Global Grocery Market Size and Share Analysis 2026-2033

Global Grocery Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 12.8 Trillion |

| Market Size (2033) | USD 18.6 Trillion |

| CAGR (2026???2033) | 4.8% |

| Largest Segment | Packaged Food Products |

| Fastest Growing Segment | Online Grocery & Quick Commerce Platforms |

| Leading End-Use Segment | Households |

| Key Trend | Omnichannel Retailing with AI-Driven Inventory and Personalized Shopping |

| Dominant Region | Asia-Pacific |

| Fastest Growing Region | Middle East & Africa |

| Primary Growth Driver | Rising Population, Urbanization, and Demand for Convenient Food Consumption |

Global Grocery Market Size & Forecast

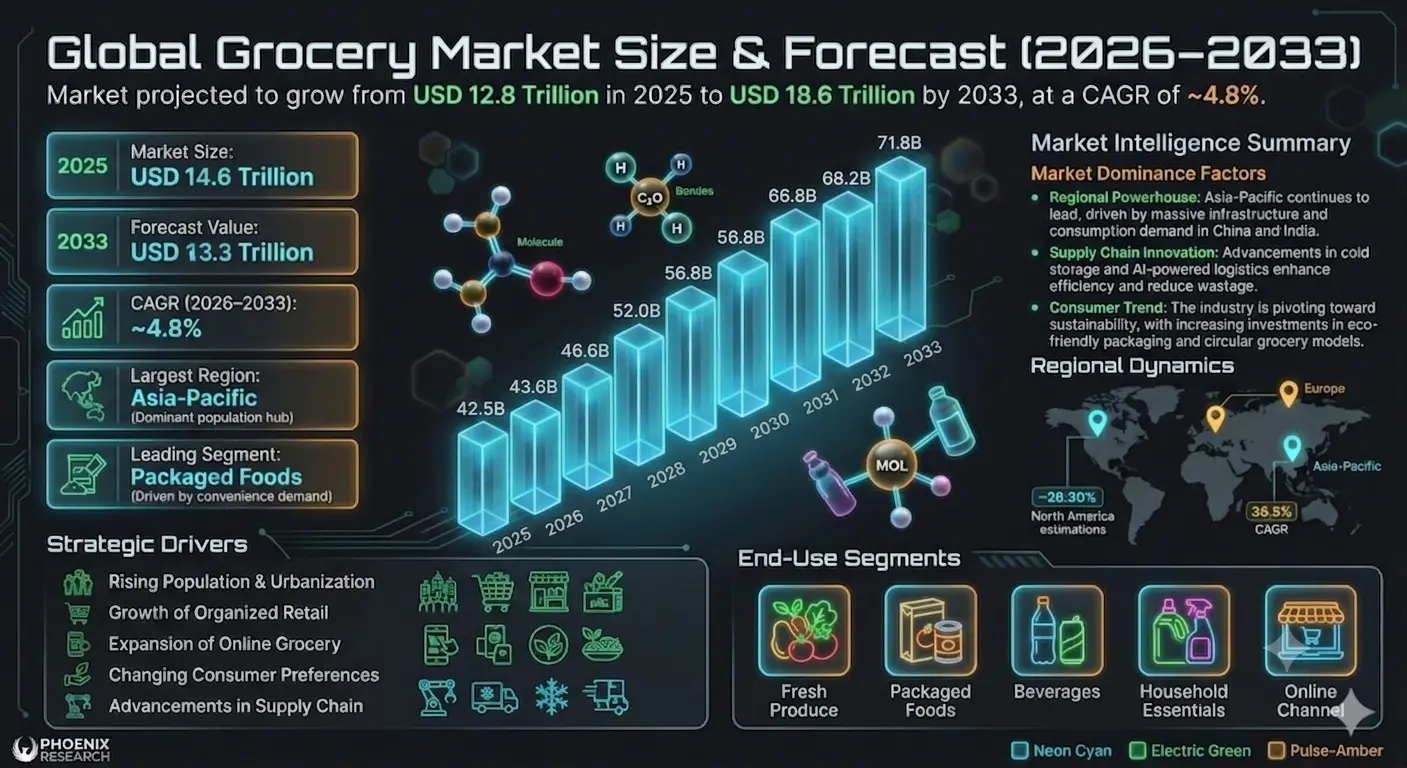

The global grocery market is projected to witness steady and sustained growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 12.8 trillion in 2025 and is expected to reach nearly USD 18.6 trillion by 2033, expanding at a CAGR of around 4.8%. This growth is driven by rising global population, increasing urbanization, evolving consumer lifestyles, and strong demand for packaged, fresh, and convenience food products. The grocery market forms the backbone of the global food retail industry, encompassing essential food and beverage products purchased for daily household consumption. It includes fresh produce, dairy products, meat and seafood, bakery items, packaged foods, beverages, frozen foods, and household essentials. Changing consumer preferences toward convenience, health-conscious eating, and time-saving shopping formats are reshaping the global grocery landscape. The expansion of modern retail formats such as supermarkets, hypermarkets, convenience stores, and online grocery platforms is further accelerating market growth. In addition, digital transformation in retail, including e-commerce grocery delivery, quick commerce models, and AI-driven inventory management, is significantly enhancing accessibility and efficiency in grocery distribution worldwide.Global Grocery Market Overview

The grocery market represents one of the largest and most essential segments of the global retail industry. It includes the sale of food and household consumables through both offline and online channels. The market plays a critical role in ensuring food security, daily consumption needs, and supply chain stability across urban and rural populations. The industry is highly diverse, ranging from traditional retail stores and local grocery shops to large-scale supermarket chains and advanced digital grocery platforms. Major players include Walmart, Tesco, Carrefour, Costco, Kroger, Aldi, Lidl, Amazon Fresh, and regional retail chains across emerging markets. The market is undergoing rapid transformation due to the rise of omnichannel retailing, where physical stores and digital platforms are integrated to provide seamless shopping experiences. Consumers increasingly prefer hybrid shopping models that combine in-store selection with online ordering and home delivery services. Supply chain modernization, cold storage expansion, and improved logistics infrastructure are also enhancing product availability and reducing food wastage across global grocery networks.Key Drivers of Global Grocery Market Growth

Rising Global Population and Urbanization

Increasing population and rapid urbanization are driving consistent demand for essential food and grocery products, especially in densely populated urban centers.Growth of Organized Retail and Supermarkets

The expansion of supermarkets, hypermarkets, and organized retail chains is transforming grocery purchasing behavior by offering wider product variety, better pricing, and improved shopping experiences.Expansion of Online Grocery Platforms

E-commerce and quick-commerce grocery delivery services are gaining popularity due to convenience, faster delivery times, and increasing smartphone penetration.Changing Consumer Preferences

Consumers are increasingly shifting toward healthy, organic, ready-to-eat, and packaged food products, influencing product innovation and retail strategies.Advancements in Supply Chain and Logistics

