologies, nanoceramic engineering, industrial automation systems, emission reduction infrastructure, and advanced sintering technologies are strengthening long-term growth opportunities globally.

Global Ceramics Market Investment & Funding Dynamics Current Scenario

Currently, the global ceramics market demonstrates rising investment activity due to increasing capital requirements for production modernization, advanced material development, energy-efficient kiln deployment, and technical ceramics manufacturing expansion. Leading market participants are heavily investing in AI-driven process optimization, automated ceramic production systems, smart quality control technologies, and sustainable raw material sourcing.

The market is attracting strong funding into advanced ceramics startups, precision manufacturing technology providers, additive ceramic solution developers, nanoceramic research companies, and sustainable industrial material innovators.

The industry is witnessing active mergers, acquisitions, strategic partnerships, and industrial collaborations as ceramic manufacturers, electronics companies, and material science firms pursue capacity expansion, technology integration, and product portfolio diversification.

Key Investment & Funding Dynamics Signals in Global Ceramics Market

- Rising demand for construction materials and infrastructure ceramics is accelerating manufacturing capacity investments.

- Expansion of advanced technical ceramics and electroceramics is increasing technology-focused capital deployment.

- Growing adoption of energy-efficient and low-emission production technologies is strengthening sustainability-driven funding.

- Strategic investments in 3D ceramic printing and nanoceramic engineering are reshaping production priorities.

- Partnerships between ceramic manufacturers, electronics companies, and industrial technology firms are improving innovation scalability.

- Increasing regulatory focus on energy efficiency, emission reduction, and industrial safety compliance is supporting investor confidence.

- Rising demand for smart ceramic applications in healthcare, electronics, and aerospace is accelerating R&D spending.

Strategic Implications of Investment & Funding Dynamics in Global Ceramics Market

- Continuous investment in advanced ceramic innovation and digital production systems is essential for long-term competitiveness.

- Capital allocation toward energy-efficient manufacturing infrastructure and technical ceramics research will strengthen market positioning.

- Companies delivering high-performance, sustainable, and precision-engineered ceramic solutions are expected to gain stronger market share.

- Strategic acquisitions and industrial partnerships will accelerate technology integration and operational scalability.

- Investments in smart ceramics, additive manufacturing, and advanced material engineering will remain major priorities.

- Compliance with energy efficiency standards, emission mandates, and industrial safety regulations will remain critical for sustained growth.

- Organizations scaling smart manufacturing capabilities and advanced ceramic ecosystems are expected to capture substantial future opportunities.

Global Ceramics Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Ceramics Market is expected to maintain strong investment growth driven by infrastructure expansion, industrial modernization, advanced electronics demand, and sustainable manufacturing transformation.

Future capital deployment will increasingly focus on smart ceramics innovation, nanoceramic development, additive manufacturing systems, automated kiln technologies, and integrated digital production ecosystems.

Precision material engineering and sustainable ceramic manufacturing systems are expected to become major long-term innovation priorities.

In conclusion, the Global Ceramics Market represents a high-growth industrial materials investment landscape where advanced material innovation, digital transformation, smart manufacturing, and sustainability-driven production ecosystems will define future capital strategies.

Technology & Innovation

Global Ceramics Market Technology & Innovation Landscape Overview

The global ceramics market is undergoing significant technological transformation driven by advancements in advanced material engineering, smart manufacturing systems, nanoceramic technologies, additive manufacturing, and energy-efficient thermal processing solutions. The evolution of ceramic technologies is increasingly focused on improving material strength, thermal resistance, precision performance, and sustainable manufacturing efficiency across traditional and advanced industrial applications.

Modern ceramic manufacturing systems are integrating AI-powered production optimization, automated kiln control systems, digital twin simulations, precision sintering technologies, and advanced raw material engineering to enhance product quality and operational consistency. These innovations are significantly improving production efficiency, reducing waste generation, and enabling superior performance characteristics.

The market is also witnessing rapid adoption of 3D ceramic printing, smart electroceramics, nanostructured ceramic composites, and low-emission manufacturing technologies that are redefining ceramic production and application capabilities worldwide.

