India White Goods Market Report, Size, Share and Forecast 2026–2033

India White Goods Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

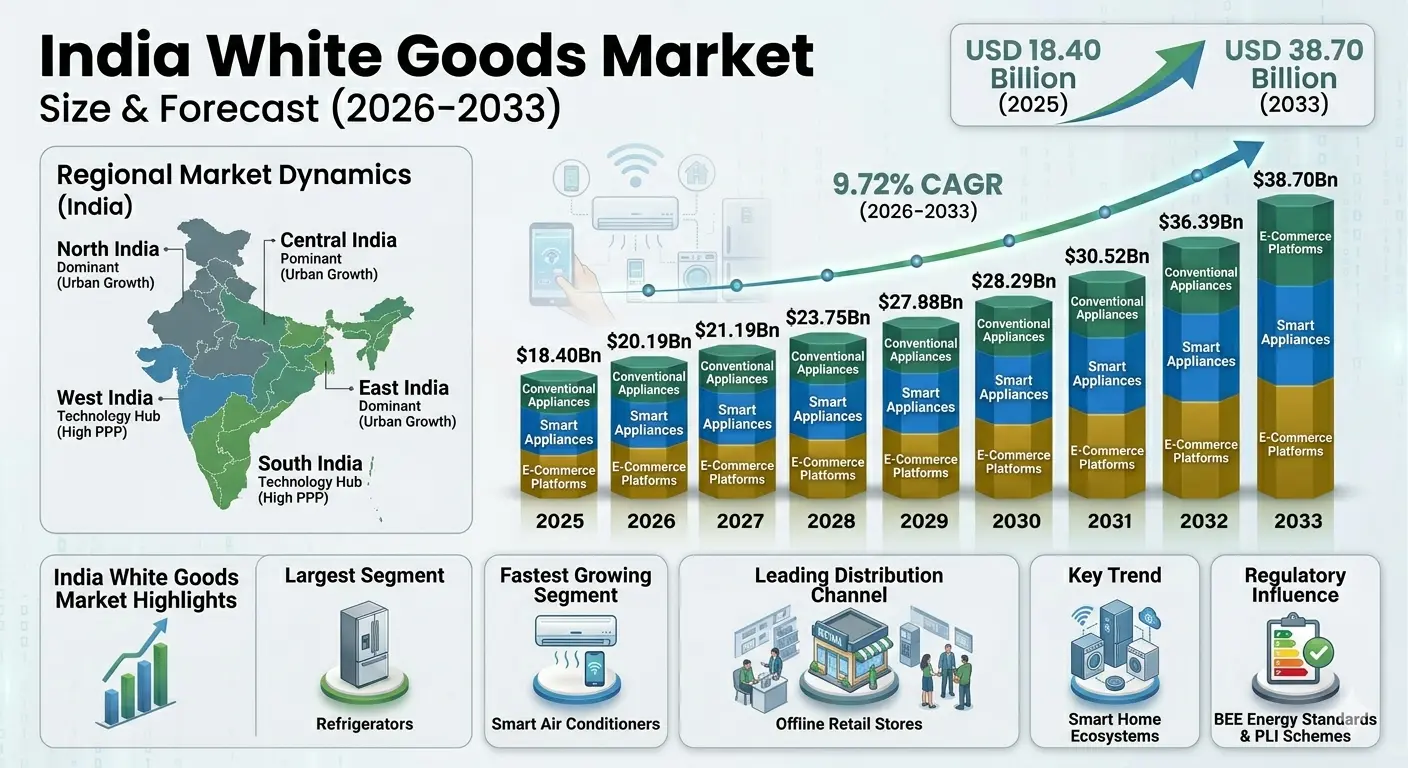

| Market Size (2025) | USD 18.40 Billion |

| Market Size (2033) | USD 38.70 Billion |

| CAGR (2026???2033) | 9.72% |

| Largest Segment | Refrigerators |

| Fastest Growing Segment | Smart Air Conditioners |

| Leading Distribution Channel | Offline Retail Stores |

| Key Trend | Smart Appliances, Energy-Efficient Products & IoT-Enabled Home Solutions |

| Regulatory Influence | BEE Energy Efficiency Standards, Make in India Initiatives & PLI Schemes |

| Future Outlook | Growth Driven by Rising Disposable Income, Urbanization & Smart Home Adoption |

India White Goods Market Size & Forecast

The India White Goods Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 18.40 billion in 2025 and is projected to reach approximately USD 38.70 billion by 2033, registering a CAGR of 9.72%. Market expansion is being driven by rising disposable incomes, rapid urbanization, increasing electrification, growing consumer preference for premium appliances, and the widespread adoption of smart home technologies. Government initiatives supporting domestic manufacturing and energy-efficient products are further accelerating market growth across the country.India White Goods Market Overview