Improvements in cold chain infrastructure, inventory management systems, and AI-powered logistics are enhancing efficiency and reducing food spoilage.Global Grocery Market Segmentation

By Product Type

The market is segmented into fresh produce (fruits and vegetables), dairy products, meat & seafood, bakery & confectionery, beverages, packaged foods, frozen foods, and household essentials. Packaged foods account for a significant share due to rising demand for convenience products.By Distribution Channel

Distribution channels include supermarkets, hypermarkets, convenience stores, traditional grocery stores, and online retail platforms. Online grocery channels are the fastest-growing segment due to rapid digital adoption.By Category

The market includes organic and conventional grocery products. Organic grocery items are gaining traction due to increasing health awareness and demand for chemical-free food products.By End User

End users include households, food service providers, restaurants, hotels, and institutional buyers. Households remain the dominant consumer segment globally.Regional Market Dynamics

Asia-Pacific dominates the global grocery market due to large population base, rapid urbanization, and expanding retail infrastructure in countries such as China, India, Japan, and Southeast Asia. North America represents a mature but highly advanced grocery market driven by strong supermarket chains, high consumer spending, and rapid growth of online grocery services. Europe is characterized by well-established retail networks, strong demand for organic products, and increasing focus on sustainability and food quality standards. Latin America is witnessing steady growth due to expanding retail modernization and increasing penetration of organized grocery chains. Middle East & Africa is emerging as a growth region supported by urban development, rising incomes, and expanding retail infrastructure.Competitive Landscape

The global grocery market is highly competitive and fragmented, with the presence of multinational retail giants, regional supermarket chains, and emerging online grocery platforms. Key players include Walmart, Amazon (Amazon Fresh), Tesco, Carrefour, Costco, Kroger, Aldi, Lidl, and regional retail operators. Companies are focusing on expanding store networks, enhancing private label offerings, and investing in digital transformation strategies to improve customer experience and operational efficiency. E-commerce giants are increasingly competing with traditional retailers through fast delivery models, subscription services, and AI-driven personalized shopping experiences. Price competition, supply chain efficiency, and customer convenience remain key competitive factors in the global grocery market.Strategic Outlook

The strategic outlook for the grocery market remains stable and positive due to its essential nature and continuous demand. Future growth will be driven by digital transformation, automation in supply chains, and increasing adoption of AI-based inventory and demand forecasting systems. Quick commerce, hyperlocal delivery models, and automated warehouses are expected to reshape grocery retailing in urban areas. Sustainability initiatives, such as reduced plastic packaging and eco-friendly supply chains, are also gaining importance. Retailers that successfully integrate physical stores with digital platforms and enhance customer convenience will maintain a strong competitive advantage in the evolving grocery ecosystem.Final Market Perspective

The global grocery market remains one of the most stable and essential industries worldwide, driven by continuous demand for food and household essentials. Despite intense competition, the market continues to expand due to population growth, urbanization, and technological advancements in retail and logistics. Future success in the grocery market will depend on digital innovation, supply chain efficiency, sustainability practices, and the ability to meet evolving consumer preferences. Companies that adapt to omnichannel retailing and data-driven operations will lead the next phase of global grocery industry transformation.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Grocery Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Grocery Market

- 2.2 Scope of the Study

- 2.3 Evolution of Global Food Retail Industry

- 2.4 Grocery Value Chain & Supply Infrastructure

- 2.5 Product Categories & Retail Formats

- 2.6 Sustainability & Regulatory Environment

- 2.7 Digital Transformation in Grocery Retail

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Global Population & Urbanization

- 4.1.2 Growth of Organized Retail & Supermarkets

- 4.1.3 Expansion of Online Grocery Platforms

- 4.1.4 Changing Consumer Preferences

- 4.1.5 Advancements in Supply Chain & Logistics

- 4.2 Restraints

- 4.2.1 Supply Chain Disruptions

- 4.2.2 Price Volatility in Food Commodities

- 4.2.3 High Operational & Logistics Costs

- 4.2.4 Food Waste & Sustainability Challenges

- 4.3 Opportunities

- 4.3.1 Growth of Quick Commerce & Hyperlocal Delivery

- 4.3.2 Expansion of Private Label Brands

- 4.3.3 AI-Driven Retail & Demand Forecasting

- 4.3.4 Sustainable & Organic Product Demand

- 4.4 Challenges

- 4.4.1 Intense Price Competition

- 4.4.2 Logistics & Cold Chain Limitations

- 4.4.3 Digital Transformation Barriers

- 4.4.4 Inventory Management Complexity

- 4.1 Drivers

- 5. Global Grocery Market Analysis (USD Trillion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Retail Channel Performance

- 5.6 Consumption & Demand Trends

- 6. Market Segmentation (USD Trillion), 2026-2033

- 6.1 By Product Type

- 6.1.1 Fresh Produce

- 6.1.2 Dairy Products

- 6.1.3 Meat & Seafood

- 6.1.4 Bakery & Confectionery

- 6.1.5 Beverages

- 6.1.6 Packaged Foods

- 6.1.7 Frozen Foods

- 6.1.8 Household Essentials

- 6.2 By Distribution Channel

- 6.2.1 Supermarkets

- 6.2.2 Hypermarkets

- 6.2.3 Convenience Stores

- 6.2.4 Traditional Grocery Stores

- 6.2.5 Online Grocery Platforms

- 6.3 By Category

- 6.3.1 Organic Grocery Products

- 6.3.2 Conventional Grocery Products

- 6.4 By End User

- 6.4.1 Households

- 6.4.2 Food Service Providers

- 6.4.3 Restaurants & Hotels

- 6.4.4 Institutional Buyers

- 6.1 By Product Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Retail Chain Benchmarking

- 8.3 Online vs Offline Channel Performance

- 8.4 Private Label Strategy Analysis

- 8.5 Omnichannel Retail Strategies

- 9. Company Profiles

- 9.1 Walmart

- 9.2 Amazon (Amazon Fresh)

- 9.3 Tesco

- 9.4 Carrefour

- 9.5 Costco Wholesale

- 9.6 Kroger

- 9.7 Aldi

- 9.8 Lidl

- 9.9 Regional Retail Chains

- 9.10 Emerging Online Grocery Platforms

- 10. Strategic Intelligence & Retail AI Insights

- 10.1 Demand Forecasting Systems

- 10.2 Inventory Optimization Analytics

- 10.3 Supply Chain Automation Tools

- 10.4 Pricing & Promotion Intelligence

- 10.5 Customer Behavior Analytics

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Quick Commerce Models

- 11.2 Growth of Omnichannel Retail Ecosystems

- 11.3 AI-Driven Retail Automation

- 11.4 Sustainable Packaging & Supply Chains

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Grocery Market Competitive Intensity & Market Structure Overview

The Global Grocery Market is one of the most competitive and structurally complex segments of the global retail industry, characterized by a mix of multinational retail giants, regional supermarket chains, traditional grocery stores, and rapidly expanding digital commerce platforms. Competition is primarily driven by pricing strategies, product assortment, supply chain efficiency, and customer convenience across both offline and online channels.