Global Ceramics Market Technology & Innovation Current Scenario

Currently, innovation in the ceramics market is centered around precision manufacturing modernization and high-performance material optimization. Traditional production methods are increasingly being enhanced through automated digital manufacturing systems that improve consistency and scalability.

Additive manufacturing and 3D ceramic printing are gaining widespread adoption for producing complex geometries with high precision, particularly in aerospace, healthcare, and electronics applications.

Nanoceramic engineering is emerging as a major innovation area, enabling enhanced mechanical durability, thermal resistance, electrical conductivity, and wear resistance for technical applications.

Smart kiln technologies are being increasingly deployed to optimize firing cycles, reduce energy consumption, and improve thermal efficiency during ceramic production.

Advanced sintering systems and precision temperature monitoring solutions are improving structural integrity and dimensional accuracy.

Sustainable manufacturing innovations, including waste heat recovery systems and low-carbon processing methods, are expanding rapidly to support regulatory compliance and environmental goals.

Key Technology & Innovation Trends in Global Ceramics Market

- 3D Ceramic Printing: Enabling precision manufacturing of complex high-performance components.

- Nanoceramic Material Engineering: Improving strength, conductivity, and durability performance.

- AI-Driven Process Optimization: Enhancing production efficiency and quality consistency.

- Smart Kiln Automation: Reducing energy consumption through intelligent thermal control.

- Advanced Sintering Technologies: Improving material density and structural performance.

- Digital Twin Manufacturing Simulation: Supporting predictive production optimization.

- Low-Emission Thermal Processing: Enabling sustainable ceramic production.

- Electroceramic Innovation: Supporting advanced electronics and semiconductor applications.

- Bio-Ceramic Development: Expanding medical implant and dental application performance.

- Automated Quality Inspection Systems: Improving precision defect detection and process control.

Strategic Implications of Technology & Innovation

Technological advancements are significantly reshaping competitive dynamics in the ceramics market by shifting competition from conventional material manufacturing toward high-performance, digitally optimized, and sustainable ceramic ecosystems.

Companies investing in advanced material science, additive manufacturing, and intelligent production automation are achieving stronger competitive differentiation through superior product performance and operational efficiency.

The growing integration of digital technologies is enabling manufacturers to improve precision, reduce production variability, and accelerate innovation cycles.

Advanced automation and predictive manufacturing systems are helping producers reduce downtime, optimize resource utilization, and enhance scalability.

However, high capital investment requirements, technical complexity, raw material cost volatility, and regulatory compliance challenges remain significant barriers to widespread modernization.

Global Ceramics Market Technology & Innovation Forward Outlook

The future of ceramic technology is expected to evolve toward fully automated, AI-optimized, and multifunctional smart material ecosystems capable of supporting next-generation industrial and consumer applications.

Emerging innovations include self-healing ceramics, intelligent thermal-responsive materials, autonomous production facilities, quantum-enabled electroceramics, and ultra-lightweight composite ceramic structures.

Advanced multifunctional ceramics may increasingly integrate sensing, conductivity, and adaptive performance capabilities for electronics and aerospace applications.

Connected manufacturing ecosystems supported by IoT and predictive analytics are expected to strengthen real-time process optimization across ceramic production facilities.

Sustainable thermal processing technologies may further enhance energy efficiency while reducing carbon emissions across large-scale manufacturing operations.

Overall, the global ceramics market is evolving toward a highly intelligent ecosystem combining advanced material science, digital automation, sustainable production systems, and precision engineering to redefine high-performance ceramic applications worldwide.

Market Risk

Global Ceramics Market Risk & Disruption Analysis

The Global Ceramics Market operates within a moderate-to-high disruption environment shaped by raw material cost volatility, energy-intensive production processes, sustainability compliance requirements, technological substitution risks, and cyclical construction sector dependence.

While the market demonstrates strong long-term growth supported by infrastructure development, industrial modernization, advanced electronics demand, and technical material innovation, it remains exposed to energy price fluctuations, environmental regulations, supply chain instability, and competitive pressure from alternative advanced materials.