White goods refer to large household appliances used for daily domestic activities, including refrigerators, washing machines, air conditioners, dishwashers, microwave ovens, and water heaters. These products are increasingly integrating smart technologies such as IoT connectivity, artificial intelligence, and energy-efficient features. The Indian market is experiencing significant transformation as consumers prioritize convenience, sustainability, and technologically advanced home appliances.Structural Drivers of Market Growth

1. Rising Urbanization and Household Formation

Rapid urban migration and increasing residential construction activities are driving demand for household appliances across metropolitan and tier-II cities. Market Implications: Manufacturers are expanding product portfolios and distribution networks to cater to growing urban consumer demand.2. Growing Adoption of Smart and Connected Appliances

Consumers are increasingly adopting IoT-enabled refrigerators, smart air conditioners, and intelligent washing machines that offer remote monitoring and automation capabilities. Market Implications: Companies investing in connected appliance ecosystems are expected to gain competitive advantages in the premium segment.3. Government Support for Domestic Manufacturing

Initiatives such as Make in India and Production Linked Incentive (PLI) schemes are encouraging local manufacturing and reducing dependence on imports. Market Implications: Domestic production capabilities are expected to improve supply chain efficiency and support long-term market growth.4. Increasing Demand for Energy-Efficient Appliances

Growing consumer awareness regarding electricity consumption and sustainability is boosting adoption of BEE-rated appliances. Market Implications: Energy-efficient products are expected to witness higher demand across residential and commercial sectors.Market Segmentation Analysis

By Product Type

- Refrigerators: Largest segment driven by widespread household adoption and premium product upgrades.

- Air Conditioners: Rapidly growing category supported by rising temperatures and increasing affordability.

- Washing Machines: Strong demand due to convenience and growing urban lifestyles.

- Microwave Ovens: Increasing penetration among middle-income households.

- Dishwashers: Emerging segment driven by changing consumer preferences and urban living.

- Water Heaters: Consistent demand across residential and commercial applications.

By Technology

- Conventional Appliances: Standard appliances with basic functionality and lower price points.

- Smart Appliances: IoT-enabled devices offering automation, connectivity, and remote control features.

By Distribution Channel

- Offline Retail Stores: Largest channel due to product demonstrations and extensive dealer networks.

- E-Commerce Platforms: Fastest-growing segment supported by digital adoption and attractive discounts.

- Brand-Owned Stores: Expanding presence for premium customer experiences and direct sales.

Regional Market Dynamics

North India

Strong demand driven by urban population growth, residential construction, and rising air conditioner adoption.South India

Major market supported by high purchasing power, technology adoption, and strong retail infrastructure.West India

Significant growth due to industrialization, urbanization, and increasing premium appliance demand.East India

Emerging market benefiting from improving electricity access and rising middle-class consumption.Central India

Growing adoption of white goods supported by economic development and expanding retail penetration.Competitive Landscape

The India White Goods Market is highly competitive, with domestic and international manufacturers competing through innovation, pricing strategies, energy efficiency, and smart technology integration. Key Companies Operating in the Market Include:- LG Electronics India

- Samsung India Electronics

- Whirlpool of India Ltd.

- Haier Appliances India

- Godrej Appliances

- Panasonic India

- Voltas Limited

- Blue Star Limited

- Bosch Home Appliances

- Hitachi Cooling & Heating India

Strategic Outlook

The future of the India White Goods Market will be shaped by technological innovation, premiumization trends, and increasing consumer demand for smart home solutions. Manufacturers are expected to focus on IoT-enabled appliances, artificial intelligence integration, predictive maintenance capabilities, and energy-efficient technologies to differentiate their offerings. The expansion of e-commerce channels, localized manufacturing facilities, and government incentives for domestic production will further strengthen market growth. Rising adoption of connected appliances and smart home ecosystems is expected to create new opportunities for appliance manufacturers and technology providers throughout the forecast period.Final Market Perspective

The India White Goods Market remains one of the fastest-growing consumer appliance markets globally. Strong economic growth, rising disposable incomes, rapid urbanization, and increasing consumer preference for technologically advanced appliances are creating substantial growth opportunities. As smart homes become more mainstream and energy efficiency gains importance, companies investing in innovation, digital connectivity, and localized manufacturing will be well-positioned to capture long-term market opportunities across India.Table of Contents

Table of Contents

- Executive Summary

- India White Goods Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading Distribution Channel Overview

- Key Market Trends in Smart & Energy-Efficient Appliances

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of White Goods

- Scope of the India White Goods Market

- Evolution of Household Appliance Industry in India

- Role of White Goods in Modern Households

- Value Chain Analysis of the White Goods Ecosystem

- Regulatory Influence (BEE Standards, Make in India & PLI Schemes)

- Transition Toward Smart, Connected & Energy-Efficient Appliances

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Rising Urbanization and Household Formation