Competitive intensity in the market is high due to low product differentiation in core grocery categories and the essential nature of demand. Retailers continuously compete on price optimization, private label expansion, discount strategies, and loyalty programs to retain customers in an environment where switching costs for consumers remain relatively low.

The market structure is highly fragmented at the global level but increasingly consolidated within organized retail segments. Large-scale players such as Walmart, Tesco, Carrefour, Costco, Kroger, Aldi, and Lidl dominate organized retail, while millions of small independent grocery stores continue to serve local and rural markets, especially in emerging economies.

Global Grocery Market Competitive Intensity & Market Structure Current Scenario

Leading Retailers & Grocery Platform Players

Walmart: Global retail leader with extensive supermarket and hypermarket networks, strong supply chain integration, and dominant presence in North America and international markets.

Amazon (Amazon Fresh & Whole Foods): Key disruptor in online grocery retail, leveraging e-commerce infrastructure, rapid delivery systems, and AI-driven personalization.

Carrefour: Major European retailer with strong global footprint and diversified grocery product offerings across multiple formats.

Tesco: UK-based retail giant focusing on omnichannel grocery retailing and advanced loyalty program ecosystems.

Aldi: Discount grocery leader known for cost-efficient operations, private label dominance, and aggressive pricing strategy.

Lidl: Strong competitor in the discount retail segment with expanding international presence and efficient supply chain model.

Costco: Membership-based wholesale retailer offering bulk grocery products with strong customer retention and pricing advantages.

Kroger: Major U.S. supermarket chain focusing on digital transformation and personalized shopping experiences.

Reliance Retail: Leading grocery and retail player in India with rapidly expanding store network and digital grocery platforms.

Regional Traditional Retailers: Highly fragmented segment across Asia-Pacific, Latin America, and Africa, serving as the backbone of grocery distribution in rural and semi-urban regions.

Key Competitive Intensity & Market Structure Signals in Global Grocery Market

A major competitive signal is the rapid shift toward omnichannel retailing, where physical stores and digital platforms are integrated to provide seamless shopping experiences. Retailers that fail to adopt digital-first strategies risk losing market share to agile e-commerce and quick-commerce competitors.

Another key factor is the rising importance of private label products. Large retailers are aggressively expanding their own branded grocery offerings to improve margins and strengthen customer loyalty, intensifying competition with established FMCG brands.

Quick commerce and hyperlocal delivery models are reshaping urban grocery consumption patterns. Companies offering 10???30 minute delivery services are increasing competitive pressure on traditional supermarkets and convenience stores, especially in densely populated cities.

Supply chain efficiency has become a critical competitive differentiator. Retailers with advanced cold chain logistics, automated warehouses, and AI-driven inventory management systems are gaining significant cost and operational advantages.

Sustainability and ethical sourcing are also emerging as important competitive factors. Companies are increasingly investing in eco-friendly packaging, waste reduction systems, and sustainable sourcing practices to align with evolving consumer expectations and regulatory requirements.

Strategic Implications of Competitive Intensity & Market Structure in Global Grocery Market

Retailers are increasingly focusing on end-to-end ecosystem control, integrating procurement, warehousing, logistics, and last-mile delivery to improve efficiency and customer experience. Vertical integration is becoming more common among large players to reduce dependency on external suppliers.

Digital transformation is reshaping competitive dynamics, with AI-driven demand forecasting, automated pricing systems, and personalized recommendation engines playing a central role in retail strategy and customer engagement.

Strategic partnerships between retailers, logistics providers, and technology companies are expanding to strengthen delivery networks and improve operational scalability in both urban and rural markets.

Emerging markets are witnessing strong competition between organized retail chains and traditional grocery stores, with organized players gradually gaining share through expansion of modern retail formats and digital adoption.

Price wars remain a persistent feature of the market, particularly in essential grocery categories, forcing retailers to continuously optimize supply chains and operational costs to maintain profitability.

Global Grocery Market Competitive Intensity & Market Structure Forward Outlook

The Global Grocery Market is expected to become increasingly digitized and technology-driven, with strong emphasis on automation, AI-powered logistics, and real-time inventory management systems. Competition will intensify further as digital-native grocery platforms continue to expand rapidly.

Quick commerce, subscription-based grocery models, and fully automated fulfillment centers are expected to redefine urban grocery retailing, significantly increasing delivery speed and operational efficiency.

Market consolidation is likely to increase in organized retail segments, as large players acquire regional chains and digital startups to expand geographic reach and strengthen omnichannel capabilities.

Sustainability will become a core competitive requirement, with retailers adopting low-carbon supply chains, reduced food waste strategies, and circular packaging systems to meet regulatory and consumer expectations.

Overall, the grocery market will remain highly competitive but structurally stable, supported by consistent demand for essential food products. Companies that successfully combine physical retail strength with digital innovation, supply chain excellence, and customer-centric strategies will lead the Global Grocery Market through 2033.

Value Chain

Global Health Tourism Market Value Chain & Supply Chain Evolution Overview

The Global Health Tourism Market value chain is undergoing a profound transformation as it evolves from traditional hospital-centric international treatment models into highly integrated, digitally enabled, and patient-centric global healthcare ecosystems that combine medical excellence with hospitality, wellness, and advanced digital coordination systems. This shift is being driven by a combination of structural global healthcare cost disparities, rising medical expenses in developed economies, increasing cross-border patient mobility, and growing consumer preference for faster access to specialized treatments, advanced medical technologies, and personalized healthcare experiences. At the same time, the expansion of wellness tourism, preventive healthcare travel, and premium recovery-focused care environments is significantly reshaping how healthcare services are delivered and consumed across international markets.

Health tourism today encompasses a wide spectrum of interconnected services including medical tourism, cosmetic surgery tourism, fertility treatment tourism, dental tourism, rehabilitation tourism, and wellness-focused preventive healthcare travel, all of which are increasingly integrated into unified patient experience ecosystems. Patients are no longer traveling solely for cost advantages but are also driven by factors such as reduced waiting times, availability of cutting-edge procedures, internationally accredited healthcare facilities, and seamless end-to-end service experiences that combine treatment, travel, accommodation, and recovery support. This growing complexity has expanded the value chain far beyond traditional healthcare delivery into a multi-layered ecosystem involving digital patient engagement platforms, international insurance coordination, medical visa facilitation services, multilingual support systems, telemedicine consultations, and AI-powered healthcare management solutions.