A defining structural characteristic of the market is its reliance on high-temperature manufacturing systems, mineral feedstock availability, kiln efficiency, and production-scale economics, where profitability is closely influenced by fuel costs, automation levels, environmental compliance, and manufacturing yield optimization.

Traditional ceramics and construction materials continue to dominate overall market volume, while high-value growth is increasingly shifting toward advanced technical ceramics, electroceramics, and precision-engineered industrial ceramic applications.

The market is also transitioning from conventional manufacturing toward digitally optimized production systems, smart ceramic materials, additive manufacturing, and low-emission kiln technologies, increasing strategic pressure for modernization.

Global Ceramics Market Current Risk Environment

The current market environment is characterized by strong industrial demand, high production sensitivity, and sustainability-driven transformation.

One of the most significant disruption factors involves energy cost volatility. Ceramic production requires energy-intensive firing processes, making manufacturers highly sensitive to fluctuations in electricity, natural gas, and industrial fuel costs.

Another major risk area is raw material supply chain exposure. Availability and pricing of clay, alumina, zirconia, silica, and specialty minerals can significantly affect production economics and operational continuity.

The market also faces substitution pressure from polymers, composites, advanced metals, and engineered lightweight materials in selected industrial applications.

Additionally, environmental regulations targeting carbon emissions, waste disposal, kiln emissions, and industrial resource efficiency are increasing compliance complexity and modernization costs.

In parallel, construction market cyclicality, global trade uncertainty, and technological performance expectations are reshaping demand patterns across traditional and technical ceramic segments.

Key Market Risk & Disruption Signals in Global Ceramics Market

- Energy Cost Volatility: High-temperature firing processes create sensitivity to industrial energy price fluctuations.

- Raw Material Supply Risk: Mineral sourcing disruptions may impact production continuity and margins.

- Environmental Compliance Pressure: Carbon reduction mandates increase operational costs and capital expenditure.

- Construction Demand Cyclicality: Infrastructure and housing slowdowns directly affect traditional ceramics demand.

- Material Substitution Threat: Advanced composites and engineered metals may replace ceramic applications.

- Technology Modernization Pressure: Need for automation and smart manufacturing raises investment requirements.

- Global Trade & Tariff Exposure: Export restrictions and logistics disruptions affect cross-border ceramic supply chains.

- Quality Standardization Risk: Precision ceramics require increasingly strict technical consistency and performance validation.

Strategic Implications of Market Risk & Disruption

The evolving disruption environment creates both industrial growth opportunities and operational complexity.

One of the most important strategic implications is the need for energy-efficient and digitally optimized manufacturing ecosystems.

Companies increasingly must invest in automated kiln systems, advanced material engineering, additive manufacturing, and emission-control technologies to remain competitive.

Vertical integration across mineral sourcing, advanced processing, precision fabrication, and end-user application development is becoming increasingly valuable.

The convergence of smart manufacturing, nanoceramics, electronics miniaturization, and sustainable industrial processes is reshaping value-chain dynamics.

Firms with stronger technological capability, low-carbon production systems, and specialization in high-performance technical ceramics are expected to strengthen long-term market leadership.

Global Ceramics Market Risk & Disruption Forward Outlook

Looking ahead to 2026???2033, the Global Ceramics Market is expected to become increasingly advanced, sustainable, and performance-driven.

- Expansion of Advanced Technical Ceramics: Industrial and electronics applications will capture growing strategic value.

- Greater Digital Manufacturing Integration: Smart production systems will improve yield and efficiency.

- Rising Sustainability Compliance: Low-emission kiln systems and cleaner production will become critical.

- Higher Adoption of Additive Manufacturing: 3D-printed ceramics will expand application flexibility.

- Growth in Electronics & Healthcare Demand: Precision ceramic components will gain value share.

- Continued Construction Market Sensitivity: Traditional ceramics will remain exposed to macroeconomic cycles.

- Stronger Supply Chain Localization: Regional sourcing strategies will improve resilience.

- Greater Industry Consolidation: Strategic partnerships and acquisitions will strengthen competitive positioning.