- Growing Adoption of Smart and Connected Appliances

- Government Support for Domestic Manufacturing

- Increasing Demand for Energy-Efficient Appliances

- Market Restraints

- High Initial Cost of Premium Smart Appliances

- Price Sensitivity in Rural and Semi-Urban Markets

- Supply Chain and Raw Material Cost Volatility

- Market Opportunities

- Expansion of Smart Home Ecosystems

- Growing Demand in Tier-II and Tier-III Cities

- Rising Penetration of Energy-Efficient Products

- Growth of E-Commerce Appliance Sales

- Market Challenges

- Intense Competitive Pricing Pressure

- Counterfeit and Unorganized Market Presence

- Infrastructure and Distribution Challenges in Remote Areas

- Structural Drivers of Market Growth

- India White Goods Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Consumer Purchasing Trends

- Smart Appliance Adoption Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Product Type

- Refrigerators (Largest Segment)

- Air Conditioners (Fastest-Growing Category)

- Washing Machines

- Microwave Ovens

- Dishwashers

- Water Heaters

- By Technology

- Conventional Appliances

- Smart Appliances

- By Distribution Channel

- Offline Retail Stores (Largest Segment)

- E-Commerce Platforms (Fastest-Growing Segment)

- Brand-Owned Stores

- By Product Type

- Regional Market Analysis

- North India

- South India

- West India

- East India

- Central India

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- Smart Appliance & Energy Efficiency Strategies

- Partnerships, Expansions & Product Launches

- Company Profiles

- LG Electronics India

- Samsung India Electronics

- Whirlpool of India Ltd.

- Haier Appliances India

- Godrej Appliances

- Panasonic India

- Voltas Limited

- Blue Star Limited

- Bosch Home Appliances

- Hitachi Cooling & Heating India

- Strategic Outlook

- Future of Smart Home Appliance Ecosystems

- Expansion of IoT-Enabled Consumer Appliances

- Growth of Domestic Manufacturing Capabilities

- Advancements in Energy-Efficient Technologies

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

India White Goods Market Competitive Intensity & Market Structure Overview

The India White Goods Market is highly competitive and moderately fragmented, with strong participation from multinational appliance manufacturers, domestic brands, and emerging smart appliance providers. Competitive intensity is primarily driven by product innovation, energy efficiency, pricing strategies, smart technology integration, distribution reach, and after-sales service capabilities.

Companies compete across refrigerators, air conditioners, washing machines, microwave ovens, dishwashers, and water heaters, with increasing emphasis on premium product offerings and connected home ecosystems. Rising consumer demand for convenience, sustainability, and intelligent appliances is intensifying competition across both urban and semi-urban markets.

The market structure is evolving from conventional appliance manufacturing toward smart, IoT-enabled, and energy-efficient product ecosystems. Strategic investments in local manufacturing, digital retail channels, and advanced consumer engagement platforms are reshaping competitive dynamics across the Indian white goods industry.

India White Goods Market Competitive Intensity & Market Structure Current Scenario

Leading India White Goods Market Companies

LG Electronics India: A leading player in refrigerators, washing machines, air conditioners, and smart home appliances with a strong nationwide distribution network.

Samsung India Electronics: Offers a broad portfolio of premium and connected home appliances, focusing on AI-powered and IoT-integrated solutions.

Whirlpool of India Ltd.: A major manufacturer of refrigerators, washing machines, and kitchen appliances known for energy-efficient and consumer-centric innovations.

Haier Appliances India: Expanding rapidly through localized manufacturing, smart appliances, and premium product offerings across key appliance categories.

Godrej Appliances: A prominent domestic brand focusing on energy-efficient refrigeration, washing solutions, and sustainable appliance technologies.

Panasonic India: Provides a diversified range of consumer appliances with growing investments in connected home and smart living solutions.

Voltas Limited: A market leader in air conditioning solutions, benefiting from strong brand recognition and extensive service infrastructure.

Blue Star Limited: Specializes in cooling and air conditioning products while expanding its presence in residential appliance segments.

Bosch Home Appliances: Focuses on premium kitchen and home appliances, emphasizing energy efficiency, automation, and product reliability.

Hitachi Cooling & Heating India: A key participant in the air conditioning segment, known for advanced inverter technology and energy-efficient systems.

Key Competitive Intensity & Market Structure Drivers

Increasing disposable incomes and rising consumer aspirations are driving demand for premium appliances, intensifying competition among domestic and international manufacturers.

The growing adoption of smart homes and IoT-enabled appliances is accelerating innovation-based competition, particularly in refrigerators, air conditioners, and washing machines.

Government initiatives such as Make in India and Production Linked Incentive (PLI) schemes are encouraging capacity expansion and strengthening domestic manufacturing competitiveness.

Energy efficiency regulations and BEE star-rating standards are influencing product development strategies and creating differentiation opportunities for manufacturers.

Rapid growth of e-commerce platforms and omnichannel retail strategies is increasing market accessibility and intensifying competition across distribution channels.

Strategic Implications of Competitive Intensity & Market Structure

Companies with strong manufacturing capabilities, extensive dealer networks, and advanced smart appliance portfolios are expected to maintain significant competitive advantages.