The upstream supply chain of the global health tourism industry is increasingly dependent on highly advanced healthcare infrastructure and technological systems, including modern hospital facilities, pharmaceutical supply networks, medical device manufacturing ecosystems, robotic-assisted surgery platforms, diagnostic imaging technologies, and AI-driven clinical decision support systems. In parallel, digital healthcare infrastructure such as cloud-based medical records, secure data exchange systems, and intelligent patient management platforms is becoming critical for ensuring continuity of care across borders. Healthcare providers are also strengthening collaborations with airlines, hospitality companies, insurance providers, and travel facilitators to build fully integrated ecosystems that enable seamless patient journeys from initial consultation to post-treatment recovery and long-term follow-up care.

Operational strategies within the health tourism value chain are increasingly focused on achieving international accreditation standards, delivering integrated treatment packages, and enhancing patient satisfaction through personalized care pathways that combine medical treatment with hospitality-level comfort and wellness-oriented recovery experiences. Healthcare providers are investing heavily in multilingual communication systems, digital medical record accessibility, telehealth integration, AI-enabled patient coordination tools, and premium hospitality partnerships in order to strengthen global competitiveness. However, despite this rapid evolution, the industry continues to face significant structural challenges including complex international regulatory frameworks, inconsistent healthcare quality standards across regions, data privacy and cybersecurity risks, visa and travel restrictions, insurance claim complexities, geopolitical instability, and ongoing shortages of specialized healthcare professionals in certain markets.

Global Health Tourism Market Value Chain & Supply Chain Evolution Current Scenario

The current global health tourism ecosystem is characterized by rapid globalization of healthcare services, increasing reliance on digital health technologies, and rising investments in internationally accredited healthcare infrastructure across both emerging and developed destinations. Countries in Asia-Pacific, the Middle East, Latin America, and parts of Eastern Europe are aggressively positioning themselves as competitive medical tourism hubs by investing in advanced hospital networks, robotic surgery capabilities, digital patient engagement platforms, and luxury healthcare recovery facilities designed to attract high-value international patients seeking both affordability and premium care experiences.

At the same time, medical tourism facilitators and healthcare travel agencies are playing an increasingly central role in integrating fragmented services into seamless end-to-end patient journeys that include treatment coordination, visa processing, travel logistics, hotel accommodation, insurance assistance, and structured post-treatment rehabilitation programs. Hospitals and specialty clinics are also forming strategic partnerships with airlines, hospitality providers, wellness resorts, pharmaceutical companies, and international insurance networks in order to create fully integrated healthcare travel ecosystems that reduce friction for patients while enhancing service quality and operational efficiency across the entire value chain.

Demand for specialized healthcare services such as cosmetic surgery, fertility treatments, orthopedic procedures, cardiology interventions, dental care, bariatric surgery, and alternative wellness therapies continues to grow at a strong pace, significantly contributing to increased international patient mobility across regions. In parallel, wellness tourism and preventive healthcare retreats are emerging as high-growth segments driven by rising consumer awareness around holistic health, mental wellness, stress management, and lifestyle-driven preventive care. Supporting these developments, AI-powered healthcare systems, digital medical records, telemedicine platforms, and virtual follow-up care solutions are rapidly becoming essential components of competitive differentiation within leading health tourism destinations worldwide.

Key Value Chain & Supply Chain Evolution Signals in Global Health Tourism Market

Several transformative structural signals are reshaping the global health tourism market value chain, with the most significant being the growing impact of rising healthcare inflation and extended treatment waiting periods in developed economies, which are driving a continuous increase in outbound medical travel toward cost-efficient and high-quality healthcare destinations in Asia-Pacific, Latin America, and the Middle East. This demand shift is fundamentally altering global patient flow patterns and strengthening the competitive positioning of emerging healthcare hubs that can deliver high-quality treatment at significantly lower costs.

In addition, rapid technological advancements in telemedicine, AI-assisted diagnostics, digital healthcare coordination platforms, and remote consultation systems are streamlining cross-border patient acquisition processes while simultaneously improving continuity of care across international healthcare systems. Wellness tourism is also undergoing a major transformation as it evolves beyond traditional spa and leisure-based offerings into medically supervised preventive healthcare ecosystems that include structured rehabilitation programs, mental wellness therapies, chronic disease management support, and integrated holistic treatment pathways designed to improve long-term health outcomes.

Governments across multiple regions are actively supporting the expansion of medical tourism through targeted policy interventions such as healthcare investment incentives, simplified visa procedures, international accreditation frameworks, and national branding initiatives aimed at positioning their healthcare systems as globally competitive destinations. At the same time, deepening integration between hospitals, hospitality providers, airlines, wellness resorts, insurance companies, and digital healthcare platforms is creating highly interconnected patient-centric ecosystems that prioritize convenience, personalization, affordability, and end-to-end service quality across the entire patient journey.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Health Tourism Market

Leading healthcare providers such as Apollo Hospitals, Bumrungrad International Hospital, Fortis Healthcare, KPJ Healthcare, Raffles Medical Group, and Cleveland Clinic Abu Dhabi are actively strengthening their global positioning through continuous infrastructure expansion, digital transformation initiatives, specialization in high-demand medical procedures, and enhanced international patient service capabilities designed to attract and retain cross-border patients. These organizations are increasingly focusing on building integrated healthcare ecosystems that combine advanced clinical expertise with premium hospitality experiences and digitally enabled patient engagement systems.

Competitive advantage in the global health tourism market is increasingly determined by a combination of clinical excellence, international accreditation, cost competitiveness, adoption of advanced medical technologies, multilingual patient support capabilities, digital healthcare integration, strong hospitality partnerships, and the ability to deliver seamless end-to-end patient journey management. Healthcare providers that successfully integrate specialized medical expertise with luxury hospitality services, AI-enabled coordination systems, wellness-oriented recovery programs, and strong international branding strategies are expected to capture the most significant share of future growth opportunities in this rapidly expanding market.

Strategic collaborations across the ecosystem involving hospitals, insurance providers, airlines, travel agencies, hospitality groups, and digital healthcare technology firms are becoming increasingly critical for improving patient acquisition efficiency, reducing operational complexity, and enhancing long-term customer retention. In the long term, success in the health tourism market will depend on the ability to balance affordability with clinical quality, ensure digital accessibility, maintain transparency in healthcare delivery, safeguard patient data privacy, and provide highly personalized post-treatment care across globally distributed healthcare systems.

Global Health Tourism Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the global health tourism value chain is expected to evolve into a highly digitalized, AI-powered, and globally interconnected ecosystem where healthcare delivery is seamlessly integrated with wellness services, hospitality experiences, and advanced digital health management platforms. Healthcare providers will increasingly adopt telemedicine-enabled international consultation models, AI-assisted diagnostic and treatment planning systems, robotic surgical technologies, cloud-based patient management infrastructure, and multilingual virtual care support systems to enhance accessibility, efficiency, and patient satisfaction across borders.

Personalized healthcare tourism packages that combine advanced medical treatment with rehabilitation services, wellness therapies, nutritional planning, mental health support, luxury hospitality experiences, and long-term preventive healthcare programs are expected to become mainstream offerings across leading global medical tourism destinations. Furthermore, emerging technologies such as AI-based diagnostics, digital twin simulations for treatment planning, wearable health monitoring devices, blockchain-enabled medical record systems, and immersive virtual follow-up care platforms will play a defining role in shaping the next generation of international healthcare delivery models.