In conclusion, the Global Ceramics Market represents a high-volume, technologically evolving, and regulation-sensitive material ecosystem, where energy efficiency, manufacturing modernization, material innovation, and sustainability alignment will define long-term competitive success.

Regulatory Landscape

Global Ceramics Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global ceramics market is shaped by energy efficiency standards, industrial emission regulations, workplace safety requirements, raw material extraction policies, environmental sustainability mandates, and product quality compliance frameworks. As ceramic manufacturing remains energy-intensive and closely linked to industrial infrastructure development, regulatory oversight is increasingly focused on reducing environmental impact, improving operational efficiency, and ensuring product reliability across international markets.

Ceramic manufacturers must comply with a broad range of regulations covering kiln energy consumption, particulate emission controls, silica dust exposure management, industrial waste handling, occupational safety protocols, and technical performance standards for construction and industrial-grade ceramic applications.

The growing adoption of advanced ceramics, digital manufacturing systems, and low-carbon production technologies is accelerating policy development around sustainable industrial modernization, smart process compliance, and circular production practices.

Global Ceramics Market Regulatory & Policy Environment Current Scenario

The current regulatory framework for the ceramics market combines environmental manufacturing regulations, industrial energy optimization requirements, occupational health and safety mandates, and product-specific technical certification standards.

In North America and Europe, strict industrial emission regulations govern particulate matter release, carbon dioxide output, nitrogen oxide emissions, and energy-intensive kiln operations. Manufacturers are increasingly required to adopt cleaner firing technologies and advanced filtration systems.

Workplace safety regulations addressing silica dust exposure, thermal processing hazards, and automated machinery operation are significantly influencing manufacturing facility upgrades and automation adoption.

Asia-Pacific markets including China, India, Japan, and South Korea are strengthening industrial environmental compliance frameworks and energy efficiency mandates as ceramic production capacity continues to expand.

Construction ceramics and technical ceramic components are also subject to building code compliance, fire resistance certification, structural durability standards, and precision performance testing across key application markets.

Key Regulatory & Policy Environment Signals in Global Ceramics Market

- Energy Efficiency Standards: Industrial kiln optimization mandates are driving ceramic manufacturing modernization.

- Emission Compliance Regulations: Environmental policies require strict reduction of greenhouse gas emissions and particulate pollutants.

- Industrial Safety Regulations: Worker protection standards are shaping silica dust management and thermal process safety systems.

- Raw Material Extraction Controls: Mining regulations are influencing sustainable sourcing and resource conservation practices.

- Product Quality Certification: Structural and advanced ceramics must comply with strict technical performance and durability standards.

- Sustainable Manufacturing Policies: Governments are promoting low-carbon ceramic production technologies and circular waste utilization systems.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging ceramic manufacturers to invest heavily in energy-efficient kiln systems, advanced emission filtration technologies, automated compliance monitoring, and sustainable raw material sourcing strategies.

Emission reduction requirements are accelerating adoption of electric kilns, hybrid firing technologies, waste heat recovery systems, and cleaner ceramic processing innovations.

Occupational safety regulations are driving implementation of dust suppression technologies, robotic material handling systems, and digitally monitored industrial safety infrastructure.

Product compliance standards are also encouraging innovation in advanced technical ceramics for electronics, healthcare, aerospace, and high-performance industrial applications.

International harmonization of environmental and technical certification frameworks is creating competitive advantages for manufacturers operating globally compliant production facilities.

Global Ceramics Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global ceramics market is expected to become increasingly sustainability-focused, energy-optimized, and digitally standardized.

Governments are likely to introduce stricter industrial decarbonization targets, expanded energy efficiency requirements, and enhanced environmental reporting obligations for ceramic manufacturing facilities.

Advanced ceramics used in healthcare, electronics, and aerospace are expected to face increasingly specialized technical validation and certification requirements.

Digital manufacturing compliance systems and smart factory operational standards are expected to gain broader regulatory relevance as Industry 4.0 adoption accelerates across ceramic production ecosystems.

Overall, regulatory and policy developments will remain a critical market influence, with companies investing in sustainable manufacturing systems, compliance automation, and energy-efficient innovation expected to maintain long-term competitive advantage.