Investment in IoT integration, artificial intelligence, predictive maintenance features, and connected appliance ecosystems is becoming essential for long-term market differentiation.

Manufacturers focusing on localized production, supply chain optimization, and energy-efficient technologies are likely to strengthen profitability and market positioning.

Strategic expansion into tier-II and tier-III cities through digital commerce and retail partnerships is creating new growth opportunities across the market.

Organizations capable of combining affordability, innovation, energy efficiency, and superior customer service will be best positioned to compete effectively in the evolving Indian white goods industry.

India White Goods Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the India White Goods Market is expected to become increasingly technology-driven as smart appliances, connected home ecosystems, and AI-enabled functionalities gain mainstream adoption.

Future competition will be shaped by advancements in IoT connectivity, voice-controlled appliances, predictive maintenance systems, and energy optimization technologies.

Manufacturers are expected to increase investments in domestic production facilities, digital sales channels, and product innovation to strengthen long-term market positioning.

Over the forecast period, companies that successfully balance affordability, smart technology integration, energy efficiency, localized manufacturing, and customer experience will be best positioned to lead the evolving India White Goods Market.

Value Chain

India White Goods Market Value Chain & Supply Chain Evolution Overview

The India White Goods Market operates through a comprehensive value chain encompassing raw material sourcing, component manufacturing, appliance production, distribution, retailing, and after-sales services. The industry plays a critical role in supporting household modernization, energy efficiency, and smart home adoption across urban and rural India.

The value chain is becoming increasingly localized due to government initiatives such as Make in India and Production Linked Incentive (PLI) schemes, which encourage domestic manufacturing and reduce import dependency. Simultaneously, the integration of IoT technologies, AI-enabled features, and energy-efficient systems is transforming product development and supply chain strategies.

Manufacturers are focusing on supply chain optimization, localized sourcing, digital distribution channels, and smart appliance ecosystems to improve competitiveness and meet evolving consumer preferences.

India White Goods Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Material & Component Supply: Procurement of steel, aluminum, copper, plastics, compressors, motors, electronic components, semiconductors, and insulation materials required for appliance manufacturing.

- Component Manufacturing: Production of compressors, control systems, circuit boards, sensors, motors, cooling systems, and other appliance components.

- Appliance Manufacturing & Assembly: Manufacturing and assembly of refrigerators, washing machines, air conditioners, microwave ovens, dishwashers, and water heaters.

- Technology Integration: Incorporation of IoT connectivity, AI-based controls, smart sensors, energy management systems, and mobile application integration.

- Distribution & Logistics: Warehousing, transportation, dealer networks, regional distribution centers, and supply chain management operations.

- Retail & Sales Channels: Offline retail stores, multi-brand outlets, brand-owned stores, and e-commerce platforms facilitating product sales.

- Installation & After-Sales Services: Product installation, warranty support, maintenance services, spare parts management, and customer support.

- End User Consumption: Residential households, commercial establishments, institutional buyers, and smart home users utilizing white goods appliances.

Company-to-Stage Mapping

- Raw Material & Component Supply: Domestic metal suppliers, electronics manufacturers, semiconductor suppliers, compressor manufacturers, and plastics producers.

- Component Manufacturing: LG Component Solutions, Samsung Electronics suppliers, Panasonic component divisions, and specialized appliance component manufacturers.

- Appliance Manufacturing & Assembly: LG Electronics India, Samsung India Electronics, Whirlpool of India, Haier Appliances India, Godrej Appliances, and Bosch Home Appliances.

- Technology Integration: IoT platform providers, semiconductor companies, smart appliance software developers, and connectivity solution providers.

- Distribution & Logistics: Third-party logistics providers, regional distributors, warehouse operators, and transportation companies.

- Retail & Sales Channels: Reliance Digital, Croma, Vijay Sales, Amazon India, Flipkart, and brand-owned retail stores.

- Installation & After-Sales Services: Authorized service centers, appliance maintenance providers, and manufacturer-supported service networks.

- End User Consumption: Residential consumers, commercial users, hospitality establishments, and institutional buyers across India.

Key Value Chain & Supply Chain Evolution Signals

- Expansion of Domestic Manufacturing: PLI schemes and Make in India initiatives are encouraging localized production and supply chain development.

- Growth of Smart Appliance Ecosystems: Increasing adoption of IoT-enabled refrigerators, washing machines, and air conditioners is transforming product value chains.

- Rising Demand for Energy-Efficient Products: BEE-rated appliances are gaining popularity due to lower electricity consumption and sustainability concerns.

- Digitalization of Distribution Channels: E-commerce platforms and omnichannel retail strategies are reshaping appliance purchasing behavior.

- Supply Chain Localization: Manufacturers are increasing local sourcing of components to improve resilience and reduce import dependence.

- Integration of AI and Predictive Maintenance: Smart diagnostics and remote monitoring capabilities are enhancing customer experience and product performance.