As consumer preferences continue to shift toward proactive health management and holistic wellness experiences, segments such as wellness tourism, regenerative medicine, fertility tourism, cosmetic surgery tourism, and preventive healthcare retreats are expected to witness sustained strong growth. Ultimately, the future of the global health tourism value chain will be defined by its transformation from fragmented medical travel services into fully integrated, digitally connected, and experience-driven global healthcare ecosystems that combine clinical excellence, technological innovation, hospitality integration, and deeply personalized patient care.

Investment Activity

Global Grocery Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Grocery Market are being driven by sustained essential goods demand, rapid expansion of organized retail infrastructure, accelerating e-commerce penetration, and the growing shift toward omnichannel grocery ecosystems. Between 2026 and 2033, capital allocation is expected to concentrate on retail network expansion, digital grocery platforms, supply chain automation, cold chain infrastructure, and quick commerce delivery models.

The market attracts strong and stable investment due to its non-cyclical nature, with grocery consumption forming a core component of daily household expenditure globally. Major global retailers such as Walmart, Tesco, Carrefour, Costco, Kroger, Aldi, Lidl, and Amazon Fresh continue to invest heavily in store expansion, private label development, warehouse automation, and last-mile delivery systems to strengthen market positioning.

A key structural shift shaping investment flows is the rapid convergence of physical retail and digital grocery platforms. This is accelerating funding into AI-driven inventory systems, predictive demand forecasting tools, automated fulfillment centers, cloud-based retail ecosystems, and hyperlocal delivery networks designed to improve speed, efficiency, and customer convenience.

Global Grocery Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by the expansion of organized retail formats, rising adoption of online grocery shopping, and increasing consumer preference for convenience-driven purchasing models. Retailers are aggressively modernizing supply chains and expanding distribution networks to meet growing urban demand.

- Asia-Pacific: Leads global investment activity due to rapid urbanization, expanding middle-class population, and strong growth in supermarket chains and online grocery platforms across China, India, and Southeast Asia.

- North America: Attracts significant capital investment driven by advanced retail infrastructure, strong e-commerce penetration, and rapid expansion of quick commerce and subscription-based grocery delivery models.

- Europe: Focuses investment on sustainable retail systems, organic grocery expansion, and modernization of established supermarket networks with strong emphasis on eco-friendly supply chains.

- Latin America & MEA: Witness growing investment in retail modernization, cold chain logistics, and expansion of organized grocery retail formats in urban centers.

Key Investment & Funding Dynamics Signals in Global Grocery Market

- Rapid expansion of online grocery platforms and quick commerce delivery models is attracting strong venture capital and corporate investment.

- Automation of warehouses, fulfillment centers, and inventory management systems is driving significant capital inflows into retail technology infrastructure.

- Growth of private label grocery brands is increasing retailer margins and encouraging investment in in-house manufacturing and sourcing capabilities.

- Cold chain and logistics infrastructure expansion is receiving strong funding to reduce food waste and improve supply chain efficiency.

- AI-driven personalization, demand forecasting, and dynamic pricing systems are emerging as key investment areas in digital grocery ecosystems.

Strategic Implications of Investment & Funding Dynamics in Global Grocery Market

- The investment landscape favors large-scale retailers with strong supply chain integration, digital capabilities, and omnichannel retail strategies.

- Technology adoption is becoming a key competitive differentiator, particularly in logistics automation, predictive analytics, and customer experience optimization.

- Strategic partnerships between retailers, logistics providers, and technology companies are accelerating the development of end-to-end grocery ecosystems.

- Regional diversification remains essential, with Asia-Pacific driving volume growth, North America leading in technological innovation, and Europe focusing on sustainability-led retail models.

- Price competition, operational efficiency, and delivery speed continue to shape investment decisions across the global grocery industry.

Global Grocery Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Grocery Market is expected to attract sustained and stable investment driven by continuous population growth, rising urban consumption, and rapid digital transformation in retail systems. Capital deployment will increasingly focus on automation, AI-based retail intelligence, and integrated omnichannel grocery platforms.

- Asia-Pacific: Will remain the dominant growth and investment hub due to expanding retail infrastructure and rapid adoption of digital grocery ecosystems.

- North America: Will continue to lead in retail technology innovation, quick commerce expansion, and advanced logistics automation systems.

- Europe: Will maintain steady investment momentum focused on sustainability, organic grocery expansion, and efficient supply chain modernization.

Sustainability initiatives, including reduced packaging waste, eco-friendly logistics, and carbon-efficient supply chains, are increasingly shaping investment priorities in the grocery sector.

Overall, the market is expected to maintain stable long-term growth supported by its essential nature and continuous demand. Companies that successfully integrate physical retail strength with digital capabilities, logistics efficiency, and data-driven operations will be best positioned to lead the Global Grocery Market through 2033.

Technology & Innovation

Global Grocery Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Grocery Market is undergoing rapid transformation as retailers, e-commerce platforms, logistics providers, and food supply chain operators increasingly adopt advanced digital technologies to improve efficiency, customer experience, demand forecasting, and end-to-end supply chain visibility. Key innovation areas include AI-driven inventory management systems, automated warehouses, smart retail stores, quick commerce platforms, cloud-based retail ecosystems, and data-driven personalization tools that are reshaping how grocery products are sourced, distributed, and consumed globally.

Digital transformation is playing a central role in reshaping the grocery retail ecosystem. Retailers are increasingly implementing omnichannel platforms that integrate physical stores with online ordering systems, enabling seamless shopping experiences across mobile apps, websites, and in-store digital kiosks. These integrated systems help improve customer engagement, reduce operational friction, and enhance real-time product availability tracking across multiple retail channels.

Artificial intelligence and machine learning technologies are becoming critical components of modern grocery operations. AI-powered systems are being used for demand forecasting, dynamic pricing, personalized recommendations, waste reduction, and supply chain optimization. These tools allow retailers to better predict consumer behavior, optimize stock levels, and minimize product spoilage while improving profitability and operational efficiency.

Automation technologies, including robotics and autonomous systems, are increasingly being deployed in warehouses and distribution centers. Automated picking systems, robotic sorting technologies, and smart logistics solutions are significantly improving order fulfillment speed and accuracy, particularly in e-commerce grocery and quick commerce models where delivery speed is a key competitive factor.

In addition, digital payment systems, contactless checkout technologies, and cashier-less store formats are gaining traction in the global grocery market. These innovations are reducing checkout time, improving convenience, and enhancing overall in-store customer experience, particularly in urban retail environments.

The innovation landscape is also expanding toward data-driven retail ecosystems where consumer purchasing behavior is analyzed in real time to optimize promotions, product placement, and inventory strategies. Advanced analytics platforms are enabling retailers to build highly personalized shopping experiences while improving supply chain responsiveness and operational agility.

Global Grocery Market Technology & Innovation Landscape Current Scenario

Currently, the global grocery market is experiencing strong digital acceleration driven by the rapid expansion of e-commerce grocery platforms, quick commerce services, and omnichannel retail strategies. Major retailers and online platforms such as Walmart, Amazon Fresh, Tesco, Carrefour, and regional grocery chains are heavily investing in digital infrastructure, fulfillment centers, and AI-powered logistics systems to strengthen competitiveness in an increasingly digital retail environment.

Online grocery delivery services have become one of the fastest-growing segments in the market, supported by rising smartphone penetration, improved internet connectivity, and changing consumer preferences toward convenience and time-saving shopping solutions. Quick commerce models offering ultra-fast delivery within minutes to hours are reshaping urban grocery consumption patterns.

Smart supply chain technologies are widely being adopted to improve inventory visibility and reduce inefficiencies. IoT-enabled tracking systems, real-time logistics monitoring, and cloud-based inventory platforms are helping retailers minimize stockouts, reduce wastage, and optimize distribution networks across regions.

Automated warehouses and robotics-driven fulfillment centers are increasingly being used to manage growing online grocery demand. These systems improve order accuracy, reduce labor dependency, and accelerate delivery timelines, particularly in high-volume urban markets.

AI-powered personalization engines are also becoming common across digital grocery platforms. These systems analyze consumer purchase history, dietary preferences, and shopping behavior to provide customized product recommendations, targeted promotions, and dynamic pricing strategies that enhance customer engagement and retention.

Additionally, digital payment ecosystems and contactless checkout technologies are now standard features across many modern grocery retail formats. These innovations are improving transaction speed, reducing physical contact, and supporting the shift toward fully digital retail experiences.

Key Technology & Innovation Trends in Global Grocery Market

- AI-Powered Demand Forecasting: Machine learning systems predicting consumer demand patterns to optimize inventory and reduce food waste.

- Omnichannel Retail Platforms: Integrated systems combining physical stores, mobile apps, and e-commerce platforms for seamless shopping experiences.

- Quick Commerce Models: Ultra-fast grocery delivery services enabling fulfillment within minutes through hyperlocal distribution networks.

- Automated Warehousing & Robotics: Robotic sorting, picking, and packaging systems improving fulfillment speed and accuracy.

- Smart Inventory Management: IoT and cloud-based systems enabling real-time stock monitoring and supply chain optimization.

- Cashier-Less Checkout Systems: AI and sensor-based stores eliminating traditional checkout counters for faster shopping experiences.

- Personalized Retail Analytics: Data-driven platforms offering customized promotions and product recommendations.

- Digital Payment & Contactless Transactions: Secure and fast payment ecosystems improving customer convenience and reducing transaction time.

- Cold Chain Optimization Technologies: Advanced logistics systems ensuring freshness and reducing spoilage in perishable goods distribution.

- Sustainable Retail Technologies: Eco-friendly packaging solutions and AI-driven waste reduction systems supporting green retail initiatives.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping the grocery market by improving operational efficiency, reducing supply chain waste, enhancing customer convenience, and enabling real-time responsiveness to consumer demand. Digital transformation is allowing retailers to integrate physical and online grocery ecosystems into unified platforms that support seamless purchasing, delivery, and post-purchase services.

For retailers and grocery operators, investment in AI-driven analytics, automation technologies, omnichannel infrastructure, and smart logistics systems has become essential for maintaining competitiveness. Companies that effectively leverage data-driven decision-making and advanced fulfillment technologies are achieving stronger customer retention, improved operational scalability, and higher profit margins.

The growing adoption of personalization technologies is enabling grocery retailers to deliver highly targeted marketing campaigns and tailored product offerings based on consumer behavior insights. This shift toward customer-centric retailing is improving engagement levels and increasing long-term brand loyalty.

At the same time, digital grocery platforms are expanding access to essential goods, particularly in urban regions where convenience and fast delivery are key purchasing drivers. Quick commerce and online grocery models are significantly reducing dependence on traditional retail formats while expanding market reach for retailers.

However, challenges such as supply chain disruptions, high technology implementation costs, cybersecurity risks, last-mile delivery inefficiencies, and regulatory complexities continue to impact market scalability. Retailers must invest in resilient digital infrastructure, secure payment systems, and efficient logistics networks to ensure sustainable growth.

Global Grocery Market Technology & Innovation Forward Outlook

Looking ahead, the global grocery market is expected to evolve into a highly digitized and automated retail ecosystem driven by artificial intelligence, robotics, predictive analytics, and hyperlocal delivery networks. Retailers will increasingly adopt intelligent systems capable of real-time demand sensing, automated replenishment, and fully optimized supply chain coordination.

Artificial intelligence will play a central role in shaping future grocery retailing through advanced personalization, predictive inventory management, dynamic pricing models, and automated customer engagement systems. These technologies will significantly improve operational efficiency while enhancing consumer satisfaction.

The expansion of quick commerce and autonomous delivery systems, including drones and self-driving vehicles, is expected to redefine last-mile grocery distribution, particularly in urban markets. These innovations will reduce delivery times and improve service accessibility for consumers.

Smart stores equipped with cashier-less checkout systems, IoT-enabled shelves, digital pricing displays, and AI-powered monitoring systems will become increasingly common in developed markets. These stores will provide seamless, frictionless shopping experiences while reducing operational costs.

Sustainability will also become a major innovation driver, with increased focus on eco-friendly packaging, food waste reduction technologies, and energy-efficient retail infrastructure. Retailers investing in sustainable supply chain practices will gain stronger consumer trust and regulatory advantages.

In conclusion, the Global Grocery Market is undergoing a major technological transformation driven by digitalization, automation, artificial intelligence, and omnichannel retail integration. Companies that successfully combine advanced supply chain technologies, personalized customer experiences, and efficient delivery ecosystems will lead the future evolution of the global grocery industry.

Market Risk

Global Grocery Market Risk Factors & Disruption Threats Overview

The Global Grocery Market operates as one of the most essential and resilient sectors of the global economy; however, it is increasingly exposed to a wide range of structural, operational, and macroeconomic risk factors that can significantly influence supply stability, pricing dynamics, and long-term profitability. While consistent demand for food and household essentials provides baseline stability, the industry is highly vulnerable to disruptions across global supply chains, inflationary cycles, regulatory frameworks, climate conditions, and evolving consumer behavior. The increasing interdependence of global sourcing networks and just-in-time inventory systems further amplifies exposure to external shocks, making risk management a critical strategic priority for all market participants.

One of the most significant risk factors in the global grocery market is supply chain disruption, which can arise from geopolitical tensions, transportation bottlenecks, trade restrictions, labor shortages, and port congestion. Because grocery products rely heavily on complex, multi-country sourcing networks, any interruption in raw material availability, agricultural output, or logistics infrastructure can quickly translate into product shortages, price volatility, and reduced shelf availability. Perishable goods such as fresh produce, dairy, meat, and seafood are particularly vulnerable due to strict storage requirements and limited shelf life, increasing operational risk for retailers and distributors.