Strategic Implications of Value Chain Evolution

- Investment in Local Manufacturing Capacity: Companies expanding domestic production can benefit from government incentives and improved cost competitiveness.

- Expansion of Smart Product Portfolios: Connected appliances offer opportunities for premium pricing and stronger customer engagement.

- Strengthening Omnichannel Distribution: Integration of online and offline channels enhances market reach and customer accessibility.

- Focus on Energy Efficiency Innovation: Advanced energy-saving technologies support regulatory compliance and consumer demand.

- Supply Chain Resilience Enhancement: Localized sourcing strategies help reduce disruptions and improve operational efficiency.

- Growth of Service-Based Revenue Models: After-sales services, extended warranties, and smart maintenance solutions are creating recurring revenue opportunities.

India White Goods Market Value Chain & Supply Chain Evolution Forward Outlook

- Expansion of domestic appliance manufacturing under government incentive programs.

- Increased adoption of IoT-enabled and AI-powered smart appliances.

- Growth of energy-efficient and environmentally sustainable product offerings.

- Further development of localized component supply chains.

- Expansion of e-commerce and omnichannel appliance retail networks.

- Integration of predictive maintenance and connected home ecosystems.

The India White Goods Market value chain is expected to become increasingly technology-driven, localized, and consumer-centric. Digital connectivity, sustainability, and manufacturing self-reliance will play critical roles in shaping future industry dynamics.

Companies that successfully combine localized manufacturing, smart appliance innovation, efficient distribution networks, and strong after-sales service capabilities will be best positioned to capture long-term growth opportunities in India’s expanding white goods industry.

Investment Activity

India White Goods Market Investment & Funding Dynamics Overview (2026???2033)

The India White Goods Market is witnessing substantial investment activity driven by rising disposable incomes, rapid urbanization, increasing demand for premium household appliances, and the growing adoption of smart home technologies. Domestic and international appliance manufacturers, private equity investors, venture capital firms, technology companies, and strategic investors are actively deploying capital toward smart appliances, energy-efficient product development, manufacturing expansion, IoT-enabled home solutions, and distribution network enhancement.

Investment momentum is further supported by government initiatives such as the Make in India program, Production Linked Incentive (PLI) schemes, and energy-efficiency regulations, which are encouraging local production and strengthening India’s consumer appliance manufacturing ecosystem. Capital allocation is increasingly focused on advanced manufacturing facilities, connected appliance technologies, AI-enabled smart devices, and sustainable product innovation.

Additionally, growing investments in digital retail platforms, omnichannel distribution models, supply chain modernization, and energy-efficient appliance technologies are creating long-term growth opportunities across the Indian white goods industry.

Current Investment & Funding Landscape

The market is currently experiencing strong capital inflows as manufacturers expand production capacity to meet rising consumer demand across urban and semi-urban regions. Companies are investing heavily in local manufacturing plants, product innovation centers, smart appliance ecosystems, and advanced supply chain infrastructure.

Significant funding is being directed toward IoT-enabled refrigerators, smart air conditioners, intelligent washing machines, and energy-efficient appliances as consumers increasingly seek convenience, connectivity, and sustainability.

Strategic partnerships among appliance manufacturers, technology providers, e-commerce platforms, and component suppliers are further accelerating innovation and strengthening market competitiveness across the value chain.

Key Investment & Funding Dynamics Signals

- Growing demand for smart and connected household appliances is driving technology-focused investments.

- Expansion of domestic manufacturing facilities under PLI schemes is attracting significant capital expenditure.

- Rising adoption of energy-efficient and BEE-rated appliances is encouraging investment in sustainable product development.

- Increasing penetration of e-commerce and omnichannel retail networks is supporting investments in digital sales infrastructure.

- Strong demand for smart air conditioners and premium appliances is accelerating funding toward innovation and product differentiation.

- Growing integration of AI, IoT, and smart home ecosystems is creating new investment opportunities across connected appliance segments.

- Supply chain localization initiatives are driving investments in component manufacturing and logistics optimization.

Strategic Implications of Investment & Funding Dynamics

- Companies investing in smart appliance technologies and connected home ecosystems are expected to strengthen long-term market leadership.

- Capital allocation toward local manufacturing and production expansion will improve cost competitiveness and supply chain resilience.

- Manufacturers focusing on energy-efficient and environmentally sustainable products are likely to gain stronger consumer preference.

- Strategic collaborations between technology companies, appliance manufacturers, and retail platforms will accelerate innovation and market penetration.

- Investments in AI-powered features, predictive maintenance capabilities, and smart connectivity solutions will enhance product differentiation.

- Compliance with BEE standards, environmental regulations, and domestic manufacturing policies will continue influencing investment decisions.

- Organizations building integrated capabilities across manufacturing, technology development, and digital distribution are expected to capture greater long-term value.

Forward Outlook

Looking ahead, the India White Goods Market is expected to maintain strong investment momentum driven by rising household incomes, expanding urban populations, increasing smart home adoption, and supportive government manufacturing initiatives.

Future capital deployment will increasingly focus on next-generation smart appliances, AI-enabled consumer electronics, energy-efficient product innovation, localized production facilities, and connected home ecosystems.

As consumers continue prioritizing convenience, sustainability, and digital connectivity, investment activity is expected to expand across smart appliance development, advanced manufacturing, retail digitization, and energy management technologies.

In conclusion, the India White Goods Market represents a high-growth consumer appliance investment landscape where smart technologies, energy efficiency, domestic manufacturing expansion, and digital retail transformation will define future funding priorities, competitive differentiation, and long-term industry growth.

Technology & Innovation

India White Goods Market Technology & Innovation Landscape Overview

The India white goods market is witnessing significant technological transformation driven by advancements in IoT-enabled appliances, artificial intelligence (AI)-based automation, smart home connectivity, energy-efficient technologies, and cloud-integrated consumer electronics ecosystems. Rising consumer demand for convenience, sustainability, and premium living experiences is accelerating the adoption of intelligent household appliances across urban and semi-urban regions.

Modern white goods are increasingly integrating Wi-Fi connectivity, voice assistant compatibility, sensor-based automation, predictive maintenance capabilities, and mobile application controls to enhance user convenience and operational efficiency. These innovations are enabling seamless integration of appliances into connected smart home environments.

The market is also experiencing strong adoption of inverter technologies, AI-driven cooling systems, smart energy management solutions, and eco-friendly refrigerants, helping consumers reduce electricity consumption while improving appliance performance and reliability.

India White Goods Market Technology & Innovation Current Scenario

Current innovation in the India white goods market is primarily centered around smart appliance ecosystems, energy optimization, and digital consumer experiences. Manufacturers are increasingly introducing connected appliances that offer remote operation, automated performance optimization, and real-time monitoring capabilities.

Smart refrigerators, air conditioners, and washing machines are becoming increasingly popular as consumers seek enhanced convenience, intelligent automation, and improved energy management.

Artificial intelligence integration is enabling appliances to learn user behavior, optimize operating cycles, monitor performance, and provide predictive maintenance alerts, significantly improving user experience and product efficiency.

Energy-efficient technologies such as inverter compressors, variable-speed motors, and advanced insulation systems are becoming standard features as consumers increasingly prioritize sustainability and lower utility costs.

Manufacturers are also expanding local manufacturing capabilities under government-supported initiatives such as Make in India and Production Linked Incentive (PLI) schemes, strengthening domestic supply chains and accelerating product innovation.

Additionally, omnichannel retail strategies and digital commerce platforms are enhancing product accessibility, enabling brands to reach a wider consumer base across metropolitan, tier-II, and tier-III cities.

Key Technology & Innovation Trends in India White Goods Market

- IoT-Enabled Smart Appliances: Connected refrigerators, washing machines, and air conditioners with remote monitoring and control capabilities.

- AI-Powered Appliance Intelligence: Adaptive cooling, smart washing cycles, predictive diagnostics, and automated performance optimization.

- Energy-Efficient Technologies: Inverter compressors, variable-speed motors, and eco-friendly refrigerants reducing power consumption.

- Voice-Control Integration: Compatibility with digital assistants such as Amazon Alexa and Google Assistant.

- Smart Air Conditioning Systems: AI-based temperature control, occupancy sensing, and intelligent energy management.

- Predictive Maintenance Solutions: Real-time system diagnostics and automated service notifications.

- Cloud-Based Appliance Connectivity: Centralized management of connected home appliances through mobile applications.

- Advanced Water-Saving Technologies: Efficient washing systems reducing water usage and enhancing sustainability.

- Sustainable Manufacturing Innovations: Environment-friendly production processes and recyclable material utilization.

- Digital Commerce & Customer Engagement: AI-driven product recommendations and enhanced omnichannel retail experiences.

Strategic Implications of Technology & Innovation

Technological advancements are transforming the white goods industry from traditional appliance manufacturing into a connected, intelligent, and sustainability-focused consumer ecosystem.

Companies investing in AI-powered smart appliances, connected home integration, and energy-efficient product development are strengthening their competitive positioning and attracting premium consumer segments.

The convergence of IoT, cloud computing, artificial intelligence, and smart home technologies is creating opportunities for value-added services, predictive maintenance solutions, and long-term customer engagement.

Government policies promoting domestic manufacturing and energy-efficient products are encouraging innovation while improving industry competitiveness and supply chain resilience.

However, affordability challenges, uneven digital infrastructure, and varying levels of smart home adoption across regions continue to influence the pace of technology penetration within the market.

India White Goods Market Technology & Innovation Forward Outlook

The future of the India white goods market is expected to evolve toward fully connected, AI-driven, and energy-optimized smart home ecosystems supported by advanced automation and digital consumer experiences.

Emerging innovations include self-learning appliances, AI-based home energy management systems, predictive maintenance platforms, and integrated multi-device smart home networks.