Inflationary pressure and rising input costs represent another major challenge for the grocery industry. Fluctuations in energy prices, transportation costs, agricultural inputs, packaging materials, and labor wages directly impact retail pricing structures and profit margins. In highly competitive grocery markets, retailers often struggle to fully pass these increased costs onto consumers, leading to margin compression. Persistent inflation can also shift consumer purchasing behavior toward lower-cost private label products, discount retailers, or reduced consumption of premium grocery categories.

Climate change and environmental risks are increasingly influencing the stability of global food supply chains. Extreme weather events such as droughts, floods, heatwaves, and storms can significantly disrupt agricultural production, reduce crop yields, and increase volatility in food commodity prices. Long-term environmental degradation and water scarcity further threaten agricultural productivity in key sourcing regions. These climate-related disruptions not only affect availability but also increase procurement costs and create uncertainty in long-term supply planning for grocery retailers.

Another critical risk factor is the increasing regulatory complexity across food safety, labeling standards, import/export controls, and sustainability requirements. Governments worldwide are tightening regulations related to food quality, traceability, packaging waste reduction, and carbon emissions. Compliance with these evolving regulations requires continuous investment in supply chain monitoring systems, quality assurance processes, and reporting infrastructure. Non-compliance can result in penalties, product recalls, reputational damage, and loss of consumer trust.

Global Grocery Market Risk Factors & Disruption Threats Current Scenario

The current global grocery market environment is characterized by strong demand stability but heightened operational volatility due to ongoing macroeconomic uncertainty, geopolitical fragmentation, and shifting consumer behavior. Retailers are facing increasing pressure to maintain affordability while managing rising procurement and logistics costs. At the same time, consumers are becoming more price-sensitive, leading to intensified competition between supermarkets, discount retailers, and online grocery platforms.

Supply chain resilience has become a central focus in the current market scenario, particularly following recent global disruptions that exposed vulnerabilities in sourcing networks and inventory systems. Many retailers are now diversifying supplier bases, increasing local sourcing, and investing in advanced forecasting technologies to reduce dependency on single-region supply chains. However, these adjustments often come with increased operational complexity and higher procurement costs, which can impact overall profitability.

Digital transformation is reshaping the competitive landscape of the grocery market, but it also introduces new risks related to cybersecurity, data privacy, and system reliability. Online grocery platforms, quick commerce services, and AI-driven inventory systems rely heavily on digital infrastructure, making them vulnerable to cyberattacks, system outages, and data breaches. Any disruption in digital platforms can directly impact order fulfillment, customer trust, and revenue continuity.

Labor shortages and workforce challenges are also emerging as significant operational risks across global grocery supply chains. The industry relies heavily on logistics workers, warehouse staff, retail employees, and transportation personnel. Rising wage pressures, labor turnover, and skill shortages in logistics and cold chain operations can reduce efficiency and increase operational costs, particularly in high-demand urban markets.

Additionally, changing consumer expectations are creating strategic pressure on grocery retailers to continuously innovate. Demand for faster delivery, healthier products, organic food options, and personalized shopping experiences is increasing. Failure to adapt to these evolving preferences can lead to loss of market share, particularly as digital-native competitors and quick commerce platforms continue to expand aggressively.

Global Grocery Market Key Risk Factors & Disruption Threat Signals

One of the most important disruption signals in the grocery market is the rapid expansion of quick commerce and hyperlocal delivery models. These platforms are redefining consumer expectations around delivery speed and convenience, forcing traditional retailers to restructure their logistics and inventory systems. While this model improves customer experience, it also increases fulfillment costs and operational complexity.

Another significant disruption trend is the increasing adoption of artificial intelligence and automation in grocery retail operations. AI-driven demand forecasting, automated warehouses, and robotic fulfillment systems are improving efficiency but also increasing dependence on complex technological infrastructure. System failures, algorithmic errors, or data inaccuracies can lead to inventory imbalances, stockouts, or overstock situations.

The growing consolidation of retail supply chains and the expansion of private label products are also reshaping competitive dynamics. Large retailers are increasingly controlling production, distribution, and pricing, which creates competitive pressure for smaller players and reduces market fragmentation. However, over-reliance on concentrated supply chains can increase systemic risk if major suppliers or distribution hubs experience disruption.

Sustainability and environmental accountability are becoming critical disruption factors as consumers and regulators demand more transparent and eco-friendly grocery supply chains. Retailers are under pressure to reduce plastic packaging, lower carbon emissions, and adopt sustainable sourcing practices. Failure to meet these expectations can result in reputational damage and reduced consumer loyalty.

In addition, the increasing integration of digital payment systems and e-commerce platforms introduces financial and technological risks. Dependence on digital ecosystems increases exposure to payment fraud, transaction failures, and platform outages, which can directly impact sales and customer satisfaction levels.

Global Grocery Market Strategic Implications of Risk Factors

To manage rising risk complexity, grocery market participants must prioritize supply chain diversification, inventory optimization, and localized sourcing strategies. Strengthening supplier networks across multiple geographies can reduce dependency on single-source regions and improve resilience against geopolitical or environmental disruptions. Investment in cold chain infrastructure and logistics modernization is also essential to maintain product quality and reduce wastage.

Retailers must also enhance digital resilience by strengthening cybersecurity frameworks, improving data protection systems, and ensuring platform stability across online grocery operations. As digital grocery channels continue to expand, maintaining secure and reliable systems will become a key competitive differentiator.

Operational efficiency can be improved through automation, AI-based forecasting, and advanced analytics, but companies must also implement strong governance systems to reduce technology-related risks. Balancing automation with human oversight will be critical to ensuring accuracy in demand planning and inventory management.

Furthermore, companies must align closely with evolving consumer expectations by expanding organic product lines, improving transparency in sourcing, and offering flexible delivery models. Retailers that successfully combine affordability, convenience, and sustainability will be better positioned to maintain long-term competitiveness in an increasingly dynamic market environment.

Finally, strategic collaboration across suppliers, logistics providers, and digital platforms will play a crucial role in building resilient grocery ecosystems. Integrated partnerships can help reduce inefficiencies, improve responsiveness to demand fluctuations, and enhance overall supply chain visibility across the global grocery market.

Global Grocery Market Forward Risk Outlook

Looking ahead, the global grocery market is expected to face continued risk from macroeconomic instability, climate variability, geopolitical fragmentation, and rapid technological disruption. While demand for grocery products will remain structurally stable, volatility in supply chains, pricing structures, and consumer behavior will continue to challenge market participants.

The future risk landscape will be increasingly shaped by digital transformation, sustainability pressures, and supply chain localization trends. Retailers that successfully integrate advanced technology, resilient logistics systems, and sustainable business practices will be better positioned to navigate uncertainty and maintain long-term growth.