Manufacturers are expected to increasingly leverage machine learning, cloud analytics, and real-time performance monitoring to deliver personalized appliance experiences and improve operational efficiency.

Government initiatives supporting domestic manufacturing, energy conservation, and digital infrastructure development will continue to accelerate technological innovation and market expansion.

Overall, the India white goods market is transitioning into a highly connected and technology-driven ecosystem where smart automation, sustainability, and intelligent consumer experiences will redefine the future of household appliances across the country.

Market Risk

India White Goods Market Risk Factors & Disruption Threats Overview

The India White Goods Market operates within a rapidly evolving consumer electronics and home appliance ecosystem driven by urbanization, rising disposable incomes, technological advancements, and expanding smart home adoption. While the industry benefits from strong demand for refrigerators, air conditioners, washing machines, and other household appliances, it faces significant risks related to raw material price volatility, supply chain disruptions, regulatory compliance requirements, and changing consumer purchasing behavior.

A major structural risk is the industry’s dependence on imported components, semiconductors, compressors, electronic circuits, and specialized materials. Global supply chain disruptions, geopolitical tensions, and currency fluctuations can significantly impact manufacturing costs and product availability.

Another important disruption factor is volatility in raw material prices, including steel, aluminum, copper, plastics, and electronic components. Rising input costs can compress profit margins and create pricing challenges in a highly competitive market.

The market is also exposed to regulatory risks associated with evolving energy efficiency standards, environmental regulations, e-waste management requirements, and product safety certifications. Compliance costs may increase as government agencies strengthen sustainability and efficiency mandates.

Additionally, intense competition from domestic manufacturers, multinational brands, and emerging direct-to-consumer appliance companies is creating pricing pressure and accelerating innovation cycles across product categories.

India White Goods Market Risk Factors & Disruption Threats Current Scenario

The current market is characterized by strong consumer demand for energy-efficient and smart appliances, supported by growing urbanization, housing development, and rising middle-class purchasing power.

Manufacturers are increasingly investing in local production facilities, smart appliance ecosystems, and digital technologies to align with Make in India initiatives and reduce import dependency.

At the same time, supply chain uncertainties, fluctuating commodity prices, and semiconductor shortages continue to impact production planning and inventory management across the industry.

Consumers are showing increasing preference for IoT-enabled appliances, inverter technologies, and premium product offerings that provide convenience, energy savings, and connected home experiences.

Competition remains intense as established brands and new entrants expand their product portfolios, strengthen distribution networks, and leverage e-commerce platforms to reach a broader customer base.

Key Risk Factors & Disruption Threats Signals in India White Goods Market

A major disruption signal is the accelerating adoption of smart home technologies, driving demand for connected appliances that integrate with mobile applications, voice assistants, and home automation systems.

Another important signal is the tightening of BEE energy efficiency standards and sustainability regulations, encouraging manufacturers to develop environmentally responsible and energy-saving products.

The rapid growth of e-commerce and omnichannel retailing is reshaping consumer purchasing patterns, reducing dependence on traditional retail formats and increasing digital competition.

Rising consumer awareness regarding sustainability, electricity consumption, and environmental impact is influencing product selection and purchasing decisions.

Increased localization of manufacturing under government-supported initiatives such as Production Linked Incentive (PLI) schemes is strengthening domestic production capabilities and supply chain resilience.

Strategic Implications of Risk Factors & Disruption Threats in India White Goods Market

Manufacturers must prioritize product innovation, smart connectivity, and energy-efficient technologies to meet evolving consumer expectations and regulatory requirements.

Investment in local manufacturing facilities, supplier diversification, and component localization strategies will be critical for reducing supply chain vulnerabilities and improving cost competitiveness.

Companies should strengthen digital sales channels, omnichannel retail strategies, and direct-to-consumer engagement models to adapt to changing buying behavior.

Compliance with BEE standards, environmental regulations, product safety requirements, and e-waste management policies will be essential for long-term market sustainability.

Strategic partnerships with technology providers, smart home ecosystem developers, and e-commerce platforms will play an important role in expanding market reach and enhancing customer experiences.

India White Goods Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the India White Goods Market is expected to evolve toward highly connected, energy-efficient, and technologically advanced household appliance ecosystems.

Smart appliances integrated with artificial intelligence, predictive maintenance capabilities, voice control, and IoT connectivity are expected to become mainstream across urban households.

Government initiatives supporting domestic manufacturing, localization, and energy conservation are likely to strengthen industry competitiveness and encourage further investments.

Sustainability trends, including environmentally friendly refrigerants, recyclable materials, and energy-saving technologies, will increasingly influence product development and purchasing preferences.

Overall, the market will remain strongly growth-oriented but increasingly shaped by technological innovation, regulatory compliance, supply chain resilience, and sustainability requirements. Long-term market leaders will be defined by their ability to deliver affordable, energy-efficient, smart, and locally manufactured white goods solutions that align with the evolving needs of Indian consumers.

Regulatory Landscape

India White Goods Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the India White Goods Market is evolving rapidly as the government focuses on strengthening domestic manufacturing capabilities, improving energy efficiency, promoting sustainable consumption, and supporting technological innovation. Regulatory frameworks are playing a critical role in shaping product standards, manufacturing investments, import-export dynamics, and consumer adoption of energy-efficient household appliances.

White goods manufacturers, component suppliers, distributors, retailers, and technology providers must comply with a range of regulations covering energy efficiency standards, product safety requirements, environmental compliance, electronic waste management, and domestic manufacturing incentives. As smart and connected appliances gain popularity, regulatory attention is also expanding toward cybersecurity, data privacy, and IoT interoperability standards.

Government initiatives such as Make in India, Production Linked Incentive (PLI) schemes, and energy conservation programs are encouraging investments in local production, advanced manufacturing technologies, and sustainable appliance development across the country.

India White Goods Market Regulatory & Policy Environment Current Scenario

The current regulatory environment is characterized by strong government support for energy-efficient appliances and domestic manufacturing expansion. The Bureau of Energy Efficiency (BEE) continues to play a central role in promoting energy conservation through mandatory and voluntary star-rating programs for household appliances.

BEE energy efficiency standards are significantly influencing consumer purchasing decisions and product development strategies. Manufacturers are increasingly focused on improving energy performance to comply with evolving efficiency benchmarks and gain competitive advantages in the market.

The Production Linked Incentive (PLI) scheme is encouraging investments in local manufacturing of air conditioners, components, and related appliances. The initiative aims to strengthen India’s manufacturing ecosystem, reduce import dependence, and improve global competitiveness.

Product safety and quality regulations remain critical for market operations. White goods manufacturers must comply with standards established by the Bureau of Indian Standards (BIS), ensuring product reliability, consumer safety, and performance consistency.

Environmental regulations, including e-waste management rules and sustainability initiatives, are also influencing product lifecycle management, recycling practices, and responsible disposal of electronic appliances across the country.

Key Regulatory & Policy Environment Signals in India White Goods Market

- BEE Energy Efficiency Standards: Mandatory and voluntary energy labeling programs promoting reduced electricity consumption and higher appliance efficiency.

- Production Linked Incentive (PLI) Schemes: Government incentives supporting domestic manufacturing, capacity expansion, and localization of appliance components.

- Make in India Initiatives: Policies encouraging local production, foreign investment, technology transfer, and manufacturing competitiveness.

- Bureau of Indian Standards (BIS) Compliance: Product quality, safety, testing, and certification requirements for household appliances and electronic equipment.

- E-Waste Management Regulations: Frameworks governing collection, recycling, disposal, and environmental responsibility throughout the product lifecycle.

- Smart Appliance & Digital Connectivity Standards: Emerging guidelines related to IoT-enabled devices, cybersecurity, consumer data protection, and connected home ecosystems.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is encouraging manufacturers to prioritize energy efficiency, domestic production, product quality, and sustainable business practices. Compliance with regulatory requirements is increasingly becoming a key factor influencing consumer trust and market competitiveness.

BEE energy efficiency regulations are accelerating innovation in low-power consumption technologies, inverter-based systems, and environmentally friendly appliance designs. Companies offering highly rated energy-efficient products are expected to strengthen their market position.

PLI schemes and Make in India initiatives are encouraging both domestic and international manufacturers to expand local production facilities, increase component localization, and improve supply chain resilience.

BIS certification requirements are driving investments in product testing, quality assurance, and compliance management systems, ensuring higher reliability and performance standards across the market.

Environmental regulations are creating opportunities for companies that adopt sustainable manufacturing processes, recyclable materials, and circular economy practices aligned with India’s long-term sustainability objectives.

India White Goods Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the India White Goods Market is expected to become increasingly focused on energy conservation, manufacturing self-reliance, sustainability, and digital innovation. Policymakers are likely to strengthen efficiency standards and expand support for advanced manufacturing investments.

BEE energy performance requirements are expected to become more stringent, encouraging broader adoption of ultra-efficient appliances, inverter technologies, and smart energy management systems. Manufacturers will likely face increasing pressure to improve product efficiency and environmental performance.

Government initiatives supporting domestic manufacturing are expected to continue evolving, with additional incentives for component localization, export competitiveness, and next-generation appliance technologies.

Environmental regulations may place greater emphasis on e-waste recycling, resource efficiency, sustainable materials, and carbon footprint reduction throughout the appliance value chain. Smart appliance adoption may also drive the introduction of stronger cybersecurity and connected-device governance standards.

Overall, the future regulatory landscape will be shaped by the convergence of BEE energy efficiency standards, PLI schemes, Make in India initiatives, BIS quality regulations, environmental sustainability requirements, and smart appliance governance frameworks. Companies capable of delivering compliant, energy-efficient, technologically advanced, and locally manufactured products will be best positioned to capitalize on long-term opportunities within the evolving India White Goods Market.