Overall, while the grocery market remains fundamentally essential and stable, its operational environment is becoming more complex, requiring continuous adaptation, strategic risk management, and investment in resilient infrastructure to ensure long-term competitiveness.

Regulatory Landscape

Global Grocery Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global grocery market is becoming increasingly complex and structured as governments, trade bodies, food safety authorities, and consumer protection agencies strengthen oversight across food production, distribution, retail operations, and digital commerce channels. The grocery sector, being directly linked to food security and public health, is subject to strict regulatory frameworks that ensure product safety, quality assurance, fair pricing, transparent labeling, and ethical sourcing across both domestic and international supply chains.

Governments across major economies are actively enforcing food safety regulations through agencies such as the FDA (United States), EFSA (Europe), FSSAI (India), and other national food standards authorities. These regulations cover hygiene standards, permissible additives, contamination control, shelf-life compliance, packaging safety, and cold chain integrity. Increasing globalization of food supply chains has further intensified the need for harmonized food safety standards to reduce risks associated with cross-border food trade and ensure consistent quality across markets.

In addition to food safety regulations, the grocery market is heavily influenced by consumer protection laws that regulate pricing transparency, misleading advertising, product labeling accuracy, and fair trade practices. Retailers are required to provide clear nutritional information, ingredient disclosures, allergen warnings, and country-of-origin labeling to ensure informed consumer decision-making. These regulations are particularly strict in developed regions such as North America and Europe, where consumer rights frameworks are highly advanced.

The rapid expansion of digital grocery platforms and e-commerce-based food retailing has introduced a new layer of regulatory oversight focused on data privacy, online transactions, digital payments, and platform accountability. Governments are increasingly regulating quick commerce models, online grocery delivery services, and AI-driven recommendation systems to ensure fair competition, data protection, and consumer safety in digital retail ecosystems. Competition authorities are also monitoring market dominance by large e-commerce players to prevent monopolistic practices and ensure a balanced retail environment.

Global Grocery Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape of the grocery market is defined by stringent food safety enforcement, rising sustainability requirements, and expanding digital commerce regulations. Developed economies maintain highly structured regulatory systems that govern every stage of the grocery supply chain, from agricultural production and food processing to retail distribution and waste management.

In Asia-Pacific, regulatory frameworks are rapidly evolving due to the expansion of organized retail and increasing demand for standardized food safety practices. Countries such as China and India have strengthened food inspection systems, labeling requirements, and import-export food safety protocols to ensure compliance with international standards. This is supporting the growth of organized grocery retail while improving consumer trust in packaged and processed food products.

In Europe, grocery market regulations are heavily influenced by sustainability policies, carbon footprint reduction mandates, and strict food traceability requirements under frameworks such as the EU Green Deal. Retailers are required to comply with environmental packaging regulations, waste reduction targets, and ethical sourcing guidelines, making Europe one of the most regulated grocery markets globally.

North America continues to focus on food safety modernization, supply chain resilience, and digital retail oversight. Regulatory agencies are increasingly addressing issues such as food recalls, supply chain disruptions, and online grocery platform accountability. There is also growing emphasis on regulating labeling accuracy for health-related claims such as ???organic,??? ???non-GMO,??? and ???natural??? food categories.

In emerging markets across Latin America, the Middle East, and Africa, regulatory systems are gradually strengthening, with governments focusing on improving food safety infrastructure, expanding retail licensing frameworks, and enhancing import quality controls. These regions are also witnessing increased alignment with international food safety standards to attract global retail investments.

Key Regulatory & Policy Environment Signals in Global Grocery Market

- Food Safety & Quality Standards: Governments are enforcing strict hygiene, contamination control, and quality assurance regulations across food production, processing, storage, and retail distribution to ensure consumer health and safety.

- Food Labeling & Transparency Requirements: Regulatory bodies mandate clear disclosure of ingredients, nutritional content, allergens, and origin information to ensure transparency and informed consumer choices.

- Sustainability & Environmental Regulations: Retailers are increasingly required to comply with packaging waste reduction policies, plastic usage restrictions, and carbon footprint reduction initiatives across supply chains.

- E-Commerce & Digital Retail Regulations: Online grocery platforms are subject to regulations covering data privacy, digital payments, algorithm transparency, and fair competition practices.

- Supply Chain Traceability Requirements: Governments are enforcing end-to-end traceability systems to track food products from farm to shelf, improving accountability and reducing food fraud risks.

- Pricing & Competition Laws: Antitrust regulations and fair trade policies are being strengthened to prevent price manipulation, monopolistic practices, and unfair market dominance by large retail chains.

Strategic Implications of Regulatory & Policy Environment in Global Grocery Market

The evolving regulatory landscape is significantly reshaping operational strategies across the global grocery market. Retailers are increasingly investing in compliance management systems, advanced quality control technologies, and transparent sourcing mechanisms to meet rising regulatory expectations. This has led to higher operational costs but also improved consumer trust and long-term brand value.

Digital transformation in grocery retail is being directly influenced by regulatory oversight, particularly in areas such as data protection, algorithm governance, and online pricing transparency. Companies operating in e-commerce grocery segments are adopting more secure platforms, improving data encryption standards, and ensuring compliance with regional digital commerce laws.

Sustainability regulations are driving major shifts in packaging design, supply chain optimization, and product sourcing strategies. Retailers are increasingly adopting eco-friendly packaging materials, reducing food waste through better inventory forecasting, and partnering with sustainable suppliers to meet regulatory expectations.

Food safety compliance requirements are pushing grocery companies to strengthen cold chain logistics, implement real-time monitoring systems, and enhance supplier auditing processes. This is improving overall product quality but also increasing dependency on technology-driven supply chain management systems.

Global Grocery Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global grocery market is expected to become more integrated, technology-driven, and sustainability-focused. Governments will likely introduce stricter food safety laws, expanded digital commerce regulations, and more aggressive sustainability mandates across retail supply chains.

Artificial intelligence and blockchain technologies are expected to play a major role in regulatory compliance, particularly in food traceability, fraud detection, and automated quality monitoring. These technologies will help regulators and retailers ensure transparency and real-time tracking of food products across global supply chains.

Sustainability regulations are expected to intensify, with stricter enforcement of carbon neutrality targets, plastic reduction policies, and circular economy practices within grocery retail operations. Retailers will be required to adopt more environmentally responsible sourcing, packaging, and distribution models.

Digital grocery platforms will face increased regulatory scrutiny regarding algorithm fairness, consumer data protection, and competitive practices. Governments are expected to establish clearer frameworks for quick commerce and AI-driven retail ecosystems to ensure fair market competition.

Overall, the regulatory and policy environment will continue to play a central role in shaping the structure, efficiency, and competitiveness of the global grocery market. Companies that proactively align with food safety standards, sustainability requirements, and digital compliance frameworks will be best positioned for long-term growth and market leadership.